Subscriber access provided by NATIONAL TAIWAN UNIV

Energy & Fuels is published by the American Chemical Society. 1155 Sixteenth Street N.W., Washington, DC 20036

Article

Economic Cost Analysis of Biodiesel Production: Case in Soybean Oil

†Yii-Der You, Je-Lueng Shie, Ching-Yuan Chang, Sheng-Hsuan

Huang, Cheng-Yu Pai, Yue-Hwa Yu, and Chungfang Ho Chang

Energy Fuels, 2008, 22 (1), 182-189 • DOI: 10.1021/ef700295c • Publication Date (Web): 02 October 2007 Downloaded from http://pubs.acs.org on December 12, 2008

More About This Article

Additional resources and features associated with this article are available within the HTML version: • Supporting Information

• Links to the 1 articles that cite this article, as of the time of this article download • Access to high resolution figures

• Links to articles and content related to this article

Economic Cost Analysis of Biodiesel Production: Case in Soybean Oil

†Yii-Der You,

‡Je-Lueng Shie,*

,§Ching-Yuan Chang,

‡Sheng-Hsuan Huang,

‡Cheng-Yu Pai,

§Yue-Hwa Yu,

‡and Chungfang Ho Chang

|Graduate Institute of EnVironmental Engineering, National Taiwan UniVersity, Number 1, Section 4, RooseVelt Road, Taipei 106, Taiwan, Department of EnVironmental Engineering, National I-Lan UniVersity, Number 1, Section 1, Shen-Lung Road, I-Lan 260, Taiwan, and Department of International

Trade, Chung Yuan Christian UniVersity, Number 200, Chung-Pei Road, Chung-Li 320, Taiwan ReceiVed May 28, 2007. ReVised Manuscript ReceiVed August 6, 2007

The economic costs of three biodiesel plants with capacities of 8000, 30 000, and 100 000 tons year-1were analyzed and assessed. The plants employ continuous processes using an alkali catalyst and the raw material of soybean oil. Six major economic cost factors were computed and examined. These include the fixed capital cost (FCC), total capital investment cost (TCC), total manufacturing cost (TMC), net annual profit after taxes (NNP), after-tax rate of return (ARR), and biodiesel break-even price (BBP). The NNP and ARR of plants with capacities of 8000, 30 000, and 100 000 tons year-1are -24× 103, 1975× 103, and 8879× 103U.S.

dollars (USD), and -10.44, 40.23, and 67.38%, respectively. The values of BBP of the three plants are 862, 724, and 678 USD ton-1(price in July 2007). The plant with a capacity of 100 000 tons year-1is economically feasible, providing a higher NNP and more attractive ARR with a lower BBP. Among the system variables of the plants examined, plant capacity, price of feedstock oil and diesel, and yields of glycerine and biodiesel were found to be the most significant variables affecting the economic viability of biodiesel manufacture. In summary, this study aims at the need to obtain useful information for economic cost analysis and assessment of the production process of biodiesel using soybean oil. It provides an appropriate indication for the promotion of biodiesel in the future, targeting the reduction of the cost of feedstock oil with the increase of the yields of valuable products with a reasonable plant capacity.

Introduction

Biodiesel has recently become more attractive in Taiwan because of its environmental benefits and the fact that it is made from renewable biological sources, such as vegetable oils and animal fats. Its commercial use as a diesel substitute began in Europe in the late 1980s. Continued and increasing use of petroleum will intensify local air pollution and magnify the global warming problems caused by CO2.1 Combustion of

petroleum diesel is a major source for emitting greenhouse gas (GHG). Apart from these emissions, it is also a major source for releasing other air contaminants, including NOx, SOx, CO, particulate matter, and volatile organic compounds (VOCs).2

Exploring new energy resources, such as biodiesel fuel, has been of growing importance in recent years. Biodiesel containing mainly fatty acid methyl esters (FAMEs) is one of such alternative energy resources. It may be obtained via four primary ways: (1) direct use and blending of oils, (2) microemulsions of oil, (3) thermal cracking (pyrolysis of vegetable oil), and (4) transesterification (alcoholysis of oil).3The most commonly used

method is transesterification of vegetable oils, such as soybean, rapeseed, sunflower, palm, coconut, tung, and waste cooking

oils. Oils from algae, bacteria, and fungi also have been investigated.1The transesterification refers to a chemical reaction

involving vegetable oil (containing mainly triglycerides) and an alcohol to form esters and glycerol. A catalyst is usually used to improve the transesterification reaction rate and yield. Glycerol is produced as a byproduct. Alcohols that can be used in the transesterification process include methanol, ethanol, propanol, butanol, and amyl alcohol.3 Methanol is the most

common alcohol employed because of its low cost. Thus, it is the alcohol of choice for the process examined in this study. Transesterification reactions can be alkali-, acid-, or enzyme-catalyzed. If the contents of free fatty acid (FFA) and water in oil are <1 and <0.5 wt %, respectively, then an alkaline catalyst is more suitable for the ester production. If the FFA content of oil is high (>1 wt %), then an acid catalyst is a good choice.4

Alkali-catalyzed transesterification is much faster than acid-catalyzed transesterification, most often used commercially, and employed for the process of this study. Many studies of alkali-catalyzed transesterification on the laboratory scale have been carried out. A reaction temperature near the boiling point of the alcohol and a range from 3:1 to 6:1 of the molar ratio of alcohol/soybean oil were recommended.5,6One limitation to the

alkali-catalyzed process is its sensitivity to the purity of reactants. The process is very sensitive to both water and FFAs. The presence of water may cause saponification of ester under

†Presented at the International Conference on Bioenergy Outlook 2007, Singapore, April 26–27, 2007.

* To whom correspondence should be addressed. Telephone: +886-3-935-3563. Fax: +886-3-+886-3-935-3563. E-mail: jlshie@niu.edu.tw.

‡National Taiwan University. §National I-Lan University. |

Chung Yuan Christian University.

(1) Shay, E. G. Biomass Bioenergy 1993, 4, 227–242.

(2) Klass, L. D. Biomass for Renewable Energy, Fuels and Chemicals; Academic Press: New York, 1998; pp 1–2.

(3) Ma, F. R.; Hanna, M. A. Bioresour. Technol. 1999, 70, 1–15.

(4) Kulkarni, M. G.; Dalai, A. K. Ind. Eng. Chem. Res. 2006, 45, 2901– 2913.

(5) Freedman, B.; Pryde, E. H.; Mounts, T. L. J. Am. Oil Soc. Chem.

1984, 61, 1638–1643.

(6) Noureddini, H.; Zhu, D. J. Am. Oil Soc. Chem. 1997, 74, 1457– 1463.

10.1021/ef700295c CCC: $40.75 2008 American Chemical Society Published on Web 10/02/2007

alkaline conditions.7,8Thus, usages of a dehydrated vegetable

oil with less than 0.5 wt % FFA, an anhydrous alkali catalyst, and an anhydrous alcohol are necessary for commercially viable alkali-catalyzed systems.5,8 This requirement is likely to be a

significant limitation to the use of waste cooking oil as a low-cost feedstock of biodiesel production. Usually, the level of FFA in waste cooking oil is greater than 2 wt %.9,10The products

formed during frying, such as FFA and some polymerized triglycerides, can affect the transesterification reaction and the biodiesel properties. Apart from these phenomena, the biodiesel obtained from waste cooking oil gives better engine performance and less emission when tested on commercial diesel engines.4

The two-step process (acid-catalyzed followed by alkali-catalyzed) is one of the better alternatives for the production of biodiesel from waste cooking oil.9However, a two-step method

is not feasible, because it requires more steps, which make the biodiesel process costly.4 In contrast to the alkali-catalyzed

process, acid-catalyzed transesterification has received less attention because it has a relatively slow reaction rate. Neverthe-less, it is insensitive to FFA in feedstock oil compared to the alkali-catalyzed system. The typical acid catalyst used in the reaction is sulfuric acid.8

A major obstacle in the commercialization of biodiesel, in comparison to petroleum-based diesel fuel, is its high cost of manufacturing, primarily the raw material cost. Biodiesel usually costs over 0.5 U.S. dollars (USD) L-1. Its cost is approximately 1.5 times that of petroleum-based diesel depending upon feedstock oils.11,12Bender13reviewed 12 reports concerning the

economic feasibility of biodiesel production, involving several feedstocks and operational scales. Calculated production costs, which included the costs of the feedstock and its conversion to biodiesel, were 0.3, 0.32–0.37, 0.4, 0.63, and 0.69 USD L-1 for fuel produced from soybean oil,14animal fats,15canola oil,

sunflower oil,14and rapeseed oil,16respectively. According to

Nelson et al.,17 the significant factors that affect the cost of

biodiesel are feedstock cost, plant size, and value of the glycerine byproduct. Waste cooking oil, which is much less expensive than pure vegetable oil, is a promising alternative to vegetable oil for biodiesel production. Restaurant waste oils and rendered animal fats are less expensive than food-grade canola and soybean oils.18The production of biodiesel from waste cooking

oil is one of the better ways to use it efficiently and

economi-cally. Canackci and Gerpen18have developed a 190 L pilot plant

using an acid-catalyzed pretreatment followed by an alkali-catalyzed transesterification. The estimated costs for biodiesel from soybean oil, yellow grease with 9% FFA, and brown grease with 40% FFA were 0.418, 0.317, and 0.241 USD L-1, respectively. Also, from the same economic reason, Haas19has

investigated the production of biodiesel from soapstock (SS), a byproduct of edible oil refining that is substantially less expensive than edible-grade refined oils. An economic analysis model using ASPEN PLUS software suggested that the produc-tion costs of soapstock and soybean oil biodiesel would be approximately 0.41 and 0.53 USD L-1, respectively, a 25% reduction relative to the estimated cost of biodiesel produced from soybean oil. For the production cost of 0.53 USD L-1of biodiesel from soybean oil, the single greatest contributor to this value was the cost of the oil feedstock, which accounted for 88% of the total estimated production cost.20Bender13and

Zhang et al.21showed that the credit for the glycerol byproduct

has a significant impact on the net value of the total manufactur-ing cost. The glycerol value led to a reduction in total production costs of 6 and 6.5% of biodiesel from Ethiopian mustard oil and used olive oil, respectively. Therefore, the use of waste cooking oil should greatly reduce the cost of biodiesel produc-tion because waste oil is available at a relatively low price. However, the data on the requirements of diesel fuel and availability of waste cooking oil for the countries using diesel fuel indicate that the biodiesel obtained from waste cooking oil may not replace diesel fuel completely,4which is also reflected

in Taiwan. Therefore, the Taiwan government plans to enable farmers to grow industrial oilseeds (e.g., sunflower seed, soybean seed, and rapeseed) to develop a share of 1–5% (B1–B5) of the biodiesel market for the fuels of public traffic vehicles, such as buses and garbage trucks.22 Bender13 and Van Dyne et al.23

affirmed that biodiesel could compete with diesel fuel if produced in agricultural cooperatives. According to Bender,13

biodiesel from Ethiopian mustard oil can compete with diesel fuel only if tax exemption is applied, whereas biodiesel from used olive oil could compete.

The promotion of the production and usage of biodiesel in Taiwan is at its initial stage. The first Taiwanese factory producing biodiesel of 3000 tons year–1 from waste cooking

oil was established in the Chiayi county of Taiwan in October 2004; however, the laws, standards of oil, and methods of testing were not standardized. Under the plan of the Nuclear-Free Homeland of Taiwan in 2005, over 700 garbage trucks in 13 counties of Taiwan were on track. It was the first extensive test on the use of biodiesel for diesel vehicles in Taiwan.24In another

study, various processes for producing biodiesel from virgin vegetable oil via alkali-catalyzed transesterification were de-veloped.25A comparison of processes using different sources

of virgin vegetable oils was presented from the point of view

(7) Liu, K. S. J. Am. Oil Soc. Chem. 1994, 71, 1179–1187.

(8) Zhang, Y.; Dubé, M. A.; McLean, D. D.; Kates, M. Bioresour.

Technol. 2003, 89, 1–16.

(9) Lepper, H.; Friesenhagen, L. Process for the production of fatty acid esters of short-chain aliphatic alcohols from fats and/or oils containing free fatty acids. U.S. Patent 4,608,202, 1986.

(10) Watanabe, Y.; Shimada, Y.; Sugihara, A.; Tominaya, Y. J. Am.

Oil Soc. Chem. 2001, 78, 703–707.

(11) Lott, M. Personal communication. QSS Group, Inc., 4500 Forbes Boulevard, Suite 200, Lanham, MD 20706, 2002.

(12) Prokop, T. Personal communication. Imperial Western Products, 14970 Chandler Street, Coachella, CA, 2002.

(13) Bender, M. Bioresour. Technol. 1999, 70, 81–87.

(14) Weber, J. A. The economic feasibility of community-based biodiesel plants. Master’s Thesis, University of Missouri, Columbia, MO, 1993.

(15) Nelson, R. G.; Schrock, M. D. Energetic and economic feasibility associated with the production, processing and conversion of beef tallow to diesel fuel. Proceedings of the First Biomass Conference of the Americas: Energy, Environment, Agriculture, and Industry, National Renewable Energy Laboratory (NREL), Golden, CO, 1993; Vol. 2, pp 848–862.

(16) Noordam, M.; Withers, R. V. Producing biodiesel from canola in the inland northwest: An economic feasibility study. Idaho Agricultural Experiment Station Bulletin Number 785, University of Idaho College of Agriculture, Moscow, ID, 1996; p 12.

(17) Nelson, R. G.; Hower, S. A.; Weber J. A. Potential feedstock supply and costs for biodiesel production. Bioenergy 1994, Proceedings of the Sixth National Bioenergy Conference, Reno/Sparks, NV, 1994.

(18) Canackci, M.; Gerpen, J. V. Trans. ASAE 2003, 46, 945–954.

(19) Haas, M. J. Fuel Process. Technol. 2005, 86, 1087–1096.

(20) Haas, M. J.; McAloon, A. J.; Yee, W. C.; Foglia, T. A. Bioresour.

Technol. 2006, 97, 671–678.

(21) Zhang, Y.; Dubé, M. A.; McLean, D. D.; Kates, M. Bioresour.

Technol. 2003, 90, 229–240.

(22) Bureau of Energy, Ministry of Economy Affairs of Taiwan (BOET). http://www.moeaec.gov.tw (accessed 2007).

(23) Van Dyne, D. L.; Weber, J. A.; Braschler, C. H. Bioresour. Technol.

1996, 56, 1–6.

(24) Chuang, G. L. A study on the influences of biodiesel in use for diesel vehicle on engine performance and characteristics of exhaust in Taiwan. Master Thesis, Graduate Institute of Environmental Engineering, National Taiwan University, Taiwan, 2007.

(25) Huang, S. H. A study on the production processes and costs of biodiesel. Master Thesis, Graduate Institute of Environmental Engineering, National Taiwan University, Taiwan, 2007.

of their processing technology. Besides the evaluation of the technology and product yield, economic feasibility is also of great importance in assessing the process viability. Thus, the main objective of the present paper is to propose a simple economic assessment method assisting the comparison of alternative production routes revealing which route can achieve a very desirable reduction in production costs. In this way, a better evaluation of the biodiesel production processes, including feedstock, chemical process, and plant capacity and design, can be achieved from both the technological and economic points of view.

Methodology

Economic Studies. Economic consideration is a key driving force

supporting the development of inexpensive feedstock and process technology for biodiesel production. Although total costs of biodiesel production depend heavily upon feedstock costs, there are some other considerations that must be taken into account. The main economic criteria noted in all of the cases cited above were the total capital investment cost (TCC), total manufacturing cost (TMC), and biodiesel break-even price (BBP). Different researchers used different economic criteria emphasizing different points of view to assess the biodiesel production processes. In the present paper, the economic criteria were based on TCC [including the fixed capital cost (FCC) and working capital cost (WCC)], TMC, after-tax rate of return (ARR), and BBP for biodiesel production. The total production cost (TPC) includes the direct operation cost (DOC), indirect operation cost (IOC), general expense (GE), and depreciation (DEPC). Therefore, TMC is equal to TPC minus the credits of byproducts of glycerine (CBP).

Reaction Process Studies. The way that biodiesel production

was examined in this study was via transesterification, which refers to a catalyzed chemical reaction involving vegetable oil (triglyc-erides) and an anhydrous alcohol to form FAME (biodiesel) and glycerol. The alkali catalyst used in this study was NaOH, and the virgin vegetable oil was soybean oil. The technology processes for producing biodiesel from various virgin vegetable oils by alkali-catalyzed transesterification were developed and discussed in

another study.25However, for the need of economic analysis, the

yields of products from different production steps of biodiesel are listed in Table 1. The yields of crude biodiesel, refined biodiesel, and glycerol via transesterification were 92.5, 62.5, and 27.5 wt %, respectively. The production process of biodiesel includes FAME distillation; therefore, the summation of products should not be 100 wt %. The results indicate the necessity of refining FAME and yielding glycerol of high price and FAME of high quality. The yield of biodiesel used in the cost analysis of this study was 62.5% of refined biodiesel. Table 2 shows the elemental analyses of virgin soybean oil, glycerol, and crude FAME, indicating that the major elemental contents of these materials are C, H, and O. The increase of the oxygen content in crude FAME can assist its combustion efficiency.

Results and Discussion

Zhang et al.8,21designed and simulated four different

continu-ous processes for biodiesel production from virgin oil or waste cooking oil using alkaline or acidic catalysts via a designed tool of HYSYS for the simulation of the flow rates and the chemicals involved. This study used the alkali-catalyzed process, economic assessment factors, and simulated model, which are similar to the previous studies,13,16,17,21 while employing the data of

experiments using local vegetable oil conducted by Huang25for

the cost evaluation. The basis, scope of calculations, and the factors of economic assessment are briefly described as follows.

1. Basis and Scope of Calculations. The cost evaluations

of this study were based on the following assumptions: (1) The Table 1. Yields of Products from Different Production Steps of

Biodiesel25

soybean oil (from Taiwan Sugar Corporation) (wt %) materials virgin soybean oil 100

NaOH solution 11

methanol 10

acetic acid 1.4

water 10

middle product crude FAME 92.5 final products glycerol 27.5 refined FAME 62.5

char 18.3

others 11.8

Table 2. Elemental Analyses of Virgin Soybean Oil, Glycerine, and Crude FAMEa

virgin

soybean oil glycerine

crude FAME C (wt %) 77.56 52.77 74.25 (0.177) (1.703) (3.87) H (wt %) 13.22 11.08 12.51 (0.057) (0.051) (0.559) N (wt %) 0.025 <0.0001 0.0005 (0.007) (<0.0001) (0.0003) S (wt %) <0.0001 <0.0001 (<0.0001) (<0.0001) balance, O (wt %) 9.2 36.15 13.2395

aNumbers in parentheses are standard deviations.

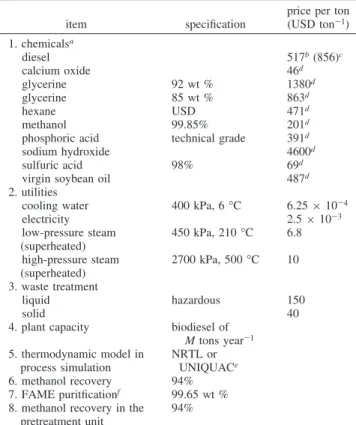

Table 3. Basic Conditions for the Economic Assessment of the Process of This Study

item specification

price per ton (USD ton-1) 1. chemicalsa diesel 517b(856)c calcium oxide 46d glycerine 92 wt % 1380d glycerine 85 wt % 863d hexane USD 471d methanol 99.85% 201d

phosphoric acid technical grade 391d

sodium hydroxide 4600d

sulfuric acid 98% 69d

virgin soybean oil 487d

2. utilities

cooling water 400 kPa, 6°C 6.25× 10-4 electricity 2.5× 10-3 low-pressure steam (superheated) 450 kPa, 210°C 6.8 high-pressure steam (superheated) 2700 kPa, 500°C 10 3. waste treatment liquid hazardous 150 solid 40

4. plant capacity biodiesel of

M tons year-1 5. thermodynamic model in process simulation NRTL or UNIQUACe 6. methanol recovery 94% 7. FAME puritficationf 99.65 wt %

8. methanol recovery in the pretreatment unit

94%

aUnless specified, all prices are in USD ton-1. Prices of chemicals are from the National Biodiesel Board (2000), http://www.biodiesel.org, Chemical Market Reporter (2000–2001), Vol. 258 (22) and Vol. 259 (9), and http://www.chemconnect.com, November 2000. Prices are based on the constant price in 2003.bDiesel price in Taiwan ) 15.12 NTD L-1 (2003) and 1 USD ) 34.41 NTD (2003). cDiesel price in Taiwan )

23.48 NTD L-1(July 2007) and 1 USD ) 32.78 NTD (July 2007).

dIncludes a 15% price increase with the shipping of materials from

U.S.A. to Taiwan (2003).eNRTL, nonrandom two liquid; UNIQUAC,

plant capacity of biodiesel production was assumed as M tons year-1. For the requirement of biodiesel in Taiwan, M can be simulated as 8000, 30 000, and 100 000 tons year-1. The 8000 tons year-1 plant capacity is consistent with the plant size discussed by Zhang et al.8,21(2) Operating hours were assumed

to be T h year-1(in general, T ) 8000 h year-1).21(3) Virgin

soybean oil, used as the feedstock for biodiesel production, was free of water and any solid impurities. (4) In the simulation, pump efficiency was assumed to be 70% and no spare pumps were taken into account. (5) The specifications and prices of superheated, low- and high-pressure steams and water are as listed in Table 3. (6) All chemical costs including raw materials, catalysts, solvent, and products are as given in Table 3. Further, all of the prices of raw materials, chemicals, catalysts, and solvent included the transportation fee from U.S.A. to Taiwan, insurance, and tax, being assumed as 15% of the costs purchased in U.S.A. (7) The chemical engineering plant index26was used

as the price index.

2. Factors of Economic Assessment. Six major economic

cost factors were computed and examined in this study. These include FCC, TCC, TMC, net annual profit after taxes (NNP), ARR, and BBP.

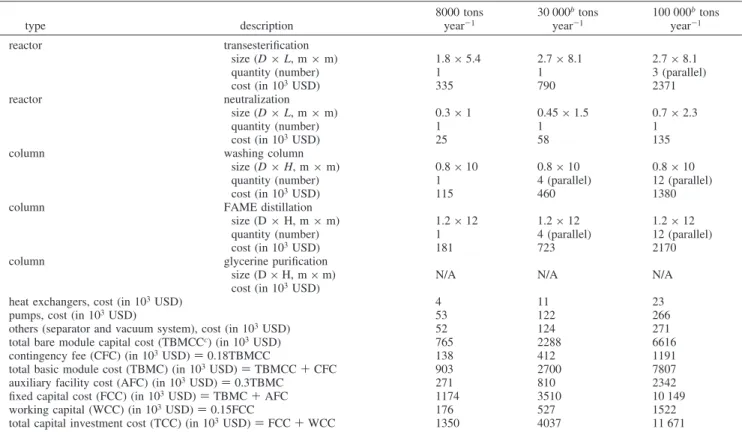

2.1. Fixed Capital Cost (FCC). FCC represents the cost of

constructing a new plant (also called grassroots capital cost). Generally, FCC consists of three parts. The first part is the total bare module capital cost (TBMCC), which is the sum of the cost of each piece of equipment in the process. Part 2 consists of contingencies and fees (CFC), which are usually estimated as a certain percentage of the TBMCC (e.g., 18% as used in the present study).21,27,28Part 3 is associated with the costs of

auxiliary facilities (AFC), including items such as the purchase

of land, installation of electrical and water systems, and construction of all internal roads. AFC is usually represented as 30% of the total basic module cost (TBMC)27,28where

CFC ) 0.18TBMCC (1) AFC ) 0.3TBMC (2) TBMC ) TBMCC + CFC (3) Therefore, FCC ) TBMCC + CFC + AFC ) TBMC + AFC ) 1.3TBMC ) 1.3(TBMCC + CFC) ) 1.3(TBMCC + 0.18TBMCC) (4) The computed results are listed in Table 4.

2.2. Total Capital InVestment Cost (TCC). TCC is calculated

by adding WCC to the FCC. WCC is usually estimated as a certain percentage of the FCC (e.g., 15% as used in this study).21,27Therefore,

TCC ) WCC + FCC ) 1.15FCC (5) FCC and TCC for the three plants with different capacities studied in this work are presented in Table 4.

2.3. Total Manufacturing Cost (TMC). TMC refers to TPC

subtracting CBP (i.e., TMC ) TPC – CBP). Therefore, TPC can be calculated as the total operating cost (TOC) adding DEPC (i.e., TPC ) TOC + DEPC). TOC is the cost of the day-to-day operation of a plant and is usually divided into three categories: DOC, IOC [or fixed operating cost (FOC)], and GE.27,28 DOC consists of raw material costs (soybean

(26) Chemical Engineering (CE). Chemical Engineering Economic

Indicators, 2001; Vol. 108 (issue 7), p 138.

(27) Ulrich, G. D. A Guide to Chemical Engineering Process Design

and Economics; John Wiley and Sons: New York, 1984; Chapters 5 and 6.

(28) Turton, R.; Bailie, R. C.; Whiting, W. B.; Shaeiwitz, J. A. Analysis,

Synthesis, and Design of Chemical Processes; Prentice Hall PTR: Upper

Saddle River, NJ, 1998; Chapters 1–3.

Table 4. Equipment Sizes, Equipment Costs, and FCCs for the Processes of This Studya

type description 8000 tons year-1 30 000btons year-1 100 000btons year-1 reactor transesterification size (D× L, m × m) 1.8× 5.4 2.7× 8.1 2.7× 8.1 quantity (number) 1 1 3 (parallel)

cost (in 103USD) 335 790 2371

reactor neutralization

size (D× L, m × m) 0.3× 1 0.45× 1.5 0.7× 2.3

quantity (number) 1 1 1

cost (in 103USD) 25 58 135

column washing column

size (D× H, m × m) 0.8× 10 0.8× 10 0.8× 10 quantity (number) 1 4 (parallel) 12 (parallel)

cost (in 103USD) 115 460 1380

column FAME distillation

size (D× H, m × m) 1.2× 12 1.2× 12 1.2× 12 quantity (number) 1 4 (parallel) 12 (parallel)

cost (in 103USD) 181 723 2170

column glycerine purification

size (D× H, m × m) N/A N/A N/A

cost (in 103USD)

heat exchangers, cost (in 103USD) 4 11 23

pumps, cost (in 103USD) 53 122 266

others (separator and vacuum system), cost (in 103USD) 52 124 271 total bare module capital cost (TBMCCc) (in 103USD) 765 2288 6616 contingency fee (CFC) (in 103USD) ) 0.18TBMCC 138 412 1191 total basic module cost (TBMC) (in 103USD) ) TBMCC + CFC 903 2700 7807 auxiliary facility cost (AFC) (in 103USD) ) 0.3TBMC 271 810 2342 fixed capital cost (FCC) (in 103USD) ) TBMC + AFC 1174 3510 10 149 working capital (WCC) (in 103USD) ) 0.15FCC 176 527 1522 total capital investment cost (TCC) (in 103USD) ) FCC + WCC 1350 4037 11 671

aIncludes a 15% price increase with the shipping of equipment from U.S.A. to Taiwan. Prices are based on the constant price in 2003.bConversion

equation of capacity: costB) costA(capacityB/capacityA)nc) costA(sizeB/sizeA)ns; nc and ns ) 0.65.cTBMCC is the sum of the cost of each piece of

equipment in the process.

oil price of U.S.A.), catalyst and solvent costs, operating labor fees, supervisory and clerical labor fees, utilities (including waste disposal), maintenance and repairs, operating supplies, laboratory charges, and expenses for patents and royalties. In brief, all charges related to materials and labors belong to this category21and are listed in Tables 3 and 5. The operating

labor fee was obtained from operation requirements for various pieces of process equipment.28Turton et al.28assumed

that an operator worked on average 49 week year-1and that there were three shifts a day for a continuously running plant. The computation of Zhang et al.21gave an operator’s fee of

24 USD h-1and total operating labor fee of 141 120 USD year-1 for three labors a day (one shift for one labor).

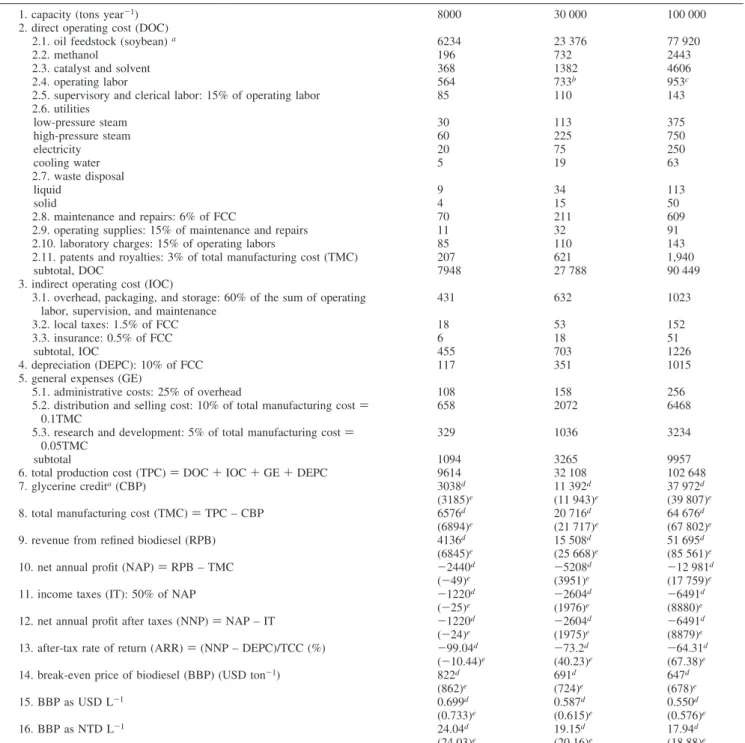

Considering the difference of labor fee between U.S.A. and Taiwan, we assumed an operator fee of 12 USD h-1and total operating labor fee of 564 480 USD year-1for 24 labors a Table 5. Total Manufacturing and Operating Costs and After-Tax Rate of Return for the Processes of This Study (in 103USD)

1. capacity (tons year-1) 8000 30 000 100 000

2. direct operating cost (DOC)

2.1. oil feedstock (soybean)a 6234 23 376 77 920

2.2. methanol 196 732 2443

2.3. catalyst and solvent 368 1382 4606

2.4. operating labor 564 733b 953c

2.5. supervisory and clerical labor: 15% of operating labor 85 110 143 2.6. utilities low-pressure steam 30 113 375 high-pressure steam 60 225 750 electricity 20 75 250 cooling water 5 19 63 2.7. waste disposal liquid 9 34 113 solid 4 15 50

2.8. maintenance and repairs: 6% of FCC 70 211 609 2.9. operating supplies: 15% of maintenance and repairs 11 32 91 2.10. laboratory charges: 15% of operating labors 85 110 143 2.11. patents and royalties: 3% of total manufacturing cost (TMC) 207 621 1,940

subtotal, DOC 7948 27 788 90 449

3. indirect operating cost (IOC)

3.1. overhead, packaging, and storage: 60% of the sum of operating labor, supervision, and maintenance

431 632 1023

3.2. local taxes: 1.5% of FCC 18 53 152

3.3. insurance: 0.5% of FCC 6 18 51

subtotal, IOC 455 703 1226

4. depreciation (DEPC): 10% of FCC 117 351 1015

5. general expenses (GE)

5.1. administrative costs: 25% of overhead 108 158 256 5.2. distribution and selling cost: 10% of total manufacturing cost )

0.1TMC

658 2072 6468

5.3. research and development: 5% of total manufacturing cost ) 0.05TMC

329 1036 3234

subtotal 1094 3265 9957

6. total production cost (TPC) ) DOC + IOC + GE + DEPC 9614 32 108 102 648 7. glycerine credita(CBP) 3038d 11 392d 37 972d

(3185)e (11 943)e (39 807)e

8. total manufacturing cost (TMC) ) TPC – CBP 6576d 20 716d 64 676d

(6894)e (21 717)e (67 802)e

9. revenue from refined biodiesel (RPB) 4136d 15 508d 51 695d

(6845)e (25 668)e (85 561)e

10. net annual profit (NAP) ) RPB – TMC -2440d -5208d -12 981d

(-49)e (3951)e (17 759)e

11. income taxes (IT): 50% of NAP -1220d -2604d -6491d

(-25)e (1976)e (8880)e

12. net annual profit after taxes (NNP) ) NAP – IT -1220d -2604d -6491d

(-24)e (1975)e (8879)e

13. after-tax rate of return (ARR) ) (NNP – DEPC)/TCC (%) -99.04d -73.2d -64.31d

(-10.44)e (40.23)e (67.38)e

14. break-even price of biodiesel (BBP) (USD ton-1) 822d 691d 647d

(862)e (724)e (678)e

15. BBP as USD L-1 0.699d 0.587d 0.550d

(0.733)e (0.615)e (0.576)e

16. BBP as NTD L-1 24.04d 19.15d 17.94d

(24.03)e (20.16)e (18.88)e aYields of refined biodiesel and glycerine (85 wt % purity of glycerine) relative to input soybean oil are 62.5 and 27.5 wt % in this study,

respectively.bOperating labor cost of 30 000 tons year-1is 1.3 times of that of 8000 tons year-1.17,21 cOperating labor cost of 100 000 tons year-1is 1.3 times of that of 30 000 tons year-1.17,21 dPrice in 2003 [diesel price in Taiwan ) 15.12 NTD L-1(2003), 1 USD ) 34.41 NTD (2003), and 1 L ) 0.85 kg (biodiesel)].ePrice in July 2007 [diesel price in Taiwan ) 23.48 NTD L-1(July 2007) and 1 USD ) 32.78 NTD (July 2007)]. Consumer price index (CPI) equation of cost: cost(July 2007)) cost2003(CPI(July 2007)/CPI2003), where CPI2003) 99.52 and CPI(July 2007)) 104.33 (in Taiwan).

Table 6. Fraction of Total Production Cost, Cost of Oil Feedstock (Virgin Soybean Oil), and Glycerine Credit for the

Processes of This Study (in Percentages)a

capacity (tons year-1) 8000 30 000 100 000 total production cost 100 100 100 glycerine credit 31.6 35.5 37.0 cost of oil feedstock (virgin soybean oil) 64.8 72.8 75.9

aYields of refined biodiesel and glycerine (85 wt % purity of

glycerine) relative to input virgin soybean oil are 62.5 and 27.5 wt % in this study, respectively.

Table 7. Economic Evaluations for Biodiesel Production Plants or Processes from the References and This Study Nelson et al. Noordam and Withers Bender Zhang et al. this work this work this work plant capacity a(tons year -1) 100 000 7800 10 560 8000 8000 30 000 100 000 process type alkali-catalyzed continuous process alkali-catalyzed batch process alkali-catalyzed continuous process process I: alkali-catalyzed process using virgin vegetable oil process II: alkali-catalyzed process using waste cooking oil process III: acid-catalyzed process using waste cooking oil process IV: acid-catalyzed process using hexane extraction alkali-catalyzed continuous process alkali-catalyzed continuous process alkali-catalyzed continuous process raw material beef tallow canola oil animal fats virgin vegetable oil and waste cooking oil soybean oil soybean oil soybean oil FCC (in 10 6USD) not reported not reported not reported process I: 1.17 process II: 2.33 process III: 2.21 process IV: 2.77 1.17 3.51 10.15 TCC (in 10 6USD) 12 not reported 3.12 process I: 1.34 process II: 2.68 process III: 2.55 process IV: 3.19 1.35 4.04 11.67 TMC (in 10 6USD year -1) 34 5.95 not reported process I: 6.86 process II: 7.08 process III: 5.15 process IV: 5.62 6.89 21.72 67.8 NNP (in 10 6USD) not reported not reported not reported process I: –1.03 process II: –1.14 process III: –0.18 process IV: –0.41 -0.024 1.975 8.879 ARR (in %) not reported not reported not reported process I: –85.27 process II: –51.18 process III: –15.63 process IV: –21.48 -10.44 40.23 67.38 BBP (in USD ton -1) 340 763 420 process I: 857 process II: 884 process III: 644 process IV: 702 862 724 678 glycerine credit (in 10 6USD) 6 0.9 1.2 for technical-grade glycerine process I: 0.73 process II: 0.68 process III: 0.77 process IV: 0.73 3.19 11.94 39.81 aIn terms of biodiesel production.

day for three shits (one shift for eight labors) in this work. Other expenses, such as supervisory and clerical labor fees, maintenance and repair expenses, and operating supplies charges were calculated individually and multiplied by related factors,21,28 as shown in Table 5. IOC includes overhead,

packaging, storage, local taxes, insurance, and depreciation. All of the items in this category are independent of the production rate in a plant.21,27,28 The last category, GE,

includes administrative costs, distribution and selling costs, and research and development charges.21,27,28The above items

are also obtained via multiplication with various constant factors as shown in Table 5.

2.4. Net Annual Profit after Taxes (NNP) and After-Tax Rate of Return (ARR). ARR is a general economic performance

criterion for the preliminary evaluation of a plant and is defined as the ratio of NNP relative to the TCC. NNP is equal to the net annual profit (NAP) subtracting income taxes (IT) (i.e., NNP ) NAP - IT).21,27 ARR was also chosen as the response

variable and objective function in the economic assessment of this study. The results are shown in Table 5.

2.5. Biodiesel Break-EVen Price (BBP). >BBP is the price

of biodiesel when the revenue from biodiesel product (RPB) is equal to TMC of a plant. The values of BBP are expressed as USD and New Taiwan dollars (NTD) in this study and are shown in Table 5 for biodiesel plants with different capacities.

Factors for Economic Assessment. The economic costs of

three biodiesel plants with capacities of 8000, 30 000, and 100 000 tons year-1were computed as presented in Tables 4 and 5. The fractions of total production cost, cost of oil feedstock (virgin soybean oil), and glycerine credit are listed in Table 6. From Table 6, the fractions of the cost of oil feedstock and glycerine credit increase with the increase of the capacity of the biodiesel plant. The total production cost decreases with the increase of the glycerine credit and the decrease of the cost of the oil feedstock. A comparison of the results of factors for economic assessment obtained in the literature and this work is given in Table 7. In this study, the plants employ continuous processes using an alkali catalyst and the raw material of soybean oil. Six major economic cost factors were examined and compared. These include FCC, TCC, TMC, NNP, ARR, and BBP. The values of NNP and ARR (Table 5) of plants with capacities of 8000, 30 000, and 100 000 tons year-1 are -24 × 103, 1975 ×

103, and 8879× 103USD and -10.44, 40.23, and 67.38%,

respectively. Therefore, both NNP and ARR turn from negative to positive when the plant capacity increases. The values of BBP of the three plants are 862, 724, and 678 USD ton-1or 0.733, 0.615, and 0.576 USD L-1, respectively (price in July 2007). From Table 5, NNP and ARR of 2003 are all negative values because the biodiesel price in 2003 (Taiwan) is so low (15.12 NTD L-1). However, with the increase of the price of diesel from 2003 (15.12 NTD L-1) to July 2007 (23.48 NTD L-1) in Taiwan, NNP and ARR increase and turn from negative to positive. The plant with a capacity of 100 000 tons year-1in this study is economically feasible, providing a higher NNP and more attractive ARR with a lower BBP. Zhang et al.21proposed four different continuous

processes for biodiesel production from virgin oil or waste vegetable oil using alkaline or acidic conditions. The values of BBP of these four processes are 857, 884, 644, and 702 USD ton-1as listed in Table 7. Therefore, the third process of the acid-catalyzed process using waste cooking oil was more economically feasible, giving lower TMC and BBP with

a more attractive ARR. As shown in Table 7, the value of BBP of the plant with a capacity of 100 000 tons year-1of this study (647 USD ton-1) is close to that of the acid-catalyzed process using waste cooking oil proposed by Zhang et al.21(678 USD ton-1). It implies that the increase in the

plant capacity with soybean oil has the same economic feasibility as using waste cooking oil as feedstock. Nelson et al.17 also evaluated the economic feasibility of a plant

producing approximately 100 000 tons year-1of biodiesel. The feedstock of beef tallow was transesterified with methanol in the presence of an alkali catalyst, yielding a low BBP of 340 USD ton-1(Table 7). However, the beef tallow is not easily available in any country. Thus, from the point of view of easy feedstock, a plant with a reasonably large capacity with an alkali-catalyzed continuous process is eco-nomically feasible, as illustrated in this study using soybean oil as feedstock. The proposed process of this work having a large plant capacity has the same economic potential as that using the low-cost feedstock of waste cooking oil.

Conclusions

Among the system variables of the plant examined, plant capacity, price of feedstock oil, and yields of glycerine and biodiesel were found to be the most significant variables affecting the economic viability of biodiesel manufacture. A plant with capacity of 100 000 tons year-1 assessed in this study is economically feasible, yielding higher NNP and ARR with a lower BBP. Increasing the plant capacity using a feedstock of soybean oil has the same economic feasibility as employing waste cooking oil as feedstock. In summary, this study aims at the need to obtain useful information for the cost analysis and assessment of the production process of biodiesel using soybean oil. The results provide an appropriate indication for the promotion of biodiesel production in the future, targeting the reduction of the cost of feedstock oil with the increase of the yields of valuable products with a reasonably large plant capacity.

Acknowledgment. The authors acknowledge the support from

the Council of Agriculture of Taiwan.

Nomenclature DEPC ) Depreciation

AFC ) Costs associated with auxiliary facilities ARR ) After-tax rate of return

BBP ) Biodiesel break-even price CBP ) Credits of byproducts of glycerine CFC ) Contingencies and fees

DOC ) Direct operation cost FAME ) Fatty acid methyl ester FCC ) Fixed capital cost FFA ) Free fatty acid FOC ) Fixed operating cost GE ) General expense GHG ) Greenhouse gas IOC ) Indirect operation cost IT ) Income taxes

M ) Plant capacity in term of biodiesel production NAP ) Net annual profit

NNP ) Net annual profit after taxes

TBMC ) Total basic module cost TBMCC ) Total bare module capital cost TCC ) Total capital investment cost TMC ) Total manufacturing cost TOC ) Total operating cost

TPC ) Total production cost VOC ) Volatile organic compound WCC ) Working capital cost

EF700295C