可轉換公司債的評價—以久津為例

41

0

0

全文

(2) 謝辭 首先最感謝呂育道老師這一年多來的指導。呂育道老師是一位真正的學者, 這一年多來,不僅從老師身上學到嚴謹治學的方法,更是看到一種儒者的風範。 非常感謝金國興老師,金老師對可轉換的理論與實務都有深入的了解,對於晚輩 也沒有保留。感謝戴天時學長對研究提出的建議,以及平日的照顧。 感謝父母無條件的支持。感謝帛熙、雅麟在我研究所這段日子,以及過去和 未來的幫助與包容。很高興能和士豪、惠文、運君以及金融計算實驗室全體同學 互相切磋。最後想告訴台大財研所有同學,很慶幸過去兩年是由各位陪伴,我將 永遠回憶這段精彩的歲月。.

(3) 摘要 這篇論文以久津實業在 2002 年發行的可轉換債公司債為例,討論可轉債的 一些性質。可轉換債券的條約往往十分複雜。我們常視可轉債為一般債券附上可 轉換為普通股的選擇權。大多數的可轉換公司債均有買回條款、賣回條款以及重 設條款。買回條款使發行者能在特定條件下,買回可轉債;賣回條款使可轉債持 有人可將債券賣回給公司;重設條款則允許了票息、轉換比例和到期日的調整。 在久津的例子中,買回條款的主要效果為強制債券持有人轉換,而轉換價格 每半年會重設一次。這篇論文使用蒙地卡羅模擬做為可轉債的定價方式,因此, 處理重設條款變得十分簡易。賣回條款是這篇論文主要關注的焦點,我將蒙地卡 羅模擬切割為幾個層級以處理之。久津實業在 2003 年 3 月 6 號爆發違約交割, 而這篇論文也會討論該事件以及其結果。.

(4) Abstract This thesis discusses the characteristics of convertible bonds (CB’s), using an issuance of the Chou Chin Industrial Corporation in year 2002 as an example. The contract of a convertible bond is usually quite complicated. We often look at the CB as a straight bond with an attached option to convert into common stocks. Furthermore, most contracts include the call provisions that the issuing company could buy back the issue under certain circumstances, the put features that the CB holders could sell the bond to the issuing company, and some reset features that allow the adjustments of the coupon rate, the conversion ratio, or the maturity date. In the Chou Chin’s case, the main effect of the call is to force the holders to convert the bonds into the common stocks. The conversion price is reset every half year. This thesis uses the Monte Carlo simulation to price the CB; therefore, handling the reset feature is straightforward. The put feature is a main concern of this thesis. A multi-layer Monte Carlo simulation is used to handle the put provisions. The Chou Chin common stock trading default event burst on March 6th, 2003, and the thesis will discuss this event and its consequences..

(5) Contents 1. Introduction 1.1 1.2. Introduction Organization of This Thesis. 1 2. 2 Preliminaries 2.1 Convertible Bonds 2.2 Monte Carlo Simulation. 3. The Chou Chin Issuance 3.1 Conversion 3.2 Call Provisions 3.3 Put Features. 4. 6. 7 9 10. Simulation Approach 4.1 Timeline of the Chou Chin Issuance 4.2 A Triple-Layer Monte Carlo. 5. 3 5. 11 14. Numerical Results 5.1 A Comparison of Issuing Price and Calculated Price 5.2 Sensitivity Analysis 5.3 Comparison of Historical and Simulated Price and the Default Story 5.4 On Credit Risk. 22 24 25. Conclusions. 33. Reference. 34. 27.

(6) List of Figures 2.1 An Ideal Convertible Bond. 3. 4.1 Timeline of the Chou Chin Issuance. 11. 4.2 Value of CB in Binomial Model. 12. 4.3 An Example of a Double-Layer Monte Carlo Simulation. 14. 4.4 A Heuristic Depiction of the Triple-Layer Monte Carlo. 15. Simulation for Pricing the Chou Chin CB Issuance 4.5 Payoff of the 10th Day before Maturity. 17. 4.6 Payoff in the End of the Month upon Called. 21. 5.1 Sensitivity Analysis for Each Parameter. 29. 5.2 Special Conversion Ratio. 30. 5.3 Comparison of Historical and Simulated Price. 31. 5.4 Cumulative Abnormal Return from the 27th of Jan. to the. 32. 4th of Mar..

(7) List of Tables 4.1 Summary of Holder Options on Three Special Points. 13. 5.1 Parameters Used in Pricing the Chou Chin’s Guaranteed. 22. Convertible Bond 5.2 Parameters Used in Pricing the Chou Chin’s. 23. Non-Guaranteed Convertible Bond 5.3 Comparison of Issuing Prices and Calculated Values. 24.

(8) Chapter 1 Introduction 1.1 Introduction This thesis discusses the characteristics of convertible bonds (CB’s), using an issuance of the Chou Chin Corporation in year 2002 as an example. The contract of a convertible bond is usually quite complicated. We often look at the CB as a straight bond with an attached option to convert into common stocks. Furthermore, most contracts include the call provisions that the issuing company could buy back the issue under certain circumstances, the put features that the CB holders could sell the bond to the issuing company, and some reset features that allow the adjustments of the coupon rate, the conversion ratio, or the maturity date. In the Chou Chin’s case, the main effect of the call is to force the holders to convert the bonds into the common stocks. The conversion price is reset every half year. This thesis uses the Monte Carlo simulation to price the CB; therefore, handling the reset feature is straightforward. The put feature is a main concern of this thesis. A multi-layer Monte Carlo simulation is used to handle the put provisions. The Chou Chin common stock trading default event burst on March 6th, 2003, and the thesis will discuss this event and its consequences.. 1.

(9) 1.2 Organization of This Thesis There are six chapters in this thesis. The first part is a brief introduction. In Chapter 2, we introduce convertible bonds and Monte Carlo simulation. In Chapter 3, we go into the Chou Chin issuance. Our approaches are introduced in Chapter 4. The simulation results and the Chou Chin default story are discussed in Chapter 5, followed by a conclusion in Chapter 6.. 2.

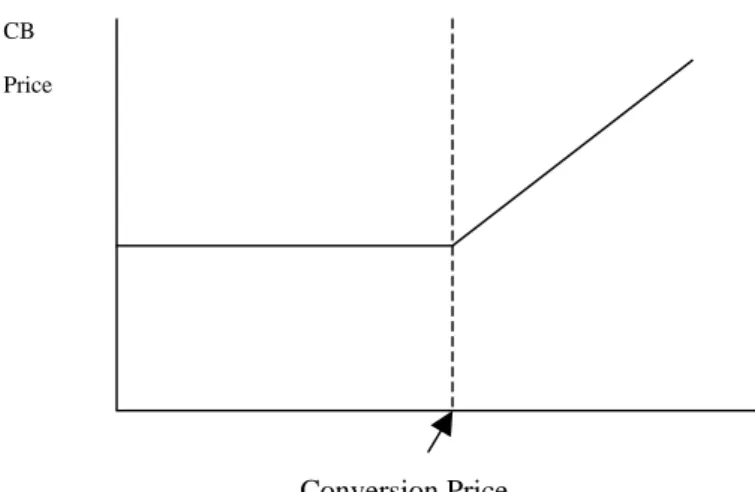

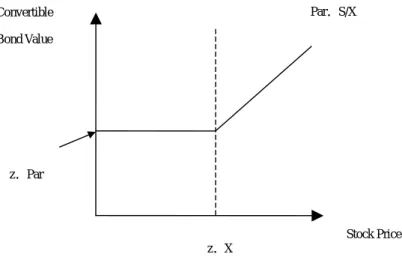

(10) Chapter 2 Preliminaries 2.1 Convertible Bonds A convertible bond (CB) is like an ordinary bond except that it can be converted into common stocks at the discretion of its owner. It provides the safety feature of a bond and the capital gains opportunity of common stocks. It is therefore often referred as a kind of hybrid securities. Let’s consider an ideal convertible bond in Fig. 2-1. Assume that there is only one conversion point. If the stock price exceeds the conversion price, the CB holder may convert the CB into common stocks, and share the appreciation of the stock’s capital gains. But if the stock price stays low under the conversion price, the CB sustains its value as a fixed-income security.. CB Price. Stock Price. Conversion Price Figure 2.1 An Ideal Convertible Bond. 3.

(11) 2.1.1 Call Provisions Most CB issuances include call provisions which enable the issuing corporation to call the bond for redemption prior to the final maturity. The call provisions indicate the circumstances under which the security can be called, the date, and the call price. Issuing corporations may call the bond when the debts can be refinanced under better terms if interest rates fall or the corporation’s financial situation improves. Sometimes the call provisions are implemented to force conversion. The famous theorem of Nobelists Franco Modigliani and Merton Miller (1958) shows that the firm’s methods of financing should be indifferent in perfect capital markets. By relaxing one or more of the perfect market’s assumptions, several widely examined theories result in important implications for the choice of financing method in general and the use of convertibles in particular. Define the conversion value as the number of shares into which an issue may be converted multiplied by the current price per share of the common stock, and the effective call price as the sum of nominal call price and accrued interest. Ingersoll (1977a) and Brennan (1977) show that it is optimal to call and force conversion as soon as the conversion value rises to the effective call price. We will adapt their results in this thesis.. 2.1.2 Reset Features Reset features are used as CB sweeteners. Under certain prescribed conditions, the reset features allow for the adjustments of the coupon rate, the conversion ratio, the maturity date, or some combination thereof. According to Calamos (1998), reset features are used as sweeteners to help troubled companies sell their bonds, and these bonds are often lower-grade, speculative issues. However, many issuances in Taiwan 4.

(12) with reset features are not from troubled companies.. 2.1.3 Put Features The convertible bonds started to include the put features in the 1980s. Under the offered terms, the holder could sell the bond back to the issuer at a stated price on a specific date. The put is at the discretion of the holder and is for a much shorter time period than the maturity date of the bond. It alleviates the interest risk of holder by reducing the time to maturity.. 2.2 Monte Carlo Simulation Monte Carlo simulation is a sampling scheme used for solving stochastic problems. It is one of the few feasible tools in many important applications within and without finance, and one of the most important elements of studying econometrics. Monte Carlo simulation may be the only strategy that succeeds consistently when the time evolution of a stochastic process is not easy to represent analytically, and it is immunized against the curse of dimensionality in general. The Monte Carlo algorithm is like to perform a probability experiment using a dice; however, a random number generator replaces the dice here. (In fact, a “pseudo-”random number generator would be used.) Assume that X1, X2,…, Xn have a joint distribution and we’re looking for the mean θ≡E[g(X1, X2,…, Xn)] for a given function g. Using the random number generator, we generate. ( x1( i ) , x 2( i ) ,..., x n(i ) ),1 ≤ i ≤ N , independently with the same joint distribution as (X1, X2,…, Xn) and let Yi ≡ g ( x1( i ) , x 2( i ) ,..., x n(i ) ).. 5.

(13) Therefore Y1, Y2,…, YN are independent and identically distributed random variables and each Yi has the same distribution as Y≡g(X1, X2,…, Xn). The average of N random variables, Y , can be used as an estimation of θ , for E[ Y ]= θ . Actually, the strong law of large numbers indicates that the procedure converges almost surely. The. number of replications, N, is referred to as the sample size.. 2.2.1 Modeling Stock Prices Assume the stock price behavior follows the geometric Brownian motion, ∆S = µS∆t + σSξ ∆t ,. (2.1). where ΔS is the change in the stock price, S, in a small interval of time, Δt; and ξ is a random drawing from the standard normal distribution. The parameter, μ, is the expected rate of return per unit of time from the stock and the parameter, σ, is the volatility of the stock price. Both μ and σ are assumed constant. In equation (2.1) we can see thatΔS/S is normally distributed with mean μΔt and standard deviation σ ∆t . That is, ∆S ∼N ( µ∆T , σ ∆T ). S. (2.2). Therefore, the stock prices S1, S2, S3,…, at timesΔt, 2Δt, 3Δt,…, can be expressed by S i +1 = S i e ( µ −σ. 2. / 2 ) ∆t +σ ∆tξ. , ξ∼N (0,1). (2.3). The number of trading days in a year is approximately 250. In this thesis, the time interval Δt is set as a day, i.e., 0.004 year.. 6.

(14) Chapter 3 Main Features of the Chou Chin Issuance In December 2002, the Chou Chin Company issued two kinds of CB, guaranteed by the Chung-ho branch of the Hwa Nan Commercial Bank and non-guaranteed, both with zero coupon. The total issuing amount of the collateralized convertible bonds is NT$300 million, and that of the non-collateralized bonds is NT$700 million. Since the two kinds of issuance are similar, this thesis will focus on the collateralized issuance. The Chou Chin First Collateralized Domestic Convertible Bond Issuance was issued on the 26th of December in 2002.. The par. value is NT$100,000, and the bonds are sold at par. The maturity is of 5 years, and on the 25th of December, 2007.. 3.1 Conversion 3.1.1 Conversion Period The convertible bonds could be converted to newly issued common stocks of the Chou Chin Company. The conversions are at the discretion of the bond holders at any time from 3 months after issuance date, to 10 days before the maturity date,. 7.

(15) except some suspension period1.. 3.1.2 Conversion Price and Reset The initial conversion price of the issuance is NT$16. In the pricing of the initial conversion price, the 24th of October in 2002 is used as the reference date. The corporation uses the 101% of the lowest among the average stock prices during 10 trading days before the reference date, during 15 trading days before the reference date, and during 20 trading days before the reference date. If there are share or cash dividends paid before the actual issuing date, the conversion price would be adjusted according to the anti-dilution clauses. The conversion price will be reset every half year. The 30th of June and the 28th of December every year before maturity is the reference date, and define the reference price as the lowest among the average stock prices during 10 trading days before the reference date, during 15 trading days before the reference date, and during 20 trading days before the reference date. The new conversion price is reset as Max(Min(PCP, 101% of RP), 80% of ICP) =Max(Min(PCP, 101% of RP), 12.8),. (3.1). where PCP is the prevailing conversion price, RP is the reference price, and ICP is the initial conversion price, NT$16. As shown in equation (3.1), the conversion price is only adjusted downward, and never below NT$12.8. This thesis would neglect the effect of newly issued stocks because the conversion price would be adjusted by anti-dilution provisions.. 1. The period at least three business days prior to the date the issuer notifies the TSE of the record date for determination of shareholders entitled to received dividends, subscription of new shares or other benefits to the record date for the distribution or allocation of the relevant dividends, rights and benefits. 8.

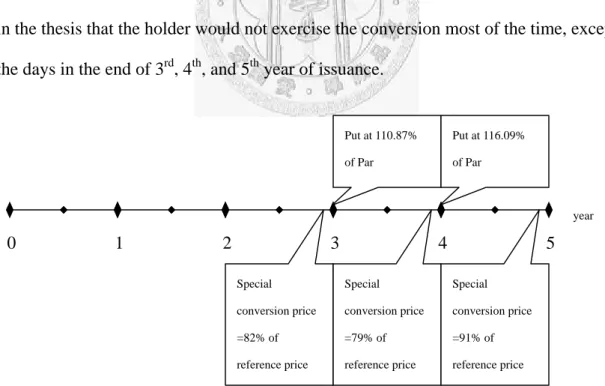

(16) 3.1.3 Special Reset In addition to the conversion reset and anti-dilution provisions described above, the 25th of November in 2005, the 25th of November in 2006, the 25th of November in 2007 (thirty days before 3rd, 4th, and 5th issuing anniversary, respectively) are the reference dates of the special conversion price. The special conversion prices are 82%2 of the reference price on the reference date in 2005, 79%3 of the reference price on the reference date in 2006, and 91% of the reference price on the reference date in 2007. The special conversion price is not constrained to be above the 80% of the initial conversion price by the reset provisions described in section 3.1.2. If the convertible bond holders are willing to exercise the special conversion, they should request within the period from the 3rd to the 9th day after the reference date.. 3.2 Call Provisions From the 4th month of the issuance to the 40th day before maturity, if the Chou Chin’s stock price has been exceeding 150% of the conversion price for straight 30 trading days, then within 30 days thereafter, the issuer may send the CB holders a registered notification that must be replied within one month to be called. The convertible bonds might be redeemed on the maturity at the prices listed below: 1. From the 31st day after issuance to the 3rd anniversary of the issuance, redeem the bond at an annual yield of 3.5%4. 2. From the day after the 3rd anniversary of the issuance to the 4th anniversary of the issuance, redeem the bond at an annual yield of 3.8%5. 3. From the day after the 4th anniversary of the issuance to the 40th day before 2 3 4 5. 80% in the non-guaranteed issues. 76% in the non-guaranteed issues. 4.5% in the non-guaranteed issues. 4.8% in the non-guaranteed issues. 9.

(17) maturity, redeem the bond at par. However, at the time when the call provisions could be triggered, the CB value is at least 150% of par value. Most of the case, the CB holders would convert the CB’s rather than surrender to be redeemed. Therefore, we can see the call as a “conversion-forcing call”.. 3.3 Put Features Within 30 days before the 3rd anniversary and 30 days before the 4th anniversary, the holder can sell the bond back to the issuer. In the 3rd anniversary, the bond is sold at 110.87%6 of the par. In the 4th anniversary, the bond is sold at 116.09%7 of par. Note that if the bond is not converted or redeemed before the maturity, we can also say that the holder “sell back” to the issuer at par at maturity.. 6 7. 114.12% in non-guaranteed issues. 120.63% in non-guaranteed issues. 10.

(18) Chapter 4 Simulation Approach 4.1 Timeline of the Chou Chin Issuance The Chou Chin issuance is quite complicated. To make it clear, a timeline is illustrated here in Figure 4.1. The conversion could be exercised anytime from the 4th month from the issuance to the 10th day before the maturity. Because the holders benefit from the stock appreciation and enjoy the downside protection, it is assumed in the thesis that the holder would not exercise the conversion most of the time, except the days in the end of 3rd, 4th, and 5th year of issuance.. Put at 110.87%. Put at 116.09%. of Par. of Par. year. 0. 1. 2. 3. 4. 5. Special. Special. Special. conversion price. conversion price. conversion price. =82% of. =79% of. =91% of. reference price. reference price. reference price. Figure 4.1 Timeline of the Chou Chin Issuance. Note that the conversion price will be reset every half year, and if the Chou Chin stock price exceeds 150% conversion price for straight 30 days, the issuer would have an option to call the CB’s back. 11.

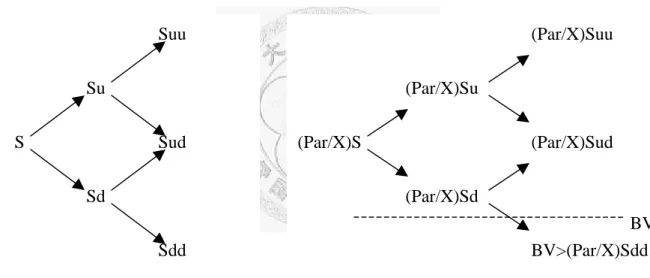

(19) Why the convertible bonds would not be converted except three special points can be explained with the binomial option pricing model (BOPM), as shown in Figure 4.2. Throughout the thesis, S denotes the stock price, Par the par value of the CB, X the conversion price. The BOPM assumes if the current stock price is S, it can go to Su with probability q and Sd with probability 1-q. Here a two-stage BOPM is used. Most of the time, the holder could convert a Chou Chin convertible bond into (Par/X) shares of common stock, and the convertible bond value is at least its straight bond value BV. Without loss of generality, assume that (Par/X)Sdd<BV<(Par/X)Sud. It’s obvious that the expected value of retaining the security as the form of CB is greater than converting it into common stocks. Suu. (Par/X)Suu. Su S. (Par/X)Su Sud. Sd. (Par/X)S. (Par/X)Sud (Par/X)Sd. Sdd. BV BV>(Par/X)Sdd. Figure 4.2 Value of CB in Binomial Model. If the convertible bonds are not redeemed or called earlier, from the 3rd day to the 9th day after the 25th of November in 2005 (near the end of 3rd year of issuance), the holder would have four options on hand. First, in the 7-day period specified earlier the holder could exercise a special conversion at a conversion price of 82% of the reference price. Second, the holder could also sell the bond back to the issuer at 110.87% of par. Moreover, the holders could convert the bonds at the conversion price. 12.

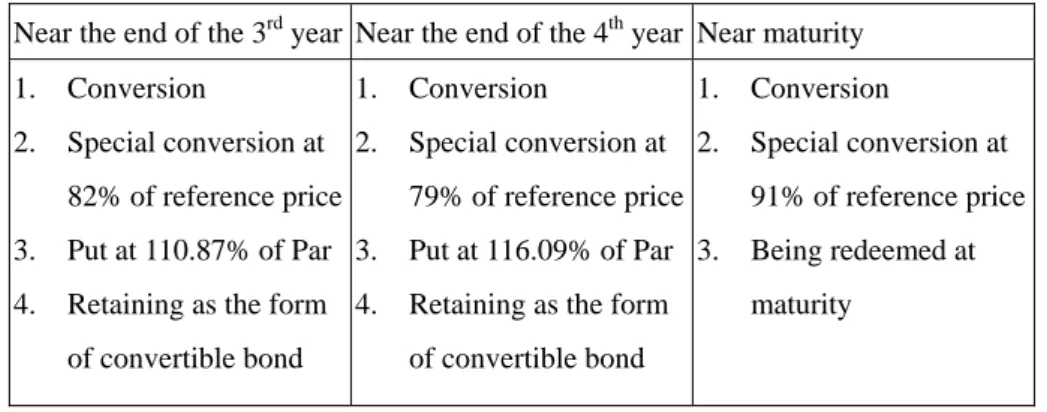

(20) Finally, the holder could also retain the securities as a form of convertible bonds if he or she expects that it is more favorable. Similarly, if the convertible bonds are not redeemed or called earlier, from the 3rd day to the 9th day after the 25th of November in 2006 (near the end of 4th year of issuance), the holders would also have four options on hand. First, in the 7-day period specified earlier the holder could convert the bond at a special conversion price of 79% of reference price. Second, the holder could also sell the bonds back to the issuer at 116.09% of par. Further, the holder can convert the bonds at the conversion price. Finally, this holder could also retain the securities as the form of convertible bonds. From the 3rd day to the 9th day after the 25th of November in 2007 (near maturity), if the convertible bonds are not redeemed or called earlier, the holders could convert the securities at conversion price or special conversion price. And if a holder does no conversion at that time, the convertible bonds will be redeemed at maturity. The holder options are summarized in Table 4.1. Since the three period mentioned above are critical to the holder, the pricing process of this thesis will focus on the holder decisions of the three points. Near the end of the 3rd year Near the end of the 4th year Near maturity 1.. Conversion. 1.. Conversion. 1.. Conversion. 2.. Special conversion at. 2.. Special conversion at. 2.. Special conversion at. 82% of reference price. 79% of reference price. 91% of reference price. 3.. Put at 110.87% of Par 3.. Put at 116.09% of Par 3.. Being redeemed at. 4.. Retaining as the form 4.. Retaining as the form. maturity. of convertible bond. of convertible bond. Table 4.1 Summary of Holder Options on Three Special Points. 13.

(21) 4.2 A Triple-Layer Monte Carlo As stated in Section 4.1, we know that there are three special points for the convertible bond holders to make decisions. The uncertainty is less in the point near maturity than in other two points, therefore it is relatively easy for the holder to make a decision in the last point. In the thesis, the Black-Scholes model will be implemented to price the convertible bond value in the days near maturity. In the end of the 4th year of issuance, the holders have to decide to convert the bonds, sell them back to the issuer, or retain them as the form of convertible bonds. The redemption price, the conversion price and the special conversion price are known at that time. Therefore, a holder would have to know the expected value of the securities retaining the form of convertible bond to help him make a decision among those options, and a Monte Carlo simulation is used in the evaluation of the expected value. Similarly, the holders would also have to make a decision in the end of the 3rd year after issuance, and Monte Carlo simulations again will be used in the evaluation. Figure 4.3 An Example of a Double-Layer Monte Carlo Simulation. 14.

(22) Therefore, it would a totally triple-layer Monte Carlo simulation. The Figure 4.3 is an example of a double-layer Monte Carlo simulation. Note the call provisions in this issuance. If the stock price of Chou Chin has been exceeding 150% of the conversion price for straight 30 days, the issuer could redeem the convertible bond. But since the redemption price is far lower than the conversion value, we can see that action as a “conversion-forcing call”. Ingersoll (1977a) and Brennan and Schwartz (1977) show that on convertible securities, it is optimal to call and force conversion as soon as the conversion value rises to the effective call price1.. Figure 4.4 A Heuristic Depiction of the Triple-Layer Monte Carlo Simulation for pricing the Chou Chin CB Issuance Every calendar year is assumed to have 250 trading days, so there will be totally 1250 trading days under consideration. If the simulation paths are not truncated by the call of issuer, in fact, there will be g paths spanned from each node in the end of the 3rd year (the 733rd day), and there will be h paths spanned from each node in the end of the 4th year. 1st to 3rd yr,. 4th yr,. 5th yr,. m=5. g=4. h=3. j=733 j=983. j=1. j=1233. 1. The sum of the nominal call price (usually given in a schedule in the contrast) and accrued interest (on bonds) or dividends (on preferred stocks). 15.

(23) Ingersoll later finds that the call is “delayed”, and explanations include a safety margin to avoid cash redemption2 or even costly financial distress.3 However, on convertible preferred stocks, Byrd, Moore, and Ramanlal (1998) argue that their results reveal no substantial delays in calling convertible preferred stocks. When the Chou Chin’s CB is callable, the conversion value will far exceed the effective call price. Further, it would provide a sufficient safety margin to avoid cash redemption. Therefore, we assume here that as long as the call provisions are triggered, the issuer will exercise the call. Since the convertible bonds are forced to convert at that time, the simulations in the path thereafter is not necessary, and the path will be truncated, the conversion value will be recorded as the simulating result of the path, and the simulation will begin with a new path. If the simulation is not truncated by the call, there will be m paths from the first to the third year of issuance, g paths in the fourth year, and h paths in the last year. Every calendar year is assumed to have 250 trading days, and a stock price is generated in each trading day. The third day after the 25th of November in 2005 is assumed to be the 733rd trading day of issuance, the third day after the 25th of November in 2006 is assumed to be the 983rd trading day of issuance, and the third day after the 25th of November in 2007 is assumed to be the 1233rd trading day of issuance, and the it is assumed holders have to make decisions on the three critical days. A heuristic depiction of the triple-layer Monte Carlo simulation for pricing the Chou Chin Issuance is shown in Figure 4.4.. 4.2.1 Simulating the Last Year Suppose that on the 983rd trading day, a holder have to make a decision. He or 2 3. See Ingersoll (1977b). See Jaffee and Shleifer (1990). 16.

(24) she knows the historical stock prices from the 1st to the 983rd trading day, and has to estimate the expected value of the convertible bonds if the securities are retained as the form of convertible bonds instead of being converted or redeemed, and compare the expected value with the redemption price, the conversion price, and the special conversion price. Therefore, a Monte Carlo simulation of h paths is used here to estimate the expected value. Now consider the days near maturity. On the 1233rd trading day, the holder could convert the bond at the special conversion price of 91% of reference price. The bond could also be converted at the conversion price until the 10th day before maturity, or be redeemed at par at maturity. Consider first the conversion and the redemption, the payoff at the 10th day before maturity (about the 5th trading day before maturity) is shown in Figure 4.5. The payoff feature could be decomposed into American call stock options and straight bonds. We can replicate that payoff by holding Par/X units of call with an exercise price of (y.X),4 and straight bonds of the par value of (y.Par) and maturity. Par.S/X. Convertible Bond Value. y.Par, Discounted Par Value Stock Price y.X. Figure 4.5 Payoff on the 10th day before maturity. 4. y stands for the discount factor of 10 days. 17.

(25) with the original convertible bond. Here I use an European option estimation as the lower bound estimation of the call value and the Black-Scholes formula is used. With the option of special conversion, on the 1233rd day CB value = Max(DPV + VAC, SCV5),. (4.1). where DPV is the discounted par value, VAC is the value of Par/X units of American call option, and SCV5 stands for the special conversion value at a conversion price of 91% of reference price. By the Black-Scholes formula, the value of a unit of call is at least5. c = S 0 N (d1 ) − y.Xe − rT N (d 2 ),. (4.2). where ln(S0 / yX ) + (r + σ 2 / 2)T d1 = σ T ln(S0 / yX ) + (r − σ 2 / 2)T d2 = . σ T. Hence, average the results of the 1233rd day of h paths and discount the average to the 983rd day, a convertible bond holder can use it as an estimator of expected value of the securities retaining the form of convertible bonds in the last year, and compare it with the redemption value, the conversion value and the special conversion value. Note that the simulating path will be truncated if in such a path that the stock price exceeds the conversion price for 30 straight days. In the days from the 26th of November in 2006 to the 40th day before maturity6, when the simulation is truncated for call provisions, the conversion value will be evaluated and the future value of the conversion value compounded to the 1233rd trading day will be used as the result of this path. The manipulation of the call provisions will be explained in detail later. 5. S0=stock price of the 1233rd trading day, r=risk-free rate, X=conversion price of CB, σ=annual volatility, and T=(7/250)year 6 About the 983rd to the 1222nd trading day of issuance. 18.

(26) 4.2.2 Simulating the Earlier Years In last section, it is mentioned that h paths are simulated after the 983rd day after issuance to help holders make a decision on the 983rd day. Similarly, g paths are simulated from the 734th to the 983rd day of issuance to help holders make a decision on the 733rd day, and m paths are simulated from the 1st to the 733rd day of issuance. In fact, if the simulation paths are not truncated by the call provisions, the g paths are generated from the end of each m paths, and h paths are generated from the end of each g paths. On the 983rd day of issuance, the holder has four option on hand, as listed in Table 4.1. The holder has to choose the best favorable one among them. Therefore, CB value = Max(SCV4, CV4, RV4, EVCB4),. (4.3). where SCV4 is the special conversion value at a conversion price of 79% of reference price, CV4 is the conversion value, RV4 is the redemption value of 116.09% of par value, and EVCB4 is the expected value, which is generated by the h simulation paths, of the security retained as the form of CB after the 983rd trading day. Average the g results on the 983rd day, and discount it to the 733rd day, we have the expected value of the security retained as the form of CB after the 733rd trading day. Hence, the CB value of the 733rd trading day of issuance should be CB value = Max(SCV3, CV3, RV3, EVCB3),. (4.4). where SCV3 is the special conversion value at a conversion price of 82% of reference price, CV3 is the conversion value, RV3 is the redemption value of 110.87% of par value, and EVCB3 is the expected value, which is generated by the g simulation paths, of the security retained as the form of CB after the 733rd trading day. Average the m results and discount it to the day of issuance, we have an estimation of the convertible bond value.. 19.

(27) 4.2.3 Handling of Call Provisions From the 4th month of issuance to the 40th day before maturity, if the Chou Chin’s stock price has been exceeding the 150% of the conversion price for straight 30 trading days, then within 30 days the issuer may send the CB holders a registered notification that must be replied within one month to be called. It is assumed here that the CB’s will be called as long as the call provisions can be triggered, and as stated in section 3.2, we can see that request as a “conversion forcing call”, and we’ll truncate the simulating path. From the 4th month, to the 25th of November in 20057, if the convertible bond is called, the value of the called bond would be evaluated, the simulation will be truncated, and the future value of the called bond on the 25th of November in 2005 would be recorded as the result of this one of m simulations. From the 4th month to the end of 3rd year after issuance, once called bye the issuer, the convertible bond would be redeemed at an annual yield of 3.5%, or be converted to common stocks at the discretion of the holder. Upon being called, the holder would have one month to make the choice. To simplify the analysis, we assume that the bond can only be converted at the conversion price, since special conversion could only happen in a very short time and we have taken care on it. Therefore in the case, a convertible bond can be seen as Par/X units of American stock call option with a maturity of one month and a exercise price of (z.X),8 and a bond with a maturity of a month, an annual yield of 3.5% and a par value the same with the original CB. The payoff is shown in Figure 4.6. Similar to the approach stated in section 4.2.1, we use the Black-Scholes formula again to price 7. Approximately from the 61st to the 733rd trading day of issuance. z=future value factor with an annual yield of 3.5% from the 4th month to the 733rd trading day of issuance. z=future value factor of an annual yield of 3.8 from the 734th to the 983rd trading day. z=1 from the 984th trading day.. 8. 20.

(28) Par.S/X. Convertible Bond Value. z.Par. Stock Price z.X. Figure 4.6 Payoff in The End of The Month upon Called The Bond value is at an annual yield of 3.5% from the 4th month to the end of 3rd year of issuance, at an annual yield of 3.8% in the 4th year, and at par in the last year.. the call option, and adding the bond value with a yield of 3.5% to it. Then compound the result to the 733rd day and record it, truncate the simulation, and start another simulation from the 1st day of issuance. Similarly, from the 734th to the 983rd day (from the 984th day to 1222nd day) of issuance, once the convertible bond is called, we use the Black-Scholes formula to price the call, and adding the bond value with a yield of 3.8% (the bond with par value) to it. Then compound the result to the 983rd (1233rd) day and record it, truncate the simulation, and start another simulation from the 734th (984th) day.. 21.

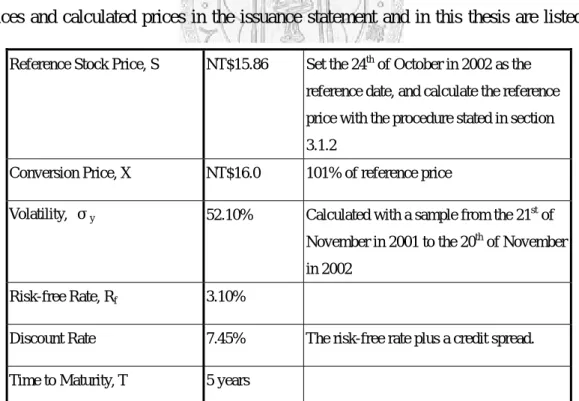

(29) Chapter 5 Numerical Results 5.1 A Comparison of Issuing Price and Calculated Price The parameters used in pricing the guaranteed and non-guaranteed convertible bonds issued by Chou Chin Industrial Co. are listed in Table 5.1 and 5.2. The issuing prices and calculated prices in the issuance statement and in this thesis are listed in Reference Stock Price, S. NT$15.86. Set the 24th of October in 2002 as the reference date, and calculate the reference price with the procedure stated in section 3.1.2. Conversion Price, X. NT$16.0. 101% of reference price. Volatility, σy. 52.10%. Calculated with a sample from the 21st of November in 2001 to the 20th of November in 2002. Risk-free Rate, Rf. 3.10%. Discount Rate. 7.45%. Time to Maturity, T. 5 years. The risk-free rate plus a credit spread.. Table 5.1 Parameters Used in Pricing the Chou Chin’s Guaranteed Convertible Bond The parameters are offered in the Issuance Statement of Chou Chin’s Convertible Bond. 22.

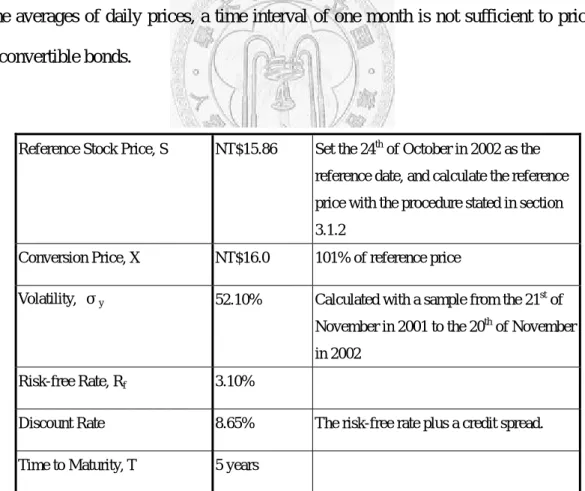

(30) Table 5.3. Take the guaranteed issue as an example. The calculated value in this thesis is NT$137,878, while the calculated value in the issuance statement is NT$109,992.92, and the issue price is NT$100,000. It’s quite a large discrepancy between the two calculated values. Which one is a better estimation? I think the issuer underestimated the value of the convertible bonds. To read the provisions in the issuances, you can find that the provisions are very favorable to the CB holders: the conversion price can only be reset downward, the convertible bonds call only be called while the stock price has been exceeding the conversion price for straight 30 days, and etc. Moreover, the issuer declares that they used a binomial tree method in pricing the convertible bonds; however, a time interval of one month is used in the tree between the nodes. Since the conversion price resets are based on some averages of daily prices, a time interval of one month is not sufficient to price the convertible bonds.. Reference Stock Price, S. NT$15.86. Set the 24th of October in 2002 as the reference date, and calculate the reference price with the procedure stated in section 3.1.2. Conversion Price, X. NT$16.0. 101% of reference price. Volatility, σy. 52.10%. Calculated with a sample from the 21st of November in 2001 to the 20th of November in 2002. Risk-free Rate, Rf. 3.10%. Discount Rate. 8.65%. Time to Maturity, T. 5 years. The risk-free rate plus a credit spread.. Table 5.2 Parameters Used in Pricing the Chou Chin’s Non-Guaranteed Convertible Bond The parameters are offered in the Issuance Statement of Chou Chin’s Convertible Bond 23.

(31) Guaranteed Issuance. Non-guaranteed Issuance. Issuing Price. NT$100,000. Calculated Value in Issuance Statement. NT$109,992.92. Calculated Value in the Thesis. NT$137,878. Issuing Price. NT$100,000. Calculated Value in Issuance Statement. NT$109,056.94. Calculated Value in the Thesis. NT$136,278. Table 5.3 Comparison of Issuing Prices and Calculated Values. 5.2 Sensitivity Analysis 5.2.1 Volatility, Initial Stock Price, and Discount Rate This section dicusses the sensitivity of various parameters on the pricing model. The results are shown in Figure 5.1, and each value is simulated with m=1000, g=100 and h=10. The simulation results of the CB value with varing volatility in the stock price are shown in Figure 5.1(a). Because of the option characteristics of the CB, the higer the volatitily , the higher the CB value. As shown in Figure 5.1(b), the CB value is positively related to the initial stock price. Figure 5.1(c) shows the simulation results for different discount rates. The CB value decreases as the discount rate increases. Since the different discount rates imply different credit ratings, the credit risk issue will be discussed later. According to our simulations, the values of guaranteed and non-guranteed issuances are quite close. That’s because although the discount rate of the non-guaranteeded issuance is higher,. 24.

(32) other provisions in the non-guaranteed issuance are more favorable to holders the than those in guaranteed issuance.. 5.2.2 Special Conversion Price Define that the special conversion price is the product of the special conversion ratio 1 and the reference price. The sensitivity ananlysis for different special conversion ratios is shown in Figure 5.2. Since a lower special conversion ratio is favorable to CB holders, we see the negative slopes in the figures. But we see that CB value is more sensitive with the conversion ratios of earlier years. The convertible bonds might be called or converted earlier; therefore, the effect on the adjustment of later year conversion ratio is less than that of earlier years.. 5.3 Comparison of Historical and Simulated Prices and the Default Story 5.3.1 Comparison of Historical and Simulated Prices Comparisons of historical traded prices and simulated CB values are shown in Figure 5.3. The data are from TEJ database2. However, because the Chou Chin’s CBs were of low liquidty, and the stock settlement default event bursted in March, 2003, the data are not available on each trading day of issuance. In Figure 5.3, the market prices are obviously lower than simulated values. In the beginning of issuance, the two numbers move in a parallel way. But as the stock price. 1. For example, in this issuance, the conversion ratio is 82% in the end of the 3rd year, 79% in the end of the 4th year, and 91% in the end of the 5th year. 2 I thank Rita Chien of TEJ Corporation for help. 25.

(33) rose, the gap between them was narrowed. To verify the undervaluation of the market, the data of the 4th of March in 2003 can be used as an example. The stock price then was NT$30.9, the traded CB price is NT$135,200, but the simulated CB value is NT$195,346. The conversion price was NT$16, nearly doubling the stock price, and the conversion can be exercised within a month, therefore the simulated results, NT195,346, nearly doubling the CB par value, is a reasonable estimation. The first explanation is that the CB market in Taiwan lacks efficiency. The Chou Chin’s CB trading volumes were quite small on most trading days. The investors in Taiwan might fail to appreciate the intrinsic value of the convertible bonds. Another explanation is that the low trading prices reflected the risk expectation for the Chou Chin CB issuance.. 5.3.2 The Default Story On the 27th of January in 2003, the Chou Chin stock price was NT$18.1. Since then, the stock price skyrocketed to NT$30.9 on the 4th of March. At the same time, the Taiwan stock market stumbled, the TAIEX Index was 4972.59 on the 27th of January, and 4499.69 on the 4th of March. During this period, the cumulative abnormal return3 on Chou Chin common stock is shown in Figure 5.4 and up to 66.17%. What abnormal was not only return but also trading volume. The average trading volume of the Chou Chin stock from the 27th of February to the 5th of March is NT$1.3 Billion, while the average of 2002 is only NT$138.6 Million. The TAIEX. 3. Cumulative abnormal return to the jth trading day is defined as j. CARj =. ∑. RSi – RMi. i =1. where RSi is the daily stock return of the ith trading day, and RMi the daily market return (the TAIEX index return) of the ith trading day. 26.

(34) started to monitor the trades on the Chou Chin stocks on the 3rd of March,4 and the stock trading defaults on the 6th of March. As we can see in section 5.3.1, the CB was significantly underpriced in the market. An arbitrage trade could be done by selling the Chou Chin common stocks and buying the convertible bonds if everything went well. However, it was said in the news that the default event might be out of improper manipulation intending to beat the bears.5 On the 14th of April, the Chou Chin Industrial Corporation declared that the convertible bonds should all be seen as matured.. 5.4 On Credit Risk The credit risk is considered in the thesis within the discount rate. However, the discount rates listed in the Issuance Statement are debatable. The discount rate of the guaranteed issuance is 7.45% and that of the non-guaranteed issuance is 8.65%. However, the former is guaranteed by the Chung-ho branch of the Hwa Nan Commercial Bank; the credit status is far better than the Chou Chin Industrial Corporation, but the credit spread of these two kinds of convertible bonds is small. Several credit risk model are developed. However, some are not appropriate here. For example, Carayannopoulos and Kalimipalli (2003) follow the Duffie and Singleton (1999) framework, and assume a functional form for the hazard rate as follows:. h(t , S ) =. 1 , e βS. (5.1). where S is for stock price and t is for time. In their model, as the stock price increases, and thus the likelihood of default diminishes, the default hazard rate approaches zero.. 4 5. See the issue of the 8th of March in 2003, Economic Daily News, Taiwan. See footnote 4. 27.

(35) But in the Chou Chin’s case, the stock prices might be manipulated improperly, and the default event happened right after the peak of the stock price.. 28.

(36) Figure 5.1 Sensitivity Analysis for Each Parameter. ( a)v o latility (%) 300000. CB Value (NT$). 250000 200000 150000 100000 50000 0 35. 40. 45. 50. 55. 60. 65. 70. 75. 80. 85. 27. 30. 33. 36. 39. 13. 15. 17. 19. 21. (b )in itial sto ck p rice ( NT$ ) 300000. CB Value (NT$). 250000 200000 150000 100000 50000 0 9. 12. 15. 18. 21. 24. (c) d isco u n t r ate (%) 300000. CB Value (NT$). 250000 200000 150000 100000 50000 0 1. 3. 5. 7. 9. 11. 29.

(37) Figure 5.2 Special Conversion Ratio. (a)Special Conversion Ratio 3 144000. CB Value (NT$). 142000 140000 138000 136000 134000 132000 130000 0.7. 0.73. 0.76. 0.79. 0.82. 0.85. 0.88. 0.91. 0.94. 0.97. 1. 8. 9. 10. 11. 8. 9. 10. 11. special conversion ratio. (b)Special Conversion Ratio 4 144000. CB Value (NT$). 142000 140000 138000 136000 134000 132000 130000 1. 2. 3. 4. 5. 6. 7. special conversion ratio. (c)Special Conversion Ratio 5 144000. CB Value (NT$). 142000 140000 138000 136000 134000 132000 130000 1. 2. 3. 4. 5. 6. 7. special conversion ratio. 30.

(38) Figure 5.3 Comparison of Historical and Simulated Prices (a)Guaranteed 250. 200. 150. Simulated CB Value Historical CB Price Stock Price. 100. 50. 0 0. 10. 20. 30. 40. 50. 60. 70. 80. 90. (b)Non-guaranteed. 250 200 150. Stock Price Historical CB Price Simulated CB Value. 100 50 0 0. 10. 20. 30. 40. 50. 31.

(39) Figure 5.4 Cumulative Abnormal Return from the 27th of Jan. to the 4th of March 70.00 60.00. CAR (%). 50.00 40.00 30.00 20.00 10.00 0.00 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11 12. 13 14 15. 16 17. 18 19 20. trading day. 32.

(40) Chapter 6 Conclusions In this thesis, I provide a Monte Carlo approach to price the convertible bond issuance of the Chou Chin Industrial Corporation with a maturity of 5 years. I assume that the CB holders will spontaneously convert or sell back the convertible bonds on only three special points, where the holders have options of special conversion or put. One of the special points is near maturity, and two other points divide the 5 years into 3 periods, and a triple-layer Monte Carlo simulation is used. This thesis also discusses the default story of the Chou Chin Industrial Corporation, and compares the simulated value with the issuing price and market price of the convertible bonds. I find both the issuer and the market underprice the convertible bonds, and it would have been an excellent arbitrage opportunity if the default trading had not happened. Therefore, the undervaluation might be because the Taiwan convertible bond market lacks of efficiency and fails to price the CB value, or reflect the risky nature of this issuance.. 33.

(41) References 1.. Calamos, John P., 1998. “Convertible Securities: the latest instruments, portfolio strategies, and valuation analysis.” New York: McGraw-Hill.. 2.. Carayannopoulos, Peter and Madhu Kalimipalli, 2003. “Convertible Bond Prices and Inherent Biases,” Journal of Fixed Income 13(3), 64-73.. 3.. Duffie, Darrell and Kenneth J. Singleton, 1999. “Modeling Term Structures of Defaultable Bonds.” Review of Financial Studies, Vol. 12, 687-720.. 4.. Ingersoll, Jonathan E., Jr. 1977a. “A Contingent-Claims Valuation of Convertible Securities,” Journal of Financial Economics 4, 289-321.. 5.. Ingersoll, Jonathan E., Jr. 1977b. “An Examination of Corporate Call Policies on Convertible Securities,” Journal of Finance 32, 463-478.. 6.. Jaffee, Dwight and Andrei Shleifer, 1990. “Cost of Financial Distress, Delayed Calls of Convertible Bonds, and the Role of Investment Banks,” Journal of Business 63, S107-S124.. 7.. Lyuu, Yuh-Dauh, 2002. “Financial Engineering and Computation: Principles, Mathematics, Algorithms.” New York: Cambridge Univ. Press.. 8.. Moore, William T., 2000. “The Life Cycle of Convertibles and Warrants,” Handbook of Hybrid Instruments, 61-81. Edited by Izzy Nelken. John Wiley & Sons.. 34.

(42)

數據

+7

相關文件

For pedagogical purposes, let us start consideration from a simple one-dimensional (1D) system, where electrons are confined to a chain parallel to the x axis. As it is well known

The observed small neutrino masses strongly suggest the presence of super heavy Majorana neutrinos N. Out-of-thermal equilibrium processes may be easily realized around the

incapable to extract any quantities from QCD, nor to tackle the most interesting physics, namely, the spontaneously chiral symmetry breaking and the color confinement..

(1) Determine a hypersurface on which matching condition is given.. (2) Determine a

• Formation of massive primordial stars as origin of objects in the early universe. • Supernova explosions might be visible to the most

2-1 註冊為會員後您便有了個別的”my iF”帳戶。完成註冊後請點選左方 Register entry (直接登入 my iF 則直接進入下方畫面),即可選擇目前開放可供參賽的獎項,找到iF STUDENT

Starting from January 2006, the CPI has been rebased to July 2004 to June 2005, apart from the compilation of the Composite CPI that reflects the impacts of price changes for

The difference resulted from the co- existence of two kinds of words in Buddhist scriptures a foreign words in which di- syllabic words are dominant, and most of them are the