Internet and e-commerce

adoption by the Taiwan

semiconductor industry

Yung-Chuan Peng and Charles V. Trappey

Department of Management Science, National Chiao Tung University, Hsinchu,

Taiwan, Republic of China

Nai-Yu Liu

United Microelectronics Corporation, Hsinchu, Taiwan, Republic of China

Abstract

Purpose – To determine the status of internet and e-commerce adoption by the Taiwan semiconductor industry, the research is designed to help government and enterprise in formulating strategic plans and making resource allocation decisions.

Design/methodology/approach – Using the three-level model of internet commerce adoption (MICA), a survey of 287 companies and web sites was designed. Semiconductor firms were placed into five categories: integrated circuit (IC) design, manufacturing, packaging, IC testing, and peripheral device manufacturing.

Findings – The MICA model shows the internet adoption ratio for semiconductor firms as 82.6 percent, significantly higher than the electronics and electrical machinery industry sector (56.5 percent). The IC manufacturing and packaging segment are in the processing stage, the final stage of development for the MICA model. One-third of the IC testing industry segment falls into the provision stage, and 36.1 percent web sites are in the processing stage. The IC design and peripherals industrial segments are located in the provision stage.

Practical implications – The IC manufacturing segment is conducting more financial transactions than the other segments – a result that matches earlier research showing that larger companies are most likely to implement e-business applications. Many enterprises in the industry are lagging with the adoption of the internet indicating a need for education and training.

Originality/value – This benchmark study provides a framework for evaluating the internet adoption status of semiconductor and other high technology firms. The MICA model is demonstrated to be suitable for evaluating the different stages of internet adoption.

Keywords Internet, Taiwan, Electronic commerce, Electronics industry Paper type Literature review

Introduction

Over the past 20 years, the electronics industry has grown to become the dominant economic contributor and strategic business sector for many countries. According to the yearbook of Industrial Technology Information Service (ITIS) 2003, the semiconductor industry has become the leading economic contributor for Taiwan. The semiconductor industry provided a GDP contribution rate of about 2-3 percent since the year 2000. As noted by many researches, the development of internet is improving operational efficiency and is significantly influencing the manufacturing supply chain (Yau, 2002). During the internet era, it is important to effectively adopt the internet and e-commerce to create competitive advantage. The government and firms need to know the status of e-commerce adoption when establishing policy and The Emerald Research Register for this journal is available at The current issue and full text archive of this journal is available at www.emeraldinsight.com/researchregister www.emeraldinsight.com/0263-5577.htm

IMDS

105,4

476

Industrial Management & Data Systems

Vol. 105 No. 4, 2005 pp. 476-490

q Emerald Group Publishing Limited

0263-5577

strategy. This research conducts a benchmark study and surveys internet and e-commerce adoption by semiconductor firms. The results benchmark the internet adoption status of the Taiwan semiconductor industry and yield statistics to support policy formulation for future industry development.

Internet technology has changed the world’s supply chain by enhancing cooperation and adoption efficiency as well as adding value to products and enterprises. The internet is a worldwide collection of interconnected computer networks (Krol and Hoffman, 1993). In recent years, electronic commerce has increased the sharing of business information, has built business relationships, and has enhanced business transactions by means of telecommunications networks (Zwass, 1997). According to recent studies, internet-based e-commerce provides a fast and efficient way of obtaining comprehensive market information, feedback from industry and supplier performance (Soliman and Youssef, 2003).

Many research projects are being conducted to document successful e-commerce processes. One such study finds that there are many processes critical to the success of e-commerce including order fulfillment, revenue generation, financial control, web management, monitoring, order generation, call center integration, and consumer behavior (Duffy and Dale, 2002). New business models are needed to conform to the electronic commerce of today’s economy. Defining the customer’s expectation in e-business is important as well as the need to invest adequately in the improvement of services (Rotondaro, 2002). The critical dimensions such as finance, legal issues, logistics, marketing, operations, security and technology, as well as strategy must be considered when planning new e-commerce ventures (Kao and Decou, 2003). Regardless of the benefits that can be gained from e-commerce, or the critical issues solved, the first thing for modern enterprise should do is to go online and adopt the internet. The e-commerce and internet adoption model used to benchmark the Taiwan semiconductor industry will be discussed in the following section.

Internet and e-commerce adoption models

The rapid adoption of the internet as a commercial medium has motivated firms to experiment with innovative ways of marketing to consumers in cyberspace (Ricciuti, 1995). Because the web must use the internet as its channel, web commerce is included in the domain of internet commerce and becomes the definition of electronic commerce (Cowan, 1998). Lim et al. (1998) indicate that innovation, organization and external factors will influence a firm’s decision to adopt e-commerce strategies. Using a survey of 162 small businesses, the authors determined that the drivers of internet adoption are different from those of traditional information system adoption, and the degree of internet adoption was strongly related to the owner’s perception of the relative advantages of using information technology. Further, the degree of information system adoption can be related to the firm’s previous innovation experience (Lee and Runge, 2001). An electronic commerce survey of the semiconductor equipment industry showed that almost all of the Semiconductor Equipment and Materials International (SEMI) members have used web sites at least two years with the larger companies being more likely to implement e-business applications (Macher et al., 2002). Many researchers are interested in e-commerce performance measures. A proposed data envelopment analysis (DEA) model evaluates e-commerce performance of firms using financial, operational, and e-commerce specific measures (Wen, Lim, and Huang, 2003).

Internet and

e-commerce

adoption

477

A search of the literature has uncovered three main ways of classifying web sites including digital business models, stages of development, and scoring systems (Davidson, 2002). This research uses a stage of development model to study the Taiwan semiconductor industry since there are no available statistics to describe this dominant industry sector in Taiwan.

The model of internet commerce adoption (MICA) is a tool for determining the level of a web site’s business enhancement and explains how a business progresses from one stage of e-commerce development to another (Burgess and Cooper, 2000). The MICA model indicates that a web site passes through three stages from infancy to maturity and includes the promotion stage, the provision stage, and the processing stage (Table I). During the promotion stage, companies construct web sites that introduces the organization’s products and services, offers basic information about the business scope, and provides news relevant to enterprise. Some of the web sites use animation and multimedia to attract the user’s attention toward a promotion target. However, users cannot send anything to the site and can only receive information from promotion web sites.

Since there is limited interaction with promotional sites, the next stage of deployment is called the provision stage where web sites provide an opportunity for visitors to send and receive information. Visitors to a provision site receive recruitment information, technical information, e-mail hyperlink access to search engines, and even language choices. The value-added information, experience sharing, and appraisal reports help attract and maintain visitors. More complex functions are also embedded as a key parts of interaction web sites. Users can search for information, such as

No. Item name Description

Promotion stage

1 Enterprise information The background and business scope of enterprises 2 Product information Product catalogs and product names

3 News of enterprise Important news relative to the company, such as new product (or functions) releases

4 Animation and multimedia Attract user’s attention to focus on major promotion target

Provision stage

5 Recruitment information List of open jobs, major mission of these jobs, and job requirements

6 Technical information (FAQ and Report) More details or advanced product information, such as datasheet, new product releases or process flows 7 E-mail hyperlink Easy for users to connect to other enterprises 8 Search service Helps visitors to quickly find information 9 Language choice Provide service for users from different nations Processing stage

10 Online resume Standard flow allows visitors’ to fill in relative information

11 E-service Visitors could query, analyze, or download, technical information.

12 Online order or inquiry Provides the standard flow to let visitors make purchases online or inquire about products and services

Table I.

Web site classification schema

IMDS

105,4

e-mail addresses, access online customer registration, or interact with message boards. Interaction is encouraged on the web sites by inviting visitors to inquire, claim, complain, challenge, or make suggestions.

In the processing stage, customers play the most active role. The important part of this stage is building and maintaining customer relationships. Applying for work, electronic services, online orders, or inquiries can be accomplished online. For example, a resume can be submitted by an applicant, visitors can query, analyze or download technical information, and online ordering is allowed. More mature transaction sites include ordering, purchasing, and delivering. These web sites, while offering the highest level functions, require firms to overcome many technical barriers. In addition to high costs, the sites require sophisticated programming knowledge to set up and maintain the site processes. However, this research surveys a company’s web site using the MICA (Table I) to determine the development stage of the Taiwan semiconductor industry internet e-commerce adoption.

The status of Taiwan semiconductor industry

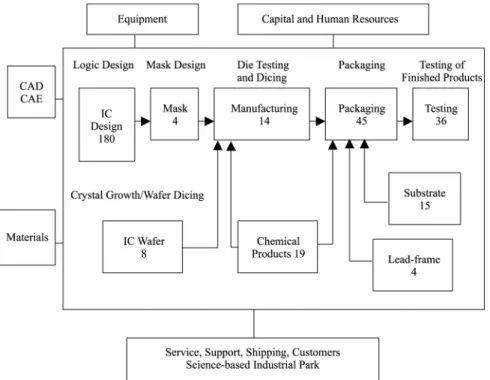

The Taiwan semiconductor industry has distinguished itself as a comprehensive industrial supply chain. The structure of semiconductor industry in Taiwan consists of upstream, midstream, and downstream segments working together cooperatively in a consolidated chain (Figure 1).

The increased manufacturing capacity in Asia, particularly in Taiwan, attributed to the success of the foundry model. Pure-play foundries supplied roughly 73 percent of the worldwide market, with sales approaching US$ 21.7 billion in 2002 (ITIS, 2003).

Figure 1. The structure of the Taiwan semiconductor industry (ITIS, 2003)

Internet and

e-commerce

adoption

479

Mask ROM owns 56 percent of the global market share and IC packaging has 30.4 percent of the market share making both global leaders. The IC Design Industry takes 26 percent of global market share following the leading country USA. The global ranking of the manufacturing capability in Taiwan followed Japan and USA and is currently facing competition from China. Table II shows the global competitive advantage of Taiwan’s semiconductor industry. According to the report of ITIS (2003), the 2002 revenue of the semiconductor industry in Taiwan reached USD$ 19.5 billion. The revenue includes USD$ 4.4 billion for IC design, USD$ 11.3 billion for IC manufacturing, USD$ 2.8 billion for IC packaging, and USD$ 949 million for IC testing (Table III). The high growth rate of the IC industry plays a key role in the economic development of Taiwan and has established the industry’s global position. The competitive advantage of the industry and the cluster effect of the channel members have made the Taiwan semiconductor industry world famous.

Hypotheses

Based on Chen’s (2001) study, the total number of online web sites for the Taiwan retail industry has reached 45 percent. Compared to the analysis of web sites of

Product and market share Global market share (percent) Global ranking Leading country

Brand Name IC 5.5 4 USA, Japan, Korea

DRAM 16.9 3 Korea, USA

SRAM 6.4 4 Japan, Korea, USA

Mask ROM 56.4 1 Taiwan

Design industry 25.9 2 USA

Manufacturing industry 7.4 4 USA, Japan, Korea Contract manufacturing 72.9 1 Taiwan

IC packaging industry 30.4 1 Taiwan

Testing industry 35.7 – –

Manufacture capabilities 14.7 3 Japan, USA Source: ITIS (2003)

Table II.

Taiwan semiconductor industry’s global market position Segment/Revenuea 1998 1999 2000 2001 2002 2002/2001(percent) Semiconductor industry 8.46 12.64 21.33 15.73 19.49 23.9 IC design 1.40 2.21 3.44 3.64 4.41 21.1 IC manufacturing 5.06 7.9 13.99 9.03 11.30 25.1 Foundry 2.80 4.19 8.85 6.11 7.36 20.5 IC packaging 1.62 1.97 2.92 2.30 2.83 23.0 Taiwan IC packaging 1.25 1.64 2.56 1.97 2.35 19.4 IC testing 0.39 0.55 0.98 0.76 0.95 25.7 Total market value ¼ Design þ

Manufacturing2 Foundry

3.66 5.93 8.57 6.56 8.35 27.3

Note:aData reported in billions of US $

Source: ITIS (2003) Table III.

Last five years revenue for Taiwan’s

semiconductor industry

IMDS

105,4

4,000 members of the Taiwan Electronic and Electrical Machinery Association (TEEMA), the number of online web sites reached 56.5 percent in 2002, a ratio higher than Taiwan’s retail industry. The greater the internationalization of the supply chain and the more international intellectual property (IP) is shared, the greater the need for the internet. Using this reasoning, we postulate that internet will be of greater benefit to the semiconductor industry.

H1. The semiconductor industry will have higher web site ratios than the

electronics and electrical machinery industry.

In 1954, Bell Labs succeeded in developing transistors to replace traditional tubes of the semiconductor industry era. Texas Instruments developed integrated circuits (IC) in 1958, and began mass-production in 1960. The newly developed IC products led to a revolution in computers and information technology. From 1960 onwards, the semiconductor industry has included IC design, IC production, IC packaging, and IC testing with each sector playing an important role in the value chain.

Previous research has shown that larger companies are more likely to implement e-business applications (Macher et al., 2002). Further, the manufacturing segment shows greater web site adoption and greater e-commerce maturity, largely due to high capital and manpower investment. For the Taiwan semiconductor industry, three additional hypotheses are constructed:

H2. The IC manufacturing segment has a greater internet adoption than other

segments in the semiconductor industry.

H3. The IC manufacturing industry should be the most mature sector and most

likely in the processing stage. Other sectors are most likely in the provision stage.

H4. The IC manufacturing segment will more readily adopt online ordering than

other segments in the semiconductor industry. Research design

The purpose of this research is to study the status of internet commerce adoption, and to evaluate the stages of development. The Burgess and Cooper MICA model was originally used to study web sites for the world’s metal industry. Given the published status and reliability of the model, this tool was selected for the coding and analysis of web sites. The hypotheses were tested using the surveyed data. According to Figure 1, the research focused on 287 enterprises including 180 IC design, 14 manufacturing, 45 packaging, 36 testing, and 12 peripheral (four mask and eight IC wafer) companies, the five segments that play the most important role in the IC industry. The authors surveyed these companies’ web site to analyze the stages of development. A census of Taiwan IC industry internet and electronic commerce adoption was conducted by using a comprehensive association list of companies. Companies that did not list a (uniform resource locator) URL in the list were called by phone to confirm whether or not they had a web site. Although a web site may contain many pages, all pages under the identical URL were browsed. There were 12 items evaluated using the code sheet

Internet and

e-commerce

adoption

481

(Table I). When the MICA item on the code sheet was found on the company web site, it was assigned the code “1”, and “0” if the item was not present. A web site with items including online resume, e-service, and online order or inquiry would be categorized as belonging to the processing stage. A web site was categorized in the processing stage, if any code “1” could be found from item 10 to item 12. If the web site did not fall into the processing stage category, then we checked the provision stage. If there was any code “1” found for item 5 to item 9, then the web site was placed into the provision stage. Finally, we would confirm that a web site was in the promotion stage if any code “1” was found from item 1 to 4, but not having any in item 5 to 12. If all the 12 items were coded “0”, that meant the company was without a web site. Besides, the ratio of the processing item was counted by accumulating the numbers of code “1” of each item from the web site in different segments to compare the maturity of web site design. For example, we count code “1” relating to an online resume item from the five segments and compare the ratio to understand the status of development.

To examine the validity of the content analysis, five web sites were selected for a pre-test. Four trained analysts conducted the pre-test. Each evaluator read the instructions and classified the sites according to the schema definitions. Five web sites were selected randomly including Mediatek and Tenx two IC design houses, Mxic, an IC manufacturer, and Kyec plus Spil – two IC packaging companies. Each tester coded 12 items on the five web sites, and then compared the code results. Using ANOVA, the

results ðp ¼ 0:993, a¼ 0:05Þ accept Ho and indicate that there is no significant

difference between the four testers. Status and analysis

A census of the web site was conducted, and all 287 companies’ web sites were browsed and the contents analyzed. The data show that over 82.6 percent of the enterprises have their own web sites, and 50 companies (about 17.4 percent) are without web sites. Thus, the sample included 237 web sites and the results are shown in Table IV. Based on the e-commerce web site classification schema, all the web sites were classified into three stages. Only one company was in the presence stage, 135 companies (about 47 percent) were in the provision stage and 101 companies (about 35.2 percent) were in the processing stage. Most web sites of the semiconductor industry were in the provision stage. The data were partitioned into IC design, IC manufacturing, IC packaging, and IC testing and peripheral IC segments for further analysis.

Taiwan IC design industry

In 2002, the revenue of IC design industry was with a growth rate of 21.1 percent compared to 2001 (Table II). ITIS (2003) predicted that the growth rate for 2003 would increase to 35 percent. The IC design industry is the up-stream segment of the industry and the products undergo polishing, production, sealing, packing and testing through later stages of manufacturing. The processing, sealing, packing and testing are in the later stages of production, since its labor outsourcing to overseas markets is usually required. The level of outsourcing reached 94.2 percent in year 2001 – more than 83.6 percent from the year 2000.

Over the past few years, the IC design industry has targeted products for the information industry. Micro-components were the main products designed, and accounted for 72.1 percent in 2001 while internal memory IC, logic and analog IC

IMDS

105,4

Segment IC Industry IC Design Manufacturing Testing Packaging Peripheral Stage No. Percent No. Percent No. Percent No. Percent No. Percent No. Percent Promotion 1 0.3 1 0.6 0 0 0 0 0 0 0 0 Provision 135 47 101 56.1 1 7.1 12 33.3 16 35.6 5 41.7 Processing 101 35.2 50 27.8 12 85.8 13 36.1 23 51.1 3 2 5 Sum.web sites 237 82.6 152 84.4 13 92.9 25 69.4 39 86.7 8 66.7 Without webs 50 17.4 28 15.6 1 7.1 11 30.6 6 13.3 4 33.3 Total Co. No. 287 100 180 100 14 100 36 100 45 100 12 100 Table IV. Stage of web site number and ratio by segment of Taiwan IC industry

Internet and

e-commerce

adoption

483

covered 16.3, 7.5 and 4.1 percent, respectively (ITIS, 2003). The IC design industry consists of 180 enterprises in Taiwan, about one-fourth of the all design houses in the world, and 152 enterprises (84.4 percent) have their own web sites. Using the e-commerce web site classification schema code (Table III), there are 101 companies (56.1 percent) in the provision stage, 50 web sites (27.8 percent) in the processing stage, and only one company (0.6 percent) in the promotion stage.

Taiwan IC manufacturing industry

The Taiwan IC manufacturing industry is ranked fourth in the world, and includes the world’s largest foundries, TSMC and UMC. In 2002, the production value of the Taiwan IC manufacturing industry was $ 378 billion NTD, maintaining a growth rate of 25.1 percent (Table I). The manufacturing industry is the largest IC industry segment, and produces electric circuits on silicon wafers. There are two types of manufacturing companies – integrated memory devices manufacturers and foundries. TSMC, UMC, EPISIL, ATC, and AMPI are foundries in the IC industry. The other nine companies in this sector, namely PSC, VIS, MOSEL, NAYA, PROMOS, WINBOND, MXIC, SIS, and ADT, are integrated memory device manufacturers. Owing to global competition, these manufacturing companies are strategically expanding production capability and are investing in research and development.

There are 14 IC manufacturing companies in Taiwan and about 92.9 percent have their own online web sites. Only one company (7.1 percent) is in the provision stage, and 85.8 percent of the firms are in the processing stage. The results of the study show that most of the IC manufacturing web sites are in the processing stage as shown in Figure 2.

Taiwan IC packaging industry

The IC package industry is the down-stream part of the IC industry and is labor intensive. Taiwan’s IC packaging industry is the best in the world with ASE, SPIL and ORIENT as the leading enterprises. Compared with the total production value in 2001, the Taiwan IC packaging industry reached a growth rate of 23.0 percent in 2002 (Table II). Packaging technology has continued to improve with higher pin counts being obtained. The high value-added business is growing, and has increased to 40.2 percent in 2001 (ITIS, 2003). There are 45 enterprises in the Taiwan IC packaging industry and 39 (86.7 percent) have their own web sites. Table IV shows that 35.6 percent (16 companies) are in the provision stage, and 23 companies (51.1 percent) are

Figure 2.

Web site classifications for the IC manufacturing industry in Taiwan

IMDS

105,4

in the processing stage. Most of the web sites in the IC packaging industry are in the processing stage.

Taiwan IC testing industry

During the year of 2002, the production value of Taiwan’s IC testing industry reached a growth rate of 26 percent (Table I). The testing industry is a down-stream sector and some of the companies provide both testing and package services. The top five companies are ASE, ChipMos, KYEC, Walton Advanced, and SPIL. The status of the Taiwan IC testing industry was surveyed. Most of the firms (51 percent) do memory chip testing, the main activity in the industry. Logic testing is the next largest service (28 percent), with mixed signal, linear testing, RF IC testing, and other testing making up the remainder. About 60 percent of the customers are located in Taiwan, 28 percent in North America, 10 percent in Japan, with the remainder in Europe (ITIS, 2003). The Taiwan IC testing segment consists of 36 enterprises and 25 companies (69.4 percent) have their own web sites. These web sites are roughly split between the 12 web sites in provision stage (33.3 percent) and 13 (36.1 percent) web sites in the processing stage (Table IV).

Taiwan IC peripheral industry

There are only 12 companies in the Taiwan IC peripheral industry sector in this study including eight IC wafer and four IC mask companies. Eight of the companies have their own web sites and most of the web sites are classified in the provision stage. Three companies (25 percent) are in the processing stage and five firms (41.7 percent) are in the provision stage (Table IV). Table IV shows the result of this study by segments and the whole IC industry. The first number indicates the number of web site, and the ratio means adoption rate in stage by different segments.

E-commerce item comparison

The results show that the IC manufacturing industry has the highest ratio of web sites and 85.8 percent web sites are in the processing stage. A little more than half of IC packaging companies’ web sites (51.1 percent) is in the processing stage. There are 13 IC testing firms’ web site about 36.1 percent, 50 IC design web sites (27.8 percent), and three web sites (25 percent) of IC peripheral companies’ web sites are in the processing stage (Figure 3).

The statistics of the processing stage shows that 56 web sites (19.5 percent) are designed with the function of online resume, 59 web sites (20.5 percent) have e-service item, and just eight web sites (2.7 percent) are designed with online order or inquiry items (Table IV). There are 11 web sites about 78.6 percent in IC manufacturing segment, 20 web sites (44.4 percent) in IC packaging segment, 12 testing web sites (33.3 percent), 2 peripheral web sites (16.7 percent), and 11 web sites in IC design segment that own online resume items. The IC manufacturing segment takes the lead with 8 web sites (57.1 percent) – 3 web sites (25 percent) in peripheral, 39 IC designing web sites (21.7 percent), 6 packaging web sites (13.3 percent), and 3 testing web sites (8.3 percent) were designed with e-service items (Figure 4). Finally, the authors found that very few web sites had the online order or inquiry item design. Only two IC manufacturing companies’ web sites (14.3 percent), one packaging web site

Internet and

e-commerce

adoption

485

(2.2 percent), and five IC design enterprises’ (2.8 percent) added the online order or inquiry items to their web sites (Table V).

Hypotheses testing

All of the 287 target enterprises’ web sites were surveyed in this research, a comprehensive study of the industry population. From the surveyed results, the number of online web sites for the IC industry reached 82.6 percent, which is higher than the online ratio of 56 percent by the electronics and electrical machinery industry. Thus, H1 – which tests that the semiconductor industry will have a higher percentage of online web sites than the electronics and electrical machinery industry, is supported. H2 tests whether the internet adoption ratio for the IC manufacturing industry is the highest in the Taiwan semiconductor industry. The internet adoption ratio of the IC manufacturing segment was found to reach 92.9 percent which is higher than the internet adoption ratio of IC design (84 percent), IC packaging (87 percent), IC testing (69 percent), and the IC peripheral segment (67 percent). Thus, it can be concluded that the IC manufacturing segment has a higher internet adoption ratio than other segments in the semiconductor industry.

Figure 4.

Processing stage items by industry segment Figure 3.

Ratio of web sites in the processing stage by industry segment

IMDS

105,4

Industry IC (287) IC design (180) Manufacturing (14) Testing (36) Packaging (45) Peripheral (12) Item No. percent No. percent No. percent No. percent No. percent No. percent Online resume 56 19.5 11 6.1 11 78.6 12 33.3 20 44.4 2 16.7 E-service 59 20.5 39 21.7 8 57.1 3 8.3 6 13.3 3 2 5 Online order or inquiry 8 2.7 5 2.8 2 14.3 0 0 1 2.2 0 0 Table V. Web site number and ratio with item in processing stage by industry segment

Internet and

e-commerce

adoption

487

The data show that 56.1 percent of the enterprises’ web sites in the IC design industry and 41.7 percent web sites of the peripheral enterprises are in the provision stage. About 85.8 percent of the enterprises’ web sites in the IC manufacturing segment are in the processing stage, 51.1 percent of firms’ web sites in the IC package industry, and 36 percent of web sites of the IC testing industry are in the processing stage. In conclusion, the maturity of internet and e-commerce of the IC manufacturing industry is better than the other four segments in the Taiwan semiconductor industry. The data shown in Table III supports H3.

Finally, the data demonstrate that there are very few web sites (only eight web sites out of 237 firm’s web sites) with online order or inquiry. From the results of Table V, the IC manufacturing segment only has two web sites about 14.3 percent with the online order or inquiry item that is higher than the online order or inquiry ratio of IC design segment with 2.8 percent, and IC packaging segment with 2.2 percent. No online order or inquiry items were found on IC packaging and peripheral industry web sites. The results conclude that the IC manufacturing segment’s online ordering items ratio are higher than the other segments in the semiconductor industry. H4 is supported by this research.

Conclusion and recommendations

This benchmark study provides a framework for evaluating the internet adoption status of Taiwan semiconductor industry firms. The twelve items of MICA are used to evaluate the development stage of the Taiwan IC industry. The internet adoption ratio by the semiconductor industry (82.6 percent) is higher than the electronics and electrical machinery industry (56 percent), and the Taiwan retail industry (45 percent). The research places the status of the Taiwan IC industry largely in the provision stage. Different industry segments have shown different levels of maturity. More than half of the web sites (51.1 percent) in the IC design segments are located in the provision stage. Moreover, 85.8 percent of the web sites of the IC manufacturing segment are in the processing stage and have a higher e-commerce adoption ratio than other sectors of the Taiwan semiconductor industry. The results agree with the results of Macher et al. (2002). Because of the large capital requirements for IC manufacturing companies, these companies have the resources and capabilities to implement more complex systems and have moved into the processing stage. One-third of the IC testing web sites (33.3 percent) are located in the provision stage and more than one-third (36.1 percent) of the web sites are located in the processing stage. Referring to the results shown in Table IV, the IC packaging segment is in the processing stage and the IC peripheral segment is still immature (in the provision stage). The results also show a low usage rate of online ordering with the total ratio for online ordering or inquiry at about 2.7 percent. Overall, Taiwan’s semiconductor industry internet e-commerce adoption requires further development.

The IC design sector is expected to offer high value services, but has shown insufficient e-commerce adoption. Perhaps the lack of capital is impacting adoption since these companies do not have as much money to invest in e-commerce systems and are more focused on innovation. Online ordering is currently not very popular, but will increase dramatically as the design houses begin cooperating on systems-on-chip (SOC) projects that rely on the reuse and trade of design components between teams. The current strategic direction for government policy is to encourage IP trade and

IMDS

105,4

reuse of design components for SOC. The IC design segment should have a higher ratio of online transactions. The Taiwan semiconductor industry focuses more on technical data and information exchange than online ordering. Further research is required to determine how the use of internet and e-commerce can increase efficiency and competitiveness. When most of the companies in the Taiwan semiconductor industry adopt e-commerce, the industry will undoubtedly become more efficient. There are still many enterprises in different segments that are not familiar with the usage of internet and e-commerce adoption. More education and training is needed to encourage the internet adoption. Further, the government should help enterprises become familiar with the use of the internet and research is needed to measure the impact of incentives and training on adoption.

References

Burgess, L. and Cooper, J. (2000), “Extending the viability of model of internet commerce adoption (MICA) as a metric for explaining the process of business adoption of internet commerce”, paper presented at the 3rd International Conference on Telecommunications and Electronic Commerce, Dallas, TX.

Chen, S.L. (2001), “Study of e-commerce involvement in Taiwan’s retail industry”, Master’s thesis, National Chiao Tung University.

Cowan, K.C. (1998), “Electronic commerce: why do we need to do anything?”, paper presented at the APEC-PECC Seminar on Electronic Commerce, Bandar Sei Begawan, 10 March. Davidson, R. (2002), “Development of an industry specific web site evaluation framework for the

Australian wine industry”, Research Paper Series: 02-9, School of Commerce.

Duffy, G. and Dale, B.G. (2002), “E-commerce process: a study of criticality”, Industrial Management & Data Systems, Vol. 102 No. 8, pp. 432-41.

ITIS–Industrial Technology Research Laboratory Industrial Economics and Knowledge Center (2003), 2003 Semiconductor Industry Yearbook, Industrial Technology Intelligence Service, ITRI-IEK- 0453- T207 (92), Taiwan.

Kao, D. and Decou, J. (2003), “A strategy-based model for e-commerce planning”, Industrial Management & Data Systems, Vol. 103 No. 4, pp. 238-52.

Krol, E. and Hoffman, E. (1993), “FYI on what is the internet? Network working group request for comments: 1462 FYI 20”, available at: http://nexus.brocku.ca/rogawa/rfc/rfc1462.html Lee, J. and Runge, J. (2001), “Adoption of information technology in small business: testing

drivers of adoption for entrepreneurs”, Journal of Computer Information Systems, Vol. 42 No. 1, pp. 44-57.

Lin, L.H., Gan, B. and Wei, K.K. (1998), “An integrated model on the adoption of internet for commercial purposes”, paper presented at the Hawaii International Conference on System Science (HICSS-31), pp. 403-12.

Macher, J.T., Mowery, D.C. and Simcoe, T.S. (2002), “E-business and disintegration of the semiconductor industry value chain”, Industry and Innovation, Vol. 9 No. 3, pp. 155-81. Ricciuti, M. (1995), “Database vendors hawk wares on internet”, InfoWorld, 9-10 January,

pp. 17-27.

Rotondaro, R.G. (2002), “Defining the customer’s expectations in e-business”, Industrial Management & Data Systems, Vol. 102 No. 9, pp. 476-82.

Soliman, F. and Youssef, M.A. (2003), “Internet-based e-commerce and its impact on manufacturing and business operations”, Industrial Management & Data Systems, Vol. 103 No. 8, pp. 546-52.

Internet and

e-commerce

adoption

489

Wen, H.J., Lim, B. and Huang, H.L. (2003), “Measuring e-commerce efficiency: a data envelopment analysis (DEA) approach”, Industrial Management & Data Systems, Vol. 103 No. 9, pp. 703-10.

Yau, O.B. (2002), “An empirical investigation of the impact of business-to-business electronic commerce adoption on the business operation of Hong Kong manufacturers”, First Monday, Vol. 7 No. 9, available at: http://firstmonday.org/issues/issue7_9/yau/index.html Zwass, V. (1997), Foundations of Information System, McGraw-Hill, New York, NY, Business Modeling with UML: “The Light at the End of the Tunnel”, available at: www. therationaledge.com/content/dec_01/m_businessModeling_bb.html.

Further reading

Alonso, G., Fiedlier, U., Hagen, C., Lazcano, A., Schuldt, H. and Weiler, N. et al (1999), “Wise: business to business e-commerce”, Proceedings Ninth International Workshop on Research Issues on Data Engineering: Information Technology for Virtual Enterprises. RIDE-VE ’99, IEEE CS Press, Los Alamitos, CA, pp. 132-9.

Bakos, J.Y. (1991), “A strategic analysis of electronic marketplace”, Journal of MIS Quarterly, Vol. 15 No. 3, pp. 295-310.

Bichler, M.J., Lee, H.S. and Chung, J.Y. (2001), “An intelligent decision making framework for e-sourcing”, paper presented at the Third International Workshop on Advanced Issues of E-Commerce and Web-Based Information Systems, WECWIS, pp. 195-201.

Camp, L.J. and Sirbu, M. (1997), “Critical issues in internet commerce”, IEEE Communication Magazine, No. 5, pp. 58-62.

Chandra, C. and Smirnov, A.V. (2001), “Virtual supply chain management: information framework and agreement network model”, paper presented at The Sixth International Conference on Computer Supported Cooperative Work in Design, pp. 466-71.

Dai, Q. and Kauffman, R.J. (2001), “Business models for internet-based e-procurement systems and B2B electronic markets: an exploratory assessment”, Proceedings of the 34th Annual Hawaii International Conference on System Sciences, pp. 2197-206.

Dangelmaier, W., Szegunis, J., Emmrich, A. and Lessing, H. (2002), “Guidelines for participating in B2B e-markets”, Proceedings of the International Manufacturing Leaders Forum in Manufacturing, pp. 130-5.

Essig, M. (2001), “Electronic procurement in supply chain management: an information economic-based analysis of electronic markets”, Journal of Supply Chain Management, Vol. 37 No. 4, p. 43.

Hoffman, D.L., Novak, T.P. and Chatterjee, P. (1995), “Commercial scenarios for the web opportunities and challenges”, Journal of Computer-Mediated Communication, Vol. 1 No. 3, available at: www.ascusc.org/jcmc/vol1/issue3/hoffman.html

Liebowitz, S. (2002), Re-thinking the Network Economy, 1st ed., Amacom Books, New York, NY. Lin, Y.J. (2000), “The impact of business services on electronic commerce – the cases of design houses in semiconductor and information industries”, Master’s thesis, National Chiao Tung University.

McGuffog, T. (1999), “E-commerce and the value chain”, Manufacturing Engineer, Vol. 78 No. 4, pp. 157-60.

Tornatsky, L.G. and Fleischer, M. (1990), The Process of Technological Innovation, Rowman & Littlefield, Portland, OR.