行政院國家科學委員會專題研究計畫 成果報告

從美國次級房貸風暴探討台灣住宅抵押貸款違約因素與不

動產抵押債權證券化風險評估之研究

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 97-2410-H-004-107- 執 行 期 間 : 97 年 08 月 01 日至 98 年 07 月 31 日 執 行 單 位 : 國立政治大學地政學系 計 畫 主 持 人 : 林左裕 共 同 主 持 人 : 楊顯爵、陳宗豪 計畫參與人員: 碩士班研究生-兼任助理人員:侯蔚楚 碩士班研究生-兼任助理人員:程于芳 報 告 附 件 : 出席國際會議研究心得報告及發表論文 處 理 方 式 : 本計畫可公開查詢中 華 民 國 98 年 09 月 21 日

行政院國家科學委員會補助專題研究計畫成果報告

從美國次級房貸風暴探討台灣住宅抵押貸款違約因素

與不動產抵押債權證券化風險評估之研究

計畫類別:■ 個別型計畫 □ 整合型計畫

計畫編號:NSC 97-2410-H-004-107

執行期間:97 年 8 月 1 日至 98 年 7 月 31 日

計畫主持人:林左裕

共同主持人:楊顯爵

計畫參與人員:陳宗豪

成果報告類型(依經費核定清單規定繳交):■精簡報告 □完整

報告

本成果報告包括以下應繳交之附件:

□赴國外出差或研習心得報告一份

□赴大陸地區出差或研習心得報告一份

■出席國際學術會議心得報告及發表之論文各一份

□國際合作研究計畫國外研究報告書一份

處理方式:除產學合作研究計畫、提升產業技術及人才培育研究

計畫、列管計畫及下列情形者外,得立即公開查詢

執行單位:國立政治大學

中 華 民 國 九十八 年 七 月 三十一 日

從美國次級房貸風暴探討台灣住宅抵押貸款違約因素

與不動產抵押債權證券化風險評估之研究

前言

本研究已整理發表於三篇學術及實務期刊,如下所列: 1. 林左裕 (2009) 再論美國次級房貸風暴對我國金融資產證券化、估價制度及投資者之啟示, 土 地問題研究季刊,31(8-3), pp. 18-34。 2. 楊顯爵、林左裕、陳宗豪(2008)住宅抵押貸款違約之研究---影響因素之顯著性分析, 台灣土地 研究, 11(2), pp. 1-36 (NSC 97-2410-H-004-107 研究成果)(TSSCI)。 3. 林左裕(2008) 美國次級房貸風暴對台灣金融資產證券化及投資者之啟示,住宅學報,17(1), pp. 111-123(TSSCI)。 以下內容僅列出上述第一篇成果之內容,另關於台灣房貸之部分,資 料已蒐集完整,實證分析部分仍在進行中,將整理實證結果後再行發表。 摘 要 自 2006 年起美國發生次級房貸風暴後,終於在 2008 年蔓延至全世界,演 變為全球之金融海嘯,全球各界也自不同面向探討次貸危機發生的原因及影響程 度,各國也積極進行相關制度與法律規範之強化,以期能亡羊補牢及防範未然。 本研究首先進行次貸危機發生原因之探討,乃美國於 2004 年起實施之「可負擔 房屋計畫」(Affordable Housing Plan)之政策鼓勵能力不足之借款人申貸及提 供保證所致,輔以證券化架構使得放款銀行或貸款創始機構得以藉證券化機制移 轉放款風險,而無需審慎查核貸款所導致之「道德風險」。其次針對我國「金融 資產證券化條例」之架構進行探討與建議,包括要求放款金融機構在進行資產證 券化時,在風險分攤之原則下,應購回並持有部分具風險等級之證券,以避免道 德風險之發生;放款銀行對抵押不動產之估價宜採具中立性之估價師報告;以及 提供收益率(殖利率)曲線為未來發生金融風暴之先行指標等。所提建議對於未 來推行金融資產證券化可有效防範類似風暴之發生,以及在金融風暴發生前可提 供投資者決策之預警依據。關 鍵 詞 : 次 級 房 貸 風 暴(subprime mortgage crisis) 、 金 融 資 產 證 券 化 (asset securitization)、收益率曲線(yield curve)、不動產抵押權擔保證券 ( mortgage-backed security, MBS )、 債 權 抵 押 擔 保 債 券 (collateralized-debt obligation, CDO) 、 可 負 擔 房 屋 計 畫 (Affordable Housing Plan)

Abstract

The subprime mortgage crisis occurred in the U.S. in 2004 caused the worldwide financial markets turbulence. Subprime mortgages are risky mortgages with both high loan-to-value and debt payment-to-income ratio, and low credit scores. The U.S. has experienced a long-term period of low interest rates since 1980. Low interest rates encouraged homebuyers to acquire risky mortgages, and pushed up the prices of real estate and mortgage-related securities. To cope with the rising inflation in 2003, the U.S. government thus raised the interest rates drastically, consequently leading to the default peak of subprime mortgages and affecting the stability of global financial markets.

This study points out that the subprime mortgage crisis was caused by the structural weakness of the mortgage securitization --- originating mortgages without holding them, and thus losing the motivation of due diligence. The author finally proposed remedy for prevention of similar crisis, such as regulations requiring mortgage originators to hold some portions of risky securitized vehicles, and then keeping to the consistency of screening mortgage application. This study also found out that the change of the shape of “yield curve“ can serve as an effective warning signal for financial crisis. The suggestions proposed in this study may effectively improve the structure mechanism of asset securitization in Taiwan, and provide investors and overall financial markets worthy pre-caution indicators for financial crisis.

「土地問題研究季刊」

(2009),31(8-3), pp.18-34

再論美國次級房貸風暴對我國金融資產證券化、

估價制度及投資者之啟示

* 一、前言 自 2006 年起美國發生次級房貸風暴後,終於在 2008 年蔓延至全世界,演 變為全球之金融海嘯,全球各界也自不同面向探討次貸危機發生的原因及影響程 度,各國也積極進行相關制度與法律規範之強化,以期能亡羊補牢及防範未然。 本研究首先進行次貸危機發生原因之探討,乃美國於 2004 年起實施之「可負擔 房屋計畫」(Affordable Housing Plan)之政策鼓勵能力不及之借款人申貸及提供保 證所致,輔以證券化架構使得放款銀行或貸款創始機構得以藉證券化機制移轉放 款風險,而無需審慎查核貸款所導致之「道德風險」。其次針對我國「金融資產 證券化條例」之架構進行探討與建議,包括要求放款金融機構在進行資產證券化 時,應購回並持有部分具風險等級之證券,以避免道德風險之發生;以及放款銀 行對抵押不動產之估價宜具中立性;以及提供收益率曲線逆轉時為未來發生金融 風暴之先行指標等。所提建議對於未來推行金融資產證券化可有效防範類似風暴 之發生,以及在金融風暴發生前可提供投資者決策之預警依據。 二、次級房貸緣起之簡介 * 本文為國科會補助研究案 NSC 97-2410-H-004-107 部分成果,謹致謝忱。本文部份資料採自作 者於2008 年 6 月「住宅學報」第 17 卷第 1 期所發表之「美國次級房貸風暴對台灣金融資產證券 化及投資者之啟示」、2008 年 11 月 11 日於「地政節」之講稿、以及 2009 年於「地政學訊」所 發表之「都是房地產惹的禍嗎?」。美國自2006 年起逐漸發生的次級房貸(subprime mortgage)違約風暴,讓全球 哀鴻遍野,據美國銀行統計全球股市下跌市值在2008 年底高達 7.7 兆美金,也 使得以往的財富管理原則深受質疑、華爾街的金融新貴們失業率激增、以及美國 在世界的強權地位搖搖欲墜,這一切都源自2007 年起陸續爆發的不動產抵押權 相關證券的違約潮,也使得世人見識到美國華爾街金融戰的專精與不負責任,但 到底是何因素使得美國不動產影響全世界? 多數文獻與報導多將次貸風暴之原因歸咎於銀行不負責任之放款及資產證 券化之機制,然資產證券化架構自1970 年起已在美國實施近 40 年,何以在 2007 年才出現問題?且銀行應不致毫無緣由地放款給無償還能力的借款人,因此其基 本原因仍需深入探討。 綜合經濟與政治因素,可歸納出次貸發生的源頭,就是美國經濟不振下,想 藉刺激所謂的「火車頭產業」---不動產,以達振興經濟的目的。小布希前一任總 統柯林頓的運氣奇佳,其任期在1990 年代,恰逢網路科技熱潮,當時只要各國 的公司名稱掛上”網路科技公司(.com)",不論獲利與否,股價至少可連續數天升 值,當時全球產業與金融市場也陶醉在此波夢幻中,由於當時經濟成長高,卻伴 隨低通膨與低失業率,有別於以往常見之「高成長、高通膨」,故被命名為「新 經濟」(new economy),也使得柳案誹聞纏身的柯林頓輕易連任。 小布希於 2000 年上任後,網路科技泡沫隨即破滅,之後歷經 911 恐怖攻擊、 以及以「搜索毀滅性武器」為名而出兵攻打伊拉克之戰等事件,在在都是勞民傷 財的事件,尤其是後者,背後的原因「據稱」是伊拉克總統海珊為報復之前老布 希當政時的攻擊,宣稱要向伊拉克購買原油的國家需使用歐元,此舉將使得美金 需求及幣值劇跌,影響小布希連任之路,遂引起小布希的「毀滅性武器搜索」之 戰,沒想到毀滅性武器之產地就在自家的後院---華爾街,所製造出來的就是諸多 以次貸包裝的衍生性金融商品,如不動產抵押權證券(mortgage-backed security, MBS) 、 債 權 擔 保 債 券 (collateralized-debt obligation, CDO) 及 信 用 違 約 交 換 (credit-default swap, CDS)等,在不動用一兵ㄧ卒及軍火下,終究導致全球經濟的

衰退(林左裕,2009)。 在一連串浪費民膏民脂的事件過程中,貨幣政策是在刺激經濟景氣最容易發 揮的了,因為不必經國會同意,只要總統任命的聯準會主席配合即可,因此美國 利率自 2001 年的 6%降至 2003 年的 1%,目的在刺激經濟景氣,沒想到產業沒回 暖,卻造成了資產標的(含股市、不動產及相關證券)的飆漲。而 2004 連任之路在 即,小布希政府遂想出以所謂的「火車頭工業」---房地產刺激經濟,其在選前提 出「可負擔房屋計畫」(Affordable Housing Plan),美其名為提升低收入戶之購屋

能力,實為「知其不可而為之」,一方面鼓勵低所得者或收入不穩定者向銀行借

款購屋,另一方面政策性要求「二房」,即聯邦房貸協會(或稱「房利美」,Federal

National Mortgage Association, FNMA)及聯邦住屋房貸公司(或稱「房地美」,Federal Home Loan Mortgage Corporation, FHLMC),出面保證貸款,以利不動產抵押債權 包裝成 MBS 後出售,此時銀行樂得不再審慎查核房貸之申請,因為只要放款出 去就可重新包裝再出售債權,賺取創始費及服務管理費。一時之間房地產熱潮持 續不退,全球證券市場也瘋狂追求高收益率的次貸相關證券,後續的過程包括雷 曼兄弟的再次包裝證券為 CDO、信評公司(如惠譽)因二房保證而給予 CDO 高級 評等、風險移轉機制下的保險公司(如美國國際集團 AIG 等)、以及扮演再保公司 角色而購買信用違約交換(CDS)的投資者等。而在石油價格持續飆漲所導致的成 本推動型通貨膨脹後,美國聯邦準備理事會(The Federal Reserve Board)只得提高利 率以平抑物價,終究引發次貸戶的違約潮,上述的各角色都因標的源頭是「次貸」 且過度「超值」包裝而紛紛中箭落馬,且源頭標的資產不良,應用各類的衍生性 商品避險亦無濟於事!因此次貸風暴可歸納為錯誤的政策所導致的金融海嘯!

回顧美國上一次的金融風暴,也與不動產有關係,就是在 1980 年代初期的 儲貸協會(saving and loan association, S&L)危機,當時的儲貸協會存款利率受法規 限制具上限,如此可達到壓低民眾購屋貸款成本之目的,及達成協助民眾完成「美 國夢」的任務,然在全球市場化之浪潮下利率持續高漲,最高達 16%,存款戶不

儲貸協會也因不堪突如其來的擠兌而倒閉 1500 家,引發該次的金融風暴。 然何以這次美國境內的次貸金融風暴蔓延至全球,原因是證券化的機制使得 世界各國、基金或個別投資者或多或少持有 CDO 或 CDS,在失去信心下,「去槓 桿」(de-leveraging) 效應一洩如注,終於釀成世界性的金融海嘯。 在不動產榮景或低利率時期,借款人可按時繳款,房貸相關證券投資人可收 取固定之本利償還收入;若無法承擔本利償額,則以轉售房屋之收益清償房貸。 然在不動產市場景氣低迷或高利率時期所引發之房市下跌,借款人可能因就業或 收入不穩定、或債務償額因利率上漲而攀升導致無法按時還款、甚至違約,尤其 以收入不穩定的信用品質較差的借款人最容易違約,且房價的下跌也使借款人面 臨房屋市價低於貸款餘額的「負權益」(negative equity)的窘境,因此借款人的違 約之機率與利率、房價及總體經濟情況息息相關。 由圖一可看出,美國聯邦基準利率自1980年的15%,降至2003年6月的歷史最 低點1%,在資金成本大為降低、融資容易下,推動房地產市場的多頭行情,房 價在2005年創21年新高,使得十年間美國人房屋自有率由65%上升至69%,但其 中有一半的融資來源屬次級房貸。終於在2004年起石油價格暴漲,引發「成本推 動型通貨膨漲」後,聯準會連續十七度調高利率,終於使得浮動利率貸款 (adjustable-rate mortgage, ARM)的借款者(尤其是次貸戶)還款能力遽跌,引發次 貸違約風暴。

資料來源: Board of Governors of the Federal Reserve System。

0 2 4 6 8 10 12 14 16 18 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2008 年 利 率 ( % ) S&L 危機 為抑制通膨而提 高利率,引發次 貸違約風暴 網路科技泡 沫破滅,降息 以刺激經濟

圖一 美國聯邦儲備銀行利率與相關金融事件 (1977-2008 年) 三、金融資產證券化之架構與相關商品之設計 金融資產證券化的目的原為降低金融機構因放款及長期持有放款債權所引發 的利率風險、流動性風險及提前清償風險等,然其前提為包裝出售之資產標的應 為審慎查核下之優質(prime)貸款債權,美國自 1970 年代開始實施此機制後,著 實達到此機制之原規劃目的,然當此機制遭誤用時,亦可能導致更嚴重之金融風 暴。當政府一方面利用此機制鼓勵銀行放款給明顯無能力之借款人購屋以刺激經 濟,另一方面政策性要求「二房」提供保證給次貸借款人以提高銀行之放款意願 時,實已種下未來違約風暴之禍因。 而次貸亦因經「二房」之保證,使得信用評等公司給予高等級(如 AA 級)之評 等,遂使得華爾街券商有極大的設計包裝空間,由圖二可看出在「二房」的保證 及資產證券化「創造債權卻不長期持有」之特色下,金融機構得以基於管理信用 風險及追求資產流動性的考量下,積極地創造債權及移轉風險,並從中賺取貸款 創始費用(origination fee)、利差及管理費用。而券商亦因市場利率低迷、投資者 因追求高報酬而失去風險意識下,得以不動產抵押債權或甚至在外流通證券,恣 意包裝成一般投資者無相關專業能力評估之證券,如 CDO 再包(CDO squared)、 CDO 三包(CDO cubed)、以及扮演再保險公司之信用違約交換(credit default swap, CDS)等,在不動產抵押債權未來現金流量提前被放款機構及證券發行機構等提 領、甚至是次貸違約現金流量歸零之情況下,金融風暴的來臨是指日可待的。 四、台灣金融資產證券化之發展現況與規範 台灣在 2002 年通過「金融資產證券化條例」,至 2008 年已有多檔案件經金 融資產證券化機制發行,發行總金額超過新台幣 1.3 兆元,惟受次貸風暴影響, 在 2008 年僅一件核准通過,如表一所示。

表一 我國金融資產證券化案件統計 單位:新台幣億元 年度 核准件數 發行金額 發行餘額 2003 5 270 159 2004 8 422 478 2005 14 1419 1653 2006 17 4119 2829 2007 10 6170 3453 2008 1 1258 3335 合計 52 13657 資料來源:金融管理委員會,2009。

現金 CDS 發行各層 級CDO 本金與 利息 避險機制 (違約、利 率等風險) 現金購買 資產擔 保證券 (如ABS、 MBS等) 資 產 1 現金 2 有價證券 3 具未來收益之債權 或應收帳款 4 機器、設備等 5 廠房、建物與土地等 企業或銀行 之資產負債表 負 債 股東權益 債、票券等 股票、 受益憑證等 資本之證券化 資產之證券化 發 行 之 證 券 發 行 之 證 券 特 殊 目 的 信 託 或 公 司 信用增強 與 信用評等 保證或保 險 MPTB、MBB、 CMO、CDO 等 投資銀 行或發 行機構 不動產抵 押債權、 MBS、 MBB、 MPTB、 Bond、 Loan、 CDO 等 保險機構 本金與 利息 現金購買 優先順位債券 Senior Note 中級順位債券 Mezzanine Note 次級順位債券 Subordinated Note 權益層級債券 Equity Note 圖二 美國次級房貸與相關證券發行架構圖 資料來源:修改自林左裕(2007)、(2008)。 再保機構 (投資者) 如FNMA 及 FHLMC 如惠譽Fitch 如雷曼兄弟 如AIG

在「金融資產證券化條例」第四條規範中之「資產」指汽車貸款債權、房 屋貸款債權或其他動產擔保貸款債權及其擔保物權、租賃債權、信用卡債權、應 收帳款債權或其他金錢債權等,在美國發生次級房貸風暴之際,對未來國內創始 機構欲藉類似架構發行MBS、CMO 或 CDO 等不動產抵押權相關證券以提高資 產流動性或擴大融資管道的途徑,正具警示之意味。金融資產證券化之立意在提 高不動產及金融資產投資者、放款者或應收帳款持有者之流動性,並降低利率、 市場及違約等風險,但若證券化之結果免除了上述法人之風險,將相關風險「全 數」移轉至金融市場及小額投資者承擔,導致前端創始機構之「道德風險」(moral hazard)進行高風險放款或投資,結果卻影響整體金融市場之秩序,則有必要檢 討此過程中疏漏之處。 綜觀我國之「金融資產證券化條例」,規範之架構除了對商品之定義及組織 設立及計畫與業務規範外,雖有信用評等及增強、監督及罰責等,但對創始機構 規範僅限於創始機構與受託機構不得為同一關係企業(金融資產證券化條例第九 條)、提供給受託機構之資料不得有虛偽或隱匿之情事(同條例第一 0 九條);對 於特殊目的公司亦僅限於「董事應以善良管理人為特殊目的管理公司處理事務, 並負忠實義務」(同條例第六十四條)。對於信用評等機構之結果則照單全收(同 條例第一 0 二條),對其功能及職責卻無任何防止道德風險之措施;而對於創始 機構進行高風險放款進而將債權證券化而移轉風險之防範則付諸闕如(林左裕, 2008)。而在薪酬之規範上,僅在同條例第六十四條簡略規範「董事之報酬,應 以章程明定之」帶過,對於董事與經理人之報酬金額標準與相對超領報酬時可能 產生之「道德風險」則未能予以防範。 又創始金融機構在進行放款額度評估時,除了其收入及工作外評估,通常 以不動產或相關抵押品為擔保而以其估計價值之某一成數(即 loan to value ratio, LTV),此時除了應參考 LTV 成數(如最高八成)之規範外,亦未見銀行不動產 放款債權中具證照之中立不動產估價師之功能,導致銀行與存款戶間之代理問題

(principal-agent problem),也給予了放款金融機構(尤其在資金浮濫時)藉證券 化架構將不良放款售出套現的機會(林左裕,2008)。且在發行證券價格的管理 上,僅在第 75 條要求載明資產基礎證券之發行總金額,對於發行金額之合理性、 與後續市場上流通價格之持續(on-going)監管上,並無明確規範。因此創始機構的 放款查核疏失、不動產擔保標的之估價偏頗、信評機構的道德風險、相關人員的 超額薪酬、以及證券發行價格的評定及流通價格的失控等漏洞的結合,就是引發 次級房貸風暴之發生的根源,未來在規範上,即應儘量針對這些漏洞進行防弊規 範,才能有效的防止下一波類似的風暴產生。 五、我國不動產抵押放款債權現況之探討 相關美國次級房貸違約之因素與影響,多篇文獻已陸續著墨,如 Capozza & Thomson (2006)、Danis & Pennington-Cross (2005)、Kiff & Mills (2007)及 Zimmerman (2007)等。楊顯爵等(2008)亦以國內資料實證得出影響不動產抵押貸款違約之因素 為「借款人個別因素」、「契約因素」及「總體因素」,其中又以「總體因素」變 動下,最易引發違約行為。在總體因素方面,又恰逢美國自 2004 年起為了抑制 通貨膨脹而引導利率上漲,終於導致經濟成長衰退、房地產市場之下跌、以及次 級房貸借款人無力承擔因利率上漲而引發之違約潮(林左裕,2008)。 另一個影響美國不動產貸款違約的重要因素為「追索權限」之限制,在美國, 不動產貸款違約情況下,在某些州之最高追索權限只侷限於該不動產標的,並不 擴及該借款人之其他所得,因此違約的「選擇權」(default option)對美國借款人較 輕易執行,即部分借款人在低利率時期輕易購屋,著眼於房價之上漲空間;也在 後續利率上漲、房價下跌後輕易違約。相對上,台灣之不動產貸款違約後,其追 索權擴及個人所得,因此違約的「權利」在台灣通常不會輕易執行,除非到最後 關頭。兩國違約追索制度的差異也會影響借款人之違約行為,也因此可預期台灣 的不動產貸款市場違約情形不會如美國般嚴重。 由表二可看出我國貸款起始年及相對違約率,在 1997 東南亞金融風暴發生後

至 2000 年,貸款違約率相對偏高,經過數年之金融改革與逾放整理後,也適逢 總體經濟景氣在 2003 年攀升,違約率遂維持在 3%以下。 表二 我國貸款起始年與相對違約率 貸款起始年 總件數 違約件數 起始百分率(%) 違約率(%) 1996 64068 4472 9 6.98 1997 51944 3976 8 7.65 1998 50062 4220 7 8.43 1999 59758 4908 9 8.21 2000 49469 3441 7 6.96 2001 42243 1988 6 4.71 2002 50051 1333 7 2.66 2003 42152 980 6 2.32 2004 42237 924 6 2.19 2005 63222 1142 9 1.81 2006 47310 566 7 1.20 2007 74084 238 11 0.32 2008 48468 8 7 0.02

資料來源:金融聯合徵信中心(2009); Chang and Lin (2009)。

由表三我國不動產抵押貸款之貸款成數與相對違約率亦可看出,貸款成數愈 高者,其違約率愈高,尤其是超過八成者,其違約率(8.29%)即明顯高於低成數者 (2-3%)。因此未來銀行就違約的考量下,應避免高成數之放款。

表三 我國不動產抵押貸款之貸款成數與相對違約率 貸款成數LTV 總數 違約數 佔總數百分比(%) 違約率(%) 0.6 及以下 160100 3802 23 2.37 0.6-0.7 228571 6921 33 3.03 0.7-0.8 111035 2882 16 2.60 0.8-0.9 162482 13467 24 8.29 0.9 以上 22860 1124 3 4.92 註:貸款成數超過 9 成以上者包含其他擔保品。

資料來源:金融聯合徵信中心(2009); Chang and Lin (2009)。

六、對我國金融資產證券化未來規範與發展及投資者之建議 由上述引發次貸風暴因素之探討,我國可積極因應相關規範以防範未然, 以下即針對以上影響因素提出雛見以供主管機關、投資者及各界參考。 (一)抵押資產標的估價之相關問題 由於不動產抵押放款之違約率與貸款成數息息相關,而貸款成數之依據為不 動產估值,因此不動產估價之中立性及合理性對違約率、甚至後續之金融風暴有 顯著之影響。在估價技術上若只用採用「比較法」,則容易在資產價格膨脹或泡 沫時期導致「追漲」的估價結果。另一值得注意的估價制度漏洞為銀行放款時, 估價人員、估價結果及放款額度均由銀行全權決定,亦可能導致金融機構與存款 戶間之「代理問題」。由圖三可看出,當景氣繁榮時,放款寬鬆後可能導致資產 價格市價之膨脹。而在景氣無以為繼,或受生產因素(如石油等)影響而衰退時, 則可能逆轉為另一惡性循環,使價格低估。因此不動產估價的中立性與合理性, 值得與目前之相關規範進行探討。

資料來源:修改自林左裕(1999)。 圖三 金融機構之估價在不同經濟景氣時之助漲助跌效應 我國自 2000 年及 2001 年頒訂「不動產估價師法」及「不動產估價技術規則」 後,即開始實施不動產估價師制度,然銀行不動產放款之估價,則仍由銀行內聘 (in-house)之估價人員進行估價。就銀行內聘人員估價之特性而論,在有業務壓力 或上級壓力,或景氣低迷時規避風險之壓力時,易對圖四中所示之金融市場造成 「助漲助跌」之效應。而當採取房仲業之資訊估價時,雖然市場交易資訊可能較 充分,但可能在飆漲或泡沫時期高估價格;或在不景氣或金融風暴時期低估價 格。因此若能採中立估價師進行估價,可兼採市價比較法與收益還原法,所得之 估值將較為穩定。 在目前國內銀行供過於求之情況下,購置不動產之貸款申請對銀行而言, 有如銀行「標購」不動產抵押債權,條件愈優渥者(如利率愈低、貸款成數愈高、 或貸款額度愈多)即可得標,由圖四即可看出,此類「競標」即使銀行面臨「逆 選擇」(adverse selection)問題,「得標」銀行在進行高成數或高估值所致之高額度 放款後,即持續面臨借款人之違約風險,尤其是在不動產景氣走低之情況下。若 能經中立之不動產估價師依市價、未來收益性及經濟情況進行合理之估價後,應 可降低違約風險及「逆選擇」問題,以及減少只依不動產市價進行估價所導致之 誰來估價? 銀行本身? 放款 寬鬆 炒作市價 資產價 格膨脹 價格高估 銀行惡 性競爭 經濟成長 經 濟 衰 退 法拍釋出 逾放增加 資產市 價下跌 誰來估價? 市價? 房仲業? 金融緊縮 價格低估

波動風險(如圖五所示)。 資料來源:本研究整理 圖四 銀行在業務壓力下進行不動產抵押放款之「逆選擇」問題 資料來源:本研究整理 圖五 經中立估價師估價後,可降低銀行不動產抵押放款之「逆選擇」問題 不動產 抵押借 款者 銀行1 銀行3 銀行2 銀行 X 解說:放款業績競爭下(尤其景氣時),條件優渥之銀行 (如放款額高或利率低者)“得標",具「逆選擇」問題。 估價師 B 估價師 C 解說:在中立客觀之估價下,應可某一程度降低「逆選 擇」與「波動過大」之問題,提升金融市場之穩定性。 銀行3 銀行2 不動產 抵押借 款者 銀行1 估價師 A

而美國在發生次貸風暴後,為確保不動產估價之正確性(accuracy)與獨立性 (independence),即積極推動「房屋評價保護新準則」(New Home Valuation Protection Code) ,其相關規範如下: 1. 未來銀行不得使用內部人員估價(in-house appraisal),亦不得使用該行所擁有或 有關係之估價公司報告書。 2. 自 2009 年 1/1 起,「二房」只能保證與購買經「中立估價師」所估價之房貸。 3. 銀行或仲介者不得在估值上指使估價師,或給予目前或未來之業務壓力。 4. 未來放款銀行必須即時提供借款人一份估價報告書。

5. 對估價師之估價結果進行「品質管制測試」(Quality Control Test) ,以 10%之 顯著水準測試其偏離程度(如以自動估價系統或大宗資料為基準) 。

6. 設立「獨立估價保護機構」(Independent Valuation Protection Institute) 。 --- 如設立「估價申訴熱線」(appraisal complaint hotlines) ,供消費者或估價師 申訴估價過程中之不公問題。 以上「房屋評價保護新準則」規範中,如資產證券化過程中經保證之不動 產抵押債權需為中立估價師之估價結果,可降低銀行內部估價人員之業務及上層 壓力;而相對上對於估價師之估價品質進行「品質管制測試」,則可有效估價師 之道德風險。此類之規範,頗值我未來進行金融資產證券化機制及維持金融秩序 之穩定性時之有效參考,故建議我國金融管理當局可再針對銀行之不動產放款估 價問題(如估價人員之資格與權限等)進行漏洞之改革,並定期對估價師進行類 似之「品質管制測試」,以防範未來金融市場因不動產估價而導致類似的失序問 題。 (二)資產相關證券之發行及流通價格上限探討

依金融資產證券化架構所發行之商品屬固定收益證券,其價格行為類似債 券,與市場利率成反向變動,在利率低迷時期,商品價格將因折現效應而上漲, 但因折現因子最小值為 1(當利率為零時),因此其價格之上限為所有利息與面 額之和1 ,當發行價格或流通價格超過此上限時,即已觸發違約風險。根據估計 在 2006 年約有 1,000 億美元次級房貸包裝進總額 3,750 億美元的 CDO 在美國市場 銷售(許振明與陳沛柔,2007),可見次貸風暴中金融資產證券化等固定收益性 商品超值銷售所引發違約情事的嚴重性。 (三)創始銀行或投資機構經理人薪籌制度之探討 由於金融資產證券化相關證券為固定收益,雖然價格與利率呈反向變動,如 上所述,其價格上漲仍有其限制,因此創始銀行或投資機構相關人員之薪酬,即 不應無限制地成長,若其薪酬愈多,即表未來證券投資者之現金流量愈少,即愈 可能引發償還能力問題或違約風險。根據統計指出,在 2006 年間美國五家主要 投資銀行之 1300 億美元收入中,有 600 億元為薪資,有 360 億是紅利及獎金, 也由於此不符合比例之高額報酬吸引財金及數理精英投入華爾街之商品設計及 銷售中(辛喬利與孫兆東,2009),後續引發次貸風暴也不足為奇。因此關於薪 酬制度之訂定,主觀機關可適度予以規範,甚或在證券存續期間持續擁有調查權 利,以降低證券在期滿前之違約風險。 (四)貸款創始機構之風險分攤原則 在以不動產及相關(債權)資產為擔保且包裝、切割為不同風險等級之證券 售 出 時 , 管 理 當 局 得 視 情 況 要 求 創 始 機 構 、 特 殊 目 的 公 司 (special purpose corporation, SPC)、發行券商或投資銀行(investment banker)購入並持有某一比例之

1 舉例而言,當某公司發行之債券面額 1000 元,票面利率 6%,十年期,每年還息,期末還本, 則在市場利率為零時,此債券發行價格最高為1600(=60x10+1000)元,當發行價格超過此上限、 或未來流通價格超過後續付息及還本之總和時,即已觸發違約風險。

風險等級較高之證券,在違約情事發生時,可先由其先行吸收,藉此機制要求創 始機構審慎查核其放款。亦即未來依金融資產證券化所發行之證券需明確劃分等 級,且風險須由創始機構及發行機構等共同承擔,否則在道德風險無法規避之前 提下,不宜以此途徑進行證券化(林左裕,2008)。 有鑑於此,歐盟於2009 年初立法通過,未來之金融資產證券化若發生損失情 事,5%需由創始機構承擔,即著眼於承擔損失之相對責任。一般雖認為此損失 承擔之要求比率過低,但此規範已顯示出主管機關認定部分之放款審核責任應歸 屬於創始機構,對未來銀行之審慎查核責任有更強化之要求與激勵。 (五)證券「每日結算」(mark-to-market)機制所衍生的問題 每日結算機制原為降低期貨、選擇權等衍生性金融商品之違約風險所制定 的制度,然當市價在恐慌性事件或不理性因素下,可能形成資產證券化相關證券 惡性循環的跌勢,尤其在目前流通世界甚廣的「結構型商品」(structured products), 常以固定收益證券與選擇權包裝成一商品發售,又在國際型投資機構有定期公佈 淨值的壓力下,每日結算制度對證券、衍生性金融商品、金融資產證券之相關商 品價格、甚至金融市場之穩定性,有助長其波動性之影響。此波的次貸風暴即因 每日結算機制導致多數證券及基金受益憑證之市場價格明顯超跌而影響其流動 性,因此國際間亦正對此機制之副作用進行探討。 (六)金融機構及投資者宜培養高度之專業預測能力 對放款銀行及投資者而言,除了個別標的之產業及個別公司風險外,最需要 注意引發金融風暴或股市遽跌的系統風險。除了經濟成長率之預測外,對於資金 的供需,收益率曲線(yield curve)之形狀即扮演著即有效的預警指標。在正常情

形下,因長期放款比起短期放款多出了「期限風險溢酬」(liquidity risk premium),

因此收益率曲線為正斜率之曲線。然當景氣逆轉時,金融市場上短期資金之需求 將遽增,使收益率曲線之斜率轉為負斜率,此時資金需求者除了自銀行提領現金

外,亦將自證券市場出售證券以求現,故可能導致股市遽跌或銀行擠兌危機,因 此當收益率曲線由正斜率轉為零或負斜率時,可為金融市場預警之有效指標。由 圖六及圖七可看出,1978 年美國之收益率曲線仍為正斜率,在 1979 年即轉為負 斜率,之後在 1980 年即發生儲貸協會危機。而圖八及圖九中之收益率曲線自 1998 年之正斜率轉為 1999 年之零斜率,也在之後的 2000 年發生網路科技泡沫破滅事 件。在 2005 年至 2007 年之收益率曲線斜率逆轉(如圖十至十二),也有效預測 了此波次貸風暴。因此未來金融機構及投資者可長期觀察收益率曲線的走勢,以 作為全面性的股市遽跌或金融風暴的先行指標,並據以因應放款或投資決策。 美國公債殖利率(yield curve)曲線圖 6 6.57 7.58 8.5 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr 30 yr 收益率(%) 圖六 美國公債殖利率曲線圖(1978/1/3) 美國公債殖利率(yield curve)曲線圖 8 9 10 11 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr 30 yr 收益率(%) 圖七 美國公債殖利率曲線圖(1979/1/2)

美國公債殖利率(yield curve)曲線圖 5 5.5 6 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr 30 yr 收益率(%) 圖八 美國公債殖利率曲線圖(1998/1/2) 美國公債殖利率(yield curve)曲線圖 0 2 4 6 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr 30 yr 收益率(%) 圖九 美國公債殖利率曲線圖(1999/1/2) 美國公債殖利率(yield curve)曲線圖 0 2 4 6 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr 30 yr 收益率(%) 圖十 美國公債殖利率曲線圖(2005/1/3)

美國公債殖利率(yield curve)曲線圖 3.5 4 4.5 5 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr 30 yr 收益率(%) 圖十一 美國公債殖利率曲線圖(2006/1/3) 美國公債殖利率(yield curve)曲線圖 4.4 4.6 4.8 5 5.2 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr 30 yr 收益率(%) 圖十二 美國公債殖利率曲線圖(2007/1/2) 七、結論與建議 金融資產證券化之設計目的原為降低放款銀行或企業持有具收益之債權或 相關資產之風險,並提升其資產流動性,可有效降低金融機構之經營風險,並減 少政府出面擔保發生危機之金融機構的情形,然前提是將優質(prime)且違約率低 的債權售出。若因政府或民間機構為提高資產型證券之市場性或其他政策因素而 對劣質或次等(subprime)的標的提供保證,再將其出售至證券市場、甚至國際上, 則可謂「倒行逆施」,將未來違約的禍害隱藏在當前的流動性中。在各國金融資 產證券化機制逐漸發展且邁向成熟之際,強化投資者與金融市場之風險管理機制 刻不容緩,因此在各步驟中的縝密規範,將可防止未來類似風暴的發生。

本研究針對金融資產證券化過程中可能的疏漏之處提出補正之芻議,如放款 銀行宜採用中立估價師的報告,以避免過度依賴市價為依據放款而導致對市價有 助漲助跌的效應;對資產相關證券之發行及流通價格應依其現金流量設定上限, 並長期追蹤觀察;對創始銀行或投資機構經理人及資產證券化過程中之從業人 員,宜設立客觀之薪籌制度標準,以避免固定現金流量下因薪籌溢領而提升違約 的機率;基於風險分攤原則,創始機構若出售貸款,應在貸款違約時分攤一比例 之損失,以有效降低放款機構之「道德風險」。又在證券「每日結算」的機制下, 若在市場失靈時可能引發惡性循環及影響證券市場流動性,則有必要研擬一套準 則在波動程度過大時適用。除此之外,金融機構及投資者宜培養對趨勢波動的敏 銳觀察力及專業性,以在股市遽跌、甚至金融風暴來臨前及時因應,而收益率曲 線之變動可視為一有效之預警指標。只要在嚴謹的規範下,將各步驟之風險及可 能弊端機率降至最低,金融資產證券化機制仍是提供放款金融機構及企業資產流 動性之極佳途徑。

參考文獻 林左裕, (1997) ,房貸抵押債權證券化之前瞻---由美國之經驗看台灣,「台灣土地金融季刊」, 4(3): 95-109。 林左裕, (1999),從東南亞金融風暴看國內不動產市場發展趨勢及金融界因應之道,「金融財 務」,2: 67-82。 林左裕, (2000, 2003, 2007),「不動產投資管理」,台北:智勝文化事業。 林左裕, (2005),不動產抵押權證券化制度之探討及架構設計,「台灣土地金融季刊」,41(2): 25-44。 林左裕, (2006),不動產證券化估價技術之研討,國土規劃及不動產資訊中心。 林左裕,(2008),美國次級房貸風暴對台灣金融資產證券化及投資者之啟示,「住宅學報」,17(1): 111-123。 林左裕,(2009),都是房地產惹的禍嗎?「地政學訊」,國立政治大學地政系。 辛喬利、孫兆東,(2009),「次貸風暴」,台北:梅霖文化事業。 陳進安,(2007),美國次級房貸市場惡化原因及影響,兆豐國際商業銀行企劃處。 許 振 明 與 陳 沛 柔 ,(2007) , 次 級 房 貸 風 暴 於 我 國 之 省 思 , 國 家 政 策 研 究 基 金 會 , http://www.npf.org.tw/particle-3037-3.html。 廖咸興,(2002) ,推動抵押債權證券與金融機構流動性,http://mx.nthu.edu.tw/~chclin/Class。 楊顯爵、林左裕、陳宗豪,(2008),住宅抵押貸款違約之研究---影響因素之顯著性分析,「台灣 土地研究」,11(2), pp. 1-36。

Capozza, D. R. & T. A. Thomson, (2004), Subprime Transitions: Lingering or Malingering in Default?

“Journal of Real Estate Finance and Economics,” 33: 241-258.

Chang, Edward, and Che-Chun Lin, (2009), Estimation of Default Rates---The Case of Taiwan, 世紀 初金融風暴學術研討會,國立政治大學經濟系主辦,2009 年 5 月。

Danis, M. A. & T. A. Pennington-Cross, (2005), A Dynamic Look at Subprime Loan Performance, Working Paper of The Federal Reserve Bank of St. Louis.

Brauneis, M. & S. Stachowicz, (2007), Subprime Mortgage Lending: New and Evolving Risks, Regulatory Requirements, “Bank Accounting and Finance,” October and November, 28-33.

Bhingarge, N., H. Khasseria & B. Yellvalli, (2007), The Subprime Mortgage Market: Current State and the Road Ahead, “Bank Accounting and Finance,” October and November, 3-10.

Federal Home Loan Mortgage Corporation, (2007), The FHLMC Reporter Factbook. International Monetary Funds, (2007), International Financial Statistics.

Kiff, J. & P. Mills, (2007), Money for Nothing and Checks for Free: Recent Developments in U.S. Subprime Mortgage Markets, Working Paper of The International Monetary Funds.

Lin, T. C., (2007), The Development of REIT Markets and Real Estate Appraisal in Taiwan, “Journal

of Real Estate Literature,” 15(2): 281-300.

Reinhart, C. M. & K. S. Rogoff, (2007), Is the 2007 U.S. Sub-Prime Financial Crisis So Different? An International Historical Comparison, Draft.

Zimmerman, T., (2007), The Great Subprime Meltdown of 2007, “The Journal of Structured Finance,” Fall, 7-20.

2009 Joint Conference of Asian Real Estate Society (AsRES)

& American Real Estate and Urban Economics Association (AREUEA)

The Feasibility Study of the Application of

the Reverse Mortgage in Taiwan

#Tsoyu Calvin Lin∗ Hong-Chih Huang∗∗ Po-Hsiang Yang∗∗∗

Abstract

With the continuously declining fertility rates and the increasing life expectancy, Taiwan has become one of the aging societies in the world. To release the financial strain of the government, a great number of literature has suggested an alternative option, Reverse Mortgage (RM), to improve the retiring life quality of the elders. However, little attention has been given specifically to the feasibility of the application of RM and the pricing model in individual countries. This study thus conducted the questionnaire and collected the data in Taiwan for analysis in order to show the implementation feasibility of RM in aging society for both the aspects of both lenders and borrowers.

First of all, to find out the factors affecting the willingness in applying for RM and the characteristic of the middle-aged homeowners, we designed a survey and a quantitative analysis of the questionnaire through Logistic Regression Analysis.

Second, under a break-even hypothesis, we analyzed the ratio of Loan to Value (LTV) a reverse mortgage lender would offer through the simulation model. Furthermore, the housing data from different metropolises of Taiwan is integrated into the study in order to determine whether if the Income Replacement Ratio of RM (IRR-RM) could meet the basic needs of Taiwanese.

Results found in this paper suggest that RM could satisfy the general need of people in Taiwan. Procedures conducted in this study may also provide precious insight for other aging countries. This paper suggests that reverse mortgage could not only solve the society issues, but also secure the retiring lives of the elders and preserve their living qualities.

Keywords: Reverse Mortgage, Logistic Regression, Simulation Analysis, Loan to Value, Income Replacement Ratio (IRR)

# The authors are grateful to the sponsorship from the National Science Foundation of Taiwan. ∗

Corresponding author, Department of Land Economics, National Cheng-Chi University, Taiwan. Email: [email protected]. Tel: + 886-2-29393091ext. 51142.

∗∗

Department of Risk Management and Insurance, National Cheng-Chi University, Taiwan. Email: [email protected].

∗∗∗

Department of Land Economics, National Cheng-Chi University, Taiwan. Email: [email protected].

1. Introduction

According to the Social Indicator announced by the Ministry of Interior in 2007, Taiwan is one of the rapidly aging societies1 in the world due to the continuously declining fertility rate and the increasing life expectancy. As shown in Figure 1, the percentage of population for ages younger than 15 will decrease from 18% to 8%, and the elders of over 65 will rapidly increase from 10% to 35% in coming forty years. Besides, the aging index2 has gone up to 58% in 2007, which is 1.5 times than the global average. Moreover, it is expected to increase dramatically to 182% in 2029, the next coming two decades; and the old-age dependency ratio3 will increase up to 35%. It implies that every three adults at least should take care of one elder; the aging society would become a serious problem in the near future.

*Figures after year 2009 are projected. 0 10 20 30 40 50 60 70 80 1992 1994 1996 1998 2000 2002 2004 2006 2008 2014 2020 2026 2032 2038 2044 2049 Years %

Ages 0-14 Ages 15-64 Ages 65 and over

Figure 1

Percentage of population by ages in Taiwan

The serious aging population has been attracting considerable attention from the government. In October 2008, Taiwan government enforced the “National Annuity” system by building the “National Annuity Law.” According to the National Annuity Law, people in Taiwan who participate in the pension insurance program and pay the insurance monthly could obtain a life annuity when they reach 65 years old. The amount of the annuity they can get depends on how long they participate in the program.

Although the pension insurance system is in a way expected to cope with the aging problem, high dependency ratio will still drag down the government’s financial system and the economic development of Taiwan (Jung, 2007). Fortunately, more and more financial innovative products have been developed to assist the elders by planning their

1

In Taiwan, the people aged 65 and older account for 7% of the general population in 1993, which is the criterion of an aging society. In 2006, it was 10% in Taiwan, compared with other country in Asia, Japan is 20%, Hong Kong is 12%, Korean is 10%, and China is 8% in 2006.

2

According to the definition of the indicators of aging population from the U.N., the aging index is calculated as the number of persons 60 years old or above per hundred persons under aged 15. 3

income after retirement, such as Life Annuities, Long-term Care Benefits, Longevity Insurance and Reverse Mortgage (RM). However, in the case of RM, it could be the most feasible scenario due to it has long been developed in Europe and the United States (Mitchell, Piggott, Sherris & Yow, 2006). Reverse mortgage is a mortgage to help the elders convert their home equity into cash. They can receive a payment by using their house as collateral. And as long as they stay alive, they do not need to repay the mortgage and can still withhold ownership and residence of the house. This approach is somewhat like a home-based annuity (Cocheo, 1993).

On the basis of the Life-cycle Hypothesis, people will use their life-time accumulated assets during their retirement years (Ando & Modigliani, 1963; Artle & Varaiya, 1978; Shefrin & Thaler, 1988). That could be the reason why the elders will finance their residence even though the financial planners have recommended that mortgages should be paid off after they retired so that they will have more funds available for other expenses and reduce the risk of not being able to afford the mortgage payments. (Karen, Melinda & Doseong, 2006; Michael, 1999), or choose to draw down their home into smaller ones or with less value (Amanda, 2007; VanderHart, 1994).

The following evidence also demonstrated the feasibility of the application of RM in Taiwan. For the elders in Taiwan, there is a tendency of their major source of the income—coming from themselves or their children—to decrease, yet the income source from the government has a reverse trend (Ministry of Interior, 2005). Besides, among the households by tenure of dwelling, the self-homeownership ratio for people aged more than 65 has reached the standard of 80% (Statistical Bureau, 2006). It shows that the Chinese traditional value, the concept of “raising children to prepare for getting old”, has gradually become outmoded. Nevertheless, considering that the income source from the government and oneself take on a large proportion and with the high self-homeownership ratio, it can be pointed out that more and more elders do not have enough income to cover their daily expense, yet they own expensive houses. In other words, they may become “living poor but dying rich” people.

Therefore, the current study suggests that reverse mortgage can be an alternative financial option for elderly people who own the home equity but limited income. Homeowners in retired life are able to consume their home equity through RM with no need to move out. Meanwhile, RM could be a way to pay for services and support seniors “aging in place” (Redfoot, 1993; Stucki, 2005).

As mentioned above, in more recent years, we have seen mounting evidence of the feasibility of the application of the reverse mortgage in aging countries. Although many researchers also consider RM as a way to enhance the economic security preparation for elders, few attempts have been made to discuss the feasibility of RM in these countries from both the RM borrowers’ and the RM lenders’ consideration. That is, for the research in the feasibility of the reverse mortgage in aging societies, little attention has been given to both the aspect of the supply and the demand.

Hence, this study aims to offer a complete analysis by considering both these two aspects. From the viewpoints of borrowers, this study attempts to find out the positive and negative factors which affect the intention of the middle-aged homeowners and see the basic need of RM for people in Taiwan if it is available in the future.

On the aspect of the lenders, this study tends to compute the Loan to Value (LTV) through the simulation analysis to explore how much the disbursement that RM lender

could offer. Furthermore, the study examines the Income Replacement Ratio (IRR-RM 4)

by comparing the pre-retirement earning and the income from RM. And then we discuss whether the application of RM could meet the basic need for the people in Taiwan or not.

2. The Concept of the Reverse Mortgages

Reverse Mortgage is a mortgage which allows older homeowners (aged 62 or older in the U.S.) to convert their lifetime home equity savings into cash. It is aptly named because the payment stream is “reversed.” Instead of making monthly payments to a lender, as in a regular mortgage, the borrower receives payment from lenders against the value of their property. Under the concept of payment pattern, the RM is basically designed to enable elderly homeowners to unlock non-liquid assets tied up to their housing equity in order to generate income (Ong, 2008). Because the elderly person is conventionally classified on the economic circumstance as “asset-rich but income-poor” group (Hancock, 1998; Rowlingson, 2006), the RM can be an alternative option for those elderly homeowners to enhance the liquidity of their poverty and improve their current consumption.

Figure 1 shows the relationship between home equity and RM throughout the life span. In stage 1, the debtor may apply for a mortgage from the bank in order to purchase a house. Then, with the accumulating repayment for the loan balance, the home equity increases over the time. Then after the debtors pay off the mortgages, they finally own the house without any debt (stage 2). But this is often achieved while the debtors reach middle age or in the latter years of their working life. If they do not have retirement plans or income sources, then it will become a serious challenge for them to face their life after retirement. Under this condition, they only own their houses earned during their life time but lack any other source of income. This dilemma may lead hem to make the difficult decision to sell their house and move to another place or reduce the daily expenses dramatically; otherwise, they can only rely on the government’s support. 4 Earning retirement -Pre RM from receipt Income RM of Ratio t Replacemen Income =

Figure 2

The Relationship between Home Equity and Reverse Mortgage throughout the Life Span

Therefore, to provide a more dignified life for the elders and increase the liquidity of real estate, the RM can serve as a feasible option for them to enhance the retirees’ life quality. As the homeowners apply for the RM, the home equity will decrease and the mortgage balance will increase as they receive the annuity from the creditor (stage 3). The amount of money they can receive depends on the borrower’s age, the current interest rate, and the appraised housing value. Generally, the more valuable the house is, the lower is the interest; and the older borrower is, the more mortgage amount the borrower can acquire (HUD, 2006).

Overall, during the payment from the creditor in the RM, the debtors receives the money without repayment of interest or principal. All of them will be contained in the mortgage balance. As long as the debtors stay alive and are still living in the house, there won’t be mortgage repayment even though the mortgage balance exceeds the house value. The repayment can only be made until the homeowners’ demise or vacating their houses (Reed & Gibler, 2003).

3. Research Method

A two-phase study was designed to explore the feasibility of RM in aging societies from both supply and demand aspect. In the aspect of the borrowers, the study conducted a survey. A questionnaire was designed for the middle-aged homeowners in Taiwan regarding their opinions and attitudes towards the feasibility of RM. The definition of the middle-aged homeowners was further designated to be those from the range 30-60 years of age in 2008. The questionnaires are conducted through the Binary Logistic Regression Model to explore the respondents’ willingness to apply for RM and relative factors.

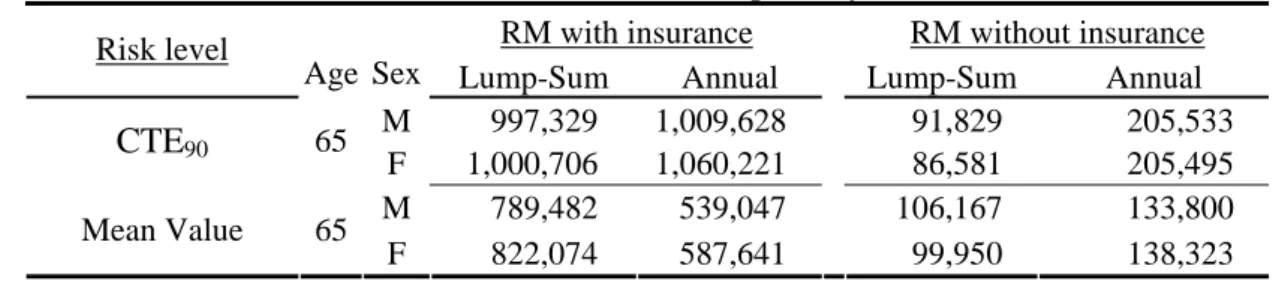

As for the lenders’ concerns, a simulation model and a RM pricing model are established in this study to indicate how much the disbursement the RM lenders could offer. Under the break-even hypothesis, the disbursement is determined by computing the LTV in RM. So, the study attempts to compute how much the LTV the RM lenders could offer with different RM payment programs. Furthermore, this study examines whether if the IRR-RM in RM could meet the basic needs for the elders in Taiwan.

(1) Method 1: Logistic Regression Model

This study assumes that the middle-aged homeowners are the likely targets for the introduction of RM and could be the most eligible beneficiaries if RM is available in the coming decades. Accordingly, the participants of this research were middle-aged homeowners, selected from a stratified random sample of middle-aged homeowners in Taiwan. Among the 1,100 Taiwan middle-aged adults, 478 (43%) completed all phases of the survey, among which 70 (6.4%) cases were discarded due to the missing values. Therefore, the valid sample of the study is 396 respondents (α =95%,

d=4.92%).

Data collection took one month (08/07/2008-09/07/2008). Data were collected through interview (27.3%), mail (27.3%), and e-mail (45.5%). The respondents were asked to fill out a questionnaire consisting of 23 items, which were divided into five main parts as follows:

Current circumstance of house

The respondents were asked to fill in the house age, the house value, how many houses they own, and whether if they rent their house.

Financial situation

The respondents were asked to answer about their financial status including asset holding, income, employment, and wealth.

Career planning

Two questions were designed to search for the planning for the respondents after retiring and the attitude toward inheritance.

Willingness

Respondents were asked for the intention of applying for reverse mortgages.

The demographic characteristics such as gender, age, address, marital status, career, number of children, and education level were asked in this section.

(2) Model Design

According to Gujarati, D. N. (2003), the probability density function of the binary logistic regression model could be written as follows:

( )

[

[

(

{

(

)

)

]

}

]

τ μ τ μ / exp 1 / exp − + − = z c z z f , −∞<z<∞ (1)The cumulative distribution function (CDF) is

(

)

[

]

(

)

[

]

∫

−∞ + − − = = x x x dz z f P τ μ τ μ / exp 1 / exp ) ( (2)Replacing the following items, β0 =−μ/τ and β0 =1/τ . The CDF is then

[

]

[

x]

x P 1 0 1 0 exp 1 exp β β β β + + + ≡ (3) The logistic regression model takes the following form:) ( ) ( ) ( 1 1 1 ) ( f x x f x f i i i e e e P Y E + = + = = = − π (4) ik k i i f x X X X Z = ( )=α +β1 1+β2 21+...+β (5) i

P is the probability of the willingness to apply for reverse mortgage from (4); and

(

1−Pi)

is the probability of unwillingness to apply for reverse mortgage , ori i ik k i i X X Z Z X i i i e e e P Y E + = + − = + − = − = − = − − + + + + − 1 1 1 1 1 1 1 1 1 ) ( 1 1 ( ... ) 2 2 1 1 β β β α π (6)

Therefore, the odds ratio was:

) ... ( 1 1 2 2 1 1 1 ) ( 1 ) ( i i i k ik i i X X X Z Z Z i i i i e e e e P P x x α β β β π π + + + + − = = + + = − = ⎟⎟ ⎠ ⎞ ⎜⎜ ⎝ ⎛ − (7)

Taking the natural log of (7), we can obtain the following Logistic Equation L , i

ik k i i i i i i i i X X X P P x x Z L α β β β π π + + + + = ⎟⎟ ⎠ ⎞ ⎜⎜ ⎝ ⎛ − = ⎟⎟ ⎠ ⎞ ⎜⎜ ⎝ ⎛ − = = ... 1 ln ) ( 1 ) ( ln 1 1 2 2 (8) Definition of Variables

The variables in the logistic regression model are described below. First, the dependence variable in the study is set as binary. In the questionnaire, respondents were asked whether or not they want to apply for RM. This study notes the answer “no” as “0” and “yes” as “1.”

As shown in Table 1, this study developed 18 independence variables and divided them into four groups:

Panel A: Demographic Variables

Demographic Variables included three continuous variables (age, education level, and number of children) and three dummy variables (gender, career, and marital status).

Panel B: Real Estate Variables

Housing age, value and location of house, leasing house or not, having second house or not were obtained in this panel. The value of the house was estimated by means of 6-point scale. Moreover, the locations of the houses were classified into four categories of areas.

Panel C: Asset and Income Variables

Three dummy variables were formed in this panel: the financial assets were measured by asking respondents the major type of their asset (excluding the home equity). This study divides the major asset type into two parts and assumes people holding the stocks, bonds or funds as their major property are more risk-taking than people holding the cash, deposit, or gold. Furthermore, if respondents have income (whether the income came from full-time job, part-time job, or retirement pension), they are classified into employment level; denoted as “1”. One continuous variable was the income, indicating the average household income per month.

Panel D: Subjective Perception Variables

Wealth variable was rated on a 5-point scale ranging from 1=poor to 5=wealthy. Two dummy variables were used for bequests and if they live alone, which indicated the respondent’s subjective perception for bequest and retirement plan.

Table 1

The Description of Variables

Variables Description Willingness p-value

Panel A: Demographic Variables

Age Age in years 0.068

Gender Gender 0.418

female =0 (40.4%) 31.3%

male =1 (59.6%) 35.2%

Marital Marital status 0.445

Married =0 (81.1%) 32.7%

Single =1 (18.9%) 37.3%

Education Educational level 0.115

Career Career type 0.112

no career or retired =0 (8.3%) 21.2% primary Industry =1 (1.0%) 0.0% secondary industry =2 (7.3%) 44.8% tertiary industry =3 (83.3%) 34.2%

Childnu Number of Children 0.529

Panel B: Real Estate Variables

no =0 (70.5%) 32.6%

yes =1 (29.5%) 35.9%

Hage Housing age in year 0.919

Hvalue Value of house (NT$) 0.931

less than 4,000 thousand =2,000,000 (16.7%) 30.3% 4,001-8,000 thousand =6,000,000 (40.9%) 34.6% 8,001-12,000 thousand =10,000,000 (23.0%) 35.2% 12,001-16,000 thousand =14,000,000 (10.6%) 28.6% 16,001-2,000 thousand =18,000,000 (3.8%) 33.3% more than 2,001 thousand =22,000,000 (5.1%) 40.0%

Letting Letting their house 0.696

no =0 (75.5%) 34.1%

yes =1 (24.5%) 32.0%

Location House location 0.610

north area =1 (88.4%) 33.7%

central area =2 (2.5%) 20.0%

south area =3 (7.1%) 32.1%

east area =4 (2.0%) 50.0%

Panel C: Asset and Income Variables

Employment Having income 0.273

no =0 (2.8%) 34.0%

yes =1 (97.2%) 18.2%

Income Average Domestic Income

per month (NT$) 0.321

less than 37 thousand =26,000 (7.1%) 25.0% 37-56 thousand =36,000 (13.6%) 33.3% 57-76 thousand =66,000 (17.7%) 25.7% 77-10.6 thousand =89,000 (24.7%) 39.8% more than 10.7 =136,000 (36.9%) 34.9%

Asset Major asset type 0.024

cash/deposit/gold =0 (54.5%) 28.7% stock/bond/fund =1 (45.5%) 39.4%

Insurance Have insurance 0.026

no =0 (35.4%) 26.4%

yes =1 (64.6%) 37.5%

Panel D: Subjective Perception Variables

Wealth 5-point scale ranging from

1=poor to 5 = wealthy 0.385

Bequest People have to take house as

a bequest 0.022

not agree =0 (41.7%) 40.00%

agree =1 (58.3%) 29.00%

Livealone Want to live without children

after retirement 0.022

no =0 (37.1%) 26.53%

(3) Method 2: The Pricing Model of Reverse Mortgage Assumption

Un-Independence of Housing Value and Interest Rate

The most important risks for lender providing the reverse mortgage are the house value risk and the interest risk. To estimate the extent that the LTV lenders could offer in the RM, it is critical to realize the fluctuation of the house value and the interest rate. This study simulated these two risks according to the following assumptions: (1) the housing return follows geometric Brownian motion process; and (2) the risk-free interest rate follows the Cox-Ingersoll-Ross (CIR) model5. However, we argue that the asset price, particularly in property, is characterized by abrupt and unanticipated large changes known as “jumps” because of the shocks such as deregulated plot ratio, key zones for development, redevelopment of old region, and some restrictive or encouraging policy. Furthermore, the financial crisis will drag down the housing price. Accordingly, this study presents the housing geometric Brownian motion process with a mean revering jump-diffusion processes, which is a generalization of the standard Merton (1976) model6.

Moreover, we noticed that the fluctuation of the house value and the interest rate are not independent in reality. Therefore we assume that the motion process of the housing value and the interest rate are correlated with one another. This study estimates the correlation coefficient between the housing value and the loan rate. According to the assumption above, the housing value and the interest rate simulation model are defined as follows:

)

,

(

~

ln

)

(

~

)

(

)

1

(

)

(

))

(

),

(

(

)

)

(

(

)

(

)

)

(

(

)

(

)

(

)

(

)

(

))

(

(

)

(

2 ) ( 1 Y N i H t N i i rH H r H H H H r rN

Y

t

P

t

N

Y

t

J

dt

t

dZ

t

dZ

Cov

t

t

J

d

t

dZ

dt

t

r

t

H

t

dH

t

dZ

t

r

dt

t

r

k

t

dr

σ

θ

λ

ρ

β

λ

σ

δ

σ

θ

∑

=−

=

=

⎪

⎩

⎪

⎨

⎧

−

+

+

−

=

+

−

=

(9) Where = ) (tdr the differentials of interest rate at some future time t following CIR model; =

k the mean-reverting intensity of interest rate;

5

We developed the model presented by Shreve (2004), “Stochastic Calculus for Finance 2, Continuous-time models,” p. 468-470.

6

=

θ the long-term mean-reverting level of the interest rate;

=

dt the differentials of time;

= r

σ the volatility of risk-free rate;

=

dZ the Wiener process with the normal distribution with a mean of 0 and a standard deviation of 1;

=

dH the differentials of house value;

= H

δ the regular expenditure rate of housing;

= H

σ the volatility of house value;

= rH

ρ Correlation coefficient of house value and interest rate;

=

− )

) (

(J t t

d λHβ the jump process, where the J(t) is the jump with Poisson

distribution; =

i

Y the jump with log-normal distribution: lnYi ~ N(θN,σY2) =

H

λ the jump frequency, which is the average number of jumps per year;

= Y

σ jump volatility, which is the standard deviation of the proportional jump.

Independence of Loan Terminations

After modeling the fluctuation of the house value and interest rate, the study supposes that the RM loan only terminates when the borrowers decease. That is, the loan termination in this study is only determined by the demise of borrowers, which is independent from the fluctuation of the interest rate and the housing price. The RM mortgage will not default during the loan term.

This study adopts the mortality of borrowers from the Taiwan Standard Ordinary Experience Mortality (2002 TSO). Once the loan terminated, this study assumes that the lenders will sell the house to repay the mortgage debt.

Break-even Program

This study suggests that the RM pricing model is conducted under the break-even program. The present value of the expected losses of the RMs should to be less than or equal to the present value of the expected premium of RMs. If the RM is under the insurance program, it is not a mutual program. The expect value of the mortgage insurance premium should be able to cover the expected losses. If the lenders provide the RM without the insurance program, they should charge the risk premium rate on the loan to incorporate the possible losses in RM.

(4) Model Design

This study derives the RM pricing model to determine the loan-to-value ratio in the RM under the break-even hypothesis based on Szymanoskis’ (1994) HECM model. However, the HECM model assumes the RM is under the mortgage insurance program by Fannie Mae and Freddie Mac in the U.S. For the RM provider, the fundamental condition is that the present value of the expected losses on a pool of RMs equals the