台灣企業建立 ISO14001 環境管理系統之決定要素

與財務績效

Firms Decisions to Certify ISO14001 EMS and their Financial Performance – An Empirical Study of Taiwan

研 究 生:劉子衙 Student:Tzu-Yar Liu 指導教授:朱博湧 Advisor:Po-Young Chu 國 立 交 通 大 學 管理科學系 博 士 論 文 A Dissertation

Submitted to Department of Management Science College of Management

National Chiao Tung University in Partial Fulfillment of the Requirements

for the Degree of Doctor of Philosophy

in Management

July, 2007

Hsin-Chu, Taiwan, Republic of China 中 華 民 國 九 十 六 年 七 月

台灣企業建立 ISO14001 環境管理系統之決定要素與

財務績效

研究生:劉子衙 指導教授:朱博湧 國立交通大學管理科學系博士班摘

要

從國際標準組織(ISO)訂頒 ISO14001 環境管理系統標準以來,全世界的許多公司紛 紛建立ISO14001 環境管理系統。截至 2005 年 4 月份為止,全球已有 88,800 家不同類 型和規模的組織通過 ISO14001 驗證。雖然已有許多實證研究檢視在先進國家推行自願 性環境管理計畫之決定要素,但是在台灣推行這些自願性計畫的動機卻很少被提及。本 研究目的在分析引導台灣上市上櫃公司建立 ISO14001 環境管理系統並尋求驗證之驅動 要素。利用1996-2004 年期間,332 家取得 ISO14001 驗證和 650 家未獲得驗證的公司之 長期追蹤調查資料為樣本,迴歸結果證明公司的外銷比率、公司規模、研發強度及科學 園區廠商等四要素會影響公司採行 ISO14001 驗證之決策。整體而言,迴歸結果顯示, 為了降低公害並改善環境品質,政府雖可透過政策性的工具,如提供補貼增加企業驗證 的誘因;或是政府長期累積對環境保護的承諾,增加公司違反環境法規的潛在成本來鼓 勵廠商推動ISO14001 環境管理系統,但政策性工具對廠商是否通過 ISO14001 驗證並無 強烈證據支持。同時,隨著全球化趨勢及相關綠色環保規範之要求,外銷導向型的台灣 企業不斷面臨來自利害相關團體之持續壓力,比如說來自跨國企業公司所加諸的綠色供 應鏈壓力,導致其較內需型產業更可能採行 ISO14001 標準,故企業為了企業形象及潛 在市場,往往也會透過取得環保驗證,自發地降低整個生產過程中對環境的潛在破壞。 整體而言,從實證結果顯示之主要管理意涵為:外銷導向的台灣企業由於承受來自全球 綠色供應鏈(greening supply chain)之壓力,急於把 ISO14001 標準視為一可接受的合法性 工具(legitimacy tool),因為它可用來協助台灣廠商交換合法性,故企業的環境活動與其 財務績效之間並無顯著的差異關係存在。

Firms Decisions to Certify ISO14001 EMS and their Financial

Performance – An Empirical Study of Taiwan

Student:Tzu-Yar Liu Advisor:Dr. Po-Young Chu

Department of Management Science National Chiao Tung University

ABSTRACT

Rare empirical studies have analyzed the responses of Taiwanese manufacturing firms to ISO 14001 despite firm responses to environmental issues being an important aspect of environmental management. This study empirically examines the determinants of firms' environmental self-governance. Export-oriented Taiwanese firms, which face supply chain pressure from multinational firms and environmental concerns from foreign consumers, are found to be more likely than domestic-focused firms to adopt ISO 14001. This study also finds that several firm attributes are decisive for firm adoption of ISO 14001. However, this study does not find a significant impact of local governors’ political party affiliation on firms’ decisions on ISO 14001 certifications. Since the institutional forces such as greening supply chain pressures have become the major driver of the moves of Taiwanese firms towards more environmentally responsible operations, the estimation results demonstrate that Taiwanese firms regard the ISO14001 standard as an acceptable means of seeking legitimacy, establishing trust and long-term relationships with a wide range of stakeholders, and deflecting the scrutiny and interest of watchdog agencies and other interested parties worldwide; thus, no significant correlation exists between environmental and financial performance.

ACKNOWLEDGMENTS

論文付梓之際,心中滿是感謝。本論文得以順利完成,首先要感謝指導老師朱博湧 與吳世英兩位教授,於論文撰寫期間之督促與悉心指導,在遭遇瓶頸時總是協助渡過難 關,解決心中的疑問,並且撥冗校閱;師恩浩瀚,永銘於心,謹誌於卷首以聊表由衷之 敬意與謝意。 口試委員于樹偉老師在環境與安全衛生管理學界享負盛名,學養豐富而治學嚴謹; 而黃仁宏老師的管理素養深厚紮實,在行銷領域所發表的文章鞭闢入裡;鄧美貞老師以 其在計量經濟和統計技巧之功力,對我論文的完成功不可沒。承蒙三位老師在論文口試 上的指正與建議,讓學生多所學習,使得本論文更加完善,在此也深表感激。 感謝朱門團隊的弘書、裕淩及杏華總是提供我許多資訊,對我的研究具有莫大影響 力,很慶幸自己能夠認識你們。感謝工研院能環所的好同事們,在我博士班修業期間, 總是給我許多的鼓勵與支持,特別因為你們的陪伴使我在工作繁忙之際,適時提供必要 協助。 最後要感謝我的母親、愛妻及岳父母,當我在工作和學業蠟燭兩頭燒之際,容忍我 的焦躁與不安。也再次謝謝我的太太_世宜對我的支持與包容,陪著我走過這一段歷 程,做我精神的後盾。還有因為對三個寶貝_怡萱、冠廷及晏圻的愛,使得我在最苦的 時候,還是可以堅強、忍耐,發揮個人最大的潛力。 謹以此論文獻給天人永隔的父親,謝謝他無怨無悔對我的栽培與付出,直到生命終 點,在病榻彌留之時仍不忘對我叮嚀與牽掛,希望今日拿到博士學位的我,更能讓父親 開心,也想告訴他,我會更加努力善盡對家人、社會及國家之職責!TABLE OF CONTENTS

摘 要

...I ABSTRACT ... II ACKNOWLEDGMENTS ... III TABLE OF CONTENTS ...VI LIST OF TABLES ... VII LIST OF FIGURES... VII

1. INTRODUCTION... 1

1.1RESEARCH BACKGROUND... 1

1.2RESEARCH OBJECTIVES... 6

1.3RESEARCH FRAMEWORK... 8

2. LITERATURE REVIEW ... 11

2.1ISO14001ENVIRONMENTAL MANAGEMENT SYSTEM... 11

2.2INTERNATIONAL TRADE... 16

2.3LOCAL POLITICAL COMPETITION... 17

2.4CERTIFICATION SUBSIDY... 20

2.5FIRM ATTRIBUTES... 21

2.6FINANCIAL PERFORMANCE... 24

3. DETERMINANTS OF A FIRM’S ISO 14001 CERTIFICATION... 30

3.1SPECIFICATION... 30

3.2DATA SOURCES... 31

3.3VARIABLE MEASUREMENT... 33

3.4RESULTS AND DISCUSSION... 43

4. ASSESSMENT OF ISO14001 EMS IN FINANCIAL PERFORMANCE52 4.1RESEARCH METHODOLOGY... 52

4.1.1 Measurement Indicators and Methods ... 52

4.1.2 Research Object... 53

4.1.3 Research Hypothesis ... 55

4.2FINDINGS... 55

4.2.1 Empirical Findings... 55

5. CONCLUSIONS... 62

5.1 Conclusion and Contribution ... 62

5.1.1 Determinants of A Firm’s ISO 14001 Certification ... 62

5.1.2 Assessment of ISO14001 EMS in Financial Performance... 63

5.2STUDY LIMITATIONS AND FUTURE RESEARCH... 64

REFERENCE ... 66

LIST OF TABLES

Table 1: No. of Taiwanese ISO 14001-certified enterprises during 1996-2004...15

Table 2: Annual no. of enterprises that have gained ISO 14001 certification ...15

Table 3: Descriptive statistics ...38

Table 4: Descriptive statistics by industry...41

Table 5: Results of the random effects probit regressions...49

Table 6: Measurement index of financial performance...53

Table 7: Sources for important parameters in this investigation ...54

Table 8: Basic analysis of ISO 14001-certified and uncertified enterprises...56 Table 9: Analysis of Nonparametric Test of ISO 14001-certified and uncertified enterprises.58

LIST OF FIGURES

Figure 1: Overview of research process ...10 Figure 2: Total no. of ISO 14001-certified enterprises globally...14

1. INTRODUCTION

1.1 Research Background

In an era defined by accelerated population growth and dwindling non-renewable resources, balancing the pursuit of economic growth with environmental conservation is becoming increasingly important in firm policy making. Since 1987, the U.N. World Commission on Environment and Development has promoted its Agenda 21, inducing nations to devise specific policies addressing sustainable development. During the past decade, sustainable development has become a common value worldwide, a way of thinking, and a watchword; national sustainable development policies have made environmental management a key issue in the twenty-first century. Additionally, growing environmental pollution and ecological destruction have also become major international concerns. In response to a resolution of the United Nations Conference on Environment and Development (UNCED) held in Rio de Janeiro in 1992 on the subject of designing an instrument for encouraging sustainable development, the ISO 14001 International Standard was issued and amended by the International Organization for Standardization (ISO) in September 1996 and November 2004, respectively. ISO 14001 requires firms to establish an Environment Management System (EMS) for supporting environmental protection, pollution prevention and continual improvement in managing the potential environmental hazards related to firm activities, products or services. However, ISO 14001 is not a performance-oriented standard; and focuses on

management processes rather than specific environmental outcomes (Bansal and Bogner, 2002). ISO 14001 is designed to be applicable to all types and sizes of organizations, and to accommodate diverse geographical, cultural and social conditions, and thus offers a more flexible standard than alternatives such as the Eco-Management and Audit Scheme (EMAS). The purpose of the ISO in designing the ISO 14001 system is to establish a basic international standard (currently, nations frequently follow their own environmental management systems, for example, the BS 7750 in the U.K., the EMAS in the E.U., Z-750 in Canada, and so on), and establishment of an international standard can avoid the formation technical barriers to trade (TBT), which could hurt both trade and business. Additionally, the ISO aims to promote a responsible attitude among individuals in the “global village.”

Although EMS implementation simply provides a framework for managing environmental impacts and provides a starting-point for developing firm-level environmental strategies (Christmann and Taylor, 2001), an EMS can help enhance firm performance by reducing waste and creating other efficiencies (Porter and van der Linde, 1995a; 1995b). The implementation of ISO14000 may provide a means of establishing a national policy of self-governance, especially in countries that lack environmental regulation or enforcement capabilities (Wilson, 1998).

Winsemius and Guntram (1992) pointed out the emerging awareness of consumers and companies regarding environmental issues; this new wave of thinking regarding sustainable development represents a grass-roots force that

governments and enterprises cannot afford to neglect. Governments and enterprises thus have increased their commitment to responsible environmental management, implementing policies to address adverse environmental impacts (Mulder, 1998; Walton et al., 1998; Gifford, 1997). Klassen and McLaughlin (1996) believed that enterprises promote environmental management to reduce the negative environmental impacts of their operations. Numerous scholars note that by promoting environmental management, companies are not only operationally successful, but also enhance their environmental performance (Eckel et al., 1992; Greeno and Robinson, 1992; Dean and Brown, 1995; Porter and van der Linde, 1995; Nehrt, 1996; Tibor and Feldman, 1996; Magretta, 1997; Weizsacker and Lovins, 1998; Stigson, 1998; Miles et al., 1999). Miles (1997) further stated that companies will have the difficulty of gaining international recognition if they are unable to obtain ISO 14001 certification.

During the recent decade, the emphasis on global environmental management has evolved from the conventional approach of command and control to the voluntary participation and avoidance approach. ISO 14001 is a voluntary scheme in the sense that firms can demonstrate their EMS consistency and management level by passing a third party certification and/or to themselves by self-declaration. Compared to the command and control approach, the voluntary scheme approach is a partnership concept based on corporate environmental management, which allows companies and government agencies to work together to identify their impact on the environment and improve their environmental performance. The empirical analyses for the U.S. Acid Rain Program reveal that voluntary participation

behavior for electric utilities can be explained via economic variables, showing cost-effective compliance strategies and low transaction costs (Montero, 1999). Moreover, empirical evidence shows that American firms have enhanced their financial performance by developing rent generating resources and capabilities, reducing resource use and process waste, improving product quality, and increasing international transactions (Delmas, 2001).

Taiwan is the 13th largest trading nation in the world, and international trade has been crucial to Taiwan’s economic development. The United States, Hong Kong, Japan, China, and Europe (notably France, Germany, the Netherlands, and the United Kingdom) remained the top buyers of Taiwanese exports in 2001, accounting for 60.5 % of total exports. The main export markets for Taiwanese firms are in Europe, Japan and North America. Taiwanese suppliers to multinational enterprises in these developed countries, including IBM, Ford, GM, Xerox, Honda, Toyota, HP, and Squibb, face pressure to pursue environmental certifications if ISO 14001 becomes a de facto requirement for selling in any value chain ending in these markets (Bansal and Bogner, 2002). Christmann and Taylor (2001) propose that globalization may have positive environmental effects since multinational ownership, multinational customers, and exports to developed countries increase self-governance of environmental performance. In reacting to this green trend and recognizing the integration of environmental management into business operations (Jiang and Bansal, 2003), Taiwanese firms have responded positively and proactively to ISO 14001 since its introduction. The Taiwanese government and numerous enterprises consider ISO 14001 to be a

“green passport” granting entry to international markets, and the ISO 14001 standard can also improve a firm’s image via increased environmental legitimacy (Jiang and Bansal, 2003).

With the growing importance of voluntary instruments for improving environmental quality, the determinants of firm decisions to voluntarily comply with environmental standards need to be well understood. Numerous empirical studies have examined the determinants of firm participation in voluntary environmental schemes in developed countries (DeCanio and Watkins, 1998; Arora and Cason, 1995; Henriques and Sardorsky, 1996; Nakamura et al., 2001). For example, DeCanio and Watkins indicate (1998) that firm-specific variables such as firm size, earnings and insider shareholders are significant determinants of voluntary participation of U.S. firms in the Green Lights program. Moreover, empirical studies have investigated the factors driving firms to seek ISO 14001 certification in developing economies such as China and Hong Kong (Cushing et al., 2005; Christmann and Taylor, 2001; Chan and Li, 2001). They generally find that exports to the developed countries are a key factor of firms’ adopting ISO 14001 certification.

Taiwan currently ranks among the top three nations worldwide in 30 products and manufacturing services (IDB, 2002) and globalization has increased the institutional and customer pressures on firms to exceed local regulatory requirements (Christmann and Taylor, 2001) though opponents of the World Trade Organization (WTO) claim that globalization has caused environmental deterioration in developing countries. From a political

perspective, Taiwan has experienced democratization over the past few decades and the central government continues to delegate responsibility for some environmental regulations to local governments. Determining the appropriate role of the various governments in the setting of environmental standards has been a key issue on the political agenda for Taiwan. However, no empirical studies have yet examined the firms’ adoption of voluntary ISO certification schemes in Taiwan. Therefore, it is imperative to investigate what factors drive firms to improve environmental protection through their adoption of ISO 14001 certification.

Recently, numerous Taiwanese enterprises have promoted ISO 14001 implementation and certification as an effective means of achieving sustainable development. Companies consider ISO 14001 to be a viable approach for helping them cultivate an ideal image and remain competitive attract sales, rather than as a regulation or limitation that brings unwanted stress. This trend also has positive societal effects. Thus, this study attempts to identify qualitative differences between companies with and without ISO 14001 certification. Additionally, this work also attempts to determine the differences in overall operational effectiveness between ISO 14001-certified and non-certified companies in terms of their efforts to balance environmental conservation and sustainable development.

1.2 Research Objectives

The general objectives of this research are to examine the factors driving Taiwanese firms to seek ISO 14001 certification. Specifically, the

objectives are as follows,

1. Investigation of determinants of firm self-governance in Taiwan from economic, social, environmental and political aspects.

2. Development of a model to assess the determinants of Taiwanese manufacturing companies to eatablish the certified ISO14001 Environmental Management System (EMS).

3. Identification of qualitative differences between companies with and without ISO 14001 certification and determination the differences in overall operational effectiveness between ISO 14001-certified and non-certified companies in terms of their efforts to balance environmental conservation and sustainable development.

To achieve the above objectives, it is based on random effects estimations of panel data over 1996-2004 in the study of determinants of firm self-governance in Taiwan. In order to investigate the factors leading a firm to become certified, firms which have adopted ISO 14001 certification at some previous point in the panel period must be omitted from the regressions. Hence, each firm in the sample has at most one observation of ISO 14001 certification. Following this procedure, this research has a final sample of 6,692 observations from 982 firms over 1996-2004.

In the study of assessing the role of ISO14001 EMS in financial performance, it is based on cross-section data during 1996-2004. This

work performs a business performance analysis of 982 listed companies, 332 of which are certified while 650 are not.

1.3 Research Framework

This research first examines the determinants driving Taiwanese firms to seek ISO 14001 certification. Particularly, it analyzes whether export ratio and local governors’ party affiliation influence a firm’s likelihood of adopting ISO 14001. Next, This study also seeks to understand the current situation of ISO 14001 certification for Taiwanese businesses and to shore up parameters used by academia to assess performance. Additionally, this study uses number of employees, total capital, and operating quota as indicators to measure enterprise size and to assign the firm to a certain industry category and attempts to use static measurements (ROE, ROA, P/E ratio, rate of gross profit) and dynamic measurements (revenue growth rates) to perform statistics analysis. This work performs a business performance analysis of 982 listed companies, 332 of which are certified while 650 are not.

The contents of this dissertation are organized as follows. The principle scheme of research process is shown in Figure 1.

Chapter 1 introduces the research background, objectives and framework involved in this research.

Chapter 2 first discusses pertinent literature such as ISO14001 Environmental Management System, international trade, local political competition, certification subsidy, firm attributes, financial performance and then presents different hypotheses.

Chapter 3 describes determinants of a firm’s ISO 14001 certification. The econometric specification, data sources, explanatory variables and the estimation results are provided and discussed in this chapter. Chapter 4 assesses the role of ISO14001 EMS in financial performance. Measurement indicators and methods, research objective, research hypothesis, empirical findings and evidence-based discussione are provided in Chapter 4.

Conclusions and recommended research directions are finally drawn in Chapter 5.

Chapter 1

Research Background & Objectives

Chapter 2

Literature review

Chapter 3

Determinants of a firm ISO14001 certification:

Econometric Specification, Data Sources & Explanatory Variables,

results & discussion

Chapter 4

Assessing the role of ISO14001 EMS in financial performance:

Research methodology & findings

Chapter 5

Conclusions & Recommendation

2. LITERATURE REVIEW

2.1 ISO 14001 Environmental Management System

During 1996, the ISO promulgated the ISO 14001 environmental management system (designed specifically for evaluating organizations) and other related standards (ISO 14004, 14010, 14011, and 14012), with the aim of providing industries with internationally recognized environmental management regulations and a certification standard. In response to the two key U.N. objectives of improving the environment and achieving sustainable development, ISO subsequently also posted environmental assessments of the products of numerous enterprises. Besides methodology and certification provided to firms by the ISO 14001 system, Technical Committee 207 (Environmental Management) focuses on producing environmental evaluations of firms and their products, and standardizing the rules and definitions of Environmental Auditing (EA), Environmental Performance Evaluation (EPE), Life Cycle Assessment (LCA), Environmental Labeling (EL), and Environmental Aspects in Product Standards (EAPS).

The Environmental Management System (EMS) comprises the core of the ISO 14000 family and has the serial number ISO 14001. The system mainly aims to enable environmental conservation via a systemized management program ― that is, the system stresses all conservation related matters, enabling management, measurement, improvement, and communication via systematic methodology, and does not address pollution prevention, clean-up technology, or emission standards. However, the system requires enterprises to prevent pollution or operate within the

parameters of sustainable development. ISO 14001 operates based on a voluntary scheme, and provides a new approach to conservation that replaces the command and control system, in which enterprises are led and legally forced by governments to adhere to certain standards. The voluntary scheme enables enterprises to assume responsibility themselves with the expectation that they will inevitably become conscious of the trends and needs of the Twenty-first Century and implement economically sound environmental management plans. Thus, the decision to implement ISO 14001 is voluntary and not binding, unlike the contractual obligations of environmental treaties.

Among the certifications of the ISO 14000 family, ISO 14001 system certification was the earliest to provide official requirements and guidelines for an international standard. ISO 14001 stresses management system, rather than technical pollution emission standard control and pollution testing technology. That is, the essence of the system lies in helping enterprises continually improve their pollution prevention abilities and enhance their environmental performance (Zhang et al., 2000). Accordingly, since promoting certification of the ISO 14000 family, ISO 14001 has increasingly caught the attention of the manufacturing industry along with the ISO 9000 quality management system certification. Certified enterprises have grown rapidly (Montabon et al., 2000; Rezaee, 2000; Chin and Pun, 1999), environmental consciousness is a critical factor in enterprise success, and certification is the only means of sustaining effective business performance (Miles et al., 1999; Magretta, 1997; Hehrt, 1996). Greeno and Robinson (1992) felt that the environmental management activities of enterprises will reduce the environmental impact of enterprise business activities, while

simultaneously enhancing their environmental performance and competitiveness.

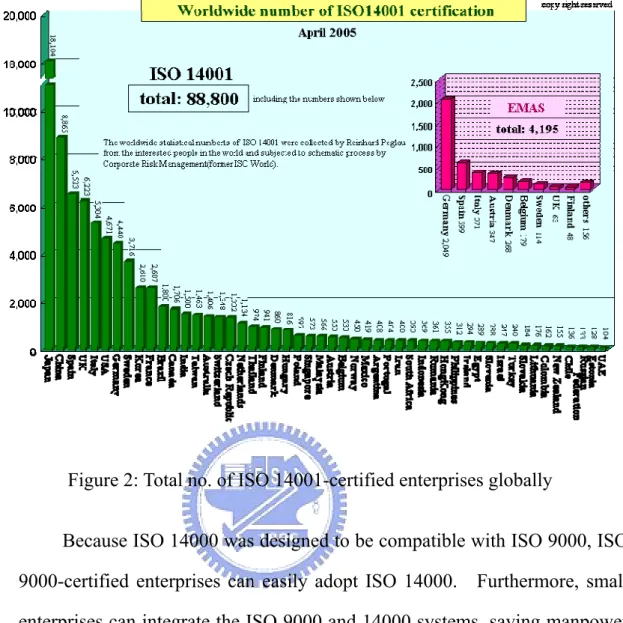

Since Taiwan is a major exporting nation, domestic industries fear that once ISO environmental management standards become industry requirement, they will become new trade barriers. However, industrial, political, and academic circles have been actively encouraging industries to promote the establishment and certification of the ISO 14001 system. Based on a survey of ISO 14001-certified enterprises performed by the Federal Environmental Agency in June 1996, the total number of certified Taiwanese enterprises was originally second just behind Japan (Steger 2000). However, since then the numbers of certified Chinese and South Korean enterprises have overtaken the number of such enterprises in Taiwan. In April 2005, certified Taiwanese businesses summed 1,463 out of total 88,800 (see Figure 2 ), ranking 14th globally in terms of countries with certified enterprises (ISO world, 2005).

Figure 2: Total no. of ISO 14001-certified enterprises globally

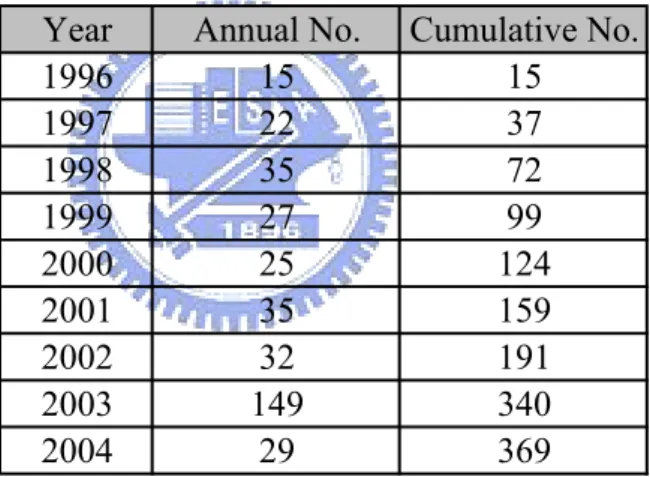

Because ISO 14000 was designed to be compatible with ISO 9000, ISO 9000-certified enterprises can easily adopt ISO 14000. Furthermore, small enterprises can integrate the ISO 9000 and 14000 systems, saving manpower and money, and becoming more efficient. Currently, 10,000 Taiwanese businesses have ISO 9001 certification, while 1,445 have ISO 14001 certification (see Table 1). Table 2 lists the statistics for listed manufacturing enterprises with ISO 14001 certification. Domestic organizations that have received ISO14001 certification are still at the primary stage in the manufacturing industry likewise, other organizations ( such as, government organizations, service industries, hospitals, schools, and so on) are still observing developments from the sidelines, or they do have the difficulties to establish the ISO 14001 system in their organizations.

Table 1: No. of Taiwanese ISO 14001-certified enterprises during 1996-2004

Year Annul No. Cumulative No.

1996 30 30 1997 80 110 1998 238 348 1999 220 568 2000 181 749 2001 212 961 2002 159 1120 2003 225 1345 2004 100 1445

Source: Taiwan Environmental Management Association/Organized by Industrial Development Bureau, MOEA, May 2005.

Table 2: Annual no. of enterprises that have gained ISO 14001 certification

Year Annual No. Cumulative No.

1996 15 15 1997 22 37 1998 35 72 1999 27 99 2000 25 124 2001 35 159 2002 32 191 2003 149 340 2004 29 369

2.2 International Trade

Reduced barriers to trade and foreign direct investment have increased globalization. Consequently, some are concerned that countries with lax environmental regulations might become pollution havens for pollution-intensive industries in a global economy with cross-country differences in environmental regulations. For example, opponents of the World Trade Organization contend that multinational firms relocate to low-income countries, whose people are so eager for jobs that their environmental regulations are weak (Dasgupta et al., 2002). Moreover, developing countries may sacrifice their environmental quality to reduce the production costs of their pollution-intensive products and to raise competitiveness of their products in foreign markets.

Taiwanese firms play an important role in the global supply chains of manufacturing, with an extensive customer base in Europe, Japan, and North America. Since these customers place a high priority on environmental protection, Taiwanese firms face direct pressures from their dominant and definitive stakeholders (Jiang and Bansal, 2003), in the form of supply chain pressure from multinational enterprises such as HP, IBM and Ford. For example, firms such as Ford, General Motors, Volvo, Toyota, and Siemens require that all or some of their suppliers be ISO 14001 certificated. Therefore, seeking ISO 14001 certification has become a key priority for Taiwanese firms because such a certification represents a green passport to the Europe and North American markets, and the lack of such certification can lead to the loss of important business opportunities (Bansal and Bogner, 2002).

Moreover, multinational customers may require their suppliers to obtain ISO 14001 certification because it is more practical than monitoring the environmental performance of their suppliers directly (Christmann and Taylor, 2001). Consequently, firms in many export-oriented Asian countries are rushing to implement ISO 14000 certification (Roht-Arriaza, 1997). A study of China-based businesses reveals broad-based empirical support for export-oriented incentives (Christmann and Taylor, 2001). Jiang and Bansal (2003) also indicate that ISO 14001 is conceived and used as a communication tool and thus increases exchange legitimacy (Suchman, 1995). Although environmental requirements vary among countries, the developed countries including the EU, Japan and the US generally demand a higher environmental standard for imported products. Therefore, this research proposes that firms with higher ratios of products exported to the EU, Japan and the US are more likely to seek ISO 14001 certification than those with lower export ratios.

2.3 Local Political Competition

The literature on environmental federalism argues that local governments may compete to attract business investment and create new jobs by setting lower local environmental standards (Jaffe et a., 1995). Local governments may race to the bottom if the central government does not impose stricter regulations on environmental standards. In contrast, economists also suggest that local policymakers would tailor policies to the

preferences of their constituents. Evidence also exists of a real and substantial response at the state and local levels comprising various programs for improving environmental quality in response to public concern (Oates, 2001).

In 1996, the then ruling Kuomintang (KMT) county magistrate approved the plan of the German chemical and pharmaceutical giant Bayer to establish a giant TDI (Toluylendiisocyanat) plant in Taichung, located in central Taiwan. This factory was to produce 100,000 metric tons of TDI annually, making it the second biggest TDI producer in the world. This investment plan was controversial, with resistance primarily being led by the opposition Democratic Progressive Party (DPP), which organized demonstrations involving up to 4,000 residents of the area around the proposed plant site. The main concern was the threat of phosgene, a poisonous by-product of TDI production, which was used as a chemical weapon during World War I.

The new Taichung county magistrate from the DPP was elected in late 1997, and announced a delay in issuing establishment permits pending a local referendum scheduled for June 1998. Consequentially, Bayer officially cancelled its investment plan in Taiwan in March 1998, and eventually relocated the facility to Texas, although it had obtained approval from the central government and had been negotiating with the local government for four years to proceed with the project in Taiwan (The New York Times, March 19, 1998).

The Bayer incident demonstrated that local governments may advocate more environmentally friendly policies to compete for votes. Since ISO

14001 is perceived to be a valuable environmental protection tool, it provides firms a systematic approach to environmental issues and demonstrates the commitment and performance of firm management to interested parties. ISO 14001 certification can further enhance firm identity and image as environmentally responsible and help minimize potential hazards associated with local government environmental policies. In Taiwan, the DPP mayors or local government magistrates are generally believed to enforce more stringent environmental protection than their KMT counterparts. ISO 14001 certification can protect firms from challenges to their environmental reputation by special interest groups, and thus firms located in the jurisdictions of DPP local governors are expected to be more likely to adopt ISO 14001 certification.

Although the investigation on the relationship between local governors’ party affiliation and ISO certification does not provide a test of a race to the bottom, it provides evidence on whether firms adjust their environmental strategies in response to the demand from various local policymakers. As noted above, local policymakers may choose different environmental standards to promote the well-being of their residents or to seek re-election. Therefore, if firm decisions on ISO 14001 certification are affected by local governors’ party affiliation, it implies that local standards for environmental quality or local policymakers’ attitude toward environmental hazards can influence the firms’ environmental protection.

2.4 Certification Subsidy

The Taiwanese government began to promote various programs for improving the environmental performance of industry during the mid 1980s. Notably, the Environmental Protection Administration (EPA) was established to develop and enforce environmental regulations, and the Industrial Development Bureau (IDB) of the Ministry of Economic Affairs (MOEA) was assigned the task of designing appropriate technologies, and providing technical assistance and financial incentives to industries practicing appropriate environmental management. IDB promoted ISO 14001 EMS using a financial subsidy approach. Firms paired with registered technical assistance providers can apply for subsidies to cover 40% to 60% of the cost of preparing ISO certification, up to a maximum of US$16,000 per case over 1996-2000 and up to a maximum of US$6,000 per case since 2001. The government budgets appropriated for subsidizing ISO certification were US$277K, US$267K, US$243K, US$173K, US$207K, US$257K, US$143K, US$170K and US$147K for the years ranging from 1996-2004, respectively (Source: Taiwan Environment Management Association). The exchange rate over this period was around NT$30 per US dollar.

Preparation and implementation costs range between US$10,000 and US$128,000 (Freeman, 1997) and can represent a barrier to ISO certification for firms with little cash flow. With financial incentives provided by the government, firms can not only save on implementation costs, but can also reduce uncertainty regarding the future value of the standard. A subsidy has been proposed to promote firm activities with risks or firm activities

producing public goods. For example, many countries adopt tax-based subsidies to stimulate R&D expenditures (Hall and Van Reenen, 2000). This government sharing of the risk of implementing environmental standards has increased firm motivation to obtain their ISO 14001 EMS. As of the end of 2004, 305 firms receiving subsidies from IDB had already received ISO 14001 certification (IDB, 2004). Firms receiving government subsidies for implementing ISO 14001 EMS are thus believed to have more incentive to seek ISO 14001 certification than those receiving no subsidies.

2.5 Firm Attributes

We also account for firm-level determinants in analyzing firm decision to adopt ISO 14001 certification. These variables include firm size, profitability, debt ratio, R&D expenditure, and location, which are discussed below.

Previous studies indicate that firm size positively influences environmental performance (Hartman, Huq and Wheeler, 1997) owing to economies of scale in pollution control equipment. Nakamura et al. (2001) indicate that certification involves significant fixed costs, which are less significant for larger organizations as compared to smaller ones. Hence, the larger a facility, the greater the potential for spreading these fixed costs across the operation (King and Lenox, 2001).

The costs of ISO 14001 implementation depend on facility size and the sophistication of the environmental management system, and range between US$10,000 and US$128,000 (Freeman, 1997). Additionally, the certified firm needs to bear annual maintenance costs of US$5,000 to US$10,000. Developing, certifying and maintaining ISO 14001 EMS can represent a significant expense for non-profitable firms with high debt ratios and consequently profitable firms are more likely to see it as a useful investment (Aragon-Correa, 1998; Clark, 1999). However, the ISO scheme also represents a way for less competitive firms to seek an advantage over more competitive rivals by playing upon the public image it generates (Chapple et al., 2001). Notably, Chapple et al. (2001) find that less profitable firms were more likely to seek ISO 14001 than profitable firms and contended that they are looking to gaining a competitive advantage through non-price competition focused on environmental quality.

Debt ratio influences capital costs and financial flexibility (Nakamura et al., 2001). Although firms with low debt ratios are expected to have more flexibility to finance new environmental programs, this proposition is less certain since debt ratio may reflect firm financial strategies adopted to reduce tax burden (Nakamura et al., 2001).

Firms are gradually acknowledging eco-efficiency as one of the major challenges in R&D practice in product innovation (Noci and Verganti, 1999). Previous studies on environmental compliance costs have traditionally focused on static cost impacts and ignored the importance of offsetting productivity benefits from innovation. In contrast, innovative solutions and

significant R&D investment can create win-win solutions for environmental problems and productivity improvement (Porter and van der Linde, 1995a). Empirical evidence also indicates that environmental innovation is more likely to occur in internationally competitive industries (Brunnermeier and Cohen, 2003). Konar and Cohen (2001) find that improved environmental performance boosts firm asset value. Firms may voluntarily seek environmental compliance as well as R&D activities to pursue higher profitability. This is particularly appropriate for firms with high R&D investment which are more likely to obtain technological solutions for their environmental problems and thus find it easier to implement the ISO standard (Nakamura et al., 2001). Established in 1980, the Hsinchu Science-based Industrial Park (HSIP) was the first science park of its kind in Taiwan. With the mission of establishing a high quality R&D base for the high-tech industry, HSIP firms enjoy investment privileges and benefits courtesy of government agencies, including preferential tax treatment, lower utility and land costs, and R&D subsidies. However, the environmental activities of HSIP firms, including pollution control plan implementation, air pollutant emissions management, and wastewater inspection are monitored more intensively by interested parties including neighboring communities, government agencies, environmental groups, and the mass media. Bansal and Bogner (2002) state that the ISO 14001 standard provides an acceptable signal, which conforms to the expectations of various stakeholders because it is externally endorsed, and requires extensive documentation. Firms with the ISO 14001 standard can thus help to establish trust and long-term relationships with stakeholders and deflect the scrutiny and interest of watchdog agencies and interest groups.

2.6 Financial Performance

The usage scope of the ISO 14001 system is such that the system standard requirements are applicable only to those environmental aspects that can be effectively controlled by the organization; the system does not assert any specific principles regarding effective environmental management. ISO 14001 and 14004 standards are simply used to assist organizations in establishing their own management systems, not to force on them regulations to achieve certain objectives. Increasing numbers of enterprises are attempting to become ISO 14001-certified of their own accord and are even requesting that suppliers become certified within certain time periods. ISO 14001 has become a key tool for assessing supplier environmental performance (Miles et al., 1997, Miles et al., 1999, Mohamed, 2001). Tibor and Feldman (1996) felt that companies, following having pushed for ISO 14001 certification, have increased their awareness of environmental issues; became more actively involved in environmental management activities, improved their environmental performance, and are more knowledgeable about conducting life cycle analyses and procuring environmentally friendly products. The research of Nakamura et al. (2001) demonstrated that enterprise ISO 14001 certification influences their consumption and procurement of products made from natural resources, such as petroleum products, water, and paper products.

Numerous scholars, both in Taiwan and abroad, hold markedly different views regarding the relationship between the environmental and financial

performance of enterprises. Some of them feel that good environmental performance positively influences financial performance. However, others are suspicious of this belief or even posit contradictory theories. Owing to different research themes and the difficulty of balancing environmental and financial performance, the results of different studies differ markedly.

Allen (1992) and Schmidheiny (1992) believed that the environmental performance resulting from promoting environmental activities can actually reduce product costs and waste, and enhance enterprise financial performance. Moreover, enterprise environmental performance can improve profitability (Bragdon and Marlin, 1972; Spicer, 1978) and reduce environmental risk (Spicer, 1978); environmental activities improve enterprise environmental performance (Moskowitz, 1972; Parket and Eilbirt, 1975; Sturdiva nt and Ginter, 1977; Arolow and Gannon, 1982; Capon et al., 1990). Furthermore, a positive relationship exists between environmental and financial performance (Bragdon and Marlin, 1972). Enterprises that are active in environmental management can significantly improve their environmental performance and upgrade their financial performance (Callan and Thomas, 1996; Ilinitch et al., 1998; Wen and Chen, 1998; An Baoyi, Xu Mulan, Liu Zhongju, 1999; Chin and Pun, 1999; Shi Lixing, Huang Fenghui, Gun Meixiu, 2000; Steger, 2000). The study of Cohen et al. (1995) demonstrated that among large enterprises in the U.S., those with superior environmental performance generally also have good financial performance. However, Nehrt (1996, 1998) observed that large enterprises that lead in terms of environmental innovation are typically the fastest way to achieve financial performance.

On the other hand, some scholars maintain that enterprise social responsibilities and financial performance are antithetical (Carter et al., 2000). Vance (1975) and Ullman (1985) both felt that environmental investments increased enterprise production costs and negatively impacted financial performance. Most of the researchers believed that introducing environmental activities into enterprise business operations negatively influences their financial performance (Freeman, 1994; Judge and Hema, 1994). Moreover, Walley and Whitehead (1994) demonstrated that enterprises generally believe that pushing for environmental-related measures and abiding by related laws and regulations will increase operating costs and negatively impact profitability. Cost increases result from the internalization of costs that were previously external, for example assuming the costs of air pollution (Bragdon and Marlin, 1972; Klassen and McLaughlin, 1996). The research of Jaggi and Freedman (1992) demonstrated that enterprises investing in pollution prevention equipment do not improve their financial performance—that is, no positive relationship exists between environmental and financial performance.

Additionally, some scholars feel that no relationship exists between enterprise social responsibilities and financial performance (Alexander and Buchholz, 1978; Abbot and Monsen, 1979). Additionally, no noticeable differential relationship necessarily exists between enterprise environmental disclosure activities and financial performance (Freedman and Jaggi, 1982; Wiseman, 1982), and nor is their any noticeable difference between enterprise environmental performance and profitability (Fogler and Nutt, 1975; Rockness et al., 1986). Mahaptra (1984) demonstrated that

companies which invest heavily in pollution clean-up are not guaranteed a good environmental performance. Jaggi (1993) felt for businesses that invest in pollution prevention and clean-up equipment, such a move is merely a temporary measure to avoid violating government regulations. Additionally, in the present case, the relationship between environmental and financial performance becomes negative. Conversely, if enterprises make a long-term investment in pollution prevention and clean-up equipment, this equipment will boost their market performance, representing a positive relationship between environmental and financial performance.

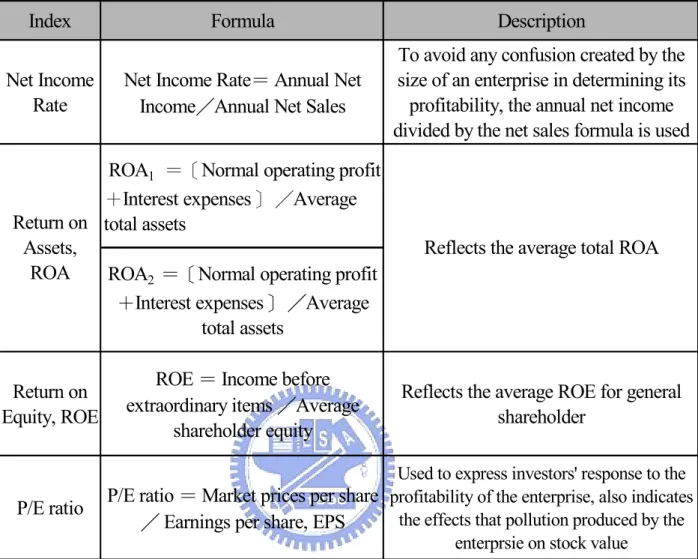

In synthesizing the above sources, owing to disparities in research subjects and methods, there is obviously still no overarching theory regarding the relationship between environmental and financial performance. This study analyzes the basic characteristics and financial performances of ISO 14001-certified and uncertified Taiwanese listed enterprises based on the research of scholars regarding ISO 14001 environmental management. Regarding an evaluation standard for measuring performance, the Taiwanese stock market breaks down enterprise finances into five categories: profitability, cash flow, ability to pay debt, capital debt management and growth capabilities. These indicators comprise the evaluation system applied to the finances of listed companies. In assessing enterprise financial performance, the business performance, cash flow, and financial circumstances reflect the profitability of that enterprise, and the enterprise goals and demands must be kept in mind when performing financial ratio analysis. Enterprise performance is defined as the degree to which the enterprise has satisfied its objective(s), and the resource use situation facing

the enterprise, which respectively indicate enterprise effectiveness and efficiency. Katzell (1975) proposed that the scope of efficiency is rather large, and includes performance, productivity, and profitability. Numerous scholars believe that financial performance is influenced by manufacturing performance, product effectiveness, and market conditions (Myers & Marquis,1969; Cooper,1979; Cooper & Kleinschmidt,1987; Zirger & Maidique, 1990).

Although Chakravarthy (1986) found evidence that methodology using profitability as a measure of performance does not accurately determine whether the operations of an enterprise are superior or not, numerous scholars still use financial indicators such as the 14 commonly used measurement parameters identified by Cooper et al. (1986): investment return rates, sales quota return rates, sales income growth rates, cash flow, and investment/market share rates, comparative product quality of competitors, comparative promotions of new products by competitors, comparative direct production costs of competitors, product R&D, manufacturing R&D, differences in return on investment (ROI), changes in ratio of ROI, and cash flow/investment ratio changes. Cooper et al. felt that although measures of profitability are limited, they are still important indicators of performance. Bettis and Mahajan (1985) use the ratio of profitability ( namely, the average of capital return rate for the past five years) to risk (namely, shortages in capital return rate for the past five years) to measure organization performance. Ranftl (1979) defined productivity as the ratio of investment to output, that is, using organization resources to effectively produce. Research indicates that financial ratio information is

clearly related to assessments of financial performance; however, past measurement indicators are based on financial indicators such as the definitions of Cohen, Fenn, and Naimon (1995) regarding accounting return rates, the view of Jaggi and Freedman (1992) and Cohen, Fenn, and Naimon (1995) regarding stock market performance, the suggestions of Jaggi and Freedman (1992) to use P/E ratio to measure stock market performance, and the four indicators used by Fullerton and McWitters (2001) in their research on the influences of enterprise financial performance (namely, EBIT, ROA, ROS, and cash flow). Bragdon and Marlin (1972) used EPS, ROE, and ROI as financial indicators to research the relationship between firm environmental and financial performance.

3. DETERMINANTS OF A FIRM’S ISO 14001

CERTIFICATION

3.1 Specification

This study follows previous empirical studies on transition decisions, such as the transition from being employed to self-employment (Bruce, 2000), in developing an empirical strategy to estimate the determinants of firm decision to adopt ISO 14001 certification. Specifically, the econometric specification is defined as follows:

)

~

(

)

|

1

(

y

it itη

i itβ

P

=

X

=

Φ

+

X

,where the dependent variable,

y

it, equals 1 if firm i obtains ISO14001 certification at time t , and 0 if firm i remains uncertified. The Xit

denotes a vector of variables including export ratio, political party affiliation of local governors, government subsides to certification, firm size, profitability, debt ratio, R&D expenditure, location and other control variables. Meanwhile, Φ represents the cumulative probability of a normal distribution and an empirical specification for the above equation is a random-effects probit. The maximum likelihood estimates for the firm-specific effects η and βi

~

are inconsistent.

As noted above, we can analyze a firm’s transition from being non-certified to certified by utilizing panel data. Moreover, estimations based

on panel data can ameliorate the endogeneity problem because firm-specific effects can be controlled for and observations from different years can increase variable variations.

3.2 Data Sources

The estimations used in this study are based on the Taiwan Stock Exchange and Over-the-Counter sample drawn from the Taiwan Economic Journal (TEJ) Data Bank. The data bank includes firms from the cement, food, plastics, textiles, machinery, electrical appliances, chemical, glass and ceramics, paper and pulp, metals, rubber, automobile and electronics industries. The final sample is comprised of a total of 332 ISO 14001-certified firms and 650 non-certified firms from 13 industries over the period of 1996-2004, after some firms were excluded due to missing or outlier values. When the panel period is short (Chamberlain, 1980), on the other hand, the conditional fixed-effects estimations will exclude the firms without transition during the panel period and limit the regressions to the 332 certified firms. Therefore, we do not estimate the fixed-effects model in this study. The observations with sales less than NT$100,000 are omitted from regressions. Nevertheless, we also utilize the whole sample to estimate the coefficients and find no significant changes in estimates.

This study is based on random effects estimations of panel data over 1996-2004. In order to investigate the factors leading a firm to become certified, firms which have adopted ISO 14001 certification at some

previous point in the panel period must be omitted from the regressions. For example, if a firm adopted ISO 14001 certification in 2000, this firm’s observations over 2001-2004 would be omitted from the regressions, leaving only the firm’s observations over the 1996-2000 period for regressions. Hence, each firm in the sample has at most one observation of ISO 14001 certification. Following this procedure, we have a final sample of 6,692 observations from 982 firms over 1996-2004.

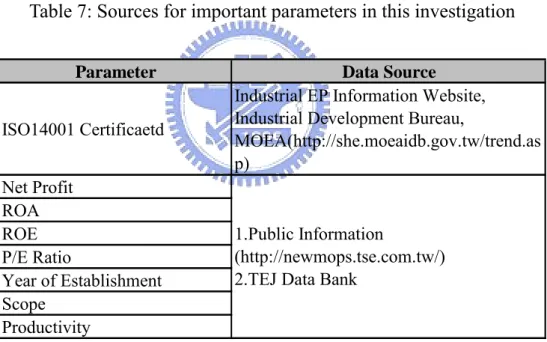

In particular, we obtain the list of ISO 14001-certified firms from the Taiwan Environmental Management Association. Since this study empirically examines various factors leading Taiwanese manufacturers to obtain ISO 14001 certification, several sources of published data have been used to measure these economic and political variables. Firm-specific financial and economic information was primarily gathered from the TEJ Data Bank and also from the Taiwan Stock Outlook published by Wealth Magazine. Information on subsidies for ISO 14001 EMS has been obtained from the websites of the Chinese National Accreditation Board (The Chinese National Accreditation Board has been transformed into the Taiwan Accreditation Foundation since 2004.), Taiwan Environmental Management Association, Bureau of Standards, Metrology and Inspection of Ministry of Economic Affairs (MOEA) and the Foundation of Taiwanese Industry Service. Meanwhile, the information of firms located in HSIP is obtained from the Administration of the Hsinchu Scientific Industrial Park. Moreover, the Central Election Committee provided the names and political affiliations of elected magistrates/mayors; while the Ministry of Interior web

site was the source for information on the regional administrative jurisdictions of elected magistrates/mayors.

3.3 Variable Measurement

The dependent variable in this study is the binary variable, ISO certification, which represents whether a firm becomes ISO certified or not. ISO certification is based on the unit of plants or sites instead of a firm. Given that only firm-level instead of plant-level information is available, ISO certification is coded 1 for firms adopting ISO 14001 certification for at least one plant or site, and 0 otherwise. Among the 332 certified firms in the sample, only 20 firms have adopted ISO 14001 certification for more than one plant or site. Therefore, we do not distinguish the firms with more than one plant or site from those with only one plant or site in the regressions.

For each of the sample firms, firm-specific variables are defined below. Export ratio represents the percentage contribution of exports to total sales revenue. However, the pressure from multinational customers may vary with destination markets. To account for this variation, this study classifies the destination markets into two groups, one with a higher environmental standard for imports while the other has a lower standard. Although no unique criterion was used for the categorization, developed countries are generally believed to require a higher environmental standard for production activities. The EU, Japan and the U.S thus comprise the higher standard group. This study then weights each firm’s export ratio by using the ratio of exports in the

firm’s industry accounted for by the higher standard group. This study calculates these ratios for each industry utilizing the trade statistics from the governments.

The dummy variable DPP governor indicates the party affiliation of local governors, and is coded as 1 if the county magistrate or city mayor for the jurisdiction where the firm’s certified sites or main sites are located is a member of the DPP, and 0 if they are a member of some other political party. Furthermore, Subsidy, a binary dummy variable, is coded 1 for certified firms that received government subsidies to offset the costs of implementing ISO 14001, and 0 otherwise. The government reduced the maximum amount of subsidy to ISO 14001 certification from a previous amount of US$16,000 to $6,000 since 2001. This exogenous policy change provides a natural experiment for investigating whether the government’s smaller subsidy would reduce a firm’s decision to become ISO certified. Therefore, we include in the regressions the variable of Subsidy since 2001, which equals 1 if a firm received any subsidies over 2001-2004.

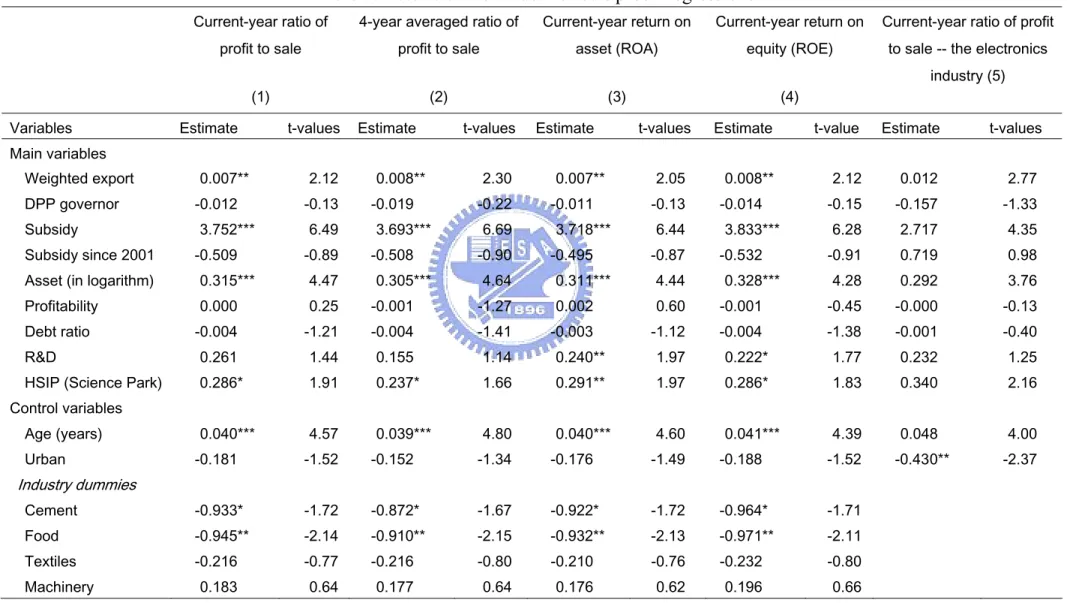

Asset denotes the logarithm of a firm’s assets and is used as a proxy for firm size. Firm profitability, Profitability, is calculated as the ratio of firm before-tax profits to total sales revenue for the current year. Previous studies have used an averaged measure to account for the volatility in profitability from year to year (Chu et al., 2005). Hence, this study also presents the estimation results based on a 4-year average profitability. To assess whether the estimates are affected by different measures of profitability, this study also utilizes return on asset and return on equity to estimate the effect of profit on

ISO 14001 adoption. Returns on assets are based only on current year data. Meanwhile, firm financial structure, Debt ratio, represents the ratio of current debts to total assets. Additionally, R&D, a proxy for relative size of firm knowledge capital, is calculated as firm R&D expenditure divided by total sales revenue. HSIP is a dummy variable used to indicate whether a firm is located in the Hsinchu Science-based Industrial Park (HSIP). HSIP is coded 1 if the firm is located in the HSIP, and 0 otherwise.

The regressions also include various control variables. This study investigates whether firms with different durations may have different likelihoods of implementing ISO 14001 EMS. Firm age is defined as the number of years between its establishment and 2004. Urban-rural disparity and income inequality exist among geographical regions and thus residents’ demand for environmental standards may vary. Therefore, it is necessary to control for possible effects owing to firms’ location in urban or county areas. Urban represents a binary dummy and is coded 1 if the firm’s main sites are located in any one of the seven urban areas in Taiwan (Taipei-Keelung, Kaohsiung, Taichung-Changhua, Jhongli-Taoyuan, Tainan, Hsinchu and Chiayi), and 0 otherwise.

Industrial pollution characteristics influence the propensity of companies to seek ISO 14001 certification. Firms in highly polluting industries or those with older technologies frequently are involved in a constant battle to reduce emissions incrementally to match increasingly stringent environmental regulations (Bansal, 2002). ISO 14001 certification should provide firms increased latitude to deal with regulators. Because the plastics industry is

generally believed to be one of the most polluted industries, it serves as the baseline industry in this study and dummies for the other 12 industries are included to control for the industry effects in the estimations. Additionally, we also include year dummies in the regressions to control for the year effects.

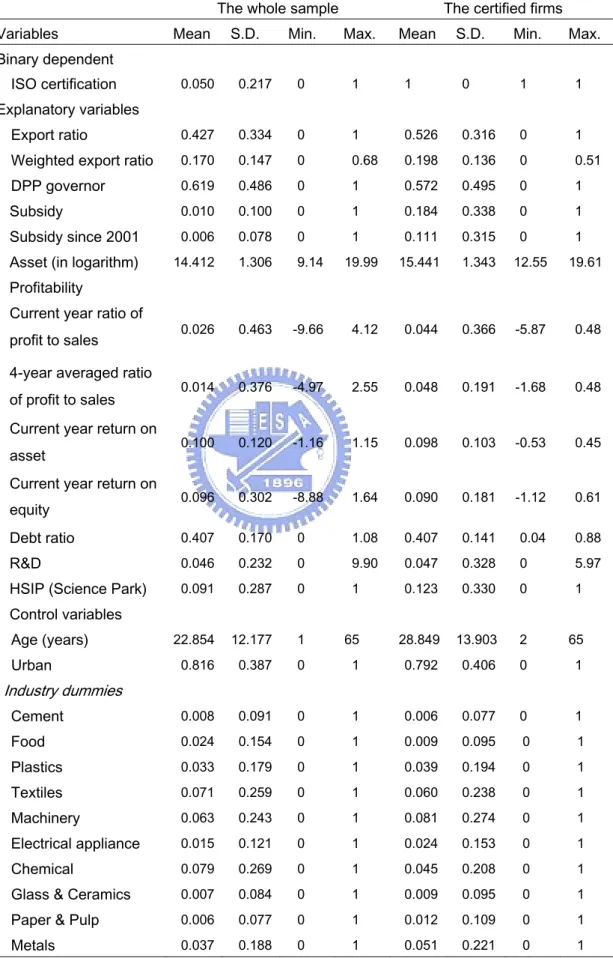

Table 3 lists the summary statistics for the final sample of 6,692 observations (see Apendix 1) from 982 firms and the subsample of certified firms. As noted above, among the sample of 982 firms, 332 firms have obtained ISO 14001 certification, comprising 5% of the total observations.

Table 3 indicates that the average export ratio is 0.427. This high export ratio supports the observation that the output of Taiwan is heavily export-oriented. To explain varying pressure from customers in different destination countries, this study categorizes export destinations into two groups, among which the EU, Japan and the US represent the countries requiring higher environmental standards for imports. The average weighted ratio of exports to the EU, Japan and the US equals 0.170. The firms located in the jurisdiction of DPP local governors and receiving subsidies for ISO 14001 certification comprise 61.9% and 1% of the total observations.

The average ratio of before-tax profit to sales equals 0.026 while the average ratio of return on asset and the average ratio of return on equity equal 0.1 and 0.096. The four-year average ratio of profit to sales equals 0.014, which is below the profitability for the current year and indicates that firms made smaller profits or incurred losses in the earlier years of the panel period.

The average values of debt ratio and R&D ratio equal 0.407 and 0.046, respectively. The mean value of R&D ratio equals 0.046 and suggests that most Taiwanese firms allocated limited budgets to R&D. The average length of firm establishment is 23 years. Most of the sampled firms’ factories are located in urban areas while most of the sampled firms are in the electronics industry.

The certified firms generally have higher mean values of weighted export, asset, and age than other observations. Compared to The whole sample, they also have higher percentages of firms receiving subsidy, and located in HSIP. A high ratio of certified firms became certified in 2003. In contrast, the percentages of certified firms located in jurisdictions of DPP governors and urban areas are lower than the other observations. It is also noteworthy that the four-year average ratio of profit to sale is negative for the certified firms and its variation is quite large.

Table 3: Descriptive statistics

The whole sample The certified firms Variables Mean S.D. Min. Max. Mean S.D. Min. Max. Binary dependent

ISO certification 0.050 0.217 0 1 1 0 1 1

Explanatory variables

Export ratio 0.427 0.334 0 1 0.526 0.316 0 1

Weighted export ratio 0.170 0.147 0 0.68 0.198 0.136 0 0.51

DPP governor 0.619 0.486 0 1 0.572 0.495 0 1

Subsidy 0.010 0.100 0 1 0.184 0.338 0 1

Subsidy since 2001 0.006 0.078 0 1 0.111 0.315 0 1

Asset (in logarithm) 14.412 1.306 9.14 19.99 15.441 1.343 12.55 19.61

Profitability

Current year ratio of

profit to sales 0.026 0.463 -9.66 4.12 0.044 0.366 -5.87 0.48

4-year averaged ratio

of profit to sales 0.014 0.376 -4.97 2.55 0.048 0.191 -1.68 0.48 Current year return on

asset 0.100 0.120 -1.16 1.15 0.098 0.103 -0.53 0.45 Current year return on

equity 0.096 0.302 -8.88 1.64 0.090 0.181 -1.12 0.61 Debt ratio 0.407 0.170 0 1.08 0.407 0.141 0.04 0.88

R&D 0.046 0.232 0 9.90 0.047 0.328 0 5.97

HSIP (Science Park) 0.091 0.287 0 1 0.123 0.330 0 1

Control variables Age (years) 22.854 12.177 1 65 28.849 13.903 2 65 Urban 0.816 0.387 0 1 0.792 0.406 0 1 Industry dummies Cement 0.008 0.091 0 1 0.006 0.077 0 1 Food 0.024 0.154 0 1 0.009 0.095 0 1 Plastics 0.033 0.179 0 1 0.039 0.194 0 1 Textiles 0.071 0.259 0 1 0.060 0.238 0 1 Machinery 0.063 0.243 0 1 0.081 0.274 0 1 Electrical appliance 0.015 0.121 0 1 0.024 0.153 0 1 Chemical 0.079 0.269 0 1 0.045 0.208 0 1

Glass & Ceramics 0.007 0.084 0 1 0.009 0.095 0 1

Paper & Pulp 0.006 0.077 0 1 0.012 0.109 0 1

Rubber 0.010 0.101 0 1 0.024 0.154 0 1 Automobile 0.003 0.052 0 1 0.015 0.485 0 1 Electronics 0.644 0.479 0 1 0.623 0.485 0 1 Year effect 1996 0.085 0.279 0 1 0.042 0.201 0 1 1997 0.098 0.298 0 1 0.054 0.227 0 1 1998 0.112 0.315 0 1 0.102 0.304 0 1 1999 0.118 0.322 0 1 0.087 0.283 0 1 2000 0.122 0.327 0 1 0.060 0.238 0 1 2001 0.124 0.329 0 1 0.105 0.308 0 1 2002 0.123 0.328 0 1 0.102 0.304 0 1 2003 0.119 0.324 0 1 0.398 0.490 0 1 2004 0.099 0.299 0 1 0.048 0.214 0 1 Observations 6,692 332 Notes:

1. A firm’s weighted export ratio is obtained by weighting the firm’s export ratio by the share of its industry products exported to the EU, Japan and the US.

2. The statistics for a 4-year averaged ratio of profit to sales are based on a subsample of 6,627 observations after observations with larger losses are excluded.

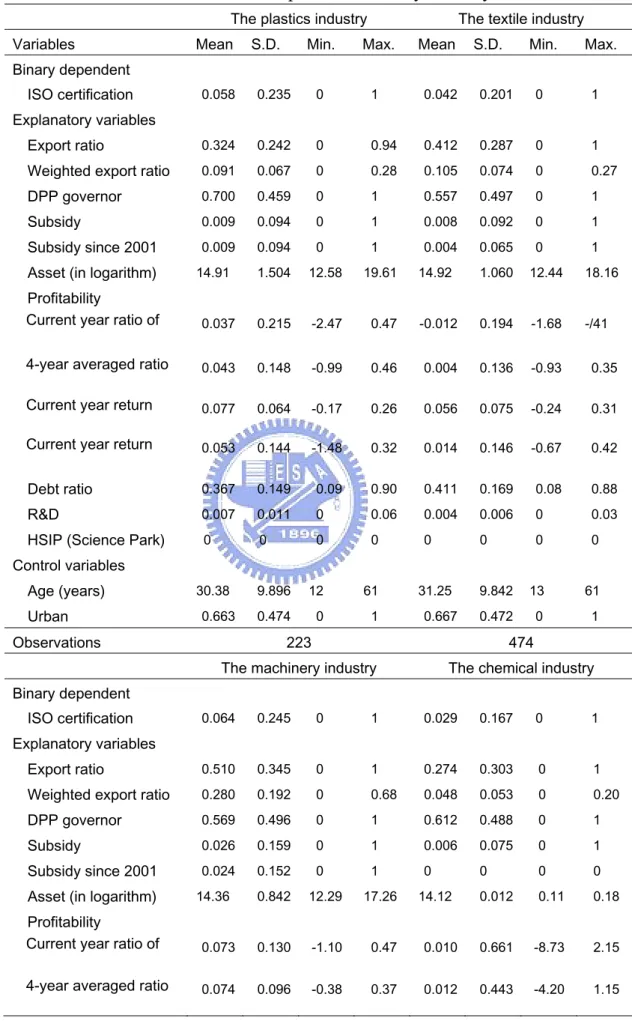

We also provide the summary statistics for each of the six industries with observations more than 200 in Table 4. Table 4 shows that the percentages of certified firms are similar among the six reported industries. The machinery industry and the electronics industry have higher ratios of export while the chemical industry exports a smaller proportion of its products. A higher percentage of firms in the machinery industry receive government subsidy. The firms in the chemical industry and the metals industry adopted ISO 14001 certification in the earlier years of the panel period while the firms in the plastics industry adopted it in the later years of the panel period. Since the HSIP was established to encourage high-tech firms’ investment, only firms in the chemical industry and the electronics industry are located in the HSIP. Moreover, the firms in the industry have a shorter period of establishment than those in other industries.

Table 4: Descriptive statistics by industry

The plastics industry The textile industry Variables Mean S.D. Min. Max. Mean S.D. Min. Max. Binary dependent

ISO certification 0.058 0.235 0 1 0.042 0.201 0 1

Explanatory variables

Export ratio 0.324 0.242 0 0.94 0.412 0.287 0 1

Weighted export ratio 0.091 0.067 0 0.28 0.105 0.074 0 0.27

DPP governor 0.700 0.459 0 1 0.557 0.497 0 1

Subsidy 0.009 0.094 0 1 0.008 0.092 0 1

Subsidy since 2001 0.009 0.094 0 1 0.004 0.065 0 1

Asset (in logarithm) 14.91 1.504 12.58 19.61 14.92 1.060 12.44 18.16

Profitability

Current year ratio of 0.037 0.215 -2.47 0.47 -0.012 0.194 -1.68 -/41 4-year averaged ratio 0.043 0.148 -0.99 0.46 0.004 0.136 -0.93 0.35

Current year return 0.077 0.064 -0.17 0.26 0.056 0.075 -0.24 0.31 Current year return 0.053 0.144 -1.48 0.32 0.014 0.146 -0.67 0.42 Debt ratio 0.367 0.149 0.09 0.90 0.411 0.169 0.08 0.88

R&D 0.007 0.011 0 0.06 0.004 0.006 0 0.03

HSIP (Science Park) 0 0 0 0 0 0 0 0

Control variables

Age (years) 30.38 9.896 12 61 31.25 9.842 13 61

Urban 0.663 0.474 0 1 0.667 0.472 0 1

Observations 223 474

The machinery industry The chemical industry Binary dependent

ISO certification 0.064 0.245 0 1 0.029 0.167 0 1

Explanatory variables

Export ratio 0.510 0.345 0 1 0.274 0.303 0 1

Weighted export ratio 0.280 0.192 0 0.68 0.048 0.053 0 0.20

DPP governor 0.569 0.496 0 1 0.612 0.488 0 1

Subsidy 0.026 0.159 0 1 0.006 0.075 0 1

Subsidy since 2001 0.024 0.152 0 1 0 0 0 0

Asset (in logarithm) 14.36 0.842 12.29 17.26 14.12 0.012 0.11 0.18

Profitability

Current year ratio of 0.073 0.130 -1.10 0.47 0.010 0.661 -8.73 2.15 4-year averaged ratio 0.074 0.096 -0.38 0.37 0.012 0.443 -4.20 1.15

Current year return 0.106 0.087 -0.30 0.58 0.097 0.101 -0.58 0.61 Current year return 0.106 0.124 -0.53 0.68 0.052 0.702 -8.88 1.18 Debt ratio 0.451 0.143 0.09 0.84 0.379 0.178 0.02 1.08

R&D 0.022 0.017 0 0.12 0.064 0.393 0 7.80

HSIP (Science Park) 0 0 0 0 0.036 0.187 0 1

Control variables

Age (years) 27.31 10.17 7 60 29.94 14.00 4 61

Urban 0.718 0.451 0 1 0.643 0.480 0 1

Observations 422 526

The metals industry The electronics industry Binary dependent

ISO certification 0.069 0.254 0 1 0.048 0.214 0 1

Explanatory variables

Export ratio 0.293 0.295 0 0.99 0.483 0.334 0 1

Weighted export ratio 0.131 0.134 0 0.49 0.199 0.143 0 0.50

DPP governor 0.772 0.420 0 1 0.626 0.484 0 1

Subsidy 0.008 0.090 0 1 0.008 0.091 0 1

Subsidy since 2001 0 0 0 0 0.006 0.077 0 1

Asset (in logarithm) 15.22 1.117 12.4 19.12 14.19 1.301 9.14 19.99

Profitability

Current year ratio of fit t l

0.008 0.137 -1.20 0.36 0.031 0.501 -9.66 4.12

4-year averaged ratio 0.003 0.085 -0.57 0.20 0.008 0.431 -4.97 2.55 Current year return 0.064 0.068 -0.27 0.32 0.114 0.134 -1.16 1.15 Current year return 0.039 0.127 -0.49 0.48 0.124 0.264 -8.88 1.64 Debt ratio 0.513 0.134 0.12 0.79 0.402 0.174 0.02 1.04

R&D 0.002 0.005 0 0.03 0.060 0.253 0 9.90

HSIP (Science Park) 0 0 0 0 0.135 0.342 0 1

Control variables

Age (years) 29.00 9.422 8 45 17.99 9.337 1 65

Urban 0.622 0.486 0 1 0.910 0.286 0 1

Observations 246 4,308

Notes:

1. To save space, we report the summary statistics for only the industries with more than 200 observations.

2. A firm’s weighted export ratios is obtained by weighting the firm’s export ratio by the share of its industry products exported to the EU, Japan and the US.