An intellectual structure of

activity-based costing:

a co-citation analysis

Hsiu-Kuei Kuo

Department of Transportation Technology and Management,

National Chiao Tung University, Taipei, Taiwan, and

Chyan Yang

Institute of Business and Management, National Chiao Tung University,

Taipei, Taiwan

Abstract

Purpose – The purpose of this paper is to show that by exploring the intellectual structure of activity-based costing (ABC) based on the citation database of Google Scholar, one can understand the evolution and core ideas of the ABC discipline.

Design/methodology/approach – This study employs the document co-citation method to model the intellectual structure of ABC between 1988 and 2008. After an initial co-citation analysis of the condition-limited literature set to find the relationships between core articles, this study further implements multivariate statistical techniques to construct representations for the ABC intellectual structure.

Findings – A total of four important subjects chronologically provide a panoramic view of the evolution of ABC. This study finds some dimensions of the results to be in accordance with prior research, but further achieves insights into the core ideas underpinning the ABC discipline. It demonstrates the validity of this study conducting a co-citation analysis based on the citation data of Google Scholar.

Research limitations/implications – The classification, core articles, and evolution of the ABC literature published in the past two decades benefit academic researchers conducting future studies that build systematically on prior research.

Practical implications – The intellectual structure of the ABC discipline explains and predicts the stages of ABC implementation’s life cycle. For the accounting profession, this helps a consultant/practitioner in sub-fields of the ABC domain to quickly and easily enlarge the coverage and viewpoints or perspectives within his/her cluster of interest and to jointly consider the successful factors of implementing ABC in an organization.

Originality/value – The empirical feasibility of using digitally archival information to model an intellectual structure of ABC is attained; and the intellectual structure and its various representations provide researchers, consultants, and practitioners with a macroscopic and dynamic view of the ABC discipline.

Keywords Google Scholar, Activity-based costing, Citation database, Co-citation analysis, Intellectual structure, Multivariate statistical analysis, Search engines, Internet

Paper type Technical paper

Introduction

In this new digital era, the dramatic switch from print collections of articles to electronic collections in a library has a large impact on researchers, because the latter

The current issue and full text archive of this journal is available at www.emeraldinsight.com/0264-0473.htm

An intellectual

structure of ABC

31

Received 17 March 2012 Revised 14 May 2012 Accepted 31 May 2012The Electronic Library Vol. 32 No. 1, 2014 pp. 31-46

q Emerald Group Publishing Limited

0264-0473 DOI 10.1108/EL-03-2012-0027

method is more convenient and time saving than the former (Zhang et al., 2011). Many libraries also embrace a wide range of databases to further help researchers conduct studies on prior research. In particular, citation databases not only aid academic institutions, federal agencies, publishers, editors, authors, and librarians in conducting citation analysis for hiring, promotion, tenure, funding, and/or reviewer and journal evaluation and selection decisions (Meho and Yang, 2007; Riahinia et al., 2011; Yuan and Hua, 2011), but also provide academic researchers with the number of citations and cited references of a published article for exploring the intellectual structure of scientific specialties through co-citation analysis (Small, 1973; Griffith et al., 1974; White and Griffith, 1981; McCain, 1986, 1990).

Because the bounded rationality of an individual limits researchers from keeping current with the developments and trends of a specific scientific specialty, many studies have employed the co-citation method to objectively explore its intellectual structure (Culnan, 1986, 1987; Ramos-Rodriguez and Ruiz-Navarro, 2004; Acedo et al., 2006; Nerur et al., 2008; Chen and Lien, 2011; Hsiao and Yang, 2011). Conducting a co-citation analysis to model an intellectual structure, needs an appropriate and available citation database as the source of data, however, the Web of Science (WoS) was the only comprehensive database until 2004 and it only provides citation data of academic-oriented articles (Bar-Ilan, 2008). Some disciplines such as activity-based costing (ABC) which is a well-known innovative technique of management accounting, have not been able to conduct the co-citation analysis because they are unable to neglect the important role and contributions of practitioner-oriented articles. Three papers simultaneously published in 2002 address the development of ABC from different perspectives, but Jones and Dugdale (2002) and Lukka and Granlund (2002) qualitatively discoursed the process of ABC construction and development, whereas Bjørnenak and Mitchell (2002) only used descriptive statistics to form the basis of their arguments. The launching of Google Scholar, which includes the citation data of practitioner-oriented and academic-oriented articles, now provides further insight into objectively exploring the core ideas underpinning the ABC discipline.

This work employs the co-citation method to model the first-ever intellectual structure of ABC between 1988 and 2008 based on the citation database of Google Scholar. We find four important subjects and their core articles which provide researchers, consultants, and practitioners with a macroscopic and dynamic view of the ABC’s evolution.

This paper proceeds as follows. We next review in section 2 previous co-citation method and the development of ABC. Section 3 explains the methodology of retrieving core articles, carrying out co-citation and multivariate statistical analyses. Section 4 states the results of multivariate statistical analysis. Section 5 presents the discussion, findings, and implications. Finally, we conclude with the contributions of this work and the limitations.

Literature review Co-citation method

The co-citation method is one of the best-known structuring methods of bibliometrics (Borgman, 1989). Small (1973) proposed the co-citation method to objectively model the intellectual structure of scientific specialties, by assuming that a co-citation matrix is a measure of the perceived similarity or conceptual linkage between two co-cited articles.

EL

32,1

As shown in Figure 1, articles A and B are associated, because they are both cited, i.e. co-cited by articles C, D, E, and F (Garfield, 2001). The number of identical citing articles defines the strength of co-citation between the two cited articles (Small, 1973). The more two articles are cited together, the closer is the relationship between them (White and Griffith, 1981). This relationship only means that authors address similar topics, not that they necessarily agree with each other (Acedo et al., 2006). Small (1973) also stated that frequently cited articles represent the key concepts, methods, or experiments in a field, and co-citation patterns can then be used to map out in great detail the relationships between these key ideas. Hence, they serve as the theoretical and empirical fundamental concepts of a scientific specialty (Small, 1973; Ramos-Rodriguez and Ruiz-Navarro, 2004).

The development of ABC

Activity-based costing (ABC) is a well-known innovative technique of management accounting. It is a costing model that identifies activities in an organization and assigns resource costs through activities to the products and services provided to customers. ABC has been used to support strategic decisions such as pricing, outsourcing, product mix, and the identification and evaluation of process improvement initiatives (Cooper and Kaplan, 1992; Swenson, 1995). The emergence of ABC originated from the new challenges facing US manufacturing businesses from global competition ( Jones and Dugdale, 2002).

Over the past two decades, ABC has spread across many industries among many countries. Simultaneously, this discipline has reached a certain degree of maturity and has accumulated a considerable amount of literature, including academic-oriented and practitioner-oriented articles that have explored various issues (Bjørnenak and Mitchell, 2002). Illuminating what the intellectual structure of ABC is and what dimensions and important parameters are included in its intellectual structure can help

Figure 1. Co-citation

An intellectual

structure of ABC

researchers systematically conduct their studies. Therefore, this study selects cited documents rather than authors as the unit of co-citation analysis since we primarily zoom in on what ABC is, rather than who is developing it.

Methodology

Figure 2 indicates the procedure for conducting a co-citation analysis to form an intellectual structure and its various representations of ABC in this study. We explain it as follows.

Define the scope of ABC articles

For the purpose of modeling an intellectual structure, any study based on the co-citation method must first establish a set of source documents in order to filter the core articles (Callon et al., 1993). Thus, we need a prior delimiting of journals through which the ABC theory is formed and then qualified articles are retrieved. To cover all the developments within the ABC theory, these articles should appear in academic and practitioner accounting journals and Harvard Business Review, based on Lukka and Granlund (2002), Bjørnenak and Mitchell (2002), and Jones and Dugdale (2002) who included the academic and practitioner accounting journals, whereas only Jones and Dugdale (2002) incorporated HBR.

Figure 2. The procedure for constructing an intellectual structure of ABC

EL

32,1

34

Set the conditions of core articles

Based on the three aforementioned articles simultaneously published in 2002, we select a set of source documents on ABC from academic and practitioner accounting journals and HBR between 1988 and 2008. We choose this 20-year period, because the words “activity-based costing” began to appear in the accounting literature in 1988 (Jones and Dugdale, 2002). In addition, McCain (1990) stated “the major controls exerted by the researchers are the selection of citation and co-citation thresholds above which papers will be retrieved”. Thus, this study restricts the frequency of citation for the included articles to be equal or greater than 20. The reason behind the threshold value 20 is that we assume an influential article over the last 20 years should have been cited at least once per year. Retrieve core articles and conduct co-citation analysis

Inputting the keywords “activity-based costing” into Google Scholar’s database, this study obtained 61 journal articles with 3,023 cited references as a source set that is consistent with the aforementioned conditions. Google Scholar counts citations from many sources, including books, working papers, conference proceedings, and so forth, and hence we must filter the cited references of each retrieved article only published in journals, so as to avoid repeatedly computing identical research published in different forms, e.g. both as a thesis and a paper.

The 61 articles are next paired with each other and the co-citation frequency of each pair is computed from referring to the cited references, yielding a 61 £ 61 matrix. We delete articles where a whole row or column in the matrix is zero, because these articles are never co-cited with the others. The co-citation frequency matrix is then transformed to a Pearson correlation matrix, which when compared to a co-citation frequency matrix offers at least two advantages (McCain, 1990; Ramos-Rodriguez and Ruiz-Navarro, 2004):

(1) Data standardization prevents scale effects from the greater difference of citation numbers between two similar articles.

(2) Articles that are not significantly related to any other ones can be deleted. Because the Pearson correlation coefficient is used as the measure of similarity of article-pairs, the higher the positive correlation is, the more similar the two articles are in the perception of citers (McCain, 1990). Thus, we filter out those non-significant related articles with others. The final reduced Pearson correlation matrix is 36 £ 36 based on 1,866 cited references, showing the relationship among the core articles of the ABC theory.

Multivariate statistical analysis

For observing and analyzing the grouping behavior of the evolution of the subject areas in ABC’s intellectual structure, this study further employs multivariate statistical techniques to analyze the 36 £ 36 co-citation correlation matrix that serves as a matrix of inter-article proximities. First, factor analysis is conducted to reduce 36 variables, representing 36 core articles, into a much smaller number of derived variables, i.e. common factors. It reveals the underlying subject matter of the 36 core articles perceived by citers and the contribution of each article to common factors.

Second, we use cluster analysis to group the 36 core articles in order to gain insights into the intellectual organization of ABC. Because cluster analysis is mainly based on

An intellectual

structure of ABC

the real distances of data, each of the 36 articles has a one-to-one mapping to its own group. To properly name groups derived from the factors of factor analysis, we compute and compare the mean scores of each factor on every group.

Third, to provide a visual aid to view the underlying structure of these groups based on cluster analysis, we use multidimensional scaling (MDS) to display the perceptual mapping of multivariate data in a two-dimensional space and measure its stress value and R-square to test the goodness-of-fit.

In short, factor analysis and MDS complement and enrich the information of cluster analysis.

The results Factor analysis

This study uses a principal components analysis with varimax rotation to extract common factors above an eigenvalue of 1, which is the most common method for co-citation analysis (McCain, 1990). Consequently, it produces four uncorrelated factors representing four subjects to explain 85.47 percent of total variance. Most articles have a high loading on only one factor as shown in Table I.

The purpose of factor analysis is to extract common factors representing the underlying subject matter of the 36 core articles perceived by citers. We use varimax rotation to produce four uncorrelated factors with high loading on only one factor for most articles in order to facilitate the distinction between different subjects. A factor loading indicates an article’s contribution to a factor. It is likely that a positive loading indicates a positive relationship with a factor. It is also likely that a negative loading presents a negative (reverse) relationship with a factor. A negative loading is as important as a positive loading. In general, only articles with loadings greater than

^0.7 are likely to be useful in interpreting or naming a factor, and factor loadings

above ^ 0.4 or ^ 0.5 are listed. Table I shows those factor loadings above ^ 0.5. On the one hand, we can use a few articles with higher loadings (either positive or negative) to name a factor. On the other hand, we also can identify the breadth of contributions of an article, i.e. whether it is a cross loading (McCain, 1990; Acedo et al., 2006).

Acedo et al. (2006) stated “articles with positive loads and those with negative loads in the same factor exhibit a disparity or divergence of theoretical developments or discussion topics, so other researchers do not tend to cite them together”. In other words, an article with a negative loading on a factor indicates that it reverses or disagrees with other articles of the same factor although they are discussing the same subject.

Factor 1 accounts for the largest variance of 44.27 percent. It has higher positive loadings on McGowan and Klammer (1997), Krumwiede (1998), Swenson (1995), Anderson (1995), Foster and Swenson (1997), Argyris and Kaplan (1994), Ittner et al. (2002), Anderson and Young (1999), and Shields (1995). Since these articles primarily explore how ABC effectively circulates and disseminates in an organization, it can be labeled as “implementation and diffusion”.

Factor 2 in this analysis explains 20.45 percent of the total variance, with higher positive loadings on Armstrong (2002), Briers and Chua (2001), and Granlund (2001). These articles study the impacts of technical innovation and introduction on society and social behavior, bringing not only benefits, but also risks. Thus, we name this factor “benefits and risks”.

EL

32,1

Factor 3 explains 14.90 percent of the total variance and has higher positive loadings on Cooper and Kaplan (1991, 1992) and Cooper (1988). These articles mainly address the fundamental concepts of the ABC technique. We name the factor “fundamental concepts”. Factor 4 only explains 5.87 percent of total variance, although its eigenvalue is greater than 1.0. It has a higher negative loading on Cooper and Kaplan (1988) who

Factorsa

Variables 1 2 3 4

31. McGowan, A.S. and Klammer, T.P. (1997) 0.973 27. Krumwiede, K.R. (1998) 0.970

36. Swenson, D. (1995) 0.968

01. Anderson, S.W. (1995) 0.963 18. Foster, G. and Swenson, D. (1997) 0.958 03. Argyris, C. and Kaplan, R.S. (1994) 0.951 23. Ittner, C.D., Lanen, W.N. and Larcker, D.F. (2002) 0.934 02. Anderson, S.W. and Young, S.M. (1999) 0.931 35. Shields, M.D. (1995) 0.918

29. Malmi, T. (1997) 0.854

19. Gosselin, M. (1997) 0.846 22. Innes, J., Mitchell, F. and Sinclair, D. (2000) 0.813 21. Innes, J. and Mitchell, F. (1995) 0.790

30. Malmi, T. (1999) 0.789

32. Ness, J.A. and Cucuzza, T.G. (1995) 0.770 08. Bjørnenak, T. (1997) 0.754 0.548 28. Maher, M.W. and Marais, M.L. (1998) 0.743 16. Drake, A.R., Haka, S.F. and Ravenscroft, S.P. (1999) 0.703 05. Babad, Y.M. and Balachandran, B.V. (1993) 2 0.647

04. Armstrong, P. (2002) 0.878

09. Briers, M. and Chua, W.F. (2001) 0.877

20. Granlund, M. (2001) 0.830

06. Banker, R.D. and Johnston, H.H. (1993) 2 0.796 24. Jones, T.C. and Dugdale, D. (2002) 0.733 07. Bhimani, A. and Pigott, D. (1992) 0.643 0.690 15. Datar, S. and Gupta, M. (1994) 2 0.641

26. Kee, R. (1995) 2 0.510

13. Cooper, R. and Kaplan, R.S. (1991) 0.914 14. Cooper, R. and Kaplan, R.S. (1992) 0.886

10. Cooper, R. (1988) 0.869

17. Foster, G. and Gupta, M. (1990) 0.620

33. Noreen, E. (1991) 0.616

25. Kaplan, R.S. and Anderson, S.R. (2004) 2 0.525 0.578

11. Cooper, R. (1989) 0.554 2 0.501

12. Cooper, R. and Kaplan, R.S. (1988) 2 0.740 34. Noreen, E. and Soderstrom, N. (1994) 0.718

Eigenvalue 15.936 7.362 5.360 2.112

Variance (%) 44.267 20.449 14.890 5.867 Cumulative % 44.267 64.715 79.605 85.473 Notes: aFactor loading above ^ 0.5 is listed; Factor 1 ¼ Implementation and diffusion;

Factor 2 ¼ Benefits and risks; Factor 3 ¼ Fundamental concepts; Factor 4 ¼ Methodology and validation

Table I. Results of factor analysis

An intellectual

structure of ABC

advocated ABC, providing more accurate cost information to assist management decision makings. In addition, this factor has a higher positive loading on Noreen and Soderstrom (1994) who challenged the assumption of ABC for overhead costs strictly in proportion to activity. Both of the two articles apply a critical type of methodology and validation of ABC although they expressed a divergently theoretical development. Thus, we name this factor “methodology and validation”.

Finally, we remind readers that these factors might be somewhat differently named, and somewhat differently interpreted, due to subjective professional judgments. Cluster analysis

Using cluster analysis to group articles provides insights into the intellectual organization of ABC (McCain, 1990). We use squared Euclidean distance and Ward’s method to present the cluster dendrogram as shown in Figure 3. It identifies different groups of 36 core articles based on their homogeneity of being cited. Based on a larger distance between four and six groups, this work determines the number of groups to be four. To name groups derived from the factors of factor analysis, we compute and compare the mean scores of four factors on each group in Table II.

Figure 3.

Hierarchical clustering of 36 core articles

Group 1 Group 2 Group 3 Group 4

na¼ 6 n ¼ 8 n ¼ 18 n ¼ 4

Factor 1 score 2 0.20 2 1.23c 0.85b 2 1.06 Factor 2 score 2 0.20 2 1.03c 0.11 1.86b Factor 3 score 1.62b 2 0.27 2 0.22 2 0.91c

Factor 4 score 0.24b 2 0.31c 0.04 0.10

Notes:aindicates that n is the number of papers in a group;bindicates the highest mean score of a

factor among the four groups;cindicates the lowest mean score of a factor among the four groups Table II.

Mean scores of four factors on the four groups

EL

32,1

Table II indicates the highest and lowest mean scores of a factor among the four groups as b and c superscripts, respectively. Note that Groups 3, 4, and 1 correspondingly score the highest mean factor scores among the four groups on Factors 1, 2, and 3. Therefore, we name Groups 3, 4, and 1 respectively as “implementation and diffusion”, “benefits and risks”, and “fundamental concepts” derived from Factors 1, 2, and 3 of factor analysis. Furthermore, Group 2 has the lowest (negative) mean factor scores on Factors 1, 2, and 4. Thus, we name Group 2 as “methodology and validation” derived from Factor 4. This categorization makes sense, because Group 2 is formed exactly by five articles with negative loadings that respectively reverse Factors 1 or 2 as well as three articles in Factor 4.

Based on the hierarchical clustering as shown in Figure 3, we finally name Cluster I as the “technical aspect”, which includes Groups 1 and 2. Cluster II is the “social aspect” combining Groups 3 and 4. Table III shows the results of cluster analysis and the contents of each group will be examined in the following discussion section. Multidimensional scaling analysis

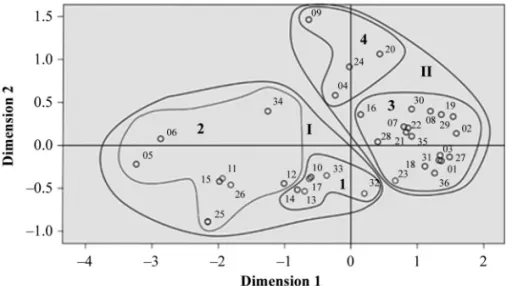

This study employs MDS analysis to perceptually map 36 articles in a two-dimensional map as shown in Figure 4, visualizing the conceptual distances between one other. We further depict the four groups based on cluster analysis in order to gain insight into the position and attributes of each group. Points with high similarities are placed close together in intellectual space, while points with high dissimilarities are placed farther apart. However, owing to the simplification of reducing space for the purpose of visualization, this necessarily distorts the original data somewhat and cannot account for all the variance in the proximity matrix (McCain, 1990). For example, point 12 is shown to be in Group 2, but appears to be in very close proximity to Group 1. McCain (1990) suggested that a higher stress value, but usually less than 0.2, is considered an acceptable trade-off for a two- or three-dimensional solution if the R-Square is high. In this work, the stress value of 0.1582 and RSQ of 0.9445 indicate an acceptable goodness-of-fit for the co-citation matrix.

Discussion and findings

After conducting the co-citation and multivariate statistical analyses, we obtain a model of intellectual structure and its various representations of the 36 core articles of ABC as shown in Table III and Figure 4, which consists of the four groups: fundamental concepts, methodology and validation, implementation and diffusion, and benefits and risks. They can be further grouped as Cluster I, the technical aspect, and Cluster II, the social aspect. Within the two-dimensional map, the proximity of core articles or groups reflects the perceived similarity in some dimensions. The dimensions include subject areas, research specialties, schools of thought, shared intellectual styles, or temporal period (McCain, 1990). Therefore, this work ascertains the dimensions of articles within groups as concisely listed in Table IV, which includes publication year, publication journal, research method, and research content.

From the publication year viewpoint as shown in Table IV, these articles are distributed from 1988 to 2004, apart from 1996 and 2003. Owing to the time frame and co-citation methodology of this study, the results present an archival view of ABC that is in favor of the ideas represented by the older articles. There is hence no way that a recently published journal article can be qualified as a core article. In addition, from the

An intellectual

structure of ABC

Cluster Group

Cluster I: Technical aspect Group 1: Fundamental concepts

10. Cooper, R. (1988) Journal of Cost Management 14. Cooper, R. and Kaplan, R.S. (1992) Accounting Horizons 13. Cooper, R. and Kaplan, R.S. (1991) Harvard Business Review 17. Foster, G. and Gupta, M. (1990) Journal of Accounting and Economics 33. Noreen, E. (1991) Journal of Management Accounting Research 32. Ness, J.A. and Cucuzza, T.G. (1995) Harvard Business Review Group 2: Methodology and validation

11. Cooper, R. (1989) Journal of Cost Management

12. Cooper, R. and Kaplan, R.S. (1988) Harvard Business Review 25. Kaplan, R.S. and Anderson, S.R. (2004) Harvard Business Review 26. Kee, R. (1995) Accounting Horizons

15. Datar, S. and Gupta, M. (1994) Accounting Review

05. Babad, Y.M. and Balachandran, B.V. (1993) Accounting Review 06. Banker, R.D. and Johnston, H.H. (1993) Accounting Review 34. Noreen, E. and Soderstrom, N. (1994) Journal of Accounting and Economics

Cluster II: Social aspect Group 3: Implementation and diffusion

27. Krumwiede, K.R. (1998) Journal of Management Accounting Research

31. McGowan, A.S. and Klammer, T.P. (1997) Journal of Management Accounting Research

01. Anderson, S.W. (1995) Journal of Management Accounting Research 36. Swenson, D. (1995) Journal of Management Accounting Research 03. Argyris, C. and Kaplan, R.S. (1994) Accounting Horizons 18. Foster, G. and Swenson, D. (1997) Journal of Management Accounting Research

02. Anderson, S.W. and Young, S.M. (1999) Accounting Organizations and Society

23. Ittner, C.D., Lanen, W.N. and Larcker, D.F. (2002) Journal of Accounting Research

19. Gosselin, M. (1997) Accounting Organizations and Society 35. Shields, M.D. (1995) Journal of Management Accounting Research 08. Bjørnenak, T. (1997) Management Accounting Research

29. Malmi, T. (1997) Management Accounting Research

22. Innes, J., Mitchell, F. and Sinclair, D. (2000) Management Accounting Research

30. Malmi, T. (1999) Accounting Organizations and Society

07. Bhimani, A. and Pigott, D. (1992) Management Accounting Research 21. Innes, J. and Mitchell, F. (1995) Management Accounting Research 28. Maher, M.W. and Marais, M.L. (1998) Journal of Accounting Research 16. Drake, A.R., Haka, S.F. and Ravenscroft, S.P. (1999) Accounting Review

Group 4: Benefits and risks

20. Granlund, M. (2001) Management Accounting Research

24. Jones, T.C. and Dugdale, D. (2002) Accounting Organizations and Society

04. Armstrong, P. (2002) Accounting Organizations and Society 09. Briers, M. and Chua, W.F. (2001). Accounting Organizations and Society Table III. Results of cluster analysis

EL

32,1

40

publication journal viewpoint as shown in Table IV, all core articles are published in nine famous journals, including both academic-oriented and practitioner-oriented journals. The research method viewpoint primarily encompasses conceptual analysis, statistical studies, mathematical modeling, and case studies. This study further combines the above three viewpoints with the research contents to find the evolution and trends of ABC as follows.

Evolution and trends

We find that four important subjects, including fundamental concepts, methodology and validation, implementation and diffusion, and benefits and risks, chronologically provide a panoramic view of the evolution of ABC. From the late 1980s to early 1990s, some articles that expounded upon the meanings, nature, and functions of the ABC technique established its fundamental concepts, as shown in Group 1. Nearly all these articles have been published in practitioner journals, particularly in Journal of Cost Management and Harvard Business Review. After a large number of firms implemented these ideas in the real world, many researchers engaged in analyzing a variety of phenomena from the technical, behavioral, organizational, contextual, and diffusion perspectives through means of scientific research from a neutral position. Consequently, subsequent articles as shown in Group 2 regarding validating and arguing ABC hypotheses appeared with positive and negative sentiments in the first half of the 1990s. After the mid-1990s, a large number of articles, as shown in Group 3 “Implementation and diffusion”, discussed how ABC effectively circulates in an organization and is widely disseminated. After the 2000s, when ABC had already been developed for a long time, as shown in Group 4, academics discussed society and social behaviors of ABC’s development process and criticized the benefits and risks from a sociological perspective.

The findings’ phenomena are in accordance with Lukka and Granlund’s (2002) arguments about different literary products produced at the different phases of the

Figure 4. Four groups on multidimensional scaling

An intellectual

structure of ABC

41

Groups Technical aspect Social aspect Dimensions Fundamental concepts Methodology and validation Implementation and diffusion Benefits and risks Publication year 1988, 1990, 1991(2) a, 1992, 1995 1988,1989,1993(2),1994(2), 1995, 2004 1992, 1994, 1994-2002 (16) 2001(2), 2002(2) Publication journal Practitioner-oriented (3) Academic-oriented (3) Practitioner-oriented (3) Academic-oriented (5) Academic-oriented (18) Academic-oriented (4) Research method Conceptual analysis (4) Statistical studies (1) Mathematical modeling (1) Conceptual analysis (3) Statistical studies (2) Mathematical modeling (3) Conceptual research (1) Statistical studies (14) Case studies (3) Conceptual research (1) Case studies (3) Research contents Expounding upon the meanings, nature, and functions of the ABC technique Validating and arguing ABC hypotheses that appear with positive and negative sentiments Discussing how ABC effectively circulates in an organization and is widely disseminated Discussing society and social behaviors of ABC’s development process and criticizing the benefits and risks from a sociological perspective Note: a The number in parenthesis indicates the number of core articles Table IV.

Characteristics of the four groups

EL

32,1

ABC development process. Articles published at the initial phase are inclined to have a conceptual construction and strong practicability. Adopting mathematical modeling, statistical studies, and case studies then profoundly turned to describe, understand, and explain the phenomenon that had occurred. Finally, the theory is more fundamentally evaluated into a wider organizational and social context.

We agree with Jones and Dugdale (2002) who portrayed ABC as a socio-technical expert system that is the joint optimization of an organization’s technical and social aspects. The intellectual structure consists of much more discussion-oriented technical and social aspects, which explain the challenges of implementing ABC due not only to technical limitations, but also requirements in the contextual environment, organizational behavior, and managerial system.

Implications

The findings of this study, including the classification, core articles, and evolution of the ABC literature published in the past two decades, benefit academic researchers conducting future studies that build systematically on prior research. For the accounting profession, the intellectual structure herein helps a consultant/practitioner in a sub-field of the ABC domain (he or she might be only in one of the camps) with the knowledge that this consultant/practitioner can quickly and easily enlarge the coverage and viewpoints or perspectives within his/her cluster of interest. Additionally, the core articles of each subject in the two-dimensional map allow them to quickly visualize and master those factors that need joint consideration to ensure the success of ABC implementation. For a company new to implementing an ABC system, the evolution stages of Figure 4 will let it know what issues lay ahead so that it can prepare resources and efforts to overcome those issues. As one veteran ABC manager pointed out, the evolution of the four groups in Figure 4 indeed depicts the industry reality. Especially valuable is his comment warning that a company evolving at stage four will face a certain trade-off in using ABC as a tool, because the complexity of customer types, product-mix, and process variations make the calculation of standard ABC costs difficult. Figure 4 explains and predicts the stages of ABC implementation’s life cycle.

Conclusions and limitations

This study presents three contributions. First, this study models the first intellectual structure of the ABC discipline through the document co-citation analysis and multivariate statistical analysis based on the citations database of Google Scholar. The results of this study illuminate the main ideas underpinning the ABC discipline. We find that four subjects – fundamental concepts, methodology and validation, implementation and diffusion, and benefits and risks – chronologically provide a panoramic view of the evolution of ABC. The core articles herein present a variety of viewpoints, both positive and negative, for each subject of this intellectual structure. There are not only technical limitations, but also considerations within the contextual environment, organizational behavior, and managerial system for implementing ABC as a socio-technical system.

Second, this study aids researchers/consultants/practitioners in breaking through the plights of bounded rationality in order to keep current with the developments and trends of the ABC discipline. The findings of this study quickly broaden a researcher/consultant/practitioner’s ABC knowledge so as to more effectively and efficiently conduct their works.

An intellectual

structure of ABC

Third, this study shows the empirical feasibility that Library Science can be applied to exploring a macroscopic and dynamic view of the ABC discipline. Due to the advent of digital documents along with the development of electronic database, we suggest that this methodology be extended and applied to other disciplines.

Finally, we have realized some limitations. One limitation of this study is that the results present an archival view of ABC that is in favor of the ideas represented by older articles, owing to the time frame and co-citation methodology. In other words, an article with a short time span normally accumulates less reference counts than older articles. Therefore, there is no way that a recently published journal article could qualify as a core article. Additionally, authors may cite articles that are just more popular and well known, but not necessarily more important, i.e. an article can have a higher number of citations, but not necessarily provide more value.

References

Acedo, F.J., Barroso, C. and Galan, J.L. (2006), “The resource-based theory: dissemination and main trends”, Strategic Management Journal, Vol. 27 No. 7, pp. 621-636.

Anderson, S.W. (1995), “A framework for assessing cost management system changes: the case of activity based costing implementation at General Motors, 1986-1993”, Journal of Management Accounting Research, Vol. 7, pp. 1-51.

Anderson, S.W. and Young, S.M. (1999), “The impact of contextual and process factors on the evaluation of activity-based costing systems”, Accounting Organizations and Society, Vol. 24 No. 7, pp. 525-559.

Argyris, C. and Kaplan, R.S. (1994), “Implementing new knowledge: the case of activity-based costing”, Accounting Horizons, Vol. 8, pp. 83-84.

Armstrong, P. (2002), “The costs of activity-based management”, Accounting Organizations and Society, Vol. 27 Nos 1-2, pp. 99-120.

Bar-Ilan, J. (2008), “Which h-index?-comparison of WoS, Scopus and Google Scholar”, Scientometrics, Vol. 74 No. 2, pp. 257-271.

Bjørnenak, T. and Mitchell, F. (2002), “The development of activity-based costing journal literature, 1987-2000”, European Accounting Review, Vol. 11 No. 3, pp. 481-508.

Borgman, C.L. (1989), “Bibliometrics and scholarly communication: Editor’s introduction”, Communication Research, Vol. 16 No. 5, pp. 583-599.

Briers, M. and Chua, W.F. (2001), “The role of actor-networks and boundary objects in management accounting change: a field study of an implementation of activity-based costing”, Accounting Organizations and Society, Vol. 26 No. 3, pp. 237-269.

Callon, M., Courtial, J.P. and Penan, H. (1993), La scientometrie, Presses Universitaires de France, Paris.

Chen, L.C. and Lien, Y.H. (2011), “Using author co-citation analysis to examine the intellectual structure of e-learning: a MIS perspective”, Scientometrics, Vol. 89, pp. 867-886.

Cooper, R. (1988), “The rise of activity-based costing-part one: what is an activity-based cost system?”, Journal of Cost Management, Vol. 2 No. 2, pp. 45-54.

Cooper, R. and Kaplan, R.S. (1991), “Profit priorities from activity-based costing”, Harvard Business Review, Vol. 69 No. 3, pp. 130-135.

Cooper, R. and Kaplan, R.S. (1992), “Activity-based systems: measuring the costs of resource usage”, Accounting Horizons, Vol. 6 No. 3, pp. 1-13.

EL

32,1

Culnan, M.J. (1986), “The intellectual development of management information systems, 1972-1982: a co-citation analysis”, Management Science, Vol. 32 No. 2, pp. 156-172. Culnan, M.J. (1987), “Mapping the intellectual structure of MIS, 1980-1985: a co-citation analysis”,

Management Information Systems Quarterly, Vol. 11 No. 3, pp. 341-353.

Foster, G. and Swenson, D. (1997), “Measuring the success of activity-based costing management and its determinants”, Journal of Management Accounting Research, Vol. 9, pp. 109-141. Garfield, E. (2001), “From bibliographic coupling to co-citation analysis via algorithmic historio-bibliography”, speech delivered at Drexel University, Philadelphia, PA, 27 November.

Granlund, M. (2001), “Towards explaining stability in and around management accounting systems”, Management Accounting Research, Vol. 12 No. 2, pp. 141-166.

Griffith, B.C., Small, H.G., Stonehill, J.A. and Dey, S. (1974), “The structure of scientific literatures II: toward a macro-and microstructure for science”, Science Studies, Vol. 4, pp. 339-365. Hsiao, C.H. and Yang, C. (2011), “The intellectual development of the technology acceptance

model: a co-citation analysis”, International Journal of Information Management, Vol. 31 No. 2, pp. 128-136.

Ittner, C.D., Lanen, W.N. and Larcker, D.F. (2002), “The association between activity-based costing and manufacturing performance”, Journal of Accounting Research, Vol. 40 No. 3, pp. 711-726.

Jones, T.C. and Dugdale, D. (2002), “The ABS bandwagon and the juggernaut of modernity”, Accounting Organizations and Society, Vol. 27 Nos 1-2, pp. 121-163.

Krumwiede, K.R. (1998), “The implementation stages of activity-based costing and the impact of contextual and organizational factors”, Journal of Management Accounting Research, Vol. 10, pp. 239-277.

Lukka, K. and Granlund, M. (2002), “The fragmented communication structure within the accounting academia: the case of activity-based costing research genres”, Accounting Organizations and Society, Vol. 27 Nos 1-2, pp. 165-190.

McCain, K.W. (1986), “Cocited author mapping as a valid representation of intellectual structure”, Journal of the American Society for Information Science, Vol. 37 No. 3, pp. 111-122. McCain, K.W. (1990), “Mapping authors in intellectual space: a technical overview”, Journal of the

American Society for Information Science, Vol. 41 No. 6, pp. 433-443.

McGowan, A.S. and Klammer, T.P. (1997), “Satisfaction with activity-based cost management implementation”, Journal of Management Accounting Research, Vol. 9, pp. 217-238. Meho, L.I. and Yang, K. (2007), “Impact of data sources on citation counts and rankings of LIS

faculty: Web of Science versus Scopus and Google Scholar”, Journal of the American Society for Information Science and Technology, Vol. 58 No. 13, pp. 2105-2125.

Nerur, S.P., Rasheed, A.A. and Natarajan, V. (2008), “The intellectual structure of the strategic management field: an author co-citation analysis”, Strategic Management Journal, Vol. 29 No. 3, pp. 319-336.

Noreen, E. and Soderstrom, N. (1994), “Are overhead costs strictly proportional to activity? Evidence from hospital departments”, Journal of Accounting and Economics, Vol. 17 Nos 1-2, pp. 255-278.

Ramos-Rodriguez, A.R. and Ruiz-Navarro, J. (2004), “Changes in the intellectual structure of strategic management research: a bibliometric study of the Strategic Management Journal, 1980-2000”, Strategic Management Journal, Vol. 25 No. 10, pp. 981-1004.

Riahinia, N., Zandian, F. and Azimi, A. (2011), “Web citation persistence over time: a retrospective study”, The Electronic Library, Vol. 29 No. 5, pp. 609-620.

An intellectual

structure of ABC

Shields, M.D. (1995), “An empirical analysis of firms’ implementation experiences with activity-based costing”, Journal of Management Accounting Research, Vol. 7 No. 3, pp. 148-161.

Small, H. (1973), “Co-citation in the scientific literature: a new measure of the relationship between two documents”, Journal of the American Society for Information Science, Vol. 24 No. 4, pp. 265-269.

Swenson, D. (1995), “The benefits of activity-based cost management to the manufacturing industry”, Journal of Management Accounting Research, Vol. 7, pp. 167-180.

White, H.D. and Griffith, B.C. (1981), “Author cocitation: a literature measure of intellectual structure”, Journal of the American Society for Information Science, Vol. 32 No. 3, pp. 163-171.

Yuan, S. and Hua, W. (2011), “Scholarly impact measurements of LIS open access journals: based on citations and links”, The Electronic Library, Vol. 29 No. 5, pp. 682-697.

Zhang, L., Ye, P., Liu, Q. and Rao, L. (2011), “Survey on the utilization of NSTL electronic resources in colleges and universities in Wuhan, China”, The Electronic Library, Vol. 29 No. 6, pp. 828-840.

About the authors

Hsiu-Kuei Kuo gained a Masters’ degree in Accounting from National Cheng Kung University and an MBA in Management Science from National Chiao Tung University in Taiwan. She is currently a PhD student in the Institute of Business and Management as well as a Lecturer in the Department of Transportation Technology and Management at National Chiao Tung University in Taiwan. Her current research interest includes accounting, performance evaluation, digital libraries, and electronic information systems. Hsiu-Kuei Kuo is the corresponding author and can be contacted at: kuei.kuo@gmail.com

Chyan Yang gained his PhD in Computer Science from University of Washington, Seattle. He also holds an MS in Information Science from Georgia Institute of Technology and an MBA in Management Science from National Chiao Tung University. He received his BS in Electrical Engineering at National Chiao Tung University. Between 1987 and 1992 he worked as an Assistant Professor in the Department of Electrical and Computer Engineering, US Naval Postgraduate School at Monterey, California. From 1992 to 1995 he was with the Institute of Management Science, National Chiao Tung University, Taiwan, as an Associate Professor. Chyan Yang is now a Professor in the Institute of Business and Management at National Chiao Tung University, Taiwan. He has been an IEEE senior member since 1992 and has has published more than 60 journal papers and 90 conference papers. His researches have been published in various SCI and SSCI journals including The Electronic Library, Journal of the American Society for Information Science and Technology, Research-Technology Management, International Journal on Information Management, IEEE Journal on Selected Areas in Communications, Industrial Marketing Management, International Journal of Manpower and Computers in Human Behavior. His current researches include information management, and strategic management. He has also worked as an advisor to several IT companies.

EL

32,1

46

To purchase reprints of this article please e-mail: reprints@emeraldinsight.com Or visit our web site for further details: www.emeraldinsight.com/reprints