e-Commerce Roadmap for Success in the Banking Industry: A Customer Relationship Management Approach

19

0

0

全文

(2) 1. Introduction The performance of banking industry in Taiwan is worse than before. In 2000, nineteen of the first hundred leading banks in Taiwan made a loss. Besides, eight of ten highest-ROE-banks in Taiwan were foreign banks with good customer management strategies (Yang, 2001). E-Commerce (electronic commerce; EC) has broken the traditional concept and rules of operating. The key of surviving and winning the game in this new competition is recognizing the power of customers and satisfying their needs, but whether the motivation is making profit or not and whether the technological application is better than competitors or not were no more important (Murphy, 2000, pp.19~28). The core competence came from the internal part of enterprise first and then joined to the relationship to their supplier and collaborator, and it should be combined with the customer relationship in the new age. The customer relationship should be viewed as a valuable asset and be managed well to turn the concept from the development of “product” into the development of “customer relationship value” (Wayland & Cole, 1997). The companies would establish their competition advantage by making use of customized activities or services (Peppers & Rogers, 1993). Customer profitability has been touted as a significant point for many years, but has its difficulty to organize as an institution along customer-based line in practical or commercial realities. Today, due to sophisticated technologies of information and communications to dissolve barriers in services, the promise of one-to-one relationships, customer-value analysis, and mass customization are now possible (Peppard, 2000). CRM involves acquiring multidimensional customer information efficiently with the integration of processes and techniques (Kalakota & Robinson, 1999, pp. 109~135), and predicting and satisfying the customers’ needs through the information of potential or existing customers. CRM is an approach of management to establish and integrate channels with the applications of techniques and technology, to provide the customized services with the analyses of customer’s data, to make target customers connect easily and joyously with companies, and to make them become one of the participant in creating the value of -2-.

(3) enterprise. The implication of strategy is evaluating effectively in the operational and competitive environment of enterprise so as to establish the sustained advantage, and chase the growth and profit of company. Financial service is characterized by its large number of customers and the needs of privacy, speed and personality, so that the way it serves will be relevant to its EC development (Seybold & Marshak, 1998, pp. 193~213). In this point, how banks create their service, satisfy the customers’ needs, strengthen the relationship with customer, and develop their customer-oriented capability and EC by CRM, will be the sources of competition advantage (Lamparello, 2000). Banking industries in The United Stares and Europe in general are preceding other regions thanks to the development of high technology and global vision. In literature, there are some cases shown that U.S. banking is beginning to come to fruition from EC; by contrast, the domestic banks are now still struggled with some perceptual issues. Taiwan’s banking industry isn’t in the face of worldwide competition yet and still focus on local market; moreover, for lack of excellent fundamental knowledge, information technology and clear laws, the EC adoption of Taiwan’s banks are progressing at a slower pace. How to develop our own unique and sustained advantage will be the important issue of financial liberalization.. 2. Electronic Commerce and Customer Relationship Management Electronic Commerce is defined as the activities applied the computer or Internet to sell and buy the product or service, broadly speaking, EC involves in the digital or electronic commercial activities (Kalakota and Whinston, 1997). The concept of CRM was derived from “contact management” in 1980 ages about collecting all the information when customers connect to companies. Today, due to advances in information and communication technology, the promise of one-to-one relationship and mass customization are now possible (Shi, 1999; MicroStrategy, 2000; Peppard, 2000, p. 2), and its will useful to provide customized product or services and to increase the commercial activities. The EC/CRM strategy in this study includes the action or planning for adopting -3-.

(4) electronic medium to cause customers connecting with business more conveniently. In this new age, the roadmap for success is now a major concern in academic, industrial, government, and other sectors (Making Strategy, 1997) and CRM not only was one of the most important applications of EC but also the key point of success (Seybold & Marshak, 1998, pp. 3~7; Bielski, 2000; Chen, et. al., 2001; Chen, et. al., 2001, p. 53). 2.1 Customer–centric EC Enterprises start to develop EC such as setting their website or making their operation electronically for the prevalence of Internet. EC in initial stages was emphasized that put the rough information of product on their website—called as “brochure-ware”. In the middle age, EC was stressed on the setting of transactional function, and customers could have a convenient way when they deal with company, but the actual direct connections between companies and customers were decreased too. Nowadays, the businesses focus on the customer and highlight the instantaneous interaction relationship between companies and customers to satisfy the special needs of individual (Seybold & Marshak, 1998, pp. 8~18). 2.2 Technology and Customer Relationship Management From the view of CRM development, CRM in initial stages was laid emphasis on the improvement of product quality and marketing function. In middle stage, it was stressed on cross-selling and providing goods quickly and precisely. The famous applications were call center and automatic sales (Hong, 2001). Founded the technology such as computer hardware, computer software, and Internet techniques, CRM could integrate marketing, customer services and diverse interaction channels, which provide customized products or services by analyzing customer’s behavior model to maximize the value of enterprise (Shi, 1999). Seeing that digitalization has a great influence on CRM, people create the new words as Electronic Customer Relationship Management (eCRM) or Electronic Commerce Customer Relationship Management (CRM). The concept of these new words and CRM are very similar but strengthen the role technology plays on CRM. -4-.

(5) 2.3 CRM for EC Success Both EC and CRM stress that customer-centric concept to construct and improve the relationship with customer, and satisfy the needs of individual. Technologies strengthen the power of CRM and make it to be the key of EC success. Why CRM is thought more and more important is because that the average cost of attracting a new customer is higher than maintaining a existing one, so that the longer the customer is remained, the higher the profit company will have (Reichheld & Sasser, 1990). In the telecommunications and chemicals industries, for example, such expertise accounts for a difference of as much as 50% in return on sales between average and high-performing CRM companies (Tynan, 2000). The purpose of CRM is maintaining the customer relationship by recognizing their preference, predicting their needs, increasing customer satisfaction and loyalty, and finally keeping them. But the domestic banks are weak in the concept of CRM issues (Chen, et. al., 2001, p. 53; Coffey, 2001). 2.4 Impact on Banking Industry from EC and CRM Banking has the characteristic of using high density of information (Porter & Miller, 1985). In theory, all business can be managed by applying software, and most finance merchandise is transported in the form of information, instead of substantial delivery (Gartner Group, 2000). In terms of the level of digitalization, all the financial goods, flow path of deals and transportation can be implemented. As a result, from the aspect of property and business, the development of EC is more important to banking. (Tong, 2000) Through the progress, EC provides lower cost and higher efficiency. In addition, the digitalized channel has not only the traditional property, but also two-way immediate communication, which cut the distance between companies and customers. In the early service of ATM, banking industry continually offers telephone banking, network banking and customer center etc., which gradually increases the investment of front system, which is directly related with customers (Tong, 2000). It’s apparent that the key-point of using information technology has been transferred to customers, because the development target of EC is all customer-oriented (Grandy, 2000). In the future, -5-.

(6) consumers’ requirement will lead the direction of every kind of financial channel and service. In terms of banking industry, whose service needs no material cost, when client maintenance rate is higher, the breadth of earning profits is higher than other industries.. 3. e-Commerce Strategy in the Banking Industry Through Customer Relationship Management Strategy means the action program which enterprises adopt in order to reach the goal. One survey through the biggest 2,000 enterprises reveals that most of them think very highly of CRM, but lacking correct recognition, even the integral strategy (Meta Group, 2000, as cited in Brown, 2000, pp. 3-5). Some local investigation also shows that CRM is the issue enterprises care for most. However, they are short of professional knowledge and technological support. (Chen, 2001) That customer relationship is the foundation stone of enterprises’ profits has been a consensus for a long time. With using Internet and applying related information technology, the prospect of large-scale customization gradually is carried out in best practices, which is outstanding case to resolve problems effectively. The experience can be the groundwork when constructing correlated field of knowledge (Laudon & Laudon, 2002, p. 373). However, the intension of EC, customer relationship management, is not as much concerned as producing or channel orientation in the past. 3.1 Exploration of EC/CRM Strategy The researches about EC/CRM are not very abundant. Therefore there still has disagreement in its definition (Dyche, 2001, p. xix; SCN Education B.V., 2001, pp. 23-26). Researchers have studied it from the aspect of function (Dyche, 2001), operation (Brwon, 2000), technology (Swift, 2001) or case study (Rosenoer, Armstrong, & Gates, 1999), but they have seldom explored it from an enterprise-wide perspective or strategic aspect. This research is an exploratory one (Emory, 1976, pp. 83-86; Yin, 1989) which is employed the literature of CRM and EC, the case study review of successful banking industry in the United States and Europe and based on the view of CRM to conclude the -6-.

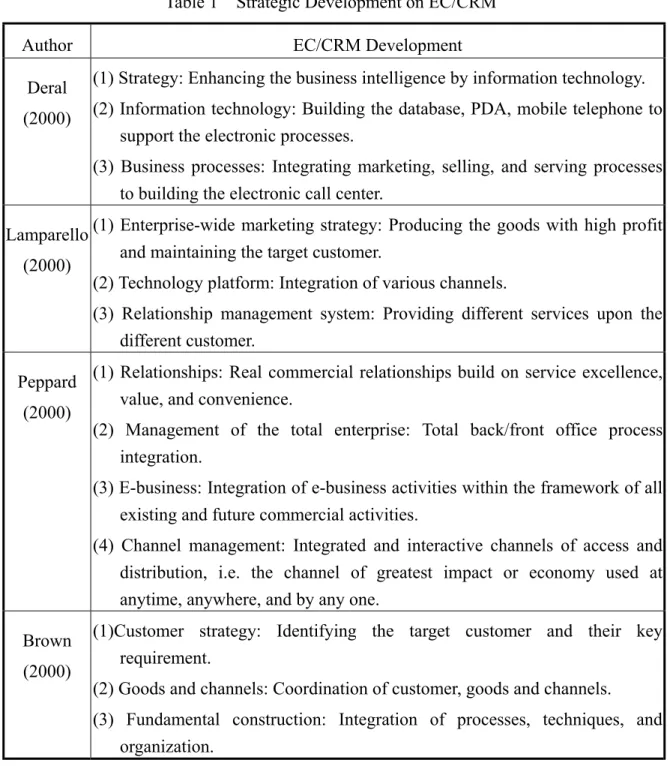

(7) strategies and achievements of EC and the theory of strategic viewpoint from CRM. Then puzzled out the theoretical strategic structure for the based of following study. 3.2 Contents of EC/CRM Strategy The purpose of CRM is to construct the electronic enterprise providing personal services with three levels—strategy, information technology and business processes (Deral, 2000). The report of investigating the profit of American banking (Lamparello, 2000) discovered that the banks adopted customer-oriented strategy will get higher profit and pointed out that CRM will involve in enterprise-wide marketing strategy, technology platform and relationship management system. Otherwise, the study focused on the CRM and EC issues of financial institutions studied it from the enterprise–wide perspective discussed with four parts (Peppard, 2000). Unlike other investigation, this study was especially emphasized the importance of the integration of channels and front/back office systems. Furthermore, the significance of the integration of processes, techniques, organization and 3W (Web, Work flow management and data Warehousing) was mentioned by Brown (2000). From the researches given above, information technology, channel management, processes integration are the basic parts of CRM strategy. The value of financial services bring is from the processes of services and the interactive connection among the strategies, services, systems, and customer evaluation Melnick et al. (2000, chap.1). If organization wants to let all parts connect tightly and run smoothly, all the dimensions of strategy should be based on the operational processes to integrate all the data (like customer data, the connection data between customer and company, the internal function data of company, the data of collaboration, the data from front/back systems) from the customer-centric viewpoint (Kolakota & Robinson, 1999, p. 122).. -7-.

(8) Table 1. Strategic Development on EC/CRM. Author Deral (2000). EC/CRM Development (1) Strategy: Enhancing the business intelligence by information technology. (2) Information technology: Building the database, PDA, mobile telephone to support the electronic processes. (3) Business processes: Integrating marketing, selling, and serving processes to building the electronic call center.. Lamparello (2000). (1) Enterprise-wide marketing strategy: Producing the goods with high profit and maintaining the target customer. (2) Technology platform: Integration of various channels. (3) Relationship management system: Providing different services upon the different customer.. Peppard (2000). (1) Relationships: Real commercial relationships build on service excellence, value, and convenience. (2) Management of the total enterprise: Total back/front office process integration. (3) E-business: Integration of e-business activities within the framework of all existing and future commercial activities. (4) Channel management: Integrated and interactive channels of access and distribution, i.e. the channel of greatest impact or economy used at anytime, anywhere, and by any one.. Brown (2000). (1)Customer strategy: Identifying the target customer and their key requirement. (2) Goods and channels: Coordination of customer, goods and channels. (3) Fundamental construction: Integration of processes, techniques, and organization.. This research will be divided into four parts. First, in “Channel management”, we discuss the customer relationship management how to contact customers and provide them goods with the channels. Subsequently, in "Customer data management”, the enterprise-database collects and integrates the data from front-ends (data of customer activities with channel) and back-ends (data of internal part in enterprise and external part with collaboration). By the process, enterprise could analyze its situation and make its strategy precisely with the information extracted from the data. This part is so crucial. However, it is neglected in the -8-.

(9) literature (Table 1). The key of CRM success is transforming the raw data from customer-ends into the useful information in order to increase the customer loyalty and company profit (Agarwal and Chisholm, 2000). Third, the activities of channel management or customer data management should be guided with the strategic goal of customer-focused to integrate the systems between front-end and back-end; make use of data from customer; convert the data into the information helpful for improving customer relationship. These actions are involved in the enterprise-wide perspective and re-engineer of business processes, which is mentioned in “Enterprise-wide strategy” in our study. All the contents above are based on the information technology that makes the activities operate efficiently in three dimensions, and all the technologies about the establishment and integration of channels, the management of customer data, and the integration of front/back offices will be discussed in “Information technology”. Four dimensions are developed and provide a guide to increase the electronic commercial events through enhancing customer relationship. Furthermore, some operational activities are categorized into each dimension to stress the EC development.. 4. The Best Practices on EC/CRM Banking industries in the United States and Europe have outstanding performance on EC (Seybold & Marshak, 1998; Peppard, 2000). Well-known banks such as Wells Fargo, Wachovia, and Bank One in American, Royal Bank of Canada in Canada, and Merita-Nordbanken in Finland (Seybold & Marshak, 1998; Rosenoer, Armstrong, & Gates, 1999; Brown-Humes, 2000; Formant, 2000; Gandy, 2000; George, 2000; Huff, et al., 2000; Swift, 2001, p. 347; Laudon & Laudon, 2002, p. 412; Turban, et al., 2002, pp. 147, 411) are viewed as business models in this paper.. The banking events, practices,. applications, and news on CRM are retrieved from the databases of the United Daily News, LEXIS-NEXIS: Academic Universe, ProQuest, and EBSCOhost to rule out critical issues on developing EC/CRM, shown in Table 2.. Even though some activities in. the other banks were reported, their details are also covered in Table 2. -9-.

(10) Table 2 Dimension. Wells Fargo. Critical EC/CRM Activities in Leading Banks Wachovia. Bank One. -Omnifarious services -Secure transaction environment Channel Management -One stop shot -Updating the service when the needs change -Improve the convince of channels -Building call center to integrate the channels -Putting the customer’s benefits first Enterprise -Establishing the interactive devices -Wide -Redefining the Strategy business goal, rules and objects -Constructing the extensive technology -Integrating the customer data and systems -Integrating in customer centric -Segment of customer -Analysis the profit of each segment Customer -Expanding the group Data Management on Internet -Grasping the high-profit customer -Collecting the customer data automatically with their bills. -Recognizing the customers’ preference of channels -Offering differential channels depend on the level of customer -Integrating channels dynamically -Closing the old branches -Centric call center -Reviewing the relationship between organization and customer in an entire perspective -Designing the operational process from the view of customer -Improving the business processes related to customer -Putting the benefit of customer first. -Endeavoring to develop the electronic channels -Offering differential services upon the characteristics of customer. -Constructing the objects model with the Information same base Technology -Integrating the data from different systems with object agent -Developing Customer Information Viewpoint (CIV). -Providing the tools to sift the customer -Developing integrative customer knowledge systems, PRO, to assist decision making -Building the data warehousing. -Segment customer with the potential profit they bring -Evaluating the existing/potential profit with the establishment of criterion, model, and systems -Finding out the customer’s personnel needs to offer personnel service. Royal Bank Of Canada. Merita -Nordbanken. -Believing the -Developing a variety development of of Mobile channels channels is very -Improving the speed important of CRM of transactions -Improving the quality of channels continuously. -Building the virtual -Integrating the enterprise by opinions of the strategy alliance technical staff and -Offering multiple the user brands - Automatic -Putting quality first operation -Integrating all the devices with event-driven value -Putting the development of EC first. -Redefining the business goal, rules and objects to integrate the systems -Participating actively in the innovation and application of technology -The WAP is the core of occupational activities -Emphasizing on the long term profit of the invest of technology -Examine on the -Narrowing the unit -Attaching customer needs of customer of customer with the mobile proactively and segment services and creating instantaneously -Establish the the needs of customer -Analyzing the profit devices of -Integrating the and preference of all evaluating the customer data across the segment of existing/potential the function and customer value of customer department -Assisting customer -Offering personnel to find put the service and advice financial service suitable for them -Offering personnel service and advice -Developing the -Applying packaged -Integrating the related technology software and channels and systems of Internet channels integrating it between front end and -Developing back end with sophisticated technology CRM system -Applying technology -Constructing media such as WAP、Web、 interactive data mart, data technology warehousing, and data -Building the data mining warehousing. 5. The Content of EC/CRM Strategy Some activities and technology used in each strategy are identified and discussed in this section. -10-.

(11) 5.1 Channel Management The establishment of the customer-centric channels could be discussed with three parts--- to build a convenient way for customer (Seybold & Marshak, 1998), to utilize various channels (Chilcott, 2001), and to integrate all the channels (Chilcott, 2001). Banking should build various channels, such as branch, call center, ATM (automatic teller machine), IVR (interactive voice response), iBanking (internet banking), PCBanking (personnel computer banking), FEDI (financial electronic data interchange), PDA (personnel digital assistant), digital net-meeting, website, Kiosk, telephone (Cable, GSM, WAP) and so on, to connect customer and then improve the convenience of all the channels. The critical channels in the future will be the Internet and mobile telephone. Each channel has its own characteristic and advantage, so that there are differences between the services each channel could provide (Peppard, 2000; Chilcott, 2001). Bank should recognize and utilize the special advantage of each channel. The integration of channels is begun with the integration of customer data. The more consistence of processing customer data between various channels, the more information all channels can share, and the more business resource can be used (Chilcott, 2001). Call center, the major integrated connection point between companies and customers, will be the focal point of EC development in the maturity of Internet (Peppard, 2000). 5.2 Customer Data Management The profit of maintaining existing customer is higher than grabbing a new one (Reichheld & Sasser, 1990). The best way to maintain the existing customer is establishing a closely interactive relation with him. It will be involved in the collection, integration and analysis of customer data (Cyber Dialogue, 2000). Organization has to collect and integrate various sources of customer data such as the customer activities from channels, the internal operation data of enterprise, and the external data from collaboration with the database, because enterprise could analyze its situation and make its strategy precisely with the information extracted from these data (Cyber Dialogue, 2000). -11-.

(12) If organization wants to construct and improve the relationship with existing customer, it must recognize the preference and behavior model of customer and then satisfy the needs of individual. The purpose of analyzing customer data is to find out the customer’s features, preferences, behavior and needs. The common analyses approach including the analysis of customer value (Wayland & Cole, 1997), customer loyalty (Eloyalty, 2000), balanced relationship (Eloyalty, 2000) and the diversity between customers (Manhattan Consulting Group, 2000). (1) Customer value analysis is to assess the actual value of customer bring to company. (2) Customer loyalty analysis is to evaluate the loyalty of customer by estimating the degree of the customer satisfaction about goods and services. (3) Relationship-balanced analysis is combined with the analysis approach above to identify the target customer. (4) Diversity analysis is to calculate the cost, revenue, and actual contribution of each customer, which is useful to find out the target customer. 5.3 Enterprise-wide Strategy If lacking of integral consideration, it will lead to every results can’t be integrated and fail to elaborate the “synergy” of enterprise. How to convert the data-centric point into customer-centric point is very necessary (Seybold & Marshak, 1998; Peppard, 2000). The extensive consideration is comprised the business strategy based on customer-centric (Seybold & Marshak, 1998, pp. 173~213; Kalakota & Robinson, 1999, pp. 81~108), the integration of front and back systems, and the re-engineer of business processes (Seybold & Marshak, 1998, pp. 33~38; Gartner Group, 2000). Bank should transfer from product-oriented way into customer-oriented way and administrate the customer data to let the every unit (person or department) in the enterprise can use the whole information in the enterprise-wide view (Seybold & Marshak, 1998). The connection activities with customer in the front end can be divided by their function into three parts, sales force automation, marketing automation, and customer -12-.

(13) services and support (Kalakota & Whinston, 1997; Meta Group, 2001). And these customer activities of three parts can be integrated as the customer data of front end. The customer data produced from the enterprise resource reengineering (ERP), supply chain management (SCM) and legacy system are the data of internal operation and external collaboration from the back end (Meta Group, 2001). If organization is unable to integrate the front-end and back-end systems, the problem such as missing data or discordant data (Gartner Group, 2000) will cause damage to enterprise. Enterprises were used to improve the business process in the priority of product selling then customer needs. However, raising the efficiency, though, it can’t increase the profit. Thus, when enterprises optimize the processes, they can consider the needs of customer as the first priority. The increase of transactions will bring more profit than before (Seybold & Marshak, 1998). 5.4 Information Technology The complete CRM framework is activated on the information technology, including the infrastructure and advanced technologies when putting into practices of channel management, customer data management, and enterprise-wide strategy. The technology to channel management including the technology used in the telephone center, such as the automatic call distribution (ACD), interactive voice response (IVR), private branch exchange (PBX) and so forth. Moreover, computer telephony integration (CTI) is another important technology to integrate computer, telephone, fax and Internet (Dearl, 2000; Mandujano, 2000). The collection, integration and analysis of customer data is founded technologically upon the data base management systems including the data mart, data warehousing, data mining and on-line analytical processing (OLAP). The technology related to the integration of massage between frond-end and back-end covers the electronic data interchange (EDI), CORBA, COM/DCOM, Java RMI and other transmission technology with middleware. All the technology above is found upon some basic technology as various -13-.

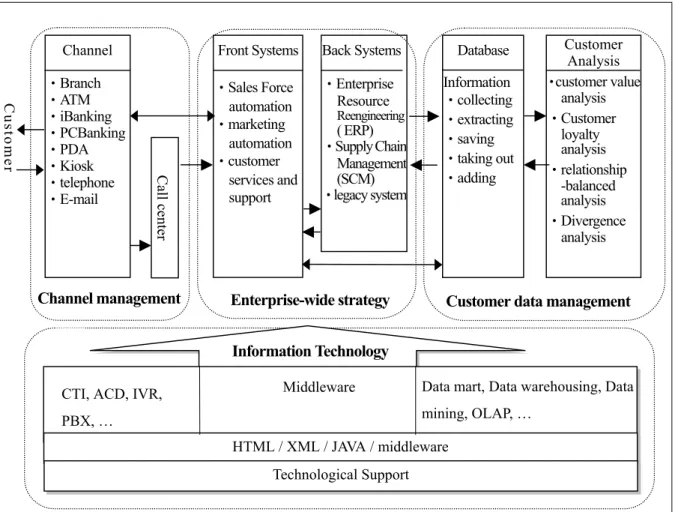

(14) programming language and multimedia language including hyper text markup language (HTML), extensible markup language (XML) and JAVA, which need a middleware to integrate them. 5.5 EC Strategy in the Banking Industry on CRM CRM is focused on customers’ benefit, and the business processes should be reengineering to follow it. And thus, the framework for major activities on each strategy can be illustrated as figure 1.. 6. The Critical Issues on EC/CRM Strategy After puzzling out the four strategies on EC/CRM, the reported critical activities on each strategy in the leading banks (Fargo, Wachovia, Royal Bank of Canada, and Merita-Nordbanken) are retrieved and identified from the databases of LEXIS-NEXIS: Academic Universe, ProQuest, EBSCOhost, and United Daily News. 6.1 The Critical Issues of Channel Management Banking industries should concern the security (Tynan, 2000) and enhance convenience (Tynan, 2000; Wachovia, 2001) of their channels and expand their service items and financial information (Wachovia, 2001) to create a joyful process for customer when they connect to banking by various channels (Merita-Nordbanken, 2001). Banking needs to recognize the characteristics and advantage of each channel (Dearl, 2000; Merita-Nordbanken, 2001) and offer the services suitable to customers by catching on the their preference of channels (Wachovia, 2001). Besides, banking can allocate its resource more efficiently if banking can provide the channels that have different levels of services according to the actual contribution of customer (Wachovia, 2001). In addition, banking ought to integrate all the channels with customer-centric perspective (Peppard, 2000; Royal Bank of Canada, 2001; Wells Fargo, 2001) and build the united way of processing customer data among various channels to unify the data of customer (Wells Fargo, 2001). Finally, banking should endeavor to develop its Internet and mobile telephone system (Merita-Nordbanken, 2001) to capture the blossoming segment of customer. -14-.

(15) Figure 1. EC/CRM Strategy in the Banking Industry. Custo mer. Front Systems. Back Systems. •Branch •ATM •iBanking •PCBanking •PDA •Kiosk •telephone •E-mail. •Sales Force automation •marketing automation •customer services and support. •Enterprise Resource. Call center. Channel. Channel management. Database Information •collecting •extracting •saving •taking out •adding. Reengineering. ( ERP) •Supply Chain Management (SCM) •legacy system. Enterprise-wide strategy. Customer Analysis •customer value analysis •Customer loyalty analysis •relationship -balanced analysis •Divergence analysis. Customer data management. Information Technology CTI, ACD, IVR,. Middleware. Data mart, Data warehousing, Data mining, OLAP, …. PBX, …. HTML / XML / JAVA / middleware Technological Support. 6.2 The Critical Issues of Customer Data Management Banking has to integrate all the customer data it collects and extracts to support the enough information for customer analysis and making decision. Banking can build up the proactive database to update the customer data automatically (Wells Fargo, 2001). It also can segment customer with multi-faceted and interpret the difference (for instance, the profit, cost, preference, loyalty and so on) between the various segments of customer (Bank One 2001; Royal Bank of Canada, 2001; Wells Fargo, 2001). Most banks evaluate the profit customers bring depending upon the current operation data. If they can establish a criterion and systems to estimate the potential revenue of customer, they will recognize the target customer more precise (Wachovia, 2001). Furthermore, the customer analysis based on individual unit must be contributive to offer the personnel service (Royal Bank of Canada, 2001; Wachovia, 2001; Wells Fargo, 2001). -15-.

(16) 6.3 The Critical Issues of Enterprise-Wide Strategy In order to succeed in EC, banking ought to construct a pleasant transactional environment and keep the good relationship to customer to attract new customer and maintain the existing one. What banking has to do is making a business strategy in the customer-centric perspective (Seybold & Marshak, 1998), putting the customer benefits first (Wachovia, 2001), reforming the business processes in the view of customer (Seybold & Marshak, 1998), and integrating all the systems as well as channels (Wachovia, 2001; Wells Fargo, 2001) by uniting the business goal, rules and objects (Wells Fargo, 2001). 6.4 The Critical Issues of Information Technology Banking industry should build sophisticated supportive framework, including HTML, XML, JAVA, Internet, service center, computer telephone integral system and channel integration (Wells Fargo, 2001). Using data mart, data warehousing, data mining and on-line data analysis, found a integral and auto-feedback database. (Merita-Nordbanken, 2001) Afterward, integrate the front end and back end system by the object model having the same foundation (Peppard, 2000). Subsequently, set service as a core, and employ middleware to integrate all applied programs of channel system and front-back end system (Peppard, 2000).. 7. Conclusion The strategy of customer relationship oriented EC is the key point between high-information-intensity banking industries to evaluate whether it is competitive or not. Nevertheless, it lacks more integral conception and framework to implement the subsequent research. This article stands in the viewpoint of customer relationship management to discuss the core of EC and category it into four strategy dimensions, meanwhile, illustrating the inter-relationship by the flow-path of enterprises. According to the successful case, property development, media report of Europe and American banks, to take one step ahead, this research concludes crucial works of every -16-.

(17) dimension, including “channel management”, which needs to establish the customers’ favorite enterprises and integrate these channels, “customer data management”, which completes the royalty analysis, relationship balance and difference assay by collecting, categorizing and analyzing the mutual data of customers, “enterprise-wide strategy”, which creates the customer-cored strategy and integrate the front-end and rear-end system, “information technology”, which introduces and develops the channel management, information management, message management and basic application. Because the manage environment and information construction are not quite the same between overseas and local situations, theses strategy frameworks can be the blueprint for our banking industry to develop EC. The following researches can treat the four EC/CRM strategy dimensions as the basis to investigate the difference between local and foreign banks. Furthermore, the research can be the guide of enterprise transformation and strategy development. In addition, it’s profit to promote the ability and efficiency of EC.. -17-.

(18) REFERENCES [1] Agarwal, R. & Chisholm, M., “US financial services modernization: Legislation + technology = Convergence,” Retrieved from http://www.csc-fs.com/LIBRARY/finmod-dnld.asp, 12/31/2001. [2] Anonymous, “Making strategy, ” The Economist, Vol. 342, No. 8006, 1997, p. 65. [3] Bank One, Retrieved from http://www.bankone.com, 12/31/2001. [4] Berry, L. L., On great service: A framework for action, New York: Free Press, 1995. [5] Bielski, L., “E-business models stress putting the customer first,” ABA Banking Journal, Vol. 92, No. 7, 2000, pp. 65-71. [6] Brown, S. A. (Ed.), Customer relationship management: A strategic imperative world of e-Business, Toronto: John Wiley & Sons Canada, 2000. [7] Brown-Humes, C., “Clients engaged in revolution: Internet banking,” Financial Times (London), July 10, 2000, p. 6. [8] Chen, J. X.; Chen, J. L.; Chen, Z. Z., Xu, Q.Y., & Liu, W. Z., The current situation and future for domestic EC market, Taipei: Market Intelligence Center of Institution for Information Industry, 2001. [9] Chen, Z. Z., Xu, Q.Y., Huang, S. Q, & Jiang, P. W., The electronic application and the future of domestic business, Taipei: Market Intelligence Center of Institution for Information Industry, 2001. [10] Chilcott, M., “Interactive retailing for the new economy customer-centric, multi-channel retailing,” Retrieved from http://www.proxicom.com, 12/31/2001. [11] Coffey, J. O., “The road to CRM nirvana,” Bank Systems & Technology, Vol. 38, No. 7, 2001, pp. 34-38. [12] Cyber Dialogue, Building customer relationships through analytical eCRM, New York: Cyber Dialogue, 2000. [13] Deral, “The framework and concept of CRM,” Retrieved from http://www.nii.org.tw/cnt/ECNews/Article/article_27.htm, 12/31/2001. [14] Dyche, J., The CRM handbook, Reading, MA: Addison-Wesley, 2001. [15] Eloyalty, “Customer loyalty: Deconstructing satisfaction,” Retrieved from http://www.eloyaltyco.com/journal/index.html, 12/31/2001. [16] Emory, C.W., Business research methods, Homewood, IL: Richard D. Irwin, 1976. [17]Formant, C., “Customer acquisition and CRM: A financial services perspective,” in S. A., Brown (Ed.), Customer relationship management: A strategic imperative in the world of e-Business, Toronto: John Wiley & Sons, 2000, pp. 87~106. [18] Gandy, A., Banking strategies and beyond 2000, New York: AMACOM, 2000. [19] Gartner Group, Industry forecast and growth factors: Online banking and electronic bill payment, Stamford, CT: Gartner Group, 2000. [20] George, N., “Nordic banks focus on Web strategies,” Financial Times (London), April 12, 2000, p. 34. [21] Griffin, J., Customer loyalty: How to earn it, how to keep it, New York: Lexington, 1995. [22] Hong, Y. X., The framework and practices of CRM systems, Taipei: Market Intelligence Center of Institution for Information Industry, 2001. [23] Huff, S. L., Wade, M., Parent, M., Schneberger, S., & Newson, P., Cases in electronic commerce, Boston, MA: McGraw-Hill, 2000. [24] Kalakota, R. & Robinson, M., E-business: Roadmap for success, Reading, MA: Addison-Wesley, 1999. [25] Kalakota, R. & Whinston, A. B., Electronic commerce: A manager's guide, MA: Addision-Wesley, 1997. [26] Lamparello, D., “Doing more for the right customers,” Bank Systems and Technology, Vol. 37, No. 1, 2000, pp. R10-R11. -18-.

(19) [27] Laudon, K.C. & Laudon, J. P., Management information systems: Managing the digital firm, Upper Saddle River, NJ: Prentice-Hall, 2002. [28] Mandujano, M., “The Latin American CRM banks,” Bank Technology News, Vol. 13, No. 11, 2000, pp. 51-55. [29] Manhattan Consulting Group, “Average doesn't win,” ABA Banking Journal, Vol. 37, No. 4, 2000, pp. 57-63. [30] Melnick, E. L., Nayyar, P. R., Pinedo, M. L., & Seshadri, S. (Eds.), Creating value in financial services: Strategies, operations and technologies, Norwell, MA: Kluwer Academic Publisher, 2000. [31] Merita-Nordbanken, Retrieved from http://www.meritanordbanken.com, 12/31/2001. [32] Meta Group, “Web design/integration crucial in CRM strategy,” Retrieved from http://www.advisor.com/Articles.nsf/aid/SmiTT171, 2001/03/29. [33] MicroStategy, “eCRM- A technology-based marketing phenomenon remember Norman Rockwell,” Retrieved from http://www.microstrategy.com/download/files/whitepappers/ecm12.pdf, 12/31/2001. [34] Murphy, T., Web rules: How the Internet is changing the way consumers make choices, Chicago, IL: Dearborn, 2000. [35] Peppard, J., “Customer relationship management in financial services,” European Management Journal, Vol. 18, No. 3, 2000, pp. 312-327. [36] Peppers, D. & Rogers, M., The one to one future: Building relationships one customer at a time, New York: Doubleday, 1993. [37] Porter, M. E. & Miller, V. E., “How information gives you competitive advantage,” Harvard Business Review, July-August, 1985, pp. 149-160. [38] Reichheld, F. F. & Sasser, W. E., “Zero defections: Quality comes to services,” Harvard Business Review, No. 68, No. 5, 1990, pp. 105-111. [39] Rosenoer, Armstrong & Gates, The clickable corporation: Successful strategies for capturing the Internet advantage, Chicago, IL: Arthur Andersen LLP, 1999. [40] Royal Bank of Canada, Retrieved from http://www.royalbank.com, 12/31/2001. [41] SCN Education B.V. (Ed.), Customer relationship management: The ultimate guide to the efficient use of CRM, Wiesbaden, Germany: Vieweg, 2001. [42] Seybold, P. B. & Marshak, R. T., Customer.com: How to create a profitable business strategies for the Internet and beyond, New York: Random House, 1998. [43] Shi, B. Y., “ The report of the application of customer relationship management in Taiwan, ” e-Business executive report, Taipei: ARC Consultants, 1999, pp. 9-15. [44] Swift, R. S., Accelerating customer relationships: Using CRM and relationship technologies, Upper Saddle River, NJ: Prentice Hall, 2001. [45] Tong, Q. S., The information development and the future in local banking industry, Taipei: Market Intelligence Center of Institution for Information Industry, 2000. [46] Turban, E., King, D., Lee, J., Warkentin, M., & Chung, H. M., Electronic commerce: A managerial perspective, Upper Saddle River, NJ: Prentice-Hall, 2002. [47] Tynan, T. G., “Web adds pressure for CRM,” American Banker, Vol. 165, No. 77, 2000, pp. 6-7. [48] Wachovia, Retrieved from http://www.wachovia.com, 12/31/2001. [49] Wayland, R. E. & Cole, P. M., Customer connections: New strategies for growth, Boston, MA: Harvard Business School Press, 1997. [50] Wells Fargo, Retrieved from http://www.wellsfargo.com, 12/31/2001. [51] Yang, L. J., “The worst year of finance in Taiwan, ” Business Weekly, Vol. 705, 2001, pp.74-81. [52] Yin R. K., Case study research: Design and methods, London: Sage, 1989.. -19-.

(20)

數據

相關文件

The Service Provider Switching Model SPSM: A Model of Consumer Switching Behavior in the Services Industry. „Migrating‟ to New

We propose a primal-dual continuation approach for the capacitated multi- facility Weber problem (CMFWP) based on its nonlinear second-order cone program (SOCP) reformulation.. The

• When a call is exercised, the holder pays the strike price in exchange for the stock.. • When a put is exercised, the holder receives from the writer the strike price in exchange

• When a call is exercised, the holder pays the strike price in exchange for the stock.. • When a put is exercised, the holder receives from the writer the strike price in exchange

• developing coherent short-term and long-term school development plan that aligns the school aims, the needs, interests and abilities of students in accordance with the

Experiment a little with the Hello program. It will say that it has no clue what you mean by ouch. The exact wording of the error message is dependent on the compiler, but it might

Peppard, J., “Customer Relationship Management (CRM) in Financial Services”, European Management Journal, Vol. H., "An Empirical Investigation of the Factors Influencing the

Internal service Quality, Customer and Job Satisfaction: Linkages and Implications for Management.. Putting the Service-Profit Chain