CVA Risk

Consultation paper | CP 20.03

December 2020

Contents

I INTRODUCTION ... 3

1 Purpose ... 3

2 Background ... 3

3 Scope of Application ... 4

4 Approaches for the Calculation of CVA Risk ... 6

5 Implementation Timeline ... 7

6 Application and Approval Process ... 8

II BASIC APPROACH (BA-CVA)... 9

7 Reduced BA-CVA ... 9

8 Full BA-CVA... 11

III STANDARDISED APPROACH (SA-CVA) ... 15

9 General Criteria ... 15

10 Regulatory CVA Calculations ... 16

10.1 Quantitative Standards... 16

10.2 Qualitative Standards ... 19

11 Components of the SA-CVA ... 21

12 SA-CVA: Risk Factor and Sensitivity Definitions... 24

12.1 Risk Factor Definitions ... 24

12.2 Sensitivity Definitions ... 26

13 SA-CVA: Delta Risk Weights and Correlations ... 27

13.1 Interest Rate Risk ... 27

13.2 Foreign Exchange Risk ... 28

13.3 Counterparty Credit Spread Risk ... 28

13.4 Reference Credit Spread Risk ... 31

13.5 Equity Risk ... 34

13.6 Commodity Risk ... 36

14 SA-CVA: Vega Risk Weights and Correlations ... 38

I INTRODUCTION

1 Purpose

1 This consultation paper sets out the Hong Kong Monetary Authority’s (HKMA) proposal for revising the current regulations on the credit valuation adjustment (CVA) capital charges in the Banking (Capital) Rules (BCR).

2 The HKMA invites comments on the proposal of this paper by 26 February 2021. Please submit your comments to your industry associations or to the mailbox at [email protected].

3 Following the close of this consultation, the HKMA will further refine its proposed revisions taking into account the feedback received.

2 Background

4 In July 2020, the Basel Committee on Banking Supervision (BCBS) issued its Targeted revisions to the credit valuation adjustment risk framework.1 The revised CVA risk framework aims at aligning its design with the new market risk framework and taking into account exposure variability driven by daily changes of market risk factors in determining the CVA risk. It follows up on an original version published in December 20172 and includes a set of amendments to address issues that have been identified through input from a wide spectrum of stakeholders. It also takes into account extensive feedback received on a consultative document3 issued by the BCBS in November 2019 and it is calibrated based on the most recent set of the BCBS’

quantitative impact study (QIS) data.

5 This consultation paper outlines the HKMA’s plans for implementing the revised CVA risk framework in Hong Kong. It covers the Basic Approach (BA-CVA) and the new Standardised Approach (SA-CVA).

6 The HKMA intends to implement the revised CVA risk framework closely aligned with the standards issued by the BCBS. Therefore, the wordings in this consultation paper follow closely the standards set out in the Targeted revisions to the credit valuation adjustment risk framework.

1 http://www.bis.org/bcbs/publ/d507.htm

2 http://www.bis.org/bcbs/publ/d424.htm

3 http://www.bis.org/bcbs/publ/d488.htm

3 Scope of Application

7 Under the revised CVA risk framework, CVA stands for regulatory credit valuation adjustment4 specified at a counterparty level which excludes the effect of the AI’s own default. CVA reflects the adjustment of default risk-free prices of derivatives and securities financing transactions (SFTs) due to a potential default of an AI’s counterparty.

8 CVA risk is defined as the risk of losses arising from changing CVA values in response to changes in counterparty credit spreads and market risk factors that drive prices of the covered transactions.

9 All AIs should calculate the CVA capital charge for covered transactions in both banking book and trading book5. Covered transactions include:

all derivatives except those transacted directly with:

– a qualifying central counterparty6 (CCP); or

– a clearing member of a CCP that falls within section 226ZA(3), (4) or (5) of the BCR where the AI concerned is a client of the clearing member, or

– a CCP that fall within section 226ZB(2), (3) or (4) of the BCR where the AI concerned is a client of a clearing member of the CCP; and

SFTs that are fair-valued by the AI for accounting purposes, where the HKMA determines that an AI’s CVA risk arising from SFTs is material. In case the AI deems the CVA risk arising from SFTs is immaterial, the AI can justify its assessment to the HKMA by providing relevant supporting documentation.

10 An AI should calculate the CVA capital charge for its CVA portfolio on a standalone basis. The CVA portfolio should include all covered transactions and eligible CVA hedges.

11 Eligibility criteria for CVA hedges are specified in paragraph 31 for the BA-CVA and in paragraph 42 for the SA-CVA.

12 An AI may enter into an external CVA hedge with an external counterparty. All external CVA hedges, i.e. both eligible and ineligible external hedges, that are covered transactions should be included in the CVA capital charge calculation.

4 Regulatory CVA may differ from CVA used for accounting purposes. For example, the effect of the AI’s own default is considered in the accounting CVA but not in the regulatory CVA.

5 Please refer to subsection 7 of the consultation paper CP 19.01 for the scope of the trading book.

6 Unless otherwise specified, “qualifying CCP” has the same meaning as specified in section 2 of the BCR.

13 If an external CVA hedge is eligible, it should be removed from the market risk capital charge calculation. Otherwise, ineligible external CVA hedges are treated as trading book instruments and are included in the market risk capital charge calculation.

14 An AI may also enter into an internal CVA hedge between the CVA portfolio and the trading book. Such an internal hedge consists of two exactly offsetting positions: a CVA portfolio side and a trading desk side.

15 If an internal CVA hedge is eligible, the CVA portfolio side should be included in the CVA capital charge calculation, while the trading desk side should be included in the market risk capital charge calculation. Otherwise, for ineligible internal CVA hedges, both positions should be included in the market risk capital charge calculation where the positions cancel each other.

16 An internal CVA hedge involving an instrument that is subject to curvature risk, the default risk charge or the residual risk add-on under the revised market risk framework as set out in section II of the consultation paper CP 19.017 is eligible only if the trading book additionally enters into an external hedge with an external counterparty that exactly offsets the trading desk’s position with the CVA portfolio.

7 https://www.hkma.gov.hk/media/eng/regulatory-resources/consultations/CP19_01_Market_Risk.pdf

4 Approaches for the Calculation of CVA Risk

17 For the purpose of determining the risk-weighted amount for CVA risk, all locally incorporated AIs will be required to calculate the CVA capital charge in accordance with the new CVA risk standards. AIs, except for those mentioned in paragraph 18, may choose to calculate the CVA capital charge under the Basic Approach (BA-CVA) or, subject to approval, the Standardised Approach (SA-CVA).

18 An AI whose aggregate notional amount of non-centrally cleared derivatives is less than or equal to HKD 1tn, instead of using the BA-CVA or the SA-CVA, may choose to set its CVA capital charge as 100% of the AI’s capital charge for counterparty credit risk. However, the HKMA may remove this option if it is determined that the CVA risk resulting from the AI’s covered positions materially contributes to the AI’s overall risk.

19 An AI that has obtained the HKMA approval for the use of the SA-CVA may carve out any netting set from the use of the SA-CVA and calculate the CVA capital charge for such carved-out netting sets by using the BA-CVA. When applying the carve-out, a legal netting set may also be split into two synthetic netting sets, i.e. one containing the carved-out transactions which is subject to the BA-CVA and the other one subject to the SA-CVA if at least one of the following two conditions is met.

The split is consistent with the treatment of the legal netting set used by the AI for calculating the accounting CVA (e.g. where certain transactions are not processed by the front office / accounting exposure model).

The HKMA approval to use the SA-CVA is limited and does not cover all transactions within a legal netting set.

20 AIs that use the BA-CVA or the SA-CVA may cap the maturity adjustment factor at 1 for all netting sets contributing to the CVA capital charge when they calculate the counterparty credit risk capital charge under the Internal Ratings Based (IRB) Approach.

21 The HKMA will incorporate the new standards into the BCR by replacing the entire Division 3 in Part 6A with a new Division. The revised framework will also necessitate some consequential changes to other Parts of the BCR. Where appropriate, technical provisions may be set out in a new Code of Practice to be issued under section 97M of the Banking Ordinance or a new Supervisory Policy Manual (SPM).

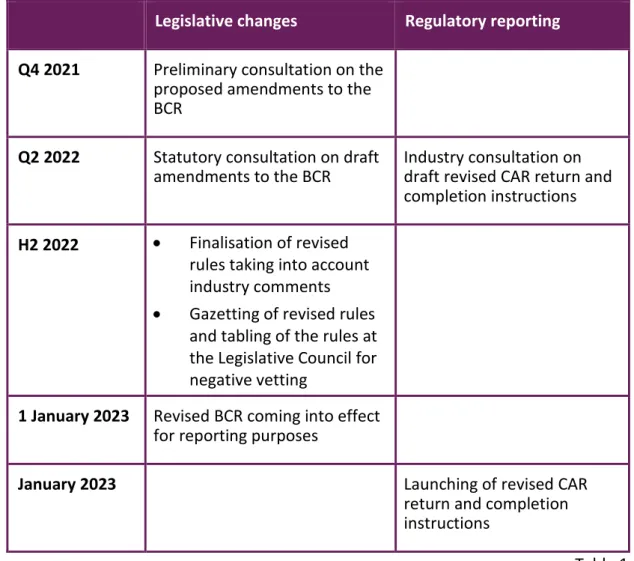

5 Implementation Timeline

22 The HKMA intends to put the new standards for reporting purposes into effect on 1 January 2023, in line with the BCBS timeline.Locally incorporated AIs shall continue the calculation of their regulatory CVA capital charges based on the rules set out in the existing BCR up to a specified date that would be no earlier than 1 January 2023.

甲、 Legislative changes Regulatory reporting Q4 2021 Preliminary consultation on the

proposed amendments to the BCR

Q2 2022 Statutory consultation on draft amendments to the BCR

Industry consultation on draft revised CAR return and completion instructions H2 2022 Finalisation of revised

rules taking into account industry comments

Gazetting of revised rules and tabling of the rules at the Legislative Council for negative vetting

1 January 2023 Revised BCR coming into effect for reporting purposes

January 2023 Launching of revised CAR

return and completion instructions

Table 1 23 As the revised CVA risk capital framework represents a significant overhaul of the current CVA risk capital framework, it is likely to have impacts on, among other things, the capital charges, systems, data and resources of AIs, particularly for those with material CVA risk exposures. All relevant AIs are therefore strongly recommended to

consider the implications of implementation for their institutions, and to start preparing for the local implementation of the revised framework in due course.

6 Application and Approval Process

24 AIs planning to adopt the SA-CVA for reporting purposes with effect from 1 January 2023 are invited to discuss their implementation plans with their usual supervisory contact at the HKMA by 30 June 2021.

II BASIC APPROACH (BA-CVA)

25 An AI using the BA-CVA may, at its discretion, choose to implement either the reduced version (reduced BA-CVA) or the full version of the BA-CVA (full BA-CVA).8 No matter which version the AI chooses, the AI should calculate and report the CVA capital charges to the HKMA on a monthly basis.

26 The full BA-CVA recognises the counterparty spread hedges and is intended for AIs that hedge their CVA risk.

27 The reduced BA-CVA eliminates the element of hedging recognition from the full BA- CVA and is intended for AIs that do not hedge their CVA risk or prefer a simpler approach.

7 Reduced BA-CVA

28 The CVA capital charge under the reduced BA-CVA (𝐵𝐴_𝐶𝑉𝐴𝑟𝑒𝑑𝑢𝑐𝑒𝑑) is calculated based on the following formula.9 The first term under the square root aggregates the systematic components of CVA risk, and the second one aggregates the idiosyncratic components of CVA risk.

𝐵𝐴_𝐶𝑉𝐴𝑟𝑒𝑑𝑢𝑐𝑒𝑑 = 𝐷𝑆 ∙ √(𝜌 ∙ ∑ 𝑆𝐶𝑉𝐴𝑐

𝑐

)

2

+ (1 − 𝜌2) ∙ ∑ 𝑆𝐶𝑉𝐴𝑐2

𝑐

where

SCVAc is the standalone CVA capital charge for counterparty c, i.e. the CVA capital charge that counterparty c would receive on a standalone basis and is calculated as set out in paragraph 29;

DS is the discount scalar which is equal to 0.65; and

𝜌 is the supervisory correlation parameter which is equal to 0.5. Its square, i.e.

𝜌2 = 0.25 , represents the correlation between credit spreads of any two counterparties. Its effect is to recognise the fact that the CVA risk an AI is exposed

8 AIs using the full BA-CVA must also calculate the reduced BA-CVA capital charge as the reduced BA- CVA is also part of the full BA-CVA capital calculations which limits hedging recognition.

9 The second term √(𝜌 ∙ ∑ 𝑆𝐶𝑉𝐴𝑐 𝑐)2+ (1 − 𝜌2) ∙ ∑ 𝑆𝐶𝑉𝐴𝑐 𝑐2 in the formula represents 𝐾𝑟𝑒𝑑𝑢𝑐𝑒𝑑

defined in MAR50.14 of the BCBS consolidated framework.

to is smaller than the sum of the CVA risk for each counterparty, given that the credit spreads of counterparties are typically not perfectly correlated.

29 The standalone CVA capital charge for counterparty c is calculated based on the following formula (where the summation is across all netting sets with the counterparty).

𝑆𝐶𝑉𝐴𝑐 = 1

𝛼∙ 𝑅𝑊𝑐∙ ∑ 𝑀𝑁

𝑁

∙ 𝐸𝐴𝐷𝑁∙ 𝐷𝐹𝑁

where

RWc is the risk weight for counterparty c that reflects the volatility of its credit spread and is set out in paragraph 30;

MN is the effective maturity for the netting set N. For AIs with the HKMA approval for the use of the internal models (counterparty credit risk) approach (IMM(CCR) approach), MN is calculated in accordance with section 168(1)(ba) of the BCR, with the exception that the five-year cap in section 168(2) of the BCR is not applied. Otherwise, MN is calculated in accordance with other subsections of section 168 of the BCR, with the exception that the five-year cap in section 168(2) of the BCR is not applied;

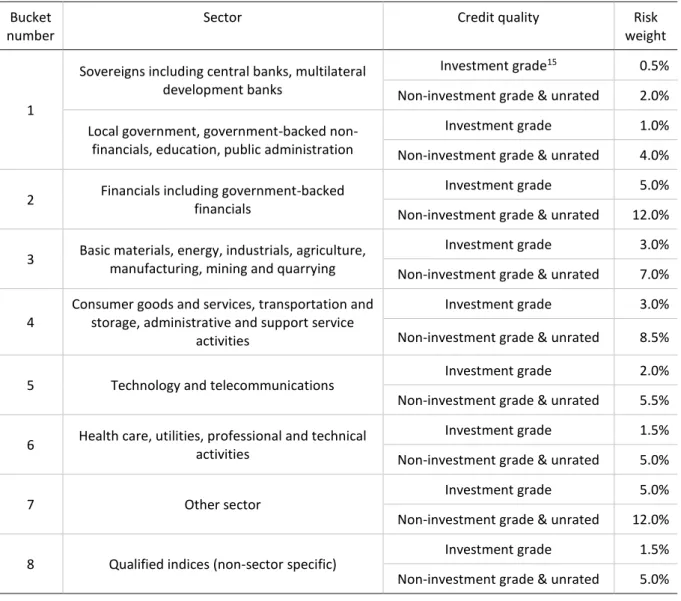

EADN is the exposure at default (EAD) of the netting set N which is calculated in the same way under the counterparty credit risk capital requirements;

DFN is the supervisory discount factor, which is equal to 1 for AIs with an HKMA approval for the use of the IMM(CCR) approach and 1−𝑒0.05∙𝑀−0.05∙𝑀𝑁

𝑁 otherwise; and

α is the multiplier used to convert effective expected positive exposure (EEPE) to exposure at default (EAD) in both the standardised approach for measuring CCR exposures (SA-CCR approach) and the IMM(CCR) approach, which is equal to 1.4.

30 The risk weights (RWc), which are based on the sector and credit quality of the counterparty, are set out in the following table. Where there is no external rating, AIs that use the IRB approach to calculate their credit risk capital charge may, subject to an HKMA approval, map the internal rating to a corresponding external rating.

Otherwise, the risk weights for unrated counterparties should be applied.

Credit quality

Sector of counterparty Investment grade10 Non-investment grade or unrated Sovereigns including central banks and multilateral

development banks 0.5% 2.0%

Local government, government-backed non-financials,

education and public administration 1.0% 4.0%

Financials including government-backed financials 5.0% 12.0%

Basic materials, energy, industrials, agriculture, manufacturing,

mining and quarrying 3.0% 7.0%

Consumer goods and services, transportation and storage,

administrative and support service activities 3.0% 8.5%

Technology and telecommunications 2.0% 5.5%

Health care, utilities, professional and technical activities 1.5% 5.0%

Other sector 5.0% 12.0%

Table 2

8 Full BA-CVA

31 The full BA-CVA recognises the effect of counterparty credit spread hedges. Only transactions used for the purpose of mitigating the counterparty credit spread component of CVA risk, and managed as such, can be eligible CVA hedges. An eligible CVA hedge should also fulfil the conditions below.

The hedging instrument is either a single-name credit default swap (CDS), a single-name contingent CDS or an index CDS.

In the case of single-name credit instruments, it must reference (i) the counterparty directly; (ii) an entity legally related to the counterparty where legally related refers to cases where the reference name and the counterparty are either a parent and its subsidiary or two subsidiaries of a common parent; or (iii) an entity that belongs to the same sector and region as the counterparty.

32 The CVA capital charge under the full BA-CVA (𝐵𝐴_𝐶𝑉𝐴𝑓𝑢𝑙𝑙) is calculated as follows:

𝐵𝐴_𝐶𝑉𝐴𝑓𝑢𝑙𝑙 = 𝛽 ∙ 𝐵𝐴_𝐶𝑉𝐴𝑟𝑒𝑑𝑢𝑐𝑒𝑑+ (1 − 𝛽) ∙ 𝐵𝐴_𝐶𝑉𝐴ℎ𝑒𝑑𝑔𝑒𝑑

10 Unless otherwise specified, “investment grade” has the same meaning as specified in section 281 of the BCR.

where

𝐵𝐴_𝐶𝑉𝐴𝑟𝑒𝑑𝑢𝑐𝑒𝑑 is the CVA capital charge under the reduced BA-CVA as set out in paragraph 28;

𝐵𝐴_𝐶𝑉𝐴ℎ𝑒𝑑𝑔𝑒𝑑 is the CVA capital charge that recognises eligible hedges and is calculated as set out in paragraph 33; and

𝛽 is a supervisory parameter that provides a floor to limit the impact of eligible hedges on the overall CVA capital charge under the BA-CVA which is equal to 0.25.

33 The CVA capital charge that recognises eligible hedges (𝐵𝐴_𝐶𝑉𝐴ℎ𝑒𝑑𝑔𝑒𝑑) is calculated based on the following formula.11 It comprises three main terms under the square root: (i) the first term aggregates the systematic components of CVA risk arising from the bank’s counterparties, the single-name hedges and the index hedges; (ii) the second term aggregates the idiosyncratic components of CVA risk arising from the bank’s counterparties and the single-name hedges; and the third term aggregates the components of indirect hedges that are not aligned with counterparties’ credit spreads.

𝐵𝐴_𝐶𝑉𝐴ℎ𝑒𝑑𝑔𝑒𝑑= 𝐷𝑆 ∙ √(𝜌 ∙ ∑(𝑆𝐶𝑉𝐴𝑐− 𝑆𝑁𝐻𝑐) − 𝐼𝐻

𝑐

)

2

+ (1 − 𝜌2) ∙ ∑(𝑆𝐶𝑉𝐴𝑐− 𝑆𝑁𝐻𝑐)2+ ∑ 𝐻𝑀𝐴𝑐 𝑐 𝑐

where

SCVAc is the standalone CVA capital charge for counterparty c as set out in paragraph 29;

DS is the discount scalar which is equal to 0.65;

𝜌 is the supervisory correlation parameter which is equal to 0.5;

SNHc is a quantity that gives recognition to the reduction in CVA risk of the counterparty c arising from an AI’s use of single-name hedges of credit spread risk as set out in paragraph 34;

IH is a quantity that gives recognition to the reduction in CVA risk across all counterparties arising from the AI’s use of index hedges as set out in paragraph 35; and

11 The second term √(𝜌 ∙ ∑ (𝑆𝐶𝑉𝐴𝑐 𝑐− 𝑆𝑁𝐻𝑐) − 𝐼𝐻)2+ (1 − 𝜌2) ∙ ∑ (𝑆𝐶𝑉𝐴𝑐 𝑐− 𝑆𝑁𝐻𝑐)2+ ∑ 𝐻𝑀𝐴𝑐 𝑐 in the formula represents 𝐾ℎ𝑒𝑑𝑔𝑒𝑑 defined in MAR50.21 of the BCBS consolidated framework.

HMAc is a quantity that characterises the hedging misalignment, which limits the extent to which indirect hedges can reduce the CVA capital charge given that they will not fully offset movements in a counterparty’s credit spread. The calculation is set out in paragraph 36.

34 The quantity SNHc is calculated based on the following formula (where the summation is across all single name hedges h that an AI has taken out to hedge the CVA risk of counterparty c).

𝑆𝑁𝐻𝑐 = ∑ 𝑟ℎ𝑐∙ 𝑅𝑊ℎ∙ 𝑀ℎ𝑆𝑁∙ 𝐵ℎ𝑆𝑁∙ 𝐷𝐹ℎ𝑆𝑁

ℎ∈𝑐

where

𝑟ℎ𝑐 is the supervisory prescribed correlation between the credit spread of counterparty c and the credit spread of a single-name hedge h of counterparty c.

The value of 𝑟ℎ𝑐 is set at:

– 100% if the hedge h directly references the counterparty c;

– 80% if the hedge h has legal relation with counterparty c; or

– 50% if the hedge h shares the same sector and region with counterparty c;

𝑀ℎ𝑆𝑁 is the remaining maturity of single-name hedge h, expressed in years;

𝐵ℎ𝑆𝑁 is the notional amount of the single-name hedge h. For single-name contingent CDS, the notional is determined by the current market value of the reference portfolio or instrument;

𝐷𝐹ℎ𝑆𝑁 is the supervisory discount factor calculated as 1−𝑒−0.05∙𝑀ℎ

𝑆𝑁 0.05∙𝑀ℎ𝑆𝑁 ; and

𝑅𝑊ℎ is the supervisory risk weight of single-name hedge h that reflects the volatility of the credit spread of the reference name of the hedging instrument.

These risk weights are based on a combination of the sector and the credit quality of the reference name of the hedging instrument as prescribed in Table 2 of paragraph 30.

35 The quantity IH is calculated as follows (where the summation is across all index hedges i that an AI has taken out to hedge CVA risk):

𝐼𝐻 = ∑ 𝑅𝑊𝑖 ∙

𝑖

𝑀𝑖𝑖𝑛𝑑∙ 𝐵𝑖𝑖𝑛𝑑∙ 𝐷𝐹𝑖𝑖𝑛𝑑

where

𝑀𝑖𝑖𝑛𝑑 is the remaining maturity of index hedge i, expressed in years;

𝐵𝑖𝑖𝑛𝑑 is the notional amount of the index hedge i;

𝐷𝐹𝑖𝑖𝑛𝑑 is the supervisory discount factor calculated as 1−𝑒−0.05∙𝑀𝑖

𝑖𝑛𝑑 0.05∙𝑀𝑖𝑖𝑛𝑑 ; and

RWi is the supervisory risk weight of the index hedge i. RWi is taken from the Table 2 of paragraph 30 based on the sector and the credit quality of the index constituents and adjusted as follows:

– for an index where all index constituents belong to the same sector and are of the same credit quality, the relevant value in the Table 2 of paragraph 30 is multiplied by 0.7 to account for diversification of idiosyncratic risk within the index; or

– for an index spanning multiple sectors or with a mixture of investment grade constituents and other grade constituents, the name-weighted average of the risk weights from the Table 2 of paragraph 30 should be calculated and then multiplied by 0.7.

36 The quantity HMAC is calculated as follows (where the summation is across all single name hedges h that have been taken out to hedge the CVA risk of counterparty c):

𝐻𝑀𝐴𝑐 = ∑(1 − 𝑟ℎ𝑐2 ) ∙ (𝑅𝑊ℎ∙ 𝑀ℎ𝑆𝑁∙ 𝐵ℎ𝑆𝑁∙ 𝐷𝐹ℎ𝑆𝑁)2

ℎ∈𝑐

where 𝑟ℎ𝑐, 𝑅𝑊ℎ, 𝑀ℎ𝑆𝑁, 𝐵ℎ𝑆𝑁 and 𝐷𝐹ℎ𝑆𝑁 have the same definitions as set out in paragraph 34.

III STANDARDISED APPROACH (SA-CVA)

9 General Criteria

37 The use of the SA-CVA requires an explicit approval from the HKMA. An AI should calculate and report the CVA capital charges under the SA-CVA to the HKMA on a monthly basis.

38 An AI should also be able to determine its regulatory capital charges according to the SA-CVA at any time at the demand of the HKMA.

39 The SA-CVA is an adaptation of the Standardised Approach under the revised market risk framework as set out in Section III of the consultation paper CP 19.01, with the following major differences.

The SA-CVA features a reduced granularity of market risk factors.

The SA-CVA does not include default risk and curvature risk.

40 The SA-CVA uses as inputs the sensitivities of regulatory CVA to (i) counterparty credit spreads and (ii) market risk factors driving the fair values of covered transactions. In calculating the sensitivities, AIs should fulfil the requirements in section 4A of the BCR and the Supervisory Policy Manual (SPM) Module CA-S-10 “Financial Instrument Fair Value Practices”.

41 An AI should meet the following criteria at the minimum to qualify for the use of the SA-CVA.

The AI should be able to model exposure and calculate, on at least a monthly basis, CVA and CVA sensitivities to the market risk factors specified in subsection 12.

The AI should have a CVA desk (or a similar dedicated function) responsible for risk management and hedging of CVA.

42 Only transactions used for the purpose of mitigating the CVA risk, and managed as such, can be eligible CVA hedges. An eligible CVA hedge should also fulfil the conditions below:

Transactions must not be split into several effective transactions.

The hedging instrument should hedge the variability of either the counterparty credit spread or the exposure component of the CVA risk.

Instruments that are not eligible for the Internal Models Approach under the revised market risk framework as set out in CP 19.01 should not be considered as eligible hedges.

43 The aggregate capital charge calculated under the SA-CVA can be scaled up by a multiplier mCVA. The basic level of mCVA is set at 1. However, the HKMA may require an AI to use a higher level of mCVA, taking into account the level of model risk for the calculation of the CVA sensitivities (e.g. if the level of model risk for the calculation of CVA sensitivities is too high or the dependence between the AI’s exposure to a counterparty and the counterparty’s credit quality is not appropriately taken into account in its CVA calculations).

10 Regulatory CVA Calculations

10.1 Quantitative Standards

44 An AI should calculate the regulatory CVA for each counterparty with which it has at least one covered position for the purpose of the CVA capital charge.

45 An AI should calculate the regulatory CVA as the expectation of future losses resulting from default of the counterparty under the assumption that the AI itself is free from default risk. In expressing the regulatory CVA, non-zero losses must have a positive sign. This is reflected in paragraph 84 where 𝑊𝑆𝑘ℎ𝑑𝑔 must be subtracted from 𝑊𝑆𝑘𝐶𝑉𝐴.

46 An AI should calculate the regulatory CVA based on at least the three sets of inputs below:

term structure of market-implied probability of default (PD);

market-consensus expected loss-given-default (ELGD); and

simulated paths of discounted future exposure.

47 An AI should estimate the term structure of market-implied PD from credit spreads observed in the markets. For counterparties whose credit is not actively traded (i.e.

illiquid counterparties), the AI should estimate the market-implied PD from proxy credit spreads estimated for these counterparties in accordance with paragraphs 48 to 50.

48 An AI should estimate the credit spread curves of illiquid counterparties from credit spreads observed in the markets of the counterparty’s liquid peers via an algorithm

that discriminates on at least the following three variables: a measure of credit quality (e.g. rating), industry, and region.

49 In certain cases, mapping an illiquid counterparty to a single liquid reference name can be allowed. A typical example would be mapping a municipality to its home country (i.e. setting the municipality credit spread equal to the sovereign credit spread plus a premium). An AI should justify to the HKMA each case of mapping an illiquid counterparty to a single liquid reference name.

50 When no credit spreads of any of the counterparty’s peers are available due to the counterparty’s specific type (e.g. project finance or funds), an AI may be allowed to use a more fundamental analysis of credit risk to proxy the spread of an illiquid counterparty. However, where historical PDs are used as part of this assessment, the resulting spread cannot be based on historical PDs only – it must relate to credit markets.

51 An AI should use the same market-consensus ELGD value to calculate the risk-neutral PD from credit spreads unless the AI can demonstrate that the seniority of the exposure resulting from covered positions differs from the seniority of senior unsecured bonds. Collateral provided by the counterparty does not change the seniority of the exposure.

52 An AI should produce the simulated paths of discounted future exposure by pricing all derivative transactions with the counterparty along simulated paths of relevant market risk factors and discounting the prices back to the reporting date using risk- free interest rates along the path.

53 An AI should simulate all market risk factors material for the transactions with a counterparty as stochastic processes for an appropriate number of paths defined on an appropriate set of future time points extending to the maturity of the longest transaction.

54 An AI should take into account any significant level of dependence between exposure and the counterparty’s credit quality in the regulatory CVA calculations.

55 For margined counterparties, an AI is permitted to recognise collateral as a risk mitigant under the following conditions:

Collateral management requirements outlined in section 1(e) of Schedule 2A of the BCR are satisfied.

All documentation used in collateralised transactions should be binding on all parties and legally enforceable in all relevant jurisdictions. The AI should have conducted sufficient legal review to verify this and have a well-founded legal basis to reach this conclusion, and undertake such further review as necessary to ensure continuing enforceability.

56 For margined counterparties, an AI should capture the effects of margining collateral that is recognised as a risk mitigant along each simulated path of discounted future exposure. The AI should appropriately capture all the relevant contractual features such as the nature of the margin agreement (unilateral vs. bilateral), the frequency of margin calls, the type of collateral, thresholds, independent amounts, initial margins and minimum transfer amounts in the exposure model. To determine collateral available to the AI at a given exposure measurement time point, the AI also should assume in the exposure model that the counterparty will not post or return any collateral within a certain time period immediately prior to that time point. The assumed value of this time period, known as the margin period of risk (MPoR), cannot be less than a supervisory floor as set out in paragraph 57.

57 For SFTs and client cleared transactions as specified in section 226Z of the BCR, the supervisory floor for the MPoR is equal to 4+N business days, where N is the re- margining period specified in the margin agreement (in particular, for margin agreements with daily or intra-daily exchange of margin, the minimum MPoR is 5 business days). For all other transactions, the supervisory floor for the MPoR is equal to 9+N business days.

58 An AI should obtain the simulated paths of discounted future exposure via the exposure models used for calculating the front office or accounting CVA, with adjustments if needed, to meet the requirements imposed for regulatory CVA calculation. The model calibration process (with the exception of the MPoR) of the regulatory CVA calculation should be the same as that of the accounting CVA calculation. The market data and transaction data used for regulatory CVA calculation and accounting CVA calculation should also be the same.

59 In generating the paths of market risk factors underlying the exposure models, an AI should demonstrate to the HKMA its compliance with the following requirements:

Drifts of risk factors should be consistent with a risk-neutral probability measure.

Historical calibration of drifts is not allowed.

The volatilities and correlations of market risk factors should be calibrated to market data whenever sufficient data exist in a given market. Otherwise, historical calibration is permissible.

The distribution of modelled risk factors should account for the possible non- normality of the distribution of exposures, including the existence of leptokurtosis, where appropriate.

60 An AI should apply the same netting recognition as in its accounting CVA calculations.

In particular, the AI can model the netting uncertainty.

10.2 Qualitative Standards

61 An AI should meet the qualitative criteria set out below on an ongoing basis. The HKMA should be satisfied that the AI has met the qualitative criteria before granting an SA-CVA approval.

62 Exposure models used for calculating regulatory CVA should be part of a CVA risk management framework that includes the identification, measurement, management, approval and internal reporting of CVA risk. An AI should have a credible track record in using these exposure models for calculating CVA and CVA sensitivities to market risk factors.

63 Senior management should be actively involved in the risk control process and regard CVA risk control as an essential aspect of the business to which significant resources need to be devoted.

64 An AI should have a process in place for ensuring compliance with a documented set of internal policies, controls and procedures concerning the operation of the exposure system used for accounting CVA calculations.

65 An AI should have an independent control unit that is responsible for the effective initial and ongoing validation of the exposure models. This unit should be independent from business credit and trading units (including the CVA desk), be adequately staffed and report directly to senior management of the AI.

66 An AI should document the process for initial and ongoing validation of its exposure models to a level of detail that would enable a third party to understand how the models operate, their limitations, and their key assumptions; and recreate the analysis.

This documentation should set out the minimum frequency with which ongoing validation will be conducted as well as other circumstances (such as a sudden change in market behaviour) under which additional validation should be conducted. In addition, the documentation should describe how the validation is conducted with respect to data flows and portfolios, what analyses are used and how representative counterparty portfolios are constructed.

67 The pricing models used to calculate exposure for a given path of market risk factors should be tested against appropriate independent benchmarks for a wide range of market states as part of the initial and ongoing model validation process. Pricing models for options should account for the non-linearity of option value with respect to market risk factors.

68 An AI should carry out an independent review of the overall CVA risk management process regularly in the its internal auditing process. This review should include both the activities of the CVA desk and of the independent risk control unit.

69 An AI should define criteria on which to assess the exposure models and their inputs and have a written policy in place to describe the process to assess the performance of exposure models and remedy unacceptable performance.

70 Exposure models should capture transaction-specific information in order to aggregate exposures at the level of the netting set. An AI should verify that transactions are assigned to the appropriate netting set within the model.

71 Exposure models should reflect transaction terms and specifications in a timely, complete, and conservative fashion. The terms and specifications should reside in a secure database that is subject to formal and periodic audit. The transmission of transaction terms and specifications data to the exposure model should also be subject to internal audit, and formal reconciliation processes should be in place between the internal model and source data systems to verify on an ongoing basis that transaction terms and specifications are being reflected in the exposure system correctly or at least conservatively.

72 The current and historical market data should be acquired independently of the lines of business and be compliant with accounting. They should be fed into the exposure models in a timely and complete fashion, and maintained in a secure database subject to formal and periodic audit. An AI should also have a well-developed data integrity process to handle the data of erroneous and/or anomalous observations. In the case where an exposure model relies on proxy market data, an AI should set internal policies to identify suitable proxies and the AI should demonstrate empirically on an ongoing basis that the proxy provides a conservative representation of the underlying risk under adverse market conditions.

11 Components of the SA-CVA

73 The SA-CVA capital charge is calculated as the sum of the capital charges for delta and vega risks calculated for the entire CVA portfolio (including eligible hedges).

74 The capital charge for delta risk is calculated as the simple sum of delta risk capital charges calculated independently for the following six risk classes:

interest rate risk;

foreign exchange (FX) risk;

counterparty credit spread risk;

reference credit spread risk (i.e. credit spreads that drive the CVA exposure component);

equity risk; and

commodity risk.

75 If an instrument is deemed as an eligible hedge for credit spread delta risk under paragraph 42, an AI should assign it entirely either to the counterparty credit spread or to the reference credit spread risk class. The AI should not split the instrument between the two risk classes.

76 The capital charge for vega risk is calculated as the simple sum of vega risk capital charges calculated independently for five of the six risk classes as set out in paragraph 74. There is no vega risk capital charge for counterparty credit spread risk.

77 The capital charges for delta and vega risks are calculated in the same manner using the same procedures set out in paragraphs 78 to 84.

78 For each risk class, (i) the sensitivity of the aggregate CVA, 𝑠𝑘𝐶𝑉𝐴, and (ii) the sensitivity of the market value of all eligible hedging instruments in the CVA portfolio, 𝑠𝑘𝐻𝑑𝑔, to each risk factor k in the risk class are calculated. The sensitivities are defined as the ratio of the change in the market value of (i) aggregate CVA or (ii) market value of all CVA hedges caused by a small change of the risk factor’s current value to the size of the change. Specific definitions for each risk class are set out in subsections 12 to 14.

These definitions include specific values of changes or shifts in risk factors. However, an AI may use smaller values of risk factor shifts if doing so is consistent with internal risk management calculations.

79 An AI should calculate CVA sensitivities for vega risk regardless of whether or not the portfolio includes options. When calculating those CVA sensitivities, the AI should apply the volatility shift to both types of volatilities that appear in exposure models:

volatilities used for generating risk factor paths; and

volatilities used for pricing options.

80 If a hedging instrument is an index, an AI should calculate the sensitivities to all risk factors upon which the value of the index depends. The index sensitivity to risk factor k is calculated by applying the shift of risk factor k to all index constituents that depend on this risk factor and recalculating the changed value of the index. For example, to calculate delta sensitivity of the Hang Seng Index to large12 financial companies, an AI should apply the relevant shift to equity prices of all large financial companies that are constituents of the Hang Seng Index and re-compute the index.

81 An AI may choose to introduce a set of additional risk factors that directly correspond to qualified credit and equity indices for the following risk classes:

counterparty credit spread risk;

reference credit spread risk; and

equity risk.

82 For delta risk, a credit or equity index is qualified if it satisfies liquidity and diversification conditions specified in paragraph 132 of CP 19.01; and for vega risks, any credit or equity index is qualified.

83 For a covered transaction or an eligible hedging instrument whose underlying is a qualified index, an AI may replace its contribution to sensitivities to the index constituents with its contribution to a single sensitivity to the underlying index. For example, for a portfolio consisting only of equity derivatives referencing only qualified equity indices, the AI may not need to calculate the CVA sensitivities to non-index equity risk factors. If more than 75% of constituents of a qualified index (taking into account the weightings of the constituents) are mapped to the same sector, the entire index must be mapped to that sector and treated as a single-name sensitivity in that bucket. In all other cases, the sensitivity must be mapped to the applicable index bucket.

12 Please refer to paragraph 130 for the definition of large market capitalisation.

84 For each risk class, an AI should determine the sensitivities 𝑠𝑘𝐶𝑉𝐴 and 𝑠𝑘𝐻𝑑𝑔 to a set of prescribed risk factors, risk-weight those sensitivities, and aggregate the resulting net risk-weighted sensitivities separately for delta and vega risk using the following step-by-step approach.

Step 1: For each risk factor k, the sensitivities 𝑠𝑘𝐶𝑉𝐴 and 𝑠𝑘𝐻𝑑𝑔 are determined as set out in paragraph 78. The weighted sensitivities 𝑊𝑆𝑘𝐶𝑉𝐴 and 𝑊𝑆𝑘𝐻𝑑𝑔 are calculated by multiplying the net sensitivities 𝑠𝑘𝐶𝑉𝐴 and 𝑠𝑘𝐻𝑑𝑔 , respectively, by the corresponding risk weight RWk as set out in subsections 13 and 14.

Step 2: The net weighted sensitivity of the CVA portfolio 𝑊𝑆𝑘 to risk factor k is obtained by13:

𝑊𝑆𝑘= 𝑊𝑆𝑘𝐶𝑉𝐴 − 𝑊𝑆𝑘𝐻𝑑𝑔

Step 3: The net weighted sensitivities should be aggregated into a capital charge Kb

within each bucket b as set out in the formula below:

𝐾𝑏= √(∑ 𝑊𝑆𝑘2+

𝑘∈𝑏

∑ ∑ 𝜌𝑘𝑙∙ 𝑊𝑆𝑘∙ 𝑊𝑆𝑙

𝑙∈𝑏,𝑙≠𝑘 𝑘∈𝑏

) + 𝑅 ∙ ∑(𝑊𝑆𝑘𝐻𝑑𝑔)2

𝑘𝜖𝑏

where:

the buckets and correlation parameters 𝜌𝑘𝑙 applicable to each risk class are specified in subsections 13 and 14; and

R is the hedging disallowance parameter, set at 0.01, that prevents the possibility of recognising perfect hedging of CVA risk.

Step 4: Bucket-level capital charges should then be aggregated across buckets within each risk class as set out in the formula below:

𝐾 = 𝑚𝐶𝑉𝐴∙ √∑ 𝐾𝑏2+ ∑ ∑ 𝛾𝑏𝑐∙ 𝑠𝑏∙ 𝑠𝑐

𝑐≠𝑏 𝑏 𝑏

where:

the correlation parameters 𝛾𝑏𝑐 applicable to each risk class are specified in subsections 13 and 14;

13 Note that the formula is set out under the convention that the CVA is positive as specified in paragraph 45.

𝑚𝐶𝑉𝐴 is the multiplier as set out in paragraph 43; and

𝑠𝑏 is the sum of the weighted sensitivities WSk for all risk factors k within bucket b, floored by –Kb and capped by Kb, and 𝑠𝑐 is defined in the same way for all risk factors k in bucket c:

𝑆𝑏 = 𝑚𝑎𝑥 {−𝐾𝑏; 𝑚𝑖𝑛 (∑ 𝑊𝑆𝑘; 𝐾𝑏

𝑘∈𝑏

)}

𝑆𝑐 = 𝑚𝑎𝑥 {−𝐾𝑐; 𝑚𝑖𝑛 (∑ 𝑊𝑆𝑘; 𝐾𝑐

𝑘∈𝑐

)}

12 SA-CVA: Risk Factor and Sensitivity Definitions

12.1 Risk Factor Definitions

Interest rate risk

85 For AUD, CAD, EUR, GBP, HKD, JPY, SEK and USD, the interest rate delta risk factors are the risk-free yields for a given currency, further defined along the following tenors:

1 year, 2 years, 5 years, 10 years and 30 years. For the calculation of the sensitivities, a given tenor for all risk-free yield curves in a given currency is to be shifted by 1 basis point.

86 For currencies not specified in paragraph 85, the interest rate delta risk factors are the risk-free yields without term structure decomposition for a given currency. For the calculation of the sensitivities, all risk-free yield curves for a given currency are to be shifted in parallel by 1 basis point.

87 The interest rate delta risk factors also include a flat curve of inflation rate for each currency. Its term structure does not represent a risk factor.

88 The interest rate vega risk factors are a simultaneous relative change of all interest rate volatilities for a given currency and a simultaneous relative change of all volatilities for an inflation rate.

Foreign exchange risk

89 The foreign exchange delta risk factors are the exchange rates between the currency in which an instrument is denominated and the reporting currency (i.e. HKD). For transactions that reference an exchange rate between a pair of non-reporting currencies, the foreign exchange delta risk factors are all the exchange rates between (i) HKD and (ii) both the currency in which an instrument is denominated and any other

currencies referenced by the instrument.14 The exchange rate is the current market price of one unit of another currency expressed in the units of HKD.

90 The single foreign exchange vega risk factor is a simultaneous relative change of all volatilities for a given exchange rate between HKD and another currency.

Counterparty credit spread risk

91 The counterparty credit delta risk factors are the relevant credit spreads for individual entities (counterparties and reference names for counterparty credit spread hedges) and qualified indices as set out in paragraphs 82 and 83, further defined along the following tenors: 0.5 years, 1 year, 3 years, 5 years and 10 years.

92 The counterparty credit risk is not subject to the vega risk capital charge.

Reference credit spread risk

93 The reference credit spread delta risk factors are the relevant credit spreads without term structure decomposition for all reference names within the same bucket. For the calculation of the sensitivities, credit spreads of all tenors for all reference names in the bucket are to be shifted by 1 basis point.

94 A reference credit spread vega risk factor is a simultaneous relative change of the volatilities of credit spreads of all tenors for all reference names within the same bucket.

Equity risk

95 The equity delta risk factors are the equity spot prices for all reference names within the same bucket. For the calculation of the sensitivities, equity spot prices for all reference names in the bucket are to be shifted by 1% relative to their current values.

96 An equity vega risk factor is a simultaneous relative change of the volatilities for all reference names within the same bucket.

Commodity risk

97 The commodity delta risk factors are all the spot prices for all commodities within the same bucket. For the calculation of the sensitivities, spot prices for all commodities in the bucket are to be shifted by 1% relative to their current values.

14 For example, for an FX forward referencing EUR/JPY, the relevant risk factors for an AI to consider are the exchange rates EUR/HKD and JPY/HKD.

98 A commodity vega risk factor is a simultaneous relative change of the volatilities for all commodities within the same bucket.

12.2 Sensitivity Definitions

99 An AI should use the prescribed formulations as set in paragraphs 102 to 104 to calculate the sensitivities for each risk class respectively.

100 An AI should calculate sensitivities for each risk class in terms of HKD.

101 For each risk factor defined in paragraphs 85 to 98, sensitivities are calculated as the change in the aggregate CVA of the instrument (or market value of the CVA hedge) as a result of applying a specified shift to each risk factor, assuming all the other relevant risk factors are held at the current level.

Delta risk sensitivities

102 An AI should calculate the delta risk sensitivities of (i) interest rate, (ii) counterparty credit spread, (iii) reference credit spread in accordance with the following formula:

𝑠𝑘 =𝐶𝑉𝐴(𝑅𝐹𝑘+ 0.0001) − 𝐶𝑉𝐴(𝑅𝐹𝑘) 0.0001

where:

𝑠𝑘 is the delta sensitivity of risk factor k;

𝑅𝐹𝑘 is the risk factor k; and

CVA(.) is the aggregate CVA (or the market value of the CVA hedges) as a function of the risk factor k.

103 An AI should calculate the delta risk sensitivities of (i) equity, (ii) commodity and (iii) foreign exchange risk factors in accordance with the following formula:

𝑠𝑘 =𝐶𝑉𝐴(1.01𝑅𝐹𝑘) − 𝐶𝑉𝐴(𝑅𝐹𝑘) 0.01

Vega risk sensitivities

104 An AI should calculate the vega risk sensitivities of (i) interest rate, (ii) foreign exchange, (ii) reference credit spread, (iv) equity and (v) commodity risk factors in accordance with the following formula:

𝑣𝑘 = 𝐶𝑉𝐴(1.01𝑅𝐹𝑘) − 𝐶𝑉𝐴(𝑅𝐹𝑘) 0.01

where 𝑣𝑘 is the vega sensitivity of risk factor k.

13 SA-CVA: Delta Risk Weights and Correlations

105 An AI should calculate the risk-weighted sensitivities in accordance with the prescribed risk weights and correlations in this section.

13.1 Interest Rate Risk

106 Each bucket represents an individual currency exposure to the interest rate risk.

107 For currencies specified in paragraph 85, the risk weights are set as follows:

Risk factor 1 year 2 years 5 years 10 years 30 years Inflation

Risk weight 1.11% 0.93% 0.74% 0.74% 0.74% 1.11%

Table 3 108 For currencies not specified in paragraph 85, a risk weight of 1.58% is set for all the

risk factors, including the inflation rate.

109 For aggregating the weighted sensitivities within a bucket which is a specified currency in paragraph 85, the correlation parameters kl are set in the following table.

Interest rate risk correlations (kl)within the same bucket for specified currencies

1 year 2 years 5 years 10 years 30 years Inflation

1 year 100% 91% 72% 55% 31% 40%

2 years 100% 87% 72% 45% 40%

5 years 100% 91% 68% 40%

10 years 100% 83% 40%

30 years 100% 40%

Inflation 100%

Table 4 110 For aggregating the weighted sensitivities within a bucket which is not a specified currency in paragraph 85, the correlation parameter kl between the risk-free yield curve and the inflation rate is set at 40%.

111 The parameter γbc of 50% should be used for aggregating across different buckets (i.e.

different currencies).

13.2 Foreign Exchange Risk

112 A foreign exchange risk bucket is set for each exchange rate between HKD and the currency in which an instrument is denominated.

113 A risk weight of 11% applies to risk sensitivities of all the currency pairs except USD/HKD.

114 The risk weight of USD/HKD is set at 1.3% on the rationale that this risk weight captures the fluctuation of USD/HKD within the Convertibility Undertaking range (i.e.

7.75 to 7.85) under the Linked Exchange Rate System.

115 A uniform correlation parameter γbc that applies to the aggregation of delta foreign exchange risk positions is set at 60%.

13.3 Counterparty Credit Spread Risk

116 The risk weights for buckets 1 to 8 are set out in the following table. The same risk weight should be applied to all tenors for a given bucket, sector and credit quality.

Bucket number

Sector Credit quality Risk

weight

1

Sovereigns including central banks, multilateral development banks

Investment grade15 0.5%

Non-investment grade & unrated 2.0%

Local government, government-backed non- financials, education, public administration

Investment grade 1.0%

Non-investment grade & unrated 4.0%

2 Financials including government-backed financials

Investment grade 5.0%

Non-investment grade & unrated 12.0%

3 Basic materials, energy, industrials, agriculture, manufacturing, mining and quarrying

Investment grade 3.0%

Non-investment grade & unrated 7.0%

4

Consumer goods and services, transportation and storage, administrative and support service

activities

Investment grade 3.0%

Non-investment grade & unrated 8.5%

5 Technology and telecommunications Investment grade 2.0%

Non-investment grade & unrated 5.5%

6 Health care, utilities, professional and technical activities

Investment grade 1.5%

Non-investment grade & unrated 5.0%

7 Other sector Investment grade 5.0%

Non-investment grade & unrated 12.0%

8 Qualified indices (non-sector specific) Investment grade 1.5%

Non-investment grade & unrated 5.0%

Table 5 117 To assign a counterparty or reference name to a sector, an AI should rely on a classification that is commonly used in the market for grouping the counterparty or reference name by industry sector. The AI should assign each counterparty or reference name to one and only one of the sector buckets in Table 5 above.

Counterparties or reference names that an AI cannot assign to a sector in this fashion should be assigned to the other sector bucket (i.e. bucket 7).

118 An AI may opt for the treatment of qualified indices as set out in paragraphs 82 and 83. If more than 75% of constituents of a qualified index (taking into account the weightings of the constituents) are mapped to the same sector, an AI should map the entire index to that sector and treat it as a single-name sensitivity in that bucket. In

15 Unless otherwise specified, “investment grade” has the same meaning as specified in section 281 of the BCR.

other cases, the AI should map the sensitivity to the applicable index bucket (i.e.

bucket 8).

119 An AI should apply the look-through approach to assign each index constituent of (i) a qualified index if the AI does not opt for the treatment as set out in paragraphs 82 and 83 and (ii) a non-qualified index to buckets 1 to 7.

120 For buckets 1 to 7, for aggregating delta counterparty credit spread risk capital charges within a bucket, the correlation parameter 𝜌𝑘𝑙 between two weighted sensitivities 𝑊𝑆𝑘 and 𝑊𝑆𝑙 within the same bucket is set as follows:

𝜌𝑘𝑙 = 𝜌𝑘𝑙(𝑛𝑎𝑚𝑒)⋅ 𝜌𝑘𝑙(𝑡𝑒𝑛𝑜𝑟)⋅ 𝜌𝑘𝑙(𝑞𝑢𝑎𝑙𝑖𝑡𝑦) where:

𝜌𝑘𝑙(𝑛𝑎𝑚𝑒) is equal to 100% if the two names of sensitivities k and l are identical, 90% if the two names are distinct but legally related, and 50% otherwise;

𝜌𝑘𝑙(𝑡𝑒𝑛𝑜𝑟) is equal to 100% if the two tenors of the sensitivities k and l are identical, and 90% otherwise; and

𝜌𝑘𝑙(𝑞𝑢𝑎𝑙𝑖𝑡𝑦) is equal to 100% if the credit quality category of the sensitivities k and l are identical (i.e. both k and l are investment grade or both of them are non- investment grade & unrated), and 80% otherwise.

121 For bucket 8, for aggregating delta counterparty credit spread risk capital charges within a bucket, the correlation parameter 𝜌𝑘𝑙 between two weighted sensitivities 𝑊𝑆𝑘 and 𝑊𝑆𝑙 within the same bucket is set as follows:

𝜌𝑘𝑙 = 𝜌𝑘𝑙(𝑛𝑎𝑚𝑒)⋅ 𝜌𝑘𝑙(𝑡𝑒𝑛𝑜𝑟)⋅ 𝜌𝑘𝑙(𝑞𝑢𝑎𝑙𝑖𝑡𝑦) where:

𝜌𝑘𝑙(𝑛𝑎𝑚𝑒) is equal to 100% if the two indices of sensitivities k and l are identical and of the same series, 90% if the two indices are identical but of distinct series and 80% otherwise;

𝜌𝑘𝑙(𝑡𝑒𝑛𝑜𝑟) is equal to 100% if the two tenors of the sensitivities k and l are identical, and to 90% otherwise; and

𝜌𝑘𝑙(𝑞𝑢𝑎𝑙𝑖𝑡𝑦) is equal to 100% if the credit quality category of the sensitivities k and l are identical (i.e. both k and l are investment grade or both of them are non- investment grade & unrated), and 80% otherwise.

122 The correlation parameters γbc that apply to the aggregation of delta counterparty credit spread risk capital charges across buckets are set out in the table below.

Cross-bucket correlations for counterparty credit spread risk (γbc)

Bucket 1 2 3 4 5 6 7 8

1 100% 10% 20% 25% 20% 15% 0% 45%

2 100% 5% 15% 20% 5% 0% 45%

3 100% 20% 25% 5% 0% 45%

4 100% 25% 5% 0% 45%

5 100% 5% 0% 45%

6 100% 0% 45%

7 100% 0%

8 100%

Table 6

13.4 Reference Credit Spread Risk

123 The risk weights for buckets 1 to 17 are set out in the following table: