Firm Maturity and the Pecking Order Theory

22

0

0

全文

(2) 180. International Journal of Business and Economics. how much investment a firm may need and profitability reflects to what extent these investment needs can be funded internally. Life cycle stages encompass variation in a firm’s level of knowledge acquisition (about industry structure and cost structure), level of initial investment and re-investment of capital, and adaptability to the competitive environment (Gort and Klepper, 1982). Accordingly, partitioning firms according to their life cycle stage predictably provides differential information about what determines profitability and growth. Dickinson (2009) demonstrates that firm life cycle affects profitability and growth, both cross-sectionally and over time. Anthony and Ramesh (1992) find empirically that stock market reactions to growth and capital expenditure are functions of the life cycle stage. In a direct study of financial life cycle of small private businesses, Berger and Udell (1998) find that firms rely more on debt financing as firms grow from “infancy” to “adolescence,” but use less debt as firms become “middle-aged” and “old.” They also report that on average, “smaller” firms have more equity, most of which comes from principal owners, and “larger” firms have more debt through bank loans and trade credit. This paper complements Berger and Udell’s (1998) work by investigating the financial life cycle of public firms. In this paper, we study two major life cycle stages, namely, growth and maturity. We then focus on the pecking order theory of financing proposed by Myers (1984) and Myers and Majluf (1984). This theory is based on the information asymmetry between investors and firm managers. Due to the valuation discount that less informed investors apply to newly issued securities, firms resort to internal funds first, then debt, and equity last to satisfy their financing needs. The empirical evidence for the pecking order theory has been mixed. ShyamSunder and Myers (1999) propose a direct test of the pecking order and find strong support for the theory among a sample of large firms. Frank and Goyal (2003) argue that the Shyam-Sunder and Myers test rejects the pecking order for small public firms. They conclude that this finding is in contrast to the theory since small firms are thought to suffer most from asymmetric information problems and, hence, should be the ones following the pecking order. More recent work by Lemmon and Zender (2010) and Agca and Mozumdar (2007) show that the Shyam-Sunder and Myers test does not account for a firm’s debt capacity, a constraint that is particularly binding for small firms. Once debt capacity constraints are accounted for, they find that the pecking order performs well even for small firms. Leary and Roberts (2010) use a different approach and estimate a two-rung empirical model. They find the pecking order performs poorly for a broad sample of firms. Using a life cycle stage classification, this paper differentiates between a size effect and a maturity effect. Although there is a positive correlation between firm size and maturity, it is important to make the distinction between large and mature as well as young and small. The size effect was first documented by Frank and Goyal (2003), who find that large firms fit the pecking order theory better than small firms. We find that this size effect only weakly exists among firms in their growth stage. For firms in their maturity stage, this size effect is not significant. When controlling for a firm’s debt capacity, this size effect disappears altogether for firms.

(3) Laarni Bulan and Zhipeng Yan. 181. in either stage, while a maturity effect remains. That is, more mature firms fit the pecking order better than younger firms after firm size is controlled for. Overall, we find that the pecking order theory describes the financing patterns of mature firms better than young firms. Using a logit regression, we find that the probability of being a mature firm is highly correlated with the probability of having publicly rated debt. The latter is used as a proxy for debt capacity in Lemmon and Zender (2010). Our findings show that firm maturity is an alternative proxy for debt capacity that captures more than just access to public debt markets. In particular, mature firms are older, more stable, and highly profitable with good credit histories. Thus, they naturally have greater debt capacity than growth firms. Their good credit histories also allow them to borrow significantly from private financial intermediaries, which in some cases may preclude the need to access public debt markets. In fact, we find that mature firms have ample unused debt capacity even when they have relatively high leverage. This indicates that firm maturity is arguably a better proxy for debt capacity than access to public debt. In sum, after controlling for firm maturity, the pecking order theory describes the financing behavior of firms, large or small, fairly well. This paper is organized as follows. Section 2 describes the data and sample selection. In Section 3, we present our results. Robustness checks are performed in Section 4, while Section 5 concludes. 2. Data We construct two samples of firms according to their life cycle stage: firms in their growth stage and firms in their maturity stage. Life cycle stages are naturally linked to firm age. Age is an important factor, but it is not the sole determinant of a firm’s life cycle stage. Firm life cycles vary widely across industries (Black, 1998) and within the same industry. Several studies in management and accounting show that firm life cycle is not a linear function of firm age, and life cycle stages are by no means necessarily connected to each other in a deterministic sequence. Miller and Friesen (1984) identify five life cycle stages: birth, growth, maturity, revival, and decline. They find that firms over lengthy periods often fail to exhibit the common life cycle progression extending from birth to decline. That is, the maturity stage may be followed by decline, revival, or even growth; revival may precede or follow decline and so on. Liu (2008) classifies firms into five life cycle stages using multivariate ranking procedures and finds that about 16% of mature firms move back to growth stages from the current year to the next. Motivated by these studies, we focus on a snapshot of a firm’s history where growth and maturity is more easily determined. We define the growth stage to be the first six-year period after the year of the firm’s IPO and the maturity stage to be a consecutive six-year period following a dividend initiation where a firm maintains positive dividends. Miller and Friesen (1984) find that, on average, each stage lasts for six years. Evans (1987) defines firms six years old or younger as young firms and firms seven years or older as old firms. Accordingly, we set the length of each.

(4) 182. International Journal of Business and Economics. stage to be six years. We find similar results using 4, 8, and 10 years for the stage length. Following standard practice, we exclude financial firms (SIC codes 60006999) and regulated utilities (SIC codes 4900-4999) and consider only firms that have securities with CRSP share codes 10 or 11. 2.1 Growth Stage Our sample is constructed from the universe of firms in the CRSP-Compustat merged database over the 1970–2008 period. We define the growth stage to be the first six-year period after the year of the firm’s IPO. This definition may not necessarily apply to some firms from a mechanical point of view. For example, Metro-Goldwyn-Mayer Inc., a movie production firm, was founded in 1930 and went public in 1997. It is “old” and mature in many respects. However, the IPO is itself an important financing decision that a firm has to make and, in many cases, indicates a significant change in the firm’s development over its life cycle. Here, we treat the IPO as an important turning point in a firm’s history and as the starting point of the growth stage. We use flow of funds data to test the pecking order theory. IPO dates are provided by Jay Ritter from 1970 to 1974. IPO dates between 1975 and 2002 are obtained from Loughran and Ritter (2008). When the IPO date is not available, we use the earliest date for which we observe a non-zero and non-missing stock price on the CRSP monthly tapes. 2.2 Maturity Stage DeAngelo et al. (2006), among others, have found that a firm’s propensity to pay dividends is a function of its life cycle stage. Bulan et al. (2007) find that firms that initiate dividends are older and highly profitable, have fewer growth opportunities, and are less risky, i.e., they are more mature. Based on these studies, we identify firms in their maturity stage by their dividend initiation history. We first use the entire Compustat industrial annual database to identify consecutive six-year periods that a firm has positive dividends. We require that such a period should immediately follow at least one year with zero or missing dividends. This is similar to Baker and Wurgler’s (2004) definition of dividend initiations. If a firm issues dividends during the first six years after IPO, we exclude this firm from the sample altogether, i.e., a firm cannot be in both growth and maturity stages at the same time. 2.3 Firm Characteristics and Comparison of Growth and Maturity Stages We construct the following variables for our analysis: book leverage, market leverage, net equity issued, net debt issued, financing deficit, tangibility, profitability, retained earnings-to-total equity ratio, R&D, and capital expenditures. We also measure a firm’s age as years from birth, where birth is the earliest year from which we have a non-missing observation among three datasets: Jay Ritter’s incorporation dataset, Compustat, and CRSP. Following Frank and Goyal (2003), we exclude firms with missing book value of assets, firms involved in major.

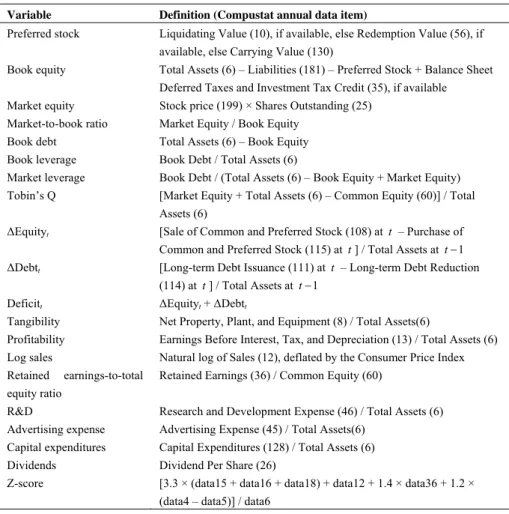

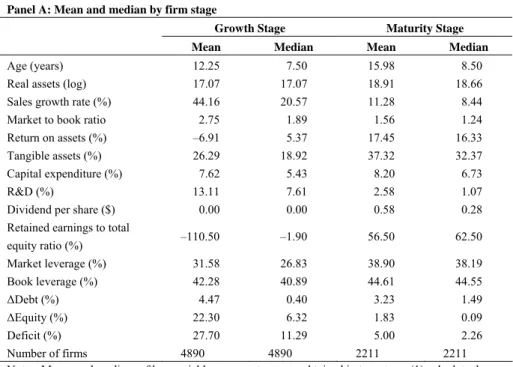

(5) Laarni Bulan and Zhipeng Yan. 183. mergers (Compustat footnote 1 with value = AB) and a small number of firms that reported format codes (data318) 4, 5, or 6. To reduce the impact of outliers and the most extremely mis-recorded data, all variables are truncated at the top and bottom 0.5 percentiles. Table 1 explains the construction of these variables in detail. Table 1. Key Variable Definitions Variable. Definition (Compustat annual data item). Preferred stock. Liquidating Value (10), if available, else Redemption Value (56), if available, else Carrying Value (130). Book equity. Total Assets (6) – Liabilities (181) – Preferred Stock + Balance Sheet Deferred Taxes and Investment Tax Credit (35), if available. Market equity. Stock price (199) × Shares Outstanding (25). Market-to-book ratio. Market Equity / Book Equity. Book debt. Total Assets (6) – Book Equity. Book leverage. Book Debt / Total Assets (6). Market leverage. Book Debt / (Total Assets (6) – Book Equity + Market Equity). Tobin’s Q. [Market Equity + Total Assets (6) – Common Equity (60)] / Total Assets (6). ΔEquityt. [Sale of Common and Preferred Stock (108) at t – Purchase of Common and Preferred Stock (115) at t ] / Total Assets at t − 1. ΔDebtt. [Long-term Debt Issuance (111) at t – Long-term Debt Reduction (114) at t ] / Total Assets at t − 1. Deficitt. ΔEquityt + ΔDebtt. Tangibility. Net Property, Plant, and Equipment (8) / Total Assets(6). Profitability. Earnings Before Interest, Tax, and Depreciation (13) / Total Assets (6). Log sales Retained. Natural log of Sales (12), deflated by the Consumer Price Index earnings-to-total. Retained Earnings (36) / Common Equity (60). equity ratio R&D. Research and Development Expense (46) / Total Assets (6). Advertising expense. Advertising Expense (45) / Total Assets(6). Capital expenditures. Capital Expenditures (128) / Total Assets (6). Dividends. Dividend Per Share (26). Z-score. [3.3 × (data15 + data16 + data18) + data12 + 1.4 × data36 + 1.2 × (data4 – data5)] / data6. Panel A of Table 2 provides descriptive statistics for each life cycle stage. The sample selection methodology outlined above results in 4,890 growth firms and 2,211 mature firms. Some interesting patterns emerge. On average, firms in their maturity stage are older, larger, and more profitable than firms in their growth stage. The median firm in the maturity stage is a year older and more than four times larger than the median firm in the growth stage. In terms of profitability, the median ROA (return on assets) for mature firms is 16.33%, while for growth firms it is 5.37%. On the other hand, growth firms experience much more rapid sales growth (more than twice that of mature firms) and higher market-to-book ratios, implying that growth.

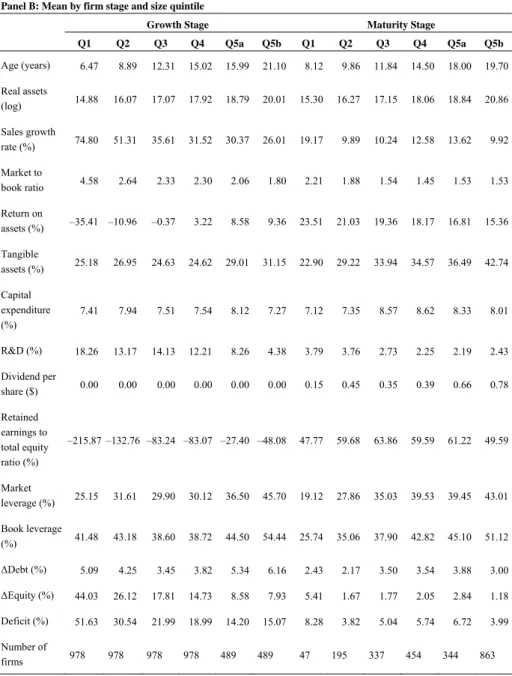

(6) 184. International Journal of Business and Economics. firms have more growth opportunities. These differences are highly significant. The table also shows that R&D expenditure for growth firms is much larger than for mature firms (six times larger), but that capital expenditure is higher for mature firms. This is also consistent with the latter having higher tangible assets. Overall, these patterns conform to our expectations of key firm attributes in these two stages of a firm’s life cycle. In terms of financing characteristics, we see that growth firms have larger financing deficits, and they rely more heavily on equity financing rather than debt, consistent with prior work. Table 2. Summary Statistics Panel A: Mean and median by firm stage Growth Stage. Maturity Stage. Mean. Median. Mean. Age (years). 12.25. 7.50. 15.98. 8.50. Real assets (log). 17.07. 17.07. 18.91. 18.66. Sales growth rate (%). 44.16. 20.57. 11.28. 8.44. Market to book ratio. 2.75. 1.89. 1.56. 1.24. Return on assets (%). –6.91. 5.37. 17.45. 16.33. Tangible assets (%). 26.29. 18.92. 37.32. 32.37. Capital expenditure (%) R&D (%) Dividend per share ($) Retained earnings to total equity ratio (%). Median. 7.62. 5.43. 8.20. 6.73. 13.11. 7.61. 2.58. 1.07. 0.00. 0.00. 0.58. 0.28. –110.50. –1.90. 56.50. 62.50. Market leverage (%). 31.58. 26.83. 38.90. 38.19. Book leverage (%). 42.28. 40.89. 44.61. 44.55. ΔDebt (%). 4.47. 0.40. 3.23. 1.49. ΔEquity (%). 22.30. 6.32. 1.83. 0.09. Deficit (%). 27.70. 11.29. 5.00. 2.26. Number of firms 4890 4890 2211 2211 Notes: Means and medians of key variables across stages are obtained in two steps: (1) calculate the mean of a variable in each stage for each firm and (2) calculate the mean and median of the variable mean across all the firms for each stage.. Panel B of Table 2 provides more detail on the financing characteristics of firms across these two life cycle stages. Frank and Goyal (2003) and Agca and Mozumdar (2007) both document a significant size effect in tests of the pecking order. We follow their strategy and divide our sample into quintiles according to firm size. To more effectively control for firm size across the two stages, we use growth firms to pin down size quintiles. We first sort the growth firms into 5 equal quintiles according to their real assets at the beginning of their growth stage. We then allocate mature firms into these growth-firm quintiles according to their real assets at the beginning of the maturity stage. Since about half of the mature firms end up in the fifth quintile, we further divide the fifth quintile into two equal parts: 5a and 5b. Except for 5b, the size distributions of the same quintile for these two.

(7) 185. Laarni Bulan and Zhipeng Yan. cohorts match up satisfactorily. The two-sample Kolmogorov-Smirnov test for the equality of the distribution of real assets between the two stages but within the same size quintile does not reject equality for quintiles 1 to 5a. Table 2. Summary Statistics (cont’d) Panel B: Mean by firm stage and size quintile Growth Stage. Maturity Stage. Q1. Q2. Q3. Q4. Q5a. Q5b. Q1. Q2. Q3. Q4. Q5a. Q5b. Age (years). 6.47. 8.89. 12.31. 15.02. 15.99. 21.10. 8.12. 9.86. 11.84. 14.50. 18.00. 19.70. Real assets (log). 14.88. 16.07. 17.07. 17.92. 18.79. 20.01. 15.30. 16.27. 17.15. 18.06. 18.84. 20.86. Sales growth rate (%). 74.80. 51.31. 35.61. 31.52. 30.37. 26.01. 19.17. 9.89. 10.24. 12.58. 13.62. 9.92. 4.58. 2.64. 2.33. 2.30. 2.06. 1.80. 2.21. 1.88. 1.54. 1.45. 1.53. 1.53. –35.41 –10.96. –0.37. 3.22. 8.58. 9.36. 23.51. 21.03. 19.36. 18.17. 16.81. 15.36. Market to book ratio Return on assets (%) Tangible assets (%) Capital expenditure (%) R&D (%) Dividend per share ($) Retained earnings to total equity ratio (%). 25.18. 26.95. 24.63. 24.62. 29.01. 31.15. 22.90. 29.22. 33.94. 34.57. 36.49. 42.74. 7.41. 7.94. 7.51. 7.54. 8.12. 7.27. 7.12. 7.35. 8.57. 8.62. 8.33. 8.01. 18.26. 13.17. 14.13. 12.21. 8.26. 4.38. 3.79. 3.76. 2.73. 2.25. 2.19. 2.43. 0.00. 0.00. 0.00. 0.00. 0.00. 0.00. 0.15. 0.45. 0.35. 0.39. 0.66. 0.78. –215.87 –132.76 –83.24 –83.07 –27.40 –48.08. 47.77. 59.68. 63.86. 59.59. 61.22. 49.59. Market leverage (%). 25.15. 31.61. 29.90. 30.12. 36.50. 45.70. 19.12. 27.86. 35.03. 39.53. 39.45. 43.01. Book leverage (%). 41.48. 43.18. 38.60. 38.72. 44.50. 54.44. 25.74. 35.06. 37.90. 42.82. 45.10. 51.12. 5.09. 4.25. 3.45. 3.82. 5.34. 6.16. 2.43. 2.17. 3.50. 3.54. 3.88. 3.00. ΔEquity (%). 44.03. 26.12. 17.81. 14.73. 8.58. 7.93. 5.41. 1.67. 1.77. 2.05. 2.84. 1.18. Deficit (%). 51.63. 30.54. 21.99. 18.99. 14.20. 15.07. 8.28. 3.82. 5.04. 5.74. 6.72. 3.99. ΔDebt (%). Number of firms. 978. 978. 978. 978. 489. 489. 47. 195. 337. 454. 344. 863.

(8) 186. International Journal of Business and Economics. Panel B shows that growth firms have a much greater need for external financing, as expected. The average financing deficit for the smallest growth firms is 51.63% while that of the smallest mature firms is 8.28%. Equity makes up a larger proportion of external finance for growth firms, but this proportion declines as the firm gets larger. In contrast, for mature firms, except for the firms in the smallest size quintile, the reliance on debt is greater than on equity. On firm performance, the two variables identified by Fama and French (2005) to be central in evaluating firms’ financing decisions, growth and profitability, both show extremely different patterns between growth firms and mature firms. The real sales growth rate is about two times higher for growth firms than for mature firms on average. It strictly decreases with firm size for growth firms, while it is quite stable for mature firms. We view higher sales growth as indicative of a greater relative value of the firms’ growth options versus the costs associated with asymmetric information. On the other hand, profitability monotonically increases with firm size for growth firms but strictly decreases with size for mature firms. In other words, for growth firms getting bigger means getting better in terms of profitability, while for mature firms the opposite is true. This latter finding is largely consistent with the existing literature on the diversification discount. Lang and Stulz (1994) and Berger and Ofek (1995) find that diversification reduces firm value. Firms that choose to diversify are poor performers relative to firms that do not. When firms are still in the growth stage, they usually don’t diversify. At this stage, getting bigger means a firm is more capable of surviving market competition. On the other hand, if a firm is in its maturity stage, getting bigger is usually achieved through mergers and acquisitions, which is usually not value-enhancing. Although the profitability of mature firms declines with increasing size, their profitability levels are still higher than those of growth firms. Under the pecking order theory, higher profitability implies that firms will have more internal funds available for financing. In sum, growth firms’ financing characteristics are quite different from mature firms’ even after controlling for firm size. We expect that the degree of information asymmetry and the relative value of growth options are functions of both firm size and life cycle stage. Therefore, we can come to much richer conclusions in tests of the pecking order by accounting for both these factors. 3. Empirical Tests 3.1 Testing the Pecking Order Theory—Aggregate Data In this section, we first adopt a test of the pecking order theory proposed by Shyam-Sunder and Myers (1999) given by: ΔDebtit = b0 + b1 Deficitit + ε it .. We then follow Lemmon and Zender (2010) by incorporating a quadratic term:. (1).

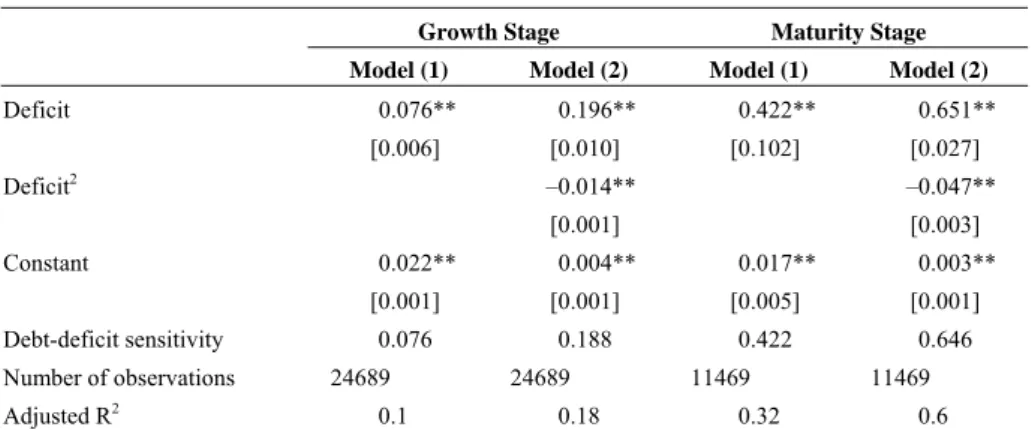

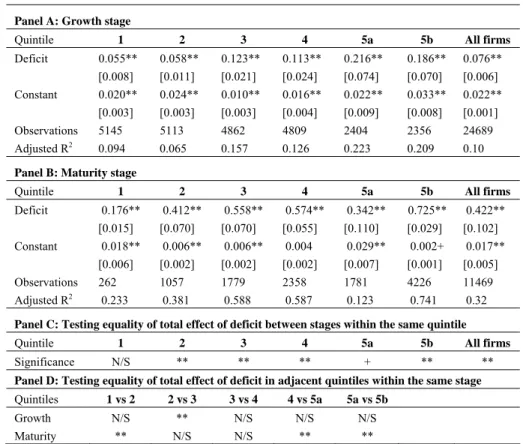

(9) 187. Laarni Bulan and Zhipeng Yan ΔDebtit = b0 + b1 Deficitit + b2 Deficitit2 + ε it ,. (2). where ΔDebt is net debt issued and Deficit is the financing deficit, i.e., uses of funds minus internal sources of funds, (both scaled by total assets). This deficit is financed with debt and/or equity. If firms follow the pecking order, changes in debt should track changes in the deficit one-for-one. Hence, the expected coefficient on the deficit is 1 (Shyam-Sunder and Myers, 1999). The quadratic specification is used to account for binding debt capacity constraints. If firms are financing their deficit with debt first and issue equity only when they reach their debt capacity, then net debt issued is a concave function of the deficit (as shown by Chirinko and Singha, 2000) and the coefficient on the squared deficit term would be negative. If firms are issuing equity first and if debt is the residual source of financing, then this relationship should be convex and the coefficient on the squared deficit term would be positive. If debt and equity are issued in fixed proportions, the deficit would have no effect on net debt issued. We first estimate both models across life cycle stages in Table 3. We use pooled ordinary least squares (OLS) with heteroskedasticity-consistent (robust) standard errors adjusted for clustering by firm. We report the total effect of the deficit, or debt-deficit sensitivity, as the percent change in net debt issued per one percent change in the financing deficit, evaluated at the sample mean. In unreported robustness tests, we include year effects and use firm fixed effects estimation; the results are very similar to those reported here.1 Table 3. Tests of Pecking Order using OLS, All Firms Growth Stage Model (1) Deficit. 0.076** [0.006]. Deficit2. Model (2) 0.196** [0.010]. Maturity Stage Model (1) 0.422** [0.102]. –0.014**. Debt-deficit sensitivity Number of observations. 0.022**. 0.004**. [0.003] 0.017**. [0.001]. [0.001]. [0.005]. 0.076. 0.188. 0.422. 24689. 24689. 0.651** [0.027] –0.047**. [0.001] Constant. Model (2). 11469. 0.003** [0.001] 0.646 11469. 0.1 0.18 0.32 0.6 Adjusted R2 Notes: Robust standard errors clustered by firm are reported in brackets. * and ** denote significance at 5% and 1% levels, respectively.. First, there is an improvement in the fit of Model (2) over Model (1). Compared to Model (1), the estimated debt-deficit sensitivities in Model (2) are increased by 0.112 and 0.224 for growth and mature firms, respectively. The coefficients on the squared deficit term are significantly negative for both categories, implying that on average, net debt issued is a concave function of the deficit. Secondly, the sensitivities are much higher for mature firms than those for growth firms. Thus, it.

(10) 188. International Journal of Business and Economics. appears the pecking order describes the financing choices of mature firms better than growth firms, contrary to conventional wisdom. In the next section, we split each life cycle stage into size quintiles to control for the size effect documented by Frank and Goyal (2003). 3.2 Controlling for Firm Size To fully control for firm size, we estimate Model (1) for each size quintile in each life cycle stage. The results are presented in Table 4. In this simple model, we do not find strong evidence of the size effect documented by Frank and Goyal (2003) in either stage. Although the debt-deficit sensitivities seemingly increase as firms get larger in both life cycle stages, the Wald test of the equality of the sensitivities between two adjacent size quintiles shows that the difference is significant only for selected size quintiles. In fact, the sensitivity for some larger firms is lower than that for smaller firm groups. For instance, the sensitivity of maturity stage quintile 5a (0.342) is significantly lower than that of quintile 4. Table 4. Tests of the Pecking Order over Life Cycle Stages Panel A: Growth stage Quintile. 1. 2. 3. 4. Deficit. 0.055**. 0.058**. 0.123**. 0.113**. 0.216**. 0.186**. 0.076**. [0.008]. [0.011]. [0.021]. [0.024]. [0.074]. [0.070]. [0.006]. 0.020**. 0.024**. 0.010**. 0.016**. 0.022**. 0.033**. 0.022**. [0.003]. [0.003]. [0.003]. [0.004]. [0.009]. [0.008]. [0.001]. Constant. 5a. 5b. All firms. Observations. 5145. 5113. 4862. 4809. 2404. 2356. 24689. Adjusted R2. 0.094. 0.065. 0.157. 0.126. 0.223. 0.209. 0.10. 2. 3. 4. 5a. 5b. Panel B: Maturity stage Quintile Deficit Constant. 1. All firms. 0.176**. 0.412**. 0.558**. 0.574**. 0.342**. 0.725**. 0.422**. [0.015]. [0.070]. [0.070]. [0.055]. [0.110]. [0.029]. [0.102]. 0.018**. 0.006**. 0.006**. 0.004. 0.029**. 0.002+. 0.017**. [0.006]. [0.002]. [0.002]. [0.002]. [0.007]. [0.001]. [0.005]. Observations. 262. 1057. 1779. 2358. 1781. 4226. 11469. Adjusted R2. 0.233. 0.381. 0.588. 0.587. 0.123. 0.741. 0.32. Panel C: Testing equality of total effect of deficit between stages within the same quintile Quintile Significance. 1. 2. 3. 4. 5a. 5b. All firms. N/S. **. **. **. +. **. **. Panel D: Testing equality of total effect of deficit in adjacent quintiles within the same stage Quintiles Growth. 1 vs 2. 2 vs 3. 3 vs 4. 4 vs 5a. 5a vs 5b. N/S. **. N/S. N/S. N/S. Maturity ** N/S N/S ** ** Notes: Robust standard errors clustered by firm are reported in brackets. +, *, and ** denote significance at 10%, 5%, and 1% levels, respectively. N/S denotes non-significance..

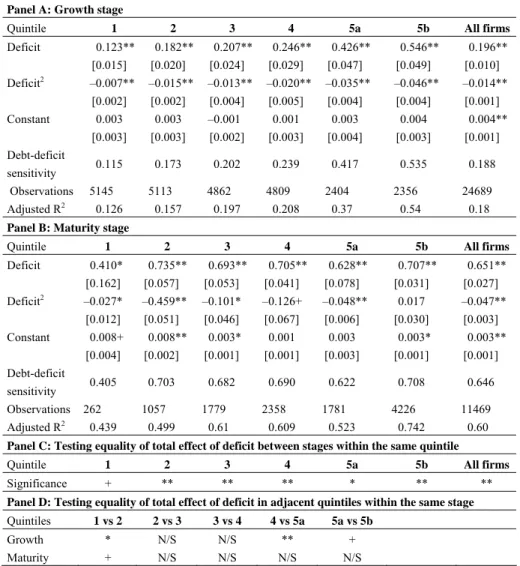

(11) 189. Laarni Bulan and Zhipeng Yan. In contrast to the weak size effect, a strong “maturity effect” is found: for firms in the same size quintile, the debt-deficit sensitivities of mature firms are larger than those of growth firms. Since Model (1) does not accurately evaluate the pecking order theory (Chirinko and Singha, 2000), Table 4 is only a benchmark case. To account for a firm’s debt capacity, we estimate Model (2) across size quintiles and life cycle stages. The results are in Table 5. Across all quintiles and stages, the coefficient on Deficit is positive while the coefficient on Deficit2 is negative and significant except for the largest quintile of mature firms. This indicates that firms are limited by their debt capacity constraints and have to issue equity. Table 5. Tests of the Pecking Order over Life Cycle Stages Panel A: Growth stage Quintile. 1. 2. 3. 4. Deficit. 0.123**. 0.182**. 0.207**. 0.246**. Deficit2 Constant Debt-deficit sensitivity Observations Adjusted R2. 5a 0.426**. 5b 0.546**. All firms 0.196**. [0.015]. [0.020]. [0.024]. [0.029]. [0.047]. [0.049]. [0.010]. –0.007**. –0.015**. –0.013**. –0.020**. –0.035**. –0.046**. –0.014**. [0.002]. [0.002]. [0.004]. [0.005]. [0.004]. [0.004]. [0.001]. 0.003. 0.003. –0.001. 0.001. 0.003. 0.004. [0.003]. [0.003]. [0.002]. [0.003]. [0.004]. [0.003]. [0.001]. 0.115. 0.173. 0.202. 0.239. 0.417. 0.535. 0.188. 5145 0.126. 5113 0.157. 4862 0.197. 4809 0.208. 0.004**. 2404. 2356. 24689. 0.37. 0.54. 0.18. Panel B: Maturity stage Quintile. 1. 2. 3. 4. Deficit. 0.410*. 0.735**. 0.693**. 0.705**. Deficit2 Constant Debt-deficit sensitivity Observations Adjusted R2. 5a 0.628**. [0.162]. [0.057]. [0.053]. [0.041]. [0.078]. –0.027*. –0.459**. –0.101*. –0.126+. [0.012]. [0.051]. [0.046]. [0.067]. 0.003*. 0.008+. 0.008**. 5b 0.707**. All firms 0.651**. [0.031]. [0.027]. –0.048**. 0.017. –0.047**. [0.006]. [0.030]. [0.003]. 0.001. 0.003. 0.003*. 0.003**. [0.004]. [0.002]. [0.001]. [0.001]. [0.003]. [0.001]. [0.001]. 0.405. 0.703. 0.682. 0.690. 0.622. 0.708. 0.646. 262. 1057. 0.439. 0.499. 1779 0.61. 2358 0.609. 1781. 4226. 0.523. 11469. 0.742. 0.60. Panel C: Testing equality of total effect of deficit between stages within the same quintile Quintile. 1. 2. 3. 4. 5a. 5b. All firms. Significance. +. **. **. **. *. **. **. Panel D: Testing equality of total effect of deficit in adjacent quintiles within the same stage Quintiles Growth. 1 vs 2. 2 vs 3. 3 vs 4. 4 vs 5a. 5a vs 5b. *. N/S. N/S. **. +. Maturity + N/S N/S N/S N/S Notes: Robust standard errors clustered by firm are reported in brackets. +, *, and ** denote significance at 10%, 5%, and 1% levels, respectively. N/S denotes non-significance..

(12) 190. International Journal of Business and Economics. Under Model (2), we find weak evidence of the size effect—but only among firms in the growth stage. For growth firms, the total effect of the deficit and R2 are increasing in firm size. The smallest quintile has a total effect of 11.5% and an R2 of 0.126 while the largest quintile (5b) has a total effect of 53.5% and an R2 of 0.54. Thus, the pecking order performs “best” for the largest firms in the growth stage. In the maturity stage, the story is quite different. We do not find evidence of this monotonic size effect at all. The total effect ranges from 40.5% to 70.8% and, except for the first two quintiles, they are not significantly different from each other at the 10% level. Thus, once a firm has reached maturity, the size effect ceases to exist. In comparing firms across life cycle stages, we find that the total effect of the deficit is significantly higher for mature firms within each size quintile. For instance, growth firms in quintile 2 have roughly the same size as mature firms in quintile 2. But, their debt-deficit sensitivity is only 17.3% compared to 70.3% of mature firms in the same size quintile. In sum, we find a weak size effect for growth firms, i.e., the total effect of the deficit is weakly increasing in firm size. For mature firms, we find the total effect of the deficit is similar across all size quintiles, with the exception of quintile 1. Comparing across stages, we find the maturity effect remains, i.e., the total effect of the deficit is significantly larger for mature firms than for growth firms. From these findings we infer that mature firms more closely exhibit financing behavior consistent with the pecking order. 3.3 Controlling for Bond Ratings Thus far we have shown that in tests of the pecking order, there is a maturity effect that dominates the size effect. We have also seen that firm size is not necessarily monotonically related to debt capacity constraints. Lemmon and Zender (2010) and Agca and Mozumdar (2007) identify firms with access to public debt markets to further control for debt capacity. The argument is that firms with bond ratings have access to low cost debt and this is a good indicator of larger debt capacity. To measure the severity of debt-capacity constraints, Lemmon and Zender (2010) use a predicted probability that a firm will have a bond rating. They show that firms with a high predicted probability of having a bond rating are larger, older, more profitable, and have lower market-to-book ratios, consistent with the characteristics of not only the mature firms in our sample but also the largest growth firms. Thus to a certain extent, our slice of the data presents in a very intuitive way a natural progression in terms of access to public debt. Mature firms are more established and have longer credit histories. The largest growth firms are the oldest firms in their cohort and are quite similar to mature firms in many respects. These are precisely the type of firms we expect to have access to the public debt markets. In Tables 6 and 7 we repeat our regressions across life cycle stages for high and low predicted bond ratings cohorts. The sample size is smaller because of data constraints.2 The results in Table 6 are consistent with a high probability of having rated debt being indicative of larger debt capacity and being less constrained. The quadratic model performs well for both growth and mature stages, and small and.

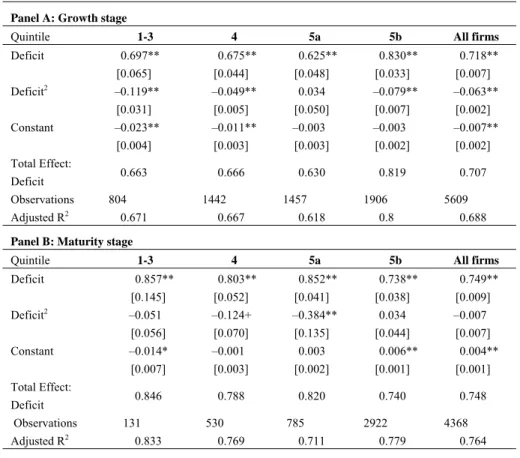

(13) 191. Laarni Bulan and Zhipeng Yan. large firms. The R2 and the total debt-deficit sensitivities are high. For all mature firms with high predicted bond ratings, the coefficient on the squared deficit term is close to 0 and insignificant. This is evidence that this group of firms do not face binding debt capacity constraints. Table 6. Tests of the Pecking Order over Life Cycle Stages: High Predicted Bond Ratings Panel A: Growth stage Quintile Deficit Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. 1-3 0.697**. 4. 5a. 5b. 0.675**. 0.625**. 0.830**. [0.065]. [0.044]. –0.119** [0.031]. All firms 0.718**. [0.048]. [0.033]. [0.007]. –0.049**. 0.034. –0.079**. –0.063**. [0.005]. [0.050]. [0.007]. [0.002]. –0.023**. –0.011**. –0.003. –0.003. –0.007**. [0.004]. [0.003]. [0.003]. [0.002]. [0.002]. 0.663. 0.666. 0.630. 0.819. 0.707. 804. 1442. 0.671. 1457. 0.667. 1906. 0.618. 5609. 0.8. 0.688. Panel B: Maturity stage Quintile. 1-3. Deficit. 0.857**. Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. 4. 5a. 5b. 0.803**. 0.852**. 0.738**. All firms 0.749**. [0.145]. [0.052]. [0.041]. –0.051. –0.124+. [0.056]. [0.070]. –0.014*. –0.001. 0.003. [0.007]. [0.003]. [0.002]. [0.001]. [0.001]. 0.846. 0.788. 0.820. 0.740. 0.748. 131 0.833. 530. [0.038]. [0.009]. –0.384**. 0.034. –0.007. [0.135]. [0.044]. [0.007]. 785. 0.769. 0.006**. 2922. 0.711. 0.004**. 4368. 0.779. 0.764. Panel C: Testing equality of total effect of deficit between stages within the same quintile Quintile. 1-3. 4. 5a. 5b. All firms. Significance. **. *. **. N/S. N/S. Panel D: Testing equality of total effect of deficit in adjacent quintiles within the same stage Quintile. 1-3 vs 4. 4 vs 5a. 5a vs 5b. Growth. N/S. N/S. **. Maturity N/S N/S N/S Notes: Robust standard errors clustered by firm are reported in brackets. +, *, and ** denote significance at 10%, 5%, and 1% levels, respectively. N/S denotes non-significance.. On the other hand, growth firms have a significant negative coefficient for the squared deficit, indicating binding debt capacity constraints remain. Thus, although these firms are likely to have access to the public debt markets, they have larger.

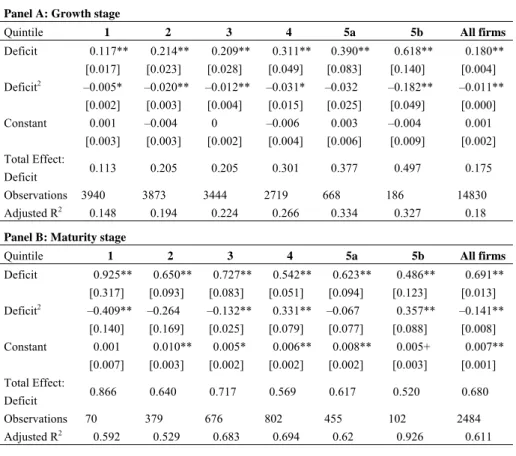

(14) 192. International Journal of Business and Economics. financing deficits due to their larger demand for external finance. Hence they resort to issuing equity more often. When we look at firms across size quintiles but within the same life cycle stage, we find that there is no size effect in either stage. That is, large firms do not necessarily fit the pecking order theory better than small firms. However, the maturity effect, though weakened (compared to Table 5), still exists. Controlling for size, most mature firms fit the theory better than growth firms. Table 7. Tests of the Pecking Order over Life Cycle Stages: Low Predicted Bond Ratings Panel A: Growth stage Quintile. 1. 2. 3. 4. 5a. 5b. Deficit. 0.117**. 0.214**. 0.209**. 0.311**. 0.390**. 0.618**. Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. All firms 0.180**. [0.017]. [0.023]. [0.028]. [0.049]. [0.083]. [0.140]. [0.004]. –0.005*. –0.020**. –0.012**. –0.031*. –0.032. –0.182**. –0.011**. [0.002]. [0.003]. [0.004]. [0.015]. [0.025]. [0.049]. [0.000]. 0.001. –0.004. –0.006. 0.003. –0.004. 0.001. [0.003]. [0.003]. [0.002]. [0.004]. [0.006]. [0.009]. [0.002]. 0.113. 0.205. 0.205. 0.301. 0.377. 0.497. 0.175. 3940. 3873. 0.148. 0. 3444. 0.194. 2719. 0.224. 0.266. 668. 186. 0.334. 14830. 0.327. 0.18. Panel B: Maturity stage Quintile. 1. 2. 3. 4. 5a. 5b. Deficit. 0.925**. 0.650**. 0.727**. 0.542**. 0.623**. 0.486**. Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. [0.317]. [0.093]. [0.083]. –0.409**. –0.264. –0.132**. [0.140]. [0.169]. [0.025]. 0.001. 0.010**. 0.005*. [0.051] 0.331** [0.079] 0.006**. [0.094] –0.067 [0.077] 0.008**. [0.123] 0.357** [0.088] 0.005+. All firms 0.691** [0.013] –0.141** [0.008] 0.007**. [0.007]. [0.003]. [0.002]. [0.002]. [0.002]. [0.003]. [0.001]. 0.866. 0.640. 0.717. 0.569. 0.617. 0.520. 0.680. 70. 379. 0.592. 676. 0.529. 802. 0.683. 455. 0.694. 102. 0.62. 2484. 0.926. 0.611. Panel C: Testing equality of total effect of deficit between stages within the same quintile Quintile. 1. 2. 3. 4. 5a. 5b. All firms. Significance. **. **. **. **. *. N/S. *. Panel D: Testing equality of total effect of deficit in adjacent quintiles within the same stage Quintile. 1 vs 2. 2 vs 3. 3 vs 4. 4 vs 5a. 5a vs 5b. Growth. **. N/S. +. N/S. N/S. Maturity N/S N/S N/S N/S N/S Notes: Robust standard errors clustered by firm are reported in brackets. +, *, and ** denote significance at 10%, 5%, and 1% levels, respectively. N/S denotes non-significance..

(15) Laarni Bulan and Zhipeng Yan. 193. Table 7 presents the regressions for firms in the low predicted bond ratings cohort or the constrained sample. Again, the panel shows no size effect at either stage, but a strong maturity effect. Moreover, in contrast with Table 6, the results are dramatically different between growth and mature firms. We observe low R2 and low debt-deficit sensitivities for growth firms. The negative coefficient on the squared deficit term indicates that debt capacity constraints are binding for these firms. In contrast, mature firms have high debt-deficit sensitivities and high R2. The results for mature firms in the low predicted bond ratings cohort are very similar to those in the high predicted bond ratings cohort. This shows that a low likelihood of having a bond rating is not necessarily an indication that the firm is debt-constrained. More specifically, mature firms are less likely to be constrained by their debt capacity, whether they have access to public debt markets or not. There are two possible reasons for this result: (1) their need for external finance is not that great and hence they rarely reach their debt capacity or (2) even in the presence of large financial deficits, mature firms are also likely to have larger debt capacity because of their credit quality. Firm maturity is essentially a substitute for access to debt markets, i.e., among firms that are less likely to issue public debt (either due to firm choice or due to supply-side factors) mature firms still have access to a low cost of debt capital. Evidence from existing work supports this view. For example, Diamond (1989) shows how a good reputation mitigates the adverse selection problem between borrowers and lenders. Thus, mature firms who are more established and have longer credit histories are able to obtain better loan rates compared to their younger firm counterparts. Petersen and Rajan (1995) present evidence of higher absolute borrowing costs for younger firms compared to those of older firms, regardless of the competitive structure of the lending market. 3.4 Analysis of Maturity Effect We have documented a dominant maturity effect in the context of the pecking order theory. In this section, we discuss in detail what we believe the maturity effect captures and why it exists. We have shown that the maturity effect is closely related to debt capacity. Mature firms are older, larger, and more profitable; they have more tangible assets and retained earnings. Therefore, they naturally have greater debt capacity. To formally test this, we first estimate the correlation between the probability of being a mature firm and the probability of having a bond rating. Lemmon and Zender (2010) argue that the likelihood that a firm can access public debt markets is a useful proxy for debt capacity and firms that are able to issue rated debt most closely conform to the assumptions underlying the pecking order. If the likelihood of being mature is highly correlated with the likelihood of having rated debt and the latter is a valid proxy for debt capacity, then we can argue that firm maturity is an alternative measure of debt capacity. We fit a logistic regression for the probability that a firm is in the maturity stage as in the predicted bond rating regression of Lemmon and Zender (2010), i.e. the explanatory variables are the natural log of assets, ROA, tangibility, market-tobook ratio, leverage, firm age and the standard deviation of the firm’s stock return..

(16) 194. International Journal of Business and Economics. We estimate the predicted probability of being in the maturity stage for each observation and find that this probability is highly correlated with the predicted probability of having a bond rating. The Pearson correlation coefficient is 0.59. Table 8. Tests of the Pecking Order over Life Cycle Stages: High Book Leverage Panel A: Growth stage Quintile Deficit Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. 1 0.123**. 2 0.163**. 3 0.196**. 4 0.188**. 5a 0.380**. 5b 0.527**. All firms 0.182**. [0.007]. [0.008]. [0.009]. [0.009]. [0.015]. [0.013]. [0.004]. –0.008**. –0.013**. –0.017**. –0.015**. –0.032**. –0.044**. –0.014**. [0.001]. [0.001]. [0.001]. [0.001]. [0.002]. [0.001]. [0.000]. –0.008+. –0.003. –0.001. 0. 0. 0.002. 0.001. [0.005]. [0.004]. [0.004]. [0.004]. [0.006]. [0.005]. [0.002]. 0.114. 0.154. 0.188. 0.180. 0.370. 0.514. 0.173. 3052 0.119. 3060 0.137. 2556 0.163. 2485 0.145. 1418 0.315. 1641. 14212. 0.52. 0.156. Panel B: Maturity stage Quintile. 1. 2. 3. 4. 5a. Deficit. 0.527**. 0.756**. 0.644**. 0.664**. 0.619**. Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. 5b 0.729**. All firms 0.651**. [0.069]. [0.045]. [0.034]. [0.024]. [0.022]. [0.013]. [0.007]. –0.035**. –0.552**. –0.044*. –0.141**. –0.047**. –0.020*. –0.047**. [0.005]. [0.064]. [0.022]. [0.016]. [0.002]. [0.008]. [0.001]. –0.003. 0.005. 0.001. –0.006*. –0.002. –0.002. –0.002. [0.010]. [0.005]. [0.005]. [0.003]. [0.004]. [0.002]. [0.001]. 0.512. 0.711. 0.637. 0.644. 0.612. 0.728. 0.645. 75. 409. 0.657. 667. 0.468. 1087. 0.579. 0.525. 884. 2589. 0.47. 5711. 0.716. 0.576. Panel C: Testing equality of total effect of deficit between stages within the same quintile Quintile. 1. 2. 3. 4. 5a. 5b. All firms. Significance. **. **. **. **. *. **. **. Panel D: Testing equality of total effect of deficit in adjacent quintiles within the same stage Quintile. 1 vs 2. 2 vs 3. 3 vs 4. 4 vs 5a. 5a vs 5b. Growth. N/S. N/S. N/S. **. *. Maturity N/S N/S N/S N/S N/S Notes: Robust standard errors clustered by firm are reported in brackets. +, *, and ** denote significance at 10%, 5%, and 1% levels, respectively. N/S denotes non-significance.. However, firm maturity must capture more than just access to public debt markets because even after controlling for predicted bond ratings, the maturity effect still remains (Table 7). The dynamic pecking order (Myers, 1984; Vishwanath, 1993) predicts that financing decisions made by firms will depend on the current and expected levels of unused debt capacity, leverage, and growth opportunities. To.

(17) 195. Laarni Bulan and Zhipeng Yan. further understand the maturity effect, we split the sample according to high and low leverage. We identify high and low leverage by comparing the previous year’s book leverage ratio to the industry (4-digit SIC) median leverage ratio in the previous year. Tables 8 and 9 present the results. Not surprisingly, we find stronger evidence for the pecking order theory among low leverage firms, which is consistent with the prediction of the dynamic pecking order theory that once firms are close to their debt capacity they will resort to issuing equity. The interesting fact is that even when the leverage ratios are high, mature firms fit the pecking order fairly well and the maturity effect is still significant. Table 9. Tests of the Pecking Order over Life Cycle Stages: Low Book Leverage Panel A: Growth stage Quintile. 1. 2. 3. 4. 5a. 5b. Deficit. 0.117**. 0.235**. 0.241**. 0.398**. 0.534**. 0.651**. Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. All firms 0.227**. [0.009]. [0.010]. [0.010]. [0.012]. [0.022]. [0.026]. [0.005]. –0.004**. –0.022**. –0.006**. –0.026**. –0.037**. –0.032*. –0.014**. [0.001]. [0.001]. [0.001]. [0.002]. [0.005]. [0.014]. [0.001]. 0.008+. 0.005. 0.005. 0.005. 0.007+. [0.005]. [0.004]. [0.003]. [0.003]. [0.005]. [0.004]. [0.002]. 0.114. 0.225. 0.240. 0.392. 0.527. 0.647. 0.222. 2093 0.159. 2053 0.209. 2306 0.339. 0. 2324 0.404. 986. 715. 0.529. 0.008**. 10477. 0.676. 0.236 All firms. Panel B: Maturity stage Quintile. 1. 2. 3. 4. 5a. 5b. Deficit. 1.230**. 0.744**. 0.711**. 0.731**. 0.772**. 0.619**. Deficit2 Constant Total Effect: Deficit Observations Adjusted R2. [0.036]. [0.030]. [0.017]. [0.018]. [0.026]. –0.538**. –0.439**. –0.131**. –0.054**. –0.201**. [0.019]. [0.031]. [0.009]. [0.015]. [0.024]. 0.003. 0.009**. 0.005**. 0.006**. 0.006*. 0.722**. [0.014]. [0.009]. 0.161**. –0.116**. [0.011]. [0.006]. 0.009**. 0.007**. [0.003]. [0.003]. [0.002]. [0.002]. [0.003]. [0.001]. [0.001]. 1.191. 0.716. 0.701. 0.727. 0.752. 0.628. 0.713. 187. 648. 0.863. 1112. 0.538. 0.669. 1271 0.734. 897. 1637. 0.643. 5752. 0.827. 0.656. Panel C: Testing equality of total effect of deficit between stages within the same quintile Quintile. 1. 2. 3. 4. 5a. 5b. All firms. Significance. **. **. **. **. *. N/S. **. Panel D: Testing equality of total effect of deficit in adjacent quintiles within the same stage Quintile Growth. 1 vs 2 **. 2 vs 3 N/S. 3 vs 4 *. 4 vs 5a. 5a vs 5b. N/S. N/S. Maturity ** N/S N/S N/S + Notes: Robust standard errors clustered by firm are reported in brackets. +, *, and ** denote significance at 10%, 5%, and 1% levels, respectively. N/S denotes non-significance..

(18) 196. International Journal of Business and Economics Table 10. Financial Distress: Altman’s Z-Scores for Each Life Cycle Stage. Panel A: Growth stage Quintile. 1. 2. 3. 4. 5a. 5b. All firms. Low leverage. –3.635. –0.787. 0.274. 0.345. 1.171. 0.609. –0.082. High leverage. –2.482. –0.498. 0.632. 0.858. 1.212. 0.374. –0.508. Panel B: Maturity stage Quintile. 1. 2. 3. 4. 5a. 5b. All firms. Low leverage. 2.966. 3.244. 2.897. 2.791. 2.582. 1.848. 2.689. High leverage. 3.304. 3.318. 3.152. 2.923. 2.679. 1.940. 2.664. Lemmon and Zender (2010) argue that the a firm’s distance from its debt capacity, which is the key point suggested in the dynamic pecking order theory, is difficult to measure, and the likelihood of having rated debt is a noisy proxy of this quantity. One possible reason why the maturity effect is consistently significant under various model specifications is that mature firms, big or small, have ample unused debt capacity. Investigating our results further, we calculate Altman (1968) Z-scores for our sample firms. The Z-score is a widely used measure of financial distress (see for instance Graham et al., 1998). Debt capacity can be deemed as the maximum amount of debt that can be issued without causing financial distress (Myers, 1984). A high Z-score indicates a low probability of being in financial distress and a relatively larger debt capacity. Table 10 shows that mature firms have very high Z-scores even when their leverage ratios are high, implying they still have unused debt capacity compared to growth firms. In sum, we find firm maturity is an alternative proxy for firm debt capacity that captures more than just access to public debt markets. In particular, mature firms are older, more stable, and highly profitable with good credit histories. Thus, they naturally have greater debt capacity than growth firms. Their good credit histories also allow them to borrow significantly from private financial intermediaries, which in some cases may preclude the need to access public debt markets. After accounting for firm maturity, the pecking order describes firm financing decisions fairly well. 4. Robustness Tests To ensure that our results are being driven by life cycle stages and not simply by our sample selection criteria, we define the growth and maturity stages in alternative ways. First, for growth firms, we limit our original sample to firms with high industry-adjusted growth rates. Second, we use the ratio of retained earnings to total equity (RE/TE) as a proxy for firm maturity. De Angelo et al. (2005) argue that the earned/contributed capital.

(19) 197. Laarni Bulan and Zhipeng Yan. mix is a logical proxy for a firm’s life cycle stage because it measures the extent to which a firm is reliant on internal or external capital. Firms with low RE/TE tend to be in the capital infusion stage, whereas firms with high RE/TE tend to be more mature with ample cumulative profits that make them largely self-financing. Furthermore, we try various combinations of different stage lengths and different definitions of growth and/or maturity stages. For instance, we use highsales-growth firms only for the growth stage and firms with high RE/TE only for the maturity stage and assume the length of each stage is 6 years. Our main conclusions still hold with various combinations of growth and maturity stage definitions and stage lengths—the size effect only very weakly exists in the growth stage and mature firms fit the pecking order better than growth firms. We also include several important factors (Rajan and Zingales, 1995) that have consistently been found to explain a firm’s financing decisions in all the regressions. Our results remain the same. Lastly, to further explore the pecking order theory within the framework of life cycles, we estimate the Leary and Roberts (2010) tworung empirical model for firms in each quintile at each life cycle stage. The results are reported in Table 11. We find no size effect for firms in both stages with regards to debt-equity issuance decisions. We again find a maturity effect, though weaker than we obtain from using the Lemmon and Zender (2010) model above, when pitting firms in their growth stage against those in their maturity stage. Table 11. Tests of Pecking Order over Life Cycle Stages: The Leary and Roberts (2010) Model Panel A: Growth stage Quintile. 1. 2. 3. 4. 5a. 5b. All firms. Average correct: First runga (%). 67.51. 63.58. 66.1. 66.11. 66.72. 62.38. 66.15. Average correct: Second rungb (%). 45.00. 44.98. 44.74. 44.08. 49.165. 50.755. 44.96. Average correct: Overallc (%). 56.26. 54.28. 55.42. 55.10. 57.94. 56.57. 55.55. Number of observations. 2773. 2424. 2117. 2082. 968. 929. 11293. Panel B: Maturity stage Quintile. 1. 2. 3. 4. 5a. 5b. Average correct: First runga (%). 71.345. 75.62. 76.215. 74.725. 68.88. 70.265. All firms 72.99. Average correct: Second rungb (%). 47.02. 57.85. 50. 50. 49.145. 49.84. 50. Average correct: Overallc (%). 59.18. 66.74. 63.11. 62.36. 59.01. 60.05. 61.50. Number of observations 135 413 736 998 715 1640 4637 Notes: “Average correct: First rung” presents an equal weighted average of the correct classifications of internal and external financing decisions, e.g., if the pecking order correctly classifies 50% (70%) of the observed internal (external) financing decisions, the average correctness of the model is 60%. “Average correct: Second rung” presents an equal weighted average of the correct classifications of debt and equity financing decisions. “Average correct: Overall” presents an average of the first rung and the second rung..

(20) 198. International Journal of Business and Economics. 5. Conclusion In this paper, we classify firms into two life cycle stages and test the pecking order theory of financing proposed by Myers (1984) and Myers and Majluf (1984). Under the Lemmon and Zender (2010) empirical framework, we identify a (weak) size effect and a (strong) maturity effect. The size effect is such that the pecking order theory better explains the financing decisions of firms as they increase in size. The maturity effect is such that mature firms’ financing decisions are better explained by the pecking order theory compared to growth firms. We find that this size effect only weakly exists among firms in their growth stage. For firms in their maturity stage, this size effect is not significant. When controlling for a firm’s debt capacity, this size effect disappears altogether, while the maturity effect remains. We find that the pecking order theory describes the financing patterns of mature firms better than that of growth firms. The likelihood of being a mature firm is highly correlated with the likelihood of having access to public debt markets. However, they are different since the maturity effect remains even after access to public debt is accounted for. We find that mature firms have ample unused debt capacity even when they have relatively high leverage. This indicates that firm maturity is an alternative and arguably better proxy for debt capacity than access to public debt. Notes 1.. We also ran the regressions using firms that are in neither growth nor maturity stages. The results are very similar to those of the growth firms. Other than the growth or maturity stages, firms can be in revival, stagnant, or decline stages. Without identifying exactly which stage the other firms are in, we cannot provide a concrete answer as to why they are different. In this paper, we focus on growth and maturity since the pecking order theory has clear implications for firms in these stages.. 2.. We combine the first three size quintiles due to the small number of observations in these quintiles.. References Agca, S. and A. Mozumdar, (2007), “Firm Size, Debt Capacity, and Corporate Financing Choices,” Working Paper. Altman, E., (1968), “Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy,” Journal of Finance, 23, 589-609. Anthony, J. and K. Ramesh, (1992), “Association between Accounting Performance Measures and Stock Prices: A Test of the Life Cycle Hypothesis,” Journal of Accounting and Economics, 15, 203-227. Baker, M. and J. Wurgler, (2004), “A Catering Theory of Dividends,” Journal of Finance, 59(3), 1125-1165..

(21) Laarni Bulan and Zhipeng Yan. 199. Berger, A. and G. Udell, (1998), “The Economics of Small Business Finance: The Roles of Private Equity and Debt Markets in the Financial Growth Cycle,” Journal of Banking and Finance, 22, 613-673. Berger, P. and E. Ofek, (1995), “Diversification’s Effect on Firm Value,” Journal of Financial Economics, 37, 39-65. Bulan, L., N. Subramanian, and L. Tanlu, (2007), “On the Timing of Dividend Initiations,” Financial Management, 36(4), 31-65. Chirinko, R. and A. Singha, (2000), “Testing Static Tradeoff Against Pecking Order Models of Capital Structure: A Critical Comment,” Journal of Financial Economics, 58, 417-425. De Angelo, H., L. De Angelo, and R. Stulz, (2006), “Dividend Policy and the Earned/Contributed Capital Mix: A Test of the Life-Cycle Theory,” Journal of Financial Economics, 81, 227-254. Dickinson, V., (2009), “Cash Flow Patterns as a Proxy for Firm Life Cycle,” Working Paper, Available at SSRN: http://ssrn.com/abstract=755804. Diamond, D., (1989), “Reputation Acquisition in Debt Markets,” Journal of Political Economy, 97(4), 828-862. Diamond, D., (1991), “Monitoring and Reputation: The Choice between Bank Loans and Directly Placed Debt,” Journal of Political Economy, 99(4), 689-721. Evans, D., (1987), “The Relationship between Firm Growth, Size, and Age: Estimates for 100 Manufacturing Industries,” The Journal of Industrial Economics, 35(4), 567-581. Fama, E. and K. French, (2005), “Financing Decisions: Who Issues Stock?” Journal of Financial Economics, 76, 549-582. Frank, M. and V. Goyal, (2003), “Testing the Pecking Order Theory of Capital Structure,” Journal of Financial Economics, 67, 217-248. Graham, J., M. Lemmon, and J. Schallheim, (1998), “Debt, Leases, Taxes, and the Endogeneity of Corporate Tax Status,” Journal of Finance, 53, 131-162. Gort, M. and S. Klepper, (1982), “Time Paths in the Diffusion of Product Innovations,” Economic Journal, 92, 630-653. Lang, L. and R. Stulz, (1994), “Tobin’s Q, Corporate Diversification, and Firm Performance,” Journal of Political Economy, 102(6), 1248-1280. Leary, M. and M. Roberts, (2010), “The Pecking Order, Debt Capacity, and Information Asymmetry,” Journal of Financial Economics, 95, 332-355. Lemmon, M. and J. Zender, (2010), “Debt Capacity and Tests of Capital Structure Theories,” Journal of Financial and Quantitative Analysis, 45, 1161-1187. Liu, M., (2008), “Accruals and Managerial Operating Decisions over the Firm Life Cycle,” Working Paper, Available at SSRN: http://ssrn.com/abstract=931523. Loughran, T. and J. Ritter, (2004), “Why Has IPO Underpricing Changed over Time?” Financial Management, 33(3), 5-37. Miller, D. and P. Friesen, (1984), “A Longitudinal Study of the Corporate Life Cycle,” Management Science, 30(10), 1161-1183. Myers, S., (1984), “The Capital Structure Puzzle,” Journal of Finance, 39, 575-592..

(22) 200. International Journal of Business and Economics. Myers, S. and N. Majluf, (1984), “Corporate Financing and Investment Decisions When Firms Have Information That Investors Do Not Have,” Journal of Financial Economics, 13, 187-221. Shyam-Sunder, L. and S. Myers, (1999), “Testing Static Tradeoff against Pecking Order Models of Capital Structure,” Journal of Financial Economics, 51, 219244. Viswanath, P. V., (1993), “Strategic Considerations, the Pecking Order Hypothesis, and Market Reactions to Equity Financing,” Journal of Financial and Quantitative Analysis, 28, 213-234..

(23)

數據

+7

相關文件

• The order of nucleotides on a nucleic acid chain specifies the order of amino acids in the primary protein structure. • A sequence of three

Quality kindergarten education should be aligned with primary and secondary education in laying a firm foundation for the sustainable learning and growth of

In order to facilitate the schools using integrated or mixed mode of curriculum organization to adopt the modules of Life and Society (S1-3) for improving their

Numerical results are reported for some convex second-order cone programs (SOCPs) by solving the unconstrained minimization reformulation of the KKT optimality conditions,

Numerical results are reported for some convex second-order cone programs (SOCPs) by solving the unconstrained minimization reformulation of the KKT optimality conditions,

Abstract We investigate some properties related to the generalized Newton method for the Fischer-Burmeister (FB) function over second-order cones, which allows us to reformulate

Microphone and 600 ohm line conduits shall be mechanically and electrically connected to receptacle boxes and electrically grounded to the audio system ground point.. Lines in

To convert a string containing floating-point digits to its floating-point value, use the static parseDouble method of the Double class..