期末報告

負債導向基金之資產配置,績效歸因與違約風險

計 畫 類 別 : 個別型計畫 計 畫 編 號 : MOST 102-2410-H-004-052- 執 行 期 間 : 102 年 08 月 01 日至 103 年 10 月 31 日 執 行 單 位 : 國立政治大學風險管理與保險學系 計 畫 主 持 人 : 張士傑 計畫參與人員: 碩士班研究生-兼任助理人員:劉柔妍 碩士班研究生-兼任助理人員:林佳儀 報 告 附 件 : 出席國際會議研究心得報告及發表論文 處 理 方 式 : 1.公開資訊:本計畫涉及專利或其他智慧財產權,2 年後可公開查詢 2.「本研究」是否已有嚴重損及公共利益之發現:否 3.「本報告」是否建議提供政府單位施政參考:否中 華 民 國 103 年 12 月 04 日

交叉補貼之情形。因此,如何計算公平合理之風險差別費 率,以避免產生影響保險公司正常經營之系統風險,降低保 險公司道德風險,為本文研究之主要議題。 依蒙地卡羅模擬法試算保險安定基金公平費率,研究結 果發現:(1)監理寬容期限增加時,安定基金公平費率增加; (2)監理標準提高,安定基金公平費率有先降後升之效果; (3)保險公司財務槓桿比例增加時,安定基金公平費率上升。 中文關鍵詞: 安定基金、風險保費

英 文 摘 要 : Life insurance companies are highly leveraged

financial institutions whose liabilities are formed by the policyholders` premiums that render the institutions responsible for meeting the claim obligations over a lengthy coverage period. The insurers have to pay their annual premium according to the risks across the entire organization.

Therefore, how to determine the risk-based premium for insurance guaranty fund in order to reduce the moral hazard become vital. In this paper, we derive the closed-form solutions of the risk-based premium charged by the insurance guaranty fund in a setting that incorporates financial leverage, asset

allocation, early closure, and capital forbearance during the grace period.

科技部補助專題研究計畫成果報告

(期末報告)

負債導向基金之資產配置、績效歸因與違約風險

計畫類別:個別型計畫

計畫編號:MOST 102-‐2410-‐H-‐004-‐052

執行期間: 2013/08/01 ~ 2014/10/31

執行機構及系所:國立政治大學風險管理與保險學系

計畫主持人:張士傑

計畫參與人員:劉柔妍、林佳儀

本計畫除繳交成果報告外,另含下列出國報告,共 __1_ 份:

出席國際學術會議心得報告

期末報告處理方式:

1.

公開方式:

非列管計畫亦不具下列情形,立即公開查詢

2.「本研究」是否已有嚴重損及公共利益之發現:否

3.「本報告」是否建議提供政府單位施政參考 否

中 華 民 國 103 年 10 月 31 日

摘要 保險安定基金以保費為基礎徵收單一費率,加 劇保險公司間交叉補貼之情形。因此,如何計 算公平合理之風險差別費率,以避免產生影響 保險公司正常經營之系統風險,降低保險公司 道德風險,為本文研究之主要議題。 依蒙地卡羅模擬法試算保險安定基金公平費 率,研究結果發現:(1)監理寬容期限增加時, 安定基金公平費率增加;(2)監理標準提高,安 定基金公平費率有先降後升之效果;(3)保險公 司財務槓桿比例增加時,安定基金公平費率上 升。關 鍵 字 :安定基金、風險保費 Abstract

Life insurance companies are highly leveraged financial institutions whose liabilities are formed by the policyholders' premiums that render the institutions responsible for meeting the claim obligations over a lengthy coverage period. The insurers have to pay their annual premium according to the risks across the entire organization. Therefore, how to determine the risk-based premium for insurance guaranty fund in order to reduce the moral hazard become vital. In this paper, we derive the closed-form solutions of the risk-based premium charged by the insurance guaranty fund in a setting that incorporates financial leverage, asset allocation, early closure, and capital forbearance during the grace period. Keywords: insurance guaranty fund, risk-based premium

一、 計畫緣由

Life insurance companies are highly leveraged financial institutions whose liabilities are formed by the policyholders' premiums that render the institutions

responsible for meeting the claim obligations over a lengthy coverage period. Therefore, the insurance guaranty fund is established to sustain the insurer’s obligations to policyholders when the insurance company fails. Cummins (1988) points out that the establishment of a guaranty fund means that the costs associated with an insolvent insurer should be spread throughout the insurance system. Taiwan Insurance Guaranty Fund (TIGF) is the insurance guaranty scheme in Taiwan, and the funding approach of the TIGF is flat-premium pre-assessment according to the enacted regulations. However, FSC of Taiwan announced that the risk-based premium of TIGF fund is enforced in 2014. Thus, in this study, we focus on discussing the fair risk-based premium of the ex ante assessment approach based on the current TIGF scheme. Furthermore, we incorporate the regulatory forbearance to fully investigate the influence of the fair premium within the scheme.

The original pricing problem is discussed for deposit insurance schemes. For example, Merton (1977) applies the put option to price the premium of deposit insurance. Then, Ronn and Verma (1986) use the market data to estimate the parameters of Merton’s put option pricing model. Duan and Yu (1994, 1999), Duan et

al. (1995) and Duan and Simonato (2002) perform a series of studies to improve the deposit insurance pricing model, such as considering stochastic interest rates, applying the maximum likelihood estimation to estimate the parameters, and using the GARCH model to describe the bank’s asset return dynamic. Lee et al. (2005) illustrate the influence of capital forbearance on the fair premium of deposit insurance. Hwang et al. (2009) investigate the premium of deposit insurance incorporating the bankruptcy costs and closure policies.

The other line of literature regarding the pricing guaranty fund problem discusses how to measure the fair premium of pension insurance. Sharpe (1976) first discusses the economic premium of the Pension Benefit Guaranty Corporation (PBGC). Marcus (1987) models the PBGC’s liability as a contingent forward. Pennacchi and Lewis (1994) incorporate the stochastic assets and liabilities into the pension insurance pricing model. Chen (2011) derives a closed-form pricing model to determine the risk-based premium for the PBGC and the sponsoring company based on a deterministic risk free rate assumption.

Moving on to the insurance guaranty fund, Cummins (1988) extends the work on deposit insurance premiums to derive the risk-based insurance guaranty fund

premium. Duan and Yu (2005) extend Cummins' one-period model into a multi-period framework. Both conclude that the risk-based premium is necessary, and the impact of some key factors, such as the leverage ratio, is enormous. However, in reality, when the assets of the insurer are below the required capital level but do not fall below the capital standard upon maturity, the regulator will give a grace period to the insurer in its capital restructuring. During this period, the insolvent insurer is allowed to continue its operations. The purpose of regulatory forbearance is to ease the financial distress of those insurers and give them the chance to recover from the financial distress situation. Thus, Yang et al. (2012) apply the deposit insurance premium-pricing model of Lee et al. (2005) to incorporate the capital forbearance mechanism into the insurance guaranty fund pricing problem. They find that the premium with regulatory forbearance is higher than the current premium rate of the TIGF. However, both the studies of Lee et al. (2005) and Yang et al. (2012) are based on the constant interest rate. As the impact of interest rate uncertainty is significant in our study, we (see Hwang et al., 2014 and Chang et al., 2014) extend the model to incorporate the volatility in modeling the stochastic process for the spot rates, and find that the premium is underpriced if the uncertainty

of the interest rate is neglected by the insurance guaranty fund.

二. 計畫目的

In order to fairly price the fair premium the fair premium rate can be expressed as,

charged by an ex ante life insurance guaranty fund (see Chang et al., 2014 for the detailed), the premium should properly reflect the default risk of the life insurance company and also incorporate the uncertainty of the interest rates into our pricing mechanism. This study first incorporates the risk-based concept into the asset allocation of the insurers, the early closure policy, the capital forbearance and the grace period according to the immediate actions of the regulators. Based on the viewpoint of financial options, the early closure can be regarded as a barrier option on the underlying asset whose price is geared toward maintaining the working capital level. The regulatory forbearance during the grace period of the capital injection schedule can be regarded as an option on a put option. Therefore, the premium is summarized as the sum of the values of these proposed options.

Our model and the numerical results illustrate that the volatility of return for the risky asset has a significant impact on the

fair premium. The premium increases with higher volatility. Furthermore, the financial leverage ratio and asset allocation strategy are critical in determining the impact of the volatility of the risky asset on the fair premium. As expected, a higher leverage ratio and a more risky investment strategy will exacerbate the negative influence of the volatility of the risky asset. Finally, the regulation of the forbearance mechanism greatly increases the cost to the insurance guaranty fund of taking over the insolvent life insurers.

三、計畫成果自評

In our study, we discuss the influences on the risk-based premium under different settings of the leverage ratios, asset allocation strategies, the interest rate uncertainty and volatilities of the risky asset. Moreover, we also analyze the effects of the capital forbearance and grace period mechanisms by comparison with Merton's put option cost (Merton, 1977). We demonstrate the sensitivity and signs of partial derivatives of these main parameters ( , , , , , ,

α β ε γ ω ω σ

1 2 r). The results help us to understand that the value of the insurance premium under forbearance varies in response to changes in these main parameters.3.1. The sensitivity of parameter

Several countries apply the risk-based capital (RBC) approach, which is used to

measure the minimum amount of capital that an insurance company needs to support its overall business operations. For example, the RBC ratio is required to exceed 200% according to the current capital regulations in Taiwan. However, the formula for the RBC ratio might not be directly translated to the minimum capital requirement α . We might indirectly adopt the proxy parameters as in the study by Lee et al. (2005) and set α equal to 1.087 and β equal to 0.95 without losing generality. Moreover, we assume that the maintenance ratio, η, is set to be 0.5. In order to compare with the premium of Merton put model, we set γ to be 100%, which means that the insurance guaranty fund has to cover the whole insured liability of the insolvent insurer to its policyholders. According to the current contract setting, the maturity might be assumed to be one year and the grace period (ε) is 6 months, as the insurer has to report the RBC ratio twice a year. The parameters of the financial instruments follow the assumptions of Boulier et al. (2001) and we set the maturity of the rolling bond ( R ) to be 10 years according to the situation of Taiwan’s government bond.

In this paper, we fix the investment proportion of cash as 10% according the financial reports of Taiwan’s life insurers.

In other words, w w1+ 2 =90%. Notice that we also compute the premium under Merton's framework and decompose our insurance guaranty fund premium into three components, which are the early closure component, the capital forbearance component and the grace period component. In order to analyze the cost of the insurance liability, we set L(0) to be 100.

Generally speaking, premium rates under the forbearance consideration are greater than those of Merton's put. For example, the premium under Merton's put is 0.0268 when the debt-to-asset ratio is 100/120 and w is 10%, but the value 1 (0.0981) is over three-fold under the regulatory forbearance. The excess premium can be regarded as the cost of some forbearance. Moreover, the main contribution of the excess premium results from the grace period when the debt-to-asset ratio is below to 1.

Firstly, the premium increases with the debt-to-asset ratio. More specifically, the premiums are 0.3830, 1.5800 and 4.8368 when the debt-to-asset ratios are 100/120, 100/110 and 100/100 under w at 1 40%. A higher leverage ratio reflects a greater risk of deficit between assets and liabilities, and thus the insurance guaranty fund naturally charges a higher premium. Moving on to the asset allocation strategies,

we find that the cost of the insurance guaranty fund rises with the investment proportions of the stock index fund. To be precise, the premium is 4.8368 when w is 1 40% and goes down to 3.7381 when w is 1 10% for a debt-to-asset ratio of 100/100. The reason is similar to the leverage ratio. The portfolio shares ( w ) of the stock 1 index fund increase the risk of financial distress of the life insurer. Then, the guaranty fund has to ask for a higher premium. Furthermore, we present the relationship between the asset allocation and the debt-to-asset ratio. We find that the slope of the solid line (debt-to-asset ratio=100/100) is larger, which suggests that the influence of the risky asset is significant when the leverage ratio is higher.

Subsequently, we illustrate the effects of the volatility of interest rates (

σ

r) in Figure 1. We set the basic scenario as being that w =1 30% , the debt-to-asset ratio = 100/120, 100/110 and 100/100.σ

r is from 0.01 to 0.05, and we find that when the volatility of the interest rate increases, the cost of the ex ante insurance guarantee fund goes up dramatically. For example, the premium is 1.1962 under the basic, but rises to 3.6922 whenσ

r is 5%. This is because the liability is volatile when the volatility of the interest rate goes up, and itincreases the probability of a mismatch of liability and asset. The results show the underpricing problem of insurance guaranty funds when they omit the uncertainty of interest rates.

Figure 1. Relationship between σr

and debt-to-asset ratio.

Figure 2 present the influence of the volatility of the risky asset return (σ1 and

2

σ

). We find that the premium of the insurance guaranty fund increases when the risky asset is more volatile. These numerical results show that the premium of the insurance guaranty fund should be adjusted according to the asset allocation strategy of the insurer.Figure 2. Relationship between σ1 and σ2.

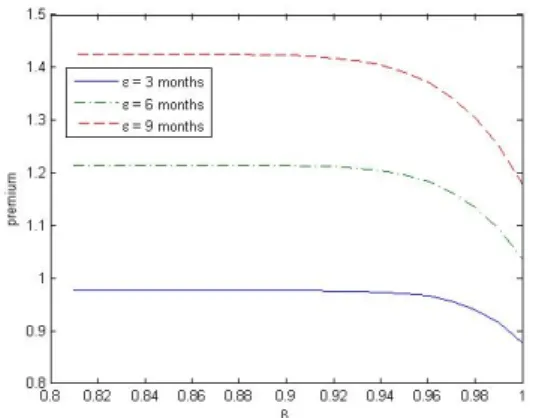

We set the basic scenario and the threshold β varies in the sequence 1, 0.97, 0.95, 0.9 and 0.8. The numerical results show that the premiums rise as the value of the forbearance threshold drops. As the forbearance threshold extends the insurance coverage to the undercapitalized insurers, the probability of the insurer surviving at auditing time T increases and thus the grace period component significantly increases. Moreover, this also shows that increases in the debt-to-asset ratio raise the sensitivities of the grace period and capital forbearance components to the forbearance threshold. Moreover, in Figure 3, we display the cross influence of the grace period ( ε ) and the threshold ( β ). As the value of the forbearance threshold lowers, the cost of the grace period component increases, while the cost of the capital component decreases. Thus, the premium increases significantly from 0.9 to 1, while it is almost flat below 0.9.

This is because the low level η=0.5 of early closure results in the cost being than 0.0001. we compare η from 0.5 to 0.8. The cost of early closure increases as η increases.

Figure 3. Relationship between β and ε.

Lee et al. (2005) and Yang et al. (2012) assume that the interest rate is fixed and incorporate the capital forbearance to derive the closed-form solution of the premium. However, stochastic interest rate is a vital assumption under fair pricing problem. Thus, the contribution of this paper is incorporating the capital forbearance mechanism into the pricing problem under the stochastic interest rate environment. The basic benchmark is the premium under s is 0%, which means r that the interest rate is fixed. We list the premium increment induced by the interest rate volatility (from 0% to 3% and 5%). Under the case of Merton’s put, there is no capital forbearance mechanism. Firstly, we find that the increments under capital

forbearance are larger than those under Merton’s put. In other words, when the interest rate is more volatile, the influence for the premium is more significant when we consider the capital forbearance mechanism. Secondly, high leverage ratio will deteriorate the influence of the stochastic interest rate. For example, when

r

s increases to 3% under the capital forbearance case, then the premium increment is 0.5189 under debt-to-asset ratio is 100/120; however, the premium increment goes up to 3.2316 under debt-to-asset ratio is 100/100.

3.2 The sensitivity of the Greeks

In this section, we discuss how the value of the insurance premium under forbearance varies in response to changes in the main parameters ( , , , , , ,

α β ε γ ω ω σ

1 2 r ). The partialderivatives of these parameters are too complicated to determine directly their signs according to their formulas of partial derivative. We ascertain the signs of the partial derivatives of these parameters through numerical experiments.

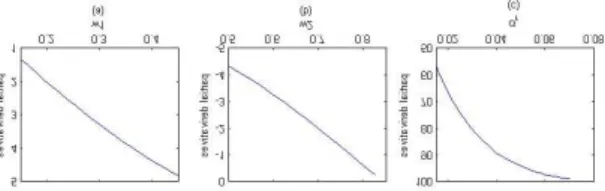

Figure 4 presents the results of partial derivatives with respect to α , β , γ and

ε . We find that ∂P(0)α

∂ drops and the sign is still positive as α rises, as shown in Figure 4(a). This means that the premium increases with the capital requirement but

its impact on the premium decreases. Figure 4(b) shows that P(0)

β

∂

∂ drops and the sign is still negative as β rises. This indicates a loose capital forbearance setting, which means that the lower β increases the premium owing to the cost of capital forbearance component, but the impact of forbearance on the premium decreases. Figure 4(c) helps us to easily understand the sign and trend of P(0)

γ ∂ ∂ . As γ increases, P(0) γ ∂

∂ rises and is positive, suggesting that the cost of the insurance guaranty fund increases when γ rises. The increased premium is owing to the cost of compensation, and the impact on the premium increases. Moving on to the grace period, Figure 4(d) helps us to easily understand the sign and trend of P(0)

ε ∂

∂ . As ε increases, ∂P∂(0)ε drops but are still positive. This illustrates that ε increases the premium owing to the cost of the grace period component, while the impact on the premium decreases.

Figure 4. The partial derivatives with respect to α , β , γ and ε .

The formula of the partial derivatives is listed in Appendix B. We find that as w 1 increases, 1 (0) P w ∂

∂ is positive and rises. It indicates that w increases the cost of the 1 insurance guaranty fund owing to the increment of the whole portfolio’s volatility, and the impact on the premium increases. On the other hand, as w2

increases, 2 (0) P w ∂

∂ rises, as shown in Figure 5(b). However, the sign remains negative, which means that w2 decreases the premium. In our model, we set the sum of

1

w and w2 to be 90%; thus, a greater w2

results in a lower w and then decreases 1 the volatility of the whole investment portfolio, while the impact of w2 on the premium lessens. Figure 5(c) helps us to easily understand the sign and trend of

(0) r P σ ∂ ∂ . As

σ

r increases, (0) r P σ ∂ ∂ is positive and rises. This demonstrates thatσ

r increases the premium owing to the increment of the whole portfolio’s volatility, and the impact on the premium increases.Figure 5. The partial derivatives with respect to w , 1 w2 and

σ

r.1. Conclusion

First, we find the premium is larger under regulatory forbearance than the traditional Merton put, which means that the cost of regulatory forbearance is enormous. Secondly, when the interest rate is more volatile, the influence for the premium is more significant under the capital forbearance mechanism case than that under Merton’s put case. Finally, we find that the premium increases with higher financial leverage and more risky asset allocation. As the financial leverage and risky asset allocation strategy play important roles in the solvency risk of the insurance company, the higher risk is reflected in a higher insurance premium.

Moreover, the volatility of the return on the risky asset is an important parameter under fair premium pricing. The premium increases with higher volatility. Thus, we suggest that the regulator should charge a different premium for the insurance guaranty fund according to the life insurer’s financial structure and risky investment strategy. Finally, premiums will rise as the values of the forbearance threshold drop, and this reminds the regulator to set a reasonable forbearance threshold.

四、參考文獻

Bacinello, A. R. 2001. Fair Pricing of Life Insurance Participating Policies with a Minimum Interest Rate Guaranteed. ASTIN

Bulletin 31: 275-297.

Ballotta, L. 2005. A Levy Process-based Framework for the Fair Valuation of Participating Life Insurance Contracts.

Insurance Mathematics and Economics 37:

173-196.

Bernard, C., O. Le Courtois and F. Quittard-Pinon. 2005. Market Value of Life Insurance Contracts under Stochastic Interest Rates and Default Risk. Insurance Mathematics and

Economics 36: 499-516.

Bernard, C., O. Le Courtois and F. Quittard-Pinon. 2006. Development and Pricing of a New Participating Contract. North American

Actuarial Journal 10:179-195.

Boulier, J. F., S. J. Huang and G. Taillard. 2001. Optimal Management under Stochastic Rates: The Case of a Protected Defined Contribution Pension Fund. Insurance Mathematics and

Economics 28: 173-189.

Briys, E. and F. de Varenne. 1994. Life Insurance in a Contingent Claim Framework: Pricing and Regulatory Implications. Geneva Papers on

Risk and Insurance Theory 19: 53-72.

Briys, E., and F. de Varenne. 1997. On the Risk of Insurance Liabilities: Debunking Some Common Pitfalls. Journal of Risk and

Insurance 64: 673-694.

Chen, A. 2011. A Risk-based Model for the Valuation of Pension Insurance. Insurance

Mathematics and Economics 49: 401-409.

Chen, A. and M. Suchanecki. 2007. Default Risk, Bankruptcy Procedures and the Market Value of Life Insurance Liabilities. Insurance

Mathematics and Economics 40: 231-255.

Cummins, J. D. 1988. Risk-based Premiums for Insurance Guaranty Funds. Journal of Finance 43: 823-839.

Duan, J. C. and J. G. Simonato. 2002. Maximum Likelihood Estimation of Deposit Insurance Value with Interest Rate Risk. Journal of

Empirical Finance 9: 109-132.

Duan, J. C. and M. T. Yu. 1994. Assessing the Cost of Taiwan’s Deposit Insurance. Pacific-Basin

Finance Journal 2: 73-90.

Duan, J. C. and M. T. Yu. 1999. Capital Standard, Forbearance and Deposit Insurance Pricing under GARCH. Journal of Banking and

Finance 23: 1691-1706.

Duan, J. C. and M. T. Yu. 2005. Fair Insurance Guaranty Premia in the Present of Risk-based Capital Regulations, Stochastic Interest Rate and Catastrophe Risk. Journal of Banking and

Finance 29: 2435-2454.

Duan, J. C., A. F. Moreau, and C. W. Sealey. 1995. Deposit Insurance and Bank Interest Rate Risk: Pricing and Regulatory Implications. Journal

of Banking and Finance 19: 1091-1108.

Grosen, A. and P. L. Jørgensen. 2002. Life Insurance Liabilities at Market Value: An Analysis of Insolvency Risk, Bonus Policy, and Regulatory Intervention Rules in a Barrier Option Framework. Journal of Risk and

Insurance 69: 63-91.

Hwang, D. Y., F. S. Shie, K. Wang, and J. C. Lin. 2009. The Pricing of Deposit Insurance Considering Bankruptcy Costs and Closure Policies. Journal of Banking and Finance 33: 1909-1919.

Lee, S. C., J. P. Lee, and M. T. Yu. 2005. Bank Capital Forbearance and Valuation of Deposit Insurance. Canadian Journal of Administrative

Sciences 22: 220-229.

Marcus, A. 1987. Corporate Pension Policy and the Value of PBGC Insurance. In Issues in

Pension Economics. Edited by Bodie, Z.,

Shoven, J.B., and Wise, D.A. University of Chicago Press.

Merton, R. C. 1977. An Analytic Derivation of the Cost of Deposit Insurance and Loan Guarantees. Journal of Banking and Finance 1: 3-11.

Miltersen, K. R. and S. A. Persson. 2003. Guaranteed Investment Contracts: Distributed and Undistributed Excess Return.

Scandinavian Actuarial Journal 4: 257-279.

Pennacchi G. G., and C. M. Lewis. 1994. The Value of Pension Benefit Guaranty Corporation Insurance. Journal of Money,

Credit and Banking 26: 735-753.

Ronn, E. I. and A. K. Verma. 1986. Pricing Risk-adjusted Deposit Insurance: An Option-based Model. Journal of Finance 41: 871-895. Rutkowski, M. 1999. Self-financing Trading

Strategies for Sliding, Rolling-horizon, and Consol Bonds. Mathematical Finance 9: 361-385.

Sharpe, W. F. 1976. Corporate Pension Funding Policy. Journal of Financial Economics 3: 183-193.

Tanskanen, A. J. and J. Lukkarinen. 2003. Fair Valuation of Path-dependent Participating Life Insurance Contracts. Insurance Mathematics

and Economics 33: 595-609.

Vasicek, O. 1977. An Equilibrium Characterization of the Term Structure. Journal of Financial

Economics 5: 177-188.

The Bankruptcy Cost of Life Insurance Industry under Regulatory Forbearance: An Embedded Option Approach. North American

Actuarial Journal 16: 513-523.

Hwang, Y. W., S. C. Chang and Y. C. Wu. 2014. Capital Forbearance, Ex Ante Life Insurance Guaranty Schemes, and Interest Rate Uncertainty, North American Actuarial

Journal. (Accepted)

Chang et al., Hsuan W. and Cheng L. Y. 2014. Fair Insurance Guaranty Premium in the Presence of Systematic Risks, Working Paper.

第

18 屆亞太風險與保險學會年會紀實

張士傑

國立政治大學風險管理與保險學系

2014 年 7 月 27-‐30 日

一. 參加會議經過 第十八屆亞太風險與保險學會年會於2014 年 7 月 27 日至 30 日於俄羅斯莫斯科 大學舉行。此次會議共有100 多篇論文發表,與會學者專家分別來自亞洲各國, 美國,歐陸的德國,以色列,英國,瑞士等20 個國家,採論文口頭報告的方式, 分6 個平行的議場進行。 此外大會特別於第一天開幕式由俄羅斯中央銀行保險監理部門Igor Zhuk 致辭, 報 告“Basic indicators of the insurance market in the Russian Federation, 2013”,同時由俄羅斯保險協會主席 Igor Yurgens 報告 “Conditions and growth prospects of Russian insurance market”。依序的圓桌座談一討論,由美國聖約翰大學E.A.G. Manton Chair 教授與保險監理 研究中心主任 W. Jean Kwon 探討"Developing issues in insurance regulation globally",通用再保險 Reinsurance AG A Berkshire Hathaway 公司俄羅斯公司 Capitolina Tourbina 博士探討"Challenges of the insurance Solvency regulation in the new insurance"。

韓國SKK 大學教授Hongjoo Jung 探討"Insurance supervision of the Republic of Korea -‐ always for financial consumers".

圓桌座談二討論,分析保險業的現在與未來,由大都會人壽Timur Gilyazov 探 討 "Review of the reform of saving pension and non-‐state pension funds",俄羅 斯 精 算 協 會 主 席 Vladimir Novikovwzp 分析"Actuarial profession and risk oriented regulation of financial markets",俄羅斯社會保險基金主席 Andrey Kigimw 的主題為”Social Insurance Fund of the Russian Federation-‐ Strategic Development Guidelines”。

圓桌三討論,主題為保險整合議題,俄羅斯 SOGAZ 保險集團執行董事 Dmitriy Talaev 的 主 題 為 "International cooperation: new horizons" , 俄 羅 斯 ROSGOSSTRAKH 副主席 Ilias Aliev 的主題為”The system of education and science in Insurance in Russia”,俄羅斯 Allianz 人壽執行副總經理 Dmitriy Popov 的主題為"Regulation of insurance rates for compulsory insurance classes",財務 雜誌主編Edvard Grebenshchikov 的主題為“Harmonization of Regulations and Integration of the Markets"。

我的論文報告排在議程第1 天第 1 場的保險公司風險管理議題,由美國聖約翰大 學E.A.G. Manton Chair 教授 Jean Kwon 主持,共同報告人為逢甲大學風險管理與 保險學系黃雅文助理教授,內容有關於保險財務風險管理,負債導向基金(如人 壽保險公司或退休基金等機構法人)之策略性資產配置及破產成本(見 Chang and Li 2007, Chang and Hwang 2009, 2010, Chang and Yang 2010, Chang, Tsai

and Hwang, 2011, Yang, Hwang 與 Chang 2012 等),以隱含選擇權評價方法檢 視基金之破產風險,其中違約風險則以基金所承受之可能破產賠付金額表示,相

關研究(見 Cummins 1988, Briys & Varenne 1994, Grosen & Jogensen 2002 等)主 要以建立選擇權模型評估基金資產負債表之違約風險,為實際反映市場之資產負

債資訊,本研究考量加入流動性溢酬下之負債公平價值,分析負債導向基金之資

產配置,績效歸因與違約風險間之關聯性。

本研究延伸Yang, Hwang 與 Chang (2012)1之資本寬容架構,並假設負債導向基

金之資產價值低於給定比例負債價值時,即進行接管監理程序。研究將建立資本 市場之資產指標收益模型,探討資產配置如何影響基金經理人之績效評估,分析 投資風險與違約成本關連性。於數值實證分析部分,將嘗試依台灣人壽保險市場 之公司資產負債資訊建立模型,依基金績效歸因與隱含選擇權模型分析投資風險 與違約成本於基金資產配置效果與投資能力之影響。資本市場假設將納入資產隨 機波動模型描述風險資產之市場風險,反映保險公司所持有資產之實際交易風 險,用以表達策略性資產配置下之績效歸因分析與下檔風險測度,並計算風險偏 好對於基金違約風險之影響程度,而為實際反映特許金融事業之資本監理因素, 也將道德風險與監理寬容等因素,於數值計算時納入模型中考量。與會學者除了 於會場中發問外,並私下進行廣泛的意見交談。 二. 會議內容及心得

此次會議主要由亞洲太平洋風險與保險學會(Asian Pacific Risk and Insurance Association, APRIA)與俄羅斯莫斯科大學所共同主辦,亞太風險與保險學會為區

域性的國際組織,此次會議除選舉學會主席、副主席、秘書等重要學會工作人員, 並且選舉26 位理事,分別代表不同的與會國家,初步將以促進區域了解與推動 風險管理與保險教育與研究為主要宗旨。本次會議分別就子議題進行討論。 本人參與年會1 整天的學會會議,積極參與國際事務與學術研究,與會期間參與 保險市場經濟結構,保險計價理論,危險理論,社會保險與退休金計畫,汽車保 險,人壽保險計價及座談討論等項目進行聆聽,收穫相當豐富。 三. 考察參觀活動 本次大會提供參觀俄羅斯國家科學院與俄羅斯大學的機會,優良的教育環境及校 園建設與規劃,令來賓稱讚不已。 四. 建議 風險管理與保險的研究發展在國際間已快速成長,相較於歐美各國於金融保險的 發展,台灣於風險管理與保險領域的研究已有顯著表現,下一屆年會預計將由 德國大學舉辦 2015 World Congress,屆時世界三大主要保險學會(美國、 歐洲與泛太平洋風險管理學會)將一起舉辦年會。 五. 攜回資料名稱及內容 攜回大會光碟片包含所有論文及相關參考資料。 An Embedded Option Approach, North American Actuarial Journal, 16(4) 1-‐11.2012.

科技部補助計畫

計畫名稱: 負債導向基金之資產配置,績效歸因與違約風險 計畫主持人: 張士傑

計畫編號: 102-2410-H-004-052- 學門領域: 財務

計畫名稱:負債導向基金之資產配置,績效歸因與違約風險 量化 成果項目 實際已達成 數(被接受 或已發表) 預期總達成 數(含實際已 達成數) 本計畫實 際貢獻百 分比 單位 備 註 ( 質 化 說 明:如 數 個 計 畫 共 同 成 果、成 果 列 為 該 期 刊 之 封 面 故 事 ... 等) 期刊論文 0 0 100% 研究報告/技術報告 0 0 100% 研討會論文 2 3 100% 篇 論文著作 專書 0 0 100% 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 0 0 100% 博士生 0 0 100% 博士後研究員 0 0 100% 國內 參與計畫人力 (本國籍) 專任助理 0 0 100% 人次 期刊論文 0 0 100% 研究報告/技術報告 0 0 100% 研討會論文 2 2 100% 篇 論文著作 專書 0 0 100% 章/本 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 2 2 100% 博士生 0 0 100% 博士後研究員 0 0 100% 國外 參與計畫人力 (外國籍) 專任助理 0 0 100% 人次