行政院國家科學委員會

獎勵人文與社會科學領域博士候選人撰寫博士論文

成果報告

訊息影響碳權排放津貼之遞延效果:歐盟排放貿易計畫實證

分析與選擇權定價

核 定 編 號 : NSC 100-2420-H-004-032-DR 獎 勵 期 間 : 100 年 08 月 01 日至 101 年 07 月 31 日 執 行 單 位 : 國立政治大學金融系 指 導 教 授 : 林士貴 博 士 生 : 李章益 公 開 資 訊 : 1.公開資訊:本計畫涉及專利或其他智慧財產權,1 年後可公 開查詢中 華 民 國 103 年 02 月 13 日

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

國立政治大學商學院金融學系

博士論文

在馬可夫狀態轉換市場下之

選擇權定價

:雙重

Esscher

transform 下馬可夫可調控高斯 HJM 模型

Valuation Of Options In A Markovian Regime-Switching

Market : Markov-Modulated Gaussian HJM Model by

Double Esscher transform

指導教授: 陳松男、江彌修 博士

研究生:李章益 撰

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

Valuation Of Options In A Markovian Regime-Switching

Market : Markov-Modulated Gaussian HJM Model by

Double Esscher transform

Ph.D. Dissertation

Submitted to the Graduate Faculty of National Chengchi University and Department of Money and Banking in Fulfillment of the Requirements for the

Degree of Doctor of Philosophy

in

Department of Money and Banking

National Chengchi University

Advisors: Dr. Son-Nan Chen Dr. Mi-Hsiu Chiang

by Chang-Yi Li

Taipei, Taiwan, Republic of China

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

謝 辭

首先誠摯的感謝指導教授陳松男老師,陳老師悉心的教導使我得以一窺金融領域 的深澳,不時的討論並指點我正確的方向,使我在這些年中獲益匪淺。陳老師對 學問的嚴謹更是我輩學習的典範。 感謝口試委員陳松男老師、江彌修老師、徐保鵬學姊、蔡恆修老師及謝明華 老師,由於老師們的指導與建議,使得我的博士論文能更臻完善。 在進入博士班就讀之初,因為從未接觸過任何一門有關財經或經濟的課程, 因此剛開始學習時徬徨無助,但感謝眾位老師的醍醐灌頂、學長姐的加油提攜、 同學的共同砥礪、學弟的相互幫忙使七年的博士班生涯活變得絢麗多彩,其中感 謝廖四郎老師、江彌修老師、林士貴老師,總能在我迷惘時為我解惑,徐保鵬學 姊、蔡宏彬、吳庭斌、周奇勳學長及湯美玲學姊等不厭其煩的指出我研究中的缺 失;感謝連育民學長、陳俊洪學弟、盧淑惠及楊啟鈞同學,你們的幫忙我銘感在 心。 「畢業並非人生的終點,而是另外一種挑戰的開始」,在未來的學術生涯裡, 我將秉持嚴謹的態度,不斷充實自己。 最後,感謝一路走來一直在我身邊支持我的家人及親人、讓我在最辛苦的時 候有所依靠,在本論文完成之屆甚懷念雙親 李德志先生與李陳富美女士養育之 鴻恩,謹以此論文獻給我摯愛的雙親、永懷雙親。 李章益 于政大 民國一零二年九月‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

i論文摘要

有越來越多的學術研究顯示,在著名的 Black-Scholes 金融市場下幾何布朗運動 並不能描述一些標的資產價數據中,比如標的資產的報酬的分布有厚尾、偏斜、 及波動叢聚的現象,而馬可夫可調控狀態轉換的金融保險模型似乎比相對於經典 的金融保險模型而言,更能貼近現實中的金融數據。在風險的觀點中,馬可夫可 調控的模型有這樣一個優點: 此模型可以隨外界環境 (經濟體的好壞、政府的政 策等) 改變自身模型的風險,使得證劵公司進而可以調整自身的政策。 另外一方面,在傳統上 Esscher transform 的測度轉換架構下,無法有足夠 的自由度(解集合)使得在馬可夫可調控的狀態轉換過程下之資產動態達到平睹過 程的條件,因此本篇論文也致力於發展雙重 Esscher transform 的轉換技巧,使得 標的資產可以使用兩種不同的馬可夫鍊容納吸收來自經濟體雙重影響。 關鍵字: 歐式選擇權,Esscher transform,馬可夫鏈,馬可夫可調控的卜瓦松 過程,波動叢聚‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

iiAbstract

The celebrated Black-Scholes financial market is based on a geometric Brownian motion to capture the price dynamics of underlying assets. However, a lot of academic studies reveal that this assumption for assets price dynamics cannot provide realistic description for some important empirical behavior of financial returns such as a kurtosis, a skewness, and volatilities clustering the return’s distribution. Compared with the classical risk model or finance model, the Markov-modulated model or Markovian regime-switching model can provide a better fit to the reality data of insurance and finance. In risk or financial theory, regime-switching risk under Markov-modulated process can capture the feature such that changed environment, such as economic growth or recession, government political, which helps the insurance policies of insurance companies to change their policies.

On the other hand, classical Esscher transform cannot provide sufficient degree of freedom, which is solution of set, such that the underlying assets under Markov-modulated regime-switching process are a martingale process. Hence, this paper is also devoted to considering the mythology of double Esscher transform which accommodate two different Markov chain capturing different effects on economics.

Keywords: European options, Esscher transform, Markov-modulated Poisson process, volatilities clustering.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

iii Contents Abstract ... ii Chapter 1 Introduction ... 1Chapter 2 Valuation Of Quanto Options In A Markovian Regime-Switching Market: A Markov-Modulated Gaussian HJM Model ... 5

2.1 Introduction ... 5

2.2 Regime-switching model ... 7

2.3 Risk-neutral Martingale measure via Esscher transform ... 10

2.4 Valuation of European quanto options ... 13

2.5 Conclusions ... 19

Chapter 3 Valuation Of Currency Options Under A Regime-Switching Gaussian HJM Model ... 20

3.1 Introduction ... 20

3.2 Econometric analysis of spot-FX rate markets ... 23

3.3 Econometric analysis of yields and bond market via RSBM ... 35

3.4 European currency options ... 42

3.5 Empirical study and numerical illustration ... 51

3.6 Conclusions ... 57

Chapter 4 Conclusions ... 59

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

ivChange of parameters under new measure ... 60

Appendix B of Chapter 2 ... 63

Lemma B ... 63

Case1: Options struck in a foreign currency ... 63

Case 2: A foreign equity call stuck in domestic currency ... 64

Case3: A guaranteed-exchange rate foreign equity call option ... 65

Case 4: An equity-linked foreign exchange call ... 67

Appendix A of Chapter 3 ... 70

Appendix B of Chapter 3 ... 74

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

vList of Tables

Table 1: Statistics Of The GBP/USD Spot-FX Rate Returns Starts Form 1

January, 1990 to 30 December, 2011. ... 27

Table2: Estimated Parameters of The BSM, The JDM And The RSJD In The

GBP/USD Spot-FX , The 100JPY/USD and The EUR/USD Spot- FX ... 32

Table 3: Estimated Parameters Of Interest Rates Under Regime-Switching

Brownian Motion. ... 37

Table4 : The Collected Options Prices Under The RSBM Model With

Constant Drift ... 51

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

viList of Figures

Figure 1: The daily data for the GBP/USD spot-FX rate starts form 1 January,

1990 to 30 December, 2011. ... 25

Figure 2: The daily data of U.K. and U.S. Zero-coupon yields with maturity

of 1 year starting form from 3 January, 2000 to 30 December 2011. . 39

Figure 3 The call option prices against spot-to-strike staring from 0.7 to 1.3

for T 1 year. ... 54

Figure 4: The call-option prices of the market data and the calibrated prices

( )

R

C t . ( The circles represent market prices, and the pluses denote

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

1Chapter 1

Introduction

The classical compound Poisson risk model is broadly known as the classical jump

diffusion model proposed by Merton (1976). In this model claim arrivals as well as

claim sizes are homogemeous in time. However a lot of feature, for example the

interest rates where macroeconomic condition plays a major role in the financial

market ( see Hamilton, J.D., (1989), Garcia and Perron (1996), Evans (1998), and

Bansal and Zhou (2002)). Since it turns out unrealistic use it to model economic grow

and recession, Markov-modulated risk model such as Markov-modulated compound

Poisson risk model, has become more and more popular over the last decades. The

Markov-modulated risk model can capture the feature that underlying assets return

need to change if the environment, such as weather condition economical or political

environment, etc, changes. For instance, in the Markov-modulated compound Poisson

risk model claim size distribution and the intensity of the claim arrival process are

modulated by an irreducible Markov chain with finite state space, and Markov chain

can be seen to describe the change in macro-economic conditions, the changes in

political regime, the impact of economic news and business cycles, etc.

The Markov-modulated risk model in options is first introduced by Naik (1993).

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

2Zhang et al. (2012), abd Shen et al. (2013) devote to develop regime-switching option

pricing with Markov chain. Naik (1993) provides an elegant treatment for the pricing

of the European option under a regime-switching model with two regimes. Elliot et al

(2005) provide a quasi explicit price formula corresponding geometric Brownian

motion by occupation time. Mamon and Rodrigo (2005) obtain the explicit solution to

European options in regime-switching economy by considering the solution of PDEs.

Elliott et al (2007) study the price of European option and American option under a

Generalized Esscher transform and a set of coupled partial-differential-integral

equations. Siu et al. (2008) study the price of European option and American option of

spot foreign exchange rate under a two-factor Markov-modulated stochastic volatility

model, and he also considers the option pricing problem in a game theoretical

approach which is found to be consistent with the result of regime-switching Esscher

transform.

However, one important feature for regime-switching pricing options is that the

market is incomplete[ 1 ] and thus, pricing the regime-switching risk becomes a challenge issue . Guo (2001) introduces a set of change-of-state contracts to complete

the market. Then by using the martingale representation technique of double

martingale introduced by Elliott (1976). Shen et al. (2013) show the price of options

1

The no arbitrage price of the derivative security is not unique. For more details see Elliot and Swishchuk (2007)

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

3can also be obtained Markovian jump proposed by Zhang et al. (2012) to fixing risk

premium under unique Esscher transform. Hence, we want to find a method to

complete the Markovian regime-switching market with two-kind Markov chain and

study the results of double Esscher transform to complete market. The idea of

completing the Markovian regime-switching is inspired by Elloitt (1976), Gerber and

Shiu (1994), and Bo et al. (2010). We also devote regime-switching jump diffusion

model by Markovian-modulated different jump intensity and adopt the double Esscher

transform corresponding two-kind HJM to price regime-switching options.

In Chapter 2, we consider the valuation of European quanto call options in an

incomplete market where the domestic and foreign forward interest rates are allowed

to exhibit regime shifts under the Heath-Jarrow-Morton (HJM) framework, and the

foreign price dynamics is exogenously driven by a regime switching jump-diffusion

model with Markov-modulated Poisson processes. We derive closed-form solutions

for four different types of quanto call options, which include: options struck in a

foreign currency, a foreign equity call struck in domestic currency, a foreign equity

call option with a guaranteed exchange rate, and an equity-linked foreign

exchange-rate call. In Chapter 3, spot foreign exchange (FX) rates usually exhibit

jumps and regime switching in a finite number of states due to change in

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

4model proposed in this paper is modeled by a Markovian system that is capable of

capturing the feature of the dynamic spot-FX rate. We also examine term-structure

data to show that the regime-switching of forward interest rates is distinct from that of

the spot-FX rate, and thereby leading to different associated impacts (or

regime-switching impacts). Hence, a regime-switching Gaussian

Heath-Jarrow-Morton (HJM, (1992)) model is introduced via another Markov chain.

The RSJD model is used along with the forward Esscher-transform technique for the

arbitrage-free condition with which European currency call options are priced under

the Markov-modulated Gaussian HJM model (MMHJM). Empirical study shows that

the RSJD model combined with the MMHJM model is a more complete and

appropriate model for pricing currency options, and the regime-switching impacts of

the spot-FX rate and forward interest rates should be properly taken into account. In

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

5Chapter 2

Valuation Of Quanto Options In A

Markovian Regime-Switching Market: A

Markov-Modulated Gaussian HJM Model

2.1 Introduction

Recent works that consider alternative option pricing models have progressed in

various directions: Zumback (2012) explores the valuation of options when

discrete-time ARCH processes drive the underlying asset prices; Xu et al. (2012) price

vulnerable options under a continuous-time jump-diffusion setting; Hsu and Chen

(2012) investigate the valuation of exchange-rate barrier options when interest rates

are driven by a Lévy process. In view of incorporating the regime switching feature

into the pricing model, Hamilton (1989) provides empirical evidence of business

cycles under a regime-shift model of hidden Markov chain, Elliott et al. (2003)

propose a regime-switching Brownian motion model with a Markov-modulated

system that captures the volatilities-clustering feature. Simonato (2011), on the other

hand, computes American option prices under a lognormal jump-diffusion setting

based on a numerical approach.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

6based on the Markov-modulated HJM (MMHJM) model of Valchev (2004) for

interest rates, and the other via the regime switching jump-diffusion model (RSJD) for

foreign stock prices. Existing literature that incorporates either discrete or continuous

regime-shifts in model parameters includes Bansal and Zhou (2002), who develop a

term structure model in which the short rates and the market price of risk are subject

to discrete-time regime shifts, and Zhu (2011), who shows that regime shifts are able

to explain the predictability of excess returns.

When a financial market is incomplete, the pricing measure is not unique. In

order to identify a risk-neutral measure for derivatives pricing under an incomplete

market, Gerber and Shiu (1994) propose the Esscher transform approach that

characterizes the risk-neutral measure by moment-generation functions, and Husmann

and Todorova (2011) apply the equilibrium approach of Jarrow and Madan (1997) to

the case of an incomplete lognormal market. In this paper, we adopt the

regime-switching Esscher transform proposed by that Elliott et al. (2005) to identify

the risk-neutral measure under which quanto call options can be priced.

Other approaches for options pricing that consider the presence of different

sources of risk, such as liquidity and credit, are also worth noting. Sample works in

this category include Ku et al. (2012), where the valuation framework of Leland

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

7under an incomplete-market setting when liquidity risk is present; Jarrow (2011), on

the other hand, argues that asymmetric information structure in fact plays an

important role in the determination of credit market equilibrium, and hence affects the

capital structure of a firm.

Subsequent parts of this article are organized as follows: In Section II, while the

domestic and foreign forward interest rates are modeled by a MMHJM model, the

exchange rate is assumed to follow a geometric Brownian motion, and the foreign

stock prices are specified by a RSJD model. In section III, we use the

regime-switching Esscher transform to construct a risk-neutral martingale measure. In

section IV, we derive closed-form solutions for four types of quanto options. The final

section concludes our research findings.

2.2 Regime-switching model

In this section, we first specify the MMHJM model for the domestic and the foreign

forward interest rates, and we also specify the RSJD model that the foreign stock

prices are assumed to follow.

2.2.1 Specifications of Markov chains

According to Elliott et al. (2005)[2], we assume that the state space of Markov chain

2

Elliott et al. (2005) also establish the occupation time of the moment generating function for Markov chain .

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

8 is a set of two states:

2 1, (1,0),(0,1)2I e e , which implies respectively, a

boom or a recession (good or bad time) for the state of economy. A continuous-time Markov chain has the transition matrix given as below:

11 11 22 22 ( ) 1 ( ) ( ) 1 ( ) ( ) p t p t t p t p t P . (2.2.1)

A Markov-Modulated Poisson Process (MMPP), ( )t , represents a particular class of doubly-stochastic Poisson processes where the jump intensity is modulated by a Markov chain ( )t . In particular, we consider a set of nonnegative numbers

1, 2

, where i, 1, i 2, denotes the intensity of the Poisson process when aMarkov chain ( )t is at state ei at time t, i.e.,

i ( ,

1 2)ei where the dot ( ) denotes the scalar product. ( )t and ( )t can be defined by the joint probability,( , )

ijn t

( ( )t n, (0) ei, ( ) t ej). The moment-generating function of thejoint probability admits a unique solution ( , )u t such that, ( , )u t

0 ( , ) n n n t u

(1 u)

t exp Ψ Λ , where Λ represents the intensity matrix 1

2 0 0 (cf.

Last and Brandt (1995)). The numerical method for computing ij( , )n t can be found

in Abate and Whitt (1992).

2.2.2 Regime-switching HJM model for the forward interest rates

Let the regime-switching feature of interest rates be represented by a Markov chain

f

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

9 space

,

(1, 0), (0,1)

f g hI e e . We use the following notations for the Markov-modulated parameters in the HJM model:

t T, , ( )f t

1( , ), ( , )t T 2 t T

f( )t and

t T, , ( )f t

v

v1,1 t T, , v1,2 t T, ( ), , f t v2,1 t T , v2,2 t T, ( ), , f t v3,1 t T , v3,2 t T, ( )f t

,(2.2.2)where

vm,1

t T, ,

vm,2

t T,

, m1, 2,and 3, represent, respectively, the volatility structures of short-, mid- and long-term interest rates.Following Valchev (2004), the dynamics of forward rates formulated by the MMHJM

model under the physical measure is given by:

, , ( )

, , ( )

, , ( )

( ),k f k f k f k

df t T t t T t v t T t dW t (2.2.3)

where Wk( )t nis a standard Brownian motion, k

D F,

denotes, respectively, a domestic or a foreign country.The domestic and the foreign money market accounts are given by:

, ( )

exp

0t

, ( )

,k t f t r uk f u du

k

D F,

, (2.2.4)where r uk

, ( )

u

f u uk

, , ( )

u

is the spot interest rate.2.2.3 Regime-switching jump diffusion model for stock prices and BSM for spot FX

rate

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

10FX. The dynamics of the spot-FX rate under the Black-Scholes framework is given

by:[3] ( ) ( ), (0) 0 ( ) X X D dX t dt d t X X t σ W , (2.2.5)

under the physical measure . Hence the price dynamics of SF( )t under the RSJD

model is found to be:

( ) ( ) exp 1 ( ; ), (0) 0 ( ) F F F F n F F F F dS t dt d t Z d t S S t σ W , (2.2.6)where l an d σl, l

F X,

, are constants, and ( )n k t

W , where k

D F,

, are, respectively, the domestic or the foreign country. A foreign MMPP F( ;t F)isused to model changes in the state of foreign economy. The jump term,

exp Zn 1

dF( ;t F), is a compound Poisson process.Z

n, where n1, 2, 3..., represents a sequence of mutually independent jump sizes. The jump size variableZ

n has a normal distribution with mean

F J, and variance2 ,

F J

. All random

variables are assumed to be mutually independent.

2.3 Risk-neutral Martingale measure via Esscher

transform

In this section, a regime-switching Esscher transform is introduced and applied to the

RSJD model such that the price dynamic process becomes a martingale.

3

We expect that the FX rate should be subject to a (much) weaker regime-switching (RS) impact of the domestic and the foreign interest rates (rDand rF ). By interest rate parity X T( ) /X t( )=

(1rD) /(1rF), the RS effects of the numerator rD and the denominator rF tend to offset with each other, and hence resulting in (much) weaker RS associated with the FX rateX T( ). In addition, by assuming away the RS of the FX rate, we avoid further mathematical complication, and thereby facilitating us to obtain a closed-form pricing model without losing its significance.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

11 2.3.1 Regime-switching Esscher measureThe filtrations of the foreign assets and the spot-FX rate are denoted, respectively, by

F t

S

and

tX . The filtration of hidden Markov chains

F

f is given byf F

T

. The join filtration of the foreign assets (or stocks), the FX rate, the foreign

forward interest rates, and the hidden Markov chain

F

f is denoted by a -algebra given by:

( ) f F SF fk T t t t X t .Two families of regime-switching parameters for the Esscher transform are

denoted, respectively, by θC

u, ( )f u

and J

F( )u

such that ( C,J) ~ on( )t

, and are given as follows:

, ( )

1,1( ), ( )1,2

( ),

2,1( ), ( )2,2

( ),

3,1( ), 3,2( )

( )

C f f C C C f f C C C u u u u u u u u u u u θ θ θ θ θ θ θ , where

( )

1 , 2

( ) J J F J F u

u

t u T T .The foreign regime-switching Esscher transform under the RSJD model takes the

following definition: (cf. Bo et al. 2010)

,( , ) ( ) exp , ( ) ( ) exp ( ) ( ; ) exp ( , ( )) ( ) ( ) exp ( ) ( ; ) ( ) C J T T C J f F F u F F F t t T T C J t f F F u F F t t u u d u u Z d u d d E u u d u t E u Z d u t

θ W θ θ W θ .(2.3.1)‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

12 ,( C, J) F , where the superscript ‘‘F ’’ indicates the foreign measure, is given as

follows: Theorem 1

, , ( )

T F f u u s u ds

1

2 , , ( ) , ( ) 2 C F u T f u F u f u V σ θ

2 2 1 1 , ( ) 2 2 C F u f u F σ θ and

J ( ) 1

J

( )

0 F F u F F u , (2.3.2) where

, , ( )

, , ( )

T F f F f u u T u

u s u ds V σ , 0 u s T T , denotes thenorm in , and n

F( )u Eexp

uZn 2, , 1 exp( ) 2 F J F J u u is the

moment-generating function of the jump size variable.

Proof (See Appendix A) □

Let SFQ F, ( )T be the time

T

foreign-stock process discounted by the foreign money market account (Fin (2.4)) under the foreign martingale measure F,(C*,, *J ) , and the superscript ‘‘Q F, ’’ denotes for the foreign risk-neutral measure.The process SFQ F, ( )T can be represented as follows:

, , ( ) ( ) Q F Q F F F S T S t

1 2 , exp , ( ) ( ) 2 T T T Q F F f F F F t t t r u u du du d u

σ

σ W , , exp ( ; ) T Q F Q F u F F t Z d u

,(2.3.3)where denotes the Euclidean norm, ,

( )

Q F F u

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

13 and Q F, uZ is normally distributed with mean

2 , 1 2F J and variance

F J2, . , ( ; ) Q F F u F therefore admits an new intensity matrix Q F,

F given by: * ,1 , * 2 2 , , 2 , , 2 exp 2 8 ( ) 0 0 ( ) F J F J J F Q F J F F J F F .

In addition, under the risk-neutral measure F,(C*,, *J ), the interest rate in

,

( )

Q F F

S T is modulated by the Markov chain f , while the jump intensities of the

,

( )

Q F F

S T are modulated by the Markov chain

F. Existing empirical studies, such asBansal and Zhou (2002), and Estrella and Hardouvelis (1991), suggest that interest

rates are not only intimately related to business cycles, but also act as economic

leading indicators. In this research we see that the stock-price dynamics are influenced by the effects of regime-switching interest rates via the Markov chain f

associated with the yield curve. This feature is incorporated into the stock-price

dynamics given in (3.3) to capture the changes in economic cycles. This formulation

is also supported by Harvey (1989) who shows that the bond market reveals more

information about future economic growth than the stock market.

2.4 Valuation of European quanto options

Without loss of generality, in the following we shall omit the superscript notation

under the RSJD model for the risk-neutral measure.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

14times of the state of Markov chain f over the option duration

t T . , That is:

2

, , , , 1 , , ( ) , ( ) , ( ) ( , ) T T T i m f i m f i m h h h h t t t V u T u du V u T u du V u T d t T

,where i

D F,

, m1, 2, 3 , and h( ,t T) , h1, 2 , denotes the two-stateoccupation time, and ( 1, 2) denotes the joint probability distribution for the

occupation times

1( , ), ( , )t T

2 t T

, which can be determined by its correspondingmoment-generating function given in Elliott et al. (2005). Therefore, the quanto call

options under study CwRS( ; t f, )n , w =1, 2, 3, 4, depend on the occupation times

and jump number (n).

For simplicity, the price notation CwRS

t; , , 1 2 n ( )t

is replaced by the notation CwRS( ; , )t f n in the pricing models given below. Then, withregime-switching of forward interest rates under the MMHJM model, a European

quanto call option can be expressed in terms of the occupation times given by

Theorem 2: Theorem 2 2 * 1 2 1 2 1 2 0 ( ) F ( , ) ( ; , , ) ( , ) T T RS w i ij w n i t t C t

Q T t n C t

n

d d

, where F i is the stationary state of Markov chain F used as initial value. □ Let

T

be an expiry date of an option and Kk, k

D F,

, be an exercise price.‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

15Four types of quanto call options CwRS( ; , )t f n ,

w

=1, 2, 3, 4, are considered andgiven by the following four corollaries.

As was observed by Reiner (1992), an investor often hedges against the currency

exposure of his/her foreign-stock investments by a large variety of options. In this

following we provide closed-form solutions for four different types of quanto options

that suffice such hedging needs.

Corollary 1: Options struck in a foreign currency

The domestic currency-denominated terminal payoff of a foreign-equity call option

stuck in foreign currency is given by:

1( ) ( ) F( ) F

C T X T S T K ,

where the terminal payoff of a foreign-stock call option is converted into domestic

currency at the spot exchange rate at expiry.

With the risk of jump and regime-switching interest rates, the arbitrage-free price of

this European quanto call option at time t is equal to

1 ( ; , ) ( ) ( ) ( 1,1) ( , , ( )) ( 1,2) RS f F F F f C t n X t S t d K B t T t d , (2.4.1) where ( ) is a cumulative normal distribution function,

2 1, 2 1 , 2 2 1 , 1 ( ) 1 ln( ) ( , , ( )) , , ( ) , , ( ) 2 F f F J F F T t T t f f F J S t K B t T d u T u du n t u T u du n

ζ ζ‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

16

1,2 1,1 2 2 1 , , f( ) F J, T t u u d d

ζ T n ,

1

u T

, ,

f( )

u

σ

F

V

F

u T

, ,

f( ) ,

u

and FK = the strike price in foreign currency.

(Proof: See Appendix B, Case1) □ Corollary 2: A foreign equity call struck in domestic currency

An investor wishes to receive a positive payoff from a foreign equity market, but

would like the underlying foreign stock to be denominated in domestic currency at

expiry. The payoff of this type of European quanto call options at expiry

T

is givenby:

2( ) ( ) F( ) D

C T X T S T K .

Then, with the risk of jump and regime-switching interest rates, the arbitrage-free

price of this type of European quanto-call options at time t is equal to

2 ( ; , ) ( ) ( ) ( 2,1) ( , , ( )) ( 2,2) RS f F D D f C t

n X t S t d K B t T

t d (2.4.2) where

2 2 2 , 2 2 2 2,1 , ( ) ( ) 1 ln( ) ( , , ( )) , , ( ) , , ( 2 ) T F D D t T f F J f t f F J u T u n t X t S t du K B u T u du n t T d

ζ ζ

2,2 2,1 2 2 2 , , f( ) F J, T t u u d d

ζ T n , ζ2

u T, ,f( )u

σF σX VD( , ,u T f( ))u and D‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

17Corollary 3: A foreign equity call option with a guaranteed exchange rate

An investor wishes to capture a positive payoff on his foreign equity investment, but

also desires to eliminate all exchange-rate risk by denominating the foreign payoff in

domestic currency.

The payoff of this type of options at expiry

T

is given by:

3( ) F( ) F

C T S T K ,

where

is the pre-specified exchange rate with which the option’s payoff is converted into domestic currency.With the risk of jump and regime-switching interest rates, the arbitrage-free price of

the call option at time t is equal to

3 ( ; , ) ( , , ( )) RS f D f C t n B t T t

4 3,1 3,2 ( ) exp , , ( ) , , ( ) ( ) ( ) ( , , ( )) T F f F f F F F f t S t u T t u T u du d K d B t T t

V σ (2.4.3) where

4 3,1 2 2 3 , ( ) ln( ) , , ( ) , , ( ) ( , , ( )) , , ( ) T F F f f F F F f t T f F J t S t u T u u T t du K B t T t d u T u du n

ξ V ξ σ

2 2 3 , 2 2 3 , 1 , , ( ) 2 , , ( ) T f F J t T f F J t u T u du n u T u du n

,

2 2 3, 3,2 1 3 , , ( ) , T f F J t d u T u d d

un , and‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

18

4 u T, , f( )u

σX VF

u T, ,f( )u

VD

u T, ,f( )u

3 u T, , f( )u F F u T, , f( )u

σ V

. (Proof: See Appendix B, Case 3) □Corollary 4: An equity-linked foreign exchange-rate call

Finally, an investor wants to hold a foreign stock whose payoff depends on the payoff

of a foreign-exchange call option. The final payoff of this type of quanto options is

given by:

4( ) F( ) ( ) D C T S T X T K .

With the risk of jump and regime-switching interest rates, the arbitrage-free price of

this quanto call option at time t is equal to

4 ( ; , ) ( ) ( ) ( 4,1) RS f F C t n S t X t d

4

4,2 ( , , ) exp ( , , ( )) , , ( ) ( ) ( , , ) T D f D F F f f F f t B t T K u T u u T u dt d B t T

σ V (2.4.4) where d4,1

4 2 4 ( , , ) ( ) ln ( , , ( )) , , ( ) ( , , ) , , ( ) T F f F f F f D D f t T f t B t T X t u T u u T u du K B t T u T u du

V σ

2 4 2 4 1 , , ( ) 2 , , ( ) T f t T f t u T u du u T u du

, 4,2 4,1 4

, , f( )

2 T t u‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

192.5 Conclusions

Through a regime-switching Brownian motion, we introduce regime shifts in the

dynamics of zero-coupon yields under a Markov-Modulated HJM (MMHJM) market.

In addition, the price dynamics of foreign stocks are also allowed to exhibit regime

shifts via the regime-switching jump diffusion (RSJD) setting. We adopt the

regime-switching Esscher transform proposed by Elliott et al. (2005) to construct the

risk-neutral measure under which the prices of quanto call options can be found. Our

research findings include explicit closed-form solutions for four different types of

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

20Chapter 3

Valuation Of Currency Options Under A

Regime-Switching Gaussian HJM Model

3.1 Introduction

Issues related to currency exchange rates are usually very popular topics that have

been extensively studied in macroeconomics and international finance. Its relevant

derivatives have also been extensively examined over the past decades. Pricing

currency options is first investigated by Biger and Hull (1983) and Garman and

Kohlhangen (1983). They model the dynamics of the spot-FX rate by a geometric

Brownian motion (GBM) with a constant drift and volatility, and derive an explicit

valuation formula for the arbitrage-free price of a European currency option under

constant domestic and foreign interest rates. However, Jorion (1988) examines FX

rates and finds that FX rates exhibit different behaviors with jumps in different time

periods. We observe with evidence showing not only jump but also

time-inhomogeneous features of the GBP/USD, the 100JPY/USD and the EUR/USD

spot-FX rates.

Regime-switching models have recently become more important in financial

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

21an exchange rate regime is affected and altered by arrivals of change in

macroeconomic variables, and that currency returns generating process cannot be

characterized by a simple diffusion process. Instead, it should be formulated with a

more complete model such as a jump-diffusion process. Nakatsuma (2000) then

proposes a regime-shift model of daily returns to fit the FX rates of the Asian

currencies which suffered from drastic devaluation during the Asian financial crisis in

1997. He also finds evidence of regime shifts in currency volatility structures. Bollen

et al., (2000) examine the adaptability of regime-switching models for formulating the

dynamics of FX rates, and their analysis suggests that the regime-switching model can

capture the real dynamics of FX rates better than alternative time series models such

as GARCH models. By modeling a regime-switching property, our study provides

evidence indicating that currency returns should be modeled with a regime-switching

jump diffusion (RSJD) model that is embedded with a Markov-modulated Poisson

process (MMPP) to capture an important feature of regime switching found in

currency returns such as the GBP/USD, the 100JPY/USD and the EUR/USD spot-FX

rates.

Stochastic interest rates have been adopted frequently in empirical and academic

research and also well-known to be an important factor for option pricing. Heath et al.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

22(HJM) model. Hamilton and Susmel (1994), Gray (1996), and Dahlquist and Gray

(2000) show that various foreign short-term rates can be well modeled by Markov

processes. Bansal and Zhou (2002) further develop a term structure model where the

short interest rate and the market price of risk are subject to discrete regime shifts. On

derivative pricing with stochastic interest rates, Amin and Jarrow (1991) provide the

valuation of foreign currency options under stochastic interest rates without regard to

regime shifts. Bo et al. (2010) introduce a Markov-modulated jump-diffusion model

(MMJDM) for spot-FX rates to capture both rate events and the time-inhomogeneous

fluctuations in currency markets. They then price currency options using the MMJDM.

However, the MMJDM is unable to capture forward-rate structure information. Since

change in the states of zero-coupon bonds (ZCBs) exhibit a regime-switching

structure, our study incorporates this important feature into the valuation of currency

options. Hence, two families of Markov chain systems are adopted for the HJM model

and the spot-FX rate, which consequently leading to regime-switching risks. In

addition, the RSJD model combined with the MMHJM model is a more complete and

appropriate model for pricing currency options.

This article is organized as follows: Section II provides an economic analysis for

regime-switching GBP/USD FX rate. With statistic descriptions and tests, the RSJD

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

23Black-Scholes model (BSM or GBM). In Section III, we investigate empirical data of

zero-coupon yield curves and deal with stochastic forward interest rates under a

regime-switching Gaussian HJM model. In Section IV, the RSJD model is

accommodated with Markovian systems of stochastic interest rates. In addition, we

apply the forward Esscher transform with a regime-switching condition under which

currency options on a spot-FX rate can be valued. Section V provides empirical study

showing that regime-switching risk exhibits a significant impact on prices of currency

options. The final section concludes the results.

3.2 Econometric analysis of spot-FX rate markets

In this section, we investigate spot-FX rates to find evidence of regime-switching risk

with the proposed Markov-chain system. The volatilities clustering feature of spot-FX

rates shows time-inhomogeneous fluctuations in different time periods, as implied by

different jump intensities that sometimes exhibit high or low intensities due to change

in the state of the economy or financial crises. In addition, a model can be used to

formularize autocorrelations by a Markovian system that is able to capture the

volatilities clustering feature of spot-FX rates (Timmermann (2000)). Hence, we

propose the RSJD model with two-state Markov chain to modulate jump intensities.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

24We note that the time-inhomogeneous fluctuation feature in a spot-FX rate is due to

regime-switching jumps. To show it, the daily data of the GBP/USD spot-FX rate and

the 100JPY/USD spot-FX rates are collected form 1 January, 1990 to 30 December,

2011, and the EUR/USD spot-FX rate is collected form 3 January, 2000 to 30

December, 2011.

Panel A: The dynamics of the GBP/USD spot-FX rates.

Panel B: The returns dynamics of the GBP/USD spot-FX rate returns.

Panel C: The dynamic returns of the squared GBP/USD spot-FX rates.

12/90 12/91 12/92 12/93 12/94 12/95 12/96 12/97 12/98 12/99 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2 2.1 2.2 12/90 12/91 12/92 12/93 12/94 12/95 12/96 12/97 12/98 12/99 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 -0.05 -0.04 -0.03 -0.02 -0.01 0 0.01 0.02 0.03 0.04 12/90 12/91 12/92 12/93 12/94 12/95 12/96 12/97 12/98 12/99 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 0 0.5 1 1.5 2 x 10-3

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

25Panel D: The probabilistic dynamics of low intensity

1 with spot-FX rate GBP/USD returns under the RSJD model.Figure 1: The daily data for the GBP/USD spot-FX rate starts form 1 January, 1990

to 30 December, 2011.

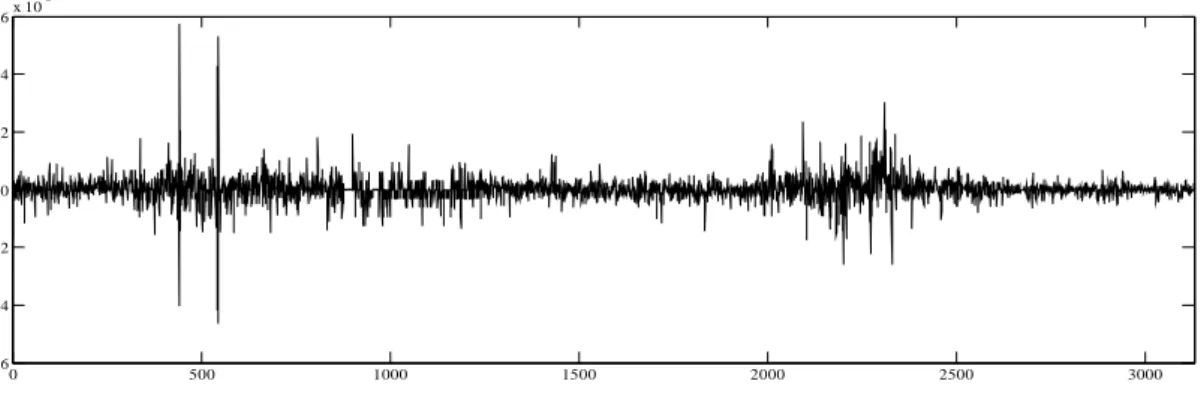

Figure1 exhibits evidence of jumps and the time-inhomogeneous fluctuations in the

GBP/USD spot-FX rate. In Panel A of Figure 1, the spot-FX rate shows two different

regions of time-inhomogeneous fluctuations during four time periods,

01/1990-12/1993, 01/1994-12/1999, 01/2000-12/2007, and 01/2008-12/2011. Panel B

provides evidence of different volatilities during the four time periods; the time

periods 01/1990-12/1993 and 01/2008-12/2011 show higher volatility than the other

two periods. Higher volatilities in these two periods are induced, respectively, by the

Oil crisis and the subprime lending crisis. The financial crises with information lag

lead to alternate high and low jump intensities with high and low volatilities. In

addition, the high and low volatilities reveal strong evidence of time-inhomogeneous

12/90 12/91 12/92 12/93 12/94 12/95 12/96 12/97 12/98 12/99 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

26fluctuations in the spot-FX rate. Furthermore, Panel C of Figure 1 reports the returns

dynamics of the squared GBP/USD spot-FX rate against time. It shows clearly that

not only there are jump trends, but also there exists a different degree of jumps with

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

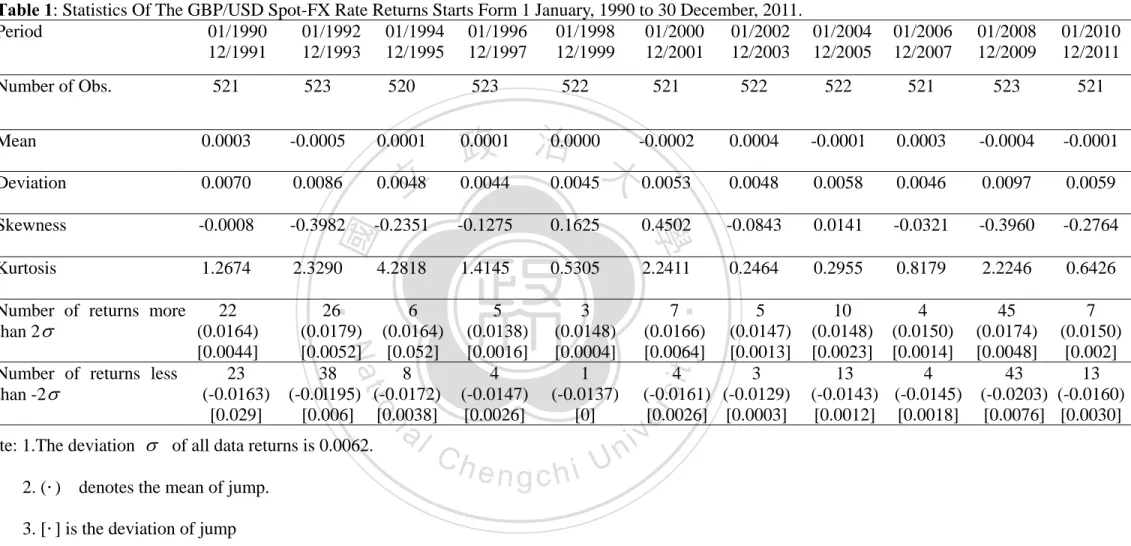

27Table 1: Statistics Of The GBP/USD Spot-FX Rate Returns Starts Form 1 January, 1990 to 30 December, 2011. Period 01/1990 12/1991 01/1992 12/1993 01/1994 12/1995 01/1996 12/1997 01/1998 12/1999 01/2000 12/2001 01/2002 12/2003 01/2004 12/2005 01/2006 12/2007 01/2008 12/2009 01/2010 12/2011 Number of Obs. 521 523 520 523 522 521 522 522 521 523 521 Mean 0.0003 -0.0005 0.0001 0.0001 0.0000 -0.0002 0.0004 -0.0001 0.0003 -0.0004 -0.0001 Deviation 0.0070 0.0086 0.0048 0.0044 0.0045 0.0053 0.0048 0.0058 0.0046 0.0097 0.0059 Skewness -0.0008 -0.3982 -0.2351 -0.1275 0.1625 0.4502 -0.0843 0.0141 -0.0321 -0.3960 -0.2764 Kurtosis 1.2674 2.3290 4.2818 1.4145 0.5305 2.2411 0.2464 0.2955 0.8179 2.2246 0.6426

Number of returns more than 2

22 (0.0164) [0.0044] 26 (0.0179) [0.0052] 6 (0.0164) [0.052] 5 (0.0138) [0.0016] 3 (0.0148) [0.0004] 7 (0.0166) [0.0064] 5 (0.0147) [0.0013] 10 (0.0148) [0.0023] 4 (0.0150) [0.0014] 45 (0.0174) [0.0048] 7 (0.0150) [0.002] Number of returns lessthan -2

23 (-0.0163) [0.029] 38 (-0.0l195) [0.006] 8 (-0.0172) [0.0038] 4 (-0.0147) [0.0026] 1 (-0.0137) [0] 4 (-0.0161) [0.0026] 3 (-0.0129) [0.0003] 13 (-0.0143) [0.0012] 4 (-0.0145) [0.0018] 43 (-0.0203) [0.0076] 13 (-0.0160) [0.0030] Note: 1.The deviation

of all data returns is 0.0062.2. (

) denotes the mean of jump. 3. [

] is the deviation of jump‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

28The descriptive statistics of GBP/USD spot-FX returns rate are reported for every two-year period in Table 1. Jumps are identified as follows: returns that are more than two standard deviations (2 ) or less than 2 from the mean are identified as jumps. Notice that a high number of jumps is associated with a high jump intensity, and vice versa, which implies that the spot-FX dynamics has two jump intensities (high and low) due to change in the state of the economy. The above result for the GBP/USD spot-FX rate carries over to the 100JPY/USD spot-FX rate and the EUR/USD spot-FX rate.

Based on the above observed phenomena of the spot-FX rate data, a hidden Markovian process is employed to formulate regime switching as an important feature for modeling the spot-FX rate dynamics, which also specifically considers jump sizes and their intensities. Hence, in the next subsections, the spot-FX rate dynamics is formulated with the RSJD model modulated by Markov chain. We then provide the estimated parameters and the test statistics for the BSM, the JDM, and the RSJD models based on the GBP/USD, the 100JPY/USD and the EUR/USD spot-FX rates. In addition, a regime-switching jump diffusion model is also established for spot-FX rates.

3.2.2 Regime-switching jump diffusion model for the spot-FX rate

A complete probability space is denoted by

, ,

with a real probability measure ,and a finite time is specified by 0, T in the continuous-time setting.

( )

t TY Y t is a continuous-time, finite-state Markov chain defined on the actual probability space

, ,

. We take the state space of Y to be a finite state set

21, 2 (1, 0), (0, 1)

Y

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

29bad time) for the state of the economy. Hence, the RSJD model of the spot-FX rate ( )

S t under the actual measure is proposed and given by:

( ) ( ) exp( ) 1 ( ), (0) 0 ( ) S n dS t dt dW t Z d t S S t (3.2.1)where and

S are constants, W t( ) is Brownian motion, ( )t is a MMPP,and the term,

eZn 1

d( )t , is a compound Poisson process.n

Z

n1

represents a sequence of mutually independent jump variables. The jump variable Zn has a normal distribution with mean

J and variance2

J

. Moreover, the MMPP ( )t

modulated by Markov chain Y has low and high jump intensity of the Poisson process denoted, respectively, by , i i1, 2. The ’s are governed by change in i the state ei of the economy modeled by Markov chain Y at time t. Specifically, we have the i

1, 2

ei , 1, i 2, where the dot ( ) denotes the scalar product, and the MMPP is governed by continuous-time Markov chain Y with a transition matrix given below:

11 11 22 22 ( ) 1 ( ) ( ) 1 ( ) ( ) Y Y Y Y Y Y p t p t t t p t p t P exp Ψ . (3.2.2) where 1 1 2 2 Y a a a a Ψ denotes a transition-rate matrix of Markov chain Y t( )

whose element

a

i,

1, i 2, represents the transition rate of the process leaving from state eiIY to the other state e , andj

a

i is the transition rate of staying at state ei.‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

30 ( , ) ij n t . Then, we have the following proposition.

Proposition 1 Under the Kolmogorov's forward equation, the moment-generating

function of the joint probability has a unique solution

0 ( , ) ( , ) n Y (1 ) n u t n t u u t

exp Ψ Λ ,where the is an intensity matrix 1

2 0 0 of the MMPP, and

0 ! n n A A n

exp , Ais a square matrix. □ The above proposition is established in Last and Brandt (1995). The ( , )u t can be used to provide estimated value to the joint probabilities ( , )n t of the MMPP. The numerical method for computing ( , )n t is proposed by Abate and Whitt (1992).Note that the RSJD model in (2.2) reduces to the JDM when

1 2 , and is given by:

ex

1 ( p ) ( ( ) ( ), (0) 0 ( ) S n) 1 dS t dt dW t dN t S S t Z . (3.2.3)where N t1( ) is a Poisson process with constant intensity

1. The RSJD model without regard to the jump term

eZn1

d( )tbecomes the well-known BSM given as follows:

( ) ( ), (0) 0 ( ) S dS t dt dW t S S t . (3.2.4)

3.2.3 Empirical analysis: the GBP/USD Foreign Exchange rate

We estimate the parameters of the discrete-time BSM, the JDM, and the RSJD models, and test the models empirically using the likelihood ratio test (LRT). The RSJD

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

31parameters are estimated using the maximum likelihood method with the Expectation Maximization algorithm (EM, Dempster et al. (1977)) and a gradient algorithm (Lange, (1995)). [ 4 ] Their standard errors are estimated using Supplemented Expectation Maximization algorithm (SEM, Meng et al. (1991)).

4

For details, see the text book: McLachlan and Krishnan 2008, The EM algorithm and extensions. John Wiley & Sons, Inc, Hoboken, New Jersey.