行政院國家科學委員會專題研究計畫 成果報告

管理一學門會計領域卓越研習營

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 95-2420-H-004-072- 執 行 期 間 : 95 年 12 月 01 日至 96 年 11 月 30 日 執 行 單 位 : 國立政治大學會計學系 計 畫 主 持 人 : 陳明進 計畫參與人員: 博士班研究生-兼任助理:曾家璿、林玉君 處 理 方 式 : 本計畫涉及專利或其他智慧財產權,2 年後可公開查詢中 華 民 國 97 年 02 月 22 日

國科會管理一學門會計領域卓越研習營結案報告

計畫編號 : NSC95-2420-H-004-072-

執行期間 : 2006 年 12 月 01 日至 2007 年 11 月 30 日

執行單位 : 國立政治大學會計學系

計畫主持人 : 陳明進

計畫參與人員 : 林玉君、曾家璿

1

行政院國家科學委員會補助專題研究計畫成果報告

國科會管理一學門會計領域卓越研習營結案報告

個別型計畫

計畫編號:NSC95-2420-H-004-072-

執行期間:95 年 12 月 01 日至 96 年 11 月 30 日

計畫主持人:陳明進

精簡成果報告

執行單位:政治大學會計系

處理方式:除產學合作研究計畫、提升產業技術及人才培育研究計畫、列管計畫及下列 情形者外,得立即公開查詢□涉及專利或其他智慧財產權,□一年R二年後可公開查詢

中華民國 96 年 11 月 30 日

2

目 錄

壹、活動舉辦目的與延聘學者………01 貳、研習營之籌備過程………01 參、活動經過………02 肆、活動內容摘要………02 伍、成果與績效評估………03 陸、檢討與建議………05 附件 一、黃鈺昌博士之簡介………06 二、活動宣導海報………08 三、活動議程………09 四、研習講義………11 五、活動剪影………40 六、專題演講摘要………43 七、論文計畫與研習心得摘要………47 八、座談會--如何提昇管理會計研究及教學能量………583

中文摘要

政治大學會計系與行政院國科會人文處於 2007 年暑期共同舉辦會計領域卓越研習 營,邀請美國亞歷桑納州立大學黃鈺昌博士來台擔任研習營演講貴賓,指導國內教師與 博士生提昇發表國際期刊與論文之能力。活動內容包括:黃鈺昌博士專題演講,講授管 理會計研究重要議題及如何於國際期刊發表論文,並分享國際上研究現況之資訊。在互 動式指導論文的部分,黃鈺昌博士對國內新進學者的五篇論文提供具體之指導。綜合座 談方面,黃鈺昌教授與國內學者針對如何提昇管理會計研究及教學能量座談,與會師生 與黃鈺昌博士互動頻繁,反應熱烈,達到擴大學術交流之目的。綜合本次活動成果,謹 提出下列建議:互動式之論文指導,有助於發表論文學者具體論文修改,值得未來國科 會舉辦卓越研習營參考。惟由於 2007 年國科會人文處會計領域卓越研習營共有五個場 次,建議未來可適度集中辦理,發揮共用資源效益,且可節省總經費支出(減少場次)。 關鍵詞:會計卓越研習營、會計研究、管理會計4

Abstract

The Department of Accounting of National Chengchi University and National Science Council co-host the 2007 Advanced Accounting Research Workshop, inviting Dr. Yuhchang Hwang of Arizona State University to help enhance the ability to publish in international journals for local teachers and PhD. students. The workshop includes an invited speech provided by Dr. Yuhchang Hwang, interactive guidance of research proposals and papers, and a panel discussion. Dr. Yuhchang Hwang addresses on several important issues of management accounting research and focuses of accounting research for international journals. As for the interactive guidance of research proposals, Dr. Yuhchang Hwang gives specific suggestions to five scholars’ research papers. During the panel discussions, Dr. Yuhchang Hwang and local scholars exchange ideas about how to stimulate excellent management accounting research and teaching. The participants interact enthusiastically with Dr. Yuhchang Hwang and other panelists, achieving the goal of sharing knowledge among scholars. In reviewing the workshop activities, we propose the following suggestions. First, interactive guidance of research proposals can provide specific and concrete suggestions to local scholars. We suggest that future workshops adopt this interactive guidance approach. Second, there is a series of five accounting workshops as planned by NSC in 2007. We suggest that the number of advanced workshops may be reduced to one or two, not only to more effectively utilize the resources but also to save the budgets.

Keywords: Advanced Accounting Research Workshop, Accounting Research, Management

1

壹、 活動舉辦目的與延聘學者

有鑒於提昇國內年青會計學者的研究能力及國際論文發表能力,是未來國內會計 研究能量重要的基礎,國科會人文處乃與國內政治大學、中興大學、成功大學、東 海大學等會計系合作,共同規劃籌辦一系列會計領域卓越研習營活動,邀請國際知 名會計學者擔任演講及指導國內學者論文寫作與發表,以深化之指導方式,提昇國 內參與學者之研究能力。 黃鈺昌博士是現在美國管理會計研究表現上非常積極、知名的一位學者,經常受 邀協助國際期刊評審,對於管理會計研究議題掌握及國際期刊論文發表,有豐富之 經驗,2007 年在美國會計學會的管理會計年度會議獲得 Outstanding Paper Award,有 關黃鈺昌博士的簡介請詳附件一。 因此,本系配合國科會規劃邀請黃鈺昌博士於暑期舉辦會計領域卓越研習營計 畫,以協助國內教師與博士生提昇發表國際期刊與論文之能力。貳、 研習營之籌備過程

政治大學會計領域卓越營自 2006 年秋末即進入籌備階段,其規劃籌備過程如下 所述: 2006 年 11 月:規劃研討會活動內容並積極聯絡黃鈺昌教授 參考會計領域學者之意見(如政大吳安妮教授等),規劃研討會進行之方式。研討會主 要規劃重點在於提升國內學者與黃老師之深化討論與後續合作之機會,故研擬卓越營 以少量研究計畫書之深入討論為主軸,並配合會計議題之坐談會,藉以鼓勵國內學者 一同參與。 2006 年 12 月:架設宣傳網站及徵稿訊息之公告 此階段主要在於宣傳本活動之訊息,宣傳方式為「網站之架設」。網站內容包括:本 卓越營之活動簡介、活動方式、大會議程及徵稿說明,網站上並有黃鈺昌教授之基本 資料。同時,開放報名參加本卓越營活動。2 2007 年 1、2 月:印製各類文宣資料(徵稿文件及邀請函) 發佈卓越營之活動消息至國內各大專院校之商學院。宣傳方式包括利用 e-mail 及寄發 書面文件,相關活動宣導海報如附件二。 2007 年 3 月:確定活動議程及活動內容 經過與黃老師多次溝通後,已確定活動議程及活動方式。故本階段進入活動內容之規 劃,包括場地安排及邀約參與座談會之來賓。 2007 年 4、5 月:審稿階段 本階段徵稿期限已截止,進入審稿階段。本卓越營邀請黃鈺昌教授及國內各大會計系 教授擔任審稿委員,共拮選出五篇研究計畫。 2007 年 6 月:公告甄選研究計畫及寄發邀請函 以網站公告審稿結果並個別通知發表者,告知其詳細之活動內容,同時寄發本活動之 邀請函至國內各大專院校商學院。本活動之報名截止日至 6 月 30 日止。 2007 年 7 月:卓越營順利舉行 卓越研習營活動過程與內容摘要請見本報告第參、肆部分。

參、 活動經過

本次活動目的為邀請黃鈺昌博士參加國科會人文處 2007 年會計領域卓越研習 營,舉辦日期為 2007 年 7 月 18 及 19 日二天,活動內容包括專題演講、指導國內學 者論文修改以及綜合座談。 相關活動議程請詳附件三,研習講義請詳附件四,活動剪影請詳附件五。肆、 活動內容摘要

本次活動共分三部分,摘述如下:3

idea discovery to paper presentation and publication」,講授管理會計研究重要議題 及如何於國際期刊發表論文。 有關專題演講之摘要請見附件六。 二、2007/7/18 下午至 2007/7/19 上午—指導國內學者論文修改及發表。 對國內學者研究計畫書或論文稿之深化指導,每位參與學者報名此項活動時,須 提出詳細研究計畫書或論文稿,論文討論活動包括三階段: (一)先由國內學者發表其研究計畫書或論文稿,讓黃鈺昌教授及其他國內參與學 者互相暸解研究議題及初步進行討論。每篇論文有 30 分鐘以上時間,強化 討論深度。 (二)由黃鈺昌教授給與每篇論文具體之指導及改進建議。 (三)每位參與學者接受黃鈺昌教授及其他國內學者建議後,再回應提出未來該論 文的修改或研究進行方式,以及希望黃鈺昌教授可以再協助之處,以利建 立後續合作聯繫之網絡關係。 本次研習營之學者論文計畫摘要與參與本研習之心得彙整如附件七。 三、黃鈺昌教授與國內學者綜合座談--「如何提昇管理會計研究及教學能量」,邀請 吳安妮主持(政大會計系教授)、及黃鈺昌博士、李書行教授(台大會計系主任)、 李佳玲教授(中正大學會計系教授)、許恩得教授(東海大學會計系主任)座談,其 相關內容摘要彙整如附件八。

伍、 成果與績效評估

一、論文深化指導與投稿經驗傳承

此次邀請黃鈺昌博士來台,冀望藉由黃鈺昌教授在美國學術界累積多年的研究經 驗協助國內學者完成可投稿於國際期刊之論文。在研習過程中,五位論文發表人分別 提出研究計畫或發表已完成之論文,黃鈺昌教授與本系吳安妮教授以直接互動的方式 逐一給予每篇論文建議與指導,並指出論文修改的方向與可能遭遇之問題,期望能幫4 助發表論文的年輕學者未來能將其論文發表於國際級期刊上。 黃鈺昌教授除了提供論文修改的寶貴意見,並以「論文的包裝、修改與行銷」為 題,把自己多年投稿與審稿經驗彙整成多項關鍵要點分享給與會師生,更以自己投稿 期刊實際所收到的審稿人評論為例,說明自己如何與審稿人應對、回答審稿人的問 題,黃鈺昌教授的不吝指導,與會師生都覺得獲益良多。此外,研習過程中,黃鈺昌 教授與本系吳安妮教授也分享自己在研究過程中所遭遇之困難,與如何越挫越勇克服 困難的研究歷程,二位資深學者以自身的歷程鼓勵在場年輕後學,對年輕學者來說是 非常寶貴的經驗傳承。 不論是發表論文的學者,或是與會的其他老師及博士班學生皆給予此次研習極為 正面的評價。他們感受到此次互動式指導論文的過程能深入探討如何提升研究議題的 貢獻,並由聽取資深學者分享之研究歷程,汲取前人經驗,所得獲益良多。

二、專題演講

在黃鈺昌教授的「Research in Managerial Accounting: idea discovery to paper presentation and publication」的專題演講中,除本校師生外,有來自國內多所大學之 教師與博士班學生參加,包括:台灣大學、台北大學、淡江大學、成功大學、中山大 學、實踐大學、中原大學、元智大學等。本專題演講在本校商學院六樓元大講堂舉行, 近 100 人的座位座無虛席。在演講過程中,台上台下互動頻繁,與會師生熱烈提問, 黃鈺昌教授也熱情回答,充分達到擴大學術交流的目標。 參與此次專題講座的老師與學生們,聽取黃鈺昌教授於會計領域研究成果與經驗 之分享,充實新知,並獲得黃鈺昌教授所帶來國際上研究現況之資訊,寬廣國際視野。

三、綜合座談

在「如何提升管理會計研究與教學能量」座談會中,與會的貴賓黃鈺昌教授,李 書行教授 (台灣大學會計系),李佳玲教授 (中正大學會計資訊系),許恩得教授 (東 海大學會計系)及本系吳安妮教授皆有熱烈精闢之討論。 許恩得教授首先分享他如何以系主任的角色號召與激勵系上老師結合研究與教5 學,他以鼓勵撰寫教科書方式帶動系上老師相互合作並藉由寫書過程激發靈感與尋找 議題。李書行教授認為教授博士班與碩士班的課程較能結合研究與教學。李佳玲教授 則是以與企業合作的方式,藉由實地參訪尋找研究議題與建立教學實例。吳安妮教授 與黃鈺昌教授則認為必須建立良好的研究伙伴關係,不但能幫助研究,也能由研究過 程腦力激盪,分享彼此的研究與教學經驗。 本次綜合座談,各位座談貴賓提供提升卓越研究與教學之實際可行作法與經驗分 享,並相互熱烈討論,對於與會師生來說不但能汲取各位座談貴賓結合研究與教學之 方法與經驗,並由討論過程獲得與國內其他學者交流之機會。 整體而言,本次會計領域卓越研習營,獲得與會貴賓及師生熱烈的迴響與正面評 價。

陸、 檢討與建議

此次卓越研習營,在政大配合提供延攬國際知名學者講學的經費協助,及政大會 計系全體師生投入籌辦,得以順利執行,綜合本次活動成果,謹提出下列建議: 一、互動式之論文深化指導,有助於發表論文學者具體論文修改,並啟發研究議題思 考及掌握能力,值得未來國科會舉辦卓越研習營參考。 二、由於 2007 年國科會人文處會計領域卓越研習營共有五個場次,分散在不同學校, 固然有擴散研究交流之效益,但因為系列活動較多場次,容易導致參加人數分散 減少,投稿論文不夠踴躍,頗為可惜。建議未來可適度集中辦理,對於旅途較遠 之學者或博士生欲參加者,可酌予補助旅費及住宿費用,發揮共用資源效益,且 可節省總經費支出(減少場次)。 三、本次研習營國際學者除了專題演講及座談會外,還須要協助五篇論文之審稿及修 改建議,須要投入許多時間且心力繁重,但國科會提供予國際學者之給付,僅有 機票及五天的日支費(每日一萬元台幣),對於國際學者的報酬明顯偏低,建議應 提高給付額。6

附件一 黃鈺昌博士之簡介

Introduction of Dr. Yuhchang Hwang

Education:

§ Ph.D., Business Administration, University of California, Berkeley; 1987. § M.S., National Chengchi University, Taiwan; 1979

§ B.A., Fu-Jen Catholic University, Taiwan; 1977

Teaching experience:

§ Associate Professor, School of Accountancy, W. P. Carey School of Business, Arizona State University; 2001- present.

q Course taught:

v Executive MBA, ACC530 Introductory Managerial Accounting

v Master of Accountancy, Master of Taxation, ACC585-- Performance Measurement

and Incentive Design

v Full-time MBA, Elective ACC585 -- Performance Measurement and Incentive

Design

v Doctoral Seminar in Managerial Accounting

v Technology MBA -- Motorola at Beijing, China; Managerial Accounting v Executive MBA (Shanghai, China) -- Managerial Accounting

v Executive Training: China Mobile –Performance Evaluation

§ Assistant Professor, School of Accountancy, Arizona State University; fall 1995 - 2001.

§ Assistant Professor, Joseph M. Katz Graduate School of Business, University of Pittsburgh; fall 1987 - 1995.

§ Teaching Assistant, University of California, Berkeley; Fall 1982 - Summer 1983, fall 1984 - Spring 1985.

§ Instructor, Second Lieutenant, Chinese Army Finance & Quartermaster School, Taiwan, Oct. 1979 - Aug. 1981.

Biography:

黃鈺昌博士目前任教於美國亞利桑納州立大學(School of Business, Arizona State University)商學院,是研究管理會計之優秀學者。黃鈺昌博士為美國 University of California — Berkeley 會計博士,在美國已有十餘年之教學與研究經驗。他的主要教 授科目包括:管理會計、財務會計、供應鏈成本管理等;而策略成本管理與績效衡量 則是他目前的主要研究領域。黃鈺昌博士的論文曾發表於 Review of Accounting

Studies (國科會會計領域國際期刊評比頂尖期刊)、Management Sciences (國科會生產

作 業 管 理 與 計 量 方 法 領 域 國 際 期 刊 評 比 第 一 名 期 刊 ) 、 Journal of Management

Accounting Research (國科會會計領域國際期刊評比 A 級期刊)、Medical Care (國科會

醫務管理國際期刊評比第二名)、Journal of Accounting and Public Policy (國科會會計 領域國際期刊評比 A 級期刊)、Journal of Accounting Auditing and Finance、 Issues in

7

黃鈺昌博士在管理會計學術上具有相當之國際知名度,經常受邀協助國際期刊評 審,包括:Journal of Management Accounting Research (Editorial Board, 1995-2002),

Management Science (2002) , The Accounting Review (1991-1996) , Journal of Management Accounting Research (1992-1994) , The Chinese Accounting Review

(1994-1999) , The 1996 American Accounting Association Annual Conference , Management Accounting Research Conference (1995-1998)。此外,黃鈺昌博士並擔任 Western Regional Director, Management Accounting Section, American Accounting Association (2002 至今)。

黃 鈺 昌 教 授 在 學 術 研 究 與 教 學生 涯 中 , 亦獲 獎 無 數, 包 括: Certificate of Appreciation, Arizona Coronary Artery Bypass Graft Study Group (August, 1998),ASU Accounting Circle Teaching Award (School of Accountancy, January 2000),Outstanding Graduate Teaching Award (Arizona State University, 1998),Katz Graduate School of Business, University of Pittsburgh summer research grants (1992, 1993, 1994, 1995), Institute for Industrial Competitiveness, Research Grant (University of Pittsburgh, 1993, 1994),Institute of Management Accounting, Research Grant (1993)。

8

附件二 活動宣導海報

應

應邀邀演演講講GGuueessttSSppeeaakkeerr:: 黃

黃鈺鈺昌昌 教教授授 Prof. YuhChang Hwang

W. P. Carey School of Business, Arizona State University 演

演講講題題目目SSppeeeecchhTTiittllee::

Research in Managerial Accounting: idea discovery to paper presentation and publication

座

座

談

談

會

會

F

F

o

o

r

r

u

u

m

m

:

:

主

主題題::如如何何提提升升卓卓越越研研究究與與教教學學

主持人:吳安妮教授 (政治大學會計系) 與談人:黃鈺昌教授 (Arizona State University)

李書行教授 (台灣大學會計系) 李佳玲教授 (中正大學會計資訊系) 許恩得教授 (東海大學會計系) 時 時間間DDaattee&&TTiimmee::22000077年年77月月1188--1199日日 JJuullyy1188--1199,,22000077,,88::3300aa..mm..ooppeenn,, 9 9::0000ssttaarrtt 地 地點點VVeennuuee::國國立立政政治治大大學學商商學學院院66FF元元大大講講堂堂 N NaattiioonnaallCChheennggcchhiiUUnniivveerrssiittyyTThheeCCoolllleeggeeooffCCoommmmeerrccee66FFYYuuaannttaaLLeeccttuurree H Haallll 主 主辦辦單單位位HHoosstt:: 行 行政政院院國國家家科科學學委委員員會會 NNaattiioonnaallSScciieennccee CCoouunncciill 國立政治大學會計學系 DDeeppaarrttmmeenntt ooffAAccccoouunnttiinngg,,NNaattiioonnaallCChheennggcchhii U Unniivveerrssiittyy

9 附件三 活動議程

國科會人文處會計領域卓越研習營議程表

2007 年 7 月 18 日、19 日

地點:國立政治大學商學院

2007 年 7 月 18 日 (三) 時 間 議 程 內 容/ 主 講 人 08:30 - 09:00 報 到 09:00 - 09:20 (商學院 6F 元大講堂) 開幕及活動介紹 開幕、來賓致詞及活動介紹 9:20 - 12:00 (商學院 6F 元大講堂) 專題演講Prof. YuhChang Hwang:

Research in Managerial Accounting: idea discovery to paper presentation and publication

12:00 - 13:00 午 餐

The Characteristics of Innovation Teams and Diversity of Performance Measurement (張菁萍,中山大學企業管理學系) 台商母公司無形資產與大陸子公司會計績效關聯性之 研究 (彭志偉,崑山科技大學會計系;楊朝旭,成功大學會 計系) 13:00 - 14:50 (商學院 3F 301 室) 論文指導場次(一) -參加學者發表論 文及討論 (每篇發表30分 鐘,Q&A共20分 鐘,本場次共3篇)

The Effect of Performance Measurement System on Breakthrough OUCH Product Development Teams in Taiwan High-Technology Sector

(Erin Lin , Dr. Magdy Abdel-Kader, Senior Lecturer, Department of Accounting, Brunel University, UK)

14:50 - 15:10 茶 敘 15:10 - 16:30 (商學院 3F 301 室) 論文指導場次(一) -參加學者發表論 文及討論 (每篇發 自治理權力觀點探討高階經營團隊、董事會、與財務 報表品質間的關連性 (張瑞當 魏若婷,中山大學企管學系)

10

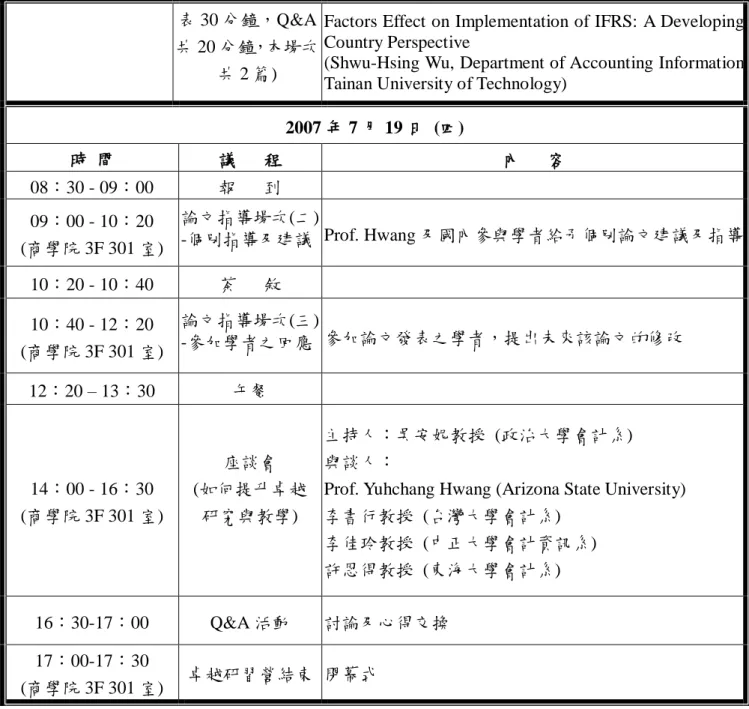

表 30 分鐘,Q&A 共 20 分鐘,本場次

共 2 篇)

Factors Effect on Implementation of IFRS: A Developing Country Perspective

(Shwu-Hsing Wu, Department of Accounting Information Tainan University of Technology)

2007 年 7 月 19 日 (四) 時 間 議 程 內 容 08:30 - 09:00 報 到 09:00 - 10:20 (商學院 3F 301 室) 論文指導場次(二) -個別指導及建議 Prof. Hwang 及國內參與學者給予個別論文建議及指導 10:20 - 10:40 茶 敘 10:40 - 12:20 (商學院 3F 301 室) 論文指導場次(三) -參加學者之回應 參加論文發表之學者,提出未來該論文的修改 12:20 – 13:30 午餐 14:00 - 16:30 (商學院 3F 301 室) 座談會 (如何提升卓越 研究與教學) 主持人:吳安妮教授 (政治大學會計系) 與談人:

Prof. Yuhchang Hwang (Arizona State University) 李書行教授 (台灣大學會計系) 李佳玲教授 (中正大學會計資訊系) 許恩得教授 (東海大學會計系) 16:30-17:00 Q&A 活動 討論及心得交換 17:00-17:30 (商學院 3F 301 室) 卓越研習營結束 閉幕式

11

附件四 研習講義

26

30

Memorandum to Associate Editor

Thank you for your encouragement and extensive constructive comments. We believe they helped us immensely to improve the focus, clarity and contributions of the paper. Compared to the previous version, the revised manuscript now contains a much deeper link to the prior literature and with stronger managerial implications. We also made significant revisions to the measurement and data analysis sections to address the issues that you and the reviewer raised. Below is an outline of our revisions to the manuscript, organized based on the sequence of the comments in your review. Whenever applicable, we briefly summarize the essence of your comments to ease the review process and to communicate our interpretation of your concerns and suggestions.

Strengths

31

the HR and organization learning literature.

By incorporating these works, the revised manuscript is now better motivated (see pp. 1-2) and is able to render evidence supporting of these recent developments (see pp. 26-27).

Theory

Motivation and Introduction.

We appreciate your suggestion to re-orient the manuscript by focusing more on testing the general implications of the contingency theory. In so doing, purchasing management becomes the context of theory testing. We further appreciate your suggestion to highlight that purchasing management is an important context for theory testing, especially with the rising interests in business-to-business e-commerce.

Accordingly, we have significantly re-written the introduction (pp. 1-2) to reflect the need to test the broad theories of the performance contingency effect between product strategy and organization design. Additional efforts were made to highlight the practical significance of the issue and our contributions to the literature (pp. 3-4). Whenever applicable, we also made the needed revisions and/or enhancements throughout the rest of the manuscript to further elaborate on the impacts of the preceding changes.

Hypothesis

a. Hypothesis 1 1) MatchingFollowing Reviewer 1’s comments we have re-worded Hypothesis 1 and

changed the word “matching” to “congruence” to better reflect a

non-binary notion of alignments between structure design and a

chosen strategy.

2) Monotonicity

Basically you suggest we make a better and more readable presentation. The reviewer expressed the same concerns. We thus revised the presentation accordingly. The discussion following H1 is now kept at the conceptual level (pp. 8-9) without resorting to the prediction of the functional form of the relationship. Instead, the testing and the discussion of the functional form are provided later in the hypothesis testing section with a series of self explanatory numeric examples derived from the analytical findings (see pp. 21-23). In addition, the managerial implications of the findings are discussed in the results and implications section (pp. 25-28). We believe the preceding changes should enable a better understanding of our unique contribution to the literature by [1] specifying the functional form of the relationship between structure and design and [2] offering the managerial insights derived from the analytical findings which are supportive of the recent thesis in the organization learning literature.

32

3) Literature review

Whenever applicable, we provided relevant literature to the preceding revisions.

b. Hypothesis 2

Your suggestions on hypothesis 2 are greatly appreciated. Upon reflection, the development of hypothesis 2 in the previous draft was not clearly written, lacking support from the prior literature, which caused unnecessary confusion, even though it does bring out an interesting contrast between “global” and “local” performance evaluation. The comments from the reviewer essentially reflect the same problem. Accordingly, H2 is now better developed: starting with a discussion in the introduction section (p. 4), with the explicit contrasts (between H2A and H2B) explaining our rationale for the predictions (pp. 10-11), and concludes with the implications of the findings (p. 28). We believe the revised manuscript now clearly articulates the merits of investigating hypothesis 2 and the basis for making differential predictions.

c. Three-way interactions

Your suggestions here, together with those relating to the introduction and motivation section, clearly point to the need for deepening the link between our manuscript and the prior contingency theory literature. We appreciate and agree with your assessment.

The previous draft treats uncertainty as a construct in measuring product strategy – a position that we should not have taken upon extensive review of the prior literature. Uncertainty and product strategy should have been treated as separate constructs regardless of their empirical correlations. We believe this misspecification caused further confusion.

In the revised manuscript, we now make it clear that the focus of the manuscript is on the performance contingency effect between structure and strategy, both are the results of adaptation to, and learning from, the changing environment (see discussion on pp. 2, second paragraph). Given this focus, we view the environmental variables (for which uncertainty is a part) as the control variables. Thus, our study is in sharp contrast to the previous works – which focus mostly on the contingency link between environment and strategy or between environment and design choices.

With this current focus, we believe it is crucial to first filter out all the environmental effects (including those related to uncertainty) from the dependent measure (i.e., ROA) before examining the interactions among the structure and strategy variables implied in the hypothesis. We also revised our analyses accordingly using a two-step regression, pp.20 and footnote 12. We believe by taking the preceding perspective, the revised manuscript is able to focus on its contributions to issues of theoretical and managerial interest. By contrast, if we were to follow the three way interaction perspective, the focus of the manuscript would be completely different and we are unsure [1] if this tradeoff is worthwhile

33

given the nature of the three way interactions remains unclear, especially with respect to the functional form and [2] our data set has sufficient power to model the underlying dynamic of the interactions.

In addition, the revised draft no longer confounds the measurement of uncertainty to that of product strategy. Per your suggestion (see later), the measurements used in the revised draft for product strategy are now directly tied to the prior literature.

Methods and Measures

1: Sample

As a response to your suggestion and reviewer’s comment (response to reviewer Point # 1), there have been several changes made to the sample. First, throughout the paper we now use 194 unique observations. Each firm accounts for a single entry. The number of observations increased because we changed the variables used in the analysis, and the new set of variables was available in 20 more observations. Table 2 was added to explain how we arrived at the 194 observations.

Per your suggestion to compare our sample to the total population, we have added Table 3, Panel B, of demographic data about our sample. This table shows, and we discuss this in the text, that the firms in our sample are larger than the average firms in COMPUSTAT. We state that one of the limitations of this study is that we have underrepresented smaller firms, so extrapolating our results to such firms may not be possible.

Unlike most surveys, response rates are not a problem in this situation because firms pay to participate in the CAPS studies. Therefore, once they become part of the organization, they participate. Thus, the "non-response bias" that occurs with other surveys is not a problem here. However, there is a self-selection bias because firms choose to participate. By comparing the sample and industry means, we have identified how the self-selection bias affects our sample.

2: Measures

a: Confirmatory Factor Analysis

Thank you for pointing out the need for using confirmatory factor analysis to validate our measurements for product strategy and organization design. We agree that this would be an ideal way. However, we did not do so for the following reasons.

1. Confirmatory factor analysis is commonly used in studies that have relied on survey responses to confirm construct validity and insure that the measurement does not suffer from perceptual bias. In contrast, measurement of the constructs in this study is based on archival data (i.e., CAPS and COMPUSTAT). While using archival data mitigates perceptual bias, it presents a sample size problem in our context. As you have correctly pointed out, the main concern we are facing by using a holdout sample for testing the validity of the constructs is the size of our sample.

34

2. However, we did follow very closely your suggestion to identify the empirical proxies for measuring product strategy based on the prior literature (see pp. 12-17). In doing so, we believe the measurement now is grounded in the prior literature and is explicit on the selection criteria (see page 13) and thus allows for replications and making comparisons to the past and future studies. As for the proxies for the design, we are restricted to the archival data set collected in the CAPS survey. Again, we now tie the measurement to the prior literature.

To make sure that the readers are aware of this orientation, we make it clear that our use of the factorial analysis is for data reduction rather than hypothesis testing (Harman 1967, Kim and Mueller 1978). Specifically, the factor analysis is for reducing the dimensionality of the proxies (for measuring product strategy and design structure) and with the resulting factor scores to be used in the later analyses when testing the main hypotheses.

3. The main focus of the study is to investigate the performance contingency effect between product strategy and design rather than validating their construct validity. In fact, given the vast amount of the literature on both constructs and the disparity in the measurement approaches (e.g., survey vs. archival) in the literature, future studies may find this investigation to be worthwhile. Granted that our measurement may suffer in precision for lacking a confirmatory analysis treatment, we believe the noise in the measurement could bias against finding the results (i.e., the interaction effects and the functional form) we hypothesized.

b. Measure for Product Strategy

In essence, your comments point to the need to tie the measurement of product strategy to the prior literature. We agree and have revised the measurements extensively to make them more credible and more focused.

To better measure Product Strategy, we reviewed the prior literature extensively to insure that the empirical proxies we now use in the revised manuscript are rooted in the prior literature. As indicated in the revised manuscript, our conceptualization of product strategy is based on Porter’s framework (see page 12-13) and is now being proxy by six measures: R&D Propensity, Advertising & Administrative to Net Sales, Relative Gross Margin, Market to Book Ratio, New Capital Investment to Sales, and Asset Utilization (see pages 13-14).

In addition, the new measure of Relative Gross Margin is a ten year moving average of the differences of a firm’s gross margin against industry mean gross margin. It thus removes the industry effects on margin.

Concerning your observation that some of these measures are correlated with ROA, we agree. In fact, by resorting to the use of “objective” rather than “subjective” measures of product strategy, it is unavoidable. However, we are comfortable with this tradeoff in that the main focus of our study is on the interaction rather than

35

the main effect (see footnote 7, p. 14).

We have also addressed your concerns on the coefficient of variation and cash flow predictability. We no longer used these two measures to proxy product strategy.

Justify the use of ROA per Accounting literature

We have reviewed the accounting literature to identify papers that are studying similar questions to ours using ROA as the dependent variable. Balakrishnan, Linsmeier, and Venkatachalam, (1996) make the argument that ROA is an appropriate performance measure when the phenomena being studied can improve a firm's gross margins and profits but may require additional assets to produce the benefits. In such cases, looking solely at income or asset utilization measures of financial performance would be inappropriate. Rather, using return on assets to combines both measures and enables an examination of their joint effect on firm performance.

c. Measures for design

In the prior version, we attempted to describe the anticipated congruencies in the discussion of the measures. This is what lead to your concerns about whether specific variables were measures of strategy or structure design. In this revised manuscript, we have discussed measures exclusively in the Measures for Product Strategy and Measures for Organization Design at Purchasing Management Level sections. We believe that this will eliminate your concern.

d. Editorial consistency – done. e. Control Variables

Thank you for your comments on the control variables. The revised manuscript now contains a much broader set of control variables as indicated by the prior literature, including those at the environmental and industry levels (see p. 19 and Appendix 1).

Analysis

a. Cross-sectional and Time series data

Your observation concurs with the reviewer’s comment (point # 1) that our earlier analysis suffered from a problem of pooling both cross-sectional and longitudinal data in the analysis. In theory, a panel data approach would be the ideal model for the analysis (Green, Ch. 16, 1993). Unfortunately, our sample is not a balanced panel (i.e., same number of years of observations from each firm); and the technique requires a minimum of two years of observation for each sample firm. Thus, under the panel analysis many of our sample firms will have to be dropped. This will further reduce the sample size. Given that we have a small sample to start with, an unbalanced panel approach is deemed impractical. For the same reason, it is impossible to have a change model.

Alternatives to a formal panel analysis are as follows. 1) Taking the mean value of the independent and dependent variables of different years of a sample firm and make it into one entry for each firm [Lang & Lundholm, 1993]; or 2) using just a single year

36

for each firm (e.g., using the most recent observation available in the sample for each firm) for the analysis.

In this revision, we have taken the first approach. Although in the current text we only report findings from the “mean value” approach; qualitatively, results from the “most recent year” approach are quite similar to those based on the “mean value” approach (please see footnote 6 in the text).

The final sample size for the analysis is 194 distinct observations and is consistent throughout the analyses in the paper. Table 2 shows how we arrived at that number. The reason that the number of unique firms in the sample increased is because we eliminated/added some variables based upon the reviewer's comments. As a result, the number of complete data sets increased from 174 to 194 firms.

b. Lag Effects:

There are two difficulties with presenting a lag model for our analysis. First, there are no clear event dates from the data set. Hence, we do not know when the firm made its strategic and design decisions. Thus, we are unable to hypothesize how long (or even if) we should lag the performance measures from the independent measures. For example, if the firm has adapted its strategy and design in the past, then the effect of those changes would already be seen in the current performance measures. Second, if firms only recently made those choices, we should not find the hypothesized performance congruency effect. Thus, using an un-lagged model biases against our results. Because of these reasons, we believe that using data from the same year is appropriate.

However, to evaluate the robustness of our findings, we also ran the model using a one-year lag model, and the results did not change (see sensitivity analyses on p. 25).

Editorial points

1. Citations:

We have added appropriate scholarly references; including many suggested by the reviewer.

2 & 3:

We have shortened the title of paper as you suggested. Also, materials not belonging in the method section have been removed.

37

Memorandum to Reviewer

Thank you for your encouragements and constructive comments. We believe, your comments and those from the associate editor, help us immensely to improve the focus, clarity and contributions of the paper. Compared to the previous version, the revised manuscript now contains a much deeper link to the prior literature and with stronger managerial implications. We also made significant revisions to the measurement and data analysis sections to address the issues that you and the associate editor raised. Below is an outline of our revisions to the manuscript, organized based on the sequence of the comments in your review. Whenever applicable, we briefly summarize the essence of your comments to ease the review process and to communicate our interpretation of your concerns and suggestions.

Sample and statistical analysis (Comment #1)

Thank you for the valuable comments; we agree with your observation that our earlier analysis suffered from a problem of pooling both cross-sectional and longitudinal data in the analysis. In theory, a panel data approach would be the ideal model for the analysis (Green, Ch. 16, 1993). Unfortunately, our sample is not a balanced panel (i.e., same number of years of observations from each firm); and the technique requires a minimum of two years of observation for each sample firm. Thus, under the panel analysis many of our sample firms will have to be dropped. This will further reduce the sample size. Given that we have a small sample to start with, an unbalanced panel approach is deemed impractical.

Alternatively, as per your suggestion, we can take the mean value of the independent and dependent variables of different years of a sample firm and make it into one entry for each firm [Lang & Lundholm, 1993]; or using just a single year for each firm (e.g., using the most recent observation available in the sample for each firm) for the analysis. Although in the current text we only report findings from the “mean value” approach; qualitatively, results from the “most recent year” approach are quite similar to those based on the “mean value” approach (please see footnote 5 in the Text).

The final sample size for the analysis is of 194 distinct observations and is consistent throughout the analysis. Table 2 shows how we arrived at that number. The reason that the number of unique firm in the sample increases is because we eliminated/added some variables based upon the reviewer's comments. As a result, the numbers of complete data sets increase from 174 to 194 firms.

Comments (#2, #3 and #4)

In essence, your above comments speak to the need to rethink the study’s motivation, research focus and its managerial implications. The associate editor also made similar (and extensive) comments.

The revised manuscript now focuses more on testing the general implications of contingency theory. In so doing, purchasing management becomes the context of

38

theory testing. We further highlight that fact that purchasing management is an important context for theory testing, especially with the rising interests in business-to-business e-commerce.

Accordingly, we have significantly re-written the introduction (pp. 1-2) to reflect the need to test the broad theories of performance contingency effect between product strategy and organization design. Additional efforts were made to highlight the practical significance of the issue and our contributions to the literature (pp. 3-4). Whenever applicable, we also made the needed revisions and/or enhancements throughout the rest of the manuscript to further elaborate on the impacts of the preceding changes.

Sharpen the difference between H1 and H2 (comment #5, #12) and Clarify H2 (Comment #9 and #10)

You suggestions are highly appreciated. Upon reflection, the development of H 2 in previous draft was not clearly written, lacking support from the prior literature, and has caused unnecessary confusions, even though it does bring out an interesting contrast between “global” and “local” performance evaluation. The comments from the associate editor essentially reflect the same problem.

Accordingly, H2 is now better developed: starting with a discussion in the introduction section (pp. 5), with the explicit contrasts (between H2A and H2B) explaining our rationale for the predictions (pp. 10-12), and concludes with the implications of the findings (pp. 28-29). We believe the revised manuscript now clearly articulates the merits of investigating H 2 and the basis for making differential predictions between H1 and H2

Definition of “matching” (Comment #6)

Per your excellent suggestion, we have reworded Hypothesis 1 and changed the word “matching” to “congruence” to a better reflection of a non-binary and adaptive nature of structure variables in the paper.

“Page 9 confusing” (Comment #7)

We agree and the revised manuscript should make the discussion clear.

Benchmarking (Comment #8)

We have brought benchmarking discussion toward the front of the paper. In the first section on pp. 5, we have included the paragraph that introduces our second research question, and motivates our analysis with a discussion of the contradicting nature of benchmarking practices with the contingency theory.

39

Monotonicity (Comment #11)

Basically you suggest a better and more readable presentation. On this the associate editor expressed the same concerns. We thus revised the presentation accordingly. The discussion following H1 is now kept at the conceptual level (pp. 8-9) without resorting to the prediction of the functional form of the relationship. Instead, the testing and the discussion of the functional form are provided later in the hypothesis testing section with a series of self explanatory numeric examples derived from the analytical findings (see pp. 22-24). In addition, the managerial implications of the findings are discussed in the results and implications section (pp. 26-29). We believe the preceding changes should enable a better understanding of our unique contribution to the extant literature by [1] specifying the functional form of the relationship between structure and design and [2] offering the managerial insights derived from the analytical findings which are supportive of the recent thesis in the organization learning literature.

Main effects vs. Interaction effects (Comment #13)

Agree, we have de-emphasized the importance of the main effects. All discussions are now focused on interaction effects and its implications.

Editorial

Thank you for your suggestions (including the citation of Doty et al). We believe the revised manuscript avoids those abuses to the minimum.

40

附件五 活動剪影

政大商學院長周行一教授親臨開幕致詞

41

論文發表

42

43

附件六 專題演講摘要

時 間:2007.7.18(三) 09:00〜:12:00 地 點 :商學院 6 樓元大講堂

主講人 :Dr. Yuhchang Hwang

主題:Research in Managerial Accounting: idea discovery to paper presentation and publication 記 錄 :翁慈青 會議記錄內容 利用這個機會和大家分享心得,分享做文章的過程,主要在討論管理會計研究趨 勢,討論內容如下所述: 1. 管理會計研究方面是主流還是不主流呢?這個問題很大。講者有很多研究是在 管理期刊中發表,事實上,做研究是很辛苦的,收到的回饋永遠是負面的。在 美國,當助理教授沒有在期限內達到發表篇數,就必須離開,故要做有興趣的 議題。 2. 一個好的研究者一定是好的老師。倘若博士生沒有實務經驗,在教管會上,根 本不知道重點在哪裡,因此作管會的學者一定要了解產業,其中,管會包括了 幾個大綱目。

Costing and Pricing

Management Control 一般而言,績效評估放在 Management Control Equity Valuation 裡,但是講者認為績效評估應該獨立出來探討

3. 到底往後管會的研究要做什麼呢?

(1)Costing and pricing:早期很多人作 cost driver 的研究,但是現在已不是趨勢, 現在有人做的研究有: a. Cost stickiness: 也就是在探討成本具有黏度關係,但是講者懷疑,到底對 產業有什麼關聯性,貢獻程度也沒那麼大。 b. Cost of quality: (a) 成本和品質管理的關係:到底做什麼品管能夠控制成本使其達到效率 極大化,醫療的部分最適合做這方面的研究,未來醫館是一個產業的 發展重點。管會可以探討醫療管理的部份,至於 IT 產業,從 IT security 來看,是很重要的,但是這些和管理會計有關嗎?我們可以從管線系 統設計 vs. 策略 vs. 成本系統管理與成本控管的角度切入。

44 (b) Process efficiency:很有發展,並且可以與產業結合。 (c) Value chain:不同部門,不同位置的員工,其績效指標是不一致的。 本身績效就會使經營管理有效性造成衝突,如何設計來解決這些問 題,也是研究議題之一。Supply chain 在管會的研究上都有在作,但 是和績效評估都沒有關係。 (2) Management Control a. Inter-organization b. Intra-organization: 是很有趣的議題,尤其是台灣電子產業。很多企業組 織型態是超乎想像的,例如,廠房裡零組件或設備屬於下游廠商,給下 游廠商的租金取決於下游廠商下單的訂貨量,如果訂貨量不如預期,我 可以用下游廠商的設備來生產產品,然後賣給下游廠商的競爭者,以達 到制衡的目的。甚至可以寫一個個案,探討這方面的契約是如何制定的, 因此不要侷限在傳統的思維觀念裡。 c. Strategic orientation: 例如 BSC,如何取加權數,這會受到主觀權重所影 響,和 missing 有關聯。例如 Reward 與 measurement 的選擇,如何放在 一起探討,都是目前面臨的問題。

(3) Agency theory and management control

a. 模型必須能夠預測或分析才適合使用代理理論模型去探討。要弄清楚代 理理論必需學個經、高等微積分、高等統計學等基礎訓練課程。 b.若要作 Linear model,講者建議用賽局理論,因為賽局理論是在找出各個 玩家的均衡解,而不是一昧的找出最適解,有時後實際的情況是各玩家 寧願增加不確定性,例如以開採阿拉伯石油為例。 (4) Performance measurement a.一般而言,被視為傳統的管理控式系統,故應該是屬於單獨的一個系統,其 架構如下: Organization Human resources Labor economics Integrated theory Performance

45

b.績效評估的研究議題:進行績效評估,誘因的設計(例如,如果要避免員 工跳槽時,該如何做),管理控制與誘因,如何從績效衡量來探討公司價 值,都是進行績效評估研究最主要的議題。

(a)誘因的設計若需要較低的 turnover,此時就需要有足夠的 information sharing , 然 後 再 考 慮 incentive design , 進 而 決 定 performance measurement。 問題與討論 1.對於一個研究者而言,即使研究議題好,仍然會有資料不足的困境,此時該怎 麼辦呢? Ans:作一個研究者,不怕沒有資料,只怕沒有議題。議題好不好很重要!沒有找 對題目,如果產業不拿來看,不願拿來參考,就是不好的研究。管會人才的 缺乏主要在於作管會的研究不易上前三大期刊,因此較少人願意作管會,然 而 Ohlson 重視的是,研究能不能提供產業參考,講者認為如果能將 Earning forecast or valuation 與 performance measurement 連結,則能結合管會和財會, 但是 performance management 是看過去的,valuation 是看未來的,如何將過 去與未來相結合探討,相信能夠提供學術界及產業界參考,並增加會計存在 的價值。 2.會不會是公司內部的 compensation 無法提供外部參考,所以才會使該研究產生 問題及困難? Ans:除了訂價和股價,會計界人士都忽略了績效指標的重要性。績效指標 vs. 績 效衡量 vs. 計價,之間應該會有關聯性存在。 Compensation 裡面對於 Cash flow, return 或 aggregation 所著重的權重不一樣,這會牽涉到績效契約及績效 指標的設計與衡量,唯有釐清架構,才能看到這些連結。

46

Agency theory

Valuation

Fundamental

47

3.當產業愈需要特殊技能的員工,員工被訓練或適合公司的型態,一旦公司訓練完這 個員工,他的特殊技能只能適合這間公司,此時員工也沒有能力跑到其他公司去了。

Ans:雖然如此,公司也需要這類員工,故員工也會希望公司能提供他們適切的 promotion 或 salary,此時就會影響公司與員工的最適契約設計。

48 附件七 論文計畫與研習心得摘要

自治理權力觀點探討高階經營團隊、董事會、

與財務報表品質間的關連性

張瑞當 魏若婷 中山大學企管所教授 中山大學企管所博士生壹、摘要

過去研究探討管理者為達成公司目標績效而進行盈餘管理的裁權行為時,乃關注 在公司治理機制與財務報表品質間的關連性,忽略自組織中治理權力的觀點探討的重 要性,代理理論強調權力是公司治理的核心問題,公司治理研究亦倡導治理權力在管 理者與董事會間分派的重要性,然而以前這類文獻亦僅關注在瞭解管理者(特別是 CEO)或董事會治理權力與公司績效間的關連。近來研究建議未來應探討高階經營團 隊,本研究考量電子業重視高階經營團隊的產業獨特性,自高階經營團隊治理權力(任 期、財務背景、持股比例、專業背景異質性)的觀點檢視自利的管理者是否會影響財 務報表品質。此外,公司治理研究主張權力維持平衡的重要性,本研究尚探討董事會 治理權力(任期、財務背景、獨立董事兼職數、董事會會議)對高階經營團隊治理權 力與企業財務報表品質間關連性會有的影響,以瞭解這些治理權力間的交互效果。貳、論文後續修改方向及參與研習營心得

一、茲就黃教授與吳教授提供的建議及本研究的回覆,本研究的改進方向及目前進度 如下: 1. 教授們的建議: 可就高階經營團隊中組織成員不同位階權力分配探討,像是探討薪酬的分配,或 是輔以訪談與調查以瞭解組織中權力的分配。49 本研究回覆: 由於探討組織成員不同位階權力分配,需要輔以訪談與調查,因此可能需徵詢某 些公司主管以深入瞭解組織中的階層權力分配狀況,或是透過管道或信件等方式 徵詢願意接受訪談的公司。 2. 教授們的建議: 本研究探討主題陳舊有待改進。 本研究回覆: 由於公司治理與盈餘管理間關連的研究主題似乎已過多研究探討,本研究擬修改 題目或朝向其他方向找尋其他感興趣及與本研究攸關的主題。 3. 教授們的建議: 若探討財務報表品質,應再納入其他的相關代理變數,及考慮其他 的構面。 本研究回覆:由於盈餘管理不能完全代表財務報表品質,因此本研究尚在思考若更 換此研究主題,則應變數財務報表品質的代理變數便不需再加強,若仍延用此變 數時,則可能再加入其他財務報表品質的代理變數。 4. 教授們的建議:針對論文理論推導部份有待再加強。 本研究回覆:由於本研究旨在探討公司治理與財務報表品質的關連,因此若未修改 題目,則在最初理論推陳的部分有待加強,因為在剛開始的前言部分,未將探討 公司治理與財務報表品質的關連作一個好的連結,以致在假設的部份欠缺邏輯合 理性。 5. 教授們的建議:可將研究中改為探討特定的人士,像是 CEO 或 CFO。 本研究回覆:本研究目前仍在思考是否僅要探討特定的重要公司人士,還是要更換 主題,因為似乎探討 CFO 會是較有趣的方向。: 二、本研究目前進度: 由於本研究是需要大修或更改另一個值得探討的研究主題,目前仍在思考此次研 習會各教授提供的建議,並考量未來研究在期刊的定位是在會計期刊或管理期刊,期 能做出一個能夠為學術期刊所接受並發表的文章。

50

The Characteristics of Innovation Teams and Diversity of

Performance Measurement

張菁萍

國立中山大學企業管理學研究所 博士生

I. Abstract

The purpose of study is to investigate the relationships among the characteristics of innovation teams, diversity of performance measurement and organizational performance. The path analysis is adopted to test the sample of 92 manufacturing companies in Taiwan. The empirical results suggest that formalized structure, innovation strategy and management support are positively related to diversity of performance measurement. In addition, diversity of performance measurement has a direct and positive association with organizational performance (including financial and non-financial performance). Finally, formalized structure, innovation strategy and management support have indirectly positive effects on organizational performance through diversity of performance measurement. Keywords: Characteristics of innovation teams, Diversity of performance measurement,

Organizational performance

II. 論文後續修改方向及參與研習營心得

茲依據黃教授與吳教授的悉心指教,未來後續修改方向一一列述如下: 1.二位教授均提到本研究之題目與研究議題相當不錯,惟需要再強化突顯創新團隊的 「特徵」部分,例如除了「知識來源」、「創新策略」之外,其他本研究所列出「正 式化」、「管理者的支持」二者似乎無法強烈地與「創新團隊的特徵」獲得連結。未 來本研究將根據二位老師的建議,運用田野調查 (field study) 訪問幾家公司來歸納 出創新團隊的特徵,並且再補強創新團隊特徵的相關文獻及經濟學、管理學等方面 的理論基礎,使得本研究之理論架構更趨於完善。 2.黃教授提醒「企業結構產業特徵」可能造成之影響,例如不同公司的產品特性在創 新團隊特徵上可能會有所不同。因此,未來將納入產品特性的考量,讓本研究之研 究內容更為豐富。51 3.二位教授指出,本研究假說 2a 及 2b 所提出的多元績效衡量與公司績效之間的關 係,由於創新所呈現出來的績效可能會有時間落遲 (lag) 之問題,而無法立即反應 於公司的績效上,況且可能會影響績效的雜音 (noise) 很多。因此,本研究將依據 黃教授的建議把焦點放在創新成功的衡量上,如產品上市時間、回應市場需求的時 間等衡量方式。 4.黃教授強調誘因計劃 (incentive scheme) 的重要性,例如升遷、訓練等因素的影響。 因此,本研究之未來研究方向可朝獎酬制度 (如個人獎酬、團隊獎酬) 方面上的探 討。 在此次研習營中,本研究有相當難得的機會,得以與黃鈺昌教授及吳安妮教授經 由互動式的討論方式來學習請益; 二位教授均殷切地提供本研究十分寶貴意見,讓身 為博士生的我獲益良多,相信在黃教授及吳教授指導之下,本研究能更臻完整,並如 同二位教授所言未來很有機會發表於相當不錯的國際期刊中。另外,更重要的是,在 這次活動中,讓我獲得很大的學習成長,對於我未來學術研究之路有非常大的幫助。

52

台商母公司無形資產與大陸子公司會計績效關聯性之研究

彭智偉 楊朝旭 崑山科技大學會計系 成功大學會計系壹、摘要

根據經濟部投審會2004年出版之大陸投資事業營運狀況調查分析報告顯示,台商赴 中國大陸投資高達45億美金,其經營績效對於台灣母公司影響甚鉅。然而,約四成台商 在中國大陸卻是處於虧損狀態。母公司無形資產具有擴充性、網路效果等經濟特性,是 海外子公司發展競爭優勢的重要資源,然而海外投資相關文獻卻鮮少研究在什麼情況下 無形資產可促進海外企業的經營成效。有鑑於此,本研究旨在探討策略及產品多角化是 否會影響台灣母公司無形資產對大陸子公司績效的外溢效果。明確而言,根據資源基礎 理論,本研究預期台灣母公司採差異化策略者,較能提升母公司無形資產對大陸子公司 的外溢效果。同時,本研究亦預期台灣母公司與大陸子公司產品為相關多角化時,大陸 子公司較能快速充分利用母公司目前擁有的無形資產,因而提升了母公司無形資產的外 溢效果。由於無形資產具有部分排它(partial excludability)的經濟特性,企業因應 之道在於快速充分利用目前擁有的無形資產,企業界可透過本研究瞭解如何透過策略及 產品多角化的規劃來提升無形資產對海外子公司的外溢效果。 關鍵字:無形資產、海外投資、外溢效果、公司策略、產品多角化。貳、論文後續修改方向及參與研習營心得

問題一:企業策略衡量及無形資產衡量有重覆使用變數的情形 回應:在企業策略的衡量有使用到研發支出變數,同時在無形資產的衡量也有使用到研 究支出變數,這可能會造成自變數之間有共線性的可能。因此,在無形資產投資 以研究發展費用、廣告費用、折舊費用與帳列無形資產等代理變數,計算出公司 與同業中位數間的差額,並以此一差額(RDF、ADF、DEPF、INTAGF)與同業中位53 數(RDI、ADI、DEPI、INTAGI)納入因素分析中求取因素分數來進行後續迴歸分 析,以克服上述的情形。 問題二:台灣母公司在大陸、香港或新加坡上市並不多,可能會影響到樣本數 回應:本文預期大陸子公司採差異化策略時,因資源有限而特別需要母公司無形資產資 源的挹注,因此母公司無形資產的外溢效果較強。但這樣的分析需要大陸子公司 在大陸、香港或新加坡上市家數夠多,才有足夠的財務報表資料可以衡量。為了 克服大陸子公司樣本數的不足,本文擬以台灣母公司採差異化策略的角度來衡量 研究假說 2,換言之,當台灣母公司採差異化策略時,其策略與資源投資搭配程 度較佳。亦即差異化策略台灣母公司相對於非差異化策略台灣母公司,其對大陸 子公司無形資產外溢效果較強。 問題三:本篇文章可以試著投管理類的期刊 回應:我們非常贊同黃鈺昌教授觀點,本文之後也會朝管理類的期刊發表。特別是歐洲 國家特別重視無形資產的議題,本篇文章以後將試著在歐洲管理類的期刊發表。 問題四:台灣母公司對於大陸子公司投資經營現況為何 回應:根據經濟部投審會調查報告,可以初步的了解台商在大陸投資的現況。本文可以 可進一步選取在大陸設立子公司的台灣上市公司進行個案的訪談,以更清楚了解 台商在大陸投資的狀況。 問題五:台灣母公司無形資產可以針對其經濟特性作更貼切分析 回應:Lev(2001)指出無形資產具有兩個重要的價值動因,分別為擴充性(scalability)及網 路效果(network effect)。擴充性係指無形資產可重複使用、保存容易、維護成本 小及邊際報酬遞增;網路效果係指網路外部性、正向回饋效果及標準化效果。在

Edvinsson and Malone(1997)和瑞典 Scandia AFS Group 亦開始了一連串有關無形 資產的研究與應用,並將無形資產區分為人力資本、結構資本及顧客資本等三大 類。本文將針對黃黃鈺昌教授的建議,分別探討人力資本、結構資本及顧客資本 與擴充性(scalability)及網路效果(network effect)的關係。

54

Factors Effect on Implementation of IFRS: A Developing Country

Perspective

Shwu-Hsing Wu

Department of Accounting Information Tainan University of Technology

I. Research Motivation

Many developing countries commit to the adoption of the fair-value-oriented of International Financial Reporting Standards (IFRS) in recent years to meet the need of the development of economy, due to the strong demand of a great level of transparent and reliable accounting information to the participants of the international capital market. There is a debate in the literature on the usefulness of fair value of IFRS accounting information in the developing countries, the usefulness of IFRS accounting information may subject to the strong enforcement of accounting standards, effective capital market infrastructure and institutions, which controls manager’s use financial reporting judgment under IFRS principles (Eccher and Healy, 2000; Chen, Sun and Wang, 2002; Ball, Robin and Wu, 2003).

China commits to substantially converge its accounting standards with International Financial Reporting Standards (IFRS) starting from Jan 1, 2007. Convergence with IFRS in China raises a concern whether the current Chinese capital market infrastructure and institutional environment base have matured to support the implementation of the fair-value-oriented accounting system? Wi-Guo Zhang, a chief accountant with the China Securities and Regulatory Commission (CSRC), points that adopting the principle-based and fair-value orientation accounting system provides big challenge for the preparers, users, and regulators of financial information in China. The application of IFRS principles rely more on financial reporting judgment than the traditional Chinese accounting system. Implementation of fair values accounting may increase opportunities in accounting manipulation when the market price is not actively (Holthausen and Watts, 2001).

Eccher and Healy (2000) argue that IFRS accounting information did not provide additional material benefit to Chinese investors in the early age of Chinese capital market infrastructure during the year 1992 - 1997, due to the ineffective control mechanism and infrastructure to monitor management’s exercise of reporting judgment under IFRS. To prevent managers using financial reporting judgment to manipulate earnings, China regulates some restriction in fair value measure in 2001. In addition, China has policy changes, and revised its regulation for shareholders’ protection, disclosure requirement, renovated institutions and financial infrastructure in recent years. Such as, in 2001 and 2002, the CSRC released a series of disclosure requirements and standards to ensure quality of disclosure; A Qualified Foreign Institutional Investor Program was introduced in 2002 to allow Foreign investors to invest in A-shares, Treasures, convertible bonds and corporate bonds listed on