國立臺灣大學理學院應用數學科學研究所 碩士論文

Institute of Applied Mathematical Sciences College of Science

National Taiwan University Master Thesis

大離差理論在系統風險和投資組合最佳化的應用

Applications of Large Deviation Theory to Systemic Risk and Portfolio Optimization

郭宣宏 Hsuan-Hung Kuo

指導教授:韓傳祥博士

Advisor: Chuan-Hsiang Han, Ph.D.

中華民國 108 年 6 月

June 2019

iii

摘要

這份論文有兩部分。在第一部分,我們會用重要抽樣法來估計稀 有事件的期望值。在常態分配或是布朗運動模型下,可以證明我們提 出的方法是有效率的。我們也會說明如何應用重要抽樣法來評估系統 風險。在第二部分,我們會應用大離差理論在有限時間的投資最佳化 上面。

關鍵詞:重要抽樣法、漸進最佳、大離差、體系風險、投資組合最佳 化

v

Abstract

There are two parts in this paper. In the first part, we will focus on estimating the expectations under a rare event with the importance sampling method. Under Normal distribution or Brownian motion, we can prove that our proposed method is efficient. We will also show how to apply the importance sampling method to measure the systemic risk. In the second part, we will apply large deviation theory to the finite-horizon investment optimization.

Keywords: importance sampling, asymptotic optimality, large deviation, systemic risk, optimal portfolio

Contents

摘要 iii

Abstract v

1 Introduction 1

Part 1 3

2 Standard Normal Case 4

2.1 Change measure . . . 4 2.2 Asymptotic variance analysis . . . 5 2.3 Numerical results . . . 7

3 Brownian Motion Case 8

3.1 Change measure . . . 8 3.2 Asymptotic variance analysis . . . 9 3.3 Numerical results . . . 11

4 Geometric Brownian Motion Case 12

4.1 Change measure . . . 12 4.2 Asymptotic variance analysis . . . 13 4.3 Numerical results . . . 17

5 Applications to Measuring Systemic Risk 18

5.1 Stochastic Volatility model . . . 18 5.2 First Passage Time Case . . . 20

Part 2 23

6 Optimal Finite-Horizon Investment 24

6.1 Constant Investment Strategy . . . 25 6.2 Deterministic Investment Strategy . . . 28

7 Conclusion 31

References 32

List of Tables

2.1 Standard normal case . . . 7 3.1 Brownian motion case . . . 11 4.1 Geometric Brownian motion case . . . 17 5.1 Results of basic Monte Carlo simulation and importance sampling scheme

with N = 160000, T = 0.5, dt = 0.002, µm = 0.1, µi = 0.08, κm = 5, κi = 3, ξm = 2, ξi = 1, θm = 0.5, θi = 0.3, αi = 5, βi = 1, m = 0.5, ρi = 0.5, ρm = 0.5. . . . 20 5.2 Results of basic Monte Carlo simulation and importance sampling scheme

with N = 40000, T = 0.5, dt = 0.002, µi = 0.08, µm = 0.1, σi = 0.3, σm = 0.5, ρ = 0.7. . . . 22

Chapter 1

Introduction

It is a trend to use Monte Carlo simulation to estimate credit risk. However, it is not effi- cient when the event become rare. For example, let Z be a random variable that follows the standard normal distribution. We are interested in the expectation E[Z1(Z < c)], where c is a negative constant. It is easy to compute the closed form−√12πe−c22 . However, when c is very small, we can see that the value will become very small, which makes it inefficient to use crude Monte Carlo to estimate it. That is, we need to sample a lot of times so that we can have a small standard error.

The importance sampling method helps us to solve the ”inefficient” problem. More specif- ically, the importance sampling method helps to reduce the variance [9]. The idea of im- portance sampling is to find a suitable change of measure so that the rare events we are interested in will become ”not rare” under the new measure, which will be called ˜P in this paper. Also, we need to reduce the variance of estimation under this new measure ˜P . Since

V arP˜ = EP˜[(f (Z)dP

d ˜P)2]− (EP˜[f (Z)dP d ˜P])2

= EP˜[(f (Z)dP

d ˜P)2]− (E[f(Z)])2,

we can see that the variance equals to 0 if we could minimize the second moment under the measure ˜P . However, it is difficult to minimize it directly since the minimization often relates to solving a nonlinear equation. Thus, we seek another way called ”asymp- totically optimal” property to solve it [9]. That is, we will check if limc→−∞ c12 ln M2 =

2 limc→−∞ 1

c2 ln M1under the measure ˜P , where M1, M2are the first moment and the sec- ond moment, respectively. If it does, it implies that the importance sampling we proposed is ”efficient”.

On the other hand, a lot of researchers use Importance Sampling to apply the theory of large deviation to analyze the asymptotic properties of the tail probability. The famous theories are Cramer Theorem, Schilder’s Theorem, Freidlin-Wentzell Theorem, etc. In financial applications, some researchers let the time T go to infinity so that these large de- viation theories can be easily applied. [8] provides a large deviations approach to optimal long-term investment. However, some investors would like to earn their money as soon as possible. Thus, we will try to apply the theory of large deviations to the finite-horizon investment.

This paper is composed of two parts. In the first part, we will apply Importance Sampling to estimate the expectation of a random variable under a rare event. In Chapter 2, we are going to apply the method under the standard normal distribution. In Chapter 3 and 4, we will extend it to Brownian motion and geometric Brownian motion. In Chapter 5, we present some applications to estimate systemic risk under different models. In the second part, we will apply the theory of large deviation to the finite-horizon investment, which will be represented in Chapter 6.

Part 1

Large Deviation Theory applied to Systemic Risk

In this part, we will use importance sampling method to measure the systemic risk under different models. In order to do this, we need to estimate the form E[1(X < c)] and E[X1(X < c)], where X is a random variable and c is a (usually negative) constant.

There have been some papers about how to estimate E[1(X < c)] efficiently, such as [1]

and [2]. Thus, we will focus on E[X1(X < c)] in this part.

Chapter 2

Standard Normal Case

Suppose Xi = ρXM +√

1− ρ2Y , where XM, Y are independent standard normal distri- bution, and ρ is correlation between Xiand XM. We are going to estimate E[Xi1(XM <

c)]. When the value c is very small, it is difficult to use Monte Carlo to estimate. Thus, we will use importance sampling by choosing a new measure ˜P such that the event{XM < c} is no more ”rare” under this measure.

2.1 Change measure

Note that

E[Xi1(XM < c)] = E[(ρXM +√

1− ρ2Y )1(XM < c)]

= ρE[XM1(XM < c)] +√

1− ρ2E[Y 1(XM < c)]

We can see that the second term is equal to 0 since XM and Y are independent. Thus, we just need to consider the first term.

The easiest way to choose a new measure ˜P such that the event {XM < c} is no more

”rare” under this measure is to make the mean of XM be c. That means XM will be a normal distribution with the mean c and the variance 1 under the new measure ˜P . Then

we can derive that

dP d ˜P =

√1

2πe−X22M

√1

2πe−(XM −c)

2 2

= e−cXM+c22 . Due to the above, we can rewrite the first term as:

E[XM1(XM < c)] = ˜E[XMexp(−cXM + c2

2)1(XM < c)].

2.2 Asymptotic variance analysis

The first moment is

M1 =−ρE[XM1(XM < c)]

=−ρ

∫ c

−∞

√z

2πe−z22 dz

= ρ

√2πe−c22 .

It implies that

c→−∞lim 1

c2 ln M1 =−1 2.

Suppose XM ∼ N(−c, 1), Z ∼ N(0, 1) under ˆP . Then the second moment is M2 = ˜E[Xi2exp(−2cXM + c2)1(XM < c)]

= ec2E[Xˆ i2exp(−2cXM)1(XM < c)d ˜P d ˆP]

= ec2E[Xˆ i2exp(−2cXM)1(XM < c)e2cXM]

= ec2E[Xˆ i21(XM < c)]

= ρ2ec2E[Xˆ M2 1(XM < c)] + (1− ρ2)ec2E[Yˆ 21(XM < c)]

= ρ2ec2E[(Zˆ − c)21(Z < 2c)] + (1− ρ2)ec2E[1(Z < 2c)]ˆ

= ρ2ec2{ ˆE[Z21(Z < 2c)]− 2c ˆE[Z1(Z < 2c)] + c2E[1(Z < 2c)]ˆ } + (1− ρ2)ec2Φ(2c)

= ρ2ec2{

∫ 2c

−∞

z2

√2πe−z22 dz− 2c

∫ 2c

−∞

√z

2πe−z22 dz + c2Φ(2c)} + (1− ρ2)ec2Φ(2c)

= ρ2ec2(1 + c2)Φ(2c) + (1− ρ2)ec2Φ(2c)

= (ρ2c2+ 1)ec2Φ(2c),

where Φ(z) is the cdf of a standard normal.

There is an important approximation to Φ(z):

z→−∞lim Φ(z) = 1

√2π(−z)e−z22 .

It implies that

c→−∞lim 1 c2 ln M2

= lim

c→−∞

1

c2[c2+ ln(ρ2c2+ 1) + ln( 1

√2π(−2c))− 2c2]

=−1.

Thus, we have the following theorem.

Theorem 1. Suppose Xi = ρXM +√

1− ρ2Y , where XM, Y are independent standard

M2 = ˜E[Xi21(XM < c)(dP d ˜P)2].

Then,

c→−∞lim 1

c2 ln M2 = 2 lim

c→−∞

1

c2 ln M1.

2.3 Numerical results

The numerical results are shown below. N is the simulation number. The value simulated by basic Monte Carlo (BMC), importance sampling (IS) and the corresponding standard error (S.E.) are given in the table. We also compare the value with the exact answer (exact).

Table 2.1: Standard normal case

c exact N BMC S.E. IS S.E.

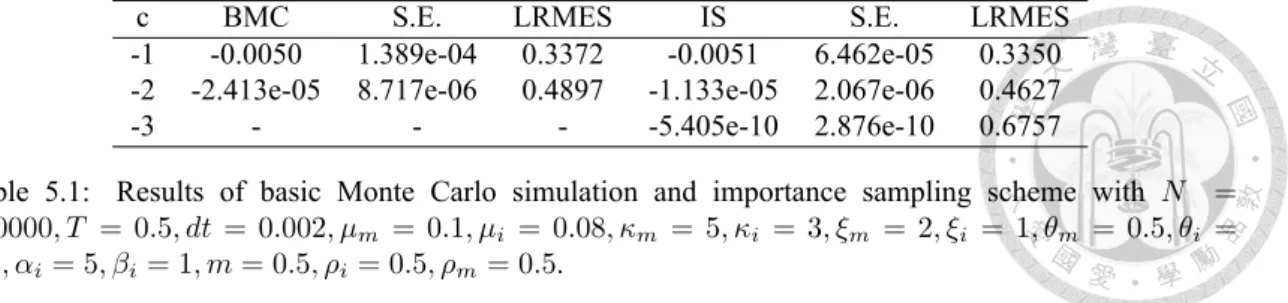

10000 -0.2418 0.0058 -0.2377 0.0026

-1 -0.2420 40000 -0.2473 0.0029 -0.2416 0.0013

160000 -0.2403 0.0015 -0.2419 6.3741e-04 10000 -0.0028 0.0013 -0.0043 7.9976e-05 -3 -0.0044 40000 -0.0041 6.4021e-04 -0.0044 3.8964e-05 160000 -0.0041 3.0699e-04 -0.0044 1.9402e-05

10000 0 - -1.4956e-06 3.3274e-08

-5 -1.4867e-06 40000 0 - -1.4769e-06 1.7267e-08

160000 -3.2663e-05 3.2663e-05 -1.5034e-06 8.6994e-09

We can see that the basic Monte Carlo method can hardly sample a rare event when c =

−5, while the importance sampling method we provide gives an accurate estimation. In addition, the sample error of importance sampling scheme is smaller than that of basic Monte Carlo method.

Chapter 3

Brownian Motion Case

Let WM t, Ztbe independent Brownian motion. Define Wit = ρWM t+√

1− ρ2Zt,

where ρ is a correlation between Witand WM t. Then Wit is also a Brownian motion. In this chapter, we are going to estimate E[WiT1(WM T < c)].

3.1 Change measure

Note that if c becomes very small, the probability of the event {WM T < c} will also be small, which means that it will be inefficient to use crude Monte Carlo method. Thus, we need to find a new measure ˜P such that the event{WM T < c} would be no more ”rare”

under this measure. The following theorem helps us to find a good measure.

Girsanov’s Theorem. [6] Let Wt, 0≤ t ≤ T be a Brownian motion. Let Θt, 0≤ t ≤ T be an adapted process. Define

Zt= exp{

∫ t 0

ΘuWu− 1 2

∫ t 0

Θ2udu}, W˜ = W −

∫ t

Θ du,

We also define a new probability measure ˜P by the formula P˜A=

∫

A

ZωdPωfor all A∈ F.

Set Z = ZT. Then E[Z] = 1 and under the probability measure ˜P , the process ˜Wt, 0≤ t ≤ T , is also a Brownian motion.

By the Girsanov’s Theorem, we can define dP

d ˜P = e−αWM T+12α2T, W˜M T = WM T − αT,

where α is a constant and ˜WM T is a Brownian motion under ˜P .

Next, we are going to determine the constant α. If we hope to make the event{WM T < c} no more ”rare”, we can simply let ˜E[WM T] = c. That is to say,

E[W˜ M T] = ˜E[ ˜WM T + αT ] = αT = c, which means that α = Tc.

3.2 Asymptotic variance analysis

Note that WM T ∼ N(0, T ) since WM T is a Brownian motion. So we can get the first moment as following:

M1 =−E[WiT1(WM T < c)]

=−ρE[WM T1(WM T < c)]

=−ρ

∫ c

−∞

√x

2πTe−x22Tdx

= ρ√

√ T

2πe−2Tc2. It implies that

c→−∞lim 1

c2 ln M1 =− 1 2T.

Before we consider the second moment, we define a new measure ˆP by dP

d ˆP = eαWM T+12α2T WˆM T = WM T + αT,

where ˆWM T is a Brownian motion under ˆP . Then we can calculate the second moment as follows:

M2 = ˜E[WiT2 1(WM T < c)(dP d ˜P)2]

= E[WiT2 1(WM T < c)dP d ˜P]

= ˆE[WiT2 1(WM T < c)dP d ˜P

dP d ˆP]

= ˆE[WiT2 1(WM T < c)eα2T]

= eα2TE[(ρWˆ M T +√

1− ρ2ZT)21(WM T < c)]

= eα2T{ ˆE[ρ2WM T2 1(WM T < c)] + ˆE[(1− ρ2)ZT21(WM T < c)]}

= ρ2eα2TE[Wˆ M T2 1(WM T < c)] + (1− ρ2)eα2TT ˆE[1(WM T < c)]

= ρ2eα2TE[( ˆˆ WM T − αT )21( ˆWM T < 2c)] + (1− ρ2)eα2TT Φ( 2c

√T)

= ρ2eα2T{ ˆE[ ˆWM T2 1( ˆWM T < 2c)]− 2αT ˆE[ ˆWM T1( ˆWM T < 2c)]

+ α2T2E[1( ˆˆ WM T < 2c)]} + (1 − ρ2)eα2TT Φ( 2c

√T)

= ρ2ec2T{−2c

√T

√2πe−2c2T + T Φ( 2c

√T) + 2c√

√ T

2π e−2c2T + c2Φ( 2c

√T)}

+ (1− ρ2)ec2TT Φ( 2c

√T)

= ec2TΦ( 2c

√T)(ρ2c2+ T ).

It implies that

c→−∞lim 1 c2 ln M2

= lim

c→−∞

1

c2 ln[e−c2T

√T

√2π(−2c)(ρ2c2 + T )]

=−1 T. Thus, we have the following theorem.

Theorem 2. Suppose Wit = ρWM t+√

1− ρ2Zt, where WM t, Ztare Brownian motion,

M2 = ˜E[WiT2 1(WM T < c)(dP d ˜P)2].

Then,

c→−∞lim 1

c2 ln M2 = 2 lim

c→−∞

1

c2 ln M1.

3.3 Numerical results

We perform the sampling again, the numerical results are shown below.

Table 3.1: Brownian motion case

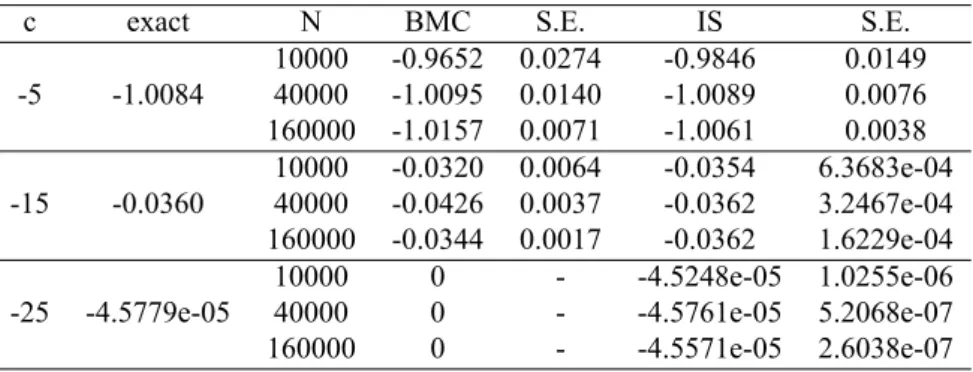

c exact N BMC S.E. IS S.E.

10000 -0.9652 0.0274 -0.9846 0.0149 -5 -1.0084 40000 -1.0095 0.0140 -1.0089 0.0076 160000 -1.0157 0.0071 -1.0061 0.0038

10000 -0.0320 0.0064 -0.0354 6.3683e-04 -15 -0.0360 40000 -0.0426 0.0037 -0.0362 3.2467e-04 160000 -0.0344 0.0017 -0.0362 1.6229e-04

10000 0 - -4.5248e-05 1.0255e-06

-25 -4.5779e-05 40000 0 - -4.5761e-05 5.2068e-07

160000 0 - -4.5571e-05 2.6038e-07

T = 30, ρ = 0.7.

Again, we can see that when c =−25, the basic Monte Carlo method cannot sample a rare event even we simulate 160000 times, while the importance sampling method we provide gives an accurate estimation. In addition, the sample error of importance sampling scheme is at least an order smaller than that of basic Monte Carlo method when c < −15.

Chapter 4

Geometric Brownian Motion Case

Let two assets be defined by the following:

dSit = µiSitdt + σiSitdWit dSmt = µmSmtdt + σmSmtdWmt, where Wit, Wmtare Brownian motion satisfying Wit = ρWmt+√

1− ρ2Zt. Wmt, Ztare independent Brownian motion.

Let rit = lnSSit

i0, rmt = lnSSmt

m0. In this chapter, we are going to estimate E[riT1(rmT < c)].

4.1 Change measure

It can be derived that

lnSiT

Si0 = (µi −σi2

2 )T + σiWiT lnSmT

Sm0 = (µm− σm2

2 )T + σmWmT. It means that the event{rmT < c} is equivalent to {WmT < c−(µm−

σ2m 2 )T

σm }. Thus, we can again use a similar method as previous chapter. That is, we define

where h is a constant and ˜WmT is a Brownian motion under ˜P . Since we hope that E[r˜ mT] = c, we can get

E[ln˜ SmT

Sm0] = (µm−σm2

2 )T + σmE[W˜ mT]

= (µm−σm2

2 )T + σmE[ ˜˜ WmT + hT ]

= (µm−σm2

2 )T + σmhT

= (µm−σm2

2 + σmh)

= c, which implies that h = c−(µm−

σ2m 2 )T σmT .

4.2 Asymptotic variance analysis

Let ˜c = c−(µm−

σ2m 2 )T

σm . Then the first moment is M1 = E[riT1(rmT < c)]

= E[((µi−σi2

2 )T + σiWiT)1((µm−σm2

2 )T + σmWmT < c)]

= (µi− σ2i

2 )T · E[1(WmT < ˜c)] + σi· E[WiT1(WmT < ˜c)]

= (µi− σ2i

2 )T · Φ( ˜c

√T)− ρσi√

√ T

2π e−2Tc2˜ . It implies that

c→−∞lim 1

c2 ln|M1|

= lim

c→−∞

1

c2ln|e−2Tc2˜ ((µi− σ2i2)T√

√ T

2π(−˜c) −ρσi

√T

√2π )|

= lim

c→−∞

1

c2(−[c− (µm−σ22m)T ]2 2T σm2 )

=− 1

2T σ2m.

Before we consider the second moment, we define a new measure ˆP by dP

d ˆP = ehWmT+12h2T WˆmT = WmT + hT,

where ˆWmT is a Brownian motion under ˆP . Then we can calculate the second moment as follows:

M2 = ˜E[riT2 1(rmT < c)(dP d ˜P)2]

= ˜E[riT2 1(rmT < c)eh2T−2hWmT]

= eh2TE[((µˆ i− σi2

2 )T + σiWiT)21(WmT < ˜c)]

= eh2T{(µi−σi2

2 )2T2E[1(Wˆ mT < ˜c)]

+ 2(µi−σi2

2 )σiT ˆE[WiT1(WmT < ˜c)]

+ σ2iE[Wˆ iT2 1(WmT < ˜c)]}

= eh2T{(µi−σi2

2 )2T2E[1(Wˆ mT < ˜c)]

+ 2(µi−σi2

2 )σiT ρ ˆE[WmT1(WmT < ˜c)]

+ σ2i(ρ2E[Wˆ mT2 1(WmT < ˜c)] + (1− ρ2) ˆE[ZT21(WmT < ˜c)])}

= eh2T{(µi−σi2

2 )2T2E[1( ˆˆ WmT < ˜c + hT )]

+ 2ρ(µi− σ2i

2 )σiT ˆE[( ˆWmT − hT )1( ˆWmT < ˜c + hT )]

+ ρ2σ2iE[( ˆˆ WmT − hT )21( ˆWmT < ˜c + hT )] + (1− ρ2)σi2T Φ(c + hT˜

√T )}

= eh2T{(µi−σi2

2 )2T2Φ(˜c + hT

√T )

+ 2ρ(µi− σ2i

2 )σiT (−

√T

√2πe−(˜c+hT )22T − hT Φ(˜c + hT

√T ))

+ ρ2σ2iE[( ˆˆ WmT2 − 2hT ˆWmT + h2T2)1( ˆWmT < ˜c + hT )]

+ (1− ρ2)σi2T Φ(˜c + hT

√T )}

= e˜c2T{(µi−σi2

2 )2T2Φ( 2˜c

√T) + 2ρ(µi− σi2

2 )σiT (−

√T

√2πe−2˜Tc2 − ˜cΦ( 2˜c

√T))

+ ρ2σ2i(−2˜c√

√ T

2π e2˜Tc2 + T Φ( 2˜c

√T) + 2˜c√

√ T

2π e2˜Tc2 + ˜c2Φ( 2˜c

√T))

+ (1− ρ2)σi2T Φ( 2˜c

√T)}

√

It implies that

c→−∞lim 1

c2 ln|M2|

= lim

c→−∞

1

c2 ln|e−˜c2T[(µi− σ22i)2T2√

√ T

2π(−2˜c) + 2ρ(µi−σi2

2 )σiT (−

√T

√2π − c˜√

√ T

2π(−2˜c)) + σ2i√

√ T

2π(−2˜c)(ρ2c˜2+ T )]|

= lim

c→−∞

1

c2(−[c− (µm−σ22m)T ]2 T σ2m )

=− 1 T σ2m.

Thus, we have the following theorem.

Theorem 3. Suppose Wit = ρWmt+√

1− ρ2Zt, where Wmt, Ztare Brownian motion, and ρ is correlation between Witand Wmt. Define two assets

dSit = µiSitdt + σiSitdWit dSmt = µmSmtdt + σmSmtdWmt. Also, let

M1 = E[riT1(rM T < c)]

= ˜E[riT1(rM T < c)dP d ˜P] M2 = ˜E[r2iT1(rM T < c)(dP

d ˜P)2], where

rit = lnSit

Si0, rmt = lnSmt Sm0 Then,

c→−∞lim 1

c2 ln|M2| = 2 lim

c→−∞

1

c2 ln|M1|.

In summary, we can get a more general theorem, shown as below.

Theorem 4. Let X, Y be random variables such that

X Y

∼ N

m1 m2

,

σ21 ρσ1σ2 ρσ1σ2 σ22

Also, let

M1 = E[Y 1(X < c)]

M2 = ˜E[Y21(X < c)(dP d ˜P)2], where

dP d ˜P = e−

(x−m1)2 2σ21

e−

(x−c)2 2σ21

. Then,

c→−∞lim 1

c2 ln|M2| = 2 lim

c→−∞

1

c2 ln|M1|.

Proof. Define a random variable Z such that Y = ρX +√

1− ρ2Z. Then Z ∼ N(m2− ρm1

√1− ρ2 ,σ22− ρ2σ12 1− ρ2 ).

Thus,

M1 = ρE[X1(X < c)] +√

1− ρ2E[Z1(X < c)]

= ρ(− σ1

√2πe−

(c−m1)2

2σ21 + m1Φ(c− m1

σ1

)) +√

1− ρ2m√2− ρm1

1− ρ2 Φ(c− m1

σ1

)

=−ρ σ1

√2πe−

(c−m1)2

2σ21 + m2Φ(c− m1

σ1 ).

Since

Φ(c− m1

σ1 )≈ √ −σ1

2π(c− m1)e−

(c−m1)2

2σ21 as c→ −∞, we can derive that

c→−∞lim 1

c2 ln|M1| = − 1 2σ12. On the other hand,

M2 = ˜E[(ρ2X2+ 2ρ√

1− ρ2XZ + (1− ρ2)Z2)1(X < c)(dP d ˜P)2]

= ρ2e

(c−m1)2

σ21 [−2σ1m1

√2π e−

2(c−m1)2

σ21 + (σ12+ (c− 2m1)2)Φ(2c− 2m1

σ1

)]

+ 2ρ(m2− ρm1)e

(c−m1)2

σ21 (− σ1

√2πe−

2(c−m1)2

σ21 − (c − 2m1)Φ(2c− 2m1

σ1 ))

we can derive that

c→−∞lim 1

c2ln|M2| = − 1 σ21. Therefore,

c→−∞lim 1

c2 ln|M2| = 2 lim

c→−∞

1

c2 ln|M1|.

Remark. Theorem 1, Theorem 2, Theorem 3 are the special cases of Theorem 4.

4.3 Numerical results

We show the numerical results again. The results are shown below.

Table 4.1: Geometric Brownian motion case

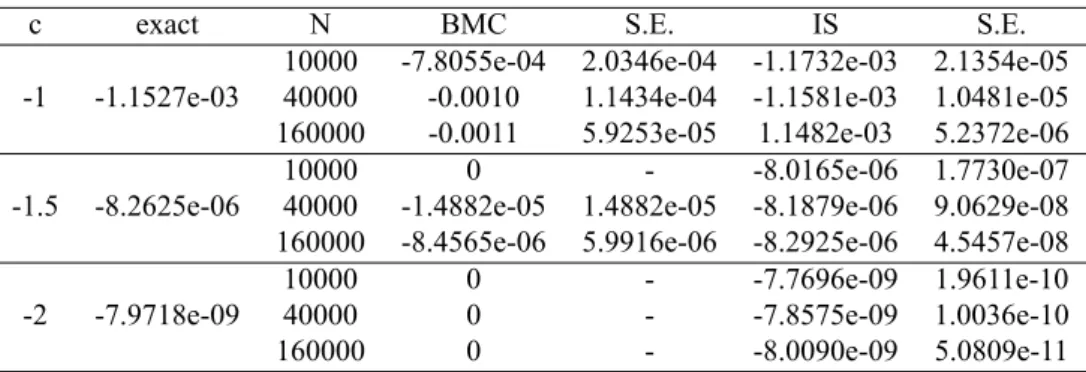

c exact N BMC S.E. IS S.E.

10000 -7.8055e-04 2.0346e-04 -1.1732e-03 2.1354e-05 -1 -1.1527e-03 40000 -0.0010 1.1434e-04 -1.1581e-03 1.0481e-05 160000 -0.0011 5.9253e-05 1.1482e-03 5.2372e-06

10000 0 - -8.0165e-06 1.7730e-07

-1.5 -8.2625e-06 40000 -1.4882e-05 1.4882e-05 -8.1879e-06 9.0629e-08 160000 -8.4565e-06 5.9916e-06 -8.2925e-06 4.5457e-08

10000 0 - -7.7696e-09 1.9611e-10

-2 -7.9718e-09 40000 0 - -7.8575e-09 1.0036e-10

160000 0 - -8.0090e-09 5.0809e-11

T = 0.5, µi= 0.08, σi= 0.3, Si0= 10, µm= 0.1, σm= 0.5, Sm0= 100, ρ = 0.7.

Here we can see that when c = −2, the basic Monte Carlo method cannot sample a rare event even we simulate 160000 times, while the importance sampling method we provide gives an accurate estimation. In addition, the sample error of importance sampling scheme is at least an order smaller than that of basic Monte Carlo method.

Chapter 5

Applications to Measuring Systemic Risk

After the 2008 financial crisis, measuring systemic risk has become a crucial issue for the financial stability. Governments are trying to figure out why the regulation failed, how much capital is required and how to address the next financial crisis. Bisias et al. [10] pro- vide a survey on the systemic risk measures and conceptual frameworks that have been developed in the past few years. There are some measures that are widely adopted, such as SRISK and ∆CoVaR. Adrian and Brunnermeier (2011) allow for tail dependence and use a quantile regression approach to estimate the ∆CoVaR. Brownlees and Engle (2012) model time-varying linear dependencies and use a multivariate GARCH-DCC model to compute the SRISK.

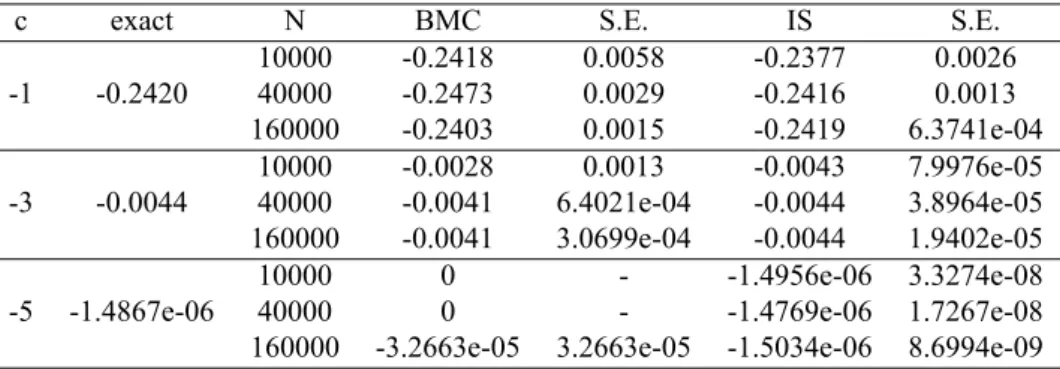

In this chapter, we will estimate the systemic risk measurement SRISK in the framework of Stochastic Volatility Model(SV model). SRISK is defined as the expected capital shortfall of a financial entity conditional on a prolonged market decline. SRISK can be considered to be a function of several variables. One of these variables is Long Run Marginal Ex- pected Shortfall(LRMES). Our goal is to estimate LRMES using the Monte Carlo method and compare it with the importance sampling method.

5.1 Stochastic Volatility model

and assume that stochastic correlation follows Jacobi process.

The overall model is constructed below:

d ln Smt = (µm− Vmt2 )dt +√

VmtdWmt

dVmt = κm(θm− Vmt)dt + ξm√

VmtdZmt d ln Sit = (µi− V2it)dt +√

VitdWit dVit = κi(θi− Vit)dt + ξi√

VitdZit d⟨Wm, Zm⟩t = ρmdt

d⟨Wi, Zi⟩t = ρidt d⟨Wm, Wi⟩t = ρitdt

dρit = αi(mi− ρit)dt + βi

√1− ρ2itdXit

where Smt, Sitdenote the market index and stock price of the i-th firm, respectively, and Vmt, Vit are the corresponding stochastic volatility. Wmt, Wit, Zm, Zi, Xit are the stan- dard Brownian motions, where ρm, ρi, ρitare correlations between each Brownian motion.

κm, κi are the mean reverting speed of corresponding volatility. θm, θi are the long-run level of the volatility. ξm, ξi are the volatility of volatility. αi represents the mean recov- ery rate. βi represents the volatility.

Define the i-th firm’s LRMES from time t to time t + h by

LRMESi,t:t+h=−E[ri,t:t+h(t + h)|Crisist:t+h]

=−E[ri,t:t+h(t + h)1(rm,t:t+h(t + h) < c)]

E[1(rm,t:t+h(t + h) < c)] , (5.1) where rm,t:t+h and ri,t:t+h are the returns of index of market and the i-th firm over the period [t, t + h].

Sometimes the ”Crisis” is a rare event, depending on the value of c. If it is a rare event, then we will introduce the importance sampling method to reduce sample variance. Otherwise, the basic Monte Carlo method is enough.

The numerical results are presented in the following table.

c BMC S.E. LRMES IS S.E. LRMES -1 -0.0050 1.389e-04 0.3372 -0.0051 6.462e-05 0.3350 -2 -2.413e-05 8.717e-06 0.4897 -1.133e-05 2.067e-06 0.4627

-3 - - - -5.405e-10 2.876e-10 0.6757

Table 5.1: Results of basic Monte Carlo simulation and importance sampling scheme with N = 160000, T = 0.5, dt = 0.002, µm = 0.1, µi = 0.08, κm = 5, κi = 3, ξm = 2, ξi = 1, θm = 0.5, θi = 0.3, αi= 5, βi= 1, m = 0.5, ρi= 0.5, ρm= 0.5.

From the numerical results, we can see that the basic Monte Carlo method doesn’t work well when c is very small. On the other hand, the standard error was reduced when we use the importance sampling method.

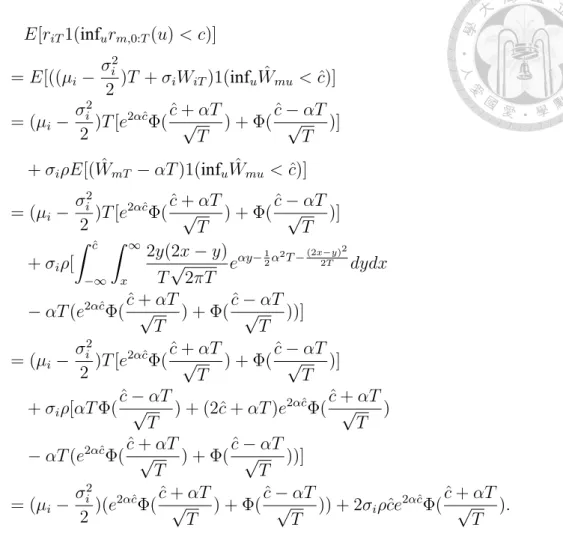

5.2 First Passage Time Case

In this section, we introduce another definition of LRMES. It is called the first passage time problem, or the hitting time problem. We will also use the Heston model, but here we define LRMES as follows:

LRMESi,0:T =−E[ri,0:T(T )|Crisis0:T]

=−E[ri,0:T(T )1(infurm,0:T(u) < c)]

E[1(infurm,0:T(u) < c)] . (5.2) The only difference between (5.1) and (5.2) is the ”Crisis” event. Here we define the ”Cri- sis” to be the minimum market return below c during the time [0, T ]. Before we show the numerical results, we need to show how to compute the denominator and the numerator of LRMES under the constant volatility model. More specifically, we need to derive the density function.

Let ˆWmt = αt + Wmt, where Wmt is a standard Brownian motion. Define ˆm(T ) = min0≤t≤TWˆmt, then we can derive the joint distribution of ˆm(T ) and ˆWmt. Then deriva- tion is similar to [6]. Let ˆZ(t) = e−αWmt−12α2t = e−α ˆWmt+12α2t. By Girsanov’s Theorem, Wˆmtis a Brownian motion under the measure ˆP . By using a similar derivation in [6], we

Hence,

P ( ˆm(T )≤ m, ˆWmT ≤ w) = E[1( ˆm(T )≤ m, ˆWmT ≤ w)]

= ˆE[ 1

Z(T )ˆ 1( ˆm(T )≤ m, ˆWmT ≤ w)]

= ˆE[eα ˆWmT−12α2T1( ˆm(T )≤ m, ˆWmT ≤ w)]

=

∫ w

−∞

∫ m

−∞

eαy−12α2Tfˆm(T ), ˆˆ W

mT(x, y)dxdy.

Therefore, under the measure P , fm(T ), ˆˆ W

mt(x, y) =−2(2x− y) T√

2πT exp(αy− 1

2α2T −(2x− y)2

2T ), x < 0, y ≥ x.

Let α = σ1

m(µm− 12σm2) and ˆc = σc

m. Then we can see that

Smt= Sm0eσmWmt+(µm−12σ2m)t

= Sm0eσmWˆmt. Hence, we can get the denominator

E[1(infurm,0:T(u) < c)]

= E[1(infulnSmu

Sm0 < c)]

= E[1(infuWˆmu< ˆc)]

=

∫ ˆc

−∞

∫ ∞

x

fm(T ), ˆˆ W

mt(x, y)dydx

=

∫ ˆc

−∞

∫ y

−∞−2(2x− y) T√

2πT eαy−12α2T−(2x−y)22T dxdy +

∫ ∞

ˆ c

∫ ˆc

−∞−2(2x− y) T√

2πT eαy−12α2T−(2x2T−y)2dxdy

= e2αˆcΦ(ˆc + αT

√T ) + Φ(ˆc− αT√ T )