國 立 交 通 大 學

財 務 金 融 研 究 所

碩 士 論 文

實質選擇權賽局與策略投資:

筆記型電腦 OEM/ODM 產業之應用

Strategic Investment as a Real Options Game:

An Application to Laptop OEM/ODM Industry

研 究 生:黃家維

指導教授:黃星華 博士

實質選擇權賽局與策略投資:

筆記型電腦 OEM/ODM 產業之應用

Strategic Investment as a Real Options Game:

An Application to Laptop OEM/ODM Industry

研 究 生:黃家維

Student: Huang, Chia-Wei

指導教授:黃星華 博士

Advisor: Dr. Huang, Hsing-Hua

國 立 交 通 大 學

財 務 金 融 研 究 所

碩 士 論 文

A Thesis

Submitted to Graduate Institute of Finance

College of Management

National Chiao Tung University

in partial Fulfillment of the Requirements

for the Degree of

Master of Science in Finance

July 2007

Hsinchu, Taiwan, Republic of China

實質選擇權賽局與策略投資:

筆記型電腦 OEM/ODM 產業之應用

研 究 生:黃家維

指導教授:黃星華 博士

國立交通大學財務金融研究所

2009 年 6 月

摘要

本篇研究建構於 Smit 與 Trigeorgis (2004) 之模型架構上,於雙占市場及 價格競爭產業基礎下,以實質選擇權賽局法分析全球筆記型電腦代工產業龍頭— 廣達電腦投資新型觸控式螢幕之筆記型電腦專案之可行性與價值。分析過程中不 僅將市場景氣變動因素納入考量,亦考慮廣達之競爭對手,包含仁寶電腦、緯創 資通及英業達之反應與決策。根據本研究結果顯示,投資該專案為廣達最適之決 策。當市場需求越大及市場不確定性越高時,廣達應加快投資速度,因為投資該 專案所產生之價值也會越高。 關鍵字:實質選擇權賽局、實質選擇權、賽局、筆記型電腦代工Strategic Investment as a Real Options Game:

An Application to Laptop OEM/ODM Industry

Student: Huang, Chia-Wei

Advisor: Dr. Huang, Hsing-Hua

Graduate Institute of Finance

National Chiao Tung University

June 2009

Abstract

This thesis follows the model of Smit and Trigeorgis (2004). Under the conditions of the price competition and the duopoly model, this thesis evaluates the feasibility and the value of the multi-touch panel laptop project for Quanta, the leader company of the laptop OEM/ODM industry, through the real options game methodology. This methodology not only considers the market uncertainty but deliberates Quanta’s competitors’ reactions including Compal Electronics, Inc., Wistron Corporation, and Inventec Corporation. The result demonstrates that investing in the project is the optimal decision for Quanta. Due to the high value of the real options of the project, Quanta should make this investment promptly when the market demand and market uncertainty are high.

Keywords: Real Options Game; Real Options; Game Theory; Laptop OEM/ODM Industry

誌 謝

「寫論文的過程只是一種訓練,重點在於獨立思考與解決問題的能力。你所 得到的,也是別人拿不走的!」恩師當時的ㄧ句話,現在聽來更加覺得深刻。最 感謝是我的恩師—黃星華博士。感激恩師在課業上細心的指導與叮嚀,感激恩師 在課餘外陪伴我打羽球紓解壓力,更感激恩師於我在上海交換學生期間給予之關 心以及回台後於我未來人生藍圖的建議。同時,感謝口試委員張興華老師、林信 助老師及李漢星老師對本篇論文所提供之諸多寶貴意見,使本篇論文更趨完善。 再者要感謝交大財金所嚴謹治學的諸位老師。首先是對我最照顧的謝鍾惠民 教授,感謝老師在所長任內對我的提攜與鼓勵。即使忙碌至極,也不曾忘記對於 我的關心;感謝本所王克陸老師、王淑芬老師、戴天時老師、李漢星老師以及應 數系吳慶堂老師,謝謝老師豐富了我的財金知識,更影響了我的人生;感謝語言 中心的吳思葦老師及秦毓婷老師,謝謝老師不嫌棄我的英語寫作能力,不斷地給 予鼓勵並耐心的指導,使自己的英語能力有些許的進步;感謝財金所辦公室的謝 佳芸小姐與沈稚螢小姐,謝謝於任職班代表期間給予所需的ㄧ切幫助。 我還要感謝親愛的家人。謝謝最疼愛我的父母親、兄嫂以及女友曉茹。正因 為你們無盡的關懷與無限的支持,我才有動力走到今天。 最後要感謝財金所九六級的同學們。雖然只有兩年短暫相處的時間,但一同 經歷了招說會、迎新、送舊以及各種大小比賽。我們一起瘋狂玩樂、一起熬夜唸 書、一起埋頭寫論文,這一切都將會是我碩班時期最美麗的回憶。謝謝星星幫的 景璁、璝志、嵐鈞、茹雲、昱聰與我一起走過研究的道路;謝謝ㄧ同住在復國社 區裡的俊文與博宇陪伴我度過寫論文的每一個夜晚;謝謝住在研二舍的祥霈、紜 齊及經銓與我一同上健身房運動紓解壓力的日子。 因為有你們,才讓我得以順利完成學業。願能與大家分享我內心之感激與喜 悅,家維在此致上最深的謝意。 黃家維 謹誌 中華民國九十八年六月Contents

Chinese Abstract ……..……….…….…….………....I

English Abstract ..……..……….…….…….………....II

Acknowledgements ..……….…….….….…...………....III

Section 1 Introduction ……….……..…….………....1

1.1 Background and Motivation ….………...………1

1.2 Purpose of the Thesis ……….…...……….…..….………...3

1.3 Research Area ………..………..…………...………...4

1.4 Procedure and Structure of the Thesis ………...…………..5

Section 2 Literature Reviews ……….…………8

2.1 Traditional Investment Methodologies ………8

2.2 Real Options ……….………...………8

2.3 Game Theory ………....………..11

2.4 Options Game ………...…….………....11

Section 3 Model Construction ………...17

3.1 Methodology ……….…..….…………...17

3.2 Model Assumptions and Constraints ………….…….…………..…….18

3.3 Decision Tree ……….………...……….18

3.4 Price Competition Model ………...…….………….……...…...22

Section 4 Case Study ……….………..30

4.1 Price Competition Industry ………...………..…..…...…………..30

4.2 Case Study ...……….………...……….……....… 31

4.3 Scenario Analyses ………..………...…….…...………….35

Section 5 Conclusions ………...…...……...……….47

Lists of Tables

TABLE 1.1: Main Differences between OEM and ODM ………...….6

TABLE 1.2: Global Market Shares and Main Clients of the Five Companies ….……..6

TABLE 2.1: Merits and Drawbacks of Six Traditional Investment Methodologies ...13

TABLE 2.2: Definitions of Important Variables between Real Options and Financial Options ………..……...………...14

TABLE 2.3: Common Corporate Real Options ………..…..15

TABLE 2.4: Successive Stages of Analysis for Real Options Game ……..……...…..16

TABLE 3.1: Definitions of the Symbols ………..…………...27

TABLE 3.2: Equilibrium Prices for Different Market Structures under Reciprocating Price Competition in Each Stage ………...………...28

TABLE 4.1: R&D Expenses of Quanta and PixArt for Touch Panel Laptops ...……39

TABLE 4.2: Estimated Quantity of Touch Panel Laptops in 2011 …………..…...…..39

TABLE 4.3: Comparison between Option Value with Game and Option Value without Game………44

TABLE 4.4: Reduced Form of the Time Period...……….……44

TABLE 4.5: Scenario Analysis of Theta of Quanta………...…………..…...…..44

TABLE 4.6: Scenario Analysis of Volatility……….…...…..……45

TABLE 4.7: Scenario Analysis of the Changes of Risk-free Rate.………...45

TABLE 4.8: Scenario Analysis of the Increment Changes of Up Moves…...…...……46

Lists of Chart and Figures

CHART 1.1: Market Shares of the Top Ten Laptop Companies ……...…….…………..7

FIGURE 1.1: Procedure of the Thesis ………....……….7 FIGURE 3.1: Illustration of the Decision Tree (Investing in the First Period) ….…….25

FIGURE 3.2: Illustration of the Decision Tree (Deferring in the First Period) …….…26

FIGURE 3.3: Illustration of the Possible Stock Prices with Two Periods ….….………29

FIGURE 3.4: Illustration of the Call Value ……….………...29

FIGURE 4.1: Outcome of the Up Moves of the Market in 2011 ……….………..40

FIGURE 4.2: Outcome of the Simultaneous Game with the Extensive and Normal Form in 2011 ……….………...40

FIGURE 4.3: Route of Decision Tree (Investing) ……….41 FIGURE 4.4: Route of Decision Tree (Deferring; up moves) …….……….…………..42

Section 1 Introduction

1.1 Background and Motivation

Eee PC, which is provided by ASUSTeK Computer Inc., was the best Christmas

present of electronic products division on Amazon.com in 2007. The features of this

small laptop, called “netbook” by Intel, are light, handy, and cheaper. In addition,

another netbook, called Aspire One, provided by Acer Inc. has become popular. Many

people know that both ASUS and Acer are Taiwanese companies; however, few

people know that more than 90 percent of laptops (also known as notebooks) around

the world are made by Taiwanese companies nowadays.

According to the statistics of Market Intelligence & Consulting Institute (MIC),

90 percent or more laptops worldwide are produced by Taiwanese laptop ODM/OEM

firms. Besides, more than 99 percent netbooks are manufactured by these firms as

well.

Tang (1999) defined that the original equipment manufacturer, or OEM, is

usually a company which uses components or parts made up by other firms in its

products, or sells an entire products of other firms under its own brand. Moreover, he

also defined that an original design manufacturer (ODM) is a company which designs

and manufactures a product which will be branded and sold by another brand firm.

TABLE 1.1 illustrates the main difference between OEM and ODM. In OEM

agreements, the OEM company focuses on fabrication and production, and the brand

company concentrates on sales and services. Moreover, most decision rights are

controlled by the brand company. Conversely, the ODM company has to design and

manufacture products, and the brand company focuses on sales and services as well.

Besides, the ODM company and the brand company usually decide and discuss

details of products together in ODM agreements.

There are five leading laptop OEM/ODM manufacturers in Taiwan. They are

Quanta Computer Inc., Compal Electronics, Inc., Wistron Corporation, Inventec

Corporation, and Pegatron Corporation. Their orders come from world famous

computer corporations, such as HP, Dell, Toshiba, SONY, Apple, etc.

(TABLE 1.2 is about here)

TABLE 1.2 shows the global market shares of the five laptop OEM/ODM

companies in 2007. Quanta and Compal own more than 50 percent of market shares

worldwide. CHART 1.1 exhibits the market shares of the top ten laptop companies,

called brand firms. They are also the critical clients for the laptop OEM/ODM

companies. Note that the market shares of the top five brand companies are more than

50 percent of the whole industry.

Quanta Research Institute, which has been training engineers to develop future

products, has invented a new laptop with touch panel responded by CMOS1. It is called “multi-touch panel laptop” by some analysts.

Besides, due to the low acceptability of Windows Vista, Microsoft is expected

to launch a brand-new operating system, called Windows 7, in the end of the third

quarter this year. The most attractive feature of Windows 7 is that it supports the

multi-touch panel function, making a keyboard and mouse assistant tools rather than

essential tools.

Because of high market shares between Quanta and other firms, this thesis is

going to look into the competitive relationship between Quanta, the leader company

of the industry, and three other companies and the value of investing in the new

multi-touch panel project. Note that Pegatron Corporation is excluded from this study

because Pegatron Corporation is not a listed company, and it is difficult to obtain the

financial statements of the company.

1.2 Purpose of the Thesis

This study aims at the four main laptop OEM/ODM firms in Taiwan. They are Quanta

Computer Inc., Compal Electronics, Inc., Wistron Corporation, and Inventec

Corporation.

Based on the industrial classification of Ministry of Economic Affair, a laptop,

which is designed for portable use and small enough to sit on one’s lap, includes a

keyboard, a display and other devices. The size is similar to an A4 paper, and the

weight is approximately to 3 kilograms.

Due to the background and motivation, this thesis is going to analyze:

1. the status of the laptop OEM/ODM industry,

2. the competitive relation between Quanta and other firms, and

3. whether Quanta should invest in the multi-touch panel laptop project by using the

options game methodology.

1.3 Research Area

1.3.1 Length of Time

Time horizon of the decision tree starts in 2008 and ends in 2011. On average, many

statistics show that most new electronic products’ life cycle are less than four years so

the lengths of time are decided. In addition, each period represents one year.

1.3.2 Source of the data

The data of this study was obtained by the financial reports of the four firms. The time

period of the data starts in the third quarter of 2002 and ends in the fourth quarter of

2008. The demand function of this research follows the Bertrand duopoly price

1.4 Procedure and Structure of the Thesis

The procedure is classified into five parts. Section one introduces the status of the

laptop OEM/ODM firms and industry. Section two reviews the related literature.

Section three derives the decision tree and the critical model. Section four calculates

the investing value of the multi-touch panel project through the options game

methodology; in addition, scenario analysis is used to evaluate the value of real

options given different conditions. Finally, Section five makes a conclusion. FIGURE

1.1 exhibits the procedure of this thesis.

TABLE 1.1

Main Differences between OEM and ODM

Main Differences OEM ODM

Works The OEM firm fabricates and produces products

The brand company focuses on sales and services; the ODM firm has to design and manufacture products Underlying Goods

of Contracts

Components, semi-finished

products, and finished products Finished products or services Contents

of Contracts The brand company decides

The brand company and the ODM firm decide each other Profits Allocation The brand company decides The brand company and the

ODM firm discuss each other Source: Chen (1996)

TABLE 1.2

Global Market Shares and Main Clients of the Five Companies

Company Market Share Main Clients

Quanta Computer Inc. 32.72 % HP, Acer, Dell, Apple, and Lenovo Compal Electronics, Inc. 23.26 % HP, Acer, Dell, Toshiba, and Lenovo

Wistron Corporation 12.42 %

HP, Acer, Dell, Lenovo, and Fujitsu -Simens

Inventec Corporation 9.36 %

HP, Acer, Toshiba, and Fujitsu -Simens

Pegatron Corporation 7.71 % Asus, Dell, and Toshiba Others’ Corporations 14.53 %

Total 100 %

CHART 1.1

Market Shares of the Top Ten Laptop Companies

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% market shares 20.10% 15.90% 14.00% 8.60% 8.20% 4.90% 4.80% 4.70% 4.10% 16.80%

HP Acer Dell Toshiba Lenovo Fujitsu Sony Asus Apple Other

Source: DisplaySearch (March, 2008)

FIGURE 1.1 Procedure of the Thesis

Introduction

Literature Reviews

Decision Tree Model

Evaluation & Scenario Analyses

Section 2 Literature Reviews

2.1 Traditional Investment Methodologies

There are six traditional investment methodologies that we often use. These six

methodologies are net present value method (NPV method), internal rate of return

method (IRR method), accounting rate of return method (ARR method), payback

period method (PB method), discounted payback method (DPB method), and

profitability index method (PI method). Every method has its unique merits as well as

its drawbacks. The crucial merits and drawbacks of these six methodologies are

summarized in TABLE 2.1.

(TABLE 2.1 is about here)

Some investment projects have to invest vast amounts of money periodically

under high uncertainty, and traditional investment methodologies cannot help

managers decide whether managers should invest in the project. Because of the

problems, the method of real options evolves.

2.2 Real Options

Black and Scholes (1973) derived the famous B-S formula pricing European options,

and Merton (1973) not only expanded the mathematical comprehension of pricing

Hayes and Abernathy (1980) and Hayes and Garvin (1982) mentioned that the

traditional methods for investment decisions eliminated the value of flexibility.

Trigeorgis and Mason (1987) also stated that the discount cash flow (DCF) method

could not reflect the authentic value of managerial flexibility.

Myers (1977) brought up the concept to combine the relation between financial

options and real options, and he pointed out that real options could be priced by

financial options. In addition, Trigeorgis (1993) indicated that the main difference

between financial options and real options was the underlying assets. He also

classified explicitly that the underlying assets of financial options were financial

securities that could be issued; on the other hand, the underlying assets of real options

were real assets that could not be issued.

(TABLE 2.2 is about here)

TABLE 2.2 explains the definitions of important variables between financial

options (for financial assets) and real options (for projects). A call option gives its

holder the right, by paying a specified cost within a period of time, to exercise the

option and acquire the underlying asset. If there are no opportunity costs of waiting or

dividend-like benefits to hold the asset, the holder will postpone the decision to

exercise until the expiration date (T). In the real option case, the underlying asset is

while the exercise price is the necessary investment outlay (at time T), IT. The ability

to defer a project with an uncertain value, VT, creates valuable managerial flexibility.

If, during the later period, market demand develops favorably and VT > IT, the firm

can make the investment and gain the net present value of the project at that time,

NPVT = VT - IT. If, on the other hand, the project value turns out to be lower than

originally expected (VT < IT), management can decide not to make the investment and

its value is truncated at zero. In this situation, the firm only loses what it has spent to

obtain the option.

(TABLE 2.3 is about here)

TABLE 2.3 exhibits the concept of the basic types of real options analyzed in the

literature. This table contains the option to defer investment in a new uncertain market,

the option to expand or contract capacity, the option to abandon, the option to switch

inputs or outputs, and the option to temporarily shut down.

Taudes (1998) analyzed the decision model of an investment project by using

the real options approach in information technology (IT) industry. In Taudes’s paper,

the NPV of an irreversible investment project can be calculated by the following

formula:

Expanded (strategic) net present value (NPV*) = Passive NPV of expected cash flows

2.3 Game Theory

Zermelo (1913) brought up the first theorem of game theory, called Zermelo’s

Theorem. Borel (1921) published four notes of strategic games and gave the first

contemporary formula of the mixed strategy. Von Neumann and Morgenstern (1944)

analyzed people’s behaviors and interactions through the strict mathematical model

which includes game theory.

Furthermore, Nash (1950) concentrated on non-cooperative games including

the theory of Nash Equilibrium. Flood and Dresher (1950) finished a famous

experiment—the Prisoner’s Dilemma. Nash (1950, 1951) proved the existence of the

Nash Equilibrium, a strategic equilibrium for noncooperative games.

Harsanyi (1967, 1968) developed incomplete information of game theory.

Kreps et al. (1982) brought the concept that sequential equilibrium enlarged the

concept of a subgame perfect equilibrium to subgames in the extensive form.

2.4 Options Game

For a project with uncertainty, managers can make a good decision by using the real

options approach considering the flexibility of a project. Meanwhile, managers also

have to deliberate competitors’ behaviors, so game theory is involved. TABLE 2.4

shows the related literatures of successive stages of analysis for the options game

problems and their varieties.

(TABLE 2.4 is about here)

Kulatilaka and Perotti (1998) pointed out that a company would gain more

market shares when it had more strategic investment of growth options. Cottrell and

Sick (2001) indicated that an enterprise would own the first mover advantages when

the enterprise was the first investor of a field, and the investment project would

generate the convenience value. They also stated how a follower might gain more

profits by using the right of wait and see.

Isik et al. (2003) found that a project decision of a company was influenced by

costs, market demand, and competitiors’ uncertainty through using the options game

method. Furthermore, Murto (2004) found out the best timing for abandoning in a

declining duopoly market by the same method. Smit and Trigeorgis (2006) also

derived the best R&D strategy for consumer electronic products, telecommunications,

TABLE 2.1

Merits and Drawbacks of the Six Traditional Investment Methodologies

Investment Model Merits Drawbacks

Net Present Value (NPV method)

1.It is easy to calculate

2.It considers all cash flows and time value of money

3.Value can be added

4.The highest-value project can be chosen from many exclusive projects

It is hard to decide an appropriate discount rate

Internal Rate of Return (IRR method)

1.It considers all cash flows and time value of money

2.It obtains an implied rate of return

1.NPV and IRR may cause different results in the same project

2.It may result in multiple real or imaginary roots

3.It is not suitable for exclusive investment projects

Accounting Rate of Return (ARR method)

1.It is easy to decide a proper investment project

2.It considers all cash flows

1.It does not deliberate time value of money and cash flows of whole periods

2.The critical point of whether to invest is subjective rather than objective

Payback Period (PB method)

1.It is easy to calculate

2.It considers the liquidity of projects

1.It ignores the cash flows which come after payback periods

2.It is not suitable for long-term periods projects

3. Time value of money is not included

Discounted Payback Period (DPB method)

1.It is easy to calculate 2.The liquidity of projects is

considered

3. Time value of money is contained

1.It ignores the cash flows which come after payback periods

2.It is not suitable for long-term periods projects

3. Time value of money is not included Profitability Index

(PI method)

It is often collocated with IRR to evaluate a project

Sometimes it has different results with NVP

TABLE 2.2

Definitions of Important Variables between Real Options and Financial Options

Call option Variable Project

Stock price V Present value of expected cash flows Exercise price I Present value of investment outlays Time to maturity T Length of deferral time

Risk-free rate r Time value of money Variance of stock returns σ2

Volatility of project’s returns Source: Smit and Trigeorgis (2004), p. 12

TABLE 2.3

Common Corporate Real Options

Type of option Relevant Research Description

Option to defer (simple option)

McDonald and Siegel (1986); Paddock, Siegel and Smith (1988); Ingersoll and Ross (1992)

Management holds a lease on (or the option to buy) valuable land or natural resources. It can wait to see if output prices justify constructing a building or plant, or developing a field. Growth Option (compound option) Trigeorgis (1988); Pindyck (1987); Chung and Charoenwong (1991); Smit (1996)

An early investment (e.g., R&D investment) or a strategic investment is a prerequisite or a link in a chain of interrelated projects, opening up future growth opportunities (e.g., a new generation product or process).

Option to abandon

Kemna (1988); Myers and Majd (1990)

If market conditions decline severely, management can abandon current operations permanently and realize on secondary markets the resale value of capital

equipment and other assets.

Option to expand or contract

McDonald and Siegel (1985); Trigeorgis and Mason (1987); Pindyck (1988); Kemna (1988)

If market demand turns out to be more favorable than expected, management may increase capacity or accelerate resource utilization. Management may also extend production if the life of the project is longer than expected. Conversely, management may reduce the scale of operations.

Option to temporarily shut down

Bernnan and Schwartz (1985)

If operations are less favorable than expected, management may temporarily halt and then start up again.

Option to switch

Kulatilaka (1988 and 1995); Aggarwal (1991); Kogut and Kulatilaka (1994); Kamrad and Ernst (1995)

If prices or demand changes, management may change the project mix of the facility (“product flexibility”). Alternatively, the same outputs can be produced by different projection processes or inputs (“process flexibility”).

TABLE 2.4

Successive Stages of Analysis for Real Options Game

Type of option game Relevant Research Problems Description Implication One-stage games

with no competition (proprietary option)

McDonald and Siegel 1986; Brennan and Schwartz 1985

View investment opportunities as simple proprietary options to invest.

Incentive to delay investment under uncertainty One-stage games with endogenous competitive reactions (shared option) Dixit 1979, 1980; Spence 1977, 1979; Kester 1984; Baldwin 1987; Trigeorgis 1988; Ghemawat and del Sol 1998; McGahan 1993; Smit and Ankum 1993

When shared opportunities face a competitive loss, a game-theoretic treatment becomes necessary.

Timing is a tradeoff between flexibility value and commitment.

Two-stage games with no competition

McGrath 1997; Bettis and Hitt 1995; Bowman and Hurry 1993

Investment in growth options; for instance, the analysis of R&D

opportunities to acquire a proprietary option to proceed with the commercialization investment in the stage 2

Negative NPV of the first stage can be justified for its growth option value

Two-stage games with endogenous

competition in stage 2

Dasgupta and Stiglitz 1980; Appelbaum and Lim 1985; Daughety and Reinganum 1990;

Spencer and Brander 1992; Kulatilaka and Perotti 1998

R&D strategy of the stage 1 faces (endogenous)

competition in production (stage 2)

Competitive strategy based on the type of investment

(proprietary/shared) and the nature of competitive reaction (reciprocating/contrarian) Two-stage games with endogenous competition in both stage

Appelbaum and Lim 1985; Spencer and Brander 1992

Strategic investment with endogenous competition in the stage 1 influences the value of stage 2 Trade-off between cooperation and competition Competition vs. cooperation in stage 1

(joint R&D ventures)

Kogut 1991 The value of stage 2 is affected by the cooperation competition of stage 1

Evolution of cooperation in technology intensive industries

Section 3 Model Construction

In the laptop OEM/ODM market, there exists high competition and low profits.

Namely, each firm’s decisions and actions are strongly and easily affected by other

firms. The main purpose of this study is to look into the competitive relationship

between Quanta and the three other firms and the value of investing in the multi-touch

panel project through the options game methodology.

3.1 Methodology

Smit and Trigeorgis (2004) published a book; they introduced real options and game

theory in detail and integrated these two approaches into an analytical method. In

Chapter 6 of this book, they took an example of an R&D investment for the

development of the latest, economical, and technological process versus a base case of

no R&D investment which continues to use the existing technology. The option value

of this R&D investment depends on endogenous competitive reactions; this example

is illustrated by the two-stage game in extensive form under different market

structures.

Correspondingly, the model of this study expands the theoretic framework from

the book to the laptop OEM/ODM industry with four-stage game under complicated

3.2 Model Assumptions and Constraints

First of all, the market structure of this model is supposed to be a duopoly market; that

is, there are two main companies dominating the industry. In order to conform to the

model and ponder the other firms’ reactions, Compal, Wistron, and Inventec are

combined to form a group which is the Quanta’s competitor, called “Others.”

Pegatron Corporation is not a listed company, so it is excluded from the study.

Second, much evidence shows that the life cycle of most of innovative

electronic products lasts three or four years, so the lengths of time are decided in four

periods.

Third, the range of up moves and down moves is fixed to recombine the nodes

of this decision tree.

3.3 Decision Tree

The convenient and interesting function of the iPhone touch panel indeed created a

shopping rush around the world; therefore, engineers who work at Quanta thought of

implementing the ideas of the iPhone touch panel in their products. After that, Quanta

was expected to gain more market shares and profits by inventing new laptops with

touch panel.

At present, touch panels can be classified into two categories, which are

types of touch panels are controlled by foreign companies, such as Synaptics, Inc.,

ALPS ELECTRIC CO., LTD, and Texas Instruments Incorporated. Due to the

constraints of the touch panel patents, Quanta decided to invent a new type of laptops

with touch panels, called multi-touch panel laptops, which are responded by CMOS.

(FIGURE 3.1 is about here)

(FIGURE 3.2 is about here)

(TABLE 3.1 is about here)

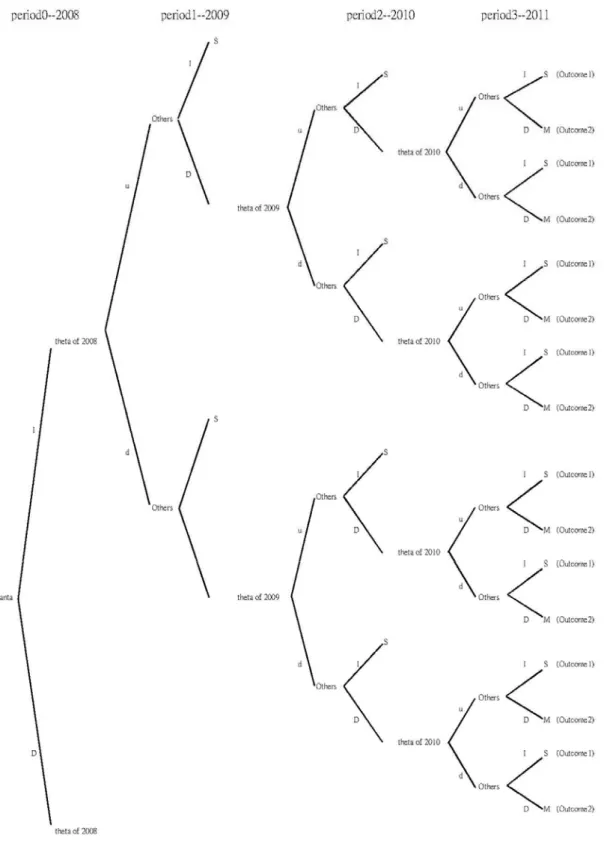

FIGURE 3.1 depicts the possible decisions and actions of Quanta and Others, if

Quanta decides to invest in the project in the first period (2008). Quanta, which is the

pioneer firm, has two options: to invest in the R&D project of multi-touch panel

laptops or not to invest in it this year. If Quanta decides to make a strategic investment

(I) for the project (investing in the project), a sequential game will occur. Investing in

the project also means that Quanta probably gains proprietary advantages and Others’

decisions must be influenced by Quanta’s decisions. One year later, the exogenous

market demand of multi-touch panel laptops, which is represented by the symbol “θ ”,

may move up (u) or down (d). Since Quanta already made the strategic investment in

2008, Others has to decide whether Others should invest in the project in this period

(2009). No matter if the market demand moves up or down, either of the two

Outcome 1: Stackelberg price leader/follower outcome (S and SL F)

If Others decides to make the strategic investment, a Stackelberg

leader/follower game is formed. In this situation, Quanta invests in the project first, so

it becomes a Stackelberg leader ( ); Others invests at a later period, so it becomes a

Stackelberg follower ( ). On the contrary, if Others invests in first, then it becomes

a Stackelberg leader; Quanta invests in a later period, it becomes a Stackelberg

follower.

L

S

F

S

Outcome 2: Monopolist outcome (M)

If Others decides not to make the strategic investment, the sequential game will

be repeated until the last period of time (2011). In 2011, if three other companies still

choose not to invest in the project, then Quanta finally turns into a monopolist (M) of

the touch panel laptop OEM/ODM market.

On the other hand, if Quanta decides to defer (D) for the project (not investing

in the project) in the first period, it means that Quanta and three other firms are

identical (producing similar laptops) and a simultaneous game will occur in the next

period (2009). FIGURE 3.2 illustrates the possible situations of deferring the project in

first period. In addition to FIGURE 3.1 and FIGURE 3.2, TABLE 3.1 shows the

In period 1 (2009), either of the two sides (Quanta and Others) can make the

investment for the project, and four possible outcomes will occur.

Outcome 3: Bertrand price equilibrium outcome (B)

First of all, if both Quanta and Others invest in this period (2009) simultaneously,

the outcome results in Bertrand price equilibrium.

Secondly, if Quanta invests in the project in this period, and Others chooses not

to invest in this period and chooses to invest in a later period, a Stackelberg

leader/follower game is formed. Accordingly, Quanta is a Stackelberg leader ( ),

and Others is a Stackelberg follower ( ). Conversely, if Quanta chooses not to

invest in the project in this period, and its competitor does; the outcome causes a

Stackelberg leader/follower game. In this situation, Quanta becomes a Stackelberg

follower ( ), and Others becomes a Stackelberg leader ( ).

L S F S F S SL

Thirdly, if Quanta invests and Others chooses to defer until the last period, then

Quanta becomes a monopolist (M) in the touch panel laptop OEM/ODM market and

vice versa.

Outcome 4: Abandon outcome (A)

Fourthly, no matter if the market demand moves up or down, if both sides

always decide to defer the project from 2008 to 2011, or they determine to abandon ,

3.4 Price Competition Model

3.4.1

Cash Flows of the ProjectSuppose that the demand for the touch panel laptops is linear in prices2:

( , , )

i i j it it i j

Q P P θ =θ −bP + dP (3.1)

where the quantity which is sold by company is related to its price and the

competitor’s price . The coefficients and ( , assuming demand

substitutes) capture the sensitive of the quantity sold to the firm’s own and its

competitor’s price settings, respectively.

i Pi

j

P b d b>0 d >0

The profits of each firm (where = Quanta or Others) are i i

πi( ,P Pi j,θi t, )=(Pi−ci)(θi t, −bPi+ Pd j)

i

i i i

(3.2)

where c is the variable cost of company . i

Based on (3.1) and (3.2), every competitive price can be obtained. The

equilibrium prices are showed in TABLE 3.2, and the derivation procedures are

exhibited in the appendix.

(TABLE 3.2 is about here)

By using these prices, predicted quantities, and the invested capital for the

touch panel laptop project, the cash flows in last period can be gained. Cash flow of the project *

(P c ) Qe stim a te d I

= − × − (3.3)

2

where = Quanta or Others, i *

i

P is the competiton price, is the variable cost,

is the estimated quantities of the touch panel laptops, and is the

invested capital for the project.

i

c

e stim a te d

Qi I

3.4.2

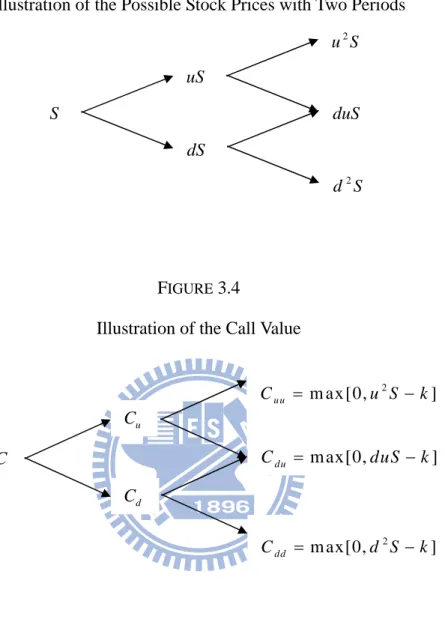

Backward Induction(FIGURE 3.3 is about here)

(FIGURE 3.4 is about here)

Cox, Ross, and Rubinstein (1979) manipulated the method of backward induction to

obtain the option value at the beginning in a discrete time structure. FIGURE 3.3

demonstrates the possible stock prices after two periods. In order to keep with the

binomial process, the stock price can take on three possible values after two periods,

where is the stock price, is the upper rate of return on the stock, and is the

lower rate of return on the stock. Besides, has to equal so that the binomial

tree can recombine in the last period.

S u d

d 1/ u

Similarly, FIGURE 3.4 shows a call with two periods remaining before its

expiration date, where is the call value, stands for a call two periods from

the current time if the stock price moves upward each period, and have

analogous definitions, and is the exercise price.

C Cuu

du

C Cdd

The call option can be obtained by3: 2 2 2 2 2 2 2 2 2 (1 ) (1 )

max[0, ] 2 (1 ) max[0, ] (1 ) max[0, ]

uu ud dd p C p p C p C C r p u S k p p duS k p d S k r + − + − = − + − − + − − = (3.4)

where p is the risk-neutral probability and r is the risk-free rate.

Finally, the option values in every node are determined through the backward

induction approach from the last period to the first period, and each firms’ optimal

decisions can be decided by the computation results at the beginning.

3

FIGURE 3.1

FIGURE 3.2

TABLE 3.1

Definitions of the Symbols

Symbol Definition Quanta Quanta Computer Inc.

Others

Three firms including Compal Electronics, Inc., Wistron Corporation, and Inventec Corporation

I A decision to invest in the project

D A decision to defer the project / Stay flexible (option value)

θ The state of market demand of multi-touch panel laptops (exogenous variable)

u Nature’s up moves d Nature’s down moves.

S Stackelberg leader (SL) / follower (SF) outcome M Monopolist outcome

B Bertrand quantity / price equilibrium outcome A Abandon (0 value)

TABLE 3.2

Equilibrium Prices for Different Market Structures under Reciprocating Price Competition in Each Stage Action (A,B) Market Structure N/M/S/A/D Equilibrium Price,

Pi

* (for qi =qj =0) Period 1(I,I) Bertrand price (B) 2 ( , )2 (2 , )

4 i t i j t j b bc d bc b d θ + + θ + − (I,D) (D,I)

Stackelberg price leader (SL) or

Stackelberg price follower (SF)

, , 2 2 2 ( ) ( ) 4 2 i t i j t j i b bc d bc dc b d θ + + θ + − − 2 , , , 2 2 2 ( ) ( ) 2 2 2 (4 2 ) j t cj bd i t bci d j t bcj dci b b b d θ θ + + θ + − + + − (D,D) Defer (D) Period 2

(DI,DI) (II,II) Bertrand price (B) 2 ( , )2 (2 , )

4 i t i j t j b bc d bc b d θ + + θ + −

(II,DI) (DI,II) Stackelberg price leader (S

L

) or

Stackelberg price follower (SF)

, , 2 2 2 ( ) ( ) 4 2 i t i j t j i b bc d bc dc b d θ + + θ + − − 2 , , , 2 2 2 ( ) ( ) 2 2 2 (4 2 ) j t cj bd i t bci d j t bcj dci b b b d θ θ + + θ + − + + − (D,D) Defer (D) Period 3

(DDI,DDI) Bertrand price (B) 2 ( , )2 (2 , ) 4 i t i j t j b bc d bc b d θ + + θ + − (DDI,III) (III,DDI) (DII,DDI)(DDI,DII)

Stackelberg price leader (SL) or

Stackelberg price follower (SF)

, , 2 2 2 ( ) ( ) 4 2 i t i j t j i b bc d bc dc b d θ + + θ + − − 2 , , , 2 2 2 ( ) ( ) 2 2 2 (4 2 ) j t cj bd i t bci d j t bcj dci b b b d θ θ + + θ + − + + −

(III,DDD) (DDD,III) Monopolist(M) ( )

2( ) t c b d b d θ + − − (DDD,DDD) Abandon (A)

FIGURE 3.3

Illustration of the Possible Stock Prices with Two Periods

2

u S uS

FIGURE 3.4

Illustration of the Call Value

S dS duS 2 d S C u C d C m ax[0, ] du C = duS −k 2 m ax [0, ] uu C = u S −k 2 m ax[0, ] dd C = d S −k

Section 4 Case Study

4.1 Price Competition Industry

Although much evidence shows that the laptop OEM/ODM industry is a price

competition industry, the competitive type of the industry still needs to be proved by

numbers. Bulow, Geanakoplos, and Klemperer (1985) and Sundaram, John, and John

(1996) indicated that the variable of Competitive Strategic Measure (CSM) is a direct

proxy of the second derivative of profit with respect to its own quantity and the

competitor’s quantity. By computing the coefficient of correlation between the change

in a firm’s profit margin (Δπf /Δ ) against the change in its competitor’s output Sf

( ), the market competitive type can be found. If CSM is greater than zero, the

market is defined as strategic complements (a price competition market); otherwise,

the market is defined as strategic substitutes (a quantity competition market). c

S

Δ

In the laptop OEM/ODM industry of Taiwan, the coefficient of correlation

between the profit margin of Quanta and the output of Others is 0.1033, so the market

is regarded as a price competition market. However, because of the highly seasonal

variation of the revenue in this industry, we use the approach of seasonal differential

4.2 Case Study

4.2.1 Assumptions

Firstly, based on the estimation of MIC, Quanta uses the CMOS technology of PixArt

Imaging Inc.4, so the invested capital for touch panel laptops in this study includes the R&D expenses of Quanta and PixArt. TABLE 4.1 shows the R&D expenses of Quanta

and PixArt for the touch panel laptop project in 2007 and 2008, and this study

assumes that 50 percent of the total R&D expenses are used in inventing touch panel

laptops.

(TABLE 4.1 is about here)

Secondly, this study assumes that the first mover (the company which invests in

the project first) can earn 5 percent additional quantity when the market moves up and

earn 3 percent additional quantity when the market moves down.

4.2.2 Estimation of Parameters

Equation (4.1) supposes that the demand for the touch panel laptops is linear in

prices5:

( , , )

i i j it it i j

Q P P θ =θ −bP + dP , = Quanta or Others (4.1) i

where the quantity which is sold by company is related to its price and the

competitor’s price . By putting the historical data of

i Pi

j

P Pi, Pj, and Qi (where

4

PixArt Imaging Inc., one of the leading companies of CMOS imaging sensors and related IC design, research, production, and sales.

i = Quanta and j = Others or = Others and i j = Quanta) into regression model, the

coefficients and d can be estimated. These two estimated coefficients and are 599.5746 and 572.3002. The time period of data starts in the third quarter of

2003 and ends in the fourth quarter of 2008. Equation (4.1) becomes:

b b

d

Q P Pi( i, j,θit)=θit −599.5746Pi+572.3002Pj, = Quanta or Others (4.2) i

After that, Pi, Pj, and Qi are put into the equation (4.2), a series of θi t,

(where = Quanta or Others) can be gained. The market demand for touch panel

laptops in 2008 is 82,573,618 when equals Quanta; the market demand for touch

panel laptops in 2008 is 107,666,161 when i equals Others. Besides, the annual

volatility of the growth rate of the laptop market demand (

i

i

σ ) is 0.4465. According to this statistic, the up moves (u) and down moves (d) are:

exp( ) exp(0.4465 1) 1.5628 u= σ T = × = , and 1 1 0.6399 1.5268 d u = = =

σ is annual volatility, and is the length of a trading period. T

where

In addition, the risk-neutral probability6 is defined by

0.02 1 e 0.4748 0.412 2.1062 0.4748 rT d e p u d × − − = = = − −

where r is the risk-free rate, which is 0.02 in this case.

4.2.3 Cash Flows of the Last Period

Equation (4.3) describes the cash flow of the last period under different outcomes,

including Cournot Nash price competition equilibrium outcome, monopolist outcome,

Stackelberg price leader/follower outcome, and abandon.

Cash flow of the project *

( ) e stim a te d i i i P c Q I = − × − (4.3) where * i

P is the competition price of different outcomes, is the variable cost,

is the estimated quantity of the touch panel laptops, and is the invested

capital for the project. In this project,

i

c

e stim a te d i

Q I

I equals NT$ 6,239(million). The average

operating costs of Quanta and Others are NT$41,290 and NT$44,091 respectively.

TABLE 4.2 illustrates the estimated quantity of touch panel laptops in the last period

(2011) under different nature moves.

(TABLE 4.2 is about here)

4.2.4 Backward Induction

If Quanta decides to invest in the project at the beginning (2008), the sequential game

will be formed.

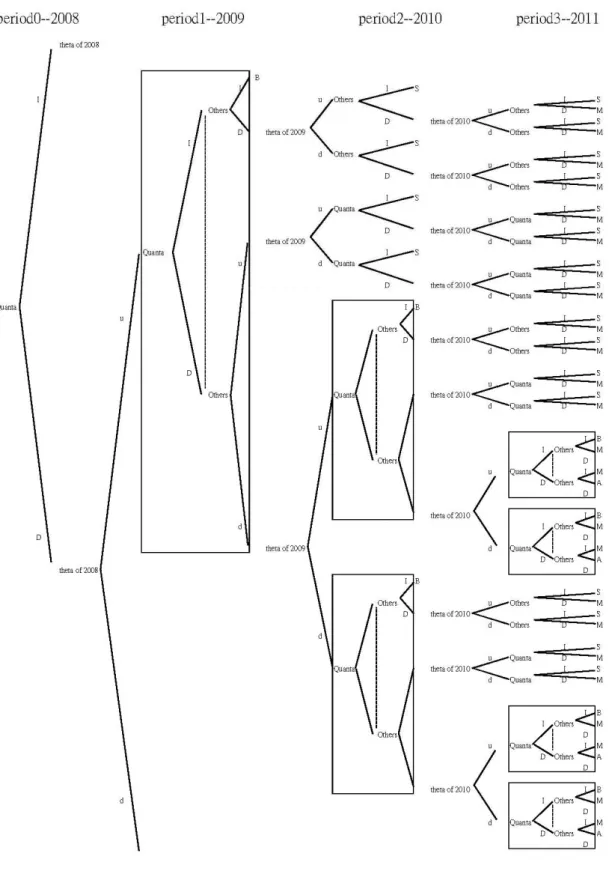

(FIGURE 4.1 is about here)

FIGURE 4.1 illustrates the cash flow of the last period if the market moves up

decide whether it should invest in the last period (2011). If Others chooses to invest,

Quanta will become the Stackelberg leader and Others will become the Stackelberg

follower. The cash flow of Quanta is NT$ 19,969,659(million), and the cash flow of

Others is NT$ 25,350,106(million). If Others decides not to invest, then Quanta will

become the monopolist. The cash flow of Quanta is NT$ 154,182,726(million), and

the cash flow of Others is NT$ 0. After that, the option value can be obtained through

the backward induction. On the other hand, a similar result can be obtained when the

market moves down (d).

0.412 19,969,659,434,487 +(1-0.412) 2,515,880,963,735 9,514,334,503,328 (1 0.02) × × = +

If Quanta decides to defer in the project at the beginning (2008), then the

simultaneous game will be formed. There exists two equilibrium of the simultaneous

game, one is pure strategy equilibrium, and the other is mixed strategy equilibrium. (FIGURE 4.2 is about here)

FIGURE 4.2 shows the simultaneous game with the extensive and normal form

in 2011 when the market moves up three times in the past three years. There exists

pure strategy equilibrium in this situation. If Quanta chooses invest in the project,

Others will decide to invest in it. However, if Quanta choose not to invest in the

project, Others will still decide to invest in the project, because Others will gain more

the optimal decision for Others. Under this decision from Others, Quanta will decide

to invest in it finally since Quanta can earn more cash flow through investing in the

multi-touch panel laptop project.

The other equilibrium is mixed strategy equilibrium. The derivation process is

showed in the Appendix 2.

According to the ultimate value, which is computed through the options game

methodology, the result shows that investing in the multi-touch panel laptop project is

optimal decision for Quanta, and the option value is NT$ 2,082,601(million). FIGURE

4.3 illustrate the route of the decision tree for the project. FIGURE 4.4 and FIGURE 4.5

show the decision route if the market moves up and down respectively.

(FIGURE 4.3 is about here)

(FIGURE 4.4 is about here)

(FIGURE 4.5 is about here)

4.3 Scenario Analyses

The result of the case study is influenced by many parameters, such as the market

demand θ , volatility σ , risk-free rate , and invested capital r I . Based on

different information which provided by different research institutes, the value of

parameters is varied. Before starting analyses, we here compare the value with game

(TABLE 4.3 is about here)

TABLE 4.3 shows the option value with game theory, and the option value

without game theory. We can easily find that the option value without game theory is

lower than it with game theory. This is because the option value without game theory

deliberates less situation so that has lower value; on the other hand, the option value

with game theory not only considers the possible situation but also deliberates the

competitors’ decision.

(TABLE 4.4 is about here)

In order to simplify the structure of the tree, we classify the time period into

three years, two years, and one year. The shorter time period which considers fewer

situations causes less option value. TABLE 4.4 presents the result of the simplification.

(TABLE 4.5 is about here)

TABLE 4.5 exhibits the option value of investment and deferral and the

decisions at the beginning when the theta of Quanta changes. Investing in the project

in the first period will be the optimal decision for Quanta when the market demand of

the touch panel laptops is greater than the base case ( = 20,643,414). Conversely,

Quanta will choose to defer at the beginning when the market demand is less than

10,000,000.

2008

Quanta

(TABLE 4.6 is about here)

TABLE 4.6 shows the influences of the changes of the volatility. Higher

volatility has both higher investment value and deferral value because the market

faces more uncertainty in the future. Quanta will decide not to invest in the project if

the volatility is less than 0.1.

(TABLE 4.7 is about here)

TABLE 4.7 presents the decision outcomes and option value when the risk-free

rate changes. Risk-free rate not only affects the discount rate directly but influences

the risk-neutral probability indirectly. No matter how the risk-free rate shifts, it can be

found that investing in the project is the optimal decision for the managers of Quanta.

(TABLE 4.8 is about here)

(TABLE 4.9 is about here)

At the beginning of this chapter, we assume that the first mover will obtain 5

percent additional quantity. TABLE 4.8 illustrates the results while the increment of

the ratio changes. This additional quantity has to be equal or more than 3 percent

since the other additional quantity is 3 percent when the market moves down. This

table shows that Quanta will choose to invest in the project whether the additional

quantity increases or decreases. On the other hand, TABLE 4.9 exhibits the changes of

to equal or less than 5 percent since the additional ratio of the up moves for the first

mover is 5 percent. This table shows that investing in the project is still the optimal

decision for Quanta because this assumption is an accommodating decision, which

TABLE 4.1

R&D Expenses of Quanta and PixArt for Touch Panel Laptops

Year Quanta PixArt

2007 2,335 256

2008 3,108 538

Total 6,239 Unit: NT Million Dollars

TABLE 4.2

Estimated Quantity of Touch Panel Laptops in 2011

Nature Moves Quantity of Quanta Quantity of Others u, u, u 163,737,157 237,666,964 u, u, d 67,043,078 97,314,043 u, d, u 67,043,078 97,314,043 d, u, u 67,043,078 97,314,043 u, d, d 27,451,156 39,845,769 d, d, u 27,451,156 39,845,769 d, u, d 27,451,156 39,845,769 d, d, d 11,240,027 16,315,069

FIGURE 4.1

Outcome of the Up Moves of the Market in 2011

Unit: NT Million Dollars

FIGURE 4.2

Outcome of the Simultaneous Game with the Extensive Form in 2011

Normal Form Invest Defer Invest (14390163, 25149785)* (139847697, 0) Defer (0, 139257502) (0, 0) Unit: NT$ million 2010 θ 9,51 4,3 35 12 ,12 8,3 97 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ S S M M Others D D I I d u Others 19 ,96 9,6 59 2 5,3 50,106 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ 15 4,1 82,72 6 0 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ 2 ,515 ,88 1 3,281 ,50 3 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ 2 2,5 63 ,18 8 0 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ 14 ,39 0,1 63 2 5,1 49 ,78 5 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ C I 139 ,84 7,69 7 0 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ 0 139,257,502 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ 0 0 ⎡ ⎤ ⎢ ⎥ ⎣ ⎦ M A M D D I Others Others 2010 d u θ Others Quanta

FIGURE 4.3

Route of the Decision Tree (Investing)

FIGURE 4.4

Route of the Decision Tree (Deferring; up moves)

FIGURE 4.5

Route of the Decision Tree (Deferring; down moves)

TABLE 4.3

Comparison between Option Value with Game and Option Value without Game Status Value of Investment Value of Deferral Decision Value with Game 2,082,602 1,953,029 Invest

Value without Game 507,769 1,481,771 Defer

Unit: NT Million Dollars

TABLE 4.4

Reduced Form of the Time Period

Time Period Value of Investment Value of Deferral Decision

3 Years 2,082,601 1,953,029 Invest

2 Years 1,498,260 1,507,340 Defer

1 Year 896,762 764,978 Invest

Unit: NT Million Dollars

TABLE 4.5

Scenario Analysis of Theta of Quanta

Theta of Quanta Value of Investment Value of Deferral Decision

80,000,000 8,770,006 -46,674 Invest 60,000,000 6,516,708 2,745,245 Invest 40,000,000 4,263,410 2,605,089 Invest 2008 Quanta

θ

=20,643,414 2,082,601 1,953,029 Invest 10,000,000 883,463 1,010,7681 Defer 7,000,000 5454,468 714,785 Defer 5,000,000 320,139 335,608 DeferTABLE 4.6

Scenario Analysis of Volatility

Volatility Value of Investment Value of Deferral Decision

0.9 10,035,469 5,853,617 Invest 0.8 7,249,203 3,315,002 Invest o.6 3,399,745 3,166,193 Invest

σ

= 0.4465 2,082,601 1,953,029 Invest 0.2 1,049,097 1,234,717 Defer 0.1 893,873 1,100,404 Defer 0.05 864,189 1,066,856 DeferUnit: NT Million Dollars

TABLE 4.7

Scenario Analysis of the Changes of Risk-free Rate

Risk-free Rate Value of Investment Value of Deferral Decision

0.20 3,236,907 3,133,771 Invest 0.10 2,604,490 2,515,210 Invest 0.05 2,279,281 2,173,702 Invest r= 0.02 2,082,601 1,953,029 Invest 0.01 2,016,938 1,875,862 Invest 0.005 1,984,105 1,836,456 Invest 0.001 1,957,841 1,804,497 Invest

TABLE 4.8

Scenario Analysis of the Increment Changes of Up Moves

Increment of Up Moves Value of Investment Value of Deferral Decision

0.20 4,227,806 2,932,966 Invest 0.15 3,370,562 1,036,882 Invest 0.10 2,662,820 2,393,075 Invest u Increment = 0.05 2,082,601 1,953,029 Invest 0.04 1,980,112 1,875,365 Invest 0.03 1,881,796 1,795,272 Invest

Unit: NT Million Dollars

TABLE 4.9

Scenario Analysis of the Increment Changes of Down Moves

Increment of Down Moves Value of Investment Value of Deferral Decision

0.05 2,123,824 1,908,965 Invest 0.04 2,103,030 1,956,614 Invest d Increment = 0.03 2,082,601 1,953,029 Invest 0.01 2,042,820 1,952,113 Invest 0.005 2,033,095 1,952,929 Invest 0.001 2,025,379 1,953,802 Invest

Section 5 Conclusions

The model of this thesis follows the theoretical frameworks from Smit and Trigeorgis

(2004). We implement the model to the laptop OEM/ODM industry with four-stage

game under complicated market structures. Under the conditions of the price

competition and the duopoly market, this study assumes that the first mover, the

company which invests in the project first, can obtain 5 percent additional quantity

when the market moves up and 3 percent additional quantity when the market moves

down. This study uses the real options game methodology which considers the market

uncertainty but deliberates Quanta’s competitors’ reactions including Compal

Electronics, Inc., Wistron Corporation, and Inventec Corporation; the result

demonstrates that the optimal decision of Quanta, the leader company of the industry,

is to invest in the multi-touch panel laptop project in the first period (2008).

Besides, there are four vital results of the scenario analyses. First of all,

investing in the project in the first period will be the optimal decision for Quanta

when the market demand of the touch panel laptops is greater than 20,643,414.

Conversely, Quanta will choose to defer the project at the beginning when the market

demand is less than 10,000,000.

Secondly, higher volatility has higher investment value and deferral value.

Thirdly, no matter how the risk-free rate shifts, it can be found that investing in

the project is the optimal decision for Quanta.

Finally, if the market moves up, Quanta which is the first mover, will choose to

invest in the project when the additional quantity is more than three percent.

Accordingly, if the market moves down, investing in the project is still the optimal

decision for Quanta when the additional quantity is less than three percent.

By the way, there are two recommendations that we can do for the future

research. Firstly, the demand function of the Bertrand duopoly price competition

model can be modified to fit the status of the laptop OEM/ODM market appropriately.

Secondly, the competiton in the laptop OEM/ODM market is fierce recently. For

example, the total shipment of Wistron in the fourth quarter of 2008 is more than the

shipment of Compal. Moreover, the total shipment of Compal in March of 2009

surpasses the total shipment of Quanta. We recommend that the decision tree be

Appendixes

Appendix 1

Derivation of Equilibrium Prices

We assume for simplicity that the demand for the laptops is linear in prices:

( , , )

i i j it it i j

Q P P θ = θ − b P + d P (A.1)

where the quantity which is sold by company is related to its price and the

competitors’ price . Besides, The coefficients and ( , assuming

demand substitutes) capture the sensitive of the quantity sold to the firm’s own and its

competitor’s price settings, respectively. The profits of each firm i (where =

Quanta or Others) are given by

i Pi j P b d b>0 d >0 i , , ( , , ) ( )( ) i P Pi j i t P ci i i t bP dPi j π θ = − θ − + (A.2) The reaction function of each firm i is gained by maximizing its profit value

( , ) i i i j

V P P

k

π

≡ over its own price , where is a constant risk- adjusted discount rate. Setting i P k 0 i i V P ∂ = ∂ , obtains , ( )(1 ) ( ) (2 ) i t j i i i i j i dP bq bc P R P b bq θ + + + = = + (A.3)

A company engaged in price competition has a best (profit-maximizing) response

to competitor price changes according to its reaction function. Substituting the expression for R P in place of i( j) in equation (A.1) gives the general asymmetric

Nash equilibrium price expression: j

, , * 2 2 2 ( ) ( ) 4 i t i j t j i b bc d bc P b d θ + + θ + = − (A.4)

If firm i invests first and firm j defers until next period (I,D), the leader will

choose the price that maximizes its own profit value, using the reaction function of the follower. Maximizing V P R Pi( ,i j( ))i over Pi , given R Pj( )i , gives a Stackelberg leader price (for qi = qj= 0):

, , 2 2 2 ( ) ( ) 4 2 i t i j t j i i b bc d bc dc P b d θ + + θ + − = − (A.5)

Taking the Stackelberg leader price into its competitor’s reaction function R P j( )i

gives the Stackelberg follower price:

2 2 2 2 2 , , , 2 2 (4 2 ) 2 ( ) ( ) (4 2 ) ( ) 2 (4 2 ) j t i t i j t j i j j j i b d db bc d bc dc bc b d P R P b b d θ − + θ + + θ + − + − = = − (A.6)

Appendix 2

Mixed Strategy Equilibrium

7Let the decision nodes labeled by an indicator set I = {1, 2, …, n}. At node i, the action set is Ai =

{

a a1i, 2i, ...,ani}

. An individual’s behavior at node i is determined by a probability vector IPi =(

p a( ), (1i p a2i), ..., ( ain))

, and the set of pure strategies is given by the cross-product of all the action sets: si =A1×A2× ×... An. When there is only a single decision to be made, the sets of actions and pure strategies are identical.However, if there is more than one decision to be made, the action sets and pure

strategies are no longer identical and there are now two. To distinguish between them,

we shall call one a “mixed strategy” and the other a “behavioural strategy.”

A mixed strategy δ specifies the probability ( )p s with which each of the pure

strategies s∈S . Suppose the set of strategies is S =

{

s s sa, , then a mixed b, c, ...}

strategy can be represented as a vector of probabilities: δ =( ( ), ( ), ( ), ...)p sa p sb p sc .Consider a two player two action game with arbitrary payoffs:

P2

Invest Defer Invest (a, b) (c, d)

Defer (e, f) (g, h) P1

Usually, we will denote the probability of using the pure strategies s by p s ( ) for player 1, and q s( ) for player 2. The payoffs for mixed strategies are then given by

1 1 2 2 1 2 1 2 1 2 ( , ) ( ) ( ) ( , ) i s S s S i p s q s s s π δ δ π ∈ ∈ =

∑ ∑

× × (A.7) In this game, we look for a mixed strategies Nash equilibrium using the Equalityof Payoffs: let (δ1,δ2) be a Nash equilibrium, and let be the support of . Then . ∗ 1 S δ1∗ ) , ( ) , ( 1 δ2∗ =π δ1∗ δ2∗ πi s i ∀s∈S1∗ Then ) ( ) ( ) 1 ( ) 1 ( ) , ( ) , ( 2 1 2 1 a e g c g c q q g eq q c aq D I − + − − = ⇔ − + = − + ⇔ = ∗ ∗ ∗ ∗ ∗ ∗ ∗ π δ δ π and