年報

治稅以法 服務以誠

Tax by the Law Service from the Heart

Inland Revenue Department

The Government of the Hong Kong Special Administrative Region

Annual Report 2015-16

Vision, Mission and Values

Vision

We aim to be an excellent tax administration that plays an important part in promoting Hong Kong’s prosperity and stability.

Mission

We are committed to –

• collecting revenue efficiently and cost-effectively;

• providing courteous and effective service to the taxpaying public;

• promoting compliance through rigorous enforcement of law, education and publicity programmes; and

• enabling staff to acquire the necessary knowledge, skills and attitude so that they can contribute their best to the achievement of our vision.

Values

Our core values are –

• Professionalism

• Efficiency

• Responsiveness

• Fairness

• Effectiveness

• Courtesy

• Teamwork

Contents

Chapter 1: Commissioner’s Foreword Chapter 2: Revenue

Chapter 3: Assessing Functions Profits Tax

Salaries Tax Property Tax

Personal Assessment Tax Treaty Network Advance Rulings

Advance Pricing Arrangement Objections

Appeals to the Board of Review Appeals to the Courts

Business Registration Stamp Duty

Estate Duty Betting Duty

Tax Reserve Certificates Chapter 4: Collection

Collection of Tax Refund of Tax

Recovery of Tax in Default Chapter 5: Field Audit and Investigation

Field Audit Investigation

Property Tax Compliance Check Chapter 6: Taxpayer Services

IRD Website

Electronic Enquiry Service Enquiry Service Centre

Tax-help Services for Completion of Tax Returns

Complaints and Compliments Performance Pledge

Chapter 7: Information Technology IT Environment

Electronic Services Chapter 8: Human Resources

Organisation Chart Establishment

Staff Promotions and Turnover Training and Development Staff Relations and Welfare The IRD Sports Association

Chapter 9: Legislative Amendments Chapter 10: Environmental Report

Green Management Policy Green Management and

Promotion of Green Awareness Environmental Protection

Performance

New Initiatives and Targets Chapter 11: Miscellaneous

Charitable Institutions General Inspection Internal Audit

Approval for Tax Return Forms and the Manner of Furnishing Tax Returns

Schedules

1 Commissioner’s Foreword

The total revenue collection of the Inland Revenue Department in 2015-16 was $291.3 billion. It was $10.6 billion lower than that of last year, yet, it is the second highest record over the years. Compared with last year, stamp duty collection recorded a significant drop. There was huge amount of stamp duty collection on one-off basis last year. The drop in number of property transactions since August 2015 also resulted in a decrease in stamp duty collection in 2015-16. In respect of salaries tax, the increase in maximum amount of tax rebate from $10,000 to $20,000 in the year of assessment 2014-15 slightly brought down the amount of salaries tax assessed. For profits tax, the slowdown of the Hong Kong economy since the second half of 2015 has triggered a sharp rise in the amount of provisional tax heldover, which in turn resulted in a smaller increase in tax collection.

2015-16 was a challenging year. Five revenue-related bills were enacted in the 2015-16 legislative session:

• Inland Revenue (Amendment) (No. 3) Ordinance 2015:

enhancing the tax appeal mechanism and improving the efficiency and effectiveness of the Board of Review

• Inland Revenue (Amendment) Ordinance 2016: effecting the concessionary revenue measures introduced in the 2016-17 Budget

• Inland Revenue (Amendment) (No. 2) Ordinance 2016: enhancing the existing interest deduction rules for the intra-group financing business of corporations; introducing a concessionary profits tax rate for qualifying corporate treasury centres; and seeking to clarify profits tax and stamp duty treatments in respect of regulatory capital securities issued by banks in compliance with Basel III capital adequacy requirements

• Securities and Futures (Amendment) Ordinance 2016: introducing a new open-ended fund company (OFC) structure in Hong Kong and providing legislative framework for registration and incorporation of OFCs and regulation of such companies and their businesses

• Inland Revenue (Amendment) (No. 3) Ordinance 2016: providing a legislative framework for the implementation of automatic exchange of financial account information in tax matters (AEOI) in Hong Kong

Tax transparency and effective exchange of information has become a focus of our work agenda. As a major financial centre and a responsible member of the international community, Hong Kong has all along been a staunch supporter of international efforts to enhance tax transparency and combat cross-border tax evasion. I am pleased that the Inland Revenue (Amendment) Bill 2016 was passed to become the Inland Revenue (Amendment) (No. 3) Ordinance 2016. As a result, Hong Kong can fulfil its commitment to commence the first information

exchange by the end of 2018. It also allows the Department and financial institutions to have an early kick-start of the requisite preparatory work. The Department is now working in full swing to develop an AEOI portal for financial institutions to submit electronic notices and relevant forms. The AEOI portal is safe, secure, and can ensure privacy of AEOI account holders and confidentiality of information exchanged during the process. Our target is to implement the AEOI portal before end of 2017.

Apart from gearing up for the implementation of AEOI, we kept on striving to further expand Hong Kong’s network of Comprehensive Double Taxation Agreements (CDTAs). In the past year, Hong Kong has made remarkable achievements in this area. Up to 31 March 2016, Hong Kong has signed CDTAs with 34 jurisdictions.

At the same time, the Department actively participated in international meetings concerning Base Erosion and Profit Shifting (BEPS). The Group of Twenty (G20) endorsed in November 2015 the package of measures proposed by the Organisation for Economic Co-operation and Development (OECD) to tackle BEPS. The BEPS Package, covering 15 specific actions, seeks to ensure that multinational corporations pay a fair share of taxes in respect of their profits, and to plug the loophole of “double non-taxation” among jurisdictions. Implementing the BEPS Package can ensure the alignment of the local tax system with international standards, whereby maintaining a fair and transparent tax environment and Hong Kong’s competitiveness. In view of this, the Government accepted the OECD’s invitation on 20 June 2016 to join, in the name of “Hong Kong, China”, as an Associate in the inclusive framework for implementing the BEPS Package. Hong Kong will work on an equal footing with the OECD, the G20 and many other countries and jurisdictions to implement the BEPS Package and to develop standards. The Government is conducting an analysis on the recommendations in the BEPS Package, with a view to mapping out work priorities. The Government will also consult the industry on the strategy for implementing the relevant proposals at an appropriate juncture and prepare for taking forward the necessary legislative amendments.

With the increasing number of CDTAs signed by Hong Kong, and the new tasks arising from the implementation of AEOI and BEPS Package, the Department will be facing ever-increasing workload in the years ahead. Despite the difficulties and challenges foreseen, we will, with high team spirit, strive for the best to accomplish our missions.

WONG Kuen-fai

Commissioner of Inland Revenue

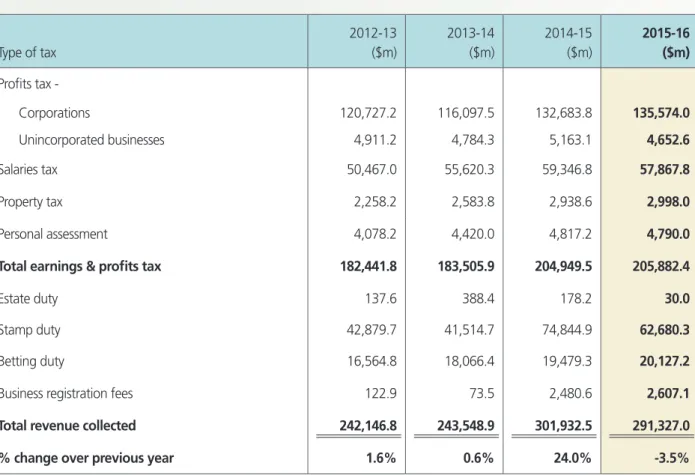

2 Revenue

In 2015-16, the Inland Revenue Department collected $291.3 billion which represents a decrease of $10.6 billion or 3.5% as compared with the previous year. The decrease mainly came from stamp duty and salaries tax. Stamp duty collections dropped by 16.3% to $62.7 billion. Salaries tax collections dropped by 2.5% to $57.9 billion.

Profits tax collections, on the other hand, increased by 1.7% to $140.2 billion. An analysis of the revenue collected by tax type is provided in Figure 1.

Figure 1 Revenue collected by tax type

2012-13 2013-14 2014-15 2015-16

Type of tax ($m) ($m) ($m) ($m)

Profits tax -

Corporations 120,727.2 116,097.5 132,683.8 135,574.0

Unincorporated businesses 4,911.2 4,784.3 5,163.1 4,652.6

Salaries tax 50,467.0 55,620.3 59,346.8 57,867.8

Property tax 2,258.2 2,583.8 2,938.6 2,998.0

Personal assessment 4,078.2 4,420.0 4,817.2 4,790.0

Total earnings & profits tax 182,441.8 183,505.9 204,949.5 205,882.4

Estate duty 137.6 388.4 178.2 30.0

Stamp duty 42,879.7 41,514.7 74,844.9 62,680.3

Betting duty 16,564.8 18,066.4 19,479.3 20,127.2

Business registration fees 122.9 73.5 2,480.6 2,607.1

Total revenue collected 242,146.8 243,548.9 301,932.5 291,327.0

% change over previous year 1.6% 0.6% 24.0% -3.5%

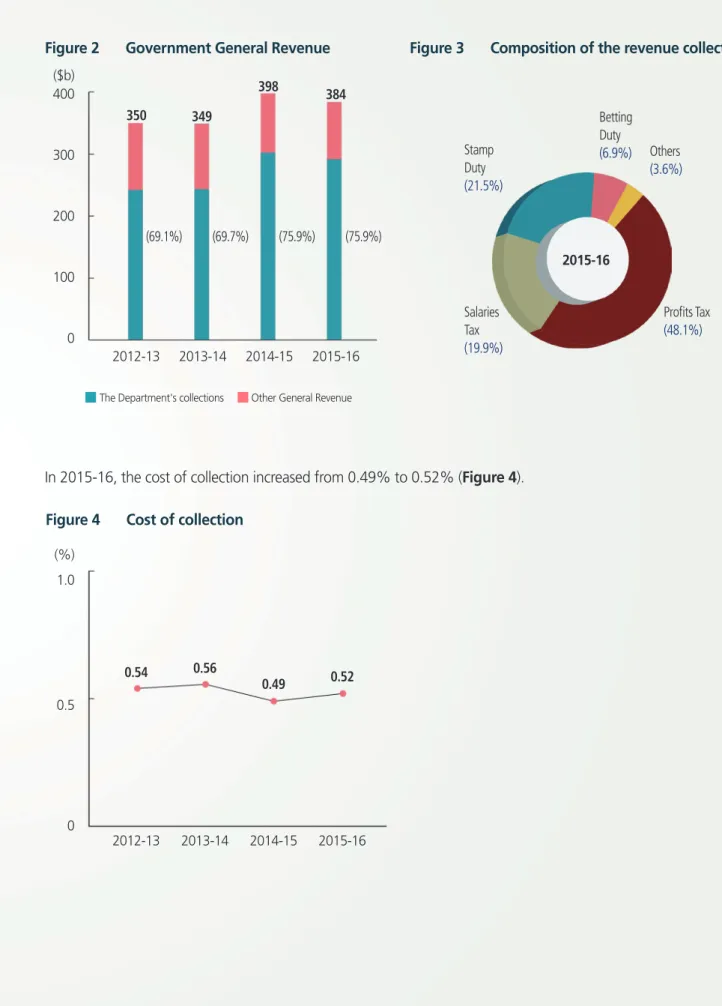

The revenue collected by the Department during 2015-16 accounted for 75.9% of the Government General Revenue (Figure 2). Profits tax and salaries tax contributed 68% of the total revenue collected while stamp duty made up a further 21.5% (Figure 3).

Figure 2 Government General Revenue 400

300

(69.1%) (69.7%) (75.9%) (75.9%) 200

100

0

2012-13 350

The Department's collections Other General Revenue

2013-14 349

398 384

2014-15 2015-16 ($b)

Figure 3 Composition of the revenue collections

Betting Duty (6.9%) Stamp

Duty (21.5%)

Salaries Tax (19.9%)

Others (3.6%)

Profits Tax (48.1%) 2015-16

In 2015-16, the cost of collection increased from 0.49% to 0.52% (Figure 4).

Figure 4 Cost of collection 1.0

0.5

0 2012-13

0.52

2013-14

0.54 0.56

0.49

2014-15 2015-16 (%)

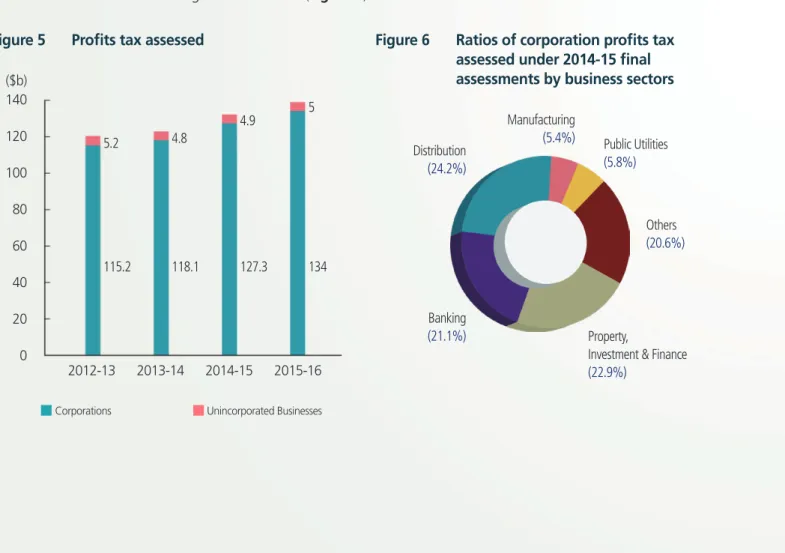

3 Assessing Functions

The Department raises revenue through taxes, duties and fees in accordance with the relevant legislation. Earnings and profits tax are assessed by reference to the incomes / profits of the taxpayers in the previous year, whereas duties and fees are charged at the time the relevant activities occur. For 2015-16, earnings and profits tax assessed increased by $5.5 billion (2.7%) (Schedule 2) as compared with the previous year. Yet, the total amount of duties and fees collected dropped by $11.5 billion (11.9%).

Profits Tax

Profits tax is levied on individuals, corporations, bodies of persons and partnerships, in respect of assessable profits arising in or derived from Hong Kong. For the year of assessment 2015-16, the tax rates for corporations and non- corporate persons remained unchanged at 16.5% and 15% respectively.

The amount of profits tax assessed in 2015-16 was $139 billion, which was $6.8 billion (5.1%) more than that of the previous year, reflecting a modest growth in the Hong Kong economy (Figure 5).

The amounts of final tax assessed in respect of different business sectors are shown in Schedules 3 and 4. Of the total final tax assessed for the year of assessment 2014-15, the property and financial sectors together contributed 44% and the distribution sector generated 24.2% (Figure 6).

Figure 5 Profits tax assessed

140 120

115.2 5.2

127.3 4.9

118.1 4.8

134 5

100 80 60 40 20 0 ($b)

2012-13

Corporations Unincorporated Businesses

2013-14 2014-15 2015-16

Figure 6 Ratios of corporation profits tax assessed under 2014-15 final assessments by business sectors

Manufacturing (5.4%) Distribution

(24.2%)

Banking (21.1%)

Public Utilities (5.8%)

Property,

Investment & Finance (22.9%)

Others (20.6%)

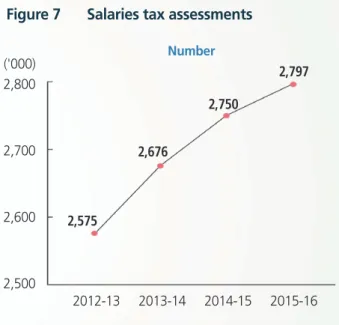

Salaries Tax

Salaries tax is charged on all incomes from any office (e.g. a directorship) or employment and pension arising in or derived from Hong Kong. The total amount of tax payable is restricted to the standard rate on the net total income (without allowances) of the individual concerned. For the year of assessment 2015-16, the standard rate remained unchanged at 15%.

As compared with the previous year, the number of salaries tax assessments made during 2015-16 increased by 1.7%. However, the total amount of tax assessed was 2.3% less after implementing the salaries tax relief measures in the 2015-16 Budget (Figure 7).

Figure 7 Salaries tax assessments

2,800

2,700

2,600

2,500

2,575

2,676

2,750 Number

2,797 ('000)

2012-13 2013-14 2014-15 2015-16

70 60 50 40 30 20 10 0

52.6 57.7 62.0 60.6

($b) Tax assessed

2012-13 2013-14 2014-15 2015-16

Analyses of salaries tax assessments and allowances granted in respect of taxpayers at various income levels for the year of assessment 2014-15 are provided in Schedules 5 and 6.

For the year of assessment 2014-15, the number of standard rate taxpayers increased by 1,841 to 29,692.

These taxpayers together contributed 39.5% of the salaries tax assessed, an increase of 2.5% compared with last year (Figure 8).

Figure 8 Standard rate taxpayers

40

30

1.6 1.7

37.0 39.5

20

10

0

2013-14

Final Assessments 2014-15 Final Assessments (%)

% of total number of taxpayers % of salaries tax assessed

Notification Requirements of Employers

Employers are required to notify the Department of commencements and cessations of employment as well as employees’ impending departure from Hong Kong for more than 1 month. Besides, employers are required to prepare annual employer’s returns to report the emoluments of each of their employees. During the year, 406,264 employers filed employer’s returns with the Department.

The Department provides e-Seminars and disseminates tax information to employers on the IRD website to help them understand the relevant statutory requirements. The contents cover completion of employer’s returns, employer’s obligations and answers to frequently asked questions. Employers can also obtain specimens of completed employer’s returns and notification through the Fax-A-Form service.

Property Tax

Property owners (including corporations) are subject to property tax which is charged at the standard rate in respect of the net assessable value of the property.

For the year of assessment 2015-16, the standard rate remained unchanged at 15%. Rents received from properties solely owned by individuals should be declared in Tax Returns-Individuals (BIR60); whilst rents received from properties jointly owned or co-owned by individuals or properties held by corporations / bodies of persons should be declared in Property Tax Returns (BIR57 / BIR58). Property owners that pay property tax in respect of premises used for their businesses can have such payments set off against their profits tax liabilities.

For corporations, income arising from properties owned by them is also subject to profits tax at the corporation rate. To obviate the need for yearly set-off of property tax against profits tax, a corporation can apply for exemption of property tax on the property concerned.

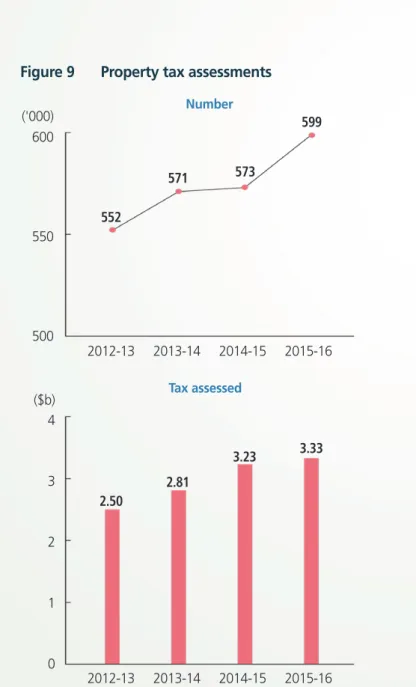

Statistics on the classification of properties and classification by number of owners, based on the records of the Department, are provided in Schedule 7. The number of assessments made in 2015-16 was more than that in the previous year by 4.5%. The total amount of property tax assessed also increased by 3.1% (Figure 9).

Figure 9 Property tax assessments

600

550

500

552

571 573

Number ('000) 599

2012-13 2013-14 2014-15 2015-16

4

3

2

1

0

2.50

2.81

3.23 3.33

($b) Tax assessed

2012-13 2013-14 2014-15 2015-16

Personal Assessment

If an individual has income chargeable to profits tax and /or property tax, he/she may elect for personal assessment.

Under personal assessment, all the incomes of the taxpayer and his or her spouse (if married) are aggregated and, after deduction of all allowances, are assessed at the progressive tax rates applicable to salaries tax. In appropriate circumstances, this would reduce the total tax liability of the taxpayer and his or her spouse.

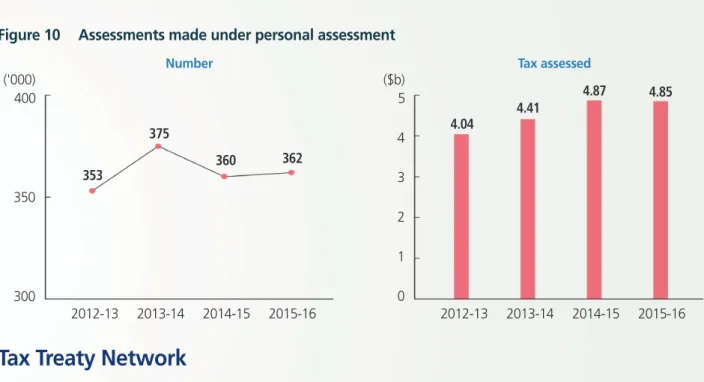

In 2015-16, both the number of assessments made and the total amount of tax assessed under personal assessment were similar to those of last year (Figure 10).

Figure 10 Assessments made under personal assessment

400

350

300

353

375

360 Number

362 ('000)

2012-13 2013-14 2014-15 2015-16

5 4 3 2 1 0

4.04 4.41 4.87 4.85

($b) Tax assessed

2012-13 2013-14 2014-15 2015-16

Tax Treaty Network

Double taxation arises where the same item of income or profit of a taxpayer is subject to tax in Hong Kong as well as in another tax jurisdiction. To establish a tax treaty network can help minimise exposure of Hong Kong residents and residents of the tax treaty partners to double taxation. It will also facilitate the flows of trade, investment and talent between Hong Kong and the rest of the world, and enhance Hong Kong’s competitiveness as an international financial, investment and commercial hub.

As at 31 March 2016, Hong Kong has signed comprehensive double taxation agreements (covering various types of income) with 34 jurisdictions. They are Austria, Belgium, Brunei, Canada, the Czech Republic, France, Guernsey, Hungary, Indonesia, Ireland, Italy, Japan, Jersey, Korea, Kuwait, Liechtenstein, Luxembourg, the Mainland of China, Malaysia, Malta, Mexico, the Netherlands, New Zealand, Portugal, Qatar, Romania, Russia, South Africa, Spain, Switzerland, Thailand, the United Arab Emirates, the United Kingdom and Vietnam.

Hong Kong, as a responsible member of the international community, is committed to enhancing tax transparency and preventing cross-border tax evasion. To comply with the latest international standard on exchange of information, Hong Kong entered into tax information exchange agreements with appropriate partners since 2014.

As at 31 March 2016, Hong Kong has signed tax information exchange agreements with 7 jurisdictions. They are Denmark, the Faroes, Greenland, Iceland, Norway, Sweden and the United States of America.

Advance Rulings

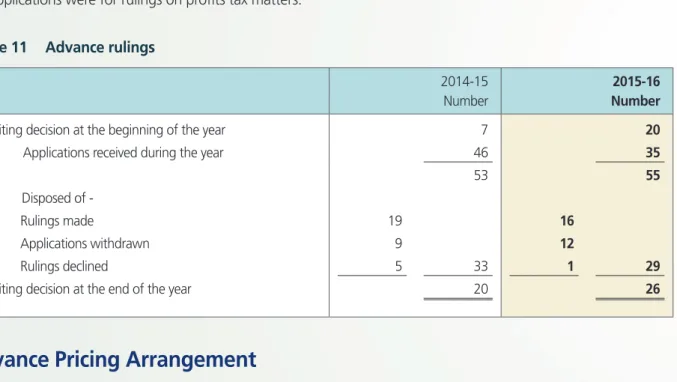

Taxpayers may apply for an advance ruling on how a provision of the Inland Revenue Ordinance applies in relation to a particular arrangement. A fee is charged for the service on a “cost recovery” basis. The applicant is required to pay an initial application fee of $30,000 for a ruling concerning the application of the “Territorial Source Principle” in a profits tax case, or $10,000 for a ruling on any other matter. An additional fee is payable if the processing time exceeds the specified limit. The Department endeavours to respond within 6 weeks of the date of application, provided that all relevant information is supplied with the application and further information from the applicant is not required.

During 2015-16, the Department completed the processing of 29 advance ruling applications (Figure 11). Most of the applications were for rulings on profits tax matters.

Figure 11 Advance rulings

2014-15 2015-16

Number Number

Awaiting decision at the beginning of the year 7 20

Add: Applications received during the year 46 35

53 55

Less: Disposed of -

Rulings made 19 16

Applications withdrawn 9 12

Rulings declined 5 33 1 29

Awaiting decision at the end of the year 20 26

Advance Pricing Arrangement

An Advance Pricing Arrangement (APA) is an arrangement that determines in advance an appropriate set of criteria for the determination of the transfer pricing of cross-border transactions between associated enterprises. The APA process gives enterprises the opportunity to reach agreements with tax administrations on the method of applying the arm’s length principle so that transfer pricing issues can be more efficiently dealt with in real time, thus avoiding the risk of transfer pricing audit later. This arrangement enables enterprises to better assess their tax exposure and facilitates their business operation.

A unilateral APA is an arrangement between the Commissioner and the enterprise concerning the transfer pricing of its cross-border transactions with an associated enterprise. As the APA process does not involve the agreement

with a comprehensive avoidance of double taxation agreement (CDTA) partner, it does not guarantee the agreement of the CDTA partner to the arrangement made.

A bilateral APA is an arrangement between the Commissioner and a CDTA partner concerning the transfer pricing of the abovementioned cross-border transactions. It therefore provides certainty to enterprises that double taxation will not arise. The same also applies to a multilateral APA which is a similar arrangement involving the partners of two or more CDTAs.

The Department rolled out the APA programme in April 2012. At present, the Department will only consider bilateral or multilateral APA applications due to resource constraints and the deficiency of a unilateral APA. Up to 31 March 2016, the Department has received quite a number of applications in relation to CDTA with different partners including the Mainland of China, Japan, Malaysia and the Netherlands. These cases are currently under different stages of the APA programme and a few of them have already been completed.

Objections

A taxpayer who is aggrieved by an assessment may lodge a notice of objection to the Commissioner within the prescribed time limit. If the objection is against an estimated assessment raised in the absence of a tax return, a properly completed return, together with the supporting accounts where applicable, must also be accompanied with the notice of objection. A significant proportion of the objections received each year arise from estimated assessments. Most of these objections are settled promptly by reference to the returns subsequently received.

Many of the other types of objections are also settled by agreement between the taxpayers and the assessors concerned. Only relatively few objections are ultimately referred to the Commissioner for determination. During 2015-16, the Department completed the processing of 79,999 objections (Figure 12).

Figure 12 Objections

2014-15 Number

2015-16 Number

Being processed at the beginning of the year 32,871 35,422

Add: Received during the year 82,293 82,237

115,164 117,659

Less: Disposed of -

Settled without determination 79,323 79,483

Determinations:

Assessments confirmed 246 313

Assessments reduced 93 113

Assessments increased 66 86

Assessments annulled 14 419 79,742 4 516 79,999

Being processed at the end of the year 35,422 37,660

Appeals to the Board of Review

A taxpayer who is dissatisfied with the Commissioner’s determination of his objection may appeal to the Board of Review (Inland Revenue Ordinance) (the Board). The Board is an independent statutory body. As at 31 March 2016, the Board consisted of a chairman and 8 deputy chairmen, who have legal training and experience, as well as 68 members. During 2015-16, the Board settled 56 appeal cases (Figure 13).

Figure 13 Appeals to the Board of Review

Number

Awaiting hearing or decision as at 1 April 2015 48

Add: Received during the year 53

101 Less: Disposed of -

Withdrawn 21

Decided:

Assessments confirmed 23

Assessments reduced in full 6

Assessments reduced in part 1

Assessments increased 4

Others 1 35 56

Awaiting hearing or decision as at 31 March 2016 45

Appeals to the Courts

A decision of the Board is final, provided that either the taxpayer or the Commissioner may, pursuant to section 69 of the Inland Revenue Ordinance, make an application requiring the Board to state a case on a question of law arising from its decision for the opinion of the Court of First Instance. With effect from 1 April 2016, the section 69 was amended to allow the taxpayer or the Commissioner to apply for leave to appeal directly to the court against the decision of the Board on questions of law without having the Board to state a case for the court’s consideration.

During 2015-16, the Court of First Instance ruled on two cases relating to the Inland Revenue Ordinance. In an appeal from the Commissioner, the Court of First Instance remitted the case with its opinion to the Board. In the other appeal concerning chargeability of benefits accrued upon termination of employment, the Court of First Instance dismissed the taxpayer’s appeal.

During the year, the Court of Appeal ruled against a taxpayer in an appeal as to whether licence fees were chargeable to tax.

The Hong Kong Court of Final Appeal Ordinance provides that, a taxpayer or the Commissioner may, with the leave of the Court of Appeal or the Court of Final Appeal, appeal against the judgment of the Court of Appeal.

During 2015-16, the Court of Final Appeal granted the Commissioner the leave to appeal against judgments of the Court of Appeal in 2 related cases, however, the relevant appeals concerning whether certain profits were trading in nature were subsequently dismissed by the Court of Final Appeal.

Figure 14 sets out the statistics concerning appeals to the Courts during 2015-16.

Figure 14 Appeals to the Courts

Court of First Instance

Court of Appeal

Court of

Final Appeal Total

Awaiting hearing or decision as at 1 April 2015 4 1 0 5

Add: Lodged during the year 1 0 2 3

5 1 2 8

Less: Disposed of -

Decided 2 1 2 5

Discontinued 1 0 0 1

Awaiting hearing or decision as at 31 March 2016 2 0 0 2

Business Registration

The Department aims to maintain an efficient business registration system. A person carrying on a business in Hong Kong must register the business and pay the required fee and levy. The number of business registrations as at 31 March 2016 stood at 1,427,064, which was an all time high. It was 21,362 more than that as at 31 March 2015 (Figure 15).

Business registration certificates are generally valid for one year, but businesses may elect for 3-year certificates. As at 31 March 2016, 20,819 businesses held 3-year certificates.

Figure 15 Number of business registrations

1,600 1,400

1,149,197 1,176,220

256,505 250,844

1,200 1,000 800 600

200 400

0

31.3.2015 31.3.2016 ('000)

1,405,702 1,427,064

Corporations Unincorporated Businesses

The amount of business registration fees and penalties collected in 2015-16 increased to $2,607 million. It represents an increase of 5.1% compared with last year (Figure 16). Business registration statistics are set out in Schedule 8.

Figure 16 Business registration statistics

2014-15 2015-16 Increase

Number of certificates paid (Main and Branch) 1,382,214 1,402,548 +1.5%

Fees (inclusive of penalties) collected ($m) 2,481 2,607 +5.1%

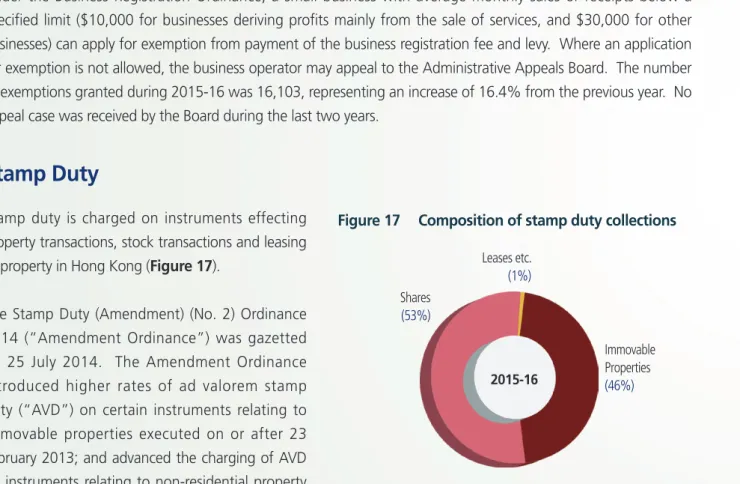

Under the Business Registration Ordinance, a small business with average monthly sales or receipts below a specified limit ($10,000 for businesses deriving profits mainly from the sale of services, and $30,000 for other businesses) can apply for exemption from payment of the business registration fee and levy. Where an application for exemption is not allowed, the business operator may appeal to the Administrative Appeals Board. The number of exemptions granted during 2015-16 was 16,103, representing an increase of 16.4% from the previous year. No appeal case was received by the Board during the last two years.

Stamp Duty

Stamp duty is charged on instruments effecting property transactions, stock transactions and leasing of property in Hong Kong (Figure 17).

The Stamp Duty (Amendment) (No. 2) Ordinance 2014 (“Amendment Ordinance”) was gazetted on 25 July 2014. The Amendment Ordinance introduced higher rates of ad valorem stamp duty (“AVD”) on certain instruments relating to immovable properties executed on or after 23 February 2013; and advanced the charging of AVD on instruments relating to non-residential property

transactions from the conveyance on sale to the agreement for sale executed on or after that date. One-off receipt of additional stamp duty chargeable on certain instruments relating to immovable properties executed during the transitional period (from 23 February 2013 to 24 July 2014) upon passage of the Amendment Ordinance resulted in significantly large collections in 2014-15. On the other hand, the number of immovable property transactions has been decreasing since August 2015. As a result, the stamp duty collections from immovable properties in 2015-16 significantly decreased by 42% as compared to that of 2014-15.

Figure 17 Composition of stamp duty collections Leases etc.

(1%) Shares

(53%)

Immovable Properties (46%) 2015-16

The number of securities transactions has increased noticeably in the first half of 2015-16. The stamp duty collections from share transactions in 2015-16 were $33.4 billion, representing an increase of 34% from the previous year.

Overall, there was a decrease of 16% in the total stamp duty collected during the year. The number of documents stamped also decreased by 8% (Figure 18 and Schedule 9).

Figure 18 Stamp duty collections

2014-15 ($m)

2015-16

($m) Increase/Decrease

Immovable Properties 49,215 28,494 -42%

Shares 24,885 33,410 +34%

Leases and other documents 745 776 +4%

Total 74,845 62,680 -16%

Estate Duty

Estate duty is charged on that part of a deceased person’s estate situated in Hong Kong. The threshold for levying duty is $7.5 million and the duty rates range from 5% to 15%, depending on the value of the estate.

The Revenue (Abolition of Estate Duty) Ordinance 2005 came into effect on 11 February 2006 abolishing estate duty in respect of persons passing away on or after that date. The estate duty chargeable in respect of estates of persons died between the period 15 July 2005 to 10 February 2006, with the principal value exceeding $7.5 million, is reduced to a nominal amount of $100. With the abolition of estate duty, the number of new cases reduced gradually to 771 in 2015-16, a drop of 14% from the last year (Figure 20).

Figures 19 and 20 show the composition of estates and cases processed for the past two years.

Figure 19 Composition of estates

10.6%

25.8%

0.7%1.7%

10.4%

52.9%

18.9%

0.4%4.7% 73.9%

Immovable Properties Quoted Shares Unquoted Shares Bank Deposits Others

2014-15

2015-16

Figure 20 Estate duty cases

2014-15 2015-16

Number Number

New cases 897 771

Cases finalised

- Dutiable 7 17

- Exempt 868 763

875 780

Estate duty of $30 million was collected during the year (Schedule 10), a decrease of $148 million (83%) compared with the previous year.

Estate duty is payable on delivery of an estate duty affidavit or account (or within 6 months from the date of the deceased’s death, whichever is the earlier). $6.3 million was received during the year in advance of the issue of formal assessments (Schedule 10).

Betting Duty

Betting duty is charged on the net stake receipts from betting on horse races and football matches and on the proceeds of Mark Six lotteries, all administered by the Hong Kong Jockey Club. In 2015-16, the rates of betting duty on these betting activities remained unchanged (Figure 21).

Figure 21 Rates of betting duty in 2015-16

Rate Horse racing

Local bets on local horse races Net stake receipts

the first $11 billion 72.5%

the next $1 billion 73%

the next $1 billion 73.5%

the next $1 billion 74%

the next $1 billion 74.5%

the remainder 75%

Local bets on non-local horse races Net stake receipts 72.5%

Mark Six lotteries Proceeds 25%

Football betting Net stake receipts 50%

The total betting duty collected in 2015-16 was 3.3% higher than that of the previous year (Figure 22 and Schedule 11).

Figure 22 Betting duty collections

2014-15 ($m)

2015-16

($m) Increase

Horse racing 11,932.5 12,316.5 +3.2%

Mark Six lotteries 1,970.3 2,032.2 +3.1%

Football betting 5,576.5 5,778.5 +3.6%

Total 19,479.3 20,127.2 +3.3%

Tax Reserve Certificates

Taxpayers may purchase Tax Reserve Certificates (TRCs) under two situations.

The first situation applies to taxpayers who wish to save for the payment of their future tax liabilities.

The Department has set up two schemes, namely the “Electronic Tax Reserve Certificates Scheme” for all taxpayers and the “Save-As-You-Earn” (SAYE) Scheme for civil servants and civil service pensioners.

With a Tax Reserve Certificate account, taxpayers may purchase TRCs by various channels, including bank auto-pay, telephone, the Internet and bank ATM.

Under the “SAYE Scheme”, civil servants and civil service pensioners can purchase TRCs through monthly deductions from their salaries / pensions. Interest is payable on the TRCs when they are redeemed for settlement of tax liabilities, based on the interest rate prevailing at the time of purchase, for a maximum period of 36 months from the date of purchase.

In 2015-16, there was an increase of 2.6% and 23.1%

respectively in the number and the amount of TRCs sold under the “Electronic Tax Reserve Certificates Scheme” but a slight decrease of 0.8% in the number and an increase of 3.5% in the amount of TRCs sold under the “SAYE Scheme” (Schedule 12). Overall, the total amount of TRCs sold decreased slightly by 0.5%

(Figure 23).

Figure 23 Certificates sold 100

60 80

20 40

0 1,604 1,812

89,480 90,299

Number

2014-15 2015-16

('000)

429.1 513.3

2014-15 2015-16

3,000

2,000

1,000

0

2,203.7

2,106.1

($m) Amount

Certificates relating to Objections and Appeals Certificates other than for Objections and Appeals

The second situation applies to taxpayers who object to tax assessments and are required to purchase TRCs in respect of the tax in dispute. Such TRCs are used to settle any tax found payable upon the finalisation of the objection or appeal. Interest is only payable on the amount of the TRC, if any, subsequently required to be repaid to the taxpayer, and is computed at floating rates over the tenure of the TRC.

4 Collection

Revenue collected by the Department includes tax, additional tax, surcharge and fines. Schedules 13 and 14 provide details of additional tax, surcharge and fines imposed by the Department in respect of earnings and profits tax during 2015-16.

Collection of Tax

Taxpayers can conveniently settle their tax liabilities by various payment methods, including electronic payment (by phone, bank ATM or via the Internet), payment in person or payment by post. Starting from 7 December 2015, taxpayers can also settle their tax liabilities by e-Cheque / e-Cashier Order. For earnings and profits tax, electronic payment remains most popular. 56% of the earnings and profits tax payment transactions in 2015-16 were made through electronic means. Figure 24 shows the respective percentages of the different payment methods used by taxpayers under earnings and profits tax and total revenue.

Figure 24 Payment methods

Earnings & profits tax 3,518,123 3,430,578

Number of transactions

2014-15 2015-16 4%

5%

40%

37%

31%

32%

17%

19%

8%

7%

204,949.5 205,882.4

2014-15 2015-16 Amount ($m)

10% 10%

68% 69%

17% 17%

3% 2%

2% 2%

Total revenue (including other duties) 5,722,596

5,890,333

Number of transactions

2014-15 2015-16 56%

4%

54%

5%

24%

24%

11%

12%

5%

5%

By ATM

By Phone Via Internet

In Person By Post

291,327 301,932.5

2014-15 2015-16 Amount ($m)

71%

14%

69%

16%

12%

12% 2%

2% 1%

1%

Refund of Tax

Tax refunds were made mainly due to two reasons, namely, overpayment of tax by taxpayers and revision of assessments. There were 612,637 refund cases in 2015-16, representing an increase of 15.1%. The total amount of refunds was $14.77 billion, representing an increase of $2.99 billion or 25.4% compared with the previous year (Figure 25).

Figure 25 Tax refunds

2014-15 2015-16

Type of tax Number Amount ($m) Number Amount ($m)

Profits tax 44,310 6,580.3 46,969 7,135.4

Salaries tax 423,833 3,239.1 495,074 3,906.6

Property tax 16,723 176.5 16,782 173.6

Personal assessment 27,447 332.8 29,051 348.6

Others 19,721 1,452.8 24,761 3,204.4

Total 532,034 11,781.5 612,637 14,768.6

Recovery of Tax in Default

Taxpayers should pay tax on or before the due date shown on the demand notes issued to them. The vast majority of taxpayers settle their tax liabilities in a timely manner.

A late payment surcharge of 5% will generally be imposed where tax is in default. If tax debts remain outstanding for more than six months after the due date, the Department may impose a further surcharge of 10% on the total unpaid amount.

Any tax in default is immediately recoverable. Recovery notices can be issued to employers, bankers, debtors and persons holding money on behalf of the defaulting taxpayers to effect collection. Actions may also be commenced in the District Court. Figure 26 summarises different types of recovery actions taken by the Department.

Figure 26 Recovery action

5% Surcharge Notice Number of notices

260

240

200 220

180

2012-13

243,089

2013-14 194,411

222,784

243,173

2014-15 2015-16

('000) Total amount

2012-13 2013-14 2014-15 2015-16 300

225

150

75

0

255

192 200

240 ($m)

10% Surcharge Notice Number of notices

18,000 20,000

16,000

12,000 14,000

10,000

2012-13

19,695

2013-14 14,545

14,014 17,277

2014-15 2015-16

Total amount

2012-13 2013-14 2014-15 2015-16 120

90

60

30

0

116

100 102 108

($m)

Recovery Notice Number of notices

150

140

130

110 120

100

2012-13

142,708

2013-14 107,277

125,131

135,654

2014-15 2015-16

('000) Total amount

2012-13 2013-14 2014-15 2015-16 10,000

7,500

5,000

2,500

0

6,954 8,776 8,277

7,532 ($m)

Upon entry of judgment, a defaulting taxpayer becomes liable to legal costs and interest on judgment debt for the period from the date of commencement of proceedings to the date of full settlement in addition to the outstanding tax. Figure 27 shows the legal costs and judgment interest collected during 2015-16.

Figure 27 Legal costs and judgment interest collected in 2015-16

$ $

Court cost

Court fees 785,195

Execution fees 24,708 809,903

Fixed cost 313,471

Judgment interest

Pre-judgment interest 2,299,168

Post-judgment interest 23,253,541 25,552,709

Total costs and interest collected 26,676,083

Furthermore, the Commissioner may apply to a District Judge to prevent a person with tax in default from leaving Hong Kong. If the District Judge is satisfied that it is in the public interest to ensure that the person does not depart from Hong Kong, or if he returns, does not depart again, without first paying the tax or furnishing security to the satisfaction of the Inland Revenue Department for payment of that tax, he shall issue the “departure prevention direction”. The person concerned has the right to appeal to the Court of First Instance of the High Court against the District Judge’s decision.

5 Field Audit and Investigation

The Field Audit and Investigation Unit is responsible for conducting field audits and investigations on businesses and individuals with a view to combating tax evasion and avoidance. Back tax is assessed and penalties are generally imposed where discrepancies are detected.

During 2015-16, the Field Audit and Investigation Unit completed 1,804 cases (including tax avoidance cases) and assessed back tax and penalties of about $2.5 billion (Figure 28).

Figure 28 Results of the Field Audit and Investigation Unit

2012-13 2013-14 2014-15 2015-16

Number of cases completed 1,802 1,802 1,803 1,804

Understated earnings and profits ($m) 16,348.0 12,936.4 12,857.9 13,888.8

Average understatement per case ($m) 9.1 7.2 7.1 7.7

Back tax and penalties assessed ($m) 3,447.7 2,540.0 2,533.1 2,538.3

Back tax and penalties collected ($m) 3,438.3 2,158.7 2,861.4 1,824.2

Field Audit

In 2015-16, there were 17 Field Audit sections. Field audit is conducted on both corporations and unincorporated businesses. The work of field auditors entails site visits to business premises and examination of accounting records of taxpayers in order to ascertain whether correct returns of profits have been made.

Anti-tax Avoidance

Two of the 17 Field Audit sections concentrate on tackling tax avoidance schemes, whereas other investigation officers and field auditors handle avoidance cases on an operational need basis. During 2015-16, the Field Audit and Investigation Unit completed 215 tax avoidance cases and assessed back tax and penalties of about $1 billion (Figure 29).

Figure 29 Results of the audit on tax avoidance cases

2012-13 2013-14 2014-15 2015-16

Number of cases completed 207 219 217 215

Understated earnings and profits ($m) 7,576.4 5,124.9 6,027.7 6,826.2

Average understatement per case ($m) 36.6 23.4 27.8 31.7

Back tax and penalties assessed ($m) 1,523.8 909.3 1,155.6 1,000.4

Investigation

In 2015-16, there were 5 Investigation sections. Investigation officers are responsible for conducting in-depth investigations into suspected tax evasion, and taking penal action (including prosecution proceedings in appropriate cases) as a deterrent.

Prosecution

One of the 5 Investigation sections is the prosecution section focusing on criminal investigation of tax evasion. Tax evasion is a serious crime. A person convicted of tax evasion could be sentenced to imprisonment for up to 3 years and fined.

During the year, the Department successfully prosecuted 3 tax evasion cases, all of which involved making false statements in connection with claims for deduction of expenses of self-education. One of them also involved making false statements in connection with claims for deduction of approved charitable donations. Among these three cases, the defendant of one case was sentenced to 4 months’ imprisonment, suspended for 3 years, and a fine of $70,000 ($10,000 for each charge) plus a further fine of $49,256 (equivalent to about 116% of the tax evaded). The defendant of another case was sentenced to 2 months’ imprisonment, a fine of $90,000 ($10,000 per charge) and a further fine of $78,407 (100% of the tax evaded). The defendant lodged an appeal against the sentence and the appeal was dismissed by the High Court in April 2016. Jail sentence was upheld. The defendant of the last case was sentenced to a community service order of 200 hours and was fined $278,800 (equivalent to 200% of the tax evaded) after being remanded for 14 days.

Property Tax Compliance Check

In addition to conducting audits on businesses, the Department also carries out verification checks on the correctness of rental income reported by property owners. In 2015-16, the Department completed compliance check on 186,229 property tax cases (Figure 30).

Figure 30 Results of the property tax compliance checks

2012-13 2013-14 2014-15 2015-16

Number of cases completed 117,923 140,705 161,860 186,229

Understated rental income ($m) 461.7 553.3 635.0 749.2

Back tax and penalties assessed ($m) 55.4 66.4 76.2 89.9

6 Taxpayer Services

IRD Website

www.ird.gov.hk

The IRD website is a very effective channel for disseminating tax information and providing electronic services to the public.

With continuous enrichment and updates, the website enables taxpayers to obtain the most current information about Hong Kong taxation in a fast and convenient manner.

Through the website, members of the public can:

• obtain information on tax law, tax returns, tax obligations and answers to frequently asked questions;

• download IRD software and tax forms;

• use the interactive program to calculate their liability under salaries tax and personal assessment; and

• access to the personalised on-line tax services provided by the Department under eTAX.

To facilitate all sectors of the community to locate the relevant tax information, there are thematic content pages for individuals, businesses, employers, tax representatives, etc.

The IRD website conforms to web accessibility guidelines and there is also a mobile version to enable all users to have quick and convenient access to tax information.

Electronic Enquiry Service

Electronic enquiry services are provided to eTAX users at <www.gov.hk/etax>. They can view their tax position in relation to their returns, assessments and payments, etc. at any time.

Enquiry Service Centre

The Department’s Enquiry Service Centre handles telephone and counter enquiries. The Centre is equipped with a computer network linked to the Department’s Knowledge Database to enable our staff to provide, as far as possible, an immediate “one-stop” service.

Telephone Enquiry Service

The Centre operates an Interactive Telephone Enquiry System (ITES) with 144 telephone lines. Callers can have access on a 24-hour basis to a wide range of tax information by listening to recorded messages. Besides, callers can obtain facsimile copies of information sheets and forms through the system. A “Leave-and-call-back” facility,

for recording information requests, and a “Fax-in enquiry” service are also available. The telephones are manned during office hours by staff who would readily serve the callers. The Centre also provides an eTAX help desk hotline to handle enquiries on eTAX services and provide technical support.

The statistics of services provided through ITES during 2015-16 are shown in Figure 31.

Figure 31 Statistics of services provided through ITES

2014-15 Number

2015-16

Number Increase/Decrease

Calls answered by staff 704,281 728,196 +3.40%

Calls answered by system 707,575 661,940 -6.45%

Leave-and-call-back messages 36,455 32,851 -9.89%

Documents supplied by fax 3,878 2,813 -27.46%

Counter Enquiry Service

Generally, the counter staff of the Centre is able to handle enquiries, collects mail items and issues forms on the spot without the need of referring callers to other sections in the Department for attention. The number of counter enquiries handled and forms issued during 2015-16 was about 0.57 million (Figure 32).

Information leaflets on topics of general interest are available for collection at the form stand located on the first floor of Revenue Tower. The public may also obtain general tax information and download forms from the IRD website and GovHK <www.gov.hk>.

Figure 32 Counter enquiries

231,852 234,315

600

400

200

0

565,598 515,601

2015-16 2014-15

('000)

No. of callers No. of enquiries

Tax-help Services for Completion of Tax Returns

On the IRD website, e-Seminars are provided for employers, property owners and individual taxpayers. Information on how to complete tax returns, fulfil tax obligations and overcome difficulties in compliance is uploaded to the website. After reading the information, taxpayers can raise enquiries electronically at the “Q&A Corner”. The Department will reply the questions on a regular basis.

The Department issued 2.48 million Individuals Tax Returns for the year of assessment 2014-15 on 4 May 2015.

To assist the taxpaying public in completing tax returns, the Department extended the service hours of telephone enquiry services in May 2015. Service hours from Monday to Friday were extended by one and a half hours till 7:00 pm and additional service was also provided on Saturday from 9:00 am till 1:00 pm. During peak periods, the Department also redeployed manpower resources and employed part-time staff to strengthen daytime telephone enquiry services.

Complaints and Compliments

If taxpayers are dissatisfied with the services provided by the Department or their problems cannot be solved satisfactorily through normal channels, the Complaints Officer may be approached for assistance.

The complaint channel provides taxpayers with the means of having individual grievances dealt with independently at a senior level. This ensures that such cases are properly handled in a fair and impartial manner. During 2015-16, 233 complaints cases were received (Figure 33). This represents a decrease of 21.5%, as compared with the previous year.

If taxpayers are dissatisfied with any administrative action taken by the Department, they may refer the matter to the Ombudsman. During 2015-16, the Ombudsman sought written comments from the Department in respect of 19 cases. In the light of these cases, the Department has reviewed relevant operations with a view to improving them.

Taxpayers may compliment the service of the Department. During the year, 173 Letters of Compliments were received.

Figure 33 Complaint cases

Not substantiated Partially substantiated Substantiated

233 297

250 200 300

0 50 100 150

2015-16 2014-15

137 180

75

92 21

25

Performance Pledge

The service standards a taxpayer can expect from the Department are set out in the performance pledges. The Department has achieved all the targets of performance pledges and excelled in some of the targeted performance with remarkable results during 2015-16.

7 Information Technology

The Department has been making extensive use of information technology to enhance operational efficiency and provide quality services to the public.

IT Environment

The Department has built up a comprehensive and integrated IT infrastructure with different types of computer application systems and platforms. The Department’s network connects the computer system and workstations of staff on different floors. Assessment process is automated by the “Assess-First-Audit-Later” system. Tax audit and investigation work is facilitated by the use of data mining and advanced analytical tools. The Document Management System and Workflow Management System enhance the control and monitoring of documents, files and workflow, facilitate the tracking of case progress, and thus enable the Department to improve overall service quality. A wide range of information is stored in the Department’s Intranet and General Enquiry Knowledge Database for convenient access by our staff at work. Moreover, e-mail and Internet facilities provide an efficient and environment-friendly communication platform for our staff.

In 2015-16, we continued to implement the system infrastructure enhancement project. System development and user acceptance testing for migration of mainframe tax applications to the midrange platform are in active progress.

Electronic Services

eTAX

The Department continues to provide a wide range of online tax services to the public, including internet filing of tax returns, stamping of property documents, business registration services, electronic notices, payments and lodgement of applications, etc.

eTAX services are widely used by the public. As at 31 March 2016, there were some 670,000 registered eTAX users. The take-up rate increased year after year (Figure 34).

Figure 34 eTAX Usage Statistics

2014-15 Number

2015-16

Number Increase/Decrease Internet filing of tax returns

- Tax Return-Individuals, Property Tax Return and Profits Tax Return 472,350 525,670 +11.3%

- Employer’s Return of Remuneration and Pensions

BIR56A 10,292 12,162 +18.2%

IR56B 78,009 86,828 +11.3%

- Employer’s Notifications of Commencement of Employment, Cessation of Employment and Employee’s Departure from

Hong Kong 15,468 17,486 +13.1%

Stamping of Property Document 290,104 262,705 -9.4%

Business Registration Number Enquiry 2,148,597 2,007,895 -6.6%

Application for Supply of Information on the Business Register

- Requisition 130,075 135,548 +4.2%

- Business registrations involved 317,072 329,239 +3.8%

Other Electronic Services

During 2015-16, some 43,800 employers furnished annual returns for 2,826,800 employees in total by diskettes, DVDs or USB storage devices. About 69% of these employers used the free software provided by the Department.

8 Human Resources

Organisation Chart of the Inland Revenue Department as at 31.3.2016

Commissioner

Deputy Commissioner (Technical)

Commissioner's Unit Appeals

Technical Research Tax Treaty

Charitable Donations Complaints Internal Audit Special Duties

Forms &

General Support

Unit 1

Assessment and Review (Profits Tax - Corporations

and Partnerships)

Unit 2

Assessment (Salaries Tax, Profits Tax -

Sole Proprietorships,

Property Tax - Sole Owners and Personal Assessment)

Deputy Commissioner (Operations) Departmental

Administration Division

Unit 3

Collection Inspection Estate Duty Stamp Duty

Business Registration

Unit 4

Field Audit and Investigation

Headquarters Unit Information

Systems Training

Enquiry Services Document Processing

Output Despatch Tax Records

Assessment (Property Tax -

Joint Owners and Corporations)

and Review (Profits Tax -

Sole Proprietorships,

Property Tax and Personal Assessment) Overall Establishment

No. of Staff

Commissioner's Office 83

Commissioner's Unit 75

Headquarters Unit 700

Unit 1 358

Unit 2 766

Unit 3 611

Unit 4 240

Total 2,833

Establishment

The Commissioner, the two Deputy Commissioners and the five Assistant Commissioners, together with the Departmental Secretary, form the top management of the Inland Revenue Department.

Members of the Top Management of the Inland Revenue Department (as at 31.3.2016)

Mr CHIU Sai-ming Assistant Commissioner (Headquarters Unit)

Mr TAM Tai-pang Deputy Commissioner

(Operations)

Mr WONG Kuen-fai Commissioner

Mr CHIU Kwok-kit Deputy Commissioner

(Technical)

Miss LEUNG Shun-chee, Evelyn

Departmental Secretary

Ms LEE Kong-chun, Doris Assistant Commissioner

(Unit 1)

Miss TSUI Siu-fong, Maria Assistant Commissioner

(Unit 2)

Ms TSE Yuk-yip Assistant Commissioner

(Unit 3)

Ms CHAN Fung-kuen Assistant Commissioner

(Unit 4)

As at 31 March 2016, the Department had an establishment of 2,833 permanent posts (including 27 directorate posts) in the Commissioner’s Office and the 6 Units of the Department. Of the total, 1,919 posts were in departmental grades (namely Assessor, Tax Inspector and Taxation Officer grades), performing duties directly concerned with taxation. The remaining 914 posts were in common / general grades, providing administrative, information technology and clerical support services (Figure 35).

Figure 35 Staff establishment 3,000

2,000

1,000

0

2,818 2,826 2,832 2,833

951 935 926 914

1,061 1,079 1,089 1,102

105 105 105 105

701 707 712 712

2015-16 2013-14 2014-15

2012-13

Assessors (Professional) Tax Inspectors

Taxation Officers

Common / general grade officers

Most of the professional officers serving in the Department were below the age of 45 (Figure 36). The ratio of male to female professional officers was 1:1.6.

Figure 36 Age and gender profiles of professional staff (on strength basis)

Age Group Male Female Total

Below 25 7 (3%) 20 (5%) 27 (4%)

25 to below 35 56 (21%) 141 (32%) 197 (28%)

35 to below 45 54 (20%) 98 (22%) 152 (21%)

45 to below 55 115 (42%) 138 (32%) 253 (36%)

55 and over 38 (14%) 39 (9%) 77 (11%)

Total 270 (100%) 436 (100%) 706 (100%)

Staff Promotions and Turnover

In 2015-16, a total of 45 departmental grade officers and 17 common / general grade officers were promoted.

Among them, 2 were in directorate rank. 206 officers joined the Department, of which 133 were new appointees and 73 were officers transferred from other grades / departments. A total of 156 officers (including 49 transferred to other departments) left the Department.

Training and Development

Staff are the Department’s valuable assets. We recognise the importance of providing opportunities of continuous learning to our staff to keep them abreast of the changing environment and to acquire the necessary knowledge to perform their duties. A variety of training courses in taxation, accounting, interpersonal skills, management, languages, computer, etc. are offered to staff members. In 2015-16, our staff received training for a total of 10,414 man-days, which was equivalent to about 3.68 man-days per officer.

The major training activities conducted for our staff during 2015-16 were as below:

Training Courses

• Induction courses for all grades of staff upon joining the Department

• Two-year taxation law and practice course for newly appointed Assistant Assessors

• Briefing sessions on legislative amendments and new services

• Refresher courses on professional knowledge

• Courses on Hong Kong Accounting Standards

• Written and spoken English courses

• Putonghua courses

• Computer courses

Workshops

• Leadership and teamwork workshop

• Mentorship workshop

• Performance appraisal workshops on English writing and interviewing skills

• Workshop on Chinese writing

• Workshop on effective communication in the workplace

• Workshop on essential supervisory skills

• Workshop on how to handle difficult taxpayers

• Workshop on interviewing and negotiation skills

• Workshop on leading innovation and change

• Workshop on performance management

• Workshop on problem solving and decision making

• Workshop on stress management

• Workshop on supervisory management

Continuing Professional Education

11 seminars were held by the Training Committee under the in-house Continuing Professional Education (CPE) Programme on the following subjects for professional officers:

• Understanding the Work of the Office of the Ombudsman

• Implementing Automatic Exchange of Financial Account Information in Tax Matters and Tackling Base Erosion and Profit Shifting (BEPS) in Hong Kong

• International Financial Reporting Standard No. 9 – Financial Instruments

• Cross-border Service Arrangement and the Related Tax Compliance Procedures in the PRC

• An Introduction to Venture Capital and Private Equity

• An Introduction to Anti-money Laundering Enforcement in Hong Kong

• International Tax Avoidance and Action Plan on BEPS

• Stamp Duty on Stock Transactions – Shanghai-Hong Kong Stock Connect and Uncertificated Securities Market

• Update on the Mainland’s Tax Development – BEPS and Transfer Pricing

• Mediation and Arbitration

• Annual Update of Appeals Cases

Speakers for 4 of the seminars were staff members and others were experts from various fields. A total of 1,209 staff members attended these seminars. The video files of the CPE seminars were uploaded onto the Department’s Intranet and a total of 599 staff members had viewed these video files.

Overseas and China Training

In order that our professional officers may broaden their horizons and acquire the necessary knowledge to cope with new and complex global issues, they are sent to participate in overseas training programmes. In 2015-16, 29 officers went to China, Korea, Malaysia and Philippines to attend training courses on different issues, 16 to universities in China for national studies courses and 2 to cities in China for thematic study programmes.

Continuous Learning

Besides the conventional classroom training, the Department employs various means to promote continuous self-learning. These include encouraging staff to take the web courses provided by the CLC Plus of CSTDI and providing financial support to officers to attend seminars and courses organised by academic and professional institutes. In 2015-16, 5 officers were sponsored by the Department to attend the relevant courses. Training materials and information are uploaded onto our Intranet for officers to study in their own time and at their own pace. This provides an effective way for the staff to acquire new knowledge and refresh what they have learnt.

Mentorship Scheme

A Mentorship Scheme for Assistant Assessors has been set up since 2008. Under this scheme, experienced officers (the mentors) will guide newly recruited Assistant Assessors (the mentees) to broaden their perception about the Department such as the organisation structure, work, connection and culture, and help them integrate into the civil service.

Staff Relations and Welfare

The Department attaches great importance to staff relations and welfare. We strive to maintain effective communication, and promote co-operation and mutual trust between the management and staff at all levels which help enhance the Department’s operational efficiency and productivity.

The Departmental Consultative Committee

The Departmental Consultative Committee provides a formal and effective platform for the management and staff to exchange views on matters of mutual concern such as recruitment, promotion, career posting, training, working environment, staff welfare, office security and safety. The Committee is chaired by the Deputy Commissioner (Operations) and composed of representatives from all staff unions / associations and staff groups in the Department.

The General Grades Consultative Committee

The General Grades Consultative Committee, chaired by the Departmental Secretary, allows staff members of the common and general grades to discuss with the management issues of specific interest to their grades.

The “Meet-the-Staff Programme”

First launched in 1996-97, the “Meet-the-Staff Programme” enables the senior management of each Unit and staff of different sections / groups to exchange ideas face to face on departmental and service-wide issues in an open and relaxed manner. It serves to supplement the formal consultative channel and effectively enhances communication between staff and the management.

The IRD Staff Suggestions Scheme

In 2015-16, 2 out of 7 suggestions made through the IRD Staff Suggestions Scheme were granted cash awards and certificates of commendation in recognition of their contributions on enhancing operational efficiency and quality of services of the Department.

The Inland Revenue Department Newsletter

The Departmental Newsletter, issued quarterly, is another channel of communication between staff and the management and serves to promote a sense of belonging in the Department. Articles are contributed by unit management for disseminating service- related issues, staff movement, staff welfare, information technology, environmental and green issues, occupational and safety matters, etc.. Staff are also keen to share their leisure activities and hobbies. The Newsletter further provides a regular roundup on the recreational activities organised by the IRD Sports Association as well as volunteer activities arranged by the IRD Volunteer Team.

The Inland Revenue General Staff Welfare Fund

Established in 1972, the Inland Revenue General Staff Welfare Fund operates on funds donated by staff on a voluntary basis. It aims to provide within a short time small amount of interest free loan, as an additional and quick emergency relief, to help staff in unexpected financial hardship. The Fund is managed by a Governing Committee, chaired by the Departmental Secretary and composed of staff representatives from the Departmental Consultative Committee, the General Grades Consultative Committee and the IRD Sports Association. The Claims Sub- committee, formed under the Governing Committee, considers and approves applications for financial assistance submitted by staff.

Commissioner’s Commendation Letter Scheme

In 2015-16, 39 officers who had provided outstanding service for a long period of time were awarded the Commissioner’s Commendation Letter. The presentation ceremony was held in April 2016.