Is There Any Impact of Credit Card on the Demand for Money? : A case of Taiwan

30

0

0

全文

(2) INTRODUCTION The question of whether the demand function for money is “stable” is one of the most important recurring issues in the theory and empirics of macroeconomic policy.. Since the 1960s,. the use of credit card in the United States has increased dramatically, as reflected in debt levels and ownership rates. Consequently, monetary economists have displayed growing interest in the impact of bank credit cards on economic variables, especially on the demand for money [see, for example, Marcus (1960), Sastry (1970), Hester (1972), Lewis (1974), White (1976), Viren (1992) and among others].. These studies put credit card usage into traditional money demand. function and discuss its effects on the demand for money. Nevertheless, based on a stable function, one would ask whether the modified function of demand for money has relatively few arguments? In words, if the traditional money demand function is at least as good as the modified model including credit card usage, why should one take credit card usage into account? The object of the present paper is to show that this modified model, in applying Taiwan’s data, does not behave as well as is not widely thought when comparing to traditional one. In particular, we show that by treating functions of money demand as a long-run equilibrium condition, and allowing for short-run dynamics, the modified model can be found which do have robust in-sample properties but forecasts badly out-of-sample. A rich tradition exists on the estimation and prediction of money demand among several countries. Nevertheless, the choice of model formulation and estimation method is a further noteworthy consideration. Until the prevalent use of cointegrating techniques, most money demand models were estimated either in log-levels or as log-differences. One of the early quarterly specifications, laid out by Goldfeld (1973), was in log-levels and became a standard formulation. However, recent advances in time series analysis have raised doubts about 1. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(3) specifying the money demand function in both of these two forms.. The analysis of time series. properties-in particular, the order of integration of economic time series-has become an important aspect of econometric modeling in recent years.. This analysis led us to reject a. Goldfeld-type log-level specification of demand for money, as well as the popular log-difference specification. As Engle and Granger (1987) have demonstrated, if a vector of variables is cointegrated, an empirical model formulated in pure first differences omits the error-correction term and thus misspecifies the dynamics. Because most theoretical models of money demand, whether based on transactions demand or portfolio choice, imply an equilibrium in levels, it is important to capture this relationship in the specification.. Besides, short-run dynamics of the money demand. functions are important as well. Hence, in this paper, we use an error-correction model (ECM) to capture the long-run cointegrating relationship between money and the driving variables, while allowing a rich display of short-run dynamics. In this approach, a long-run equilibrium money demand model (cointegrating regression) is first fit to the levels of the variables, and the calculated residuals from that model are used in an error-correction model which specifies the system’s short-run dynamics.1. Such an approach. permits both the levels and first-differences of the nonstationary variables to enter the money demand function, thereby avoid “the spurious regression phenomenon” arising in log-level form specification and avoid questioned appropriateness of the first-difference form. Our finding of cointegration facilitates an examination of the short-run modified money demand model satisfied a battery of in-sample diagnostics and also easily compares its the prediction accuracy with a traditional model, over a three-year post-estimation sample period, using dynamic forecasts. In. 1. This approach is popularized by Hendry and Richard (1982) as well as Hendry, Pagan and Sargan (1983). 2. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(4) addition, we apply the statistical inference of Diebold and Mariano (1995) to assess the statistical significance of forecast accuracy, and compare out candidate model with the alternative of traditional function of demand for money. The outline of the remainder of this paper is as follows.. Section 2 presents two. specifications of money demand and indicates their error-correction model with a brief illustration of variables used. Section 3 describes the data we used, scrutinizes the procedures of empirical analysis and indicates the empirical results.. The summary observations are stated in. the final section.. 2.. Money Demand Specifications This section develops an empirical model, which describes an alternative hypothesis that the. credit card usage affects Taiwan’s demand for money, say M1b. The traditional textbook formulation of the demand for money, M , typically relates the demand for real money balances to the interest rate and some measure of economic activity such as real GDP; that is,. M / P = f (Y , r b ) , where Y is the real income (real GDP), r b is rate of return on bond, and P is the price level.2 In order to characterize a broad traditional Taiwan’s demand for M1b, one should not ignore the effect of the stock market. Friedman (1988) postulated that the direct relationship between stock market and the real cash balance can be rationalized in three different ways: a wealth effect, a risk-spreading effect, and a transactions effect, and concluded a rise in stock prices would bring about a decrease in the velocity of money because the wealth effect is greater than the substitution effect when applying data from the United States. Indeed, a declining velocity of 2. The origins of this simple equation can be explained by a variety of stories. For example, the well-known Tobin’s (1958) theory emphasizes speculative considerations in addition to the transaction motive. 3. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(5) money due to rising stock prices is the most important factor in explaining the relatively stable price level in Taiwan during the 1980s, which has found by Lin and Lee (1989). Thus, a comprehensive traditional money demand can be modeled as following: M / P = f (Y , r b , r s , SV ) ,. where SV is the total trading value of stock market, and r s is the rate of return on equity. Since stock market movements reinforce the variation of velocity, incorporating stock market variables, like total trading value of stock and the rate of return on stock, into Taiwan’s demand for money is reasonable and necessary. There are several long-run M1b specifications used in the literature. A specification of money demand, which is developed by Hetzel (1989),3 to be taken in this paper is that the asset markets opportunity costs of holding money are measures of the interest foregone by holding money rather than a money market instrument. Specifically, the opportunity costs of holding M1b are measure as the interest spreads on market bond yield (and stock return)4 minus a weighted average of the explicit rates of interest paid on the components of M1b. Now, define rs b ≡ r b − r m and rs e ≡ r e − r m to be bond market and stock market opportunity cost of holding M1b, respectively. Accordingly, the postulated long-run money demand equation has the form: M / P = αY β 2 {exp[ β 3 (rs b ) + β 4 (rs e ) + U t ]}SV β5 , where α is a constant term and U is long-run disturbance term.. The parameter β i ( i =. 2, . . .,5) measures the long-run money demand elasticity of the corresponding variable. Equation (1) says that the public’s demand for real M1b balances depends upon two scale. 3 4. This money demand specification was also applied in Hetzel and Mehra (1989), and Mehra (1993) The rate of return on equity is measured as [(SPt SPt −1 ) − 1]⋅100% , where SP is stock price index. 4. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics. (1).

(6) variables, Y and SV, as well as two opportunity cost variables, rs b and rs e . Let little letters denote the natural logarithm of corresponding capital letters.. The empirical. model is that of log-linear long-run money demand function, which we take the natural logarithm form on the equation (1):. mt = α 0 + α1 yt + α 2 rstb + α 3 rste + α 4 svt + U t ,. (2). where α 1 = log(α ) , α 1 > 0 , α 2 < 0 and signs of α 3 , and α 4 can be positive or negative.. Of particular interest to the student of monetary theory is the impact of the use of credit cards on the real balance holding. Regarding this issue, several previous studies [see, e.g., Sastry (1970), White (1976), and among others] have introduced credit cards into an inventory money demand model, and theoretically emphasized that the credit card usage has negative effect on household’s currency holding. Especially, Akhand and Milbourne (1986) have taken two additional issues, card use fees and endogenous decision of credit card usage, into consideration in the previous modified inventory theory of money demand and have highlighted that the use of credit cards lowers the income elasticity and raises the absolute value of the interest elasticity. Suppose that the credit card usage do have effects on Taiwan’s M1b. Then, an additional variable that appear as arguments in the equation (3) is the transaction amount by credit card. Thus a modified model of log-linear long-run money demand function can be rewritten as:. mt = β 0 + ( β10 + β11crt ) yt + ( β 20 + β 21crt )rstb + β 3 rste + β 4 svt + Vt ,. (3). where cr stands for the ratio of transaction amount using credit card to total consumption expenditure, and Vt is the long-run random disturbance term.. We can rearrange the terms in. equation (3) as follows:. mt = β 0 + β10 yt + β11cryt + β 20 rstb + β 21crrstb + β 3 rste + β 4 svt + Vt , 5. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics. (3’).

(7) where cryt = crt × yt and crrstb = crt × rstb . According the analysis of Akhand and Milbourne (1986), the parameters of β 11 and β 21 , which are all expected to be negative, catch the reinforced effects of credit card usage on the income elasticity and interest elasticity, respectively. Cointegration implies that there exist one or more long-run relationships between real demand for money and a given set of variables that explain it, deviations from which tend to be eliminated over time and are therefore useful in predicting future money demand, whereas nothing is useful for predicting future money demand if money demand evolve as a traditional one. The error-correction model of demand for money contains two parts. The first is a long-run equilibrium money demand function described as the above. A contingent short-run dynamic adjustment model characterizes the second part as the form, when the effects of credit card usage is not included in the model: n1. n2. n3. n4. n5. s =0. s =0. s =0. s =0. s =1. ∆mt = δ 0 + ∑ δ 1s ∆yt − s + ∑ δ 2 s ∆rstb− s + ∑ δ 3 s ∆rste− s + ∑ δ 4 s ∆svt − s + ∑ δ 5 s ∆mt − s + δ 6U t −1 + ε t. (4). and a modified one, when the model contains the effects of the use of credit card: n′1. n′ 2. n′ 3. n′ 4. n′ 5. s =0. s =0. s =0. s =0. ∆mt = γ 0 + ∑ γ 1s ∆yt − s + ∑ γ 2 s ∆cryt − s + ∑ γ 3 s ∆rstb− s + ∑ γ 4 s ∆crrstb− s + ∑ γ 5 s ∆rste− s s =0. n′ 6. n′ 7. s =0. s =1. + ∑ γ 6 s ∆svt − s + ∑ γ 7 s ∆mt − s + γ 8Vt −1 + ξ t. (5). where all variables are as defined above and where ε and ξ are the short-run random disturbance term; ∆ , the first difference operator; ni ( i = 1,2,...,5 ) and n ′j ( j = 1,2,...,7 ), the number of lags; and U t −1 as well as Vt −1 , the lagged value of the long-rum random disturbance terms. Equations (4) and (5) give the short-run determinants of M1b demand, which include current and past changes in the scale and opportunity cost variables and the lagged value of the residual from the long-run money demand function. The parameters, δ 6 and γ 8 , that appear on U t −1 and 6. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(8) Vt −1 are error-correction coefficients, which are expected to exhibit a negative sign [Hendry and. Ericsson (1991) and Mehra (1991)]. Error-correction models possess a realistic presumption; actual M1b balances do not always equal what the public wishes to hold on the basis of the long-run factors specified in equations (2) and (3’). This property is presented by the presence of U t −1 and Vt −1 in equations (4) and (5). In the short run, therefore, the public adjusts its money balances to correct any disequilibrium in its long-run money holdings. The parameters δ 6 and γ 8 measure the role such disequilibria play in explaining the short-run movements in money balances.5 According to the argument from Engle and Granger (1987), we know that if the variables included in the long-run money demand model are nonstationary but cointegrated, then the error-correction form given above is likely to exist, that is, both δ 6 and γ 8 are nonzero. The money demand models described above can be estimated in two alternative ways. The first method, which suggested by Engle and Granger (1987), is a two-step procedure. In the first step, the long-run equilibrium money demand equation is estimated using a consistent estimation procedure, and the residuals are calculated. In the second step, the short-run money demand equation is estimated with the lagged value of the long-rum random disturbance term replaced by residuals estimated in step one. This two-step procedure is based on the assumption that all of the variables included in the long-run money demand model are nonstationary. Under these assumptions, ordinary least squares estimates of equations (4) and (5) are consistent. The unit root test results described in the next section, however, suggest that the empirical measure of the opportunity cost used here in equations (4) and (5) is stationary. Estimation of equations (4) and. It should be noticed that the size of the parameters δ 6 and γ 8 on the error correction term in (4) and (5) are not necessarily indicative of the speed of adjustment of money demand to their long-run level (see, for example, Mehra (1991) for a detailed explanation on this point). 5. 7. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(9) (5) by ordinary least square is in general inappropriate [see, for example, West (1988)]. An alternative procedure suggested by Small and Porter (1989), which can avoid the problem due to the stationarity of one of the regressors in the long-run money demand model, is to replace the lagged value of the long-rum random disturbance term by the lagged levels of the variables and estimate the short-run and long-run parameters jointly.. In words, one can. substitute the equation (2) into the equation (4), and obtain a pooled equation like (6) as follows: n1. n2. s =0. s =0. n3. n4. n5. s =0. s =1. ∆mt = δ 0 + ∑ δ 1s ∆yt − s + ∑ δ 2 s ∆rstb− s + ∑ δ 3 s ∆rste− s + ∑ δ 4 s ∆svt − s + ∑ δ 5 s ∆mt − s s =0. + δ 6 (mt −1 − α 0 − α 1 yt −1 − α 2 rs. − α 3 rs. b t −1. (6). − α 4 svt −1 ) + ε t .. e t −1. And plug the equation (3’) into the equation (4), which would give a combined equation of modified model as follows: n′1. n′ 2. n′ 3. n′ 4. n′ 5. s =0. s =0. s =0. s =0. ∆mt = γ 0 + ∑ γ 1s ∆yt − s + ∑ γ 2 s ∆cryt − s + ∑ γ 3 s ∆rstb− s + ∑ γ 4 s ∆crrstb− s + ∑ γ 5 s ∆rste− s s =0. n′ 6. n′ 7. s =0. s =1. + ∑ γ 6 s ∆svt − s + ∑ γ 7 s ∆mt − s + γ 8 (mt −1 − β 0 − β 10 yt −1 − β11cryt −1 − β 20 rstb−1. (7). − β 21crrstb−1 − β 3 rste−1 − β 4 svt −1 ) + ξ t . To obtain an expansion form, one can rearrange the terms in equations (6) and (7): n1. n2. s =0. s =0. n3. n4. n5. s =0. s =0. s =1. ∆mt = (δ 0 − δ 6α 0 ) + ∑ δ 1s ∆yt − s + ∑ δ 2 s ∆rstb− s + ∑ δ 3 s ∆rste− s + ∑ δ 4 s ∆svt − s + ∑ δ 5 s ∆mt − s + δ 6 mt −1 − δ 6α 1 yt −1 − δ 6α 2 rs. b t −1. − δ 6α 3 rs. e t −1. (6’). − δ 6α 4 svt −1 + ε t ,. and n′ 2. n′1. n′3. n′ 4. s =0. s =0. ∆mt = (γ 0 − γ 8 β 0 ) + ∑ γ 1s ∆yt − s + ∑ γ 2 s ∆cryt − s + ∑ γ 3 s ∆rstb− s + ∑ γ 4 s ∆crrstb− s s =0. s =0. n′ 5. n′ 6. n′ 7. s =0. s =0. s =1. + ∑ γ 5 s ∆rstb− s + ∑ γ 6 s ∆svt − s + ∑ γ 7 s ∆mt − s + γ 8 mt −1 − γ 8 β10 yt −1 − γ 8 β11cryt −1 − γ 8 β 20 rstb−1 − γ 8 β 21crrstb−1 − γ 8 β 3 rste−1 − γ 8γ 4 svt −1 + ξ t .. 8. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics. (7’).

(10) As can be seen, the long- and short-run parameters of the money demand model now appear in equations (6’) and (7’). By Phillips (1986) as well as Sims, Stock, and Watson (1990), we know that as long as the nonstationary variables appearing in equations (6’) and (7’) are cointegrated, regressions (6’) and (7’) can be estimated using a consistent estimation procedure and are not “spurious”. Besides, the second method has a distinct advantage over the first one. To test hypotheses about the long-run parameters of equations (6’) and (7’), it is easier to do so under the second framework than under the two-step method.. The reason is that the residuals in. the equilibrium model estimated in step one of the first procedure are likely to be serially correlated and possibly heteroscedastic. unless further adjustments are made.. Thus, the usual t- and F-ratio test statistics are invalid. In contrast, the residuals in the money demand regression. equations (6’) and (7’) are likely to be well behaved, validating the use of the standard test statistics in conducting inference. Furthermore, all parameters in the equations (2) and (3), as well as in (4) and (5) can be recovered from those of (6’) and (7’).. For example, the long-run income elasticity can be. recovered from the long-run part of the model (6’) and (7’). Note that calculation of the standard errors of the individual parameter to long-run income, opportunity costs and financial risks is not straightforward because the parameters come out in (6’) and (7’) in a nonlinear manner.. 3.. Empirical Analysis. 3.1. Data Explanation In this section, the money demand regressions (6’) and (7’) are estimated using Taiwan’s quarterly data from 1985:1 to 2001:4. The data consist of seasonally adjusted observations. All of these data are taking from AREMOS Economic Statistical Databanks of Ministry of 9. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(11) Education, Taiwan.. The money demand regressions include the levels and first-differences of. money, income, opportunity costs, trade amount of stock, private final consumption expenditure and transaction amount using credit card. index.. Real balance is M1b deflated by consumer price. The scale variable Y is real gross domestic product (GDP).. The data of SV is real. trading value of stock market, which is trading amount of stock market deflated by consumer price index. The data of cr ratio is constructed by the transaction amount using credit card divided by private consumption expenditure The monetary aggregates are defined by Central Bank.. Since components of M1b consist. of currency (CU), checkable deposits (CD), passbook deposits (PD) and deposit money passbook savings deposits (DPSS), we calculate a weighted average rate of return on M1b using rates on the components of these aggregates as follows:. RM 1b = (. DPSS PD × rate on PD) + ( × rate on DPSS ), M 1b M 1b. where RM1b is the own rate of return of M1b. Note that currency and checkable deposits enter into with a zero weight because they do not pay any explicit rate of return.. We use the variable. rates on passbook deposits and deposit money passbook savings deposits of First Commercial Bank as proxies for these two rates. The proxy of private bond rate we use is a variable rate on 3-month time deposits-First Commercial Bank. The proxy of the capital gain or loss on equity is constructed by the growth rate of stock price index (1968 = 100).. 3.2. Empirical Procedure Traditionally, statistical evaluation of an econometric model focuses on “in-sample” analysis of the residuals from a fitted model. This methodology has powerful theoretical and practical justification. However, it is not always particularly natural or effective. A number of studies 10. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(12) [see, for example, Christ (1956) and Goldberger (1959), each of which evaluates the predictive ability of the Klein-Goldberger model of the U.S. economy] find that models that seem to fit well by traditional in-sample criteria do poorly at out-of-sample prediction.. This has led observers. such as Klein (1992) to argue that the “...ability to make useful ex-ante forecasts is the real test of a model.” A very general test of predictive ability, which is suggested by Diebold and Mariano (1995), is one that tests for equal forecast accuracy across two demand functions to using outside the sample period.6. This test is similar in the spirit to that of Vuong (1989) in the sense that it. proposes methods for measuring and assessing the significance of divergences between models and data. Furthermore, this test is based directly on predictive performance and allows forecast errors to be potentially non-Guassian, nonzero mean, serially correlated, and contemporaneously correlated. To construct a test of this type, throughout, we assume that the forecasting models are parametric. The parameter estimates are a function of observables known at time t. Then the forecast is based upon a function of the parameter estimates. The sample is split into in-sample and out-of-sample portions. As shown below, unit root and cointegration test results together imply that equations (6’) and (7’) can be consistently estimated by ordinary least squares and the resulting parameter estimates are not subject to the spurious regression phenomenon.7. However, as West (1988). points out, if a single variable in equation (2) and (3’) is stationary, then ordinary least squares estimates are inconsistent. In that case, West suggests using an instrumental variables procedure. 6. Suppose we wish to evaluate the accuracy of two models, call them Model 1 and Model 2. Let u1t and u 2t be. the scalar forecast errors from the two models. Let L(u it ) be the measure of forecast accuracy. We have L(u it ) = u it2 and L(u it ) = u it . Let Ft = L(u 2t ) − L(u1t ) and define µ ≡ E (Ft ) . The two models forecast equally. well if µ = 0 . Model 1 forecasts better than Model 2 if µ > 0 , and conversely if µ < 0 . 7 See Granger and Newbold (1974) and Engle and Granger (1987). 11. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(13) Moreover, Mehra (1993) also points out that if the contemporaneous values of the explanatory variables in equations (6’) and (7’) are correlated with the disturbance term, consistent estimation requires an instrumental variables procedure. To avoid those problems described above, we estimating equations (6’) and (7’) by generalized method of moments (GMM).. GMM estimation obtains consistent parameter. estimates even when U in equation (2) and V in equation (3’) are serially correlated and/or heteroscedastic and/or not normally distributed. Before estimating the M1b money demand regressions, we choose ni and n ′j by AIC.. The instruments for both regressions are set to. consist a constant and four lagged values of all first-difference variables. We also examine whether the short-run dynamic money demand equation is properly specified. The method used here is to check the null hypothesis that the error term is orthogonal to instruments using Hansen (1982) statistics procedure.. The Hansen statistic tests for the. instrument-residual orthogonality. Suppose q is the number of instrumental variables, and r is the number of parameters to be estimated. Under the null hypothesis, the test statistic is asymptotically distributed as χ q2− r . Then, we examine whether the modified model, called unrestricted model, dominate the traditional model, called restricted model, using two in-sample diagnostic tests. The first test checks for the null hypothesis that the restricted model is correctly specified. Let T be the number of observations, k be the number of regressors for restricted model and l be the number of additional regressors for unrestricted model.. This hypothesis may of course be tested by. computing an ordinary F statistics as. ( RSSR − USSR) / l , (USSR /(T − k − l ). 12. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(14) where RSSR and USSR are the sums of squared residuals from restricted model and unrestricted model, respectively. This is an example of what some authors, notably Pagan (1984) and Pagan and Hall (1983), call “variable addition tests”.. If the resulting test statistic is large (so that the. associated P value is small), it is plausible to reject the null hypothesis and thus conclude that the restricted model is misspecified.. The second in-sample test method adopted in this paper is so. called noise ratio. The test method is based on signal extraction framework (see Appendix for a detailed description), which is developed by Durlauf and Hall (1989) and applied by Durlauf and Maccini (1995) to examine an inventory model. The noise, which places a lower bound on the ability of the model to explain the data, is useful in ranking the empirical performances of models under consideration if the model is correctly specified. Finally, the GMM estimates are employed to construct a statistics proposed by Diebold and Mariano (1995) to test whether the out-of-sample point predictions of modified money demand yield significant improvements over those of the traditional one. In carrying out this exercise, we reserved the last 12 data points-corresponding to the period 1999:1 through 2001:4-for forecasting performance and postsample tests of equal forecast accuracy for two competing models. The models (6’) and (7’) above are estimated up to the end of 1998.. The estimated. values of equations are then used to forecast the money demand for 4 forecasting horizons, namely one, two, three and four quarters ahead over the period 1999:1 to 2001:4.. This process. will be continued for all remaining observations and both mean square prediction error (MSPE) and mean absolute prediction error (MAPE) statistics are calculated over the four forecasting horizons. The parameters and hence MSPE as well as MAPE for these models are also sequentially re-estimated as described above by both rolling and recursive estimation methods. We employ these estimators to construct t ratios for testing whether modified money demand yield significant improvements over the traditional one in the sense of out-of-sample point 13. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(15) prediction.. 3.3. Empirical Results Unit Root Test Results Equations (2) and (3’) have been written as cointegrating regressions. This, of course, presumes that each of the series considered is integrated of order one (i.e., I (1) in the traditional notation), which prompts the researcher to test for unit roots in the time series under consideration. In this paper, we use two unit root tests to check the stationarity of time series. The first statistics we used is the GLS-detrended Dickey-Fuller statistics (DF-GLS), which is proposed by Elliot, Rothenberg, and Stock (1996).. The DF-GLS statistics is derived by a. simple modification of the ADF tests in which the data are detrended so that explanatory variables are “taken out” of the data prior to running the test regression. The second statistics we used is KPSS statistics, which is developed by Kwiatkowski, Phillips, Schmidt, and Shin (1992). The KPSS test differs from the other unit root tests in that the series is assumed to be (trend-) stationary under the null. When using those classical methods in trying to determine the nature of non-stationarity in time series data, it would be robust to perform tests of the null hypothesis of stationarity as well as tests of the null of a unit root.. For these reasons we also conduct KPSS tests. In running DF-GLS statistics to test the presence of unit roots to these variables in levels and. the first differences, we set the maximum order of autoregression to be ten8 and apply the AIC criterion to select the optimal lag lengths.. In running KPSS statistics to test for the existence of. stationary to these variables in levels and the first differences, the selection method of bandwidth. 8. We use an information criterion selection method proposed by Hayashi (2000, p. 594) to choose a maximum lag. 14. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(16) parameter we used is Newey and West’s (1994) Bartlett kernel based estimators.. The reported. critical values for the LM test statistic are based upon the asymptotic results presented in KPSS (Table 1, p. 166). The test results are reported in Table 1. For the null of levels of the series, except for rs e , the entries in the columns for DF-GLS and KPSS indicate that all variables cannot reject the null hypothesis of nonstationary at the 5 percent, or even the 1 percent significant level. After first differencing, with no exception, the entries in the columns for DF-GLS and KPSS indicate that all series reject the null hypothesis of nonstationary at the 5 percent significant levels.. Suppose. that we accept the combination of results from the DF-GLS and the KPSS tests, these results suggest that presence of a single unit root in m, y, sv and rs b , and financial opportunity cost variable rs e does not have a unit root and is thus stationary.. Cointegration Test Results A basic assumption that is necessary to yield reliable estimates of the money demand parameters is that U in equation (2) and V in equation (3’) are stationary. Since the levels of the variables included in equations (2) and (3’) are generally nonstationary, the stationary of U and V requires that these nonstationary variables be cointegrated as discussed in Engle and Granger (1987).. For this reason, the existence of a long-run equilibrium relationship among the levels of. the nonstationary variables in equations (2) and (3’) has to be checked. The intuition behind the definition of cointegration is that even if each time series is nonstationary, there might exist linear combinations of such time series that are stationary. that case, multiple time series are said to be cointegrated and share some common stochastic trends. We can interpret the presence of cointegration to imply that long-run movements in these cointegrated time series are related to each other. That is, the existence of a long-run 15. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics. In.

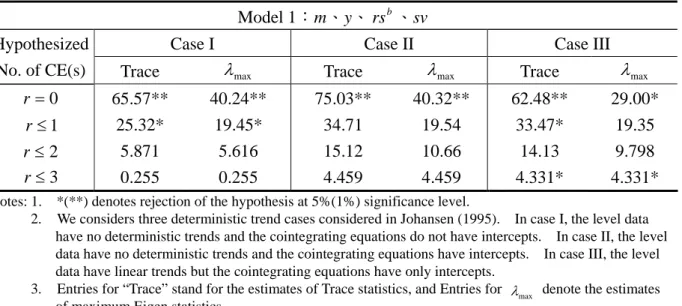

(17) equilibrium relationship among the levels of the nonstationary variables is proven by the presence of cointegration. To study the long-run features for these two sets of time series, the approach used here, but by no means the only one available in practice, is generally known as the Johansen procedure. The unit root test results presented above imply that except for rs e all other variables included in the long-run money demand equations (2) and (3’) are nonstationary.. That is to say. m, y, sr b , sv, cry, and crrs b are integrated of order 1, but rs e is integrated of order 0. Let Model 1 and Model 2 present demand equation (2) and (3’), respectively. Corresponding to our model setting, we consider the three possibilities of cointegration regression model. Case I allows for neither deterministic trends in level data nor intercepts to be presented in the cointegration relations. In case II, the level data have no deterministic trends, but there are intercepts presented in the cointegration relations. Case III specifies a model with linear trends in the data, but no any intercept in the cointegration space. Table 2.1 and Table 2.2 present tests of the null hypothesis of r cointegrating vectors against the alternative of r + 1 cointegrating vectors for a series of two alternative models considered. The results of the trace and maximum eigenvalue tests for the money demand models are provided. As shown in the tables, no matter which case is applied, both Model 1 and Model 2 are cointegrated. The entries in column for trace statistics indicates that there, at least, are one cointegrating equation at 5% significance level among these variables for both models. The results of maximum eigenvalue tests also provide the similar conclusion for both models.. These. test results suggest that, for both models, a reliable cointegration among these nonstationary variables is present.. 16. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

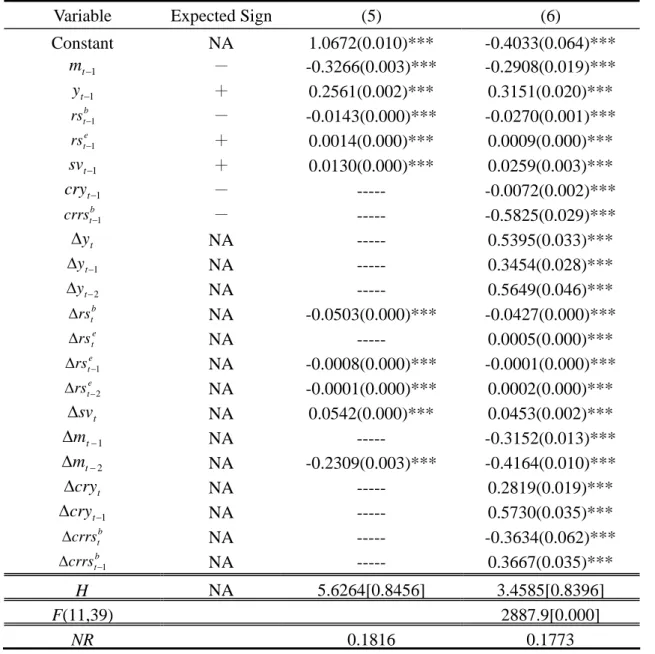

(18) Estimating and In-Sample Evaluating the Money Demand Regressions The results of estimating regressions (6’) and (7’) are reported in Table 3. The cell in the table that denoted by OLS or GMM in each column indicates the estimation method that is used in the regression analysis.. 9. The specifications of both models, which can be shown by looking. at the entries in the rows for H, appear acceptable.. The Hansen test of instrument-residual. orthogonality is reported in the row for H. As indicated by the p-value, the entry in this row does not reject the hypothesis of instrument-residual orthogonality for the specification. Thus, the null hypothesis that both equations (6’) and (7’) are correctly specified is not rejected by these tests for the Taiwan data set. In Table 3, the entries in each column present both models as the results of scale, opportunity costs, and transaction asset holding variables. The coefficients are estimated plausibly for both equations. All estimated coefficients, which provide reasonable point-estimates of the long-run and short-run parameters, possess the theoretically correct signs and are generally statistically significant. We derive the point estimates of the long-run real GDP and market opportunity cost elasticities from the long-run parts of regressions (6’) and (7’). The estimated long-run real GDP elasticities in regressions (6’) and (7’) are, respectively, 0.8 and 1.1. And money market opportunity cost elasticities in regressions (6’) and (7’) are, respectively, 0.04 and 0.09. Moreover, in Table 3, the testing results of two in-sample diagnostic statistics provide evidence that credit card usage substantially affects Taiwan’s demand for money. First, the entry in the row for F indicates that, as indicated by the P value, the estimates of variable addition test statistics, denoted by F, does reject the null hypothesis that the traditional model is. 9. We have deleted insignificant variables from the regressions. 17. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

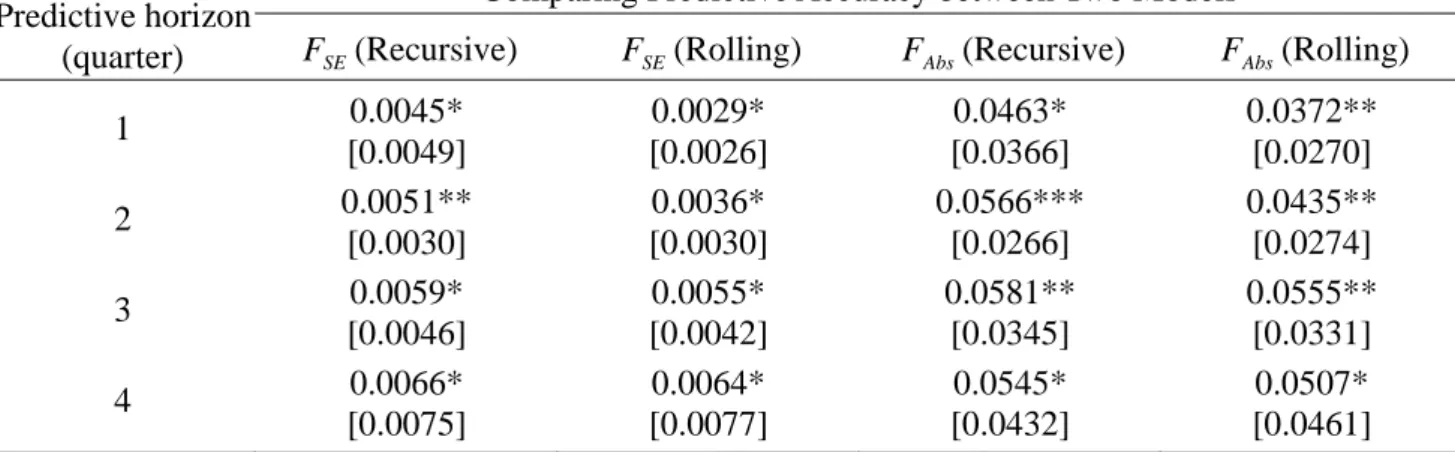

(19) misspecified. Second, the comparison of entries in the row for NR indicates that the modified model performs better than the traditional model, since the noise ratio value for the modified model is lower than that of the traditional model.. Overall, the evidences disallow acceptance. of the null hypothesis, and thus conclude that the traditional model is misspecified in the sense of in-sample test. Nevertheless, as shown below, the modified model that seem to fit well by conventional in-sample criteria do perform poorly at out-of-sample prediction.. Evaluating Forecast Accuracy Table 4 reports mean square prediction error (MSPE) and mean absolute prediction error (MAPE) of money demand for the forecast horizon of one, two, three and four quarters over the forecasting period.. The results from the forecasting exercise are of considerable interest: in all. instances the estimated traditional model clearly outperforms the modified model across the range of forecasting horizons. However simply comparing the values of the MSPE or the MAPE, does not give any idea of the significance of the difference. Therefore, we also adopt the test suggested by Diebold and Mariano (1995), and the testing results are reported in the Table 5. The entries in all cells show that the superiority of the traditional model relative to the modified model is slightly supported since the null of equal accuracy is rejected by t ratios for both regression methods and all forecasting horizons. Therefore, the testing results from Table 4 and Table 5 provide evidence that, in predicting demand for money, the traditional money demand model may still be more useful than that of the modified model. 4. SUMMARY. Predication is of fundamental importance in all of the sciences, including economics.. 18. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(20) Forecast accuracy is obviously important to users of forecasts because forecasts are used to guide decisions. Predictive performance and model adequacy are inextricably linked─predictive failure implies model inadequacy. Thus, comparisons of forecast accuracy are principally important to economists interested in discriminating among competing economic models. It has been recognized plausible in the literature that there may be a relevant credit card usage helping to determine the demand for money. Empirically, many economists have noted that the use of credit cards significantly reduces the amount of currency, which is required in transactions [see, for example, Duca and Whitesell (1995), Lin (1993, 1997) and among others]. However, the findings reported in this paper are in sharp contrast to the conventional wisdom, while taking comparisons of forecast accuracy between different money demand models into consideration. In this paper we re-examined models of demand for money with and without credit card usage by using Taiwan’s macroeconomic data. It is found that the money demand model with credit card usage that seem to fit well by conventional in-sample criteria do perform poorly at out-of-sample prediction. We believe that our results are significant, contrasting with much, if not all, of the extant empirical evidence on this issue. Overall, our finding suggests that the traditional money demand model, interpreted carefully and with allowance made for complex short-run dynamics, may still be usefully applied.. References: Akhand, H. and Milbourne, R., (1986), “Credit Cards and Aggregate Money Demand,” Journal of Macroeconomics, 8, pp. 471-78. Christ, C., (1956), “Aggregate econometric models”, American Economic Review, 66, 385-408. 19. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(21) Diebold, F. X. and R. S. Mariano, (1995), “Comparing Predictive Accuracy,” Journal of Business and Economic Statistics, 13, pp. 253-63. Duca, J. V. and Whitesell, W. C., (1995), “Credit Cards and Money Demand: A Cross-sectional Study,” Journal of Money, Credit, and Banking, 27, pp. 604-23. Durlauf, S. N. and R. E. Hall, 1989, “Bounds on the Variances of Specification Errors in Models with Expectations,” NBER working Paper No. 2936. Durlauf, S. N. and M. A. Hooker, 1994, “Misspecification versus Bubbles in the Cagan Hyperinflation Model,” in Colin P. Hargreaves ed., Nonstationary Time Series Analysis and Cointegration, Oxford University Press. Durlauf, S. N. and L. J. Maccini, 1995, “Measuring noise in inventory models,” Journal of Monetary Economics, 36, 65-89. Elliott, Graham, Thomas J. Rothenberg and James H. Stock, (1996). “Efficient Tests for an Autoregressive Unit Root,” Econometrica, 64, pp. 813-36. Engle, R. F. and C. W. J. Granger, (1987), “Cointegration and Error-Correction: Representation, Estimation and Testing,” Econometrica, 55, pp. 251-76. Friedman, M., (1988), “Money and the Stock Market,” Journal of Political Economy, 96, pp. 221-245. Goldberger, A.S., (1959), Impact Multipliers and Dynamic Properties of the Klein-Goldberger Model, Amsterdam: North-Holland. Goldfeld, S. M., (1973), “The Demand for Money Revisited” Brookings Papers on Economic Activity, 3, pp. 577-683. Granger C. W. J., and P. Newbold, (1974), “Spurious regressions in Dynamic Econometrics,” Journal of Econometrics, 2, pp. 111-20. Hayashi, Fumio., (2000), Econometrics, Princeton University Press. Hendry, D. F. and N. R. Ericsson, (1991), “An Econometric Analysis of U.K. Money Demand in Monetary Trends in the United States and the United Kingdom by Milton Friedman and Anna J. Schwartz” American Economic Review, 81, pp. 8-38.. 20. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(22) Hendry, D. F., A. R. Pagan, and J. D. Sargan, (1983), “Dynamic Specification,” In Handbook of Econometrics, edited by Z. Griliches and M. Intriligator, Amsterdam: North Holland. Hendry, D. F. and J. F. Richard, (1982), “On the Formulation of Empirical Models in Dynamic Econometrics,” Journal of Econometrics, 20, 3-33. Hansen, L. P., (1982), “Large Sample Properties of The Generalized Method of Moments Estimators,” Econometrica, 50, pp. 1029-53. Hester, D. D., (1972), “Monetary Policy in the ‘Checkless’ Economy,” Journal of Finance, 27, pp. 279-93. Hetzel, R. L. (September/October 1989), “M2 and Monetary Policy,” Economic Review (Richmond), pp. 14-29. Hetzel, R. L. and Mehra, Y. P., (1989), “The Behavior of Money Demand in the 1980s,” Journal of Money, Credit, and Banking, 21, pp. 455-63. Johansen, Soren (1995), Likelihood-based Inference in Co-integrated Vector Autoregressive Models, Oxford University Press. Klein, L.R., (1992), “The Test of a Model is It's Ability to Predict”, manuscript, University of Pennsylvania. Kwiatkowski, D., P. C. B. Phillips, P. Schmidt & Y. C. Shin (1992). “Testing the Null Hypothesis of Stationary against the Alternative of a Unit Root,” Journal of Econometrics, 54, pp. 159-78. Lewis, K. A., (1974), “A Note on the Interest Elasticity of the Transactions Demand for Cash,” Journal of Finance, Vol. 29, pp. 1149-52. Lin, C-Y and J-C Lee, (1989), “The Velocity of Money and the Stock Market,” Quarterly Journal of the Central Bank, 11, pp. 38-45, (in Chinese). Lin, C-Y, (1993), “Demand for Money and Credit Card: An Intrinsic Analysis,” Quarterly Journal of the Central Bank, 15, 4, pp. 56-87. (in Chinese). Lin, C-Y, (1997), “Taiwan’s M2 Money Demand—An Analysis of the Impact of Systematic Components,” Quarterly Journal of the Central Bank, 19, 1, pp. 40-70. (in Chinese).. 21. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(23) Marcus, E., (1960), “The Impact of Credit Cards on Demand Deposit Utilization,” Southern Economic Journal, Vol. 26, pp. 314-16. Mehra, Y. P., (May/June 1991), “An Error-Correction Model of U.S. M2 Demand,” Economic Review (Richmond), pp. 3-12. Mehra, Y. P., (1993), “The Stability of the M2 Demand Function: Evidence from an Error-Correction Model,” Journal of Money, Credit, and Banking, 25, pp. 455-60. Newey, W. and K. West, (1994), “Automatic Lag Selection in Covariance Matrix Estimation,” Review of Economic Studies, 61, pp. 631-53. Pagan, A.R., (1984) “Model Evaluation by Variable Addition,” Chapter 5 in Quantitative Economics and Econometric analysis, eds. K. F. Wallis and D. F. Hendry, Oxford, Basil Blackwell. Pagan, A.R. and A.D. Hall, (1983) “Diagnostic tests as residual analysis,” Econometric Reviews, 2, 159-218. Phillips, P. C. B., (1986), “Understanding Spurious Regressions in Econometrics," Econometrica, 55, pp. 277-301. Sastry, A. S. R., (1970), “The Effect of Credit on Transactions Demand for Cash,” Journal of Finance, Vol. 25(4), pp. 777-81. Sastry, A. S. R., (1971), “The Effect of Credit on the Interest Elasticity of the Transaction Demand for Cash: Reply,” Journal of Finance, Vol. 26(5), pp. 1163-65. Sims, J. H. Stock, and M. W. Watson, (1990), “Inference in Linear Time Series Models with Some Unit Root,” Econometrica, 58, pp. 113-44. Small, D. H., and R. D. Porter, (1989), “Understanding the Behavior of M2 and V2” Federal Reserve Bulletin, pp. 244-54. Tobin, J., (1958), “Liquidity Preference as Behavior Towards Risk,” Review of Economic Studies, 25, 67, 65-86. Viren, M. (1992), “Financial Innovations and Currency Demand: Some new Evidence,” Empirical Economics, Vol. 17(4), pp. 451-61.. 22. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(24) Vuong, Q. H. (1989), “Likelihood Ratio Tests for Model Selection and Non-nested Hypotheses,” Econometrica, 57, pp. 307-33. West, K. D., (1988), “Asymptotic Normality, When Regressors Have a Unit Root” Econometrica, 56, pp. 1397-1417. White, K. J., (1976), “The Effect of Bank Credit Cards on the Household Transactions Demand for Money,” Journal of Money, Credit, and Banking, Vol. 8, pp. 51-61.. Table 1. The Results of Unit Root Test. Level Variable Equation. 1st Difference. DF-GLS. Equation. KPSS. DF-GLS. KPSS. includes Lags Statistics Band Statistics includes Lags Statistics Band Statistics m y. Both Both. 9 1. -2.100 -1.086. 6 6. 0.158* 0.247**. Const Both. 0 0. -3.641** -7.024**. 5 3. 0.360 0.074. rs b rs e sv cry. Both. 1. -1.980. 6. 0.174*. Const. 0. -5.031**. 4. 0.119. Const Const. 3 10. -2.418* -0.374. 4 6. 0.302 0.613*. Const Const. 1 9. -10.14** -2.354*. 12 4. 0.128 0.279. Both. 9. -3.140. 6. 0.272**. Both. 0. -8.902**. 1. 0.117. Const. 9. -1.489. 6. 0.943**. Const. 1. -4.795**. 1. 0.247. crrs. b. Notes:1. *(**) denotes rejection of the hypothesis at 5%(1%) significance level. 2. DF-GLS stands for the GLS-detrended Dickey-Fuller unit root test developed by Elliot, Rothenberg, and Stock (1996), and KPSS denote a unit root test developed by Kwiatkowski, Phillips, Schmidt, and Shin (KPSS, 1992).. 3.. The optimal lags for DF-GLS test were chosen by AIC (Akaike information criterion). We use an information criterion selection method proposed by Hayashi (2000, p. 594) to choose a maximum lag, which is equal to 10. The term “Band” in the KPSS stands for selected automatic bandwidth using Newey and West’s (1994) Bartlett kernel based estimators. The term “Const” stands for the test regression including constant only and the term “Both” denotes the test regression including both constant and linear trend.. 23. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(25) Table 2.1 The Result of Cointegration Test for Traditional Money Demand Model 1:m、y、 rs b 、sv Hypothesized. Case I. Case II. Case III. No. of CE(s). Trace. λmax. Trace. λmax. Trace. λmax. r=0. 65.57**. 40.24**. 75.03**. 40.32**. 62.48**. 29.00*. r ≤1. 25.32* 5.871. 19.45* 5.616. 34.71 15.12. 19.54 10.66. 33.47* 14.13. 19.35 9.798. 0.255. 0.255. 4.459. 4.459. 4.331*. 4.331*. r≤2 r≤3 Notes: 1. 2.. *(**) denotes rejection of the hypothesis at 5%(1%) significance level. We considers three deterministic trend cases considered in Johansen (1995). In case I, the level data have no deterministic trends and the cointegrating equations do not have intercepts. In case II, the level data have no deterministic trends and the cointegrating equations have intercepts. In case III, the level data have linear trends but the cointegrating equations have only intercepts. 3. Entries for “Trace” stand for the estimates of Trace statistics, and Entries for λmax denote the estimates of maximum Eigen statistics.. Table 2.2. The Result of Cointegration Test for Modified Money Demand Model 2:m、y、cry、 rs b 、 crrs b 、sv. Hypothesized. Case I. Case II. Case III. No. of CE(s). Trace. λmax. Trace. λmax. Trace. λmax. r=0. 132.8**. 46.82**. 153.0**. 46.91**. 128.8**. 38.97. r ≤1. 85.99** 54.30**. 31.68* 22.16. 106.1** 69.52**. 36.61* 25.67. 89.81** 54.23*. 35.58* 21.48. 31.59**. 16.81. 43.85**. 20.99. 32.76*. 19.37. 14.78*. 11.75*. 22.86*. 16.74*. 13.38. 8.581. 3.029. 3.029. 6.126. 6.126. 4.803*. 4.083*. r≤2 r≤3. r≤4 r≤5 Notes: 1. 4.. *(**) denotes rejection of the hypothesis at 5%(1%) significance level. We considers three deterministic trend cases considered in Johansen (1995). In case I, the level data have no deterministic trends and the cointegrating equations do not have intercepts. In case II, the level data have no deterministic trends and the cointegrating equations have intercepts. In case III, the level data have linear trends but the cointegrating equations have only intercepts. 5. Entries for “Trace” stand for the estimates of Trace statistics, and Entries for λmax denote the estimates of maximum Eigen statistics. 24. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(26) Table 3. The Results of GMM Estimation Variable. Expected Sign. (5). (6). Constant mt −1 yt −1. NA - + - + + - - NA NA NA NA NA NA NA NA NA NA NA NA NA NA. 1.0672(0.010)*** -0.3266(0.003)*** 0.2561(0.002)*** -0.0143(0.000)*** 0.0014(0.000)*** 0.0130(0.000)*** ---------------------0.0503(0.000)*** -----0.0008(0.000)*** -0.0001(0.000)*** 0.0542(0.000)*** -----0.2309(0.003)*** -----------------. -0.4033(0.064)*** -0.2908(0.019)*** 0.3151(0.020)*** -0.0270(0.001)*** 0.0009(0.000)*** 0.0259(0.003)*** -0.0072(0.002)*** -0.5825(0.029)*** 0.5395(0.033)*** 0.3454(0.028)*** 0.5649(0.046)*** -0.0427(0.000)*** 0.0005(0.000)*** -0.0001(0.000)*** 0.0002(0.000)*** 0.0453(0.002)*** -0.3152(0.013)*** -0.4164(0.010)*** 0.2819(0.019)*** 0.5730(0.035)*** -0.3634(0.062)*** 0.3667(0.035)***. NA. 5.6264[0.8456]. 3.4585[0.8396] 2887.9[0.000] 0.1773. rstb−1. rste−1. svt −1 cryt −1 crrstb−1. ∆yt ∆y t −1. ∆y t − 2 ∆rstb ∆rs te ∆rste−1 ∆rs te− 2. ∆svt ∆m t − 1 ∆mt − 2 ∆cryt ∆cryt −1 ∆crrstb ∆crrstb−1. H F(11,39) NR Notes: 1.. 0.1816. *(**)(***) denotes 10%(5%)(1%) significance level. Numbers in the brackets denote the standard error.. 2. H is the statistics of Hansen test. Numbers in the parentheses denote the significance level.. 25. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(27) Table 4. Out of sample forecast: the traditional model versus the modified model The traditional model (without consideration of the usage of credit cards) Predictive horizon MAPE (Recursive) MAPE (Rolling) MSPE (Recursive) MSPE (Rolling) (quarter) 1 0.000270 0.000256 0.013013 0.011922 2 0.000236 0.000249 0.012029 0.012497 3 0.000263 0.000280 0.012811 0.013610 4 0.000258 0.000269 0.012948 0.013575 The modified model (with consideration of the usage of credit cards) Predictive horizon MAPE (Recursive) MAPE (Rolling) MSPE (Recursive) MSPE (Rolling) (quarter) 1 0.004764 0.003114 0.059350 0.049112 2 0.005328 0.003815 0.068603 0.055953 3 0.006170 0.005816 0.070893 0.069133 4 0.006866 0.006689 0.067444 0.064246 Notes: 1.. Predictive horizon 1, 2, 3, and 4 stand for, using the information set available at time t, the forecasting of demand for money at time t+1, t+2, t+3 and t+4, respectively. 2. The sample size is extended period by period with recursive method while it is fixed with rolling method.. Table 5. Test of Equal Predictive Accuracy for two competing models. Predictive horizon (quarter) 1 2 3 4. Comparing Predictive Accuracy between Two Models FSE (Recursive). FSE (Rolling). FAbs (Recursive). FAbs (Rolling). 0.0045* [0.0049] 0.0051** [0.0030] 0.0059* [0.0046] 0.0066* [0.0075]. 0.0029* [0.0026] 0.0036* [0.0030] 0.0055* [0.0042] 0.0064* [0.0077]. 0.0463* [0.0366] 0.0566*** [0.0266] 0.0581** [0.0345] 0.0545* [0.0432]. 0.0372** [0.0270] 0.0435** [0.0274] 0.0555** [0.0331] 0.0507* [0.0461]. Notes: 1. Predictive horizon 1, 2, 3, and 4 stand for, using the information set available at time t, the forecasting of demand for money at time t+1, t+2, t+3 and t+4, respectively. 2. The sample size is extended period by period with recursive method while it is fixed with rolling method. The null hypothesis is “Model 2 forecasts equally well as Model 1.” *(**)(***) denotes rejection of the hypothesis at 25%(10%)(5%) significance level. Numbers in the brackets denote the standard error. 3. FSE measures Ft while L(u it ) = u it2 and F Abs measures Ft while L(u it ) = u it .. 26. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(28) Appendix Durlauf and Maccini (1995) provide a new statistic, noise ratio (NR), which can help us to understand the sources of misspecification of a model by showing how the empirical performance is affected by varying model attributes. In assessing the magnitude of the variance of model noise, first of all, let us define g t and it’s subsequent variant as the implied Euler equation expectation errors of one particular model, which is used to describe the representative agent's behavior in the stock market. Under the null hypothesis that representative agent's behavior in the market is really indicated by Et [h( xt +i ,θ 0 )] , we can write g t = h( xt +i ,θ 0 ) .. Under the null hypothesis that the true economic model holds in the sense of rational expectations, g t equals some combination of the information which lies in I t − I t −1 . We indicate the value of this particular combination of new information as vt .. Then we can write. H 0 : g t = vt ,. where. E[ v t I t ] = 0 .. Under any alternative H 1 , the variable g t may be defined as the sum of vt and the variable N t that indicates the component of g t which deviates from the null. So, H 1 can be written as: H 1 : g t = vt + N t .. We shall refer to N t as model noise. Let L t be the econometrician’s information set, where Lt ⊆ I t , and let proj (⋅ Lt ) denote an operator, which linearly projects a variable onto this information set Lt . 27. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics. Since v t is.

(29) orthogonal to L t by definition, we can construct an estimate of model noise by using the following procedure: proj (⋅ Lt ) ⋅ g t = proj (⋅ Lt ) ⋅ vt + proj (⋅ Lt ) ⋅ N t = N t t .. (3). Although N t is unobservable, one can obtain N t t by using signal extraction procedure.. As. shown in Durlauf and Hall (1989) and Durlauf and Hooker (1994), N t t is the solution to the signal extraction problem that attempts to identify the unobservable N t from the observable data. According to their proof, the variance of estimated model noise is the lower bound on the variance of the actual model noise; that is, var[ proj ( g t Lt )] = var[ proj ( N t Lt )] = var( N t t ) ≤ var( N t ),. ∀g t .. (4). The var[ proj ( g t Lt )] provides a measure of how far the data deviates from the null model. Once estimates of the lower variance bound of the model noise are obtained, it is useful to consider a following estimated metric, which Durlauf and Maccini (1995) define as noise ratio (NR):. NR = var( N t|t ) / var( g t ) This metric normalizes the estimated noise variance bound. Since the numerator of NR is a lower bound on the variance of the model noise, one may interpret the noise ratio as measuring at least what percentage of the variance of the Euler equation innovation is attributable to the variance of the component that deviates from null. In empirical studies of macroeconomic models, it is recognized that no model is likely to be correctly specified due to measurement errors and many auxiliary assumptions employed for the sake of analytical or statistical convenience. In order to ask whether each null model fully explains the data, the standard specification tests could not keep away from having obscurity in 28. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(30) ranking the usefulness of macroeconomic models.. Nevertheless, the assessment of noise ratios. across various models provides a straightforward criterion to evaluate the degree to which a model well approximates observed data behavior. In words, in the sense of in-sample test, a model with a lower noise ratio approximates the data better than a model with a higher noise ratio.. 29. 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(31)

數據

+2

相關文件

The difference resulted from the co- existence of two kinds of words in Buddhist scriptures a foreign words in which di- syllabic words are dominant, and most of them are the

Over there, there is a celebration of Christmas and the little kid, Tiny Tim, is very ill and the family has no money to send him to a doctor.. Cratchit asks the family

There are three major types of personal finance products: mortgages, personal loans and credit cards. Mortgage is a long-term loan that is used for buying a

The remaining positions contain //the rest of the original array elements //the rest of the original array elements.

The min-max and the max-min k-split problem are defined similarly except that the objectives are to minimize the maximum subgraph, and to maximize the minimum subgraph respectively..

Experiment a little with the Hello program. It will say that it has no clue what you mean by ouch. The exact wording of the error message is dependent on the compiler, but it might

To convert a string containing floating-point digits to its floating-point value, use the static parseDouble method of the Double class..

• Adds variables to the model and subtracts variables from the model, on the basis of the F statistic. •