Computing, Information and Control ICIC International c⃝2011 ISSN 1349-4198

Volume 7, Number 12, December 2011 pp. 6837–6847

PARTICLE SWARM OPTIMIZATION BASED ON BACK PROPAGATION NETWORK FORECASTING EXCHANGE RATES

Jui-Fang Chang1 and Pei-Yu Hsieh2

1Department of International Business

National Kaohsiung University of Applied Sciences No. 415, Chien Kung Road, Kaohsiung 807, Taiwan

2Department of Accountancy

National Cheng Kung University No. 1, University Road, Tainan 701, Taiwan

Received April 2010; revised August 2010

Abstract. This research constructs a new forecasting model. Particle Swarm

Opti-mization (PSO) is utilized to select the optimal input layer neurons, and then predict exchange rates by the Back Propagation Network (BPN), which called PSOBPN model. The model is applied to forecast exchange rate NTD/USD. We hope to improve tradi-tional neural network that utilized the try-and-error method to find out the better neurons of input layer efficiently. The results show that the PSOBPN achieves the best perfor-mance forecasting and is most closely matched with the actual exchange rate.

Keywords: Particle swarm optimization, Back propagation network, Exchange rate forecasting

1. Introduction. Since the collapse of Bretton Woods Agreement in 1973, every country gave up traditional fixed exchange rate and started to accept floating exchange rate in the world. In floating exchange rate system, it is possible for every country that its exchange rate often drastically moves. Therefore, the issue about prediction of exchange rate be-comes very important. How to predict future exchange rate correctly is an important mission for multinational corporations.

There are some exchange rate prediction models in tradition such as Monetary Model, Portfolio Balance Approach Model theory, Purchasing Power Parity Model and Balance of Payment Approach Model. These approaches are often adopted to predict the exchange rate. Fang and Kwong (1991) compared ARIMA with economic model to forecast foreign exchange rate, and their result showed that the economic model had better performance for the prediction. Chang (1991) used OLS method and the ARIMA model integrated with macroeconomic model and prediction combination model and then observed their forecast effect. The practical result showed that the long-term prediction effect was better than the short-term when using the macroeconomic model. Although the macroeconomic model integrated with ARIMA model could consolidate the prediction effect of macroe-conomic model, the effect was not significant and that forecast combination model could even increase prediction effect. Wei (1994) used ARIMA, economic model and forward currency model with rolling regression method to forecast the exchange rate of CAD/USD, JPY/USD, Pound/USD and DM/USD. The result showed ARIMA had the strongest pre-diction ability of all models in the short term, and the economic model in the long term. Mehran and Shahrokhi (1997) used Mean Absolute Error (MAE), Mean Square Error

(MSE) and Root Mean Square Error as standards (RMSE) to forecast the exchange rate. The result has shown that ARIMA was better than the other models in most periods. Gil-Alana and Toro (2002) used fractional integrated ARIMA model to forecast the ex-change rate of Canada, U.K., France, Italy and Japan in relation to U.S. dollars. In this research, they set up ARIMA (p, d, f) of each country and according to d, discovered the fact that the real exchange rate of France, Canada and the U.K. remained unchanged. Chen (2003) used ARIMA, GARCH and Markov model with rolling regression method to forecast JPY/U.S. dollar, N.T. dollar/U.S. dollar, SGD/U.S. dollar and KOW/U.S. dollar. The author found that Markov model had the best prediction ability among the three models.

Rauscher (1997) conducted the empirical study, and they found that BPN is better than traditional Error Correction Model (ECM) in exchange rate forecast. Nelly and Weller (2002) proved Genetic Algorithms (GA) is better than traditional time series model in fluc-tuation of exchange rate. Andr´e, Newton and Leandro (2007) compared neural network with traditional econometrics. They found nonlinear mathematical models of multilayer perception and radial basis function neural networks are able to provide a more accurate forecast than the traditional auto regressive moving average (ARMA) and ARMA gen-eralized auto regressive conditional heteroskedasticity (ARMA-GARCH) linear models. Chen and Daouk (2000) adopted general regression neural network (GRNN), multi layer feed forward network (MLFN) and random walk model to predict exchange rate. The au-thors used weekly data of the Canadian dollar, the JPY and the British pound and found that GRNN was the best one among the three methods. Kwan and Liu (1995) investi-gated the out-of-sample forecasting ability of recurrent and feed forward neural networks based on empirical exchange rate data. A two-step procedure is proposed to construct the appropriate networks, in which networks are selected based on the Predictive Stochas-tic Complexity (PSC) criterion, and the selected networks are estimated by using both recursive Newton method and the method of nonlinear least squares. The results show that PSC is a sensible criterion for selecting networks and for certain exchange rate series, some selected network models have significant market timing ability and/or significant lower out-of-sample mean squared prediction error relative to the random walk model. Rauscher (1997) used monthly data from 1986 to 1997 and the cointegration method to get a long-term equilibrium function between foreign exchange rate and the macroeco-nomic factors. He used the long-term equilibrium function and macroecomacroeco-nomic factors of the Monetary School as the input variables of BPN and got the empirical results. BPN was better than the error correction model when forecasting the direction of the exchange rate variation. Leung, Chen and Daouk (2000) adopted general regression neural network (GRNN), multi layer feedforward Network (MLFN) and random walk model to predict exchange rate. The authors used weekly data of the Canadian dollar, the JPY and the British pound and then discovered that GRNN was the best among the three methods. Natarajan, Saravanan and Periasamy (2006) claimed that estimation of tool life generally requires considerable time and material and hence it is a relatively expensive procedure. They used PSO and BPN to train neural network, and compared PSO with BPN. The result found out PSO is preferred to BPN. Geethanjali, Slochanal and Bhavani (2008) proposed which monitors and discriminates the different operating conditions of power transformers. PSO technique is used to train the multi-layered feed forward neural net-works to discriminate different operating conditions. These two ANNs were trained by using back propagation neural network algorithm (BPN) and PSO technique and then the simulated results are compared. Comparing the simulated results of the above two cases, training the neural network by PSO technique gives more accurate (in terms of sum square error) and also faster (in terms of the number of iterations and the amount

of simulation time) results than BPN. The PSO trained ANN-based differential protec-tion scheme provides faster, more accurate, more secure and reliable results for power transformers.

This research focuses on using the characteristics of PSO and BPN for efficiently fore-casting exchange rate, and compares the performance on above models with MSE, MAE and RMSE. This paper is structured as follows. Section 1 would propose some literature. Section 2 describes the three methodologies applied in this research. Section 3 illustrates data and experiment design. Section 4 compares the forecasting results among the PSO, the BPN and the PSOBPN models. Section 5 makes the conclusion and some suggestions. 2. Methodology.

2.1. Particle swarm optimization. PSO is a relatively novel evolutionary algorithm that might be used to find optimal solutions to numerical problems. Social-psychologist electrical engineer Russell Eberhart and James Kennedy (1995a, 1995b) in 1995 first brought up PSO. The primary forecasting model of PSO shows as following equation.

∧

St = β0+ β1x1+ β2x2+ ... + βD−1xD−1 (1)

PSO algorithm explores the optimal target through local history and global commu-nications in populations that consist of potential solutions, called particles, which are initially randomly generated in the first population. Then, the new population of particle swarm is generated by moving each particle to the next step based on a given update pol-icy. For achieving a high efficiency of searching the optimal solution in high dimensions, PSO drives the particle swarm to move toward the higher-object-value region based on the best experiences of each particle and the entire populations. Thus, PSO approaches the optimal point at a much higher speed than evolutionary optimization. Each particle indicates a candidate solution; if we have D-dimensional parameters in solution, the i-th particle for the t-th iteration can be represented as

Bit=(βi,0t , βi,1t , βi,2t , βi,3t , βi,4t , ..., βi,Dt −1) (2) where N is the population size. The particle will move according to an selected velocity, based on the corresponding particle’s experience and the experience of its companions. Assume that the previous best position of the i-th particle at the t-th iteration is repre-sented as

Pit= (pti,1, pti,2, ..., pti,D) (3)

At this step, we would define an objective or fitness evaluation for every particle. Usually on science problems or forecast error, researchers would find the minimal value of their fitness function. The fitness function in this thesis is set as below:

M inimize M AP E = n ∑ 1 (St∧ −St ) / St n (4) where ε(.) is the ( ∧ St−St ) /

St , to minimize the forecasting errors is adopted as the

fitness function.

Then, the values of fitness function M AP E are expected to decrease by iterations.

LB ≤ Bit≤ UB (5)

ε(Pit)≤ ε(Pit−1)≤ ... ≤ ε(Pi1) (6)

The velocity of the i-th particle at the t-th iteration, Vit can be represented as

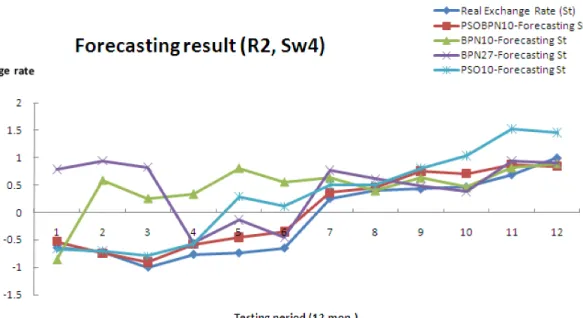

Figure 2. Forecasting the trend of fluctuation

optimal selection of input-layer neurons by PSOBPN had better forecasting ability than 27 input-layer neurons.

6. Contribution and Suggestion. In this research, we find out the fact that the opti-mal input layer neurons for BPN which rely on PSO would give optiopti-mal solution. This method replaces the traditional ANN that used the try-and-error method to find the input layer neurons. After the experiment, we propose a set of variables and weight that could be the consult when investors or managers forecasting the exchange rate. Meanwhile, investors could also know which variables and how many lagged period are explainable. We recommend it will be better to apply other currencies over a longer period of time. We also suggest that the future research could use the nonlinear PSO model, and compare its performance by utilizing other methods.

Acknowledgment. The authors gratefully acknowledgement the helpful comments and

suggestions of the reviews which have improved presentation. REFERENCES

[1] A. Kumamoto, A. Utani and H. Yamamoto, Advanced particle swarm optimization for comput-ing plural acceptable solutions, International Journal of Innovative Computcomput-ing, Information and

Control, vol.5, no.11(B), pp.4383-4392, 2009.

[2] A. A. P. Santos, N. C. A. da Costa Jr. and L. dos S. Coelho, Computational intelligence approaches and linear models in case studies of forecasting exchanges, Expert Systems with Applications, vol.33, no.4, pp.816-823, 2007.

[3] C. Wang, P. Sui and W. Liu, Improved particle swarm optimization algorithm based on double mutation, ICIC Express Letters, vol.3, no.4(B), pp.1417-1422, 2009.

[4] J.-F. Chang, A performance comparison between genetic algorithms and particle swarm optimization applied in constructing equity portfolios, International Journal of Innovative Computing,

Informa-tion and Control, vol.5, no.12(B), pp.5069-5080, 2009.

[5] H. Fang and K. K. Kwong, Forecasting foreign exchange rate, Journal of Business Forecasting, pp.16-19, 1991.

[6] G.-C. Chou, Forecasting Ability of Long Term and Short Term Exchange Rate Forecasting Models, Master Thesis, National Cheng Kung University, 2003.

[7] R. Eberhart and J. Kennedy, A new optimizer using particle swarm theory, The 6th International

[8] R. Eberhart and J. Kennedy, Particle swarm optimization, IEEE International Conference on Neural

Networks, pp.1942-1948, 1995.

[9] J. Nagashima, A. Utani and H. Yamamoto, Efficient flooding method using discrete particle swarm optimization for long-term operation of sensor networks, ICIC Express Letters, vol.3, no.3(B), pp.833-840, 2009.

[10] M. T. Leung, A. S. Chen and H. Daouk, Forecasting exchange rates using general regression neural networks, Computers and Operations Research, pp.1093-1110, 2000.

[11] U. Natarajan, R. Saravanan and V. M. Periasamy, Application of particle swarm optimisation in artificial neural network for the prediction of tool life, Int. J. Adv. Manuf. Technol., pp.1084-1088, 2006.

[12] C. J. Nelly and P. A. Weller, Predicting exchange rate volatility: Genetic programming versus GARCH and RiskMetrics(TM), The Federal Reserve Bank of St. Louis, vol.84, no.3, pp.43-54, 2002. [13] F. A. Rauscher, Exchange rates forecasting: A neural VEC approach to non-linear time series