- 1 -

Positive or Negative Signal? Empirical Study of the Signal Effect of Director & Officer Insurance and Moral Hazard in Taiwan

Chun-Yuan Chen*

Abstract

The release of economically relevant information is important for the evaluation of firms’ outstanding securities and the ability to attract investment in the future. Some literature claim that Director & Officer (D&O) insurance has a positive effect on firms’ value but others disagree. In order to enhance corporate governance, some countries mandate D&O insurance as compulsory for corporations. Taiwan has developed D&O insurance in recent years. This paper intends to test whether D&O insurance brings positive or negative signal in Taiwan.

Two major empirical works were used to conduct to clarify this issue. First, the model proposed by Ohlson (1995) concerning evaluating value of firms was applied test the effect of D&O insurance. After the initial test of regression, further regression analyses with interaction terms were carried out to test how the relationship between market value of firms and corporate governance were affected by D&O insurance. Second, this paper analyzes moral hazard and opportunistic behavior caused by D&O insurance. It was found that the signal effect of D&O insurance in Taiwan is sustained and not affected by opportunistic behavior and moral hazard. In conclusion, implications and recommendations about the revision of relevant regulations were also provided.

Keywords: D&O insurance, corporate governance, monitoring hypothesis, signal hypothesis, Ohlson model, opportunistic behavior, moral hazard

* J.S.D. Candidate, University of Illinois at Urbana-Champaign. Ph.D. Candidate, China University of Political Science and Law, China. Ph.D. in Law, National ChengChi University, Taiwan.

- 2 -

1. Introduction

The release of economically relevant information is important for the evaluation of firms’ outstanding securities and the ability to attract investment in the future.1 According to the reasoning of signal hypothesis, the purchase of D&O insurance will release signal to investors and investors will evaluate the purchase of D&O insurance positively. Thus, D&O insurance purchase should have positive effect on firms’ stock price. However, with the protection of insurance, directors might have more opportunistic behavior or moral hazard.2 Then the purchase of D&O insurance will no longer emit positive signal. In contrast, investors will worry about D&O insurance because the insurance may encourage risky behavior. Therefore the signal effect of D&O insurance is disputable.

In order to clarify this issue, two major empirical works will be conducted in this paper. In the first part, this paper uses the famous model proposed by Ohlson (1995) concerning evaluating value of firms to test the effect of D&O insurance. If there is positive relationship between D&O insurance and stock price, the positive effect of D&O insurance is implied. In contrast, inverse association between D&O insurance and stock price implies D&O insurance emits negative signal to the market. In the second part, this paper will analyze moral hazard and opportunistic behavior raised from D&O insurance. If the answer is positive, then as concerned by literatures, D&O insurance would induce moral hazard and opportunistic behavior and thus convey negative signal to the market.

2. Literature review

2.1 Corporate governance and market value of firms

Albeit the discussion of corporate governance is sprouting, it should be wondered that firm’s corporate governance behavior indeed increase their market value? However, in the United States, many empirical works cannot provide strong evidence for the relationship between corporate governance behavior and increase of market value.3 Similar problems are also addressed in emerging market. Bernard S. Black, Hasung Jang and Woochan Kim test the relationship between corporate governance and

1

See Robert M. Lawless, Stephen P. Ferris, and Bryan Bacon, The Influence of Legal Liability on Corporate Financial Signaling, 23 J. Corp. L. 209 (1998).

2

See Chen Lin, Micah S. Office and Hong Zou, Hong, Directors’ and Officers’ Liability Insurance and Acquisition Outcomes, pp. 27 (July 18, 2010). Journal of Financial Economics (JFE), Forthcoming. Available at SSRN: http://ssrn.com/abstract=1641645, last visited on Feb. 15, 2012.

3

See Bernard S. Black, Does Corporate Governance Matter? A Crude Test Using Russian Data, 149 U. Pa. L. Rev. 2131, 2131 (2001). Different argument like corporate governance can increase Apple’s market value, see In re Apple Computer, Inc. Derivative Litig., No. C 06-4128 JF (HRL), 2008 WL 4820784, at 2 (N.D. Cal. Nov. 5, 2008)

- 3 -

market value of firms in Korea by OLS regression and instrument variables.4 They find that corporate governance is an important but maybe casual factor of market value of firms.5 Bernard S. Black also carries out empirical analysis in Russian.6 He concludes that firm’s corporate governance will affect their market value significantly if countries’ constraints on corporate governance are limited.7

However, different argument advocates corporate governance would substantially affect market value and shareholders.8 Lawrence D. Brown and Marcus L. Caylor test the association between firms’ performance and Gov-Score, which is composed by 51 corporate governance factors. They find firms with better governance indeed have better profit, more value and more benefit for shareholders.9 Lucian A. Bebchuk, Alma Cohen and Allen Ferrell test the association between market value and corporate governance arrangements which are based on six provisions: staggered boards, limits to shareholder bylaw amendments, poison pills, golden parachutes, and supermajority requirements for mergers and charter amendments. They find the index of such arrangements is inversely associated with market value.10 Literatures also proposes that market value of firms would be affected their corporate governance in Russia.11

2.2 D&O insurance, signal effect and market value of firms 2.2.1 Positive effect

Some literature proposes the positive effect of D&O insurance on firm’s performance and market value. Sanjai Bhagat, James A. Brickley and Jeffrey L. Coles find that D&O insurance has positive on shareholder wealth and no negative effect is found.12 Jinyoung Park also finds the D&O insurance can positively contribute shareholder’s wealth.13 He tests the association between D&O insurance coverage and the quality

4

See Bernard S. Black, Hasung Jang and Woochan Kim, Does Corporate Governance Predict Firms' Market Values? Evidence from Korea, 22 J.L. Econ. & Org. 366, 366 (2006).

5 Id. 6

See Bernard S. Black, Does Corporate Governance Matter? A Crude Test Using Russian Data, 149 U. Pa. L. Rev. 2131, 2131 (2001).

7 Id. 8

See Lucian A. Bebchuk, Alma Cohen and Allen Ferrell, What Matters in Corporate Governance? pp. 1 (September 1, 2004). Review of Financial Studies, Vol. 22, No. 2, pp. 783-827, February 2009; Harvard Law School John M. Olin Center Discussion Paper No. 491 (2004). Available at SSRN: http://ssrn.com/abstract=593423 or doi:10.2139/ssrn.593423, last visited on Feb. 15, 2012. 9

See Lawrence D. Brown and Marcus L. Caylor, Corporate Governance and Firm Performance, pp. 1 (December 7, 2004). Available at SSRN: http://ssrn.com/abstract=586423 or doi:10.2139/ssrn.586423, last visited on Feb. 15, 2012.

10

Id, at 39. 11

5 L of Intl Trade § 151:3. 12

See Sanjai Bhagat, James A. Brickley, Jeffrey L. Coles, Managerial Indemnification and Liability Insurance: The Effect on Shareholder Wealth, 54.4 The Journal of Risk and Insurance 721, 733 (1987). 13

- 4 -

of firms’ voluntary disclosure.14 He finds that there is an association between insurance coverage and forecast frequency and precision.15 The more insurance coverage, the more disclosure occurs. There is also more precise and timely.16 Besides, positive response from market is given to such information.17 All these results imply the positive signal effect of D&O insurance.

2.2.2 Negative effect

It is controversy that whether D&O insurance increase firm performance and shareholder’s wealth. The negative viewpoint mainly bases on the problem and risk that might be induced by D&O insurance. If D&O insurance represents the potential risk, opportunistic behavior and moral hazard, firms would avoid purchasing D&O insurance to damage the reputation and value of firms.

Irene Y. Kim tests Canadian market and confirms the hypothesis that opportunism in financial reporting can be predicted by excess D&O insurance coverage.18 Besides, litigation risk, corporate governance quality, high-tech industry, and leverage are inversely related to D&O insurance coverage.19 In consequence, opportunistic behavior is implied. Narjess Boubakri and Nabil Ghalleb again test Canadian market and have more negative conclusion. D&O insurance indeed induces opportunistic behavior and has negative impact on firms’ performance in the future.20 Besides, their findings show that insurer cannot distinguish opportunistic risk and mandatory reporting is not so helpful.21 Under such circumstance where asymmetric information and moral hazard are obvious, regulation and limitation are recommended.22

Chen Lin, Micah S. Officer, Rui Wang and Hong Zou test Canada D&O insurance market and find that there is an association between D&O insurance coverage and higher as-issue bond yields, higher loan spreads, and higher risk taking. This result

on Voluntary Disclosure: Evidence from Canadian Firms, University of Michigan working paper, pp. 30, Available at http://som.umflint.edu/research/docs/20052006/200506_JP_I.pdf, last visited on Feb. 15, 2012. 14 Id. at 3. 15 Id, at 4. 16 Id. 17 Id. 18

See Irene Y. Kim, Directors’ and Officers’ Insurance and Opportunism in Accounting Choice, Duke University working paper, pp. 21 (2005). Available at

http://www.efmaefm.org/efma2006/papers/764024_full.pdf, last visited on Feb. 15, 2012. 19

Id. 20

See Narjess Boubakri and Nabil Ghalleb, Does Mandatory Disclosure of Directors’ and Officers’ Liability Insurance Curb Managerial Opportunism? Evidence from the Canadian Secondary Market, Ninth Annual Asian Academic Accounting Association Conference Program, pp. 29-30 (November 29, 2008). Available at

http://69.175.2.130/~finman/Reno/Papers/Does_Mandatory_Disclosure_Curb_Managerial_Opportunis m.pdf, last visited on Feb. 15, 2012.

21

Id, at 30. 22

- 5 -

demonstrates that debt holder percepts that higher D&O insurance coverage implies higher risk.23 The concerns about moral hazard and asymmetric information are also implied. Chen Lin, Micah S. Office and Hong Zou again test the association between D&O insurance and acquirer cumulative abnormal announcement returns (CARs). They find there is an inverse association. This means acquirers with higher D&O insurance coverage have less acquisition synergies and pay more premiums.24 This implies D&O insurance might induce moral hazard.25

John M. R. Chalmers, Larry Y. Dann, Jarrad Harford find there is an inverse association between D&O insurance coverage and the performance of 3-year stock price.26 And managers who have high D&O insurance coverage have poor performance in the future.27 Narjess Boubakri, Martin Boyer, and Nabil Ghalleb further confirm this result. They find managers purchase D&O insurance for opportunistic earnings, and insurers would charge more premiums for those who have higher opportunistic risk.28 By testing Canadian market, Boyer finds that there is a moral hazard problem for managers because D&O insurance reduces their ability to increase cash flow.29 Peter Egger, Doina Radulescu, and Ray Rees find that if senior executives have some incentives to make short run gains, they must be insured to prevent the adverse consequences.30

Generally speaking, majority of previous literatures support the hypothesis that D&O insurance might induce moral hazard or opportunistic behavior. If this conclusion is

23

See Chen Lin, Micah S. Officer, Rui Wang and Hong Zou, Directors’ and Officers’ Liability Insurance and the Cost of Debt, pp. 20-1 (June 16, 2011). Available at SSRN:

http://ssrn.com/abstract=1865679, last visited on Feb. 15, 2012. 24

See Chen Lin, Micah S. Office and Hong Zou, Hong, supra note 2, at 26-7. 25

Id, at 27. Besides, moral hazard is a significant concern in liability insurance. D&O liability insurance may considerably nullify the deterrence effects of litigation against directors, causing directors to be less attentive to their duties to shareholders. See Clifford G. Holderness, Liability Insurers as Corporate Monitors, 10INT'L REV.L.&ECON.115,115(1990).

26

See John M. R. Chalmers, Larry Y. Dann, Jarrad Harford, Managerial Opportunism? Evidence from Directors' and Officers' Insurance Purchases, 57.2 The Journal of Finance 609, 633 (2002). They provide two interpretations for the use of D&O insurance. First, managers use insurance to solid theirs ability to exploit from inside information. Secondly, D&O insurance is used to protect the assets of managers and firms from litigations. Even though these two interpretations are not exclusive, their evidence implies that the former is more important. Id.

27 Id. 28

See Narjess Boubakri, Martin Boyer, and Nabil Ghalleb, Managerial Opportunism in Accounting Choice: Evidence From Directors' And Officers' Liability Insurance Purchases, HEC Montreal working paper, pp. 29-30 (2008). Available at

http://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2008-athens/GH ALLEB.pdf last visited on Feb. 15, 2012.

29 See M. Martin Boyer, Three Insights from the Canadian D&O Insurance Market: Inertia, Information and Insiders, 14 Conn. Ins. L.J. 75, 103 (2007).

30

See Peter Egger, Doina Radulescu, and Ray Rees, D&O Insurance, Corporate Governance and Managerial Incentives, ETH, Zurich; CES and University of Munich working paper, pp.22 (February 15, 2011). Available at http://www.sgvs.ch/congress11/upload/p_115-420219.pdf, last visited on Feb. 15, 2012.

- 6 -

also true in Taiwan market, then D&O insurance itself is no longer good news. D&O insurance represent not only the cover of litigation risk, but also the trigger of moral hazard and opportunistic behavior.

2.3 Introduction of the Ohlson model

When evaluating firm value, non-accounting is usually and relatively less explored.31 The Ohlson model can give a direct link between accounting amount and firm value. With the following refinement, Ohlson model has been frequently applied in the valuation model of firms in accounting research.32 The model postulates abnormal earnings by following two equations:33

~xta1xta vt ~1t1 (1)

v~t1 vt ~2t1 (2)

Where vt indicates the information not yet captured by accounting and

~

is mean 0disturbance term.34 Ohlson model is applied to evaluate how D&O insurance and corporate governance might affect firms’ market value.

3. Hypothesis development

In addition to Ohlson model, this paper also follows the thoughts of Lawrence D. Brown and Marcus L. Caylor which tests the relationship between firm performance and corporate governance,35 to test the relation between firm performance, corporate governance and D&O insurance purchase. This paper assumes D&O insurance have positive effect on firms’ market value. The detailed hypothesis can be presented below.

3.1 Test of signal effect of D&O insurance 3.1.1 Signal hypothesis

The core issue that should be defined first is, is D&O insurance a positive or negative signal to the market? Even though D&O itself is positive news, if it is accompanied by other information such as more internal risks, will this negatively affect firms’

31

See Alnoor Bhimania, Mohamed Azzim Gulamhussenb, Samuel Da-Rocha Lopesc, Accounting and non-accounting determinants of default: An analysis of privately-held firms, 29:6 Journal of

Accounting and Public Policy 517, 520 (2010). 32

See Chii-Shyan Kuo, THE PRICING AND DETERMINANTS OF THE DISCRETIONARY COMPONENT OF

EMPLOYEE STOCK OPTION VALUE 51,ProQuest (2007) . 33

See Kin Lo and Thomas Z. Lys, The Ohlson Model: Contribution to Valuation Theory, Limitations, and Empirical Applications pp. 12 (February 2000). Sauder School of Business Working Paper. Available at SSRN: http://ssrn.com/abstract=210948 or doi:10.2139/ssrn.210948, last visited on Feb. 15, 2012.

34 Id. 35

- 7 -

performance and market price? If D&O insurance protects directors and officers and lets them concentrate on management without worrying about litigation risk, D&O insurance will have positive signal effect. In contrast, if D&O insurance implies that firms might be not confident about their businesses, and firms might be in potential litigation trouble. Even worse, if the problems of moral hazard and adverse selection have been induced, then the purchase of D&O insurance is a bad news to the market. Whether or not D&O insurance can spur firms to optimize their corporate governance is an important signal to the market.36 Under the theory of signal hypothesis, the purchase and coverage of D&O insurance will convey a positive signal to the market and thus improve the market value of insured firms. The hypothesis is set up below: H1: The purchase and coverage of D&O insurance is positively related to the market value of firms.

3.1.2 Corporate governance hypothesis

In addition to the main hypothesis, other relevant variables are used as control variables. As discussed in the literature review, the effect of corporate governance on firms’ market value is controversial. If D&O insurance is an outside monitoring mechanism for corporate governance, it would be reasonable to believe that D&O insurance and other governance mechanisms affect insured firms’ market value. This paper assumes other corporate governance mechanisms would positively affect firms’ market value.

H2: The quality of corporate governance is positive related to the market value of firms.

3.2 Test of opportunistic behavior

3.2.1 Opportunistic hypothesis

As mentioned above, there is much literature discussing D&O insurance, opportunistic behavior and accounting discretion. Moral hazard is tested in this section. Due to D&O insurance shielding litigation risk, insured firms may engage in more risky behaviors. If the insured directors, managers and firms behave opportunistically for an extended period of time, this is easy to be found by insurers.

36

See Sean J. Griffith, Unleashing a Gatekeeper: Why the SEC Should Mandate Disclosure of Details Concerning Directors' & Officers' Liability Insurance Policies, pp. 28(March 24, 2005). U of Penn, Inst for Law & Econ Research Paper No. 05-15. Available at SSRN: http://ssrn.com/abstract=728442 or doi:10.2139/ssrn.728442, last visited on Feb. 15, 2012.

- 8 -

Insurers will adjust premium or even discontinue contract in response to risky behavior. In addition to long term performance, attention should be paid to short term performance after the purchase of D&O insurance. This study diverges from the previous literature on shareholder wealth and long term performance by focusing on short term performance.

In short term performance, D&O insurance purchase might cause volatility of returns. The protection of insurance, allows directors and officers assurances to limit concern regarding litigation risk, expect intentional behavior. In order to maximize their benefit, rational directors and officers might do a highly volatile investment which has higher risk and higher return, as long as this is not excluded by policy exclusions. They will not do this in the long term, because insurers will discover opportunistic behavior and raise the rates. So after D&O insurance purchase, directors and officers might increase opportunistic investment, but not to the extent that is excluded by policies or in the long term to avoid exposure.

The null hypothesis is developed as follows: in Taiwan, D&O insurance would not increase the firms’ volatility of returns and short term investments. In other words, D&O insurance would not cause opportunistic behavior and moral hazard of firms. As a result, the theory regarding the positive signal effect of D&O insurance will not be influenced by these concerns. The hypothesis may be named “neutral hypothesis” and is as follows:

H3: D&O insurance would not increase the firms’ volatility of returns and short term investments

This study uses the standard deviation of ROE as dependent variable, and the standard deviation ROA, EPS, debt-asset ratio and short term investment of firms for robustness check. If there is no moral hazard and opportunistic behavior in the Taiwan market, the purchase of D&O insurance and its coverage shall be not significantly related to these dependent variables. This leads to the fowling sub-hypotheses: H3a: The purchase of D&O insurance is not related to the standard deviation of ROE, ROA, EPS, debt-asset ratio and short term investment of firms.

H3b: The coverage of D&O insurance is not related to the standard deviation of ROE, ROA, EPS, debt-asset ratio and short term investment of firms.

3.2.2 Corporate governance hypothesis

- 9 -

governance of firms is used as control variables. In general, firms having better corporate governance might have less volatility in returns.37 Hence, this paper hypothesizes that the quality of corporate governance is negatively related to the volatility in returns, which contains the standard deviation of ROE, ROA, EPS, debt-asset ratio and short term investment of firms. This hypothesis may be called “corporate governance hypothesis” and is as follows:

H4: The quality of corporate governance of firms is inversely related to the standard deviation of ROE, ROA, EPS, debt-asset ratio and short term investment of firms.

4. Data, variables, methods and research design 4.1 Data

Data used in this paper is collected from Taiwan Economic Journal (TEJ)38 and Market Observation Post System (MOPS).39 There were 1,239 observations in 2008, 1,327 observations in 2009, and 1,241 observations in 2010. These observations exclude data which do not take into account the D&O insurance.

4.2 Variables

4.2.1 Test of signal effect of D&O insurance

Utilizing the Olhson model, accounting and non-accounting information affects firms’ market value. Researchers traditionally use stock price as market value. In D&O insurance literature, M. Martin Boyer also uses market value of equity as the measure of the wealth of shareholder.40 This study uses the market value of firms as the dependent variable. According to the regulation in Taiwan, within three months after

37

Firms with poor corporate governance usually have poor performance, poor profit and higher volatility. See Dr. Laurence J. Stybel, Maryanne Peabody, A New Balance Of Power Means New Boardroom Opportunity for General Counsel, 23 No. 5 Of Counsel 9 (2004). Besides, CalPERS' stated goal is also to “join in the dialogue of corporate governance and reduce volatility and increase

long-term share values.” See Deborah J. Martin, The Public Piggy Bank Goes to Market: Public Pension Fund Investment in Common Stock and Fund Trustees' Social Agenda, 29 San Diego L. Rev. 39, 45 (1992). Moreover, problems of corporate governance would cause market volatility. See Yuwa Wei, Volatility of China's Securities Markets and Corporate Governance, 29 Suffolk Transnat'l L. Rev. 207, 208 (2006). In emerging market of Brazil, firms satisfying better corporate governance standards are less sensitive to changes in market and have less volatility in stock prices. See Ronald J. Gilson, Henry Hansmann, Mariana Pargendler, Regulatory Dualism as a Development Strategy: Corporate Reform in Brazil, the United States, and the European Union, 63 Stan. L. Rev. 475, FN 79 (2011). 38

See http://www.tej.com.tw/twsite/, last visited on Feb. 15, 2012. 39

See http://emops.twse.com.tw/emops_all.htm, last visited on Feb. 15, 2012. 40

See M. Martin Boyer, Directors' and Officers' Insurance and Shareholder Protection, pp. 9 (March 2005). Available at SSRN: http://ssrn.com/abstract=886504 last visited on Feb. 15, 2012.

- 10 -

the close of each fiscal year, listed firms have to publicly announce and register with the competent authority financial reports duly audited and attested by a certified public accountant, approved by the board of directors, and recognized by the supervisors.41 Firms are required to disclose the information regarding D&O insurance after three months of each fiscal year. Prior to November 24, 2010 when the authority amended the regulation, this period was four months. Therefore, the data from different periods following different regulations are used in this study. In order to assess the influence of finance information more accurately, the average stock price of firms of May as dependent variable is used in panels of 2008 and 2009. The average stock price of April is assigned as dependent variable in panel of in 2010. Regarding independent variable, the variables bv and EPS represent the book value of and earnings per share of firms. Regarding the proxy variable of D&O insurance, purchase is a binary variable, which is coded as “1” when firms with insurance and “0” otherwise. Then variable lncoverage is the natural logarithm of D&O insurance coverage. In order to analyze the effect of D&O insurance on firms’ performance completely, this paper will use these two D&O insurance proxy variables in separate panels. The variable purchase would be used in panel A, and the variable lncoverage would be used in panel B.

In terms of the proxy variables of corporate governance, this paper would like to consider non-accounting information and the factors concerning directors and D&O insurance. First of all, it is usually believed that the duality of the chairman of board (COB) and Chief Executive Officer (CEO) is negatively related to market value of firms. Under agency theory, the duality of COB and CEO might cause interest conflict and damage the benefit of firms. Maria Carapeto, Meziane Lasfer and Katerina Machera test this issue by event study, and their research strongly support agency theory.42 They find that the announcement of split of COB and CEO would cause positive abnormal returns and vice versa.43 In order to test the influence of duality of COB and CEO on the performance of firms, this paper sets up the variable dual. It is a dummy variable, which is granted 1 when the chairman of board is identical to CEO and 0 otherwise.

Ideally, independent directors are not affected by interest conflict and it is usually considered as a good mechanism for corporate governance. 44 Accordingly,

41

Securities and Exchange Act (Amended 2010. 11. 24) Article 36 sec1. 42

See Maria Carapeto, Meziane Lasfer and Katerina Machera, Does Duality Destroy Value?, pp. 15 (January 12, 2005). Cass Business School Research Paper. Available at SSRN:

http://ssrn.com/abstract=686707, last visited on Feb. 15, 2012. 43

Id. 44

See Perry E. Wallace, Accounting, Auditing and Audit Committees after Enron, Et Al.: Governing outside the Box without Stepping off the Edge in the Modern Economy, 43 Washburn L.J. 91, 114

- 11 -

appointment of independent or outside directors should convey positive signal to the market and have a significant positive price effect. However, Bernard S. Black, Hasung Jang and Woochan Kim argue that even in developed countries there is no evidence to prove that firms with more independent directors have better performance or higher share price.45 Moreover, appointment of additional independent directors may signal that firms plan to address business problem.46 Some empirical research propose that more independent directors have no statistically significant effect on board’s performance. Some literature even argue that more independent directors would make board’s performance worse.47 In emerging market, Rajesh Chakrabarti, Krishnamurthy Subramanian and Frederick Tung test India market and find that independent director is indeed an importance component of monitoring function and adds the value of firms.48 Even though the results are controversial, but the importance of independent director is undisputable. This paper hypothesizes that the number of independent directors is positively or negatively related to market value of firms. The variable idirector indicates the number of independent directors.

The value of shares may be affected the ownership structure of firms. In firms with dispersed ownership, individual shareholders have less possibility and more cost to control the firms. They also have less incentive to monitor firms. As a result, control is in the hand of management.49 On the other hand, in firms with concentrated ownership, controlling shareholders and blockholders have more incentive to monitor management.50 However, blockholders are also a source of agency cost because they may act for their own benefits and other investors may have to pay for such costs. If investors expect more cost than benefit from ownership, they will discount the shares. In contrast, if investors expect more benefit than cost, they may be willing to pay more.51 Every ownership structure may have different impacts on investors. This is also why securities law regulates the disclosure of ownership structure.52 Besides, dominant owner might also influence firms’ performance and corporate governance.53

(2003). 45

See Bernard S. Black, Hasung Jang and Woochan Kim, supra note 4, at 408. 46

See Sanjai Bhagat and Roberta Romano, Event Studies and the Law: Part Ii: Empirical Studies of Corporate Law, 4 Am. L. & Econ. Rev. 380, 402 (2002).

47

See Sanjai Bhagat & Bernard Black, The Uncertain Relationship Between Board Composition and Firm Performance, 54 Bus. Law. 921, 943 (1999).

48

See Rajesh Chakrabarti, Krishnamurthy Subramanian and Frederick Tung, Independent Directors and Firm Value: Evidence from an Emerging Market, pp.20 (June 28, 2010). Available at SSRN: http://ssrn.com/abstract=1631710, last visited on Feb. 15, 2012.

49

See Michael C. Schouten, The Case for Mandatory Ownership Disclosure, 15 Stan. J.L. Bus. & Fin. 127, 135 (2009). 50 Id. 51 Id. 52 Id. 53

- 12 -

Jayesh Kumar tests Indian market and finds that the shares of directors would significantly influence firms’ performance beyond a certain threshold.54

These factors such as board and ownership structure also affect the risk of directors and related with D&O insurance. This paper sets up following variables to be proxies. The variable Intrlrisk indicates the number of directors and officers appointed by parent company or the controlling group. If the chairman of the board, the CEO, the financial manager or supervisory director is appointed by the parent company or the controlling group, the value will be 1 and 0 otherwise. The final summation ranges from 0 to 4. This variable might be negatively related to market value of firms. The variable ctrldirector indicates the number of controlled directors. This paper hypothesizes that it is negatively related to market value of firms. The variable sd indicates the number of shares of directors and smh indicates the number of shares of major shareholders. These variables are also expected to be negatively related to market value of firms.

In conclusion, in order to consider the effect of D&O insurance and corporate governance on firms’ market value, this paper adds D&O insurance and corporate governance into Ohlson model and reformulates the new equation below. DO represents the proxy variable of D&O insurance, including purchase and lncoverage. CG represents the proxy variables of corporate governance, including dual, intrlrisk, idirector, sd, smh and ctrldirector.

MV = a0 + a1BV + a2 EPS + a3 CG+a4 DO (3)

4.2.2 Test of opportunistic behavior

Regarding the evaluation of opportunism, the standard deviation of revenues is usually used as proxy variables. When testing managerial opportunism caused by D&O insurance, John M. R. Chalmers, Larry Y. Dann and Jarrad Harford use standard deviation of revenues and operating income as proxy variables.55 Jens Hagendorff, Ignacio Hernando, Maria J. J. Nieto and Larry D. Wall use the standard deviation of ROE as a proxy variable of riskiness.56 Michael Bradley and Dong Chen, similarly,

Research, pp. 23. Available at

http://unpan1.un.org/intradoc/groups/public/documents/APCITY/UNPAN023822.pdf, last visited on Feb. 15, 2012.

54

Id, at 23-4. 55

See John M. R. Chalmers, Larry Y. Dann and Jarrad Harford, supra note 26, at 625. 56

See Hagendorff, Jens, Hernando, Ignacio, Nieto, Maria J. J. and Wall, Larry D., What Do Premiums Paid for Bank M&As Reflect? The Case of the European Union (April 20, 2010). Banco de Espana Working Paper No. 1011. Available at SSRN: http://ssrn.com/abstract=1592887, last visited on Feb. 15,

- 13 -

use standard deviation of monthly stock returns as a dependent variable in assessing corporate risk-taking.57 In measuring the volatility of firms’ accounting performance, Seunghan Nam uses the standard deviation of ROE to test its volatility.58 The reason is that ROE is a more relevant measure from the viewpoint of shareholder, and other proxy variables such as ROA, EPS and growth of EPS also have similar results. This paper follows previous literature and uses the standard deviation of ROE as the proxy variable of opportunistic behavior.59 They are used as the dependent variables of regressions. For a test of robustness, this paper uses standard deviation of ROA, EPS, debt-asset ratio and short term investment as dependent variables in different panels. Regarding independent variables, the dummy variable, purchased insurance or not, and the amount of coverage are used as the proxy variables for D&O insurance. The variables about corporate governance are applied as control variables. They include capital of firms, industry of firms, ROE, remuneration for directors, the number of directors, the number of independent directors, the number of controlled directors, shares owned by director and major shareholder, duality of CEO and COB, internal risk, debt-asset ratio and prior significant litigation

[Insert Table 1 here]

4.3 Methods and research design

Ordinary least square (OLS) regression is used in this research. After an initial test of regression, further regression analyses are conducted by generating interaction terms which consisted of D&O insurance and other significant variables. The relationships between market value of firms and how those variables are affected by D&O insurance can be tested. For robustness, the binary variable, insured or not, is used in panel A, and insurance coverage is used in panel B.

Regarding the test of opportunistic behavior, the proxy variables of opportunistic behavior are used as independent variables, and D&O insurance and other control variables are used as independent variables. For robustness, this paper uses standard

2012. 57

See Michael Bradley and Dong Chen, Corporate governance and the cost of debt: Evidence from Director Limited Liability and Indemnification Provisions, 17 Journal of Corporate Finance 83, 92 (2011).

58

See Seunghan Nam, The Impact of Non-audit Services on Capital Markets (October 2006). Available at SSRN: http://ssrn.com/abstract=693422, last visited on Feb. 15, 2012.

59

Similarly, Standard deviation of ROE is also often used as proxy variable for risk for insurer. See J. David Cummins and Gregory P. Nini, Optimal Capital Utilization by Financial Firms: Evidence from the Property-Liability Insurance Industry, 21. 1-2 Journal of Financial Services Research 15, 23 (2002).

- 14 -

deviation of ROE, ROA, EPS, debt-asset ratio and short term investment as dependent variables to carry out different regressions. The statistical software packages used are SPSS and STATA.

5. Empirical result and analysis

5.1 Test of signal effect of D&O insurance 5.1.1 Descriptive analysis

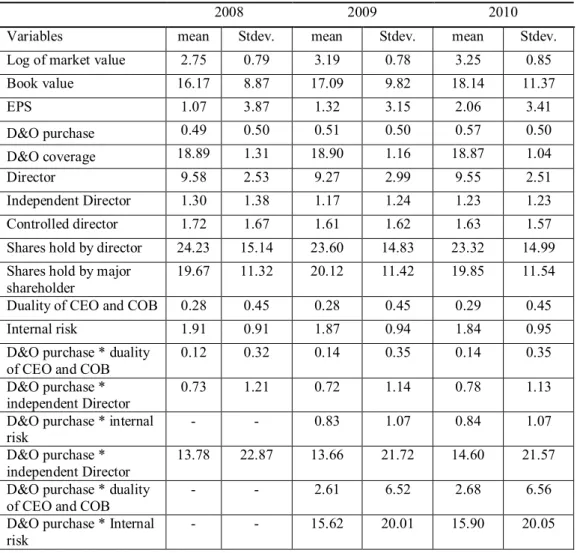

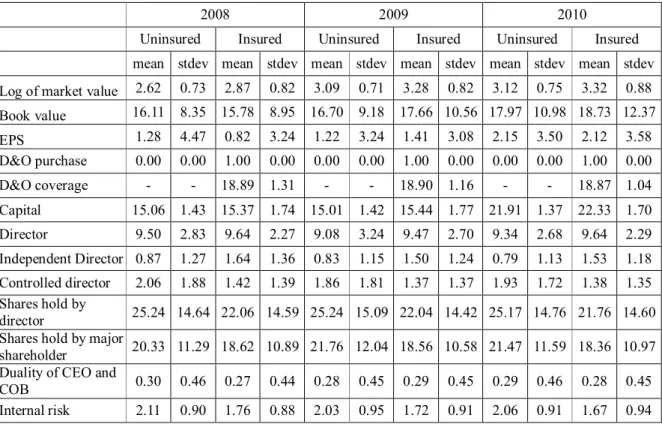

From 2008 to 2010, the mean of market value, book value and EPS all grow gradually. The standard deviations also increase slightly. Similarly, the insured rate has the same tendency. The average of the binary variable, purchase, in 2008 is 0.49, and this means the overall insured rate is around 49%. Then the insured rate is 51% in 2009 and 57% in 2010. The mean of coverage also increases gradually from 2008 to 2010, but the standard deviation is less. This indicates that more firms begin to increase insurance coverage, but the difference between coverage becomes less. This matches with the intuition about the insurance market. When the insured ratio is low, some firms purchase a large amount and some purchase nothing, and thus, the deviation is larger. When more and more firms start to buy insurance, the difference between coverage will decrease and the deviation of coverage will become less.

[Insert Table 2 to 3 here]

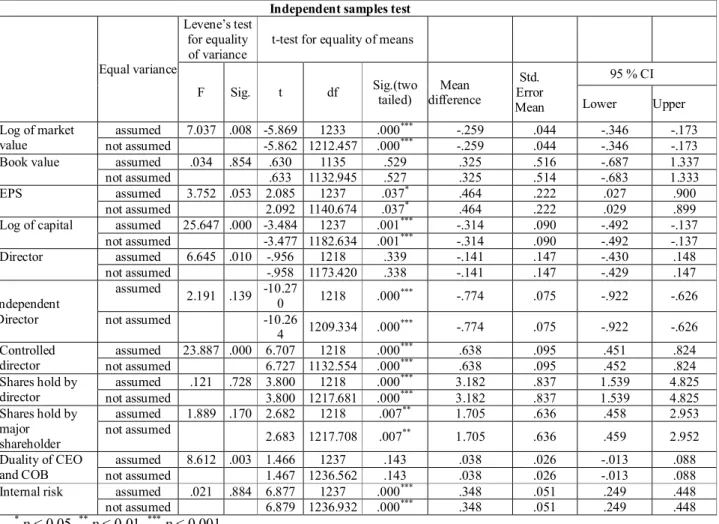

In order to further observe the difference between insured firms and uninsured firms, independent sample tests are conducted in this section. It is found that the difference of means between insured and uninsured firms is significant. This indicates that insured firms have significantly higher market value than uninsured firms from 2008 to 2010. Two implications can be drawn from this result. First, firms that purchase D&O insurance also have higher market value, and this implies D&O may be beneficial for firms’ market value. The effect and magnitude of D&O insurance will be tested by following regression analyses. Secondly, firms with higher market value may purchase more insurance.

[Insert Table 4 to 6 here]

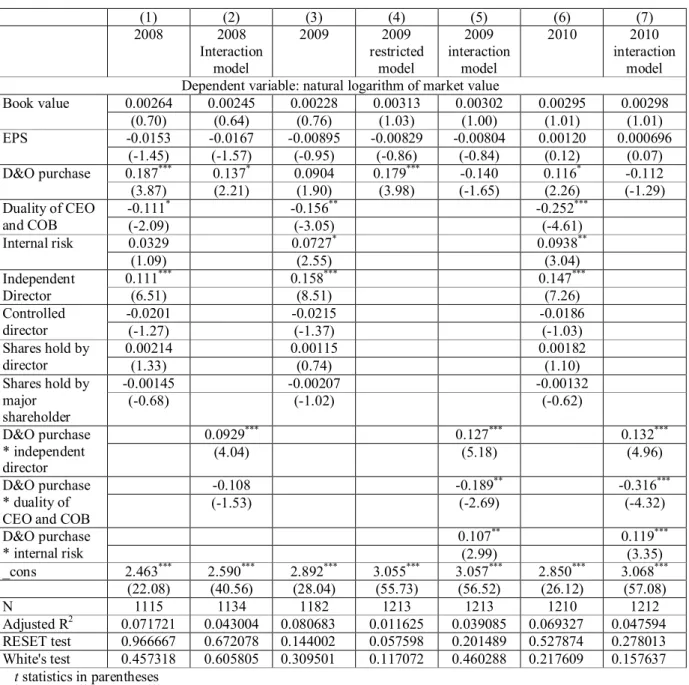

- 15 -

In panel A, the dummy variable, insured or not, is used as proxy variable of D&O insurance. From the result of 2008, it is found that the variables of D&O insurance purchase and the number of independent directors are positively significant. This indicates that they will increase the market value of insured firms. The purchase of D&O insurance indeed conveys a positive signal to the market and thus increases the market price. What’s more, the coefficient 0.187 of purchase is largest, compared with the number of independent directors and other variables which are not significant. All this demonstrates signal hypothesis is highly supported.

For further testing the effect of D&O insurance, the interaction term of purchase and idirector is generated in regression, excluding other insignificant variables. In result, the variable purchase_idirector is positively significant. This indicates that the relationship between the market value of firms and the number of independent directors will be positively affected by the purchase of D&O insurance. An independent director usually is considered to have positive effect on corporate governance. D&O insurance can mitigate potential risk of directors and thus encourage people to resume this position and act according to their profession and morals without worrying about litigation liability.

Regarding the result of 2009, the t-test of the variable is 1.90, and this is close to 2.0 but not significant at 0.05 level. This paper reorganizes the regression and only uses bv, eps and purchase as independent variables. In the restricted model, purchase is very positively significant at 0.001. This is strong evidence for a positive signal effect of D&O insurance. In 2010, the significant variables are purchase of D&O insurance, duality of chairman of board of directors and CEO, internal risk, and number of independent directors. The coefficient of purchase is positive and just less than idirector but larger than intrlrisk and dual. This also shows strong positive signal effect of D&O insurance and signal hypothesis is supported.

Similarly, interaction regressions of 2009 and 2010 are carried out to test the effect of insurance. Interaction terms are generated by multiplying significant variables with purchase. The results of the interaction model of 2009 and 2010 are very similar. The variable purchase_idirector is positively significant, indicating the relationship between market value of firms and the number of independent directors will be positively affected by the purchase of D&O insurance. This also matches the result of 2008. In addition, the relationship between market value and internal risk is also positively affected by insurance purchase. This implies that the effect of insurance to control risk can still convey a positive signal to investors. However, purchase_dual is negatively significant and this indicates when firms purchase D&O insurance and their chairman of board of directors and CEO are the same person, this will convey a

- 16 -

negative signal to the market.

[Insert Table 7 here]

For robustness, the coverage of insurance is used as a proxy variable of D&O insurance in panel B. The results are similar to panel A. From 2008 to 2010, coverage of insurance is positively significant and the magnitudes are quite high compared with other variables. This indicates among the firms with insurance, the amount of coverage will positively and significantly affect firms’ market value. This is very strong evidence for the signal effect of D&O insurance. The result of 2009 supports signal hypothesis but the test score of RESET test is less than 0.05. As a result, some problem about specification is implied. This paper uses restrict regression where only bv, eps and lncoverage are used as independent variables. Similarly, lncoverage is positively significant. Signal hypothesis is still supported.

Next, interaction terms are generated by multiplying significant variables with the coverage of insurance. From 2008 to 2010, the relationship between market value and number of independent directors is positively affected by insurance coverage. This implies insurance indeed conveys a positive signal to the market. In addition, in 2009 and 2010 lncoverage_intrlrisk is positively significant and lncoverage_dual is negatively significant. When coverage and internal risk are high, market value of firms will increase. This confirms the result that D&O insurance indeed conveys a positive signal to investors. However, when firms have D&O insurance and the chairman of the board and CEO are identical, a negative signal will be conveyed and the market value of firms will decrease. This result matches with the result of panel A which uses binary variable, insured or not, as a proxy variable.

[Insert Table 8 here]

5.2 Test of opportunistic behavior

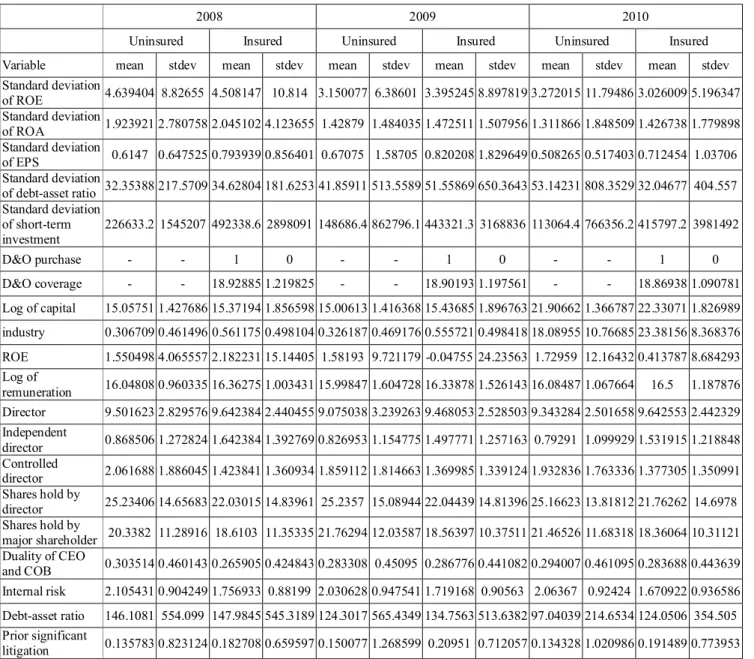

5.2.1 Descriptive analysis

The volatilities of ROE, ROA, EPS, debt-asset ratio and short term investment are represented by their standard deviation respectively. The results show that the insured firms usually have higher average and variation of volatility. In 2008, except ROE, insured firms are higher than uninsured firms in means and variations of ROA, EPS, debt-asset ratio and short term investment. In 2009, insured firms are almost higher

- 17 -

than uninsured firms in all proxy variables, except the variation of short-term investment is much less. The results in 2010 are more diversified, insured firms have lower means in volatility of ROE and debt-asset ratio, but higher in ROA, EPS and short-term investment. Regarding variation, except EPS, insured firms have less variation in the volatility of ROE, ROA, debt-asset ratio and short-term investment. Generally speaking, it is suspicious that insured firms have more volatility in returns and investments.

[Insert Table 9 here]

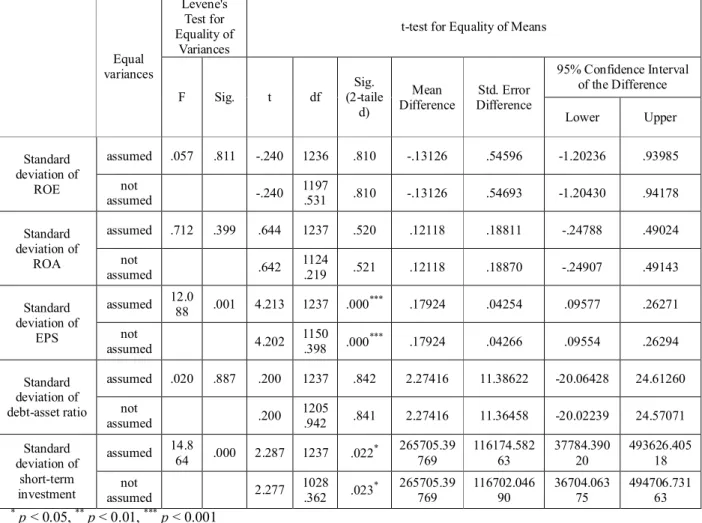

For more precision, independent sample tests are carried out to test whether the differences of the means of volatility between insured and uninsured firms are significant. In 2008, volatility of EPS and short-term investment are significant at 5% level. This indicates insured firms indeed have higher volatility than uninsured firms in EPS and short-term investment. In 2009, only short-term investment is significant, and this indicates that insured firms have higher volatility than uninsured firms in short-term investment. The result of 2010 is similar to 2008. Volatility of EPS and short-term investment are significant and insured firms have higher volatility than uninsured firms in these variables.

[Insert Table 10 to 12 here]

The result of independent sample test indicates insured firms have significantly higher volatility than uninsured firms in EPS and short-term investment. This implies firms might have more opportunistic behavior in EPS and short-term investment after D&O purchase.

5.2.2 Regression analysis 5.2.2.1 2008

Binary variable insurance purchase is used in panel A, and numeric variable nature logarithm of coverage is used in panel B. In panel A, standard deviations of ROE, ROA, EPS, debt-asset ratio and short-term investment are used as dependent variables in respective regressions. The variables insurance purchase is not significant in these regressions. This indicates no statistically significant evidence proving that the

- 18 -

purchase of D&O insurance will increase opportunistic behavior. In panel B, insurance coverage is positively significant when dependent variables are standard deviation of ROE, ROA and EPS, but not significant when dependent variables are standard deviation of debt-asset ratio and short-term investment. This indicates that firms with more coverage may have some intention to conduct opportunistic behavior, but the evidence is not consistent. Besides, remuneration of directors is positively related to the standard deviations of ROA, debt-asset ratio and short-term investment. This implies that with more remuneration directors will perform less opportunistic behavior. If D&O insurance is regarded as a part of the compensation package for directors, this result matches with the previous empirical result, in which risky behavior is not observed.

[Insert Table 13 and 14 here]

5.2.2.2 2009 and 2010

In 2009, the evidence concerning risky behavior of directors is similar to the result of 2008. The variable, insurance purchase, is still not significant with all dependent variables, and insurance coverage is only positively significant with standard deviations of ROA and debt-asset ratio. In 2010, the purchase of D&O insurance is still not significant when dependent variables are standard deviations of ROE, ROA, EPS and debt-asset ratio, but significant when the dependent variable is a standard deviation of short-term investment. This indicates that the purchase of insurance will positively increase the deviation of short-term investment. However, the coverage of insurance is insignificant when dependent variables are ROE, ROA, EPS, debt-asset ratio and short-term investment. This demonstrates that the increase of insurance coverage will not statistically cause significant variance in earnings and investment behavior. In other words, no evidence is found to prove insurance coverage is positively causing the opportunistic behavior and moral hazard of firms.

[Insert Table 15 to 18 here]

5.2.2.3 Interaction regression of 2010

In 2010, the purchase of D&O insurance is negatively significant when the dependent variable is the standard deviation of short-term investment. The coefficient -133134.5 is comparatively large in magnitude. Contrary to the concern that insurance may

- 19 -

cause firms to conduct opportunistic behavior, the empirical result presents that purchasing insurance will decrease the deviation of short-term investment. In other words, the purchase of insurance will decrease opportunistic behavior about short-term investment. In order to further analyze how the relationship between opportunistic behavior and other control variables is affected by insurance, interaction terms are generated by multiplying the variable purchase with other control variables to carry out interaction regressions.

In the interaction regression of 2010, the variable purchase_indptdirector is negatively significant. This indicates that when firms have D&O insurance and the number of independent directors increase, the deviation of short-term investment will decrease. This result confirms that purchasing D&O insurance does not increase opportunistic behavior about short-term investment. The variable purchase_lncapital is also negatively significant. This means when firms have insurance and larger capital, they will engage in less opportunistic behavior about short-term investment. All these results not only reject the argument that purchasing insurance may cause risks, but also indicate that possessing insurance can decrease opportunistic behavior about short-term investment. Again, the concern about the moral hazard of D&O insurance is rejected.

[Insert Table 19 here]

6. Conclusions

From the empirical tests in this paper, it is sustained that D&O insurance indeed conveys a positive signal to the market. Purchasing D&O insurance and increasing insurance coverage both cause the increase of market value of firms. This implies that a firm may purchase D&O insurance for bettering its reputation albeit its litigation risk is low. Even though insurance costs premium, but it can convey a positive signal which is even more significant than the book value and EPS of firms. Hence, the empirical result provides very strong evidence for the signal hypothesis and explains why firms will do so even though they have good corporate governance and their litigation risk is comparatively low.

In terms of opportunistic behavior and moral hazard, empirical evidence shows that the purchase of D&O insurance and its coverage are not statistically significant and consistent in causing variances of earnings and investments. Especially in 2010 almost all statistics are not significant and the only significant result actually rejects the moral hazard concern. In other words, current evidence cannot reject the

- 20 -

hypothesis that D&O insurance will not cause opportunistic behavior and moral hazard of firms. In consequence, even though some literature argues that insurance may cause opportunistic behavior and moral hazard or even damage firms eventually, the empirical work does not find significant evidence. In conclusion, the signal effect of D&O insurance in Taiwan is sustained and not affected by opportunistic behavior and moral hazard.

21

Appendix

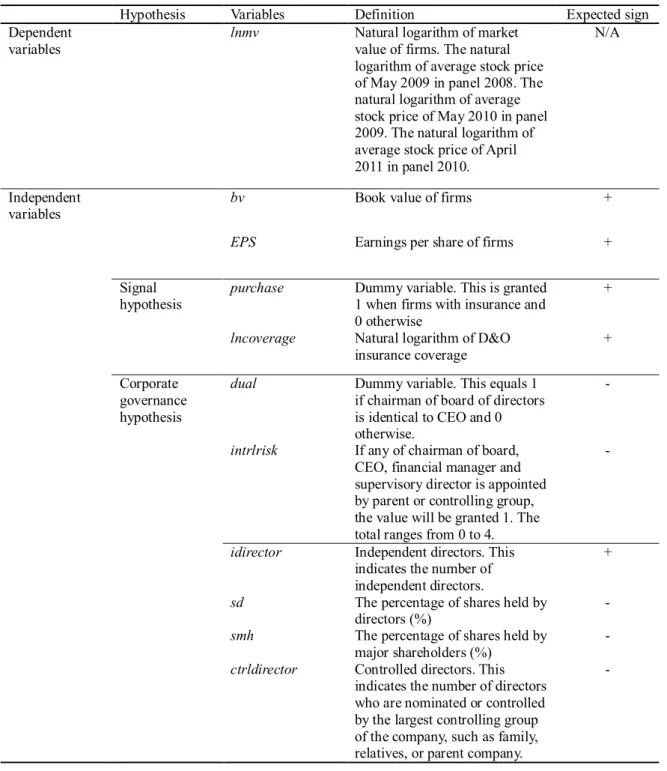

Table 1. Table of variables

Hypothesis Variables Definition Expected sign Dependent

variables

lnmv Natural logarithm of market value of firms. The natural logarithm of average stock price of May 2009 in panel 2008. The natural logarithm of average stock price of May 2010 in panel 2009. The natural logarithm of average stock price of April 2011 in panel 2010.

N/A

Independent variables

bv Book value of firms +

EPS Earnings per share of firms +

Signal hypothesis

purchase Dummy variable. This is granted 1 when firms with insurance and 0 otherwise

+

lncoverage Natural logarithm of D&O insurance coverage

+

Corporate governance hypothesis

dual Dummy variable. This equals 1 if chairman of board of directors is identical to CEO and 0 otherwise.

-

intrlrisk If any of chairman of board, CEO, financial manager and supervisory director is appointed by parent or controlling group, the value will be granted 1. The total ranges from 0 to 4.

-

idirector Independent directors. This indicates the number of independent directors.

+

sd The percentage of shares held by directors (%)

-

smh The percentage of shares held by major shareholders (%)

-

ctrldirector Controlled directors. This indicates the number of directors who are nominated or controlled by the largest controlling group of the company, such as family, relatives, or parent company.

22

Table 2. Descriptive statistics (1)

This table contains the descriptive statistics of variables used in this paper. Regarding the control variables which are significant in regressions, this paper creates interaction term which is the product of these control variables and proxy variable of D&O insurance to test how the association between firms’ value and these control variable affected by D&O insurance.

2008 2009 2010

Variables mean Stdev. mean Stdev. mean Stdev. Log of market value 2.75 0.79 3.19 0.78 3.25 0.85 Book value 16.17 8.87 17.09 9.82 18.14 11.37 EPS 1.07 3.87 1.32 3.15 2.06 3.41 D&O purchase 0.49 0.50 0.51 0.50 0.57 0.50 D&O coverage 18.89 1.31 18.90 1.16 18.87 1.04 Director 9.58 2.53 9.27 2.99 9.55 2.51 Independent Director 1.30 1.38 1.17 1.24 1.23 1.23 Controlled director 1.72 1.67 1.61 1.62 1.63 1.57 Shares hold by director 24.23 15.14 23.60 14.83 23.32 14.99 Shares hold by major

shareholder

19.67 11.32 20.12 11.42 19.85 11.54

Duality of CEO and COB 0.28 0.45 0.28 0.45 0.29 0.45 Internal risk 1.91 0.91 1.87 0.94 1.84 0.95 D&O purchase * duality

of CEO and COB

0.12 0.32 0.14 0.35 0.14 0.35

D&O purchase * independent Director

0.73 1.21 0.72 1.14 0.78 1.13

D&O purchase * internal risk

- - 0.83 1.07 0.84 1.07

D&O purchase * independent Director

13.78 22.87 13.66 21.72 14.60 21.57

D&O purchase * duality of CEO and COB

- - 2.61 6.52 2.68 6.56

D&O purchase * Internal risk

23

Table 3. Descriptive statistics (2)

This table contains the descriptive statistics of variables, comparing the firms with D&O insurance and the firms without D&O insurance. In general, firms with D&O insurance have larger capital, directors and independent directors than firms without D&O insurance. Firms with D&O insurance also have less controlled directors, shares hold by directors and major

shareholders, duality of CEO and COB, and internal risk.

2008 2009 2010

Uninsured Insured Uninsured Insured Uninsured Insured mean stdev mean stdev mean stdev mean stdev mean stdev mean stdev

Log of market value 2.62 0.73 2.87 0.82 3.09 0.71 3.28 0.82 3.12 0.75 3.32 0.88 Book value 16.11 8.35 15.78 8.95 16.70 9.18 17.66 10.56 17.97 10.98 18.73 12.37 EPS 1.28 4.47 0.82 3.24 1.22 3.24 1.41 3.08 2.15 3.50 2.12 3.58 D&O purchase 0.00 0.00 1.00 0.00 0.00 0.00 1.00 0.00 0.00 0.00 1.00 0.00 D&O coverage - - 18.89 1.31 - - 18.90 1.16 - - 18.87 1.04 Capital 15.06 1.43 15.37 1.74 15.01 1.42 15.44 1.77 21.91 1.37 22.33 1.70 Director 9.50 2.83 9.64 2.27 9.08 3.24 9.47 2.70 9.34 2.68 9.64 2.29 Independent Director 0.87 1.27 1.64 1.36 0.83 1.15 1.50 1.24 0.79 1.13 1.53 1.18 Controlled director 2.06 1.88 1.42 1.39 1.86 1.81 1.37 1.37 1.93 1.72 1.38 1.35 Shares hold by director 25.24 14.64 22.06 14.59 25.24 15.09 22.04 14.42 25.17 14.76 21.76 14.60 Shares hold by major

shareholder 20.33 11.29 18.62 10.89 21.76 12.04 18.56 10.58 21.47 11.59 18.36 10.97 Duality of CEO and

COB 0.30 0.46 0.27 0.44 0.28 0.45 0.29 0.45 0.29 0.46 0.28 0.45 Internal risk 2.11 0.90 1.76 0.88 2.03 0.95 1.72 0.91 2.06 0.91 1.67 0.94

24

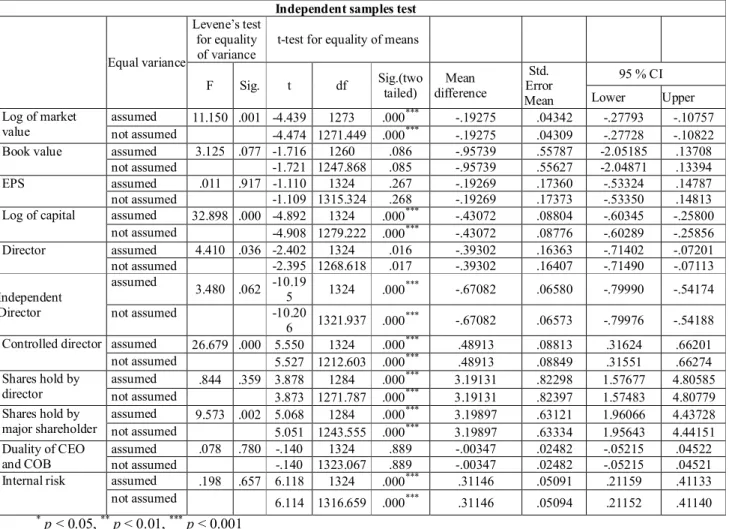

Table 4 Independent samples test of 2008

This table contains independent sample test of 2008. This is to test the difference between firms with D&O insurance and without D&O insurance is significant or not. Except book value, director and duality of CEO and COB, other variables are significant. This indicates the differences of mean in table 3 are significant.

Independent samples test

Equal variance

Levene’s test for equality of variance

t-test for equality of means

F Sig. t df Sig.(two tailed) Mean difference Std. Error Mean 95 % CI Lower Upper Log of market value assumed 7.037 .008 -5.869 1233 .000*** -.259 .044 -.346 -.173 not assumed -5.862 1212.457 .000*** -.259 .044 -.346 -.173 Book value assumed .034 .854 .630 1135 .529 .325 .516 -.687 1.337 not assumed .633 1132.945 .527 .325 .514 -.683 1.333 EPS assumed 3.752 .053 2.085 1237 .037* .464 .222 .027 .900

not assumed 2.092 1140.674 .037* .464 .222 .029 .899 Log of capital assumed 25.647 .000 -3.484 1237 .001*** -.314 .090 -.492 -.137 not assumed -3.477 1182.634 .001*** -.314 .090 -.492 -.137 Director assumed 6.645 .010 -.956 1218 .339 -.141 .147 -.430 .148 not assumed -.958 1173.420 .338 -.141 .147 -.429 .147 Independent Director assumed 2.191 .139 -10.27 0 1218 .000 *** -.774 .075 -.922 -.626 not assumed -10.26 4 1209.334 .000 *** -.774 .075 -.922 -.626 Controlled director assumed 23.887 .000 6.707 1218 .000*** .638 .095 .451 .824 not assumed 6.727 1132.554 .000*** .638 .095 .452 .824 Shares hold by director assumed .121 .728 3.800 1218 .000*** 3.182 .837 1.539 4.825 not assumed 3.800 1217.681 .000*** 3.182 .837 1.539 4.825 Shares hold by major shareholder assumed 1.889 .170 2.682 1218 .007** 1.705 .636 .458 2.953 not assumed 2.683 1217.708 .007** 1.705 .636 .459 2.952 Duality of CEO and COB assumed 8.612 .003 1.466 1237 .143 .038 .026 -.013 .088 not assumed 1.467 1236.562 .143 .038 .026 -.013 .088 Internal risk assumed .021 .884 6.877 1237 .000*** .348 .051 .249 .448 not assumed 6.879 1236.932 .000*** .348 .051 .249 .448

25

Table 5 Independent samples test of 2009

This table contains independent sample test of 2009. This is to test the difference between firms with D&O insurance and without D&O insurance is significant or not. Except book value, EPS, director and duality of CEO and COB, other variables are significant. This indicates the

differences of mean in table 3 are significant.

Independent samples test

Equal variance

Levene’s test for equality of variance

t-test for equality of means

F Sig. t df Sig.(two tailed) Mean difference Std. Error Mean 95 % CI Lower Upper Log of market value assumed 11.150 .001 -4.439 1273 .000*** -.19275 .04342 -.27793 -.10757 not assumed -4.474 1271.449 .000*** -.19275 .04309 -.27728 -.10822 Book value assumed 3.125 .077 -1.716 1260 .086 -.95739 .55787 -2.05185 .13708 not assumed -1.721 1247.868 .085 -.95739 .55627 -2.04871 .13394 EPS assumed .011 .917 -1.110 1324 .267 -.19269 .17360 -.53324 .14787 not assumed -1.109 1315.324 .268 -.19269 .17373 -.53350 .14813 Log of capital assumed 32.898 .000 -4.892 1324 .000*** -.43072 .08804 -.60345 -.25800 not assumed -4.908 1279.222 .000*** -.43072 .08776 -.60289 -.25856 Director assumed 4.410 .036 -2.402 1324 .016 -.39302 .16363 -.71402 -.07201 not assumed -2.395 1268.618 .017 -.39302 .16407 -.71490 -.07113 Independent Director assumed 3.480 .062 -10.19 5 1324 .000 *** -.67082 .06580 -.79990 -.54174 not assumed -10.20 6 1321.937 .000 *** -.67082 .06573 -.79976 -.54188 Controlled director assumed 26.679 .000 5.550 1324 .000*** .48913 .08813 .31624 .66201 not assumed 5.527 1212.603 .000*** .48913 .08849 .31551 .66274 Shares hold by director assumed .844 .359 3.878 1284 .000*** 3.19131 .82298 1.57677 4.80585 not assumed 3.873 1271.787 .000*** 3.19131 .82397 1.57483 4.80779 Shares hold by major shareholder assumed 9.573 .002 5.068 1284 .000*** 3.19897 .63121 1.96066 4.43728 not assumed 5.051 1243.555 .000*** 3.19897 .63334 1.95643 4.44151 Duality of CEO and COB assumed .078 .780 -.140 1324 .889 -.00347 .02482 -.05215 .04522 not assumed -.140 1323.067 .889 -.00347 .02482 -.05215 .04521 Internal risk assumed .198 .657 6.118 1324 .000*** .31146 .05091 .21159 .41133

not assumed 6.114 1316.659 .000***

.31146 .05094 .21152 .41140 * p < 0.05, ** p < 0.01, *** p < 0.001

26

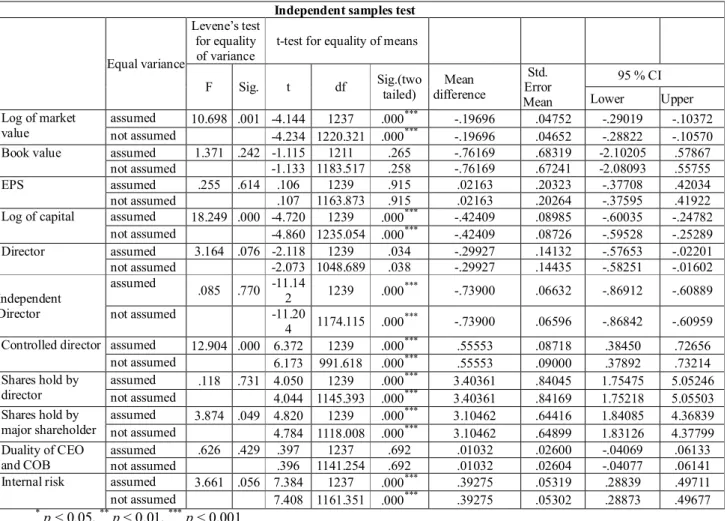

Table 6 Independent samples test of 2010

This table contains independent sample test of 2010. This is to test the difference between firms with D&O insurance and without D&O insurance is significant or not. Except book value, EPS, director and duality of CEO and COB, other variables are significant. This indicates the

differences of mean in table 3 are significant.

Independent samples test

Equal variance

Levene’s test for equality of variance

t-test for equality of means

F Sig. t df Sig.(two tailed) Mean difference Std. Error Mean 95 % CI Lower Upper Log of market value assumed 10.698 .001 -4.144 1237 .000*** -.19696 .04752 -.29019 -.10372 not assumed -4.234 1220.321 .000*** -.19696 .04652 -.28822 -.10570 Book value assumed 1.371 .242 -1.115 1211 .265 -.76169 .68319 -2.10205 .57867 not assumed -1.133 1183.517 .258 -.76169 .67241 -2.08093 .55755 EPS assumed .255 .614 .106 1239 .915 .02163 .20323 -.37708 .42034 not assumed .107 1163.873 .915 .02163 .20264 -.37595 .41922 Log of capital assumed 18.249 .000 -4.720 1239 .000*** -.42409 .08985 -.60035 -.24782 not assumed -4.860 1235.054 .000*** -.42409 .08726 -.59528 -.25289 Director assumed 3.164 .076 -2.118 1239 .034 -.29927 .14132 -.57653 -.02201 not assumed -2.073 1048.689 .038 -.29927 .14435 -.58251 -.01602 Independent Director assumed .085 .770 -11.14 2 1239 .000 *** -.73900 .06632 -.86912 -.60889 not assumed -11.20 4 1174.115 .000 *** -.73900 .06596 -.86842 -.60959 Controlled director assumed 12.904 .000 6.372 1239 .000*** .55553 .08718 .38450 .72656 not assumed 6.173 991.618 .000*** .55553 .09000 .37892 .73214 Shares hold by director assumed .118 .731 4.050 1239 .000*** 3.40361 .84045 1.75475 5.05246 not assumed 4.044 1145.393 .000*** 3.40361 .84169 1.75218 5.05503 Shares hold by major shareholder assumed 3.874 .049 4.820 1239 .000*** 3.10462 .64416 1.84085 4.36839 not assumed 4.784 1118.008 .000*** 3.10462 .64899 1.83126 4.37799 Duality of CEO and COB assumed .626 .429 .397 1237 .692 .01032 .02600 -.04069 .06133 not assumed .396 1141.254 .692 .01032 .02604 -.04077 .06141 Internal risk assumed 3.661 .056 7.384 1237 .000*** .39275 .05319 .28839 .49711 not assumed 7.408 1161.351 .000*** .39275 .05302 .28873 .49677 * p < 0.05, ** p < 0.01, *** p < 0.001

27

Table 7 The result of regression panel A

This table contains the result of regression where binary variable purchasing D&O insurance or not is used as the proxy variable of D&O insurance. Dependent variable is the natural logarithm of firms’ market value. Interaction is generated by the product of D&O insurance purchase and the significant variable. This is to test how the association between firms’ market value and control variables is affected by D&O insurance.

(1) (2) (3) (4) (5) (6) (7) 2008 2008 Interaction model 2009 2009 restricted model 2009 interaction model 2010 2010 interaction model Dependent variable: natural logarithm of market value

Book value 0.00264 0.00245 0.00228 0.00313 0.00302 0.00295 0.00298 (0.70) (0.64) (0.76) (1.03) (1.00) (1.01) (1.01) EPS -0.0153 -0.0167 -0.00895 -0.00829 -0.00804 0.00120 0.000696 (-1.45) (-1.57) (-0.95) (-0.86) (-0.84) (0.12) (0.07) D&O purchase 0.187*** 0.137* 0.0904 0.179*** -0.140 0.116* -0.112 (3.87) (2.21) (1.90) (3.98) (-1.65) (2.26) (-1.29) Duality of CEO and COB -0.111* -0.156** -0.252*** (-2.09) (-3.05) (-4.61) Internal risk 0.0329 0.0727* 0.0938** (1.09) (2.55) (3.04) Independent Director 0.111*** 0.158*** 0.147*** (6.51) (8.51) (7.26) Controlled director -0.0201 -0.0215 -0.0186 (-1.27) (-1.37) (-1.03) Shares hold by director 0.00214 0.00115 0.00182 (1.33) (0.74) (1.10) Shares hold by major shareholder -0.00145 -0.00207 -0.00132 (-0.68) (-1.02) (-0.62) D&O purchase * independent director 0.0929*** 0.127*** 0.132*** (4.04) (5.18) (4.96) D&O purchase * duality of CEO and COB

-0.108 -0.189** -0.316*** (-1.53) (-2.69) (-4.32) D&O purchase * internal risk 0.107** 0.119*** (2.99) (3.35) _cons 2.463*** 2.590*** 2.892*** 3.055*** 3.057*** 2.850*** 3.068*** (22.08) (40.56) (28.04) (55.73) (56.52) (26.12) (57.08) N 1115 1134 1182 1213 1213 1210 1212 Adjusted R2 0.071721 0.043004 0.080683 0.011625 0.039085 0.069327 0.047594 RESET test 0.966667 0.672078 0.144002 0.057598 0.201489 0.527874 0.278013 White's test 0.457318 0.605805 0.309501 0.117072 0.460288 0.217609 0.157637 t statistics in parentheses * p < 0.05, ** p < 0.01, *** p < 0.001

28

Table 8 The result of regression panel B

This table contains the result of regression where D&O insurance coverage is used as the proxy variable of D&O insurance. Dependent variable is the natural logarithm of firms’ market value. Interaction is generated by the product of D&O insurance purchase and the significant variable. This is to test how the association between firms’ market value and control variables is affected by D&O insurance. (1) (2) (3) (4) (5) (6) (7) 2008 2008 Interaction model 2009 2009 restricted model 2009 interaction model 2010 2010 interaction model Dependent variable: natural logarithm of market value

Book value 0.00488 0.00563 -0.00246 -0.00270 -0.00277 0.000810 0.000697 (0.89) (1.04) (-0.62) (-0.67) (-0.70) (0.21) (0.18) EPS -0.0231 -0.0247 0.00149 0.00297 0.00332 0.00901 0.00948 (-1.54) (-1.65) (0.11) (0.21) (0.24) (0.70) (0.73) D&O coverage 0.0855** 0.0786** 0.0726* 0.0693* 0.0576* 0.0831** 0.0671* (3.29) (3.16) (2.47) (2.43) (2.06) (2.59) (2.13) Duality of CEO and COB -0.0974 -0.186* -0.283*** (-1.21) (-2.46) (-3.63) Internal risk 0.0459 0.0888* -0.0101** 0.106* (0.98) (2.04) (-2.59) (2.35) Independent Director 0.0964*** 0.125*** 0.00619** 0.137*** (3.94) (4.78) (3.08) (4.89) Controlled director 0.00891 0.0267 0.0245 (0.31) (0.96) (0.81) Shares hold by director -0.000794 -0.00293 0.0000341 (-0.33) (-1.26) (0.01) Shares hold by major shareholder -0.00403 -0.000783 -0.00523 (-1.27) (-0.25) (-1.71) D&O coverage * independent director 0.00524*** 0.00651*** 0.00681*** (4.16) (4.83) (4.66) D&O coverage * duality of CEO and COB

-0.0101** -0.0162*** (-2.59) (-3.93) D&O coverage * internal risk 0.00619** 0.00693*** (3.08) (3.49) _cons 1.075* 1.161* 1.706** 2.009*** 1.903*** 1.475* 1.695** (2.01) (2.44) (2.85) (3.69) (3.55) (2.30) (2.81) N 589 598 630 643 643 687 687 Adjusted R2 0.038323 0.042437 0.048590 0.005253 0.051483 0.061634 0.060122 RESET test 0.141161 0.11381 0.0223193* 0.882908 0.0757121 0.359164 0.105843 White's test 0.861329 0.704846 0.378663 0.68037 0.803455 0.611807 0.171698 t statistics in parentheses * p < 0.05, ** p < 0.01, *** p < 0.001