行政院國家科學委員會專題研究計畫 成果報告

兩類路徑相關型衍生性金融商品之積分計價公式與高速計

價演算法(3/3)

計畫類別: 個別型計畫 計畫編號: NSC93-2213-E-002-002- 執行期間: 93 年 08 月 01 日至 94 年 07 月 31 日 執行單位: 國立臺灣大學資訊工程學系暨研究所 計畫主持人: 呂育道 報告類型: 完整報告 報告附件: 出席國際會議研究心得報告及發表論文 處理方式: 本計畫可公開查詢中 華 民 國 94 年 10 月 12 日

兩類路徑相關型衍生性金融商品之積分計價公式與高速計價演算法(3/3) 計劃編號:NSC 93-2213-E-002-002- 執行期限:93/08/01—94/07/31 主持人:呂育道 臺灣大學資訊工程系教授 一、中文摘要 衍生性金融商品為一種價值決定於某標 的資產(如股票)的金融商品,其定價問題等 同於計算隨機變數期望值折現。路徑相關型 衍生性金商品的價值取決於標的資產價格之 全部或部分歷史,它們的定價通常是複雜的 計算問題。算術平均式選擇權又稱亞洲式選 擇權,其價值取決於基本資產價格之算術平 均,此種選擇權十分受到資本市場歡迎,但 定價十分困難。本計劃研究亞洲式選擇權之 訂 價 問 題 , 結 果 如 下 : (1) 一 個 有 效 率 的

( )

2.5 O n 近似演算法,且誤差為O n( )

−1 ,(2) 一個文獻上第一個打破指數障礙者的保證收 歛 ( )O n 2 演算法。 英文摘要Financial derivatives are financial instruments whose payoff depends on some underlying asset such as stock. Mathematically speaking, pricing such instruments amounts to calculating the discounted expected value of a random variable. Path-dependent derivatives are derivatives whose payoff depends on the history of the underlying asset’s price. Pricing is computationally nontrivial for such derivatives. Arithmetic average options are also known as Asian options. Their price depends on the arimetic average of historic stock prices. They are very popular in the capital markets. This proposal investigates the pricing of Asian options. Our findings are: (1) an efficient

( )

2.5O n -time approximation algorithm with an error of

( )

1O n− , and (2) a convergent O( )n

2 -time exact algorithm, the first to break the exponential barrier in the literature.

二、計劃緣由與目的

Derivatives are financial instruments whose payoff depends on some underlying asset such as

stock. Mathematically speaking, pricing such products amounts to calculating the discounted expected value of a random variable. These products represent a quantum leap in the capital markets because they provide tools for managing financial risks and speculation. The notional market size of derivatives is in the trillions US dollars range (72 trillion US dollars as of June of 1998). Research in this area therefore has important practical implications and has been extremely active. See Lyuu (2002) for a survey.

Path-dependent derivatives are derivatives whose payoff depends nontrivially on the history of the underlying asset’s price. The price is usually described as a continuous-time stochastic process (see the next figure). For our purpose, we will take the asset prices to be a time series

0, 1, , n

S S … S , where the price S is a lognormal i

random variable with a known mean and variance. Pricing is usually computationally nontrivial for path-dependent derivatives.

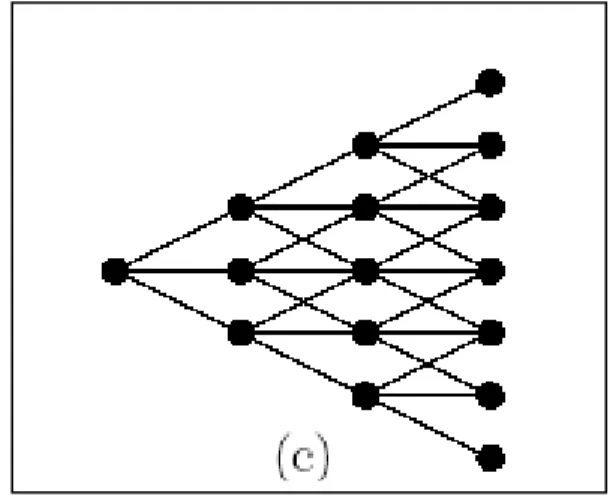

In practice, the lognormal variables are approximated by a binomial random walk (see

the figure below).

The purpose of our proposal is the pricing of the prominent path-dependent derivative: the Asian option. Polynomial-time pricing algorithms are not available for this option and in fact are not expected to be available. The purpose of this proposal is therefore polynomial-time approximation and subexponential-polynomial-time exact algorithms that converge to the true price.

The payoff of an Asian option is

0 max , 0 1 n i i S X n = ⎛ ⎞ ⎜ ⎟ ⎜ − ⎟ + ⎜ ⎟ ⎜ ⎟ ⎝ ⎠

∑

A tremendous amount of research has been carried out to attack the pricing problem of Asian options. It can be said that this is one of the most important problems in computational finance and financial economics [Hull97,Lyuu02].

In the analytical approach, the goal is to come up with a closed-form or semi-closed-form formula. The problem with this approach is two-fold. First, none of the formula in the literature is exact. Hence, they will fail on some input almost surely, and the accuracy cannot be improved, being a formula. Second, some Asian options can be American-style, which means they can be terminated at any time. Formulas cannot handle this early exercise feature.

In the Monte Carlo simulation approach, simulation of the asset price is conducted with the resulting payoffs then averaged. This method is quite general and when coupled with variance-reduction techniques or quasi-Monte Carlo sequences can be quite effective. The difficulty with this methodology is three-fold. First, the computed result has no a priori guarantee. Even

though the computed value can be proved to converge to the true value as n goes to infinity, the random noise means only stochastic bounds are available. Second, it cannot handle early exercise. Third, it is not very efficient.

Now we come to the approximation-algorithm approach [Hoch97]. Exact values can often be computed given

( )

nO 2 time bound. The complexity makes such algorithms useless. Our purpose is then to design efficient approximation algorithms.

The Asian option can always be priced by an

( )

nO 2 -time brute-force algorithm. This algorithm accomplishes the task by enumerating all possible price paths on the binomial model (see the next figure). We intend to design approximation algorithms that are efficient in practice and that converge weakly to the exact value.

三、實驗方法

Our first goal is a polynomial-time approximation algorithm with error guarantees. Specifically, we will construct an

( )

2.5O n -time algorithm with an error of

( )

1O n− .

The binomial model with n steps has a total of 2

/ 2 n

∼ nodes, whereas the total number of states (paths) is 2∼ . To allocate only n

( )

2.5O n

states to represent the whole 2∼ states, some n

approximation error must inevitably arise. There

S0

n

are three issues facing us. First, how do we allocate the

( )

2.5O n states? Second, which interpolation scheme to use when a missing state is called for? Third, what is the resulting error bound?

A node on the binomial model which has a low probability of occurrence should be able to tolerate large errors. Hence they should be handed fewer states. The technical problem is to balance the probability and the error nicely so that they together give an error of only

( )

1O n− . The whole issue is certainly a constrained optimization problem for which the Lagrange multiplier method is uniquely suitable for.

We start with the observation that, for European-style Asian options, a node only needs to work on states with a price sum up to some constant, say Y; any price sum over Y can be exactly priced [Aingworth00]. It implies that when we allocate k states to the node, the error it introduces is at most Y k/ . Next, as linear interpolation is guaranteed not to blow up the error, we resort to it. Finally, by combining this local error with the each node’s probability, we are able to write down the total error. By minimizing that total error subject to the constraint that the total number of states (the sum of all k) is

( )

2.5O n , the mathematics fit together perfectly. Interestingly, the number of states allocated to a node is proportional to its probability to the power of 1/ 3. This analysis relies on the asymptoric result of Bender.

The algorithm compares well with other numerical methods. Table 1 at the end of the report shows that the algorithm is not only faster but also converges faster when compared to the standard Hull-White algorithm and the superfast PDE method of [Forsyth02]. In fact, our analysis relies on the methodologies of [Forsyth02] too.

Table 2 compares our algorithm against analytical approximations. It shows that our algorithm converges fast, especially when the volatility σ is high. This is very important because no papers in the literature publish results with a volatility more than 50% with the exception of [Aingworth00].

We now move on to our second result: Breaking the exponential barrier. The major contribution is a novel trinomial model that does not require interpolation and is furthermore convergent (see the next figure). The algorithm must be an exact discrete-time algorithm without approximation. Our algorithm can price both European- and American-style Asian options. In contrast, the previous approximation algorithm handles only European-style Asian options. Convergence to the continuous-time value is guaranteed as the model matches the first and second moments of the continuous-time model at each node [Duffie96]. Such theoretical guarantee is lacking in most approximation schemes in the literature.

The ideas draw from [Dai02]. First, we will use trinomial models instead of binomial models for the extra degrees of freedom they offer. It is well-known that the option value is homogeneous of degree one in the asset price. We can therefore multiply the exercise price and all the asset prices on the model by some number

x, price the option, and finally divide the

calculated option value by x. This, together with the extra degrees of freedom afforded by the trinomial model, is exploited to construct a trinomial model with integer asset prices. This means that the price sum

0 i j i S =

∑

of any path 0, 1, , iS S … on the model will be integers as well. S

Recall that the payoff and the exercise value are both determined by the price sum.

The key insight can now be stated. The price sums of paths reaching any given node are finite in number and enumerable, being integers between some minimum and maximum price sums, which are integers. The integral property

will eventually allow backward induction to dispense with approximations. The algorithm is thus exact.

Nothing is gained with the above manipulations unless the number of states is reduced from exponential to subexponential. Let

σ be the stock price volatility and T be the maturity of the option (in years). It turns out that if we multiply all stock prices by

2 (0.5 ) 2 0 0.25 r T Tn n e T S σ σ σ − + ,

we will be able to find integer stock prices on the trinomial model. And as the above factor is proportional to 2O( )n , the trinomial model’s node count is also proportional to 2O( )n . The analysis is quite technical, and we will skip it. This is the first exact algorithm to break the exponential barrier in the literature.

Our theoretical algorithm is like the multiresolution algorithm of [Dai02]. The experiments there suggest that the algorithm is efficient and practical. For example, it can run for n up to 160 without difficulties. This is impossible for the brute-force algorithm because

160 76

3 ∼2.2 10× , an astronomical state count!

四、結論與討論

Both of our approximation and exact algorithms are breakthroughs in the literature. The approximation algorithm achieves a good error bound with a time bound of only

( )

2.5O n .

This is very close to the optimal time bound of

( )

2O n , the size of the binomial model. The error bound is

( )

1O n− . The techniques rely on asymptotic analysis and Lagrange multipliers. This can be the first result that introduces Lagrange multipliers into the pricing of options.

The exact algorithm has a running time of only O( )n

2 . It is the first exact algorithm that provably breaks the exponential barrier! Before a polynomial-time exact algorithm shows up, this remains the best exact algorithm in the literature. In fact, it is not likely that a polynomial-time algorithm exists at all.

五、參考文獻

[Aingworth00] Aingworth, Donald, Rajeev Motwani, and Jeffrey D. Oldham. “Accurate Approximations for Asian Options.” In

Proceedings of the 11th Annual ACM-SIAM Symposium on Discrete Algorithms, San Francisco, 2000.

[Atkinson89] Atkinson, K. E. An

Introduction to Numerical Analysis. 2nd ed. New York: Wiley, 1989.

[Bender74] Bender, E. A. “Asymptotic Methods in Enumeration.” SIAM Review, 16, No. 4 (1974), pp. 485–515.

[Curran94] Curran, Michael. “Valuing Asian and Portfolio Options by Conditioning on the Geometric Mean Price.” Management

Science, 40, No. 12 (December 1994), pp. 1705– 1711.

[Dai02] Dai, Tian-Shyr and Yuh-Dauh Lyuu. “Efficient, Exact Algorithms for Asian Options with Multiresolution Lattices.” Review of

Derivatives Research, Vol. 5 (2002), pp. 181– 203.

[Duffie96] Duffie, Darrell. Dynamic Asset

Pricing Theory. 2nd ed. Princeton, New Jersey: Princeton University Press, 1996.

[Forsyth02] Forsyth, P. A., K. R. Vetzal, and R. Zvan. “Convergence of Numerical Methods for Valuing Path-Dependent Options Using Interpolation.” Review of Derivatives

Research, Vol. 5 (2002), pp. 273–314.

[Fu98] Fu, Michael C., Dilip B. Madan, and Tong Wang. “Pricing Continuous Asian Options: A Comparison of Monte Carlo and Laplace Transform Inversion Methods.” Journal of

Computational Finance, 2, No. 2 (Winter 1998/9), pp. 49–74.

[Hoch97] Hochbaum, Dorit S. (Ed.)

Approximation Algorithms for NP-Hard Problems. Boston: PWS, 1997.

[Hull93] Hull, John C., and Alan White. “Efficient Procedures for Valuing European and American Path-Dependent Options.” Journal of

[Hull99] Hull, John C. Options, Futures,

and Other Derivatives. 4th ed. Englewood Cliffs, New Jersey: Prentice-Hall, 1999.

[Lyuu02] Lyuu, Yuh-Dauh. Financial

Engineering & Computation: Principles, Mathematics, and Algorithms. Cambridge, U.K.: Cambridge University Press, 2002.