1

College of Management

I-Shou University

Master Thesis

The effect of moral intensity on ethical decision

process: An empirical study of accounting

professionals in Vietnam

Advisor:

Dr. Shu-Hui Su

Graduate Student: Nguyen Thi Thao

(Sara)

3

Acknowledgements

Firstly, I would like to show my deep gratefulness to my advisor, Dr. Shu-Hui Su, who gave me the research orientation and useful meticulous consultancy during my research process. Thanks to my advisor’s enthusiasm guidance, I can finish my thesis and also get experience and skill to approach and solve problems in the research activity. I am always thankful for my advisor’s effort that she put in guiding me. You are my grate professor that I am lucky to have.

Next, I would like to send my sincere gratitude to some auditors as well as my partners who helped me to conduct this survey and collect data from respondents. Due to their zealous help and collaborations, my survey could be implemented more quickly and conveniently.

Then, I want to thank all representatives from 5 companies taking part in this survey. I would like to appropriate their ardent cooperation during the survey process.

4

Abstract

The purpose of the study is to investigate the relationship between moral intensity and ethical decision making within the field of accounting. The hypotheses were based on Jones’s (1991) issue-contingent model which identifies six components of moral intensity that influence individual ethical decision-making. To examine the difference in perceived moral intensity and ethical decision process, this research analyzes the perception of moral intensity, moral recognition, moral judgment and moral intention as dependent variables by different accounting issues as an independent variable. Additionally, the research also examined whether a relationship existed between moral intensity and demographic factors related to ethical decision-making such as age, gender, education background and working experrience.

By adapting four scenarios involving accounting ethical dilemma from the study of Flory et al (1992), a survey was administered to the sample, accountants in business organizations in Vietnam. The results of this study supported the finding of Leitsch (2004) that the perception of moral intensity and the specific stages of the ethical decision-making process were affected by ethical issue. In addition, the result showed significant differences in the responses to the characteristics of ethical dilemmas exist with respect to demographic variables. The results of the study implied that accountants with higher education background tend to make ethical decision. The results implied that the male accountants tended to agree unethical decision; while, the research found the younger accountants or accountants with short term working experience tended to be easier to perceive the unethical situation. This study is expected to provide a further understanding of the effect of the characteristics of moral issues on the process of ethical decision-making and the relationships among the factors that affect the ethical decision-making of accounting professionals.

Keyword: accounting ethics, moral intensity, moral recognition, moral judgment, moral intension

5

Table of content

Acknowledgements ... 3 Abstract ... 4 List of Tables ... 7 List of Figures ... 8 Chapter 1: INTRODUCTION... 9 1.1 Research Background ... 91.2 Problem Statement and Research Questions ... 10

1.3 Research Significance ... 10

Chapter 2: LITERATURE REVIEW ... 12

2.1 Ethical decision making ... 12

2.2 Moral intensity ... 13 2.3 Demographic variables ... 16 2.3.1 Gender ... 16 2.3.2 Education background ... 17 2.3.3 Working experience ... 18 2.3.4 Age ... 18 Chapter 3: METHODOLOGY ... 20 3.1 Conceptual framework ... 20 3.2 Research design ... 22 3.3 Survey instrument ... 22 3.4 Measurement ... 23 Chapter 4 RESULTS ... 27

Summary of the findings ... 46

Chapter 5 CONCLUSION ... 49 5.1 Research Summary ... 49 5.2 Research Limitations ... 50 5.3 Research Implications ... 50 Reference ... 51 APPENDIX A ... 57

6

7

List of Tables

Table 3..1 Hypotheses and Statistical Tests ... 25

Table 4. 1 Selected Demographic Characteristics of the Sample ... 27

Table 4. 2 Means and Standard Deviation. ... 29

Table 4. 3 Multivariate tests of moral sensitivity/moral intensity (MSMI) components for accounting issues. ... 30

Table 4. 4 Multivariate tests of moral judgment/moral intensity (MJMI) components for accounting issues ... 31

Table 4. 5 Multivariate tests of moral intentions/moral intensity (MRMI) components for accounting issues ... 32

Table 4. 6 Means of Age ... 34

Table 4. 7 MANOVA Test of Components of Moral Intensity and Age ... 35

Table 4. 8 Means of Gender ... 36

Table 4. 9 MANOVA Test of Components of Moral Intensity and Gender ... 37

Table 4. 10 Means of Education ... 39

Table 4. 11 MANOVA Test of Components of Moral Intensity and Education ... 40

Table 4. 12 Pairwise Comparisons of Components of Moral Intensity and Education ... 41

Table 4. 13 Means of Working experience ... 45

Table 4. 14 MANOVA Test of Components of Moral Intensity and Working experience ... 45

8

List of Figures

Figure 3. 1 A model of accountant’ ethical decision process in accounting scenarios Adapted from Jones (1991) and Frey (2000) ... 21

9

Chapter 1: INTRODUCTION

Chapter one describes the background of the research problem, introduces outline the importance and significance for further research related to moral intensity and ethical decision making in the field of accounting with research questions and research objectives.

1.1 Research Background

Accounting professional ethics recently received a lot of attention. The stories regarding unethical behavior of accounting professionals keep happening and the situation seems not to have been improved. Many believe that ethics are the foundation of public accounting practice. By appealing to the notion of ethical issues in accounting, the researchers enter into the profound consideration of what constitutes ethical behavior and how such behavior is motivated. This study extends prior research related to the influence of moral issues on the process of ethical decision-making by examining whether accounting professionals in Vietnam perceived differently to a set of ethical dilemmas.

To ensure high ethical standards for accountants in implementing professional judgment, understanding the factors associated with improving levels of moral development is very important and of practical value. Previous studies have examined the influence of the components of moral intensity on the stages such as moral recognition, moral judgment and moral intention (Frey, 2000; May and Pauli, 2002). These studies found the components of moral intensity significantly influence the ethical decision making process of various subjects. However, few studies have investigated how these issue characteristics affect the specific steps of the ethical decision process and their relationship with other personal factors by accounting professionals such as accountants in business organization. Therefore, this research will make considerable effort to identify and investigate the factors related to the ethical decision process of accounting professionals and provide supporting evidence to an association between moral intensity and personal variables such as gender, educational achievement and working experience and age.

10

1.2 Problem Statement and Research Questions

The accounting scandals of Enron, WorldCom and other corporations have caused great damage of confidence in the integrity of accounting and business. Business and accounting ethical issues have drawn the attention of the media and public. And as a result (Carson, 2003), they become singular important in the field of business and accounting research as never before. There is also a consequence for researchers in business ethics that ethical behavior is a complicated interaction of organizational customs, personality characteristics, and current societal beliefs, which affect individual ethical decision-making (Herndon et al., 2001).

Based on the literature review of the study by Craft (2013), several research questions for this study were developed as the followings:

1. Is there any difference between the accountants’ perception of the dimensions of moral intensity and their ability to recognize that a moral issue exists?

2. Is there any difference between the accountants’ perception of the dimensions of moral intensity and the likelihood that they will judge an unethical action as inappropriate? 3. Is there any difference between the accountants’ perceptions of the dimensions of moral

intensity and their intentions to respond ethically to a moral conflict?

4. Does the relationship exist between the accountants’ perception of the dimensions of moral intensity and demographic factors such as age, gender, education background, and working experience?

1.3 Research Significance

The social consequences are derived from the ethical behavior of all citizens and organizations. In the work environment, efficiency experts take into consideration ethical accounts related to individual performance in quality control as conceal, deceive customers about the usual sales commission, theft stealing office supplies, or more common, and often lied about a sick day. This type of regular incidents, as well as more serious fraud, for example, cheating on

11

expense accounts, bribery, collusion prices, and discrimination against industry peers amounts very precious money, perhaps billion each year (Jones, 1997) and the damage cost the company's image.

Recently, there have been many types of research about the effect of moral intensity on the ethical decision process in many countries in the world. However, those types of research mainly investigated developed countries such as The UK, The US, Australia, France, The Netherlands, Canada and Germany and the Asia-Pacific region like Hong Kong, Singapore, China, Indonesia, Malaysia and Taiwan. Therefore, this empirical study of accounting professionals in Vietnam will extend the results of previous researches related to the investigation of the effect of moral intensity on the ethical decision process of developing nations.

Proper ethics and ethical behavior are extremely important in accounting for a variety of reasons. To begin with, accountants are often privy to sensitive information regarding their clients, such as Social Security or bank account numbers. This gives accountants a good deal of power in regard to their clients and it is important that the trust between an accountant and their clients not be abused (Geoffrey, 2016). For example, in Vietnam, the mismanagement of many companies was because the accountants who make unethical decisions greatly affect the company's operations. Thus, along with other previous research results, the results of this study are expected to be able to help Vietnamese accountant to improve their ethical decision making in the future.

12

Chapter 2: LITERATURE REVIEW

Ethics in accounting is one of the most important concerns in the world of business today. The field of business ethics deals with questions about whether specific business practices are acceptable. Regardless of their legality, actions taken in such situations will surely be judged as right or wrong, as either ethical or unethical. The very nature of business ethics is controversial and there is no universally acceptable approach for addressing these issues. On the other hand, governments encourage organizational accountability for ethical and legal conduct. However, the public accounting profession has long relied on its reputation for integrity and veracity as justification for its professional status and monopoly privileges based on claims of acting in the public interest. If such status and privileges are to be justified and sustained, it becomes ethically imperative for the profession to give serious consideration to what constitutes ethical behavior, how such behavior is motivated and what rights and interests of affected parties may have (Dillard, 2002, pp. 49-64). This section presenting a scholarly review of earlier work provides an appropriate history and recognizes the priority of the work of others in moral intensity and ethical decision making.

2.1 Ethical decision making

Several methods are being developed for the moral complexity of decision by the researchers (eg, Ferrell & Gresham, 1985; Hunt & Vitell, 1986; Jones, 1991; Trevino, 1986). According to Rest’s (1986) four stages process, individuals must first recognize the presence of an ethical choice, after that make an ethical determination, institute ethical intention, and eventually engage in moral behavior. In making ethical judgments, individuals formulate deontological and teleological evaluations concerning the ethical character of the act. Business ethical theories generally regard unethical behavior as harming others and consider ethical dilemma as when an individual is torn between a choice affecting the well-being, interests or prospects of others (Rest, 1986). Several scholars have developed models or guidelines of business ethics. Overall theoretical models suggested that ethical decision-making was influenced by personal, organizational and societal factors (Paolillo & Vitell, 2002).

13

The intensity of the actual ethical dilemma is one of important factors that alter individuals’ ethical decision (Jones, 1991). After analyzing previous research models, Jones (1991) put forward an “issue-contingent model” of ethical decision-making. He based his model on “the impact of moral intensity.” This moral intensity is the variation in response by individuals to different ethical issues according to the specific features of the issue, such as the severity of the issue. Jones (1991) defined moral intensity as being composed of six elements including “magnitude of consequences, social consensus, and probability of effect, temporal immediacy, proximity, and concentration of effect.” Moral intensity is increased if the results of the action create great harm or huge benefit either to the individual or to the “related others” (often called “stakeholders” in business jargon to refer to interested parties in the issue). An important concept of a “threshold effect of moral intensity” emerges from the study by Chia & Mee (2000). Their investigations confirm Jones’s theory that the moral characteristics or intensity of its consequences in any issue reveals differentiated stages of moral development. Different steps in this process are formed by the changing social consensus. For example, major consequences are more likely to be blamed on the lack of moral judgment of the decision-maker, while minor consequences often are blamed on those affected by the decision.

2.2 Moral intensity

According to Jones (1991, pp.374-378), moral intensity comprises the following six attributes:

Magnitude of consequences: Jones said that the importance of the consequences is the

"sum of the damage (or benefits) makes the victim (or beneficiary) of ethical behavior in question" (p. 374). One example he provided was an act causing death is a cause bigger consequences minor injury. Jones said that the inclusion of the extent of the consequences is a component of moral strength is not only common sense but also in line with empirical evidence. Two market research ethics review by Jones are in Fritzsche & Becker (1983) and Fritzsche (1988), the results showed a positive relationship between the magnitude of the consequences and ethical behavior. One of the recent studies, Vasquez-Párraga Hunt (1993) have shown that

14

the positive relationships between organizational consequences and moral decisions of a manager. High moral intensity will be recognized as ethical issues more often and will most likely result in a more virtuous intention or ethics.

Social consensus: According to Jones (p. 375), social consensus is "level of social

agreement that a proposed action is evil (or good)". Because "social consensus" is a rather vague term, most of them can be influenced by the extent to which the important people (eg, family, friends, others employees) agree "that a proposed action is evil (or good)". The interesting thing is, Hunt & Vitell (1986, 1993) defined "cultural norms" as a factor in the pattern of their marketing ethics. Although no detail has been given by them, cultural norms have been described as a structural impact on various aspects of decision making and ethical issues as perceived alternatives how ethical awareness. According to Jones, the logic is the reason why a social consensus is defined as a dimension of moral strength. As he explains "It is difficult to act ethically if a person does not know what good moral regulation in a situation, a high degree of social consensus reduces the ambiguity will existence "(p 375) Citing the work of Laczniak & Inderrieden (1987), Jones also defended its inclusion of social consensus with the empirical evidence. The following statement by Laczniak & Inderrieden (1987, p. 304) has been interpreted by Jones, "In order for individuals to respond appropriately to a given situation, the agreement must exist to be whether or not this is appropriate behavior. " Of course, this "agreed value" does not necessarily ensure that moral action will be taken in a given situation…

Probability impact: The probability of effect is defined as "a general function of the

probability that the action in question will actually occur and act in question would actually harm (benefits)" (Jones, p. 375). This size has the moral strength and Vitell matching Hunt (1986, 1993), who described "the probability of consequences" as part of the evaluation of a teleological individuals. In particular, citing the work of the day tons (1979), Hunt & Vitell said "a personal preference alternatives in situations with a moral content to be balanced against the possibility that the actions contribute to the achievement of personal goals "(p. 9). According to Jones, the inclusion of the dimension of moral strength is a matter of logic. In other words, as he illustrates, the magnitude of a moral action would be "discounted" if either its probability of harm or its probability is less than 1.00. Following to this concept and in line with the general

15

recommendations of the impact of moral strength, we believe that the probability of a negative result has a positive impact on the perception of a moral to market and of the intention of a marketer.

Temporal immediacy: Jones (p. 376) defines the instantaneous power is "the period

between the present and on the consequences of ethical behavior in question." Jones said that "people tend to discount the impact of events occurring in the future.... “The greater the interval, the greater the discount" (p. 376) According to Jones, this may be because people tend to realize that the greater the time between action and its consequences, is lower than the probability of the actions caused any harm.

Proximity: It is defined as "a feeling of closeness (social, cultural, psychological or

physical) that the moral agent with the victim (the beneficiary) of evil (good) actions in question asked "(p. 376). Jones asserted that "people care more about others, those close to them (social, cultural, psychological, or physical) than they do to those who are far off" (p. 376). Almost a factor of ethical decision-making in line with the moral model of Hunt & Vitell (1986, 1993), where "the importance of stakeholder" is defined as a structure affects the moral judgment of the marketer. Based on their evaluation of the work of Brenner & Molander (1977) and Zey-Ferrell, Weaver & Ferrell (1979), an important stakeholder groups the following is recorded: customers, shareholders, employees, colleagues, interfaces and management. Perceived importance of stakeholders is the focus of a study by Vitell & Singhapakdi (1991), who found that the strict implementation of the code of ethics in an organization can have a positive impact pole on the way marketers assess their importance. They also found that Machiavellians tend to place importance on personal preferences rather than on the interests of customers.

Concentration effects: Effective concentration is defined as "a function of the inverse of

the number of people affected by the actions of certain intensity" (Jones, 1991, p. 377). The concept of effective concentrations is consistent with the philosophy of utilitarianism normative ethics, which essentially said that "an action is right only when it creates for everyone a better balance better result than the negative consequences other available alternatives (for example, "the best for the greatest number ')" (Hunt & Vitell, 1986, p. 7). since the concentration of impacts extreme action means a "bad" for a large number of people or else it is "extremely bad"

16

for a few, then, according to a philosophy of pragmatism, it will be less than one ethical action does not have a high concentration of negative impact.

2.3 Demographic variables

Ethical and unethical conduct is the product of a complex combination of influences. At the center of the model is the individual decision maker. He or she has a unique combination of personality characteristics, values and moral principles, leaning toward or away from ethical behavior. In a review of empirical studies, researchers classified the variables that predict ethical attitudes and behavior as individual beliefs originating from: nationality, religion, gender, age, education, working experience; and situational factors that influence ethical belief and decision-making such as referent groups, rewards and sanctions, code of conduct, type of ethical conflict, organization effect, industry, and business competitiveness. Generally, these two categories can also be subdivided into three categories: personal/demographic, cultural, or economic factors (Ford & Richardson, 1994).

2.3.1 Gender

Gender differences in ethical perception and decision-making are consistent with a masculine success-orientation (males are more concerned with materials and success) and a female relationship-orientation (females are most interested in relationships and assisting people) (Franke, Crown & Spake 1997). Thorne (1999) investigated the association between demographic variables and the moral development of Canadian accounting students and compares it with American accounting students. The result was similar to U.S based findings and the moral development of the sample of Canadian accounting students is associated with both years of education and gender, with no significant association with age or audit experience.

Regarding the perception of ethical issues by male and female, Derry (1989) finds there is no significant difference between males and females in the moral reasoning of managers when involving work-related conflicts. However, Betz et al. (1989) found men are more likely to engage in actions regarded as unethical. Some studies have supported the findings that women take more ethical positions than men (Luthar, et al., 1997; Sims et al., 1996; Weeks et al., 1999).

17

Conversely McCuddy & Peery (1996) as well as McDonald & Kan (1997) found no significant correlation exists between ethical perception and gender.

In an empirical study of ethical judgment on selected accounting issues, Stanga & Turpen (1991) found no gender differences in ethical judgments. However, much of the existing research implies that female accountants and female accounting students tend to be more ethical than their male counterparts (Ameen, et al. 1996; Lampe & Finn, 1992; Shaub, 1994). Shaub’s (1994) found that there are no significant correlations between age and the levels of ethical reasoning in his subjects of auditors. Nevertheless, females were found to have higher ethical reasoning scores and female accounting students are less tolerant of unethical academic behaviors than their male counterpart.

Although the findings in the literature are mixed, the predominance of experiential evidence suggests that there are gender differences in ethical perceptions and attitudes (Franke, et al., 1997; Weeks, et al., 1999; Whipple and Swords, 1992). Sims et al. (1996) found that males were more likely to pirate software. Okleshen & Hoyt (1996) compared the ethical perception and decision-making of business students in the United States and New Zealand. They found that females are less tolerant of situations involving ethical dilemmas than their male counterparts. Luthar, DiBattista, & Gautschi (1997) examined ethical attitudes and perceptions of business students and found that female students exhibit more favorable attitude towards ethical behaviors than males.

2.3.2 Education background

Development of this sensitivity is important because ethical conflicts can occur “when accountants perceive that their duties toward one group are inconsistent with their duties and responsibilities toward some other group or their own self-interests” (Mintz 2007, 34). Shaub, Finn and Munter (1993) suggest that ethics education could improve ethical sensitivity by focusing on recognition skills.

Kohlberg (1981) theorizes that people who better understand complex and nuanced issues will display more sophisticated levels of moral reasoning. Grounded in this view, researchers

18

frequently hypothesize positive relationships between education and ethical judgment. Empirically, the evidence does not appear to support this view. Many studies fail to find a link between education and ethical judgments (Swaidan et al., 2003), while others report negative relationships (Chiu, 2003). Although these empirical results might seem contrary to Kohlberg's theory, they may actually support it. Higher levels of education might encourage people to more fully consider alternate perspectives or extenuating circumstances rather than judging complex ethical issues in narrow absolute terms. If so, a negative relationship between education and strictness of ethical judgments could be explained under Kohlberg

.

2.3.3 Working experience

As with other antecedents, contradictory empirical evidence exists among studies of work experience and ethical judgments. Chiu (2003) reports that work experience lessens the strictness of ethical judgments, while Kidwell et al. (1987) and Weeks et al. (1999) find that work experience leads to stricter ethical judgments. Some studies find the variables to be unrelated (e.g., Barnett and Valentine, 2004; Schepers, 2003). According to Hunt and Vitell (2007), socialization to workplace norms at least indirectly affect ethical judgments. If so, the more time spent in a job strengthens socialization outcomes. Unlike education, which may improve one's ability to apply ethical standards, workplace socialization may actually raise the ethical standards themselves. As such, more work experience could produce stricter ethical judgments.

2.3.4 Age

The literature suggests that age is a factor in determining ethical perception and decision-making. Johnson et al. (1986) found the older managers tend to place higher importance on trust and honor and allocate less importance to money and advancement, compared to younger executives. Arlow (1991) substantiated an inverse relationship between age and individual Machiavellian orientation. Nyaw & Ng (1994) found that older respondents were less tolerant of unethical behavior than younger ones. And also, in an investigation of expatriate and local managers in Hong Kong, McDonald & Kan (1997) found older employees are less likely to express agreement to an unethical action than younger employees. However, Borkowski & Ugras

19

(1992) suggest that college freshmen and juniors were more justice-oriented (fairness and equality) than MBAs, who tended to be more utilitarian when faced with ethical dilemmas. Additionally, based on self-reporting, Sims et al. (1996) found older students pirate software more frequently than younger students. Ruegger & King (1992) suggest that age is a determining factor in ethical decision-making and found age has correlated to good ethical attitudes. It is not certain whether it is age or practical experience associated with age in work place that causes individuals to change their ethical positions

20

Chapter 3: METHODOLOGY

3.1 Conceptual framework

A review of the existing literature concerning the impact of issue characteristics and demographic factors on the ethical decision-making process was presented in the previous chapters. These studies suggested many opportunities for further researches. Some of these issues will be investigated in the present study. The purpose of this study is to investigate the influence of the components of moral intensity (magnitude of consequences, social consensus, probability of effect, temporal immediacy, concentration of effect, and proximity) on the ethical decision process (moral recognition, moral judgment, and moral intentions) in accounting ethical dilemma. Additionally, demographic variables such as age, gender, education background and working experience are examined to how it affects moral intensity and its influence on the ethical decision-making process of accountant. Therefore, based on the earlier literature review and research questions, the null hypotheses of this study were developed as the followings:

H1: There is no significant difference between the perception of moral intensity and moral recognition of accountant under different accounting ethical issues.

H2: There is no significant difference between the perception of moral intensity and moral judgment of accountant under different accounting ethical issues.

H3: There is no significant difference between the perception of moral intensity and moral intention of accountant under different accounting ethical issues.

H4: There is no significant relationship between the perception of moral intensity and age. H5: There is no significant relationship between the perception of moral intensity and

21

H6: There is no significant relationship between the perception of moral intensity and education background.

H7: There is no significant relationship between the perception of moral intensity and working experience.

Figure3. 1: A model of accountant’ ethical decision process in accounting scenarios Adapted from Jones (1991) and Frey (2000)

22

3.2 Research design

The theoretical Framework of this study is shown on Figure3. 1. The research methodology will utilize four standardized scenarios taken from the Flory et al. (1991) study. The questions were adapted from the researches of Singhapakdi et. al (1996) and May & Pauli (2002). Scales developed by these types of research to measure the variables, such as moral recognition, moral judgment, moral intentions and the six dimensions of moral intensity (magnitude of consequences, social consensus, likelihood of effect, temporal immediacy, concentration of effect, and proximity), will be applied in this study. In addition, the subjects will be asked to respond to demographic questions regarding age, gender and education/work experience. This study is to measure the components of moral intensity and to examine its influence on ethical decision-making process of accountant in Vietnam.

3.3 Survey instrument

A questionnaire consisted of four scenarios, varying in moral intensity, each describing an ethical dilemma and a subsequent action to identify the moral perception of participants. Scenarios are commonly adopted in research instruments used in ethics studies in various fields (Bolliot et al., 2012; Lincoln & Holmes, 2011; Su, 2006). The use of scenarios is generally considered a good device of improving the quality of data from questionnaires. The scenarios were adapted from the study of Flory et al. (1992) to examine a multidimensional ethics scale. The similar survey instrument for accounting student has been adapted by the studies of Leitsch (2004) and Yang & Wu (2009). The questionnaire of this study contained four ethical scenarios and each scenario contained nine questions related to ethical variables (See Appendix 1).

The four ethical scenarios, in which the subjects were expected to perceive an unethical action, are discussed below:

The first scenario described a situation related to approving questionable expense reports. The ethical dilemma involved a threat to the job security of accountant in business organization. The respondents may or may not perceive this scenario as unethical action.

23

The second scenario described a situation related to manipulating company books. The ethical dilemma involved a threat to the integrity of the financial reporting. The respondents may or may not perceive earnings management in this scenario as unethical behavior.

The third scenario described a situation related to passing company policy. The ethical dilemma involved that the accountant had previously violated company policy and now decides to do it again. The respondents may or may not perceive this issue as unethical behavior.

The fourth scenario described a situation related to extending questionable credit. The ethical dilemma involved that a violation of company policy. The company policy is not clearly identified. Therefore, the respondents may or may not perceive this violation as unethical behavior.

3.4 Measurement

By quoting the description from the research of Yang & Wu (2009, pp.340-341), the measurement of ethical variables in each scenario was discussed below:

Moral recognition

According to the research of Singapakdi et al (1996), moral recognition, the first step of ethical decision making process, was assessed based on the degree to which respondents agreed with the following statement: “The situation involved an ethical problem”(item#1). The respondents revealed their level of agreement using a seven-point Likert-type scale (1=disagree strongly, 7= agree strongly).

Moral judgment

According to the research of May and Pauli (2002), moral judgment, the second step of ethical decision making process, was assessed based on the degree to which respondents agreed with the following statement: “He or she (the decision maker) in the above situation should do the proposed action” (item#2, reversed code). The respondents revealed their level of agreement using a seven-point Likert-type scale (1=disagree strongly, 7= agree strongly).

24 Moral intention

According to the research of Singapakdi et al, (1996), moral intention, the third step of ethical decision making process, was assessed based on the degree to which respondents agreed with the following statement:” I would act in the same manner as that of the decision-maker in the above scenario” (Item #3, reversed code) . The respondents revealed their level of agreement using a seven-point Likert-type scale (1=disagree strongly, 7= agree strongly).

Moral intensity

Based on Jones (1991) and adapted from previous research (Singapakdi et al, 1996, May & Pauli, 2002), the components of moral intensity were measured by following questions. The respondents revealed their level of agreement using a seven-point Likert-type scale (1=disagree strongly, 7= agree strongly).

The assessments of six dimensions of moral intensity are shown below:

Magnitude of Consequences: “The overall harm (if any) done as a result of (the decision-maker’s) decision would be very small” (Item# 4, reversed code).

Social Consensus: “Most people would agree that the (decision-maker’s) decision is wrong” (Item #5).

Probability of effect: “There is a very small likelihood that the (decision-maker’s) decision will actually cause any harm (Item #6, reversed code).

Temporal immediacy: “The (decision-maker’s) decision will not cause harm in the immediate future” (Item #7, reversed code).

Concentration of effect: “The (decision-maker’s) decision will harm few people (if any)” (Item #8, reversed code).

25

Demographics: This study also considers the personal characteristics such as age, gender, education background, and working experience.

There were several hypotheses that were developed to examine the research questions posed. The null and alternative hypotheses and statistical tests are summarized in Table 3.1

Table 1 . Hypotheses and Statistical Tests

Hypotheses Statistical Test

H10:

H1a:

There is no significant difference between the perception multivariate analysis of variance of moral intensity and moral recognition of accountant under different accounting ethical issues.

There is a significant difference between the perception of moral intensity and moral recognition of accountant based on different accounting ethical issues.

MANOVA with repeated measure

H20:

H2a:

There is no significant difference between the perception of multivariate analysis of variance moral intensity and moral judgment of accountant under different accounting ethical issues.

There is a significant difference between the perception of moral intensity and moral judgment of accountant under different accounting ethical issues. MANOVA with repeated measure H30: H3a:

There is no significant difference between the perception of multivariate analysis of variance moral intensity and moral intention of accountant based on different accounting ethical issues.

There is a significant difference between the perception of moral intensity and moral intention of accountant based on different

MANOVA with repeated measure

26 accounting ethical issues.

H40:

H4a:

There is no significant relationship between the perception of multivariate analysis of variance moral intensity and age.

There is a significant relationship between the perception of moral intensity and age.

MANOVA

H50:

H5a:

There is no significant relationship between the perception of multivariate analysis of variance moral intensity and gender.

There is a significant relationship between the perception of moral intensity and gender.

MANOVA

H60:

H6a:

There is no significant relationship between the perception of multivariate analysis of variance moral intensity and education background.

There is a significant relationship between the perception of moral intensity and education background.

MANOVA

H70:

H7a:

There is no significant relationship between the perception of multivariate analysis of variance moral intensity and working experience.

There is a significant relationship between the perception of moral intensity and working experience.

27

Chapter 4 RESULTS

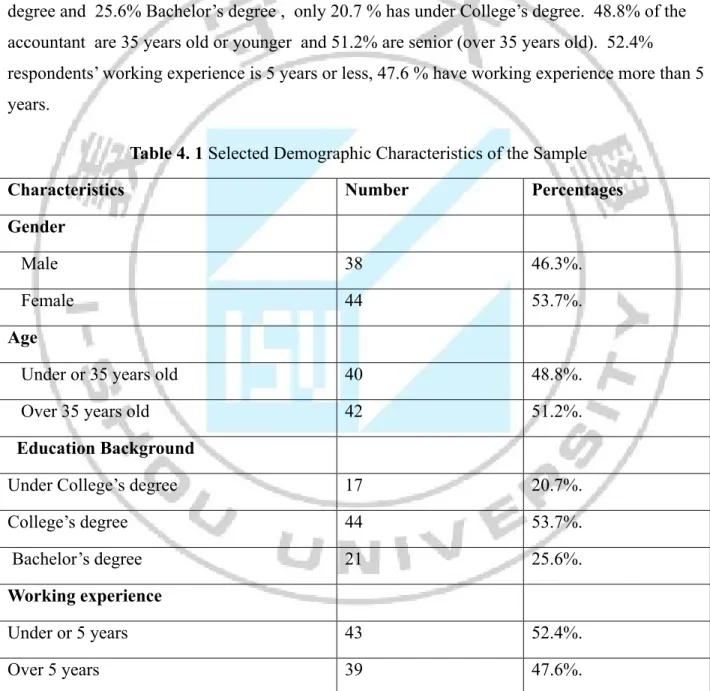

Total subjects of this research are 82 accountants in Vietnam . Table 4.1 showed there are 38 male participants represent 46.3%, 44 female participants represent for 53.7%. The result shows the accountant in Vietnam is well-educated, around 53.7% respondants has College’s degree and 25.6% Bachelor’s degree , only 20.7 % has under College’s degree. 48.8% of the accountant are 35 years old or younger and 51.2% are senior (over 35 years old). 52.4% respondents’ working experience is 5 years or less, 47.6 % have working experience more than 5 years.

Table 4. 1 Selected Demographic Characteristics of the Sample Characteristics Number Percentages Gender

Male 38 46.3%.

Female 44 53.7%.

Age

Under or 35 years old 40 48.8%.

Over 35 years old 42 51.2%.

Education Background

Under College’s degree 17 20.7%.

College’s degree 44 53.7%.

Bachelor’s degree 21 25.6%.

Working experience

Under or 5 years 43 52.4%.

28

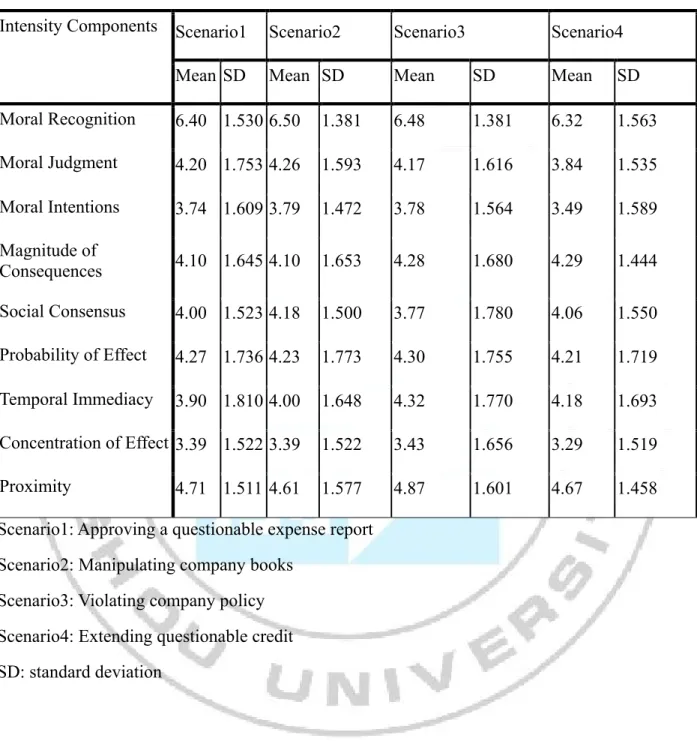

The moral intensity scale reliability was assessedusing Cronbach’s coefficient alpha, a common measure used to test the consistency among scales. The moral intensity components of this study were summed to yield a global alpha score of moral intensity ( ‘α=0.812). Table 4.2

presented the means and standard deviations of moral decision making process ( Moral Recognition , Moral Judgment, Moral Intentions ) and the components of moral intentions (Magnitude of Consequences, Social Consensus, Probability of Effect, Temporal Immediacy, Concentration of Effect, Proximity) by each scenario; Scenario 1 (approving questionable expense report), Scenario 2 (manipulating company books), Scenario 3 (violating company policy), Scenarios 4 (extending questionable credit). While the accountants perceived Scenario 2 (Manipulating company books) to be the most unethical action (m =6.50) they also recognized the ethical nature in the other scenarios, where neutral ratings = 4 (Table 4.2). Overall, the perceived moral intensity seemed to vary depending on the nature of the situation within the scenario. The result supported Jones (1991) theory that individuals tend to perceive some situations more '' morally intense '' than others.

The table 4.2 showed that the respondents were overall strongly agree about the situation involves an ethical problem at all scenarios, for example, the mean of moral recognition in each scenario is above 6; Scenario 1 (6.40), Scenario 2 (6.50), Scenario 3 (6.48), and Scenario 4 (6.32). Regarding to moral intentions, most accountants were disagreed about if they were the company controller, they would make the same decision. Last, the result showed that most accountants agree about that accountants’ decision will affect their co-workers (Proximity).

29

Table 4. 2 Means and Standard Deviation.

Intensity Components Scenario1 Scenario2 Scenario3 Scenario4

Mean SD Mean SD Mean SD Mean SD

Moral Recognition 6.40 1.530 6.50 1.381 6.48 1.381 6.32 1.563 Moral Judgment 4.20 1.753 4.26 1.593 4.17 1.616 3.84 1.535 Moral Intentions 3.74 1.609 3.79 1.472 3.78 1.564 3.49 1.589 Magnitude of Consequences 4.10 1.645 4.10 1.653 4.28 1.680 4.29 1.444 Social Consensus 4.00 1.523 4.18 1.500 3.77 1.780 4.06 1.550 Probability of Effect 4.27 1.736 4.23 1.773 4.30 1.755 4.21 1.719 Temporal Immediacy 3.90 1.810 4.00 1.648 4.32 1.770 4.18 1.693 Concentration of Effect 3.39 1.522 3.39 1.522 3.43 1.656 3.29 1.519 Proximity 4.71 1.511 4.61 1.577 4.87 1.601 4.67 1.458 Scenario1: Approving a questionable expense report

Scenario2: Manipulating company books Scenario3: Violating company policy Scenario4: Extending questionable credit SD: standard deviation

30

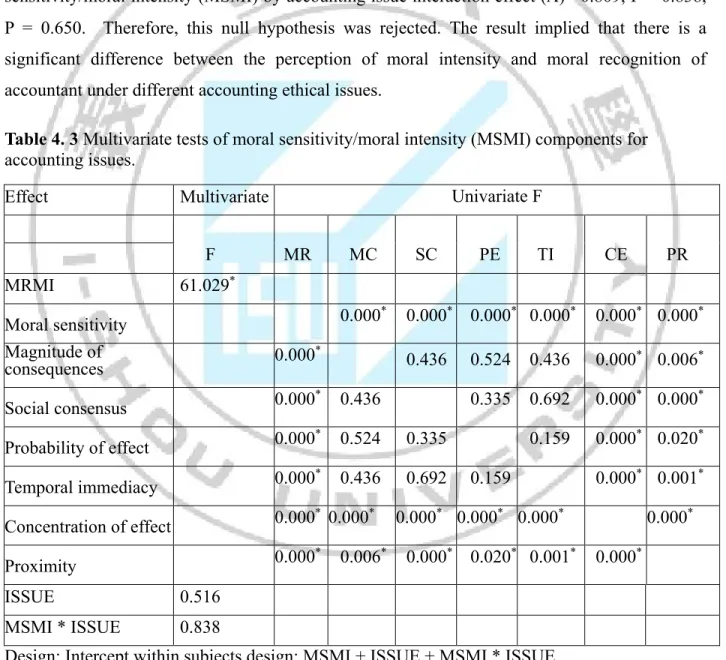

Null Hypothesis 1 addressed there is no significant difference between the perception of

moral intensity and moral recognition of accountant under different accounting ethical issues. A MANOVA with repeated measures on scenarios was conducted on all seven dependent variables. As the results shown on Table 4.3, the multivariate analysis revealed a significant moral recognition / moral intensity (MRMI) effect Wilks’ ()= 0.172 , F = 61,029 , p = 0,000, a accounting issue (ISSUE) main effect Wilks’ ()=0.981, F = 0.516, P = 0.672, and moral sensitivity/moral intensity (MSMI) by accounting issue interaction effect ()= 0.809, F = 0.838, P = 0.650. Therefore, this null hypothesis was rejected. The result implied that there is a significant difference between the perception of moral intensity and moral recognition of accountant under different accounting ethical issues.

Table 4. 3 Multivariate tests of moral sensitivity/moral intensity (MSMI) components for

accounting issues.

Effect Multivariate Univariate F

F MR MC SC PE TI CE PR MRMI 61.029* Moral sensitivity 0.000* 0.000* 0.000* 0.000* 0.000* 0.000* Magnitude of consequences 0.000* 0.436 0.524 0.436 0.000* 0.006* Social consensus 0.000* 0.436 0.335 0.692 0.000* 0.000* Probability of effect 0.000* 0.524 0.335 0.159 0.000* 0.020* Temporal immediacy 0.000* 0.436 0.692 0.159 0.000* 0.001* Concentration of effect 0.000* 0.000* 0.000* 0.000* 0.000* 0.000* Proximity 0.000* 0.006* 0.000* 0.020* 0.001* 0.000* ISSUE 0.516 MSMI * ISSUE 0.838

Design: Intercept within subjects design: MSMI + ISSUE + MSMI * ISSUE. * Statistically significant at 0.05 level.

31

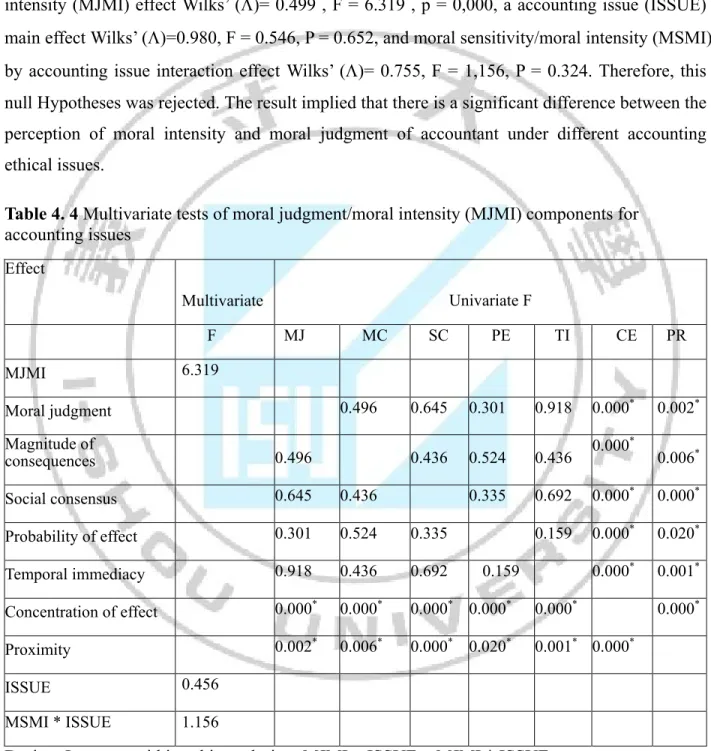

Null Hypothesis 2 addressed There is no significant difference between the perception of

moral intensity and moral judgment of accountant under different accounting ethical issues. A MANOVA with repeated measures on scenarios was conducted on all seven dependent variables. As shown on Table 4.4, the multivariate analysis revealed a significant moral sensitivity/ moral intensity (MJMI) effect Wilks’ ()= 0.499 , F = 6.319 , p = 0,000, a accounting issue (ISSUE) main effect Wilks’ ()=0.980, F = 0.546, P = 0.652, and moral sensitivity/moral intensity (MSMI) by accounting issue interaction effect Wilks’ ()= 0.755, F = 1,156, P = 0.324. Therefore, this null Hypotheses was rejected. The result implied that there is a significant difference between the perception of moral intensity and moral judgment of accountant under different accounting ethical issues.

Table 4. 4 Multivariate tests of moral judgment/moral intensity (MJMI) components for

accounting issues Effect Multivariate Univariate F F MJ MC SC PE TI CE PR MJMI 6.319 Moral judgment 0.496 0.645 0.301 0.918 0.000* 0.002* Magnitude of consequences 0.496 0.436 0.524 0.436 0.000 * 0.006* Social consensus 0.645 0.436 0.335 0.692 0.000* 0.000* Probability of effect 0.301 0.524 0.335 0.159 0.000* 0.020* Temporal immediacy 0.918 0.436 0.692 0.159 0.000* 0.001* Concentration of effect 0.000* 0.000* 0.000* 0.000* 0.000* 0.000* Proximity 0.002* 0.006* 0.000* 0.020* 0.001* 0.000* ISSUE 0.456 MSMI * ISSUE 1.156

Design: Intercept within subjects design: MJMI + ISSUE + MJMI * ISSUE. * Statistically significant at 0.05 level.

32

Null Hypothesis 3 addressed there is no significant difference between the perception of

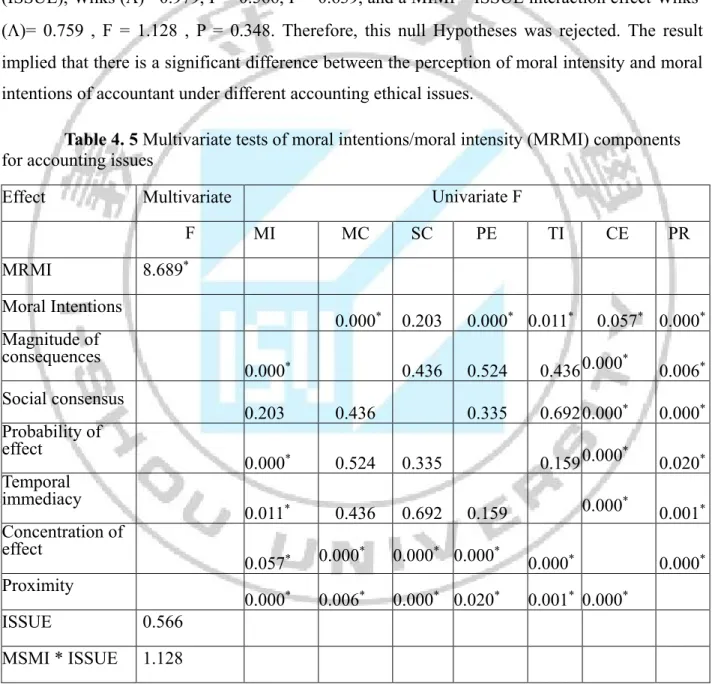

moral intensity and moral intention of accountant under different accounting ethical issues. A repeated measures MANOVA was also conducted on seven dependant variables. As shown on Table 4.5, the multivariate analysis revealed a significant moral intentions/components of moral intensity (MIMI) effect Wilks’ ()= 0.593, F = 8.689, P = 0.000, a accounting issue main effect (ISSUE), Wilks ()= 0.979, F = 0.566, P = 0.639, and a MIMI * ISSUE interaction effect Wilks’ ()= 0.759 , F = 1.128 , P = 0.348. Therefore, this null Hypotheses was rejected. The result implied that there is a significant difference between the perception of moral intensity and moral intentions of accountant under different accounting ethical issues.

Table 4. 5 Multivariate tests of moral intentions/moral intensity (MRMI) components

for accounting issues

Effect Multivariate Univariate F

F MI MC SC PE TI CE PR MRMI 8.689* Moral Intentions 0.000* 0.203 0.000* 0.011* 0.057* 0.000* Magnitude of consequences 0.000* 0.436 0.524 0.436 0.000* 0.006* Social consensus 0.203 0.436 0.335 0.692 0.000* 0.000* Probability of effect 0.000* 0.524 0.335 0.159 0.000* 0.020* Temporal immediacy 0.011* 0.436 0.692 0.159 0.000* 0.001* Concentration of effect 0.057* 0.000* 0.000* 0.000* 0.000* 0.000* Proximity 0.000* 0.006* 0.000* 0.020* 0.001* 0.000* ISSUE 0.566 MSMI * ISSUE 1.128

Design: Intercept within subjects design: MIMI + ISSUE + MIMI*ISSUE. * Statistically significant at 0.05 level.

33

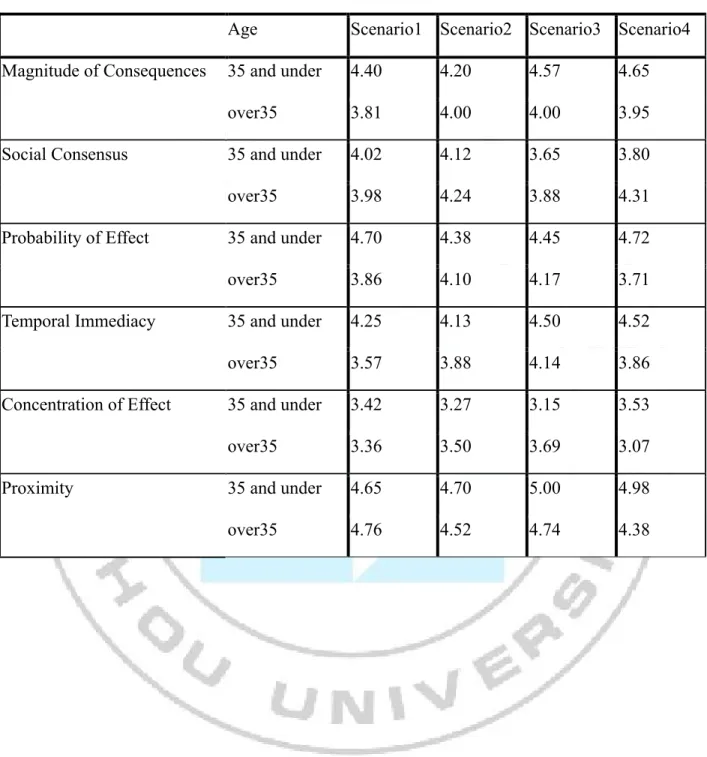

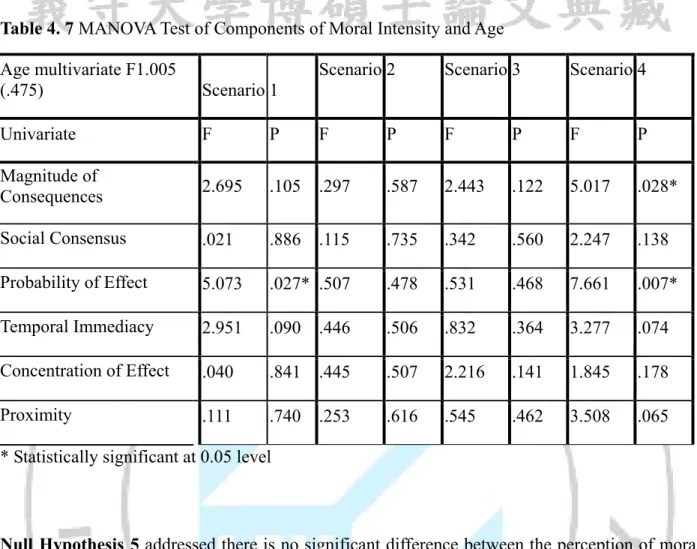

Null Hypothesis 4 addressed there is no significant difference between the perception of

moral intensity and age. A MANOVA was conducted to evaluate the relationship between age (Younger subjects under or 35 years old; Older subjects over 35 years old) and the perceived influence of the components of moral intensity (Magnitude of Consequences, Social Consensus, Probability of Effect, Temporal Immediacy, Concentration of Effect, Proximity). The independent variable was age and the dependent variable was each of the components of moral intensity by scenario. Table 4.7 showed the univariate result of magnitude of consequences for Scenario 4 (F = 5.017, p = .028) is significant. According to the means shown on Table 4.6, the result implied that the younger respondents (M=4.65) tend to disagree that the overall harm (if any) done as a result of accountants’ decision would be very small, compared to the older subjects (M=3.95). The univariate results of probability of effect for Scenario 1 (F = 5.073, p = .027) and Scenario 4 (F = 7.661, p = .007) are significant. The results implied that the younger respondents (M=4.70 or 4.72) tend to disagree that there is a very small likelihood that accountants’ decision will actually cause any harm, compared to the older subjects (M=3.86 or 3.71). However, the rest of components of moral intensity has F < 4 and p> .05, it means that rest of components of moral intensity is no significant with age. The multivariate result (F=1.005, P=.475) suggested no significant relationship between the perception of moral intensity and age. Therefore, this null Hypothesis was accepted.

34

Table 4. 6 Means of Age

Age Scenario1 Scenario2 Scenario3 Scenario4 Magnitude of Consequences 35 and under 4.40 4.20 4.57 4.65

over35 3.81 4.00 4.00 3.95

Social Consensus 35 and under 4.02 4.12 3.65 3.80

over35 3.98 4.24 3.88 4.31

Probability of Effect 35 and under 4.70 4.38 4.45 4.72

over35 3.86 4.10 4.17 3.71

Temporal Immediacy 35 and under 4.25 4.13 4.50 4.52

over35 3.57 3.88 4.14 3.86

Concentration of Effect 35 and under 3.42 3.27 3.15 3.53

over35 3.36 3.50 3.69 3.07

Proximity 35 and under 4.65 4.70 5.00 4.98

35

Table 4. 7 MANOVA Test of Components of Moral Intensity and Age

Age multivariate F1.005

(.475) Scenario 1 Scenario 2 Scenario 3 Scenario 4

Univariate F P F P F P F P Magnitude of Consequences 2.695 .105 .297 .587 2.443 .122 5.017 .028* Social Consensus .021 .886 .115 .735 .342 .560 2.247 .138 Probability of Effect 5.073 .027* .507 .478 .531 .468 7.661 .007* Temporal Immediacy 2.951 .090 .446 .506 .832 .364 3.277 .074 Concentration of Effect .040 .841 .445 .507 2.216 .141 1.845 .178 Proximity .111 .740 .253 .616 .545 .462 3.508 .065

* Statistically significant at 0.05 level

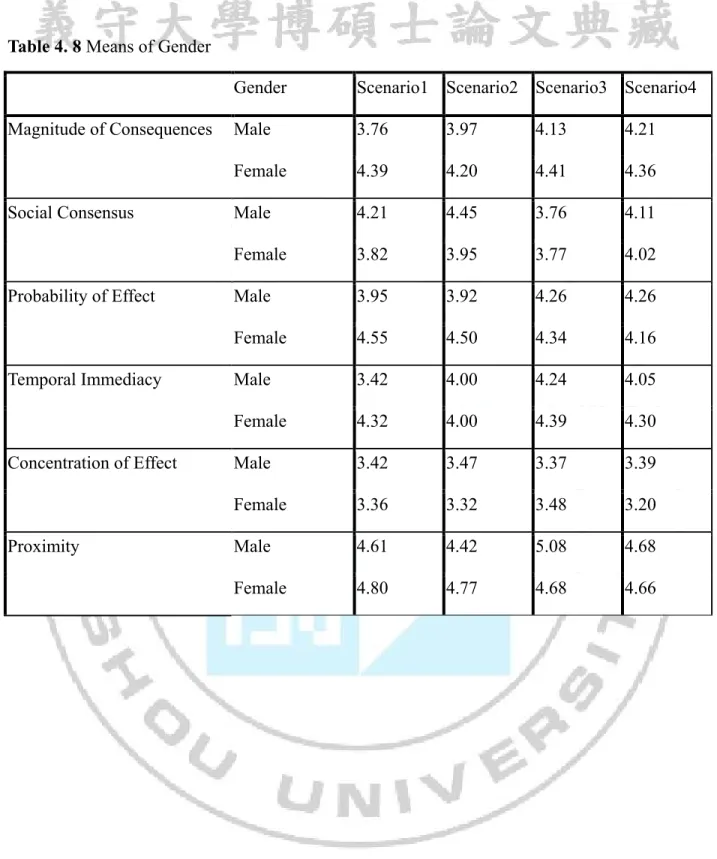

Null Hypothesis 5 addressed there is no significant difference between the perception of moral

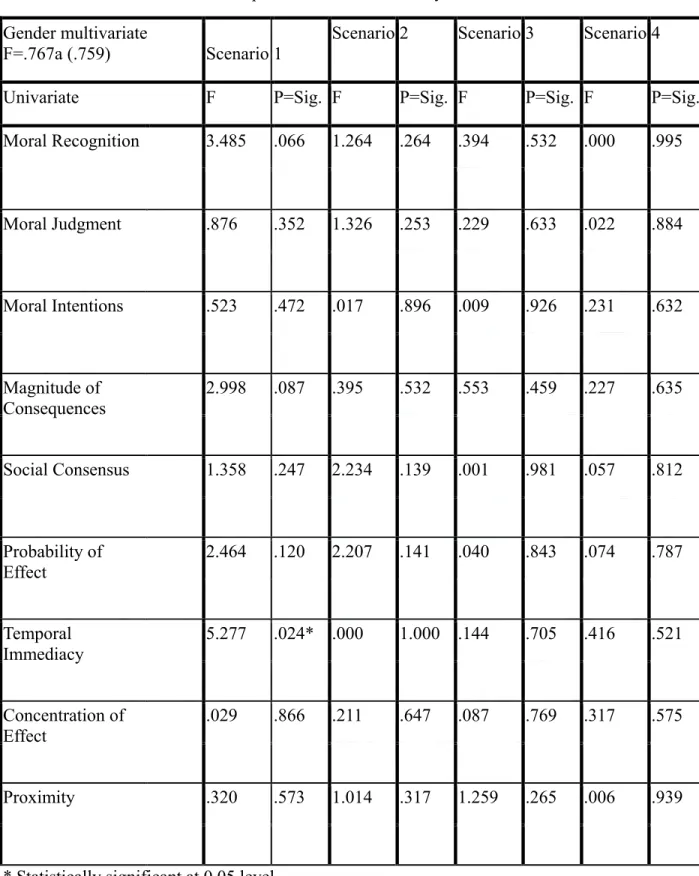

intensity and gender. A MANOVA was conducted to evaluate the relationship between gender (Male or Female) and the perceived influence of the components of moral intensity (Magnitude of Consequences, Social Consensus, Probability of Effect, Temporal Immediacy, Concentration of Effect, and Proximity). The independent variable was gender and the dependent variable was each of the components of moral intensity by scenario. Table 4.9 showed the univariate result of temporal immediacy for Scenario 1 (F = 5.277, p = .024) is significant. According to the means shown on Table 4.8, the result suggested that the male respondents (M=3.42) tend to agree that accountants’ decision will not cause harm in the immediate future, compared to the female subjects (M=4.32). However, the rest of components of moral intensity has F < 4 and p> .05, it means that rest of components of moral intensity is no significant with gender. The multivariate result (F=.767, P=.759) suggested no significant relationship between the perception of moral intensity and gender. Therefore, this null Hypothesis was accepted.

36

Table 4. 8 Means of Gender

Gender Scenario1 Scenario2 Scenario3 Scenario4

Magnitude of Consequences Male 3.76 3.97 4.13 4.21

Female 4.39 4.20 4.41 4.36

Social Consensus Male 4.21 4.45 3.76 4.11

Female 3.82 3.95 3.77 4.02

Probability of Effect Male 3.95 3.92 4.26 4.26

Female 4.55 4.50 4.34 4.16

Temporal Immediacy Male 3.42 4.00 4.24 4.05

Female 4.32 4.00 4.39 4.30

Concentration of Effect Male 3.42 3.47 3.37 3.39

Female 3.36 3.32 3.48 3.20

Proximity Male 4.61 4.42 5.08 4.68

37

Table 4. 9 MANOVA Test of Components of Moral Intensity and Gender

Gender multivariate

F=.767a (.759) Scenario 1 Scenario 2 Scenario 3 Scenario 4

Univariate F P=Sig. F P=Sig. F P=Sig. F P=Sig.

Moral Recognition 3.485 .066 1.264 .264 .394 .532 .000 .995 Moral Judgment .876 .352 1.326 .253 .229 .633 .022 .884 Moral Intentions .523 .472 .017 .896 .009 .926 .231 .632 Magnitude of Consequences 2.998 .087 .395 .532 .553 .459 .227 .635 Social Consensus 1.358 .247 2.234 .139 .001 .981 .057 .812 Probability of Effect 2.464 .120 2.207 .141 .040 .843 .074 .787 Temporal Immediacy 5.277 .024* .000 1.000 .144 .705 .416 .521 Concentration of Effect .029 .866 .211 .647 .087 .769 .317 .575 Proximity .320 .573 1.014 .317 1.259 .265 .006 .939

38

Null Hypothesis 6 addressed there is no significant difference between the perception of

moral intensity and education background. A MANOVA was conducted to evaluate the relationship between education background (Under College’s degree, College’s degree and Bachelor’s degree) and the perceived influence of the components of moral intensity (Magnitude of Consequences, Social Consensus, Probability of Effect, Temporal Immediacy, Concentration of Effect, Proximity). The independent variable was education background and the dependent variable was each of the components of moral intensity by scenario. Table 4.11 showed the multivariate result (F=1.474, P=.041) suggested a significant relationship between the perception of moral intensity and education background. Therefore, this null Hypothesis was rejected and the significant differences were noted. The components of moral intensity were considered for further examination. The univariate results shown on Table 4.11 indicated that there is significant difference between the perception of moral intensity (social consensus, probability of effect) and education background. In particular, a pair wise comparison was conducted to note the significant differences between subjects with different education background found on Table 4.12.

The univariate result of social consensus for Scenario 2 (F = 4.212, P = .018) is significant. The results of pairwise comparison shown on table 4.12 revealed there is significant difference between the subjects with under college’s degree and the subjects with college’s degree in the component of moral intensity (social consensus) (Scenario 2, P = .005). Based on the means shown on Table 4.10, the finding implied that the subjects with under college’s degree (M=5.06) tend to agree that most people would agree that accountant’s decision is wrong, compared to the subjects with college’s degree (M=3.86).

The univariate results of probability of effect for Scenario 2 ( F=3.257, p=.044), Scenario 3 ( F=3.659, =.030) and Scenario 4 (F=4.136, p=.020) are significant. The results of pairwise comparison revealed there is significant difference between the subjects with under college’s degree and the subjects with bachelor’s degree in the component of moral intensity (probability of effect) for all scenarios (Scenario 1, P = .037) (Scenario 2, P = .013) (Scenario 3, P = .011) (Scenario 4, P = .016). The results implied that the subjects with under college’s degree (M=3.53 or 3.47 or 3.65 or 3.76) tend to agree that there is a very small likelihood that accountant’s

39

decision will actually cause any harm, compared to the subjects with bachelor’s degree (M=4.71 or 4.9 or 5.10). In addition, the results of pair wise comparison also showed there is significant difference between the subjects with college’s degree and the subjects with bachelor’s degree in the component of moral intensity (probability of effect) for Scenario 3 (P = .046) and Scenario 4 (P = .011). The results implied that the subjects with college’s degree (M=4.18 or 3.59) tend to agree that there is a very small likelihood that accountant’s decision will actually cause any harm, compared to the subjects with bachelor’s degree (M= 5.10).

In particular, the results of pair wise comparison revealed there is significant difference between the subjects with under college’s degree and the subjects with bachelor’s degree in the component of moral intensity (temporal immediacy) for Scenario 2 ( P = .043) and Scenario 4 ( P = .027). The results implied that the subjects with under college’s degree (M=3.29 or 3.59) tend to agree that accountant’s decision will not cause harm in the immediate future, compared to the subjects with bachelor’s degree (M=4.38 or 4.81).

Table 4. 10 Means of Education

Education Scenario1 Scenario2 Scenario3 Scenario4 Magnitude of Consequences Under College’s

degree 4.06 3.82 3.71 3.94

College’s degree 4.18 4.02 4.41 4.27 Bachelor’s degree 3.95 4.48 4.48 4.62 Social Consensus Under College’s

degree 4.59 5.06 4.18 4.47

College’s degree 3.86 3.86 3.93 4.16 Bachelor’s degree 3.81 4.14 3.10 3.52 Probability of Effect Under College’s

degree 3.53 3.47 3.65 3.76

40

Bachelor’s degree 4.71 4.90 5.10 5.10 Temporal Immediacy Under College’s

degree 3.24 3.29 3.88 3.59

College’s degree 4.16 4.09 4.32 4.11 Bachelor’s degree 3.90 4.38 4.67 4.81 Concentration of Effect Under College’s

degree 3.59 3.47 2.82 3.71

College’s degree 3.23 3.43 3.68 3.36 Bachelor’s degree 3.57 3.24 3.38 2.81

Proximity Under College’s

degree 4.35 4.53 4.53 4.59

College’s degree 4.77 4.52 4.73 4.55 Bachelor’s degree 4.86 4.86 5.43 5.00

Table 4. 11 MANOVA Test of Components of Moral Intensity and Education

Education multivariate

F=1.474 (.041)* Scenario 1 Scenario 2 Scenario 3 Scenario 4

Univariate F P. F P F P F P Magnitude of Consequences .141 .869 .826 .441 1.275 .285 1.045 .357 Social Consensus 1.633 .202 4.212 .018* 2.197 .118 1.989 .144 Probability of Effect 2.347 .102 3.257 .044* 3.659 .030* 4.136 .020* Temporal 1.623 .204 2.255 .112 .921 .403 2.624 .079

41 Immediacy

Concentration of

Effect .539 .585 .142 .868 1.686 .192 1.772 .177

Proximity .606 .548 .342 .712 1.878 .160 .720 .490

* Statistically significant at 0.05 level.

Table 4. 12 Pair wise Comparisons of Components of Moral Intensity and Education

Dependent

Variable (I) Education (J) Education Scenario 1

Scenario

2 Scenario 3 Scenario 4 Magnitude of

Consequences Under College’s degree College’s degree .796 .675 .145 .424 Bachelor’s

degree .845 .231 .162 .154

College’s degree Under College’s

degree .796 .675 .145 .424

Bachelor’s

degree .604 .305 .880 .368

Bachelor’s degree Under College’s

degree .845 .231 .162 .154

College’s

degree .604 .305 .880 .368

Social

Consensus Under College’s degree College’s degree .097 .005* .627 .478 Bachelor’s

42 College’s degree Under

College’s

degree .097 .005 .627 .478

Bachelor’s

degree .893 .468 .076 .122

Bachelor’s degree Under College’s

degree .118 .055 .063 .062

College’s

degree .893 .468 .076 .122

Probability of

Effect Under College’s degree College’s degree .100 .140 .274 .689 Bachelor’s

degree .037* .013* .011* .016*

College’s degree Under College’s

degree .100 .140 .274 .689

Bachelor’s

degree .412 .130 .046 .011

Bachelor’s degree Under College’s

degree .037* .013* .011* .016*

College’s

degree .412 .130 .046 .011*

Temporal

Immediacy Under College’s degree College’s degree .075 .090 .392 .271 Bachelor’s

degree .257 .043* .179 .027*

College’s degree Under College’s

43 Bachelor’s

degree .595 .502 .461 .118

Bachelor’s degree Under College’s

degree .257 .043 .179 .027

College’s

degree .595 .502 .461 .118

Concentration of

Effect Under College’s degree College’s degree .411 .930 .071 .428 Bachelor’s

degree .973 .644 .301 .072

College’s degree Under College’s

degree .411 .930 .071 .428

Bachelor’s

degree .399 .636 .492 .169

Bachelor’s degree Under College’s

degree .973 .644 .301 .072

College’s

degree .399 .636 .492 .169

Proximity Under College’s

degree College’s degree .336 .988 .663 .919 Bachelor’s

degree .312 .529 .086 .391

College’s degree Under College’s

degree .336 .988 .663 .919

Bachelor’s

44 Bachelor’s degree Under

College’s

degree .312 .529 .086 .391

College’s

degree .835 .430 .099 .245

* Statistically significant at 0.05 level.

Null Hypothesis 7 addressed there is no significant difference between the perception of

moral intensity and working experience. A MANOVA was conducted to evaluate the relationship between working experience (under or 5 years; over 5 years) and the perceived influence of the components of moral intensity (Magnitude of Consequences, Social Consensus, Probability of Effect, Temporal Immediacy, Concentration of Effect, Proximity). The independent variable was working experience and the dependent variable was each of the components of moral intensity by scenario. Table 4.14 showed the univariate result of magnitude of consequences for Scenario 1 (F = 4.720, p = .033), Scenario 3 ( F=10.149, p=.002) and Scenario 4 (F=4.395, p=.039) are significant. According to the means shown on Table 4.13, the result implied that the respondents with working experience under or 5 years (M=4.47 or 4.81 or 4.20) tend to disagree that the overall harm (if any) done as a result of accountants’ decision would be very small, compared to the subjects with working experience over 5 years (M=3.69 or 3.95).

In addition, the univariate results of probability of effect for Scenario 4 ( F=9.768 p=.002) is significant. The results implied that the respondents with working experience under or 5 years (M=4.74) tend to disagree that there is a very small likelihood that accountants’ decision will actually cause any harm, compared to the subjects with working experience over 5 years (M=3.62). The univariate results of proximity for Scenario 4 (F=6.410, P=.013) is significant. The results implied that the respondents with working experience under or 5 years (M=5.05) tend to agree that accountants’ decision will affect his co-workers, compared to the subjects with working experience over 5 years (M=4.26). However, the rest of components of moral intensity has F < 4 and p> .05, it means that rest of components of moral intensity is no significant with working experience. The multivariate result (F=1.535, P=.094) suggested no significant relationship between the perception of moral intensity and working experience. Therefore, this null hypothesis was accepted.

45

Table 4. 13 Means of Working experience

Working experience Scenario1 Scenario2 Scenario3 Scenario4 Magnitude of

Consequences 5years and under 4.47 4.42 4.81 4.60

over5years 3.69 3.74 3.69 3.95

Social Consensus 5years and under 3.93 4.02 3.49 4.02

over5years 4.08 4.36 4.08 4.10

Probability of Effect 5years and under 4.58 4.51 4.51 4.74

over5years 3.92 3.92 4.08 3.62

Temporal Immediacy 5years and under 4.26 4.19 4.58 4.49

over5years 3.51 3.79 4.03 3.85

Concentration of Effect 5years and under 3.51 3.26 3.19 3.30

over5years 3.26 3.54 3.69 3.28

Proximity 5years and under 4.65 4.67 4.88 5.05

over5years 4.77 4.54 4.85 4.26

Table 4. 14 MANOVA Test of Components of Moral Intensity and Working experience

Working experience F=

1.535a (.094) Scenario 1 Scenario 2 Scenario 3 Scenario 4

Univariate F P F P F P F P

Magnitude of

46 Social Consensus .188 .666 1.025 .314 2.271 .136 .053 .819 Probability of Effect 3.014 .086 2.290 .134 1.259 .265 9.768 .002* Temporal Immediacy 3.557 .063 1.154 .286 2.042 .157 3.015 .086 Concentration of Effect .572 .452 .703 .404 1.934 .168 .004 .952 Proximity .123 .726 .150 .699 .011 .916 6.410 .013*

* Statistically significant at 0.05 level.

Summary of the findings

The results of this study supported the finding of Leitsch (2004) that the perception of moral intensity and the specific stages of the ethical decision-making process were affected by ethical issue. In addition, the result showed significant differences in the responses to the characteristics of ethical dilemmas (probability of effect) exist with respect to demographic variables such as education background. The findings suggested that the accountant with lower education background tend to agree that there is a very small likelihood that unethical decision will actually cause any harm, compared to the accountant with higher education background.

For further examination, this study found there was a significant difference with respect to working experience in the perceptions of moral intensity (magnitude of consequences). The result implied that accountant with short term working experience tend to disagree that the overall harm (if any) done as a result of unethical decision would be very small, compared to accountant with long term working experience. Also, this study found there was a significant difference with respect to age in the perceptions of moral intensity (magnitude of consequences probability of effect). The results implied that older accountants tend to agree unethical decision in the situation like Scenario 4 (extending questionable credit), compared to the younger ones. Finally, there was a significant difference with respect to gender in the perceptions of moral intensity (temporal immediacy). The finding suggested that the male accountants tend to agree

47

that unethical decision will not cause harm in the immediate future in the situation like Scenario 1 (approving questionable expense report), compared to the female accountants.

The results of this study suggested that the particular characteristics of ethical dilemmas influence accounting professionals’ ability to recognize, judge, and their intentions in regards to the ethical nature of accounting issues. The results also implied that accountants with higher education background tend to make ethical decision. The finding of this research that the male accountants tended to agree unethical decision is consistent with the implication of previous study (Shaub, 1994). While, the research found the younger accountants or accountants with short term working experience tended to be easier to perceive the unethical situation, which is not similar with the implication of the study of Su (2006).

Table 4. 15 Summary of the findings

Null Hypotheses The results

H10: There is no significant difference between the perception of moral

intensity and moral recognition of accountant under different accounting ethical issues.

Rejected

H20: There is no significant difference between the perception of moral

intensity and moral judgment of accountant under different accounting ethical issues.

Rejected

H30: There is no significant difference between the perception of moral

intensity and moral intention of accountant under different accounting ethical issues.

Rejected

H40: There is no significant relationship between the perception of moral

intensity and age. Accepted

H50: There is no significant relationship between the perception of moral

48

H60: There is no significant relationship between the perception of moral

intensity and education background. Rejected

H70: There is no significant relationship between the perception of moral