Performance of Service-Node-Based Mobile

Prepaid Service

Ming-Feng Chang, Wei-Zu Yang, and Yi-Bing Lin, Senior Member, IEEE

Abstract—In the recent years, mobile prepaid service has be-come an important mobile application with rapid growth of sub-scription rate. The most widely deployed prepaid solution today is the service node approach that deducts and updates the prepaid credit during a phone call. Implementation of the service node ap-proach may generate large number of credit checks that signifi-cantly degrades the performance of a service node. We investigate how the number of credit checks affects the workload of the service node and the bad debt that a service provider may bear. We pro-pose an analytic model to derive the optimal credit checking/up-dating frequency for the service node approach. The analytic anal-ysis is validated against simulation experiments. Our study indi-cates that the number of credit checks increases rapidly when the call pattern is irregular. We also observe that in order to reduce the checking cost of the service node, the prepaid service provider should encourage the customer to make long calls by giving them discounts.

Index Terms—Global system for mobile communications (GSM), mobile phone network, prepaid service, service node.

I. INTRODUCTION

R

ECENTLY, the mobile prepaid service has become pop-ular. In USA, the prepaid calling market grew 56% to about two billion US dollars in 1998 and is expected to main-tain a high growth rate to 2005 [1]. By 2001, it is predicted that more than 40% global system for mobile communications (GSM) customers will subscribe to prepaid service [1]. At the end of 2003, mobile prepaid service will account for 62% of the cellular user base [2]. In Australia, Telstra started prepaid service with 100 000 customers and had exceeded the system capacity in early 1999 [3]. In Taiwan, FarEastone reported that more than 40% of their customers subscribed to prepaid service in May 1999.From the customer’s point of view, prepaid service provides an immediate service without a long-term contract or regular bills. From the system provider’s point of view, prepaid service enlarges the customer base and reduces operation overhead such as printing monthly bills and checking customer’s credit before providing service. In prepaid service, the revenue is received typically one and half month earlier than the postpaid service.

Manuscript received August 21, 2000; revised February 2, 2001. This work was supported in part by the MOE Program of Excellence Research under Con-tract 90-E-FA04-4, CCL/ITRI, Ericsson, FarEastone National Science Council under Contract NSC 90-2213-E-009-156, and the Lee and MTI Center for Net-working Research, NCTU.

The authors are with the Department of Computer Science and Infor-mation Engineering, National Chiao Tung University, Hsinchu, Taiwan, R.O.C. (e-mail: [email protected]; [email protected]; [email protected]).

Publisher Item Identifier S 0018-9545(02)02512-4.

In summary, prepaid service improves the cash flow for the op-erators, reduces the time of cost reclamation and increases the capability of competition.

Prepaid service works as follows. To initiate the prepaid ser-vice, a customer purchases a prepaid card from the operator. The prepaid card includes an associated directory number and the credit. The prepaid service is usually activated immediately or within a certain number of days after the initialization. When the customer originates a prepaid call, the corresponding charge is decremented from the remaining prepaid credit. Most prepaid systems have configured credit thresholds [4]. If customer’s bal-ance is below the threshold, the customer will hear a whisper tone reminding this person to recharge while he/she is talking.

Once the balance reaches zero, the customer cannot originate calls, but may be allowed to receive phone calls for a period (e.g., six months). Prepaid service can be reactivated by pur-chasing a top-up card to recharge the prepaid credit. The top-up card is like a scratch card with a secret code inside it. The cus-tomer dials a toll-free number and follows the instructions of an interactive voice response (IVR) to input the phone number and the secret code. The prepaid system verifies the secret code and refreshes customer’s account. On the other hand, if the balance remains zero for a period without being recharged, the prepaid system deletes the customer record and the customer cannot originate or receive any phone calls.

Four billing technologies are used in prepaid service: hot billing approach, service node approach, intelligent network (IN) approach and handset-based approach [5]. The hot billing approach uses call detail records (CDRs) produced by the wireless switch (i.e., mobile switching center) to process the prepaid usage. These records are generated after call comple-tions and are transported from the mobile switching center (MSC) to the prepaid service center. Hot billing approach is cost effective because it does not require major changes in the network infrastructure [6]. However, since a CDR can only be transmitted until the call is completed, the prepaid credit may become negative at the end of a phone call. This incurs the one call exposure problem that may cause large loss to the service providers.

In the handset-based approach, the prepaid credit and balance information is stored in the SIM card of a handset. In GSM handset-based prepaid service, during the call set-up or tariff switching, the MSC provides tariff parameters to the handset through the GSM phase 2 supplementary message AOC (advice of charge) [5]. The handset converts the AOC message into a sequence of SIM commands that modify the balance information in the SIM card. During the conversation, the handset decrements the prepaid credit on a real-time basis. 0018-9545/02$17.00 © 2002 IEEE

Fig. 1. Service node architecture for prepaid service.

Similar to the hot billing approach, the handset-based approach does not incur major modification to the carrier’s infrastructure. However, the prepaid system requires GSM phase-II-compliant handsets. This requirement restricts the market penetration. In addition, security is a serious problem with this approach. To eliminate the possibility of fraud, network needs to act as a backup to keep track of the prepaid credit usage.

The intelligent network approach is considered as a complete solution for the prepaid service. It migrates the service control and service development functions from the MSCs to the pre-paid service control point (P-SCP). The SCP contains service logic programs (SLPs) and associated data to provide IN ser-vices [7]. When an MSC encounters a prepaid call, it communi-cates with the P-SCP through SS7 links, asking the P-SCP to de-cide how the call should be processed. The P-SCP performs the service control functions (e.g., checking credit and activating a countdown timer) based on the customer’s credit and sends a re-sponse message back to the MSC. After receiving the message, the MSC performs the P-SCP instructions to accept or reject the prepaid call. Since the P-SCP is not on the voice path, the intelligent network solution allows real-time call control with low capacity expansion cost. However, not all carriers are inter-ested in implementing this approach because of the investment on P-SCP and the necessity for software modifications in all MSCs.

The service node approach is the most widely deployed pre-paid solution today and is viewed as a stepping-stone to the intel-ligent network approach. Compared with the intelintel-ligent network approach, the service node approach integrates the functions of the MSC and service control point (SCP) in a closed configura-tion [8]. The service node usually collocates with an MSC and is connected to the MSC using high-speed T1/E1 trunks. For each prepaid call, the MSC routes the call to the service node for call processing. After the service node performs the service control functions, the prepaid call is routed back to the MSC and then to the called party. If the called party is a wire-line tele-phone, then the MSC sets up a trunk to the switch (i.e., central office) in the PSTN. The PSTN switch performs call switching and connects to the wire-line telephone. Thus, to set up a mobile prepaid call, it requires two ports on the service node and four ports on the MSC. Since the service node is on the voice path, this approach allows real-time call control. However, the cost of capacity expansion in the service node approach is higher than that of the intelligent network approach. On the other hand, a

new signaling protocol is required in the IN approach to sup-port prepaid services. Upgrading all MSCs to supsup-port the new signaling protocol is expensive. Such a new protocol is not re-quired in the service node approach.

We have studied the hot billing approach in [9]. The com-parison of the four prepaid approaches can be found in [10]. This paper investigates the performance of the service node ap-proach and is organized as follows. Section II describes the call origination procedures of the service node approach. Section III presents the analytic model for the service node approach. Nu-meric results are presented in Section IV, and the conclusions are given in Section V.

II. THESERVICENODEAPPROACH

We use the GSM network as an example to illustrate the ser-vice node architecture and the prepaid call origination proce-dure. Fig. 1 depicts the architecture of the service node ap-proach. The service node, which controls the call processing for prepaid calls, can be viewed as an extended platform from the existing telecommunication network. Customer billing and ac-count information is stored in the prepaid billing platform (PBP) to support real-time call rating. When a customer subscribes to the prepaid service, the prepaid billing platform creates the sub-scriber record including the MS identities, amount of the pre-paid credit, the date of initialization and related authentication information. Prepaid service is activated within a short time after the service is subscribed. In the service node approach, the cus-tomers can interact with the IVR for service query and credit recharging. The IVR can also communicate with a customer when the prepaid credit is low.

The prepaid call origination procedure is illustrated in Fig. 2 and is described in the following steps.

Step 1) A prepaid customer originates a prepaid call by di-aling the called party’s phone number.

Step 2) The MSC identifies that the call is a prepaid call and routes the call to the service node.

Step 3) The service node requests the prepaid billing plat-form to verify if the customer has sufficient credit to make this call.

Step 4) If the call is granted, the service node activates a countdown timer for charging and sets up a trunk back to the MSC. Eventually, the call is routed from the MSC to its destination. During the conversation, the prepaid credit is decremented in real time at the

Fig. 2. The prepaid call origination procedure.

Fig. 3. Case i): The charges for prepaid calls where the last call is forced to terminate by the service node. service node according to the carrier-defined rate

plan.

Step 5) If the prepaid credit becomes negative before the end of the conversation, the call is forced to termi-nate by the service node. In this case, the call may be rerouted to the IVR to play announcements re-minding the customer to recharge the prepaid credit. Step 6) After the prepaid call completes, the credit is up-dated at the prepaid billing platform. In the low credit case, the IVR may also be instructed to play a warning message to the customer.

The service node checks and decrements the prepaid credit periodically during the conversation to avoid potential large bad debt. However, the capability of the service node may be lim-ited since all service control and call-switching functions are implemented on the service node. Theoretically by upgrading the processing power of the switch or service node, the service node will permit a real-time credit monitoring. However, in a real mobile phone network operation, the processing budget for a service node should be accurately planned. An example of pro-cessing budget planning for a telecommunication node can be found in [11]. In real operation, a service node may process over 10 000 prepaid calls simultaneously. To support real-time mon-itoring for so many simultaneously calls, the cost for upgrading processing power is too high, and is not justified. Thus, the op-erators always ask the following question: “What is the credit checking frequency so that the sum of the credit checking cost and the bad debt is minimized?” This paper utilizes analytic and simulation models to investigate the performance of the service node, and answers the above question. After the answer is found, the operator can choose the appropriate processing power for the service node so that it can support, say, over 10 000 simultane-ously prepaid calls at the selected credit checking frequency.

III. THEANALYTICMODEL

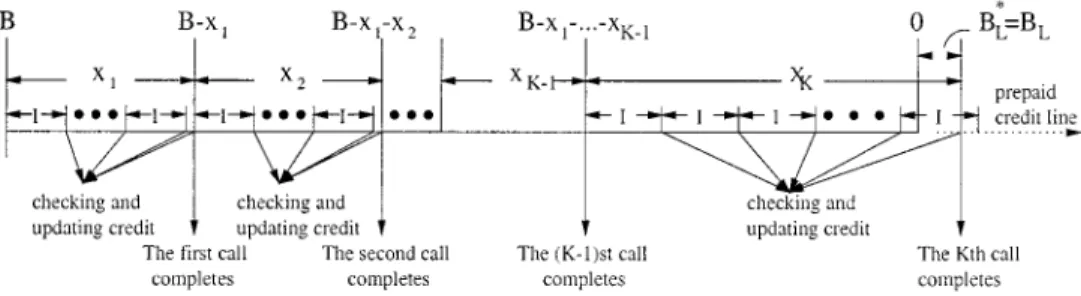

In this section, we propose an analytic model to derive the ex-pected number of credit checks ( ) and the expected bad debt ( ) in the service node approach. Let be the pre-paid credit and be the number of calls that a customer has made when the prepaid credit runs out. We assume that a cus-tomer will consume all the prepaid credit before he/she gives up the prepaid service. When a customer is in conversation, the ser-vice node periodically decrements the customer’s credit by the amount until either the call completes or the credit becomes negative.

Let be the charge of the th call. The

last (i.e., the th) call terminates in one of the two cases: Case i) The service node discovers that the prepaid credit

runs out by periodic checks and the call is forced to ter-minate (see Fig. 3).

Case ii) The last call completes before the service node dis-covers that the credit becomes negative (see Fig. 4). In Figs. 3 and 4, the horizontal line is the “prepaid credit line” that illustrates the decrement of the prepaid credit due to peri-odic credit checks during the calls (the vertical lines). For the derivation purpose, let be the charge of the last call if the service node would not terminate the call when the credit

be-comes negative. We assume that are

inde-pendent and identical random variables and the expected value . Let be the loss of the service provider and be the corresponding value if the last call were allowed to com-plete (i.e., the amount between when the credit is exhausted and when the call completes). Note that equals to in Case ii). Since the call holding times are independent and identically distributed, the call completion in the service node approach can be modeled by a renewal process [12]. Let be the

Fig. 4. Case ii): The charges for prepaid calls where the last call completes before the service node discovers that the credit becomes negative. expected number of credit checks assuming that the total credit

is . In this case, the th call is allowed to complete normally. Let be the expected number of credit checks for a call. Based on the Wald’s equation [12], can be expressed as

(1) Let be the expected number of credit checks in the service node approach (i.e., the expected number of credit checks when the total prepaid credit is ). From (1),

can be approximated as

(2) Let be the accumulated charge of the first calls. That

is, . Let and be

the density and distribution functions of , respectively. From the renewal theory [12, p. 100], the expected value can be derived as

(3) We consider two cases for prepaid credit : fixed credit and recharged credit. In the fixed credit case, is fixed. In the recharged credit case, a customer may recharge the prepaid credit several times before the customer gives up the prepaid service.

A. Fixed Credit Case

In the fixed credit case, the prepaid credit is a constant. In PCS services, the call holding times are usually assumed to be expo-nentially or Erlang distributed [13]–[15]. Erlang distribution is used so that we can obtain close form for the analytical model. Furthermore, Erlang distribution is more general than the expo-nential distribution, and it can be used to investigate the case when the variance of the call holding time distribution is small. Note that the effect of call dropped due to handover is already considered in the call holding times in our model. In a real PCS network, the measured call holding times include both complete calls and dropped calls.

Since the charge of a call is proportional to its call holding time, can be assumed to have an Erlang

den-sity function with mean and variance

(i.e.,

and

). Then, can be expressed as

(4)

From (3), can be expressed as

When is sufficiently large, an approximation for has been derived in [9]

(5)

From (5) and the Wald’s equation, with sufficiently large, can be expressed as

(6)

From (2) and (4)–(6), is approximated as

Next, we derive the expected loss of the service provider as follows. Let and be the probability that Case i) and Case ii) occur, respectively. Then, is expressed as

Let be the number of credit checks of the last call. The expected bad debt of the service provider in Case i) can be expressed as

Case i)

(8) where is the density function of the charge of accu-mulated calls and

(9)

(10) and

(11) The term represents a trivial situation in Case i) where the first call consumes all prepaid credit (i.e., ). The loss of the service provider is . The terms and represent the situation where a customer has made

complete calls before prepaid credit runs out. Since the last call is forced to terminate at the th credit check, the bad debt of the service provider is . The term represents the situation in Case i) where . The call charge of the last call is larger than and the total

charge of prior calls satisfies .

The term represents the special situation in Case i) where and the total charge of prior calls satisfies . From (28)–(30) in Appendix I, , and are expressed as

(12)

(13)

Using a similar approach as above, the expected bad debt in Case ii) can be expressed as

Case ii)

(15)

where , and are

(16)

(17) and

(18) From (31)–(33) in Appendix II, , , and are expressed as

(19)

(21)

When , is exponentially distributed. From (7), (8), (12)–(15), (19)–(21) with , can be expressed as

(22)

B. Recharged Credit Case

In the recharged credit case, a customer may recharge his/her prepaid card before the credit runs out. At the beginning, a cus-tomer purchases an initial credit and then recharges his/her credit several times. Let be the amount of single recharged credit and be the number of recharges that a customer has made before he/she gives up the prepaid service. We assume that is a geometric random variable with the parameter (i.e., is the recharge probability). Then, the probability mass function of is expressed as

The prepaid credit equals to and its expected

value equals to . First, we consider

the case where the call charge has an Erlang distribution with

mean and variance . To derive

, we assume that the last call is allowed to complete normally. The probability that calls are completed before total credit runs out given can be expressed as

(23)

From (36) in Appendix III, (23) can be expressed as

Thus, can be expressed as

(24)

From (24), can be expressed as

(25) From (2), (4), (24), and (25), can be approximated as

Using a similar approach as the fixed credit case [see (8)], the expected bad debt in Case i) can be expressed as

Case i) (26)

Similar to the fixed credit case [see (15)], the expected bad debt in Case ii) can be expressed as

TABLE I

COMPARISON OFANALYTIC ANDSIMULATIONMODELS(FIXEDCREDITCASE,

E[x ] = NT$36, V ar[x ] = 1296, I = NT$12)

TABLE II

COMPARISON OFANALYTIC ANDSIMULATIONMODELS(RECHARGED

CREDITCASE,E[B] = NT$500, B = NT$100, p = 2=3; E[x ] = NT$36,V ar[x ] = 1296)

From (7), (8), and (15) and (26) and (27), can be ex-pressed as

IV. NUMERICEXAMPLES

This section investigates the performance of the service node approach based on the analytic model developed in the previous section. Simulation experiments have been conducted to vali-date the analytic results. Each simulation experiment was re-peated 500 000 times to ensure stable results. To reflect the situ-ation of prepaid service in Taiwan, the expected charge of a call is assumed to be NT$36, and the expected prepaid credit are NT$100, NT$300, NT$400 and NT$500. Tables I and II com-pare the results of analytic and simulation models. The tables indicate that the analytic results are consistent with the simula-tion results.

A. Effects of the Variation of Call Charges

This subsection studies the effect of the variation of call charges on and for fixed credit and recharged credit cases. The call charge is assumed to have a Gamma distribution. The Gamma distribution is selected because it has been widely used in the PCS studies [14] and can be shaped to represent many distributions. A Gamma distribution has the density function

for

where ( ) is the shape parameter, ( ) is the scale

param-eter and . The mean of Gamma

distri-bution is and the standard derivation is . Let be the coefficient of the variation of call charge; equals to the ratio of the standard derivation to the mean of the distribution. For Gamma distribution, . In our experiment, ranges from to 10. A large represents that there are more short calls and long calls.

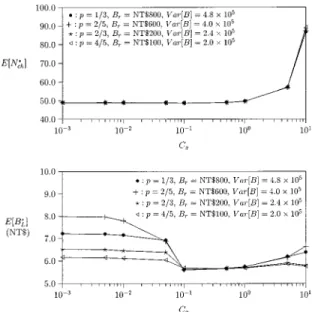

Fig. 5. Effects ofC in the fixed credit case (B = NT$500, I = NT$12).

Fig. 6. Effects ofC in the recharged credit case (E[B] = NT$500, B = NT$100,E[x ] = NT$36 and I = NT$12).

In both fixed credit (see Fig. 5) and recharged credit (see Fig. 6) cases, the service node periodically checks and updates prepaid credit with NT$12. The coefficient of variation ranges from 10 to 10 . In the fixed credit case, the prepaid credit equals to NT$500. The call charges have a gamma dis-tribution with mean NT$38, NT$37.2, NT$37, NT$36 and NT$35, respectively. In the recharged credit case, the ini-tial prepaid credit NT$100 and the mean of prepaid credit is NT$500. The number of recharges is assumed to have a geometric distribution and the recharge probability varies as 1/3, 2/5, 2/3 and 4/5. In this experiment, we only present the results where the call charges have a gamma distribution with mean NT$36. Similar conclusions can be drawn for with various means.

Both figures show that for , and

are sensitive to , but insensitive to . We explain this phenomenon in Appendix III. The figure also shows that

Fig. 7. Effects ofI on E[B ]=I (E[x ] = NT$36).

when , increases sharply in both fixed credit and recharged credit cases. The reason is that when increases, the number of short calls, whose call charges are less than , also in-creases. For each short call, a small amount of credit ( ) is consumed and a credit check is required. As a result, the number of credit checks increases as the number of short calls increases. We call this the short call effect. To avoid this effect, the prepaid service provider can implement billing policies to discourage short calls (e.g., higher rates in the first minute of a prepaid call and lower rates for the remaining call holding time).

B. Effect of on

Fig. 7 plots as a function of in the fixed credit case. The mean of call charges is NT$36 and ranges from NT$0.2 to NT$36. In this experiment, we consider two scenarios where NT$400 and NT$500, respectively.

Intuition suggests that would be equal to . How-ever, the figure shows that is equal to 1/2 when

and is sufficiently small (e.g., NT$0.2). It is inter-esting to note that when , almost linearly decreases as increases. The reason is that as increases, the probability that the th call terminates normally (rather than be forced to terminate by periodical checks) increases. Thus, the expected loss becomes smaller than . We also ob-serve that when is large (e.g., ), appears to vary with an irregular pattern. As increases, the number of small and large also increases. When is large, the proba-bility that the last call depletes all or most of the credit becomes large. For the same , the bad debt depends on the values of and . We can see that the pattern of variation in Fig. 7(a) and (b) are different when .

C. The Cost Function

Two costs are associated with the service node: the credit checking/updating cost and the bad debt. The credit checking cost and the bad debt are two conflicting factors, since smaller represents smaller and larger . Consider a cost

function , where is the credit checking

cost of the service node. The cost provides the net effect of credit checking cost and bad debt. Fig. 8 plots as a function

of and , where NT$36 and . Both

fixed credit and recharged credit cases are considered in this ex-periment. The triangle in the curves represents the cost for the optimal .

Fig. 8. The cost function C (E[x ] = NT$36, V ar[x ] = 1296). Consider the fixed credit case where NT$500. For

, the credit checking cost is high and NT$6 should be selected. For , the credit checking cost is low and NT$1 should be selected. In addition, for the same , the value of optimal increases as increases. Although the above re-sults are intuitive, our analysis quantitatively computes the pre-paid service overhead to select the optimal checking interval according to the capability of the service node. For the examples in Fig. 8 (which are consistent with the real network operation), acceptable values range from NT$1 to NT$6.

V. CONCLUSION

This paper studied the service-node based approach for the prepaid service. We described the system architecture and the procedures for call origination. An analytical model was pro-posed to analyze the performance in the fixed credit and the recharged credit cases. The analytic results were validated by simulation experiments. We observed the following results:

• If the call pattern of a prepaid customer is very irregular (i.e., many short calls and many long calls), it is desir-able that more credit checks will be needed on the ser-vice node. To avoid large number of credit checks on the service node, the service provider can implement billing policies to discourage short calls (e.g., higher rates in the first minute of the prepaid call and lower rates for the re-maining call holding time).

• Intuition suggests that the expected bad debt approximates to half of the amount of one credit check. However, our results show that it is incorrect when the variation of call charge is high or the amount of single credit check is large. • A cost function was used to determine the minimal cost for the service-node-based approach. The minimal cost can be achieved by properly setting the credit checking/updating interval to balance the workload of the service node with

the bad debt. This optimal interval of credit checking can be determined by using our modeling technique.

APPENDIX I

DERIVING [ CASEI)]FOR THEFIXEDCREDIT AND ERLANGCALLCHARGECASE

This appendix derives Case i) for the fixed credit and Erlang call charge case. From (9), is expressed as

(28)

From (10), is expressed as

(29) From (11), is expressed as

(30)

From (8) and (28)–(30), Case i) can be obtained. APPENDIX II

DERIVING [ CASE II)]FOR THEFIXEDCREDIT AND ERLANGCALLCHARGECASE

This appendix derives Case ii) for the fixed credit and Erlang call charge case. From (16), is expressed as

(31)

(32)

(33)

From (15) and (31)–(33), Case ii) can be obtained. APPENDIX III

DERIVING FOR

THERECHARGEDCREDITCASE This appendix derives

for the recharged credit case. From (23), is expressed as

(34)

From [9], [16]

(35)

From (35), (34) can be rewritten as

(36)

APPENDIX IV

EXPLAINING THEPHENOMENONTHAT AND

AREINSENSITIVE TO THEVARIATION OFCALLCHARGEWHEN

This section explains that and are insensitive to in the fixed credit and recharged credit cases when

(i.e., see Figs. 5 and 6). First, we illustrate the effect of on in the fixed credit case. When is sufficiently small, the call charges can be considered as fixed. Let be the remaining credit after a customer has made complete calls. Then, we observe that can be approximated by the following equation

(37)

When is sufficiently small, equals to

and can be approximated by . If

cannot divide , then can be approximated

by . Otherwise, can be approximated by

. The reason is that when is sufficiently small, the values of fall in a small interval which is symmetric to . Half of the calls whose call charges are smaller than require credit checks. The other calls whose

call charges are larger than require credit checks. From (37), can be approximated as

if cannot divide

if divides .

(38)

Next, we illustrate the effect of on in the fixed credit case. When , if cannot divide , can be approximated by . Otherwise, if divides

, the zero credit line falls into either just before the service node is going to check the credit or after a credit check has just occurred. The bad debt approximates 0 or , accordingly. Thus, can be approximated as

if cannot divide if divides .

(39)

One can verify that the approximations in (38) and (39) are con-sistent with the results shown in Fig. 5.

In the recharged credit case, let the number of recharge of a customer be and the number of credit checks be . Then, the prepaid credit equals to . When

, can be approximated by (38). We observe that the expected number of credit checks in the recharged credit

case can be approximated by .

Let be the bad debt of the customer who has

recharged for times. When , can

be approximated by (39). Thus, in the recharged credit case,

can be approximated by .

These approximations are consistent with the results in Fig. 6. ACKNOWLEDGMENT

The authors would like to thank the anonymous reviewers for their valuable comments that have significantly improved the quality of this paper.

REFERENCES

[1] L. V. Tracey, “Prepaid calling: Market update,” Telecommun., Apr. 1999. [2] J. Martin, “Wireless prepaid billing: A global overview,” Telecommun.,

Sept. 1999.

[3] J. Stokes, “The prepaid frenzy,” Mobile Commun. Asia, p. 19, Feb. 1999. [4] F. Slavick, “Prepay it again, Sam,” Billing World, Jan. 1999.

[6] A. Arteta, “Prepaid billing technologies—Which one is for you?,”

Billing World, pp. 54–61, Feb. 1998.

[7] U. Black, The Intelligent Network: Customizing Telecommunication

Networks and Services. Englewood Cliffs, NJ: Prentice-Hall, 1998. [8] R. Pilcher, “Intelligent networks move advanced services ahead,”

Telecommun., Nov. 1998.

[9] M.-F. Chang, Y.-B. Lin, and W.-Z. Yang, “Performance of hot billing mobile prepaid service,” Comput. Networks J., vol. 36, no. 2, pp. 269–290, July 2001.

[10] Y.-B. Lin, C. H. R. Rao, and M.-F. Chang, “Mobile prepaid phone ser-vices,” IEEE Personal Commun. Mag., vol. 7, no. 3, pp. 6–14, Jun. 2000. [11] Y.-B. Lin and I. Chlamtac, Wireless and Mobile Network

Architec-tures. New York: Wiley, 2001.

[12] S. M. Ross, Stochastic Processes. New York: Wiley, 1983.

[13] R. Guerin, “Channel occupancy time distribution in a cellular radio system,” IEEE Trans. Veh. Technol., vol. 36, pp. 89–99, Aug. 1987. [14] Y.-B. Lin, “Performance modeling for mobile telephone networks,”

IEEE Network Mag., vol. 11, no. 6, pp. 63–68, Nov./Dec. 1997.

[15] Y.-B. Lin and I. Chlamtac, “Effects of Erlang call holding times on PCS call completion,” IEEE Trans. Veh. Technol., vol. 48, pp. 815–823, Mar. 1999.

[16] J. Riordan, “Combinatorial identities,” Rockefeller Univ., 1968.

Ming-Feng Chang received the Ph.D. degree in computer science from the University of Illinois at Urbana-Champaign, in 1991.

He is currently an Associate Professor in the De-partment of Computer Science and Information En-gineering, National Chiao-Tung University, Taiwan, R.O.C. His research interests include internet com-munication, mobile computing, and VLSI system de-sign. His current research projects include “VoIP for Wireless Networks,” “Interworking of VoIP Proto-cols,” and “Cache Model for WAP Applications.”

Wei-Zu Yang received the M.S. degree from the De-partment of Computer Science and Information En-gineering, National Chiao Tung University, Taiwan, R.O.C., in 1992. He is currently working toward the Ph.D. degree at the same university.

His research interests include performance mod-eling of PCS and ATM networks.

Yi-Bing Lin (SM’01) received the B.S.E.E. degree from the National Cheng Kung University in 1983, and the Ph.D. degree in computer science from the University of Washington, Seattle, in 1990.

From 1990 to 1995, he was with the Applied Research Area at Bell Com-munications Research (Bellcore), Morristown, NJ. In 1995, he was appointed as a Professor in the Department of Computer Science and Information Engi-neering (CSIE), National Chiao Tung University (NCTU), Taiwan, R.O.C. In 1996, he was appointed as Deputy Director of Microelectronics and Informa-tion Systems Research Center, NCTU. From 1997 to 1999, he was elected as Chairman of CSIE, NCTU. He is an Editor of Computer Networks, an Area Ed-itor of ACM Mobile Computing and Communication Review, a Columnist of

ACM Simulation Digest, and an Editor of the International Journal of Commu-nications Systems, ACM/Baltzer Wireless Networks, Computer Simulation Mod-eling and Analysis, and the Journal of Information Science and Engineering. He

was Guest Editor for the ACM/Baltzer MONET Special Issue on Personal Com-munications. He is the coauthor of Wireless and Mobile Network Architecture (New York: Wiley). His current research interests include design and analysis of personal communications services network, mobile computing, distributed simulation, and performance modeling.

Dr. Lin is an Associate Editor of IEEE NETWORK, an Editor of IEEE JOURNAL ONSELECTED AREAS OFCOMMUNICATION: WIRELESSSERIES, and an Ed-itor of IEEE Personal Communications Magazine. He was a Guest EdEd-itor for IEEE TRANSACTIONS ONCOMPUTERSSpecial Issue on Mobile Computing and for IEEE Communications Magazine—Special Issue on Active, Programmable,

and Mobile Code Networking. He was Program Chair for the 8th Workshop on Distributed and Parallel Simulation, General Chair for the 9th Workshop on Dis-tributed and Parallel Simulation, and Program Chair for the 2nd International Mobile Computing Conference. He received the 1998 and 2000 Outstanding

Re-search Awards from the National Science Council, R.O.C., and the 1998 Out-standing Youth Electrical Engineer Award from CIEE, R.O.C. He is an Adjunct Research Fellow of Academia Sinica.

![Fig. 7. Effects of I on E[B ]=I (E[x ] = NT$36).](https://thumb-ap.123doks.com/thumbv2/9libinfo/7749615.148630/10.918.461.822.89.466/fig-effects-i-e-b-i-e-nt.webp)