New Evidence on US Current Account Sustainability

21

0

0

全文

(2) 2. International Journal of Business and Economics. might impose excessive burden on future generations, as the accumulation of large external debt could imply increasing interest payments and lower standards of living. Empirically, the stationarity of the current account has been tested by many authors, most of them rejecting this hypothesis with traditional unit-root tests (e.g., Trehan and Walsh, 1991; Gundlach and Sinn, 1992; Otto, 1992; Wickens and Uctum, 1993; Liu and Tanner, 1996; Wu, 2000; Lau et al., 2006). Evidence of nonstationarity is obtained in Glick and Rogoff (1995) and Bergin (2001). On the other hand, stationarity in the current account series is suggested by Bergin and Sheffrin (2000). Another approach to examine the stationarity of current accounts is based on cointegration between exports and imports, testing the restriction that the cointegrating vector is (1, −1) , as in Husted (1992), Fountas and Wu (1999), and Arize (2002). This approach focuses on the long-run relationship between exports and imports and imposes that both individual variables are integrated of order 1. As in the previous case, these studies have yielded conflicting evidence depending on the economies, the sample period, and the testing procedures considered. While some studies, such as Husted (1992) or Arize (2002), show that there is a long-run relationship between imports and exports for the US case, implying that trade deficits are sustainable, other studies, such as Fountas and Wu (1999), show that the hypothesis of no long-run relationship cannot be rejected, concluding that the US trade deficits are not sustainable. In this article, we re-examine the external sustainability issue using an approach based on fractional integration for the US current account. We examine the orders of integration of exports and imports in the US economy by means of various procedures for testing order of integration ( I(d ) ) statistical models. Moreover, we also examine the difference between exports and imports from a fractional viewpoint; that is, we test the order of integration in a cointegrating relationship based on the assumption that the cointegrating vector is (1, −1) . If the order of integration of the differenced series is smaller than the values obtained for the individual series, there is a long-run equilibrium relationship between exports and imports and the deficit is sustainable. The outline of the paper is as follows. In Section 2 we provide a brief motivation for the use of time series models to analyze external sustainability. Section 3 briefly presents the testing procedures. Section 4 reports the empirical results using quarterly data on imports and exports in the US for the time period 1960:Q1–2006:Q3. In Section 5 we examine the possibility of structural breaks, while Section 6 contains concluding comments. 2. External Sustainability Model Following Husted (1992), the current budget constraint can be expressed as: C0 = Y0 + B0 − I 0 (1 + r0 ) B−1 ,. (1).

(3) 3. Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. where C0 is current consumption, Y0 is output, I 0 is investment, r0 is the one period world interest rate, B0 is international borrowing (which could be positive or negative), and (1 + r0 ) B−1 is the historically given initial debt of the representative agent, corresponding to the country’s external debt. In order to obtain the intertemporal budget constraint, we iterate equation (1) forward, obtaining: ∞. B0 = ∑ μtTBt + lim μ n Bn , n→∞. (2). t =1. where TBt = X t − M t = Yt − Ct − I t is the trade balance for period t and X t and M t are respectively exports and imports for period t . Defining λ0 = 1 (1 + r0 ) , μt is the discount factor, defined as the product of the first t values of λ . Equation (2) states that the amount a country borrows (or lends) in international capital markets must equal the present value of future trade surpluses given that the limit in (2) should equal zero. If that limit is strictly negative, the economy’s expenditure exceeds the present value of its output by an amount that never converges to zero; that is, the economy is bubble financing its expenditures. The opposite situation, where the limit is strictly positive, can also be ruled out since lending less increases the amount of resources available for domestic consumption at no additional cost. In order to derive a testable empirical model, we need to rewrite (1). Assuming that the world interest rate is stationary with unconditional mean r , we can write: Z t + (1 + r ) Bt −1 = X t + Bt ,. (3). where Z t = M t + (rt − r ) Bt −1 , and solving (3) we obtain: ∞. [. ]. M t + rt Bt −1 = X t + ∑ λ j −1 ΔX t + j − ΔZ t + j + lim λt + j Bt + j , j =0. j →∞. (4). where λ = 1 (1 + r ) and Δ = (1 − L) is the first difference operator. The left-hand side of (4) represents spending on imports and interest payments on net foreign debt. We assume that X and Z are both nonstationary I(1) processes: X t = α1 + X t −1 + ε 1t , Z t = α 2 + Z t −1 + ε 2 t ,. (5) (6). where (α j ) j =1, 2 are drift parameters and the (ε jt ) j =1, 2 are stationary I(0) processes, defined as processes with positive and finite spectral density functions. In this case, (4) can be expressed as: X t = α + MM t − lim λt + j Bt + j + ε t , j →∞. (7).

(4) 4. International Journal of Business and Economics. where MM t = M t + rt Bt −1 , α = [(1 + r ) 2 r ](α 2 − α1 ) , and ε t = ∑ j =0 λ j −1 (ε 2 , t + j − ε 1, t + j ) . Then, if the limit term in the above expression equals zero, (7) can be transformed into a standard regression equation: ∞. X t = a + bMM t + et ,. (8). and we should expect b = 1 , and { et } stationary I(0) . Note that straightforward algebra leads to the equation ε t = λε t +1 + λ−1 (ε 2 t − ε 1t ) , which may be expressed in terms of an first-order autoregressive ( AR(1) ) process. If these conditions hold, it means that the balance of the current account, on average, equals zero, and hence that the current account is sustainable. If b < 1 while the residuals remain stationary, we can conclude that X t and MM t share an equilibrium, though it will not satisfy the intertemporal budget constraint since it implies a continuously deteriorating current account balance. Lastly, if stationarity cannot be confirmed, we conclude that X t and MM t are not cointegrated, which means that the variables do not converge towards a long-term equilibrium and, therefore, that sustainability does not hold. The reason for making the distinction between these two unsustainable cases, i.e., cointegration with b < 1 and no cointegration, is simply because they portray different degrees of unsustainability. Remember that b = 1 is a relatively strong condition for sustainability. There exist a number of cointegration tests (e.g., Engle and Granger, 1987; Johansen, 1991), which are all well documented in the literature. However, all these methods are based on what may be called “classical” cointegration in the sense that they assume (or test in an “a priori” step) that the individual series are I(1) , while the equilibrium errors must be I(0) stationary. In this article we extend that approach and consider fractional orders of integration in the individual and in the differenced series. Given an I(0) process { ut , t = 0, ± 1, K }, we say that { xt , t = 0, ± 1, K } is I(d ) if: (1 − L) d xt = ut , t = 1, 2,K ,. (9). where the polynomial on the left-hand side above can be expressed in terms of its binomial expansion such that, for all real d : ∞ ⎛d ⎞ d (d − 1) 2 (1 − L) d = ∑ ⎜⎜ ⎟⎟ (−1) j Lj = 1 − dL + L −K . 2 j =0 ⎝ j ⎠. If d > 0 , xt is said to have long memory because of the strong association between observations widely separated in time. The fractional differencing parameter d plays a crucial role from both theoretical and empirical viewpoints. If d < 0.5 , xt is covariance stationary and mean-reverting, with the effect of the shocks dying away in the long run. If d ∈ [0.5, 1) , xt is no longer covariance stationary but is still mean-reverting, while d ≥ 1 implies nonstationarity and non-mean-reversion. Thus,.

(5) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 5. the fractional differencing parameter d plays a crucial role for our understanding of the economy and economic planning. In particular, a variable having a unit root supports the view that any shock to the economic system will have a permanent effect, so a policy action will be required to bring the variable back to its original long-term projection. On the other hand, if d < 1 , fluctuations will be transitory and, therefore, there is less need for policy action, since the series will in any case return to its trend sometime in the future. 3. The Testing Procedures. Most commonly-used unit-root tests (e.g., Dickey and Fuller, 1979; Phillips and Perron, 1988) have been developed in AR alternatives of the form: (1 − ρL) xt = ut ,. (10). where the unit-root null corresponds to: H0 : ρ = 1.. (11). Conspicuous features of these methods for testing unit roots are the non-standard nature of the null asymptotic distributions which are involved and the absence of Pitman efficiency. This is associated with the radically variable long-run properties of AR processes around the unit root. Under (10), xt is explosive for ρ > 1 , covariance stationary for ρ < 1 , and nonstationary but non-explosive for ρ = 1 . In view of these abrupt changes, the fractional processes have become rival alternatives to the AR model when testing unit roots. There exist many approaches when estimating and testing the fractional differencing parameter d (see, e.g., Fox and Taqqu, 1986; Sowell, 1992). In this article we use both parametric and semiparametric methods. 3.1 A Parametric Testing Procedure. Robinson (1994) proposes a Lagrange multiplier (LM) test of the null hypothesis: H 0 : d = d0 ,. (12). for any real value d 0 in a model given by (9) and where the xt can be the errors in a regression model: yt = β ′ zt + xt ,. (13). where β = ( β1 ,K, β k )T is a k ×1 vector of unknown parameters and z t is a k ×1 vector of deterministic regressors that may include, for example, an intercept (e.g.,.

(6) 6. International Journal of Business and Economics. zt ≡ 1 ) or an intercept and a linear time trend (e.g., zt = (1, t )T ). Clearly, the unit root corresponds then to the null hypothesis: H0 : d = 1 .. (14). Fractional and AR departures from (11) and (14) have very different long-run implications. In (9), xt is nonstationary but non-explosive for all d ≥ 0.5 . As d increases beyond 0.5 and through 1, xt can be viewed as becoming “more nonstationary” (in the sense, for example, that the variance of partial sums increases in magnitude), but it does so gradually, unlike in the cases of (10) around (11). The functional form of the test statistic (denoted rˆ ) can be found in Robinson (1994). He showed that under certain regularity conditions: rˆ →d N (0,1) as T → ∞ ,. (15). where →d means convergence in distribution. Thus, we are in a classical largesample testing situation, and the conditions on ut in (9) are far more general than normality, with a moment condition only of order 2 required. 3.2 A Semiparametric Estimation Method. Robinson’s (1995) Gaussian semiparametric method is basically a Whittle estimate in the frequency domain, considering a band of frequencies that degenerates to zero. The explicit form of the estimate dˆ is given in Robinson (1995), where it is shown that: m (dˆ − d 0 ) →d N (0,1 4) as T → ∞ ,. (16). where m is the bandwidth parameter, d 0 is the true value of d , and the only additional requirement is that m → ∞ more slowly than T → ∞ . 4. Empirical Results on US External Sustainability. The data used in this study are quarterly, seasonally adjusted data for US exports of goods and services ( X t ) and imports of goods and services plus unilateral transfers and net interest payments ( MM t ) over the period 1960:Q1–2006:Q3. We also employ measures of real exports ( X t Pt ) and imports ( MM t Pt ) measured in billions of chained 2000 dollars. Finally, nominal and real values of GNP were used to create export/income and import/income ratios in nominal ( X t Yt , MM t Yt ) and real terms ( X t Yt Pt , MM t Yt Pt ). Using these data, the current account balance and the current account balance to income ratio in nominal and real terms are calculated. All data were taken from the US Department of Commerce, Bureau of Economic Analysis. All alternative proxies used in this paper have been used in the literature; for example, Husted (1992) expressed current account balance, exports, and imports in real and nominal terms..

(7) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 7. Figure 1. Plots of Original Series. Xt. MM t 800000. 600000. 600000. 400000 400000. 200000. 0. 200000 0. 60Q1. 06Q3. 60Q1. X t Yt. 06Q3. MM t Yt. 50. 80. 40. 60. 30 40. 20 20. 10 0. 0. 60Q1. 06Q3. 60Q1. X t Pt. 06Q3. MM t Pt. 500000. 800000. 400000. 600000. 300000 400000. 200000 200000. 100000 0. 0. 60Q1. 06Q3. 60Q1. X t Yt Pt. 06Q3. MM t Yt Pt. 50. 60. 40. 50 40. 30. 30. 20. 20. 10 0. 10 0. 60Q1. 06Q3. 60Q1. 06Q3. Figure 1 displays plots of the eight series and we observe that all seem to be nonstationary, with values increasing across the sample. Figure 2 contains similar plots but based on the first differenced data. We see here that they may have in some cases a stationary appearance..

(8) 8. International Journal of Business and Economics Figure 2. Plots of First Differenced Series. (1 − L) X t. (1 − L) MM t 60000. 40000. 40000. 20000. 20000. 0 0. -20000 -40000. -20000 -40000. 60Q1. 06Q3. 60Q1. (1 − L) X t Yt. 06Q3. (1 − L) MM t Yt 4. 3 2. 2. 1 0. 0 -1. -2. -2 -3. -4. 60Q1. 06Q3. 60Q1. (1 − L) X t Pt. (1 − L) MM t Pt. 40000. 40000. 20000. 20000. 0. 0. -20000. -20000. -40000. -40000. 60Q1. 06Q3. 06Q3. 60Q1. (1 − L) X t Yt Pt. 06Q3. (1 − L) MM t Yt Pt 4. 3 2. 2. 1 0. 0 -1. -2. -2 -3. -4. 60Q1. 06Q3. 60Q1. 06Q3. Denoting any of the series yt , we employ the model in (9) and (13) with zt = (1, t )T for t ≥ 1 and zt = (0, 0)T otherwise. Thus, under the null hypothesis (12):.

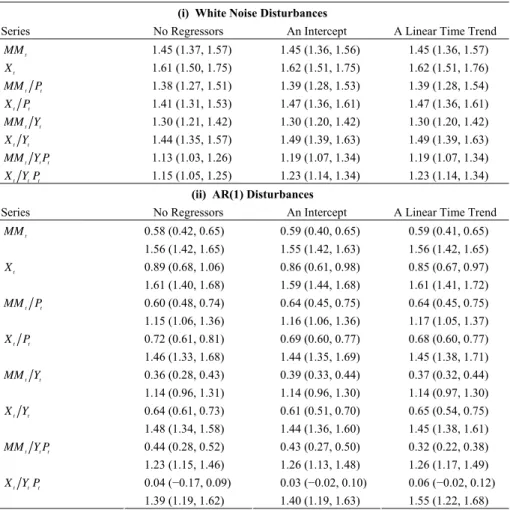

(9) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia yt = β 0 + β1t + xt , t = 1, 2,K ,. (17). (1 − L) xt = ut , t = 1, 2,K,. (18). d0. 9. and we treat separately the cases β 0 = β1 = 0 a priori, β 0 unknown and β1 = 0 a priori, and both β 0 and β1 unknown, i.e., we consider respectively the cases of no deterministic components in the undifferenced regression (17), an intercept, and an intercept and a linear time trend. We examine the test statistic for d 0 = 1 (a unit root) and for d 0 between 0 and 2 in increments of 0.25, thus including a test for stationarity (when d 0 = 0.5 ), for I(2) (when d 0 = 2 ) as well as other fractionally integrated possibilities. We first estimate the order of integration using traditional unit-root tests (i.e., the ADF of Dickey and Fuller, 1979, and the KPSS of Kwiatkowski et al., 1992) and cointegration tests (of Engle and Granger, 1987, and of Johansen, 1991). We do not report estimates but they are available upon request. The ADF and KPSS unit-root tests suggest that the original variables (imports and exports in nominal and real terms and as percentages of GNP) are nonstationary I(1) series. Furthermore, these tests suggest that the differences between exports and imports, i.e., the trade balance (as before, in nominal and real terms and as percentages of GNP) are again nonstationary I(1) series. We also test for cointegration between imports and exports using the procedure of Engle and Granger (1987). The results indicate that exports and imports series are not cointegrated, i.e., we cannot reject the null hypothesis of a unit root on the residuals of the estimated equation between exports and imports. When we apply Johansen’s maximum eigenvalue test and the trace test, we find some evidence of cointegration between exports and imports, but only when these variables are in nominal terms. However, there is no evidence of cointegration when these variables are in real terms or expressed as percentages of GNP. The values reported in Table 1 are those values of d 0 that produce the lowest test statistic in absolute value across d where H 0 cannot be rejected, which is an approximation to the maximum likelihood estimate. Separate panels display results based on white noise disturbances and on AR(1) disturbances. The 95% confidence intervals in parentheses are constructed by testing values of d from a grid and retaining only those values for which we fail to reject the null at the 5% level. Starting with the panel for white noise disturbances, we observe that though the orders of integration are higher for nominal values than for real ones, the unit-root null hypothesis is rejected in all cases in favor of higher orders of integration. Moreover, if the data are deflated by GNP, the values are still above 1, though close to the unit root for real series. This happens for the three cases of no deterministic terms, an intercept, and an intercept and a linear time trend. We see that for the first four series, these intervals oscillate between 1.27 (for real imports, MM t Pt , with no regressors) and 1.76 (for nominal exports, X t , with a linear time trend), while for the remaining four series, the values range between 1.03 (for the real imports ratio, MM t Pt , with no regressors) and 1.63 (for the nominal exports ratio with an intercept). We also observe that for all series, the results are very similar for the cases of an intercept and of an intercept and a linear trend, suggesting that the time.

(10) 10. International Journal of Business and Economics. trend might not be required when modeling these series. In fact, the coefficients associated to the time trend are not found to be significantly different from zero, while those corresponding to the intercept are significant in practically all cases. Table 1. Estimates and 95% Confidence Intervals of d with Robinson (1994) Tests (i) White Noise Disturbances. Series. No Regressors. An Intercept. MM t. 1.45 (1.37, 1.57). 1.45 (1.36, 1.56). A Linear Time Trend 1.45 (1.36, 1.57). Xt. 1.61 (1.50, 1.75). 1.62 (1.51, 1.75). 1.62 (1.51, 1.76). MM t Pt. 1.38 (1.27, 1.51). 1.39 (1.28, 1.53). 1.39 (1.28, 1.54). X t Pt. 1.41 (1.31, 1.53). 1.47 (1.36, 1.61). 1.47 (1.36, 1.61). MM t Yt. 1.30 (1.21, 1.42). 1.30 (1.20, 1.42). 1.30 (1.20, 1.42). X t Yt. 1.44 (1.35, 1.57). 1.49 (1.39, 1.63). 1.49 (1.39, 1.63). MM t Yt Pt. 1.13 (1.03, 1.26). 1.19 (1.07, 1.34). 1.19 (1.07, 1.34). X t Yt Pt. 1.15 (1.05, 1.25). 1.23 (1.14, 1.34). 1.23 (1.14, 1.34). (ii) AR(1) Disturbances. Series. No Regressors. An Intercept. A Linear Time Trend. MM t. 0.58 (0.42, 0.65). 0.59 (0.40, 0.65). 0.59 (0.41, 0.65). 1.56 (1.42, 1.65). 1.55 (1.42, 1.63). 1.56 (1.42, 1.65). 0.89 (0.68, 1.06). 0.86 (0.61, 0.98). 0.85 (0.67, 0.97). 1.61 (1.40, 1.68). 1.59 (1.44, 1.68). 1.61 (1.41, 1.72). 0.60 (0.48, 0.74). 0.64 (0.45, 0.75). 0.64 (0.45, 0.75). 1.15 (1.06, 1.36). 1.16 (1.06, 1.36). 1.17 (1.05, 1.37). 0.72 (0.61, 0.81). 0.69 (0.60, 0.77). 0.68 (0.60, 0.77). 1.46 (1.33, 1.68). 1.44 (1.35, 1.69). 1.45 (1.38, 1.71). 0.36 (0.28, 0.43). 0.39 (0.33, 0.44). 0.37 (0.32, 0.44). 1.14 (0.96, 1.31). 1.14 (0.96, 1.30). 1.14 (0.97, 1.30). 0.64 (0.61, 0.73). 0.61 (0.51, 0.70). 0.65 (0.54, 0.75). 1.48 (1.34, 1.58). 1.44 (1.36, 1.60). 1.45 (1.38, 1.61). 0.44 (0.28, 0.52). 0.43 (0.27, 0.50). 0.32 (0.22, 0.38). 1.23 (1.15, 1.46). 1.26 (1.13, 1.48). 1.26 (1.17, 1.49). 0.04 (−0.17, 0.09). 0.03 (−0.02, 0.10). 0.06 (−0.02, 0.12). Xt MM t Pt X t Pt MM t Yt X t Yt MM t Yt Pt X t Yt Pt. 1.39 (1.19, 1.62) 1.40 (1.19, 1.63) 1.55 (1.22, 1.68) Notes: Point estimates are values of d producing the lowest test statistics in absolute value; 95% confidence intervals are in parentheses.. The significance of the above results, however, might be largely due to the unaccounted for I(0) autocorrelation in ut . Thus, we also fit other models, taking into account a weakly autocorrelated structure on the disturbances. We impose AR processes, and the results show a lack of monotonicity in the value of the test statistic with respect to d 0 . Such monotonicity is characteristic of any reasonable statistic given correct specification and adequate sample size. The test statistic is one-sided. Thus, for example, we should expect that if H 0 is rejected with d 0 = 0.5 against alternatives of the form d > d 0 , an even more significant result in this.

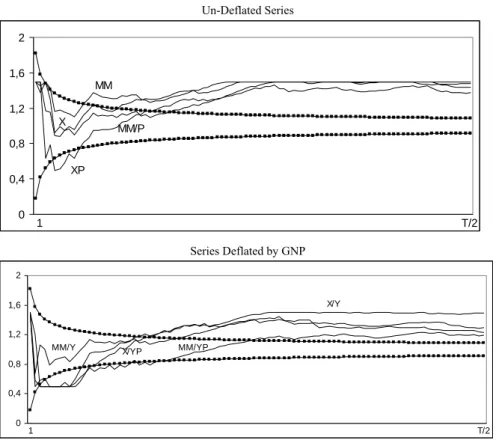

(11) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 11. direction should be expected when d 0 = 0.4 or 0.3 is tested. The lack of monotonicity could be explained in terms of model misspecification as is argued, for example, in Gil-Alana and Robinson (1997). However, it may also be due to the fact that the AR coefficients are Yule-Walker estimates and thus, though they are smaller than 1 in absolute value, they can be arbitrarily close to 1. A problem then may occur in that they may be capturing the order of integration by means, for example, of a coefficient of 0.99 in the case of AR(1) disturbances. The lower panel in Table 1 displays the estimates and confidence intervals for the AR(1) case. We observe two different types of estimates of d where monotonicity is achieved. These intervals are either strictly smaller than 1 or substantially greater, especially for the un-deflated series. For the deflated series, the values of d 0 that produce the lowest statistic range between 0.03 and 0.65 and between 1.14 and 1.55. A careful inspection at these results shows that in the former case, the AR coefficients exceed 0.99 in all cases, implying that they are competing with the orders of integration in describing the nonstationarity. Note that this is a well-known problem in econometrics. Thus, for example, standard techniques used for testing unit roots (e.g., Dickey and Fuller, 1979; Phillips and Perron, 1988) have very low power in the context of AR alternatives which are close to the unit root, and the same situation occurs if the alternatives are of a fractional form (Diebold and Rudebusch, 1991; Hassler and Wolters, 1994; Lee and Schmidt, 1996). Other less conventional forms of I(0) autocorrelation (like the exponential spectral model in Bloomfield, 1973) are also performed on the series, and the results are completely in line with the nonstationary models, finding values of d greater than 1 for the un-deflated series and around 1 for the deflated series. In order to verify that the series are truly nonstationary, we also perform the semiparametric procedure described in Section 3.2. The analysis is carried out based on the first differenced data, adding then 1 to the estimated values of d to obtain the proper orders of integration of the series. The upper panel in Figure 3 displays estimates of d for the un-deflated series while the lower part displays the estimates for the deflated series, and in both cases we report the results for the whole range of values of the bandwidth m . We also include in the figure the 95% confidence intervals corresponding to the unit root. Starting with the un-deflated series, we observe that, except for the initial values of the bandwidth, practically all the estimates are above the I(1) interval, which is in line with the results reported in the upper panel of Table 1 and also with the second set of intervals in the lower panel. If we concentrate on the deflated series, we also observe that most of the values are above 1, and only for the real import series we obtain values within the I(1) interval. Next we investigate whether the current account deficits are sustainable or not. One possibility here is to perform the analysis in a similar way as in Engle and Granger (1987) but using fractional models. That is, we can calculate the OLS regressions of exports on imports (or vice versa) and use Robinson (1994) tests to determine the degree of integration in the estimated residuals from the cointegrating regression. However, two problems arise here. First, the cointegration framework, at.

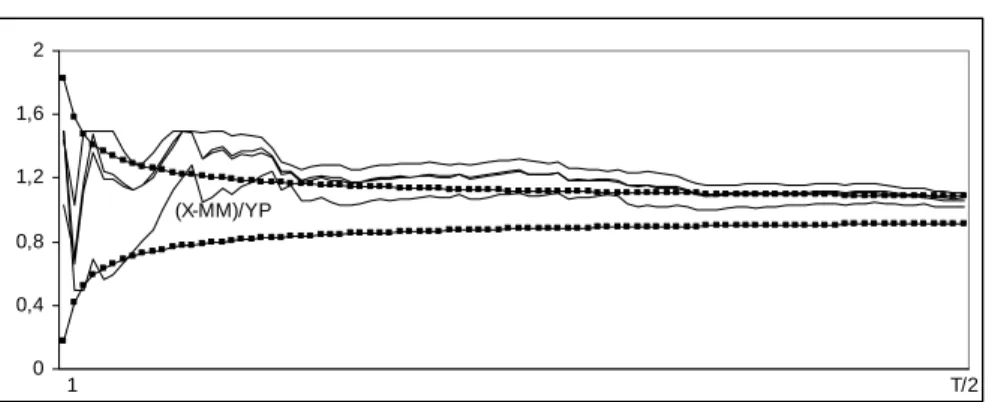

(12) 12. International Journal of Business and Economics. least in its bivariate context, requires both individual series to have the same order of integration, and we have seen using fractional models that different orders of integration may occur, especially for the deflated data. Another problem appears in that the residuals used are not actually observed but obtained from minimizing the residual variance of the cointegrating regression. Then, in finite samples, the residual series might be biased towards stationarity. As a result, we expect the null to be rejected more often than is suggested by the normal size of Robinson (1994) tests, and the empirical size of these tests should rely on Monte Carlo simulation experiments (Gil-Alana, 2003). In this respect, we prefer to work with observed data and test the order of integration of the differences between exports and imports. In other words, we test the order of integration, imposing a given cointegrating vector (1, −1) . Thus, if d < 1 in the deflated values, for example, we obtain evidence of cointegration, implying that a long-run equilibrium relationship exists between the two variables. Figure 3. Estimates of d Based on the Whittle Estimate of Robinson (1995). Un-Deflated Series 2 1,6 MM 1,2 X. MM/P. 0,8 XP. 0,4 0. 1. T/2. Series Deflated by GNP 2 X/Y. 1,6 1,2 MM/Y. X/YP. MM/YP. 0,8 0,4 0. 1. T/2. Notes: The horizontal axis reflects the bandwidth m while the vertical axis corresponds to estimated values of d . The broken lines are 95% confidence intervals of the unit root ( I(1) ) hypothesis..

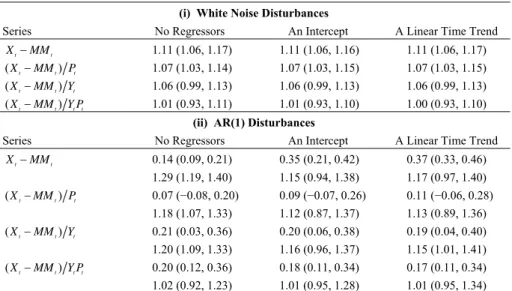

(13) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 13. Table 2 reports the confidence intervals for the same test statistic as in Table 1 but based on the current account. The results here are much more conclusive than in Table 1. Starting with the case of white noise disturbances, the differenced series X t − MM t and ( X t − MM t ) Pt are once more greater than 1, ranging between 1.03 and 1.17. Lower values are obtained for the deflated series, ( X t − MM t ) Yt and ( X t − MM t ) PtYt , and unit roots cannot be rejected for either series. If the disturbances are AR(1) , we are faced with the same problem as before, and two sets of intervals are obtained. In one, all values of d are in the stationary region, while the other is the nonstationary case with values of d about 1 or slightly greater. Table 2. Estimates and 95% Confidence Intervals of d with Robinson (1994) Tests (i) White Noise Disturbances. Series. No Regressors. An Intercept. A Linear Time Trend. X t − MM t. 1.11 (1.06, 1.17). 1.11 (1.06, 1.16). 1.11 (1.06, 1.17). ( X t − MM t ) Pt. 1.07 (1.03, 1.14). 1.07 (1.03, 1.15). 1.07 (1.03, 1.15). ( X t − MM t ) Yt. 1.06 (0.99, 1.13). 1.06 (0.99, 1.13). 1.06 (0.99, 1.13). ( X t − MM t ) Yt Pt. 1.01 (0.93, 1.11). 1.01 (0.93, 1.10). 1.00 (0.93, 1.10). (ii) AR(1) Disturbances. Series. No Regressors. An Intercept. A Linear Time Trend. 0.14 (0.09, 0.21). 0.35 (0.21, 0.42). 0.37 (0.33, 0.46). 1.29 (1.19, 1.40). 1.15 (0.94, 1.38). 1.17 (0.97, 1.40). ( X t − MM t ) Pt. 0.07 (−0.08, 0.20) 1.18 (1.07, 1.33). 0.09 (−0.07, 0.26) 1.12 (0.87, 1.37). 0.11 (−0.06, 0.28) 1.13 (0.89, 1.36). ( X t − MM t ) Yt. 0.21 (0.03, 0.36) 1.20 (1.09, 1.33). 0.20 (0.06, 0.38) 1.16 (0.96, 1.37). 0.19 (0.04, 0.40) 1.15 (1.01, 1.41). X t − MM t. ( X t − MM t ) Yt Pt. 0.20 (0.12, 0.36) 0.18 (0.11, 0.34) 0.17 (0.11, 0.34) 1.02 (0.92, 1.23) 1.01 (0.95, 1.28) 1.01 (0.95, 1.34) Notes: Point estimates are values of d producing the lowest test statistics in absolute value; 95% confidence intervals are in parentheses.. Figure 4 plots estimates of d based on the Whittle semiparametric approach for the four differenced series. We see that for small bandwidths, the four series are within the I(1) interval. However, for larger bandwidths, all series but ( X t − MM t ) Yt Pt are above the interval. In general, results presented in this section suggest that there is no evidence of cointegration of any degree in these series. 5. Potential Presence of a Structural Break. In this section we are concerned with the effect that a potential break in the data may have had on our results. The behavior of some variables, such as the exchange rate policy changes that occurred during the sample interval, may have changed the import-export relationship analyzed above. The implication of structural changes in unit-root tests has attracted the attention of many authors. Thus, Perron (1989) found that the 1929 crash and the 1973 oil crisis were a cause of non-rejection of unit roots.

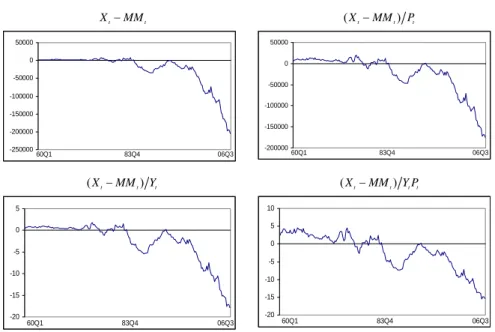

(14) 14. International Journal of Business and Economics. in many macroeconomic series. This question has also been specifically studied by Bai and Perron (1998) and other authors, some of them arguing that the date of the break should be endogenous. The relation between structural change and fractional integration is a topic that has been recently investigated (e.g., Granger and Hyung, 1999; Bos et al., 1999, 2002; Diebold and Inoue, 2001). Figure 4. Estimates of d Based on the Whittle Estimate of Robinson (1995) 2 1,6 1,2 (X-MM)/YP 0,8 0,4 0. 1. T/2. Notes: The horizontal axis reflects the bandwidth m while the vertical axis corresponds to estimated values of d . The broken lines are 95% confidence intervals of the unit root ( I(1) ) hypothesis.. We look at the possibility of structural breaks by including dummy variables in the regression model in (13). An advantage of this procedure is that the limit distribution of the test statistic is unaffected by the inclusion of the breaks. A drawback is that we have to specify a priori the time and the type of the break. In Figure 5 we observe, after a 20-year period with no major oscillation in the US current account deficit, two important increases in this variable, occurring in the mid-1980s and 1990s. From 1980 to 1986, the current account deficit increased from 0 to 3.5% of GNP in 1987 and after rising to be roughly in balance in 1991, it returned to a deficit, reaching a record deficit of 4.8% of GNP in 2003. Based on this graphical analysis, we try two different time breaks. We follow Husted (1992) and choose 1983:Q4 as the breakpoint corresponding to the first important current account balance decline in the 1980s. After analyzing different break points around 1983, he chose this point since it yielded the regression with the smallest mean square error. As we can see in Figure 5, all proxies of the current account behavior (i.e., X − MM , ( X − MM ) P , ( X − MM ) Y , and ( X − MM ) YP ) are relatively close to zero from 1960:Q1 to 1983:Q4. There are primarily two interrelated factors responsible for most of the decline in the currentaccount balance around 1983 and 1991. One is the relatively rapid growth of income in the US compared with that in other major industrialized countries after the global recession in 1982, when US GNP started to grow at a rate of 7%. Moreover, after the recession in 1991, the average annual growth rate of real GNP in the US was 3.7%, while over the same period, the annual growth rates in the European Union, Japan, and Germany were 2.2, 1.2, and 1.5%, respectively. Consequently, US imports rose much more strongly than US exports during these periods. Another.

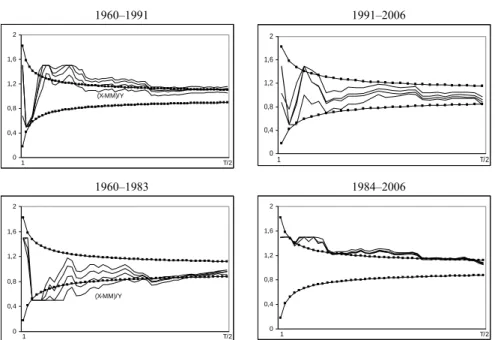

(15) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 15. important factor which directly affects trade flows is the dollar exchange rate. The declines in the current-account balance in the mid-1980s and 1991 were accompanied by an appreciation of the real exchange rate. In fact, between 1981 and 1985, the exchange rate appreciated 50% against the currencies of the major US trading partners, while it appreciated around 25% from 1991 through 2001. Figure 5. Plots of the Current Account Deficit. X t − MM t. ( X t − MM t ) Pt. 50000. 50000. 0. 0. -50000 -50000. -100000 -100000. -150000 -150000. -200000 -250000. 60Q1. 83Q4. 06Q3. -200000. 60Q1. ( X t − MM t ) Yt. 83Q4. 06Q3. ( X t − MM t ) Yt Pt 10. 5. 5. 0. 0. -5 -5. -10. -10. -15 -20. -15 -20. 60Q1. 83Q4. 06Q3. 60Q1. 83Q4. 06Q3. Table 3 presents for the four differenced series the values of d 0 that produce the lowest statistics for the subperiods 1960:Q1–1990:Q4 and 1991:Q1–2006:Q3 and the subperiods 1960:Q1–1983:Q3 and 1983:Q4–2006:Q3; that is, we separate samples according to the two proposed break dates. Looking at the results for a break at 1991:Q1, we observe that the values are systematically smaller during the second subperiod, and, though not reported, the unit-root null hypothesis is almost never rejected in the two subperiods. However, a very different picture is obtained for a break at 1983:Q4. Here, the values are systematically higher for the second subperiod, and this happens for the three types of regressors and also for both white noise and autocorrelated disturbances. Figure 6 displays estimates of d based on the semiparametric procedure. The results are consistent with those in Table 3. Splitting the sample at 1991 produces results that are, in most cases, within the I(1) interval, especially during the second subperiod. However, if the break is assumed at 1983:Q4, we observe evidence of mean reversion (values of d below the I(1) interval) in the first subperiod for ( X t − MM t ) Yt , and values of d within the I(1) interval for the remaining series. However, most series are above the unit-root confidence bands in the second subperiod..

(16) 16. International Journal of Business and Economics Table 3. Lowest Statistics for Each Subperiod Using Robinson (1994) Tests (i) White Noise Disturbances. 1960–1991 Series. NR. I. 1992–2006. LT. NR. I. LT. 1960–1983 NR. I. LT. 1984–2006 NR. I. LT. X t − MM t. 1.16. 1.16 1.16. 0.95 0.96. 0.96. 0.89 0.92 0.92 1.09 1.08 1.08. ( X t − MM t ) Pt. 1.11. 1.10 1.10. 0.90 0.91. 0.90. 0.86 0.89 0.89 1.08 1.07 1.06. ( X t − MM t ) Yt. 1.12. 1.12 1.12. 0.87 0.88. 0.87. 0.85 0.89 0.89 1.06 1.05 1.05. ( X t − MM t ) Yt Pt. 1.06. 1.03 1.03. 0.83 0.82. 0.82. 0.84 0.84 0.84 1.07 1.06 1.06. (ii) AR(1) Disturbances. 1960–1991 Series. NR. I. LT. 1992–2006 NR. I. 1960–1983. LT. NR. I. LT. 1984–2006 NR. I. LT. X t − MM t. 1.23. 1.22 1.22. 1.08 1.09. 1.08. 0.36 0.31 0.22 1.27 1.25 1.25. ( X t − MM t ) Pt. 1.13. 1.11 1.11. 1.01 1.02. 1.02. 0.49 0.55 0.58 1.25 1.25 1.24. ( X t − MM t ) Yt. 1.18. 1.17 1.17. 0.99 0.99. 0.99. 0.14 0.28 0.28 1.25 1.24 1.23. ( X t − MM t ) Yt Pt 1.07 1.02 1.02 0.93 0.93 0.93 0.37 0.51 0.53 1.25 1.26 Notes: NR means no regressors, I means an intercept, and LT means a linear time trend.. 1.26. Figure 6. Estimates of d Based on the Whittle estimate of Robinson (1995). 1960–1991. 1991–2006. 2. 2. 1,6. 1,6 1,2. 1,2 (X-MM)/Y 0,8. 0,8. 0,4. 0,4. 0. 0 1. T/2. 1. 1960–1983. T/2. 1984–2006. 2. 2. 1,6. 1,6. 1,2. 1,2. 0,8. 0,8 (X-MM)/Y. 0,4. 0,4. 0. 0. 1. T/2. 1. T/2. Notes: The horizontal axis reflects the bandwidth m while the vertical axis corresponds to estimated values of d . The broken lines are 95% confidence intervals of the unit root ( I(1) ) hypothesis.. In the light of this, we assume the break occurs at 1983:Q4 and perform once more the tests of Robinson (1994) but this time using the regression model:.

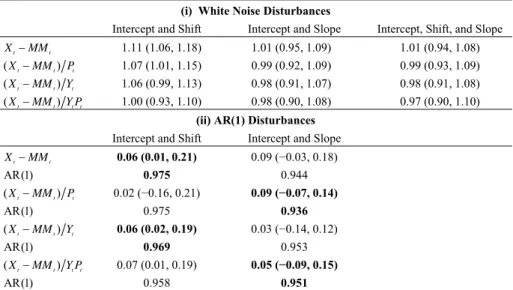

(17) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 17. yt = β 0 + β1 D1t + β 2 D2t + xt , t = 1, 2,K ,. and (9), where D1t = 1I (t > Tb ) (representing a mean shift) and D2 t = tI (t > Tb ) (representing a slope shift), with I (⋅) the indicator function and Tb = 1983:Q4 . We examine separately the case of an intercept and a shift dummy (i.e., β 2 = 0 a priori), an intercept and a slope dummy (i.e., β1 = 0 a priori), and a combination of both ( β1 and β 2 unknown) for the two cases of white noise and AR(1) disturbances. Table 4. Estimates and 95% Confidence Intervals of d with Robinson (1994) Tests (i) White Noise Disturbances. Intercept and Shift. Intercept and Slope. Intercept, Shift, and Slope. X t − MM t. 1.11 (1.06, 1.18). 1.01 (0.95, 1.09). 1.01 (0.94, 1.08). ( X t − MM t ) Pt. 1.07 (1.01, 1.15). 0.99 (0.92, 1.09). 0.99 (0.93, 1.09). ( X t − MM t ) Yt. 1.06 (0.99, 1.13). 0.98 (0.91, 1.07). 0.98 (0.91, 1.08). ( X t − MM t ) Yt Pt. 1.00 (0.93, 1.10). 0.98 (0.90, 1.08). 0.97 (0.90, 1.10). (ii) AR(1) Disturbances. X t − MM t. AR(1). Intercept and Shift. Intercept and Slope. 0.06 (0.01, 0.21). 0.09 (−0.03, 0.18). 0.975. 0.944. ( X t − MM t ) Pt AR(1). 0.02 (−0.16, 0.21) 0.975. 0.09 (−0.07, 0.14). ( X t − MM t ) Yt AR(1). 0.06 (0.02, 0.19). 0.03 (−0.14, 0.12). 0.969. 0.953. 0.936. ( X t − MM t ) Yt Pt 0.07 (0.01, 0.19) 0.05 (−0.09, 0.15) AR(1) 0.958 0.951 Notes: Point estimates are values of d producing the lowest test statistics in absolute value; 95% confidence intervals are in parentheses. Results in bold are cases where the dummy variables are significant at the 5% level.. We observe in Table 4 that if the disturbances are white noise, the unit-root null hypothesis is rejected for the un-deflated series (i.e., X t − MM t and ( X t − MM t ) Pt ) in the case of a shift dummy. However, for the deflated series with a shift dummy and for all series in the other two cases, the unit root cannot be rejected. If we assume an AR(1) structure for the disturbances, (which seems to be much more realistic), the first thing we note is that for the cases of an intercept and a shift dummy and of an intercept and a slope dummy, monotonicity is achieved across the whole region of values of d , unlike what happened in all previous specifications, also based on AR(1) disturbances ut . We see that the values of d where H 0 cannot be rejected are in all series smaller than 0.5, thus implying stationarity and mean-reverting behavior. The lowest statistics are obtained at values of d ranging between 0.01 (for ( X t − MM t ) Pt with a shift dummy) and 0.10 (for X t − MM t with a slope dummy), and, though in all cases the AR coefficients are still very close to 1 (ranging between 0.936 and 0.975), they are smaller than in the previous tables. We finally observe that the coefficients for the dummies associated with the lowest statistics are significant in the case of the shift dummy for the X t − MM t and.

(18) 18. International Journal of Business and Economics. ( X t − MM t ) Yt series and of the slope dummy for the real series ( X t − MM t ) Pt and ( X t − MM t ) Yt Pt . Thus, we conclude that some evidence of sustainability is obtained when a break at 1983 is taken into account.. 6. Concluding Comments. Current account sustainability has been tested by many authors and for many countries. However, in spite of the huge literature on this topic, we are still far from a consensus about its behavior. Most of the work in this area has been conducted through the use of classic techniques, testing the existence of unit roots and/or cointegration in the context of AR processes and integer orders of differentiation. In this article we examine the stochastic behavior of US exports and imports by means of fractional integration. We employ both parametric and semiparametric methods. The results show that the orders of integration of the series are above 1, especially for un-deflated series. We also examine the US current account deficit by looking at the order of integration of the differences between exports and imports and, though the values of d are slightly smaller than those of the individual series, the unit-root model cannot statistically be rejected for the deflated series, suggesting no evidence of fractional cointegration. The fact that the current account deficits are nonstationary I(d ) with d ≥ 1 implies that there is no mean reversion, and shocks affecting the series will persist forever. According to the external sustainability model, this implies that current account deficits are not sustainable and could grow without limit. However, a graphical inspection of the US current account balance shows that after a 20-year period of no major movements (1960–1980), the current account deficit suffered two substantial increases in the 1980s and 1990s, which suggests that the importexport relationship may have suffered structural breaks during the period analyzed. We also consider the possibility of structural breaks at 1983:Q4 and 1991:Q1. The results strongly support the existence of a break at 1983. Including dummy variables in the regression model in Robinson (1994) to take into account this break, the results indicate that the differenced series are stationary, implying that the current accounts are sustainable though with a component of long-memory behavior. The fact that there is a long-run relationship between exports and imports, which shifted in 1983, and thus that the US current account deficit is sustainable, is consistent with the conclusions of Husted (1992), though it contrasts with other studies such as Fountas and Wu (1999), who find evidence against the sustainability of the US current account deficit over the period 1967:Q1–1994:Q4..

(19) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 19. References. Arize, A. C., (2002), “Imports and Exports in 50 Countries. Tests of Cointegration and Structural Breaks,” International Review of Economics and Finance, 11, 101-115. Bai, J. and P. Perron, (1998), “Estimating and Testing Linear Models with Multiple Structural Changes,” Econometrica, 66, 47-78. Bergin, P. R., (2001), “How Well Can We Explain the Current Account in Terms of Optimizing Behavior,” Department of Economics, University of California Davis. Bergin, P. R. and S. M. Sheffrin, (2000), “Interest Rates, Exchange Rates and Present Value Models of the Current Account,” Economic Journal, 110, 535558. Bernanke, B., (2005), “The Global Saving Glut and the US Current Account Deficit,” Remarks at the Sandridge Lecture, Virginia Association of Economists, Richmond, Virginia. Bloomfield, P., (1973), “An Exponential Model in the Spectrum of a Scalar Time Series,” Biometrika, 60, 217-226. Bos, C. S., F. Franses, and M. Ooms, (1999), “Long Memory and Level Shifts: Reanalyzing Inflation Rates,” Empirical Economics, 24, 427-449. Bos, C. S., F. Franses, and M. Ooms, (2002), “Inflation, Forecast Intervals and Long Memory Regression Models,” International Journal of Forecasting, 18, 243264. Dickey, D. A. and W. A. Fuller, (1979), “Distribution of the Estimators for Autoregressive Time Series with a Unit Root,” Journal of the American Statistical Association, 74, 427-431. Diebold, F. X. and A. Inoue, (2001), “Long Memory and Regime Switching,” Journal of Econometrics, 105, 131-159. Diebold, F. X. and G. Rudebusch, (1991), “On the Power of Dickey-Fuller Tests Against Fractional Alternatives,” Economic Letters, 35, 155-160. Engle, R. and C. W. J. Granger, (1987), “Cointegration and Error Correction: Representation, Estimation and Testing,” Econometrica, 55, 251-276. Fountas, S. and J. Wu, (1999), “Are the U.S. Current Account Deficits Really Sustainable?” International Economic Journal, 13(3), 51-58. Fox, R. and M. S. Taqqu, (1986), “Large-Sample Properties of Parameter Estimates for Strongly Dependent Stationary Gaussian Time Series,” Annals of Statistics, 14, 517-532. Gil-Alana, L. A., (2003), “Testing of Fractional Cointegration in Macroeconomic Time Series,” Oxford Bulletin of Economics and Statistics, 65, 517-529. Gil-Alana, L. A. and P. M. Robinson, (1997), “Testing of Unit Root and Other Nonstationary Hypotheses in Macroeconomic Time Series,” Journal of Econometrics, 80, 241-268..

(20) 20. International Journal of Business and Economics. Glick, R. and K. Rogoff, (1995), “Global Versus Country-Specific Productivity Shocks and the Current Account,” Journal of Monetary Economics, 35, 159192. Granger, C. W. J. and H. Hyung, (1999), “Occasional Structural Breaks and Long Memory,” Discussion Paper 99-14, University of California, San Diego. Gundlach, E. and S. Sinn, (1992), “Unit Root Tests of the Current Account Balance: Implications for International Capital Mobility,” Applied Economics, 24, 617620. Hassler, U. and J. Wolters, (1994), “On the Power of Unit Root Tests against Fractional Alternatives,” Economic Letters, 45, 1-5. Husted, S., (1992), “The Emerging US Current Account Deficit in the 1980s. A Cointegration Analysis,” Review of Economics and Statistics, 74, 159-166. Johansen, S., (1991), “Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models,” Econometrica, 59, 1551-1580. Kwiatkowski, D., P. C. B. Phillips, P. Schmidt, and Y. Shin, (1992), “Testing the Null Hypothesis of Stationarity Against the Alternative of a Unit Root: How Sure Are We That Economic Time Series Have a Unit Root?” Journal of Econometrics, 54, 159-178. Lau, E., A. Z. Baharumshah, and C. T. Haw, (2006), “Current Account: MeanReverting or Random Walk Behavior?” Japan and the World Economy, 18, 90107. Lee, D. and P. Schmidt, (1996), “On the Power of the KPSS Test of Stationarity against Fractionally Integrated Alternatives,” Journal of Econometrics, 73, 285-302. Liu, P. and E. Tanner, (1996), “International Intertemporal Solvency in Industrialized Countries: Evidence and Implications,” Southern Economic Journal, 62, 739-749. Otto, G., (1992), “Testing a Present-Value Model of the Current Account: Evidence from US and Canadian Time Series,” Journal of International Money and Finance, 11, 414-430. Perron, P., (1989), “The Great Crash, the Oil Price Shock, and the Unit Root Hypothesis,” Econometrica, 57, 1361-1401. Phillips, P. C. B. and P. Perron, (1988), “Testing for a Unit Root in Time Series Regression,” Biometrika, 75, 335-346. Robinson, P. M., (1994), “Efficient Tests of Nonstationary Hypotheses,” Journal of the American Statistical Association, 89, 1420-1437. Robinson, P. M., (1995), “Gaussian Semiparametric Estimation of Long Range Dependence,” Annals of Statistics, 23, 1630-1661. Sowell, F., (1992), “Maximum Likelihood Estimation of Stationary Univariate Fractionally Integrated Time Series Models,” Journal of Econometrics, 53, 165-188. Trehan, B. and C. Walsh, (1991), “Testing Intertemporal Budget Constraints: Theory and Applications to U.S. Federal Budget and Current Account Deficits,” Journal of Money, Credit and Banking, 23, 206-223..

(21) Juncal Cuñado, Luis Alberiko Gil-Alana, and Fernando Perez de Gracia. 21. Wickens, M. and M. Uctum, (1993), “The Sustainability of Current Account Deficits: A Test of the US Intertemporal Budget Constraint,” Journal of Economic Dynamics and Control, 17, 423-441. Wu, J. L., (2000), “Mean Reversion of the Current Account: Evidence from the Panel Data Unit Root Test,” Economics Letters, 66, 215-222..

(22)

數據

+6

相關文件

Wang, Solving pseudomonotone variational inequalities and pseudocon- vex optimization problems using the projection neural network, IEEE Transactions on Neural Networks 17

Then, it is easy to see that there are 9 problems for which the iterative numbers of the algorithm using ψ α,θ,p in the case of θ = 1 and p = 3 are less than the one of the

volume suppressed mass: (TeV) 2 /M P ∼ 10 −4 eV → mm range can be experimentally tested for any number of extra dimensions - Light U(1) gauge bosons: no derivative couplings. =>

Define instead the imaginary.. potential, magnetic field, lattice…) Dirac-BdG Hamiltonian:. with small, and matrix

incapable to extract any quantities from QCD, nor to tackle the most interesting physics, namely, the spontaneously chiral symmetry breaking and the color confinement..

• Formation of massive primordial stars as origin of objects in the early universe. • Supernova explosions might be visible to the most

We have also discussed the quadratic Jacobi–Davidson method combined with a nonequivalence deflation technique for slightly damped gyroscopic systems based on a computation of

To complete the “plumbing” of associating our vertex data with variables in our shader programs, you need to tell WebGL where in our buffer object to find the vertex data, and