行政院國家科學委員會專題研究計畫 成果報告

股價指數買賣權平價理論的實證研究-探討高頻資料的證

據

計畫類別: 個別型計畫 計畫編號: NSC94-2416-H-004-032- 執行期間: 94 年 08 月 01 日至 95 年 07 月 31 日 執行單位: 國立政治大學財務管理學系 計畫主持人: 杜化宇 報告類型: 精簡報告 處理方式: 本計畫可公開查詢中 華 民 國 95 年 9 月 18 日

1. Introduction

The put-call parity(hereafter, PCP)formalized by Stoll (1969) uses the

no-arbitrage principle to price put(call)options relative to call(put)options. It has

been the subject of numerous empirical studies, but these studies typically focuse on

“direct” tests of whether arbitrage strategies earn ex post profits. They target on

testing the implication of whether the absolute deviation from fair value is less than

the cost of arbitrage. Earlier empirical studies testing the PCP include Gould and

Galai (1974), Klemkosky and Resnick (1979,1980), Evnine and Rudd (1985), Chance

(1987), and Ronn and Ronn (1989), among others. Their conclusions are best

summarized by noting that while PCP holds, on average, there are frequent,

substantial violations of PCP involving both overpricing and underpricing of calls or

puts. However, all previous studies that test PCP use American options. As shown by

Merton (1973), the PCP need not hold for American options, because the possibility

of an early put exercise cannot be completely ruled out when the portfolio is

established. Therefore, it is not possible to conclude from these studies whether, or to

what extent, observed PCP violations are due to market inefficiency or due to the

value of early exercise.

Kamara and Miller (1995) avoid the early exercise problem by testing European

options on the S&P500 stock index traded on the Chicago Board of Options

Exchange (CBOT). Using daily and intradaily prices, they find violations of PCP that

are much less frequent and smaller than those reported in studies using American

options. Furthermore, these violations reflect the premia for immediacy risk.

Some problems regarding the “direct” test of PCP have been addressed by the

recent disagreement regarding the efficiency of the market for exploiting arbitrage

Kleidon (1992) and Miller, Muthuswamy and Whaley (1997) caution that

non-synchronous trading may create the illusion of apparent arbitrage opportunities.

Kamara and Miller (1995) find that these violations of PCP suggest that the trading

strategies underlying PCP are subject to significant liquidity (immediacy) risk.

Variations in the deviations from PCP bounds are systematically positively related to

proxies for liquidity risk in the stock and option markets. Their empirical studies

provide evidence that liquidity (immediacy) risk is a substantial impediment to the

role of arbitrage in pricing assets and is likely to produce deviations from predictions

of arbitrage-based asset pricing models.

Previous arbitrage models have ignored the impact of short-sale restrictions,

early liquidation before maturity, the opportunity cost of funds for index arbitrage,

and the magnitude of transaction costs. Neal (1996) provides a detailed analysis of

actual S&P500 index futures arbitrage trades and directly relates these trades to the

predictions of index arbitrage models. He shows that (1) short-sales restrictions are

unlikely to have a large effect on mispricing. About half the arbitrage trades are

executed for institutions. Since institutions are typically net long in stocks, they can

avoid short-sale restrictions by selling the stock directly; (2) an estimate of the

implied opportunity cost of arbitrage funds is 88 basis points higher than the Treasury

bill rate; (3) the average price discrepancy captured by arbitrage trades is small, which

is consistent with an efficient market for exploiting arbitrage opportunities; (4) early

liquidation is the rule, not the exception, which is consistent with the finding of

Sofianos (1993). He concludes that “ the ability of these models to explain arbitrage

trades, however, is surprisingly low.”

In contrast with previous studies, this paper presents a model of the option price

mean reversion is appealing in several aspects. First, the threshold of mean reversion

should be interpreted more broadly than as simply reflecting proportional transaction

costs, but also as resulting from the tendency of traders to wait for sufficiently large

arbitrage opportunities to open up before entering the market and trading (Neal

(1996), Sofianos (1993)). Second, the assumption of an instantaneous trade can be

replaced with the presumption that it takes some time to observe an arbitrage

opportunity and then execute transactions and that trading is infrequent (Neal (1996)).

Third, in a market with heterogeneous agents who face different levels of transactions

costs, margin requirements, or position limits, agents essentially face no-arbitrage

bands of different sizes. Fourth, in a market with heterogeneous participants, asset

prices may reflect irrational bubbles on “fads” resulting in the persistence of PCP

deviations.

The first contribution of this paper is to employ the variance ratio (VR) statistic

to test for the mean reversion and make an appropriate allowance for

heteroskedasticity when basing inference on the VR statistic by using the Gibbs

sampling approach in the context of a three-state Markov-switching model. The

framework provides a rationale for the behavior of option prices, since it allows us to

understand the question of whether option prices do adjust to put-call parity, and if so,

how fast do they adjust as market frictions are present. As suggested by Kim, Nelson,

and Startz (1998), the sampling distribution of the VR is substantially affected by the

particular pattern of heteroskedasticity during the sample period. Simulation methods

that assume heteroskedasticity or allow for persistence in heteroskedasticity, but not

conditioned on the particular pattern of the historical period, produce a biased test,

leading us to reject the null hypothesis of no mean reversion too often.

suggested by Kim, Nelson, and Startz (1998), that standardizes historical returns,

using the Gibbs sampling approach to allow for uncertainty in parameters and states

while conditioning on the information in the data. Gibbs sampling is a Markov chain

Monte Carlo simulation method for approximating joint and marginal distributions by

sampling from conditional distributions1. Since dividend payments and liquidity premiums exhibit seasonal patterns (Harvey and Whaley (1994) ; Eleswarapu and

Reinganum (1993)), Gibbs sampling makes appropriate use of the information in the

historical data. At the end of each iteration of the Gibbs sampling, we compare the

estimate of the VR from the standardized historical data with the corresponding VR

from “randomized” data. We then estimate a p-value by counting how often the

former falls below the latter.

It is finally found that dividend uncertainty and/or the trading system might play

key roles in explaining equity index arbitrage behavior. The empirical result shows

that PCP deviations from electronic screen-traded DAX index option, which is

calculated as if the dividends are reinvested in the index, displays mean reversion at

long horizons. On the other hand, those deviations from the floor-traded S&P 500

index option, which is not corrected for dividend payments, vary randomly.

Section 2 of this paper first defines the deviation from put-call parity. Section 3

describes the data and introduces two comparable index options. Section 4 presents a

VR statistic for testing mean reversion in a framework of a three-state

Markov-switching variance model. Section 5 introduces an extended version of the

Bayesian Gibbs sampling approach and data augmentation. Section 6 describes the

VR tests based on historical and standardized deviations of data. Section 7 presents

empirical results. Finally, Section 8 concludes the paper.

1

Useful references include Casella and George (1993), Gelfand and Smith (1990), and Chib and Greenberg (1996).

2. Deviations from Put-call Parity

Put-call parity (PCP) is a well-known relation that exists, in a perfect capital

market, between the prices of European call and put options with similar terms on the

same underlying stock. In a frictionless market, the following relation must hold:

Ct− = −Pt It Dt −Xe−r T t( −)/ 365 (1a) ( )/ 365 (1b) T r t t D =

∑

d eτ − τ− t τ=where is the known annualized continuous risk-free interest rate rt

Ct is the market price of the European call at time t

Pt is the market price of the European put at time t

T is the expiration date of the option

X is the exercise (or strike) price of the option

It is the market value of the index at time t

Dt is the present value of the sum of the τ -time known non-stochastic

dividends (dτ) to be paid during the option period.

If the parity condition described in equation(1)is valid and the financial

markets are efficient, then the riskless interest rate for the options’ maturity can be

inferred from equation(1). As mentioned above, when market frictions are present,

the deviations from PCP can fluctuate within a bounded interval without giving rise to

any arbitrage profit. In other words, the implied interest rate derived from equation

(1)may not be riskless.

The implied interest rate as suggested by Brenner and Galai (1986) from

equation(1)of the European PCP is

(

)

' 365 t t t t t I D C P r Ln T t X − − + ⎛ = − × ⎜ − ⎝ ⎠ ⎞ ⎟ (2)Thus, the deviations(et)from PCP can be written as

rt' =rt +et (3) where rt denotes the riskless rate of return.

As described in Neal (1996), the “implied” interest rate, , can be treated as

the opportunity cost of arbitrage funds. Since arbitrageurs face uncertainty about

execution prices, the future value of dividends, the problem of immediacy and early

liqudation, and the magnitude of tracking error, the index arbitrage does not

necessarily provide a risk-free return. It is reasonable to assume that the opportunity

cost of arbitrage funds will exceed the risk-free rate and the deviation can be regarded

as the “risk premium” or reflects the cost of transaction

' t

r

2

. Neal (1996) further found

that the implied opportunity cost of arbitrage funds exceeds the Treasury bill rate and

the arbitrage decision is sensitive to the opportunity cost of funds.

Neal (1996) estimates the implied opportunity cost of arbitrage funds and shows

that the cost is 88 basis points higher than the Treasury bill rate. An opportunity cost

exceeding the risk-free rate is consistent with the risk of index arbitrage as noted in

Kawaller (1987).

The presence of the term allows for short-run deviations from PCP. If the

sequence exhibits mean reversion, then the deviations from equilibrium must be

temporary. Thus, PCP is said to hold. On the other hand, if the sequence

{

is serially random, then the deviations from equilibrium are permanent in nature. Thus,we can reject the theory of PCP. Our “indirect” test, as shown in the following

sections, is to determine whether t e

{ }

et}

t e{ }

e exhibits mean reversion. t2

These transaction costs include bid-ask spread, commission fees, differential interest rates, and execution costs, etc. in both stock and option markets.

3. Data and Two Comparable Equity Index Option: S&P500 and

DAX

Neal (1996) and previous studies ignore the effect of dividend uncertainty on

equity index arbitrage3. To illustrate the importance of dividend uncertainty on arbitrage, we consider two European index options, S&P500 and DAX, for

comparison purposes. The daily closing prices of two equity indices and options are

used. These data, provided by DATASTREAM, cover the period of August 23, 1999

through March 20, 2003. Because options on the S&P500 index are not corrected for

dividend payments, the put-call parity may contain an additive term of dividend

payments as shown in (1a) and (1b), but with unknown. On the other hand, the

DAX index is an example of a performance index (Grünbichler and Callahan (1994)).

On ex-dividend days, the DAX is calculated as if the dividends are reinvested in the

index so that the put-call parity for DAX index options can be expressed as t

D

Ct− = −Pt It Xe−r T t( −)/ 365 In the above equation, the dividend payments do not appear on the functional form of

PCP. In other words, the PCP deviations ( ) from the implied interest rates in

equation (3) are absent of dividend risk.

t

e

Like Neal (1996), we implement the realized dividends, as reported in the

S&P500 and DAX bulletins, as proxies for the future dividends on the PCP model.

The uncertainty of dividend payments can produce large errors of option pricing as

indicated by earlier studies (Harvey and Whaley (1992)).

These are two other specific features which lead to a relatively low level of risk

associated with ex ante arbitrage strategies in DAX as compared with S&P5004. First,

3

As suggested by Harvey and Whaley (1992), Neal (1996) uses the realized dividends, as reported in the S&P500 bulletin, as proxies for future dividends on the cost-of-carry model.

4

the DAX index is narrow, consisting of only 30 blue chips of the German equity

market which represent about 60% of the market capitalization and 85% of the trade

volume. Arbitragers are able to trade a perfect matching basket at reasonable costs and

in a reasonable span of time. Thus, tracking error risk can be avoided and the

execution risk is relatively low. Second, there is little execution risk in the derivatives

(futures and options) market as the German Futures and Options Exchange (DTB) is

an electronic screen-trading market5. It is believed that price discovery is faster in a screen-based trading system, because it is less costly to operate and may therefore

offer lower bid-ask spreads. The possibility of remote access may increase the number

of traders and thereby also lead to an increase in liquidity.

Based on these specific features of Germany’s markets, one would expect that

arbitrage opportunities can be exploited very quickly and that ex ante arbitrage

strategies are nearly risk free. Consequently, the PCP would not allow for large and

long-lasting arbitrage opportunities.

The deviations from equation (3) for S&P500 and DAX are drawn in Figures

1 (a) and (b), respectively. A preliminary look shows that shocks to the deviations for

both indices may be temporary in nature with a tendency to revert to some mean level.

However, the mean for S&P500 is subject to more occasional level shifts over time.

The actual patterns for S&P500 and DAX need more careful investigation. t

e

5

After September 1998, the DTB merged with SOFFEX, the Swiss Options and Futures Exchanges, to create Eurex, a cross-border exchange.

4. Variance Ratio Statistics in a Markov-Switching Variance Model

The indirect test in our model employs variance ratio (VR) statistic, which is

due to Cochrane (1998) and Lo and MacKinlay (1988). This test allow

heteroscedasticity in the data and, more importantly, does not require the assumption

of normality. Under the null of a heteroscedastic random walk process, Lo and

MacKinlay(1989)show that the variance ratio test is more powerful than the

Box-Pierce Q test and the Dickey-Fuller unit root test against several alternative

hypotheses. In addition, it offers a very straight-forward interpretation of how rapidly

a series reverts back to, or diverges from, its mean value.

If one-period deviations are serially random, then we have

et ~iid

(

µ,σ2)

(4) and since the k-period deviation is the accumulation of k successive et,Var

( )

etk =kσ2 (5) The VR statistic is defined in the deviation context as

( )

( )

( )

k e Var e Var k VR k t 1 = t (6)which is unity under the serially random hypothesis. On the other hand, if the series

exhibits mean reversion, so that changes in either direction tend to be offset over time

by moving back toward the starting point, then Var e

( )

tk will be less than k times as large as , such that VR will be less than unity. We therefore take values forVR of one or above as evidence against the PCP model.

( )

tVar e

6

6

The sample variance ratio, VR k , can be expressed as one plus a positively-weighted sum of the first ( )

k-1 sample autocorrelations. As shown by Cochrane (1988), the approximated value of the sample variance ratio is:

( ) 1 1 ( ) 1 2 k j k j VR k j k ρ − = − = +

∑

where ρ( )j is the jth-order sample autocorrelation of one-period deviations in this study. If the

variance ratio is greater than one, less than one, or equal to one, then autocorrelations between

t

One explanation for mean reversion is the presence of a transitory component in

asset prices. To judge whether a sample VR is significantly below unity, one needs to

know the sampling distribution of the VR under the null hypothesis. Poterba and

Summers (1988) and Lo and MacKinlay (1989) use the VR to test for mean reversion

in stock prices and conclude that a transitory component accounted for a substantial

fraction of the variance in stock returns over horizons of several years. The inference

was based on a Monte Carlo simulation of the sampling distribution of the VR under

the null hypothesis of serially random returns.

Kim, Nelson, and Startz (1991) estimate the sampling distribution of the VR by

randomizing actual returns and also suggest a “stratified randomization” that

preserves the historical pattern of high and low volatility periods. The fact that the

latter reveals substantially weaker evidence of mean reversion than the former

suggests that the specific pattern of heteroskedasticity in the sample period may play

an important role in inference. However, their approach assumes that the

econometrician has certain knowledge of the pattern, yet does not exploit any

information from the pattern of heteroskedasticity in the estimation of the VR.

Furthermore, a resampling of returns is limited by segregation into subperiods

according to volatility.

Kim, Nelson, and Startz (KNS, hereafter)(1998) find that the sampling

distribution of the VR is affected by the particular pattern of heteroskedasticity, such

as the Great Depression, during the sample period. They use a model with a

three-state Markov-Switching process estimated by an extension of the Bayesian

Gibbs sampling approach of Albert and Chib (1993) in which the parameters as well

as the unobserved states are viewed as random variables for which we obtain a

deviations are positive, negative, or zero and the series of deviation exhibit “mean aversion”, “mean reversion”, or “random walk”, respectively.

conditional distribution given the data. It suggests two changes in the way that that

interpret the VR in the presence of heteroskedasticity. First, they fully utilize the

information in the data about the pattern of heteroskedasticity in simulating the

sampling distribution of the VR without pretending to have prior knowledge of the

pattern. Second, they modify the VR statistic to make more efficient use of the

information in the data about mean reversion by weighting observations appropriately

based on information in the data about the timing and magnitude of volatility changes.

Following KNS, we consider the following three-state Markov-switching model

of stock index returns:

et ~ N

(

0,σt2)

, (7) σt2 =σ12S1t+σ22S2t+σ32S3t (8) SKt =1 if St =k, and SKt= 0, otherwise;k =1, 2, 3 (9) Pi1+Pi2 +Pi3 =1, where Pr[

St = jSt−1 =i]

= pij, i j, =1, 2, 3 (10) σ12 <σ22 <σ32 (11) where is demeaned deviation, and is an unobserved state variable whichevolves according to a first-order Markov process with transition probabilities in (10). t

e St

The adoption of a three-state Markov switching variance model is suggested by

KNS for several reasons. Porterba and Summers (1988) use VR statistics to

investigate whether stock prices are mean-reverting, taking data that consists of

monthly total returns on all NYSE stocks for both value-weighted and equal-weighted

portfolios from 1926 through 1985. In measuring the statistical significance of the VR

statistic, they implement an estimate of the standard error based on Monte Carlo

simulations assuming independently and normally-distributed returns. Although stock

returns are actually unconditionally non-normal and heteroskedastic with high

VR statistic with heteroskedasticity is no different from that with homoskedasticity. In

other words, it suggests that the degree of persistence in heteroskedasticity does not

affect the distribution of the VR statistic very much.

Instead of using Monte Carlo simulations, which require a distributional

assumption, Kim, Nelson, and Startz (1991) employ “randomization” methods to

estimate the unknown distribution of the VR for the same sample period7. To estimate the distribution of the VR statistic under the null, they first shuffle the date to destroy

any time dependence, and then recalculate the test statistic for each reshuffling. They

presente results for a “stratified randomization” that preserves the historical pattern of

heteroskedasticity. Their results suggest that significance levels are much lower than

previously reported. Even though their stratified randomization provides a way to

retain information in historical heteroskedasticity in returns, their division of the

sample into low- and high-variance states is arbitrary and limited.

KNS criticize the above two papers for (1) Poterba and Summers (1988)

reported a Monte Carlo experiment that mimics the actual persistence of volatility, but

does not preserve the historical pattern. This may be valid when the particular

historical pattern of heteroskedasticity, such as the Great Depression, does not affect

the sampling distribution of the VR statistic. (2) In the presence of persistence in

heteroskedasticity, the randomization destroys any time dependence in variance. Thus,

the usual randomization method may fail, because errors are not interchangeable.

Employing a three-state Markov-switching variance model, KNS find that the

empirical distribution of the VR is much different from that in the homoskedastic case,

7

Randomization focuses on the null hypothesis that one variable is distributed independently of another. Randomization shuffles the data to destroy any time dependence and then recalculates the test statistic for each reshuffling to estimate its distribution under the null. Repeating the experiment, we count how many times the calculated variance ratio after randomization falls below the value of the actual historical statistic in order to estimate the significance level. The advantage of this approach is that the null hypothesis is very simple and no assumptions are made concerning the distribution of stock prices.

when the pattern of heteroskedasticity is the historical one. The distribution has wider

variance and is more skewed than in the homoskedastic case. This suggests that the

VR tests of Poterba and Summers (1988) based on Monte Carlo experiments and

those of Kim, Nelson, and Startz (1991) based on the usual randomization method

have the wrong size, rejecting the null of random returns in favor of mean reversion

5. Bayesian Gibbs Sampling and Data Augmentation

The Markov-switching variance model from (7) to (11) could traditionally be estimated using the maximum likelihood estimation method of Hamilton (1989)

and Hamilton and Susmel (1994). However, the MLE approach, which is based on

asymptotic normality, may not be valid when the sample size is not large enough. In

addition, it is difficult to determine how large the sample size should be in order for

asymptotic normality to hold. In this paper we employ an extended version of Albert

and Chib’s(1993)Bayesian Gibbs sampling approach to estimate the model8.

The Gibbs sampler is a path-breaking technique for generating random samples

from a multivariate distribution by using conditional distributions without having to

compute the full joint density. In regime-switching models, the full joint density is

extremely difficult to calculate, but the conditional distributions are easy to evaluate.

In addition, the Gibbs sampling approach can provide us with a way to deal with

uncertainty associated with underlying parameters and unknown states of the model.

It is an iterative Monte Carlo technique that generates a simulated sample from the

joint distribution of a set of random variables by generating successive samples from

their conditional distribution9.

In the Gibbs sampling approach, all the parameters of the model are treated as

random variables with an appropriate but unknown prior distribution. Thus, random

variables to be drawn in the above model from(7)to(11)are given by

{

, 1,2,...}

, and ~ T t S St = t = σ12,σ22,σ32{

11 12 21 22 31 32}

~ , , , , ,P P P P P P P=Starting from arbitrary initial values of the parameters, Gibbs sampling proceeds by

taking:

8

Advantages of the Gibbs sampling approach over the maximum likelihood method are discussed in detail in Albert and Chib(1993).

9

For more details of the Gibbs sampling approach to a three-state Markov-switching variance model given below, readers are referred to Kim and Nelson (1999).

Step 1:a drawing from the conditional distribution of given the data, , , and ~ S σ12 σ22 2 3 σ P ;then ~

Step 2:a drawing from the conditional distribution of given the data, , ,

and 2 1 σ S~ σ22 2 3 σ P ;then ~

Step 3:a drawing from the conditional distribution of given the data, , ,

and 2 2 σ S~ σ12 2 3 σ P ;then ~

Step 4:a drawing from the conditional distribution of given the data, , ,

and 2 3 σ S~ σ12 2 2 σ P ;then ~

Step 5:a drawing from the conditional distribution of ~

P given the data, , , and . ~ S σ12 2 2 σ 2 3 σ

By successive iteration from step 1 to step 5, the procedure simulates a drawing

from the joint distribution of all the state variables and parameters in the model. It is

straightforward then to summarize the marginal distribution of any of these, given the

data10.

KNS find that the sampling distribution of the VR is affected by the particular

pattern of heteroskedasticity, and that this effect is also substantially important in the

case of daily deviations of PCP. Simulation methods that assume heteroskedasticity or

allow for persistence in heteroskedasticity, but are not conditioned on the particular

pattern of the historical period, produce a biased test, leading the investigator to reject

the null hypothesis of no mean reversion too often. Since dividend payments and a

liquidity premium exhibit seasonal patterns (Harvey and Whaley (1994), Eleswarapu

and Reinganum (1993)) in the data, we follow KNS and consider two new tests of

mean reversion that are conditioned on the information that the data contain the

historical pattern of heteroskedasticity. We employ a resampling strategy for

10

For details of the Gibbs sampling approach to a three-state Markov-switching variance model given above, readers are referred to Kim and Nelson (1999) P219-224.

estimating the sampling distribution of the VR that standardizes historical returns

using estimated variances. Instead of conditioning on the estimates of these variances

and the dates of regime switches, the Gibbs sampling approach is used so as to allow

for uncertainty in these parameters and states while being conditioned on the

6. Tests Based on the Variance Ratios of Historical and Standardized

Deviations

This section suggests a modification of the VR statistic to make more efficient

use of the information in the data about mean reversion by weighting observations

appropriately based on the information in the data about the timing and magnitude of

volatility changes.

Assume that

et ~

(

0,σt2( )

θ)

θ =

{

σ12,σ22,σ32,P11,P12,P21,P22,P31,P32}

where et is the demeaned deviation which shows heteroskedasticity with variance

2 t

σ

θ is a vector of parameters that describes the dynamics of σt2

By standardizing historical returns before calculating the VR test statistic,

appropriate weights can be assigned to observations depending on their volatility. An

additional complication of this approach is that unlike the test based on original

returns, the test statistic itself is subject to sampling variation due to uncertainty in the

parameters that describe the dynamics of heteroskedasticity. Thus, we compare two

distributions:the distribution (due to parameter uncertainty) of the VR test statistic for

standardized historical returns and the distribution of the VR test statistic under the

null hypothesis estimated from randomizing the standardized returns.

A natural way to randomize returns without losing time dependence in historical

returns would be the following:

Step 1:Standardize et to obtain

⎭ ⎬ ⎫ ⎩ ⎨ ⎧ = = e t T e t t t , 1,2,... * σ

Step 3:Destandardize etr* to obtain

{

etr =etr*×σt,t=1,2,...T}

From the above procedure, we obtain the following four data series:

1. original series et

2. standardized series et*

3. randomized standardized series etr*

4. randomized de-standardized series etr

Step 4:Calculate VRs for each series. They are respectively VR

( )

k ,VR*( )

k ,VRr*(

k)

and VRr

( )

k , k =1,2,...K .Step 5:Repeat the Gibbs sampling and steps 1 to 4.

These steps are repeated, say, M times to get the posterior distribution of the VR

for standardized historical returns, VR*

( )

k , and the empirical distribution of the VR under the null of no mean reversion, VRr*( )

k . To estimate the significance level for the test of mean reversion, we count how many times the variance ratio for thestandardized and randomized returns

(

VRr*( )

k)

from Gibbs-sampling-augmented randomization falls below the variance ratio for standardized historical returns( )

(

VR* k)

from Gibbs sampling. For comparison purposes, we also conduct the same analysis for the original returns. Thus, the p-value, which is defined as

[

( )

( )

]

M k VR k VR of No p r >= . for original returns

and

( )

( )

M k VR k VR of No p r ] [ . * * * = >for standardized returns.

It is important to calculate the above p-values exactly rather than using a

standard deviation under an assumption of normality for VR, because its sampling

If the variance of deviations for each time point σt2 or the parameters θ that govern the evolution of are known, then the above procedure would be

straightforward. In practice, or the parameter 2

t

σ

2 t

σ θ associated with has to be

estimated using historical data. Because

2 t

σ

θ is subject to parameter uncertainty, the standardized deviations are also subject to sampling variation.

To incorporate the effect of uncertainty in the parameters associated with the

variance of deviations, we augment the Gibbs-sampling approach introduced in

Section 5 with the standardizing step of the above procedure. As in Section 5, each

run of Gibbs sampling based on historical returns provides us with particular

realizations of the set,

{

St,t=1,2,...T}

and{

}

2 3 2 2 2 1,σ ,σσ , which are used to calculate according to Equation(8). Using , t =1,2,…T, simulated in this way, we can

proceed with the above Steps 1 through 3. 2

t

σ 2

t

σ

If the above procedure is repeated, say, 10,000 times, with each iteration

augmented by simulations of from each run of Gibbs sampling, then we have

10,000 sets of randomized returns. These artificial histories are conditioned on the

information about the pattern of heteroskedasticity contained in the historical returns,

incorporate parameter uncertainty, and are consistent with the null of mean reversion

due to randomization. For each of these 10,000 sets of artificial histories, the variance

ratio statistic is calculated, which can be used to estimate the empirical distribution of

the variance ratio statistic. To estimate the significance level, we calculate the

p-values to know how many times the variance ratios for the artificial histories fall

below the variance ratios for original historical returns. 2

t

7. Empirical Results

The procedures for Gibbs-sampling described in the previous sections are

applied here to the PCP deviations of S&P 500 and the DAX. Gibbs-sampling is run

such that the first 2,000 draws are discarded and the next 10,000 are recorded. We

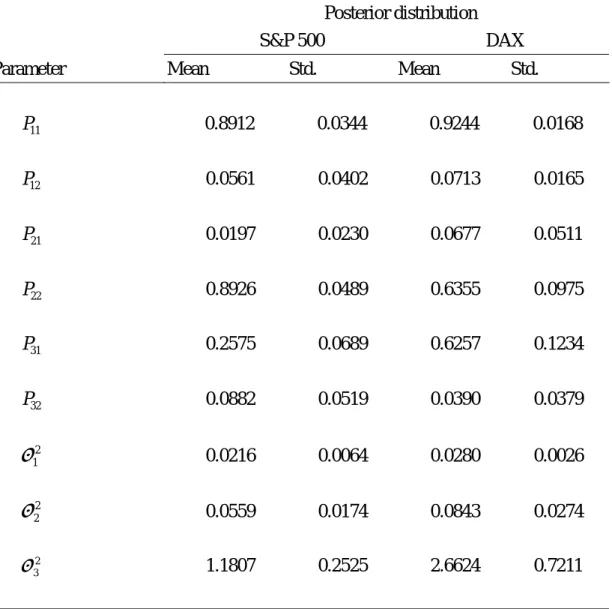

employ almost non-informative priors for all the models’ parameters. Table 1 presents

the marginal posterior distributions of the parameters that result from Gibbs-sampling

for the PCP deviations of S&P 500 and the DAX, respectively. At the end of each run

of Gibbs-sampling, we have a simulated set of

{

St, t =1,2...T}

and thus, of{

Sjt,t =1,2,...T, j=1,2,3}

, and . Figures 2(a), 2(b), 2(c) and Figures 3(a), 3(b), and 3(c) depict probabilities of low-, medium-, and high-variancestates for the PCP deviations of S&P 500 and the DAX, respectively, that result from

the Gibbs-sampling simulation.

3 , 2 , 1 , 2 = j j σ P%

Using the particular realizations of the states and the parameters for each run of

Gibbs-sampling, we can calculate σt2 for t=1,2,LT using equation (8). Thus, when all the iterations are over, we have 10,000 sets of realized variances

{

t t T}

T , 1,2,L ~2 = σ2 =

σ of PCP deviations. Figures 2(d) and 3(d) plot the average of

10,000 sets of σ~T2, which are our estimates of the variance of the S&P 500’s and the DAX’s PCP deviations. Tables 2 (a) and (b) present variance ratios for original daily

deviations from PCP for S&P 500 and DAX, respectively. Only the DAX displays

mean reversions at long horizons. The smallest p-value is 0.028 at 45 days lag.

Table 3 (a) and (b), in which variance ratios for standardized daily deviations

from PCP for S&P 500 and DAX are presented, respectively. The DAX also displays

mean reversion at long horizons and its smallest p-value is 0.028 at a lag of 40 days.

The evidence is weak that the standardized returns approach to estimating the VRs

8. Summary

Previous studies indicate that when market frictions are taken into account, the

deviations from PCP can fluctuate within a bounded interval without giving rise to

any arbitrage profit. This study presents a model of the option price mean reverting to

a function form of PCP. The variance ratio test is employed to examine whether the

deviations of PCP exhibit mean reversion. We make appropriate allowance for

heteroskedasticity when basing inference on the VR statistic by using the

Gibbs-sampling approach in the context of a three-state Markov switching model.

The empirical result shows that PCP deviations from the electronic

screen-traded DAX index options, which are calculated as if the dividends are

reinvested in the index, display mean reversion at long horizons. On the other hand,

those deviations from floor-traded S&P 500 index options, which do not correct for

Table 1:The estimated parameters from the Bayesian Gibbs-sampling approach to a three-state Markov-switching model of heteroskedasticity for S&P 500’s and DAX’s daily PCP deviations

Posterior distribution

S&P 500 DAX Parameter Mean Std. Mean Std.

P11 0.8912 0.0344 0.9244 0.0168 P12 0.0561 0.0402 0.0713 0.0165 P21 0.0197 0.0230 0.0677 0.0511 P22 0.8926 0.0489 0.6355 0.0975 P31 0.2575 0.0689 0.6257 0.1234 P32 0.0882 0.0519 0.0390 0.0379 σ12 0.0216 0.0064 0.0280 0.0026 σ22 0.0559 0.0174 0.0843 0.0274 2 1.1807 0.2525 2.6624 0.7211 3 σ

Table 2(a):Variance ratios for original daily deviations from PCP in S&P500

Lag(days) VR sampling distribution

(

VRr( )

k)

K VR(k) Mean Std Median p-value

2 1.4616 1.0343 0.0621 1.0340 1.0000 5 2.1525 1.0796 0.1266 1.0738 1.0000 10 1.1489 0.9957 0.0578 0.9950 0.9950 15 1.1816 0.9699 0.0922 0.9671 0.9854 20 1.2202 0.9536 0.1177 0.9491 0.9824 25 1.2907 0.9561 0.1385 0.9490 0.9864 30 1.3059 0.9564 0.1602 0.9467 0.9790 35 1.2527 0.9491 0.1812 0.9376 0.9440 40 1.1663 0.9425 0.2004 0.9288 0.8667 45 1.1181 0.9464 0.2172 0.9284 0.7957 50 1.0792 0.9496 0.2341 0.9290 0.7294

Note:1. The sampling distribution is based on Gibbs-sampling-augmented randomization.

2. The p-value is the frequency with which the simulated VR is smaller than the historical sample value, which is observed in the Gibbs-sampling-augmented randomization under the null hypothesis.

Table 2(b):Variance ratios for original daily deviations from PCP in DAX

Lag(days) VR sampling distribution

(

VRr( )

k)

K VR(k) Mean Std Median p-value

2 1.2283 1.0245 0.0648 1.0245 0.9991 5 1.5501 1.0438 0.1184 1.0401 0.9999 10 1.0528 0.9789 0.0471 0.9794 0.9456 15 1.0141 0.9520 0.0808 0.9529 0.7782 20 0.9131 0.9313 0.1043 0.9315 0.4293 25 0.8369 0.9294 0.1237 0.9257 0.2279 30 0.7666 0.9291 0.1450 0.9230 0.1305 35 0.6626 0.9216 0.1671 0.9131 0.0513 40 0.5893 0.9153 0.1859 0.9049 0.0282 45 0.5635 0.9174 0.2007 0.9050 0.0237 50 0.5484 0.9189 0.2158 0.9029 0.0254

Note:1. The sampling distribution is based on Gibbs-sampling-augmented randomization. 2. The p-value is the frequency with which the simulated VR is smaller than the historical

sample value, which is observed in the Gibbs-sampling-augmented randomization under the null hypothesis.

Table 3(a):Variance ratios for standardized daily deviations from PCP in S&P500

Lag(days) VR posterior distribution

(

VR*( )

k)

VR sampling distribution(

VRr*( )

k)

k Mean Std Median Mean Std Median p-value

2 1.5519 0.0209 1.5503 1.0001 0.0346 0.9998 1.0000 5 2.6193 0.0887 2.6043 0.9998 0.0758 0.9981 1.0000 10 1.3209 0.0387 1.3120 0.9982 0.0645 0.9984 1.0000 15 1.4444 0.0788 1.4244 0.9971 0.1047 0.9938 0.9996 20 1.5463 0.0975 1.5243 0.9963 0.1358 0.9911 0.9997 25 1.6176 0.0995 1.6000 0.9959 0.1619 0.9890 0.9995 30 1.6019 0.0992 1.5897 0.9958 0.1850 0.9862 0.9959 35 1.5043 0.0997 1.4955 0.9961 0.2063 0.9827 0.9811 40 1.3640 0.1008 1.3590 0.9966 0.2263 0.9803 0.9228 45 1.2431 0.1001 1.2410 0.9971 0.2449 0.9760 0.8256 50 1.1392 0.1031 1.1396 0.9975 0.2622 0.9726 0.7141

Note:1. The sampling distribution is based on Gibbs-sampling-augmented randomization 2. The p-value is the frequency with which the realizations of the Gibbs sampling of the

posterior distribution are smaller than the corresponding realization under the null hypothesis. 26

Table 3(b):Variance ratios for standardized daily deviations from PCP in DAX

Lag(days) VR posterior distribution

(

VR*( )

k)

VR sampling distribution(

VRr*( )

k)

k Mean Std Median Mean Std Median p-value

2 1.3804 0.0299 1.3852 1.0001 0.0343 1.0002 1.0000 5 2.0731 0.0830 2.0853 1.0001 0.0752 0.9979 1.0000 10 1.1008 0.0201 1.1017 0.9970 0.0642 0.9966 0.9388 15 0.9341 0.0389 0.9332 0.9963 0.1050 0.9931 0.2978 20 0.8265 0.0461 0.8252 0.9960 0.1367 0.9906 0.1166 25 0.8670 0.0449 0.8664 0.9963 0.1632 0.9876 0.2313 30 0.8349 0.0455 0.8347 0.9970 0.1868 0.9845 0.2062 35 0.7005 0.0483 0.7003 0.9976 0.2081 0.9801 0.0641 40 0.6078 0.0504 0.6068 0.9983 0.2281 0.9769 0.0277 45 0.6136 0.0526 0.6121 0.9991 0.2467 0.9728 0.0411 50 0.6213 0.0542 0.6196 1.0000 0.2645 0.9683 0.0580

Note:1. The sampling distribution is based on Gibbs-sampling-augmented randomization. 2. The p-value is the frequency with which the realizations of the Gibbs sampling of the

posterior distribution are smaller than the corresponding realization under the null hypothesis. 27

Figure 1(a):Daily PCP Deviations from S&P500

Figure 1(b):Daily PCP Deviations from DAX

Figure 2(a):Probability of a Low-variance State for S&P500’s PCP Deviations (Gibbs Sampling)

Figure 2(b):Probability of a Medium-variance State for S&P500’s PCP Deviations (Gibbs Sampling)

Figure 2(c):Probability of High-variance State for S&P500’s PCP Deviations (Gibbs Sampling)

Figure 2(d):Estimated Variance of S&P500’s PCP Deviations (Gibbs Sampling)

Figure 3(a):Probability of a Low-variance State for DAX’s PCP Deviations (Gibbs Sampling)

Figure 3(b):Probability of a Medium-variance State for DAX’s PCP Deviations (Gibbs Sampling)

Figure 3(c):Probability of a High-variance State for DAX’s PCP Deviations (Gibbs Sampling)

Figure 3(d):Estimated Variance of DAX’s PCP Deviations (Gibbs Sampling)

33

Reference

Albert, J. H. and Chib, S.(1993)“Bayes Inference via Gibbs Sampling of

Autoregressive Time Series Subject to Markov Mean and Variance Shifts”,

Journal of Business and Economic Statistics, 11, 1-15.

Brenner, M. and D. Galai (1986), “Implied Interest Rate”, Journal of Business, 59,

493-507.

Bühler, W. and A. Kempf, (1995), “DAX Index Futures:Mispricing and Arbitrage in

German Markets”, Journal of Futures Markets, 15, 833-59.

Casella, G. and E. I. George, (1993) “Explaining the Gibbs Sampler”, The American

Statistician 46(3), 167-174.

Chance, D. M.(1987)“Parity Tests of Index Options”, Advances in Futures and

Options Research, 2, 47-64.

Chib, S. and E. Greenberg, (1996) “Markov chain Monte Carlo simulation methods in

Econometrics”, Econometric Theory, 12, 409-431.

Cochrane, J. H.(1988)“How big is the random walk in GNP? ” Journal of Political

Economy, 96, 893-920.

Eleswarapu, V.R. and M.R. Reinganum, (1993), “The Seasonal Behavior of the

Liquidity Premium in Asset Pricing”, Journal of Financial Economics, 34, 373-86.

Evnine, J. and A. Rudd,(1985)“Index Options:The Early Exercise”, Journal of

Finance, 40, 743-55.

Gelfand, A. E. and A. F. M. Smith, (1990) “Sampling-Based Approaches to Calculating

Marginal Densities”, Journal of American Statistical Association, 85(410),

398-409.

Gould, J. P. and D. Galai,(1974)“Transaction Costs and Relationship Between Put and

34

Grünbichler, A., F. Longstaff, and E. S. Schwartz, (1994), “Electronic Screen Trading

and the Transmission of Information:An Empirical Examination”, Journal of

Financial Intermediation, 3, 166-87.

Hamilton, J. D.(1989), “A New Approach to the Economic Analysis of Nonstationary

Time Series and the Business Cycle”, Econometrica 57, 357-84.

___________(1990), “Analysis of Time Series Subject to Change in Regime”, Journal of Econometrics, 45, 39-70.

Harris, L.(1989)“The October 1987 S&P500 Stock-Futures Basis”, Journal of Finance, 43, 77-99.

Harvey, C. R. and R. E. Whaley (1992), “Dividends and S&P100 Index Option

Valuation”, Journal of Futures Markets, 12, 123-137.

Kamara, A. and T. W. Miller, (1995) “Daily and Intradaily Tests of European Put-Call

Parity”, Journal of Financial and Quantitative Analysis, 30, 519-39.

Kawaller, I.(1987)“A Note:Debunking the Myth of a Risk-Free Return”, Journal of

Futures Markets, 7, 327-31.

Kim, C. J. and Nelson, C. R. (1999), State-Space Models with Regime Switching:

Classical and Gibbs-sampling Approaches with Application, MIT press

Kim, M. J. , Nelson, C. R. and Startz, R.(1991)“Mean Reversion in Stock Prices?A

Reappraisal of the Empirical Evidence”, Review of Economic Studies 58, 515-28.

Kim, C. J. , Nelson, C. R. and Startz, R.(1998)“Testing for Mean Reversion in

Heteroskedasticity Data Based on Gibbs-Sampling-Augmented Randomization”,

Journal of Empirical Finance, 5, 131-54.

Kleidon, A.(1992)“Arbitrage, Nontrading and Stale Prices”, Journal of Business, 65,

483-507.

Klemkosky, R. C. and B. G. Resnick,(1979)“Put-Call Parity and Market Efficiency”,

35

___________,(1980)“An Ex Ante Analysis of Put-Call Parity”, Journal of Financial

Economics, 8, 363-78.

Lo, A. W. and A. C. MacKinlay,(1989)“The Size and Power of the Variance Ratio Test in Finite Samples:A Monte Carlo Investigation”, Journal of Econometrics, 40,

203-38.

Merton, R. C.(1973)“The Relationship between Put and Call Option Prices:

Comment”, Journal of Finance, 28, 183-84.

Miller, M. , J. Muthuswamy, and R. Whaley,(1994)“Predictability of S&P500 Index

Basis Changes:Arbitrage Induced or Statistical Illusion?” Journal of Finance, 49,

479-514.

Neal, R.(1996)“Direct Tests of Index Arbitrage Models”, Journal of Financial and

Quantitative Analysis, 31, 541-62.

Poterba, J. M. and L. H. Summers,(1988)“Mean reversion in Stock Prices:Evidence

and Implications”, Journal of Financial Economics, 22, 27-59.

Ronn, A. G. and E. I. Ronn,(1989)“The Box Spread Arbitrage Conditions:Theory,

Tests and Investment Strategies”, Review of Financial Studies, 2, 91-108.

Sofianos, G..(1993)“Index Arbitrage Profitability”, Journal of Derivatives, 1, 6-20.

Stoll, H. R.(1969)“The Relationship between Put and Call Option Prices”, Journal of