R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

37

Environmental Subsidy and Audit Policies with Self-Reporting

RUEY- JI GUO*

Department of Accounting, Soochow University, Taiwan

ABSTRACT

Both the subsidy on the investment in abatement of pollution and the tax imposed on the pollution level, subject to possible audit, can be considered two important incentives contributing toward alleviating the costly externalities to pollution generated by optimizing economic firms. Also, under existing environmental regulations, firms are often required to self-report their compliance status to reduce necessary supervising and legal enforcement costs. Assuming the related tax rates of pollution are exogenous, this paper examines the interplay between environmental subsidy and audit policies, specifically under a self-reporting regime, to shed light on some policy implications. One of the major results indicates that, as environmental audit is difficult and costly, the subsidy on the investment in abatement of pollution will be relatively more effective and justifiable. Nevertheless, under a self-reporting regime, there is not such an obvious policy substitutability between subsidy and audit measures as that in Guo and Wang (2004), which has no self-reporting regime.

Key words: subsidy policy; audit policy; self-reporting.

1. INTRODUCTION

In practice, firms are often required to self-report their environmental compliance status to reduce necessary supervising and legal enforcement costs. As Kaplow and Shavell (1994) argue, enforcement schemes with self-reporting offer society two advantages, including saving enforcement resources as well as eliminating risk-bearing costs (a benefit when actors are risk-adverse). Innes (1999) also notes that remediation or clean-up benefits impart two advantages to the employment of self-reporting beyond those identified elsewhere, i.e. self-reporting firms always engage in efficient remediation and the government can costlessly impose stiffer non-reporter penalties, thus reducing the government enforcement effort required to achieve a given level of violation deterrence. Hence, if the self-reporting cost is insignificant, it seems desirable for the regulator to take a self-reporting regime into account as it determines adequate environmental policies.

To induce polluting firms to make necessary investments in environmental protection, investment subsidies can be used as a prominent policy measure to alleviate political economy costs resulting from environmental tax (Arguedas &

van Soest 2009). In the prior literature, while Kneese and Bower (1968), Mills (1972), Harberger (1980), Slitor (1976), Baumol and Oates (1979), and Fisher (1983) present some negative opinions on investment tax credit or subsidy from government, there are still a couple of positive viewpoints for subsidy policy. For instance, Laplante (1990) finds, in the Cournot oligopoly market model, if

*Corresponding author. Email:[email protected]

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

38

government offers some kind of subsidy (e.g. investment tax credit) on de-pollution equipment, it will avoid the collusion between a firm and its competitor, and the firm will undertake the investment in de-pollution equipment and make its output fulfill the optimal demands of society. Kort, van Loon, and Luptacik (1991) point out, while an increase in subsidy rate on investment in de-pollution equipment raises governmental expenditures, more investment in that equipment will foster lower pollution levels and higher economic growth. Thus, it will contribute to future tax revenues and employment opportunities. In particular, subsidy policy has a much more prominent effect on the investment in considerably expensive capital goods. Rajah and Smith (1993) also argue that even if the subsidy on investment in pollution abatement may augment the public sector’s expenditures and become a hidden protection, it remains one of the important policy measures that could be coupled with environmental taxes. However, as Isik (2004) notes, the uncertainty on subsidy policies could have some potential impact on the investment decision.

In recent literature, Arguedas and van Soest (2009) show that policies consisting of a menu of emission taxes and investment subsidies can potentially induce firms to self-select as well as aid governments to distinguish between firms that need to receive a subsidy to adopt a new technology and firms that would adopt that technology even without subsidies. Using agent-based simulations, Cantono and Silverberg (2009) explore when a limited subsidy policy can trigger diffusion that would otherwise not happen, and they find that the introduction of a subsidy policy seems to be highly effective for a given high initial price level only for learning economies in a certain range. Toshimitsu (2010) argues that, paradoxically, a subsidy policy degrades the environment, and that an optimal policy depends on the degree of marginal social valuation of environmental damage.

That is, if the marginal social valuation of environmental damage is larger than a certain value, a consumer-based environmental subsidy policy is not socially optimal. Furthermore, McGilligan, Sunikka-Blank and Natarajan (2010) examine the impact that subsidy can make in bolstering the performance of an Energy Performance Certificate by reducing carbon emissions in the residential sector.

They perform a cost–benefit analysis using the concept of the Shadow Price of Carbon and present a model which allows the carbon savings for any level of subsidy to be calculated. Their model suggests that subsidization of the installation of hot water tank insulation, draught proofing measures, loft insulation and cavity wall insulation may be cost-effective, but that the subsidization of others, most notably interior solid wall insulation, are unlikely to significantly bolster carbon savings.

Provided that a firm has made the necessary investment in abatement of pollution, under a self-reporting regime, there remains some incentive for it not to honestly declare the realized pollution state and pay the required pollution tax.

Hence, the audit of pollution state is regarded as an important measure to induce a polluting firm to present an honest report. In the past literature, there has been a lot of research on audit systems, such as Antle (1982 & 1984), Baron and Besanko (1984), Demski and Sappington (1987), Penno (1990), Baiman, Evans and Nagarajan (1991), Kofman and Lawarree (1993 & 1996), etc. Meanwhile, there are also considerable discussions specifically related to environmental audit measure, including Doyle (1992), Morelli (1994), Campbell and Byington (1995), Franckx

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

39 (2002), as well as Friesen (2006).

Despite lots of papers concerned with either subsidy or audit policies, little attention has been concentrated on simultaneously dealing with subsidy, audit, and self-reporting in environmental policies. Following the model of Guo and Wang (2004), this paper examines the interplays among these regulatory measures in order to shed light on some policy implications and finds that, under a self-reporting regime, there seems no obvious policy substitutability between subsidy and audit measures. This is a little different from the result of Guo and Wang, which has no self-reporting regime. In next section, we characterize the basic model used in this article. The related analyses and results are presented in section III. Finally, section IV summarizes the prominent results of this research as well as possible policy implications.

2. THE MODEL

It is assumed in this paper that the regulator can manipulate two policy measures, i.e. subsidy and audit, to induce a polluting firm to make a higher investment in abatement of pollution. Meanwhile, the firm’s self-reporting regime will be employed under the assumption of no reporting cost. The overall decision process can be regarded as a one-period game played by a firm and a regulator, both of whom are assumed to be risk neutral. Moreover, it is assumed the firm is required to make at least a low investment (Il) in abatement of pollution without subsidy from the regulator since the related business is a pollution-producing one.

At the beginning of the period concerned, the regulator decides and announces a subsidy rate β (and β ∈

[ ]

0,1) for the portion of increased investment (ΔΙ ≡ Ιh − Ιl) if the firm makes a high investment (Ιh) rather than a low investment (Ιl) in abatement of pollution; i.e., the amount of subsidy is βΔΙ. The firm will then choose to make either a high or a low investment in abatement of pollution according to the regulator’s subsidy policy and subsequent possible audit policy.Furthermore, it is assumed that the firm is required to declare its investment level to the regulator in order to either conform to the lowest investment regulation or apply for an investment subsidy. Thus, the investment level is common information.

Similar to the setting of Malik (1993), the pollution generated by the regulated firm is denoted by a binary random variable Ρ and it is the firm’s private information.

Under low investment, with probability θ, a high pollution state (Η) occurs and Ρ takes on high value of Ρh; and with probability 1−θ, a low pollution state (L) occurs and Ρ takes on low value of Ρl, where Ρl < Ρh. That is, under low investment, Ρr (Ρ = Ρh) = θ and Ρr (Ρ = Ρl) = 1−θ. In this paper, we assume the firm’s investment level (or control effort) has an influence on the pollution level of Ρ, rather than on probability of θ.1 Hence, under high investment, with the same probability of θ, state H will result in a pollution level dΡh, and with probability 1−θ, state L will

1 θ can be regarded as the probability of a good economy or high output, and 1− θ corresponds to a bad economy or low output.

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

40

contribute to a pollution level dΡl, where 0 < d < 1. In other words, it is assumed that Ρr (Ρ = dΡh) = θ and Ρr (Ρ = dΡl)= 1−θ under high investment. Whatever pollution level happens, it is assumed that social damage cost (external cost) per unit of pollution level is s. Furthermore, Ρh, Ρl, and d are all common information.

Under a self-reporting regime, the polluting firm is required to declare the realized state of pollution. Having made a high (low) investment in the abatement of pollution, the firm can choose reporting a pollution level, dΡh or dΡl (Ρh or Ρl), to the regulator, and then pay a certain amount of pollution tax. In this paper, ϒh and ϒl are the firm’s decision variables used for reporting decisions, where 0 ≤ ϒh ≤ 1 and 0 ≤ ϒl ≤ 1. Meanwhile, ϒh = 1 (ϒl= 1) means the firm makes a high (low) investment and honestly declares a high pollution state given state H occurs, but ϒh

= 0 (ϒl = 0) implies declaring a low pollution state. Obviously, there is no incentive for a firm to declare a high pollution state if the pollution state is low. Under high (low) investment, the pollution tax will be tdΡh (tΡh) if state H is realized and the firm honestly reports it to the regulator (i.e. ϒh = 1 (ϒl = 1)), and the pollution tax will be tdΡl (tΡl) if state L is realized and the firm declares a state of low pollution.

However, provided the firm presents a report of low pollution after state H occurs (i.e. ϒh = 0 or ϒl = 0) and is found to be under-declaring by the auditor, the pollution tax will be adjusted up to t′dΡh or t′Ρh depending upon whether the firm has made a high or low investment in abatement of pollution. The punitive tax rate, t′, is assumed to be larger than the normal tax rate, t, and t is assumed to be less than s. Meanwhile, in consideration of the complexity of the factors influencing tax rates, this paper doesn’t intend to deal directly with the issue on optimal pollution tax policy. Both t and t′ are assumed to be exogenously determined. Nevertheless, via the use of audit policy, the regulator still can determine an optimal value of

“expected pollution tax revenues” given the pollution tax rates. Sandmo (2002) and Backlund (2003) have some discussions on the related issues.

Since there is an economic incentive for the firm to under-declare the pollution state (when state Η occurs) and to avoid higher pollution tax, the regulator can consider taking an audit action to verify the firm’s report (when the latter declares a low pollution state). In the model, the regulator will choose an audit probability (αh or αl) depending upon the investment level (Ih or Il) to verify the firm’s report of a low pollution state. In the latter analyses, Α denotes the cost of a complete audit, and q represents the audit quality, which is the probability that the audit result correctly shows the state is H given state H occurs. In contrast, 1−q is the probability that the audit result shows the state is L given the realized pollution state is H. For simplification, it is assumed the probability that the audit result shows the state is L given state L occurs is one.

The timing of the related events in the model is summarized as follows:

(1) At the beginning of the period concerned, the regulator announces a subsidy policy of investment in abatement of pollution. The subsidy rate for the portion of increased investment (ΔΙ ≡ Ιh−Ιl) is β, where β ∈[0 ,1].

(2) The firm will then choose to make a high or low investment (Ih or Il) in abatement of pollution in consideration of the regulator’s subsidy policy and subsequent audit policy.

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

41

(3) Nature determines whether the state of pollution is “high” (with probability of θ) or “low” (with probability of 1 − θ).

(4) Depending on the actual investment level and the realized state of nature, the firm decides to declare a high (Η) or low (L) pollution state to the regulator in consideration of the regulator’s audit policy and will pay the pollution tax calculated by a normal tax rate, t, if the report is not found incorrect.

(5) According to the actual investment level (Ih or Il), which is common information, the regulator will decide an audit probability (αh or αl) of sending an independent auditor (at a cost of Α) to verify the firm’s report of low pollution state.

(6) Given a realized state of high pollution and a report of low pollution state presented by the firm, there is a probability of q that the audit action will reveal a high pollution state if audit action has been undertaken. When the firm is found to be under-declaring the pollution state, the pollution tax will be calculated by a higher (punitive) tax rate, t′, instead of t.

(7) Transfers are realized.

A representation of the game model is shown in Figure 1, with the definitions of related variables being shown in Table 1.

Figure 1. Game tree *.

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

42

*R: regulator.

F: firm.

N: nature.

b: subsidy.

a: audit.

na: no audit.

Η: nature determines a high pollution state.

L: nature determines a low pollution state.

H ′: the firm declares a high pollution state.

L′: the firm declares a low pollution state.

E(CR)i : net expected external costs (considered by regulator) in track i.

E(CF)i : net expected environment costs (related to firm) in track i, and the others follow the same definitions as aforementioned.

Table 1. Definitions of variables

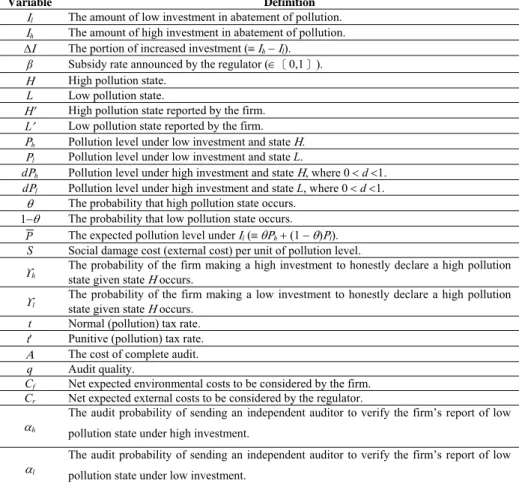

Variable Definition Ιl The amount of low investment in abatement of pollution.

Ιh The amount of high investment in abatement of pollution.

ΔΙ The portion of increased investment (≡ Ιh − Ιl).

β Subsidy rate announced by the regulator (∈[0,1]).

Η High pollution state.

L Low pollution state.

Η′ High pollution state reported by the firm.

L′ Low pollution state reported by the firm.

Ρh Pollution level under low investment and state Η. Ρl Pollution level under low investment and state L.

dΡh Pollution level under high investment and state Η, where 0 < d <1.

dΡl Pollution level under high investment and state L, where 0 < d <1.

θ The probability that high pollution state occurs.

1−θ The probability that low pollution state occurs.

P The expected pollution level under Ιl (≡ θΡh + (1 − θ)Ρl).

S Social damage cost (external cost) per unit of pollution level.

ϒh The probability of the firm making a high investment to honestly declare a high pollution state given state Η occurs.

ϒl The probability of the firm making a low investment to honestly declare a high pollution state given state Η occurs.

t Normal (pollution) tax rate.

t′ Punitive (pollution) tax rate.

Α The cost of complete audit.

q Audit quality.

Cf Net expected environmental costs to be considered by the firm.

Cr Net expected external costs to be considered by the regulator.

αh

The audit probability of sending an independent auditor to verify the firm’s report of low pollution state under high investment.

αl

The audit probability of sending an independent auditor to verify the firm’s report of low pollution state under low investment.

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

43 Table 1. Definitions of variables (continued)

Variable Definition Variable Definition Α1 ≡

( )

1θ−θ qd(t′Ρh−tΡl)1 ΔΙ4 ≡t(

P−dPl)

Α2 ≡

( )

1θ−θ q(t′Ρh−tΡl) ΔΙ5 ≡(1−θ)α1A+(1−d)sPα1 ( )

) (tPh tPl q

Pl Ph t

′ −

≡ − β1

I P t d Δ

− −

≡1 (1 )

ΔΙ1 ≡(1−d )tP β2

( )

I dPl P t

Δ

− −

≡1

ΔΙ2 ≡t

(

P−dPl)

β3ItPl d Δ

− −

≡1 (1 ) ΔΙ3 ≡(1−d )tPl

3 RESULTS

Following Guo and Wang (2004), the firm’s objective is to minimize the net expected environmental costs (Cf).2 In contrast, the regulator intends to minimize the net expected external costs derived from pollution (Cr).3 Basically, the overall analyses in this section can be classified into two parts. The first one is to address various possible strategy interplays between the regulator’s audit policy and the firm’s reporting decision, and the second one is to deal with those between the regulator’s subsidy policy and the firm’s investment decision subject to the results of analyses in part one. With respect to the analyses of part one, the related results under high and low investment will be summarized in Lemmas 1 and 2, respectively.

Lemma 1.

Given q ≥ ( )

) (tPh tPl

Pl Ph t

′ −

− , if Α ≤

( )

1−θθ qd(t′Ρh − tΡl) ≡ Α1, then αh*= qt((tP′Phh−−PtPl)l)and ϒh*= 1; otherwise, αh*= 0 and ϒh*= 0.

Proof. See Appendix.

It is shown in Lemma 1 that, under high investment and in response to the regulator’s audit policy, the firm’s optimal reporting strategy is one of either honestly declaring high pollution state or dishonestly declaring a low pollution state, given the realized pollution state is high. Responding to the firm’s possible strategies, the regulator’s optimal audit policy will be dependent on audit cost. If audit cost (Α) is not larger than Α1, the regulator will adopt a mixed strategy of

2 Net expected environmental costs= investment in abatement of pollution - investment subsidy revenue + expected pollution tax.

3 Net expected external costs= expected social damage cost - expected pollution tax revenue + investment subsidy expenditure + expected audit cost.

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

44

random audit to induce the firm to honestly declare the pollution state. On the contrary, if audit cost is larger than Α1, the regulator won't undertake any audit action. Specifically, Α1 is contingent on the probability of high pollution, audit quality, normal tax rate, punitive tax rate, and high/low pollution level under high environmental investment. Furthermore, if the firm has made a low investment in abatement of pollution, we also can obtain a similar strategy profile. The related results are summarized in Lemma 2.

Lemma 2.

Given q ≥ ( )

) (tPh tPl

Pl Ph t

′ −

− , if Α ≤

( )

1−θθ q(t′Ρh − tΡl) ≡ Α2, then αl*= qt((tP′Phh−−PtPl)l) andϒl*= 1; otherwise, αl*= 0 and ϒl*= 0.

Proof. See Appendix.

In Lemma 2, it can be found the firm’s optimal reporting strategy remains to be a strategy of either honest declaration or dishonest declaration, given that the realized pollution state is high. Moreover, the regulator’s optimal audit policy will still depend on the condition of audit cost. The regulator won’t use a random audit policy unless the audit cost is less than or equal to Α2 ,which is larger than Α1. Meanwhile, Α2 is contingent on the probability of high pollution, audit quality, normal tax rate, punitive tax rate, and high/low pollution level under low environmental investment. While the threshold for using a random audit under low investment is different from that under high investment, the probabilities of random audit under both low and high investments are indifferent, i.e. αl*= αh* =

( )

) (tPh tPl q

Pl Ph t

−

′

− ≡ α1. To simplify the denotation in the following analyses, Α1 and Α2 are used to represent the expressions

( )

1θ−θ qd(t′Ρh − tΡl) and( )

1−θθ q(t′Ρh − tΡl),respectively. Also, since q < ( )

) (tPh tPl

Pl Ph t

′ −

− will result in ϒh* = ϒl* = 0 (no matter how much the audit cost is) and make a self-reporting regime useless, q ≥ ( )

) (tPh tPl

Pl Ph t

′ −

− is

an implied assumption in this paper.

After understanding possible interplays between the firm’s reporting decision and the regulator’s audit policy, we get a step further to considering the possible strategic interplays between the firm’s investment decision and the regulator’s subsidy policy. In the following Lemmas 3, 4, and 5, according to the condition of audit cost, the regulator’s optimal subsidy policy will be presented at the right moment to induce a high investment in abatement of pollution.

Lemma 3.

Under Α ≤ Α1, if ΔΙ ≤ ΔΙ1, then β = 0 is enough to induce Ι = Ιh; but if ΔΙ > ΔΙ1, then β ≥ β1 is necessary to induce Ι = Ιh. Meanwhile, ΔΙ ≡ Ιh − Ιl, Ι1 ≡ (1-d)tP, P

≡ θPh + (1 − θ)Ρl, and β1 ≡ 1 −

I P t d Δ 1− )

( .

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

45 Proof. See Appendix.

As the audit cost is relatively low, i.e. Α ≤ Α1, Lemma 3 shows that if the increased investment (ΔΙ) doesn’t exceed the savings in expected pollution tax (ΔΙ1), the firm will choose to make a high investment in abatement of pollution even in the absence of subsidy. However, if the increased investment is larger than the savings in expected pollution tax, the firm will tend to make a low investment in abatement of pollution unless the potential loss can be compensated by the investment subsidy.

From the results of Lemmas 1, 2, and 3, we can derive the possible strategy equilibrium in Proposition 1.

Proposition 1.

Under Α ≤ Α1,

(1) if ΔΙ ≤ (1-d)tP , then β* = 0, Ι* = Ιh, αh = α1, and ϒh* = 1;

(2) if (1−d)tP<ΔI<(1−d)sP, then β* =β1, Ι* = Ιh, αh* = α1, ϒh* = 1;

(3) if ΔI ≥(1−d)sP, then β* = 0, Ι* = Ιl, αl* = α1, and ϒl* = 1;

where ΔΙ ≡ Ι − Ιl, P≡ θΡh + (1 − θ)Ρl, α1 ≡ ( )

) (tPh tPl q

Pl Ph t

′ −

− , and β1 ≡ 1 −

I P t d Δ 1− )

( .

Proof. See Appendix.

From the results of Proposition 1, as audit cost is relatively insignificant, the regulator will offer the firm an investment subsidy only when the increased investment is larger than the latter’s savings in expected pollution tax, but less than the savings in expected social damage from pollution. Otherwise, the investment subsidy will become either unnecessary (if ΔI ≤(1−d)tP), or uneconomical (if

P s d I ≥(1− )

Δ ). Since audit cost is relatively lower, the regulator will undertake a random audit if the firm declares a low pollution state no matter whether the firm has made a high investment or not. Responding to the regulator’s audit policy, the firm will choose to honestly declare its pollution state irrespective of making a high or low investment.

Next, in Lemma 4, provided the audit cost is relatively moderate (i.e. Α1 < Α

≤ Α2), we can acquire a result similar to Lemma 3.

Lemma 4.

Under Α1 < Α ≤ Α2, if ΔΙ ≤ ΔΙ2, then β = 0 is enough to induce Ι = Ιh; but if ΔΙ

> ΔΙ2, then β ≥ β2 is necessary to induce Ι = Ιh. Meanwhile, ΔΙ ≡ Ιh − Ιl, ΔΙ2 ≡ t

(

P−dPl)

, P ≡ θΡh + (1 − θ)Ρl, and β2 ≡( )

I dPl P t

Δ

− −

1 .

Proof. See Appendix.

As shown in Lemma 4, if the increased investment (ΔΙ) is not more than the savings in expected pollution tax (ΔΙ2) , the firm will be inclined to make a high investment in abatement of pollution even without subsidy; but if the increased investment exceeds the savings in expected pollution tax, the firm will choose to make a low investment in abatement of pollution unless the potential loss can be

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

46

compensated by the investment subsidy. Nevertheless, the threshold of subsidy in Lemma 4 is higher than that in Lemma 3 since ΔΙ2 > ΔΙ1, but the rate of subsidy in the former is lower than that in the latter since β2 <β1.

From the results of Lemmas 1, 2, and 4, we can obtain another possible strategy equilibrium, specifically under Α1 < Α ≤ Α2, in Proposition 2.

Proposition 2.

Under Α1 < Α ≤ Α2,

(1) if ΔΙ ≤t

(

P−dPl)

, then β* = 0, Ι* = Ιh, αh* = 0, and ϒh* = 0;(2) if t

(

P−dPl)

< ΔΙ < (1 − θ)α1Α +(1−d )sP, then β* = β2, Ι* = Ιh, αh* = 0, and ϒh* = 0;(3) if ΔΙ ≥ (1 − θ)α1Α +(1−d )sP, then β* = 0, Ι* = Ιl, αl* = α1, and ϒl* = 1; where ΔΙ

≡ Ιh − Ιl, P≡ θΡh + (1 − θ) Ρl, α1 ≡ ( )

) (tPh tPl q

Pl Ph t

−

′

− , and β2 ≡ 1 −

( )

I dPl P t

Δ

− .

Proof. See Appendix.

In Proposition 2, as audit cost is relatively moderate (i.e. Α1 < Α ≤ Α2), the regulator will tend to offer the investment subsidy only when the increased investment is larger than the firm’s savings in expected pollution tax, but less than the regulator’s savings in both expected audit cost and expected social damage from pollution. Otherwise, the investment subsidy will become either unnecessary (if ΔΙ ≤ t

(

P−dPl)

) or uneconomical (if ΔΙ ≥ (1 − θ)α1Α + (1−d )sP). Under the subsidy policy, the firm will make a high investment in abatement of pollution provided the increased investment is less than the sum of the regulator’s savings in expected audit cost and the savings in expected social damage from pollution.Since audit cost is moderate, the regulator will take a random audit only when the firm has made a low investment. Responding to the regulator’s possible audit policy, the firm will choose to honestly declare a high pollution state, given that a high pollution state is realized only if the latter has made a low investment. In other words, having made a high investment, the firm will under-declare the pollution state given a realized state of high pollution.

Finally, as audit cost becomes considerably significant (i.e. Α > Α2), the regulator’s optimal subsidy policy to induce the firm to make a high investment in abatement of pollution is presented in Lemma 5.

Lemma 5.

Under Α > Α2, if ΔΙ ≤ ΔΙ3, then β = 0 is enough to induce Ι = Ιh; but if ΔΙ > ΔΙ3, then β ≥ β3 is necessary to induce Ι = Ιh. Meanwhile, ΔΙ ≡ Ιh − Ιl, ΔΙ3 ≡ (1 − d)tΡl, and β3 ≡ 1 −

I tPl d Δ

− ) 1

( .

Proof. See Appendix.

Comparing the result of Lemma 5 with those of Lemmas 3 and 4, it can be found that the threshold of subsidy in Lemma 5 is lower than those in Lemmas 3 and 4, but the rate of subsidy in Lemma 5 is higher than those in Lemmas 3 and 4.

In fact, since ΔΙ2 > ΔΙ1 > ΔΙ3, and β2 < β1 < β3, ceteris paribus, there exist the highest

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

47

threshold of subsidy and the lowest rate of subsidy as Α1 < Α ≤ Α2, but it can lead to the lowest threshold of subsidy and the highest rate of subsidy as Α > Α2.4

Hence, from the results of Lemmas 1, 2 and 5, we can derive the possible strategy equilibrium under Α > Α2, as shown in Proposition 3.

Proposition 3.

Under Α > Α2,

(1) if ΔΙ ≤ (1 − d)tΡl, then β* = 0, Ι* = Ιh, αh* = 0, and ϒh* = 0;

(2) if (1 − d) tΡl < ΔΙ <(1−d )sP, then β* = β3, Ι* = Ιh, αh* = 0, and ϒh* = 0;

(3) if ΔΙ ≥(1−d )sP, then β* = 0, Ι* = Ιl, αl* = 0, and ϒl* = 0; where ΔΙ ≡ Ιh − Ιl, P≡ θΡh + (1 − θ) Ρl, and β3 ≡ 1 −

I tPl d Δ

− ) 1

( .

Proof. See Appendix.

As audit cost becomes considerably significant, the regulator will offer the investment subsidy only if the increased investment is larger than the firm’s savings in expected pollution tax, but less than the savings in expected social damage from pollution. Otherwise, the investment subsidy will be neither necessary (if ΔΙ ≤ (1 − d)tΡl) nor economical (if ΔΙ ≥ (1−d )sP). Under the subsidy policy, the firm will make a high investment in abatement of pollution provided the increased investment is less than the savings in expected social damage from pollution.

Additionally, since audit cost is relatively significant, it is uneconomical for the regulator to undertake any audit action no matter whether the firm has made a high investment or not. Thus, the firm will tend to dishonestly declare a low pollution state under a high pollution state no matter what investment the firm has made.

From the results of Propositions 1 to 3, there are different policy combinations within various possible ranges of audit cost. It is obvious that the strategy equilibrium will change with audit cost. The related results are summarized in Table 2, where it can be found that as audit cost becomes considerably significant (i.e. Α > Α2), the regulator will be inclined to use a subsidy policy and to totally abandon audit policy. In that case, not only does the threshold of subsidy become lower (i.e. ΔΙ1 < ΔΙ2) than that as the audit cost is insignificant (i.e. Α ≤ Α1), but also the subsidy rate will be relatively higher (i.e. β3 >β1). That implies, as environmental audit is difficult and costly, that the subsidy on the investment in abatement of pollution can be much more effective and justifiable. Additionally, if audit cost is relatively moderate (i.e. Α1 < Α ≤ Α2), the regulator will tend to take an effective (random) audit policy for low-investment firms, but will give up audit measure for high-investment firms.

4 ΔΙ3 denotes the savings in expected pollution tax as Α > Α2 and the firm makes a high (rather than low) investment.

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

48 Table 2. Policy summary*

The Range of Audit Cost Α ≤ Α1 Α1 < Α ≤ Α2 Α > Α2

Audit Policy αh* = αl* =

) (

) (

tPl Ph t q

Pl Ph t

′ −

− αh* = 0, αl* =

) (

) (

tPl Ph t q

Pl Ph t

′ −

− αh* = αl* = 0

Self-Reporting Decision ϒh* = ϒl* = 1 ϒh* = 0, ϒl* = 1 ϒh* = ϒl* = 0

Possible Subsidy Policy and Investment Decision

⎪⎩

⎪⎨

⎧

=

= Ih I

i *

* 0 )

( β

if ΔΙ ≤ ΔΙ2

⎪⎩

⎪⎨

⎧

=

= Ih I ii *

* 1 )

( β β

if ΔΙ2 < ΔΙ < ΔΙ3

⎪⎩

⎪⎨

⎧

=

= Il I ii *

* 0 )

( β

if ΔΙ ≥ ΔΙ3

⎪⎩

⎪⎨

⎧

=

= Ih I

i *

* 0 )

( β

if ΔΙ ≤ ΔΙ4

⎪⎩

⎪⎨

⎧

=

= Ih I ii *

* 2 )

( β β

if ΔΙ4 < ΔΙ < ΔΙ5

⎪⎩

⎪⎨

⎧

=

= Il I ii *

* 0 )

( β

if ΔΙ ≥ ΔΙ5

⎪⎩

⎪⎨

⎧

=

= Ih I

i *

* 0 )

( β

if ΔΙ ≤ ΔΙ1

⎪⎩

⎪⎨

⎧

=

= Ih I ii *

* 3 )

( β β

if ΔΙ1 < ΔΙ < ΔΙ3

⎪⎩

⎪⎨

⎧

=

= Il I ii *

* 0 )

( β

if ΔΙ ≥ ΔΙ3

*Α1 ≡

( )

1θ−θ qd(t′Ρh − tΡl), Α2 ≡( )

1−θθ q(t′Ρh − tΡl), ΔΙ1 ≡ (1 − d)tΡl, ΔΙ2 ≡ (1 − d)tP , ΔΙ3 ≡ (1 − d)sP ,ΔΙ4 ≡ t

(

P−dPl)

, ΔΙ5 ≡ (1 − θ)α1Α + (1 − d)sP , and ΔΙ1 < ΔΙ2 < ΔΙ3 (ΔΙ4) < ΔΙ5. In addition, β3 >β1given the same ΔΙ.4. CONCLUSIONS

To induce a polluting firm to make a necessary investment in environmental protection, the regulator needs to employ some policy measures as economic incentives. Among others, the subsidy on the investment in abatement of pollution and the tax imposed on the pollution, subject to possible audit, are often regarded as two important incentives contributing toward alleviating the costly externalities of pollutions generated by optimizing economic firms. Since there is some evidence in the literature to justify a self-reporting regime, this paper simultaneously addresses the issues of subsidy, audit and self-reporting in environmental policy. Following Guo and Wang (2004), this paper uses a principal-agent model to examine the interplays among these regulatory measures.

Assuming the auditor is absolutely independent and has basic audit capability, i.e. audit quality is over some threshold level, we find that in response to the regulator’s audit policy the firm’s optimal reporting strategy under high (or low) investment is either honestly declaring a high pollution state or dishonestly declaring a low pollution state given that the realized state of pollution is high. In contrast, responding to the firm’s possible strategy, the regulator’s optimal audit policy will be either a mixed one with some audit probability or a pure one with no audit, depending on the condition of audit cost. While the threshold for using

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

49

random audit under high investment is stricter than that under low investment, the probabilities of random audit under either high or low investments are indifferent and mainly contingent on audit quality, tax rates and pollution levels.

A little different from the result of Guo and Wang (2004), under a self-reporting regime, there seems to be no strong policy substitutability between subsidy and audit measures. As shown in this paper, when audit cost is insignificant, the regulator can still resort to subsidy measures in addition to an effective audit policy, while such a subsidy measure will never be considered under no self-reporting in Guo and Wang. Nevertheless, as audit cost becomes considerably significant, the regulator will be inclined to adequately use subsidy policy and totally abandon audit policy. In that case, not only does the threshold of subsidy become lower than that as audit cost is insignificant, but also the subsidy rate is relatively higher. That implies, as environmental audit is difficult and costly, the subsidy on the investment in abatement of pollution can be much more effective and justifiable.

If audit cost is relatively moderate, the regulator will take an effective audit action only if the firm has made a low investment; and responding to the regulator’s audit policy, the firm will honestly declare its pollution state. In contrast, under high investment, the firm will under-declare the pollution state, given a high pollution state occurs, due to no audit threat. When audit cost is insignificant, in consideration of the effective audit from the regulator, the firm will honestly declare a high pollution state no matter if it is under high or low investment.

Essentially, whether the regulator needs to employ a subsidy policy or not depends not only on if the subsidy is necessary to induce high investment but also on if subsidy policy is economically better than the no subsidy policy. Additionally, the normal tax rate on pollution plays a prominent role in both subsidy and audit polices. Ceteris paribus, the lower is the normal tax rate of pollution, the higher the subsidy rate will be, but the lower will be the probability of a random audit.

However, as the normal tax rate of pollution increases, it will enhance the possibility of the firm voluntarily undertaking a high investment, even in the scarcity of a subsidy.

REFERENCES

Antle, R. (1982). The auditor as an economic agent. Journal of Accounting Research, 20, 503-527.

Antle, R. (1984). Auditor independence. Journal of Accounting Research, 22, 1-20.

Arguedas, C., & van Soest, D. P. (2009). On reducing the windfall profits in environmental subsidy programs. Journal of Environmental Economics and Management, 58(2), 192-205.

Backlund, K. (2003). On the role of green taxes in social accounting.

Environmental and Resource Economics, 25, 33-50.

Baiman, S., Evans, J., & Nagarajan, N. (1991). Collusion in auditing. Journal of Accounting Research, 29, 1-18.

Baron, D., & Besanko, D. (1984). Regulation, asymmetric information and auditing.

Rand Journal of Economics, 15, 447-470.

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

50

Baumol, W. J., & Oates, W. E. (1979). Economics, Environmental Policy, and the Quality of Life. New Jersey, USA: Prentice-Hall, Inc., Englewood Cliffs.

Campbell, S. N., & Byington, J. R. (1995). Environmental auditing: an environmental management tool. Internal Auditing, 11(2), 9-18.

Cantono, S., & Silverberg, G. (2009). A percolation model of eco-innovation diffusion: The relationship between diffusion, learning economies and subsidies. Technological Forecasting and Social Change, 76(4), 487-496.

Demski, J., & Sappington, D. (1987). Hierarchical regulatory control. Rand Journal of Economics, 18, 369-383.

Doyle, J. (1992). Audits are their own reward. The Environmental Forum, 9(1), 38-39.

Fisher, A. C. (1983). Resources and Environmental Economics. Cambridge, UK:

Cambridge University Press.

Franckx, L. (2002). The use of ambient inspections in environmental monitoring and enforcement when the inspection agency cannot commit itself to announced inspection. Journal of Environmental Economics and Management, 43, 71-92.

Friesen, L. (2006). The social welfare implications of industry self-auditing.

Journal of Environmental Economics and Management, 51, 280-294.

Guo. R., & Wang, T. (2004). Investment, subsidy, and audit in environmental protection. Journal of Social Sciences and Philosophy, 16 (4), 505-531.

Harberger, A. C. (1980). Tax neutrality in investment incentives. In Aaron, H., Boskin, M. (Eds.) The Economics of Taxation (pp. 299-313). Washington, DC, USA: The Brookings Institution.

Innes, R. (1999). Remediation and self-reporting in optimal law enforcement.

Journal of Public Economics, 72, 379-393.

Isik, M. (2004). Incentives for technology adoption under environmental policy uncertainty: implications for green payment programs. Environmental and Resource Economics, 27, 247-263.

Kaplow, L., & Shavell, S. (1994). Optimal law enforcement with self-reporting of behavior. Journal of Political Economy, 102(3), 583-606.

Kneese, A. V., & Bower, B. T. (1968). Managing Water Quality. Economics, Technology, Institution. Baltimore, USA: Johns Hopkins University Press.

Kofman, F., & Lawarree, J. (1993). Collusion in hierarchical agency. Econometrica, 61, 629-656.

Kofman, F., & Lawarree, J. (1996). On the optimality of allowing collusion.

Journal of Public Economics, 61, 383-407.

Kort, P. M., van Loon, Paul J. M., & Luptacik, M. (1991). Optimal dynamic environmental policies of a profit maximizing firm. Journal of Economics, 54(3), 195-225.

Laplante, B. (1990). Producer surplus and subsidization of pollution control device:

a non-monotonic relationship. The Journal of Industrial Economics, 39(1), 15-23.

McGilligan, C., Sunikka-Blank, M., & Natarajan, S. (2010). Subsidy as an agent to enhance the effectiveness of the energy performance certificate. Energy Policy, 38(3), 1272-1287.

Malik, A. S. (1993). Self-reporting and the design of policies for regulating

R. J. Guo/ Asian Journal of Arts and Sciences, Vol. 2, No. 1, pp. 37-56, 2011

51

stochastic pollution. Journal of Environmental Economics and Management, 24, 241-257.

Mills, E. S. (1972). Economic incentives in air-pollution control. In Goldman, M. I.

(Ed.), Ecology and Economics (pp. 145-146). New Jersey, USA: Prentice-Hall, Inc., Englewood Cliffs.

Morelli, J. A. (1994). Performing environmental audits: an engineer’s guide.

Chemical Engineering, 101(2), 104-113.

Penno, M. (1990). Auditing for performance evaluation. The Accounting Review, 65, 520-536.

Rajah, N., & Smith, S. (1993). Taxes, taxes expenditures, and environmental regulation. Oxford Review of Economic Policy, 9(4), 41-65.

Sandmo, A. (2002). Efficient environmental policy with imperfect compliance.

Environmental and Resource Economics, 23, 85-103.

Slitor, R. E. (1976). Pollution Taxes. Taxation and Development. New York, USA:

Praeger Publishers.

Toshimitsu, T. (2010). On the paradoxical case of a consumer-based environmental subsidy policy. Economic Modelling, 27(1), 159-164.

Ruey-Ji Guo is currently a professor in the Department of Accounting, Soochow University, Taiwan.

He earned his Ph.D. degree in Accounting from National Taiwan University. His recent research interests focus on management accounting, audit decision, and environmental policy. His papers have been published in Economic Modelling, Journal of Social Sciences and Philosophy, Sun Yat-Sen Management Review, Taiwan Academy of Management Journal, Pan-Pacific Management Review, Journal of Accounting and Corporate Governance, amongst others.