Directors

’Share Collateralization, Earnings Management

and Firm Performance

董監事股權質押、盈餘管理與公司績效相關性之研究

Lanfeng Kao (高蘭芬) Assistant Professor Department of Finance National University of Kaohsiung

This version: Sept. 2005

Directors’Share Collateralization, Earnings Management

and Firm Performance

Abstract

This study examines the association between director’s share collateralization and

earnings manipulation. The results indicate that directors’share collateralization is

significantly positive with earnings management and the positive association is

stronger when the directors own more shares. Earnings management attributable to

boards’share collateralization causes severe agency problems and hurts firm

performance. I find that earnings management attributable to share collateralization

is negative related with firm performance.

Keyword: Share collateralization, Directors’personalleverage,Board of directors, Earnings management, Abnormal accruals

.

董監事股權質押、盈餘管理與公司績效相關性之研究

中文摘要

本研究探討董監事持股質押是否降低公司盈餘品質,以及與董監事質押有關 的盈餘操縱行為是否傷害公司績效。研究結果顯示,董監事股權質押與公司異常 應計項目存在顯著正向關係,顯示董監事個人的融資行為會影響公司盈餘報導的 品質。此外,董監事質押與異常應計項目間的正向關係會隨著董監事持股的增加 而增強,隱含當董監事與公司存在利益衝突時,董監事持股增加會使董監事質押 所引發的盈餘品質下降的問題更嚴重。實證結果也發現因董監事質押所引發的盈 餘操縱與公司績效存在顯著負相關。 關鍵字:董監事質押、盈餘管理、董事會Directors’Share Collateralization, Earnings Management

and Firm Performance

1. Introduction

The effects of board-of-director characteristics and ownership structure on

financial reporting process have been a popular research topic in corporate

governance (for example, Klein (2002), Fan and Wong (2002), and Peasnell et al.

(2000)). Researchers focus on the monitoring role of board of directors and examine

the effectiveness of the board characteristics (such as board size, independent

directors, and remuneration committees) as internal corporate governance

mechanisms. However, there is a growing literature suggesting that the boards of

directors are ineffective and even address the interest conflicts between board of

directors and outside shareholders. In Asia, most listed companies are controlled by

families or owner groups and the role of board of directors in a family-controlled

business attracts attentions of the SEC and investors. Typically, the controlling

groups have tight control over the listed companies and the majority shareholders

serve as the chief executive officer (CEO) and directors of the companies. Board

members could influence the CEO’s decisions including financial reporting to

maximize the wealth of directors (or controlling families) and expropriate the benefit

of outside minority shareholders when interest conflicts exist between directors (or

families) and outsider shareholders.

Share collateralization of directors which is the focus of this paper, reflects the

financial pressure of directors. Because shares of listed firms are widely accepted by

financial institutions as collaterals and because the voting rights and control rights of

the collateralized shares are still kept by shareholders, many directors facing financial

money. However, directors who pledge their shares as collaterals need to pledge

more shares once the market value of the collateralized shares falls below the required

margin. Due to threat of margin requirement, the collateralizing directors have

incentives to manage reported earnings to avoid the drop of shares prices leading to

the downgrade of the quality of reported earnings. The potential agency conflicts

related to the creditability of accounting reporting between directors and outside

shareholder are worth examining. However, since the share collateralization is

directors’personal financial decisions, most countries (such as USA and Hong Kong)

do not impose any regulation on share collateralization even disclosure requirement.

Lack of the information about the personal leverage of board members, little research

works on this issue. Since Taiwan SEC requires the listed firms to disclose the

directors’share collateralization information, I have an opportunity to study the

agency problems of share collateralization by board members.

Agency problems of share collateralization by directors have been an important

governance issue in Taiwan after the Asian financial crisis in 1997. The main reason

is that the financial distress Taiwanese companies generally experience high

percentage of share collateralization by directors. Not only for distressed companies,

according to statistics from the securities exchange, board of directors in Taiwan

pretty much collateralize their shares for personal funding. Up to November 2000,

the year after the Asian financial crisis in 1997 and Taiwan local financial turmoil in

1998, only 28% (147 firms) of the listed firms did not have shares collateralized by

their boards of directors. There are 312 firms (34% of the listed firms) with a

collateralization ratio (defined as the number of shares collateralized by the board of

directors divided by the total number of shares owned by the board of directors) lower

50%; 103 firms (20%) with collateralization ratio higher than 50%; 21 firms (4%)

with collateralized share ratio higher than 90%; 17 firms (3.24%) with

collateralization share ratio between 80% and 90%; 16 firms (3.05%) with

collateralization ratio between 70% and 80%. Moreover, 40% of the stocks traded in

the over-the-counter market experience share collateralization by their board of

directors.

In this study, I examine the relation between earnings management and share

collateralization by board members and investigate whether the earnings management

attributable to share collateralization hurts firm performance. There are two main

contributions from this study. The first contribution is that this paper extents the

research about the effects of board-of-director characteristics on earnings

management. To date, the literature has focus on identify the association between

characteristics of board of directors and financial report quality. Especially, the link

between the dependence of board and activities related to earnings manipulation

behaviors has been most emphasized (Dechow et al., 1996; Beasley, 1996; Klein,

2002). However, the percentage of listed Asian companies affiliated with business

groups are quite high (Claessens, Fan, and Lang, 2002). It is easy to find that most

of boards of directors of listed firms in Asia are controlled by a family and majority of

board members lack of independence. Chen, Fan and Wong (2004) find that the

governance function of board of directors is weak in China. Thus, it is not

comprehensive to only focus on the governance role of board without considering the

interest conflicts between board of directors and outside shareholders. The second

contribution of this paper is to study the interest conflicts induced by board members.

In this paper, I address that directors’personal leverage conducts could induce the

earnings manipulation and argue that the requirement by SEC to disclosure the

information to investors is necessary.

Share collateralization by board of directors is very popular and is an important

issue of corporate governance in Taiwan. However, previous studies about structure

of board of directors on earnings management or earnings quality generally neglect

the effect of share collateralization on the earnings reporting. This paper tries to

make up the deficiency.

2. The mechanisms of share collateralization

Stock investors in Taiwan can take their shares to the financial institutions as

collateral to raise a debt. Due to the liquidity of the listed stocks, financial

institutions in Taiwan prefer the debt-raisers to use listed shares as collaterals. The

debt raisers who collateralize their shares at the financial institutions still keep the

voting rights and the cash flow rights of the shares unless they default. When

shareholders collateralize their shares at financial institutions, they can borrow up to

60% of the base value of collateralized shares and hold the debt up to one year. The

base value of the collateralized shares is measured based on the preceding closing

price or the average closing price three months prior to the collateralization date

whichever is lower. The stock price fluctuates leading to the appreciation or

depreciation of the collateralized shares. On the one hand, when the market value of

collateralized shares increases, the collateralizing shareholders can continue to hold

the debt. On the other hand, when the market value of the collateralized shares

decreases and falls below the required margin, the financial institutions will ask the

collateralizing shareholders to collateralize more shares. If the debt-raisers cannot

to be closed.

There is no particular regulation on the share collateralization of minority

shareholders. However, Taiwan SEC asks the firms with their directors

collateralizing shares at financial institutions to disclose the details of share

collateralization on the website of Taiwan Stock Exchange everyday. When a firm

with directors’share collateralization would like to issue equity offerings, the details

of share collateralization must be disclosed in the prospectus.

As we mentioned in the introduction, directors’share collateralization is very

popular in Taiwan. What is the purpose of collateralizing shares to raise a debt?

The Commercial Times1 (October 7, 2000) reports that the minority shareholders

collateralize their shares to increase the leverage on their stock investments. The

Commercial Times also indicates that the directors collateralize their shares and use

the fund raised from share collateralization to buy more shares of the firm to gain

control over the firm. For example, a director holds 100 shares of the firm, which is

10% of the ownership of the firm. The director can raise debt through collateralizing

all his shares and buy 60 more shares of the firm from the open market. In this case,

the director’s holding increases from 10% to 16% and he gains more control over the

firm. Anecdote evidence shows that the capital from collateralized shares is hardly

contributed to firms’projects.

3. Related literature

3.1 Board-of-director characteristics, corporate governance and financial reporting quality

The research to date in this area examines the association between the

characteristics of board of directors (such as size and composition of the board,

number of outside independent directors, and remuneration committees) and financial

reporting quality, earnings manipulation and financial statement fraud (McMullen,

1996; Dechow et al., 1996; Beasley, 1996; Carcello and Neal, 2000; Klein, 2002;

Anderson et al., 2004). Generally speaking, these studies suggest that independence

of board or auditing committee has linkage with the activities associated with earnings

manipulation behaviors. For example, Beasley (1996) and Dechow et al. (1996) fine

that the proportion of independent directors on the board (used to proxy for board

independence) is inversely related to likelihood of financial statement fraud. Klein

(2002) also finds a negative association between the abnormal accruals and board

independence.

Since the basic design of corporate governance is that the shareholders elect the

board of directors and then board of directors selects the management, researchers

focus on the monitoring role of board of directors and examine the effectiveness of

the board membership and characteristics as internal corporate governance

mechanisms. However, for family-controlled businesses, board of directors is

controlled by families or owner groups and is inefficient on behalf of shareholders in

monitoring management which is common dominated by controlling family. Even

for a non family-controlled firm, it is not unusual that board itself is the source of

conflicts of interest. In common practice, many firms establish conflicts of interest

policy to prevent a board member develops an actual or potential or conflict of

interest with the company (for example, FedEX, Micorn).

Previous studies find that the deviation of ownership (cash flow right) and

control right of controlling shareholders (or directors) in Asia produces agency

quality of reported earnings (Fan and Wong, 2002). Fan and Wong (2002) find that

the increase of control right and deviation between control and cash flow rights make

the agency conflicts more severe and the purpose of providing accounting information

by management is not to reflect the firm’s true transaction. For self-interest,

controlling shareholders tend to manipulate earnings to cover the effect of

expropriation of wealth on earnings, or to report earnings in total instead of details.

Those behaviors hurt the creditability of accounting information. If investors do not

trust the accounting reporting, the relation between earnings information and stock

return will decrease. Share collateralization is quite popular for public firms in

Taiwan. Related research in accounting discipline finds that the share

collateralization decreases the informativeness of accounting earnings (Kao and

Chiou, 2002). Kao and Chiou (2002) find that the higher the extent of share

collateralization by directors, the lower the relation between corporate earnings

information and stock returns. They conjecture that due to worries of providing

more shares for margin requirements, managements who collateralize their shares

have stronger incentives to manage earnings to avoid the drop of share prices. The

strong incentive of earnings management makes reported earnings less creditable and

therefore decreases the relation between reported earnings and stock return.

However, Kao and Chiou (2002) do not test whether the management does manage

earnings. This study will try to make clear the relation between share

collateralization and earnings management. Once the relationship is valid, the

arguments by Kao and Chiou (2002) can be more powerful.

3.2 Share collateralization by board of directors and firm performance

research ever examines the agency problem of share collateralization by board of

directors and the relationship between share collateralization and firm performance.

The listed firms in Taiwan are required to disclosure periodically the information of

share collateralization by the board members, manager and major shareholders. This

disclosure requirement provides data for researcher to study the effect of the directors’

personal loan on firm performance. To date, research on collateralized shares

generally focuses on the relationship between financial distress and collateralized

shares or focuses on the relationship between firm performance and collateralized

shares during the period of Asia financial crisis. Previous studies do not reach

consistent conclusion about the relation between performance and collateralized

shares. Chiou et al. (2002) point out that collateralized shares of board of directors

raise the possibility of being in distress. Chen and Hu (2003) show firms with a

higher shareholders’personal leverage will have a higher risk and worse performance

in the future. Kao et al. (2004) indicate that there is an inverse relationship between

collateralized shares and firm performance and that the inverse relationship exists

only for group-controlled firms. Kao et al. (2004) also provide evidence that

monitoring mechanisms by institutional investors, creditors and dividend policy can

effectively reduce the agency problem of shares used as collateral and thus can

improve firm performance.

4. Empirical design

4.1 Hypotheses development(1). Share collateralization and earnings management

The effects of board-of-director characteristics (such as size, composition and

manipulation and financial statement fraud have been a topic of corporate governance

in accounting research (McMullen, 1996; Dechow et al., 1996; Beasley, 1996;

Carcello and Neal, 2000; Klein, 2002; Anderson et al., 2004). To date, researcher

mainly focuses on the overseeing functions of board of directors. For example,

Beasley (1996) and Dechow et al. (1996) find that board independence is inversely

related to likelihood of financial statement fraud. And, a negative association

between the abnormal accruals and board independence are documented by Klein

(2002). However, board of directors in Asia is often controlled by families or owner

groups and it is inefficient on behalf of outside minority shareholders in monitoring

management and controlling shareholders. Previous studies find that the deviation

of ownership and control right of controlling families (or directors) in Asia produces

agency problem and decreases firm value (Claessens et al., 2000) and therefore hurts

the quality of reported earnings (Fan and Wong, 2002).

This paper examines whether the directors’personal leverage has negative

impact on quality of financial reporting process and eventually hurts firm

performance. A director is not prohibited to pledge his shares for a personal loan.

Share collateralization is personal financial decision of board members and should not

be related to firm activities under the assumption of separation between ownership

and management. However, Claessen et al. (1999) point out that, except in Japan,

most of listed firms in East Asia are affiliated with business groups or families. For

example, 65.6% of listed Taiwanese firms in 1996 are family-controlled. Yen and

Lee (2001) also find that the 76% of listed firms in Taiwan are family-controlled and

66.45% of board of directors is controlled completely by families. For a

family-controlled or group-controlled firm, majority of board members are related to

opportunity of participating in management activities (including earnings reporting

process) makes the director’s personal loan linked to firm operations.

Due to the liquidity of the listed stocks, financial institutions in Taiwan prefer

the debt-raisers to use listed shares as collaterals. The directors usually also prefer to

collateralize their shares at the financial institutions because the collateralizing

shareholders still keep the voting rights and the cash flow rights of the shares unless

they default. Therefore, the change of share collateralization level can reflects the

personal financial pressure of an individual director. Due to worries of providing

more shares for margin requirements, managements who collateralize their shares

have stronger incentives to manage earnings to avoid the drop of share prices. Kao

and Chiou (2002) show that share collateralization of board members decreases the

informativeness of accounting earnings, measured by the earnings-return relation.

The findings provide evidence of the possible earnings manipulation and decrease of

earnings quality attributable to share collateralization of board members. Based on

the reasoning, I propose the following hypothesis:

Hypothesis 1: The more shares collateralized by board of directors, the higher the extent of earnings management.

The function of the board of directors is to monitor the managers and to

maximize shareholder value. However, directors should have proper incentives for

performing their job well. One incentive comes from having directors own shares of

the company they oversee. Since directors who own shares of the firm will benefit

directly from the increase in values, they are willing to monitor manager and make

sure managers maximize share value. Thus, in theory, the governance function of

directors improves as directors’ownership increases. Nevertheless, once there exist conflicts of interest between directors and firms, directors who own more ownership

are more influential over firms to benefit their own. For directors who have

incentives to influence management to exercise extra earnings manipulation, the more

ownership could help them to achieve their purposes. Based the above argument, the

hypothesis 2 is proposed.

Hypothesis 2: The positive association between earnings management and pledged shares by board members is stronger when board members own more shares.

(2).The effect of earnings management attributable to share collateralization on Firm

performance

Shares collateralization by boards of directors or other large shareholders is

considered as personal conducts and is not prohibited. In theory, it should be

irrelevant to the operations of the firm under the separation of ownership and

management. However, the separation of ownership and management does not fit

firms in Taiwan leading to a connection between personal share collateralization of

board members and firm performance.

To date, research on collateralized shares supports that share collateralization by

board members is related to financial distress and future worse performance (Chiou et

al, 2002; Chen and Hu, 2003; Kao et al., 2004 ). The possibility of being in distress

increases with the level of share collateralization of board of directors (Chiou et al.,

2002). Researchers also find that firms with higher shareholders’personal leverage

tent to have higher risk (Chen and Hu, 2003) and worse future performance (Chen and

Hu, 2003; Kao et al., 2004). Kao et al. (2004) indicate that there is an inverse

relationship between collateralized shares and next period firm performance for

family-controlled firms. In addition, they show that outside governance mechanisms

improve firm performance. Due to worries of the agency conflicts induced by the

directors’personal leverage, Taiwan’s SEC requires the listed firms to disclose the

information of share collateralization by the board members, manager and large

shareholders and remind the investors to notice this disclosure before making

investment.

In this paper, in addition to reexamining the association between firm performance

and share collateralization, I emphasize on opportunistic earnings manipulation of

management induced by share collateralization of directors (proposed by hypothesis 1)

and study whether earnings management attributable to share collateralization by

directors hurts firm performance. Therefore, I propose the following hypothesis.

Hypothesis 3: There exists a negative association between earnings management attributable to directors’share collateralization and firm performance.

4.2 Empirical methodology

(1). Earnings management and the characteristics of board

To examine the association between earnings management and the characteristics

of board, I employ the following regression.

dummies year IND BM LEV SIZE T OWN T OWN PLEDGE PLEDGE EM ) ( * ) ( * ) ( * ) ( * ) _ ( * ) _ * ( * ) ( * 7 6 5 4 3 2 1 0 (1) where,

EM = the measurement of earnings management measured by absolute value of

abnormal accruals. Abnormal accruals are accruals that can be manipulated and

is typically used as the measure of earnings management. This paper applies

absolute values of abnormal accruals as a measure of earnings management.

Accruals are the difference between net income and cash flow from operations.

Accruals consist of discretionary and non-discretionary accruals. I use a

modified Jones (1991) model to estimate expected or nondiscretionary accruals

for each two-digit industry code for each year from 1997-2004. Abnormal or

discretionary accruals are measured by subtracting normal accruals from total

accruals.

PLEDGE = PLED, PLED_T or DIFPLED_T. These three variables measure the

extent of shares of common stock that is held by board members and used as

collateral to financial institutions to borrow money. PLED= share

collateralization ratio of board members which is defined as total shares owned

by board members divided by the total shares outstanding.

PLED_T=ln(PLED+0.5/N), the logarithm transformation of PLED (share

collateralization ratio by board members) which is practically from 0% to 100%

and is highly skewed to the right. Here, 0.5/N is added to accommodate the

cases where PLED is zero. DIFPLED_T=ln(1+DIFPLED), the logarithm

transformation of DIFPLED which is the difference of share collateralization

ratio of board members between a year and its preceding year with range from

-100% to 100% . One is added to DIFPLED to accommodate the case where

DIFPLED is equal to -100% (Cox, 1970).

OWN_T=ln(OWNERSHIP), the logarithm transformation of OWNERSHIP, where OWNERSHIP, is ownership of board members defined as the total shares held

by the board members divided by the total shares outstanding.

SIZE= logarithm of sales. LEV= debt-to-asset ratio.

equity.

IND= industry dummy. The value is 1 for electronic firms; 0 otherwise.

Following Klein (2002), this paper includes 2 control variables: financial

leverage (debt-to-asset ratio) and political costs (measured by logarithm of the sales).

In addition, Loebbecke et al. (1989) argue that financial statement fraud is related

with rapid company growth. If a company has been experiencing rapid growth,

management may have motivation to misstate the financial statements during a

downturn to give the appearance of stable growth. Book-to-market value (BM) is

used here to control for the effect of growth on possible accounting manipulation. In

addition, one industry dummy and seven yearly dummies are also employed to

account for the unobserved variation.

Hypothesis 1 examines the association between earnings management and

pledged shares by board members. If hypothesis 1 is valid, then the regression

coefficients ( in equation (1)) of three share collateralization measures should be1

significantly positive implying that share collateralization increases the willingness of

board member to influence the accounting reporting. Hypothesis 2 tests whether the

positive association between earnings management and pledged shares proposed in

hypothesis 1 is more severe for firm with high percentage of share holding by board

members than in firm with lower percentage. While regression coefficient in1 equation (1) represents the impact of collateralized shares on earnings management,

the magnitude of 1 2(OWN_T) in the equation measures the impact of collateralized shares on earnings management conditional on different levels of board

ownership. When hypothesis 2 is supported, results should indicate positive,

statistically significant estimates s on the interaction terms PLER*OWN_T,2

collateralized shares on earnings management varies directly with the holdings of

board members and board members with higher ownership have higher incentive to

engage in accounting manipulation due to share collateralization.

(2). Firm performance and earnings management attributable to share collateralization

Hypothesis 3 tests whether the earnings management attributable to share

collateralization hurts the firm performance. The following empirical model is

employed to test the hypothesis:

es year dummi IND LEV PERF LAG SIZE PERF STD edicted_EM PERF ) ( * ) ( * ) _ ( * ) ( * ) _ ( * ) Pr ( * 6 5 4 3 2 1 0 (2) where,

PERF=CFO, ROA, ROE or ROE1. These four variables are used to proxy for firm

performance. CFO=cash flow from operations deflated by lagged total assets.

ROA= return on assets. ROE= return on common equity. ROE1= income

before extraordinary items scaled by lagged common equity.

Predcited_EM = predicted component of abnormal accruals that is related to share

collateralization by board members.

) _ * ( * ˆ ) ( * ˆ _

Predicted EM 1 PLEDGE 2 PLEDGE OWN T , where ˆ1 and 2

ˆ

s are the estimates of equation (1) and the variable PLEDGE is either

PLED_T or DIFPLED_T depending on level or change of share collateralization

ratio are used.

STD_PERF = standard deviation of CFO, ROA, ROE or ROE1 over the sample

period.

SIZE = logarithm of sales.

LEV = debt-to-asset ratio.

IND = industry dummy. The value is 1 for electronic firms; 0 otherwise.

I use accounting profit ratios (cash flow from operations deflated by lag total

assets, return on assets, return on equity and income before extraordinary items scaled

by lagged common equity) to measure firm performance. The accounting profit ratio

is an estimate of what management has accomplished and is not affected by investor

psychology (Demsetz and Villalonga, 2000). Predcited_EM is the predicted

component of abnormal accruals that is related to share collateralization by board

members, including the predicted component of earnings management induced by

share collateralization ratio itself and predicted component induced by the effect of

ownership of directors on association between earnings management and share

collateralization ratio. The sign of coefficient is expected to be negative,1 implying that these earnings manipulation due to share collateralization reduces the

firm performance.

Follow Core et al. (1999), variables STD_PERF and SIZE are included in the

regression equations to control for the possible effects of risk and size on accounting

performance, respectively. Variable IND is included in Equations (2) to control for

the relatively high performance of electronic industry in Taiwan stock market. Prior

period performance and yearly dummies are also employed to account for the

unobserved variation.

5. Empirical Results

5.1 Sample

This paper examines the relationship between earnings management and share

attributable to share collateralization hurts firm performance. Our sample consists of

listed firms in Taiwan, and the data on collateralized shares held by boards of

directors and financial data are from the TEJ database. Since TEJ began to report the

proportion of collateralized shares owned by stockholders in 1996 and the differences

of the proportion of collateralized shares are measured, our sample period covers a

8-year period from 1997-2004. I delete firm-year observations with (1) missing

beginning-of-year total assets or insufficient data to calculate accruals; (2) fewer than

six observations in any industry-and-year combination; (3) operating cash flows,

earnings before extraordinary items, discretionary accruals, or nondiscretionary

accruals more than three standard deviations away from their respective means. In

addition, firms in the banking industry are also excluded because the nature of their

financial reports is different from those of firms in other industries. Based on the

above criteria, the total number of observations is 5433.

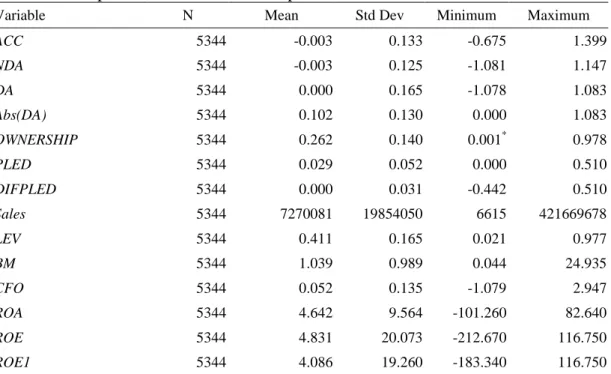

Table 1 shows the descriptive statistics for the sample firms. The average total

accruals (deflated by lagged total asset) are less than zero (-0.3%) and meet the

expectation. Because of the depreciation, on average the reported net income is

expected to be less than cash flows from operation. Accruals are decomposed into

the nondiscretionary (expected) and discretionary (abnormal) parts based on the

modified Jones (1991) model. The average nondiscretionary accruals (NDA) are

-0.3% with standard deviation of 12.5%. The average abnormal accruals (DA) are

0.0% and thus no evidence of systematic upward or downward earnings management

is detected. The absolute values of abnormal accruals (Abs(DA)) are employed to

measure the extent of earnings management. Table 1 report that the average extent

of earnings management is 10.2% of the total assets. The maximum value of

26.2%, with the minimum of 0.13% and the maximum of 97.8%. On average, the

level of share collateralization ratio (PLED) and the change of share collateralization

ratio (DIFPLED) are 2.9% and 0.0%, respectively. The highest pledge ratio in the

sample is 51%. The standard deviations of PLED and DIFPLED are 5.2% and 3.1%,

respectively. The mean and standard deviation of sales of sample firms are 7.27

billions and 19.85 billions. The mean and standard deviation of leverage (LEV) are

41.1% and 16.5%. On average, the book-to-market ratio (BM) is 1.039. Cash

flows form operations deflated by lagged assets (CFO), Returns on total asset (ROA),

return on equity (ROE) and ratio of income before extraordinary items to equity

(ROE1) are measures of firm performance. The means of CFO, ROA, ROE and

ROE1 are 5.2%, 4.642%, 4.831% and 4.086%, respectively.

[Table 1 about here]

5.2 Cross-sectional analyses

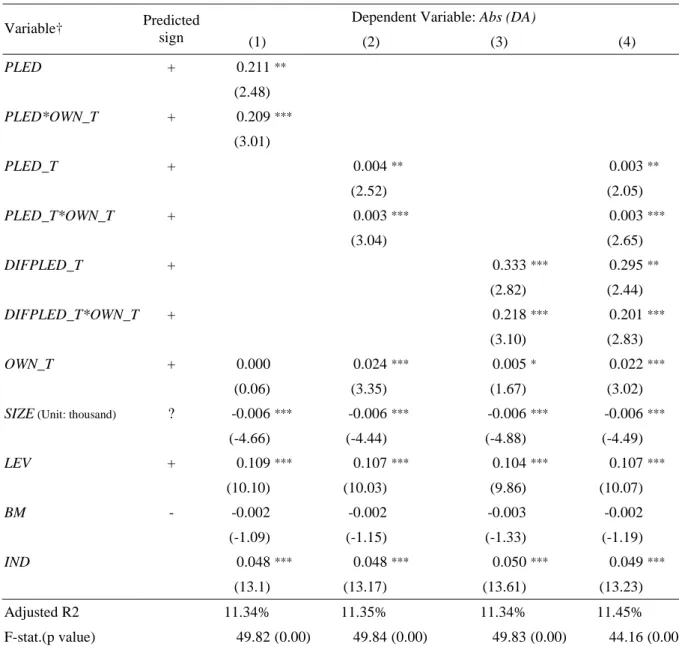

Table 2 reports the OLS regression estimates of 3 alternative measures of share

collateralization ratio (level of share collateralization ratio PLED, logarithm

transformation of share collateralization ratio PLED_T and logarithm transformation

of change of share collateralization ratio DIFPLED_T) on absolute values of

discretionary accruals for equation (1). Columns (1), (2) and (3) of table 2 shows

that 3 alternative measures of share collateralization ratio are significantly positively

related to accounting discretions. The coefficients on Table 2 for PLED, PLED_T

and DIFPLED_T are 0.211, 0.004 and 0.333 with t-values are 2.48, 2.52, and 2.82,

respectively. The results support the argument that share collateralization increases

the motivation of board member to influence the reported earnings (hypothesis 1).

In column 4, PLED_T and DIFPLED_T are included and the results show that both

measures of earnings manipulation (coefficients for PLED_T and DIFPLED_T are

0.003 and 0.295, and t-values are 2.05 and 2.44, respectively).

While regression coefficient in equation (1) is used to examine the impact of1 collateralized shares on earnings management, the magnitude of 1 2(OWN_T) in equation (1) measures the impact of collateralized shares on earnings management

conditional on different levels of board ownership. The sign of coefficient is2 expected to positive implying that the increase of ownership of directors makes the

positive association between earnings manipulation and share collateralization more

severe. Table 2 shows the coefficients for the interaction terms PLED*OWN_T (in

column #1), PLED_T*OWN_T (in column #2), and DIFPLED_T*OWN_T (in column

#3) are 0.209, 0.003, and 0.218, respectively (t-values are 3.01, 3.04, and 3.10,

respectively). Those coefficients are all significantly positive which is consistent

with the argument that more ownership held by board member can increase the board

members’ability to manipulate the earnings, and thus exaggerate the impact of share

collateralization on earnings manipulation. Results of Table 2 support the

hypotheses 2.

[Table 2 about here]

The association between the firm’s performance and the extent of accounting

discretion attributable to share collateralization by board member is examined using a

cross-sectional multiple regression (equation (2)). The regression equation includes

one of the four measures of firm’s performance (cash flows from operations deflated

by lagged total assets, return on assets, return on equity, and income before

extraordinary items deflated by total equity) as a dependent variable and includes two

predicted measures of discretionary accruals (PredictedEM1 and PredictedEM2)

management attributable to share collateralization. PredictedEM1 is the predicted

value of accounting discretion due to the level of share collateralization by board

member impact of conditional on different levels of board ownership, while

PredictedEM2 is the predicted value of accounting discretion due to the change of

share collateralization ratio conditional on different levels of board ownership. The

regression model also includes standard deviation of firm performance, logarithm of

sales, and debt-to-asset ratio as control variables to control for the possible effects of

firm risk, size and leverage on performance. In addition, lagged values of firm’s

performance, one industry dummy, and seven year dummy variable are contained in

the regression to control for the unobserved variation.

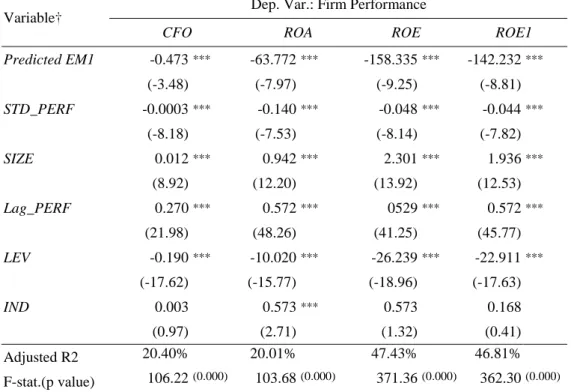

The regression result of performance on earnings management due to share

collateralization and other control variables are presented in Table 3. The results in

panel A show that the predicted component of accounting discretion due to level of

share collateralization (PredictedEM1) is significantly negatively correlated with four

measures of accounting performance (significant at 1% level), implying the earnings

manipulation due to higher level of share collateralization indeed hurts the

performance. The effect of change of share collateralization on firm performance

has similar results to the effect of level. Panel B shows that the predicted component

of accounting discretion due to change of share collateralization (PredictedEM2) is

significantly negatively correlated with ROE and ROE1 (t-values are -2.83 and -2.27,

respectively), while the effects of PredictedEM2 on CFO and ROA are not supported

(t-values are 1.55 and -1.01, respectively). The results indicate that the earnings

manipulation due to increase of share collateralization ratio has negative impact on

firm performance. Table 3 implies that agency problems associated with the

As to other control variables, the effect of standard deviation of each accounting

performance (STD_PERF) and the effect of leverage (LEV) on all measures of firm

performance are significantly negative, indicating that high risk and leverage firms

have worse performance during the sample period. Size and prior period

performance (Lag_PERF) have significantly positive impact on firm performance.

[Table 3 about here]

6. Conclusion

The paper finds that the personal financial loan of board members using firm

shares as collateral to borrow money from banks increases the managers’motivation

to manage earnings. Moreover, the influence of collateralized shares on earnings

management increases directly with the ownership of board members, implying that

board members with more ownership have higher ability to influence the accounting

manipulation due to share collateralization. The paper also finds that the predicted

component of earnings management arising from personal financing behavior of

board members has a statistically significant negative relation with firm operating

performance. Overall, the results indicate that share collateralization by board

members could induce the agency problems. The share collateralization by board

member increases the motivation of management to manipulate earnings

opportunistically and the management opportunism finally hurts the firm

Reference

Anderson R., S. Mansi, and D. Reeb, 2004. Board characteristics, accounting report integrity, and the cost of debt. Journal of Accounting and Economics 37, 315-342.

Bartov, E., F. Gul and J. Tsui, 2000. Discretionary-accruals models and audit qualifications. Journal of Accounting and Economics 30, 421-452.

Beasley, M.S., 1996. An empirical analysis of the relation between the board of director composition and financial statement fraud. The Accounting Review 71, 443-465.

Carcello, J. and T. Neal, 2000. Audit committee composition and auditor reporting. Accounting Review 75, 453-467.

Chen, D. H., Joseph Fan, and T. J. Wong, 2002. Do politicians jeopardize

professionalism? Decentralization and the structure of Chinese corporate board. Working paper, School of Business and Management, Hong Kong University of Science and Technology Clear Water Bay, Hong Kong.

Chen, Y. and S.Y. Hu, 2003. The controlling shareholders’personal leverage and firm performance. Working paper, National Taiwan University, Taiwan.

Chiou, Jeng-Ren, Ta-Chung Hsiung, and Lanfeng Kao, 2002. A study of the relationship between financial distress and collateralized shares. Taiwan Accounting Review 3(1): 79-111.

Claessens, S., S. Djankov and L. Lang, 1999. Expropriation of minority shareholders in East Asia. Working paper, World Bank, Washington, DC.

Claessens, S., S. Djankov and L. Lang, 2000. The separation of ownership and control in East Asia corporations. Journal of Financial Economics 58: 81-112.

Claessens, S., S. Djankov, J. Fan and L. Lang, 2002. Disentangling the incentive and entrenchment effects of large shareholders. Journal of Finance 57(6), 2741-2771.

Core, J., R. Holthausen and D. Larcker. 1999. Corporate governance, chief executive officer compensation, and firm performance. Journal of Financial Economics 51: 371-406.

Cox, D.R., 1970. The Analysis of Binomial Data, Methuen & Co., London.

Dechow, P., R. Sloan and A. Sweeney, 1996. Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research 13, 1-36.

Demsetz, H. and B. Villalonga, 2000. Ownership structure and corporate performance. working paper, University of California, Los Angeles.

Fan, J. and T.J. Wong., 2002. Corporate ownership structure and informativeness of Accounting Earnings in East Asia. Journal of Accounting and Economics 33, 401-425.

Jones, J., 1991. Earnings management during import relief investigations. Journal of Accounting Research 29, 193-228.

Kao Lanfeng and J. R. Chiou, 2002. The effect of collateralized shares on informativeness of accounting earnings. NTU Management Review 13(1), 1-36. (in Chinese)

Kao Lanfeng, J. R. Chiou and Anlin Chen, 2004. The agency problems, firm performance and monitoring mechanisms: The evidence from collateralized shares in Taiwan. Corporate Governance: An International Review 12(3),

389-402

Klein, A., 2002. Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics 33: 375-400.

Loebbecke, J., Martha M. and John J. Willingham, 1989. Auditors' experience with material irregularities: Frequency, nature, and detectability. Auditing: A Journal of Practice and Theory 9 (1), 1-28.

McMullen, D. A., 1996. Audit committee performance: An investigation of the consequences associated with audit committees. Auditing: A Journal of Practice and Theory (Fall), 1-28.

Peasnell, K., P. Pope, and S. Young, 2000. Board monitoring and earnings management: Do outside directors influence abnormal accruals? Working paper, Lancaster University.

Warfield, T.D., Wild, J.J., Wild, K.L., 1995. Managerial ownership, accounting choices, and informativeness of earnings. Journal of Accounting and Economics 20(1), 61-91.

Yeh, Y. H. and T. S. Lee, Corporate governance and performance: The case of Taiwan, The Seventh Asia Pacific Finance Association Annual Conference, Shanghai, 2001.

Table 1 Descriptive Statistics for the sample firms, 1997-2004

Variable N Mean Std Dev Minimum Maximum

ACC 5344 -0.003 0.133 -0.675 1.399 NDA 5344 -0.003 0.125 -1.081 1.147 DA 5344 0.000 0.165 -1.078 1.083 Abs(DA) 5344 0.102 0.130 0.000 1.083 OWNERSHIP 5344 0.262 0.140 0.001* 0.978 PLED 5344 0.029 0.052 0.000 0.510 DIFPLED 5344 0.000 0.031 -0.442 0.510 Sales 5344 7270081 19854050 6615 421669678 LEV 5344 0.411 0.165 0.021 0.977 BM 5344 1.039 0.989 0.044 24.935 CFO 5344 0.052 0.135 -1.079 2.947 ROA 5344 4.642 9.564 -101.260 82.640 ROE 5344 4.831 20.073 -212.670 116.750 ROE1 5344 4.086 19.260 -183.340 116.750

Sample description and variable definition:

The sample contains 5344 firm-year observations over 1997-2004.

* Ownership of directors of KPT INDUSTRIES LTD. (凱聚, Code1805) from May, 2002 to December, 2004 is only 0.13%.

ACC is total accruals which are the difference between net income before extraordinary items and cash flows from operations, deflated by lagged total assets.

NDA is nondiscretionary accruals that are estimated for each firm-year as the expected value of accruals based on the cross-sectional modified Jones (1991) model.

DA is abnormal accruals that are the difference between total accruals and estimated expected accruals using the cross-sectional modified Jones (1991) model.

Abs(DA) is the absolute values of discretionary accruals.

OWNERSHIP is ownership of directors which is measured as the total shares held by the board members divided by the total shares outstanding.

PLED is share collateralization ratio of directors which is defined as the total shares owned by board members and pledged to financial institutions as collaterals divided by the total shares outstanding.

DIFPLED is the difference of share collateralization ratio of board members between a year and its preceding year.

SALES is the sales of the firm. LEV is debt deflated by total asset.

BM is the book value of total common equity divided by the market value of common equity. CFO is cash flow from operations deflated by lagged total assets.

ROA is return on total assets. ROE is return on common equity.

Table 2 Multivariate models of absolute values of abnormal accruals on three measures of pledged share ratio

Dependent Variable: Abs (DA) Variable† Predicted sign (1) (2) (3) (4) PLED + 0.211** (2.48) PLED*OWN_T + 0.209*** (3.01) PLED_T + 0.004** 0.003** (2.52) (2.05) PLED_T*OWN_T + 0.003*** 0.003*** (3.04) (2.65) DIFPLED_T + 0.333*** 0.295** (2.82) (2.44) DIFPLED_T*OWN_T + 0.218*** 0.201*** (3.10) (2.83) OWN_T + 0.000 0.024*** 0.005* 0.022*** (0.06) (3.35) (1.67) (3.02)

SIZE(Unit: thousand) ? -0.006*** -0.006*** -0.006*** -0.006***

(-4.66) (-4.44) (-4.88) (-4.49) LEV + 0.109*** 0.107*** 0.104*** 0.107*** (10.10) (10.03) (9.86) (10.07) BM - -0.002 -0.002 -0.003 -0.002 (-1.09) (-1.15) (-1.33) (-1.19) IND 0.048*** 0.048*** 0.050*** 0.049*** (13.1) (13.17) (13.61) (13.23) Adjusted R2 11.34% 11.35% 11.34% 11.45% F-stat.(p value) 49.82 (0.00) 49.84 (0.00) 49.83 (0.00) 44.16 (0.00)

Sample is for 5344 Taiwan firm-years observations from 1997 to 2004.

*/**/*** represents statistical significance at the 10%, 5% and 1% levels, respectively. Sample description and variable definition:

Abs(DA) is the absolute values of discretionary accruals.

PLED is share collateralization ratio of directors which is defined as the total shares owned by board members and pledged to financial institutions as collaterals divided by the total shares outstanding.

PLED_T is defined as Ln(PLER+0.5/N), the logarithm transformation of PLED (share collateralization ratio by board members) which takes values from 0 to 1 and is highly skewed to the right. Here, 0.5/N is added to accommodate the cases where PLED is zero.

DIFPLED_T is defined as Ln(1+DIFPLED), the logarithm transformation of DIFPLED which is the difference of share collateralization ratio of board members between a year and its preceding year and takes value from -1 to 1 . One is added to DIFPLED to accommodate the case where DIFPLED is equal to -1.

OWN_T is defined as Ln(OWNERSHIP), the logarithm transformation of OWNERSHIP, where OWNERSHIP is ownership of directors which is measured as the total shares held by the board members divided by the total shares outstanding.

Size is the logarithm of sales. LEV is debt deflated by total asset.

BM is the book value of total common equity divided by the market value of common equity. IND = industry dummy. The value is 1 for electronic firms; 0 otherwise.

Table 3 Firm performance on predicted earnings management due to share collateralization

Panel A: Multivariate models of firm performance on predicted earnings management due to level of share collateralization ratio (Predicted EM1)

Dep. Var.: Firm Performance Variable†

CFO ROA ROE ROE1 Predicted EM1 -0.473*** -63.772*** -158.335*** -142.232*** (-3.48) (-7.97) (-9.25) (-8.81) STD_PERF -0.0003*** -0.140*** -0.048*** -0.044*** (-8.18) (-7.53) (-8.14) (-7.82) SIZE 0.012*** 0.942*** 2.301*** 1.936*** (8.92) (12.20) (13.92) (12.53) Lag_PERF 0.270*** 0.572*** 0529*** 0.572*** (21.98) (48.26) (41.25) (45.77) LEV -0.190*** -10.020*** -26.239*** -22.911*** (-17.62) (-15.77) (-18.96) (-17.63) IND 0.003 0.573*** 0.573 0.168 (0.97) (2.71) (1.32) (0.41) Adjusted R2 20.40% 20.01% 47.43% 46.81% F-stat.(p value) 106.22(0.000) 103.68(0.000) 371.36(0.000) 362.30(0.000) Panel B: Multivariate models of firm performance on predicted earnings management due to change of share collateralization ratio (Predicted EM2)

Dep. Var.: Firm Performance Variable

CFO ROA ROE ROE1

Predicted EM2 0.493 -18.528 -111.854*** -84.157** (1.55) (-1.01) (-2.83) (-2.27) STD_PERF -0.0003*** -0.155*** -0.048*** -0.044*** (-8.13) (-8.37) (-8.12) (-7.76) SIZE 0.0102*** 0.880*** 2.172*** 1.818*** (7.65) (11.38) (13.10) (11.73) Lag_PERF) 0.272*** 0.589*** 0551*** 0.595*** (22.13) (50.31) (43.49) (48.31) LEV -0.189*** -9.910*** -26.011*** -22.641*** (-17.50) (-15.51) (-18.66) (-17.31) IND 0.006 0.628*** 0.559 0.144 (1.62) (2.95) (1.28) (0.35) Adjusted R2 44.92% 44.12% 47.16% 46.44% F-stat.(p value) 335.80(0.000) 325.12(0.000) 367.35(0.000) 356.92(0.000)

Sample is for 5344 Taiwan firm-years observations from 1997 to 2004.

**/**/*** represents statistical significance at the 10%, 5% and 1% levels, respectively.

PredictedEM1 is the predicted value of accounting discretion due to the level of share collateralization by board member impact of conditional on different levels of board ownership. PredictedEM2 is the predicted value of accounting discretion due to the change of share collateralization ratio conditional on different levels of board ownership. STD_PERF is the standard deviations of CFO, ROA, ROE or ROE1 over the sample period. LAG_PERF is firm performance of the prior year. The definitions of the remaining variables please refer to note of Table 1.