行政院國家科學委員會

獎勵人文與社會科學領域博士候選人撰寫博士論文

成果報告

Two essays on corporate hedging policy and firm

value of global airline industry

核 定 編 號 : NSC 96-2420-H-004-009-DR 獎 勵 期 間 : 96 年 08 月 01 日至 97 年 07 月 31 日 執 行 單 位 : 國立政治大學財務管理研究所 指 導 教 授 : 張元晨 博 士 生 : 林瑞椒 公 開 資 訊 : 本計畫涉及專利或其他智慧財產權,2 年後可公開查詢

中 華 民 國 98 年 02 月 11 日

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

國立政治大學財務管理所

博士論文

The Effects of Hedging on Firm Value and Analyst Forecast

Accuracy: Evidence from the Global Airline Industry

指導教授:張元晨博士

研究生:林瑞椒

中華民國九十八年一月

Table of Contents

List of Figures and Tables……….iii

Preface………...iv

Acknowledgements………v

Abstract……….vi

Chapter I. Introduction………..…1

Chapter II. Does Hedging Add Value? Evidence from the Global Airline Industry 1. Introduction………..4

2. Literature Review……….…………8

2.1 Hedging and Firm Value………...……8

2.2 Incentives for Hedging Activities……….…..10

2.2.1 Tax Incentives………...10

2.2.2 Managerial Incentives………..11

2.2.3 Financial Distress and Underinvestment Costs………...12

3. Sample Description………...13

3.1 Hedging Variables……….….14

3.2 Proxy for Firm Value……….……….15

3.3 Other Variables………...……16

4. Does Jet Fuel Hedging Increase Airlines’ Value?...20

5. The Determinants of Jet Fuel Hedging of Global Airlines……….……25

5.1 What Factors Explain Airlines’ Hedging Behavior?...25

5.2 Does Underinvestment Problem Play An Important Role in Explaining Airlines’ Hedging Behavior?...28

6. Sensitivity Checks………..31

6.1 Using Different Proxy to Measure Firm Value………...31

6.2 Does “Trend” or “Volatility” of Jet Fuel Price Affect Firms’ Hedging Behavior?...32

Chapter III. Corporate Hedging Activities and Analyst Forecast Accuracy: Evidence from the Global Airline Industry

1. Introduction………..……..53

2. Sample Selection and Variables Description………....……..55

2.1 Sample Selection………..……..55

2.2 Variables Description……….……..….…….55

3. Empirical Analysis and Results……….….……56

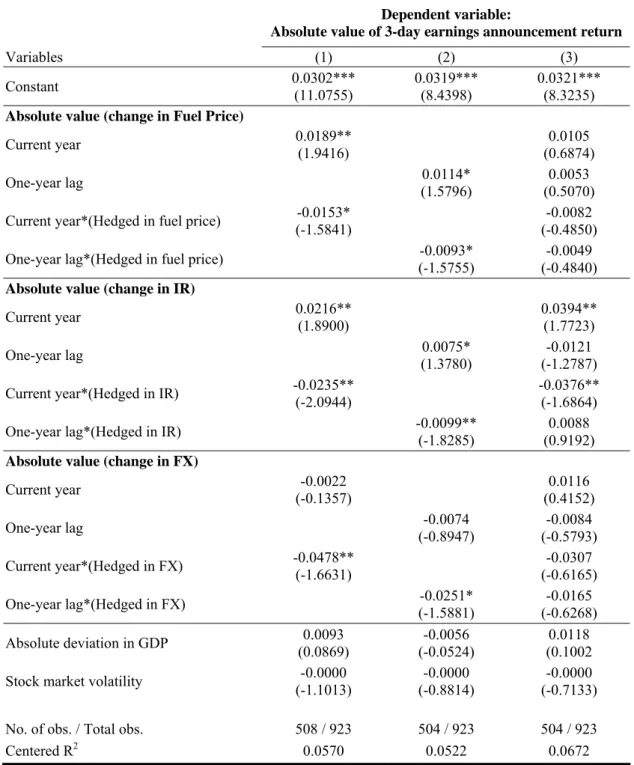

3.1 The Impact of Changes in Fuel Price, Interest Rate and Foreign Exchange Rate on Earnings Announcement Returns…..…….…..56

3.2 The Impact of Changes in Fuel Price, Interest Rate and Foreign Exchange Rate on Analysts’ Forecast Errors ………....60

3.3 The Impact of Changes in Fuel Price, Interest Rate and Foreign Exchange Rate on Revisions in Analysts’ Forecasts……...……...65

4. Conclusions………..………..66

Chapter IV. Conclusions and Future Research……….………83

Appendix………..85

List of Figures and Tables

Figures

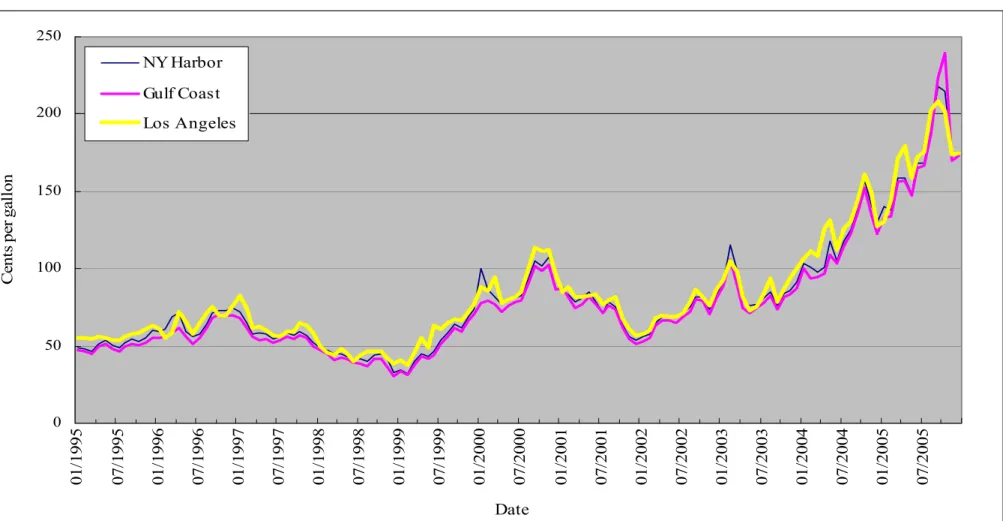

Figure 2-1. Average Monthly Jet Fuel Prices (Cents per Gallon)……..………..……35

Tables

Table 2-1. Global Airline Companies in the Sample………....…..….36 Table 2-2. Summary Statistics of Variables Used in Regression Models……….…...37 Table 2-3. The Impact of Hedging Behavior on Firm Value………...….41 Table 2-4. Determinants of Jet Fuel Hedging by Global Airlines………..…..45 Table 2-5. The Influence of Hedging on Firm Value via Capital Expenditures…..….49 Table 3-1. Summary Statistics of Macroeconomic Risk Exposures………...68 Table 3-2. Summary Statistics of Earnings Announcement Returns and

Macroeconomic Control Variables Used in Regressions……….…..69 Table 3-3. The Impact of Fuel, interest rate and foreign exchange rate Changes on

Three-day Earnings Announcement Returns………..70 Table 3-4. Summary Statistics of Analysts’ Forecast Errors and Other Control

Variables Used in Regressions………..…….74 Table 3-5. The Impact of Fuel, interest rate and foreign exchange rate Changes on

Absolute Analysts’ Forecast Errors……….…..….75 Table 3-6. The Impact of Fuel, interest rate and foreign exchange rate Changes on

Preface

This dissertation encompasses two essays to examine the effects of hedging activities on firm value and analyst forecast accuracy. These essays have been transformed into working papers. The first working paper, based on Chapter II is entitled ” Does hedging add value? Evidence from the global airline industry”. It has been presented in the 16th conference on the Theories and Practices of Securities Financial Markets on Dec. 5, 2008 at the National Sun Yat-sen University in Kaohsiung. The second working paper, entitled “Corporate hedging activities and analyst forecast accuracy: Evidence from global airline industry “, is currently under revision and will be sent to conferences in the near future.

Acknowledgements

I would first and foremost like to express my deep gratitude to my adviser,

Professor Yuanchen Chang. His patience and unlimited support helped me finish this

dissertation. I hope that one day I would become as good an advisor to my students as Chang has been to me.

The members of my dissertation committee, professors C. Edward Wang,

Dar-Hsin Chen, Yao-Min Chiang, and Yi-Tsung Lee, for their great comments and insightful advice that help improve the quality of my dissertation and provide useful suggestions for my future research.

I would also like to express my deep thanks to Professor Pai-Ta Shih, my adviser

of master’s degree. Thanks for his encouragement to help me overcome many

depressed situations during my doctoral life.

Besides, many friends have helped me stay sane through these years. Their support and care helped me overcome setbacks and stay focused on my graduate study. I greatly value their friendship and deeply appreciate their belief in me. I would like to thank Hsiangping Tsai especially, thank for her encouragement and listening.

Most importantly, none of this would have been possible without the love and patience of my family. I am grateful for their constant source of love, concern, support and strength all these years. I heartily appreciate my family who has given meaning to all the effort I have done.

Rueyjiau Lin January 20, 2009

Abstract

Two essays are comprised in this dussertation to examine whether jet fuel hedging has effects on firm value and analysts’ forecast accuracy in the global airline industry. Using global data allows us to cmpare the differences of jet fuel hedging behavior and incentives for hedging across different sub-samples. Furthermore, we also examine how jet fuel hedging affects analysts’ forecast erros across different sub-samples and its implications for firm disclosures about their risk exposures in the financial reports.

In the first essay, we examine whether jet fuel hedging increases the market value of airline companies around the world. Using a sample of 70 airline companies from 32 countries over the period 1995 to 2005, we find that jet fuel hedging is not significantly positively related to their firm value in the global airlines, but this positive relationship holds in the various sub-samples and is significant for US and non-alliance firms. Moreover, our results show that the risk-taking behavior of executives and the tendency to avoid financial distress are important determinants for the jet fuel hedging activities of non-US airline companies. Alleviating the problem of underinvestment is also an important factor to explain the jet fuel hedging activities of US and non-alliance firms. Our results add support to the growing body of literature which finds that hedging increases firm value for global airline companies.

In the second essay, we examine the extent analysts revise their earnings forecasts in response to oil price, interest rate and foreign exchange rate shocks they have observed during the year, and whether these revisions contain additional information about how current and past price shocks affect reported earnings, using

the sample of the global airline industry. Empirical results indicate that jet fuel hedging can increase analysts’ forecast revisions in the total sample, and in the sub-sample of the volatile fuel price period. These results can also be seen in US and non-US airlines, and airlines with both strong and weak governance. Overall, our results show that oil price shocks play an important role in investor and analyst information uncertainty with regard to the global airline industry. Consequently, corporate risk disclosures only provide limited information about firms’ financial risk exposures.

Chapter I

Introduction

Since the September 11 terrorist attacks, many airline companies are eager to improve their cost structure by saving operation expenses due to higher fuel prices. The extreme volatility in fuel prices is a huge burden for the global airline industry. According to IATA’s (International Air Transport Association) estimation, $425 million extra operating expenses were incurred from every additional dollar increased in the price per barrel for the U.S. airline industry in 2005. If an airline company is able to control its fuel costs, it can operate more competitively in the market. For example, Southwest Airlines, the largest U.S. aircraft by market value, and the global role model for low-cost airlines, is known to undertake hedging activities against higher fuel prices. It hedged about 85% and 70% of its requirements for the years 2004 and 2005, respectively, cutting fuel and oil costs by $196 million in the second quarter of 2005. We collect hedging data for 70 airline companies across 32 countries, and it allows us to test the relationship between hedging activities and firm value in a more global content. Furthermore, we examine whether jet fuel hedging can affect analysts’ forecast errors through its effect on firm value. We expect that jet fuel hedging can increase firm value and affect its earnings per share. In the second essay, we will examine if analysts can realize this effect and take it into account when making their forecasts. Investigating whether current year and one-year lagged fuel price shocks have impact on the formation of analysts’ forecast is one of our objects in the second essay. In addition, we also inspect whether airline companies’ fuel hedging activities have any influence on analysts’ earnings forecasts. We expect that airlines with jet fuel hedging would decrease analysts’ forecast errors, because hedging activities can reduce the earnings’ volatility and it makes analysts’

forecasts more accurate.

The first essay of this dissertation examines the relationship of jet fuel hedging activities and firm value, and explores the determinants of jet fuel hedging for airline companies around the world. Using a sample of 70 airline companies from 32 countries over the period 1995 to 2005, we find that jet fuel hedging is not significantly positive related to their firm value in the world’s airline companies, but this positive relationship holds in the various sub-samples and is significant for US and non-alliance firms. Moreover, we find that economies of scale and the use of currency derivatives are important determinants for total sample. Our results also show that the risk-taking behavior of executives and the tendency for them to avoid financial distress are important determinants for the jet fuel hedging activities of non-US airline companies. Alleviating the problem of underinvestment is also an important factor to explain the jet fuel hedging activities of US and non-alliance firms. Our results add support to the growing body of literature which finds that hedging increases firm value for global airline companies.

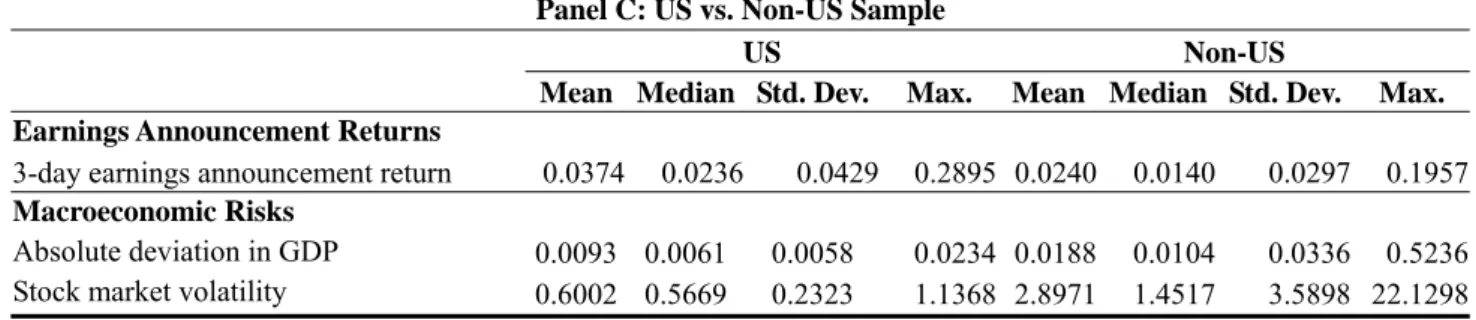

The second essay of this dissertation examines the association between the shocks to financial markets and investors’ uncertainty about firm’s financial risk exposures. We use a sample of 71 airline companies in 32 countries from 1995 to 2007 to test the abnormal returns of airline companies around earnings announcements and its association of earnings forecasts. Our results show that recent oil price surge plays an important role on analyst forecast errors in the global airline industry. We compare the effects of oil, interest rate and currency hedging activities on airline companies and find that oil hedging increases the analysts forecast errors, while interest rate and foreign exchange hedging reduce the analysts forecast errors. It suggests that analysts concern more about firms engaged in oil prices

hedging due to the volatile nature of oil prices.

The remainder of this dissertation is structured as follows. Chapter II explores the effects of jet fuel hedging on firm value, and the incentives of fuel hedging. Chapter III examines the association between risk exposures and investors’ information uncertainty. Chapter IV provides the conclusions and future research of this dissertation.

Chapter II

Does Hedging Add Value?

Evidence from the Global Airline Industry

1. Introduction

In response to the recent leap in oil prices, more and more airline companies are engaged in hedging activities. According to the Modigliani-Miller theorem, in a perfect market hedging should add no value to the firm. However, the assumption of perfect market does not hold in the real world, and whether hedging can increase firm value is mixed in the literature. Allayannis and Weston (2001) examine the relationship between currency hedging activities and firm value in the U.S. market and conclude that hedging can increase firm value for a large sample of U.S. non-financial firms. Carter, Rogers and Simkins (2006a, b) find that jet fuel hedging is positively related to the market value of airline companies. Conversely, Jin and Jorion (2006) find that there is no relationship between hedging activities and firm value for U.S. oil and gas producers from 1998 to 2001. However, these studies focus mainly on the relationship between currency hedging activities and firm value in the U.S. market and the aim of this study is to examine whether jet fuel hedging can increase firm value in the global airline industry.

The academic literature has also focused on exploring which factors contribute to the hedging activities and risk management theory provides several reasons to explain why firms may hedge. Smith and Stulz (1985) and Leland (1998) propose that tax issues are related to such activities, while Smith and Stulz (1985), Bessembinder (1991), and Froot et al. (1993) argue that reduction of underinvestment or financial distress costs contribute to hedging. Furthermore, the risk-taking incentives of

managers are also related to hedging behavior (Stulz, 1984; Smith and Stulz, 1985; Tufano, 1996; Rogers, 2002). Because the airline industry is an internationally competitive industry, variable fuel prices increase earnings volatility, a problem that hedging may be able to alleviate. Furthermore, it is hard to transfer surging oil price to customers through rising of fuel surcharge on tickets for airline companies due to their competitive operating environment. Therefore, using 70 airline companies from 32 countries during the period 1995 to 2005, we examine the sources of jet fuel hedging premium. Because such companies are subject to significant price risk due to volatile jet fuel price, this allows us to investigate the sources of added value from jet fuel hedging activities using data from global airline companies.1

Since September 11, 2001 terrorist attacks, many airline companies are eager to improve their cost structure to save operating expenses due to higher fuel prices. Figure 2-1 depicts the average monthly spot jet fuel prices at three locations during our sample period. It is seen that the Gulf Coast fuel price reached $2.4 per gallon in October, 2005, while the average fuel price was $0.51 per gallon at the end of 2001. Thus, from 2001 to 2005, the average fuel prices had risen 37 percent. The extreme volatility in fuel prices during this period was a huge burden for airline industry, because fuel costs are the second largest category of operating expenses.2 According

to IATA’s (International Air Transport Association) estimation, $425 million extra operating expenses were incurred from every additional dollar increased in the price per barrel for the U.S. airline industry in 2005. If an airline company is able to control fuel costs, it can operate more competitively in the market. For example,

1 I use kerosene-type jet fuel at three major US trading locations (New York Harbor, U.S. Gulf Coast,

and Los Angeles) following Carter et al. to describe the trend of fuel prices. The sample period is from 1995 to 2005, the average monthly jet fuel price is 80.61 cents per gallon, and its standard deviation is 37.8 cents per gallon.

2 For example, jet fuel costs were an average of 14.29% of total operating expenses in the U.S. airline

Southwest Airlines, the largest U.S. aircraft by market value, and the global role model for low-cost airlines, is known to undertake hedging activities against higher fuel prices. It hedged about 85% and 70% of its fuel requirements for the years 2004 and 2005, respectively,3 cutting fuel and oil costs by $196 million in the second

quarter of 2005.4 However, as our data contains 70 airline companies across 32

countries, it allows us to test the relationship between hedging and firm value in a more global content.

This research contributes to the current literature in the following ways. Firstly, the volatility of jet fuel prices in the sample period for this study is much larger than those in the previous studies (Carter et al., 2006a, b).5 It is thus expected that jet fuel

hedging would increase firm value more significantly during our sample period. Secondly, compare to Carter et al. (2006a, b), we use data from 32 countries to examine the relationship between jet fuel hedging and firm value, and this study is the first to examine the hedging behaviors of jet fuel prices from a global perspective. Thirdly, we partition the entire sample into different sub-samples to better explore the determinants of jet fuel hedging premium.

Our regression analysis show that, on average, jet fuel hedging is not valuable for airline companies. This finding is contrary to the results of Allayannis and Weston (2001) and Carter et al. (2006a), who find that the usage of hedging derivatives can add value to the firm. Moreover, US airlines those engage in fuel hedging activities increase their firm value by approximately 7.87%. We also show that non-US

3 The hedge ratio of fuel requirements are collected from 10-K filings in the U.S. Securities and

Exchange Commission (EDGAR).

4 Done, K., July 15, 2005, “Southwest sees profits up 41%,” Financial Times London, p. 32.

5 In our sample period, the annualized standard deviation of jet fuel prices is 30.35% compared to

Carter et al.’s (2006a, b) report of 27%, measured from 1992 to 2003. The standard deviation of average monthly fuel prices is 37.8 cents per gallon in our sample period, as compared with their report of 15.7 cents per gallon.

airlines and airlines with an alliance6 that hedge for fuel price risks add nothing to

their firm value. We also show that fuel hedging is more valuable in the volatile period than in the stable period. This result provides evidence that airline companies can avoid declines in their value due to soaring oil prices by undertaking hedging activities. Compare to Carter et al. (2006a, b), we find that jet fuel hedging can not add value to firms for non-US airlines. They may use other substitutes to transfer the fuel price risk. For non-US airlines, they engage in fuel hedging activities to reduce financial distress costs and comply with managers’ risk-aversion hedging incentives. On the other hand, alleviating underinvestment problems plays an important role on the determinants of jet fuel hedging for US airlines, but it is not significant for non-US airlines.

We also investigate the determinants of jet fuel hedging for airline companies around the world. The evidence shows that hedging to reduce the probability of incurring financial distress plays an important role for non-US airlines and in the period of stable fuel prices, and that alliance airlines and airlines in the volatile period hedge fuel price risk exposures to preserve their higher profitability. Moreover, it is seen that jet fuel hedging is motivated by managerial risk aversion for non-US airline companies, but we also find that jet fuel hedging is motivated by managerial risk-taking behavior for airlines in the stable period, which is suggested by Galai and Masulis (1976) and Saunders et al. (1990). Conversely, airlines in the stable period engage in fuel hedging activities are motivated by managerial risk-taking behavior. In addition, a fuel pass-through mechanism can substitute for fuel hedging using

6 An airline alliance is an agreement between two or more airlines to cooperate for the foreseeable

future on a substantial level. The degree of cooperation is different between alliances. Star Alliance, SkyTeam and Oneworld are the three largest alliances in the world so far. In addition, a number of alliances between cargo airlines have formed recently, such as the WOW Alliance between Lufthansa Cargo, Singapore Airlines Cargo, SAS Cargo Group and Japan Airlines Cargo.

derivatives for the global airline companies, US and non-US airlines, non-alliance airlines and airlines in the volatile period. Consistent with Froot et al. (1993) and Carter et al.’s (2006a) findings, our results show that mitigating underinvestment problems is an important reason to hedge for US airlines, non-alliance airlines and airlines in the stable period. Finally, we also document that economies of scale and the use of currency derivatives are also important in explaining all airlines’ fuel hedging behavior.

The rest of this essay is organized in the following way. Section 2 gives a brief overview of hedging theories. Section 3 describes the sample and specifies the measures of hedging activities, firm value and other explanatory variables. Section 4 presents the estimated results for the impact of jet fuel hedging on airline firm value. Section 5 explores the determinants of why airline companies use derivatives to hedge jet fuel risk exposures, and Section 6 concludes this paper.

2. Literature Review

In the Modigliani-Millers’s world, hedging would not add value to a firm if the financial market is perfect. However, in the real world, the financial market is not frictionless and hedging may influence the cash flow of the company. A number of academic researches have studied the relation between hedging activities and firm value. In addition, a considerable amount of literature has been focused on exploring what factors influence firms’ hedging activities.

Allayannis and Weston (2001) find that there is a positive relation between the usage of foreign exchange derivatives and firm value, using a sample of 720 large non-financial firms with foreign sales from 1990 to 1995. They find that the hedging premium is significant at about 4.87% of firm value, and it is larger in the period of dollar appreciation. Nain (2004) divides his sample into 548 derivatives users and 2,711 non-derivative users of U.S. firms with ex-ante foreign exchange exposure from 1997 to 1999. He shows that that foreign exchange risk management can increase firm value (proxied by Tobin’s Q) if many of their competitors hedge. Conversely, Guay and Kothari (2003) argue that based on the magnitudes of the notional amount of the derivatives used by U.S. firms, the value premium is insignificantly related to a firm’s hedging position.

Bartram, Brown and Fehle (2004) use a large sample of 7,319 non-financial companies in 50 countries from 2000 to 2001 to examine the impact of interest rate and foreign exchange derivatives usage on firm value. They document that the usage of derivatives is a value-adding activity, and the result is more significant for interest rate than foreign exchange hedging. Previous research also examines whether hedging of commodity risk exposures is related to firm value in the U.S. market. Lookman (2004) investigates exploration and production companies that hedge commodity price risk and the impact on firm value. He classifies oil price into primary and secondary risk to show that undiversified exploration and production companies that hedge primary risk are associated with lower value. On the other hand, he shows that for diversified companies, which have both exploration and production segments, hedging is associated with higher value. Callahan (2002) finds that the extent of gold hedging is negatively related to a firm’s stock price using a sample of 20 North American gold mining firms over the period 1996 to 2000.

Carter et al. (2006a, b) study the fuel hedging of 28 companies in the U.S. airline industry during the period of 1992 to 2003. Their results show that jet fuel hedging can increase firm value, and the hedging premium is economically significant. Jin and Jorion (2006) argue that risk management has no effect on 119 U.S. oil and gas producers in the period of 1998 to 2001. In contrast, Chang, Gu and Xu (2005) examine the relationship between oil and gas hedging and firm value in Canada, and find that gas production hedging has a negative effect on firm value, while gas reserve hedging has a positive impact. This result indicates that Canadian oil and gas producers can increase their firm value by hedging gas production and reserves.

2.2 Incentives for Hedging Activities

Following Smith and Stulz’s (1985) discussion of the motivations for hedging behaviors, a growing number of researchers have examined the issue. This line of empirical evidence suggests the following reasons why firms may hedge.

2.2.1 Tax Incentives

If hedging benefit can offset hedging cost, a firm may be willing to use hedging instruments to lessen its expected tax liability and reduce the variability of its pre-tax firm value. Such hedging activity associated with tax incentives can increase the firm’s expected post-tax value. Smith and Stulz (1985) indicate that the convexity of the tax function makes firms hedge more, which in turn increases their value. Leland (1998) also shows that hedging can increase the debt capacity of a firm, and thus reduce their expected tax payments.

Graham and Smith (1999) use a simulation method to analyze more than 80,000 firms in the U.S. They find that 50% of their sample face convex effective tax functions and 25% face linear tax functions. They show that approximately one-quarter of the companies with convex tax functions can obtain substantial tax savings from hedging, a result that is consistent with Smith and Stulz (1985). Graham and Rogers (2002) conclude that hedging exposures of foreign exchange and interest rates enhance firm value as a result of increased debt capacity, but they find no evidence that a firm’s hedging behavior responds to tax convexity.7

2.2.2 Managerial Incentives

Because information is asymmetric between insiders (managers) and outsiders (shareholders), it gives managers an opportunity to serve on their own interests and expropriate shareholders’ benefits. Smith and Stulz (1985) indicate that the compensation function is linear and convex to firm value, which may influence managers’ hedging decisions. When managers hold a substantial fraction of a firm’s stock, they hedge more. DeMarzo and Duffie (1995) argue that the optimal hedging policy adopted by managers depends on the type of accounting information made available to outside shareholders. Following this argument, managers’ skills and abilities are monitored more closely by outside investors. In addition, Tufano (1996) takes manager-shareholder agency problems into account and shows that managers may damage firm value by hedging. The results of his study reveal that tying managers’ wealth to firm value affects hedging policies. Meanwhile, Breeden and Viswanathan (1998) show that managers with poor skills may not hedge and manage

7 We do not discuss this issue in the following analysis, because the explanatory variable (tax loss

carryforwards) is only available for airlines listed in US. Considering it would reduce our sample substantially and make our results meaningless.

risk exposures adequately without monitoring by outsiders. Finally, Rogers (2002) uses a simultaneous equation method to show that CEOs’ risk-taking incentives have negative influences on firms’ currency and interest rate hedging activities.

An alternative view is to regard the common stock of a firm as a call option. Thus, the market value of a firm rises as its risk increases (Galai and Masulis, 1976). In addition, Saunders et al. (1990) find that managers with more equity in their firm tend to increase risk in the banking industry, although. There are also several empirical studies that find insignificant evidence to support managerial incentives as determinants of firms’ risk management behaviors (Géczy, Minton and Schrand, 1997, Gay and Nam, 1998, Allayannis and Ofek, 2001, and Haushalter, 2000).

2.2.3 Financial Distress and Underinvestment Costs

Financial distress usually occurs when a firm’s revenue fails to meet its expenditures. Hedging can reduce the probability of incurring financial distress costs, and creates profitable investment opportunities through minimizing the volatility of a firm’s cash flow in the foreseeable future. Mayers and Smith (1982) show that a firm’s insurance contracts can reduce the expected transactions costs of bankruptcy, while Smith and Stulz (1985) also show that hedging can lower the expected costs of financial distress. Lel (2006) uses a sample of ADRs cross-listed in the U.S. and concludes that financial distress costs are related to a firm’s hedging activity, although. Evidence from Mian (1996) and Tufano (1996) does not support this conclusion.

According to the pecking order theory, the external cost of capital is more expensive than the internal cost of capital for firms facing valuable investment

projects, so there may be an incentive to hedge risk to assure they have enough funds to alleviate underinvestment. Froot et al. (1993) show that hedging can ensure that companies have sufficient internal funds to complete profitable investment opportunities by lowering the variability of internal funds. Gay and Nam (1998) analyze the relation between a firm’s derivatives use and underinvestment problems, examining the interacting influences among firms’ investment opportunities, cash stocks, and internal cash flows to identify the position of underinvestment. They argue that firms with good investment opportunities tend to use derivatives to hedge their risks.

Haushalter (2000) examines the risk management activities of 100 oil and gas producers from 1992 to 1994. He finds that the correlation between the extent of hedging and financial leverage is positive, which supports the argument that a company can reduce financial contracting costs through hedging activity. Finally, Carter et al. (2006a, b) indicate that hedging fuel costs can help airline companies to manage their potential underinvestment problem, as well as reduce the costs of financial distress.

3. Sample Description

This paper analyzes the relationship between jet fuel hedging, firm value and hedging incentives for a sample of global airline companies. We gather the financial data for these firms from the COMPUSTAT database. The information regarding whether these companies use jet fuel derivatives, interest rate and foreign exchange derivative holdings is collected from the footnotes in their annual reports, 10-K filings or 20-F forms provided by Mergent Online database (SIC codes 4512 or 4513) and

airline companies’ websites. All the companies in our sample indicate that they purchase or hold financial derivative instruments for hedging rather than speculating purposes. Examples of airline companies disclose about their managing of fuel price risk are presented in the Appendix.

The criteria of our sample screening are as follows. First, a total of 131 companies from 41 countries are retrieved from Mergent Online database. Second, companies with less than three annual reports during the sample period or with incomplete information on fuel costs and expenses in their reports8 are excluded from

our sample. This restriction reduces the sample size to 74 airline companies from 33 countries. Finally, we further remove 4 airlines companies with missing data for common stock price and required accounting data over our sample period. Our final sample contains 70 airline companies in 32 countries from 1995 to 2005. Table 2-1 shows the sample of global airline companies used in this study. It is seen that 31 airline companies in our sample are from the US, while the rest of the sample countries have one to three airline companies each. The sample period for each of the airline company varies due to the availability of annual reports.

3.1 Hedging Variables

Firms listed on the US markets are required to disclose derivatives usage in their financial reports, which they must file periodically with the SEC, following the US GAAP and the Financial Accounting Standards Board (FASB) rules. However, many firms outside the US to disclose their hedging activities on a voluntary basis,

8 We use the keywords “fuel” and “oil” to search, but couldn’t find any corresponding information.

For example, Aircruising Australia Ltd. which engages in the operations of special interest tour programs and air cruises within and from Australia, but there is no information about fuel expenses and hedging activity in its annual report.

and thus we gather jet fuel hedging information from the footnotes and management discussions in their financial statements. In estimating the hedge ratio for jet fuel, we use the percentage rate of next year requirements hedged which is disclosed in the annual reports. Following Carter et al. (2006a),9 we estimate the hedge ratio for

fuel requirements using the notional value (amount) disclosure or gallons of fuel hedged. In this study, we use both hedge ratio and dummy variable methods (equal to one if firms have positive fuel hedged, zero otherwise) to examine our empirical results.

It is seen in our sample that the more airline companies hedge for jet fuel prices, the less the fuel costs account for their total operating expenses.10 For example,

Transmile Group BHD did not hedge for the risk exposure of jet fuel price in the sample period, and its average jet fuel costs as a percentage of total operating expenses is 36.70%, more than double the average of our total sample firms. In contrast, Iberia, Lineas Aereas de Espana, S.A. and Deutsche Lufthansa AG are all aggressive in hedging activities against higher fuel prices. Their average hedge ratios are 83.19% and 73.14%, respectively and their average percentage of jet fuel costs to total operating expenses are only 12.59% and 9.65%.11

3.2 Proxy for Firm Value

9 Airline companies listed in the US usually disclose the percentage rate of next year requirements

hedged directly, but others outside the US almost disclose the notional value (amount) of derivatives or gallons of fuel hedged. In addition, some airline companies only disclose if they have used financially derivatives to hedge the risk exposure of jet fuel price. Therefore, we also use a dummy variable in empirical tests.

10 We don’t report the results due to space limitations, but they are available upon request.

11 I have divided total sample into two sub-groups according to variable HRD, which indicates whether

airline companies engage in fuel hedging activities or not. Furthermore, I examine if there is significant difference of percentage of jet fuel costs to the total operating expenses for these two sub-samples. The result seems to show that fuel hedging activities of airline companies can reduce their fuel costs at some level.

We measure firm value using Tobin’s Q, which is defined as the ratio of the market value of financial claims on the firm to the replacement cost of firm’s assets. The calculation of Tobin’s Q requires the market value of long-term debt and the replacement cost of fixed assets, but these data are usually not easy to obtain. For this reason, we use the simple approximation of Tobin’s Q, which is developed by Chung and Pruitt (1994),12 their method offers the advantages of computational

efficiency and data availability. We construct Tobin’s Q for each airline company using data from COMPUSTAT and the airline companies’ annual reports. It is measured as follows:

Tobin’s Q = [market value of common stock + liquidating value of preferred stock + (short-term liabilities) – (short-term assets) + book value of long-term debt]/(book value of total assets) (2-1)

all of these accounting data of equation (2-1) are retrieved from COMPUSTAT and measured at the end of year t.

3.3 Other Variables

To examine whether jet fuel hedging can add value to airline companies and the incentives for such activities, we include the following explanatory variables used by

12 Before Chung and Pruitt (1994), the more exact calculations of Tobin’s Q that were typically

employed were developed by Lindenberg and Ross (1981) and Lang and Litzenberger (1989). But their calculation procedures are very complex and cumbersome, for example, L-R’s procedure involves calculating the value of the firm’s long-term debt adjusted for its age structure and the firm’s inflation-adjusted net capital stock. Chung and Pruitt (1994) report that the R2 values of their regressions never fall below 0.966, which means their approximate Tobin’s Q can explain at least 96.6% of the total variability in L-R’s Q.

Allayannis and Weston (2001) and Carter et al. (2006a) in our empirical models.

(a) Firm size: The log of total assets is used to control for the size effect. Most previous studies document that hedging is positively related to firm size (e.g. Nance et al., 1993). This is due to the fact that large firms are more likely to use derivatives than small firms because of the large start-up costs and economies of scale of hedging.

(b) Cash holdings and dividend indicator: If firms fail to obtain sufficient funds when they have good investment opportunities, they may be forced to give up these projects. Consequently, when firms face external financial constraints, their cash holdings become more important. We use a dividend dummy to proxy the ability to access funding from the financial market, since if a firm pays a dividend, it is less likely that they are subject to capital constraints. We expect cash holdings and dividend-paid out ratios to have a negative relationship with hedging activities.

(c) Long-term debt divided by total assets: We use long-term debt divided by total assets to proxy for financial constraints, and we expect firms with a higher debt ratio to hedge jet fuel costs more.

(d) Cash flow to total sales ratio, cash to total sales ratio, Altman’s Z-score and S&P

credit rating score: These four variables are also used to proxy for financial

constraints. If airline companies can generate sufficient cash flow, they are less likely to be affected by financial constraints, and thus may have fewer incentives to hedge.13

(e) Capital expenditures to total sales ratio: Following Allayannis and Weston (2001), we use capital expenditure to total sales ratio as a proxy for the amount of investment opportunities. Froot et al. (1993) and Géczy et al. (1997) show that firms engage in hedging activities are more likely to have greater investment opportunities, so we expect this variable to be positively related to hedging.

(f) Fuel pass-through agreements: If firms have pass-through agreements to facilitate them passing the risk of volatile fuel prices to their partner airlines, they may be less inclined to hedge. We measure this variable by assigning a value of one when firms disclose their fuel pass-through agreements, and zero otherwise.

(g) Charter operation indicator: Charter agreements, like fuel pass-through agreements, allow airline companies to share the risk of volatile fuel prices with a particular customer. When a company discloses that it operates charter flights in its annual report, we set this variable as equal to one, and zero otherwise.

(h) IR derivatives use: If an airline holds interest rate derivatives, this variable is equal to one, and zero otherwise.

(i) Foreign exchange derivatives use: If an airline holds foreign exchange derivatives, this variable is equal to one, and zero otherwise.

(j) Executive options-to-shares outstanding, executive shares-to-shares outstanding,

CEO options-to-shares outstanding and executive shares-to-shares outstanding:

These four variables are used to proxy for managerial incentives to hedge. If managers’ wealth is closely tied to firm’s value, they may engage in hedging activities for their own interests at the expense of other shareholders.

including them reduces our sample size substantially. Although credit rating score is a good explanatory factor, the results do not change when it is excluded

Variables of (a)-(e) are retrieved from COMPUSTAT, and measured at the end of year

t. In addition, we collect data of (f)-(j) from the footnote of firms’ annual reports at

the end of year t.

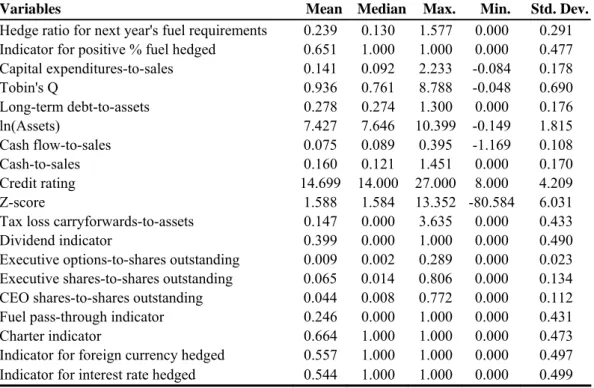

Table 2-2 presents the summary statistics for the entire sample as well as for the other sub-samples. Panel A of Table 2-2 shows summary statistics for the full sample. The mean value of hedge ratio for next year’s fuel requirements is 23.9%.14

It is seen that 65.1% of our sample hedge against the risk exposure of fuel price and about 55% of airline companies use derivatives to hedge the risks of variations in interest rate and foreign currency. The percentage of firms using charter agreements is higher than the percentage using fuel pass-through. Panel B of Table 2-2 shows the summary statistics for US and non-US airline companies. The average hedge ratio for jet fuel of US airlines is 12.3%, which is higher than the 10.9% documented in Carter et al. (2006a). It appears that the hedge ratio of non-US airlines is higher than US airlines, at 25.4%. The percentage of fuel pass-through and charter agreements for non-US airlines is also higher than US airlines, at 5.2% and 34.7%, respectively.

Panel C of Table 2-2 presents the summary statistics for airlines with and without alliances. We can see that airlines with alliances have greater jet fuel hedging than these without, and the former also use more interest rate and foreign currency derivatives than non-alliance airlines. The summary statistics for sub-samples based on the periods of stable fuel price and volatile fuel price are presented in panel D of Table 2-2. The average annual jet fuel prices in our sample are 54.50 and 102.50 cents per gallon in the stable and volatile periods, respectively. The fuel price almost

14 This average ratio is estimated across all non-missing firm-year observations. Other averages are

as follows: 34.8% across all firms with an equally-weighted basis and 39.6% across firm-year observations with a positive hedge ratio.

doubled from the stable to volatile period, while the standard deviations of fuel prices were 8.18 and 38.67 cents per gallon, respectively.15 The price of jet fuel was not

only soaring rapidly, but also was volatile during our sample period. We can see that the mean value of hedge ratio in the volatile period for our sample firms is greater than that in the stable period. It could be that airline companies in the volatile period hedge more to protect their profits from the rising oil price, and also that they use more fuel pass-through and charter agreements to mitigate the oil price risk.

4. Does Jet Fuel Hedging Increase Airlines’ Value?

We use the following model to examine the relationship between airlines’ fuel derivatives usage and its impact on firm value.

log(TobQ)it = α + β1 CapExpit + β2 LTDAit + β3 log(Assets)it + β4 CFSit

+ β5 Cashit + β6 Dividendit + β7 HRDit + β8 PassThuit

+ β9 Fxhedgeit + εit (2-2)

where log(TobQ)it is the natural logarithm of Tobin’s Q for firm i in year t. CapExpit

is the capital expenditures to total sales ratio for firm i in year t, and LTDAit is the

ratio of long-term debt divided by total assets for firm i in year t. log(Assets)it is the

natural logarithm of firm’s total assets for firm i in year t. CFSit, Cashit and

Dividendit are the cash flow to total sales ratio, cash to total sales ration and dummy

15 The data used to estimate the average annual jet fuel price and standard deviation for these two

variable of firm’s cash dividend paid for firm i in year t, respectively. HRDit is the

indicator for jet fuel hedged for firm i in year t. PassThuit and Fxhedgeit are dummy

variables of fuel pass-through agreements and foreign exchange derivatives use for firm i in year t, respectively. And εit is the error term.

We use two models to run the regressions.16 In Model 1, we use a dummy

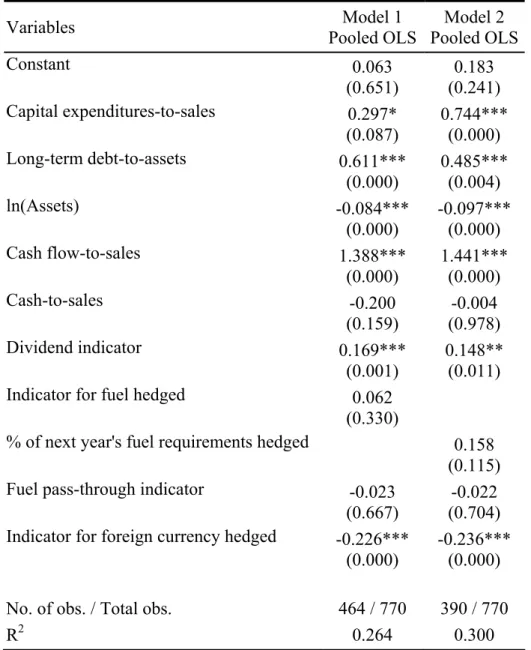

variable for fuel-hedging (HRD) in pooled OLS regressions which account for correlation of the observations across time for a given firm (firm effect) and correlation across firms for a given year (time effect), and report p-values using standard errors corrected for both clustering by firm and clustering by year suggested by Petersen (2009). The difference between Models 1 and 2 is that the fuel-hedging dummy variable used in Model 1 is replaced by the percentage of next year’s fuel hedging requirements (HR) in Model 2. The dependent variable is the natural logarithm of firm value, which is proxied by Tobin’s Q.

Table 2-3 reports the results regarding the relationship between jet fuel hedging and airline value. Contrary to Allayannis and Weston (2001) and Carter et al. (2006a), our empirical results show that there is not a significantly positive relation between hedging activities and firm value. In panel A of Table 2-3, we can see that jet fuel hedging does not add value to airline companies significantly, and this result is robust to different measures of jet fuel hedging proxies. In Model 1, although the coefficient for fuel hedging is positive (6.2%), it is not statistically significant. This illustrates that an airline which uses derivatives to hedge fuel price risk has no effect on its firm value. In Model 2, the percentage of next year’s fuel requirement hedged was used as an indicator for jet fuel hedging. Our results indicate the coefficient is

16 The correlation coefficient matrix shows that there is only one coefficient great than 0.5 among

variables. We also use the VIF (Variance Inflation Factor) to examine the concern of multicollinearity. The results show that all of these variables used in empirical tests have low VIF values, which indicate that the problem of multicollinearity is not serious.

positive but not statistically significant. This results is consistent with Jin and Jorion’s (2006) findings, they find that hedging does not seem to affect firms’ market value for U.S. oil and gas producers. Overall, our results show that investors seem not to value airlines’ jet fuel hedging activities, and do not reward hedging firms with a higher valuation.

In Panel B of Table 2-3, we focus on the sub-groups of US and non-US airlines, with 31 firms in the former group and 39 in the latter. Our results for the US sample are similar to those reported in Carter et al. (2006a), in that airlines which engage in fuel hedging activities can increase firm value. The coefficient for fuel hedging in Model 2 is statistically significant at the 10% level when a continuous hedging measure is used and the average hedging premium is 7.87%.17 In contrast to the US

airline companies, there is no significantly positive relationship between fuel hedging and firm value for non-US airlines. However, the summary statistics in Panel B of Table 2-2 show that the average percentage of fuel hedged for next year’s fuel requirements of non-US airlines is higher than that for the US airlines. It seems that the higher level of jet fuel hedging has lower effectiveness for the non-US airlines.

We also explore whether it is possible for non-US airlines to shift fuel price risk with alternatives such as fuel pass-through or charter agreements for jet fuel hedging. The results from Models 1 and 2 for the non-US sample show that fuel pass-through is an important mechanism to offset the risk of rising fuel-prices,18 and the coefficients

of fuel pass-through are statistically significant in the two models of non-US airlines.

17 The average hedge ratio is 27.14% across firm-year observations, with positive hedging in US

airlines.

18 Another mechanism of transferring fuel price, the risk-charter agreement, also plays an important

role to reduce risks for non-US airlines. We do not include it in the regressions because it will reduce our sample size in the following analysis. The function of charter agreements is similar to fuel pass-through for airline industry, so we drop it in the tests. Our results are robust to this variable. The same reason is also applied for indicator of interest rate.

The average percentages of using fuel pass-through and charter agreements with positive fuel hedging are 4.55% and 28.83% for US airlines, and the figures are much higher (29.31% and 80.93%) for non-US airlines. Comparing the summary statistics presented in Panel B of Table 2-2, it sees that US airlines with positive fuel hedging employ less fuel pass-through and charter agreements, while non-US airlines with positive fuel hedging have more fuel pass-through and charter agreements. Notably, this shows that US airlines are more efficient at hedging with jet fuel derivatives than non-US airlines are. Thus, non-US airlines need to use additional mechanisms to transfer their jet fuel risk exposures, if they are to receive the same benefits as US firms.

In Panel C of Table 2-3, we focus on sub-samples based on airlines with and without alliances. There are 31 airline companies that are part of alliances in our sample, and 39 firms that are not. It is found that jet fuel hedging adds no value to alliance airlines, but can increase firm value for non-alliance airlines. The coefficient is statistically significant at the 1% level, and the average hedging premium is 19.48%.19 This indicates that non-alliance airlines with positive hedging

for jet fuel can add 19.48% hedging premium to their firm value compared to firms without hedging.

It is an interesting question as to why fuel hedging has a positive impact on the firm value of non-alliance airlines, while only an insignificant effect on that of alliance airlines. One possible explanation is that the operational efficiencies of airlines with alliances is already high, so their firm values are affected less by oil price changes (Kleymann and Hannu, 2001). Kleymann and Hannu (2001) show that alliance airlines have benefits of resource utilization to increase labor and aircraft

19 The average hedge ratio is 38.13% across firm-year observations, with positive hedging in

productivity, and also that their costs for procured goods and services are lower. As such, their cash flows and ultimately firm value are less vulnerable to variations in fuel price. In contrast, non-alliance airlines are more vulnerable to variations in fuel price, and so hedging can increase their competitiveness and has a positive influence on firm value.

Panel D of Table 2-3 reports the regression results for the sub-samples of stable and volatile fuel price periods. The evidence shows that fuel hedging can increase firm value, but the coefficient is not statistically significant for both periods. In the preceding section, we found that the averages and standard deviations of jet fuel prices are different in these two periods. In the stable period, airlines’ operating cash flows and profit are less threatened by rising fuel price, and hence hedging has a smaller impact on firm value. We can see that the mean value of the hedge ratio is smaller in the stable period than in the volatile period, and fuel pass-through and charter agreements are also used less often to reduce the fuel price risk in the stable period. On the other hand, we expect that airlines’ operating cash flows and profit are affected more by the soaring fuel price, and in order to keep their earnings and capital expenditures stable, firms need to hedge fuel price risk more in the volatile period. However, we do not observe this significantly positive relation in our empirical results. Maybe we should extend our studying period to reflect the influence of the changes of fuel price on firm value.

Table 2-3 provides important evidence that jet fuel hedging has no significant effect on firm value for the global airline companies, although the results vary for different geographic regions, whether joining alliances or not, and for times of stability and volatility. The empirical results demonstrate that this positive and significant relationship can be observed in the sub-samples of US airlines,

non-alliance airlines.

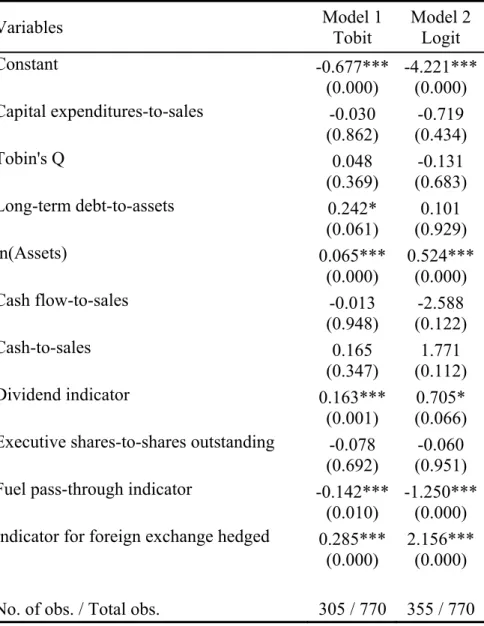

5. The Determinants of Jet Fuel Hedging of Global Airlines

5.1 What Factors Explain Airlines’ Hedging Behavior?

Previous researchers have found several reasons for firms’ hedging activities, and these can be classified into three categories, namely tax incentives, managerial incentives, and financial distress and underinvestment costs. In this section, we examine whether these factors provide explanations for the hedging premium in the global airline industry. The model is specified as follows.

HRit = α + β1 CapExpit + β2 LTDAit + β3 log(Assets)it + β4 CFSit

+ β5 Cashit + β6 Dividendit + β7 ExeSharesit + β8 PassThuit

+ β9 Fxhedgeit + εit (2-3)

where HRit is the % of next year’s fuel hedging requirements at the end of the fiscal

year, and ExeSharesit is the % of shareholdings executive management held to the

total shares outstanding at the end of the fiscal year. The rest of variables are the same as in Equation (2-2). We use two models to examine this relationship. In Model 1, we apply the Tobit model using the percentage rate of next year’s fuel hedging requirements at the end of the fiscal year as the dependent variables. We take account of fixed effects in each regression. In Model 2, we apply the Logit model using a dummy variable equaling one if a firm’s hedge ratio is greater than zero,

and zero otherwise as the dependent variable. We also use standard errors corrected for both clustering by firm and clustering by year suggested by Petersen (2009) to report p-values.

In Panel A of Table 2-4, the results show that firm size, fuel pass-through and whether the firm engaged in currency hedging or not all have a significant impact on airlines’ hedging behavior. The positive coefficient on firm size suggests that economies of scale also play an important role for such companies. This result is consistent with that in Nance et al. (1993), and implies that economies of scale in risk management may apply to the operational and transaction costs of hedging, and the high start-up costs of risk management may only be affordable by large companies. It is seen that fuel pass-through agreements also have explanatory power in the regression models. The coefficients in both models are negatively significant, which indicates that fuel pass-through is an method of transferring jet fuel price risk. In addition, airlines engaged in foreign currency hedging activities also have more jet fuel hedging. In Model 1, we find that dividend paid can affect fuel hedging decision for the global airlines. The coefficient is positive at the 1% significant level, which is consistent with Breeden and Viswanathan (1999). They document that better-performing firms may have incentives to hedge to preserve their higher profitability.

In Panel B of Table 2-4, we examine the hedging incentives between US and non-US airlines. We find that the coefficients of firm size and the usage of currency hedging are significant to explain airlines’ hedging activities. Consistent with Carter et al. (2006a), we find that fuel pass-through has a negative impact on US and non-US airlines’ hedging behavior, due to the fact that fuel pass-through is an important alternative in mitigating the risk exposure of jet fuel price, and it can reduce the use of

fuel hedging derivatives. For non-US airlines, the coefficients of cash flow-to-sales and executives’ shareholdings are statistically significant at the 5% and 1% level respectively. The negative coefficient of cash flow-to-sales is consistent with a financial constraints argument, which implies that airlines that generate sufficient cash flows tend to have lower incentives to hedge. The positive coefficient of executives’ shareholdings demonstrates that the higher the executives’ shareholdings, the more the firms tend to hedge. This result is consistent with prior studies (Smith and Stulz, 1985; Tufano, 1996), and suggests that the more the executives’ wealth is tied to firms, the more likely they are to hedge for fuel price risk.

In Panel C of Table 2-4, we examine the hedging incentives for airlines with and without alliances. The results show that the coefficient for dividend payout has a positive impact on alliance firm’s hedging decision, which is against our earlier expectations. However, Breeden and Viswanathan (1999) suggest that better-performing firms may have incentives to hedge in order to maintain higher profitability, and results that are not reported indicate that the average ROE and ROA for alliance airlines are better than non-alliance airlines in the sample period.20 Thus,

alliance airlines may want to hedge more so that they are less affected by fuel price changes. For non-alliance airlines, fuel pass-through is significantly related to hedging activities. Compared to alliance airlines, they do not enjoy the benefits of operational efficiencies from alliances, so their cash flows are more vulnerable to fuel price changes. They use more other substitute mechanisms to transfer the risk of fuel price.

Panel D of Table 2-4 reports the results of hedging determinants for stable and volatile fuel price periods. The coefficients for firm size and foreign currency usage

20 Average ROE and ROA are -4.23% and 0.60% for alliance airlines, and are much higher (-14.31%

are also statistically significant in both periods. In the stable fuel price period, airlines tend to hedge to reduce the financial distress costs, because the coefficient of debt ratio are positively and significantly related to hedging activities, and the coefficient of cash-to-sales are negatively related to fuel hedging activities. These results comply with traditional theories that hedging provides incentives to reducing the probability of financial distress. On the other hand, the coefficients of cash-to-sales and dividend payout are positively and significantly related to hedging, which indicates that better-performing airlines want to protect their profit levels during times with volatile fuel prices period. We show that executives’ shareholdings are negatively related to hedging activities, and this is consistent with the findings in Galai and Masulis (1976) and Saunders et al. (1990). They find that managers with higher equity ownership tend to take more risk. Our results also show that fuel pass-through is a good substitute for fuel hedging in volatile periods, and the greater the use of the pass-through mechanism, the less hedging that airlines need to engage in.

5.2 Does Underinvestment Problem Play An Important Role in Explaining Airlines’ Hedging Behavior?

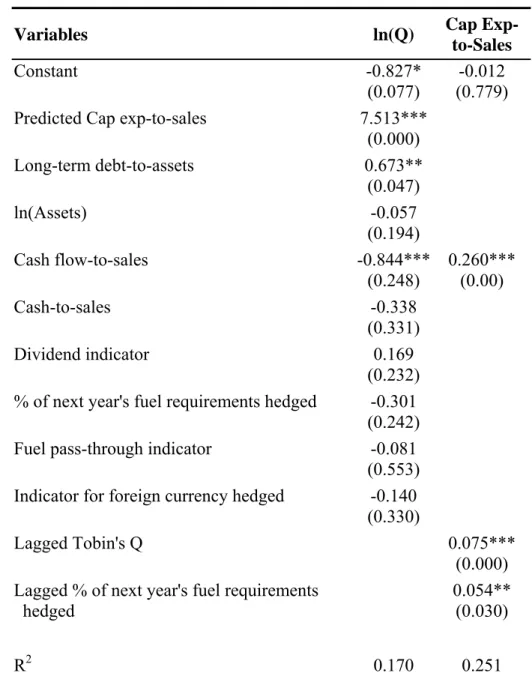

Airline companies tend to undertake hedging activities in order to make sure that future capital expenditures are less affected by high jet fuel prices. Jet fuel hedging can allow them to obtain sufficient funds to undertake valuable investments in the future, and thus, current capital expenditures might be the result of earlier hedging. Consequently, investors would value capital expenditures made by hedgers more highly, because they send a signal that good investment opportunities are expected in the near future. To examine this issue, we use a two-stage regression model, as

follows:

CapExpit = γ + δ1 CFSit + δ2 lag(TobQ)it + δ3 lag(HR)it + υit (2-4)

log(TobQ)it = α + β1 Pred(CapExp)it + β2 LTDAit + β3 log(Assets)it

+ β4 CFSit + β5 Cashit + β6 Dividendit + β7 HRDit

+ β8 PassThuit + β9 Fxhedgeit + εit (2-5)

where lag(TobQ)it and lag(HR)it are lagged Tobin’s Q and lagged percent hedging

variables respectively. Pred(CapExp)it is the predicted value of capital expenditures

from Equation (2-4). υit is the error term of Equation (2-4). The rest of variables

are the same as in Equation (2-2). We use 2SLS (tow-stage lease square) estimate controlling for fixed effects in the empirical regressions, which is suggested by Pagan (1984). In the first-stage regression, we use capital expenditures-to-sales ratio as the dependent variable, and cash flow-to-sales, lagged Tobin’s Q, and lagged percentage rate of jet fuel hedging as the independent variables, as shown in Equation (2-4). The estimated values of capital expenditures-to-sales ratio obtained from Equation (2-4) are then used in the second-stage regression to estimate the link between firm value and the independent variables in Equation (2-5).

Table 2-5 reports these results, and from Panel A, we can see that the coefficient of lagged Tobin’s Q to capital expenditures is positively significant at the 1% level, and the effect of lagged hedging ratio on capital expenditures is also significantly positive. This results show that alleviating the problem of underinvestment is an important factor leading firms to engage in jet fuel hedging activities in the global

airlines. Panel B of Table 2-5 shows that US airlines hedge to mitigate underinvestment problem because the coefficient of lagged hedge ratio on capital expenditures is 11.9%, which is positive and statistically significant at the 1% level. It is thus seen that fuel hedging in the last period can increase firm value by ensuring and enhancing current capital expenditures, and the implied hedging premium from the models is 19.7% [e.g., (0.2714×0.119×8.823) + (-0.325×0.271)]. The first term in the parentheses is the percentage of the hedging premium attributable to the effect of hedging on capital expenditures. This term is more than 100%, which provides evidence in support of Carter et al.’s (2006a) findings that the determinants of jet fuel hedging by airlines are largely consistent with an underinvestment theory. However, the results also show that current capital expenditures are not positively related to fuel hedging undertaken in the last period for the non-US airlines. Thus, hedging to ensure future profitable investment opportunities is not an important concern for non-US airlines.

In Panel C of Table 2-5, the evidence shows that reducing the problem of underinvestment is not an important factor in alliance airlines’ hedging activities, because the coefficient of lagged hedging ratio is not positively related to current capital expenditures. We find that lagged Tobin’s Q also has an insignificant effect on current capital expenditures, and thus, alleviating the underinvestment problem does not play an important role in determining fuel hedging for alliance airlines. In the previous section, we saw that the most important factor in fuel hedging for alliance airlines is to stabilize their profitability. When airline companies expect to have good investment opportunities in the near future, they can finance the project with internally generated funds, which can reduce the effect of fuel hedging on capital expenditures. In contrast, non-alliance airlines hedge to alleviate underinvestment

problems, which is consistent with findings of Froot et al. (1993) that hedging can reduce cash flow volatility to ensure sufficient internally generated funds to complete profitable projects in bad times. The implied hedging premium from the models is 15.35% [e.g., (0.381×0.142×6.999) + (-0.591×0.381)], and the percentage of the hedging premium attributable to the effect of hedging on capital expenditures is more than 200%.

Panel D of Table 2-5 reports the results as to whether reducing underinvestment problems is related to hedging activities in the stable and volatile fuel price periods. In the period of 1995 to 1999, when the fuel price is relatively stable, the airlines tend to hedge to ensure that future capital spending is less affected by fuel prices. The hedging premium is 6.36%, and the effect of hedging on capital spending is also more than 200%. On the other hand, the effect of hedging on capital expenditures is insignificant during the volatile period. Investors place more value on capital expenditures made by hedgers in the stable rather than volatile period, possibly due to the fact that airline companies have better investment opportunities in the stable period, and they tend to use derivatives to hedge fuel price risk to ensure that they can take advantage of them.

6. Sensitivity Checks21

6.1 Using Different Proxy to Measure Firm Value

We use accounting performance measures of ROA and ROE to replace natural logarithm of Tobin’s Q in Equation (2-2). The results show that there is insignificantly positive relationship between jet fuel hedging and firm value in Model

1 and Model 2 when using ROE to proxy firm value, while this positive relationship is significant in Model 1 when using ROA to proxy firm value. Moreover, we also use Tobin’s Q that does not take natural logarithm to run the regression of Equation (2-2), the result shows that jet fuel hedging has significantly positive impact on firm value in Model 2.

6.2 Does “Trend” or “Volatility” of Jet Fuel Price Affect Firms’ Hedging Behavior? According to the rise or fall of jet fuel price comparing with previous year, we divide our sample into two sub-groups. The results show that the higher percentage airline companies hedge, the more their firm value increase in the rising-period. The coefficient is statistically significant at 10% level. On the contrary, the evidence shows that this positive relation is not significant in the falling-period and the coefficients are smaller than those in the rising-period.

7. Conclusions

This paper provides the first in-depth analysis of the impact of jet fuel hedging on the market values of global airlines and the determinants for their hedging behavior. Using a unique data set of 70 airline companies in 32 countries from 1995 to 2005, we find that jet fuel hedging enhances the value of airline companies around the world. Moreover, we show that airlines residing in the US that engage in fuel hedging increase their firm value, while airlines not residing in the US add no extra value to their firms. In addition, we fail to find a significant relationship between fuel hedging and firm value for airlines with alliances, although this relationship is significant for airlines without them. Finally, there is no evidence revealing that fuel

hedging is more valuable in the volatile fuel price period than in the stable fuel price period. This result indicates that airline companies can not protect their firm value from being hurt by surging oil prices by undertaking adequate hedging activities.

Furthermore, we explore the determinants for the jet fuel hedging of global airline companies. The evidence shows that hedging reduces financial distress costs for non-US airlines, and in the period of stable fuel prices. In contrast, alliance airlines and airlines in the volatile period hedge fuel price risk exposures to protect their profitability. Moreover, jet fuel hedging is motivated by managerial risk aversion for non-US airlines, which is consistent with traditional theory, as suggested by Smith and Stulz (1985) and Tufano (1996). On the other hand, our regression analysis also suggests that managerial risk-taking incentives are supported by airlines in the stable period. In addition, we find that the fuel pass-through mechanism can substitute for fuel hedging by derivatives. Consistent with Froot et al. (1993) and Carter et al.’s (2006a) findings, our results show that alleviating underinvestment problems to protect future positive NPV projects is an important consideration for the global airline companies and in the sub-samples of US airlines, non-alliance airlines and airlines in the stable period. Finally, we illustrate that economies of scale and the use of currency derivatives are important factors to explain the fuel hedging behavior of airline companies.

Further research can investigate the impact of corporate governance on risk management in the global airline industry. The differences in corporate governance (including internal and external factors) across countries and their effects on hedging behavior can be examined using internal airline data. Both firm-level governance mechanisms (e.g., ownership and board structures) and country-level governance mechanisms (e.g., investor protection rights) will enable us to investigate the different

Figure 2-1. Average Monthly Jet Fuel Prices (Cents per Gallon) 0 50 100 150 200 250 01/ 1995 07/ 1995 01/ 1996 07/ 1996 01/ 1997 07/ 1997 01/ 1998 07/ 1998 01/ 1999 07/ 1999 01/ 2000 07/ 2000 01/ 2001 07/ 2001 01/ 2002 07/ 2002 01/ 2003 07/ 2003 01/ 2004 07/ 2004 01/ 2005 07/ 2005 Date C ent s pe r ga ll on NY Harbor Gulf Coast Los Angeles