銀行與存戶之存款契約的賽局模型 ─兼論銀行擠兌的經濟分析 - 政大學術集成

27

0

0

全文

(2) Abstract Title: A Game Theoretic Model of Deposit Contracts between the Bank and the Depositor Extend Study on the Economic Analysis of Bank Run School: Graduate Institute of Public Finance National Chengchi University Author: Chiao-Hsin Lin Keywords: Deposit contract; Bank run; Lender; Signal; Subgame perfect equilibrium. This paper which extends the settings of Chen and Hasan (2008) uses the game theoretic. 政 治 大. model to focus on the topics of not only interactive policies between a bank and a depositor. 立. but bank runs. Our study discovers that depending on different economic terms, the bank will. ‧ 國. 學. probably propose two different deposit contracts for depositor to accept or not. After the acceptance of the deposit contract, the depositor will choose his withdrawal time on the basis. ‧. of different liquidity preferences. On the other hand, bank runs occur only when one of the. y. Nat. n. Ch. engchi. 1. er. io. al. disclosed to depositors.. sit. deposit contracts is proposed and the negative information of the investment project is. i n U. v.

(3) 摘要. 本文延伸 Chen and Hasan (2008) 之設定,使用賽局模型討論銀行與存戶互動決 策及銀行擠兌之議題。本研究發現於不同的經濟條件下,銀行可能提出兩種不同的均衡 存款契約以供存戶接受與否。待存戶接受該存款契約後,存戶根據其流動性偏好型態選 擇其提領時間。另一方面,銀行擠兌只可能發生在其中一種存款契約且負面訊息揭露給 存戶之情況。. 政 治 大. 關鍵詞:存款契約、銀行擠兌、子賽局完全均衡. 立. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 2. i n U. v.

(4) CONTENTS. 1. 2. 3.. Introduction .................................................................................................................... 4 The Model ....................................................................................................................... 7 The Equilibrium ........................................................................................................... 10 14. 【Lemma 1】. 【Proposition 1】 18 4.. Bank Run ...................................................................................................................... 21 【Proposition 2】 21 【Corollary 1】. 22. 5. Concluding Remark ..................................................................................................... 24 References ............................................................................................................................. 26. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 3. i n U. v.

(5) 1. Introduction Since the outbreak of the 1997 Asian financial crisis, Hong Kong's Bank of East Asia (abbreviated to BEA) firstly suffered a bank run on September 22, 2008. The event resulted from that people spread malicious rumors about BEA’s stability via Short Message Service (SMS). They told the stories that BEA was encountering financial difficulties because of the capital losses from investment in Lehman bonds and American International Group (AIG). BEA was said to be taken over by the government of Hong Kong. Then Deputy Chief Executive of BEA issued a statement. 政 治 大 mongers were an attempt to undermine the stability of the financial system. However, 立 to clarify that the financial position of BEA was healthy and indicated that the rumor. queues of depositors sought to withdraw money from banks. To solve the problem of. ‧ 國. 學. bank run, the Chief Executive Officer of BEA clarified again and the monetary. ‧. authority of Hong Kong and the Financial Secretary were publicly behind BEA and. io. er. ultimately subsided on September 25, 2008.. sit. y. Nat. guaranteed the safety and soundness of the banking system. This event thus. Some literature studies about the issue of bank runs. Diamond and Dybvig. n. al. (1983) point out that under. v i n C hdeposit insuranceUsystem, the engchi. bank will provide a. superior deposit contract. And such a deposit contract will be likely to prevent the occurrence of bank runs. Chari and Jaganathan (1988) find that a bank run is induced by adverse information of the bank and the properties of information about the underlying investment returns will influence the choice between deposit contracts or equity contracts in the absence of deposit insurance system. Cooper and Ross (1998) indicate that the banks cope with its deposit contract design and investment decisions according to the probability of bank run. Besides, banks may provide a deposit contract to prevent bank runs. But under certain conditions, banks will choose a deposit with the risk of bank runs in order to get a higher expected return from the 4.

(6) investments. Chen (1999) finds that on the condition of sequential service constrains and information asymmetry, the negative information from few banks may lead to large-scale panic run even to the collapse of the entire financial system. Samartín (2003) points out that bank runs are likely to be induced by message or panic. The deposit contract can be properly designed to avoid bank runs. But in some cases, the bank run may generate more benefits. Goldstein and Pauzner (2005) modify the model of Diamond and Dybvig (1983) and find that when the bank improves overall welfare and designs a deposit contract, there will be a trade-off between the trading. 政 治 大 contract. Alonso (1996) analyzes the banking environment and finds that negative 立. liquidity benefits and the costs of a bank run which are both brought from the deposit. information about the investment performance of the bank may lead to bank runs.. ‧ 國. 學. Banks can prevent the occurrence of bank runs by designing appropriate deposit. ‧. contracts. In some cases, avoiding bank runs can maximize the profits of the banks.. sit. y. Nat. However, the occasional runs can be the optimum bank behavior in other cases. Chen. io. er. and Hasan (2006) indicate that increasing the information transparency of banks will make higher incidence of infectious runs, thereby reducing depositors’ welfare. They. al. n. v i n also point out that it can reduceC the incidence of runsU h e n g c h i if the deposit insurance system. is designed as that some depositors are fully insured and the others are partially insured. Ennis and Keister (2006) point out that the bank will provide a deposit contract with risk of runs when the incidence of runs is very small. In the case of not preventing bank runs, the bank will choose to hold an amount of reserves just equal to the demand of withdrawal. When the cost of early liquidating investment is high, a rise in the incidence of runs may lead the bank to reduce the investment. Chen and. Hasan (2008) use the symmetric pure-strategy subgame-perfect equilibrium to explain why the bank run is caused by depositors’ panic. They note that in large-scale bank runs, the depositors were often unable to distinguish between good banks and 5.

(7) bad banks, so they swarm into banks to withdraw. Maeda and Sakai (2008) propose that basing on the lender of last resort theory (LLR), the original deposit contract resulting in bank runs may make allocation of funds more efficient because the central bank can provide liquidity supply for banks with insufficient liquidity. The model established by Chen and Hasan (2008) assumes that the bank makes zero economic profit and is in a passive position. Depositors make strategic decisions against changes in the economic environment, while the bank does not fight for its own interest. This is more like a model in which the depositor makes decision by. 政 治 大 which there is an interaction between the bank and the depositor. There are two types 立. himself. We modify the setting of Chen and Hasan into a competitive game model in. of depositors who will make decisions for profit maximization separately. We. ‧ 國. 學. establish a decision-making phase to solve for the equilibrium. The conclusion is that. ‧. according to different economic terms, there will be two different deposit contracts. sit. y. Nat. proposed by the bank. And the depositor will choose withdrawal time in light of his. io. er. liquidity preference. Moreover, we find that only one of these two contracts will bring about bank runs when the depositors receive the negative information of the. al. n. v i n investment project. This paper C can provide the otherU h e n g c h i angle for viewing the issue of bank runs.. The structure of the paper is organized as follows: Section 1 is the introduction. Section 2 describes the settings of our model. Section 3 solves for the equilibrium. Section 4 discusses bank runs. Concluding remarks are in Section 5.. 6.

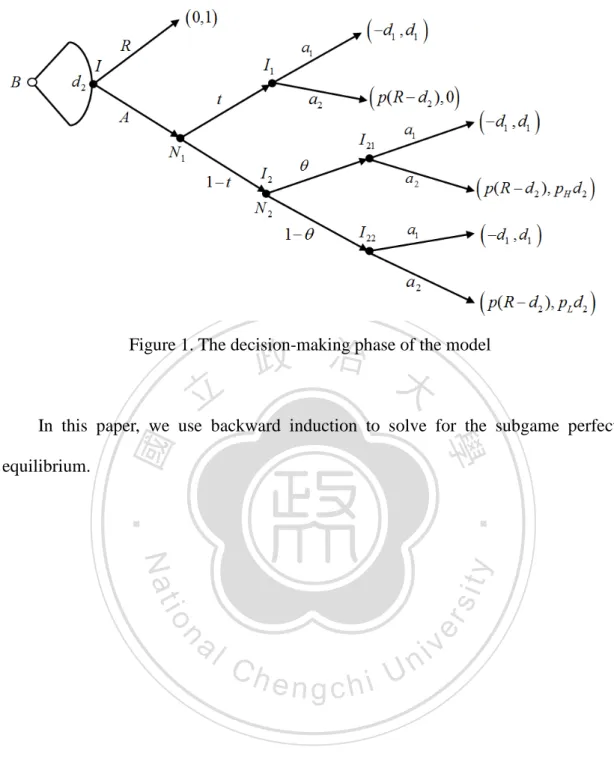

(8) 2. The Model The settings of this paper are mainly base on and thereby modified from the theoretical model of Chen and Hasan (2008). 1. . Suppose there are three. decision-making dates (date 0, 1, and 2), besides a bank and a risk-neutral depositor existing in the society. At period 0, the depositor possesses a unit of endowment, then choosing whether he saves the endowment at the bank or not. In the meanwhile, the bank provides a deposit contract d 2 (i.e., the bank will gives the depositor d 2 when the contract matures at period 2, yet the depositor will get d1 , if he. 政 治 大. withdrawals at period 1 in advance, and we continue the settings of Chen and Hasan. 立. (2008), d 2 > d1 > 1 ) to attract the depositor. If the depositor rejects the deposit. ‧ 國. 學. contract, he still retains the original endowment, while the bank gets no return, and. ‧. finally the game ends; if the depositor accepts the deposit contract, then the Bank. sit. y. Nat. may use the funds to carry out an investment plan. This investment plan expires at. io. er. period 2, one of its expected returns is R with probability p , yet the other is 0 with probability (1- p ) . Suppose the plan’s expected rate of return pR > 1 , and if. n. al. Ch. engchi. i n U. v. the bank liquidates the investment at period 1, liquidation value of this investment plan is 0. In order to discuss the liquidity needs the depositor may face, assume that before the end of period 1, the depositor will divide into two types. It means that he will become type 1 with probability t , who must consume at period 1 to get utility, or will get no consumer utility at period 2, while the remaining probability (1 − t ) is. 1. The biggest difference between our paper and Chen and Hasan (2008) is that the bank in our model. can actively choose the size of. d1 and d 2 to maximize its profits, and only one depositor is set to. divide into two types to discuss his interactive decisions with the bank. Nevertheless, the banking system in Chen and Hasan (2008) is perfectly competitive, so the bank’s decision making is relevant to market zero-profit condition, and there are large numbers of the depositors who divide into two types. 7.

(9) type 2, who has no need for liquidity at period 1. Assume that depositor does not know his type at period 0, and the depositor of type 2 will receive a public signal s concerning p at period 1. The public signal s is of positive information H with probability θ , and is of negative information L with probability (1 − θ ) , where. θ ∈ (0,1) . The probability is pH ≡ pq / [ pq + (1 − p )(1 − q )] when the expected return is R caused by s = H , while pL ≡ p (1 − q )/[p (1 − q ) + (1 − p )q ] is the probability when a return is R caused by s = L , where q ∈ (1/ 2,1) is the precision of the signal s resulting in pL ≤ p ≤ pH . 2 In Figure 1 we display the. 政 治 大. above-described problems are in a decision-making phase, which the action of the. 立. depositor withdrawing in period 1 is a1 , while in period 2 is a2 . On the other hand,. ‧ 國. 學. we do not introduce an insurance system in the discussion, that is, once banks fails in the investment plan, the depositor will receive no reward. According to the above. ‧. description, if the depositor withdraws at period 1, the depositor gets d1 , while the. sit. y. Nat. io. n. al. er. bank pays −d1 ; if the depositor withdraws at period 2, the bank will get p( R − d 2 ) ,. i n U. v. the depositor of type 1 will get no utility because of not satisfied his liquidity needs,. Ch. engchi. and the depositor of type 1 will get pH d 2 and pL d 2 respectively based on the quality of the signal.. 2. The settings of. pH and pL are similar with Chen and Hasan (2008). 8.

(10) 政 治 大. Figure 1. The decision-making phase of the model. 立. In this paper, we use backward induction to solve for the subgame perfect. ‧. ‧ 國. 學. io. sit. y. Nat. n. al. er. equilibrium.. Ch. engchi. 9. i n U. v.

(11) 3. The Equilibrium At the decision point I 21 , after the depositor of type 2 receives the signal of positive information H , the expected utility of his withdrawal in period 2 (i.e., taking action a2 ) is:. pH d 2 ≡. pq d2 pq + (1 − p )(1 − q ). (1). Compare equation (1) with the utility d1 of the depositor of type 2 withdrawing in period 1 (i.e., taking action a1 ), we suppose pqd 2 /[ pq + (1 − p )(1 − q )] is not less. 政 治 大. than d1 , meaning he will withdraw in period 2 after receiving the signal of positive. 立. information H . 3. ‧ 國. 學. At the decision point I 22 , after the depositor of type 2 receives the signal of. ‧. negative information L , the utility of taking action a2 is:. p (1 − q ) d2 p (1 − q ) + (1 − p )q. sit. (2). er. io. al. y. Nat. pL d 2 ≡. n. Compare equation (2) with the utility d1 of the depositor of type 2 taking action. Ch. engchi. i n U. v. a1 , we get when p (1 − q )d 2 /[ p (1 − q ) + (1 − p )q ] is more (less) than d1 , he will withdraw in period 2(1). Then at the decision point I1 , the utilities of the depositor of type 1 taking action a2 and a1 are 0 and d1 respectively, so he will take action a1 . Nevertheless, at the decision point I 2 , we will discuss it in two situations. Situation 1 is that the depositor of type 2 chooses to withdraw in period 1 after receiving the signal of negative information L , and in the meanwhile his expected utility is 3. The assumption that the depositor of type 2 chooses to withdraw at period 2 after receiving positive information, is mainly to avoid the condition that two types of the depositor both withdraw at period 1. 10.

(12) θ pH d 2 + (1 − θ )d1 . Under such situation, giving deposit contract d 2 the bank proposes, the expected utility of the depositor accepting the contract (i.e., taking action A ) is: td1 + (1 − t )[θ pH d 2 + (1 − θ )d1 ] = td1 + (1 − t )[. θ pqd 2 pq + (1 − p )(1 − q ). + (1 − θ )d1 ]. (3). Compare equation (3) with the utility 1 of rejecting the deposit contract (i.e., taking action R ), we get when td1 + (1 − t ){[θ pqd 2 ] /[ pq + (1 − p)(1 − q)] + (1 − θ )d1 } is more (less) than 1, he will accept (reject) the contract. Furthermore, situation 2 is that. 政 治 大. the depositor of type 2 chooses to withdraw in period 2 after receiving the signal of. 立. L , and in the meanwhile his expected utility is. 學. ‧ 國. negative information. θ pH d 2 + (1 − θ ) pL d 2 . Under such situation, giving deposit contract d 2 the bank. θ pqd 2. io. = td1 + (1 − t )[. pq + (1 − p )(1 − q ). al. +. y (1 − θ ) p (1 − q )d 2 ] p (1 − q ) + (1 − p )q. sit. td1 + (1 − t )[θ pH d 2 + (1 − θ ) pL d 2 ]. er. Nat. action A ) is:. ‧. proposes, the expected utility of the depositor accepting the contract (i.e., taking. (4). n. v i n C h 1 of rejecting theUdeposit contract, we get when Compare equation (4) with the utility engchi td1 + (1 − t ) pd 2 {[θ q] /[ pq + (1 − p)(1 − q)] + [(1 − θ )(1 − q)] /[ p(1 − q) + (1 − p) q]}. is. more (less) than 1, he will accept (reject) the contract. Finally, back to the decision point I , the bank proposes a deposit contract d 2 to attract the depositor. The depositor of type 1 must withdraw in period 1, while after receiving negative information the depositor of type 2 also withdraws in period 1 under situation 1, yet withdrawing in period 2 under situation 2. From now on, we define the expected utility of the bank under situation 1 as VB1 :. 11.

(13) VB1 ≡ t (−d1 ) + (1 − t )[θ p ( R − d 2 ) + (1 − θ )(−d1 )]. (5). And the expected utility of the bank under situation 2 is defined as VB 2 :. VB 2 ≡ t (−d1 ) + (1 − t )[θ p ( R − d 2 ) + (1 − θ ) p ( R − d 2 )]. (6). From equation (6), we can simplify VB 2 into t (−d1 ) + (1 − t ) p ( R − d 2 ) . Because the operation purpose of the bank is profit maximization, the following below is the subgame perfect equilibrium under two situations to separately maximize VB1 and. VB 2 .. 政 治 大 First, according to the assumption above, no matter under which situation, at the 立. ‧ 國. 學. decision point I 21 , the depositor of type 2 will withdraw in period 2 after receiving the signal of positive information H , that is. pq + (1 − p )(1 − q ) d1 pq. sit. (7). er. io. al. y. Nat. d2 ≥. ‧. transposed into:. pqd 2 /[ pq + (1 − p )(1 − q )] ≥ d1. n. If situation 1 holds, at the decision point I 22 , the term of the depositor of type 2. Ch. engchi. i n U. v. withdrawing in period 1 after receiving the signal of negative information L is. p (1 − q )d 2 /[ p (1 − q ) + (1 − p )q ] ≤ d1 , meaning:. p (1 − q ) + (1 − p )q d1 ≥ d 2 p (1 − q ). (8). Combine equation (7) and equation (8), and we can arrange the inequality as:. p (1 − q ) + (1 − p )q pq + (1 − p )(1 − q ) d1 ≥ d 2 ≥ d1 p (1 − q ) pq. (9). It means the below conditions must be fulfilled:. p (1 − q ) + (1 − p )q pq + (1 − p )(1 − q ) d1 ≥ d1 p (1 − q ) pq We subtract the above two equations as: 12. (10).

(14) p (1 − q ) + (1 − p )q pq + (1 − p )(1 − q ) d1 − d1 p (1 − q ) pq =. =. pq (1 − q ) + (1 − p )q 2 − pq (1 − q ) − (1 − p )(1 − q ) 2 d1 pq (1 − q ). (1 − p )[q 2 − (1 − q) 2 ] d1 pq (1 − q ) (1 − q ). (11). Because of q ∈ (1/ 2,1) , the term of (1 − p )[q 2 − (1 − q ) 2 ] /[ pq (1 − q ) ] > 0 is fulfilled. Next, at the decision point I , given deposit contract d 2 , the term of the depositor. 政 治 大. accepting the contract is td1 + (1 − t ){[θ pqd 2 ] /[ pq + (1 − p )(1 − q )] + (1 − θ )d1 } ≥ 1 ,. 立. meaning:. {1 − [1 − θ (1 − t )]d1 }[ pq + (1 − p )(1 − q )] (1 − t )θ pq. ‧ 國. 學. d2 ≥. (12). {1 − [1 − θ (1 − t )]d1 }[ pq + (1 − p )(1 − q )] (1 − t )θ pq. Ω1 ≡. pq + (1 − p )(1 − q ) d1 pq. Ω2 ≡. p (1 − q ) + (1 − p )q d1 p (1 − q ). sit. n. er. io. al. y. Nat. Ω0 ≡. ‧. We make the following definition for the convenience of mathematical symbols:. Ch. engchi. i n U. v. Equation (9) and equation (12) combined, the terms that d 2 is not less than Ω0 and d 2 ∈ [Ω1 , Ω 2 ] must be fulfilled under situation 1. We can see the term of equation (10), Ω 2 − Ω1 > 0 , is definitely fulfilled in the foregoing. Under Ω 2 − Ω1 > 0 definitely fulfilled, the terms, that d 2 must not less than Ω0 and. d 2 ∈ [Ω1 , Ω 2 ] , make Ω 2 − Ω0 ≥ 0 have to be fulfilled. In the foregoing we suppose d1 > 1 , so Ω1 > Ω0 ,and Ω 2 − Ω0 ≥ 0 will be fulfilled. Because the bank will lower d 2 as far as possible to reap more benefits, we get d 2 = Ω1 under situation 1. 13.

(15) If situation 2 holds, at the decision point I 22 , the term of the depositor of type 2 withdrawing in period 2 after receiving the signal of negative information L is. p (1 − q )d 2 /[ p (1 − q ) + (1 − p )q ] ≥ d1 , meaning:. p (1 − q ) + (1 − p )q d1 ≤ d 2 p (1 − q ). (13). Combine equation (7), equation (13) and the definition of Ω1 and Ω 2 , and we can get the term which d 2 must not less than Ω 2 . Next, at the decision point I , given deposit contract d 2 , the term of the depositor accepting the contract is. 政 治 大. td1 + (1 − t ) pd 2 {[θ q] /[ pq + (1 − p)(1 − q)] + [(1 − θ )(1 − q)] /[ p(1 − q) + (1 − p) q]} ≥ 1. 立. meaning:. ‧ 國. 學. d2 ≥. (1 − td1 )(2qp − p − q )(2qp − p − q + 1) (1 − t ) p[θ + p (2q − 1)(q + θ − 1) − q ( q + 2θ − 2 ) − 1]. ,. (14). ‧. We define the right side of the in inequality (14) as Ω3 , combine the constraint. sit. y. Nat. on d 2 ≥ Ω 2 , and get the term which d 2 must not less than max[Ω 2 , Ω3 ] . Next, we. er. io. substitute Ω3 and Ω2 as d 2 into equation (4), then the results are equal to 1 and. n. al. more than 1 separately, so. v i n ΩC >h Ω is obtained. Because engchi U d 2. 3. 2. must not less than. max[Ω 2 , Ω3 ] and the bank will lower d 2 as far as possible, d 2 = Ω2 is obtained under situation 2. Combine the above analysis of two situations, we can get the following lemma: 【Lemma 1】Only one deposit contract of Ω1 and Ω 2 is the deposit contract equilibrium d 2 . (1) d 2 = Ω1 : The utility of the bank is VB1 , the depositor of type 1 withdraws in period 1, and the depositor of type 2 at I21 withdraws in 14.

(16) period 2, yet at I22 withdraws in period 1. (2) d 2 = Ω2 : The utility of the bank is VB 2 , the depositor of type 1 withdraws in period 1, and the depositor of type 2 at I21 and I22. both. withdraws in period 2. From Lemma 1 we can know the difference between the depositor decisions is just that at the decision point I22 , the depositor of type 2 will withdraw in period 1 under situation 1, while withdraw in period 2 under situation 2. Since d 2 is the. 政 治 大. protection offered to the depositor when the deposit contract expires at the end of. 立. period 2. Different d 2 will make the depositor of type 2 have different decisions,. ‧ 國. 學. d 2 is Ω1 under situation 1, yet under situation 2 is Ω2 . Because Ω 2 >Ω1 , it. ‧. sit. Nat. situation 2 rather than withdraw in period 1 under situation 1.. y. makes the depositor of type 2 have greater incentive to withdraw in period 2 under. n. al. er. io. Now we compare the size of VB1 and VB 2 to determine the bank’s optimum. Ch. i n U. v. choice on d 2 . First subtract equation (6) from equation (5), and we get: 4. engchi. −d1 (1 − t ){θ (1 − p ) + q[1 − q − θ (3 − 2 p − q )]} q (1 − q ). (15). As θ approaches 0, then equation (15) is less than 1. Nevertheless, as θ approaches 1, then equation (15) is more than 1. Besides, we differentiate equation (15) with respect to θ and get: −d1 (1 − t )[(1 − p ) − q (3 − 2 p − q )] d1 (1 − t )[(1 − p)(2q − 1) + q(1 − q)] = >0 q (1 − q ) q (1 − q ). (16). Combine the interpretation of equation (15) and equation (16), and we can get the. 4. The values of the equations analyzed below are all established under the assumption of. q ∈ (1/ 2,1) .. 15.

(17) probability θ of the depositor receiving positive information is higher (lower), VB1 is likely to be more (less) than VB 2 , meaning the bank is likely to choose d 2 to equal to Ω1 ( Ω 2 ). Intuitively, although under situation 1 the bank will face the risk of the depositor of type 2 withdrawing early in period 1 after his reception of negative information, when the probability θ of the depositor receiving positive information is higher, the probability of the bank facing such a risk is lower. Moreover, under situation 1 the amount d 2 of bank giving to the depositor who. 政 治 大. withdrawals at period 2 is lower, so the bank prefers Ω1 . On the contrary, under. 立. situation 2 the amount d 2 of bank giving to the depositor who withdrawals at. ‧ 國. 學. period 2 is higher, but when the probability θ of the depositor receiving positive information is lower, the probability of the bank facing the risk of the depositor’s. ‧. withdrawal at period 1 is higher, so the bank prefers Ω2 . Next, as p approaches 0,. y. Nat. er. io. sit. then we are unable to determine whether equation (15) is positive or not. 5 Nevertheless, as p approaches 1, then equation (15) is less than 0. We differentiate. n. al. Ch. equation (15) with respect to p and get: −d1 θ (1 − t )(2q − 1) <0 q (1 − q ). engchi. i n U. v. (17). Combine the interpretation of equation (15) and equation (17), and we can get the probability p of the bank obtaining R is higher (lower), VB1 is likely to be less (more) than VB 2 , meaning the bank is likely to choose d 2 to equal to Ω 2 ( Ω1 ). Intuitively, under situation 1 the bank will face the risk of the depositor of type 2 5. As. p. approaches. 0,. the. numerator. of. equation. (15). approaches. −d1 (1 − t )[θ (1 − 2q ) + q (1 − q )(1 − θ )] ; meanwhile, as θ approaches 0, equation (15) is less than 0; as θ approaches 1, equation (15) is more than 0. As a result, as p approaches 0, whether equation (15) is positive or not depends on other parameters. 16.

(18) withdrawing early in period 1 after the reception of negative information, and when the probability p of the bank obtaining R is lower, the probability of the bank facing such a risk is higher. Moreover, under situation 1 the amount d 2 of bank giving to the depositor who withdrawals at period 2 is lower, so the bank prefers Ω1 . On the contrary, under situation 2 the amount d 2 of bank giving to the depositor who withdrawals at period 2 is higher, but when the probability p of the bank obtaining R is higher, the probability of the bank facing the risk of the depositor’s. 政 治 大 approaches 1/2, then equation 立 (15) is less than 0. Nevertheless, as. withdrawal at period 1 is lower, so the bank prefers Ω2 . On the other hand, as q q approaches 1,. ‧ 國. q and get:. 學. then equation (15) is more than 0. Next, we differentiate equation (15) with respect to. ‧. d1 θ (1 − t )(1 − p )[1 − 2q (1 − q )] >0 q 2 (1 − q ) 2. Nat. y. (18). io. sit. Combine the interpretation of equation (15) and equation (18), and we can get the. er. precision q of the signal s is higher (lower), VB1 is likely to be (more) less than. al. n. v i n C hto choose d to Uequal to , meaning the bank is likely engchi. VB 2. 2. Ω1 ( Ω 2 ). Intuitively,. under situation 1 the bank will face the risk of the depositor of type 2 withdrawing early in period 1 after the reception of negative information, and when the precision q of the signal is higher, given the reception of positive information, the probability. pH of the bank obtaining R is higher, so the probability of the bank facing such a risk is lower. Moreover, under situation 1 the amount d 2 of bank giving to the depositor who withdrawals at period 2 is lower, so the bank prefers Ω1 . On the contrary, under situation 2 the amount d 2 of bank giving to the depositor who 17.

(19) withdrawals at period 2 is higher, but when the precision q of the signal is lower, the probability of the bank facing the risk of the depositor’s withdrawal at period 1 is higher, so the bank prefers Ω2 . Integrate the above analysis, and we can obtain the following proposition 1: 【Proposition 1】The bank deposit contract equilibrium arose from different model parameters are as follows: (1) When the probability θ. of the depositor receiving positive. information is higher (lower), VB1 is likely to be more (less) than. 政 治 大. VB 2 , meaning the bank is likely to choose d 2 to equal to Ω1 ( Ω 2 ).. 立. ‧ 國. 學. Moreover, as θ approaches 0, the bank will choose d 2 to equal to Ω 2 . Nevertheless as θ approaches 1, the bank will choose d 2 to. ‧. equal to Ω1 .. y. Nat. io. sit. (2) When the probability p of the bank obtaining R is higher (lower),. er. VB1 is likely to be less (more) than VB 2 , meaning the bank is likely to. al. n. v i n C h to Ω ( Ω ). Moreover, to equal engchi U. choose d 2. 2. 1. as p approaches 1,. the bank will choose d 2 to equal to Ω 2 . (3) When the precision q of the signal s is higher (lower), VB1 is likely to be more (less) than VB 2 , meaning the bank is likely to choose d 2 to equal to Ω1 ( Ω 2 ). Moreover, as q approaches 1/2, the bank will choose d 2 to equal to Ω 2 . Nevertheless, as q approaches 1, the bank will choose d 2 to equal to Ω1 . 18.

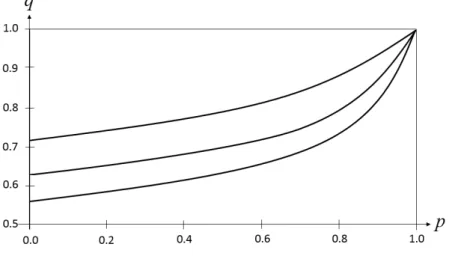

(20) The following below we use numerical simulation calculation to show the results of Proposition 1 with the actual values of the parameters. From the foregoing we learn that equation (15) cannot be determined whether it is positive or not, and the part which the sign of equation (15) cannot be determined is:. θ (1 − p) + q[1 − q − θ (3 − 2 p − q)]. (19). Equation (19) is set to be zero, and the solution of θ is. q(1 − q) q (1 − q ) + (2q − 1)(1 − p). (20). We get equation (20) is more than 0, then substitute θ =1/ 3 into equation (19), and get q is:. 1 ( p ± p 2 − 2 p + 2) 2. 立. 政 治 大 (21). ‧ 國. 學. Next, we substitute θ =1/ 2 into equation (19), and get q is:. ‧. 1 (2 p − 1 ± 5 − 8 p + 4 p 2 ) 2. (22). y. Nat. Finally, we substitute θ =2 / 3 into equation (19), and get q is:. sit. (23). er. io. 1 (4 p − 3 ± 16 p 2 − 32 p + 17) 2. al. n. v i n C h to lower left inUFigure 2 separately represent q . The curves from upper right engchi. Now we set that in Figure 2 the horizontal axis shows p and the vertical axis shows. the relationship between q and p when equation (21), equation (22) and equation (23) are positive. From equation (17) and equation (18) we can learn that p and q are respectively positive or negative associated with equation (15). It means that as. p is higher, VB 2 is more likely to be greater than VB1 , yet as q is higher, VB 2 is more likely to be less than VB1 . As a result, the part above the curve represents the scope of VB1 > VB 2 , and the part below the curve represents the scope of VB 2 >VB1 .. 19.

(21) Figure 2. The Relation Curve between q and p. 政 治 大. Besides, from figure 2 we can learn that with the increase of θ , the scope of. 立. VB1 > VB 2 is greater, meaning VB1 is more likely to be more than VB 2 , which. ‧ 國. 學. represents the bank is more likely to choose d 2 under situation 1.. ‧. n. er. io. sit. y. Nat. al. Ch. engchi. 20. i n U. v.

(22) 4. Bank Run The setting of Chen and Hasan (2008) is that as long as all the depositors withdraw at period 1, the bank run will occur, we extend their definition. From Lemma 1 we can learn that deposit contract equilibrium d 2 involve Ω1 under situation 1 and Ω 2 under situation 1. However in our model, the bank run can only happen when d 2 = Ω1 which the depositor of type 1 withdraws at period 1, and the depositor of type 2 at I21 withdraws at period 2, while at I22 withdraws at period. 政 治 大. 1. It makes two types of depositor may withdraw at period 1, and then leads a bank run to occur.. 立. From the foregoing we learn that in Figure 2 the part above the curve represents. ‧ 國. 學. the scope of VB1 > VB 2 . Because under situation 1 the utility VB1 of the bank is. ‧. higher, it makes the bank to choose deposit contract d 2 = Ω1 , in turn triggering the. y. Nat. sit. occurrence of bank runs. From Figure 1 we know that bank runs occur when. n. al. er. io. negative information is revealed, the incidence of runs is 1 − θ . On the other hand,. i n U. v. the part below the curve represents the scope of VB 2 > VB1 , and under situation 1 the. Ch. engchi. utility VB 2 of the bank is higher, so it makes the bank to choose deposit contract. d 2 = Ω2 . Bank runs will never happen under such a situation, and the incidence of runs is 0. This is Proposition 2: 【Proposition 2】Only when the bank chooses d 2 = Ω1 and negative information is revealed, bank runs may happen. Nevertheless, when the bank chooses d 2 = Ω2 , bank runs will never happen. Meanwhile from Proposition 1 we can arrange the following Corollary 1: 21.

(23) 【 Corollary 1 】 When the probability θ of the depositor receiving positive information is higher, the probability p of the bank obtaining R is lower, and the precision q of the signal s is higher, the bank is likely to choose d 2 to equal to Ω1 , therefore bank runs are easier to occur. Proposition 2 states that only when the bank chooses the contract d 2 = Ω1 may have two types of the depositor both withdraws at period 1. Nevertheless, the background of economic conditions described by Corollary 1 is the condition that the bank chooses the contract d 2 = Ω1 . The intuitive reason of Corollary 1 already. 政 治 大 has an associated discussion before Proposition 1 is inferred. Intuitively, due to 立. ‧ 國. 學. Ω 2 >Ω1 , under the condition that the bank chooses the contract d 2 = Ω1 , because the. benefits of withdrawing until the next period is relatively lower, the depositor. ‧. receiving negative information tends to withdrawing early at period 1.. sit. y. Nat. Next, we discuss the similarities and differences between Chen and Hasan (2008). n. al. er. io. and our model concerned the situation of bank runs. The former emphasizes there. i n U. v. both are an individual minimum threshold success ratio of the investment plan. Ch. engchi. whether the information is revealed or not. When depositors expect the success ratio is less than the minimum threshold, the bank run phenomenon will occur. Besides, the values of two minimum thresholds are uncertain. From another point of view, the bank runs we deduce will occur when the bank proposes the deposit d 2 = Ω1 and the depositor receives negative message. Known by Corollary 1, the lower the success ratio p of the investment plan, the more our model is prone to meet with a bank run. So the probability p of the bank obtaining R to both Chen and Hasan (2008) and our model makes an impact of the same direction on the occurrence of bank runs. It is that the lower the probability p of the bank obtaining R , the lower 22.

(24) the expected return got from the depositor withdrawing until the next period, so there is a strong motivation for the depositor to withdraw at period 1. In addition, the bank in our model has policy selection to the deposit contract, and in response to different economic conditions it will then select a deposit contract in advance to avoid a bank run. However, the banking industry is set to be perfectly competitive in Chen and Hasan (2008). It is the disparity between our model and Chen and Hasan (2008).. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 23. i n U. v.

(25) 5. Concluding Remark A bank runs is a phenomenon that the impacts of the panic in financial crisis or relevant negative information about the bank make depositors lose confidence in the solvency of bank, and thus large numbers of depositors seek to withdraw money from banks. Because banks will turn their deposits into other investments, they do not always retain cash meaning that the deposits which banks keep are limited. Once the bank encounters focused and intensive withdrawals, it will fall into crisis of liquidity shortage, probably leading to operational difficulties, even the risk of. 政 治 大 run is highly contagious. When a bank run occurs, if the bank does not take timely 立 bankruptcy. It is seen to be a sudden and concentrated hazard. Meanwhile, the bank. measures or obtain other assistance, it often causes a larger-scale run, thereby. ‧ 國. 學. resulting in the collapse of the banking system, hence the government will intervene. ‧. when necessary as a result.. sit. y. Nat. We expand the settings of Chen and Hasan (2008), which originally assume that. io. er. the bank is perfectly competitive, so the deposit contract is decided by the economic environment. We alter their model and assume that the bank owns the initiative of. al. n. v i n C hand aims for maximizing participating in decision making, its own benefits. They engchi U originally assume numerous depositors jointly participate in decision making, while there is only one depositor along with the bank as players in our model, and the depositor divided in two types of liquidity preference patterns will make decisions for profit maximization separately. According to the interactive strategy game equilibrium of the bank and the depositor, the bank may propose two equilibria of the deposit contract for the depositor to accept it or not, and which deposit contract it proposes will depend on different economic conditions the bank faces. After the bank proposes the deposit contract and the depositor accepts it, the depositor in two different types of liquidity 24.

(26) preference will decide when to withdrawal in accordance with their respective demand. We find that bank runs will occur only when the bank offer one of the contracts and the depositor receives the negative message. Future research can be extended to the introduction of a deposit insurance system to explore whether the deposit contract the bank provides will change, or under the protection of the deposit insurance system, whether the depositor will postpone the moment of withdrawal, even whether the occurrence of bank run will be put off. On the other hand, the research can also be extended to whether the degree to how fast. 政 治 大 and other issues. In addition, we know that the higher the overdue loan ratio is, the 立 the depositor receives negative information will affect the occurrence of bank runs. easier the panic run will occur. The reason is that the loan quality will be lower and. ‧ 國. 學. makes depositors worry about the security of their deposits. The research can be. ‧. considered the existence of the overdue loan ratio to conform to reality. We look. sit. y. Nat. forward to the follow-up extension study to better understand the actual operation of. io. n. al. er. the banking system and to reduce the likelihood of bank runs.. Ch. engchi. 25. i n U. v.

(27) References Alonso, I. (1996), “On avoiding bank runs,” Journal of Monetary Economics, 37, 73-87. Chari, V. V. and R. Jaganathan (1988), “Banking Panics, Information, and Rational Expectations Equilibrium,” Journal of Finance, 43, 749–761. Chen, Y. (1999), “The Role of the First Come, First Served Rule and Information Externalities,” Journal of Political Economy, 107, 946–968. Chen, Y. and I. Hasan (2006) “The Transparency of the Banking System and the. 政 治 大 Intermediation, 15, 307–331. 立. Efficiency of Information-Based Bank Runs,” Journal of Financial. Chen, Y. and I. Hasan (2008), “Why Do Bank Run Look Like Panic? A New. ‧ 國. 學. Explanation, ” Journal of Money, Credit and Banking, 40:2–3,535-546.. sit. y. Nat. Distortions,” Journal of Monetary Economics, 41, 27-38.. ‧. Cooper, R. and T. W. Ross (1998), “Bank Runs: Liquidity Costs and Investment. io. er. Diamond, D. W. and P. H. Dybvig (1983), “Bank Runs, Deposit Insurance and Liquidity,” Journal of Political Economy, 91, 401–419.. al. n. v i n C h“Bank Runs and Investment Ennis, H. M. and T. Keister (2006), Decisions engchi U Revisited,” Journal of Monetary Economics, 53,217-232.. Goldstein, I. and A. Pauzner (2005), “Demand-Deposit Contracts and the Probability of Bank Runs,” Journal of Finance, 60, 1293–1327. Maeda, Y. and Y. Sakai (2008), “Microeconomic Foundation of Lender of Last Resort from the Viewpoint of Payments,” Japanese Economic Review, 59, 178-193. Samartín, M. (2003), “Should bank runs be prevented?” Journal of Banking and Finance, 27, 977–1000. 26.

(28)

數據

Outline

相關文件

The difference resulted from the co- existence of two kinds of words in Buddhist scriptures a foreign words in which di- syllabic words are dominant, and most of them are the

好了既然 Z[x] 中的 ideal 不一定是 principle ideal 那麼我們就不能學 Proposition 7.2.11 的方法得到 Z[x] 中的 irreducible element 就是 prime element 了..

volume suppressed mass: (TeV) 2 /M P ∼ 10 −4 eV → mm range can be experimentally tested for any number of extra dimensions - Light U(1) gauge bosons: no derivative couplings. =>

For pedagogical purposes, let us start consideration from a simple one-dimensional (1D) system, where electrons are confined to a chain parallel to the x axis. As it is well known

The observed small neutrino masses strongly suggest the presence of super heavy Majorana neutrinos N. Out-of-thermal equilibrium processes may be easily realized around the

incapable to extract any quantities from QCD, nor to tackle the most interesting physics, namely, the spontaneously chiral symmetry breaking and the color confinement..

(1) Determine a hypersurface on which matching condition is given.. (2) Determine a

• Formation of massive primordial stars as origin of objects in the early universe. • Supernova explosions might be visible to the most