Credibility of Financial Reporting and Auditor Independence

Under Alternative Legal Systems

− Theory and Experimental Evidence

NSC Final Report

(Project No.: 94

−2416−H−004−035)

Hung-Chao Yu

Department of Accounting

College of Commerce

National Chengchi University

Wenshan, Taipei, 11605

TAIWAN, ROC

1. INTRODUCTION

During recent years, two critical issues have emerged that may be detrimental to the U.S. capital

markets: one is the managers’ fraudulent financial reporting and the other one is the auditor’s

independence. On one hand, financial accounting information is the product of corporate accounting

and external reporting systems that measure and routinely disclose audited, quantitative data

concerning the financial position and performance of publicly held companies. In essence, credible

financial reporting enhances the efficient allocation of scare financial capital to promising investment

opportunities, which in turn maximizes the shareholders’ wealth. On the other hand, auditor

independence not only increases the likelihood that firms’ financial statements are in conformity with

the GAAP, but also encourages investors to rely more on the financial statements. Therefore,

companies’ honest financial reporting and auditor independence have long been regarded as two

cornerstones to the prosperity and success of the capital markets (Bushman and Smith 2003). However,

due to recent many accounting scandals (e.g., Enron, WorldCom, Merck, Global Crossing), a call to

restore public trust through improving the credibility of companies’ financial reporting and auditor

independence has been emphasized by regulators, accounting practitioners, and auditing academic (e.g.,

Abbott, Parker, Peters, and Raghunandan 2003; Citron 2003; Cote 2002; Craswell, Stokes, and

Laughton 2002; Dopuch, King, and Schwartz 2003; Gerde and White 2003; Hodge 2003; Kaiser and

Perris 2003; Kopel 2003; Lousteau and Reid 2003; SEC 2003).

In this study I examine how a well-designed legal system imposing on the auditor may serve as an

effective mechanism to induce manager’s credible reporting and improve auditor independence.

Generally speaking, a complete legal system affecting the auditing profession consists of liability

regimes and damage apportionment rules. In essence, liability regimes determine whether an auditor is

held liable for damage losses incurred by investors; damage apportionment rules determine the share

regimes that has been extensively explored by prior studies in auditor’s legal liabilities: the strict

regime (ST), in which the auditors are held liable, given that a loss occurred to the investors, regardless

of the due care level, and the negligence regime (NE), in which the auditors are not liable if they have

provided the due-care level of services. Obviously, under the ST regime the degree of auditors’ due

care does not eliminate qualified investors’ or other parties’ standing to sue but the NE regime does. I

also analyze three damage apportionment rules: the joint-and-several rule (JS), the hybrid

proportionate rule (HP), and the pure proportionate rule (PR). On one hand, the JS rule (which is still

in use by the United Kingdom and several European countries) provides full insurance to the investors

where the liable auditors are responsible for the full amount of unpaid damage losses, regardless of

whether they have exerted due professional care. Under the PP rule (which is now used in Canada and

New Zealand), on the other hand, the liable auditors are responsible for only the share of damages that

the court holds them responsible for causing. The Private Securities Reform Act of 1995 replaced the

venerable JS rule with the HP rule, in which the auditors are responsible for paying up to 50% more in

damages over their initially assessed share if there is an unpaid portion of the damages and investors

satisfy certain net worth and loss conditions (King and Schwartz 1997). In other words, the HP rule

provides investors with a limited amount of public companies’ insolvency insurance while the PR rule

does not (Hillegeist 1999). Because these three damage apportionment rules are currently used by

different countries, a comparison of the effects of these three rules together with different legal regimes

on managers’ credible reporting and auditor independence should bear important policy implications

from an international perspective.

My study further contributes to the literature in three other aspects. First, while prior analytical

and experimental studies comparing the relative effectiveness of different legal systems have generally

2000; Radhakrishnan 1999; Schwartz 1997)1 or damage apportionment rules (e.g., Boritz and Zhang

1997; Chan and Pae 1998; Dopuch, King, and Schatzberg 1994; Dopuch, Ingerman, and King 1997;

Hillegeist 1999; Narayanan 1994) alone on audit effort and firm’s investments, few attempts, if any,

have ever been made to incorporate both components in investigating manager’s reporting and

auditor’s independence behavior. Second, my study separates audit failure into two types: a technical

audit failure (resulting from the imperfection of audit technology or a lack of due professional care)

and an independence audit failure (resulting from auditor’s intentionally compromising his

independence). This distinction is important because previous studies have generally assumed that the

audit technology has one-sided error and defined audit failure as the probability that a firm with a high

audited report is actually of low type (e.g., Dye 1993; Dye, Balachandran, and Magee 1990; Melumad

and Thoman 1990; Hillegeist 1999; Pae and Yoo 2001; Schwartz 1997; Thoman 1996), but often

overlook the possibility and existence of independence audit failure. More important, since a technical

audit failure represents an unknowing violation of the securities laws, the 1995 Reform Act rules that

the auditor is held liable for damage losses proportionately.2 In contrast, an independence audit failure

involves a situation in which the auditor knowingly commits a violation of the securities laws.

Consequently, the 1995 Reform Act requires that the auditor be held liable for the total damages jointly

and severally. Finally, a common feature of many prior auditor liability studies (e.g., Melumad and

Thoman 1990; Hillegeist 1999; Pae and Yoo 2001; Schwartz 1997; Thoman 1996) is that the firm’s

type is determined exogenously by the nature. My study extends previous research by endogenizing

firm type through manager’s investment decision. That is, the firm’s type is determined by the

manager’s investment and the resulting realized outcome. I emphasize on manager’s investment

decision because the regulators and accounting academic have argued that many firms in the U.S.

1Schwartz (1997) emphasizes the determination of damage loss itself and concludes that a damage measure that is

independent of the actual investment together with a strict liability regime will motivate the auditors to exert the socially optimal effort level and induce the socially optimal level of investment. The damage apportionment rules are not considered in her study.

capital market strive only to meet their forecasts, but not to provide results that are in the shareholders’

best interest (Kieso et al. 2004). I posit that undertaking appropriate investment projects should

maximize firm’s value, which is beneficial to the shareholders.

I adopt the experimental economics methodology to address the issues of interest because of

several reasons. First, there is a lack of naturally occurring data on important variables (in the real

world, for instance, it is impossible to vary auditors’ damage apportionment rules and observe

subsequent changes in manager’s reporting behavior). Also, laboratory experiments provide a more

precise measure of auditor independence than the empirical-archival studies (e.g., the use of proxies

such as the ratio of nonaudit service fees to audit fees). Second, since the model to be tested in this

study makes strong assumptions about manager and auditor (e.g., the ability to make rational and

statistical inferences) and their strategic interactions (e.g., different equilibria), this study intends to test

the behavioral validity of the model. If the experimental results support the model, this support may

come in spite of ex ante behavioral considerations to the contrary. If the results do not support the

model predictions, a theoretical basis of explaining why they are not should be pursued (Kachelmeier

1996a, 1996b; Smith 1989, 1994). As Swieringa and Weick (1982, p. 81) points out, deliberate

artificiality “… allows for more direct tests of theory, and this more direct access to theoretical

propositions may improve generalization, because it is the theoretical statements, not raw findings, that

are used to explain or describe phenomena in the real world.” Finally, it is impossible to vary the

combinations of legal system in the real world and observe different players’ corresponding behavior.

Therefore, the ability of empirical-archival research to offer policy insights is inherently limited

(Kachelmeier and King 2002). Since the policy-makers’ perspective demands ex ante insights of

manager’s and auditor’s likely responses that could exist, laboratory experiments provide a controlled

environment to address auditing policy issues. In light of this, my purpose is to use the laboratory as a

uses.

The remainder of this research proposal is organized as follows. Section 2 describes the basic

model setting. Section 3 explains the experimental procedures. Section 4 lists tasks to be finished if

this research proposal is approved.

2. BASIC MODEL SETTING 2.1 Basic Model Setting:

Suppose a firm intends to expand its operations but does not have readily available internal funds.

Therefore, its risk-neutral manager must seek to raise capital from outside investors. The scale of the

expansion is flexible and can be adjusted to the amount of the investment I (Table 1 shows definitions

of the variables and parameter values for the illustrative example). To simplify the model setting, I

assume that the investors are willing to provide I to the firm for carrying out the expansion. After

obtaining the money, however, the manager may choose to invest the whole amount of I on a high-cost

innovative project (denoted by Ihigh) or only invest part of I on a low-cost established project (denoted

by I ) because the manager needs to exert a corresponding effort level low i M

e to undertake investment

i

I (where i ∈ {high, low}) at an effort cost ( i )

M

e

C . The realized earnings ω is private information to the manager and can be either high (denoted by H) or low (denoted by L), depending on the dollar

amount invested. Given the investment amount Ii , I define ρ(Ii) to be the probability that the

outcome is H, where ρ(Ii) is increasing in Ii and ρ(Ii)∈ (0, 1). In the numerical example, if I low

is undertaken, the manager has a 0.80 probability of receiving L and a 0.20 probability of receiving H

(i.e.,ρ(Ilow) = 0.2). In contrast, if Ihigh is undertaken, the manager would have a 0.80 probability of receiving H and a 0.20 probability of receiving L (i.e.,ρ(Ihigh) = 0.8). To be responsible for the investors who provide the funds, the manager prepares a financial report Rk, where k∈{H,L}, and

pays a flat audit fee F to hire an independent auditor to verify the credibility of his report Rk.3 I

assume that, if the actual outcome is H, the manager will always report RH. If the actual outcome is L,

however, the manager may report either RH or RL. The auditor chooses an effort level eA at a cost

) (eA

C and obtains an audit signal ξ regarding the probable outcome of the earnings level. Let SH (or

SL) denote the audit signal that the earnings level is high (or low), ξ∈ {SH, SL}.

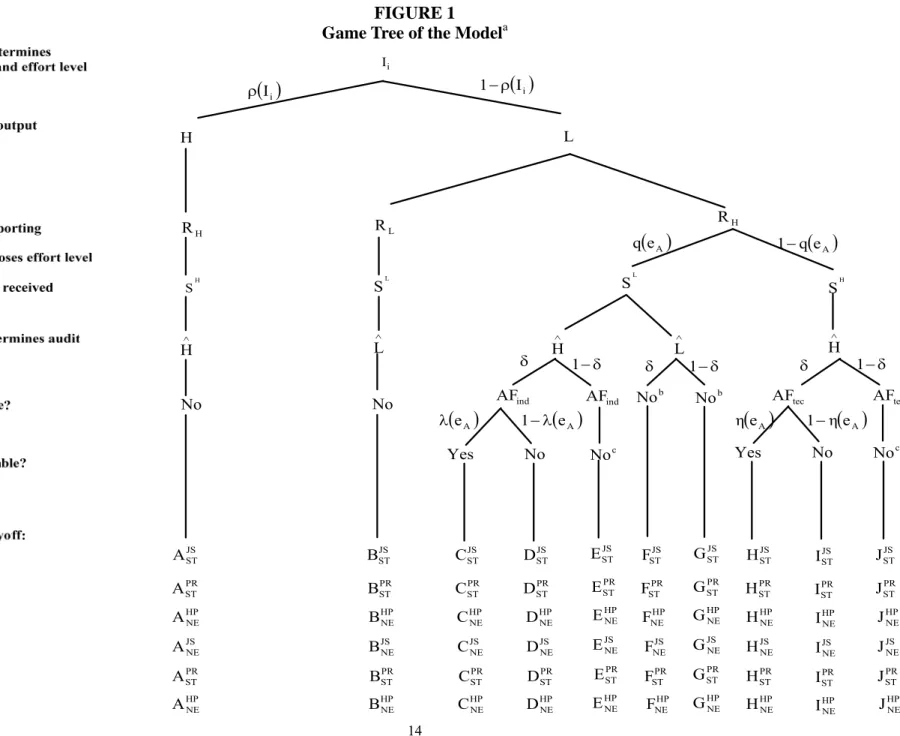

[Insert Table 1 and Figure 1 here]

Since the audit technology is imperfect, there is no audit evidence from which the auditor can

infer the investment outcome with certainty. Following Schwartz (1997) and Hillegeist (1999), I

assume that the audit technology has one-sided errors: If the true outcome is H, the auditor will not

obtain SL (i.e., p(SH |H) = 1), no matter what effort level the auditor exerts. If the true output is L,

however, the auditor will obtain a correct signal SL with probability ( )

A e q (i.e., p(SL |L) = ( ) A e q ) and

obtain an incorrect signal SH with probability 1 ( )

A e q − (i.e., p(SH |L) = 1 ( ) A e q − ). Consistent with

Schwartz (1997), this q(eA) serves as a measure of audit quality, which is increasing in auditor’s

effort level. For simplicity and tractability purposes, I assume that the auditor has two effort level to

choose: a low effort level (denoted by low A

e ) or a high effort level (denoted by high A

e ). In the numerical

example, if the true outcome is H, the auditor will always obtain signal SH with probability one. If the

true outcome is L, on the other hand, the auditor will obtain signal SL with probability 0.7 if he exerts

high A

e (i.e., ( high)=0.7) A

e

q but will obtain the correct signal with probability 0.3 if he only exerts low A e (i.e., ( low)=0.3) A e q .

Based on the audit signal obtained, the auditor issues a report r ∈ { Hˆ , Lˆ } to the investors. Following Dopuch, King, and Schwartz (2001), I also assume that the auditor’s report affects

3Instead of incorporating a formal bidding process, a flat audit fee can simplify the experimental setting for the subjects.

This setting also allows my model to focus cleanly on auditor’s effort and independence strategies and manager’s investment and reporting decisions without bringing in undue complexity into the model. Hillegeist’s (1999) has indicated that the audit fee is fixed in the U.S. current audit environment.

manager’s compensation: An Hˆ report results in a higher compensation for the manager than an Lˆ

report (denoted by MHˆ and MLˆ, respectively). If the audit signal is SH, the auditor can only issue an

Hˆ report. This setting is consistent with current auditing practice in which the auditor will issue an

unqualified opinion when audit evidence shows that there is no material misstatement in client’s

financial statements. It should be noted, however, that signal SH may come from three possible

scenarios: (a) the true outcome is H, (b) the true outcome is L and the auditor has 0.3 probability of

obtaining SH when he exerts high A

e , and (c) the true outcome is L and the auditor has 0.7 probability of

obtaining SH when he exerts low A

e . I refer to scenarios (b) and (c) as technical audit failures (denoted

by AFtec) because the auditor cannot effectively discover the true outcome of the investment due to his

imperfect audit technology. Therefore, the AFtec rate can be defined as the conditional probability that

the auditor receives an RH report from the manager and obtains an audit signal SH when the realized

earnings level is L (i.e., AFtec ≡ ( | , H)≡ H R S L p p(RH |L)(1−ρ(Ii))(1−q(eA))/ [ρ(Ii)+p(RH |L) ))] ( 1 ))( ( 1

( −ρ Ii −q eA , where ∂AFtec/∂eA <0 and ∂AFtec/∂Ii <0, ceteris paribus). When an AFtec

occurs, the auditor’s legal liability will depend on the state of the economy and the auditor’s effort

level. In particular, if the state of the economy is good (with probability 1−δ), I assume that the firm will not go bankrupt (even though the earnings level is L) and, therefore, the investors will not sue the

auditor for damage compensations. In contrast, a lawsuit against the auditor will be triggered when the

state of the economy is bad (with probability δ) because the firm cannot survive as a going-concern due to its low earnings level.4 During its deliberations, the court compares its own (noisy) observation

4I assume that the manager will get zero payoff and is not liable for the bankruptcy because of two reasons. First, exclusion

of a liability rule for the manager is consistent with the traditional notion of “deep pockets,” where the auditor must pay all the damages in a number of security cases even though the manager is also guilty of negligence and fraud (Dopuch and King 1992). Second, Palmrose (1994) observes that about 58 percent of all the auditor litigation cases involve the financial failure (or distress) of the client. It should be noted, however, that the Sarbanes-Oxley Act has imposed new legal liabilities on the corporate management. For example, Section 305 rules that, if a public company is required to prepare a restatement due to "material noncompliance" with financial reporting requirements, the CEO and CFO shall reimburse the

of the audit’s quality to its interpretation of the legally required “due care” level of audit quality in

determining whether to hold the auditor liable for AFtec. I assume that, in expectation, the court will

find the auditor negligent with probability η(eA), where η(eA) is decreasing in auditor’s effort level.

In the numerical example, the auditor has 0.3 (or 0.7) probability of being held liable if he exerts high A e

(or low A

e ). Note that in my model this η(eA) is manipulated to be less than one (either 0.3 or 0.7) under

the negligence legal regime (denoted by NE) but is equal to one under the strict legal regime (denoted

by ST) to reflect the fundamental difference between these two legal regimes. If the court holds the

auditor liable, it then determines the relative fault of each co-defendant (i.e., the manager and auditor).

This determination forms the fundamental basis of how the total damage losses Dtec should be split

between the auditor and the manager. Since there is no well-defined formula or guidance on how the

Dtec should be split, I assume that, in expectation, the auditor is held responsible for k percent of Dtec,

where k∈(0,1). To highlight the impacts of different damage apportionment rules in conjunction with legal regimes on manager’s reporting and auditor independence, I create a game setting in which the

auditor is always solvent but the manager is bankrupt by the end of the trial. Therefore, the auditor has

to pay his share of the total damages α⋅k⋅D to the investors. Following Hillegeist (1999), this tec α is

the proportional damage multiplier which can characterize the three damage apportionment rule. More

specific, α⋅k = 1 for the JS rule and α = 1 (or > 1) for the PP (or HP) rule. The damages Dtec are set

equal to the investors’ economic losses resulting from their reliance on the fraudulent financial

statements. Following Schwartz (1997), the damages Dtec are set to be independent of the actual

investment Ii.

Alternatively, if the audit signal is SL, the imperfect audit technology can ensure the auditor that the

true investment outcome is L. In this situation, the auditor may issue either an Hˆ or Lˆ report,

company for any bonus or other compensation received during the twelve months following the issuance or filing of the non-compliant document and any profits realized from the sale of securities of the company during that period.

depending on his independence. Since the manager’s compensation is influenced by auditor’s report, the

manager has strong motivation to induce the auditor to issue an Hˆ report. To create a setting in which

the auditor will compromise his independence to the highest level, I assume that the manager provides two

incentives (or threats) to the auditor: one is the present value of quasi rents accrued in future audit

engagements (DeAngelo 1981), denoted by ER, and the other one is manager’s side payment to the

auditor in the current period (Lee and Gu 1998), denoted by SP. Under this setting, the auditor has two

reporting strategies to choose. If he intends to keep ER and accepts the SP, the auditor will issue an Hˆ

report. I refer to this scenario as an independence audit failure (denoted by AFind) because the auditor

intentionally misrepresents the true outcome of the investment due to his lack of independence.5

Therefore, the AFind rate is the conditional probability that the auditor issues an Hˆ report when the audit signal is SL, i.e., ( ˆ | L)

S H

p . When an AFind occurs, the auditor’s legal liability will still depend on the state of the economy and his effort level. If the state of the economy turns out to be good, the investors

will not sue the auditor for damage losses because the firm is not bankrupt. In contrast, the investors will

file a lawsuit against the auditor when the state of the economy is bad because the firm cannot survive.

Since the auditor commits a knowing violation of the securities laws, the 1995 Reform Act rules that he

will be held liable for the AFind damages jointly and severally. Again, I assume that, in expectation, the

court will find the auditor negligent with probability λ(eA). If the court holds the auditor liable, it then

determines the total damages Dind the auditor should pay to the investors.6, 7

5In real audit failure cases, the issue of whether AFtec (resulting from the imperfection of audit technology or a lack of

professional care) and AFind (resulting from auditor’s intentionally compromising independence) are independent is not

clear and, therefore, I do not consider this issue explicitly. Instead, my model setting takes as given that AFtec and AFind

are independent because the ability to detect material misstatements is a function of auditor’s competence (or audit technology) while the propensity to correct (or report) material misstatements is a function of auditor independence (Khurana and Raman 2004).

6Since the audit signal is SL but the auditor issues a Hˆ report, I assume that the auditor will counterfeit the audit evidence to make it look like SH in case he is sued by the investors. This assumption is reasonable and practical because otherwise the auditor will always be held liable when there is a lawsuit against him. By forging the audit evidence in support of SH, the auditor has an opportunity to defend himself before the court that he has exerted high effort and, therefore, reduces the possibility of being held liable to an audit failure. A most recent case filed by the SEC on September 25, 2003, supports

If the auditor refuses the SP and insists on issuing an Lˆ report (i.e., the auditor is independent), the

manager will have to restate his report and replace the auditor at an adjustment-and-switching cost

(denoted by ASC). Because the auditor is dismissed, he will lose the present value of future quasi rents ER.

This one-period game then ends. Appendix summarizes different players’ payoffs under different game

outcomes and legal environments.

2.2 Players’ Equilibrium Strategies and Hypotheses:

The analysis of the above one-period two-player game proceeds by backward induction because

of the game’s sequential nature. However, the complexity of the model setting and the legion of

endogenized variables introduce ambiguity into the analytical results due to some “high order” effects

that may attenuate the comparisons and intuition among different legal environments. I will overcome

this problem by solving the game using the parameter values specified in Table 1.

3. EXPERIMENTAL DESIGN AND PROCEDURES

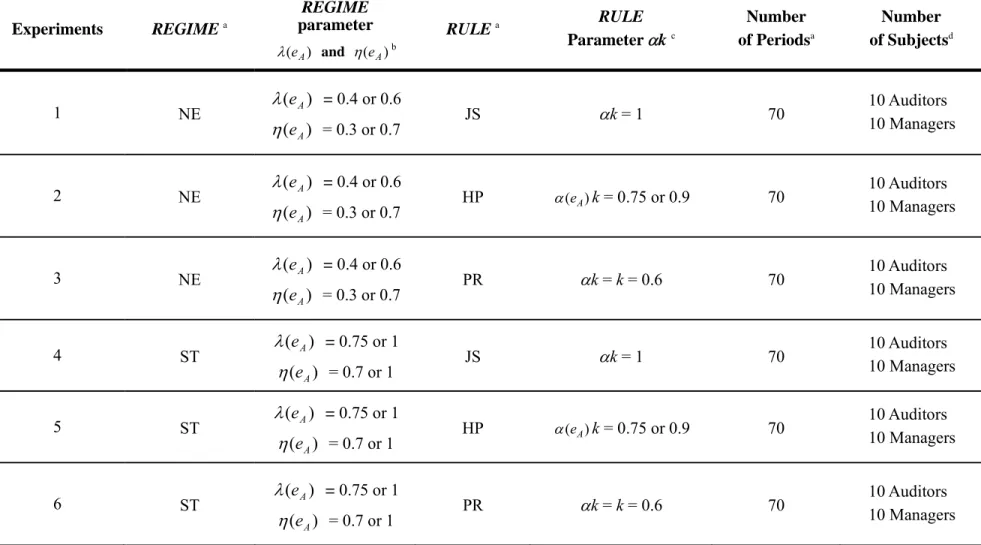

To test the hypotheses of interest, I adopts a 2×3 factorial design, with two between-subject variables: REGIME (manipulated at two levels: NE vs. ST) and RULE (manipulated at three levels: JS

vs. HP vs. PR). Each experiment consists of 70 periods. Each period simulates the one-period game

between auditor and manager specified in section 2.1. Table 2 summaries the experimental design.

[Insert Table 2 here]

my assumption. In this case, a former Ernst & Young partner, Thomas Trauger, asked Oliver Flanagan, a former senior manager of Ernst & Young, to alter the electronic workpapers for the NextCard’s 2000 audit in fear of being investigated by the SEC. This is one of the first cases in the U.S. in which an auditor has been accused of destroying key audit documents in an effort to obstruct an investigation brought under the Sarbanes-Oxley Act of 2002.

7I set the probabilities that the auditor will be held liable for AF

tec and AFind to be different (i.e., η(eA)and λ(eA), respectively) because the merits of these two types of audit failure are not the same in real litigation cases. Also, they are subject to different damage apportionment rules (i.e., joint-and-several vs. proportionate). Note that: (a) I design ( high)

A

e

λ

to be greater than ( high)

A

e

η under the NE legal regime because the auditor is less likely to be held liable for AFtec due to

the safe-harbor provision for forward-looking information specified in the 1995 Reform Act, and (b) I assume that the court is able to distinguish between these two types of audit failure once it determines that the auditor is held liable.

A notional currency called Experimental Dollars (EDs) will be used in the experiments. In each

experiment, all communications and interactions between players will be handled by a system of

networked personal computers. I will conduct a pilot test before the formal experiments to test the

appropriateness of the experimental instructions. In the formal four experiments, the subject pool

consists of 80 senior Business School students, with ten auditor-subjects and ten manager-subjects

randomly assigned to each experiment. Students participate in two sessions. At the half-hour training

session, subjects receive written instructions that are read aloud by the experimenter. After clarifying

questions are answered, a quiz (consists of ten true-false questions) will be given to ensure that all

subjects have understood the instructions and how their decisions might affect their cash payments. All

subjects are paid US $0.10 for each question they answer correctly. The cash that each subject receives

in the quiz is in addition to his or her cash earnings in the formal experiments. This training session is

scheduled because of the relative complexity of the experiments.

Immediately following the training session will be the two-and-half-hour experiment session. All

subjects should draw to determine the role they will play in the experiment and the experimental

periods then commence. At the beginning of each period, each manager-subject will be endowed with

12,000 EDs and each auditor-subject will be endowed with 10,000 EDs. Each subject plays the same

role throughout all 80 periods.

The steps for each experimental period are described below:

Step 1: At the beginning of each period, the computer randomly assigns each auditor to a manager.

Auditors are not informed of their assigned managers. This “manager-auditor” relation holds

in that period only. This procedure is important to the experiments because my model does not

consider auditor’s and manager’s reputation effect.

Step 2: At the beginning of each period, each manager-subject is provided with two investment

investment (with an effort cost of 6,500 EDs). All manager-subjects know that if I is low

undertaken, there is a 0.70 probability of receiving L and a 0.30 probability of receiving H. In

contrast, if Ihigh is undertaken, the manager would have a 0.70 probability of receiving H and

a 0.30 probability of receiving L. Each manager-subject can only choose one investment

project to undertake.

Step 3: The manager-subject privately determines the investment to be undertaken by choosing either

“High Investment” or “Low Investment” on the computer screen. This becomes the

manager-subject’s private information.

Step 4: The manager-subject privately determines the investment to be undertaken by choosing either

“High Investment” or “Low Investment” on the computer screen. This becomes the

manager-subject’s private information.

Step 5: The realized earnings is determined by the computer following the probability distribution

specified in Step 2 and is shown on each manager-subject’s screen. The manager-subject

determines the earnings report by choosing either “High Earnings” or “Low Earnings” on the

computer screen.

Step 6: The manager-subject pays a flat audit fee 4,500 EDs to hire an auditor-subject to credibly

verify the outcome of the investment.

Step 7: Each auditor-subject privately determines the effort level to be exerted by choosing either

“High Effort Level” (with an effort cost of 2,600 EDs) or “Low Effort Level” (with an effort

cost of 1,000 EDs) on the computer screen. Each auditor-subject knows that if the realized

earnings is H, he will always obtain a “High” audit signal SH with probability one. If the

realized earnings is L, the auditor-subjects will obtain a “Low” signal SL with probability 0.7 if

he exerts high A

e but will obtain the correct signal with probability 0.3 if he only exerts low A

Step 8: Based on the auditor-subject’s effort choice and the realized earnings, the computer determines

the audit signal according to the probability distribution specified in Step 7.

Step 9: Upon observing the audit signal, the auditor-subject privately determines the audit report by

choosing either “High Earnings Report” or “Low Earnings Report” on the computer screen

based on the reporting rules and the corresponding legal liabilities specified in section 3.1.

Step 10: Each player’s payoff is determined and the experimental period terminates.

4. EXPERIMENTAL RESULTS

The experimental results from the preliminary analyses generally support the model predictions. Please contact the author for details.

FIGURE 1 Game Tree of the Modela

i I H H S ∧ H No

( )

Ii ρ 1−ρ( )

Ii L H R RH L R( )

eA q 1−q( )

eA L S ∧ L ∧ H δ 1−δ indAF AFind AFtec AFtec

( )

eA 1−λ Yes Noc b No b No H S δ 1−δ ∧ H δ 1−δ c No( )

eA λ JS ST A No L S ∧ L No JS ST B Yes( )

eA η No( )

eA η 1− JS ST C JS ST D JS ST E JS ST F JS ST G JS ST H JS ST I JJSST PR ST A PR ST B PR ST C PR ST D ESTPR FSTPR PR ST G PR ST H PR ST I PR ST J HP NE A HP NE B HP NE C HP NE D EHPNE FNEHP HP NE G HP NE H HP NE I HP NE J JS NE A JS NE B JS NE C JS NE D EJSNE FNEJS JS NE G JS NE H JS NE I JS NE J PR ST A PR ST B PR ST C PR ST D EPRST FSTPR PR ST G PR ST H PR ST I PR ST J HP NE A HP NE B HP NE C HP NE D HP NE E HP NE F HP NE G HP NE H HP NE I JHPNEaThe variables shown in this game tree are defined as follows: I

i denotes the manager’s investment amount, where i ∈ {high, low}; H and L denote the high and low investment outcomes,

respectively; ρ(Ii) denotes the probability that the outcome is H when the manager invests Ii amount; Rk denotes the manager’s financial report, where k ∈ {H, L}; q(eA) denotes the audit

quality when the auditor’s effort level is eA; SH and SL denote the audit signals that the investment outcome is H and L, respectively; Hˆ and Lˆ denote the auditor’s high-outcome and

low-outcome report, respectively; δ denotes the probability that the state of the economy is bad; AFind and AFtec denote auditor’s independence and technical audit failure, respectively; λ(eA)

denotes the probability that the auditor will be held liable by the court when an AFind occurs; η(eA) denotes the probability that the auditor will be held liable by the court when an AFtec occurs; ST and NE denote the strict and negligence legal regimes, respectively. Letters A to J denote managers’ and auditor’s possible payoffs under different game outcomes (see Appendix for detailed descriptions).

bThere is no audit failure under these two scenarios (no matter whether the state of economy is good or bad) because the auditor’s report correctly informs the investors of the investment outcome and, thus, is not misleading.

cEven though an audit failure occurs under these two scenarios, the auditor is not held liable by the court because the state of economy is good and, therefore, the firm will not go bankrupt. In my model, only a violation of the going-concern will trigger a lawsuit against the auditor.

TABLE 1

Summary of Notations and Parameter Values

Variables Definitions Parameter Values

(1) Investment Parameters:

i

I Investment project i ∈ {high, low}

ω Outcome of the investment ω∈ {H, L}

) (Ii

ρ Probability that the investment outcome is H ρ(Ihigh)=0.7, 3ρ(Ilow)=0.

(2) Manager’s Parameters:

i M

e Manager’s effort level for investment Ii i ∈ {high, low} )

(eMi

C Manager’s effort cost when his effort level is i M

e C(eMhigh)= 6,500, C(elowM )= 4,200

Mr Manager’s compensation when audit report is r MHˆ = 24,000, MLˆ=16,000 SP Side payment paid by the manager to the auditor 2,800 EDs

ASC Manager’s restating cost plus switching cost because the

auditor is dismissed 7,000 EDs

(3) Auditor’s Parameters:

F Audit fees 5,500 EDs

j A

e Auditor’s effort level j ∈ {high, low}

) ( j

A e

C Auditor’s effort cost when his effort level is eAj ( high)=2,600

A e C , ( low)=2,200 A e C

ξ Audit signal obtained ξ ∈ {SH, SL}

) ( j

A e

q Audit quality ( high)=0.7

A e q , ( low)=0.3 A e q

r Audit report type r∈{Hˆ,Lˆ}

ER Present value of all future quasi rents 6,000 EDs

(4) Legal Liability Parameters:

δ Probability that the state of economy is bad 0.6 )

( j

A

e

λ Probability (auditor is held liable for AFind)

NE regime: ( high) A e λ = 0.4, λ(elowA )= 0.6 ST regime: ( high) A e λ = 0.75, ( low) A e λ = 1 ) ( j A e

η Probability (auditor is held liable for AFtec)

NE regime: ( high) A e η = 0.3, ( low) A e η = 0.7 ST regime: ( high) A e η = 0.7, ( low) A e η = 1

Dtec Total damage losses due to AFtec 8,000 EDs

Dind Total damage losses due to AFind 14,500 EDs

k The percent of Dtec or Dind paid by the auditor k = 0.6 α The proportional damage multiplier

JS rule: αk = 1

HP rule:α(ehighA )= 1.25, α(elowA )= 1.5 PR rule: α = 1

TABLE 2 Experimental Design Experiments REGIMEa REGIME parameter ) (eA λ and η(eA)b RULEa RULE Parameter αk c Number of Periodsa Number of Subjectsd 1 NE λ(eA) = 0.4 or 0.6 ) (eA η = 0.3 or 0.7 JS αk = 1 70 10 Auditors 10 Managers 2 NE λ(eA) = 0.4 or 0.6 ) (eA η = 0.3 or 0.7 HP α(eA)k = 0.75 or 0.9 70 10 Auditors 10 Managers 3 NE λ(eA) = 0.4 or 0.6 ) (eA η = 0.3 or 0.7 PR αk = k = 0.6 70 10 Auditors 10 Managers 4 ST λ(eA) = 0.75 or 1 ) (eA η = 0.7 or 1 JS αk = 1 70 10 Auditors 10 Managers 5 ST λ(eA) = 0.75 or 1 ) (eA η = 0.7 or 1 HP α(eA)k = 0.75 or 0.9 70 10 Auditors 10 Managers 6 ST λ(eA) = 0.75 or 1 ) (eA η = 0.7 or 1 PR αk = k = 0.6 70 10 Auditors 10 Managers

aThis study adopts a 2×3 factorial design, with two between-subject variables: REGIME (manipulated at two levels: NE vs. ST) and RULE (manipulated at three levels:

JS vs. HP vs. PR). NE and ST denote negligence and strict legal regimes, respectively; JS, HP, and PR denote joint-and-several, hybrid, and proportionate damage apportionment rules, respectively. Each experiment consists of 70 periods.

bUnder both the NE and ST regimes, the probabilities that the auditor will be held liable by the court when there is an AF

ind and AFtec are λ(eA) and η(eA), respectively.

cIn the experiment as well as in my model, the auditor has to pay αk percent of the total D

tec (or Dind) when there is an AFtec (or AFind), where k is the percent of Dtec or Dind paid by the auditor and α is the proportional damage multiplier. In the experiments I manipulate αk to be 1, 0.75 or 0.9, and 0.6 under the JS, HP, and PR damage rules, respectively, to capture the basic difference among these three rules.

dThe subject pool will consist of 120 senior Business School students, with 10 auditor-subjects and 10 manager-subjects randomly assigned to each experiment. All

subjects shall draw to determine the role they will play in the experiments. At the beginning of each period, each manager-subject is endowed with 12,000 EDs and each auditor-subject is endowed with 10,000 EDs. Each subject plays the same role throughout all 70 periods.

REFERENCES

Abbott, L.J., S. Parker, G.F. Peters, and K. Raghunandan. 2003. An empirical investigation of audit fees, nonaudit fees, and audit committees. Contemporary Accounting Research 20 (Summer): 215-234.

Bloomfield, R.J. and T.J. Wilks. 2000. Disclosure effects in the laboratory: Liquidity, depth and the cost of capital. The Accounting Review 75 (January): 13-42.

Boritz, J. and P, Zhang. 1997. The implications of alternative litigation cost allocation systems for the value of audits. Journal of Accounting, Auditing, and Finance 12 (Fall): 353-372.

Bushman, R.M. and A.J. Smith. 2001. Financial accounting information and corporate governance.

Journal of Accounting & Economics 32: 237-333.

Bushman, R.M. and A.J. Smith. 2003. Transparency, financial accounting info5rmation, and corporate governance. FRBNY Economic Policy Review (April): 65-87.

Chan, D.K. and S. Pae. 1998. An analysis of the economic consequences of the proportionate liability rule. Contemporary Accounting Research 15 (Winter): 457-480.

Citron, D.B. 2003. The UK’s framework approach to auditor independence and the commercialization of the accounting profession. Accounting, Auditing & Accountability Journal 16 (February): 244-274.

Cote, M. 2002. Auditor independence. CA Magazine 135 (September): 68.

Craswell, A., D.J. Stokes, and J. Laughton. 2002. Auditor independence and fee dependence. Journal

of Accounting & Economics 33 (June): 253-275.

DeAngelo, L. 1981. Auditor size and audit quality. Journal of Accounting and Economics 3 (1): 183-199.

Dopuch, N., D. E. Ingberman and R. R. King. 1997. An experimental investigation of multi-defendant bargaining in ‘joint and several’ and proportionate liability regimes. Journal of Accounting and

Economics 23 (3): 189−221.

Dopuch, N. and R. R. King. 1992. Negligence versus strict liability regimes in auditing: An experimental investigation. The Accounting Review 67 (January): 97-120.

Dopuch, N., R. R. King, and J. W. Schatzberg. 1994. An experimental investigation of alternative damage-sharing liability regimes with an auditing perspective. Journal of Accounting Research 32 (Supplement): 103-139.

Dopuch, N., R.R. King, and R. Schwartz. 2003. Independence in appearance and in fact: An experimental investigation. Contemporary Accounting Research 20 (Spring): 79-119.

Dye, R. 1993. Auditing standards, legal liability, and auditor wealth. Journal of Political Economy 101: 887-914.

Dye. R., B.V. Balachandran, and R. Magee. 1990. Contingent fees for audit firms. Journal of

Accounting Research 28 (Autumn): 239-266.

Gerde, V.W. and C.G. White. 2003. Auditor independence, accounting firms, and the SEC. Business

and Society 42 (March): 83-115.

The Accounting Review 74 (July): 347-369.

Hodge, F.D. 2003. Investors’ perceptions of earnings quality, auditor independence, and the usefulness of audited financial information. Accounting Horizon 17 (supplement): 37-48.

Kachelmeier, S. 1996a. Discussion of “Tax advice and reporting under uncertainty: Theory and experimental evidence.” Contemporary Accounting Research 13 (Spring): 25-48.

Kachelmeier, S. 1996b. Do cosmetic reporting variations affect market behavior? A laboratory study of the accounting emphasis on unavoidable costs. Review of Accounting Studies 1 (2): 115-140. Kachelmeier, S. and R.R. King. 2002. Using laboratory experiments to evaluate accounting policy

issues. Accounting Horizon 16 (September): 219-232.

Kaiser, G.S. and T.G. Perris. 2003. Auditor independence. National Law Journal 25 (March): B8. Khurana, I.K. and K.K. Raman. 2004. Litigation risk and the financial reporting credibility of Big 4 vs.

Non-Big 4 audits: Evidence from Anglo-American countries. The Accounting Review 79 (April): 473-495.

Kieso, D.E., J.J. Weygandt, and T.D. Warfield. 2003. Intermediate Accounting. 11th edition. NY: John Wiley and Sons.

Kirk, R.E. 1982. Experimental Design: Procedures for the Behavioral Science. CA: Brooks/Cole Publishing Company.

King, R. R. and R. Schwartz. 1997. The Private Securities Litigation Reform Act of 1995: A discussion of three provisions. Accounting Horizon 11 (March): 92-106.

King, R.R. and R. Schwartz. 1999. Legal penalties and audit quality: An experimental investigation.

Contemporary Accounting Research 16 (Winter): 685-710.

King, R.R. and R. Schwartz. 2000. An experimental investigation of auditors’ liability: Implications for social welfare and exploration of deviation from theoretical predictions. The Accounting

Review 75 (October): 429-451.

Kopel, J.L. 2003. The SEC’s new auditor independence rules. Insights: The Corporate & Securities

Law Advisor 17 (March): 18-30.

Lee, C.W. and Z.Y. Gu. 1998. Low balling, legal liability and auditor independence. The Accounting

Review 73 (October): 533-555

Libby, R., R.J. Bloomfield, and M.W. Nelson. 2002. Experimental research in financial accounting.

Accounting, Organizations and Society 27 (November): 775-810.

Lousteau, C.L. and M.E. Reid. 2003. Internal control systems for auditor independence. The CPA

Journal 73 (January): 36-41.

Melumad, N.D. and L. Thoman. 1990. On auditors and the courts in an adverse selection setting.

Journal of Accounting Research 28 (Spring): 77-120.

Narayanan, V. G. 1994. An analysis of auditor liability rules. Journal of Accounting Research 32 (Supplement): 39-64.

Pae, S. and S-W Yoo. 2001. Strategic interaction in auditing: An analysis of auditors’ legal liability, internal control system quality, and audit effort. The Accounting Review 76 (July): 333-356. Palmrose, Z-V. 1994. The joint & several vs. proportionate liability debate: An empirical investigation

Private Securities Litigation Reform Act of 1995. Public Law No. 104-167. Washington D.C.: US Government Printing Office.

Radhakrishnan, S. 1999. Investors' recovery friction and auditor liability rules. The Accounting Review 74 (April): 225-240.

Sarbanes-Oxley Act of 2002. Public Law No. 107-204. Washington D.C.: US Government Printing Office.

Schwartz, D. 1997. Legal regimes, audit quality and investment. The Accounting Review 72 (July): 385-406.

Securities and Exchange Commission (SEC). 2003. Strengthening the Commission’s Requirements

Regarding Auditor Independence. January. Washington, D.C.: Government Printing Office.

Smith, V. L. 1976. Experimental economics: Induced value theory. American Economic Review (May): 274-279.

Smith, V. L. 1989. Theory, experiment and economics. Journal of Economic Perspectives 3 (Winter): 151-169.

Smith, V. L. 1994. Economics in the laboratory. Journal of Economic Perspectives 8 (Winter): 113-131.

Swieringa, R. and K. Weick. 1982. An assessment of laboratory experiments in accounting. Journal of

Accounting Research 20 (Supplement): 56-101.

Thoman, L. 1996. Legal damages and auditor efforts. Contemporary Accounting Research 13 (Spring): 275-306.

APPENDIX 1

Players’ Payoffs under Different Legal Regime and Damage Apportionment Rule Combinationsa

Panel A: ST_JS Setting

Game Outcomes Manager Auditor

JS ST A MHˆ−C(eM)−F F−C(eA)+ER JS ST B M C(e ) F M Lˆ − − F−C(eA)+ER JS ST C 0 F−C(eA)+SP−Dind JS ST D NAb NAb JS ST E MHˆ −C(eM)−SP−F F−C(eA)+SP+ER JS ST F 0 F−C(eA) JS ST G M C(eM) ASC F Lˆ − − − F−C(eA) JS ST H 0 F−C(eA)−Dtec JS ST I NAb NAb JS ST J M C(eM) F Hˆ− − F−C(eA)+ER Panel B: ST_PR Setting

Game Outcomes Manager Auditor

PR ST A MHˆ−C(eM)−F F−C(eA)+ER PR ST B M C(e ) F M Lˆ − − F−C(eA)+ER PR ST C 0 F−C(eA)+SP−k⋅Dind PR ST D NAb NAb PR ST E MHˆ −C(eM)−SP−F ERF−C(eA)+SP+ PR ST F 0 F−C(eA) PR ST

G MLˆ −C(eM)−ASC−F F−C(eA)

PR ST H 0 F−C(eA)−k⋅Dtec PR ST I NAb NAb PR ST J MHˆ−C(eM)−F F−C(eA)+ER

APPENDIX 1 (cont’d)

Players’ Payoffs under Different Legal Regime and Damage Apportionment Rule Combinations (cont’d)

Panel C: ST_HP Setting

Game Outcomes Manager Auditor

HP ST A MHˆ−C(eM)−F F−C(eA)+ER HP ST B M C(e ) F M Lˆ − − F−C(eA)+ER HP ST C 0 F−C(eA)+SP−α⋅k⋅Dind HP ST D NAb NAb HP ST E MHˆ −C(eM)−SP−F ERF−C(eA)+SP+ HP ST F 0 F−C(eA) HP ST

G MLˆ −C(eM)−ASC−F F−C(eA)

HP ST H 0 F−C(eA)−α⋅k⋅Dtec HP ST I NAb NAb HP ST J MHˆ−C(eM)−F F−C(eA)+ER

APPENDIX 1 (cont’d)

Players’ Payoffs under Different Legal Regime and Damage Apportionment Rule Combinations (cont’d)

Panel D: NE_JS Setting

Game Outcomes Manager Auditor

JS NE A MHˆ−C(eM)−F F−C(eA)+ER JS NE B MLˆ−C(eM)−F ERF−C(eA)+ JS NE C 0 F−C(eA)+SP−Dind JS NE D 0 F−C(eA)+SP JS NE E MHˆ −C(eM)−SP−F SPF−C(eA)+ER+ JS NE F 0 F−C(eA) JS NE G M C(eM) ASC F Lˆ− − − F−C(eA) JS NE H 0 F−C(eA)−Dtec JS NE I 0 F−C(eA) JS NE J MHˆ −C(eM)−F F−C(eA)+ER

Panel E: NE_PR Setting

Game Outcomes Manager Auditor

PR NE A MHˆ−C(eM)−F F−C(eA)+ER PR NE B MLˆ −C(eM)−F F−C(eA)+ER PR NE C 0 F−C(eA)+SP−k⋅Dind PR NE D 0 F−C(eA)+SP PR NE E MHˆ −C(eM)−SP−F SPF−C(eA)+ER+ PR NE F 0 F−C(eA) PR NE

G MLˆ−C(eM)−ASC−F F−C(eA)

PR NE H 0 F−C(eA)−k⋅Dtec PR NE I 0 F−C(eA) PR NE J MHˆ −C(eM)−F F−C(eA)+ER

APPENDIX 1 (cont’d)

Players’ Payoffs under Different Legal Regime and Damage Apportionment Rule Combinations (cont’d)

Panel F: NE_HP Setting

Game Outcomes Manager Auditor

HP NE A MHˆ−C(eM)−F F−C(eA)+ER HP NE B MLˆ−C(eM)−F ERF−C(eA)+ HP NE C 0 F−C(eA)+SP−α⋅k⋅Dind HP NE D 0 F−C(eA)+SP HP NE E MHˆ −C(eM)−SP−F SPF−C(eA)+ER+ HP NE F 0 F−C(eA) HP NE G M C(eM) ASC F Lˆ− − − F−C(eA) HP NE H 0 F−C(eA)−α⋅k⋅Dtec HP NE I 0 F−C(eA) HP NE J MHˆ −C(eM)−F F−C(eA)+ER a

See Table 1 for the definitions and parameter values of all variables shown in this Appendix.

bSince λ(e

A) and η(eA) equal one under the strict legal regime, game outcomes D and I in Panels A, B, and C do not

APPENDIX 2

Numerical Solutions of the Game

The strategy spaces for the Auditor and the Manager, respectively, are as follows:

For the Auditor: {(Exert high effort, Report high when audit signal is low), (Exert low effort, Report low when audit signal is low), (Exert high effort, Report low when audit signal is low), (Exert low effort, Report high when audit signal is low)}

The Manager: {(High investment, Report High), (Low investment, Report High), (Invest Low, Report High), (Invest Low, Report Low)}

The payoff functions for both players are as follows: 1. Under NE_JS (or ST_JS):

Payoff functions for the Auditor: )) , ( ), ˆ , (( Aj i A e H H I U =(ρ(Ii)+(1−ρ(Ii)(1−δ))⋅ER+F−C(eAj)+(1−ρ(Ii))(−q(eAj)⋅δ⋅Dtecη(eAj)+ )) ( ))( ( 1 ( −q eAj SP−δ⋅Dind⋅λ eAj )) , ( ), ˆ , (( Aj i A e L H I U =(ρ(Ii)+(1−ρ(Ii)(1−δ)⋅q(eAj))⋅ER+F−C(eAj)−(1−ρ(Ii))(1−q(eAj))⋅δ⋅Dtec⋅η(eAj) )) , ( ), ˆ , (( j i A A e H L I U = ( j) A e C F ER+ − )) , ( ), ˆ , (( Aj i A e L L I U =ER+F−C(eAj)

Payoff functions for the manager: )) , ( ), ˆ , (( Mi j M e H H I U =(ρ(Ij)+(1−ρ(Ij))(1−δ))MH−Ij−F−(1−ρ(Ij))(1−q(ei))(1−δ)SP )) , ( ), ˆ , ((i j M e L H I U =(ρ(Ij)+(1−ρ(Ij))q(ei)(1−δ))(MH)−Ij−F+(1−ρ(Ij))(1−q(ei))(ML−ASC) )) , ( ), ˆ , ((i j M e H L I U =ρ(Ij)MH +(1−ρ(Ij))ML−Ij−F )) , ( ), ˆ , ((i j M e L L I U =ρ(Ij)MH+(1−ρ(Ij))ML−Ij−F

2. Under NE_PR (or ST_PR):

Payoff functions for the Auditor:

)) , ( ), ˆ , (( i j A e H H I U =(ρ(Ij)+(1−ρ(Ij)(1−δ))ER+F−ei+ )) ( ))( ( 1 ( ) ( ) ( ))( ( 1 ( −ρ Ij −q ei δDtecη ei + −q ei SP−kδDindλ ei )) , ( ), ˆ , (( i j A e L H I U =(ρ(Ij)+(1−ρ(Ij)(1−δ)q(ei))ER+F−ei ) ( )) ( 1 ))( ( 1 ( −ρ Ij −q ei δkDtecη ei − )) , ( ), ˆ , (( i j A e H L I U =ER+F−ei )) , ( ), ˆ , (( i j A e L L I U =ER+F−ei

Payoff functions for the manager:

)) , ( ), ˆ , (( i j M e H H I U =

SP e q I F I M I Ij) (1 ( j))(1 )) H j (1 ( j))(1 ( i))(1 ) ( (ρ + −ρ −δ − − − −ρ − −δ )) , ( ), ˆ , (( i j M e L H I U = ) ))( ( 1 ))( ( 1 ( ) ))( 1 )( ( )) ( 1 ( ) ( (ρ Ij + −ρ Ij q ei −δ MH −Ij−F+ −ρ Ij −q ei ML−ASC )) , ( ), ˆ , (( i j M e H L I U =ρ(Ij)MH +(1−ρ(Ij))ML −Ij −F )) , ( ), ˆ , (( i j M e L L I U =ρ(Ij)MH +(1−ρ(Ij))ML−Ij −F 3. Under NE_HP (or ST_HP):

Payoff functions for the Auditor:

)) , ( ), ˆ , (( i j A e H H I U =(ρ(Ij)+(1−ρ(Ij)(1−δ))ER+F−ei+ )) ( ) ( ))( ( 1 ( ) ( ) ( ))( ( 1 ( −ρ Ij −q ei δDtecη ei + −q ei SP−α ei kδDindλ ei )) , ( ), ˆ , (( i j A e L H I U =(ρ(Ij)+(1−ρ(Ij)(1−δ)q(ei))ER+F−ei ) ( ) ( )) ( 1 ))( ( 1 ( −ρ Ij −q ei δα ei kDtecη ei − )) , ( ), ˆ , (( i j A e H L I U =ER+F−ei )) , ( ), ˆ , (( i j A e L L I U =ER+F−ei

Payoff functions for the manager:

)) , ( ), ˆ , (( i j M e H H I U = SP e q I F I M I Ij) (1 ( j))(1 )) H j (1 ( j))(1 ( i))(1 ) ( (ρ + −ρ −δ − − − −ρ − −δ )) , ( ), ˆ , (( i j M e L H I U = ) ))( ( 1 ))( ( 1 ( ) ))( 1 )( ( )) ( 1 ( ) ( (ρ Ij + −ρ Ij q ei −δ MH −Ij−F+ −ρ Ij −q ei ML−ASC )) , ( ), ˆ , (( i j M e H L I U =ρ(Ij)MH +(1−ρ(Ij))ML −Ij −F )) , ( ), ˆ , (( i j M e L L I U =ρ(Ij)MH +(1−ρ(Ij))ML−Ij −F

(1) Under the Negligence (NE) legal regime (λ(eH) = 0.4,λ(eL) = 0.6, η(eH) = 0.3, η(eL) = 0.7): (a) The JS_NE regulation system:

Undertake Ihigh,

report high when realized earnings is L

Undertake Ihigh,

report low when realized earnings is L

Undertake Ilow,

report high when realized earnings is L

Undertake Ilow,

report low when realized earnings is L Exert ehigh,

Report high when SL (7547.6, 9604.8) (9020, 9600) (5744.4, 7745.2) (9180, 8700)

Exert ehigh,

Report low when SL (7186.4, 8580) (9020, 9600) (4901.6, 5354) (9180, 8700)

Exert elow,

Report high when SL (7296.6, 9739.2) (9300, 9600) (4625.4, 8058.8) (9300, 8700)

Exert elow,

(b) The PR_NE regulation system:

Undertake Ihigh,

report high when realized earnings is L

Undertake Ihigh,

report low when realized earnings is L

Undertake Ilow,

report high when realized earnings is L

Undertake Ilow,

report low when realized earnings is L Exert ehigh,

Report high when SL (7891.76, 9604.8) (9020, 9600) (6547.44, 7745.2) (9180, 8700)

Exert ehigh,

Report low when SL (7238.24, 8580) (9020, 9600) (5022.56, 5354) (9180, 8700)

Exert elow,

Report high when SL (7766.76, 9739.2) (9300, 9600) (5722.44, 8058.8) (9300, 8700)

Exert elow,

Report low when SL (7580.64, 9300) (9300, 9600) (5288.16, 7034) (9300, 8700)

(c) The HP_NE regulation system:

Undertake Ihigh,

report high when realized earnings is L

Undertake Ihigh,

report low when realized earnings is L

Undertake Ilow,

report high when realized earnings is L

Undertake Ilow,

report low when realized earnings is L Exert ehigh,

Report high when SL (7762.7, 9604.8) (9020, 9600) (6246.3, 7745.2) (9180, 8700)

Exert ehigh,

Report low when SL (7218.8, 8580) (9020, 9600) (4977.2, 5354) (9180, 8700)

Exert elow,

Report high when SL (7414.14, 9739.2) (9300, 9600) (4899.66, 8058.8) (9300, 8700)

Exert elow,

Report low when SL (7368.96, 9300) (9300, 9600) (4794.24, 7034) (9300, 8700)

(2) Under the Strict (ST) legal regime (λ(eH) = 0.75,λ(eL) = 1, η(eH) = 0.7, η(eL) = 1): (a) The JS_ST regulation system:

Undertake Ihigh,

report high when realized earnings is L

Undertake Ihigh,

report low when realized earnings is L

Undertake Ilow,

report high when realized earnings is L

Undertake Ilow,

report low when realized earnings is L Exert ehigh,

Report high when SL (6735.35, 9604.8) (9020, 9600) (3849.15, 7745.2) (9180, 8700)

Exert ehigh,

Report low when SL (7013.6, 8580) (9020, 9600) (4498.4, 5354) (9180, 8700)

Exert elow,

Report high when SL (6681, 9739.2) (9300, 9600) (3189, 8058.8) (9300, 8700)

Exert elow,

(b) The PR_ST regulation system:

Undertake Ihigh,

report high when realized earnings is L

Undertake Ihigh,

report low when realized earnings is L

Undertake Ilow,

report high when realized earnings is L

Undertake Ilow,

report low when realized earnings is L Exert ehigh,

Report high when SL (7501.61, 9604.8) (9020, 9600) (5637.09, 7745.2) (9180, 8700)

Exert ehigh,

Report low when SL (7231.76, 8580) (9020, 9600) (5007.44, 5354) (9180, 8700)

Exert elow,

Report high when SL (7397.4, 9739.2) (9300, 9600) (4860.6, 8058.8) (9300, 8700)

Exert elow,

Report low when SL (7399.2, 9300) (9300, 9600) (4864.8, 7034) (9300, 8700)

(c) The HP_ST regulation system:

Undertake Ihigh,

report high when realized earnings is L

Undertake Ihigh,

report low when realized earnings is L

Undertake Ilow,

report high when realized earnings is L

Undertake Ilow,

report low when realized earnings is L Exert ehigh,

Report high when SL (7153.51, 9604.8) (9020, 9600) (4824.86, 7745.2) (9180, 8700)

Exert ehigh,

Report low when SL (7089.2, 8580) (9020, 9600) (4674.8, 5354) (9180, 8700)

Exert elow,

Report high when SL (6860.1, 9739.2) (9300, 9600) (3606.9, 8058.8) (9300, 8700)

Exert elow,