Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue underlined headings to activate hyperlinks to the relevant module.

—————————

Purpose

To explain the MA’s approach towards implementing the Basel III Countercyclical Capital Buffer (CCyB) as part of the capital adequacy framework for AIs incorporated in Hong Kong.

Classification

A non-statutory guideline issued by the MA as a guidance note.

Previous guidelines superseded

This is a new guideline.Application

To all locally incorporated AIs.

Structure

1. Introduction

1.1 Terminology 1.2 Background

2. Overview of the CCyB framework 2.1 Objectives

2.2 The CCyB as an extension of the capital conservation buffer

2.3 AI-specific CCyB rates 2.4 Jurisdictional CCyB rates

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

3. The MA’s approach to determining and announcing the Hong Kong jurisdictional CCyB rate

3.1 The steps in the decision process 3.2 The MA’s Initial Reference Calculator 3.3 The Comprehensive Reference Indicators 3.4 Determining the macroprudential policy stance 3.5 Deciding on the Hong Kong jurisdictional CCyB rate 3.6 Public communication regarding the Hong Kong

jurisdictional CCyB rate

4. The MA’s approach to recognising overseas jurisdictional CCyB rates

4.1 The Basel Committee standard of jurisdictional reciprocity 4.2 Recognition of other jurisdictions’ CCyB rate decisions 4.3 Application of exceptional treatment in extraordinary

circumstances

Annex 1 – Calculating the Basel Common Reference Guide for Hong Kong

Annex 2 – Calculating the Composite CCyB Guide Annex 3 – Buffer release: The Indicative CCyB Ceiling

Annex 4 – Illustrative back-testing of the Initial Reference Calculator Annex 5 – Mapping the Comprehensive Reference Indicators to a macroprudential policy stance

—————————

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

1. Introduction

1.1 Terminology

1.1.1 Unless otherwise specified, abbreviations and terms used in this module follow those used in the Banking (Capital) Rules (“BCR”) and in the Banking (Disclosure) Rules (“BDR”). In this module, “AI” means “locally incorporated AI” and “BO” means “Banking Ordinance” unless otherwise specified.

1.2 Background

1.2.1 As the Basel Committee has observed, one of the most destabilising elements of a financial crisis is the procyclical amplification of shocks throughout the banking system, financial markets and the broader economy. The losses incurred in the banking sector during a downturn, which has been preceded by a period of excess credit growth, can be extremely large. These losses can destabilise the banking sector and effectively spark a vicious circle, whereby problems in the financial system can contribute to a downturn in the real economy that then feeds back in to the banking sector. In an endeavour to address these issues, the Basel Committee has developed a series of measures to help ensure that the banking sector serves as a “shock absorber”, instead of a transmitter or amplifier of risk to the financial system and the broader economy. One of these measures is the Basel III Countercyclical Capital Buffer (CCyB).1

1.2.2 The Basel III regulatory capital standards issued by the Basel Committee provide for the implementation of a CCyB beginning on 1 January 2016.2 Owing to the

1 See Basel Committee, Basel III: A global regulatory framework for more resilient banks and banking systems, issued by the Basel Committee in December 2010 and revised June 2011 (“Basel III document”), paras.18, 29 and 136.

2 The requirements for the CCyB are contained in the Basel III document, paras.136-150, and in Guidance for national authorities operating the countercyclical capital buffer, issued by the Basel

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

CCyB’s focus on excessive aggregate credit growth, the Basel Committee has indicated an expectation that jurisdictions will only be likely to deploy it infrequently.

1.2.3 The BO provides for the MA to make rules prescribing capital requirements for AIs incorporated in Hong Kong (see BO §97C(1)). In doing so, the MA may give effect to banking supervisory standards relating to capital issued by the Basel Committee, subject to such modifications as the MA sees fit in light of local circumstances (see BO

§97C(3)(b)).

1.2.4 The MA has made the BCR under BO §97C and the BDR under BO §60A and has, by the Banking (Capital) (Amendment) Rules 2014 and the Banking (Disclosure) (Amendment) Rules 2014, incorporated provisions for the imposition of capital requirements arising from the operation of the CCyB into the BCR and for corresponding disclosures into the BDR respectively.

1.2.5 This module provides an overview of the CCyB framework in Hong Kong and describes the MA’s approach to taking decisions with regard to the setting of the CCyB rates applicable to AIs. This module is intended to complement AIs’ understanding of the BCR and BDR but should not be read as in any sense substituting or amending the text of the BCR or BDR.

2. Overview of the CCyB framework

2.1 Objectives

2.1.1 The primary aim of the CCyB is to provide a measure of protection to the banking sector against the build-up of system-wide risk associated with periods of excessive aggregate credit growth. The CCyB seeks to achieve this by ensuring that banks, and the banking sector in aggregate, accumulate additional capital during any observed “credit boom”, which can be used later (“released”) to absorb any losses or meet any increased capital requirements when system-wide risk crystallizes,

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

probabilities of default increase, and the financial system enters a phase of stress and contraction. This should, in turn, help to maintain the flow of credit to corporates and individuals and thereby lessen the impact of the stress on the real economy after a period of exuberant credit growth.

2.1.2 As a secondary benefit, the CCyB may also tend to lean against the build-up of excessive exuberance in the credit cycle in the first place, potentially containing credit growth to some degree and perhaps thereby helping to moderate swings in asset prices and/or the economy. However, this potential moderating effect is not the primary objective envisaged for the CCyB.

2.2 The CCyB as an extension of the capital conservation buffer

2.2.1 The CCyB is an additional “layer” of Common Equity Tier 1 (CET1) capital which takes effect as an extension of the Basel III capital conservation buffer (CB) (see BCR §[…]).

Like the CB requirement, the CCyB requirement is expressed as a percentage of an AI’s total risk-weighted amount (RWA). An AI’s CET1 capital must first be used to meet all of its minimum capital requirements (including any Pillar 2 (BO §97F) add-on), before the remainder can contribute to the extended buffer range (see BCR §[…]).

This is illustrated in the “capital stack” below (assuming full phase-in of Basel III minimum ratios and buffers and that the AI is not designated as a G-SIB or D-SIB and hence not subject to any additional Higher Loss Absorbency capital requirement generally associated with such designation):

Countercyclical Capital Buffer (0% → 2.5% of RWA) Capital Conservation Buffer (2.5% of RWA)

Pillar 2 CET1 capital ratio add-on (if any) Minimum CET1 capital ratio (4.5% of RWA)

Buffer capital

Minimum regulatory capital

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

2.2.2 As an extension of the CB, the CCyB is not regarded as a

“hard” minimum capital requirement. If an AI’s CET1 capital ratio falls within the CB buffer zone (as extended by the CCyB when applicable) restrictions will be imposed on discretionary profit distributions (see BCR

§[…]).

2.3 AI-specific CCyB rates

2.3.1 An AI’s “AI-specific CCyB rate” is essentially the rate (expressed as a percentage of the AI’s RWA) by which the AI’s CB is extended by CCyB requirements applicable to the AI.3

2.3.2 An AI must determine its own AI-specific CCyB rate as the weighted average of the applicable jurisdictional CCyB rates (see Sub-section 2.4 below), effective at the date for which the determination is made, in respect of the jurisdictions (including Hong Kong) where the AI has private sector credit exposures. 4 The weight to be attributed to a given jurisdiction’s applicable CCyB rate is the ratio of the AI’s aggregate RWAj for its private sector credit risk exposures (in both the banking book and the trading book) in that jurisdiction5 to the sum of such aggregate RWAj across all jurisdictions in which the AI has private sector credit risk exposure.6 (See BCR §[…]).

2.4 Jurisdictional CCyB rates

2.4.1 The applicable jurisdictional CCyB rate. The jurisdictional CCyB rate is the CCyB rate in respect of a particular jurisdiction, including Hong Kong, (expressed as a ratio of Common Equity Tier 1 capital to risk- weighted assets as defined in the relevant regulatory

3 This corresponds to the “CCyB ratio” as defined in BCR §[…].

4 As defined in BCR §[…], “private sector credit exposures” exclude exposures to banks regardless of whether the latter are under public sector or private sector ownership.

5 See [SPM being drafted, which will be issued for industry consultation in due course] for further details on the determination of the jurisdictional allocation of private sector credit exposures.

6 This sum can be larger than the AI’s total private sector credit RWA to the extent that the latter may

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

standards applicable in that jurisdiction) which is in effect at the date for which an AI is calculating its AI-specific CCyB rate (see BCR §[…]). However, the applicable jurisdictional CCyB rate for the purposes of calculating an AI’s AI-specific CCyB rate (see para. 2.3.2 above) may differ from the jurisdictional CCyB rate if the MA has determined and announced the application of a higher or lower rate (in respect of a given jurisdiction outside Hong Kong) in the circumstances described in Section 4 below (see BCR §[…]).

The Hong Kong jurisdictional CCyB rate. The MA’s approach to determining and announcing the Hong Kong jurisdictional CCyB rate is described in Section 3 below.

Applicable jurisdictional CCyB rates for other jurisdictions. The MA’s approach to recognising jurisdictional CCyB rates for other jurisdictions is described in Section 4 below.

2.4.2 Pre-announcement periods. A different treatment applies to increases and decreases of jurisdictional CCyB rates in respect of the time period (“pre-announcement period”) between their announcement and their coming into effect (see BCR §[…]):

CCyB rate increases: The pre-announcement period for an increase (including an increase above 0% - i.e.

buffer activation) in the Hong Kong jurisdictional CCyB rate will usually be 12 months, unless the MA announces a shorter period of not less than 6 months (see para. 3.5.4 below for a description of the circumstances which might lead the MA to adopt a such a shorter pre-announcement period).

Similarly, unless otherwise determined by the MA in the circumstances described in Sub-section 4.3 below, an increase in another jurisdiction’s applicable jurisdictional CCyB rate (including from zero or when first activated) will become effective in respect of AIs in accordance with the pre-announcement period set by the relevant authority in that jurisdiction (in other words, the “applicable” jurisdictional CCyB rate will

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

follow the timing of the underlying jurisdictional CCyB rate), but:

(a) if the pre-announcement period is less than 6 months, AIs may instead adopt 6 months; or (b) if the pre-announcement period is more than 12

months, AIs must instead adopt 12 months.

CCyB rate decreases: A decrease in the Hong Kong jurisdictional CCyB rate will become effective immediately upon being announced. A decrease in another jurisdiction’s applicable jurisdictional CCyB rate will become effective in respect of AIs as announced by the relevant authority in that jurisdiction, unless the MA determines a different effective date in respect of AIs in the circumstances described in Sub-section 4.3 below.

2.5 Reporting and disclosure requirements

2.5.1 Quarterly reporting to the MA. An AI is required to report to the MA its AI-specific CCyB rate and related information on a quarterly basis through Return MA(BS)3

“Capital Adequacy Ratio of an Authorized Institution Incorporated in Hong Kong” [to be modified to incorporate CCyB-related information]. The quarterly report covers both point-in-time and forward-looking information as discussed below:

Point-in-time information. This refers to data as of the report’s quarter-end date and includes the following items:

The AI-specific CCyB rate calculated on the basis of the latest applicable jurisdictional CCyB rates in effect at the quarter-end date (see para. 2.3.2 above).

The RWAj for private sector credit exposures as of the quarter-end date, corresponding to each jurisdiction in which the AI has private sector credit exposure, used in the above calculation.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

The applicable jurisdictional CCyB rates, in respect of each jurisdiction in which the AI has private sector credit exposure, used in the above calculation.

Forward-looking information. This refers to information as of the end of each of the subsequent four quarters following the report’s quarter-end date and includes:

The AI-specific CCyB rate calculated on the basis of (i) any applicable jurisdictional CCyB rates that are currently in effect or preannounced and are expected to be in effect on any of the subsequent four quarter- end dates (including for Hong Kong and for other jurisdictions), and (ii) the same risk-weighted amounts used for the calculation of the point-in-time AI-specific CCyB rate as of the report’s quarter-end date (as described above).

The jurisdictional CCyB rates in respect of each jurisdiction in which the AI has private sector credit exposure, which have been used in the above calculation (i.e. incorporating any expected pre- announced changes).

2.5.2 Half-yearly public disclosure. As set out in BDR §§24B and 45B, AIs are required to publicly disclose, the following information as part of their twice yearly Pillar 3 disclosure in the “Capital Disclosures Template”:

Their AI-specific CCyB rate calculated on the basis of the latest applicable jurisdictional CCyB rates in effect at the half-year-end date (see paras. 2.3.1 and 2.3.2 above).

The RWAj as of the half-year-end date, corresponding to each jurisdiction in which the AI has private sector credit exposure, used in the above calculation.

The applicable jurisdictional CCyB rates, in respect of each jurisdiction in which the AI has private sector credit exposure, used in the above calculation.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

3. The MA’s approach to determining and announcing the Hong Kong jurisdictional CCyB rate

This section describes the MA’s approach to determining the level of the Hong Kong jurisdictional CCyB rate and the timing of its activation, increase, decrease or release. The approach takes as its starting point an “Initial Reference Calculator” that is transparently calculated and made public. The decision process then builds upon the Initial Reference Calculator by incorporating the analysis of information from a broader set of “Comprehensive Reference Indicators” and other appropriate sources. The final policy decision is then taken on the basis of informed judgement and will be publicly communicated, with a reasoned justification when the decision departs from the guide provided by the Initial Reference Calculator in either a “tightening” or

“loosening” direction.

3.1 The steps in the decision process

3.1.1 Main issues in CCyB decisions. As noted in Sub- section 2.1 above, the primary objective of the CCyB is to make the banking sector more resilient against system- wide risk associated with excessive aggregate credit growth. Given this objective, decisions on whether to activate, increase, decrease or release the Hong Kong jurisdictional CCyB rate hinge on an assessment of: (i) the extent to which any aggregate credit growth in Hong Kong may be deemed excessive (and thus suggest CCyB build-up); (ii) the risks that may be building up across the banking system – because of credit growth and/or other factors; (iii) the fragility of the Hong Kong banking system vis à vis such risks; and (iv) the degree to which an excessive credit contraction may be underway or is likely imminent (and thus suggest CCyB relase).

3.1.2 Ongoing systemic risk monitoring: the MA’s systemic

“dashboard”. Making adequate and timely decisions on the CCyB (and indeed on the deployment of other macroprudential policy instruments) presupposes an ongoing monitoring and analysis of relevant current and forward-looking information on the state of, and trends in, the banking system that may bear on issues such as those mentioned in para. 3.1.1 above. The MA’s

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

approach in this regard is to regularly monitor and analyse the following:

The “Basel Common Reference Guide”. To provide a common starting point across jurisdictions, the Basel Committee expects national authorities to calculate, regularly disclose and consider in their CCyB decisions, a non-binding common reference guide based on a methodology that measures the

“credit/GDP gap” (i.e. the extent to which the aggregate private sector credit/GDP ratio exceeds its long term trend). In line with the Basel Committee guidance, the MA will calculate and publish the Basel Common Reference Guide on a quarterly basis as set out in paras. 3.2.2 and 3.6.1 below and in Annex 1. However, as the Basel Committee has noted, although this guide can help signal the need for CCyB build-up, it is likely to be too slow for timely signalling of the need for CCyB release. The MA will consider the Basel Common Reference Guide in its CCyB decisions but it will only be one of the MA’s reference points.

The Initial Reference Calculator. The MA has developed for Hong Kong a methodology, referred to as the Initial Reference Calculator, based on which the MA will calculate and publish, on a quarterly basis, an indicative CCyB rate guide by combining the credit/GDP gap driving the Basel Common Reference Guide with additional indicators on local property prices and rents, the interbank risk spread and average loan quality (see further details in Sub- section 3.2 and para. 3.6.1 below and in Annexes 2 and 3). In contrast to the Basel Common Reference Guide, the Initial Reference Calculator provides a guide for both the build-up of the CCyB and the timely (partial or full) release of the CCyB in the presence of early signs of banking system stress.

The MA will use the Initial Reference Calculator as a starting point for CCyB decisions. The MA will monitor (on an ongoing basis depending on each indicator’s frequency of update):

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

- the current readings and (if available) forecasted short-term path of each of the four indicators ((i) credit/GDP gap, (ii) property price/rent gap, (iii) interbank rate spread and (iv) loan quality) used as inputs for the Initial Reference Calculator;

- the resulting Initial Reference Calculator’s CCyB rate guide and its components (see Sub-section 3.2 below) based on current and forecasted inputs, with and without applying the caps on buffer guides, is discussed in para. 3.2.4 below.

A set of Comprehensive Reference Indicators. The MA will also monitor and analyse on an ongoing basis a broader set of indicators that can help the MA to develop a more complete view of systemic risk by covering risk factors that may not be adequately captured by the Basel Common Reference Guide and the Initial Reference Calculator (see Sub-section 3.3 below for details).

Other relevant information and analyses. Finally, the MA will consider in its CCyB decisions any other information, be it of a quantitative or qualitative nature, that may come to light or be available at the relevant time and that may be relevant in the context of the MA’s mandate of promoting the general stability and effective working of the banking system.

Such information may be obtained through the MA’s ongoing monitoring of events at the local, regional and global level that may carry implications for banking system risk in Hong Kong. It may also derive from focused studies or analyses of particular issues (including the assessment of potential improvements in the Initial Reference Calculator and/or in the set of Comprehensive Reference Indicators).

3.1.3 Determining the “macroprudential policy stance”.

Based on the analysis of the available information as described in para. 3.1.2 above, and before considering a decision on the Hong Kong jurisdictional CCyB rate, the MA will first focus on deciding whether the broad systemic picture – including not only the current situation but also foreseeable short- to medium-term trends –

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

suggests that the appropriate macroprudential policy stance, relative to that indicated by the Initial Reference Calculator, should be “neutral”, “tightening” or

“loosening”. Given the quarterly calculation and publication of the Basel Common Reference Guide and of the Initial Reference Calculator, the MA will review its macroprudential policy stance on at least a quarterly basis (see further discussion in Sub-section 3.4 below).

3.1.4 Deciding on the Hong Kong jurisdictional CCyB rate.

Once a macroprudential policy stance has been determined, the MA will consider and assess the available policy options (including possible combinations of CCyB rate levels with other complementary or alternative macroprudential policy instruments designed to bolster the resilience of the banking sector). Before reaching a decision, the MA may also consult any other parties as the MA may deem appropriate in order to arrive at an informed judgement based on all relevant information (see further discussion in Sub-section 3.5 below).

The public announcement of the decision will include a reasoned justification where there is any divergence from the Initial Reference Calculator (see Sub-section 3.6 below).

3.1.5 Performance review. The MA intends to undertake periodic reviews of the performance of the Initial Reference Calculator, and of the CCyB decision making process more broadly, with a view to enhancing them wherever deemed appropriate. Accordingly, this module may be updated from time to time following the usual consultation.

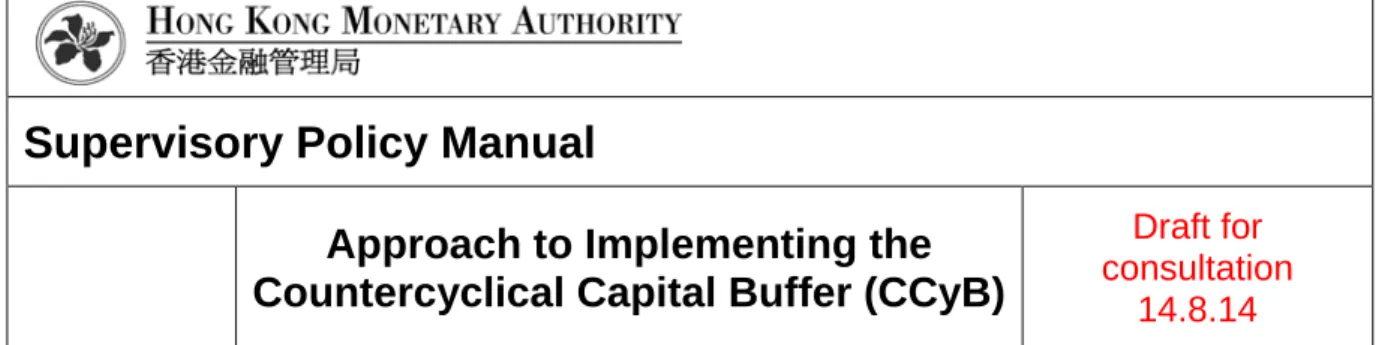

3.2 The MA’s Initial Reference Calculator

3.2.1 Determination of the Initial Reference Calculator’s CCyB rate guide. The Initial Reference Calculator produces quarterly an initial guide between 0% and 2.5%

of total RWA (subject to the phase-in schedule discussed in para. 3.2.4 below) for the level of the Hong Kong jurisdictional CCyB rate. The Initial Reference Calculator’s CCyB rate guide will be the lower of the

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

components of the Initial Reference Calculator (see Diagram 1):

A Composite CCyB Guide based on two “primary gap indicators”: a credit/GDP gap and a property price/rent gap (see details in para. 3.2.2 below). This guide would signal the activation of the Hong Kong CCyB and subsequent changes in its rate in response to increasing or decreasing signs of excessive credit growth and/or property prices.

An Indicative CCyB Ceiling based on two “primary stress indicators”: an interbank risk spread and a loan quality indicator (see details in para. 3.2.3 below). These indicators can provide an early signal of significant stress in the banking system that could lead to excessive credit constraint if the CCyB is not released in a timely manner. In the presence of such a signal, the Indicative CCyB Ceiling could become

“binding” within the Initial Reference Calculator and indicate a buffer reduction (including the possibility of a full release).

In the absence of significant systemic stress, as and when the “credit boom” gradually deflates, the Composite CCyB Guide” should signal a gradual reduction of the CCyB rate. Since the Initial Reference Calculator selects the lower of the Composite CCyB Guide and the Indicative CCyB Ceiling, it may happen that, if the primary gap indicators driving the Composite CCyB Guide were to decrease to sufficiently low levels, they could cause the Initial Reference Calculator guide to drop even below the level that would result from the application of the Indicative CCyB Ceiling.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

Diagram 1: The Initial Reference Calculator (IRC)

Initial Reference Calculator

Composite CCyB Guide

Indicative CCyB Ceiling

Interbank Risk Spread

Loan Quality Indicator Basel Common

Reference Guide

Property Buffer Guide

Credit/GDP Gap

Property Price/Rent Gap

Primary Stress Indicators Primary Gap Indicators

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

3.2.2 Composite CCyB Guide based on primary gap indicators. The Basel Committee in its “Guidance for national authorities operating the countercyclical capital buffer” and related studies published by the Bank for International Settlements (BIS) present cross-country evidence supporting both the use of the credit/GDP gap as a predictor of banking crises and the Basel III calibration of the Basel Common Reference Guide for signalling an indicative buffer level, driven by the credit/GDP gap (see Box 1).7 Other empirical research by BIS staff based on global data 8 shows that the combination of sustained rapid credit growth and large increases in asset prices appears to heighten the probability of an episode of financial instability. Finally, the MA’s own analysis of local Hong Kong data suggest that combining information on property market valuation with the credit/GDP gap can improve predictive power in terms of identifying “excessive” credit growth in Hong Kong and reducing the “signal-to-noise” ratio 9 in comparison to relying on the credit/GDP gap alone.10

The MA will calculate an indicative “Composite CCyB Guide” based on the two primary gap indicators identified (namely the credit/GDP gap and the property price/rent gap). This Composite CCyB Guide will thus combine information on the degree to which both credit growth and property market valuations are deviating from their respective long-term trends, reflecting the greater

7 See e.g. M. Drehmann, C. Borio, and K. Tsatsaronis, “Anchoring Countercyclical Capital Buffers: The Role of Credit Aggregates”, BIS Working Papers No. 355, November 2011 and A.M. Taylor, “The Great Leveraging”, BIS Working Papers No. 398, December 2012.

8 See C. Borio and P. Lowe, “Asset prices, financial and monetary stability: exploring the nexus”, BIS Working Papers No. 114, July 2002.

9 The “signal to noise” ratio in this context is the ratio of the number of episodes of banking system stress due to credit losses correctly predicted by the indicator(s) to the number of false warnings of such episodes provided by the same indicator(s) over a sample period.

10 Although endeavours have been made to test the relevance of other indicators, given the absence of systemic banking crises and the scarcity of banking system stress episodes in Hong Kong in the past few decades, local historical data have proved insufficient to enable any robust statistical identification of indicators that are significantly better suited for Hong Kong than those that have been proven to possess strong predictive power by reference to global data.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

significance of the joint occurrence of large credit/GDP and property price/rent gaps in signalling the build-up of systemic risk as compared with the credit/GDP gap alone.

The Composite CCyB Guide will be calculated as 1.1 times the simple geometric mean of the following two buffer guides:11

The Basel Common Reference Guide. The MA will calculate the Basel Common Reference Guide (with a maximum resulting CCyB level of 2.5% of RWA) in accordance with the methodology devised by the Basel Committee for both calculating the credit/GDP gap and mapping that credit/GDP gap into an indicative jurisdictional CCyB rate guide (see summary in Box 1). The measure of credit to be used in the calculation of the credit/GDP gap for Hong Kong is the stock of total loans and advances outstanding at the Hong Offices of AIs as reported in the MA’s Monthly Statistical Bulletin, excluding “other loans for use outside Hong Kong”, as at the end of the quarter corresponding to the (annualized) quarterly GDP data point. A more detailed description of the calculation of the Basel Common Reference Guide for Hong Kong is included in Annex 1.

The Property Buffer Guide. The Property Buffer Guide (also with a maximum level of 2.5% of RWA), as described in Box 2, is constructed and will be calculated in a similar manner to the Basel Common Reference Guide but based on the residential property price/rent gap in Hong Kong (i.e. the deviation of the ratio of the residential property price index to the rental index from the ratio’s long-term trend).

11 The 1.1 multiplier roughly recalibrates the statistical distribution of the Composite CCyB Guide back to the Basel Committee expectation, to address the fact that the geometric mean of the two guides, which are not perfectly correlated, will always have a smaller standard deviation than the Basel Common Reference Guide alone.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

Box 1. Basel III: The Credit/GDP Gap and the Basel Common Reference Guide Buffer driver. As a reference point for formulating and explaining buffer decisions, the jurisdictional authority first calculates the Basel Common Reference guide. This involves three steps:

1) calculate the aggregate private sector credit-to-GDP ratio as a percentage;

2) calculate the credit/GDP gap expressed as the difference between the current ratio and its long term trend; and

3) map the credit/GDP gap into the indicative buffer level guide, expressed as a percentage of RWA.

As far as available data allows, aggregate private sector credit is to be measured in the broadest possible terms, from all possible sources, to the domestic non-bank private sector (including non-bank financial sector) in a jurisdiction.

To calculate the trend of the private sector credit/GDP ratio, a one-sided Hodrick-Prescott filter with a high smoothing parameter (λ = 400,000) is to be used.

Buffer level guide. The indicative buffer level guide for the jurisdiction for which the credit/GDP gap has been calculated should be determined as follows:

Credit / GDP gap Indicative Buffer Level Guide Less than 2% (lower threshold) 0%

More than 10% (upper threshold) 2.5%

Between 2% and 10% Level of buffer varies linearly between 0 and 2.5% in proportion to the excess of the credit/GDP gap above the lower threshold of 2%.

(If the 2.5% cap on the buffer level guide is not applied, the same formula can be used to calculate proportionately higher buffer level guides beyond 2.5% as the credit/GDP gap exceeds 10%.)

_______________

Source: Annex 1 of Basel Committee Guidance for national authorities operating the countercyclical capital buffer, December 2010.

See Annex 1 of this module for further details on how the MA will calculate the Basel Common Reference Guide for Hong Kong.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

Box 2 – The Property Price/Rent Gap and the Property Buffer Guide for the CCyB Property price/rent gap. The indices used for computing the residential property price/rent ratio for Hong Kong are the private domestic property price index and the private domestic property rental index produced by the Rating and Valuation Department of the Hong Kong Government. The “property price/rent gap” is defined as the difference between the current price/rent ratio and the long-term trend of this ratio, where the difference is expressed as a percentage of the trend. To calculate the trend of the price/rent ratio, a one-sided Hodrick- Prescott filter with a high smoothing parameter (λ = 400,000) is used.

Property buffer guide. The corresponding Property Buffer Guide is calculated in a similar way to the Basel Common Reference guide (see Box 1), using the same thresholds on the basis that rental adjustment has been observed to be significantly more flexible in Hong Kong than in most other jurisdictions and, as a result, the price/rent ratio time series is not much more volatile than the credit/GDP ratio:

Property Price/Rent Gap Property Buffer Guide Less than 2% (lower threshold) 0%

More than 10% (upper threshold) 2.5%

Between 2% and 10% Buffer level to vary linearly between 0% and 2.5% in proportion to the excess of the property price/rent gap above the lower threshold of 2%.

(If the 2.5% cap on the buffer level guide is not applied, the same formula can be used to calculate proportionately higher buffer level guides beyond 2.5% as the credit/GDP gap exceeds 10%.)

_______________

See Annex 2 for further details.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

However, since property prices have historically tended to peak around 2 years before a crisis across countries12, the MA will be cautious about reducing the Hong Kong jurisdictional CCyB rate when property prices turn downwards while the credit/GDP gap remains large and there are no indications of banking system stress.

A more detailed discussion of the methodology for determining the Property Buffer Guide and the Composite CCyB Guide is included in Annex 2.

3.2.3 Indicative CCyB Ceiling based on primary stress indicators. A key principle underlying the CCyB is that the buffer should be released promptly once significant stress is observed within the banking sector in order to minimise any credit constraint which might amplify the adverse effects of a financial cycle downturn. Swiftly releasing a buffer, which has been accumulated on top of credibly robust “hard” minimum capital requirements, should allow the banking system in aggregate to absorb losses that materialise, or to meet any increase in minimum capital requirements arising as a result of the stress, and thus permit the banking system to continue lending to support the economy.

In contrast to the process for the build-up of the CCyB, the Basel Committee has not provided any common reference guide for triggering the release of the CCyB.

The MA considers that reliance cannot reasonably be placed upon the credit/GDP gap or the property price/rent gap as timely indicators for the release of the CCyB when the banking system encounters significant stress. Both indicators will likely be “lagging” in the sense that they may move down too late for a buffer release to be sufficiently prompt to prevent a credit contraction.

The primary stress indicators. The MA therefore will calculate an “Indicative CCyB Ceiling” to provide an

12 See e.g. the 2011 paper by Drehmann, Borio, and Tsatsaronis cited in footnote 7 above.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

indicative signal for the swift release of the CCyB, based upon two “primary stress indicators” which the MA considers can provide an adequately early warning of potentially significant stress within the banking system:

Interbank risk spread. The risk spread in the reference interbank lending rate reflects the perception, by interbank market participants, of the risk of lending to a prime bank in that market. A significant rise in this spread can be a good early indicator of banking system stress, especially during sudden, acute stress episodes. The MA will use the 3-Month HIBOR 13 spread over the corresponding risk-free rate (measured by the 3-Month Overnight Index Swap rate) as one of the two primary indicators of stress in Hong Kong’s banking system that would drive the Indicative CCyB Ceiling.

Loan quality indicator. The second primary stress indicator aims at providing a measure of the deterioration in loan quality within Hong Kong’s banking system, which should give some early signal of impending credit losses. This indicator is more relevant when systemic risks play out more gradually.

The MA will use the quarter-on-quarter change in the aggregate gross classified loan ratio of retail banks (as published in the “Asset Quality of Retail Banks”

statistical table in the MA’s Monthly Statistical Bulletin) for this purpose.

The Indicative CCyB Ceiling. Based on the schedule described in Table 1 below, the two primary stress indicators are used to set an indicative ceiling for the CCyB rate if they exceed their respective thresholds. As

13 The HIBOR (Hong Kong Interbank Offered Rates) are the rates of interest for Hong Kong Dollar deposits for the relevant period calculated by The Hong Kong Association of Banks (HKAB) each day and displayed on the website of HKAB. The fixings are made on the basis of quotations provided by currently 20 banks designated by HKAB as reference banks and are available for HKD deposit maturity ranging between overnight deposits and 12 months. The fixings are determined by averaging the middle quotes after excluding the highest three quotes and lowest three quotes received from the reference banks. (Source: HKAB website as of 31 July 2014.)

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

noted in para. 3.2.1 above, if the ceiling turns out to be lower than the buffer level indicated by the Composite CCyB Guide, then the Initial Reference Calculator will be lowered, thus signalling that any extant CCyB should (absent any tightening macroprudential policy stance resulting from consideration of countervailing information from the Comprehensive Reference Indicators or other sources) be partially or fully released (see Annex 3 for a more detailed discussion of the rationale for the Indicative CCyB Ceiling).

The greater the severity of the stress detected by the primary stress indicators, the lower the Indicative CCyB Ceiling. A gradual buffer release would be signalled to the extent that the readings on the primary stress indicators increase gradually as systemic stress worsens over time. But an immediate and full release of the buffer may be signalled if the stress episode has a sudden and strong onset, so that either or both of the primary stress indicators reach or overstep their respective highest threshold (bottom row in Table 1). That said, in order to avoid volatility in ceiling levels due to short-term variations in the HIBOR spread, the latter should stay above the respective threshold for more than 30 days to have any effect on the operation of the Indicative CCyB Ceiling.

Conversely, if both primary stress indicators are below the thresholds shown in the top row of Table 1, then there would be no ceiling (this is not shown in the table).

Frequency of calculation. The “Indicative CCyB Ceiling” in Table 1 will normally be calculated and considered at the time of each quarterly review (see para. 3.1.3 above). But in order to cater for the prospect of economic circumstances deteriorating rapidly, the MA will retain the flexibility to review the primary stress indicators and act earlier, in relation to them, if needed in response to the severity of any stress being experienced by the banking sector.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

Table 1. Primary stress indicators and the Indicative CCyB Ceiling

Primary Stress Indicators

Indicative CCyB Ceiling

Indicative Minimum Ceiling

Duration If either:

the Interbank Risk Spread (3-Month HIBOR

Spread)*

Or:

the Loan Quality Indicator (Quarter-on- Quarter Increase in

Classified Loan Ratio)

> 1.0% > 0.5% ≤ 2.0% 3 Months

> 1.5% > 1.0% ≤ 1.5% 3 Months

> 2.0% > 1.5% ≤ 1.0% 6 Months

> 2.5% > 2.0% ≤ 0.5% 9 Months

> 3.0% > 2.5% 0% 12 Months

* The spread should stay above the respective threshold for more than 30 days for the trigger to operate.

Indicative minimum ceiling duration. Once part or all of the CCyB has been released in response to stress within the banking sector, in line with the Indicative CCyB Ceiling in Table 1, it would be the MA’s general intention that, irrespective of any subsequent upswing in the Composite CCyB Guide or the Indicative CCyB Ceiling, no decisions to activate or increase the CCyB above the last Indicative CCyB Ceiling would then be made within a certain minimum period of time, i.e. there will be an “indicative minimum ceiling duration”. This is to give AIs a degree of comfort that the effect of a buffer release will not be cancelled in short order by a swift subsequent build-up, so as not to hinder the intended effect of buffer release in terms of maintaining lending in times of stress. To help the industry form at least some expectation in this regard,

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

an indicative minimum ceiling duration associated with each level of the Indicative CCyB Ceiling is included in the fourth column of Table 1. The indicative minimum ceiling duration in turn influences the future path of the Initial Reference Calculator so that there will be a general expectation that, the lower the Indicative CCyB Ceiling, the longer (up to a maximum of 12 months) would be its effect on the Initial Reference Calculator in signalling no subsequent CCyB increase above that ceiling.

Flexibility with respect to the indicative minimum ceiling duration. Whilst the indicative minimum ceiling duration is, as its name suggests, “indicative” of general intention, it will not be strictly “binding” on the MA. So the MA could take a decision to diverge from the Initial Reference Calculator (see Sub-section 3.5 below), if there were extraordinary unforeseen circumstances where the preservation of financial stability may require renewed buffer build-up at an earlier point in time. (This may, for example, be the case where a sudden wave of capital inflows sharply reverses a phase of credit contraction and threatens to overheat the economy and/or generate asset price bubbles.)

3.2.4. Cap on buffer Guides and phase-in. Once the Basel III regulatory capital standard is fully phased-in, the indicative CCyB rate guides resulting from the Basel Common Reference Guide, from the Property Buffer Guide and from the Composite CCyB Guide will be capped at 2.5% of RWA. In accordance with the Basel Committee schedule, this cap on the CCyB rate guides will be phased-in in parallel with the CB as follows (see BCR §[…]):

1 Jan. 2016 1. Jan. 2017 1. Jan. 2018 1. Jan. 2019

0.625% 1.25% 1.875% 2.5%

3.2.5. Expression of the CCyB rate guides in multiples of 25 basis points. The CCyB rate will be expressed in

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

multiples of 25 basis points (without rounding up). Thus activation of the Hong Kong jurisdictional CCyB would be signalled by the Initial Reference Calculator’s CCyB rate guide (as drawn from the Composite CCyB Guide but subject as discussed in para. 3.2.3 above to the operation of an Indicative CCyB Ceiling) moving from zero to a positive level of at least 25 basis points.

Similarly, the Initial Reference Calculator would signal an extant CCyB to increase or decrease in multiplies of 25 basis points as driven by the expansions and contractions of the two primary gap indicators as synthesised into the Composite CCyB Guide, unless the CCyB is released (partially or in its entirety) in response to significant stress within the banking sector “triggering” the operation of the Indicative CCyB Ceiling as discussed in para. 3.2.3 above.

3.3. The Comprehensive Reference Indicators

3.3.1. The Comprehensive Reference Indicators which the MA will monitor on an ongoing basis (see para. 3.1.2 above) include a broad set of aggregate indicators of systemic conditions covering items as illustrated in Table 2 below, as far as data is available.

3.3.2. The indicators included in Table 2 and their suggested interpretation should be regarded as illustrative and not exhaustive or restrictive. The appropriate set of Comprehensive Reference Indicators may evolve over time, as further data is collected or the relevance of the indicators is reassessed based on experience. Hence, rather than fix definitely the set of Comprehensive Reference Indicators to be reviewed, the MA will make the current list available on its website.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

Table 2. Illustrative list of Comprehensive Reference Indicators Tending to support – Tightening bias? Loosening bias?

Aggregate / average banking indicators

Credit growth (total / sectoral) Fast/ Accelerating Slow / Negative Bank leverage

(Basel III Leverage Ratio, CET1 / RWA)

High / Rising Low Bank maturity mismatch

(Net Stable Funding Ratio, core funding ratio, loan / deposit ratio)

Large / Increasing Small

Currency mismatch (net FX position / equity) Large / Increasing Small Average risk weight (total and IRB) Low / Falling High / Rising Liquidity (LCR, LMR, other Basel III metrics)

Profitability (ROA, ROE) Hong Kong property sector

Property price growth Fast/Accelerating Slow/Negative

(Real) mortgage interest rate Low High

Average DSR Rising from low

base

Decreasing from high base

Average LTV ratio High / Rising Low

Commercial property price / rent ratios High / Rising Low Non-financial sector leverage

Household debt / GDP ratio High / Rising Low

Financial leverage of listed local corporations (debt / equity, debt / EBITDA14)

High / Rising Low

Imputed private sector DSR15 High / Rising Low

Macroeconomic imbalances

Current account deficit / GDP High / Rising Low / Surplus Gross or net external liabilities / GDP High / Rising Low

Fiscal deficit / GDP High / Rising Low / Surplus

External factors (indirect impact on HK economy) Credit / GDP gap in globally / regionally

important economies

High / Rising Low Property valuation indicators (price / rent, price /

income, average LTV ratios, etc.) in globally / regionally important economies

High / Rising Low

14 Earnings before interest, taxes, depreciation and amortization.

15 E.g. as defined in M. Drehmann and M. Juselius, “Do debt service costs affect macroeconomic and financial stability?” BIS Quarterly Review, September 2012.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

3.4. Determining the macroprudential policy stance

3.4.1. Macro-prudential analysis. The MA will determine, based on the broad systemic picture – including not only the current situation but also foreseeable short- to medium- term trends – provided by the analysis of the available information, whether its macroprudential policy stance should be, broadly speaking, characterized as “neutral”,

“tightening” or “loosening” relative to the signal generated by the Initial Reference Calculator:

“neutral”, meaning that no reasons have been identified to justify a deviation from the Initial Reference Calculator;

“tightening”, meaning that there may be justification for electing to implement a higher CCyB rate than that otherwise signalled by the Initial Reference Calculator where the MA considers that, in the prevailing circumstances, such a course of action is appropriate for the purposes of bolstering or securing banking sector stability; or

“loosening”, meaning that there may be justification for electing to implement a lower CCyB rate than that otherwise signalled by the Initial Reference Calculator or, indeed no buffer at all, despite the Initial Reference Calculator indicating a rate above 0%, where the MA considers that the prevailing circumstances are such that this course of action is appropriate for the purposes of mitigating anticipated adverse effects of banking system stress on the banking sector (including where any resulting contractionary effects on credit supply might threaten the health of the real economy).

3.4.2. Interpreting the Comprehensive Reference Indicators. In the context of the macroprudential analysis, the Comprehensive Reference Indicators will need to be interpreted (and selected) in terms of the light that they may shed on:

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

the build-up of latent systemic risk within the banking system and the economy more broadly (tending towards supporting buffer activation and buffer build- up), e.g.: credit growth; leverage in the balance sheets of banks and nonbanks in collateralized lending, in derivatives, etc.; liquidity, maturity and currency mismatches, levels of interest rate risk and exchange rate risk within banks and nonbanks; asset valuation gaps; and macroeconomic imbalances;

the prospects for significant deleveraging by the banking sector due to crystallizing systemic risk (tending towards supporting buffer release), e.g.:

rising delinquencies, loan loss provisions, asset impairments, model-based risk weights and banking sector losses; as well as any corresponding credit slowdown or contraction; and

loss of liquidity or other stresses in the financial markets due to heightened uncertainties about counterparty solvency (limiting the scope for counteracting deleveraging through buffer release), e.g.: spiking risk spreads, collapsing “market- allowed” leverage (e.g. rising haircuts or margins on collateral) and/or funding outflows.

3.4.3. Mapping the indicators to a policy stance. Table 2 suggests some possible links between the Comprehensive Reference Indicators and the policy stance. However, the interpretation of the different indicators will vary depending on the phase of the credit cycle and other specific circumstances – including how other indicators in the set behave. Hence, it is not possible to establish in any reliable way an unambiguous link between an indicator and an appropriate macroprudential policy stance, and therefore any analysis supporting policy recommendations will necessarily involve the use of judgement. Annex 5 provides an illustration of how the indicators may suggest a macroprudential policy stance depending on the phase of the credit cycle.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

In both phases of the credit cycle, the “default setting” will be a neutral stance (i.e. of following the signal provided by the Initial Reference Calculator) unless strong evidence across the set of indicators, in the direction of either tightening or loosening, suggests otherwise.

The decision on the appropriate macroprudential policy stance will also be based on a consideration of the comparative risks attached to erring on one side or the other.

3.5. Deciding on the Hong Kong jurisdictional CCyB rate

3.5.1. Guided discretion. As discussed above, whilst the Initial Reference Calculator is intended to provide a degree of guidance to the MA and to the market, the MA will retain discretion to diverge from the Initial Reference Calculator if the MA considers that there is strong evidence to support an alternative course of action for the purpose of mitigating systemic risk or instability within the banking system in Hong Kong. In other words, discretion will be retained to cater for volatile, fast moving and hitherto unforeseen circumstances affecting the local economy, as well as any potential for the quantitative indicators incorporated within the Initial Reference Calculator to miss important systemic risk factors.

3.5.2. Preliminary considerations. Once a macro-prudential policy stance has been adopted, the MA will consider:

whether evidence in support of a “tightening” or

“loosening” stance is sufficiently strong as to warrant divergence from the Initial Reference Calculator (by determining a different course of action with regard to the activation, increase, decrease or release of the CCyB in Hong Kong);

what additional tools (if any) could or should appropriately be deployed to support or complement the effects of the CCyB (see para. 3.5.6 below); and

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

whether, given the circumstances, the MA should elect not to take any action but to wait until a subsequent date upon which updated information can be reviewed to decide whether action is warranted.16

3.5.3. Decision when adopting a “neutral” macroprudential policy stance. If a “neutral” macroprudential policy stance is adopted, then the CCyB decision will be in line with the policy signalled by the Initial Reference Calculator as noted in para. 3.2.1 above.

3.5.4. Decisions when adopting a “tightening” policy stance. If a “tightening” macroprudential policy stance is adopted:

Case where the Initial Reference Calculator does not signal an Indicative CCyB Ceiling. In a situation where the Initial Reference Calculator signals excessive credit growth indicating either the activation of the CCyB or a change in the level of the CCyB rate in accordance with the Composite CCyB Guide based on the “primary gap indicators”, a

“tightening” stance may warrant:

- a higher CCyB rate level (and thus a faster build-up or slower decrease), relative to the indicative level signalled by the Initial Reference Calculator17 (see below the criteria for setting a CCyB rate higher than 2.5% in extraordinary circumstances); and/or

16 In so far as they may help obtain a more complete or accurate view of relevant circumstances, the above considerations and related discussions could also lead to a revision of the previously determined macroprudential policy stance.

17 This includes the case where, as set out in BCR §[…], the MA may, following consultation with the Banking Advisory Committee, the Deposit-taking Companies Advisory Committee, The Hong Kong Association of Banks and The DTC Association, accelerate the phase-in of the Hong Kong jurisdictional CCyB rate relative to the schedule shown in para. 3.2.4 above if the MA reasonably considers that such action is warranted by the extent of any excessive credit growth in Hong Kong during the phase-in period and the MA is satisfied that such variation would have the effect of increasing authorized institutions' resilience to the risks arising from such excessive credit growth.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

- a pre-announcement period for the CCyB rate increase shorter than 12 months (but not shorter than 6 months).

Setting a CCyB rate higher than 2.5% in extraordinary circumstances. As set out in BCR §[…], the MA may, following consultation with the Banking Advisory Committee, the Deposit-taking Companies Advisory Committee, The Hong Kong Association of Banks and The DTC Association, set the Hong Kong jurisdictional CCyB rate at a level in excess of 2.5% if (i) a Hong Kong jurisdictional CCyB rate at a level of 2.5% has been in effect for a period of not less than 6 months; (ii) the MA is satisfied on reasonable grounds that the pace of credit growth has not slowed to any material extent during that period; and (iii) the MA considers it necessary to set a Hong Kong jurisdictional CCyB ratio in excess of 2.5% to protect AIs from the expected consequences of excessive credit growth and the build-up of system- wide risk in Hong Kong. Without limiting the discretion provided by BCR §[…], the MA intends to use the following guidelines in determining whether conditions (ii) and (iii) above are fulfilled, before considering whether the use of that discretion is necessary:

- The quarterly year-on-year rate of growth of the aggregate credit measure18 used to calculate the credit/GDP gap (see Annex 1) has not decreased by more than [20%] percent of the year-on-year growth rate as of the quarter-end date immediately before the 2.5% Hong Kong jurisdictional CCyB rate came into effect;

18 The quarterly year-on-year growth rate of the credit measure is the rate of change expressed as a percentage relative to the value of the credit measure as of the end of the corresponding quarter of the previous year.

Supervisory Policy Manual

Approach to Implementing the Countercyclical Capital Buffer (CCyB)

Draft for consultation

14.8.14

- The uncapped19 Basel Common Reference Guide and the uncapped Property Buffer Guide (see para.

3.2.2 above) both indicate a CCyB rate higher than 3.5% or either of them indicates a CCyB rate higher than 4.5%, after both have been above 2.5% for at least 6 months since a 2.5% Hong Kong jurisdictional CCyB rate last became effective; and

- The Comprehensive Reference Indicators unambiguously confirm the picture provided by the Guides and the need to additionally bolster AIs’

resilience for the purpose of protecting AIs and the Hong Kong banking system from the expected consequences of excessive credit growth and the build-up of system-wide risk in Hong Kong. In this context, the MA will consider the pace of aggregate credit growth to be excessive if the quarterly year- on-year rate of growth of the aggregate credit measure used to calculate the credit/GDP gap still exceeds [15%].

Case where the Initial Reference Calculator signals an Indicative CCyB Ceiling. In a situation where the Initial Reference Calculator signals banking system stress indicating the reduction or release of the buffer through an Indicative CCyB Ceiling based on the

“primary stress indicators” (see Table 2), a

“tightening” stance may warrant:

- a slower buffer release through a higher CCyB ceiling relative to that indicated by Table 2; or

- a shorter minimum ceiling duration relative to that indicated by Table 2, if there were extraordinary unforeseen circumstances where the preservation of financial stability might require renewed buffer build-up at an earlier point in time; or

19 The “uncapped” Guides referred to here are the Guides calculated using the respective formula that maps the corresponding primary gap indicators to the resulting CCyB rate guide, but without subjecting the latter to an upper limit (i.e. 2.5% or its phase-in value during 2016 to 2019).