國⽴台灣⼤學管理學院企業管理碩⼠專班 碩⼠論⽂

Global MBA College of Management

National Taiwan University Master Thesis

手機應用程式 VS 購物網站給台灣消費者的體驗

Comparing the mobile app VS desktop website online shopping experience for Taiwanese consumers

李志濠

Zhihao Daniel Lee

指導教授: 陳家麟博⼠

Advisor: Chialin Chen, Ph.D.

中華民國 106 年 7 ⽉ July 2017

論⽂審定書

Acknowledgement

From 2013 to 2015, I have had the chance to work with various brands that were keen to build their presence via online marketing. A part of that involved designing and building websites as well as mobile apps for our clients. A lot of that work provided the inspiration and the industry knowledge that prompted this study. A big shout out goes to my ex-colleague Rachel Poo who provided the latest updates on the industry and important sources of information.

I would like to express my deepest gratitude to Professor Chialin Chen (Director of GMBA and Associate Dean of College of Management) for his patience, guidance and unwavering support throughout this study.

In addition, I would also like to thank all my GMBA classmates for the encouragement and support during these past few months. Special mention to Luke Chen, Melody Lin, Matthew Keyser and Penny Chang, for helping in recommending suitable interview candidates, working on trial interviews with me or giving advice. Thank you all.

Lots of appreciation goes to the interview candidates who took the time out of their busy schedules to share their personal thoughts. Without whom we would not have any results whatsoever.

Lastly to my close friends and family who supported me quietly throughout the time I was busy working on this study.

Abstract

It has been 10 years since the introduction of the iPhone, and during this time we have seen a global trend of consumers shifting focus to mobile apps. In particular, the retail industry has sought to develop assets that would allow them to ride this wave. With the balance of power seemingly being tipped in favor of mobile apps, some firms have also chosen to neglect websites, whilst others remain cautious and try to take small steps towards building multi-channel assets.

Both websites and mobile apps have been integral to growth of online shopping. What motivates us to carry out this study is recognizing that whilst for some countries mobile apps are pushing ahead, the statistics in Taiwan paint a slightly different picture. For a nation with high Smartphone adoption rate, high-speed Internet connectivity and a solid network of infrastructure, Taiwan surprisingly shows an unexpected inclination towards websites and not mobile apps.

Utilizing Alex Osterwalder’s’ Value Proposition Canvas allows us to try to uncover some underlying reasons why consumers still prefer purchasing via desktop websites.

Analyzing current value offerings for both platforms will allow us to see how they fare in the eyes of the consumer. With a deeper understanding of our local consumers, we can ascertain if platforms have been providing the right kind of value that our Taiwanese consumers are looking for.

Keywords: Online Retail, Mobile Apps, Websites, Value creation, Value Proposition Canvas, Shopping Platforms

Table of Contents

Acknowledgement ... iv

Abstract ... v

Table of Contents ... vi

List of Tables ... viii

List of Figures ... viii

1. BACKGROUND AND MOTIVATION ... 1

1.1 The Rise of Mobile Internet Retail ... 1

1.2 Online Shopping in Asia Pacific ... 2

1.3 Online Shopping in Taiwan ... 4

1.4 The Unrealized Opportunity ... 6

1.5 Our Focus ... 8

2. LITERATURE REVIEW ... 9

2.1 Motivations of Online Retail Behavior ... 9

2.2 Personalities and Experiences Approach ... 11

2.3 Summary of Literature Review ... 13

3. METHODOLOGY ... 13

3.1 Value Creation As A Foundation ... 13

3.2 Osterwalder’s Canvas ... 14

3.3 Insights Through Interviews ... 17

4.4 Surveying More Consumers ... 19

4. DEVELOPING OUR VALUE CANVAS ... 19

4.1 Carrying Out the Research ... 19

4.2 Customer Profile - Exploring Customer Jobs ... 20

4.3 Customer Profile - The Customer Pains ... 25

4.4 Customer Profile - Finding Customer Gains ... 33

4.5 Approaching The Value Map ... 40

4.6 Selecting Our Cases to Examine ... 41

4.7 Momoshop - Pain Relievers ... 43

4.8 Momoshop - Gain Creators ... 46

4.9 The Momoshop Value Map ... 48

4.10 Carousell - Pain Relievers ... 50

4.11 Carousell – Gain Creators ... 52

4.12 The Carousell Value Map ... 55

4.13 The Resulting Matchup ... 56

4.14 Additional Interview Insights ... 60

5. CONFIRMING & COMPARING FINDINGS ... 68

5.1 Conducting Online Survey ... 68

5.2 Survey Findings - Customer Profile ... 69

5.3 Other Insights From Survey ... 76

5.4 The Similarities ... 79

5.5 The Inconsistency ... 80

6. LIMITATIONS ... 81

6.1 Limitations of Interview ... 81

6.2 Limitations of Survey ... 81

6.3 Inherent Platform Characteristics ... 82

7. IMPLICATIONS ... 83

7.1 For Mobile App Platforms ... 83

7.2 For Website Retail Platforms ... 85

8. CONCLUSION ... 88

9. REFERENCES ... 90

10. APPENDIX ... 93

List of Tables

Table 1.2.1 – Historical YOY Growth % ... 2

Table 1.2.2 – Historical Retail Value ... 2

Table 3.2.1 – Building blocks of the Canvas ... 16

List of Figures

Figure 1.2.2 – Research vs. Purchase device ... 3Figure 1.3.1 – Taiwan situation Smartphone ... 4

Figure 1.3.2 – Purchase Device ... 5

Figure 1.4.1 – Comparing other Countries ... 6

Figure 1.4.2 – Singapore vs. Taiwan ... 7

Figure 1.4.3 – Most Common Activities on Smartphone ... 8

Figure 2.1.1 – Technology Acceptance Model by Childers ... 10

Figure 2.2.1 – Technology Acceptance Model by O’Cass ... 12

Figure 3.2.1 – Arriving at the Canvas ... 15

Figure 3.2.2 – The Value Proposition Canvas ... 15

Figure 4.2.1 – First Component of Customer Profile ... 21

Figure 4.2.2 – Ranked Customer Jobs Section ... 23

Figure 4.3.1 - Second Component of Customer Profile ... 25

Figure 4.3.2 - Ranked Pain Points (MOBILE) ... 27

Figure 4.3.3 - Ranked Pain Points (WEBSITES) ... 31

Figure 4.3.4 – Comparing Pains (Mobile Apps Vs. Websites) ... 32

Figure 4.4.1 - Third Component of Customer Profile ... 33

Figure 4.4.2 – User Journey & Expectations ... 36

Figure 4.4.3 – Ranked Customer Gains Section ... 36

Figure 4.4.4 – Completed Customer Profile for Online Shopping ... 39

Figure 4.5.1 – Main Components of Value Map ... 40

Figure 4.3.2 – Internet Retail Sites/Apps used by Interviewees ... 41

Figure 4.9.1 – Completed and ranked Value Map (Momoshop) ... 49

Figure 4.12.1 - Completed and ranked Value Map (Carousell) ... 55

Figure 4.13.1 – Value Customer Fit (Momoshop) ... 56

Figure 4.13.2 – Value Customer Fit (Carousell) ... 58

Figure 5.1.1 – Survey Respondents Breakdown ... 68

Figure 5.2.1 – Motivations for Online Shopping ... 69

Figure 5.2.2 – Gender Differences in Motivations ... 70

Figure 5.2.3 – Motivations by Priority ... 71

Figure 5.2.4 – Browsing vs. Purchasing ... 72

Figure 5.2.5 – Platform Preference ... 73

Figure 5.2.6 – Improved Apps lead to Increased Usage ... 73

Figure 5.2.7 – Frustrations Using Mobile Apps ... 74

Figure 5.2.8 – Ranking Frustrations ... 74

Figure 5.2.9 – Expectations of Respondents ... 75

Figure 5.3.1 – Do Online Consumers Still Shop Offline ... 76

Figure 5.3.2 – Motivations for Offline Shopping ... 76

Figure 5.3.3 – Payment Preferences ... 77

Figure 5.3.4 – Would Use LINE Marketplace? ... 78

Figure 5.3.5 – Pull factors for LINE marketplace ... 79

1. BACKGROUND AND MOTIVATION

1.1 The Rise of Mobile Internet Retail

Transformations have been happening in all aspects of business since the introduction of the smartphone and with it the rise of the mobile Internet. Much of these transformations, centered on advertising and marketing products, have happened at an incredible pace over the last decade (M. Johnston, 2015), pushing businesses out of their comfort zone to adopt new strategies as a response to this ‘mobile uprising’. The speed at which businesses have had to adapt to both increasing market competition and demanding consumer preferences have rendered companies quickly irrelevant if they were unwilling or unable to keep up. In 2015, US retailer Radio Shack could no longer keep up with having too many brick-and-mortar shops and the quickly transitioning Internet shopping landscape saw them filing for bankruptcy (A. Gara, 2015) despite a brand name that resonated with technology enthusiasts across the country.

Industries across the board felt the effects as mobile Internet took flight, but perhaps none as strikingly as the retail industry. Before the introduction of the smartphone, consumers were already shopping online via desktop computers, and most major retailers had invested in e-commerce websites in a bid to capture a slice of the online shopping market. Then online shopping became a whole new ball game as consumers were opened to a world where they could browse, search and purchase directly from their smartphones. This presented retailers a new channel or avenue to reach out to their audiences and create meaningful, timely interactions (S. Levin, 2015) and at the same time consumers now had access to information while on the go, no longer being restricted to Internet cafes or home. This was the beginning of mobile Internet retailing.

1.2 Online Shopping in Asia Pacific

Online shopping presents a huge market opportunity in the APAC region, an average growth rate of 34% over the last 5 years Table 1.2.1 (Passport Stats, 2017) only served to encourage more new entrants. Last year in Asia Pacific alone, consumers have spent more than US$523’216 Million on Internet shopping, Table 1.2.2 (Passport Stats, 2017) and this number is expected to increase as developing nations such as Indonesia, Philippines and Vietnam catch up on the technology front.

Table 1.2.1 – Historical YOY Growth %

Table 1.2.2 – Historical Retail Value

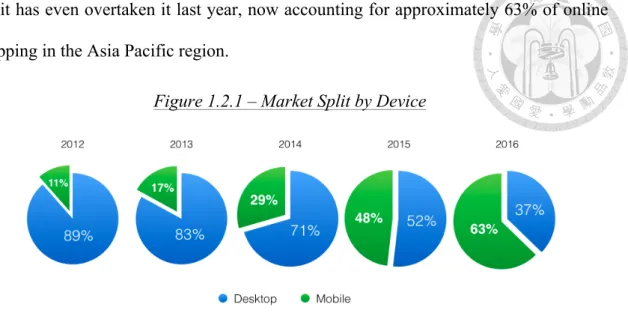

What is interesting to note is that this growth in Asia Pacific is now being driven by mobile Internet shopping and the many new shopping apps that are used by consumers.

Having only begun with US$19’318 million in 2012, mobile retail has in a short span of 3 years closed the gap on desktop retail, reaching US$200’177 million in 2015 see Table 1.2.2 (Passport Stats, 2017). As illustrated below in Figure 1.2.1 (Passport Stats, 2017), we can clearly see that mobile retail has not only caught up to desktop shopping

but it has even overtaken it last year, now accounting for approximately 63% of online shopping in the Asia Pacific region.

Figure 1.2.1 – Market Split by Device

Such statistics may point towards a mobile-centric audience in the future, and some firms may be tempted to believe building a website retail presence is unnecessary, but many consumers have more than one device that they access the Internet with, and use multiple devices at different junctures of the retail journey. Based on a 2015 Q4 report of online sales, approximately 37% of transactions have consumers doing research on one device and then completing the purchase on another device (State of Mobile Commerce, 2015). Whether they finally make the purchase using their desktop or mobile, a notable percentage of consumers have researched or initially considered the item using the other device as shown in Figure 1.2.2 (H. Leggatt, 2016).

Figure 1.2.2 – Research vs. Purchase device

It is thus important also for companies to establish a strong Omni-channel strategy. By using various digital and physical Channels to provide a seamless shopping experience, retail stores are better able to differentiate themselves from competitors (E. Sopadjieva, M. Dholakia, B. Beth, 2017).

1.3 Online Shopping in Taiwan

As we turn our attention to the scenario here in Taiwan, it is also pretty similar in that many consumers own more than one device, 2.7 connected devices per person as shown in Figure 1.3.1 (Consumer Barometer, 2017) and 89% of Taiwanese use their smartphones just as often as their desktop computers.

Figure 1.3.1 – Taiwan situation Smartphone

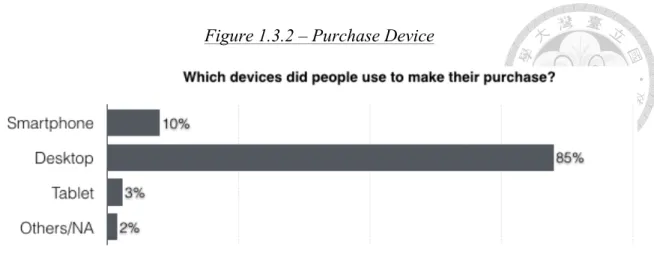

Consumers have more devices and are spending more time on their smartphones, however, that doesn’t mean that mobile Internet retail has completely taken over online shopping here in Taiwan. In fact, if we dig deeper into online purchase behavior in Taiwan, only about 10% out of a group of people surveyed by Google in 2015 said that they made the purchase via their smartphone, Figure 1.3.2 (Consumer Barometer, 2015) while majority still made purchases via their desktop.

Figure 1.3.2 – Purchase Device

Other reports estimate that 70% of Taiwanese online shoppers have tried using their smartphones to make purchases (SP Ecommerce, 2015) and insist that Taiwan is a mobile ready nation. While the proportion of mobile to desktop purchase rates in Taiwan may lag behind the Asia Pacific overall proportion, Taiwan’s overall Internet retail market is in no way small, boasting an average growth rate of 10-15% annually over the last 5 years (M. Fulco 2017) and reaching sales of US$34 billion in 2015.

Taiwan’s high Internet penetration rate is only but one of the reasons why online shopping is such a success here. Fast Internet connectivity speeds, a unique consumer culture, a very wide selection of available merchandise, a comprehensive logistics infrastructure, and ease of payment with a solid convenience store network supporting (C. Quek, 2016) means the Taiwan market can only continue to grow larger in the future. There are many more articles and different opinions that dive further into the current state of online shopping in Taiwan, but the main focus of this paper isn’t to figure out the trending statistics or potential growth rates of mobile Internet retail.

1.4 The Unrealized Opportunity

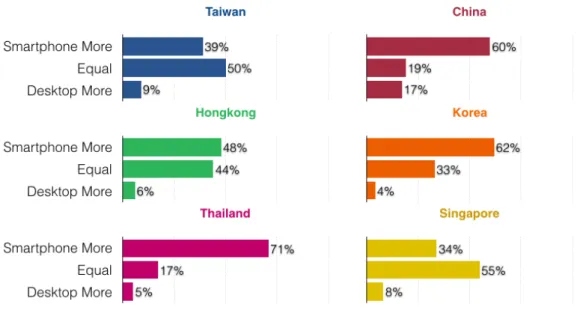

As mentioned earlier, consumers in Taiwan own multiple devices and spend plenty of time on their mobiles, in fact most Taiwanese go online using their smartphones either more than desktops (39%) or equally (50%) as illustrated in Figure 1.4.1 (Consumer Barometer, 2015).

Figure 1.4.1 – Comparing other Countries

While Taiwan’s percentages may fall behind some others such as China, Korea, or Thailand, it is still a indicative sign that with the amount of time consumers spend on their smartphones the mobile platform is a huge unrealized opportunity for retailers. To put things in perspective, Singapore’s percentages show a somewhat similar trend to Taiwan, with 34% spending more time on their mobile and 55% equally distributing their time between mobile and desktop. We should thus expect Taiwanese consumers to have an almost similar likelihood to purchase using their mobiles when compared to Singapore. A quick statistical check with Google’s Consumer Barometer Survey reveals that even though Taiwan consumers spend more time on the smartphone, they actually

purchase less from this device, Figure 1.4.2 (Consumer Barometer, 2015). Singaporeans are almost twice as likely to purchase using smartphones.

Figure 1.4.2 – Singapore vs. Taiwan

It might perplex retailers as to why with the amount of time consumers are willing to spend on their smartphones that mobile retail has not been as prevalent here in Taiwan as it has in some other parts of the region.

Even before having to dive into researching the possible cause of this, it is fair to guess that consumers in Taiwan are spending plenty of time on their smartphones engaging in other activities. Most common guesses would include the use of Social Media such as Facebook, Instagram and YouTube, and Figure 1.4.3 (Consumer Barometer, 2016) shows a much clearer breakdown of how the Taiwanese are spending their time on their smartphones on a weekly basis. Bulk of those surveyed said they would be using search, Social Media and watching videos online, followed by checking email, checking for directions and doing product research. Even with this survey being slightly biased in that the time frame is too narrow and only considers a person’s weekly activities, as little as 12% said they would be using their smartphones for online shopping.

Figure 1.4.3 – Most Common Activities on Smartphone

1.5 Our Focus

Many have pointed out that Taiwan has the potential to be a strong mobile Internet retail ground, yet we observe a current mismatch between actual times spent on smartphones and the choice of where to make a purchase. Perhaps consumers in Taiwan are not ready for mobile retail, or perhaps there are some underlying causes as to why mobile shopping apps have yet to capture the hearts of the average online shopper.

What this paper hopes to explore and identify are some of the consumer preferences when shopping online using mobile and desktops. We will try to get an understanding of what considerations the Taiwanese online consumers have, and how both mobile apps and desktop websites have succeeded or failed in addressing those needs. By comparing how Taiwanese consumers feel about each platform, it will give us a slightly clearer picture of why there is a stronger preference for website retail over mobile app retail. At the end of this paper, perhaps we would have some basic consumer insights that would allow current and new, mobile or desktop online shopping platforms to find better solutions that centers on user needs and preferences.

2. LITERATURE REVIEW

2.1 Motivations of Online Retail Behavior

Just as every company does market research before actually developing a product, so too should retailers who are going into the space of Internet shopping. One such area of study that is commonly used is the motivations for online retail behavior. There are definitely functional benefits to online shopping thanks to the multitude of information available at fingertips and quick accessibility that allow users to lower their search cost (Alba et al., 1997). Other scholars have also directed online shopping motivations to the

‘fun’ and ‘entertaining’ aspects of connecting with online media and brands while shopping (B. Orwall, 2001).

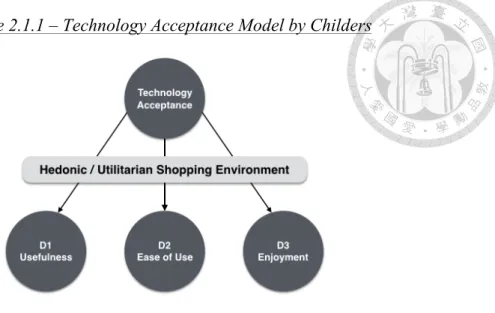

Online retail is now driven by both utilitarian and hedonic motives (T.L. Childers et al., 2001), and this mix of efficiency and experience will further push the adoption of technology assisted shopping. Childers and his team explores this topic by using a framework known as Technology Acceptance Model or TAM (F.D. Davis, 1993), and touched upon 3 determinants: Usefulness, Ease of Use and Enjoyment. The study shows that these 3 basic determinants mentioned all have a positive relationship to the acceptance of technology assisted shopping, but Childers takes it one step further in his study by adding the context of the shopping environment.

By adding a context to the shopping environment (Figure 2.1.1) and classifying them as either utilitarian or hedonic, the hypotheses and results allow us to better distinguish the effects of the 3 determinants.

Figure 2.1.1 – Technology Acceptance Model by Childers

Childers’ research also acknowledges that the 3 determinants are but perceptions of consumers and the analysis required additional factors or antecedents that would be enable them to measure how consumers felt about each determinant. These antecedents include the flexibility of navigation so that consumers can complete the search for information (Alba et al, 1997), the technology’s convenience and overall accessibility, (D.L. Hoffman & T.P. Novak, 1996). As well as the obvious lack of physical touch whilst shopping online (Alba et al, 1997). After carrying out two separate studies to cater to different shopping environments, they present their findings in which both set of results point towards enjoyment being a consistent and strong determinant of acceptance toward online shopping. Similarly, usefulness and ease of use were also significant across both studies. Needless to say, enjoyment has a stronger effect then ease of use when in a hedonic environment, but in a utilitarian context it is the other way around. The paper urges us to note the varying level of significance depending on given contexts and that consumer’s attitudes or expectations may change. Childers concludes their study managing to prove their various hypotheses, highlighting how even in a goal-driven e-commerce environment, it is important to consider that by increasing the level of enjoyment for consumers, retailers are able to better differentiate themselves from brick-and-mortar shops.

2.2 Personalities and Experiences Approach

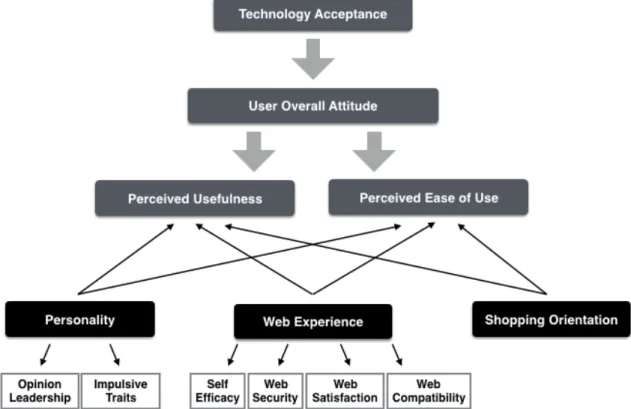

The adoption of web retail or Internet shopping is based on a prospective user’s overall attitude towards the technology (A. O’Cass and Fenech, 2003) and can be broken down into two major thoughts - perceived Usefulness and perceived Ease of Use (F.D. Davis, 1989; E. Karahanna and Straub, 1999). This is similar to the paper by Childers in using a TAM approach to study behavior towards adoption of Internet retailing, but O’Cass adds a different dimension to the study based on three factors that might influence consumer perceptions of Usefulness and Ease of Use.

The first factor mentioned is personality, and O’Cass brings up several authors who point out that opinion leadership influences innovative behavior. These opinion leaders have often been associated with early adopters, choosing to accept the perceived risk to meet their own needs (A. O’Cass and Fenech, 2003), and more importantly act as advocates or opponents afterwards. Personality is also reflected through a consumers’

spontaneity or susceptibility to impulse buying online (S. Beatty and Ferrell, 1998) just as he or she would while shopping at a physical store after touching and experiencing the product in the carefully crafted environment.

The other major factor that is brought up by O’Cass is consumers’ personal web experiences. The retailer or web designer creates most of the user experience, where the sites’ security, layout as well as navigation all come together to ensure consumer has a positive and satisfying experience. Shopping online does indeed contain a level of perceived risk in terms of information security, financial risks, not getting the product, poor quality of product etc. so how consumers view the security of a retail site is really important. Only with a satisfied experience will an online consumer be willing to take it

to the next step and make a purchase. A less commonly remembered part of the personal web experience factor is how long or how comfortable a consumer is with using a particular technology, otherwise known as self-efficacy (F.D. Davis, 1989). As a consumer interacts or uses multiple sites, they accumulate more personal experience, and this may create a belief in their efficacy for its extension into retail usage for purchasing products.

Last but not least, the compatibility between the technology and the users’ needs, values, past experiences and routines (E.M. Rogers, 1983). This means that the retail technology needs to provide the consumers real value and not just provide an additional storefront on the Internet (A. O’Cass and Fenech, 2003). Then this compatibility, or as O’Cass refers to as shopping orientation, will be able to positively influence both perceived Usefulness and Ease of Use.

Figure 2.2.1 – Technology Acceptance Model by O’Cass

The Figure 2.2.1 above summarizes the factors as well as components laid out by O’Cass, and his study concludes by highlighting how the many antecedents (Opinion Leadership, Impulsiveness, Shopping Orientation, Web Shopping Compatibility, Internet Self-Efficacy, Perceived Web Security, and Satisfaction with Web sites) affects Internet users beliefs about online retail.

2.3 Summary of Literature Review

Have most people begun simply with the topic of online shopping; there would have been many various paths to take to analyze this domain. The studies undertaken by Childers and O’Cass have hovered on the consumer behavioral aspects and sought to better understand the motivations of buyers in acceptance of technology. The utilitarian vs. hedonic argument presents us with very tangible aspects of discussion like how the navigation and accessibility affect a user. Whilst O’Cass approaches the topic exploring how experiences and personal learning will determine a users’ confidence in using web retail. Both studies provide us insight on the factors that may influence perceptions of consumers and are inline with what this paper hopes to explore.

3. METHODOLOGY

3.1 Value Creation As A Foundation

As mentioned earlier, technology is only deemed useful if it provides consumers with some kind of real value (A. O’Cass and Fenech, 2003), thus as we explore the choice between online shopping devices in Taiwan, it is important to understand the thoughts of the Taiwanese consumers and what value they are seeking.

Well known for his work on the Business Model Canvas (BMC) widely used in business schools around the world, Alex Osterwalder also has a second book titled Value Proposition Design focused on the topic of finding and using value to create meaningful products. This is an extension of his earlier work which we all know as the BMC, and the nine business building blocks it comprises: Key Partners, Key Resources, Key Activities, Customer Relationships, Channels, Customer Segments, Value Propositions, Cost Structure and Revenue Streams. They are all important building blocks, but it is the value and customer segments that make Alex Osterwalder’s work relevant to this paper.

The BMC was designed to allow a firm to fully describe all aspects of their business in one quick glance and often used where groups can come together to discuss or analyze corporate decisions together. However, filing in some parts of the BMC may be a long drawn out process, involving many contrasting or conflicting ideas from co-workers, and this is where Value Proposition Design comes into play. The main concept of Alex Osterwalder’s sequel book is about applying a set of tools to simplify the otherwise messy search for value propositions that customers want. With these set of tools, a team can continually evaluate if they have strayed from what customers desire. “Value proposition design is a never-ending process in which you need to evolve your value propositions constantly to keep it relevant to customers.” (A. Osterwalder et al., 2014)

3.2 Osterwalder’s Canvas

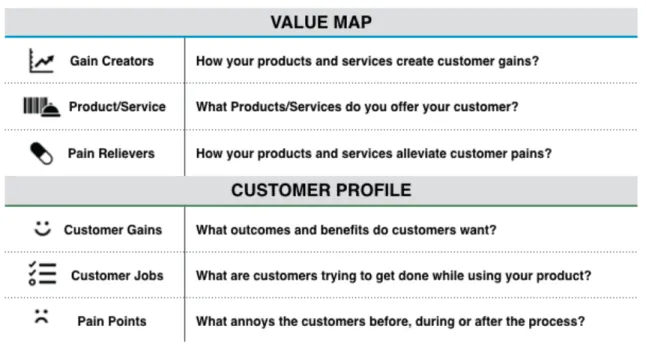

At the heart of the Value Proposition Design framework is Osterwalder’s Value Proposition Canvas, which zooms into two of the building blocks within the BMC mentioned earlier - Value Proposition and Customer Segments, Figure 3.2.1 (A.

Osterwalder et al., 2014). His approach first brings us from a broad view of business context down to the specifics of creating value for the business, and the Value Proposition Canvas zooms in further to focus on creating the value for customers.

Figure 3.2.1 – Arriving at the Canvas

The canvas as shown in Figure 3.2.2, comprises of two sides. The Value Map where a firm figures out what are the values they can deliver through their product/service and the other side is Customer Profile, in which the target audience’s objectives, goals and desired solutions are observed.

Figure 3.2.2 – The Value Proposition Canvas

A customer-inspired approach requires us to understand the “Gains”, “Jobs” and

“Pains” of the customer and then tailor our product/service to satisfy the needs and also relieve the pains they may have. Many a times, companies come up with products/services that do not actually provide the value that customers seek, leaving a manager with many questions on performance and sometimes spending unnecessary money to carry out marketing efforts that remain futile. In order to avoid that, firms need to find a fit between value map and customer profile, and Osterwalder explains the elements on both sides of the Value Proposition Canvas, as shown in Table 3.2.1 below.

(A. Osterwalder et al., 2014)

Table 3.2.1 – Building blocks of the Canvas

After understanding each element of Osterwalder’s Value Proposition Canvas, we can now move on to explore the customer profile of Taiwanese consumers and also what they think about the current market players’ offerings. This would be similar to exploring customer perceptions about Usefulness and Ease of Use, which as we have seen earlier influence customers’ attitude towards adoption. This will be mainly achieved using two main tools, interviews and surveys.

3.3 Insights Through Interviews

We recognize that there are many variables that could influence a consumer’s choice of shopping platform. The customer demographics, the product category, as well as the type of mobile application operating system they are using. These are all variables that might throw a statistical study in a particular direction. If we were to approach this paper with the same statistical testing methods, it would mean carrying out a study based on preconceived ideas of the variables and would be biased. However, this paper assumes that we know nothing about how the Taiwanese consumers feel towards online shopping. Thus instead of approaching this with a statistical analysis, or using a Technology Acceptance Model (TAM) like Childers and O’Cass, this paper will adopt a more qualitative approach of exploration using interviews.

By utilizing in-depth interviews, it will allow us to thoroughly explore feelings and motivations of customers. A semi-structured style will be used so consumers can freely share their thoughts, which may jump from one to the other while conversing. Basically this allows much more space for interviewees to answer on their own terms than structured interviews, but still provide some amount of structure for comparison across multiple interviewees (R. Edwards and J. Holland, 2013). A list of questions in the form of an interview guide will be used, but there is flexibility in the arrangement of how questions are asked and how the interviewee can respond. With the freedom to probe for answers, it is easier to follow a line of discussion opened up by the interviewee, and a dialogue can ensue. (R. Edwards and J. Holland, 2013)

Interviews also allow us to select individuals that fulfill a certain criteria – experience, gender and age. Consumers with sufficient online shopping experience will be better

able to share some of the challenges or feelings of using the current online platforms.

Also as more and more men take to online shopping, we wanted to ensure a gender balance in our choice of interviewees and while there is an increasingly broad age bracket of consumers shopping online, we wanted to narrow it down. For our study the focus will remain only on a broadly defined “youth” category that comprises University students and young professionals, we believe this group have the right spending power and make up the bulk of online shoppers. As such we will adopt a single Customer Profile comprising of both students in the mid to late twenties and young working professionals in the early thirties.

The final interviewees were selected through asking around personal networks, and consisted of 4 individuals. (Their names are kept anonymous to maintain privacy but we shall refer to them as stated below)

1) Y: Female, University Student, 25 yrs old 2) C: Male, University Student, 26 yrs old 3) L: Female, Working Professional, 33 yrs old 4) H: Male, Working Professional, 34 yrs old

The insights and sharing from our interviewees would give us the required ingredients to fill out the Customer Profile of Osterwalder’s Value Proposition Canvas.

4.4 Surveying More Consumers

Since the interviews will focus on just a few individuals, as a closure to our study an online questionnaire will also be used to poll a larger sample sized audience. The survey enables us to reach out to more online consumers and test if the insights from the interview are representative of these consumers or simply just the thoughts of a few select individuals. The survey will focus on consumer goals and habits, their preferences, pains and expectations of online shopping platforms. It will also allow us to get additional perspectives from the larger audience that may have been left out from our conversations with the interviewees.

Together both set of results would provide us a much more comprehensive picture of the consumer preferences, the thoughts and also the motivations behind the online retail scene here. It also serves as a check at the end of our paper to confirm how accurately we have filled out our Value Proposition Canvas.

4. DEVELOPING OUR VALUE CANVAS

4.1 Carrying Out the Research

Over a period of 3-4weeks, we met up with our interview candidates, preferably at less formal settings to give them an environment that they would be comfortable in. Each interview lasted an hour, giving us ample time to talk freely about the topic, with much of the interview being held with a casual conversation style.

Instead of taking notes during the interview, we sought permission to record the audio clips of the interview. This allowed us to focus much more on having meaningful conversation with the interviewees and not have to be distracted with taking notes, it was great as it allowed us to have a much simpler job when going back to listen to the interview. The interviewees were more than willing to help in this aspect, feeling none of the pressure of being recorded whatsoever. They not only provided us insights based on the questions asked, but also points that we didn't even consider. Qualitative interviewing also meant we were able to adjust as we went along - learning points from the first interview were then taken into consideration during the later interviews.

The interview results were then collated, compared and use to populate the Customer Profile, which consists of 3 main components, and we will go through them in the following sections.

(I) Customer Jobs (II) Pain Points (III) Customer Gains.

4.2 Customer Profile - Exploring Customer Jobs

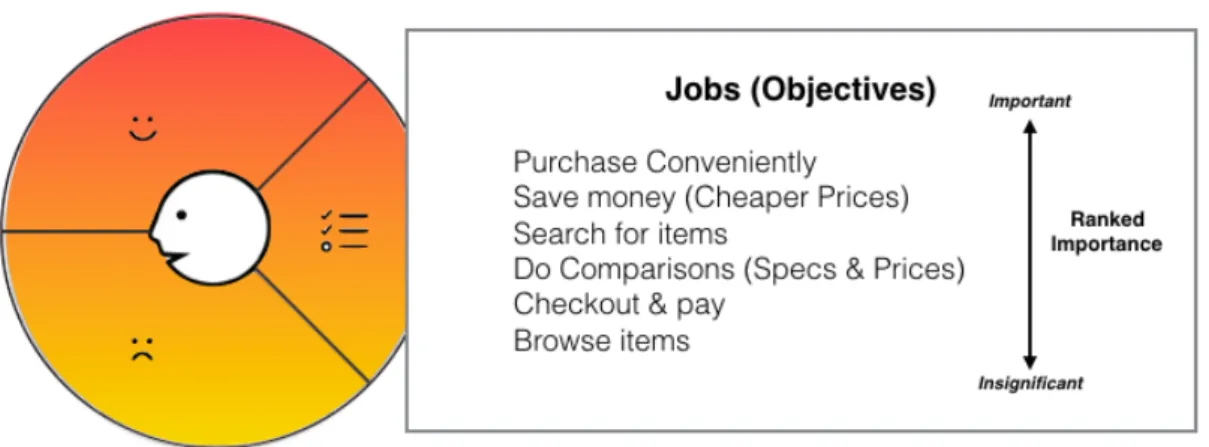

Our first step to completing the Customer Profile is to explore the goals and objectives of users based on our detailed interview insights. Shopping online has become somewhat of a norm to many people in this day and age, yet many people have rarely given it much thought why they are going online to buy something or what drives them to choose to use the online method. Figure 4.2.1 below summarizes the questions that we need to answer.

Figure 4.2.1 – First Component of Customer Profile

A variety of reasons were mentioned during the interviews including finding items that would not have been sold in Taiwan stores, purchasing from overseas brands, saving money with generally lower prices, and also saving time when they can browse and find many items online. Here one of our interviewees mentioned about the purchase objective of getting items from overseas:

Y: "Online shopping allows me to find some things I can’t find elsewhere, for example a hair care shampoo that you can’t find in Taiwan. Other items that you can only find from overseas and ship them over."

At the same time, one of the common themes that came up from all four of the interviewees was convenience and how buying something online now allowed them the freedom to do it without having to go out around looking for something. They were now able purchase items using less effort than going out to the store, searching for it and going from store to store until finally making the purchase or giving up.

Y: "I bought a Bluetooth earpiece recently as they could deliver in 24 hours, and I wanted to get it quickly, but overall it is also mainly because of the convenience of getting it from searching to purchasing to delivered to me"

L: "Sometimes you're just too busy to go to the store, and if you need daily items you can just purchase them online via PC Home. I think convenience is also key, it means I don't have to go out and look for something"

With this new simplicity of online shopping, consumers do not have to expend as much effort in looking for items and buying it. This reduction in effort provides consumers convenience that makes it meaningful to shop online, and also saves time for users. If we simply followed a model of a user’s journey, the “Jobs” that our respondents shared with us were the browsing, searching for items, comparing, and checking out or paying for items.

However Osterwalder’s canvas wasn’t based on simply identifying the customer jobs along the user journey, but also takes into consideration the level of importance for those goals and objectives. When asked what were the main goals or to rank the importance of the “Jobs”, our interviewees all cited convenient purchasing and saving money with cheaper prices off the top of their head.

L: "Price! Some things you can’t buy in Taiwan, but you can find online. Also some things you can find at the actual stores, but it will be cheaper online as they don’t have to pay for overheads"

H: "Price is cheaper and saves effort instead of going out to buy stuff as it is more convenient"

C: "Convenient, now I can quickly find and buy many things without actually running to the physical store"

All 4 of our interviewees gave very similar answers and with the responses that we managed to obtain, it was then easy to fill in the Customer Jobs section while ranking them in level of importance.

Figure 4.2.2 – Ranked Customer Jobs Section

As seen in the ranked list, the primary objective when going online to shop was basically to purchase items conveniently from the comfort of home or even while they were on the go. This was followed by the ability to save money thanks in part to cheaper prices offered online. The variety of available products online also allowed for users wanting to search for hard to find goods or a particular item to turn to online shopping. In the midst of the shopping process, users would want to compare items in terms of size, technical specifications and prices. One of our younger interviewees felt that it was actually a major part of her shopping journey.

Y: "Comparing items and prices is one main objective while I’m shopping. For the Bluetooth earpiece I purchased recently, I did a lot of comparisons to find the best deal."

Not ranked so high on the list are the checkout & payment process, and surprisingly the browsing of items. Upon a deeper look into some of the responses, we realized that our

interviewees could be broken down into 3 distinct groups, those that didn’t browse but just went online with something in mind, those that were browsing regularly whilst shopping online and those that lie somewhere in between. Only one of our interviewees had indicated to have really browsed shopping platforms on a regular basis. Perhaps offering a valid explanation to why Browsing was not ranked as important by our interviewees.

Our conversations not only allowed us to find out the “Jobs” users were trying to accomplish, how they were ranked in level of importance, but it also provided plenty of feelings and thoughts that revolved around usefulness and ease of use. With the latest technologies, consumers are able to shorten the time required at each stage of the purchase journey: Log on, Search, Compare, Decide & Pay, Delivery & Collection, thereby allowing them to be more satisfied with the whole shopping experience.

Still this online shopping experience must continue to develop and improve. It must be able to help consumers find what they are looking for easily and quickly, and provide consumers the convenience to purchase items from anywhere. It must provide sufficient range of products so consumers can find various items and it must be able to offer consumers attractive prices. Consumers have very clear goals that they want to achieve shopping online and if online platforms fail to assist consumers in achieving them, they have planned to fail.

4.3 Customer Profile - The Customer Pains

Moving on to the second component of the Value Proposition Canvas, we set out to explore the “Pains” or frustrations that users have while going through the online shopping experience.

Figure 4.3.1 - Second Component of Customer Profile

To provide more clarity while examining the “Pains” of consumers, we will look at websites and mobile apps separately. Since prior research and our interviewees have both told us that Taiwanese consumers do not favor apps, let us first take a look at the frustrations of using mobile apps.

Of course we all know that the mobile screen being smaller will pose certain issues with consumers, but hearing some of these issues from the interviewees offered a clearer understanding of why it mattered.

Y: "I don’t use apps because most of the time I like to compare and open many websites. On the desktop you can open many windows to compare items and prices. On apps you can’t open multiple apps without switching in between and you can’t view multiple items at once to compare.”

C: "One downside is not able to view many things at once on mobile app, on the app you can only see 4-6 items at once, but on the desktop you can view many more things. So harder to do comparisons on the mobile so that is also a problem - especially comparing across different sites is almost impossible.”

L: "Viewing experience on mobile is terrible as you can’t view many items at once - you always have to keep clicking next page next page - I think its one of the annoyances.”

Clearly the limitations of displaying multiple items on a smaller screen has had huge influence on consumers, in terms of the difficulty in comparing and also the excessive navigation users have to go through while browsing or searching for something on the app. This limited view of items goes beyond just viewing photos of items but also the details and information presented when users are looking into the specifics of a product.

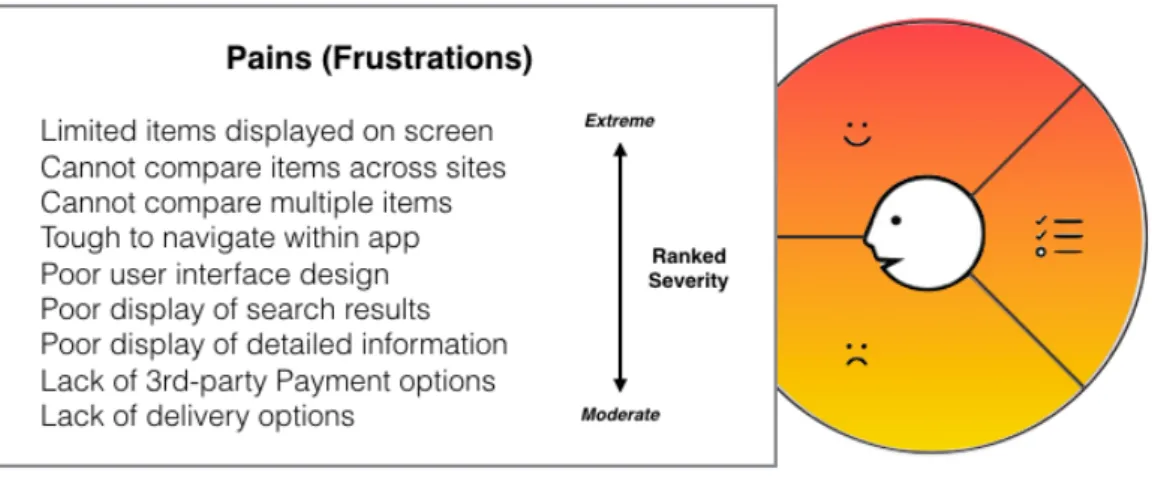

Other frustrations include lack of delivery options, lack of third-party payment options, difficulties in browsing and the way search results are displayed.

When considering some other product/service categories, perhaps pain points or frustrations do not heavily dissuade the user and many a times users might just chose to overlook such frustrations. This does not seem to be the case when it comes to using mobile apps for online shopping, which seems surprising even more so since we are so reliant on our smartphones these days. When asked if those pain points and frustrations actually affected their purchase decisions, 3 out of 4 interviewees insisted that because of their frustrations they would choose to use a different app, or abandon the mobile app altogether and revert to website shopping.

C: "If they have limited delivery options then, I will choose another seller/site.

Also if I’m doing comparisons then I wouldn’t choose to use mobile app but the desktop."

Y: "For me it’s a major consideration. I don’t browse or purchase on app as I can’t do my comparisons and ‘homework’ or research on the products.”

L: "It does affect, if I have to click through many pages then I will just forgo this app and go to nicer designed overseas sites. Some of the overseas sites are also nicer looking.”

Although our interviewees did not provide too long a list of frustrations for using mobile apps, they did all reiterate points that centered on simplicity and convenience.

Those also made up some of the points that were ranked higher in terms of “Pains”

while using mobile apps for shopping.

Figure 4.3.2 - Ranked Pain Points (MOBILE)

The top frustration for consumers was the limited number of items mobile apps displayed. This not only affected the browsing experience, the way search results were

displayed but also the navigation and overall user experience as mentioned above in some of our direct quotes from interviewees. This was pretty much what we expected, but the next few “Pains” were unexpected – in that consumers were really keen on comparison features or bothered by the difficulty in trying to compare while using the mobile app. This highlights the importance of comparisons while seeking to make a purchase and is somewhat reflective of the brick-and-mortar shopping journey as well.

Consumers have a tendency to want to get the most value out of their shopping, thus are looking to compare and contrast items, choosing the one that gets them the most bang for their buck.

Although the next few points in the list of frustrations could very well be a cause of the small screen size mobile app developers have to work with, we have decided to look at it independently of that. Poor user interface, unintuitive navigation and display of information are all a choice of design. Some apps have gotten it right, and have thrived in the mobile retail scene. Some have just placed less thought into design and tried to shrink down the website into a mobile app. The user experience is thus not ideal, when the flow and the display of information have not been calibrated to a mobile app shopping process.

The final two “Pains” are less critical to our interviewees, and in part just poorer execution of value-added features for customers. These are frustrations that could often be overlooked by users if they find what they are looking for and really like a certain product.

Now let us compare that with the website experience that our users have. Here the answers were far less homogeneous, with different interviewees basing their answers on different phases of the shopping experience. Some were more frustrated with the initial browsing and searching phases of shopping as explained below.

Y: "Because I really like to click and open many windows while searching for something, there are some annoyances. Some products are identical but are being sold by different sellers, but it is only after I clicked everything that I realize that actually I’m wasting time looking at duplicates. Also for comparing across websites that is still sometimes not as easy.”

C: "For some websites in which the layout is very messy, then it becomes overwhelming! Some example like on one page you are bombarded with 200 items, which makes it difficult to shop too, so I think there should be a balance between how many items to display - mobile app too little vs. desktop too many.”

Others were focused more on the latter stages of the shopping experience, the decision making portion and the payment.

L: " Price comparison is a big factor for me when trying to make a decision, so maybe in the sense of comparing the process has to be easier. Also maybe when making payment, the filing in of information - sometimes that is annoying to have to keep redoing.”

The website experience clearly involves a different set of issues for consumers. We also note that the frustrations for using websites have a less critical impact on a user’s

decision to continue using the platform to purchase goods. Pain points have to be rather severe for it to deter consumers from using the site to purchase.

C: "If the website has a very poor layout, it turns you away at the first step. That’s why I like to buy clothes at the physical store, but other than that I will still make a purchase as long as I need it. I feel it is also helped by the refund policy in Taiwan, which makes it easy for me to purchase and if it doesn’t match my expectation then I can return it.”

L: "If I really can’t find something because of the poor search results then I will go elsewhere to find it. Especially in Taiwan it is also very easy to get items offline, unlike US where they have to travel very far to a store.”

Nonetheless, we were able rank the various “Pains” asking our interviewees to estimate the severity of those frustrations that they mentioned. As different users had different frustrations we had aggregated them into a single list based on how agitated the users were regarding their own pain points.

Some of our interviewees had felt that the frustrations were a little annoying but did not have too much difference on whether they would continue to use the stated platform - in this case websites for online shopping. Others felt the annoyances were really hindering a smooth seamless user experience, and was something that should really be improved upon. The more it disrupted their shopping experience, the higher it would be ranked.

Figure 4.3.3 - Ranked Pain Points (WEBSITES)

The first page that users land on when visiting a retail site plays a very important role, as they say first impression counts. Whether a site has come up with a suitable layout design and balances amount of information displayed with the simplicity of the page, this strongly influences the way users react to the site. Thus explaining why an overcrowded landing page becomes the top frustrations for users.

C: "PCHome I don’t like because its really messy and I don’t like the interface.

Momoshop I’ve used, but Taobao is too messy and you need a separate account.”

H: "Most websites have done a good job but for like Yahoo sometimes the various site links are all over the place, and unclear if the offers are for Auctions or Retail etc.”

The other frustrations such as poor display of search results, and the difficulty involved in doing comparisons are somewhat similar with those experienced on a mobile app.

Then at the bottom of the list is the need for users to key in repetitive information every time they are making a purchase.

If we put them side-by-side, we clearly see the list is much longer on the left side of Figure 4.3.4 for mobile. They both have different “Pains” independent of each other, but some occur in varying degrees on both platform types. When using mobile apps, it is almost impossible to do comparisons, in contrast when using websites users can open multiple browser windows to compare items although it is also just an out of the box way to do comparisons. It makes it possible but the difficulty in doing it still makes it a pain point.

Figure 4.3.4 – Comparing Pains (Mobile Apps Vs. Websites)

Still when asked to summarize their overall experience with using current mobile apps or websites, our interviewees felt that it was a generally good experience. There will definitely be many areas that can be improved, one being the general user interface (UI) or user experience (UX) of local apps or websites as highlighted by one of our interviewees.

L: “So far everything is fine, but in general the UI for many Taiwanese sites still fall behind international ones like Amazon - then the overall experience just falls short.”

The pain points mentioned for both platforms are definitely concerns for the online shopping industry here in Taiwan, but more importantly it gives us certain insights as to why websites are still the current choice for a large proportion of local consumers.

4.4 Customer Profile - Finding Customer Gains

The last and final piece of the Customer Profile is the expectations or “Gains” that consumers have when they use online shopping platforms. Some of these may be labeled as required gains where consumers find they are a necessity i.e. ‘Must-have’, whilst others may be expected gains where they would feel more like ‘nice-to-haves’.

Figure 4.4.1 - Third Component of Customer Profile

For this section, we really wanted to find out what were the expectations when shopping online, and how they would benefit from stated features or functions.

Y: “Mmmm, Filters - Price filters or other types of filters. Categories! Items must be well categorized. This will help me to find what I want easily and quickly. Also must be clear in the details of delivery, for example Momoshop will state the expected time you have to wait to receive the item.”

C: “Search must be accurate, recommended items after the search must be related or items that I might be interested to purchase too. Search results must show some basic details so I can decide if I am interested, instead of making me click an item to see even the most basic details. If I don’t have to click into each item to view the basic details, I can already do comparisons while viewing the search results displayed. Filtering or sorting functions are important too.”

Again it was noted that the some interviewees highlighted more points related to the search and comparison phase of the shopping. For them, online shopping is focused on finding items easily, comparing details and prices and at the end finding the most value for money option.

Other comments were more comprehensive of the entire user journey while shopping for an item. From browsing, to search and recommendations, viewing item details, reading up on the item reviews and finally to registering an account, the checkout and payment process.

L: "Make browsing simpler, categorizing must be very accurate & the overall user experience must be comfortable. Reviews & comments must be allowed so I know the quality of the product I’m buying. Registering for the platform must be easy, and paying for items must be quick and simple.”

Even so, one major point was brought up in all our conversations - Trust. With numerous cases of credit card fraud or people stealing information, security and safety becomes a major consideration for online shoppers. Our interviewees had two major

causes of concerns (1) Do you trust the quality of the product and (2) do you trust the security of the payment?

Y: “Trust - sometimes I don’t trust the quality of products on a platform - for instance Taobao, some products are imitations and poor quality.”

C: “Reviews on seller or products and rating systems are important - so that I know who to trust. The product quality must be good.”

H: “Reviews & ratings - very important for trust. Safety for payment.”

Besides the issue of trust, the general consensus garnered from all our interviewees was that they wanted to buy quality products through more accurate search and reviews, be assured of a strong payment security and have an overall easier task navigating while shopping.

Though these functions aren’t revolutionary in today’s digital age, it is reflective of how we are often bombarded by so much information sometimes there is an overload of news, offers and promotions. Consumers that feel there are too many options and there is an information overload would seek solutions that allowed them to filter and sort through the different sources of information easily.

The resulting expectations are mapped along side parts of the user journey where they belong and can be summarized in Figure 4.4.2 below. Here the user journey also represents some of the tasks or “Jobs” consumers were trying to achieve when they choose to do online shopping and we can see how the expectations or “Gains” match up to them.

Figure 4.4.2 – User Journey & Expectations

Each step of the user journey shows some of the expectations that they have, and it helps us to see how users feel about each part of the journey. At the same time, we then put together the list of “Gains” according to the level of priority or ranking that our respondents indicated.

Figure 4.4.3 – Ranked Customer Gains Section

According to the interviewees, the quality of the products available or being assured of trustworthy sellers tops the chart. Nobody wants to be browsing and searching online to

keep running into scams and fake goods. The requests for product review and seller ratings are but tools with which the users are able to discern for themselves if the items they are keen on purchasing are really what they see on photos.

The second ranked item was the security of their personal information or secure transactions. Even though this item was only mentioned by interviewees after they talked about products and browsing, they explained that this was just a really basic requirement that they didn’t think about at the start.

H: “If you can’t trust the site to keep your information safe, why would you even want to shop there? They all need better payment security and protection for consumers against fraud etc. many older folks are being tricked etc.”

Coincidentally the next couple of items ranked highly by our interviewees also corresponded to the first two phases of the user journey – the search and browse, followed by the comparison stage. They expected the search logarithms to return accurate results and recommendations, speeding up the time needed to find items with clever filtering functions, and also the ability to make comparisons easily – perhaps something that no app or site has managed to nail so far, but we will look into this in the following section.

The way products are categorized will also determine how a user has to navigate through the pages, and users hope to benefit with an easier time using the platform. This is followed by the simplicity in the way information is displayed and also the ease at which users can make a purchase.

Some of the “nice-to-haves” include a simple sign up process if needed, as some platforms require you to have an account to use it. Although this is not so much of a hassle these days as many allow 3rd-party integration such as signing up using your Facebook account or your Google account. Our interviewees also mentioned good customer service that is available when you want it, and reward points as possibly some great new benefits online platforms can provide for consumers.

Y: “Customer chat? I think some websites have it and even though I may not use it too often but I think it will be a nice to have when you really need to ask something you don't have to write emails and wait for replies.”

L: “VIP or Birthday Reward Points that could be used across various sites - such a user experience would be cool.”

All in all, we wouldn’t say this list of expectations are too much, customers are really looking for features, functions that would lead to benefits in terms of Usefulness and Ease of Use. Both studies from Childers and O’Cass have touched upon these 2 building blocks to ascertain technology adoption by consumers; here we have just taken a different approach in finding out what are the bits and pieces that matter to consumers.

Having taken you through Customer Jobs, Pain Points as well as Customer Gains, we now can proceed to place all three components of the Customer Profile on the same page. In the figure below is a clearer picture of how it all fits together.

Figure 4.4.4 – Completed Customer Profile for Online Shopping

A consumer’s objectives and expectations are derived from their desire to utilize online shopping to purchase goods, thus we are considering them to be identical for both platforms. However, here we have chosen to present both sets of frustrations - those while using apps and those while carrying out online shopping via websites, so as to make it easier for you to see how the Pain points can be attributed to the platform in question. Here we also note how some Pains occur in both sides but in varying degrees.

In Mobile Apps, users felt they were unable to carry out any comparisons, whilst in Websites they felt it was difficult to do them.

In the next section, we will examine the value that each platform is able to bring to the market and subsequently when matching Value Map to Customer Profile we will also consider each platform independently.

4.5 Approaching The Value Map

We started our study with an understanding that online platforms needed to use a customer-inspired approach to tailor or build their product. The product or service itself is not going to create value for consumers. The solution provided has to match the consumers’ expectations, relieve their pains and satisfy their needs in order to really create value (A. Osterwalder et al., 2014).

The Value Map consists of 3 main components as shown below:

Figure 4.5.1 – Main Components of Value Map

Here we will use two real cases to help us assess how mobile apps and websites are faring in terms of creating value for consumers. Accordingly, the remainder of this chapter will be analyzed based these two cases to come up with a separate Value Map for each of them.

4.6 Selecting Our Cases to Examine

The figure below summarizes some of the retail platforms commonly used by our interviewees. Aside from the obvious big names, other sites commonly mentioned were the Yahoo Auction and Retail sites, as well as marketplace apps Shopee and Carousell.

Figure 4.3.2 – Internet Retail Sites/Apps used by Interviewees

The Taiwan market has plenty of popular retail sites, including local ones such as PCHome, Momoshop and Rakuten (SP Ecommerce, 2015). Market Intelligence &

Consulting Institute (MIC), a Taipei-based global ICT industry research organization, also conducted a survey earlier this year to evaluate consumer-shopping habits.

According to that survey, the three most popular online retailers in Taiwan are Yahoo Taiwan, PCHome and Momoshop (M. Lubin, 2017). PCHome and Momoshop were also the two main sites that our interviewees talked about, indicating these sites did have a higher mindshare or top-of-mind brand recall for Taiwanese online shoppers.

Momoshop is the shopping website of parent company Momo that also operates in TV shopping and Catalogue Shopping. According to publicly available financial statements

total revenue for Momo grew 9.5% in 2016 to NT$280.8 billion, making it still the largest e-commerce company in Taiwan (P. He, 2017). Putting aside revenues from TV and Catalogue shopping, Momoshop posted the highest revenue growth in 2016. Whilst its’ total revenue of NT$205.8 billion fell short of PCHome’s NT$257.4 billion, but it clocked a growth of 20% as compared to PCHome which had a 12.5% growth. Even though Momoshop is smaller in scale it has shown a higher growth rate than PCHome.

Thus for our website case, we will examine the functions and features of Momoshop to fill out our Value Map.

As for the mobile app scene in Taiwan, several retail platforms have developed mobile applications versions of their shop, but when we asked our interviewees they mainly focused on C2C marketplace apps such as Carousell and Shopee.

Both apps were founded in Singapore but have since officially launched apps across South-East Asia and shown incredible growth. Carousell was earlier to the scene here in Taiwan, launching in 2014 with much excitement. Two years after its launch in Taiwan, there are over 10 million product listings put up by its active members, making its Taiwan operations the second largest after Singapore (The China Post, 2016). Shopee on the other hand, has only been in Taiwan since the middle of 2015, but it has aggressively tried to draw the crowds by using a free delivery model. With the free delivery model launched at the end of 2015, gross orders and also users increased tremendously (Lisa, 2016). Their growth hacking strategy had definitely been successful, with app downloads and app store rankings now outpacing Carousell.

However, Shopee has not disclosed details of the free delivery deal that it has struck with convenience stores and logistics services, but the amount of cash drain may be