Local institution contingencies for the effects of local

market orientation on foreign SMEs’ performances:

Evidence from an emerging market

當地機構的權變因素對當地市場導向與績效之影響—

以外國中小企業於新興市場營運為例

Tsai-Ju Liao1

Department of Insurance and Finance, National Taichung University of Science and Technology

Sheng-Hung Yu

The Department of Business Administration, National Yunlin University of Science and Technology

I-Chien Liu

Department of Insurance and Finance, National Taichung University of Science and Technology

Tai-Ying Chiou

Department of Insurance and Finance, National Taichung University of Science and Technology

Abstract: Foreign small- and medium-size enterprises (SMEs) often adopt local market-oriented strategies to capture emerging market opportunities, but such strategies do not guarantee success. This study provides a multi-institutional framework for understanding how local institutions influence the effect of local market orientation on the performance of foreign SMEs. Analyzing a sample of 6147 Taiwanese manufacturing firms investing in China, this study finds that well-established legal and financial institutions have a positive moderating effect on the relationship between local market orientation and foreign SME performance. Furthermore, we disentangle agglomeration economic institutions by distinguishing between specialized and diversified agglomeration economies and show the positive moderating effects. This study contributes to both academia and industry by testing how foreign SMEs characterized by

1

Corresponding author: Tsai-Ju Liao, Department of Insurance and Finance, National Taichung University of Science and Technology, No. 129,Sec. 3,Sanmin Rd, North District,Taichung City 404, Taiwan. E-mail: tjliao@nutc.edu.tw.

constrained resources rely on local institutions to overcome liabilities of foreignness.

Keywords: Local market orientation, legal institutions, financial institutions, agglomeration economic institutions, performance.

摘要:外國中小企業 (SME) 常採用當地市場導向策略,以獲取新興經濟發 展的機會。但是這樣的策略並不保證成功。本研究提供多重機構構面之架構, 以瞭解當地機構如何影響當地市場導向對外國中小企業績效的影響。本研究 分析 6147 家台灣製造商投資中國為樣本,發現良好的法律與財務機構對當 地市場導向與外國中小企業績效之關係有正向干擾效果。再者,本研究拆解 群聚經濟機構為專業化與多樣化群聚經濟,並發現其對當地市場導向與外國 中小企業績效之關係有正向干擾效果。本研究對於資源有限的外國中小企業 如何利用當地機構,以克服其外國人負債提供理論與實務上的見解與貢獻。 關鍵詞:當地市場導向、法律機構、財務機構、群聚經濟機構、績效.

1. Introduction

Due to the rapid growth that often characterizes emerging economies, many ambitious small- and medium-sized enterprises (SMEs) seek to exploit emerging market opportunities, but foreign SMEs are typically regarded as resource-constrained, lacking the market power to operate viably in local markets (Hessels and Terjesen, 2010). This is believed to be especially true for foreign SMEs from emerging economies. In such cases, the SMEs will likely rely heavily on local institutions for access to local resources. Several previous studies have stressed the impact of differing institutional distances across countries (e.g., Bevan, Estrin, and Meyer, 2004), while largely ignoring the variations that may exist within a single nation. Such differences are particularly characteristic of China. Because of China’s uneven implementation of economic liberalization policies, the implications of institutional variation within it require further exploration. While recent studies have started to examine the different facets of institutions such as legal system development and intellectual property rights (e.g. Li, Vertinsky, and Zhang, 2013b; White, Boddewyn, and Galang, 2015) and informal relationships with governments

(Kotabe, Jiang, and Murray, 2011; Zhou, 2014) distinctively, relatively little research has integrated other formal and informal institutions within one framework. Moreover, given the fact that foreign SMEs have limited capacity to change institutions, North (1990) and Chang and Park (2005) suggest to choose a location with favorable formal and informal institutional contexts (including legal) as well as financial and agglomeration economic institutions that are important indicators of the general business environment in emerging economies.

The legal institutions that provide contract and legal expertise to solve local disputes are of critical concern to foreign SMEs seeking to adopt a local market orientation in emerging economies. Since emerging economies are known to be complex and sometimes unstable environments characterized by information asymmetry and operational uncertainty (Chen et al., 2009), well-developed legal institutions can help to reduce foreign SMEs’ transaction costs and foreign liabilities (Bruton, Ahlstrom, and Obloj, 2008). Furthermore, adopting a local market orientation generally gives rise to enhanced local trade and local cooperation. In fact, the degree of local market orientation exists along a continuum, rather than being treated as dichotomous. We suspect that foreign SMEs adopting a higher degree of local market orientation are likely to benefit more from well-established legal institutions than are those foreign SMEs implementing a lower degree of local market orientation.

Lack of access to financing has also been identified as a key obstacle to the survival of foreign SMEs (Zhu, Wittmann, and Peng, 2012). While most studies have used the presence of public equity markets as a proxy for financial institutions (e.g., Guler and Guillén, 2010), the liability of smallness increases the difficulty for foreign SMEs seeking to gain capital through the public equity markets. Accordingly, this study focuses on the availability of credit from banks. Specifically, if financial institutions generate a greater proportion of loans to the private sector, then this indicates greater freedom for financial institutions. In addition, although foreign SMEs may hold a scarcity of assets such as financial capital and technical capabilities, they particularly may need much more financial resources to effectively contend with international and local competitors in increasingly competitive local markets (Danis and Shipilov, 2012). If local financial institutions can provide greater financial support, then foreign

SMEs, to some extent, can devote themselves to the development of new and innovatory products, but it takes a long time and a large amount of costs to fully develop and commercialize product innovations (Chin, Huang, and Lee, 2018). Thus, having access to sources of financial resources is essential to the successful development of foreign SMEs in local markets (Xiao and North, 2012). Along these lines, as foreign SMEs adopting a greater level of local market orientation can acquire local financial support, it would likely help them to enter a new market to capture and benefit much more from fleeting market opportunities; thus, well-developed financial institutions likely provide greater value to foreign SMEs adopting a higher degree of local market orientation.

With regard to agglomeration of economic institutions, this study defines it as the ecosystem that emerges when foreign firms choose to co-locate their enterprises in regions where many other foreign firms are located. Most studies have discussed the effects of geographically-agglomerated firms in the same industries (i.e., specialized agglomeration economies) (Chang and Park, 2005), while ignoring the effects of geographically proximate firms in different industries (i.e., diversified agglomeration economies). Specialized agglomeration economies serve as sources of industry-specific resources and knowledge (Gilbert, McDougall, and Audretsch, 2008). In contrast, the benefits of diversified agglomeration economies are realized through the exchange of knowledge across diverse industries (Jacobs, 1969), thus increasing the likelihood of serendipitous events that provide innovative ideas and enhance innovation. Given the fact that a local market orientation requires foreign SMEs to continuously innovate and modify their products to establish themselves in local markets, we anticipate that both specialized and diversified agglomeration economies are greater significant drivers of the performance of foreign SMEs adopting a higher degree of local market oriented strategies.

This paper makes several contributions to the existing literature. First, we explicitly integrate institutional and strategic perspectives that allow us to derive relevant institutional contingencies based on the value of a local market orientation. Second, this study helps to unpack the “black box” of institutions by capturing the effects of local legal, financial, and agglomeration economic attributes. Furthermore, we shift the focus from examining whether institutional environments matter, to studying how they matter to foreign SMEs

with different levels of local market orientation, which appears more meaningful. Third, by distinguishing between specialized and diversified agglomeration economies, this study suggests that these two distinct regional economic institutions may be the keys for SMEs to overcome the liabilities of foreignness and smallness. Fourth, we contribute to the literature by testing how a foreign SME from an emerging economy operates in another emerging economy, as those SMEs with constrained resources face many hurdles in host countries.

2. Literature review

The internationalization of SMEs has increasingly attracted the interest of scholars (Kiss, Danis, and Cavusgil, 2012), with most studies focusing on foreign SMEs investing in advanced countries (Bruton et al., 2008). Recently, however, foreign SMEs have begun to invest in newly liberalized emerging markets and to adopt those local market orientations that will enable them to benefit from rapid economic growth. There are several possible reasons why this may be the case: to either preempt or avoid being preempted by their rivals’ entry into a specific host country; to reduce the costs of communication with and learning about customers; and to lower transaction costs including transportation, tariffs, as well as import barriers on foreign-made products (Nachum and Zaheer, 2005). Additionally, Li, Wei, and Liu (2010) suggest that local market orientation encourages the refining and adapting of existing technologies for current needs. Along these lines, foreign SMEs characterized by local market orientation likely utilize their capabilities efficiently and effectively (Yayla et al., 2018), thus improving their performance.

Implementing such a locally oriented strategy is not likely to benefit all foreign SMEs (Halaszovich and Lundan, 2016; Liu, Li, and Xue, 2011). Some scholars find that local market orientation tends to be positively associated with profitability (Li, Liu, and Thomas, 2013c), while others present the reverse (Ito and Fukao, 2010). One possible reason for this discrepancy in findings, according to institutional researchers, is that institutions determine what arrows a firm has in its quiver as it struggles to formulate and implement strategies and to create competitive advantages (Ingram and Silverman, 2002).

an unfamiliar local community, such an orientation may be associated with a higher level of outcome uncertainty and a greater probability of failure (Li et al., 2013c). Being aware of this, local market-oriented foreign SMEs are likely to search for local institutional support to mitigate the uncertainty and risk posed by their strategic orientation. Practically speaking, however, institutional development is far from consistent or complete across regions in emerging economies such as China (Gao et al., 2010; Cai, Boateng, and Guney, 2019). China has been undergoing a radical change from a centrally-planned to a market-based economy, and the change has been accompanied by heterogeneous institutional transitions in political systems, legal frameworks, financial systems, and economic institutions. One stream of research has examined the impact of formal political institutions, investment regulations (Djankov et al., 2002), and formal legal frameworks that are able to support property rights (Zhou, 2014) and intellectual property rights (Li et al., 2013b).

Another stream of research has highlighted the effects of informal institutions. Since informal institutions are less transparent, they can easily become a source of uncertainty (Meyer and Nguyen, 2005). Furthermore, even though a legal framework can be changed radically to create a new set of formal rules (e.g., laws and regulations), the transformation of informal institutions often lags behind changes in the law (e.g. Bevan et al., 2004). Given the fact that the unobservability and unpredictability of informal institutions are sources of significant uncertainty for foreign SMEs, this study chooses to integrate the impacts of formal and informal institutions. Existing research on informal institutions in the context of China has focused on the establishment of trust-based relationships with local governments (Zhou, 2014; Zhao and Lu, 2016) and local partners (Kotabe et al., 2011), with less attention on the ecosystem of informal institutions. Recent studies have begun to explore the effects of legal institutions on ownership decisions (Henisz, 2000), the impact of the emergence of financial institutions on the entrance of U.S. venture capital investors (Guler and Guillén, 2010), and the influence of economic institutions on Japanese firm owners’ involvement (Delios and Beamish, 1999). To our knowledge, little research has been conducted on the influence of both formal institutions (i.e., legal and financial institutions), and informal institutions (i.e., agglomeration economic institutions) in the context of foreign SMEs from one

emerging economy operating in another emerging economy. Due to the distinct characteristics of emerging economies, this study looks to fill that gap in the research.

2.1 Legal institutions

Although China’s legal system has undergone significant changes, the development of legal institutions characterized by legal expertise under the implementation of these changes has remained limited (Fernandez and Weinstein, 2004). In any given locality, it takes time to establish the legal institutions required to underpin the law, as well as to train lawyers who will deliver knowledge about—as well as help carry out—laws and legal proceedings (Bevan

et al., 2004). Thus, this study takes the proportion of lawyers within a region as

a proxy for the development of legal institutions.

Lawyers act to protect the legitimate interests of various parties (Guler and Guillén, 2010). First, lawyers enable the credible communication of information between parties to a transaction and help to resolve conflicts about or discrepancies in information. Second, lawyers work to handle credit defaults or behavior that could be construed as violations of contracts. Third, lawyers often take on the role of knowledgeable business advisers for foreign firms by providing high quality professional services and play a critical role in sustaining legal institutions, and efficient legal infrastructures facilitate the establishment and enforcement of contracts while reducing the transaction costs of doing business (Li et al., 2013b). Indeed, examining a sample of domestic SMEs within a technology cluster in China, Zhang and Li (2010) find that company ties to law firms are positively related to product innovation. When it comes to local resource exchanges with a variety of parties, the availability of advice from local professional sources becomes essential for foreign SMEs. To advance the literature, we further examine whether legal institutions moderate the relationship between foreign SMEs with a local market orientation and enterprises’ performance.

2.2 Financial institutions

Emerging economies are generally known for having underdeveloped or poorly functioning financial institutions, resulting in the diminished availability

of credit (Chakrabarty, 2009). While the development of public equity markets is often taken as a proxy for the development of financial institutions (Chacar, Newburry, and Vissa, 2010), it cannot be wholly assumed that there is a common model for financial institutions across emerging economies. In fact, for most emerging economies—including China—the central government maintains tight control on public equity markets to avoid instability. The result of such control is that bonds and equities remain at around only 10% and 5% of total financial services, respectively, while bank lending remains at a level above 85% (Milana and Wu, 2012). Therefore, in China the best proxy for financial institutions appears to be bank lending markets.

While foreign firms making international expansions are supposed to hold sufficient financial resources from their home countries, most foreign SMEs only carry constrained financial recourses. In such cases, debt financing from local banks is important in helping foreign SMEs expand their presence in local markets. However, in China the allocation of bank lending is often distorted (Gao et al., 2010). Specifically, financial assets in some regions are disproportionately composed of loans allocated to state-owned enterprises (SOEs) (Wu and Shea, 2008). This constrains the availability of loans for foreign SMEs’ medium- and long-term investment needs, thus hampering their ability to engage in product innovation, market expansion, and organizational growth (Levin and Zervos, 1998).

As prior studies have demonstrated the positive role of well-established financial institutions, it is still not clear whether financial institutions influence the performance of foreign SMEs operating in emerging economies. Furthermore, even though foreign SMEs may acquire financial resources from their home markets, it is not enough when they continuously engage in expanding local markets and developing new products. Our study suggests that heterogeneity in the development of China’s financial institutions across regions may partially explain variations in the performance of local market-oriented foreign SMEs.

2.3 Agglomeration economic institutions: Specialized and diversified agglomeration economies

agglomeration economies—i.e., those economies created by a geographically concentrated group of foreign firms—that are highly subject to economic externalities. While research on agglomeration has highlighted benefits, including accessibility to specialized suppliers, workers, and market demand (Marshall, 1920; Teller, Alexander, and Floh, 2016; Cieslik and Gauger, 2018), the presence of such benefits simply is not enough to explain spatial agglomeration. Research has begun to point out that agglomeration facilitates knowledge spillover, which plays a key role in helping firms overcome liabilities of foreignness (e.g., Bronzini, 2007).

Several studies have highlighted the knowledge spillover that occurs within a group of geographically proximate foreign firms in the same industries (e.g., Lamin and Livanis, 2013; Hecht, 2017), hereafter referred to as “specialized agglomeration economies.” In situations of collocation with other foreign firms in similar fields, new ideas can be quickly disseminated through observation, imitation, and the rapid inter-firm movement of skilled labor. Thus, foreign SMEs benefit from the complementarities and synergies that arise from the technological improvements undertaken by other firms in a cluster.

Knowledge externalities may not just exist in the same industry. Another line of research presents a different type of knowledge spillover, occurring in clusters of foreign firms in different industries (Feldman and Audretsch, 1999), hereafter referred to as “diversified agglomeration economies.” A greater diversity in the local economy likely produces a more abundant and diverse supply of technical knowledge that could potentially spill over. Jacobs (1969) proposes inter-industry spillovers, explaining that important knowledge transfers often come from outside a core industry. Such economic diversity also promotes innovative behavior (Maine, Shapiro, and Vining, 2010), which in turn fosters firm performance and often firm value.

The empirical results associated with the relationship between specialized agglomeration economies and performance are surprisingly not consistent. Gilbert et al. (2008), surveying a sample of initial public offerings (IPOs) among technology-based ventures in the U.S., and Li (2004), exploring a sample of foreign firms operating in China, find that locating within geographic clusters can contribute to the absorption of external knowledge as well as facilitate innovation enhancement and performance improvement. In contrast, Feldman

and Audretsch (1996) note that industry localization does not significantly increase firm growth or innovative activity.

The empirical evidence on diversified agglomeration economies is also mixed. Using regional-level aggregate data, Feldman and Audretsch (1999) present that the proximate presence of firms from diverse industries facilitates economic growth. Employing firm-level data from the information and communication technology industry, Maine et al. (2010) show that proximity to a cluster within a diverse metropolitan area is associated with firms’ superior performance. However, Bronzini (2013), examining a sample group of industrial and service-oriented Italian firms, observes that specialized agglomeration economies encourage inward foreign investment, whereas diversified agglomeration economies have no impact.

We suspect that such inconsistent findings may result from ignoring firms’ strategic orientation, which will cause very different interactions with different types of agglomeration economies. As foreign SMEs become increasingly oriented toward local markets in emerging economies, they face highly dynamic environments associated with significant uncertainty, thus encouraging them to search for external information and to engage in environmental analysis (Chou, Yang, and Chiu, 2016). Furthermore, foreign SMEs typically suffer from serious unfamiliarity with local environments, including a lack of knowledge of local resource holders such as buyers or customers. Accordingly, these foreign SMEs may place significant value on specialized and diversified agglomeration economies. We seek to examine the interaction effect of specialized and diversified agglomeration economies and local market orientations on foreign SMEs’ performance.

3. Hypotheses

3.1 The effect of local market orientation and legal institutions

Legal institutions affect the relationship between local market orientation and the performance of foreign SMEs in two ways. First, the facilitating effect of legal institutions may be due to the fact that local market orientation will expose foreign SMEs to local market volatility and unpredictability in emerging

economies. In general, foreign SMEs tend to face high risk from ex-ante inverse selection and ex-post opportunistic recontracting from transaction parties (Henisz, 2000). In such situations, the presence of lawyers allows for more consistent contract enforcement and the protection of property rights (Zhang and Li, 2010). Subsequently, well-established legal institutions would likely reduce contractual hazards and reinforce the performance of foreign SMEs.

Second, frequent changes in taxation and regulation increase the difficulties for foreign SMEs of immediately adapting to local legal frameworks. Due to unfamiliarity with local laws and customs, foreign SMEs may be forced to engage in costly preparations for potential disputes, which may increase the cost of their interactions with local resource providers, including suppliers and consumers. Well-established legal institutions, characterized by a sufficient number of trained lawyers, are likely to reduce transaction costs for foreign SMEs in cases of transaction disputes. The presence of local legal expertise also does not merely facilitate the knowledge of local laws on the books, but offer an experience-based, culturally sensitive expertise that grows from day-to-day legal practice, as well as creativity in dealing with the economic, political, and cultural contexts in lawyers’ work is embedded (Liu, 2008). Such legal institutions give rise to the resolution of the non-fulfillment of contractual obligations, as well as support land registration and legal services for foreign direct investment (FDI). We thus expect that foreign SMEs adopting a greater degree of local market orientation will realize significantly more value from well-established legal systems. This leads us to put forth the following hypothesis.

Hypothesis 1. There is a stronger positive relationship between foreign

SMEs’ local market orientation and their performance when local legal institutions are firmly established.

3.2 The effect of local market orientation and financial institutions When conjecturing that a high degree of local market orientation does not guarantee a high level of profit, it is important to consider whether the value of local market orientation is contingent on financial institutions. Foreign SMEs targeting local market orientation must continue to develop new products to match market changes and to pay attention to expanded options. However, due

to their liabilities of smallness, foreign SMEs’ financial resources brought from their home countries are limited. In such cases, if foreign SMEs choose to locate within a better-established financial institutional context, then they are better positioned to access financial resources, including loans, as well as to leverage potential market opportunities. In contrast, a lack of local credit availability may become a major inhibitor to the growth of foreign SMEs, as it may force them to turn to other more expensive sources (Park, Li, and Tse, 2006). Similarly, Zhang, Ding, and Ke (2019) find that technological innovation needs strong financial support to enhance the growth of SMEs.

China has pursued incremental transformation by decentralizing government control. Some internal regions have seen significant movement toward more openness, and well-developed financial institutions are pushing for better support of non-state firms (Park et al., 2006). However, other regions have been constrained in the development of free financial institutions, because their local governments have seized the opportunity to pursue their own interests. Additionally, China is awash in bad debt and has come to be known for its “triangle debt” problem (Liao and Young, 2012). Hence, the lack of a well-developed financial institutional context likely increases transaction costs and makes it more difficult for foreign SMEs to achieve their goals of market expansion, as well as influence the profits derived from local market penetration.

Wolpert (2002) further suggests that local banks sit at the intersection of many firms and can facilitate the exchange of information about operational issues among firms. Therefore, regions characterized by liberalized financial institutions may enable foreign SMEs to plug into local networks to broaden the scope of their external financial and knowledge search, as well as reduce their search costs (Zhang and Li, 2010). Subsequently, the facilitating effect of local market orientation on the performance of foreign SMEs will be improved. Therefore, we propose the next hypothesis.

Hypothesis 2. There is a stronger positive relationship between foreign

SMEs’ local market orientation and performance when local financial institutions are firmly established.

3.3 The effect of local market orientation and specialized agglomeration economies

Variation in the performance of foreign SMEs adopting a local market orientation can be attributed to their locations’ differing levels of specialized agglomeration economies. Specialized agglomeration economies—i.e., pools of geographically proximate intra-industry foreign firms—create a market for high-quality labor and suppliers and help foreign SMEs cope with the underdeveloped factor characteristic of emerging markets (Li, Chen, and Shapiro, 2013a). Furthermore, intra-industry agglomeration provides ample opportunities for inter-organizational knowledge spillovers, either through face-to-face interactions or as a result of the mobility of knowledge-carrying employees (Lamin and Livanis, 2013; Rigby and Brown, 2015). This is because knowledge is sticky and place-specific, and the ability to transfer knowledge decays with distance. When foreign SMEs adopt a greater level of local market orientation, they require a deeper involvement in local markets. By interacting with a group of technologically-advanced foreign firms, foreign SMEs likely gain significant access to advanced technology and management skills (Kotabe et al., 2011), adapt to local manufacturing conditions, and ensure a good match with local market requirements. Accordingly, as foreign SMEs become more highly local market-oriented, they will likewise become more attracted to locations with specialized agglomeration economies than will their less local market-oriented counterparts.

It could be argued that the presence of an intra-industry, geographically proximate group of foreign firms is likely to become a hotbed of competition (Teller et al., 2016). In fact, Baum and Mezias (1992) find that competition among large generalist organizations at the center of a particular market actually works to liberate the peripheral resources most likely to be used by small organizations - that is, increased concentration among generalist organizations likely increase failure among large generalists, but decrease failure among small specialists. In this way, many foreign SMEs could exploit locally available resources without directly competing with large generalists. Therefore, specialized economies derived from intra-industry foreign firm agglomerations help foreign SMEs increase their local search depth, while lowering search costs.

Such local search depth also allows foreign SMEs to align their initiatives with industry trends appropriately. Accordingly, we propose the following hypothesis.

Hypothesis 3. There is a stronger positive relationship between foreign

SMEs’ local market orientation and performance when the local specialized agglomeration economy is firmly established.

3.4 The effect of local market orientation and diversified agglomeration economies

Instead of assuming that local market orientation always enhances the performance of foreign SMEs, we incorporate diversified agglomeration economies into our examination of how local search breadth enhances the relationship between local market orientation and foreign SME performance. First, for foreign SMEs adopting a local market orientation, the absorption and application of inter-industry knowledge are of significant strategic importance in the generation of rents (Cheng, 2017). Such knowledge helps foreign managers explore new, locally relevant ways of doing things, reduces redundancy, and enhances their knowledge diversity (Kotabe et al., 2011). They can also understand what local customers want and what products other geographically proximate foreign firms offer, thus providing an opportunity for them to see the gaps in products and services and to modify their own products accordingly. Along these lines, foreign SMEs that collocate with a group of foreign firms from diverse industries have a better chance of broadening their knowledge search scope than those without such a location (Maine, Shapiro, and Vining, 2010). Thus, diversified agglomeration economies enable foreign SMEs to understand domestic market demands and competition, thereby facilitating innovation as well as performance. Jaffe, Trajtenberg, and Henderson (1993) note that knowledge spillovers are not confined to closely related industries, as approximately 40% of citations do not come from the same primary patent class as the original patent. Li et al. (2013a), using information from Chinese manufacturing firms from 2000 to 2006, find that firms improve product innovation when they are located in cities with a group of firms in different industries. Similarly, Basile, Pittiglio, and Reganati (2017) state that industry variety reduces the likelihood of firm exit.

Second, foreign firms in different industries are less likely to compete with one another and may be more willing to share knowledge than firms within the same industry. In contrast, when foreign SMEs are strategically oriented toward exports and more focused on international markets, they will rely less upon local diversified externalities in their search for locally relevant innovations and modifications. Given such circumstances, the value of diversified agglomeration economies, with respect to firm performance, will be limited. Conversely, diversified agglomeration economies interacting with SMEs having a local market orientation are likely to enhance the performance of foreign SMEs. Thus, we put forth the following hypothesis.

Hypothesis 4. There is a stronger positive relationship between local market

orientation and foreign SMEs’ performance when diversified agglomeration economies are firmly established.

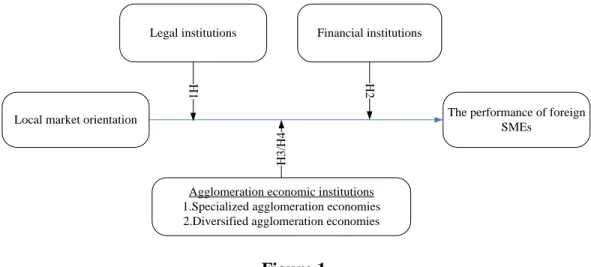

Figure 1 illustrates our research framework for this relationship.

4. Methodology

Our data come from Taiwanese manufacturing SMEs investing in China. These ventures are listed in a directory of Taiwanese firms’ foreign expansions, published by the China Credit Information Service (CCIS), one of Taiwan’s

Agglomeration economic institutions 1.Specialized agglomeration economies 2.Diversified agglomeration economies

H1 H2

Legal institutions Financial institutions

Local market orientation The performance of foreign

SMEs

H3/H4

Figure 1

largest business data publishing services (Luo and Chung, 2013). Our data allow us to focus on emerging-economy SMEs’ activities in a different emerging economy. In 2014, SMEs accounted for more than 97.61% of firms in Taiwan (Small and Medium Enterprise Administration, 2015). The significance of SMEs makes Taiwanese SMEs an interesting and, we believe, an appropriately representative subject for study. Following the European Union’s definition, we categorize firms with fewer than 250 employees as SMEs. Additionally, Taiwanese companies have invested heavily in China, becoming its eighth largest source of FDI (National Bureau of Statistics, 2015). Taiwan’s government statistics confirm this, reporting that the average percentage of Taiwanese firms investing in China relative to all other foreign countries was 60.26% for each year over the period between 1991 and 2016 (Investment Commission, 2016). Although Taiwan and China are neighboring countries with many cultural similarities, Taiwanese SMEs are not free from the liabilities of foreignness. O’Grady and Lane (1996) point out that countries sharing languages often have different institutions that do not allow for the simple transfer of business practices and attitudes across borders.

The choice of China as the host country is typically made on the grounds that China has emerged as one of the world’s largest recipients of FDI. Furthermore, China is an unevenly developed country with significant regional differences in legal and financial institutional quality, as well as in agglomeration economies (Du, Lu, and Tao, 2008), giving rise to distinct formal and informal constraints in different regions. This considerable institutional diversity across regions makes China an ideal context in which to explore how a local market-oriented strategy aligns with the impact of institutional forces in influencing the performance of foreign SMEs.

The second dataset on legal and financial institutional indices was developed by the National Economic Research Institute (NERI) (Fan, Wang, and Zhu, 2011). This index assigns each of the 31 provinces, municipalities, and autonomous regions a score that captures their progress in the development of legal and financial institutions. A higher score means better institutional development. Data supplied by NERI have been used to examine China’s institutional development in several previous economic and finance studies (e.g., Gao et al., 2010). The third dataset related to agglomeration economies also

comes from CCIS. We randomly cross-checked the data with information derived from the China Statistical Yearbook compiled by the National Bureau of Statistics of China and found them to be similar.

We choose to study the period between 2004 and 2006 for two reasons. First, a constitutional amendment in 2004 acknowledged that citizens’ lawfully owned private property is inviolable (Chen, 2007). In addition, at that time local private firms were encouraged to conduct their operations within local markets. Given such conditions, foreign SMEs were confronted with enormous challenges related to new, often dysfunctional competitive situations, as well as volatile markets. Second, given the availability of data and the elimination of the confounding effect of the 2007-2008 financial crisis, we employ the time period 2004-2006 to measure economic performance when testing our hypotheses. While the findings obtained from the time period between 2004 and 2006 seem out of date, several international business studies have also presented a wide gap between the published date and the time period covered by their surveys. For example, Chakrabarty (2009) uses data gathered between 1995 and 1996, while Cai, Boateng, and Guney (2019) examine a sample of European Union firms operating in China from 1997-2008. Such studies, to some extent, demonstrate that the examination of a historical trajectory is deserved. Each emerging economy may also have had different starting points and have arrived at different stages in the process. Our theoretical and managerial implications provided in China can likely be applied to another emerging economy that takes a similar path in its specific stages of development (like Vietnam).

Given the fact that not all firms have disclosed sales and performance data for each year, with some even leaving the sample set, we have to be extremely scrupulous in creating our final panel. Our dataset originally contained 14662 records of 6257 foreign SMEs for the time period 2004-2006. After deleting records with obviously inaccurate numbers (e.g., negative sales and negative local sales), we were left with 14251 observations 6215 firms. We then dropped 135 records whose founding year was before 1979, due to the fact that China began to implement its “open door” policy in 1979. We were left with 14116 observations on 6146 firms. We also dropped 74 observations corresponding to firms that entered and exited the database within two years.

Only firms with at least two years of operations were kept, in order to allow us to have reliable measures of firm performance. This procedure leaves a working sample of 14042 records on 6147 foreign SMEs for the time period 2004-2006.

We use pooled time-series data in testing the hypotheses, as potential autocorrelation is often presented in time series data. The results of the Breusch–Pagan test do not enable us to exclude the possibility of heteroskedasticity (p < .01). Therefore, we employ the generalized least square (GLS) analysis and choose a random effects model over a fixed effects approach, as the number of years of observations in this study is limited (Nielsen, 2010). Furthermore, a random-effects model enables us to consider both interfirm and intrafirm variations over time. We also conduct a Hausman test to determine which effects would be more suitable, and the result is not significant (p > .05), showing support for the use of random-effects models (Wooldridge, 2002). To correct for heteroskedasticity, we report the results with robust standard errors by applying the Huber-White sandwich estimator of variance to produce valid standard errors (White, 1980).

4.1 Measurement

Performance. Following previous studies (Luo and Chung, 2013), we

utilize return on assets (ROA) to measure foreign SME performance, defined as net income divided by total assets. ROA takes into account the efficiency of using a foreign SME’s assets and hence reflects its profitability.

Local market orientation. In keeping with Meyer and Nguyen’s (2005)

study, we employ the proportion of local sales as an indicator of a foreign SME’s local market orientation, specifically measuring it as the ratio of local sales to total sales. A higher percentage of local sales demonstrates that foreign SMEs pay more attention to local markets’ requirements and local consumers’ desires.

Legal institutions. As suggested by Zhang and Li (2010), Li et al. (2013b),

and Che and Wang (2013), we measure legal institutions as the ratio of the number of lawyers to total provincial population using data from NERI. A score for each province is then normalized to a value between 0 and 10, proportionately, to measure legal institutional conditions relative to other provinces. We match the index with our multi-year data. Score indices beyond the base year of 1997 are relaxed from the 0–10 restriction to reflect

institutional changes over time.

Financial institutions. Aligned with Levine and Zervos (1998), we

calculate the proportion of banking loans to the non-government sector as a proxy for financial institutions using data from NERI. Such a ratio quantifies the financial institutional development in terms of the credit given specifically to the non-government sector. Indeed, Chakrabarty (2009) observes that a lack of such credit is related to a financial institutional void of credit availability.

Specialized agglomeration economies. We use the level of

geographically- concentrated foreign firms in related industries as a proxy for specialized agglomeration economies. Following Li’s (2004) and Bronzini’s (2007) suggestion, this measure is defined as the ratio of foreign firms within an industry in a region to all firms in the industry nationwide. Industries are classified according to the Standard Industrial Classification (SIC) three-digit industry codes. These industry- and province-specific measures capture the extent to which foreign firms in an industry are clustered within a province.

Diversified agglomeration economies. In creating this variable, we use a

measure of it inspired by the Herfindahl index, which is equal to the sum of the squared foreign firms’ proportion across all the three-digit industries within a province (Feinberg and Gupta, 2004). Furthermore, a common measure of diversity is the inverse of such a Herfindahl index. This study therefore gives the diversity measure by DIVi = 1/∑ℎ𝑖𝑖=1𝑥𝑥𝑖𝑖𝑖𝑖2, where xij denotes the share of total foreign firms in three-digit industry j within province i to all firms within province i, where h denotes being across all three-digit industry codes. The Shapiro–Wilk test reveals that diversified agglomeration economies are not normally distributed. Hence, we take the natural logarithm of such data.

Control variables. Prior studies have primarily focused on how internal

firm factors and external factors influence foreign SME performance; thus, we control for the following variables. Firm age is operationalized as the logarithm of the number of years since the founding of a foreign SME. Firm size is measured by the logarithm of the number of employees and represents the size of the available pool of resources or capabilities that could be exploited upon entering a new local market. Net working capital (in ten thousands of RMB) measures a firm’s capabilities to maintain the quality of its operations, as well as its credit, should it need to recover from an operating loss (Chen and Chuang,

2009). According to the Organization for Economic Co-operation and Development’s (OECD) (2003) industry classification, the industry dummy variable is coded as 1 if a foreign SME belongs to the high- or medium-high technology manufacturing sector. The low- or medium-low technology sector is offered as an alternative. Additionally, we insert several external factors with the aim of disentangling the effect of agglomeration from the effect of the geographical distribution of productive factor endowments. Potential market demand is operationalized as the yearly growth rate of consumption. Strong market potential likely influences foreign SMEs’ performance. Labor supply is presented as the manufacturing employee population within a province (in increments of 10,000); we expect that a large regional labor supply would influence foreign SMEs’ local operations and activities. Additionally, we include the growth rate of labor costs in the manufacturing sector (in thousands of RMB) to reflect the relative cost of regional labor within a province (Chang and Park, 2005). The growth rate of labor costs tends to have a negative effect on the performance of foreign SMEs.

This study examines the hypotheses related to local market orientation and institutions by using the following regression specification:

Performancei,t = f( Control variables +β1 Local market orientationi,t +β2 Legal institutionsi,t + β3 Financial institutionsi,t + β4 Specialized agglomeration economiesi,t +β5 Diversified agglomeration economiesi,t +β6 Local market orientation * Legal institutionsi,t +β7 Local market orientation * Financial institutionsi,t + β8 Local market orientation * Specialized agglomeration economiesi,t + β9 Local market orientation * Diversified agglomeration economiesi,t), where i stands for firm, and t stands for year.

5. Results

Table 1 provides the means, standard deviations, and correlations of all the var ia ble s. The dat a are inspect ed care fu lly be fo re t he ana lys is. Our results show that 37.15% of the firms are present in 2004, 31.59% of the firms are in 2005, and 31.26% of the firms are in 2006. Regarding firm size, our results report that 21.36% of the firms have fewer than 50 employees, 32.15% have between 51 and 100 employees, 22.26% have between 101 and 150

Table 1

Correlation matrix and descriptive statisticsa

Min Max Mean S.D. 1 2 3 4 5 6 7 8 9 10 11 12 13

1.Performance 0.00 12.50 .05 .19 1.00 2.Local market orientation 0.00 1.00 .78 .36 .02** 1.000 3.Legal institutions -0.14 10.00 5.72 2.79 .01 -.26** 1.00 4.Financial institutions 2.69 12.61 10.45 1.38 .01 -.17** .02 1.00 5.Specialized agglomeration economies 0.00 0.38 0.05 0.05 .03** -.01 -.07** -.16** 1.00 6.Diversified agglomeration economiesb 4.83 9.61 5.86 .96 .06** -.15** -.21** -.29** .12** 1.00 7.Firm ageb 1.39 3.43 2.51 .32 -.01 -.03** .02 -.10** .02** -.06** 1.00 8.Firm sizeb .69 5.52 4.47 .70 .01 -.16** -.03** .10** .02** -.05** .04 1.00 9.Networking capital -68.10 68.50 0.44 2.02 .09** -.01 .05 .02* -.01 -.03 .03 .05** 1.00 10.Industry dummyc .00 1.00 .33 .47 .03 .08 .02 .05** -.04 -.04 -.09 -.08** .05** 1.00 11.Potential market demand 104.10 118.20 111.63 2.63 .04 .11 .10** .32** -.08** .13** -.11** .02* -.01* .05** 1.00 12.Labor supply 1.40 387.30 149.37 119.98 .02 .04 -.30** .20** -.04** -.12** -.05** .07** .03** .02* .12* 1.00 13.Growth rate of labor cost -.08 .16 .02 .06 -.03** .01 -.32** .25** -.03** -.06** -.08** .04** -.02* .02** .08** -.08** 1.00

a: n=2200*3; ** indicates significant at .01; * indicates significant at .05. b: Logarithm. c: Coded 0/1. por at e Ma nage m ent R ev iew Vol . 3 9 No . 1, 201 9 21

employees, 14.69% have between 151 and 200 employees, and 9.54% have between 201 and 250 employees. Regarding firm age, our results show that 0.55% of the firms are less than 5 years old, 33.91% are between 6 and 10 years, 34.72% are between 11 and 15 years, 29.3% are between 16 and 20 years, 1.29% are between 21 and 25 years, and 0.19% are between 26 and 31 years. The length of operation within our sample ranges from 4 years to 31 years, with a mean of 12.91 years and a standard deviation of 3.90 years.

In our study the Taiwanese investments illustrate an extensive geographic and industrial distribution throughout China, with almost all provinces (except Xizang) represented, as well as every Standard Industrial Classification (SIC) two-digit manufacturing industry except SICs 21 (tobacco industry). Table 2 shows the distribution of foreign SMEs by industry and by region. Specifically, our findings suggest 93.58% of firms are in the coastal area, which is similar to Filatotchev et al. (2007) report of 92.63%. The rate of firms in computer equipment and electrical equipment industries is 27.45%, which corresponds to Chiang, Liao, and Liu’s (2008) finding of 29.83%. Along these lines, the similarities of sample characteristics make our study compatible with previous ones.

Table 3 summarizes the regression results based on the random effects models. We first estimate Model 1 with control variables. The findings show that net working capital, industry dummy, and potential market demand are positively related to performance (b = .001, p < .01; b = .001, p < .05; b = .003, p < .05, respectively, in Model 1). The growth rate of labor costs is negatively associated with performance (b = -.108, p < .05). Net working capital indicates a firm’s credit in defending its operating loss. The greater net working capital is, the greater is the financial performance realized by foreign SMEs. Regarding industry dummy, different sectors have different technological opportunities. Particularly, the spillover effects of economic knowledge externalities seem to be more significant in high-technology industries and thus enhance the profit potential of foreign SMEs (Tihanyi et al., 2003). Potential market demand is related to market size and economic development. Foreign investors likely value local market size as it can improve their financial performance (Hong, 2007). Additionally, labor costs can be used to analyze the regional labor market. Locations with low labor costs are expected to be more

Table 2

Frequency distribution of foreign SMEs by industry and by region Industry No. of firms Percentage Region No. of

firms Percentage

Food and kindred products 839 5.97% Beijing 207 1.47%

Textile mill products 850 6.05% Tianjin 231 1.65%

Apparel and other finished products made from fabrics and similar material

476 3.39% Hebei 134 0.95%

Shanxi 12 0.09%

Lumber and wood products, except furniture 317 2.26% Inner Mongolia

4 0.03%

Furniture and fixtures 233 1.66% Liaoning 293 2.09%

Paper and allied products 391 2.78% Jilin 25 0.18%

Printing, publishing, and allied industries 151 1.08% Heilongjiang 19 0.14%

Chemicals and allied products 1,264 9.00% Shanghai 2,282 16.25%

Petroleum refining and related industries 16 0.11% Jiangsu 2,929 20.86% Rubber and miscellaneous plastics products 1,313 9.35% Zhejiang 1,570 11.18%

Leather and leather products 231 1.65% Anhui 74 0.53%

Stone, clay, glass, and concrete products 595 4.24% Fujian 1,844 13.13%

Primary metal industries 509 3.62% Jiangxi 41 0.29%

Fabricated metal products, except machinery and transportation equipment

1,072 7.63% Shandong 514 3.66%

Henan 84 0.60%

Industrial and commercial machinery and computer equipment

1,739 12.38% Hubei 89 0.63%

Hunan 91 0.65%

Electronic and other electrical equipment and components, except computer

2,116 15.07% Guangdong 3,269 23.28%

Guangxi 52 0.37%

Transportation equipment 695 4.95% Hainan 22 0.16%

Measuring, analyzing and controlling instruments;

photographic, medical an

349 2.49% Chongqing 29 0.21%

Sichuan 126 0.90%

Miscellaneous manufacturing industries 886 6.31% Guizhou 15 0.11%

Total sample 14,042 100.00% Yunnan 27 0.19%

Shanxi 36 0.26% Gansu 11 0.08% Qinghai 5 0.04% Ningxia 2 0.01% Xinjiang 5 0.04% Total sample 14,042 100.00%

Table 3

Regression results for performancea

Model 1 Model 2 Model 3

Control variables

Firm ageb -.009(.006) -.005(.006) -.006(.006)

Firm sizeb .003(.003) .003(.003) .003(.003)

Networking capital .001(.001)*** .001(.001)*** .001(.001)***

Industry dummyc .001(.004)** .009(.004)** .009(.004)**

Potential market demand .003(.001)** .001(.001)** .002(.001)**

Labor supply .001(.000) .001(.001) .000(.000)

Growth rate of labor cost -.108(.023)** -.085(.022)*** -.083(.022)***

Independent variables

Local market orientation .004(.005) -.007(.007)

Legal institutions .001(.001)* -.001(.001)

Financial institutions .003(.002)** .003 (.002)*

Specialized agglomeration economies .004(.005) .003(.004)

Diversified agglomeration economiesb .014(.003)*** .014(.003)***

Interaction

Local market orientation * Legal

institutions .009(.003)***

Local market orientation * Financial

institutions .013(.003)***

Local market orientation * Specialized

agglomeration economies .009(.005)*

Local market orientation * Diversified

agglomeration economies .010(.006)* _cons .047(.002)*** .047(.002)*** .049(.002)*** Wald chi-square 111.62*** 141.15*** 156.35*** Df 7 12 16 Observations 14042 14042 14042 Number of firms 6147 6147 6147 R2 0.021 0.025 0.028

a: The method of General Linear Square (GLS) Random-Effects models is used to estimate the parameters of models, in which *** indicates significant at .01, ** indicates significant at .05, and * indicates significant at .10. Robust standard errors are reported in parentheses.

b: Logarithm. c: Coded 0/1.

attractive to foreign investors (Bissoon, 2012). Model 2 adds the independent variables, and Model 3 includes the examined interaction effects that are deemed necessary for testing this study’s hypotheses. To minimize the distortion caused by multi-collinearity, each scale is mean-centered (Aiken and West, 1991).

Before the analyses of interaction effects, the direct impact of local market orientation on foreign SMEs’ performance is examined. The results show that local market orientations do not have a significant effect on the performance of a foreign SME (b = -.007, p > .10). One possible reason might be that foreign SMEs adopting local market orientation need institutional support to operate in host countries. Furthermore, our results suggest that the interaction of local market orientation and legal institutions is positively related to the performance of foreign SMEs (b = .009, p < .01), thus supporting H1. To gain further insight into this relationship, we plot the interaction and conduct t-tests to examine the differences in slopes. This involves splitting the moderator (legal institutions) into a high group (two standard deviations greater than the mean) and a low group (two standard deviations less than the mean) and re-estimating the relationship between local market orientation and the performance of foreign SMEs.

The plot in Figure 2, Panel A shows that the slope of this line for high-legal institutions is significantly different from that for low-legal institutions (p < .01). The interaction term for local market orientation and financial institutions is positively related to performance (b = .013, p < .01), thus supporting H2. Figure 2, Panel B shows that when financial institutions are better established, there is a greater positive link between local market orientation and performance (p < .01). Such a case is similar to the matter of investment motivation proposed by Nachum and Zaheer (2005). Investment motivation likely interacts with institutional environments to influence firm performance. Recent studies have also suggested that well-established legal institutions are able to effectively handle inconsistent behavior that violates contracts in the context of the economic growth of cities in China (Che and Wang, 2013) and in the situations of entrepreneurial performance (Zhou, 2014). In addition, Guler and Guillén (2010) acknowledge that well-established legal institutions and equity markets induce venture capital firms to make foreign direct investments.

Panel A Panel B Figure 2

Interaction effects: Legal and financial institutions

The interaction between local market orientation and specialized agglomeration economies is positively related to the performance of foreign firms (b = .009, p < .10), thus supporting H3. The plot in Figure 3, Panel A shows that the positive slope between local market orientation and performance is stronger when the degree of specialized agglomeration economies is high than when it is low (p < .01). Similarly, the product of local market orientation and diversified agglomeration economies is positively related to performance (b = .010, p < .10), thus supporting H4. Figure 3, Panel B shows a greater positive

Panel A Panel B Figigure 3

relationship between local market orientation and performance when the level of diversified agglomeration economies is high than when it is low (p < .01). Li, Yang and Yue (2007), looking at foreign subsidiaries in China in 1979-1995, also find that a community characterized by both the same industries and by different industries has a positive effect on foreign entry.

We may suspect whether the differences in the types of agglomeration economy matter to the performance of foreign SMEs. In order to examine whether the moderating terms of specialized and diversified agglomeration economies result in different effects, we conduct a t test to examine the relative influence of specialized and diversified agglomeration economies (Chan and Makino 2007).2 The resulting t value is .064 (p > .01), indicating that the moderating roles of specialized agglomeration economies in effecting the benefits of local market orientation seem to be equal to that of diversified agglomeration economies. There are two possible reasons to explain why this may be the case. First, although specialized agglomeration economies may carry positive and negative impacts on firms, foreign SMEs may see great benefits, while avoiding most of the disadvantages caused by agglomeration, because foreign SMEs focusing on niches can exploit most of the available resources without directly competing with large firms. In such cases, a good combination of specialized agglomeration and local market orientation would likely enhance the performance of foreign SMEs. Second, while previous empirical studies of diversified agglomeration economies show positive or no impacts on firms, foreign SMEs adopting local market orientation can gain benefits from diversified agglomeration, because foreign SMEs needs to broaden their local search breadth to adapt to local markets and to explore local market demands. Diversified agglomeration economies likely provide rich and valuable channels to foreign SMEs for absorbing new ideas and knowledge and thus increase differentiation by producing gaps.

While each model’s R2 is low, several studies in the field of agglomeration and international business have presented similar cases with low R2 (Knoben,

2

𝑡𝑡 = 𝑏𝑏1−𝑏𝑏2 �𝑆𝑆𝑏𝑏12 +𝑆𝑆

𝑏𝑏22

2009; Kuo et al., 2012). A possible reason for these results may lie in our institutional variables at the province level. Specifically, our sample to some extent is concentrated in several provinces; 23.28% of the firms operate in Guangdong, 20.86% in Jiangsu, 16.25% in Shanghai, 13.13% in Fujian, and 11.18% in Zhejiang. Such a sample structure likely leads to low variation of institutional variables at the province level and results in low R2 of our empirical models. Due to restricted data availability, we have only institutional variables at the province level. Future studies may improve R2 by extending the institutional variables to the city level.

We may also wonder whether financial flexibility would likely change the interaction term of financial institutions and local market orientation, because not all foreign SMEs are financially-constrained. Financially flexible firms are able to readily fund investment when profitable opportunities arise, while avoiding financial distress in the face of negative shocks (Ma and Jin, 2016). Most researchers have shown that financial flexibility could be attained through conservative leverage policies and liquidity holding decisions (Baños-Caballero, García-Teruel, and Martínez-Solano, 2016). In keeping with this line of research, we consider leverage and liquidity as proxies for financial flexibility. Leverage is calculated as the percentage of total debt to total assets, whereas liquidity is computed as current assets divided by current liabilities. Using these two proxies for financial flexibility, we divide our sample into different subsample groups.

We first classify foreign SMEs into low and high leverage firms by the medium of leverage (.504) and then employ our regression models separately as shown in Table 4. Regardless of low or high leverage foreign SMEs, the interaction terms of local market orientation and financial institutions are positively significant (b = .010, p < .01 in Model 4 for low leverage foreign SMEs; b = .006, p < .10 in Model 5 for high leverage foreign SMEs in Table 4). It indicates that for foreign SMEs adopting local market orientation, well-established financial institutions would likely provide superior support and values to their continuous innovation and help drive improved performance. Only for high leverage foreign SMEs do specialized and diversified agglomeration economies positively moderate the relationship between local

Table 4

Regression results for performance in different levels of financial flexibilitya Model 4 - Low Leverage Model 5 - High Leverage Model 6 - Low Liquidity Model 7 - High Liquidity Control variables Firm ageb -.016(.008)*** .013(.013) .026(.012)*** -.042(.008)*** Firm sizeb .003(.003) .013(.007)** .010(.006)* .008(.003)*** Networking capital .001(.001)*** .001(.001)*** .001(.001)*** .001(.001)*** Industry dummyc .012(.005)*** .007(.006) .006(.006) .009(.004)**

Potential market demand .002(.001)*** .002(.001)* .001(.001) .002(.001)***

Labor supply -.001(.001) .001(.001) .001(.001)** -.001(.001)

Growth rate of labor cost -.056(.024)*** -.045(.032)* -.045(.031)* -.061(.025)***

Independent variables

Local market orientation .003(.008) -.015(.010)* -.024(.011)*** .005(.008)

Legal institutions .001(.001) .002(.001)* .002(.001) -.001(.001) Financial institutions .001(.002) .006(.003)** .007 (.003)*** -.001 (.002) Specialized agglomeration economies .002(.003) .004(.007) .003(.005) .005(.007) Diversified agglomeration economiesb .014(.003)*** .020(.005)*** .018(.005)*** .014(.003)*** Interaction

Local market orientation * Legal institutions

.003(.004) .004(.004) .008(.005)** .004(.004)

Local market orientation * Financial institutions

.010(.004)*** .006(.004)* .009(.004)*** .009(.004)***

Local market orientation * Specialized agglomeration economies

-.001(.007) .008(.004)*** .010(.007)* .004(.004)

Local market orientation * Diversified agglomeration economies .003(.006) .012(.009)* .014(.009)* .001(.006) _cons .068(.003)*** .031(.004)*** .029(.004)*** .074(.003)*** Wald chi-square 140.06*** 73.88*** 79.01*** 131.94*** Df 16 16 16 16 Observations 7025 7017 7065 6977 Number of firms 3627 3698 3750 3628 R2 0.029 0.008 0.009 0.036

a: The method of General Linear Square (GLS) Random-Effects models is used to estimate the parameters of models, in which *** indicates significant at .01, ** indicates significant at .05, and * indicates significant at .10. Robust standard errors are reported in parentheses.

b: Logarithm. c: Coded 0/1.

market orientation and performance separately (b = .008, p < .01; b = .012, p < .10, in Model 5). The reason may be that high leverage foreign SMEs (i.e., low financial flexibility) are less able to access and restructure their financing at a low cost (Zainudin, Ibrahim, Said, and Hussain, 2017). As such, they likely turn to acquire resources provided by geographic concentrations of firms within the same industry or heterogeneous industries. In sum, foreign SMEs characterized by high leverage not only need the assistance of financial institutions, but also require specialized and diversified agglomeration economies to gain access to external resources.

Second, we categorize firms according to the liquidity of foreign SMEs and consider those firms with a greater ratio than the sample median (i.e., the medium of current ratio is 1.37) as firms with more financial flexibility. The results of low liquidity firms are in Model 6, while those of high liquidity firms are in Model 7. We see that the moderating role of financial institutions at affecting the benefits of local market orientation seems to be equal, regardless of whether foreign SMEs’ liquidity is high or not (b = .009, p < .01 in Model 6; b = .009, p < .01 in Model 7). Furthermore, legal institutions have a positive moderating effect on the relationship between local market orientation and performance for low liquidity foreign SMEs (b = .008, p < .05 in Model 6), but not for high liquidity foreign SMEs (b = .004, p > .10 in Model 7). Specialized agglomeration economies moderate higher for the relationship between local market orientation and performance in the low liquidity group than in the high liquidity group (b = .010, p < .10 in Model 6; b = .004, p > .10 in Model 7). Similarly, the positive moderating effect of diversified agglomeration economies on performance is greater for the low liquidity group than in the high liquidity group (b = .014, p < .10 in Model 6; b = .001, p > .10 in Model 7). In sum, the value of local market orientation in performance is likely to be realized more with well-established legal institutions, specialized agglomeration economies, and diversified agglomeration economies for low liquidity foreign SMEs (i.e., financially-constrained foreign SMEs) than for high liquidity foreign SMEs (i.e., non-financially-constrained foreign SMEs).

We finally bring a specific liberation act into our analyses to compare the differences of foreign SMEs’ performances between ex-ante and ex-post periods of the act. We choose the year 2004, because the China government enacted a

constitutional amendment for citizens to lawfully own private property. With the guarantee of private property rights, the operation and development of local private firms began to boom. Increasing competition made it imperative for foreign SMEs operating in local markets to gain access to resources supported by institutional environments. Thus, using data between 2004 and 2006 seems to be an appropriate way to test our hypotheses in the ex-post period of the private property liberation act.

Due to restricted data availability, we only possess data of 2003 to examine our hypotheses in the ex-ante period of the private property liberation act. The findings employed by a linear regression model show no significant interaction effects (p > .10), indicating that only the results in the period of 2004-2006 demonstrate significant moderating roles of institutional factors, while not for the period of 2003. Accordingly, we posit that institutional factors have greater impacts on foreign SMEs’ performance in the period of lawfully owned private property, as compared to the period of unguaranteed private property.

5.1 Robustness test

We test the sensitivity of our results in several ways. First, we examine other performance measures, such as return on equity (Luo and Chung, 2013). The results from both are similar, shown in Model 8 of Table 5. Second, because the data contain observations of foreign SMEs across several years, there may be unobserved characteristics or propensities that influenced the foreign SMEs in their performance. We therefore include two year dummies to control for the three years. The results are similar and presented in Model 9 of Table 5. Third, we also estimate our regression using lagged-structure models by regressing performance in year t+1 on all independent variables in year t to correct for potential endogeneity. The results do not change, though the remaining sample size consists of 7949 observations, which are reported in Model 10 of Table 5.

Fourth, while the number of lawyer represents a sufficient proxy for the development of legal institutions, several studies have suggested measuring the impact of patents granted to establishments (Delios and Beamish, 1999; Guler and Guillén, 2010). Therefore, an alternative measure used is the growth rate of the ratio of patent applications granted to gross capital within a province, which

Table 5

Regression results for performance in robustness testsa Model 8 performance: ROE Model 9 year dummy Model 10 lag Control variables Firm ageb .064(.098) -.006(.007) -.011(.011) Firm sizeb .013(.030) .003(.003) -.005(.003) Networking capital .000(.001) .001(.001)*** .001(.001)*** Industry dummyc .067(.084) .009(.004)*** .003(.005)

Potential market demand -.020(.020) .003(.001)*** .005(.003)**

Labor supply -.481(.509) -.001(.001) -.001(.001)

Growth rate of labor cost -.112(.077)* -.095(.023) -.077(.038)

Independent variables

Local market orientation -.004(.001) .005(.008) -.007(.013)

Legal institutions -.020(.017) -.004(.001) -.007(.004)

Financial institutions .003(.018) .001 (.002) -.002 (.004)

Specialized agglomeration economies .004(.030) .002(.004) .008(.008) Diversified agglomeration economiesb .015(.038) .009(.002)*** .007(.005)* Interaction

Local market orientation * Legal

institutions .023(.016)* .006(.003)*** .005(.004)

Local market orientation * Financial

institutions .005(.003)* .009(.003)*** .010(.004)***

Local market orientation * Specialized

agglomeration economies .006(.004)* .009(.005)** .128(.009)*

Local market orientation * Diversified

agglomeration economies .009(.006)* .008(.005)* .012(.008)* Year 2005 .020(.009)*** Year 2006 .030(.008)*** _cons .118(.029)*** .033(.005)*** .043(.009)*** Wald chi-square 84.57*** 175.64*** 79.02*** Df 16 18 16 Observations 14028 14042 7949 Number of firms 6147 6147 4544 R2 0.028 0.033 0.019

a: The method of General Linear Square (GLS) Random-Effects models is used to estimate the parameters of models, in which *** indicates significant at .01, ** indicates significant at .05, and * indicates significant at .10. Robust standard errors are reported in parentheses.

b: Logarithm. c: Coded 0/1.