The Puzzle of the Discount Price for the Foreclosed House:

Does the Factor of Competition Explain more Discounts?

*Chin-Oh Chang**

Department of Land Economics, National Chengchi University Mucha, Taipei 116, Taiwan, ROC

Tel: +886-2-29387478, Fax: +886-2-86619365 E-mail: [email protected]

Chien-An Wang

Department of Banking and Finance, National Chi-Nan University 1 University Rd., Puli, Nantou 545, Taiwan, ROC

TEL: (049)2910960 Ext.3129, FAX: (049)2914511 E-mail: [email protected]

Yi-Ju Chen

Research and Consultancy Savills (Taiwan) Limited 12F-3,Exchange Square, No. 89, Sung Ren Road, Xin-Yi District,

Taipei City, Taiwan E-mail:[email protected]

* We appreciate the financial support of the National Science Council, ROC under Grant number:

NSC92-2415-H004.

The Puzzle of the Discount Price for the Foreclosed House:

Does the Factor of Competition Explain more Discount?

Abstract

Using the data of the foreclosed houses and the brokerage houses in Taipei from 2001-2002, we try to answer “Does the factor of competition explain more price discount?” Three main empirical results are found: (1) The average price for the foreclosed houses in the biding market is lower 17.20% than that for the brokerage houses in the searching and bargaining market, controlling other things being equal. We propose the market mechanism such as the foreclosed-housing risk of the buyer exposure, and the participant number of biding can explains more for the deep-discount price. (2) The price discount is 15.99% if one bidder involves. Moreover, the more participant number of biding is, the lower price discount between auction market and search market is. This implies that full information disclosure can increase the competition and reduce the price discount of foreclosed houses in the court-oriented auction market.

I. Introduction

Traditionally, there are two mechanism intermediaries that deal with the transaction of the housing market: The first mechanism is called the search market or listing market, which is through the housing broker to exercise the private bargaining process; the second mechanism is the auction market which is applied to the sell of the non-performance loan (hereafter, NPL), particularly to the housing collateral. There are also three sub-types of auction markets in Taiwan: the most common is the foreclosed house, auction by court indirectly, auctions by banks directly, and auctions by bank companies1 newly. Among them, the foreclosed house occupied the most transaction amounts. According to the Statistics of Construction published by the Building Research Institute of the Interior Ministry it indicates that the shared ratio of the 17,000 foreclosed cases to

1 From the perspective of the auction, the common situation for foreclosed housing, auction by

banks, and auction by the bank company: all of this means that the lender who wants to buy the house, because of a broken contract, causes the creditor bank to auction the real estate. The difference lies in: three different organizations that practically carry out auctions. More details: (a) Foreclosed housing is based on law enforcement: the process of foreclosure is the first

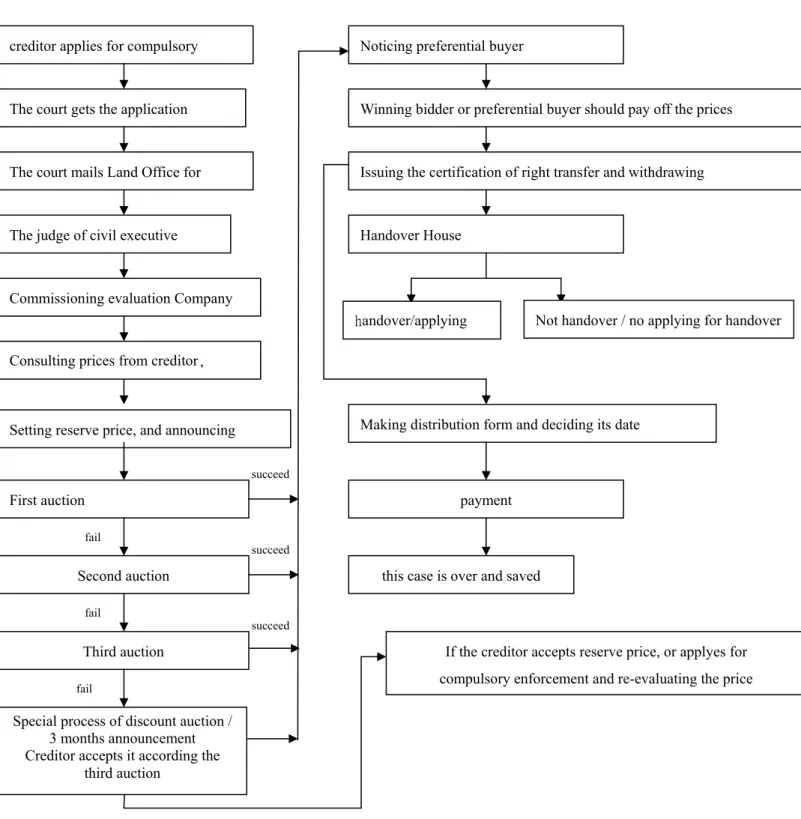

procedure that NPL financial institutions (mostly banks) will be required to take in accordance with "law enforcement" in the name of the implementation, then an appeal to the courts for the enforcement procedure to liquidate claims (in this study referring to the auction house) is made. So, foreclosed homes are the most traditional method of real estate auction, and having the most history, the actual number of cases is the highest. As for the process of foreclosed housing and of the starting bid setting, please refer to the Appendix for a more detailed explanation.

(b)Auction by banks refers to banks accepting the cases that the court had auctioned and/or directly commissioned the professional seller to auction. Since its start in July of 2001, City Bank commissioned a business organization in Hong Kong, CB Richard Ellis, to auction its excess collateral houses, and introduce live bidding (public, oral auction) throughout the auctioning community.

(c) Auctions by the bank company are based on Article 15 of the Financial Institution Merger Act, establishing "Taiwan financial assets Service Co., Ltd. (TFASC)," whose main business is to assist the court in the implementation of the auction, as well as commissioned by the bank to auction its bad assets. So far, the type of auction objects can be divided into auction by the bank company and auction by banks. In October of 2002, TFASC launched the exceeded house auction, which was commissioned by the court. Therefore, its auction process is similar to that of a foreclosed house, except in practice, foreclosed housing is still the main case when banks deal with such NPL. If the fourth foreclosure is still not sold, the items will appear up for auction by banks, so most people think that the quality of auction by banks may be worse than that of foreclosed houses.

all sold cases is 8.79% in 2001, increasing to more than 20,000 and shared 11.44% in 2002. In spite of the rising trend of foreclosed cases, it gets little attention for the academic researcher, policy-markers and real estate investors. One interesting topic is the “discount price puzzle” of the foreclosed houses, even we control the quality of housing (Chang and Tsai, 1997). From the viewpoint of market mechanism, our study tries to explain this puzzle owning to two main reasons: Firstly, the different price mechanism between the "bidding" process in the foreclosed market and the “bargaining” process in the search market, cause the price gap under the control the same housing quality. Secondly, the information asymmetry and the competition degree of these two different markets imply the different risk of these two cases and cause the price gap. As far as the price mechanism is concerned, Wang (2004) supports the efficiency of the bidding mechanism based on the foundation of behavior finance. He insists that the bidding process will allocate the resource into the most valuable use and reach the favorable price2. However, he can not explain why the foreclosed price in Taiwan is lower than the bargaining price in spite of the efficiency of bidding process. Moreover, the contrary conclusion would be found in related non-Taiwan data research. For example, Krishna (2002) suggests that the auction market provides more information about the object and then pushes the price up to the normal market price. Using both data of the foreclosed bidding and the search bargaining in Austin of Texas, Quan (2002) confirmed the premium phenomenon existing in auction market by the GMM selection model. Lusht (1996) estimated the average premium of bidding is 8% for the data of Melbourne in Australia. Dotzour, Moorhead, and Winkler (1998) estimated the premium figure is about 5.9 to 9.5 %. Hence, the price discount for the foreclosed bidding cases existing in Taiwan is anomalous and unique, and this drives our motivation

Several possible reasons can be explained the abnormality of price discount for the foreclosed bidding cases. One is the difference of design of bidding

2 Bidding ensures that the seller with the lowest cost can do business, and the buyer was guided to

the seller who has the highest efficiency; to the contrary, bargaining need to come up with a negotiation strategy, and spending time with bargaining; in the end, the final outcome might not be able to be made with an agreement, so the transaction costs are relatively higher (Mayer, 1998).

mechanism. The "first-price sealed-bid action" system was approved in the court-foreclosed case and the bank company bid. The bidders wrote their price willing to pay on the bidding sheets, and then the price sheets are sealed. The houses of the auction object will be sold to the highest bidder after publishing the bid sheets while all bidding prices are listed in public. Relatively, the open auction market is normal in other countries, and the prices are formed as the way of "English auction". That is, starting from the auction price that the auctioneer has set, then bidders will gradually raise their own prices until no one is willing to bid; the highest price is the winning bidder. Radosveta and Salmon (2004) pointed out that, generally, bidders prefer English auctions, because they can guess the bidding behaviors by the number of competitors and, then, the bidders in the English auction share lower risk than those of a sealed auction do. In other words, they believe that bidders will have a higher willingness to bid than during a sealed-bid auction under an English auction, and the actual price will be pushed.

Second, the foreclosed houses always have less information, and leads lower competition. Base on the theory of information asymmetry, Akerlof (1970) suggests that the lemons problem3 as the foreclosed cases, exist the price discount. For details some, the court-foreclosed houses have more uncertainly and invisible risk, such as the high uncertainty of complete property rights, including the problem of not inspecting and handing over the auction house; though it does so often, it is hard to prevent the possibility of house destruction. Most people think that foreclosed houses are at a higher risk, believing good quality will not be in the foreclosed housing market. According to the “hedonic price” theory of Rosen’s (1974) study, the market price of a house is composed of a bundle of

3 The so-called Lemons Problem means, under information asymmetry, that the buyer can not

ensure the quality of products that the seller sells, so they are only willing to pay an overall average price. With such prices, the seller is not willing to sell the best quality products available to them, and tends to also not sell the lesser quality products (lemons). But, the buyer knows the possible behavior of the seller, so some buyers prefer the transparent information market, and reduce the consumption in this market, ultimately leading to to a "credit rationing" effect. However, strictly speaking, the foreclosed house market and the lemon market are not fully applied. For example, being a seller in a foreclosed house market is not voluntary, most of the buyers tend to be investors, though the seller would raise the starting bid to avoid been auctioned, the purpose in raising prices is different from the lemon market. In addition, the seller will not deliberately market the products (cost of dishonesty) in order to sell out.

utility the discount in foreclosed houses reflects the different intangible risks. More detailed will be discussed next paragraph.

As far as the information asymmetry is concerned, the information of foreclosed houses in Taiwan is not fully disclosed and less transparency. For example, the information of court- foreclosed cases is usually only posted on court bulletin boards and a limited public channel, such as the Transparent

Housing Market magazine and the website of individual bank’ credit department.

On the contrary, foreclosed cases in other country are exercises by the professional companies, and the auction information is revealed publicly at a certain period. Quan (1994) found that the more transparency of information disclosure, will leads to the higher housing price, owing to more bidders to participate in and competitive bidding behavior.

As far as the less competition is concerned, the Statistics of Taipei Court-Foreclosed Housing indicates the only one bidder shares 46.6% of all auction cases, and lower bidding price may be due to this less competition4. Three possible explanations will be suggested: Firstly, some ignorant design of current physical auction system makes oligopoly benefits shared by certain “professional investors”. For example, it is easier for experienced investors to distinguish potential competitor from a single auction box makes. Some illegal cases show that these “professional” investors have the common acknowledge via threaten ways that only one bidder will be. That is, the bidder will pay the reserve price, even if the auction will continue and the reserve price next time will be lower than the price at the former round. Relatively, Christy and Zaichkowsky (2003) argue that the “really “professional bidders decide their auction strategy following the observation other competitors’ intentions.

Secondly, the different process to form reserve price: the starting price of foreclosed houses in Taiwan is evaluated by the court delegated agent, such as the private appraisal company, then the court will refer to the opinions of the creditor and the debtor (the owner of the foreclosed house). However, the debtors (the owner of the foreclosed house) have incentives to disagree all because they are

4 For more detailed analysis of the foreclosed housing information, please refer to statistical data

unwilling to deal with by auction for their any property. The price is also set in other countries by the professional appraisal company, however, the delegated auction company usually set the lower starting price to attract more buyers to participate in the auction, and then the market price will be revealed, even if the higher price is forced.

Finally, the restrictive funding for the court-foreclosed houses: the participants are required to pay 20% of starting price for deposit, and the bidder needs to settle remains within seven days. Financing in such urgent periods causes the higher cost of foreclosed houses than that of search market, and makes the entrance obstacle for the generals. Mayer (1998), using the auction data of the Los Angeles housing market, found that single-sites are sold with a premium; relatively, condominiums are sold on a discount because of the inferior quality and time poorly matched. On the contrary, the sample of single-site auction share the premium because of the more attention and more competition in the local market.

All in all, products in the Taiwanese real estate market apply to a “bidding auction system”, produced in the real estate of NPL after financial turmoil. Therefore, by comparing domestic and foreign differences in mechanism design of real estate auction, we can discuss the differences in forming reasons of premium and discount in auctions and search markets. Generally, although the information exposed is still insufficient in the search market, compared to the foreclosed market, the search market has better “information disclosure” and “competitive power”. Furthermore, by discussing the above two reasons, and providing feature suggestions pertaining to the “auctioning” of Taiwanese foreclosed houses, an upgrade from the final bid to the level that should be will be this research’s contribution.

The structure of the paper is as follows: Section two will further describe the domestic market of foreclosed housing numbers, the amount, competition (such as auction period), and other characteristics. Section three is about the analysis of sources of information and statistics of variables’ basic descriptions. Section four is the model of establishment, and the reports of empirical results, which mainly analyze whether the price of a foreclosed house is lower than the price of the

search market. If it is, how much lower is it than in the search market? What is the main cause behind the price difference? And, especially, questioned will be whether the "market competition" can explain discount phenomenon more or not. Finally, section five discusses conclusions and policy recommendations.

II. The Characteristics of Foreclosed Housing Market in Taiwan

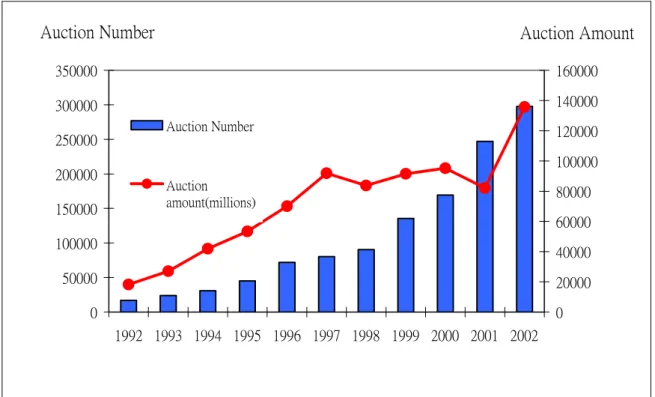

Figure 1 shows statistics of national foreclosed housing numbers and the amount known from 1992 to 2002, a total of ten years. In 1992, there were 17,000 cases; after 1996, it shows a rapid growth trend; 1999 is the first time that the case of national foreclosed houses broke 100,000, and the amount of final bids has thus increased significantly. Then, in 2001, cases of foreclosed houses rose once again, and creating more than 200,000 cases nationally. Finally, in 2002, the amount of the final bid of national foreclosed houses increased to 135.655 billion NT dollars. So, we see the rapid growth of the foreclosed housing market.

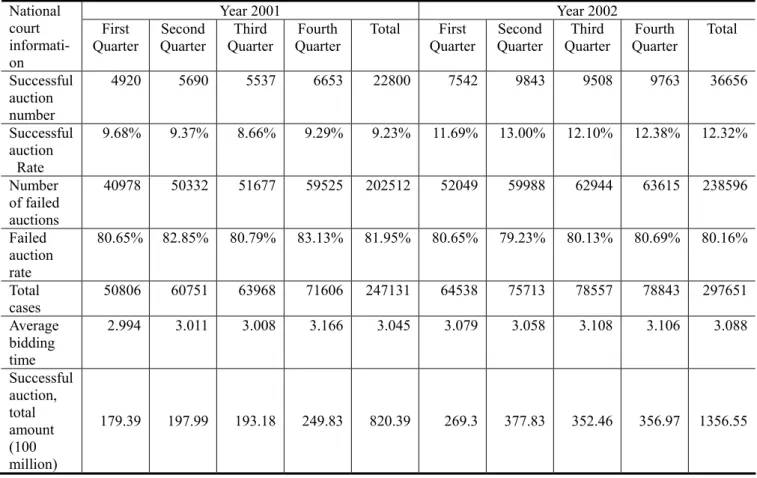

Table 1 is based on the National Court, which provides more detailed classified information on foreclosed houses, showing statistics from the time of 2001 to 2002, totaling two years. It is concerned with successful and failed auction numbers, successful and failed auction rates, average auction times, the total amount of successful auctions, and so forth. In especially, we have to notice that a “high number of auctions” represents that the bottom price of the first auction may be higher than the average market price, which causes a high auction time and high failed auction rate. The statistical data in the table shows that in the first season of 2001, the court announced there was more than 50,000 real estate auction cases, and the successful auction rate was 9.68%, the failed auction rate was 80.65% , and the average auction times was 2.994 bids; in the fourth season of 2001, the court announced that real estate auction cases had exceeded 70,000, the successful auction rate was 9.29%, the failed auction rate was 83.12%, and the average auction times had increased to 3.166 bids; in 2002, during its first season, the court noticed real estate auctions slightly decrease to 60,000 cases, but the successful auction rate increased to 11.69%, the failed auction rate to 80.65%, and the average auction times to 3.079 ; during the fourth season of 2002, national courts announced that real estate auction cases numbered at slightly over 7,000, its successful auction rate was 12.38%, the failed auction rate was 80.69% , and the average times was 3.106. Overall, the foreclosed housing market has developed rapidly in recent years, the total number of cases has increased steadily,

and the successful auction rate has continually increased since the fourth season of 2001, but since the second season of 2000, it has stabilized; the average auction time remains around three bids.

Table 2, Panel B represents research studies of the time from 2001 to 2002 and its residential samples are geographically only in Taipei, and its comparative characteristics statistics of the foreclosed housing market shows: (1) the average auction times is 3.06. (2) The average amount of bidders is 2.77 within a single successful auction case. The data reveals there are less than three competitors in every foreclosure case, and the participants are relatively insufficient. (3) In each successful auction case, 74.17% of cases are handovered; a proportion much higher than not-handovered cases which numbered at 80% before the Compulsory Execution Law was updated in 1996. (4) The rate of objects described as vacant is only at 25.87%5. In the table, the auction time of foreclosed houses in Taipei is not much different from three auction times of national foreclosed houses. But, in regards to (2), (3), (4), and other data, the court does not publish “national” foreclosed market information, so there is no way to compare data.

5The information is from the successful auctioning of foreclosed houses in the Transparency Real

Estate Journal. In the column of “usage condition”, it is clearly pointed out that the auction is vacant or uninhabited; it is the sample’s identification of vacant houses.

0 50000 100000 150000 200000 250000 300000 350000 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 Auction Number 0 20000 40000 60000 80000 100000 120000 140000 160000 Auction Amount Auction Number Auction amount(millions)

Figure 1 National Foreclosed Housing Auction Numbers and Auction Amount from 1992 to 2002 in Taiwan

Table 1 Statistics of Each Quarter for National Court Foreclosed Houses from 2001-2002 Year 2001 Year 2002 National court informati-on First

Quarter Quarter Second Quarter Third QuarterFourth Total First Quarter QuarterSecond Quarter Third Quarter Fourth Total Successful auction number 4920 5690 5537 6653 22800 7542 9843 9508 9763 36656 Successful auction Rate 9.68% 9.37% 8.66% 9.29% 9.23% 11.69% 13.00% 12.10% 12.38% 12.32% Number of failed auctions 40978 50332 51677 59525 202512 52049 59988 62944 63615 238596 Failed auction rate 80.65% 82.85% 80.79% 83.13% 81.95% 80.65% 79.23% 80.13% 80.69% 80.16% Total cases 50806 60751 63968 71606 247131 64538 75713 78557 78843 297651 Average bidding time 2.994 3.011 3.008 3.166 3.045 3.079 3.058 3.108 3.106 3.088 Successful auction, total amount (100 million) 179.39 197.99 193.18 249.83 820.39 269.3 377.83 352.46 356.97 1356.55

Note: 1. the statistics information only applies to the number of successful auctions, and number of failed auctions, not including withdrawn numbers, so the total does not reach 100%. 2. The measurement of the final bid is one-hundred million.

III.

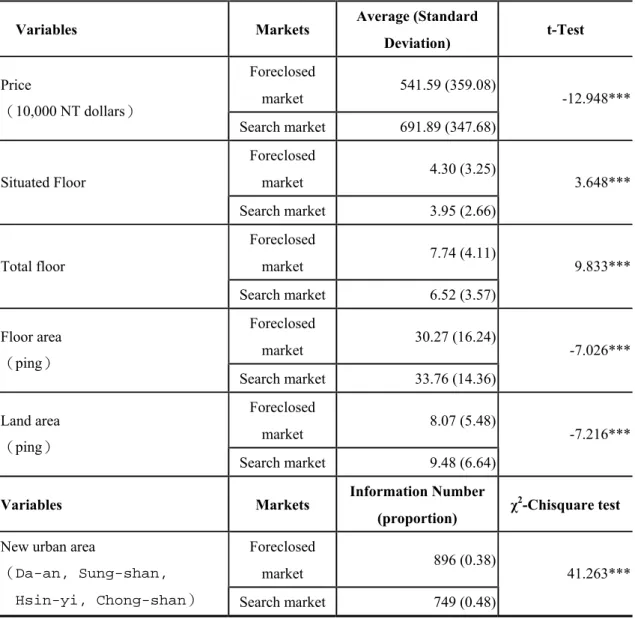

The DataAlthough the first two sections separately describe Taiwan and Taipei City two regional foreclosed housing markets, including case number, amount, and auction times, etc, it is shown only in bargain information recorded in Taipei City’s brokerage-searching market which of the two has more active trading activities. Based on available and comparative information of foreclosed housing (mainly observed samples) and bargaining (control samples), the follow-up evidence can only be selected from the time of 2001 to 2002, in Taipei, as successful foreclosed housing auction and search market transactions information, to use as study samples. About "successful foreclosed housing auction information": the study uses the court’s successful auction information published by the Transparent Real Estate Journal, initially selecting 2,485 "residential category" cases of successful foreclosed housing auctions’ information as the study scope6, then removed some missing items, and ultimately coming up with 2,354 available samples. As for the "search market information": it is from a large domestic brokerage company who provides 2,079 cases of brokerage transaction information. Then we removed partially missing cases numbering at 323 cases, and 164 cases of official information, so finally the available samples totaled 1,546. About the "price" and "entities quality": basic descriptive statistics of variables are shown in Panel A of Table 2 below:

(1) About "residential prices": Whole samples’ (including foreclosed houses and transaction houses through intermediary bargaining) standard residential prices are at NTD 5.9654 million. Among them, the average final bid for

6 In the process information selection, this study will exclude the following "non-residential

simple" seven samples: (1) pure land auction, (2) pure housing auction, (3) different bidding objects but mortgage together, (4) the entire building auction, (5) office purpose (more than 150 square meters, and the status of the rental purpose is for corporate office), (6) additional build samples, because the additional build will account into auction, but it not necessarily gains property rights protection, so this data will be retained first, not included in analysis, (7) other samples can be seen if it is non-residential by seeing its current situation, such as: market stalls.

foreclosed houses is NTD 5.4159 million, less than the search market’s average transaction price, which is NTD 6.9189 million. The foreclosed market compared to the search market averages lower at about NTD 1.503 million.

(2) About "residential quality": (a)Foreclosed housing is on average situated on the 4.3rd floor and the construction’s average total floor height is 7.74 floors,

foreclosed house comparisons to the search market is on average higher by 0.35 floors, the average floor area is 30.27 pings, and the average land area held is 8.07 pings. (b) For the "search market transactions sample", the average situated floor is 3.95th floors, construction’s average total floor is

6.52 floors, average floor area is 33.76 pings, and the average land area held is 9.48 pings. Therefore, foreclosed house compares to search market are average higher for 1.22 floors, the average floor area is less for 3.49 pings, and land area held is less for 1.41 pings.

(3) About "residential location": this study was conducted according to general housing prices and the actual situation of urban development; it divides Taipei City’s twelve districts into three categories: the new urban areas, the old urban areas, and suburban areas. Its classification standards implied economy significance, which is a vital factor of price: "economic location" rather than "administrative location". Before, while Lin, Yang, and Chang (1996) was discussing the Taiwanese domestic price index, they were still using "economic location," the classified methods used by foreign research7. Within

the successful 2,354 cases of foreclosed homes, the new urban areas took up 48%, the old urban areas 17%, and the suburban areas 34%. Within the 1,546 cases of the search market, the new urban areas took up 38 %, old urban areas

7 Thanks to one of reviewers’ reminder to this question. The classified standard is as follows:

(1)new urban area are Da-an, Sung-shan, Hsin-yi, Chong-shan. (2) Old urban area is Chong-Cheng, Wan-hua, Da-tong. (3) Suburbs means the area around Taipei City, which are Wen-shan, Bei-tou, Shih-lin, Nan-kang and Nei-hu.

18%, and suburban areas 44%. Therefore, foreclosed houses that were situated in new urban areas were less average than the search market, which was at 10%; foreclosed houses that were situated in suburban areas were more average than the search market being at 9.69%.

Table 2 The Statistics of Successful Foreclosed House Auction Sample And of Search Transaction Sample in Taipei City from 2001 to 2002

Panel A: Comparison of Residential Price and Attributes

Variables Markets Average (Standard

Deviation) t-Test Foreclosed market 541.59 (359.08) Price (10,000 NT dollars) Search market 691.89 (347.68) -12.948*** Foreclosed market 4.30 (3.25) Situated Floor Search market 3.95 (2.66) 3.648*** Foreclosed market 7.74 (4.11) Total floor Search market 6.52 (3.57) 9.833*** Foreclosed market 30.27 (16.24) Floor area (ping) Search market 33.76 (14.36) -7.026*** Foreclosed market 8.07 (5.48) Land area (ping) Search market 9.48 (6.64) -7.216***

Variables Markets Information Number

(proportion) χ

2-Chisquare test

Foreclosed

market 896 (0.38)

New urban area

(Da-an, Sung-shan,

Hsin-yi, Chong-shan) Search market 749 (0.48)

Foreclosed

market 423 (0.18)

Old urban area

(Chong-cheng, Wan-hua,

Da-tong) Search market 267 (0.17)

0.313

Foreclosed

market 1035 (0.44)

Suburban area

(Wen-shan, Bei-tou, Shih-lin, Nan-kang and

Nei-hu) Search market 530 (0.34)

36.437***

Panel B: Statistics of “Market Risk” and “Competition” Variable Data of Foreclosed Houses

Variables Markets Average/ Information

Number

Standard Deviation/ Proportion

Auction Times Foreclosed

market

3.06 0.80

Bidding numbers Foreclosed

market

2.77 2.92

Handover or not(Handover) Foreclosed market

1746 74.17%

Vacant house or not (Vacant) Foreclosed market

609 25.87%

Note: ***、**、* separately represent at significant level 1%, 5%, and 10%, “successful foreclosed house

auction sample ” and “search market transaction sample” in Taipei City have significant difference.

Source: Transparent Real Estate Journal and Brokerage Co..

In terms of the difference among t-test and chisquare test in Panel A: although the average price in foreclosed housing is lower than the search market, the floor area and location conditions are worse than those in the search market. According to Rosen’s (1974) hedonic price theory, price and residential quality have replacement, but without controlling residential quality, it is difficult by superficial price difference to judge whether the main reason of price difference between foreclosed houses and search market is from a worse quality of foreclosed houses or not. So this study, in Panel B of Table 2, further focuses on “market competition (such as auction times, and the number of bidders)”, and “the

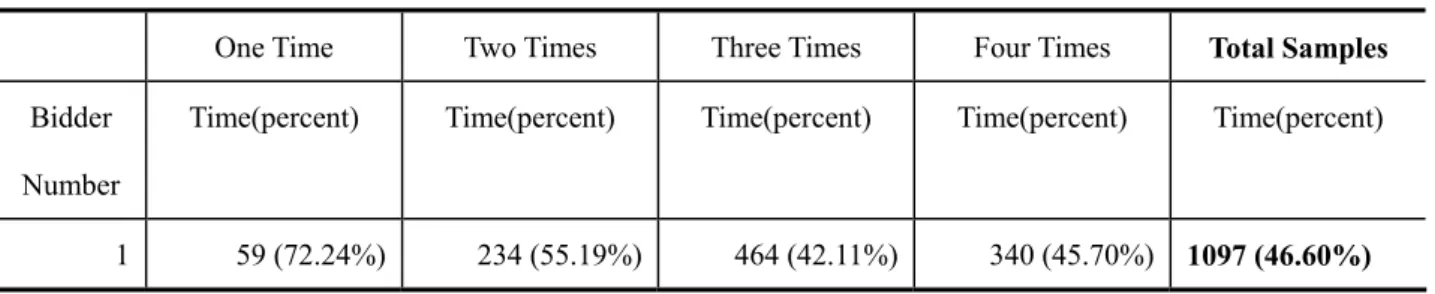

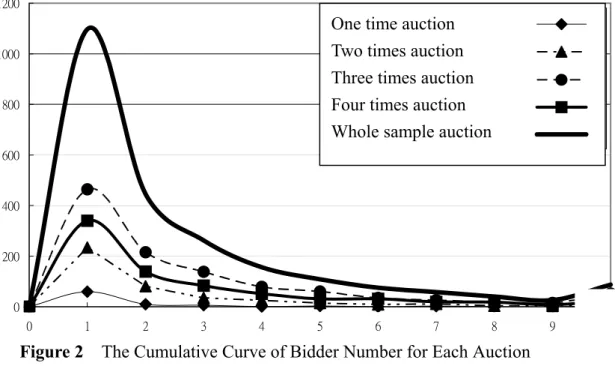

characteristics of intangible risk products (such as handover or not, vacant house or not)”, to analyze other factors that may affect discount phenomenon. Among them, the "market competition" further cross-analysis of the relationship between “auction times” and "the number of bidders" in Table 3. Figure 2 illustrates the cumulative picture of bidder numbers. Its important findings are as follows:

(1) In terms of “auction times”: within all 2,354 samples, 84 auction cases ended with one time auction (3.56%); 424 cases ended with two time auctions (18.01%); 1,102 cases ended with three time auctions (46.81%); and 744 cases ended with four time auctions (31.61%). Here, we can see that more than half of the cases needed to be auctioned for over three times, and in accordance with the appendix, which is about pricing rules of foreclosed houses, the starting price is at 64% (= 100% * 0.8 * 0.8, which means second time and third time are 80% of the prier time price).

(2) In terms of “the number of bidders”: within all 2,354 cases of successful foreclosed housing auctions, total samples in Taipei from 2001 to 2002, one-bidder cases are numbered at 1,097, and the rate is 46.6% (=1097/2354); two-bidder cases number at 445 (the rate is 18.90%); three-bidder cases are numbered at 262 (the rate is 11.13%). So, cases with more than four bidders are at a rate of 23.37%. There are 76.63% of foreclosed house cases that are lower than three bidders.

(3) In terms of the cross-analysis of “auction times” and “competitive bidders”: in the three times of successful auction samples, the rate of only one bidder was as high as 42.11%, of only two bidders 9.51%, and of three bidders 12.52%. The rate of bidders below three was as high as 74.14% during the four times of successful auction samples. The rate of only one bidder is high at 45.70%, of only two bidders 18.68%, and of only three bidders 11.16%. Thus, the rate of below three bidders is as high as 75.54%. We can see from the above that, though the reserve price had a 6.4 discount (three times) and a

5.12 discount (four times), it is much lower than in the search market. In successful auctions, the rate of only one bidders is very high, and the rate of below three bidders is, on average, as high as 70%, so the statistical data once again shows that the bidder is still not enough for each successful auction sample.

(4) In the one-bidder, successful auction case, we found the proportion of advanced price by final bid or reserve price. The proportion of advanced price implies whether the bidding function works or not. By calculation, we find its average is 1.038, so the average premium is 3.8%. Compared with auction by banks its average premium is 7% (Pong and Chang, 2004), foreclosed auctions are relatively low at a premium level.

The above statistical information provides this study with an addition to the traditional intuition "residential entities quality" factor; people should take "market competition", "product’s invisible risk", and so on factors, into account in accordance to the theoretical foundation that causes the foreclosed house discount phenomenon. Furthermore, the reasons why foreclosed houses lack competitive bidding may be related to a lack of information exposure, so fewer people are involved in bidding, and a very high percentage of one-bidder auctions come as a result.

Figure 3 The Relationship between Auction Times and Bidder Numbers from 2001 to 2002

One Time Two Times Three Times Four Times Total Samples

Bidder Number

Time(percent) Time(percent) Time(percent) Time(percent) Time(percent)

2 10 (11.90%) 81 (19.10%) 215 (19.51%) 139 (18.68%) 445 (18.90%) 3 6 (7.14%) 35 (8.25%) 138 (12.52%) 83 (11.16%) 262 (11.13%) 4 1 (1.19%) 25 (5.90%) 79 (7.17%) 51 (6.85%) 156 (6.63%) 5 3 (3.57%) 14 (3.30%) 60 (5.44%) 31 (4.17%) 108 (4.59%) 6 - 9 (2.12%) 35 (3.18%) 31 (4.17%) 75 (3.19%) 7 2 ( 2.38%) 11 (2.59%) 26 (2.36%) 19 (2.55%) 58 (2.46%) 8 - 4 (0.94%) 18 (1.63%) 18 (2.42%) 40 (1.70%) 9 - 3 (0.71%) 15 (1.36%) 8 (1.08%) 26 (1.10%) Above 10 3 (3.57%) 8 (1.89%) 52 (4.72%) 24 (3.23%) 87 (3.70%) Total 84 (3.57%) 424 (18.01%) 1102 (46.81%) 744 (31.61%) 2354 (100%)

Figure 2 The Cumulative Curve of Bidder Number for Each Auction Source: Transparent Real Estate Journal

Some people argue that the study should take normal real estate commodity, and cases both dealing with bargaining and auction, as samples (such as Lusht, 1996; Dotzour, Moorhead and Winkler, 1998; Quan, 2002, etc.). Doing so tries to control same quality of the samples and see if it caused by some of "mechanism" of foreclosed bidding, and of the bargaining (or of different auction systems), that is the main reason behind price difference.

Theoretically, we fully agree with this view, but then in the process of getting samples have the following problems: (1) domestic auctions lack normal real estate cases, Wang (2004) had studied, so far, the "only one self-auction house" case8;(2) foreign documentation suggests that auctions do not necessary

8 This means that new houses sell in such a way (the implementation of non-NPL) that is directly

sold by auction, such as "Taipei Garden" (a completed case), that is near Wanfang Community station of the MRT Muzha line. One of the landowners, Namchow group, commissioned DTZ to sell it by “English public auction” on September 26, 2003.

0 200 400 600 800 1000 1200 0 1 2 3 4 5 6 7 8 9 10以上 競標數 競標數累計 一拍拍定 二拍拍定 三拍拍定 四拍拍定 全樣本 Accumulative bidder number

One time auction Two times auction Three times auction Four times auction Whole sample auction

partake in the discount phenomenon, but the purpose of this study was to explore why the foreclosed housing market has such serious discount phenomena within its confines. In addition to people’s cognition, foreclosed housing has poor quality; however, under “houses’ entity quality control”, if there are still significant discount phenomena, then there should be other important factors affecting the discount, such as, as this study has mentioned, prior statistics about “auction time” and “the number of bidders” that show factors.

IV. The Model and Empirical Results

1. The Model9

The following two important documents affect the establishment of foreclosed house price model: (1) Rosen’s (1974) “hedonic price theory10”, that argues residential prices are composed by a bundle of goods, including internal and external residence. The internal residence goods include floor area, floors, construction type and others. The external goods include location, the neighborhood, and others. (2) Quan’s (2002) "market mechanism" which explains the “price” model11 . This paper will control residential quality by Rosen’s hedonic theory price theory, then taking Quan‘s (2002) concept of "foreclosed house market," and "search market" to represent different "market mechanism difference," and analyzing it’s influence on foreclosed house. The empirical model is equation (1):

μ

δ

β

α

+ + + = X C P i (1)9 thanks for the reminder from reviewer, surely, the model of house’s price more consider

"self-relevant time," fewer people put "relevance on space" into construction mode into consideration, this may due to "the geographic coordinates of the sample space " that is difficult to get. More detailed explanation please refer to the Lee and Lin’s (2007) explanation.

10 Rosen’s (1974) theoretical model is based on the assumption of fully competitive market, but it

is applies in not exactly competitive real estate market. Therefore, this study believes that Rosen’s fully competitive market assumptions should be loosened. Also, the foreclosed housing market is one of real estate markets, which is what this study wants to discuss, so there should not be logic problem by using the hedonic price theory to analyze.

11 In Quan’s (2002) model, the "market choice" is endogenous variables, which uses hedonic price

model: Pi=βXi +δDi + ui , and semi-logarithmic:log (Pi)=βXi +δDi + ui to analyze the price

difference of market choice. Among them, Xi is the real estate characteristics that affects price, Di

is the market choice variables. And the purpose of this study quotes Quan’s (2002) model is by using Di to analyze the price difference of Taiwanese auction and search market.

Among them, P is the real estate price sample after taking the log12. Xi(i=1, 2, 3,…, 7) is according to hedonic price, which determines the seven main characteristics which impact real estate price, including “situated floor, floor square, total floors, floor area, floor area square, land held area, location,” and so on variables13. The analysis of statistics of variables’ basic description is already explained in section 3 of table 2’s Panel A; C is the variable of market mechanism, C = 1 represents foreclosed house market, C = 0 means search market;

μ

is an error term. Also, in order to understand the factor that causes market price difference, the study will extends the variable of market mechanism in equation (1) further to equation (2): μ θ γ δ β α + + + + + = Xi C Mi (C*Mi) P (2)Among them, Mi (i= 1, 2, 3) is the extension of the variable of market mechanism, including "market risk" and "market competition," this study will use “handover or not” and “vacant house or not” to represent market risk, as well as the use of "the number of bidders" to represent the degree of competition. The analysis of statistics of variables’ basic description is already explained in section 3 of table 2’s Panel B. As for the “interaction terms” represents interactive impact of two classified sample and focus variables. Taking “ M (degree of 3

competition)” and “C = 1 means foreclosed house market,” their goods sample as an example. C* M3, the variables’ coefficient means: under the other same variables, if the degree of competition in the foreclosed house market increases

12 Because of the regression model of the “price’s logarithmic”, it can solve the regression model

from merging or separating two samples, thus encountering the "heterogeneous variability" problem. For more details, please refer to Gujarati (2003), Chapter 8,9,13, in particular Chapter 9, which is related to the description of the virtual variables setting, or Greene (2000), Chapter 8, Wooldridge (2000), and other discussions about "virtual variable, restrictive F-test" measurement theory.

13 This study lacks the variable data of “age of house,” coupled with mainly related residential

quality variables that are included, and based on past documents (Lusht, 1996; Frew and Jud, 2003; Lin, 1992; Chang and Liou, 1992; Chang, Lin, and Yang, 1996; Lee, 1999 and others’ studies), all found that the age of house variables are absolutely not the key variables, so this study does not include the "age of house" variable as a model.

one unit (such as the units used in this study is “the number of people”), the price of logarithm will increaseθ units. In the following empirical estimation, the model then broken down for “if taking into interaction terms (divided into 2I and 2II models)” to handle.

Each variable’s setting method and direction of theoretical expectations are as follows, among them, (1) to (5) describe the variablesXiof relevant real estate entities characteristics, (6) is the variable C for the market mechanism, and (7) - (8) are separately the variableMiof market risks and the degree of market competition :

(1) In terms of “situated floor” and “situated floor square”: According to Lin, Yang and Chang (1996) suggest that situated floor’s influence of curve of second degree on residential price. Due to the first floor with the highest price, and price will increases with floor’s height, so fourth floor has the lowest price; but because high floors have good view, so the price will increase with floor’s height as a quadratic term. Therefore, the study applies situated floor’s linear term and quadratic term as variables, which is expected to affect prices as "negative then positive" non-linear relationship.

(2) In terms of “total floors”: According to Lee’s (1999) indicated that, total floors has significant impact on price, and the higher floor the more expensive. Therefore, this study expects to total floors’ impact on residential price should be "positive."

(3) In terms of "floor area" and "floor area square": Lusht(1996); Frew and Jud(2003), and other documents indicate "floor area" is the most important factor that impacts on residential price. Domestic research (Lin, 1992; Chang and Liou, 1992; Lin, 1996; Chang and Tsai, 1997)have similar conclusion. This study, because of diminishing consumer marginal utility, the floor area’s impact on prices is not linear. Therefore, the study applies floor area’s linear term and quadratic term as variables, which is expected to affect prices

as "positive then negative" non-linear relationship.

(4) In terms of "land area": Chang and Tsai(1997) study pointed out that the greater the land area, the higher the price, so land area’s impact on price is expected to be a positive relationship. This study argues that the samples of residential land area held are limited, so its impact on price should not have diminishment in terms of marginal return. Therefore, land area held’s influence on price is part of a "positive", linear relationship.

(5) In terms of “location characteristics”: The study expects a new urban area with convenience is better than the old, so prices should be higher than in older urban areas, while suburban area compared to the old urban area, because of its accessibility and traffic being poorer than that of older urban areas, the prices should be lower than old urban areas. Also, based on one of Lin, Yang and Chang’s (1996) study, the results of the location and extent of the impact on prices is only second in importance to the floor area, this study will be the Taipei District 3: new urban, old urban, and rural settings for the dummy variable. Expectations in terms of setting the direction and approach are as follows: take the old urban areas as a basis, the new urban (D1 = 1) areas compared to the older urban areas. Due to better environment and better convenience than the old urban areas, we expect location’s impact on price to be a "positive" relationship; suburbs (D2 = 1) compared to the older urban areas have poorer environment and convenience, so we expect the location’s impact on prices to be a "negative" relationship.

(6) In terms of "market mechanism": Lusht (1996) first suggested that "market difference" will affect prices, using the OLS model into the variable of auctions and of search market mechanisms doing empirical analysis. Then, Quan (2002) suggests market choice variables. Quan believes that market choice variables are “inwardly born”, thus we have applied a hedonic price model to market choice variables for analyzing different market prices. This study adopted Quan’s (2002) concept. In order to test if price would be

different under different market mechanisms, the paper took different market mechanisms of the foreclosed housing market and search markets as examples. This was done by using virtual variables C, foreclosed house 1, and search market 0 for testing. Along with controlling residential quality, analyzing different market mechanisms’ influence on price, and the market mechanism variables’ impacts on price, a "negative" relationship was expected. Some argued that foreclosed markets and search market mechanisms have varied differences. If only virtual variables are used to represent the auction and search market, there might be a danger of over-simplifying. But, through what was shown in past documents, in Taiwan, there are technical difficulties in getting information, so this study can only apply foreign models, such as Quan’s (2002) model; therefore, model (2) is the one that tests different market mechanisms, its influence of “degree of competition” on prices. As for the "market risk variable", it uses additional variables for Taiwanese foreclosed house’s special market risks. (7) In terms of “market risk”: the study uses “handover or not” and “vacant

house or not” to represent the risk of ownership. The virtual variable of handover is 1, and the virtual variable of not handover is 0. In the auction market, there is handover and is not, but in the search market, only handover is recognized, which means gaining ownership of property; relatively, not being handovered has a lower product risk, so the expectation of being handover or not has “positive” impact on price. The variable of the vacant house is 1, and the variable of non-vacant house is 0. In the auction market, there are vacant and non-vacant houses, but the search market is considered to be vacant. So whether it is vacant house or not, it still has the risk of being occupied and the expectation of being a vacant house or not has a "positive" impact on price.

(8) In terms of "market competition": Quan (1994) and Mayer (1998) suggest that the degree of competition is the main cause that affects the premium discount of the auction market, but they were limited to further empirical

analysis. Thus, this study firstly offers market competition variables, by using "the number of bidders" as a proxy variable, and further testing different degrees of the competition’s impact on market price (Christy and Zaichkowsky, 2003). In auction theory, the higher level of information disclosure, the higher degree of market competition, and the final bidding price will thereby increase with the bid. Therefore, the number of foreclosed house bidders implied its economic significance; while under the same quality real estate circumstances, “a high degree of competition in the market” means through "competitive" mechanism causes over-pricing phenomenon. To the contrary, "a low level of competition in the market" causes a phenomenon in under-pricing14. The higher the amount of bidders, the higher the final price is, and the closer to “same quality” housing when dealing with usual intermediary search methods. As for the question of why the intense or lack of market competition causes over-pricing or under-pricing phenomenon, this study believes that it is related to “ exposure(or being understood) of real estate ‘information’”; the reason affects “the amount of information (quality)”, which may be in the turnover process of usual intermediary search housing and foreclosed housing. At the same time, because "search market" turnover information is restricted by no representative variables, this study can only assume that the search market is more full information and has an unlimited number of participants. But in order to not have an infinite number of participants that ultimately diverge, this study uses the composite number of foreclosed housing bidders as a measure of market competition variables. When there are more competitors in the search market, assuming the competitor number in the market is ∞ , its composite number is 1 /

14 Because the way that Taiwanese foreclosed housing auctions are first price-sealed bids, it is

possible to have many items up for bid put into the same bid during one auction. Bidders are more difficult to detect than the number of potential bidders, so theoretically the number of bidders should not directly affect price. However, this study believes that most of bidders in the Taiwanese foreclosed housing market are investors, who should have higher sensitivity to foreclosed markets; therefore, they know potential bidders from other information channels. By way of the aforementioned, they decide their bidding acts by predicting the number of bidders.

∞, so the search market is set to be 0; the foreclosed house market is the composite number of real competitors as a measure of competition. So, the more competitors, the fuller degree of competition, and the closer the variable is to 0 after becoming composite number. This means that the degree of market competition is close to the search market. This study believes that the search market has more ways to expose information, and a higher degree of market competition than foreclosed housing, which, because of the small number of bidders and lack of competition, the price may be discounted; therefore, when there are more bidders, the foreclosed house’s price and competition will increase as well, even coming close to the same quality of one by bargain. Thus, the price of foreclosed houses should be discounted less compared to the price of the search market, and the expected variables of market competition’s impact on price are "negative" relations.

(9) Other factors: the difference between foreclosed housing and search market, besides the above emphasized “handover or not,” “vacant house or not,” “number of bidders,” and other market mechanism factors, the “repayment method” is different as well. In terms of the current domestic practical operation, the general conditions of the mortgage of foreclosure and of usual mortgage loans from banks are similar, such as a limit on loans and repayment procedures (both can be credited to 70-80%), but foreclosure has a shorter loan time (usually six months or less). Also, the interest rate is slightly higher, so this might be one of the reasons that cause a small number of bidders.In summary, the previous eight variables that are used to explain that the two differences in residential prices reach the criteria of the follow-up model up to 70%; at the same time, these other factors are not the focus of this study, so the effect will be reflected in the estimation of residual terms, or reflected in one of the proxy variables of market mechanism “number of bidders.” Therefore, the follow-up discussion will focus on the

mentioned 6th to 8th variables: "the market mechanism, market risk, and market competition" focal variables.15

2. Empirical Results

Table 4 shows the empirical results of models (1) and (2). Amongst the results, the fit criteria (R ) of model (1) is 0.7306, and model (2) can be divided into 2 two sub-models: one is model (I) with no interaction terms, it R is 0.7262, 2 and the other, model (II), has interaction terms, it R is 0.755. The three 2 models do not explain much, and almost all variables in the models keep with the claimed expected direction of the third section, and having 1% significant effect (in addition to the variable, “handover or not”, and its interaction term aren’t significant; vacancy or not and its interaction term, their variable is only significant at 10% level), indicating that the adopting variables explains well in models.To be more detailed, in the case of a situation where "other variables remain unchanged", each variable’s influence on “direction and coefficient” on real estate is as follows:

(1) In terms of control variables in “quality” category, with other items being under equal circumstances: (a) the linear term and quadratic term’s coefficient of the situated floor (X1) and the situated floor square (X2) in model (1) and (2) are separately negative and positive, which means that the situated floor’s impact on total price is a “negative then positive”, non-linear relationship. (b) The total floors’ (X3) coefficient in model (1) and (2) are both “positive,” which means the higher the total of floors in buildings more impacts pricing. (c) The linear term and quadratic term’s coefficient of floor area (X4) and floor area square (X5) in models (1) and (2) are separately positive and negative, and this once again proved floor area’s impact on

15 The loan application process of general payment in advance for foreclosed houses is as follows:

(1) before bidding, they must first pay a 20 to 30% deposit toward what they can they bid. (2) If the winning bidder wins the auction after the opening bidding, he/she has to pay off 70 to 80% of the remaining balance amount to the court. (3) The winning bidder applies for “the loan of payment in advance for foreclosed houses” from the bank according to the payment notice of the court. The bank will provide an 80% loan of the balance amount due, so foreclosure’s loan percentage from banks is similar to usual houses.

price as being “positive then negative.” When the floor area increases, so does the price, but any increase to a certain floor area means that its impact on total price gradually becomes more negative because of diminishing marginal utility. (d) Held land area’s (X6) coefficient in models (1) and (2) are “positive,” meaning that the larger the held land area, the higher the total price. (e) About location variables: a new urban variable (X7_L1) in models (1) and (2) are both “positive,” representing the new urban area’s functions and environmental quality of life as being better than in old urban areas, so location conditions have a positive impact on total price. To the contrary, the suburbs’ variables (X7_L2) in models (1) and (2) are both “negative,” meaning suburbs, compared to older urban areas, are poorer in location conditions, so the location conditions have a negative impact on total price. (2) In terms of empirical results of “market mechanism variables (C)”: Under

the same "housing quality” circumstances, the model’s (1) coefficient, -0.18871, reaches a “negative effect” at 1% significant level. After calculation of the converting coefficient, we found that a foreclosed house’s average discount rate is higher than the search market by 17.20%16. It proves that the two different “market mechanisms” of pricing certainly are one of the main factors that makes foreclosed housing’s price lower than search market’s price. The same result appears in model (2) (coefficient in interaction terms’ two sub-models are separately -0.18772 and -0.18709, and it reaches “negative effect” at 1% significant level). Therefore, under a different estimate model, foreclosed housing’s average discount rate is more robust than search market’s; it is within about 20%).

(3) In terms of “market risk”: under “housing quality” and “foreclosure or search house of constant sample circumstances:

16 Semi-logarithmic model takes its virtual independent variables, and its percentage calculation

method of the dependent variable Y’s impact is : anti log (β) -1. So the market mechanism variables’ influence rate on price is anti log (-18.78%) -1 = 17.20%.

a. "Handover or not (M1)": though the coefficient, -0.00953, in model (2, I) is “negative”, it does not have a significant impact; coefficient 0.01751 in model (2, II), and its coefficient of interaction term, -0.02578, are no different from 0 at 10% significant level. This study deeply discusses the reasons that may be the result in Taiwan’s foreclosed housing market. Handover or not cannot completely guarantee that the winning bidder gets complete ownership. Although the house has handovered, the bidder might face the original tenants or occupants who demand the bidder pay relocation costs to leave, or the house’s destruction; ownership risks remain in existence. Therefore, whether handover or not, there is no significant effect on price.

b. “Vacancy or not (M2)”: the coefficient, 0.0562, in model (2, I) (which is significant at a 1% level), has a “positive” impact on price. After the calculation of the converting coefficient, we found that the average impact rate is at 5.78%17, meaning the lower the occupation risk, the higher the prices. In addition, the coefficient in model (2, II) is 0.0493 (t = 2.05, the coefficient is significant at 5% level), and its interaction term is 0.06172 (t = 1.70, the coefficient is significant under 10% level), so this study believes that the above may be related to the source restriction of “vacancy” information; setting “intermediary search samples (C = 0)” as “vacant house (M2 = 0)” causes this error. Because it may mix with samples that are both “foreclosure (C = 1)” and “vacant house” (C * M2 = 0), which cannot be differentiated and estimated, its effect does not reach 1% effect.

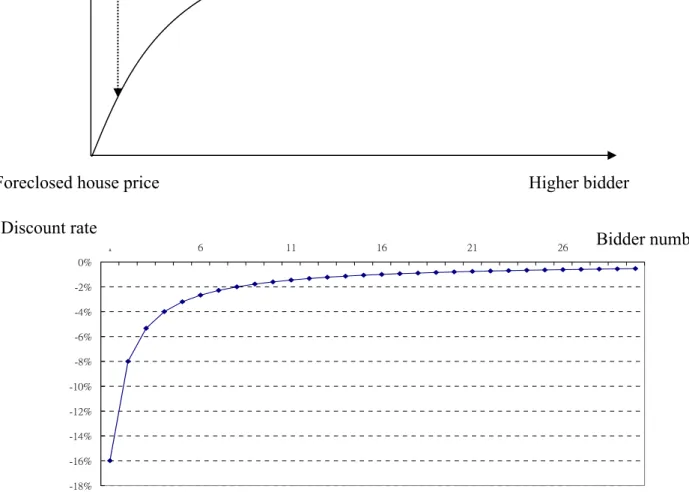

(4) In terms of “market competition (M3)”: under the same “housing quality”, “foreclosure or search house”, and “market risk,” the coefficient in model (2, I) is -0.15991 (which is significant at 1% level); the coefficient in model (2,

II) is -0.16002 (t = -13.56, the coefficient is significant at a 1% remarkable effect); and its coefficient of interaction term is -0.15975 (t = -19.44, the coefficient is significant at 1% level). So, the three coefficients do not differentiate much. We found, after calculation of converting coefficient, that when there is only one bidder, the foreclosed housing price discount was 15.99%18; when there are two bidders, the discount reduces to 7.995%; if

there are five bidders, the discount is only 3.198%. It reveals the lower degree of market competition; the larger seriousness of the discount situation; and the higher the degree of market competition, foreclosed house’s price would increase because of bidding, so a low degree of competition could easily lead to a foreclosed house deviated from real market prices. Figure 3’s first half part is based on Quan (1994) and Mayer’s (1998) “theory” relationship diagram of market price undercutting and the number of bidders; the second half part is in accordance with the empirical results of this study charted “empirical” relationship diagram of price undercutting and the number of bidders. Both of the diagrams match perfectly, which means, with an increasing number of bidders, the market price difference will show a diminishing marginal slope on a nonlinear curve, approximating to market price. The effect in terms of this study’s samples, when there are less than six bidders, along with an increasing number of bidders, the shrinking of the foreclosed discount rate grows, but when it is more than six bidders, the shrinking effect of the foreclosed discount is slightly lowered. So, here it is shown that there is an interesting phenomenon: when there are over twenty bidders, foreclosed houses are at the state of a slight discount, which does not, as foreign documents show, that auction may also be subject to the premium phenomenon. This study has discussed the possible reasons in the introduction section: foreclosure, in quality of invisible product, still reflects the pattern of financing (such as how to pay off all prices in such a short time,

18 Take the average of three coefficients, 15.99%, as an example. This study takes a composite of

bidder numbers as a measure of the degree of competition. When there is one bidder, the variable is 1/1, and their impacts on price is 1 × (-- 15.99%) = 15.99%. When there are two bidders, the variable is 1/2, and their impacts on price is 1/2 × (15.99%) = 7.995%. So, when the number of bidder changes, its impacts on price can be calculated by these methods.

and even shorter loan time), safety transactions (such as handover or not), and other risks, so discount reflects risk premium in these sections.

Overall, the three empirical models show: the coefficient of the “housing quality” variable does not change a lot because of the extension of market mechanism variable, which causes excessive fluctuation. Its coefficient is only differentiated before the third decimal point. According to Quan’s (1994) view, most of a market mechanism’s impacts on pricing in a model (1) can be explained by model’s and (2) extended by variables, such as handover or not, vacant house or not, and the degree of market competition. Furthermore, “the degree of competition variables” is significant in the mode of the two sub-models and a variety of robust testing models; therefore, it explains most of the market mechanism variables’ impacts on price.

3. Robustness Tests

This study had tried to include “auction times” variables for robustness tests. Most people believe that the foreclosed house auction market is bad in assets, and good quality products do not go into the foreclosed market. The worse the quality of the product, the lower the price so, under lemon psychology, people often use “auction times” as a proxy variable of market price difference (such as the third auction being 64% of market price). Another meaning is mentioned previously in the second section: “more auction times” represents the starting bid in first auction as being too high, which may not fit the market price, and cause high auction times and a high rate in the failure of auctions. This study has tried to discuss each auction time’s discount phenomenon as compared to the search markets’. Foreclosed housing is based on actual successful auction times, and the design of the auction times) of the search market is zero, but the empirical results of variable design are not significantly well. Therefore, whether an auction times can accurately express market price difference or not still needs to be studied further.

-18% -16% -14% -12% -10% -8% -6% -4% -2% 0% 1 6 11 16 21 26 競標人數 折價幅度

Figure 3 Relationship between Market Price Undercutting and Number of Bidders

Note: (1) The first half is based on Quan (1994) and Mayer’s (1998) “theory” relationship diagram of market price undercutting and the number of bidders; (2) The second half is in accordance with the empirical results of this study, charted as “empirical” relationship diagram of price undercutting and the number of bidders.

法拍屋價格

Search Market Price (market equilibrium price)

競標人數愈多

Foreclosed house price Higher bidder

Large discount Smaller discount Discount rate Bidder number

Table 4 Empirical Results of Different Market Prices

Variables Expected sign Model (1) Model (2): I Model (2): II

Intersection 4.9541 (174.91)*** 4.9094 (155.58)*** 5.2697 (117.52)*** Situated floor (X1) - -0.05359 (-11.69)*** -0.05372 (-11.62)*** -0.1020 (-7.74)*** Situated floor square (X2) +

0.00266 (8.57)*** 0.00269 (8.61)*** 0.003218 (9.36)*** Total floors (X3) + 0.02606 (14.29)*** 0.02462 (13.43)*** 0.01929 (12.14)*** Floor area (X4) + 0.05167 (57.09)*** 0.05157 (56.16)*** 0.04972 (35.72)*** Floor area squared (X5) -

-0.00029 (-31.79)*** -0.00029 (-31.11)*** -0.00105 (-38.39)*** Held land area (X6) +

0.00932 (7.89)*** 0.00949 (7.97)*** 0.02057 (11.26)*** New urban area (X7_ L1)

(new urban area sample =1) + 0.1759 (12.57)*** 0.17361 (12.27)*** 0.1529 (9.85)*** Suburban area (X7_ L2)

(suburban area sample=1) -

-0.07201 (-4.99)*** -0.08704 (-5.98)*** -0.1068 (-3.75)*** Market mechanism variable (C) (C=1, foreclosed house sample) - -0.18871 (-18.08)*** -0.18772 (-19.49)*** -0.18709 (-15.41)*** Handover or not (M1) (M1=1, handover sample) + - -0.00953 (-0.66) 0.01751 (1.28) Vacant house or not (M2)

(M2=1, vacant house sample) + - 0.0562 (4.17)*** 0.0493 (2.05)** Market competition (M3) (measure: number of people) - - -0.15991 (-11.24)*** -0.16002 (-13.56)*** Interaction term C* M1 + - - -0.02578 (-0.95) Interaction termC* M2 + - - 0.06172

(1.70)* Interaction term C* M3 - - - -0.15975 (-19.44)*** Adj-R2 0.7306 0.7262 0.7550 Collinoint 6.63215 6.72642 5.9028 F-term 29.3126 35.8728 37.9910 Number of oberservation 3900 3900 3900

Note: 1. ***、**、* separately represents at 1%, 5%, and 10% significant level.

2. ( ) is t value. 3. Collinoint < 10 means variables have no serious multicollinearity phenomenon.

V. The Conclusion and Policy Implication

Using the data of the 2,354 cases for court-foreclosed houses and 1,546 cases for the brokerage houses in Taipei from 2001-2002, we hypothesize two key factors to answer “Does the factor of competition explain more price discount?”: (1) the housing physical quality (which is the control variable in this paper); (2) the market mechanism: this construct can be separated into two dimensions further. One is the risk premium for the court-foreclosed houses (where risk is proxy “handover or not” and “vacant or not”). The brokerage houses are dealt by the broker searching, and usually have less risk involved because of features of “vacancy and handover”. Another is the competition (which is proxy the number of bidding). We argue the united-price will be driven by the increasing of full-competition in the foreclosed cases, even if the physical quality is controlled at the same features.

Through statistical analysis and the econometric modeling of logistic regression, three main empirical results are found: (1) The average price for the foreclosed houses in the biding market is lower 17.20% than that for the brokerage houses in the searching and bargaining market, controlling other things being equal. We propose the market mechanism such as the foreclosed-housing risk of the buyer exposure, and the participant number of biding can explains more for the deep-discount price. (2) The price discount is 15.99% if one bidder

involves. Moreover, the more participant number of biding is, the lower price discount between auction market and search market is. This implies that full information disclosure can increase the competition and reduce the price discount of foreclosed houses in the court-oriented auction market. In other words, along with the increasing to the bidding number, the rate of market differential prices would be reduced to a marginal slope in the curved pattern of nonlinear approximation, then close to price of search market.

Comparing with the empirical results of previous literature, we argue the “discount” phenomenon is not a necessity generated by the foreclosed “bidding auction” system. For example of foreign real estate auction markets, the higher prices by auction also can be achieved, owing to higher competition, more transplant and sufficient information disclosure, lower transaction costs, et al. Our empirical results have some implication to the improvement of foreclosed house auction system in Taiwan: as far as the policy-markers are concerned, the authority can create a full information disclosure system, reducing transaction risk, and enhancing the market competition. The data indicates that a deal by auction actually required the three auction times. The inefficiency of auctions shows the policy markers who must pay more attention about the decision of reserve price.

As far as the investors of court-foreclosed houses are concerned, their investment patterns are in the pursuit of “high-risk, high-reward”. They believe the return of foreclosed housing market is higher, however they always ignore the uncertain risk of foreclosed housing market will cause the significant loss19. Furthermore, our findings suggest that, under housing quality control, the

19 The risk of foreclosed houses is not only in property rights, but also in the fact that houses may

be be occupied by the former owner or any other person, who may also demand removal cost and other additional costs even though it is a “handover house”. Therefore, their expectation reward/risk = loss probability * loss price. For example, after winning a handover residence, its market price is 500 million, and its winning bid is 400 million dollars. On the surface, it seems to be discounted by 20%, and have earned 100 million; however, the case may require additional costs to be paid, such as removal costs because of being occupied, taxes, and housing costs that the former owner owed, or the winning bidder has to face the house being vandalized. So, the payment of ownership and of complete housing conditions may be more than its earning. If the winning bidder is unable to obtain ownership, or the house is destroyed, then that is all part of its losses. In addition, the spiritual and time wasting problems of dealing with foreclosed houses are incalculable.

differential price of foreclosure and search market is 17.20%, less than 20%. Although, the price of foreclosed house is cheaper than the price of search market, however, the discount is below 30%20, which is not as general expected.

20 According to the information, it is shown that, from the successful foreclosed housing auction

information in Taipei, from 2001 to 2002, the ratio of winning bids and reserve price is 69.7%, and its discount is about 30%.

References

Akerlof, G., A., (1970), “The Market for Lemons: Quality Uncertainty and the Market Mechanism”. The Quarterly Journal of Economics, 84(3), 488-500. Allan, M. (2001), “Discount in Real Estate Auction:Evidence from South

Florida”. The Appraisal Journal, vol. 69, 28-43.

Chang, Chin-Oh & Liou, Xiou-Ling 1992. “Discussion of Real Estate Quality, Prices, and Consumer Price Index” (房地產品質、價格與消費者物價指數之 探 討 in Chinese). National Chengchi University Journal, Vol. 67, pp 369-400。

Chang, Chin-Oh & Tsai, Fin-Lian, 1997. “A Study on Foreclosed Housing Price Influence – Taking Taipei City as an Example” (法拍屋價格影響因素之研究-以台北市為例in Chinese). Proceedings of the Six Annual Conference at the

Chinese Housing Studies Association.

Chiu, Kuo-Hsun, & Chang, Chin-Oh 2003. “Disposition of the Non-Performing Loans in Taiwan” (我國不良債權處理方式之研究 in Chinese). Management

Review. 22(1), pp 75-97.

Christy, L., J., & Zaichkowsky, J.L. (2003), “Bidding Behavior at the Auction”.

Psychology and Marketing, 20(4), 303-322.

Dotzour, G.., M., Moorhead, E. & Winkler, D., T. (1998), “The Impact of Auction on Residential Sales Pricing in New Zealand”. Journal of Real Estate

Research, 16(1), 57-70.

Frew, J., & Jud, G. D. (2003), “Estimating the Value of Apartment Buildings”.