國立臺灣大學社會科學院經濟學系在職專班 碩士論文

Mid-Career Master Program Department of Economics College of Social Sciences

National Taiwan University Master Thesis

以動態一般均衡模型評估石油稅對台灣經濟之影響

The Impact on Oil Tax of Taiwan:

A Dynamic Stochastic General Equilibrium Model Approach

黃孝怡 Hsiao-Yi Huang

指導教授﹕林建甫博士 Advisor: Chien-Fu Lin, Ph.D.

中華民國 102年 1月

January, 2013

i

Content

誌謝……….. ….vi

摘要………..….vii

Abstract………viii

Chapter 1 Introduction

1.1 Oil and Macroeconomic………..……….……... 11.2 DSGE model………..…...………...…1

1.3 Oil Tax and DSGE model………..………..4

1.4 Literature review……..………..………...………...4

1.5 Structure of the paper……..………..……….………….…6

Chapter 2 DSGE model

2.1 Household………72.2 Firms………...………10

2.2.1 Final firms………...10

2.2.2 Intermediate firms………...11

2.3 Log-Linearized Model……...……….……...13

Chapter 3Estimation methodology

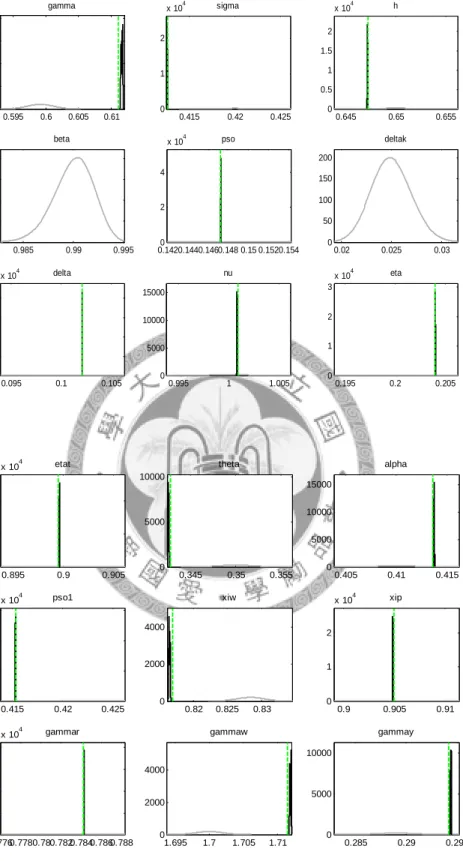

3.1 Parameter estimation……… 173.2 Priors distribution………. 18

3.3 Posteriors distribution……….. 24

3.4 Solving of the DSGE model……….26

Chapter 4Experiment result

4.1 Estimated results………...284.2 Estimated Impulse responses of structural shocks………...………….35

ii

4.2.1 The production factor shock………..35

4.2.2 The consumer preference shock………36

4.2.3 The price adjustment cost shock………...38

4.2.4 The wage adjustment cost shock………..….39

4.2.5 The oil price shock………....41

4.2.6 The capital utilization shock……….………..………..……….41

4.2.7 The interest rate adjustment cost shock……….43

Chapter 5Discussion about Oil Tax

5.1 Oil tax and the DSGE model………..………. 455.2 Impulse responses of structural shocks - the amount of oil tax is proportion to oil price ………..46

5.2.1 The production factor shock………..………46

5.2.2 The consumer preference shock………....46

5.2.3 The price adjustment cost shock………...47

5.2.4 The wage adjustment cost shock………...48

5.2.5 The oil price shock………50

5.2.6 The capital utilization shock………..51

5.2.7 The interest rate adjustment cost shock……….52

5.3 Impulse responses of structural shocks - the amount of oil tax is proportion to amount of oil consumption……….……….…..53

Chapter 6 Conclusion

………...………..55Reference

………...57Appendix A: Log-linear Model of DSGE model

…………...……....…………...……...59Appendix B: Dynare core

………..………..………...…….61iii

List of Figures

Fig 1.1 The structural chart of a DSGE model………...…..……….... 3

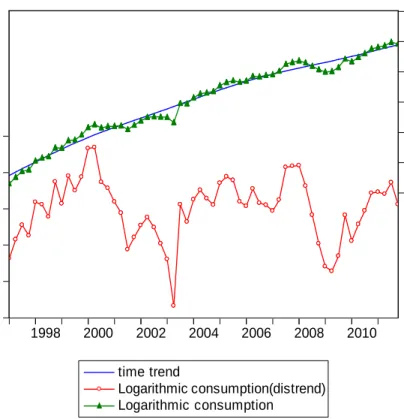

Fig 3.1 Taiwan’s quarterly data from 1997Q1 to 2011Q4-Consumption ………..…….. 19

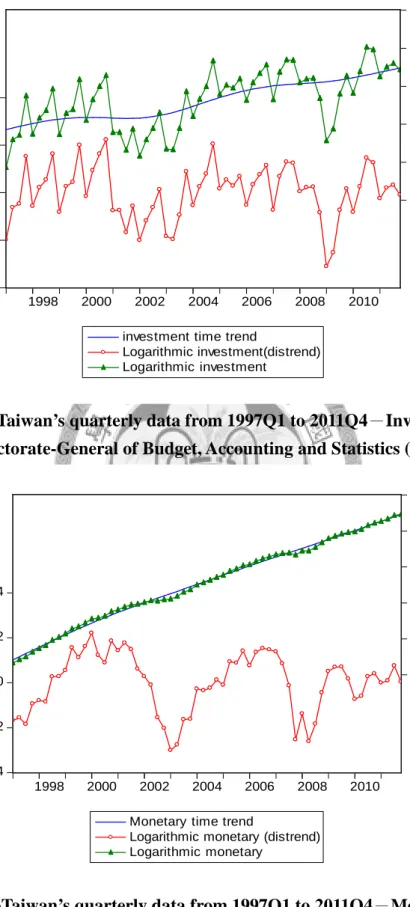

Fig 3.2Taiwan’s quarterly data from 1997Q1 to 2011Q4-Investment……….….….. … 20

Fig 3.3 Taiwan’s quarterly data from 1997Q1 to 2011Q4-Monetary……….….…. …...20

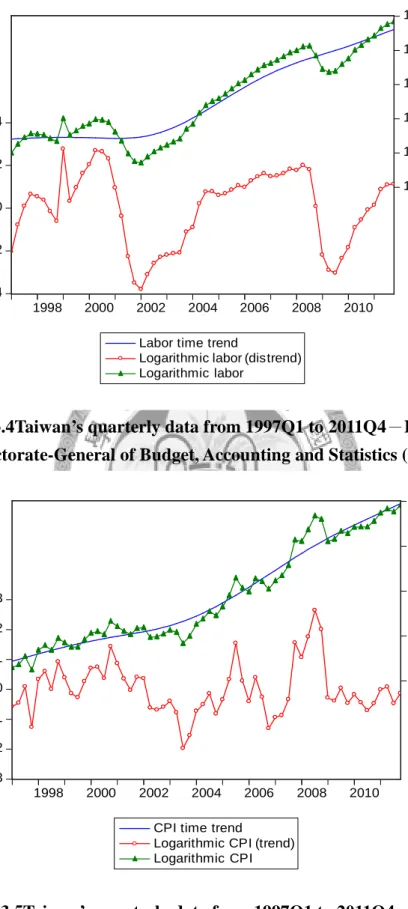

Fig 3.4 Taiwan’s quarterly data from 1997Q1 to 2011Q4-Labor……….…………..….. 21

Fig 3.5 Taiwan’s quarterly data from 1997Q1 to 2011Q4-CPI……….……….….. 21

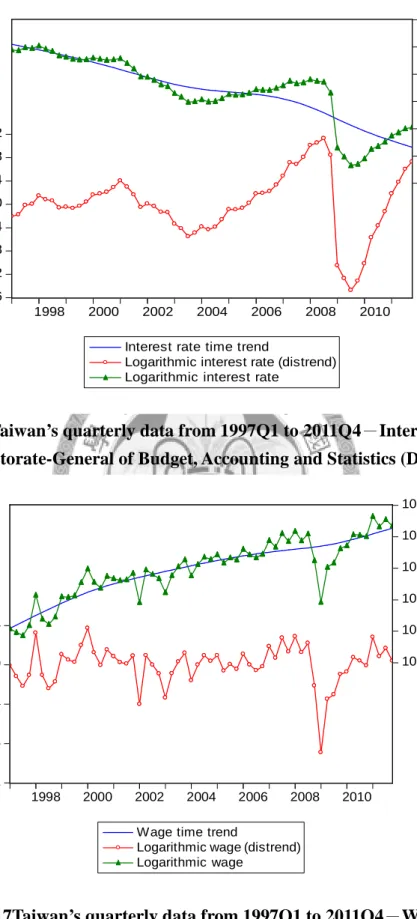

Fig 3.6 Taiwan’s quarterly data from 1997Q1 to 2011Q4-Interest rate……….………... 22

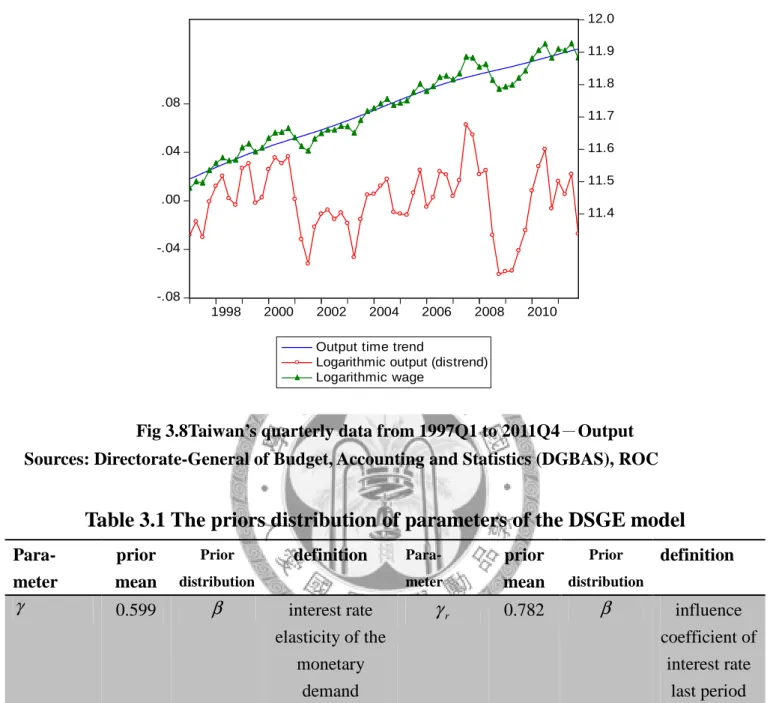

Fig 3.7 Taiwan’s quarterly data from 1997Q1 to 2011Q4-Wages……….…...…….22

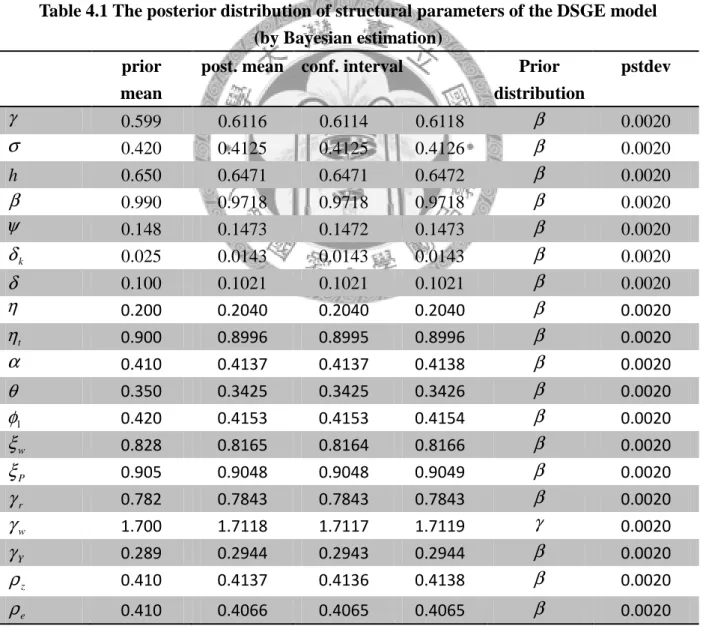

Fig 3.8 Taiwan’s quarterly data from 1997Q1 to 2011Q4-Output……….…... 23

Fig 4.1 The prior distributions of the DSGE model (1)………..…...……..…... 30

Fig 4.2 The prior distributions of the DSGE model (2)………..…...…….….... 31

Fig 4.3 The prior distributions and posteriors of the DSGE model (1)…………..…...…..…..…...32

Fig 4.4 The prior distributions and posteriors of the DSGE model (2)……….……...…... 33

Fig 4.5 The smoothed shock of the DSGE model………..…...…….……...34

Fig 4.6 The comparison between estimated output and Taiwan’s quarterly historical data…….... 35

Fig 4.7 Impulse response to a 1% production factor shock………...………... 37

Fig 4.8 Impulse response to a 1% consumer preferences shock………...……...…... 38

Fig 4.9 Impulse response to a 1% price adjustment cost shock……….…..…... 39

Fig 4.10 Impulse response to a 1% wage adjustment cost shock……….…....…... 40

Fig 4.11 Impulse response to a 5% oil price shock………...…...……....…... 42

Fig 4.12 Impulse response to a 1% capital utilization shock……….……...……...…... 43

Fig 4.13 Impulse response to a 1% interest rate adjustment cost shock………... 44

Fig 5.1 Impulse response to a 1% production factor shock (oil tax is considered)……….... 47

iv

Fig 5.2 Impulse response to a 1% consumer preferences shock(oil tax is considered)…...…... 48

Fig 5.3 Impulse response to a 1% price adjustment cost shock (oil tax is considered)………... 49

Fig 5.4 Impulse response to a 1% wage adjustment cost shock (oil tax is considered)………... 50

Fig 5.5 Impulse response to a 5% oil price shock (oil tax is considered)……….…..….... 51

Fig 5.6 Impulse response to a 1% capital utilization shock (oil tax is considered)…..…….…... 52

Fig5.7 Impulse response to a 1% interest rate adjustment cost shock (oil tax is considered)….... 53

Fig 5.8 Impulse response to a 5% oil price shock (oil tax is considered)……….…..….... 54

v

List of Tables

Table 3.1 The priors distribution of parameters of the DSGE model………….……….... 23 Table 4.1 The posterior distribution of structural parameters of the DSGE mod……...……….... 28 Table 4.2 Theoretical moments of the DSGE model………...…………... 29 Table 5.1 Theposterior distribution and means for the structural parameters.…………....……... 45

vi

誌謝 誌謝 誌謝 誌謝

本文得以完成,主要感謝指導教授林建甫教授的辛勤指導,林建甫教授兩年來以言教與 身教引領我進入經濟學的領域,林老師恢宏的視野與深刻的學術涵養永遠是我們所追尋的目 標。在口試過程中,感謝政治大學經濟系翁永和教授、台灣海洋大學海洋事務與資源管理研 究所莊慶達教授和台灣師範大學環境教育研究所葉欣誠學長的對於本文的精闢建議與寶貴 意見,使本文能夠更為充實。尤其感謝亦師亦友的葉欣誠學長,在此也祝葉教授在環保署副 署長的任內政躬康泰。

轉換跑道進入智慧財產局從事專利審查工作以來,由於專利審查業務的複雜與專業性,

不可避免的需要長官與同仁的指導與協助,尤其是本科的杜科長在國、負責複核新進人員審 查意見的耀文與人傑學長,以及其他的同事與先進,感謝他們平時對我的照顧與協助,使我 在工作上能夠減少許多錯誤,讓我能有足夠的時間與心力完成在職班的課業。

最後,由於銘揚同學的鼓勵,美絨、藝聞同學的協助,使論文與口試可以順利完成,在 此一併感謝。

vii

摘要 摘要 摘要 摘要

本文試圖以發展並估計一個新凱恩斯動態隨機一般均衡模型以探討石油稅對台灣經濟的 影響。本文主要依循 ChristianoChristiano、Eichenbaum and Evans(2005)、Ireland (1997) 與 Peersmanand Stevens (2012)發展的模型,模型的結構參數以 Bayesian 方法估計,模型構建假 設調整工資的頻率較少。在此模型中,石油作為生產的輸入,也是消費的一部分,石油和其 他類型的消費產品之間有靈活的替代彈性。我們並模擬具有石油稅時動態隨機一般均衡模型 的結果並和比較根據不同的石油稅率假設時動態隨機一般均衡模型的結果。

本文的主要結果是生產要素的衝擊,消費者偏好衝擊,工資調整成本衝擊將立即引起輸出和 附加價值的生產消費的提升。資金利用率造成輸出的提升導因於的勞動量的改變。價格調整 成本衝擊、石油價格衝擊將升通貨膨脹和減緩消費。利率調整的成本衝擊將使輸出和附加值 商品下降。石油稅會影響消費者的偏好並加強價格調整的負面影響,石油稅也將減少工資調 整的效應、消費和生產。不同石油稅率造成的估計衝擊沒有明顯的不同。在政策的意義上來 說,石油稅可能會降低石油的消費量並衝擊經濟成長,但不同類型的石油稅間不會有明顯的 差別。

關鍵字 關鍵字

關鍵字關鍵字:New Keynesian、DSGE 模型、石油稅

viii

Abstract

This paper is an attempt to develop and estimate a New Keynesian dynamic stochastic general equilibrium model of Taiwan. In this paper, the model is following Christiano, Eichenbaum and Evans(2005), Ireland (1997) and Peersman and Stevens (2012).The structural parameters of this model are estimated by using a Bayesian approach and the model is constructing by being assumed to adjust wages infrequently. Oil is used as an input to production and is also a part of the household’s consumption in this paper.There is a flexible elasticity of substitution between oil and other types of consumption goods in the consumption bundle. We also simulate the DSGE model including oil tax and compare the results under various oil tax rules.

The main results of this paper are the production factor shock, consumer preference shock, wage adjustment cost shock will immediately rise output and the value-add production consumption. The capital utilization shock will rise output due to the raise of number of labor. The price adjustment cost shock, oil price shock will rise inflation and fall consumption. The interest rate adjustment cost shock will fall output and added-value goods.Then the oil tax will affect the consumer preference and strengthen the negative effects of price adjustment, and the oil tax will reduce the effects of wage adjustment, the consumption and production. The estimated impulses between the oil tax rule which the amount of oil tax is proportion to oil price and the oil tax rule which is that the amount of oil tax is proportion to the amount of oil are not obviously different.

The main contribution of this paper is that we simulate how the exogenous shocks would affect macroeconomic by using the estimated DSGE model. And the numerical results show that the variables are not substantially affected by the presence of nominal rigidities. This paper also aims to explore the complications of the effects between these exogenous shocks. The suggestions of this paper are followings. First, the oil tax would reduce oil consumption and impact economic growth. Second, the effects of different types of oil tax are not obviously different.

ix

Keywords::::New Keynesian, DSGE model, oil tax

1

Chapter 1 Introduction

1.1 Oil and Macroeconomic

The macroeconomic effects of oil include oil price and oil consumption. Oil can usually be used for several applications. Petrolasconsumption goodscan be used as fuel and oilas production goods can be usedas raw materials forpetrochemical industries.Oil price fluctuations are usually treated as a exogenous disturbances where are unrelated to any economic fundamentals (Peersman and Stevens, 2012). Sudden and protracted oil price increases are generally accompanied by economics contractions and high inflation (Hamilton, 1983).Researchers and policymakers are often interesting in the impacts of oil price shocks on output and the effects related to the endogenous policy responses of monetary policy and tax policy.Changes in oil prices have a direct impact on the price level of the economy, they affect consumption decisions, and also influence the cost structure of firms and through this channel have a second-rounded effect on domestic prices. Wage and price indexation can propagate the effects of oil-price shocks on inflation and output. Recent empirical studies have revealed that the effects of oil shocks became muted after the mid-1980s. These studies obtained similar conclusions: the typical response to an oil shock is a decrease in the real GDF growth rate and real wage, leading to inflation and so on. (Hongzhi, 2010 ).

In general, oil tax would induce the rising of oil price and inflation. The contractionary effect of oil price shock can be due to the endogenous tightening of the monetary policy.However,oil tax would induceoil consumption and carbon dioxide emissions, so it is important for energy saving and carbon reduction.

1.2 DSGE model

The function of a model of analysis and simulation for economy is twofold : to serve as a tool for policy analysis and to serve as a tool for forecasting key macroeconomic variables (Medina an Soto, 2011). Not only the first-round effects of different shocks can be understood but also second-round

2

effects can be considered.In the past, general economic forecasting models of business cycle are in the form ofsimultaneous-equations structural models. The linear structures of these models are as the same as the Vector Autoregressive model. So the Vector Autoregressive model is used to be as the main analytic tool for economic forecasting. However, there are some of the following problems:

first the correct number of variables needs to be excluded, and second the projected future values are required for the exogenous variables in the system.

One of advantages of the model is that the structural interpretation of the disadvantage of the Luca’s critique on the traditional analysis of policy effects (Medina and Soto,2006)( Liao and Teng, 2008). Lucas(1976) indicated that estimated functional forms obtained for macroeconomic models in the Keynesian tradition and the Vector Autoregressive model do not correctly account for the dependence of private agent’s behavior on anticipated government policy rules. The famous “Lucas critique”pointed out:

"Given that the structure of an econometric model consists of optimal decision rules of economic agents, and that optimal decision rules vary systematically with changes in the structure of series relevant to the decision maker, it follows that any change

in policy will systematically alter the structure of econometric models."

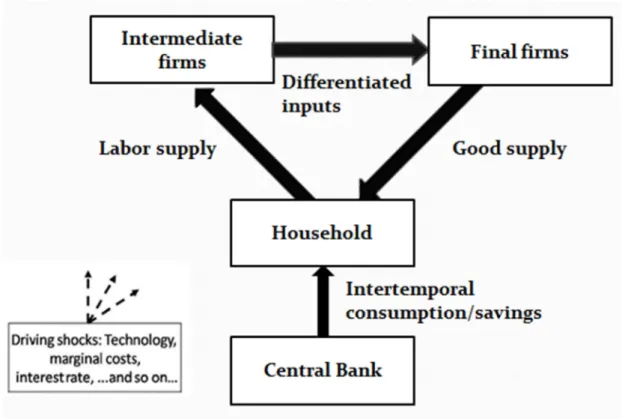

Relatively, DSGE models can handle both the possibilities of structural changes and the problems of nonlinearities, since DSGE models are able to identify that the actions of rational agents are not only dependent on government policy variables, but also on government policy rules (Liu and Gupta, 2007). The purpose of DSGE models is to interpret how the microeconomic principles derive aggregate economic phenomena including business cycles, economic growth, and the effects of monetary and fiscal policy. Figure 1.1 shows the typical structure of a DSGE model. DSGE models also study how the economy evolves over time and how the economy is affected by random shocks such as technological change, fluctuations in the price of oil, or macroeconomic polices. The

3

decision-makers in DSGE model, often called 'agents', may include households, firms, and governments or central banks and DSGE models are constructed on the basis of assumptions about agents' preferences. There are two issues considered in DSGE models: one is that it is possible to ask whether the policies considered are Pareto optimal, another is or how well agents satisfy some other social welfare criterion derived from preferences. In recent years, the DSGE model has been the baseline framework used for theoretical analysis of monetary policy and tax policy.

Fig 1.1 The structural chart of a DSGE model

The DSGE model is the best decision of households’ utility and firms’profit in different constraints. But the original DSGE model is nonlinear so that it will be log-linearized to obtain a linearized steady state model. Then the first order Taylor’s expansion of a DSGE model will be transfer to simultaneous equations. The deviations of endogenous variables, which be obtained by solving the simultaneous equations present the fluctuations of endogenous variables. In fact, there are many uncertainties in real economic environment and these uncertainties could be presented by

4

applying exogenous shocks.

The hypotheses of the RBC-DSGE model includes rationalexpectation, perfect elasticity of wage and price, and the market is clean. However, the hypotheses of the new Keynesian DSGE model includes rational expectation, nominal rigidityof wage and price, and the market is not always clean.

There are three methods for estimating the structural parameters of a DSGE model: calibration, maximum likelihood estimation and Bayesian estimation. And the log-linearized model of the DSGE model can be solved by Blanchard and Kahn method.

1.3 Oil Tax and DSGE model

The DSGE model has been used to analyze these issues for several countries’ economic model in some literatures. The model is framed in the New Keynesian assumption where firms are assumed to adjust prices infrequently and wages are set. Oil is used as an input in production and also a part of the technology used by domestic firms. The oil-price shock can generate an income effect that affects consumption and labor decisions. It also affects the marginal costs faced by domestic firms and through this channel, their pricing decisions. As well as, monetary policy modeled as a Taylor’s rule endogenously reacts to the movements in inflation and output caused by the oil-price shock.

There are several DSGE models related to oil-price, including Smets and Wouters(2003), Liu and Gupta (2007), De Fiore and Beidas-Storm and Poghosyan (2009), Unalmis and Unsa (2009), and Hongzhi (2010)in recent decades. The DSGE model including oil -price let us better understand the mechanisms through which oil-price shocks affect inflation, output and the endogenous responses of monetary policy. We can make policy analysis overcoming the Lucas Critique by using this methodology approach. In this paper, we present the dynamic stochastic general equilibrium model (DSGE model) which is the model of Taiwanese economy. The main building blocks of the model will be described and the results of the estimation of key parameters will be discussed.

1.4 Literature review

5

Many central banks set monetary policy which means interest rates by operating directing on bank reserves to achieve lower prices and stable inflation. In order to carry out this job, many central banks have used a variety of macroeconomic models to understand what drive inflation and how changes in monetary policy feed through the economy into inflation.

In the 80’s, Hamilton (1983) provided sudden and protracted oil price increases are generally accompanied by economics contractions and high inflation. An important factors to drive inflation is oil prices. As the rise in oil prices from $75 a barrel in 2007 Q3 to $121 a barrel in 2008 Q2 was associated with a rise in CPI inflation from 1.8% in 2007 Q3 to 4.8% in 2008 Q3. Millard (2011) estimated a DSGE model of the United Kingdom, the model was estimated using Bayesian techniques on data for the period 1996 Q2 to 2008 Q4.

De Fiore, Lombardo and Stebunovs(2006)built a DSGE model characterized by two oil importing countries and one oil-exporting country and evaluated the performance of simple Taylor-type interest rate rules when the economy is hit by oil price shocks and calibrated the model.

Unalmis et al. (Unalmis, Unalmis and Unsa, 2009 ) develop a strickly-price DSGE model through which they analyze the effects of various shocks, namely, the increase in aggregate demand,unexpected oil supply disruption and the precautionary oil demand on an oil importing small open economy and on the rest of the world. The study shows the impacts of the productivity and fiscal policy shocks which leading to a rise in the world aggregate demand and a subsequent surge in the real price of oil are different on inflation.

Because the oil-importing country is a standard new Keynesian economy model, the structure of the economy is closely related to the closed economy models of Christiano, Eichenbaum and Evans(2005) and Smet and Wouters(2003). Peersmanand Stevens (2012)developed and estimated a structural model of US and oil producing countries including a well-specified oil market in which oil prices are endogenously determined.

6

By investigating the dynamics induced by the various oil shocks, the results which show the real oil prices fluctuations are mostly exogenous with respect to US macroeconomic developments.

Beidas-Storm andPoghosyan(2009) presented and estimated a small open economic DSGE model for the Jordanian economy. The model features nominal and real rigidities, imperfect competition and habit formation in the consumer’s utility function, and oil imports are explicitly modeled in the consumption basket and domestic production. This study used Bayesian methods to estimate the model, by combining priors and the likelihood function to obtain the posterior distribution of structural parameters. Golosov, Hassler, Krusell,and Tsyvinski(2011) analyze a DSGE model with an externality through climate change from using fossil energy. The results of this study is an analytical derivation of a simple formula for the marginal externality damage of emissions. The formula allows the optimal tax to be easily parameterized and computed.

1.5 Structure of the paper

This paper is an attempt to develop and estimate a New Keynesian dynamic stochastic general equilibrium model of Taiwan. In tis paper, following Christiano, Eichenbaum and Evans(2005), Ireland (1997) and Peersman and Stevens(2012).The structural parameters of this model are estimated by using a Bayesian approach and the model is constructing by being assumed to adjust wages infrequently.Oil is used as an input to production and is also a part of the household’s consumption.

The rest of the paper is organized as follows: Chapter 2 presents the basic structure of the DSGE model. Chapter 3 describes the basic theorems of numerical simulation and parameter estimations of the DSGE model. Chapter 4 studies the effects of different economic shocks to the DSGE model.

Chapter 5 discusses the influences of oil tax on the DSGE model and the main results are explained in chapter 6.

7

Chapter 2 The DSGE model

The dynamic stochastic general equilibrium (DSGE)model with the Keynesian rigid prices assumption was used in the real business cycle to lie at the heart of the workhorse New Keynesian models of macroeconomics analysis. By log-linearizing the first-order conditions of optimizing households and firms they allow to handle small and mid-scale models with excellent predictive properties. DSGE models are also used in macroeconomics forecasting.

2.1 Household

Households obtain utility from consuming the final goods C and disutility from supplying hours t of labor N and t M corresponds to the total nominal balances held at the beginning of period t. t Households own the capital stock and make investment and capital utilization decisions.

Household’s lifetime utility function

(2.1)

E denotes the rational expectation operator using information up to time t=0, o β∈[0,1]is the discount factor. The utility function displays external habit function, b∈[0,1] denotes the importance of the habit stock, which is the last period’s aggregate consumption. σ >0 capturesintertemporal substitution attitudes of households and φ>0 is the elasticity of the labor supply which respect to the real wage and γ >0 is the interest rate elasticity of the monetary demand which respect to the real wage. Preferences display habit information, whose strength is measured by the parameter h.

The consumption bundle is a composite of core (non-fuel) consumption goods and imported fuel:

(2.2)

( ) ( )

− +

+ −

− − +

−

−

−

∞

∑

= ]1 1

[ 1 1

1 1

1 0

0 φ

φ γ

γ σ

σ

φφ γγ

σσ

β t

t t t

t t

t

t N

P hC M

C b

E

( )

, 1 11 1 , 1

) ( )

( 1

) (

− −

−

− +

= η

η η η η

η η

η δ

δ C j C j

j

Ct Zt Ot

8

where CO,trepresents fuel consumption, andCZ,t is a bundle non-fuel consumption. The

parameter ηis the elasticity of substitution between oil and core consumption, and δ defines their corresponding share. Households maximize their utility subject to the following budget constraint:

t t

t j j t t t t t k t t t

j t

t j t

t j t

t j t

t t

j j t t j

t P

Div P

K T u f P u P R P W P B P M P M R P I B

C + + + = −1 + −1 + + 1 [ − ( )] + +

(2.3) whereItj denotes investment expenditure, Wtj is the nominal wage,Btj denotes holdings of a riskless bond that costs the inverse of the gross nominal interest rate (Rt >1) and pays one unit of currency next period. Ttj denotes nominal transfers from (or lump-sum taxes paid to ) the government, Ktj denotes holdings of the capital stock, u denotes capital utilization rate and t

k

Rt is the rental rate which households rent capital to the firms that produce intermediate goods, denotes dividends that intermediate firms pay to households. And [Rtkut −Ptf(ut)]Ktj is the rent of the net capital.

Household’s capital accumulation equation is

t t

t t t

K

t I

I I S z K

K (1 ) (1 ( ))

1 1

+

+= −δ + −

(2.4) where δk is capital deprecation rate, ( )

+1 t

t t

I I

S z is investment adjustment cost and

0 ) ( ) (

1 ' 1

=

=

+

+ t

t t

t t t

I I S z I

I

S z in steady state.

The following is a Langrange function including representative household’s utility and budget constraint.

( ) ( )

−

−

−

−

−

−

− Ψ

−

−

−

−

− + + + + −

−

+ −

− −

=

+

−

−

+ −

−

−

∞ −

=

∑

] )) ( 1 ( ) 1 ( [

] )]

( [

) (

[ 1 ]

1 [ 1

1 _ 1

1 1

1 1 1

1 1

0 0

t t

t t t

I t

t t j t j t t t

k t j t j t j t

j t j t t

j j t t j t t t t

t t t

t t

t t

I I I S z K

K Q Div T

K u u

R N W B

M R M

I B C P P N

hC M C b

E V

δ φφ λ

γγ σσ

β

φ φ γ

γ σ

σ

Div

9

(2.5)

And we can obtain first order condition of by maximizing the Langrange function.

0 )

(

1

1 − =

−

∂ =

∂ −

− t t

t r t t

P hC

C C b

V σ λ (2.6)

0 }

{ )

( ) (

1 1

=

− +

=

∂

∂

+

−

t t t t t t

t t

t t

P E

P P b M

P M

V σ β λ λ

(2.7)

0 }

{ 1 − =

∂ =

∂

+ t t t

t

t E R

B

V β λ λ (2.8)

0 )}

1 ( ))

( (

{ 1 1 1− 1 + 1 1 − − =

∂ =

∂

+ + +

+ +

+ t t t t t t t

k t t t t

Q P Q

P u

f u R K E

V β λ δ λ

(2.9) }

) (

{ )

( 1

)) ( 1

( 1 1 1 ' 1 1 1 1 1

1 1 '

1 t

t

t t t

t t t

t t

t t t t t

t t

t t t t t

t t t

t I

I I

I z I

I S z P Q P

I E I z I

I S z I Q

I S z I Q

V + + + + + + +

+

−

−

−

− +

=

−

∂ =

∂

λ β λ

(2.10) )

'(

t t k

t P f u

R = (2.11)

whereQt is Langrange multiplier and it means the value of capital investment. Calvo(1983) claimed the assumptions of fully flexible prices and wages are sometimes inconsistent with some empirical evidences on prices and wage adjustment. The Calvo model assumes that there is a fixed probability 1−ξw that a household canre-optimize its nominal wage in each period.In the constraint of aggregate demand for labor is

1 1

0

1

) ) (

( −

−

∫

= tw

w t w t w t

dj j N

Nt t θ

θ θ θ

(2.12) , the labor demand of the household j is

10

t t

t

t N

W j j W

N = ( ))−θtw (

) (

(2.13) ,whereNt( j) is the demand of the jth labor, Wt( j) is the price , W is the wage and t θtw is the wage elasticity of the labor demand. The aggregate wage is

w t w w t

t w

t w t

t w t

t w t

t W j dj W W

W =

∫

−θ −θ = ξ π − − −θ + −ξ −θ 1−θ1

*1 1

1 1 1

1 1

0

1 ] [ ( ) (1 ) ]

) (

[ (2.14)

whereWt* is the optimum wage,

=

= + + − ≥

+

0 1

1 ... 1

1 1

k Wt πtπt πt k k

A household choose the optimal wages to maximize the real value of the sum of utility from period t to period t+k :

∑

∞= +

+ + 0 +

) , ,

( ) ( max

k t kt

kt t

kt t

kt t k w

t N

P M C U

E βξ

(2.15) And the first order condition is

( )

∑

∞= −

− + +

+

+ + +

+

+ =

− + −

0

1 1 1

*

0 )

( max

k

k t k t k t

k t k w t

k t tk k t

t t k t t k w t

hC C

b

N X b

P U W N E E

σ

µ φ

βξ

where

1

*

1 = −

+

+ w +

k t

w k t

t θθ

µ . . (2.16)

2.2 Firms

The firms of a country which is a gross oil importer produce non-oil goods. Intermediate goods producers combine oil with other input factors in the production process of non-oil goods. Each of these different type of goods is produced by a single firms, which faces monopolistic competition.

2.2.1 Final firms

The production function of the final goods producers is

11

1 1

0

1

) (

− −

=

∫

P t

P t

P t P t

di i Y Yt t

θ θ θ θ

(2.17)

P

θt is the variable demand elasticity. The aggregate demand of the ith intermediate input goods for final goods producers from maximizing final goods profits is

i t

t

i Y

P i i P

Y

P

θt

−

= ( ) )

(

(2.18) substituting (2.17) into (2.18) to obtain the relation between the prices of intermediate goods and the prices of final goods:

P P t

t di

i P Pt t

θ − −θ

=

∫

11 1

0

) 1

(

(2.19)

2.2.2 Intermediate firms

The technology of the intermediate firm is given by production function

1 1 1

1 1

) ( ) 1 ( ) (

− −

−

+ −

= α

α α α α α

α

α η

η t gti

i t t i

t VA O

Y

(2.20) with

,where VA is the value added output, t O is oil, gt α >0defines the elasticity of substitution between value-add and oil in production, θ captures the share of labor in GDP, ηt represents the share of the added-value production factors in gross output, and εtTFPis the total factor productivity.

The following demand curves for labor and oil are implied by cost minimization:

t k t k

t t

t w r r k

nˆ =−(ˆ −ˆ )+(1+ˆ )ˆ (2.21)

t t o t

gt p s VA

O =−α(ˆ −ˆ )+ ˆ with t tTFP

k t

t r w

sˆ =(1−θ)ˆ +θˆ −εˆ

. (2.22)

θ

ε θ −

= tTFP( ti) ( tS,i)1

i

t N K

VA

12

The real marginal costs of intermediate firms equal is

(

η −α + −η −α)

−α ={

η[

ε θ −θ]

−α + −η −α}

−α= 1

1 1 1

S, 1 1

1 1

1 (1 )( ) ( ) ( ) (1 )( )

)

( ti t gti t tTFP it t i t igt

t

t VA O L K O

MC f f

, (2.23)

The Calvo model assumes that each period there is a fixed probability ξp that a household canre-optimize its price. The inflation adjustment isPt(i)=πt−1Pt−1(i). A firm choose the optimal price to maximize the real value of the sum of profits from period t to period t+k :

( )

( )max *

0

. P X P MC Y i

E t tk t k t k t k

k k t t

t + + +

∞

= + −

∑

ξ(2.24) where

t k k t k t

t β λλ

ζ ,+ = + , and ζt,t+k =βkin steady state.

And the first order condition from maximizing profits is

0 )

( )

(

0

* 1

1

, =

−

∑

∞= + +

−

− + +

+ k

k t k

t p t t t

k t k t k t t t k

p P P i MC

P i P Y

E ζ µ

ξ

(2.25) and

where

The followings are the exogenous shocks of the DSGE model:

investment adjustment cost shock : (2.26)

production facto shock : (2.27)

consumer preferences shock : (2.28)

z t t z z

t z z

z =(1−ρ )ln +ρ ln −1 +η ln

ε ε

ε ε ρ ε η

ρ

ε t

TFP t TFP

TEP

t =(1− )ln + ln −1 +

ln

b t t b b

t b b

b =(1−ρ )ln +ρ ln −1+η ln

−1

=

+

+ p +

k t

p k P t

k

t θθ

µ

0 )

1 ( )

( )

1 ( )

( 1 1

1

* 1 1 1 1

0 0

* 0 1 1

0 0 =

− −

+

− − + +

+ +

− + +

+ +

+

−

− +

t p t

t p t t t

t t t t t t

k p t

t p t t t t t t t

t P P i MC

P i P Y E

MC i P P P

i P Y

E θθ

λ β λ θθ

λ β λ

13

price adjustment cost shock :

(2.29) wage adjustment cost shock :

(2.30) interest rate adjustment cost shock :

(2.31) capital utilization shock :

(2.32) real oil price shock :

(2.33) where and x are the values of the exogenous shocks in steady state.

isdistributed (iid) series with mean 0 and standard deviation is variance σz.

All households are consistent in symmetrical equilibrium, such as Pt(i)=Pt, Nt(i)= Nt,

t

t i Y

Y( )= ,Kt(i)=Kt, and all parameters are constant in steady state.

2.3 Log-Linearized Model

Log-linearization producer is in line with the one presented in Campbell (1994) and Uhig (1995).

Variables are denoted in the letters without subscript t denote steady state vales. Big letters with subscript t denote variables without any transformation. Letters with subscript t and hat above denote log deviations of particular variable from steady state. Below I present how log-linearization procedure is applied. Deviation of capital from steady state is equal:

X X

Xˆt =ln t −ln

t

t X X

X ln ˆ

ln = +

Taking exponents of both sides we get:

p t p t p p p p

t

µ µ

µ µ ρ µ η

ρ

µ =(1− )ln + ln −1 + ln

w t w t w w w w

t

µ µ

µ µ ρ µ η

ρ

µ =(1− )ln + ln −1 + ln

ν ν

ν ν ρ ν η

ρ

νt =(1− )ln + ln t−1 + t ln

u t t u u

t u u

u =(1−ρ )ln +ρ ln −1 +η ln

pO t t O pO O pO t

O p p

p , =(1−ρ )ln +ρ ln ,−1+η ln

) 1 , 1 (−

x∈ ρ

x

ηt

14

t t t

t

t X X X X

X

e e e

e

ln=

ln +ˆ=

ln ˆThus:

X e X Xe

Xt = Xˆt ⇒ Xˆt = t

Next step is to take the first order Taylor approximation of eXˆtaround the steady state thus Xˆt =0, though we get:

t t

X e e X X

eˆt = 0 + 0( ˆ −0)=1+ ˆ

Thus:

ˆ ) 1 ˆ (

1 t t Xt X Xt

X

X = X ⇒ = +

+ or

X X Xˆt = Xt −

The variable Kˆ multiplied by 100 informs by what percentage capital at time t diverges from the t

steady state. So for example if Kˆ is equal 0.2 we interpret that capital is 20% above the steady t state.

The followings are log-linear equations of the DSGE model. Combine (2.5 ) ,(2.6) and (2.7) to obtain monetary demand equation:

t t

t

t c hc r

m h ˆ

) 1 ˆ (ˆ ) 1 ( ˆ 1 1

1 ββ

σ

γ − = −

+ −

− − (2.34)

Combine ( 2.5) and ( 2.7) to obtain Euler’s equation:

ˆ}) {ˆ

ˆ } ˆ {

1 ( ) 1 ˆ (

} 1 {ˆ 1

ˆt 1 t t 1 t 1 rt Et t 1 Et bt 1 bt h

c h h c h

hE

c − + − −

+ + − + +

= + + − σ π + +

(2.35) Obtain investment equation from (2.10) and (2.11):

}) ˆ ˆ 1 {

ˆ 1 1 ˆ 1 } 1 {ˆ 1

ˆt Et it 1 it 1 qt Et zt 1 zt

i −

+ + + +

+ +

= + + − β +

β β

ψ β

β

β

(2.36) where

Obtain capital process equation from ( 2.4):

t K t K

t k i

kˆ (1 )ˆ ˆ

1 = −δ +δ

+ (2.37)

) 1 (

"

) 1

'( f f

u =

ψ

u k t

t

rˆ =uˆ ψ

15

Combine ( 2.14 ) and ( 2.17 ) to obtain real wage equation:

ˆ )) (ˆ

) 1 ( ˆ 1

1

ˆ ( ˆ

) 1 (

) 1

)(

1 } ( ˆ { ˆ

ˆ 1 ˆ )

( ˆ 1 ˆ 1

1

* 1

1 1

1

−

+ +

−

−

− −

−

− + −

−

− − + +

+

− + +

=

t t t

t t w

w w

t t

t t

t t

t

c h h c

n

w w

E w

w

σ φ

ξ µ

β ξ

π βξ β

π β β π

(2.38) Technology equation of the intermediate firm is:

gt t t

t

t VA o

yˆ =η ( ˆ )+(1−η )ˆ

(2.39) where

the demand curves for labor and oil by minimizing cost

t k t k

t t

t w r r k

nˆ =−(ˆ −ˆ )+(1+ˆ )ˆ , (2.40)

t t t O

gt p s VA

Oˆ (ˆ ˆ ) ˆ

, − +

−

= α , where sˆt =(1−θ)rˆtk +θwˆt −εˆtTEP . (2.41) Combine( 2.19 ) , ( 2.13 ) and ( 2.25 ) to obtain inflation equation:

ˆ ) )ˆ 1 ˆ ( ( ˆ

) 1 (

) 1 )(

1 } ( {ˆ ˆ 1

1

ˆ 1 1 1 t tk t tp

w w w

t t t

t E a αr α w µ

ξ β ξ π βξ

β π β

π β − + + − −

+

−

− − + +

= + − +

(2.42)

The balance condition of goods market is:

p t p t

p

t c i

y ˆ

)) 1 ( 1 ˆ (

)) 1 ( 1 (

)) 1 ( 1 ˆ (

δ β µ

αβδ δ

β µ

αβδ δ

β µ

− + −

−

−

−

−

= −

(2.43) The Taylor’s rule of Central Bank’s monetary policy is :

t t r t y t w r

t y r

rˆ =(1−γ )(γ πˆ +γ ˆ )+γ ˆ−1+νˆ

(2.44) The followings are the log-linearized equations of exogenous shocks, including

investment adjustment cost shock

(2.45) production factor shock

(2.46)

z t t z

t z

zˆ =ρ ˆ−1+η

εε ηε

ρ

ε t

TEP t TEP

t = ˆ−1 +

ˆ

t t

TEP t

t n k

A

Vˆ =εˆ +θˆ +(1−θ)ˆ

16

consumer preferences shock

(2.47) price adjustment cost shock,

(2.48) wage adjustment cost shock

(2.49) oil price shock

(2.50) interest rate adjustment cost shock

(2.51) capital utillzation shock

u t t u

t u

uˆ =ρ ˆ−1+η

. (2.52)

b t t b

t b

bˆ =ρ ˆ−1+η

p t p t p p t

µ µ ηµ

ρ

µˆ = ˆ−1+

w t w t w w t

µ µ ηµ

ρ

µˆ = ˆ−1+

νν ην

ρ

νˆt = ˆt−1+ t po

t o t po o

t p

pˆ = ρ ˆ −1 +η