國立臺灣大學企業管理碩士專班 碩士論文

Global MBA College of Management

National Taiwan University Master Thesis

宏達電無機成長之分析

The Need for Inorganic Growth – Case Study on HTC Corporation

李維恩

Wei-En “Wayan” Lee

指導教授: 胡星陽 博士 Advisor: Shing-Yang Hu, Ph.D.

中華民國 101 年 6 月 June 2011

Acknowledgements

I want to recognize my thesis advisor, Dr. Shing-Yang Hu, Chairperson of the Department of Finance at National Taiwan University for his guidance and patience throughout last year. Even though Dr. Hu was very busy, he still set aside some time to advise and comment on my thesis. It is an honor to work with him. In addition, I would also like to thank the Global MBA office for my countless questions regarding the planning and execution of the thesis. Without the help of the faculty and staff, it would be very difficult for me to complete my MBA at NTU.

Outside of school, I’d like to thank my ex-colleagues and professional friends for information regarding the industry. Particular to Roy Lin (Acer, Marketing Manager), Susan Lin (Macquarie, Sales Trading Executive), Dan Tang (Macquarie, Tech Analyst), Jon Chow (Citi, Research), Michael Liu (KGI, Semiconductor Strategist), and Magnus Ip (HTC, Software Product Manager).

With the help of my professional relationships, I was able to obtain information regarding the smartphone industry (Gartner, IDC, Bloomberg Terminal) which would otherwise be very costly.

Lastly, this thesis would not have been possible without the constant support from my fiancé and soon to be wife, Pearl Chen. Her inspiration and patience allowed me to take time away from her to work on this thesis. I am forever indebted to my family, who has supported me throughout my life and career.

The Need for Inorganic Growth – Case Study on HTC Corporation

By Wei-En Lee

National Taiwan University, GMBA June 2012

Submitted to National Taiwan University Global MBA Program as is required by the School of Management upon graduation, Master of Business Administration

ABSTRACT

“Organic Growth”, in simple terms, is the process of business expansion by maintaining to operate its primary businesses in existing or new markets while using the same enterprise model. “Inorganic Growth” on the other hand is the method of growth that a company deals with mergers or acquisition of new businesses to “open-up” new markets and innovations.

Looking at HTC’s transaction lists throughout history, it is well documented that the company had always been an ODM, relying on adding new capacity and manufacturing services to build “High Tech Computers” or smartphones for consumers. During the 2010-2011 period, there was a rush of transactions including Abaxia (Mobile software company, 2010), OnLive (Cloud computing video games, 2011), Saffron Digital (Mobile videos, 2011), KKBOX (Online music, 2011), S3 (Graphic chipsets, patents, 2011), Dashwire (Cloud computing software for syncing, 2011) and Beats (Music accessories and software, 2011).

Although Taiwan is a relatively small market when compared to the world with only 23 million people (Official National Statistic, 2011) vs China’s 1.3 billion and United States 312 million people, Taiwan is considered one of the biggest contributors of global technology with HTC Corporation (TT:2498) recently awarded #1 brand in Taiwan and top 100 brand globally (Interbrand, 2011).

This abstract will elaborate on HTC’s strategic reasons for entering the stage of inorganic growth. Furthermore, the abstract will discuss HTC Corporation’s (“HTC”) historical decisions, and its transition to become a dominant brand. This report will discuss the different types of growth strategies with the rationale for increasing hardware, content, and software to enhance its products.

Thesis Supervisor: Dr. Shing-Yang Hu

Title: Chairperson to the Department and Graduate Institute of Finance

Table of Contents

I. Introduction

a. Motivation………...1

b. Data Collection………..………...1

c. Structure of the Study………2

II. Literature Review a. Organic Growth………..2

b. Inorganic Growth………..4

i. Horizontal Merger………...6

ii. Vertical Merger………...6

iii. Conglomerate Merger………...7

c. Motives for Mergers & acquisitions………...8

i. Efficiency Theories………...8

ii. Synergy Theory………...8

c.ii.1. Staff reductions………...8

c.ii.2. Economies of scale ……….8

c.ii.3. Acquire new technologies ………...8

iii. Diversification Hypothesis ………....9

iv. Stock Market Driven Acquisitions………9

d. Organization Structure & Design Strategy………...9

i. Low Cost Leadership………...10

ii. Differentiation………...10

iii. Focused………..11

III. HTC Background & Industry Analysis a. Introduction of HTC……….....11

b. Evolution of HTC……….12

c. Mobile Phone Industry………15

IV. Inorganic Stage Analysis a. Financials………..18

b. Market Share & Product Mix……….…21

c. Organization Structure & Design...……….…..25

d. Acquisition Analysis & Roadmap...………...28

V. Saffron Digital – Analysis i. Cloud Computing Trends………....31

ii. Digital Content Analysis……….…….34

VI. Conclusion………..38

References………...40

Appendix………....44

Tables & Additional Figures…….……….……….…..48

List of Illustrations

Illustration 1 – Growth Strategies Flow Path………5

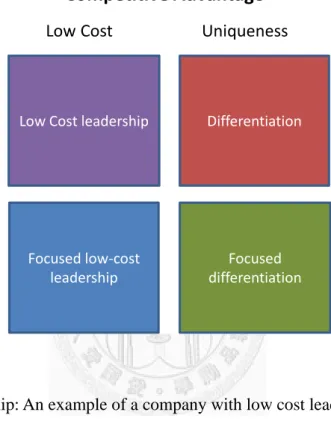

Illustration 2 – Competitive Advantage………..10

Illustration 3 – HTC’s Timeline………..15

Illustration 4 – QFII Holding for HTC………...21

Illustration 5 - Roadmap of Industry VS HTC………...30

Illustration 6 – HTC Watch ………37

List of Figures, Tables

Figure 1 – Smartphone VS Feature Phone in 2011……….16Figure 2 – Global Smartphone Operating Systems……….17

Figure 3 – Monthly Sales ………18

Figure 4 – Stock Price & PE Ratios………19

Figure 5 – HTC Earnings Per Share……….………...20

Figure 6 – Smartphone Type Growth 2011……….………22

Figure 7 – HTC ASP VS Unit Shipment Graph………….……….23

Figure 8 – Operating System Market Share & Growth…..……….24

Figure 9 – Android Market Share breakdown………….………25

Figure 10 – Operating Margins by Comparable Companies..……….26

Figure 11 – Penetration Rate………..……….32

Figure 12 – Precedent Transactions ………….….……….….34

Figure 13 – Online VS Physical Digital Content...……….…36

1 I. Introduction

a. Motivation

The motivation behind this thesis study on HTC is based on the current perceived failure of the general PC industry, particularly Acer. Despite the fact that Acer has grown into a global company, the speed of technology & innovation by competitors such as Apple has shifted growth away from Acer’s hardware business model. When putting HTC side by side, HTC is on a

similar path with Acer’s branded strategy. In this competitive environment, HTC has to decide its next move toward long term growth. The motives of this thesis are to show the competitive environment of the hardware industry and the need for value creation.

b. Data Collection

Most financial data is collected from the annual reports and from the Taiwan Economic Journal (TEJ). TEJ has been collecting and printing financial and general information of the Taiwan industry for more than 10 years. It is considered a trustworthy source. In some cases where financial data is not readily obtained, secondary sources such as business journals, magazines, and newspapers are used. There are also good sources of interviews with executive leadership and professionals from related industries. Each of these articles also comes from respected sources such as Wall Street Journal, New York Times, Economics…etc. Smartphone industry data came from Gartner and IDC, two research companies in the global IT industry.

This costly research from Gartner / IDC were sponsored by Macquarie Securities / Citibank.

Research from Vision Mobile, a market analysis and strategy firm, was also used. Other book sources were used to complement the research and support the arguments.

2 c. Structure of the Study

The structure of this thesis will be divided into six sections. The first section discusses the motivation behind the HTC topic and the data collection. Section two will discuss the literature review concepts that will be utilized in this thesis re: Organic Growth, Inorganic growth – M&A, and Organization Structure & Design. In the third section, the company background will be examined followed by the inorganic growth analysis in Section four. Section four will explore HTC’s financials, market share, product mix, organization structure and roadmap analysis.

Section five is about the acquisition of Saffron Digital in detail and the rationale behind it. Last section concludes on HTC’s strategy for the future.

II. Literature Review a. Organic Growth

Corporate entrepreneurship, innovation, or organic growth according to Peter Drucker is often the end result of management developing the principles, practice, and discipline (Drucker, 1985). The definition of organic growth is the process of expanding overall customer base, increasing output per customer or representative and new sales. To execute organic growth, companies must have the “strategy and practice of conceiving, fostering, launching and managing new businesses – not just new products or services” (Robert C. Wolcott, 2010). As companies grow, they evolve structures, processes and cultures that emphasize efficiency in addressing their business markets. Operation rules are implemented and then supervision is added to manage operations. Standard of operations “SOP” are standardized at the end. For an enterprise to grow its core efficiently, this standardization is a positive thing (Mintzberg, 1979).

3

Many executives often speak of mergers & acquisition “M&A” as drivers to company growth, which “many large corporations do better at corporate entrepreneurship and organic growth than most people think” (Robert C. Wolcott, 2010). The myth that large companies are not good at new business creation is in many ways untrue. An example would be Boeing’s development and the launching of the 787 Dreamliner airplanes. The resources, capabilities and credibility of an established company were the keys to enable such development. An acquisition would most certainly delay the already late Dreamliner airline (Kesmodel, 2011).

To state again, organic growth represents the true growth for the core of the company as it means the growth rate that a company can achieve by increasing output, such that new sales channel without the profits from takeovers, acquisition or mergers that make up inorganic growth.

Companies that grow organically believe greatness comes from its work in process, execution ability, behavior, alignment in culture, structure, HR, and engineering processes (Hess, 2006).

Although there are many literatures about the growth via M&A (Sirower, 1997) and how companies lose in acquisition, organic growth also has flaws that must be considered. According to a well-known economist Edith Penrose's book “The Theory of the Growth of the Firm,” she pointed out that organic growth has many limits and assumptions. Growths that proceed in linear fashions only keep expanding if there are unlimited amounts of resources. One example she provided was that if an individual puts emphasis on one project, he/she may not be able to focus on an existing project that was necessary for the planning and execution of company goals.

Individual or groups of individuals can only physical do a maximum number of things at once.

Market uncertainty and risk is also a concern for organic growth theories. The fact that the future can never be known with accuracy means that the planning of business firms is based on

4

expectations of the company executives. Penrose concluded that a firm’s expansion plans are restricted by risks and uncertainty that it faced (Penrose, 2009).

b. Inorganic Growth

In finance literature, inorganic growth strategies refer to external growth by takeovers, mergers, and acquisition or simply mergers & acquisitions (“M&A”). These terminologies are frequently used synonymously, although there is a clear difference in the economic implications of takeover and merger (Singh, 1971). Together, M&A is fast and allows the immediate

utilization of acquired assets (Bruner, 2004). These types of strategies are vehicles that help companies enter new markets, expand increase clients, cut competition, and grow quickly. With acquisition, the buyer could quickly employ new technology with respect to products, people, and processes. As a result, there would be a higher chance of unlocking shareholder value for the company (Bruner, 2004).

5 Illustration 1 – Growth Strategies Flow Path

Inorganic growth strategies are a big part of the corporate finance world. Every day investment bankers from multinational corporations (“MNC”) or boutique investments banks arrange M&A deals by bringing opportunities up to the buyer and the target (“seller”). On the other hand, if a company is looking to get smaller, deals can also go the opposite direction and breakup (“spin off”). For a company to grow inorganically, one could either enter into strategic alliances, joint ventures with a partner, or grow through M&A.

According to Aswath Damodaran, a professor of finance at NYU Stern’s School of Business, he said there are many forms of acquisitions. Acquisition can be either mergers or

Growth Strategies

Source: Inorganic Growth Strategies, Latha Chari

6

consolidation, acquisition of equity (“stock shares”), or assets (Damodaran, 2002). A merger refers to the combined effect of one firm by another, which suggests that the buyer would retain the target and all its assets and liabilities. Acquisitions are similar to a merger in the sense that the motives be a degree of control in the company’s business, except that the acquisitions are of the assets or the stock shares. Acquisition of stocks, refers mainly the acquirer will have more voting rights. These voting rights will allow the acquirer to be more involved in the company strategies. Acquisitions of assets on the other hands is where a firm can acquire another firm by buying all of its assets or specific assets, avoiding potential problems of having resisting minority shareholders (Damodaran, 2002).

Types of Mergers

1. Horizontal merger: Merging two companies with similar type of business operations is called a horizontal merger. The rationale behind this type of merger is to achieve economic scale or scope in the production procedures. Typical horizontal mergers are often used as a way to decrease firm competition within the same industry (McPherson Gordon, 2012). For example, the merger between Microsoft and Yahoo would have a horizontal merger in the search side of Microsoft’s business. A more recent horizontal merger in the technology space would be the establishment of Global Foundries Inc. It is a merger of AMD’s chip manufacturing business and Singapore Chartered Semiconductor Manufacturing company.

2. Vertical merger: The goal of this type of merger refers to a situation where a company is combined with a complementary business within a value chain. For instance, a pure

7

foundry company may merge with a fabless (design house) to become a more rounded manufacturer. With this consolidation, the hope is that the company can do both design and manufacture of the chips and also implement its chips through more channels and customization. There are many other reasons for vertical integration mergers. The primary reason is the reduction of uncertainty regarding the availability of quality inputs, and also the uncertainty regarding the demand for its products. This integration may also allow economies of integration, which would make firms more cost efficient because of lower distribution and production cost. Firm resources would be used at more optimal levels (McPherson Gordon, 2012). An example of a recent vertical merger would be software giant Google’s acquisition of the Motorola's device manufacturing sector.

3. Conglomerate merger: This is when two vastly different companies merge, such as a technology company and an industrial company. In most cases, companies would act in this type of merger when their businesses have reached a mature stage with very little opportunities for growth. To continue to grow for its shareholders, companies will seek to diversify their business through mergers and lower the overall risks. While this type of merger does not appear to provide any benefit other than diversification, the potentially diversification could lead to new channels for existing company businesses (McPherson Gordon, 2012). An example of this would be the Asia Cement acquiring a small portion of Far East Telecommunication as a way to diversify its operation. The question one asks is why would a cement company also operate a telecommunication company?

8 c. Motives for Mergers & Acquisitions

Efficiency Theories: These theories include differential efficiency theory and inefficiency theory. Differential theory suggest that if company A is more efficient than company B and both companies are in the same industry, then A can raise the efficiency of B to at least the level of A through a M&A transaction. Inefficiency theory suggests that the same company B’s inefficiency is public knowledge and that not only company A but also the controlling group in any other industry can bring company B’s efficiency to acquirer’s own level through M&A (Thomas Copeland, 1988).

Synergy Theory: Through the efficiency theories raises the synergy theory, which can be interpreted as a result of combining and coordinating the value added parts of a company with the redundant parts of the company.

a. Staff reductions: The general meaning here is the better allocation of resources through staff reductions. Whether it is to replace inefficient staff with more efficient staff or the disposal of redundant/ or unprofitable divisions (Stephen A.

Ross, 2006).

b. Economies of Scale: Synergy can also be a consequence of economies of scale, in both operational and financial standpoint (Richard Brealey, 2002). With

economies of scale, the firm can bring down the production or distribution cost and/or lower the marginal cost of debt and higher debt capacity.

c. Acquire new technologies: Sometimes acquiring new yet proven technologies by a larger firm may prove to be synergistic. To stay competitive, the new

technologies would provide the company an opportunity to maintain or develop

9

its competitive edge. A successful acquisition however would depend on how the company can utilize new technologies with existing platforms and the integration of firm cultures (Cheng F. Lee, 2006).

Diversification Hypothesis: This hypothesis states that M&A occurs due to management’s interest in protecting their human capital that is crucial to its own compensation by diversifying.

According to Harvard Business School economist Michael Jensen in his journal, “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure,” he argues that managers do not have the capacity to diversify while the company shareholders could. Managers’

compensation is very dependent on performance of their company. It would be in the interest of the company to diversify at a level to protect the employees (Michael Jensen, 1976).

Stock Market Driven Acquisitions “SMDA”: In this theory, there is an important motive for firms to make acquisition finance by its overvalued stocks. By acquiring through stocks rather than cash, the perception is that the acquirer gains at the expense of the target and the merged firm loses value. (Robert Vishny, 2003)

d. Organization Structure & Design Strategy

Michael Porter in his book “Competitive Strategy: Techniques for Analyzing Industries and Competitors” describes business as having three generic types of strategies that are common to maintain competitive advantage. They are cost leadership, low cost leadership, and focus. The focused strategy, because of its concentration on specific market or buyer group, is further divided into focused low cost and focused differentiation. In total there are four basic strategies, as shown below in the table (Berman, 2002). Porters discussed how companies who adopted a low-cost, differentiated or focus strategy achieved higher average profits compared to those that

10

did not adopt one of the three strategies. However, he also emphasized that managers also need to maintain flexibility in their strategic thinking (Daft, 2010).

Illustration 2 – Competitive Advantages

1. Low Cost leadership: An example of a company with low cost leadership strategy would be that of notebook suppliers. The strategy’s primary goal is to increase market share by keeping costs low compared to its competitors. To keep costs low, the company must continuously seek efficient facilities; pursue cost reductions, and use tight controls to produce products or services more efficiently than its competitors (Daft, 2010).

2. Differentiation: In a differentiation strategy, organizations attempt to distinguish their products or services from others in the industry. According to Porter, uniqueness does not lead to differentiation unless it is valuable to the buyer (Porter, 1998). An organization may use advertising, special product features, unique customer service or new technology

Focused low‐cost leadership Low Cost leadership

Focused differentiation Differentiation

Competitive Advantage

Low Cost UniquenessBroad

Narrow

Competitive

Scope

Source: Understanding the Theory and Design of Organizations, Richard Daft

11

to achieve the differentiation perception. This strategy usually targets customers who are not particularly concerned about the pricing of the products or services, so the strategy can be quite profitable. Apple is a good example of a company that believes in the differentiated strategy. They care about both the design and feel, but also how the products integrate to people and software. While this strategy may help reduce

competition from substitute products, company will require a number of costly activities in the design and structure of the company to be successful.

a. Give time and resources to strong marketing abilities and creative employees b. Revolving business on product or service

c. Increase in R&D for software integration and design

3. Focused: The focused strategy is another step further in a differentiated and low cost strategy. In this strategy, the organization will concentrate on a specific regional market or buyer group within differentiated or low cost strategy. A good example of a company with a focused strategy would be Toyota’s Scion cars. Toyota was able to produce a stylish car for the younger 18-34 years age group.

III. HTC Background & Industry Analysis a. Introduction of HTC

Functioning originally as an equipment manufacturer “OEM” and later transformed into a manufacturer “ODM”, HTC was the key supplier of telecommunication companies such as T- Mobile, Vodaphone, NTT Docomo, and Orange. Based on its success as an effective supplier in 2006, HTC decided to launch into a brand strategy targeting PDAs and smartphones under its

12

new “HTC” brand name. The company was founded in 1997 by Cher Wang, HT Cho and Peter Chou (David B Yoffie, 2009).

In 1997, HTC focused on the notebook industry new innovation of Pocket PC technology.

Slowly becoming a key player supplying in this field, HTC later joined with Microsoft in the development of devices using the Windows CE operating system (David B Yoffie, 2009). In cooperation with Microsoft, HTC eventually attempted to design its own Pocket PC models for consumers. Even though HTC’s first PC Pocket prototypes earned many technological

innovation awards, HTC was initially losing money in the venture of this competitive industry.

At this stage, HTC was still relatively immature in its technology skills, software, and design for Pocket PCs. As a result, HTC decided to focus on handheld devices and invested heavily into R&D for the next few years (Weitao, 2005).

HTC’s major breakthrough came in 2000 when HTC obtained a contract to supply the IPAQ for Compaq, a well-known brand at that time until it was acquired by HP in 2002

(www.compaq.com). The IPAQ was a commercial success in the market and proved to the technological world the competence and design manufacturing of HTC. With the success of the IPAQ, HTC realized that they wanted to be unique, so they started to design customized phones with the various carriers in the US & Europe. With the acclaimed design manufacturing &

hardware, the successful launch of handspring products & Palm Treo phones followed afterward.

By 2004, HTC had USD$1bn in revenues. In 2006, HTC’s revenues had reached USD$2.2bn.

b. Evolution of HTC

The success of HTC can be attributed to the many decisions it made in terms of transforming from the traditional ODM to a global brand that it is today. In the beginning, HTC was only known to a select few specific large telecom companies that were turning them for ODM jobs.

13

The many phones HTC designed and manufactured for others included the IPAQ, Palm Treo 650 and the famous T-Mobile G1 (first android enabled smartphone). Additionally, HTC made an aggressive move toward its hardware design department and introduced many “first” into the market. It was the 1st company to produce Microsoft’s 3G smartphone, 1st to develop the android phone (T-Mobile G1), and the 1st official Google phone (Nexus One).

Going through many well managed risks one after the other, the 10+ years old HTC had caught the attention of global players such as Samsung, LG, and even Apple. With their multitude of successful hits, it’s no wonder that HTC would want to start redefining themselves as a global brand instead of an ODM company. Their heavy focus on design of each and every one of their products became the basis for the company (David B Yoffie, 2009).

Adapting American Business Ideals

There is one important aspect about HTC’s operations really set it apart from other

Taiwanese manufacturers. Right from the start, CEO Peter Chou had set up a rule that each HTC employee had to have proper English language training. Even though the company was based in Taiwan, Chou had envisioned a company with a global impact. In order to achieve this, he had HTC adapted to one of the most avant-garde American Business ideal. Employees had to embrace the idea that failing was actually tolerable within the company. Horace Luke, the ex- Chief Innovation Officer at HTC mentioned that the “target failure rate of 95%” did exist in the R&D division. He explained that in order to maximize the full potential of the department, it all boiled down to how well the company can retain the good ideas from all the bad ones. It is better to fail fast and early rather than later, which he quoted: “That’s very different from the culture at Taiwan, where you have to be successful all the time.” (Ganapati, 2009)

14 Effective Marketing Campaign

HTC set out to change the mobile industry with a brand position they called “Quietly

Brilliant.” In order to inform every one of its decision to become a global consumer brand, HTC decided to launch what they called the “YOU” campaign across 20 countries to promote their entry into the mobile market. The basic tagline for the campaign was “You don’t need to get a phone. You need a phone that gets you”. The idea is to emphasize on HTC’s goal to focus on the people, their needs, and how can a HTC mobile device suit them. (Video from HTC’s official YouTube subscription)

The YOU campaign was centered at delivering “broad, global visibility and understanding of HTC’s unique brand promise” which is all about the consumer and not just the device. CEO Peter Chou said HTC aimed for more than 40% global brand recognition by the end of 2010. By 2011, HTC’s name will go head to head with other current major global brands. This campaign was only the first of many to carry out the Quietly Brilliant brand positioning of HTC, and showed the world that HTC is truly an innovative company.

15 Illustration 3 – HTC’s Timeline

c. Mobile Phone Industry

This industry is comprised of many moving parts. There are the operators, the designers, the manufacturers, and the software developers; and all of them play a critical role in the mobile phone industry. In addition, the industry is also defined by two business approaches: the vertical model of companies like Apple & RIM or the horizontal model of smartphone companies like HTC, Samsung and LG (in PCs it was Acer, Asustek & HP). In the Vertical model, Apple is involved in all parts of the development such as software and hardware. On the other hand, companies like HTC are primarily involved on the hardware side of the business and followed the horizontal approach.

Source: Harvard Business Case - "HTC Corp in 2009" by David B Yoffie, Renee Kim (2009)

16 Figure 1 – Smartphone VS Feature Phone in 2011

The mobile phone industry is divided into two primary categories —feature phones and smartphones. Feature phones, which is the by-product outcome of simple phones (B/W screens, dial pad, address book) target consumers rather than business users with its unique features, design or size. These feature phones are usually in the mid-price range with a standard UI and function such as music players, basic calendar and camera.

With the entrance of smartphones into the marketplace along with more advanced wireless networks, the demand skyrocketed. To effectively use the improving wireless networks, business users demanded better productivity tools, such as “push” e-mail that delivered faster mobile communication. These desires for productivity provided an opportunity for various software giants to create the various operating systems, user interfaces, and unique screens.

17 Figure 2 – Global Smartphone Operating Systems

Source: Public Technology Websites – Engadget, Phonearena

As smartphones added cameras, music, GPS, and games, consumers started to adopt high end smartphones. As a result, feature phones started decreasing. While feature phones continue to dominate today, many phone vendors such as HTC, Samsung, LG, Motorola have started to launch lower end / mid end smartphones to convert the feature phone users.

IV. Inorganic Stage Analysis

The business environment today is constantly changing with respect to competition, products, people, unique processes, manufacturing, market segments, customers and intellectual properties.

All of these are the necessities in the daily operations of a company. For a company to beat competitors and increase shareholder value, the company will need to surpass all these environmental elements. Since the founding of HTC in 1997, the company had adapted its capabilities with market needs and is now a well-known brand globally. Within the last couple years, HTC entered an inorganic growth phase by acquiring businesses that can add value to the sustainability of the company. This section aims to understand the reasons for acquiring new

Platform Platform Owner Initial OS Launch Geographic origins Current Status

Android Google 2008 US Leads in smartphone sales

Bada Samsung 2010 Korea Little market share in Korea

BlackBerry OS RIM 2000 (Java) Canada Replaced by new QNX OS

BREW Qualcom 2001 US Weak OS, almost nonexistant

iOS Apple 2007 US Leads in Tablets, and proven

OS

Symbian Nokia 2000 Europe Phasing out

webOS HP 2009 US Acquired by HP, cancelled to

be open source

Windows Mobile Microsoft 2002 US Phasing out to WP7

Windows Phone Microsoft 2010 US Great reviews, unproven OS

18

businesses by looking at its financial statements, market share & product mix, organization structure & design strategy, and the road map analysis.

a. Financials

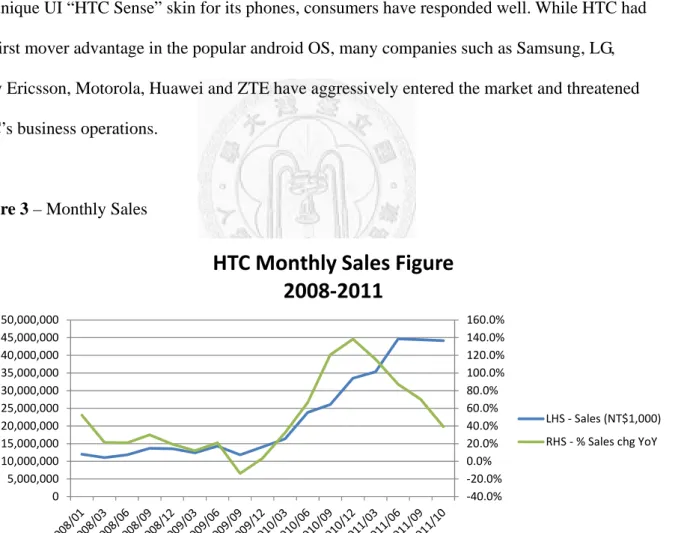

From looking at the annual reports for HTC, it is evident that HTC has been quite successful.

The company was able to position itself as a high end brand and continued to be an important brand in the smartphone industry. By entering the market through its own brand and providing the unique UI “HTC Sense” skin for its phones, consumers have responded well. While HTC had the first mover advantage in the popular android OS, many companies such as Samsung, LG, Sony Ericsson, Motorola, Huawei and ZTE have aggressively entered the market and threatened HTC’s business operations.

Figure 3 – Monthly Sales

‐40.0%

‐20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

0 5,000,000 10,000,000 15,000,000 20,000,000 25,000,000 30,000,000 35,000,000 40,000,000 45,000,000 50,000,000

HTC Monthly Sales Figure 2008‐2011

LHS ‐ Sales (NT$1,000) RHS ‐ % Sales chg YoY

Source: HTC Annual Reports – 10K, 10Q

The chart above looks at the top line growth by month from 2008-2011. According to the chart, HTC’s brand initiative did not blossom until late 2009. However, the sales growth was

19

aggressively high with YoY % growth of 3.6% in December 2009 and spiking to 212% YoY % sales growth in January 2011. The average YoY % growth from November 2009 to May 2011 was 99.6%. One thing to notice was that the sales growth started to mature. According to HTC’s statement filed to the Taiwan Stock Exchange, unconsolidated sales in January 2012 fell 53.52%

to NT$16,108,401,000 from NT$34,654,934,000 in January 2011. With sales growing less than expected, while competition remaining fierce, the stock price started to decrease. The company’s month high closing price was NT$1,187 on April 2011 but dropped all the way to NT$477 on November 2011 as seen in the figure below.

Figure 4 – Stock Price & PE Ratios

Source: Macquarie Research, Citi Research

The figure above represents the downward trend of HTC’s stock price with its P/E ratio from the Taiwan Stock Exchange. Despite many quarters of record breaking revenues and EPS, investors always look at future forecasts as a mean to buy a stock. Below is a chart showing the

0.0x 5.0x 10.0x 15.0x 20.0x 25.0x 30.0x 35.0x

0 200 400 600 800 1000 1200 1400

2007/12 2008/03 2008/06 2008/09 2008/12 2009/03 2009/06 2009/09 2009/12 2010/03 2010/06 2010/09 2010/12 2011/03 2011/06 2011/09

Stock Price & P/E Ratio 2008‐2011

LHS ‐ Stock Price RHS ‐ P/E‐TSE calc.

20

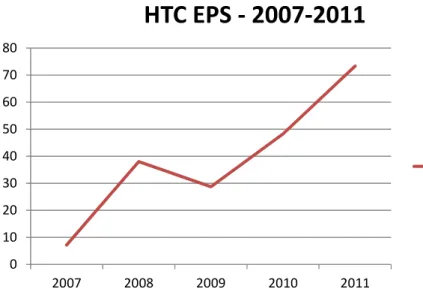

EPS growth from NT$7.15 in 2007 to the NT$73.32 in 2011. By looking at the EPS, it appeared that the company was doing well. However, stock performance is forward looking and analysts like to be certain the company can outperform. To justify a high stock price, HTC would need to increase its margins, gain market share, and find alternative revenue streams. Given the lack of technological opportunity, lack of innovation & technical personnel and the lack of market opportunities in Taiwan, investor will have a higher pressure for HTC to improve company financial results.

Figure 5 – HTC Earnings Per Share

Source: Macquarie Research, Citi Research

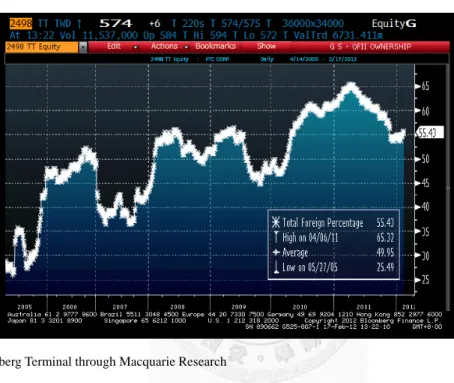

HTC’s competitive environment has intensified so much that Qualified Foreign Institutional Investors (QFIIs) have started to take money out of HTC. By looking at the chart below through the Bloomberg terminal, the average HTC QFII % holding from 2005-2011 was 49.95% with high of 65.3% in 2011 (Bloomberg) while average QFII % holding in general (Tech+fcial+

nontech) was around 33%. This showed that HTC’s investors were starting to lose faith, taking

0 10 20 30 40 50 60 70 80

2007 2008 2009 2010 2011

HTC EPS ‐ 2007‐2011

EPS (NT$)

21

money out of the company and reinvesting it into other companies for growth. In order for foreign institutional investors to start investing again, HTC will need to innovate aggressively to get back to its old QFII holding %.

Illustration 4 – QFII Holding for HTC

Source: Bloomberg Terminal through Macquarie Research

In the next section, the smartphone industry along with company product portfolios will be discussed to strengthen its inorganic growth rational.

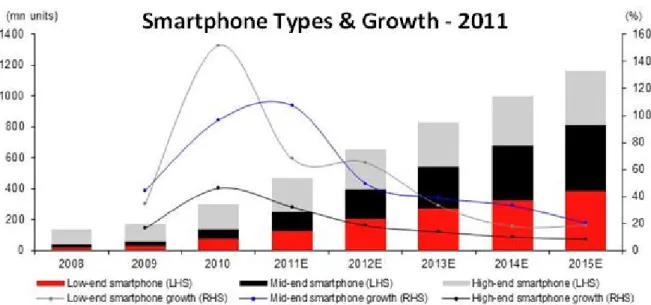

b. Market Share & Product Mix

Despite the tremendous growth of the smartphone industry, HTC has been a beneficiary of higher end smartphone devices with higher average selling price since the beginning. According to Macquarie Analyst Daniel Chang, high-end smartphones for HTC should account for 50%+ in 2Q11. With the strong contribution from these high end phones, the average selling price (“ASP”) was likely to come down, affecting the company margins and profitability. Looking at the chart

22

below from Gartner, the high-end smartphones which HTC focused on, it was clear that it was low on growth versus the mid and low end. Furthermore, companies such as Samsung, LG, Motorola, Tier 3 brands, Huawei and ZTE have entered aggressively under the android OS platform. Apple continued to dominate in its iOS thus pressuring HTC to launch low-mid end devices at lower prices. Android, iOS, Symbian (Nokia), RIMM, and Windows OS account for 51%, 24%, 12%, 9% and 2% global market share respectively in the 4th quarter of 2011 (Gartner, 2012).

Figure 6 – Smartphone Type Growth 2011

Source: Gartner Research 2011, Macquarie Research

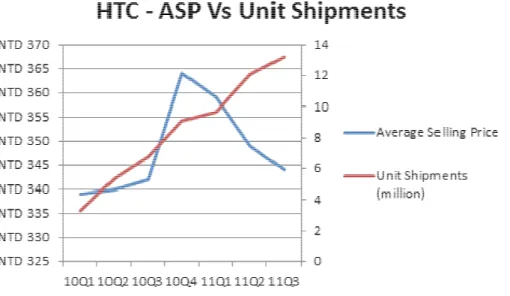

Pressures at HTC were mounting due to slow growth in high end phones and competitive threats from companies with experience in volume cycles. Looking below, we noticed the

average selling price of HTC phones increasing to its high of US$364 and decreasing throughout 2011 as seen from the figure below. The reason for the ASP decrease was due to operators

23

shifting away subsidies from the high end smartphones launched by tier one brands to mid or low smartphones. With this unexpected change, HTC had to change its product mix in 2011 in order to compete on pricing. Phone launched that are less than US$300 were HTC ChaCha, HTC Explorer, HTC Salsa and the HTC Wildfire.

Figure 7 – HTC ASP VS Unit Shipment Graph

Source: HTC Annual Report – 10K, 10Q

According to Gartner, the dominate OS is clearly Android with around 47% of the 471 million units smartphone industry in 2011. IOS itself through Apple is in second place with 20%

of the smartphone industry. While Android OS went from 67 million units to 219 million units, Android OS has grown as a consequence of the open source platform and the decreasing popularity of Blackberry OS, Symbian, Windows OS.

24 Figure 8 – Operating System Market Share & Growth

Global Smartphone Market Share (1,000 units) 2010 1Q11 2Q11 3Q11 4Q11 2011 Total

Android 67,220 36,350 46,776 60,490 75,906 219,523

Growth QoQ 29% 29% 25%

Symbian 111,580 27,598 23,853 19,500 17,458 88,410

Growth QoQ ‐14% ‐18% ‐10%

iOS 46,600 16,883 19,629 17,295 35,456 89,263

Growth QoQ 16% ‐12% 105%

Research In Motion 48,000 13,004 12,652 12,701 13,184 51,541

Growth QoQ ‐3% 0% 4%

Bada NA 1,862 2,056 2,479 3,111 9,508

Microsoft 12,380 2,582 1,724 1,702 2,759 8,767

Other NA 1,495 1,051 1,018 1,167 4,730

Grand Total 99,775 107,741 115,185 149,042 471,743

Source: Vision Mobile, 2011

Although RIM and Microsoft have begun investing back into its OS, both companies have had a tough time attracting new users from the likes of Android and iOS. Symbian from Nokia on the other hand was discontinued and started to develop Windows Phone 7 OS phones.

In the android platform, vendors have the ability to create its own phones with the OS and differentiate itself. For example, Samsung has been successful because of its conglomerate manufacturing, bargaining power, and Amoled screens. HTC has been successful with its unique design and HTC Sense UI. Huawei and ZTE from China have been successful because of its low cost manufacturing and low price phones. The graphs below show HTC’s market share in

android, decreasing from 50%+ in 2009 to 18% in 3Q11. Although market share is only a partial story, the graphs shows the losing competitive edge of HTC to companies such as Samsung and Huawei. At the end of the day, profitability is a better measurement of performance.

25 Figure 9 – Android Market Share Breakdown

Source: Gartner Research, Macquarie Research

c. Organization Structure & Design

It is quite often that companies do not have a clear competitive strategy. Whether the

company believes in a differentiated strategy or a cost leadership strategy, many companies may be conflicted because of the hybrid attempt. For HTC, a differentiated strategy will allow it to be

Global % breakdown by Android Vendor 1Q11 2Q11 3Q11

HTC 22% 22% 18% ↓

LG 11% 10% 7% ↓

Motorola 11% 9% 7% ↓

Samsung 28% 31% 35% ↑

Sony Ericsson 9% 8% 9% −

ZTE 2% 4% 5% ↑

Huawei 7% 6% 7% −

26

more sustainable in the long term because of non-conflicting mentality on high price phones with low price threats. While the company knows it needs to be differentiated, it has performed with mixed reviews. According to HTC UK’s CEO Phil Robertson, he said: "We have to get back to focusing on what made us great – amazing hardware and a great customer experience. We ended 2011 with far more products than we started out with. We tried to do too much. So 2012 is about giving our customers something special. We need to make sure we do not go so far down the line that we segment our products by launching lots of different SKUs" (Millett, 2012). Mr.

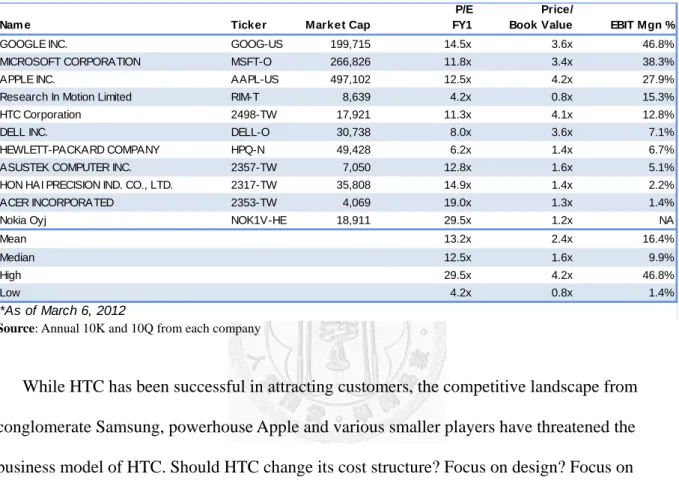

Robertson discussed how HTC wants to refocus on hardware and its software experience. With a congruent experience from fewer HTC devices, this experience will provide customers a truly valuable smartphone.

Historically speaking, it has been tough for Taiwanese companies to get out of the cost leadership mindset. For example, some of Taiwan’s biggest industries include LED, computers, LCD, components, and electronic manufacturing – all of which focused on being low cost. In these industries, market share generally suggested the success of the company. Acer, now a global provider of notebook PCs, has since gained an enormous amount of market share worldwide through its outsourcing strategy. Acer retreated from its ODM “low cost strategy”

business in 2000 and focused on branding. By outsourcing its manufacturing downstream into a competitive environment, Acer can manufacture at low prices while charging higher prices. It can been seen in Acer’s financial statements that after the divestiture of Wistron, the company’s EBIT margins improved from 1.6% in 2001 to 2% in 2002. Additionally, the company increased its revenues from 30bn NT$ in 2001 to 629bn NT$ with a 2.8% EBIT margin in 2010. Despite the market share gains and increased revenues by 21x since 2001, the company’s design structure

27

failed to implement a sustainable differentiated strategy as margins went downwards since the end of 2010 (Acer Group, 2011).

Figure 10 - Operating Margins by Comparable Companies

Nam e Ticker Market Cap

P/E FY1

Price/

Book Value EBIT Mgn %

GOOGLE INC. GOOG-US 199,715 14.5x 3.6x 46.8%

MICROSOFT CORPORATION MSFT-O 266,826 11.8x 3.4x 38.3%

APPLE INC. AAPL-US 497,102 12.5x 4.2x 27.9%

Research In Motion Limited RIM-T 8,639 4.2x 0.8x 15.3%

HTC Corporation 2498-TW 17,921 11.3x 4.1x 12.8%

DELL INC. DELL-O 30,738 8.0x 3.6x 7.1%

HEWLETT-PACKARD COMPANY HPQ-N 49,428 6.2x 1.4x 6.7%

ASUSTEK COMPUTER INC. 2357-TW 7,050 12.8x 1.6x 5.1%

HON HAI PRECISION IND. CO., LTD. 2317-TW 35,808 14.9x 1.4x 2.2%

ACER INCORPORATED 2353-TW 4,069 19.0x 1.3x 1.4%

Nokia Oyj NOK1V-HE 18,911 29.5x 1.2x NA

Mean 13.2x 2.4x 16.4%

Median 12.5x 1.6x 9.9%

High 29.5x 4.2x 46.8%

Low 4.2x 0.8x 1.4%

*As of March 6, 2012

Source: Annual 10K and 10Q from each company

While HTC has been successful in attracting customers, the competitive landscape from conglomerate Samsung, powerhouse Apple and various smaller players have threatened the business model of HTC. Should HTC change its cost structure? Focus on design? Focus on software, or focus on capacity? Answering these questions will serve HTC’s future corporate strategy and prevent itself from the likes of notebook manufacturers – Acer, Asus, Dell, HP, all focused on hardware specs and low costs. In short, if HTC’s smartphone does not grow its software / platforms through inorganic growth, the company may end up losing its competitive edge in hardware industry.

28 d. Acquisition Analysis & Roadmap

HTC’s investments into the various companies can be explained with the diversification theory and the synergy theory. By acquiring value added software enhancement companies such as Abraxia and Dashwire, HTC can enhance the experiences of its users by adding new technologies to the UI. With an increase in the overall friendliness of the customized Android OS and Windows OS, HTC’s brand name is becoming more valuable. Along with software

acquisitions, HTC also invested in various businesses such as Saffron, KKBOX, Onlive and Beats that aims to pave the path for HTC’s future.

1. Saffron Digital - Since the US$48 million acquisition, the company has integrated the technology to HTC phones and tablets under “HTC Watch”. With the HTC Watch application, users are able to stream movies and TV shows through any internet connection. This application would act as the digital video content for HTC. This particular acquisition will be analyzed in depth in the next section.

2. KKBOX – In 2011, HTC acquired an 11% stake in KKBOX for US$10 million. KKBOX is an online subscription based music service provider. The service has been launched in Taiwan, Hong Kong and Japan.

3. Onlive – The US$40 million dollar investment in Onlive aims to make HTC the ultimate gaming machine. The idea here is the ability to play games on mobile devices without the need for a separate console.

4. Beats – To watch movies, listen to music and play videos games all require headphones or music software. It’s an even better incentive that the headphones are stylish and durable. HTC acquired a 51% stake of Beats by Dre for US$300 million which is a JV involving Dr. Dre and Interscope record Chairman Jimmy Iovine.

29

By investing, acquiring and partnering with these various companies, HTC has not only diversified its risks in being strictly a hardware company but added intangible value for the HTC phones. Looking at the roadmap below, the strategic rational can be seen similar to Apple’s model. While the company is not an exact comparable, HTC’s forward strategy is looking to be more sustainable when compared to hardware companies.

30 Illustration 5 - Roadmap of Industry VS HTC

Source: Personal Analysis, Public Knowledge

31 V. Saffron Digital / Digital Content Analysis

HTC’s US$48 million acquisition of Saffron Digital, now HTC Watch for HTC, was a rational decision. Below is an analysis of the acquisition conducted with industry trends & M&A activities and its business environment. Although the acquisition is still at its infant stage, the proof below will allow the reader to understand why the acquisition was rational and that HTC made a good choice in Saffron Digital.

In brief, Saffron Digital is a London-based company that specializes in the mobile content delivery services focusing around video. According to Saffron’ s then Chief executive Shashi Fernando, the company will continue to be an independent company and serve its clients such as Sony Ericsson, Nokia, Microsoft Vodaphone, T-Mobile, UK Broadcaster Sky and Paramount Digital Entertainment. He also said “The idea is that our technology allows you to get closer to the iTunes ecosystem in the delivery of a connected home and on the move.” Thus suggested that this technology is essential to combat the forces of Apple’s iTune media software (Bradshaw, 2011). The company is listed in the Deloitte Technology Fast 50 2010, has been named one of UK’s top 100 technology and media companies in the Tech Media Invest Top 100 for 2009/2010 and was named Best Video Service Provider in the Mobile Entertainment 2010 awards.

(Business Wire, 2011)

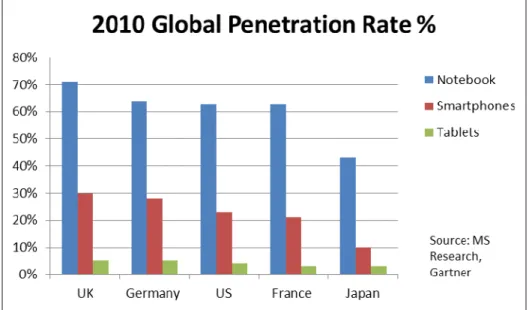

a. Cloud Computing Trends

Driven by trends like cloud computing, software as a service, social networking, and mobile communication, HTC needs to bolster its information technology, particularly to cloud computing if it wants to create sustainable value for its current and prospective customers. The acquisition of Saffron followed the economic transformation of the global technology

environment to operate in the “cloud.” For example, music use to be purchased and listened

32

physically, however the business model has changed to “cloud” music. In this method, music is selected through the use of the internet and is automatically downloaded to the music player or device. Similarly, internet delivery services such as video conferencing and streaming video content are also cloud computing innovations. As internet usage becomes standard as seen in the chart below, with penetration rate as high as 70% in the UK, and with smartphone and tablet usage rising, it is safe to say that cloud computing innovations will be part of the future.

Figure 11 – Penetration Rate

According to Accenture’s Video Over Internet Consumer Usage Survey, a survey of more than 6,500 consumers around the major markets, the video viewing habits have changed

dramatically and new business models have emerged. While the survey suggested that

“consumers are still watching traditional TV, but they’re also viewing content over an amazing range of other devices and interacting with content and people during the viewing experience”

(Accenture, 2011). In fact, 85% of people age 18-24 are internet video consumers and even

33

consumers over the age of 65, 2/3rd of the survey responders were joining the internet video movement. One key finding in the survey was that consumers liked special features such as the ability to watch videos in multiple devices, which was possible from the Saffron acquisition. The point from these survey results suggested that the traditional video business model (big box retailer and TVs) were no longer the dominant form of video content delivery. Consumers wanted compelling functions such as video storage, customization of content, and ease of use in multiple platforms such as Laptops/Desktops, mobile devices and tablets such as the iPad.

To further demonstrate the correlation of HTC’s Saffron acquisition with market demands, M&A has been growing. In the first quarter of 2011, Global IT M&A have gone up 26%, 794 reported acquisitions, with total value up 124%, at a value of US$27 billion. According to Joe Steger, a Global Technology Transaction Services Leader at E&Y, stated that “These trends speak to the rapid pace of change driven by the cloud, social networking, smartphone mobility, and the way in which technology is becoming an increasing part of everyday life – not just something we do at work. On the business side, the trends reflect that information is becoming a larger component of the value of all products and services” (Steger, 2011). The use of mobile and internet began to soar in 2010 for entertainment, business conferencing and personal video calling purposes. Thus many multinational companies were responding by acquiring strategic companies. Since HTC acquired 100% of Saffron for cloud computing digital media, Taiwan based Acer acquired iGware, a cloud computing company with the infrastructure tools for portable devices for US$395 million (Ben Boissevain, 2011).

In terms of HTC’s 100% acquisition of Saffron, it was very difficult to determine if the valuations was fair given the limited information on Saffron. However, given the market’s demand for these types of companies, precedent transactions had revenue multiples at around

34

4.1x and EBITDA multiples of around 20.3x which were much higher than 2011-2012 tech valuations of 2.0x revenue multiples and 8.1x EBITDA multiple. As an established company like HTC continue to acquire small cloud companies, the universe of good acquisitions targets will shrink with valuations ultimately falling back to the norm. Although Saffron may be an expensive acquisition, the justifications to acquire it are the following:

1. New technologies for the company - digital content capabilities, software, licensing 2. Talented employees, technical engineers

3. New channels of distribution Figure 12 – Precedent Transactions

Date Announced Acquirer Target EV Revenue EBITDA EV/Revenue EV / EBITDA

4/27/2011 CenturyLink SAVVIS $2,962.68 $973.44 $229.18 3.0x 12.9x

4/4/2011 APAX Partners Epicore Software $951.45 $453.29 $54.35 2.1x 17.5x

3/11/2011

Golden Gate Capita;

Infor global solution Lawson Software $1,779.35 $755.16 $134.36 2.4x 13.2x

2/14/2011

EchoStar Satellite Services

Hughes

Communications $1,941.52 $1,043.33 $209.01 1.9x 9.3x 2/1/2011 Time Warner Cable NaviSite $327.77 $130.99 $26.59 2.5x 12.3x

1/27/2011 Verizon Terremark $1,841.76 $340.71 $82.10 5.4x 22.4x

1/21/2011 ACF Industries XO Holdings $1,006.77 $1,529.24 $190.75 0.7x 5.3x 11/22/2010 Attachmate Corp Novell $1,017.93 $811.87 $117.51 1.3x 8.7x

9/20/2010 IBM Netezza Corp $1,593.42 $223.32 $19.71 7.1x 80.8x

8/23/2010 HP 3Par $2,215.83 $204.08 $6.46 10.9x 343.0x

Average 4.1x 20.3x

*Excluded HP’s acquisition of 3Par in the EBITDA multiple.

Source: Personal Analysis, Public Data

b. Digital Content Analysis

HTC acquired Saffron Digital because of its existing business in the streaming video industry. The business of streaming video content has been expanding rapidly with an increasing number of companies such as Netflix, Hulu, YouTube, Amazon, TV cable providers and Apple were already established in this business. The future of the video streaming business is

encouraging and offers value added service to each individual company.

35

Looking at the trends alone, the physical need to have stores to rent or purchase videos (Movies, TV shows) is diminishing, similar to the decrease in music CD stores. The best example would be Blockbuster’s downfall as a store retailer to Netflix’s DVD by Mail business which cuts the huge SG&A costs that are needed to operate its 3,000+ stores and store employees.

Not to mention the cost of crude oil (used to formulate gas for automobiles) reaching to

>US$140/barrel, adding to the company and customer’s commute expenses. Today, Netflix has continued to innovate and now provides streaming videos instantly without the need to wait for DVDs to be sent to the customer’s location. With this additional step, cost savings in postage and physical DVDs allowed Netflix to compete with retailers as its competitive advantage. This business model not only lead to the downfall of Blockbuster’s retailer model but it create a variety of streaming competition.

According to IHS, 27% of American now stream TV shows and movies, up from 16% in 2010. The research firm also surveyed individuals in the US and concluded that Americans were willing to pay for more movies online rather than purchase of the physical version. As seen in the chart below by IHS, the market for online video/transactions was forecasted to reach 3.4 billion views/transactions in 2012, approximately 1 billion more than physical view/transactions in the same year. "After more than 30 years of buying and renting movies on tapes and discs, this year (2012) marks the tipping point as U.S. consumers now are making a historic switch to Internet- based consumption, setting the stage for a worldwide migration of consumption from physical to online," Cryan said from IHS (Cryan, 2012).

36 Figure 13 – Online VS Physical Digital Content

In the US, Netflix, YouTube, Blockbuster (now owned by Dish Networks), Apple & Hulu are the dominate players, however, the biggest growth for digital content are in the Asia Pacific region where HTC has a strong presence and is well equipped to capture a market share. In Asia, the penetration of internet usage is at a low 26% (Internet World Stats, 2011), so the opportunity in Asia digital content has a lot of room for growth. With Saffron incorporated on HTC’s phones and tablet, it has the capability to view contents in multiple ways.

37 Illustration 6 – HTC Watch

While the video content industry has various factors to show its attractiveness, the acquisition of Saffron Digital does not come without risks. Saffron, still in its growing stage, currently remained as an independent company from the HTC parent. Although HTC has allowed Saffron to operate on its own, the unapparent conflict of interests exists for HTC and its competitors who also employed on Saffron's technologies. Some of the major obstacles for Saffron’s clients are how long Saffron can be self-sufficient and how much should they rely on Saffron. Saffron’s IPs and licenses provide an immediate platform to its current clients; it may not always be so in the long term. As Saffron’s digital content tools immersed deeper into HTC Watch’s strategy, Saffron will need to put more dedication into the parent company. Will resources be shifted to favor HTC rather than clients? Will there be any changes in leadership? From the perspective of a client, the long term implications are definitely questionable.

Lastly, M&A transactions are not valuable unless the management conducts proper post-integration planning. According to Mergermarket’s survey with 100 corporate

executives globally, the primary causes of failed mergers are due to conflicting goals (44%), poor communications (21%), management team disputes (20%), and conflicting cultures (15%) with 70% of respondents acknowledging the fact that cross border transactions such as HTC, Taiwan

38

& Saffron Digital, UK have lower success rates than the norm (Mergermarket, 2009). It will be imperative for HTC to focus on the alliance uncertainty such as synergy, structural, project risks, and people instability with continuous top management involvement. While the integration process will be difficult as the cultures are different between UK/Taiwan, however, ultimately with careful planning and dedication the success rate of the Saffron acquisition may prove to be positive and influential.

VI. Conclusion

Inorganic growth via mergers & acquisitions can be a very effective way for an organization to increase shareholder value. However, research has shown that success rate is less than 50%, and most of the values are obtained by the seller (BCG, Kees Cools, 2005). In spite of the relatively unappetizing odds of success in M&A, the Boston Consulting Group has found out that companies in general perform better when they regularly engage in M&A versus those that rely on organic growth – capturing 12.4% return rather than 9.6% return of the organic strategy.

In addition, companies are able to gain more market share and are able to grow twice as fast.

While M&A can be an important strategy for companies like HTC, companies must define the role of M&A in their corporate strategy, conduct careful valuations of the acquisition / target industry market, and develop a well-defined integration plan to be successful.

Since the acquisitions by HTC in 2011, HTC’s stock has fallen by more than 45% year to date. Although the steep drop can be due to over-evaluation of the stock to begin with from institutional investors, the company stock may have had further downside if there had not been innovative new technologies for HTC. By having new business models through acquisitions, HTC has been able to improve its market position and prevent the accelerated competition from

39

Samsung. The acquisitions by HTC have yet to flourish, although the success of them will mainly depend on the careful execution of company. The continuous attempt for acquisitions will allow HTC to improve its integration processes. In the long term, inorganic growth through acquisitions will be a key part to HTC’s business strategy.

40

References

Accenture plc. "Consumers of all ages are going over-the-top." Consumer Usage Survey. 2011.

pp 1-12

Ben Boissevain, David Cummings, Rob Forgione. Mergers & Acquisitions in the Cloud Sector.

New York: Agile Equity, 2011. pp 1-4

Berman, Barry. "Should Your Firm Adopt a Mass Customization Strategy?"." Business Horizons (July-August 2002): pp 51-60.

"Bloomberg." Bloomberg Terminal

Bradshaw, Tim. Financial Times. 7 February 2011. <http://www.ft.com/intl/cms/s/0/4264b330- 32e3-11e0-9a61-00144feabdc0.html#axzz1qlrKvGpA>.

Bruner, Robert F. Applied Mergers and Acquisitions. Hoboken, New Jersey: John Wiley & Sons, Inc., 2004. pp 138-148

BusinessWire, a Berkshire Hathaway Company, “David McDonald Appointed as CEO of Saffron Digital,” 2011.

<http://www.bloomberg.com/apps/news?pid=conewsstory&tkr=HTJ:GR&sid=agMicung CkVg>

Cheng F. Lee, Alice C. Lee. Encyclopedia of Finance. USA: Springer, 2006. pp 543, 669, 664 Cryan, Dan. iSuppli, a subsidiary of IHS. 22 March 2012. <http://www.isuppli.com/Media-

Research/News/Pages/US-Audiences-to-Pay-More-for-Online-Movies-in-2012-than-for- Physical-Videos.aspx>.

Daft, Richard L. Understanding the Theory and Design of Organizations. South-Western, Cengage Learning, 2010. pp 105-106, 385-386