論資遣費對資遣率之影響:以台灣2005年勞退新制為例 - 政大學術集成

50

0

0

全文

(2) 謝辭 這篇論文能夠順利完成,首先要感謝我的指導教授 – 陳鎮洲老師,老師不 僅在每一次的 meeting 中都非常細心的檢查我的論文進度內容,提出許多可以改 進的部分,而且對於我的想法與做法往往都給予很肯定的回應,讓我有許多空間 去發揮嘗試,使得我在從尋找論文的題目到順利通過口試的過程中,透過老師的 指導協助,真的充分體驗到做研究會遇到的種種環節與問題,並也學到了許多獨 立自主解決問題的能力。此外,由於我的論文是以英文書寫,因此光是文意邏輯 的表達上就有許多的困難,而老師不論是繁瑣的標點符號,或是整體文章敘述的. 政 治 大 除了我的指導教授之外,在兩年的碩士生涯中,也很感謝所有系上的必修課 立. 通順與否,都非常耐心的逐一檢查並給予修正,真的是非常感謝老師。. ‧ 國. 學. 與選修課老師,不論這些課程內容是否直接與我的論文,甚致是未來的就業有關, 我都很開心能夠修習這些課程,讓我對於經濟學這樣一門博大精深的學問能夠更. ‧. 加窺知一二。而其中特別要感謝的是李浩仲老師,在碩一下結束的暑假中因為擔. sit. y. Nat. 任老師的助理而有機會閱讀大量的英文 paper,並從中學到了許多有關勞動經濟. n. al. er. io. 學的計量方法與議題,對於日後的論文寫作有莫大的幫助。. i Un. v. 能夠順利渡過這兩年,還要感謝所有碩士班同學們的陪伴,雖然我們這屆的. Ch. engchi. 人數特別少,卻也因此使得大家能夠更容易凝聚在一起,不論是聚餐、班遊、畢 業照團拍等活動,我們都擁有極高的出席率,相信這在一般的碩士班裡面是非常 不容易的事!而有關課業上的各種大小事,也都是班上同學們互相扶持,一起努 力克服解決的,只能說:「認識你們,有你們真好!」 最後,即將邁入職場,心情不免有著許多期待,也有許多不安,然而,不變 的是永遠在一旁支持、關心我的家人們,感謝你們一路上的呵護關愛,讓我可以 順利的完成學業,也謝謝所有鼓勵我前進的朋友們! 吳智鳴 謹誌於 國立政治大學經濟學系 中華民國一百零二年六月.

(3) 論資遣費對資遣率之影響: 以台灣 2005 年勞退新制為例. 研究生:吳智鳴 指導教授:陳鎮洲 博士. 摘要 政 治 大 本研究以 2005 年勞退新制為例,探討資遣費對資遣率之影響。在勞退新 立. ‧ 國. 學. 制實施之後,資遣費的給付額度不僅大幅減少,還多了上限,因此,基於資遣費 往往被視為雇主所直接面對的資遣成本,資遣率是否會受到勞退新制中資遣費改. ‧. 變的影響,為本研究欲探討分析的議題。本研究資料來源為人力運用擬-追蹤調. sit. y. Nat. 查資料庫,研究方法使用差異中之差異法(difference in differences),並依. n. al. er. io. 據員工是否適用於勞基法,將樣本劃分為實驗組與對照組進行分析。實證結果顯. i Un. v. 示,資遣費對於資遣率並無顯著的影響力,因此政府若希望資遣費制度能有預防. Ch. engchi. 雇主任意資遣員工的效果,則現行的資遣費制度可能無法達到此目標,而未來是 否需要針對資遣費進行修法仍有討論空間。. 關鍵字:資遣費、資遣率、差異中之差異法、勞動退休金條例、台灣.

(4) The Impact of Severance Pay on Layoff Rate: Evidence from 2005 Labor Pension Act in Taiwan. Graduate Student: Chih Ming Wu Advisor: Dr. Jenn Jou Chen. This study uses. Abstract 治 政 大 the 2005 Labor Pension Act (LPA) 立. in Taiwan as the. ‧ 國. 學. quasi-experiment to analyze the impact of severance pay on the layoff rate. After implementation of LPA, severance pay is reduced significantly and constrained by an. ‧. upper boundary. Since severance pay is often considered as the firing cost, whether. Nat. sit. y. the layoff rate is affected by the largely reduced severance pay is what this study. n. al. er. io. expects to analyze. Data used in this study are drawn from the Manpower Utility. i Un. v. Quasi – Longitudinal Survey (MUQLS). In order to apply the difference in. Ch. engchi. differences method, the observations are divided into the treatment group and the reference group according to the coverage of the Labor Standards Act (LSA). The empirical results suggest that severance pay has no significant impact on the layoff rate. Therefore, if severance pay is expected to prevent the arbitrary layoff, the current severance pay system might not achieve this goal and some modifications of this system might be necessary.. Key words: Severance pay; Layoff rate; Difference in differences; Labor Pension Act; Taiwan.

(5) Index 1. Introduction ................................................................................................................ 1 2. Labor Pension Act ...................................................................................................... 8 3. Data .......................................................................................................................... 12 4. Model ....................................................................................................................... 16 5. Descriptive Statistics ................................................................................................ 22 6. Results ...................................................................................................................... 25 7. Conclusion ............................................................................................................... 31 Reference ..................................................................................................................... 33. 治 政 Appendix ...................................................................................................................... 35 大 立 ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i Un. v.

(6) Index of Tables Table 1: Comparison of Severance Payment Systems between LSA and LPA ........... 11 Table 2: Summery Statistics (2000-2011) .................................................................... 22 Table 3: Basic Characteristics of Laid off Employees and non-Laid off Employees .. 24 Table 4: The Frequency Table of Layoff between Reference Group and Treatment Group (Before and After LPA, 2000-2011) ................................................... 24 Table 5: Impacts of the Severance Pay on the Layoff Rate (Average Marginal Effects) ........................................................................................................................ 30 Table A1: Employees Who Are Not Applicable to LSA .............................................. 35. 治 政 Table A2: Classification Rules of Reference Group and大 Treatment Group ................. 36 立 Table A3: The Variation of the Coverage of LSA and the Corresponding Classification ‧ 國. 學. Rules ............................................................................................................ 40. ‧. Table A4: Data of Layoff Proportions from 2000 to 2011 ........................................... 43. n. er. io. sit. y. Nat. al. Ch. engchi. i Un. v.

(7) Index of Figures Figure 1: Casual Effects in the Difference In Differences Model ............................... 19 Figure 2: Proportions of Laid off Employees from 2000 to 2011................................ 19 Figure 3: Shares of Reference Group and Treatment Group from 2000 to 2011......... 21. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i Un. v.

(8) 1. Introduction The issue of job security regulations has been a very important topic in labor economics. Many studies have used evidence from their respective countries to analyze the impacts of job security regulations on the labor market. In this context, one of the mostly analyzed regulations is the severance pay, which is often considered as the cost of firing an employee. Severance pay is a payment required to be made by the employer when an. 政 治 大 specific reasons. Precise regulations 立 with regard to severance pay are different across. employee is laid off, or when an employee leaves the firm voluntarily for some. ‧ 國. 學. countries. For example, severance pay can be very large in some undeveloped countries but relatively small in some developed countries. Generally, the difference. ‧. in severance payment systems across countries is usually caused by different expected. Nat. sit. y. usage of the severance pay.. n. al. er. io. According to Wu (2005), the usage of severance pay can be summarized into five. i Un. v. ways from a legal viewpoint. First, it can be taken as substitute for unemployment. Ch. engchi. insurance, as well as compensation for retirement pension when the employee is laid off before retirement. Second, when the employee is laid off involuntarily, the employer can use severance pay to compensate the employee for letting him/her be unemployed. Third, it can help ease the financial burden of the employee during the period of job search. Fourth, severance pay can also be taken as postponed wages. But in reality, there are few countries which have legislated severance payment regulation from this viewpoint. Fifth, employer can appreciate the employee for contributions in the past years by paying severance pay. Besides, Kuo (2000) also indicates that severance pay can reduce the incentive for the employer to lay off the employee 1.

(9) arbitrarily. In other words, severance pay regulations can prevent or discourage arbitrary layoffs to some extent. As described above, severance pay can be used in many ways, and regulations are decided by the expected usage of the payment. Usually, severance pay is regarded as an appealing regulation in developing countries (Parsons 2011) and the reason might be that most of the labor security regulations in these countries are not complete and thus severance pay plays a relatively important role in their labor market. At present, developing counties such as Taiwan, South Korea, Hong Kong and Singapore have severance pay systems in place. Besides, undeveloped countries such as China,. 治 政 India, Malaysia and Thailand also have their own severance 大 pay systems (Huang 立 2006). ‧ 國. 學. Although there are relatively few developed countries which have specific. ‧. severance pay systems, some kinds of regulations which are very similar to severance. sit. y. Nat. pay are legislated in these countries also. In Germany, a payment called “Abfindung”. io. er. is made when the layoff is illegal and the laid off employee tends to leave the firm. al. instead of going back. The corresponding amount then depends on the position of the. n. iv n C employee in the firm, and what thehemployer can afford. e n g c h i U Since such kind of payment can be taken as compensation for unemployment, one can regard it as severance pay (Wu 2005). Different from Germany, severance pay in Japan seems more like a part of the retirement pension system. To be specific, job displacement payment is made when an employee leaves the firm before the regulated job seniority, and the corresponding amount is just the accumulated retirement pension payment based on the job seniority (Lin 2000). Since the job displacement payment can be used as compensation for unemployment and financial support during the period of job search, it can be regarded as severance pay. 2.

(10) In Taiwan, the severance payment system is directly regulated by provisions in the Labor Standards Act (LSA) and is isolated from the retirement pension payment. According to LSA, severance pay is required to be paid when the employee is laid off involuntarily due to reasons such as business contraction, shutdown or personnel adjustment. Besides, severance pay can also be mandatory when the employee voluntarily quits the job for some specific reasons listed in LSA. Before implementation of the Labor Pension Act (LPA) in 2005, severance pay under LSA used to be the substitution of unemployment, compensation for retirement pension payment and prevention of arbitrary layoffs. Therefore, despite the severance. 治 政 pay system of Taiwan being very similar with England 大and Australia, the amount of 立 severance pay is much larger in Taiwan. However, after implementation of LPA, the ‧ 國. 學. usage of severance pay is mainly for prevention of arbitrary layoffs and the amount of. ‧. payment has become very small. Therefore, whether the layoff decision of the. io. er. to analyze by using some appropriate econometric methods.. sit. y. Nat. employer is affected by the reduced severance pay is exactly what this study expects. al. When it comes to severance pay, most studies refer to Lazear (1990), which has. n. iv n C reported some important empiricalhresults. Theoretically, e n g c h i U severance pay can have no effect in a perfect market when a properly designed labor contract is there (Lazear. 1987). However, using macro data from 22 OECD countries over 29 years, Lazear (1990) found that even the employer can choose to hire part-time or temporary employees in order to avoid severance pay, severance pay and advance notice requirements still reduces employment. Also, severance pay is supposed to discourage the willing of labor participation, thus reducing the labor force and increasing the unemployment. Different from Lazear (1990), Kugler (1999) used the repeated-cross sectional data from Colombian National Household Survey (NHS) to analyze the impact of the 3.

(11) Colombia labor market reform of 1990 on labor turnover where an important policy change is a substantial reduction of severance pay. To examine the corresponding impacts before and after the reform, difference in differences method is applied by taking the employees in the former sector as the treatment group. The empirical results show that increased firing cost reduces unemployment only when the effect of the exit hazard rate on unemployment is greater than the exit hazard rate when out of unemployment, and vice versa. Instead of analyzing employment, unemployment or turnover, Marinescu (2009) focuses on the impact of layoff rate by analyzing the British policy change in 1999.. 治 政 After this reform, the tenure required for entitlement 大to protection against unfair 立 layoff dropped from 24 to 12 months. This means employees with 12 to 23 months of ‧ 國. 學. tenure cannot be unfairly laid off easily as before. Therefore, firing cost increased. ‧. substantially as the policy change extended the coverage of employees to whom the. sit. y. Nat. severance pay system is applicable. Data drawn from the U.K. Labour Force Survey. io. er. (longitudinal data) is used, and the difference in differences method is applied by. al. using employees with 24 to 48 months of tenure as the reference group. The empirical. n. iv n C results show that firing hazard for h workers with 12 to e n g c h i U23 months of tenure decreases by 26 % relative to the reference group, which is consistent with the expectation. Recently, there have been a lot of studies which have examined the impact of severance pay on the labor market. For example, Hofer, Schuh and Walch (2011) use the Austria Employment Protection Legislation (EPL) reform of 2002 to examine the impact of severance pay on voluntary separation. However, the results suggest that severance pay has only limited impacts. Bassanini and Garnero (2012) exploit a unique dataset to compare hiring and separation rates between different OECD countries and businesses or industry sectors over 13 years. By decomposing the effect of regulations on number of layoffs, their results show that severance pay appears to 4.

(12) have no significant impacts on worker flows. Actually, severance pay is often a small part of a policy reform, which makes estimation of the effect of severance pay in isolation very difficult (Parsons 2011). Except for Bassanini and Garnero (2012), none of the studies mentioned above isolate the effects of severance pay from other broader interventions and, therefore, they may have attributed too much to severance plans. Moreover, Parsons (2011) reviews a lot of severance pay related empirical literatures and finds that “severance benefit mandates, unaccompanied by other labor regulations, have little apparent impact on labor market behaviors.”. 治 政 While earlier studies have often neglected effects大 from other regulations, recent 立 studies tend to suggest that severance pay has only modest or no impacts on the labor ‧ 國. 學. market. It is interesting to examine the effect of the reduced severance pay on the. ‧. layoff rate in Taiwan.. sit. y. Nat. Until now, papers which discuss the relationship between severance pay and the. io. er. labor market of Taiwan are mainly based on the legal viewpoint. Only a small number. al. of papers have examined the impact of severance pay on the labor market of Taiwan. n. iv n C by using econometric methods. For (2006) analyzed the impact of h example, e n g cHuang hi U severance pay on the unemployment rate by using macro data which include undeveloped and developing countries of eastern Asia over the period 1980 to 2003. The results show that for undeveloped countries, severance pay has negative effects on unemployment rate in the short as well as the long run. And for developing countries, severance pay has negative and positive effects on the unemployment rate, short run and long run. In this study, based on micro data set, the implementation of the Labor Pension Act (LPA) in Taiwan is used as a quasi-experiment for examining the effect of severance pay on layoff rate. The policy change involves two important regulations. 5.

(13) First, retirement pension system has changed from defined benefit plan (DB) into defined contribution plan (DC). Second, severance pay for involuntary separation is reduced significantly, while the eligibility conditions for severance pay have remained unchanged. Since only severance pay is directly considered as the firing cost, identifying the effect of severance pay is not that difficult; one would naturally expect the effect on the layoff rate to be positive (i.e. it would rise). Nevertheless, it is worth noticing that in the new pension system, employers are forced to contribute to retirement pension for the employees. Therefore, employers might be more inclined to recruit employees. 治 政 who might not be laid off in the future. Besides, Blanchard 大 and Katz (1997) indicate 立 that firing cost may affect the efficiency of sorting workers into the jobs they are best ‧ 國. 學. suited to, thus affecting productivity. As a result, employees hired after the reform. ‧. might meet the expectations of the employers and have higher productivity, resulting. sit. y. Nat. in a lower layoff rate.. io. er. Whether an employee had been laid off in the last year could be observed by. al. using the quasi-longitudinal data and the information with regard to the last job was. n. iv n C used as control variables. Besides, h difference in differences e n g c h i U method is used to capture the effect of policy change by controlling the common time trends. Definition of the treatment and reference group is based on what kind of protection an employee was entitled to. To be specific, employees to whom LSA was applicable are defined as the treatment group, and employees to whom LSA was not applicable are defined as the reference group. This study uses many different windows of observations to analyze severance pay effects and most of the results suggest that severance pay has no significant effect on the layoff rate. After dropping observations difficult to identify, i.e. whether they are affected by the reduced severance pay or affected only by the reduced severance 6.

(14) pay, there is still no significant correlation between severance pay and layoff rate. However, despite these results not being so surprising, as recent studies have shown, some constraints of this study could still affect the accuracy of the estimation for the effect of severance pay. The rest of this study is organized as follows. Section 2 describes details of the Labor Pension Act (LPA) and outlines how it is different from the Labor Standard Act (LSA). It also mentions the reasons why the government wants to implement this reform. Section 3 briefly describes the dataset used in this study and explains the process of classifying the treatment and reference groups as well. Section 4 explains. 治 政 the simple idea of the difference in differences method 大 and the corresponding 立 assumptions. Section 5 presents descriptive statistics and Section 6 shows the results. ‧ 國. 學. Section 7 presents the conclusions and some constraints faced in this study.. ‧. n. er. io. sit. y. Nat. al. Ch. engchi. 7. i Un. v.

(15) 2. Labor Pension Act In Taiwan, labor can be divided into two groups: those to whom the Labor Standards Act (LSA) is applicable and those not covered by LSA. The latter group includes occupations such as teachers, doctors and employees in the public sector; these occupations have their corresponding regulations of labor contracts. However, employees covered by LSA still account for bulk of the labor force. LSA, which was implemented in July 1984, regulated all labor contracts (except for employees to whom LSA is not applicable) until implementation of the Labor. 政 治 大 of LPA are the retirement pension system and the severance payment system. 立. Pension Act (LPA) in July 2005. The two major policy changes after implementation. ‧ 國. 學. The severance payment system of LSA requires the employer to pay a severance pay pursuant to Article 11, Article 13, Article 14 and Article 20 (Table 1). According. ‧. to these regulations, one can divide the obligation of severance pay into two situations.. sit. y. Nat. First, severance pay is mandatory when the layoff is caused by reasons such as. io. al. er. business contraction, shutdown or personnel adjustment. Second, the employer has to. v. n. pay a severance pay when the employee voluntarily leaves the firm due to negative. Ch effects on his/her life or health.. engchi. i Un. The amount of severance pay depends on the period of time for which the employee has worked in the firm continuously. According to Article 17 of LSA, the employee has to be paid a severance pay equal to the average monthly wage drawn during his/her tenure at the firm for every year of the tenure. Thus there are no constraints on the amount of severance pay; the severance pay can be a large amount if the employee has worked at the firm for a long time. The retirement pension system in LSA is defined benefit plan (DB), and it requires that the employee work in the same firm. That is, the job seniority used to 8.

(16) measure the retirement pension payment will be zero once the employee leaves the firm. However, in Taiwan, most of the firms are medium or small sized enterprises and they operate for only about 13 years on average. Besides, employees change jobs every eight years on average. As a result, more than 75% of the employees cannot receive the retirement pension payment offered by the firm under the pension system of LSA (Chang 2004). Since retirement pension pay is difficult to receive, the expensive severance pay can be regarded as the compensating payment for the laid off employee. Also, the Employment Insurance Act had not been implemented until 1999 and thus severance. pay can reduce such incentives to some extent.. 學. ‧ 國. 治 政 pay can be viewed as a substitute of unemployment insurance 大 as well. And, to avoid 立 the fact that firms might tend to lay off employees who are going to retire, severance ‧. To improve the retirement pension system, the LPA has changed the system from. sit. y. Nat. defined benefit plan (DB) to defined contribution plan (DC). Under the defined. io. er. contribution plan, the employer has to contribute 6 % of the monthly wage of the. al. employees to their individual accounts for labor pension at the Bureau. And the most. n. iv n C employees leave the firm without h ecan ngchi U. important change is that. breaking off the. accumulation of the job seniority. That is, the job seniority can be accumulated across different jobs. As a result, the employees can receive the retirement pension for sure once they reach the required age and job seniority in the new pension system. However, implementation of LPA does not force every employee who was originally covered by LSA to choose the new pension system. In fact, employees can decide whether the plan can bring more benefits, depending on the current job seniority or some other factors. Employees who opted for the old pension system (LSA) were also allowed to switch to the pension system until June 2010. Only employees who had never worked before or had changed jobs after implementation of 9.

(17) the LPA had to choose the new pension system (LPA). Since the pension system has been reformed and unemployment insurance is implemented by the Employment Insurance Act in 1999, severance pay seems to have a much lower utility. Therefore, the amount of severance pay is inevitably reduced after the improvement of the pension system. According to Article 12 of LPA, for each year of work by the employee, severance pay is now only half of monthly wage. Moreover, severance pay cannot be more than six months of average wage. Compared to the LSA, the reduction in severance pay is obviously very large. As a measure to discourage arbitrary layoffs and to address the weak substitution. 治 政 of unemployment insurance (Lin 2000, Chang 2004),大 severance payment system has 立 still been retained in LPA, and the requirements of severance pay are the same as LSA. ‧ 國. 學. Besides, an employee can either receive the retirement pension pay or the severance. ‧. pay when he/she leaves the firm before implementation of LPA. However, it is. sit. y. Nat. possible for employees to receive both retirement pension and severance pay by. io. er. choosing LPA. Moreover, LPA enables employees to change job without worrying. al. about loss of job seniority, thus increasing the dynamics of the labor market. However,. n. iv n C at the same time, whether the reduced pay increases the incentive for firing h eseverance ngchi U has become an important topic which deserves to be analyzed.. 10.

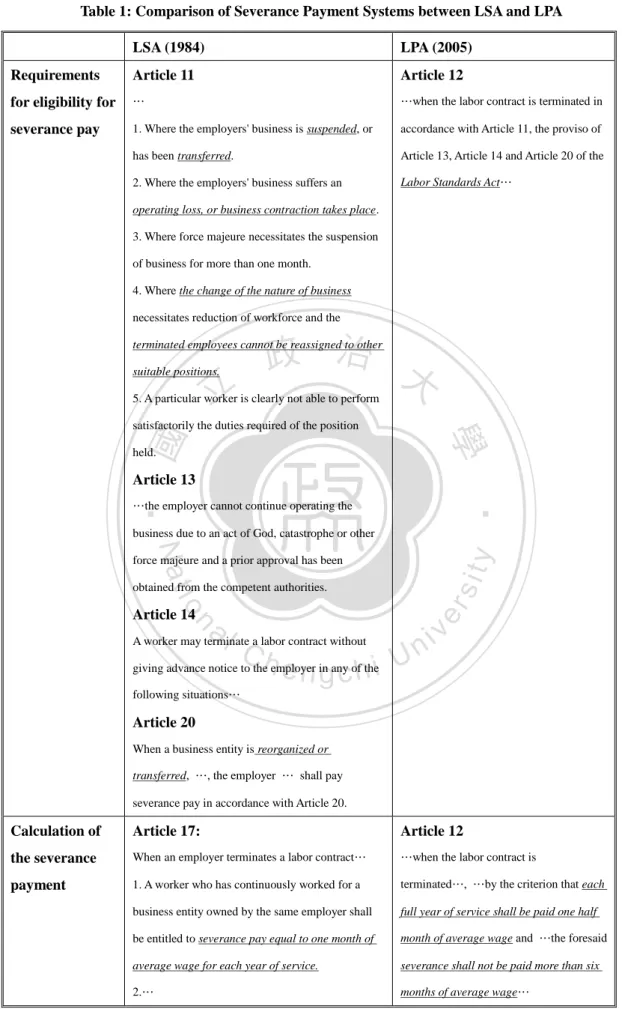

(18) Table 1: Comparison of Severance Payment Systems between LSA and LPA LSA (1984). LPA (2005). Requirements. Article 11. Article 12. for eligibility for. …. …when the labor contract is terminated in. severance pay. 1. Where the employers' business is suspended, or. accordance with Article 11, the proviso of. has been transferred.. Article 13, Article 14 and Article 20 of the. 2. Where the employers' business suffers an. Labor Standards Act…. operating loss, or business contraction takes place. 3. Where force majeure necessitates the suspension of business for more than one month. 4. Where the change of the nature of business necessitates reduction of workforce and the. 政 治 大. terminated employees cannot be reassigned to other suitable positions.. 立. 5. A particular worker is clearly not able to perform. ‧ 國. 學. satisfactorily the duties required of the position held.. Article 13. ‧. …the employer cannot continue operating the business due to an act of God, catastrophe or other. y. Nat. sit. force majeure and a prior approval has been. io. al. n. Article 14. er. obtained from the competent authorities.. i n C U giving advance notice to theh employer in any of thei eng ch A worker may terminate a labor contract without. v. following situations…. Article 20 When a business entity is reorganized or transferred, …, the employer … shall pay severance pay in accordance with Article 20.. Calculation of. Article 17:. Article 12. the severance. When an employer terminates a labor contract…. …when the labor contract is. payment. 1. A worker who has continuously worked for a. terminated…, …by the criterion that each. business entity owned by the same employer shall. full year of service shall be paid one half. be entitled to severance pay equal to one month of. month of average wage and …the foresaid. average wage for each year of service.. severance shall not be paid more than six. 2.…. months of average wage…. Source: Labor Standards Act and Labor Pension Act of Taiwan (translated by council of labor affairs) 11.

(19) 3. Data The data used to analyze the impact of implementation of Labor Pension Act (LPA) on layoff are drawn from the Manpower Utilization Quasi-longitudinal Survey (MUQLS). MUQLS is constructed from the Manpower Utilization Surveys (MUS) of Taiwan by linking the overlapping observations for two consecutive years. And MUS, which is a cross-sectional database, was started in 1978 and is administered in May each year. MUS provides a lot of information such as workplace, occupation, income and. 政 治 大 Therefore, MUQLS generated from MUS does not only let individual observations 立 job seniority which can be used when analyzing human resources related topics.. ‧ 國. 學. become repeatedly observable but also provide more valuable information. As described in Section 1, employees not covered by the Labor Standards Act. ‧. (LSA) are treated as the reference group for applying the difference in differences. sit. y. Nat. method. However, information from MUQLS does not directly tell us whether an. io. er. employee is covered by LSA. Therefore, it is necessary to formulate some. al. iv n C U the Council of Labor Affairs, h e nannounced According to the latest regulations g c h i by n. classification rules to specify which group the employee belongs to.. industries and occupations listed in Table A1 are not covered under LSA. Classification as treatment group and reference group is according to this information. However, some industries or occupations listed in Table A1 cannot be easily defined to match with occupations mentioned in MUQLS. For example, employees hired in private schools are not applicable to LSA; instead, they are protected by the Private School Law. And, unfortunately, MUQLS takes all education related jobs as one occupation, making the classification difficult to execute. Therefore, both subjective and objective classification rules are required for classification. Table A2 12.

(20) lists all classification rules used to specify which groups do the occupations mentioned in MUQLS belong to. Basically, there are three objective classification rules, linkages of industries, occupations and sectors of employer. The first two are straightforward and provide most of the necessary information to execute the classification. However, some kinds of occupations are not applicable to LSA only if the employer is a public sector organization. For example, employees hired in hospitals (except for doctors and some crafts, blue collar and menials) are not covered by LSA only when the hospitals belong to the public sector. Thus, knowing the sectors of employers can help divide. 治 政 the employees into treatment group and reference group 大more accurately in such kinds 立 of situations. ‧ 國. 學. When information provided from objective classification rules is not sufficient. ‧. for classification, some subjective classification rules are required. In general, the. sit. y. Nat. level of income and scale of the workplace can be helpful when classifying some. io. er. kinds of jobs. For example, doctors, lawyers and accountants are the jobs which have. al. relatively higher incomes. Hence, using the general standard level of income for such. n. iv n C jobs can be an appropriate way tohdistinguish themUfrom the relatively low-skilled engchi jobs in the same industries. Information of the scale of workplace is also useful for distinguishing jobs which belong to the same industry but are different in terms of the scale of workplace. For example, it is difficult to segregate employees in private schools from a relatively rough classification of occupations such as the education industry. Moreover, employees in cram schools are covered by LSA but the corresponding information makes it hard to distinguish them from those hired in private schools. However, despite both being education-related jobs in private sector, private schools generally hire more employees than cram schools. As a result, setting an appropriate interval of 13.

(21) the scale for private schools could be a reasonable way to define employees of private schools. Still some industries or occupations need to be eliminated due to the movement from being not covered by LSA to coverage under LSA because of the policy change. For example, employees hired in labor unions were originally not covered under the Labor Standards Act earlier but LSA became applicable to them after 1 December in 2003. To assure the accuracy of difference in differences model (see Section 4 for details), it is necessary to eliminate such kinds of observations so that the composition of the treatment group and the reference group remains unchanged. Table A3 lists all. 治 政 such industries and occupations with corresponding classification rules, which are the 大 立 same as the rules used in Table A2. 1. ‧ 國. 學. After completing the classification for the treatment group and the reference. ‧. group, as well as the elimination of inconsistent observations, laid off employees need. sit. y. Nat. to be defined. As mentioned above, MUQLS is a repeated cross-sectional database. io. al. er. where each employee can be regarded as having been investigated twice, in two. n. consecutive years. Therefore, whether an employee has been laid off or not depends on the information in the. Ch second. eobservation ngchi. iv n year; U information. from the first. observation year is used to control the individual characteristics. The MUQLS asked two important questions to respondents, related to the state of employment. The first asks about the number of times the respondent had changed jobs in the last year. The second asks about the reasons for changing the job if the employee did change job in the last year. Moreover, possible reasons listed in response to the second question include voluntary reasons such as “salary is not fair”, “workplace environment is not ideal”, “no prospects”, “lack of job security” and. 1. After eliminating all inconsistent observations, on average, there are about 7000 employees covered by LSA and about 800 employees to whom LSA is not applicable, in each year. 14.

(22) involuntary reasons such as “business contractions”, “shutdown” , “personnel adjustment”, “marriage or birth”, “retirement”, etc. According to the Labor Standards Act, layoff caused by situations such as “businesses are suspended”, “business contractions”, “terminated employees due to the change of nature of business cannot be transferred to proper positions” require the employer to pay severance pay. As a result, by combining the information from MUQLS and the definition from the Labor Standards Act, laid off employees can be defined. And here is the definition: laid off employees are employees who have ever been laid off in the last year due to business recession, shutdown or personnel adjustment.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 15. i Un. v.

(23) 4. Model In order to evaluate the impact of implementation of the Labor Pension Act on layoff rate, employees are divided into treatment and reference groups, to apply the difference in differences strategy as described before. Besides, whether an employee has been laid off also divides employees into two groups. One of them cover employees who have ever been laid off in the last year due to business recession, shutdown or personnel adjustment, and the corresponding outcome variable LAYOFF is assigned the value of 1. The other group covers employees who have not been laid. 政 治 大. off in the last year and hence the corresponding outcome variable is assigned the. 立. value of 0.. ‧ 國. 學. Since the outcome variable LAYOFF, which indicates whether an employee has ever been laid off is a binary variable, probit regression is estimated as follows:. ‧. sit. y. Nat. 𝐿𝐴𝑌𝑂𝐹𝐹 ∗ = 𝛽𝑋 + γ1 𝐿𝑆𝐴 + 𝛾2 𝐼𝑀𝑃 + 𝛾3 𝐿𝑆𝐴 ∗ 𝐼𝑀𝑃 + 𝜀. er. io. 𝐿𝐴𝑌𝑂𝐹𝐹 = 1 if 𝐿𝐴𝑌𝑂𝐹𝐹 ∗ > 0, 𝑎𝑛𝑑 0 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒.. al. n. iv n C U regression with the standard h models where the first line of the regression e n g isc the h i latent normally distributed error term 𝜀, and the second line is an index function which depends on the value of the latent variable LAYOFF*. To control the individual characteristics, variables such as monthly income, gender, years of education, age, job seniority, household size, head of household and working area are all included in the vector 𝑋. Besides, all of the control variables are based on the job corresponding to the first observation year. To be specific, years of education are defined by the average number of years required in Taiwan to complete the corresponding highest education. 0 years are 16.

(24) assigned to those who have not ever attended formal education before; 6 years to elementary school; 9 years to junior high school; 12 years to senior high school; 16 years to college, 18 years to master degree and 22 years to doctoral degree. Household size means the number of members over the age of 15 in the family. Job seniority is measured in years as the education. Whether an employee is the head of the household or not is indicated as a dummy variable. Besides, working area of the employee is controlled by setting three dummy variables which indicate northern area, central area, southern area and the eastern area. Also, when the sample analyzed includes the year of 2008, then dummy variable is set to control the possible effect caused by the subprime crisis.. 立. 政 治 大. The main variables used to derive the difference in difference estimates are LSA,. ‧ 國. 學. IMP and their interaction term LSA*IMP. LSA is a dummy variable which indicates. ‧. application of the Labor Standards Act and takes the value of one if an employee is. sit. y. Nat. covered under the Labor Standards Act. IMP is a dummy variable which takes the. io. er. value of one when the observation is investigated in the period after implementation. al. of Labor Pension Act. Moreover, the interaction term LSA*IMP takes value of one. n. iv n C when the employee is covered under Standards Act and also belongs to the h ethenLabor gchi U period after the policy change. The expected difference of layoff rates of the reference group before and after the policy change is. E(LAYOFF|LSA = 0, IMP = 1) − E(LAYOFF|LSA = 0, IMP = 0) = 𝛾2. and the expected difference of layoff rates of the treatment group before and after the policy change is 17.

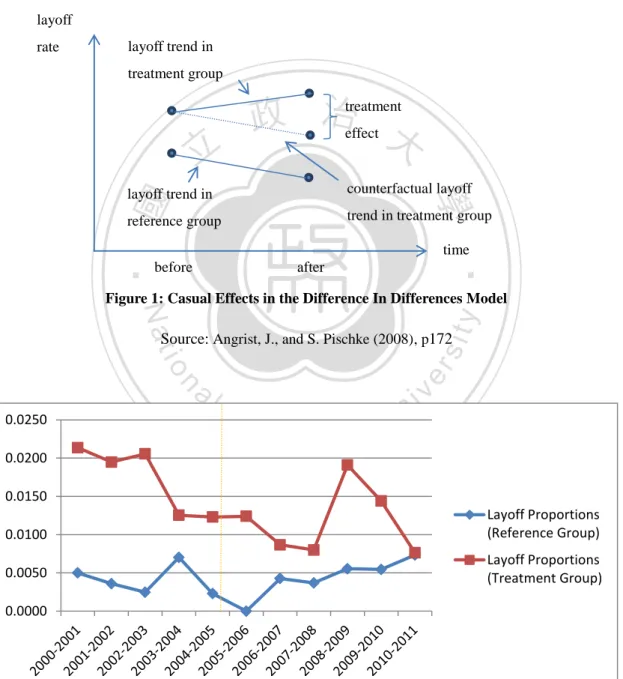

(25) E(LAYOFF|LSA = 1, IMP = 1) − E(LAYOFF|LSA = 1, IMP = 0) = 𝛾2 + 𝛾3. Therefore, difference in differences estimate is. [E(LAYOFF|LSA = 1, IMP = 1) − E(LAYOFF|LSA = 1, IMP = 0)] −[E(LAYOFF|LSA = 0, IMP = 1) − E(LAYOFF|LSA = 0, IMP = 0)] = (𝛾2 + 𝛾3 ) − 𝛾2 = 𝛾3. which is just the coefficient of the interaction term LSA*IMP and exactly indicates. 治 政 the effect of the Labor Pension Act. 大 立 Usually, the common trends assumption has to be satisfied when applying the ‧ 國. 學. difference in differences method. Referring to Joshua and Jöhn-Steffen (2008), Figure. ‧. 1 illustrates the conceptions of the common trends assumption and the deviation. sit. y. Nat. induced by the treatment. From Figure 1, one can see that the reference group only. io. er. faces the trend effect, and the treatment group faces both trend effect and treatment. al. effect. In order to find the treatment effect, one has to specify these two effects by. n. iv n C taking the trend of the reference group counterfactual measure of the treatment h easn the gchi U group. Therefore, the trend faced by the treatment group and reference group have to be the same; otherwise the counterfactual measurement could be biased, causing inaccuracy in difference in differences estimates. Here, common trends assumption requires that the trend of layoffs before implementation of the Labor Pension Act should be the same for all employees, irrespective of whether they are covered by the Labor Standard Act or not. Data of multiple periods are used to investigate the common trends assumption. Table A4 shows the proportion of laid off employees from 2000 to 2011 and Figure 2 plots all of them to show the long run trends. From Figure 2, one can see that the 18.

(26) layoff proportions of the treatment group declined gradually before implementation of LPA. After implementation of LPA, its trend became noisy. At first, it continued to decline from 2006 to 2007, but then rose dramatically in 2008 which is the year of the subprime crisis. After 2008, it declined again and reached the same level as the reference group.. layoff rate. layoff trend in treatment group. 立. 政 治treatment effect 大 counterfactual layoff. reference group. trend in treatment group. ‧ 國. 學. layoff trend in. ‧. time. before. after. sit. y. Nat. Figure 1: Casual Effects in the Difference In Differences Model. io. n. al. er. Source: Angrist, J., and S. Pischke (2008), p172. 0.0250. Ch. engchi. i Un. v. 0.0200 0.0150 0.0100. Layoff Proportions (Reference Group). 0.0050. Layoff Proportions (Treatment Group). 0.0000. Figure 2: Proportions of Laid off Employees from 2000 to 2011 Note: The dash line indicates the time of implementation of Labor Pension Act. 19.

(27) Like the treatment group, layoffs of the reference group also declined before implementation of LPA, except for the period from 2003 to 2004. After LPA, it has a relatively stable trend compared with the treatment group. Therefore, it seems that employees not covered by LSA can provide a good measure of counterfactual layoff rate before implementation of the LPA. However, there are still some facts that need to be addressed before analyzing results of the regressions. Actually, using the fact whether employees are covered by LSA as the standard of segregating employees into treatment and reference groups can cause some bias in results.. 治 政 First, implementation of the Labor Pension Act did 大not force all employees who 立 were originally covered under the Labor Standards Act to choose the Labor Pension ‧ 國. 學. Act. Only employees who had never worked before or changed the job after. ‧. implementation of LPA were forced to choose it. As a result, employees who were. sit. y. Nat. originally under the Labor Standards Act may still choose LSA so that the severance. io. er. pay would not change when they are laid off. Such kinds of situations can cause. al. inconsistencies within the treatment group. That is, some employees in the treatment. n. iv n C group may not be affected by the reduction pay. To deal with such kinds h e n gofcseverance hi U. of situations, employees who tend to choose LSA rather than LPA are eliminated according to some specific conditions. Section 6 describes the process in detail. Second, given that most of the employees who are not covered by the Labor Standards Act are public servants, selection bias may be a problem. Most employees in the public sector are generally risk averse and they do not tend to expose themselves to situations which may induce layoff. Therefore, the effect of the change of time may not be the same for the treatment group and the reference group. That is, the common trends assumption may be violated. However, Figure 2 shows that the trends for treatment and reference group seem to evolve similarly before the 20.

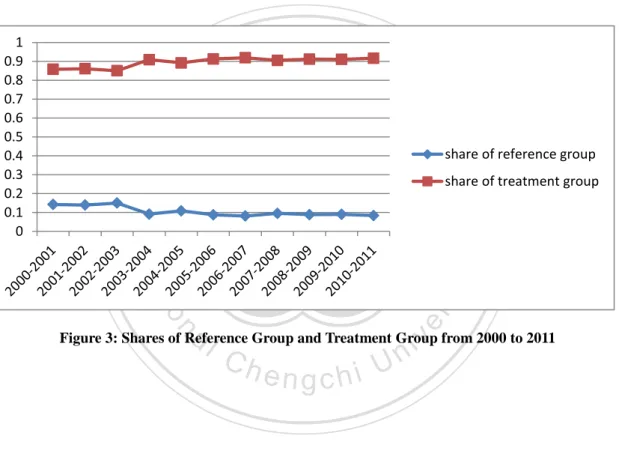

(28) implementation of LPA. Hence, such kinds of problems might not affect the results so much. Third, implementation of LPA may lead to reallocation of job. But this concern could be eliminated by comparing the shares of the two groups over the entire period from 2000 to 2011, as showed in Figure 3. The share of reference the group is 11% on average, and the share of the treatment groups is 89% on average. It seems shares of the two groups are very stable and do not have any apparently large change.. 立. 政 治 大. ‧ 國. 學. share of reference group share of treatment group. ‧. io. sit. y. Nat. n. al. er. 1 0.9 0.8 0.7 0.6 0.5 0.4 0.3 0.2 0.1 0. i Un. v. Figure 3: Shares of Reference Group and Treatment Group from 2000 to 2011. Ch. engchi. 21.

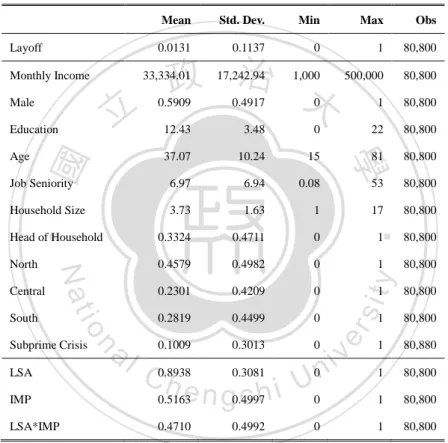

(29) 5. Descriptive Statistics The various time periods used to analyze the layoff rate are from 2000 to 2011. Table 2 lists the summary statistics for the period from 2000 to 2011, including mean, standard deviation, minimum, maximum and number of observations. After dropping observations with missing values, the sample size, which covers the period from 2000 to 2011, is 80800. Table 2: Summary Statistics (2000-2011) Mean. Std. Dev.. Min. Max. Obs. 0.0131. 0.1137. 0. 1. 80,800. 33,334.01. 17,242.94. 1,000. 500,000. 80,800. 0.5909. 0.4917. 0. 1. 80,800. 12.43. 3.48. 0. 22. 80,800. 37.07. 10.24. 15. 81. Job Seniority. 6.97. 6.94. 0.08. 學. 80,800. 53. 80,800. Household Size. 3.73. 1.63. 1. 17. 80,800. Head of Household. 0.3324. 0.4711. 0. North. 0.4579. 0.4982. 0. 0.2301. 0.4209. 0. 0.2819. 0.4499. 0. Layoff Monthly Income. 立. LSA IMP LSA*IMP. 80,800. 1. 80,800. y. al. n. Subprime Crisis. ‧. io. South. Nat. Central. 1. iv 0.3081 0n C0.8938 h e n g0.4997 0.5163 c h i U0 0.1009. 0.3013. 0.4710. 0.4992. 0. 0. 1. 80,800. 1. 80,800. 1. 80,880. 1. 80,800. 1. 80,800. 1. 80,800. sit. Age. ‧ 國. Education. er. Male. 政 治 大. Table 3 lists the differences in income, age, years of education, household size and job seniority between laid off employees and non-laid off employees. From Table 2, one can see that the average monthly income of laid off employees (27,555 NT dollars) is much lower than the average monthly income of non-laid off employees (33,411 NT dollars). This may imply that relative to employees who have higher monthly income, employees who have lower monthly income are more likely to be laid off. 22.

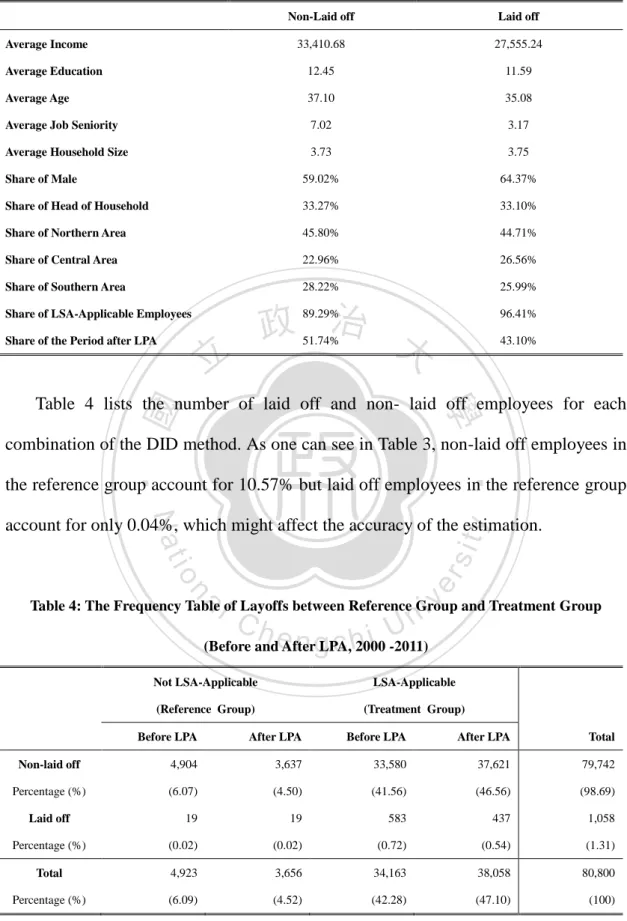

(30) From Table 3, one can also see that the average years of education for laid off employees and non-laid off employees are both around 12 years. The average age of laid off employees (35 years old) is slightly lower than the average age of non-laid off employees (37 years old). The job seniority of laid off employees (3.2 years) is much lower than non-laid off employees (7.0 years). The average household sizes are quite the same for both (3.7 people per household). Instead of listing mean values of dummy variables or categorical variables, Table 2 lists the corresponding percentage of these variables. One can see that males account for 59.02% of non-laid off employees and 64.37% of laid off employees. This. 治 政 suggests that males account for a higher percentage 大 of the laid off employees than 立 females. ‧ 國. 學. The heads of households account for 33.27% of non-laid off employees and. sit. y. Nat. similar proportions of heads of households.. ‧. 33.10% of laid off employees. It seems both non-laid off and laid off employees have. io. er. Employees who work in the northern area account for 45.8% of non-laid off. al. n. employees and 44.71% of laid off employees. Employees who work in the central area account for 22.96%. iv n C of non-laid and h e n goffc employees hi U. 26.56% of laid off. employees. Employees who work in the southern area account for 28.22% of non-laid off employees and 25.99% of laid off employees. It seems the distributions of working place are quite similar for both non-laid off and laid off employees.. 23.

(31) Table 3: Basic Characteristics of Laid off Employees and non-Laid off Employees Non-Laid off. Laid off. 33,410.68. 27,555.24. Average Education. 12.45. 11.59. Average Age. 37.10. 35.08. Average Job Seniority. 7.02. 3.17. Average Household Size. 3.73. 3.75. Share of Male. 59.02%. 64.37%. Share of Head of Household. 33.27%. 33.10%. Share of Northern Area. 45.80%. 44.71%. Share of Central Area. 22.96%. 26.56%. Share of Southern Area. 28.22%. 25.99%. Average Income. 政 治 大. Share of LSA-Applicable Employees Share of the Period after LPA. 立. 89.29%. 96.41%. 51.74%. 43.10%. ‧ 國. 學. Table 4 lists the number of laid off and non- laid off employees for each combination of the DID method. As one can see in Table 3, non-laid off employees in. ‧. the reference group account for 10.57% but laid off employees in the reference group. Nat. n. al. er. io. sit. y. account for only 0.04%, which might affect the accuracy of the estimation.. i Un. v. Table 4: The Frequency Table of Layoffs between Reference Group and Treatment Group. Ch. engchi. (Before and After LPA, 2000 -2011) Not LSA-Applicable. LSA-Applicable. (Reference Group). (Treatment Group). Before LPA. After LPA. Before LPA. After LPA. Total. Non-laid off. 4,904. 3,637. 33,580. 37,621. 79,742. Percentage (%). (6.07). (4.50). (41.56). (46.56). (98.69). 19. 19. 583. 437. 1,058. Percentage (%). (0.02). (0.02). (0.72). (0.54). (1.31). Total. 4,923. 3,656. 34,163. 38,058. 80,800. Percentage (%). (6.09). (4.52). (42.28). (47.10). (100). Laid off. Note: Numbers in parentheses are cell percentages.. 24.

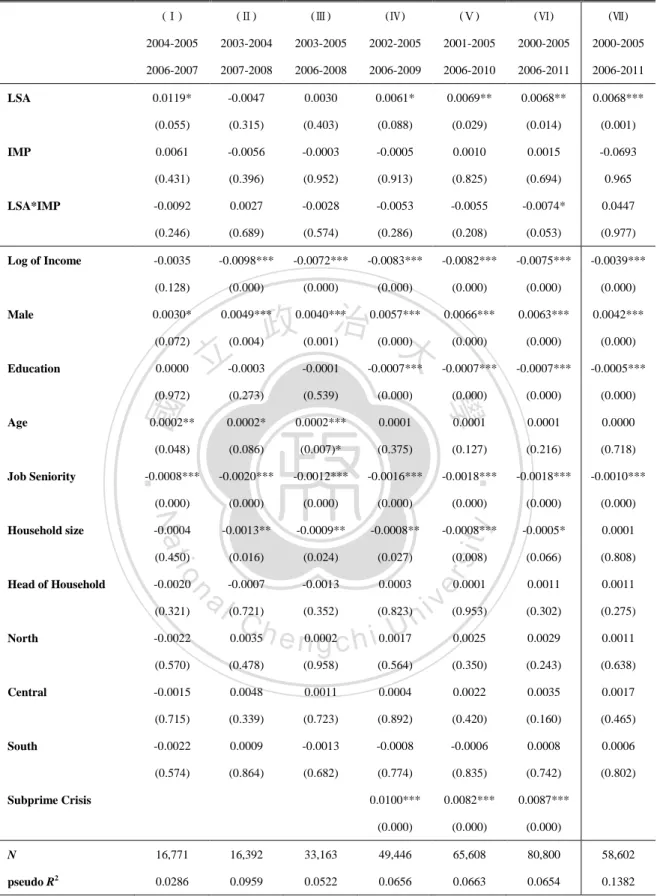

(32) 6. Results Table 5 shows the results of the difference in differences model (DID). Column Ⅰfrom Column Ⅵ in Table 5 represents different windows of observations used in the estimation. Column Ⅶ presents the results by dropping some observations which might affect the accuracy of the analysis. First, Column Ⅶ excludes the period from 2003 to 2004 due to the abnormally high layoff in the reference group (Figure 2). Second, according to the older pension system in LSA, employees who satisfy some specific conditions tend to choose the. 政 治 大. older pension system. If this is the case, they would not be affected by the severance. 立. pay change.. ‧ 國. 學. Such kinds of specific conditions are the requirements for the employees to apply for retirement pensions in the older pension system, which are listed as follows:. ‧. “1. When the worker attains the age of fifty-five and has worked for fifteen years.. sit. y. Nat. 2. When the worker has worked for more than twenty-five years.. io. er. 3. When the worker attains the age of sixty and has worked for ten years.”. al. iv n C assure the remaining employees in h theetreatment i Uare indeed covered by LPA. n g c hgroup n. Employees who satisfy the requirements above are excluded from the sample to. Third, employees hired in the period after the policy change must be the ones to whom LPA is applicable. These employees might find it easier to meet the expectations of the employers and have higher productivity, resulting in lower layoff rates. Therefore, Column Ⅶ also eliminates such kinds of employees in order to get pure estimates of the severance pay effect. Generally, most of employees to whom LSA is not applicable belong to the public sector and have relatively higher job security than other employees. As a result, one would expect that the layoff rate of employees in non-public sector businesses 25.

(33) (treatment group) will be higher. That is, the corresponding coefficient of LSA should be positive. Except for the results in Column Ⅱ and Column Ⅲ, Table 5 shows that employees who are covered by the Labor Standards Act do have higher layoff rates. In Column Ⅶ, one can see that layoff rate increases by 0.68% on average for the treatment group, relative to the reference group. As Figure Ⅱ shows, laid off rates for both the treatment group and the reference group are declining before implementation of the Labor Pension Act. However, there are no obvious trends in layoffs in the two groups after implementation of LPA. Hence, the coefficient of IMP (time trend effect) is. 治 政 ambiguous and hard to predict. Actually, all results in 大each column show that time 立 trend does not have significant effect on the layoff rate. ‧ 國. 學. The interaction term LSA*IMP reflects the effect of policy change, and one. ‧. would expect it to be negative due to the reduction of severance pay. However, the. sit. y. Nat. results from columnⅠto columnⅤsuggest that the severance pay seems to have no. io. er. significant effects on the layoff rate.. Although the DID estimate in Column Ⅵ suggests that the severance pay has. al. n. iv n C significant negative impact on the layoff it is inconsistent with the expectation of h e nrate, gchi U a positive impact on the layoff rate. In fact, one should notice that the negative result might have been caused by employees hired after the policy change, as explained. above. After dropping such observations, Column Ⅶ suggests that severance pay does not have any significant impact on the layoff rate. The remaining effects of the control variables are described as follows. Log of income is expected to have negative effect on the layoff rate. One of the reasons is that employees who have higher income are usually important to the firm and have some characteristics which are hard to be substituted by other employees. Therefore, employees with higher income are not easily laid off even in business contractions or 26.

(34) other similar situations. Results from Column Ⅱ to Column Ⅶ suggest that log of income does have significant effect on the laid off rate. In Column Ⅶ, one can see that a one percent increase in income results in a decrease of 0.39% in layoff rate, on average. The effect of gender on the laid off rate is opposite to the expectation. Usually, one will expect that females are more easily laid off than males due to gender discrimination. However, all results from Column Ⅰ to Column Ⅶ show that males face higher layoff rates than females. In Column Ⅶ, one can see that the layoff rate increases by 0.42% on average for males relative to females. This result might be. 治 政 explained by the fact that most females are white collar大 workers or work in the service 立 industry, and such kinds of jobs generally prefer females than males. Also, many ‧ 國. 學. males are menial or blue collar workers, and such kinds of jobs are relatively easy to. ‧. suffer layoffs, thus causing the higher layoff rate for males.. sit. y. Nat. Generally, skilled workers or workers in important positions have higher. io. er. education and these workers are relatively hard to be laid off. As a result, education is expected to have negative effect on the layoff rate. The results from Column Ⅳ to. al. n. iv n C suggest that educationhdoes have a significant e n g c h i U effect on layoff rate. In. Column Ⅶ. Column Ⅶ, one can see that a one year increase in education will decrease the layoff rate by 0.05% on average. Age seems to have positive effect on the layoff rate, as the results suggest, but the effects are significant only in Columns Ⅰ, Ⅱ and Ⅲ. In Column Ⅲ, one can see that one year increase in age increases the layoff rate by 0.02% on average. The reasons why older workers face higher layoff rate might be the fewer opportunities for promotion relative to young workers. That is, older workers might have less creativity and productivity than young workers, hence resulting in the higher layoff rate. Different from age, job seniority reflects relatively higher and abundant 27.

(35) experience and skills. Therefore, one would expect that higher job seniority will lead to a lower layoff rate. In fact, all results from Column Ⅰ to Column Ⅶ suggest that job seniority does have a significant effect on the layoff rate. In Column Ⅶ, one can see that a one year increase in job seniority results in decrease of the layoff rate by 0.010% on average. Household size means the number of members over the age of 15 in the family. Since a larger household size implies that employees have more responsibilities, one would expect such kinds of employees will work harder in order to support his/her family. Hence, employees with larger household size are supposed to have lower. 治 政 layoff rates. The results from Column Ⅱ to Column 大 Ⅵ suggest that household size 立 does have negative effect on the layoff rate. ‧ 國. 學. Whether an employee is the head of the household might affect the responsibility. ‧. he/she faces and hence the effect on the layoff rate should be negative. However, none. io. er. household has a significant effect on the layoff rate.. sit. y. Nat. of the results from Column Ⅰ to Column Ⅶ show that being the head of the. al. Working areas control the differences caused by some specific characteristics of. n. iv n C each area. According to the development issued by the Economic Bureau in 1979, h e nplan gchi U Taiwan can be separated into four areas, northern, central, southern and eastern area. Generally, one would expect that more developed areas such as the northern area will have higher layoff rate due to the competition. However, all results from Column Ⅰ to Column Ⅶ suggest that the four areas are not significantly different in terms of the layoff rate. The subprime mortgage crisis began in September 2008 and resulted in the global recession and financial crisis. Not only the stock market but also export industries in Taiwan were affected by this event, thus resulting in business contraction and involuntary unemployment. Treating the year 2008 as a dummy variable, the 28.

(36) results from Column Ⅳ to Column Ⅵ show that subprime mortgage did have a significant effect on the layoff rate. In Column Ⅶ, the estimate of subprime mortgage crisis effect is absent because the number of employees laid off in the year of 2008 happens to be zero, after excluding observations which might affect the accuracy of the analysis. Nevertheless, in Column Ⅵ, one can still see that layoff rate increases by 0.88% on average when the subprime crisis happens.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 29. i Un. v.

(37) Table 5: Impact of Severance Pay on Layoff Rate (Average Marginal Effects). Education. Household size. 2003-2004. 2003-2005. 2002-2005. 2001-2005. 2000-2005. 2000-2005. 2006-2007. 2007-2008. 2006-2008. 2006-2009. 2006-2010. 2006-2011. 2006-2011. 0.0119*. -0.0047. 0.0030. 0.0061*. 0.0069**. 0.0068**. 0.0068***. (0.055). (0.315). (0.403). (0.088). (0.029). (0.014). (0.001). 0.0061. -0.0056. -0.0003. -0.0005. 0.0010. 0.0015. -0.0693. (0.431). (0.396). (0.952). (0.913). (0.825). (0.694). 0.965. -0.0092. 0.0027. -0.0028. -0.0053. -0.0055. -0.0074*. 0.0447. (0.246). (0.689). (0.574). (0.286). (0.208). (0.053). (0.977). -0.0035. -0.0098***. -0.0072***. -0.0083***. -0.0082***. -0.0075***. -0.0039***. (0.128). (0.000). (0.000). (0.000). (0.000). (0.000). (0.000). 0.0030*. 0.0049***. 0.0040***. 0.0057***. 0.0066***. 0.0063***. 0.0042***. (0.072). (0.004). (0.001). (0.000). (0.000). (0.000). (0.000). -0.0003. -0.0001. -0.0007***. -0.0007***. -0.0007***. -0.0005***. (0.972). (0.273). (0.539). (0.000). (0.000). (0.000). (0.000). 0.0002**. 0.0002*. 0.0002***. 0.0001. 0.0001. 0.0001. 0.0000. (0.048). (0.086). (0.007)*. (0.375). (0.127). (0.216). (0.718). -0.0008***. -0.0020***. -0.0012***. -0.0016***. -0.0018***. -0.0018***. -0.0010***. (0.000). (0.000). (0.000). (0.000). (0.000). (0.000). (0.000). -0.0004. -0.0013**. -0.0009**. -0.0008**. -0.0008***. -0.0005*. 0.0001. (0.450). (0.016). (0.024). (0.027). (0.008). (0.066). (0.808). 0.0011. 0.0011. (0.302). (0.275). 0.0029. 0.0011. 0.0000. Central. South. -0.0022. 政 治 大. a l (0.721) (0.352) (0.823) i v (0.953) n C U 0.0035h e 0.0002 0.0017 0.0025 i h ngc. n. -0.0020 (0.321). North. 立. io. Head of Household. 2004-2005. ‧. Job Seniority. (Ⅶ). 學. Age. (Ⅵ). y. Male. (Ⅴ). sit. Log of Income. (Ⅳ). er. LSA*IMP. (Ⅲ). ‧ 國. IMP. (Ⅱ). Nat. LSA. (Ⅰ). -0.0007. -0.0013. 0.0003. 0.0001. (0.570). (0.478). (0.958). (0.564). (0.350). (0.243). (0.638). -0.0015. 0.0048. 0.0011. 0.0004. 0.0022. 0.0035. 0.0017. (0.715). (0.339). (0.723). (0.892). (0.420). (0.160). (0.465). -0.0022. 0.0009. -0.0013. -0.0008. -0.0006. 0.0008. 0.0006. (0.574). (0.864). (0.682). (0.774). (0.835). (0.742). (0.802). 0.0100***. 0.0082***. 0.0087***. (0.000). (0.000). (0.000). Subprime Crisis. N. 16,771. 16,392. 33,163. 49,446. 65,608. 80,800. 58,602. pseudo R2. 0.0286. 0.0959. 0.0522. 0.0656. 0.0663. 0.0654. 0.1382. Note: ColumnsⅠ to Ⅳ do not cover the period of subprime mortgage, so the dummy of subprime crisis is not included. Column Ⅶ excludes the period from 2003 to 2004, and eliminates employees who chose LSA rather than LPA. Besides, employees who had never worked before or had changed jobs after the reform are dropped in Column Ⅶ as well. The dummy of subprime crisis is absent in Column Ⅶ since the number of employees laid off in the year of 2008 happens to be zero after dropping some specific observations. p-values in parentheses: * p<0.1, ** p<0.05, *** p<0.01 30.

(38) 7. Conclusion This study uses implementation of the Labor Pension Act as the quasi-experiment to analyze the impact of severance pay on the layoff rate. In order to apply the difference in differences method, whether the LSA is applicable to an employee is the key to classification for the treatment group and the reference group. The results show that severance pay seems to have no significant impact on the layoff rate. Although the DID estimate from the sample with the largest window (2000 to 2011) is significantly positive, it might have been caused by the effect of the. 政 治 大 hired after the policy change and some other observations which might have affected 立 improved pension system instead of the severance pay. After dropping the employees. ‧ 國. 學. the accuracy of the analysis, the DID estimate shows that the severance pay has had no significant impact on the layoff rate. Other control variables such as income,. ‧. gender, education, job seniority and household size all have significant effects on the. io. er. significant effect on the layoff rate as well.. sit. y. Nat. layoff rate. And the macroeconomic event - subprime crisis - seems to have had a. al. iv n C U the significant effects of such performance of the employee, it is h notesurprising n g c htoi see n. Since factors such as income and job seniority are directly connected with the. kinds of factors. Besides, layoffs usually occur when the economy is facing a downturn and thus it is natural to expect layoff rate to be mainly affected by the macroeconomic related factors. However, though one might expect the reduced severance pay to increase the layoff rate, results of the analysis refute this expectation. It seems that even if severance pay is reduced by a large amount, it has no significant effects on the layoff rate. Instead, what affect the layoff are factors which have direct connections with work performance or the macroeconomic related factors. 31.

(39) Moreover, As LPA has improved the pension system and unemployment insurance has been implemented in 1999, severance pay is only expected to prevent arbitrary layoffs at present. But the results in this study suggest that severance pay does not affect layoff rate significantly. Hence, as a preventive measure against arbitrary layoffs, whether the current severance payment system should be modified or kept as it is could be discussed more in the future. Finally, there are some constraints in this study which need to be addressed. First, the data drawn from MUQLS do not directly tell us whether an employee is covered under LSA and thus it is inevitable to make some errors when classifying the. 治 政 treatment group and the reference group. Second, the number 大 of laid off employees in 立 the reference group is much lower relative to the treatment group, which might affect ‧ 國. 學. the accuracy of the analysis as well.. ‧. In addition to the layoff rate, there are still many possible impacts of the. sit. y. Nat. severance pay such as the turn off rate, unemployment and employment. Future. io. n. al. er. research could use the evidence from Taiwan to examine these corresponding effects.. Ch. engchi. 32. i Un. v.

(40) Reference 1.. 吳姿慧(2005),『我國資遣費給付制度之檢討 – 以德國「勞動契約終止保護法」與「企業 組織法」之規定為參照』,中原財經法學,第 15 期,頁 267-338. 2.. 林振賢(2000),「也談資遣費問題 -- 兼述日本退職金制度 – 上」,中國勞工,第 1004 期, 頁 20-23. 3.. 郭明政(2000),「勞基法資遣費與退休金制度之改革」,政大勞動學報,第 9 期,頁 37-64. 4.. 張誌純(2004),「企業組織再造程序員工權益之研究 – 以資遣費為中心」,成功大學碩士 論文. 5.. 政 治 大. 黃怡綾(2006),「資遣費制度與國家發展的關係及其對勞動市場的影響:以台灣等東亞十國 為例」,中央大學碩士論文. 立. 『行業就業指南』,行政院勞工委員會. 7.. 『重要教育統計資訊』,台北市政府教育局,http://www.edunet.taipei.gov.tw/. 8.. 勞動基準法,行政院勞工委員會. 9.. 勞工退休金條例,行政院勞工委員會. 10.. Angrist, J., and S. Pischke (2008), “Mostly Harmless Econometrics: An Empiricists’ Companion,”. ‧. ‧ 國. 學. 6.. er. io. sit. y. Nat. al. n. iv n C U and Worker Flows in OECD h e n“Dismissal Bassanini, A., and A. Garnero (2012), g c h iProtection Princeton University Press, Princeton, NJ.. 11.. Countries: Evidence from Cross-Country/Cross-industry Data,” Labour Economics, Vol.21, No.1, 25-41 12.. Hofer, H., U. Schuh and D. Walch (2011), “Effects of the Austrian Severance Pay Reform,” in Reforming Severance Pay: An International Perspective, 177-194. 13.. Kugler, Adriana D. (1999), “The Impact of Firing Costs on Turnover and Unemployment: Evidence from the Colombian Labour Market Reform,” International Tax and Public Finance, Vol.6, No.3, 389-410. 33.

(41) 14.. Lazear, Edward P. (1987), “Employment at Will, Job Security, and Work Incentives,” in Proceedings of the Conference on Employment, Unemployment, and Hours of Work, Science Center Berlin. 15.. Lazear, Edward P. (1990), “Job Security Provisions and Employment,” The Quarterly Journal of Economics, Vol.105, No.3, 699-726. 16.. Marinescu, I. (2009), “Job security legislation and job duration: Evidence from the United Kingdom,” Journal of Labor Economics, Vol.27, No.3, 465-486 Parsons, Donald O. (2011), “Mandated Severance Pay and Firing Cost Distortions: A Critical Review of the Evidence,” IZA Discussion Paper, No.5776. 立. 政 治 大. 學 ‧. ‧ 國 io. sit. y. Nat. n. al. er. 17.. Ch. engchi. 34. i Un. v.

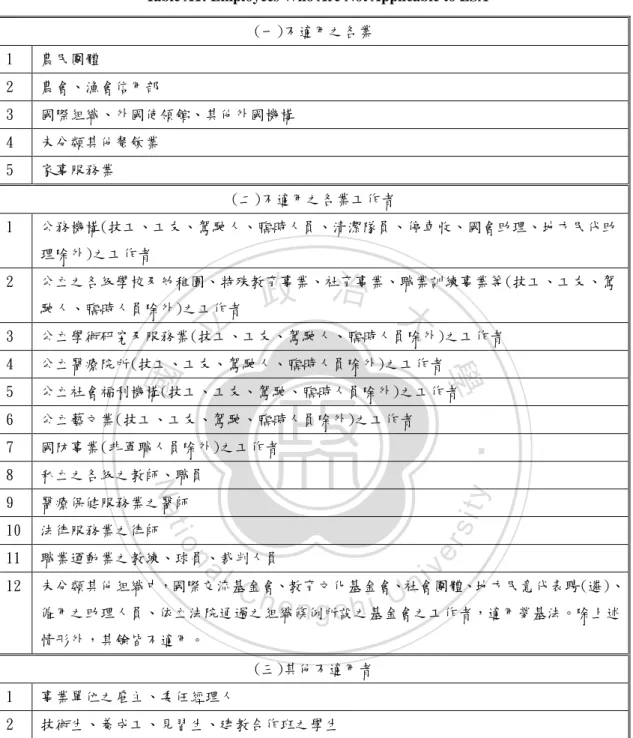

(42) Appendix Table A1: Employees Who Are Not Applicable to LSA (一)不適用之各業 1. 農民團體. 2. 農會、漁會信用部. 3. 國際組織、外國使領館、其他外國機構. 4. 未分類其他餐飲業. 5. 家事服務業 (二)不適用之各業工作者. 1. 公務機構(技工、工友、駕駛人、臨時人員、清潔隊員、停車收、國會助理、地方民代助 理除外)之工作者. 2. 政 治 大. 公立之各級學校及幼稚園、特殊教育事業、社育事業、職業訓練事業等(技工、工友、駕 駛人、臨時人員除外)之工作者. 立. 公立學術研究及服務業(技工、工友、駕駛人、臨時人員除外)之工作者. 4. 公立醫療院所(技工、工友、駕駛人、臨時人員除外)之工作者. 5. 公立社會福利機構(技工、工友、駕駛、臨時人員除外)之工作者. 6. 公立藝文業(技工、工友、駕駛、臨時人員除外)之工作者. 7. 國防事業(非軍職人員除外)之工作者. 8. 私立之各級之教師、職員. 9. 醫療保健服務業之醫師. 10. 法律服務業之律師. 11. 職業運動業之教練、球員、裁判人員. 12. 未分類其他組織中,國際交流基金會、教育文化基金會、社會團體、地方民意代表聘(遴)、. ‧. ‧ 國. 學. 3. n. er. io. sit. y. Nat. al. Ch. engchi. i Un. v. 僱用之助理人員、依立法院通過之組織條例所設之基金會之工作者,適用勞基法。除上述 情形外,其餘皆不適用。 (三)其他不適用者 1. 事業單位之雇主、委任經理人. 2. 技術生、養成工、見習生、建教合作班之學生. 資料來源:勞工保險局全球資訊網(website of Bureau of Labor Insurance) http://www.bli.gov.tw/. 35.

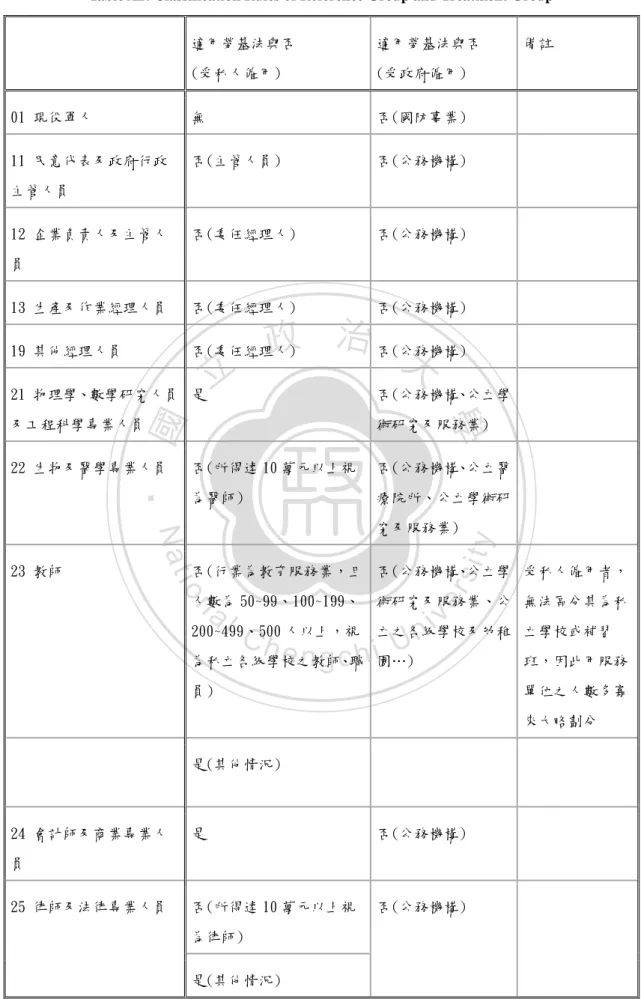

(43) Table A2: Classification Rules of Reference Group and Treatment Group 適用勞基法與否. 適用勞基法與否. (受私人僱用). (受政府僱用). 01 現役軍人. 無. 否(國防事業). 11 民意代表及政府行政. 否(主管人員). 否(公務機構). 否(委任經理人). 否(公務機構). 13 生產及作業經理人員. 否(委任經理人). 否(公務機構). 19 其他經理人員. 否(委任經理人). 備註. 主管人員 12 企業負責人及主管人 員. 立. 否(公務機構、公立學. 學. 及工程科學專業人員. 為醫師). 療院所、公立學術研. ‧. 否(公務機構、公立醫. 究及服務業). sit. Nat. 23 教師. 否(所得達 10 萬元以上視. 否(行業為教育服務業,且 否(公務機構、公立學 受私人僱用者,. io. 人數為 50~99、100~199、. n. al. Ch. 200~499、500 人以上,視. er. 22 生物及醫學專業人員. 術研究及服務業). y. ‧ 國. 21 物理學、數學研究人員 是. 政 治 否(公務機構) 大. 術研究及服務業、公 無法區分其為私. i Un. v. 立之各級學校及幼稚 立學校或補習. engchi. 為私立各級學校之教師、職 園…). 班,因此用服務. 員). 單位之人數多寡 來大略劃分. 是(其他情況). 24 會計師及商業專業人. 是. 否(公務機構). 否(所得達 10 萬元以上視. 否(公務機構). 員 25 律師及法律專業人員. 為律師) 是(其他情況) 36.

(44) 26 社會科學及有關專業. 是. 否(公務機構、公立學. 人員. 術研究及服務業). 29 其他專業人員. 是. 否(公務機構、公立學 術研究及服務業). 31 物理、工程科學助理專 是. 否(公務機構、公立學. 業人員. 術研究及服務業). 32 生物科學及醫療助理. 否(所得達 10 萬元以上視. 否(公務機構、公立學. 專業人員. 為醫師). 術研究及服務業). 是(其他情況). 政 治 大 人數為 50~99、100~199、 術研究及服務業、公 立 200~499、500 人以上,視 立之各級學校及幼稚. 33 教學及有關助理專業. 否(行業為教育服務業,且 否(公務機構、公立學 受私人僱用者,. 為私立各級學校之教師、職 園…) 員). ‧. 是(其他情況). 班,因此用服務. sit. y. 來大略劃分. er. al. 是. 業務監督人員 36 行政助理專業人員. 立學校或補習. 否(公務機構). n. 35 政府行政監督及企業. 是. io. 專業人員. 無法區分其為私. 單位之人數多寡. Nat. 34 財務及商業服務助理. 學. ‧ 國. 人員. Ch. iv n U e n g c h i否(公務機構). 否(行業為教育服務業,且 否(公務機構). 受政府僱用者,. 人數為 50~99、100~199、. 若為國會助理或. 200~499、500 人以上,視. 民意代表助理,. 為私立各級學校之教師、職. 則適用勞基法,. 員). 但資料中無法判 別. 是(其他情況). 37 海關、稅務及有關政府 無. 否(公務機構). 助理專業人員 37.

(45) 39 其他助理專業人員. 否(若行業為職業運動業, 否(公務機構) 代表為職業運動業之教 練、球員、裁判人員) 是(其他情況). 41 辦公室事務人員. 否(行業為教育服務業,且 否(公務機構) 人數為 50~99、100~199、 200~499、500 人以上,視 為私立各級學校之教師、職 員) 是(其他情況). 立. 否(行業為教育服務業,且 否(公務機構). 學. 人數為 50~99、100~199、 200~499、500 人以上,視. ‧. ‧ 國. 42 顧客服務事務人員. 政 治 大. 為私立各級學校之教師、職 員). sit. y. Nat. io. n. al. er. 是(其他情況). Ch. i Un. v. 51 個人服務工作人員. 是. 否(公務機構). 52 保安服務工作人員. 是. 否(公務機構). 53 模特兒、售貨員及展售 是. 否(公務機構). engchi. 說明人員 60 農、林、漁、牧工作人 是. 否(公務機構). 員 71 採礦工及營建工. 是. 否(公務機構). 72 金屬、機具處理及製造 是. 否(公務機構). 有關工作者 38.

(46) 73 精密儀器、手工藝、印 是. 否(公務機構). 刷及有關工作者 79 其他技術工及有關工. 是. 否(公務機構). 81 固定生產設備操作工. 是. 否(公務機構). 82 機械操作工. 是. 否(公務機構). 83 組裝工. 是. 否(公務機構). 84 駕駛員及移運設備操. 是. 是(駕駛人). 作者. 作工 是. 92 生產體力工. 是. 99 其他非技術工及體力 工. 立. 政 治 是(技工、工友) 大 否(公務機構). 學. 是. 是(技工、工友). ‧. ‧ 國. 91 小販及服務工. 註:上表中,學校教師與職員規模部分,參考台北市政府教育局的『重要教育統計資訊』中之各. y. Nat. 級學校教職員數。醫師、律師與會計師之薪資水準,則是參考行政院勞工委員會之『行業職業就. n. er. io. al. sit. 業指南』中的各職業薪資概況。. Ch. engchi. 39. i Un. v.

(47) Table A3: The Variation of the Coverage of LSA and the Corresponding Classification Rules 適用勞基法之行. 中華民國職業分類標準. 中華民國職業分類標準. 中華民國職業分類標準. 業與起始實施日. 第六版(2000~2002). 第七版(2002~2007). 第八版(2007~2011). 90.1.21. *個人服務工作人員. *個人服務工作人員. *個人服務工作人員. 受僱於縣(市)政. *受政府僱用. *受政府僱用. *受政府僱用. 府從事停車場業. *個人服務業. *未分類其他服務業. *未分類其他服務業. (無法定義). (無法定義). (無法定義). 92.12.1. *非主管或經理人員. *非主管或經理人員. *非主管或經理人員. 勞工團體僱用勞. *受私人僱用. *受私人僱用. 工. *社會服務業. 大 *宗教、職業及類似組織. 94.6.30. *受政府僱用. *受政府僱用. *受政府僱用. *社會服務業. *醫療保健服務業. *非參加政府考試分發. *非參加政府考試分發. 期. 務之人員 92.10.1 政黨僱用勞工. *醫療保健服務業 *非參加政府考試分發. ‧. 聘僱). ‧ 國. 時人員(不含約. *宗教、職業及類似組織. 學. 公立醫療院所臨. 立. 治 政 *受私人僱用. Nat. *非主管或經理人員. 全國性政治團體. *受私人僱用. *受私人僱用. 僱用勞工. *社會服務業. 97.1.1. *非技工、工友、駕駛或 *非技工、工友、駕駛或 *非技工、工友、駕駛或. sit. *受私人僱用. er. *宗教、職業及類似組織 *宗教、職業及類似組織. n. al. *非主管或經理人員. y. *非主管或經理人員. io. 94.6.30. Ch. e n現役軍人 gchi. i Un. v. 公務機構之非依. 現役軍人. 現役軍人. 公務人員法制進. *受政府僱用. *受政府僱用. *受政府僱用. 用之臨時人員. *公務機構及國防事業. *公務機構及國防事業. *公共行政及國防、強制. (不含約聘僱). *非參加政府考試分發. *非參加政府考試分發. 性社會安全事業 *非參加政府考試分發. 97.1.1. *受政府僱用. *受政府僱用. *受政府僱用. 公立教育訓練服. *社會服務業. *教育服務業. *教育服務業. 務業之非依公務. *非參加政府考試分發. *非參加政府考試分發. *非參加政府考試分發. *受政府僱用. *受政府僱用. *受政府僱用. 人員法制進用之 臨時人員(不含 約聘僱) 97.1.1. 40.

數據

+7

相關文件

• Zero-knowledge proofs yield no knowledge in the sense that they can be constructed by the verifier who believes the statement, and yet these proofs do convince him...

Practice: What is the largest unsigned integer that may be stored in 20 bits. Practice: What is the largest unsigned integer that may be stored in

For goods in transit, fill in the means of transport in this column and the code in the upper right corner of the box (refer to the “Customs Clearance Operations and

, A echelon form ( reduced echelon form) pivot column vectors.. elementary row operations column

Al atoms are larger than N atoms because as you trace the path between N and Al on the periodic table, you move down a column (atomic size increases) and then to the left across

Murphy.Woodward.Stoltzfus.. 17) The pressure exerted by a column of liquid is equal to the product of the height of the column times the gravitational constant times the density of

• Zero-knowledge proofs yield no knowledge in the sense that they can be constructed by the verifier who believes the statement, and yet these proofs do convince him....

• Zero-knowledge proofs yield no knowledge in the sense that they can be constructed by the verifier who believes the statement, and yet these proofs do convince him..!.