由國際分工與兩岸分工之觀點 分析台灣IT產業之機會與挑戰 - 政大學術集成

44

0

0

全文

(2) 由國際分工與兩岸分工之觀點 分析台灣IT產業之機會與挑戰 From the Perspective of Labor Division in Global and Cross-Strait to Analyze the Challenges and Opportunities of Taiwan IT Industry 研究生:施至鴻 指導教授:吳文傑立. Student: Joseph Shih 政 治 大 Advisor: Jack Wu. ‧ 國. 學 ‧. 國立政治大學. y. Nat. 商學院國際經營管理英語碩士學位學程. er. io. sit. 碩士論文. al. n. v C h A Thesis U n i i Program e n g c hMBA Submitted to International National Chengchi University in partial fulfillment of the Requirements for the degree of Master in Business Administration 中華民國一O三年七月 July 2014.

(3) Acknowledgements IMBA is my second master degree, but the learning process and experience is quite different from my first legal master degree. First, this time I am not a full time student but have to work and take care of my family concurrently with my study. Second, MBA program is quite different from what I familiar with as a legal background person. Third, this is an English taught program that I have to study by using the English language which is also very challenging. All of above 3 differences make my IMBA study full of challenges and surprise.. 政 治 大. I really appreciate of my family’s support in my IMBA study period, thank for their. 立. understanding that I have to sacrifice much of time to be with them in order to take the classes. ‧ 國. 學. as well as complete one after another reports and exams. Besides, I also have great thanks to. ‧. my advisor Jack Wu for giving me valuable advice in the thesis writing. At last, I would like to express my deeply appreciation to all the IMBA faculties that offering such a wonderful. y. Nat. er. io. sit. study environment that open my mind to the business world, and to all my lovely IMBA classmates, with your accompany in study make my IMBA life more colorful and memorable.. n. al. Ch. engchi. i. i Un. v.

(4) Abstract From the Perspective of Labor Division in Global and Cross-Strait to Analyze the Challenges and Opportunities of Taiwan IT Industry By Joseph Shih. 政 治 大 industry to invest in China.立 During the past 20 years’ swift development and investment in. Follow the globalization of international economic, it is an inevitable trends that Taiwan’s IT. ‧ 國. 學. China, we observe some potential risks exist in Taiwan’s IT industry. Such as over reliant on China’s market, over incline of in transferring capital, technology and resources. In nowadays,. ‧. Taiwan’s IT industry is gradually losing its advantages since China has built up its IT industry. Nat. n. al. In some fields, China’s IT industry even has intensive. er. io. reliance on Taiwan’s IT industry.. sit. y. cluster with complete supply chains from upstream to downstream and they decrease the. i Un. v. competition with Taiwan IT industry. The industry distribution between Taiwan and China. Ch. engchi. changed from vertical specialization to vertical and horizontal specialization concurrently. In order to find ways to avoid the negative competition, this thesis study the integration and embeddedness during the life cycle of IT development between cross-strait IT industry, and make SWOT analysis of cross-strait IT industry. Therefore, conclude the principles of Balanced Development and Globalized Cooperation so as to well guide the cooperation and competition between cross-strait IT industry.. On the one side, we suggest well applying. China’s technology resources as well as markets so as to lead its technology resources to be applied by IT industries; on the other side, we suggest targeting and well developing China’s channels and market which has great potential by way of building co-brand with China IT. ii.

(5) companies. The thesis finally sum up some strategies, it not only speed up the development of Taiwan IT industry in overall technology level, but also take care of China IT industry’s continuing growth which is a win-win solution to create advantages of both cross-strait IT industry.. Keywords: (International Labor division), (Cross-Strait work division), (Co-Optition of Cross-Strait IT Industry), (國際分工), (兩岸分工), (兩岸 IT 產業競合). 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. iii. i Un. v.

(6) TABLE OF CONTENTS 1.. Introduction ...................................................................................................................... 1. 2.. The Development of Labor Division in Global and Cross-Strait IT Industry:........... 3 2.1.. The Changes of Global Labor Division in IT Industry ............................................... 3. 2.1.1. The Development of Labor Division in Global IT Industry: .................................. 3 2.1.2. The Development of Labor Division in East-Asia IT Industry: ............................. 4. 學. 3.. ‧ 國. 2.2.. 政 治 大 The Changes of Cross-Strait Labor Division in IT Industry ...................................... 6 立. The Potential Risk of the Development of Cross-Strait IT Industry ........................... 8 The Difficulties and Issues of Taiwan IT Industry ...................................................... 8. ‧. 3.1.. 3.1.1. The Over Reliant of Taiwan IT industry to China’s Market ................................... 8. y. Nat. er. io. sit. 3.1.2. The Over Incline of the Transfer in Capital, Technology and Resources ............... 9 3.1.3. The Growth and Decline of Global Competition in Cross-Strait IT Industry ...... 11. al. n. iv n C The Difficulties and IssueshofeChina IT Industry n g c h i U ...................................................... 12. 3.2. 4.. The Interaction and Co-Opetition of Cross-Strait IT Industry ................................. 15 4.1.. The Life Circle and Dynamic Development of IT Industry ....................................... 15. 4.1.1. The Technology Development Process and IT Industry Life Circle: ................... 15 4.1.2. The Dynamic Development of IT Industry: Industry Integration and Embeddedness .................................................................................................................. 16 4.2.. The Current Interaction of Cross-Strait IT Industry: ............................................... 19. 4.2.1. The Changes of Industry Integration and Embeddedness .................................... 19. iv.

(7) 4.2.2. The Changes of Cooperation and Competition in Cross-Strait IT Industry ......... 21 A.. Changes of Cooperation ....................................................................................... 21 (I) Escalation of Investment Level ........................................................................... 21 (II) The Changes for the nature of Investment ......................................................... 21 (III) From Single Industry Investment to Multiple Industries Investment ............... 21 (IV) Management localization .................................................................................. 22 (V) Increasing the percentage of Local Purchase ..................................................... 22. 政 治 大. (VI) Reinvestment in China Market ......................................................................... 22. 立. Changes of Competition ....................................................................................... 23. 學. ‧ 國. B.. (I) Cross-Strait IT industries are competing in International Market ....................... 23 (II) The Exportation Business of Taiwan IT Industries are gradually shifting to. ‧. China’s IT Industries ................................................................................................ 24. y. Nat. The Co-Optition of Cross-Strait IT Industry ............................................................ 24. io. sit. 4.3.. n. al. er. 4.3.1. SWOT Analysis of Cross-Strait IT Industry......................................................... 24 (I). Ch. i Un. v. SWOT Analysis of Taiwan IT Companies Invested in China .............................. 24. engchi. (II) SWOT Analysis of China Local IT Companies ................................................... 26 4.3.2. The Principles of Co-Optition: ............................................................................. 27 (I). Principle of Balanced Development ..................................................................... 28. (II) Principle of Globalized Cooperation .................................................................... 29 4.3.3. The Strategies of Co-Optition............................................................................... 30 (I). Develop IT industry policies and regulations to systematically regulate the. investment and technology transfer in China in good order ......................................... 31 (II). Reverse the current scenario of over incline to China in product manufacturing,. v.

(8) making global arrangement of the division of works ................................................... 31 (III). Continue on R&D to escalate the technologies in product, manufacturing and. engineering ................................................................................................................... 31 (IV). Create innovative products instead of being as market follower...................... 31. (V). Enhance the ability to quickly response to the market demand ....................... 31. (VI). M&A or Strategic Alliance in Cross-Strait and Global IT Companies ............ 31. (VII) Develop co-brands with China IT companies to develop China market and then. 政 治 大. expand to the world-wide market ................................................................................. 31. 立. Conclusions ..................................................................................................................... 32. 學. ‧ 國. 5.. Reference ................................................................................................................................. 34. ‧. n. er. io. sit. y. Nat. al. Ch. engchi. vi. i Un. v.

(9) List of Figures and Tables Figure 1: Flying Geese Paradigm ............................................................................................ 5 Figure 2 The Changes of Taiwan’s Exportation Weight from 2000 to 2013........................ 9 Figure 3 The Weight of Taiwan IT Product Manufactured in China ................................ 10 Figure 4 Life Circle of IT Industry ....................................................................................... 16. 政 治 大. Figure 5 Industry Integration through Life Circle of IT Industry .................................... 17. 立. Figure 6: Industry Embeddedness through Life Circle of IT Industry ............................. 18. ‧ 國. 學. Figure 7: Industry Integration through Life Circle of Cross-Strait IT Industry ............. 20. ‧. Figure 8: Industry Embeddedness through Life Circle of Cross-Strait IT Industry ....... 20. y. Nat. er. io. sit. Figure 9 Dynamic competition in cross-strait IT industry ................................................. 29. al. n. iv n C Table 1 MSCI Taiwan Index by thehWeight of Main e n g c h i UIndustry (2014/4/25) ....................... 8 Table 2 The Difference of MSCI Emerging Market Index for the Past 10 Years ............ 12 Table 3 MSCI China Index by the Weight of Main Industry (2014/4/25) ....................... 13. vii.

(10) 1. Introduction Taiwan, with its advantages of high quality technical human resources, management flexibility, skilled of production and healthy capital market, which create a good environment to develop its OEM/ODM business model in IT industry and established a complete IT supply chains from upstream to downstream during the period from 1980 to 1990. The IT industry in this thesis is defined as information and electronic industry, electronic components &. 政 治 大 began to make scaled investment 立 in China and the labor division in cross-strait has significant. materials industry, electronic testing & assembly industry. Since late 1990, Taiwan IT industry. ‧ 國. 學. changes during the recent 20 years. In nowadays, we can see a highly shift and integration trend between Taiwan and China, we also see that China’s IT industries are no longer highly. ‧. dependent of Taiwan’s IT industries, but become more influential and begin to compete with. sit. y. Nat. Taiwan’s IT industries. Taiwan’s economic growth is highly dependent on the development of. n. al. er. io. IT industry, if the Taiwan government doesn’t have appropriate industry policy and the IT. i Un. v. companies don’t have correct development strategies, it might severely impact Taiwan’s. Ch. engchi. economic. The purpose of this thesis is trying to analyze and conclude some principles and strategies for the government as well as the IT companies in order to make win-win solutions for the development of cross-strait IT industry.. This thesis begins with the introduction to development of labor division in global and cross-strait IT industry, so that we can have an overall understanding of the trend and changes of labor division. Then, we analyze the potential risks in Taiwan and China separately which gives us warning signals within such development trend of IT industry. To avoid the potential risk, we need to come out some concrete solutions for the potential issues. Therefore, we use. 1.

(11) the concepts of “Life Circle” as well as “Integration” and “Embeddedness” in IT industry to structure a prediction model to predict the trend and requirements of IT industry in different development stage. Furthermore, we apply such models to the current interaction between cross-strait IT industry and also summarize the changes of cooperation and competition which proves the interaction of cross-strait IT industry follows such prediction model. In the end, through the SWOT analysis between cross-strait IT industry, we conclude some principles and strategies that can be taken into consideration that benefit the future development of both Taiwan and China IT industry.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 2. i Un. v.

(12) 2. The Development of Labor Division in Global and Cross-Strait IT industry: 2.1.. The Changes of Global Labor Division in IT Industry. 2.1.1. The Development of Labor Division in Global IT Industry: To discuss about the development of labor division in IT industry, we can trace back to around 1940 of the Science and Technology Innovation which trigger the swift development of. 政 治 大. IT industry. During the past 60 year history, the development of labor division in IT industry. 立. followed the Factor Endowment Theory and can be divided by the following four stages:. ‧ 國. 學. (i). Kick-off Stage. During 1940~1960, this period is the kick-off stage of IT industry. Most of the. ‧. IT companies are located in USA which makes USA become monopoly in. y. Nat. n. al. er. io. sit. product R&D, product development to product production.. Ch. (ii) Initial Expansion Stage. engchi. i Un. v. In 1960~1980, USA made strategic adjustment of its industry policy during the cold war. It transfer part of its IT industry to west Europe and Japan which trigger the swift development of IT industry in west Europe and Japan.. (iii) Asia’s Swift Development Stage In 1980~1990, USA, west Europe and Japan begin to shift part of its basic IT industry to Asia countries like India, Taiwan, Hong Kong, Singapore and South Korea which trigger Asia’s development of its IT industry. India made. 3.

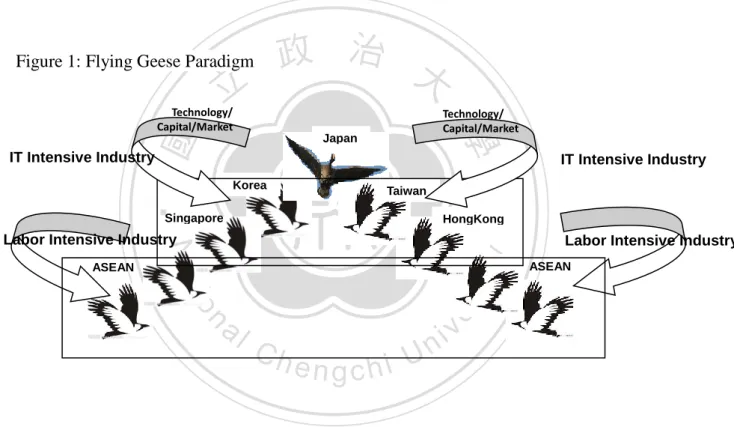

(13) great progress in Software industry, it became the second biggest of software export country that made India stood in important position in Global IT industry. Taiwan also developed its OEM/ODM business model in IT industry and established a complete IT supply chains from upstream to downstream. This made Taiwan stood in an important position in the global IT product production.. 政 治 大. (iv) Cluster in China Stage. 立. Since 1990, due to the China’s reform and open policy, China became the new. ‧ 國. 學. cluster to attract most of the IT investment world wide. Now, the original IT industry cluster is facing reorganization and a new IT industry cluster is. ‧. establishing.. sit. y. Nat. n. al. er. io. From the above four stages, we find that the global labor division of IT industry. i Un. v. changes from horizontal labor division in USA in 1940 to vertical labor division in. Ch. engchi. USA, west Europe, Japan and Asia countries respectively in 1990. Now, the global labor division is that USA, west Europe and Japan focus on IC design and electronic materials R&D; Taiwan and South Korea focus on product design, tri-run production of high-end IT product and centralized management center; As to China, it plays the role as the major OEM manufacturers of world wide IT products.. 2.1.2. The Development of Labor Division in East-Asia IT Industry: In Asia, during the period from 1970 to 1980, the development of labor division followed the model “Flying Geese Paradigm” as below Figure 1. Japan stood in the core position of 4.

(14) Science and technology that played as the head geese that led Asia’s economic development through the supply of capital and technology, open market and shipment of traditional industries. Asia four dragons played the role as the Geese’s wing which developed its technology intensive industries by applying Japan’s capital, technology and market. At the same time, they also shipped the labor intensive industries to AESAN. Thus, ASEAN played the role as the Geese tail which really depended on the economic development of Japan.. Figure 1: Flying Geese Paradigm. 立. 政 治 大 Technology/ Capital/Market. 學. ‧ 國. Technology/ Capital/Market. Japan. IT Intensive Industry. Korea. Singapore. ‧. Taiwan. HongKong. n. al. Labor Intensive Industry ASEAN. er. io. sit. y. Nat. Labor Intensive Industry ASEAN. IT Intensive Industry. Ch. engchi. i Un. v. However, since 1977 Asia’s economic down term, Japan’s economic dropped severely which affected its position as the Geese head. Besides, ASEAN began to change its industry policy to avoid over dependent on Japan’s economic development. In addition, due to the China’s reform and open policy, China began to join the global labor division and made swift economic progress by applying its advantages of low cost labors, resources and huge market potential. As a result, the traditional vertical labor division of Flying Geese Paradigm collapsed owing to the. 5.

(15) gap among Japan, Asia four dragons and China narrowed down and even has some extent of similarity.. 2.2.. The Changes of Cross-Strait Labor Division in IT Industry Taiwan, with its advantages of high quality technical human resources, management. flexibility, skilled of production and healthy capital market, which create a good environment to develop its OEM/ODM business model in IT industry and established a complete IT supply. 政 治 大. chains from upstream to downstream during the period from 1980 to 1990. Taiwan’s. 立. representative IT industries include information and electronic industry, electronic components. ‧ 國. 學. & materials industry and electronic testing & assembly industry, which made Taiwan stood in. ‧. an important position in the global IT product production.. y. Nat. io. sit. Since late 1990, due to the changes of Taiwan’s economic environment and China’s. n. al. er. reform and open industry policy which triggered the trend of Taiwan’s IT industries to make. Ch. i Un. v. big scale of investments in China in order to apply its low cost of labor, land, resources and. engchi. secure the potential big market. The business model of labor division in the beginning of this trend is that Taiwan IT industry be responsible for product design and have its low-end product to be manufactured in China. In this process, China’s IT companies still need to import key components and materials from Taiwan companies which also boost Taiwan’s economy and then China companies export the finished product to world-wide that boost China’s economy. This business model works well for around 10 years, but through the process of experience learning, technology transfer and exchange of human resources, China’s IT companies also got the ability to manufacture high-end product, and then further began to. 6.

(16) build up its own IT industry and completed supply chains. Therefore, the cooperation between cross-strait gradually changed from vertical labor division to horizontal integration and strategic alliance. At the this same period, more and more local companies start to manufacture key components and materials of IT products, this resulted in the increase of percentages in localized purchasing in China instead from Taiwan. Now, the IT industry cluster from upstream to downstream are more and more complete which enable China subsidiaries the ability to make self operation and management more and more independently.. 立. 政 治 大. To conclude the trend of labor division between cross-strait IT industries, we divide it by the. ‧ 國. 學. following five stages: (i). Stage 1: Shift of low capital and labor intensive industry. ‧. (ii) Stage 2: Shift of high capital and technical intensive industry. y. Nat. sit. (iii) Stage 3: Horizontal integration and strategic alliance. n. al. er. io. (iv) Stage 4: increasing localized purchasing, sales and high-end human resources. i Un. v. (v) Stage 5: increasing the independent management on local subsidiaries. Ch. engchi. From the past 20 years’ development of cross-strait labor division, we can see a highly shift and integration trend between Taiwan and China. And we also see that China’s IT industries are no longer highly dependent of Taiwan’s IT industries, but become more influential and begin to compete with Taiwan’s IT industries.. 7.

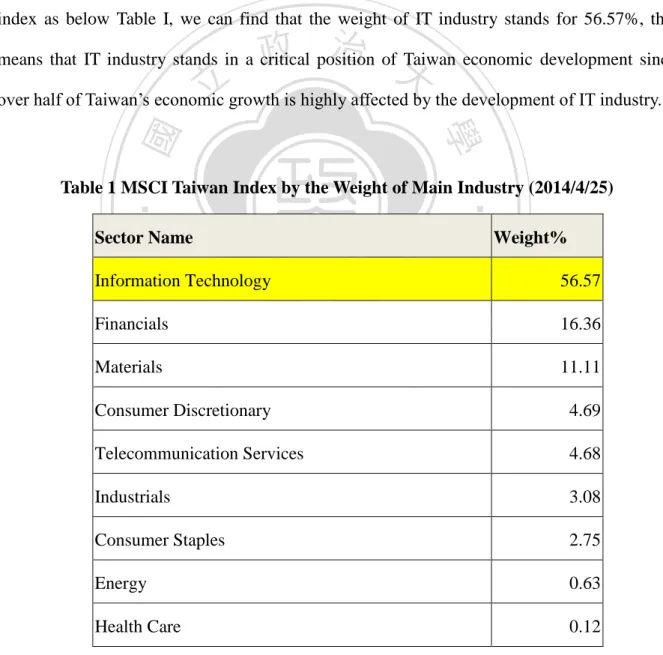

(17) 3. The Potential Risk of the development of Cross-Strait IT Industry 3.1.. The Difficulties and Issues of Taiwan IT Industry. 3.1.1. The Over Reliant of Taiwan IT industry to China’s Market If we observe the MSCI Taiwan index which is a world-wide recognized investment decision index as below Table I, we can find that the weight of IT industry stands for 56.57%, this. 政 治 大. means that IT industry stands in a critical position of Taiwan economic development since. 立. over half of Taiwan’s economic growth is highly affected by the development of IT industry.. ‧ 國. 學 ‧. Table 1 MSCI Taiwan Index by the Weight of Main Industry (2014/4/25). sit. y. Nat. Sector Name. io. al. n. Financials. er. Information Technology. Materials. Ch. engchi U. v ni. Weight% 56.57 16.36 11.11. Consumer Discretionary. 4.69. Telecommunication Services. 4.68. Industrials. 3.08. Consumer Staples. 2.75. Energy. 0.63. Health Care. 0.12. 8.

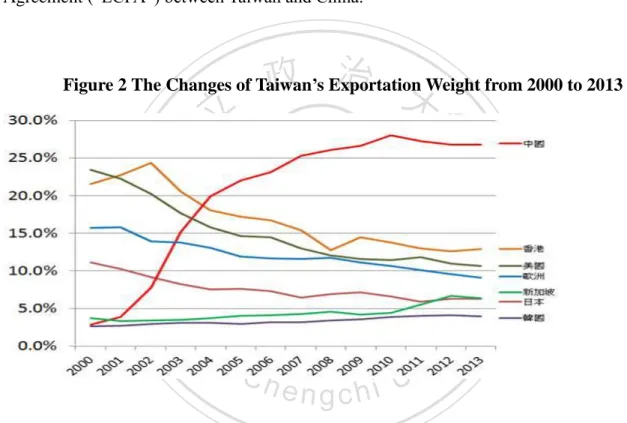

(18) However, since 1990 Taiwan’s IT industry began to make scaled investment in China which raised the extent of the economic reliant on China. We can also find from the Figure II below, the weight of Taiwan’s exportation to China in 2000 is 2.5%, but in 2010 it increase to 26%. The exportation percentages to China increase dramatically, we can foresee that the trend will continue to increase after the execution of Economic Cooperation Framework Agreement (“ECFA”) between Taiwan and China.. 政 治 大. Figure 2 The Changes of Taiwan’s Exportation Weight from 2000 to 2013. 立. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i Un. v. 3.1.2. The Over Incline of the Transfer in Capital, Technology and Resources As mentioned before, Taiwan IT industry made swift and scaled investment in China during the past 10 years, the representative IT companies such as PC & Notebook manufacturer ex. Acer, Ben Q, Compal, Liteon, Foxconn and FIC; the Mainboard manufacturer ex. Gigabyte, FIC and ECS; the PCB manufacturer ex. WUS, Compeg and Unitech; and the LCD manufacturer ex. CPT, AUO and Chemei. The purpose of these IT companies’ investments are to reduce the production cost through taking advantage of China’s. 9.

(19) low cost of labor, land and resources. But via the process of shift the skill of product manufacturing, it also transfer the technology, experience of management & production to China IT companies which result in a great improvement and escalation of product production and R&D . Therefore, Taiwan’s IT industry is facing the issues of over incline of capital, technology and resources to China.. According to the statistic of Institute of Information Industry, in 2004 the total value of. 政 治 大. Taiwan’s IT hardware products is US$62.7 billion, but US$48.7 billions (73.3%) is attributed. 立. by the production in China. From the below Figure 3, we can also find the trend of China. ‧ 國. 學. production weight is increasing dramatically from 22.8% to 73.3% since 1997 to 2004. This exist the potential risk that Taiwan IT industry is too reliant on the production in China, it. ‧. might cause big problems if any industry policy changes by China government or economic. n. al. er. io. sit. y. Nat. fluctuation in China.. Ch. i Un. v. Figure 3 The Weight of Taiwan IT Product Manufactured in China US 10 million. engchi. Out Put Values of WW IT Hardware Industry Weight of China IT Industry. 10. By %.

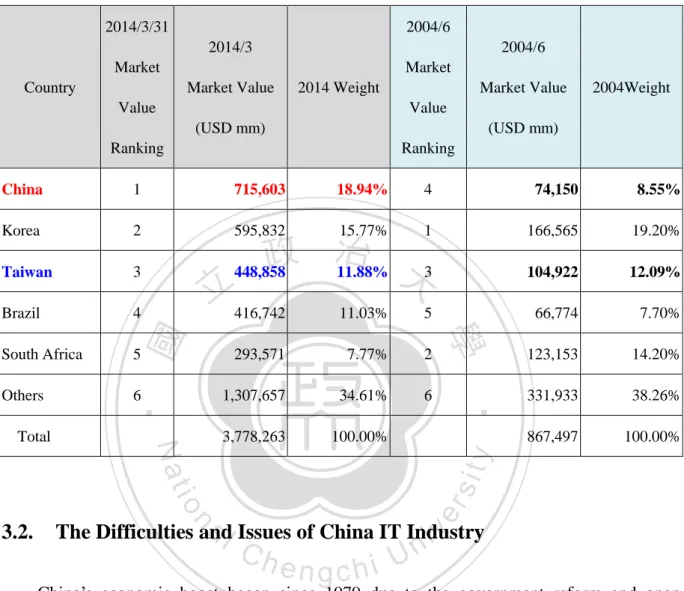

(20) 3.1.3. The Growth and Decline of Global Competition in Cross-Strait IT Industry Because of China’s inducing of the great investment from Taiwan and world-wide IT industry, China became a world factory and attracting a big deal of capital and direct orders which quickly expand China’s exportation to world-wide. For example, according to 2002 MIC statistic, in 2001 China’s total out-put value of IT hardware industry is 28 billion, but in. 政 治 大. 2002 it jumped to 35.2 billion which has exceed Taiwan and became the No.2 world-wide.. 立. In US market, after both Taiwan and China entering into WTO, China’s IT product. ‧ 國. 學. became more and more competitive. According to 2013 statistic of Ministry of Economic. ‧. Affairs, R.O.C., the market share of China’s product has jump from 3.08% to 18.7% between. sit. y. Nat. 1990 and 2012 which is now ranked No.1 world-wide. Compared to Taiwan, the market share. io. er. of Taiwan product dropped year after year and in 2013 is 1.7% which is ranked No. 11 world-wide. As to Taiwan’s market share of information and communication product is 3.2%. n. al. which is ranked 6 world-wide.. Ch. engchi. i Un. v. We can also compare to the MSCI emerging market Index between 2004/3 and 2014/3 in below Table 2, during this 10 years, the weight of China increase from 8.55% to 18.94%, but the weight of Taiwan dropped from 12.09% to 11.88%. This reveals that Taiwan is facing the sever competition and under the risk of losing its competitiveness.. 11.

(21) Table 2 The Difference of MSCI Emerging Market Index for the Past 10 Years 2014/3/31. 2004/6 2014/3. 2004/6. Market. Market. Country. Market Value. 2014 Weight. Value. Market Value. 2004Weight. Value (USD mm). (USD mm). Ranking. Ranking. China. 1. 715,603. 18.94%. 4. 74,150. 8.55%. Korea. 2. 595,832. 15.77%. 1. 166,565. 19.20%. Taiwan. 3. 448,858. 104,922. 12.09%. Brazil. 4. 66,774. 7.70%. 123,153. 14.20%. 331,933. 38.26%. 867,497. 100.00%. 293,571. 7.77%. 2. 6. 1,307,657. 34.61%. 6. 3,778,263. 100.00%. a l Issues of China IT Industry The Difficulties and iv n. 3.2.. er. io. sit. y. 5. ‧ 國. 5. Nat. Total. 11.03%. ‧. Others. 立416,742. 學. South Africa. 政 治 11.88% 大3. Ch. n engchi U. China’s economic boost began since 1979 due to the government reform and open industry policy, but the dramatic economic growth seems to slow down whiling entering into the 21 century. To figure out the reasons, we can find that China government pursues the economic growth by emphasizing too much on the GDP growth, but lack of promoting of innovation and entrepreneurship. Huge amount of capital were replaced to make investment on real estate rather than invest in innovation, knowledge and production.. 12.

(22) From the perspective of Chinese traditional culture, we can also find that it emphasizes more on the collective efforts but lacks of promoting the independent spiritual. It is highly restricted by Confucianism which somehow encourages the people to follow the tradition rather than pursue for innovation. Owing to the potential influence of Chinese culture as well as China government policy’s over incline in GDP growth, Chinese people love to pursue wealth rather than seek for creativity and new knowledge. Although China’s economic make dramatic growth since 1979, most of the accumulated wealth is not being invested in. 政 治 大. technology development but in real estate which caused the price increase, raised of labor. 立. wages and then attribute to the overall inflation in China market. Above scenarios are. ‧ 國. 學. reflected in China’s MSCI index as below table which shows that financial industry stands for 39% in H stocks and 61.6% in A stocks. Obviously that the market is over incline to financial. ‧. industry, IT industry only stands for 13.15% in H stocks and 2% in A stocks which are far less. y. Nat. sit. than financial industry. As we mentioned before, according to Factor Endowment Theory,. n. al. er. io. China has the advantages to develop IT industry by its low cost labor resources. But now the. i Un. v. over incline to financial industry raise the labor wages, the effects is that it decreased China’s. Ch. engchi. competitive advantages to develop IT industry.. Table 3 MSCI China Index by the Weight of Main Industry (2014/4/25) MSCI Index (H Stocks). Sector Name. Financials. Energy. MSCI Index (A Stocks). Weight%. Sector Name. 39.39 Financials. 16.1 Consumer Discretionary. 13. Weight%. 61.16. 10.16.

(23) Information Technology. 13.15 Consumer Staples. Telecommunication Services. 11.59 Industrials. Consumer Staples. 7.09 Energy. Consumer Discretionary. 3.65 Health Care. Industrials. 3.28 Materials. Utilities. 立. 4.58. 4.3. 2.65. 2.06 Telecommunication Services. 學. 0.45 Utilities. ‧. io. sit. y. Nat. n. al. er. Health Care. 6.1. Information Technology 政 3.23治 大. ‧ 國. Materials. 6.67. Ch. engchi. 14. i Un. v. 2. 1.24. 1.15.

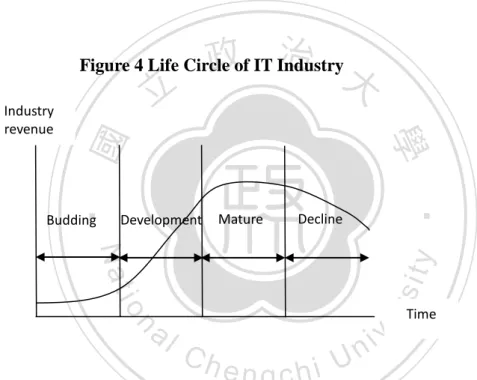

(24) 4. The Interaction and Co-Opetition of Cross-Strait IT Industry 4.1.. The Life Circle and Dynamic Development of IT Industry. 4.1.1. The Technology Development Process and IT Industry Life Circle: To observe the technology development process of IT industry, from inducing new technology to well development of technology, first we could divide it by the following 4 major stages: (1) Technology Acquiring: technology could be acquired through import of high tech equipments, transfer of technology or joint venture with high tech companies in. 政 治 大. developed countries, etc; (2) Technology Expansion: this means the acquired technologies. 立. are expanded to the overall IT industry by the movement of high tech human resources,. ‧ 國. 學. exchange of acquired technology or mutual sharing of technology knowledge, etc, so the. ‧. technology level of the overall IT industry was escalated; (3) Self-Technology Development: this means improvement of the acquired technologies, innovate the manufacturing process or. y. Nat. er. io. sit. develop new functions through copy, reverse engineering or expand product functions, so that the overall industries are upgraded to a higher level; (4) IT Industry Cluster: When the. n. al. Ch. i Un. v. technologies are successful induced and then further developed and expanded, this would. engchi. trigger IT companies gathered in same geographic areas so as to integrate mutual requirements from upstream to downstream, and ease the movement of technology, human resources, capital and information. As a result, a completed supply chains are established due to the effects of IT industry cluster which reduce the transaction costs and strengthen the competition power of each individual IT company within this IT industry cluster.. Second, we can also observe the development process of IT industry via the perspective of industry life circle. Like the product, industry also has its life circle which could be divided. 15.

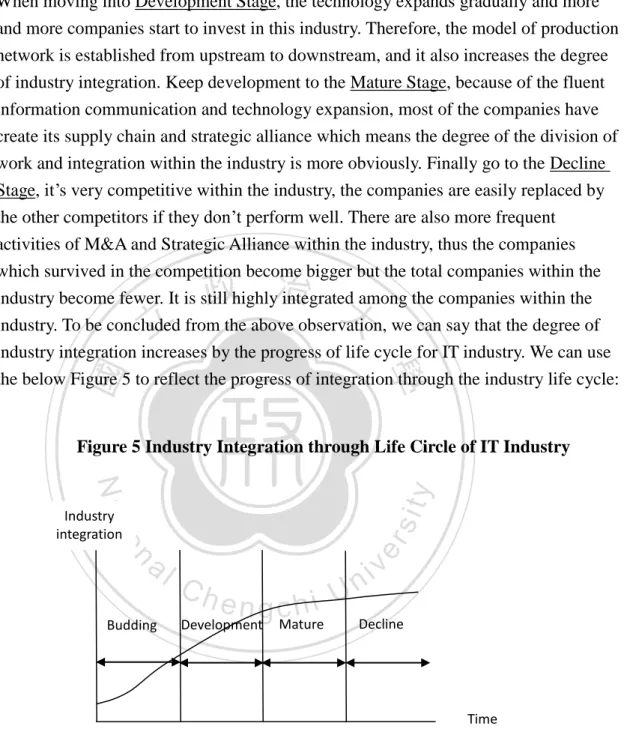

(25) by 4 stages as below Figure 4: (1) Budding (2) Development (3) Mature (4) Decline. In the stages of Budding, the fundamental science just initially be developed and still not yet be developed in application science. But in the Development and Mature stages, the studies in the application science are more than the studies in the fundamental science. At last, in the Decline stage, both fundamental science and application science are mature and the gap between each other is very few.. 政 治 大. Figure 4 Life Circle of IT Industry. 立. Budding. Development. ‧. ‧ 國. 學. Industry revenue. Decline. Mature. n. er. io. sit. y. Nat. al. Ch. engchi. i Un. v. Time. 4.1.2. The Dynamic Development of IT Industry: Industry Integration and Embeddedness The advantages of an industry are determined by the complementary of the companies within such industrial district. We can observe and analyze the dynamic changes of industry advantages from the perspective of “Industry Integration” and “Industry Embeddedness”. (i). Industry Integration Industry Integration means the degree of the labor division within an industry. In Budding Stage, the Industry Integration is low due to only few first movers engage in the technology innovation. All the investments are done by first movers themselves in order to expand the market share and pursue for the advantages of economic scale. 16.

(26) When moving into Development Stage, the technology expands gradually and more and more companies start to invest in this industry. Therefore, the model of production network is established from upstream to downstream, and it also increases the degree of industry integration. Keep development to the Mature Stage, because of the fluent information communication and technology expansion, most of the companies have create its supply chain and strategic alliance which means the degree of the division of work and integration within the industry is more obviously. Finally go to the Decline Stage, it’s very competitive within the industry, the companies are easily replaced by the other competitors if they don’t perform well. There are also more frequent activities of M&A and Strategic Alliance within the industry, thus the companies which survived in the competition become bigger but the total companies within the industry become fewer. It is still highly integrated among the companies within the. 政 治 大 industry. To be concluded 立 from the above observation, we can say that the degree of ‧. ‧ 國. 學. industry integration increases by the progress of life cycle for IT industry. We can use the below Figure 5 to reflect the progress of integration through the industry life cycle:. Figure 5 Industry Integration through Life Circle of IT Industry. sit. y. Nat. n. al. er. io. Industry integration. Budding. Ch. engchi. Development. Mature. i Un. v. Decline. Time. (ii). Industry Embeddedness The Industry Embeddedness means the degree of similar companies collected in the same industrial district. The reasons that similar companies collected in the same industrial district is because they can get the service and/or production elements very easily and quickly, like human resources, key materials or components, technical service, 17.

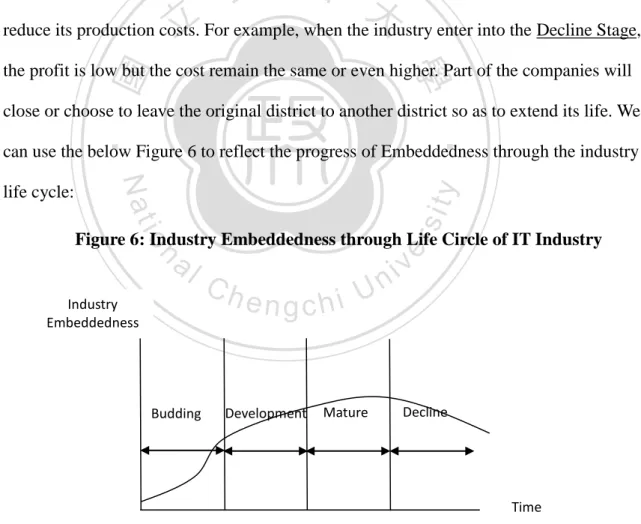

(27) water and electricity, transportation, etc. Industry Embeddedness is also highly affected by government industrial policy and the local resources endowment. In Budding Stage, the industry embeddedness is low due to the production elements and services are rarely existed. Through the development of industry life cycle, the more completeness of industry network is, the higher degree of the Industry Embeddedness. However, the interesting thing is that the degree of Embeddedness decreases when the degree of industry network reaches to certain levels. We call it the “Floating Embeddedness”. 政 治 大. which means the whole industry will shift and re-embed in another district in order to. 立. reduce its production costs. For example, when the industry enter into the Decline Stage,. ‧ 國. 學. the profit is low but the cost remain the same or even higher. Part of the companies will close or choose to leave the original district to another district so as to extend its life. We. ‧. can use the below Figure 6 to reflect the progress of Embeddedness through the industry. io. sit. y. Nat. life cycle:. n. al. er. Figure 6: Industry Embeddedness through Life Circle of IT Industry. Industry Embeddedness. Budding. Ch. engchi. Development. i Un. Mature. v. Decline. Time. 18.

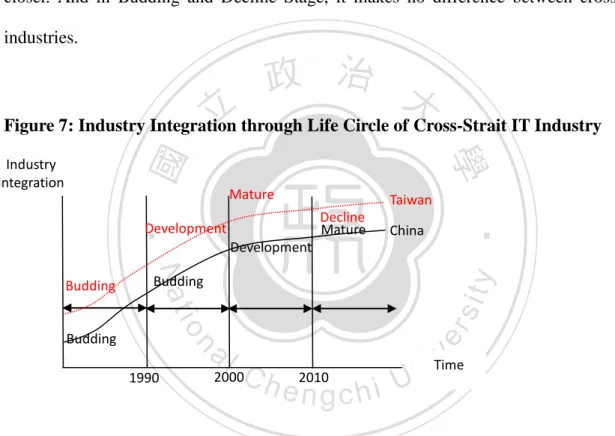

(28) 4.2.. The Current Interaction of Cross-Strait IT Industry:. 4.2.1. The Changes of Industry Integration and Embeddedness From the perspective of Industry Integration and Industry Embeddedness that we discussed in Article 4.1 to see the changes of interaction of cross-strait IT industry, for those IT companies invested in China in the early stage around late 1990, most of these IT companies are low technology intensive and belong to Mature or Decline Stage which has more demand on Industry Integration. Therefore, the purpose of investment in China is. 政 治 大. seeking for division of work, most of the key components are still supplied by Taiwan IT. 立. companies and then assembled and manufactured in China. However, in recent years, Taiwan. ‧ 國. 學. IT companies which are in high intensive technology industry within the Development Stage invest in China increasingly. The intention for those companies to invest in China are seeking. ‧. for the shift of Industry Embeddedness since the investment environment in China are more. y. Nat. sit. and more mature and complete, and they can find most of the production elements at low cost. n. al. er. io. compared to Taiwan. Figure 7 and Figure 8 express the dynamic development and trend of. i Un. v. cross-strait IT industry in its demand of integration and embeddedness. As a result, the. Ch. engchi. industrial distribution between Taiwan and China changed from vertical specialization to vertical and horizontal specialization concurrently. This means the competition environment exist both competition and cooperation of cross-strait IT industries. The results are attributed by two reasons: (1) for those mature industries, it’s difficult to distinguish the division of works. Once these companies decided to move to China, the related production activities through upstream to downstream will then follow accordingly. (2) China IT companies will also seek for more independent and expansion in it business operation in order to increase effectiveness.. 19.

(29) Though the technology development in Taiwan IT industry are ahead of China’s IT industry due to the longer period of development and network with worldwide IT companies, China IT industry is chasing with swift speed. The technology gap between cross-strait IT industries is differing according to the different development stage. In Development Stage, Taiwan’s IT industry is more advanced than China, but in Mature Stage the gap is becoming closer. And in Budding and Decline Stage, it makes no difference between cross-strait IT industries.. 政 治 大. 立. Figure 7: Industry Integration through Life Circle of Cross-Strait IT Industry. Mature. Taiwan Decline Mature. Development. China. Development. y. Nat. n. al. er. io. Budding. sit. Budding. Budding. 1990. ‧. ‧ 國. 學. Industry integration. Ch. 2000. 2010. engchi. v iTime n U. Figure 8: Industry Embeddedness through Life Circle of Cross-Strait IT Industry Industry Embeddedness Mature. Decline. Development Development Budding. Mature. China Taiwan. Budding. Budding 1990. 2000. 2010. 20. Time.

(30) 4.2.2. The Changes of Cooperation and Competition in Cross-Strait IT Industry A. Changes of Cooperation For the past 20 years, there are some major changes of cooperation between cross-strait IT industry. (I) Escalation of Investment Level. 政 治 大. In the early stage, the cross-trait investments focus on traditional industry, till now on,. 立. the investment are spreading to high-tech industry. Thus, not only in industry level but also in. ‧ 國. 學. technical level as well as operation level are totally escalated in cross-strait cooperation.. ‧. (II) The Changes for the Nature of Investment. y. Nat. sit. Due to labor quality was promoted, China not only has low cost of labor resources, but. n. al. er. io. also have high quality of R&D human resources. Taiwan IT companies’ investment level. i Un. v. therefore also changes from production model to both production and R&D model. Ch. engchi. concurrently. More and more Taiwan IT companies cooperate with China local research institutes and universities in order to adopt its R&D resources and develop new technology and product. (III) From Single Industry Investment to Multiple Industries Investment As mentioned before, once Taiwan IT companies decided to move to China, the related production activities from upstream to downstream will then move accordingly. This completes the supply chain and also enhances the embeddedness of China IT industry.. 21.

(31) (IV) Management Localization In early stage, Taiwan IT companies only take advantages of China’s low cost labor resources, most of the technical and management level are distributed from Taiwan HQ. But till now, they gradually recruit local management manpower due to the quality of labor was overall promoted through learning and movement of human resources in recent years.. 政 治 大. (V) Increasing the percentage of Local Purchase. 立. Due to the completed IT supply chain was established, it cause the IT companies no. ‧ 國. 學. longer need to import key components from Taiwan, they just purchase it from local IT companies which not only lower down the transportation cost but also shorter the transit time. ‧. period.. sit. y. Nat. io. n. al. er. (VI) Reinvestment in China Market. i Un. v. China’s market is more and more open after executing its reform policy which collects. Ch. engchi. huge amounts of capital from world-wide, including Taiwan, to invest in China’s market. Taiwan IT companies are attracted by the government incentive policy, a big portion amount of money earned from China market are reinvested in the China market instead of returning back to Taiwan market. This trend somehow affects Taiwan’s IT industry to collect investment capital which slow down the development speed of Taiwan IT industry as well.. 22.

(32) B. Changes of Competition. (I) Cross-Strait IT industries are competing in International Market As we mentioned above, China market introduces investments from world-wide after its adopting the reform policy and also join in WTO. These investments not only bring in the capital, but also bring in technology, management skill and production experience. In such. 政 治 大. good circle, more orders are generated naturally from world-wide. Taiwan IT companies. 立. contribute a lot in this progress which promote China IT industries in production skill and. ‧ 國. 學. R&D field. Now, Taiwan IT companies’ subsidiaries in China are more independent and financial, management and production, they even get the orders directly from customers. ‧. instead of from Taiwan parent companies. Thus, Taiwan IT industries are now facing the over. y. Nat. sit. incline to China market in capital, technology and products, and cross-strait IT industries are. n. al. er. io. directly competing in international market. According to 2002 MIC statistic, in 2001, China’s. i Un. v. total out-put value of IT hardware industry is 28 billion, but in 2002 it jumped to 35.2 billion. Ch. engchi. which has exceed Taiwan and became the No.2 world-wide. In US market, the market share of China’s product has jump from3.08% to 18.7% between 1990 and 2012 which is now ranked No.1 world-wide. According to 2013 statistic of Ministry of Economic Affairs, compared to Taiwan, the market share of Taiwan product dropped year after year and in 2013 is 1.7% which is ranked No. 11 world-wide. As to Taiwan’s market share of information and communication product is 3.2% which is ranked 6 world-wide. These all reflects that Taiwan IT industries are losing it market share and competitiveness in the international market.. 23.

(33) (II) The Exportation Business of Taiwan IT Industries are Gradually Shifting to China’s IT Industries According to CCID’s report in 2002, China overpasses Taiwan and became the 2nd IT exportation country since the end of 2002, more than 70% exportation products are invested by Taiwan companies. We can also see the reports of ITIS program by Institute for Information Industry, in 1995, Taiwan companies’ domestic production are 72% and China production are 14%, but in 2002, domestic production are 34.1% and China production are. 政 治 大. 51%. We believe the percentage is increasing continually today. Thus, it’s very obvious that. 立. the exportation business of Taiwan IT industries are gradually shifting to China’s IT. Nat. io. 4.3.1. SWOT Analysis of Cross-Strait IT Industry. al. n. (I) (i). sit. The Co-Optition of Cross-Strait IT Industry. er. 4.3.. y. ‧. ‧ 國. 學. industries.. i Un. v. SWOT Analysis of Taiwan IT Companies Invested in China Strength. Ch. engchi. Taiwan IT companies have complete and swift supply chains which make it with the ability to manufacture products efficiently. Besides, Taiwan also develops many high level human resources specialized in technical as well as in IT management, this create the advantage to run the IT companies with highly flexibility and quickly response to the market demand. With such strength, it also enables Taiwan IT companies to collect capital easily and make further investment in operation.. (ii). Weakness. 24.

(34) The research and development ability are still limited, most of the key technologies and components are still kept in foreign main players. This limits the development and profit potential of Taiwan IT companies, since it’s very easy to be controlled and highly rely on the foreign companies. In addition, Taiwan IT companies lacks of ability to develop its own brand and also need to strengthen the ability to develop international channels in order to expand market as well as profit potential.. (iii). Opportunities. 立. 政 治 大. Due to complete supply chain and efficient manufacturing abilities as well as long. ‧ 國. 學. term relationship with the international big IT companies, they have more trust and are more willing to cooperate with Taiwan IT companies. Furthermore, China market is still. ‧. full of potential, with similar culture and language, Taiwan IT companies have more. y. Nat. sit. advantages than foreign companies to develop China Market. Though it’s difficult to. n. al. er. io. develop brands in China’s market due to the protection policy of China government,. i Un. v. Taiwan IT company may consider to cooperate with China IT companies to develop. Ch. engchi. co-brands in China market first and then further expand to world-wide market. This may release the concerns of China government’s protection policy and take advantages of culture similarity to well develop channels and markets in China.. (iv). Threat With the transfer of technologies and movement of IT human resources during. recent 10 years, Taiwan IT companies are now facing strongly competition from China’s local IT companies. On the other hand, the other risk exit on the unstable government policy and legal system, it’s still controlled by and highly rely on the personnel who have 25.

(35) the relationship with the government. At last, the labor cost in China is increasing year by year, it’s no longer an advantage of China market.. (II) (i). SWOT Analysis of China Local IT Companies Strength China government fully supports its local IT industries with many incentive. programs to induce foreign companies to make investment and transfer of technologies.. 政 治 大 China also has strong basic R&D results and high quality of technical human resources, 立 In addition, the potential China market is also very attractive to induce investments.. ‧ 國. Weakness. ‧. (ii). 學. which are a strong fundamental to develop its IT industries.. The capital market in China is not very active, the investments in IT industries are. y. Nat. er. io. sit. still highly rely on foreign IT companies. Besides, the operation and management efficiency is poor and has limited relationship with international IT companies.. n. al. (iii). Ch. Opportunities. engchi. i Un. v. The market demand of IT product in China is increasing rapidly which creates more opportunities to make investments locally. Furthermore, with such investments, it will gradually improve the quality of operation and management of IT industries. Also, the technology transfer from foreign companies will escalate the local technical level and expand to local IT industries.. (iv). Threat The competition will be more intensive due to the market is open with less limitation 26.

(36) after China join as the WTO members. The environment issue is also a potential risk which will increase the cost to build up new factories of IT companies. We also need to pay attention of the over investment in IT industries which might cause the waste of resources and further decrease the profit margin.. 4.3.2. The Principles of Co-Optition: Taiwan IT industries develop longer than China IT industries, the integration and. 政 治 大. embeddedness of Taiwan IT industries are more complete than China IT industries. Even in. 立. the same life cycle, the depth of technology level between cross-strait IT industries is different.. ‧ 國. 學. However, different industry has different characteristics and benefits, cross-strait IT industries. market.. ‧. shall develop its own product by applying its unique advantages in order to be success in the. y. Nat. er. io. sit. The life cycle of Taiwan IT industry is different from China’s IT industry. According to our observation, Taiwan IT industry is positioned in the Mature stage or in the process from. n. al. Ch. i Un. v. Mature stage to Decline stage which has both high demand on integration and embeddedness.. engchi. But in China IT industry, it is positioned in Development stage or in the process from Development stage to Mature stage which has more demand on embeddedness than demand on integration. In such situation, the demand of embeddedness is stronger than the demand of integration, according to the theory we introduced in Article 4.1.2 and 4.2.1, it will trigger the shift of embeddness of Taiwan IT industry from Taiwan market to China market. The industrial distribution between Taiwan and China changed from vertical specialization to vertical and horizontal specialization concurrently. This means the competition environment exist both competition and cooperation of cross-strait IT industries.. 27.

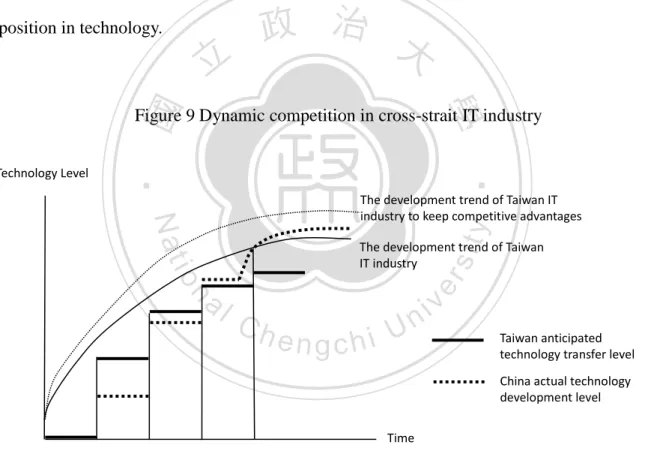

(37) Therefore, below we conclude two principles for the Co-Optition of cross-strait IT industries. (I). Principle of Balanced Development. Since the depth of technology level in Taiwan IT industry is better than China’s IT industry, for those Taiwan IT companies which is in Mature stage and faced difficulties to continue development in Taiwan market, it exist benefit for them to invest in China market and transfer its existing technology to China companies. Due to this actions not only extend. 政 治 大. its product life cycle, but also recover part of its investment in technologies R&D. However,. 立. this actions shall be well regulated by government policy, too much intervention and. ‧ 國. 學. regulations or too loose management all might damage Taiwan IT industry’s advantages and create more competitors as well as speed the collapses of Taiwan IT industry. Appropriate. ‧. industry policy shall well guide the way of development of Taiwan IT companies, taking care. y. Nat. sit. of both the balance of cross-strait development as well as the market mechanism. It’s also. n. al. er. io. very important for Taiwan IT companies to continue on R&D and make innovation in order to. i Un. v. escalate the technologies in product, manufacturing and engineering, and develop new. Ch. engchi. products as well as build up the ability to quickly response to the market demand. This is the only way for Taiwan IT industry to strengthen its competitiveness and keep in ahead of China IT industry. From below Figure 9 of Dynamic competition in cross-strait IT industry, we can find that in stage A, the technology level of Taiwan IT industry is higher than China IT industry. Though lots of investment and technology transfer happened in stage B, China IT industry’s technology level is still lower due to the related infrastructure is not ready. But in stage C, the technology gap is getting smaller through the learning process and gradually mature of IT 28.

(38) infrastructure. Then, in stage D, China IT industry’s technology level start to surpass Taiwan IT industry which might result in having some explosive progress in development in certain technology or getting certain technology from other sources than Taiwan. If Taiwan IT industry cannot strengthen its IT technology level promptly, China IT industry will continue leading the way in technology and the gap will become bigger and bigger. This tells why it’s really critical for Taiwan IT industry to keep escalation of its technology level while cooperating with and technology transfer to China IT industry in order to maintain its leading position in technology.. 立. 政 治 大. ‧ 國. 學. Figure 9 Dynamic competition in cross-strait IT industry. ‧. Technology Level. The development trend of Taiwan IT industry. n. al. er. io. sit. y. Nat. The development trend of Taiwan IT industry to keep competitive advantages. Ch. engchi. i Un. v. Taiwan anticipated technology transfer level China actual technology development level. Time. (II). Principle of Globalized Cooperation. For those Taiwan IT companies which are positioned in the process from Mature stage to Decline stage, the technology gap between cross-strait companies is very minor, the division of works also changes from vertical work division to horizontal work division. The business. 29.

(39) model of China IT companies which are invested by Taiwan IT companies are no longer by Taiwan design and manufactured in China, but gradually changes to consolidate with local China IT companies to direct compete with Taiwan IT companies. If the situation continues, the intensive competition between cross-strait IT industries will really damage both sides. Therefore, the only way to make a win-win solution is to apply both sides’ resources strategically and cooperate to compete in the global market by increasing the integration for exchange of R&D, capital and human resources between cross-strait IT industries.. 學. ‧ 國. 立. 政 治 大. 4.3.3. The Strategies of Co-Optition. To observe China’s economic development history, China’s IT resources are mainly. ‧. owned by the government and they conduct the R&D activities based on the mission assigned. y. Nat. sit. by the planned economy system, thus, China lacks of the experience of market-oriented. n. al. er. io. economy to efficient make use of IT resources to escalate its ability of IT industry. On the. i Un. v. other side, though Taiwan’s IT industry develops high tech human resources and amount of. Ch. engchi. capitals, it is still not sufficient to meet the demand of IT human resources in global IT competition. As a result, it’s very important for Taiwan IT companies to apply above 2 principles and take China IT companies as partners to make global arrangement plans. On the one side, to well apply China’s technology resources so as to lead its technology resources to be applied by IT industries; on the other side, to target and well develop China’s channels and market which has great potential by way of building co-brand with China IT companies. In this way, it can speed up the development of Taiwan IT industry and overall technology level which can also create advantages in global network of work division. Below we conclude and summarize some suggestions of strategies generated from the above 30.

(40) principles for Taiwan IT industry: (I). Well design IT industry policies and regulations to systematically regulate the investment and technology transfer in China in good order. (II). Reverse the current scenario of over incline to China in product manufacturing, making global arrangement of the division of works. (III). Continue on R&D to escalate the technologies in product, manufacturing and engineering. 政 治 大. (IV). Create innovative products instead of being as market follower. (V). Enhance the ability to quickly response to the market demand. (VI). M&A or Strategic alliance in cross-strait and global IT companies. This is the. 立. ‧ 國. 學. effective and efficient ways to acquire the critical technologies, complete. ‧. channels as well as experience of globalized management so as to establish. y. Nat. n. al. er. io. chains.. sit. economic scale effects in integration of productions, marketing and supply. (VII). i Un. v. Develop Co-Brands with China IT companies to develop China market and. Ch. engchi. then expand to the world-wide market. 31.

(41) 5. Conclusions Due to the globalization of international economic, in order to compete in the global market, it is an inevitable trends that Taiwan’s IT industry to invest in China. During the past 20 years’ swift development and investment in China, we observe some potential risks exist in Taiwan’s IT industry. Such as over reliant on China’s market, over incline of in transferring capital, technology and resources. In nowadays, Taiwan’s IT industry is gradually losing its. 政 治 大 upstream to downstream and 立they decrease the reliance on Taiwan’s IT industry.. advantages since China has built up its IT industry cluster with complete supply chains from In some. ‧ 國. 學. fields, China’s IT industry even competes with Taiwan IT industry. The industry distribution between Taiwan and China changed from vertical specialization to vertical and horizontal. ‧. specialization concurrently. The way to secure Taiwan IT industry’s advantages is not to block. Nat. sit. y. the competition, but to find a ways to guide the cooperation and competition between. n. al. er. io. cross-strait IT industry. Through the study of integration and embeddedness during the life. i Un. v. cycle of IT development between cross-strait IT industry, and make SWOT analysis of. Ch. engchi. cross-strait IT industry. We conclude that cross-strait IT industry shall make co-optition under the principles of Balanced Development and Globalized Cooperation.. Taiwan IT industry. shall take China IT companies as partners to make global arrangement plans. On the one side, to well apply China’s technology resources as well as markets so as to lead its technology resources to be applied by IT industries; on the other side, to target and well develop China’s channels and market which has great potential by way of building co-brands with China IT companies. The strategies includes continuing on R&D to escalate the technologies in product, manufacturing and engineering, create innovative products instead of being as market follower, enhance the ability to quickly response to the market demand, M&A or Strategic 32.

(42) alliance in cross-strait and global IT companies to acquire critical technologies, complete channels as well as experiences of globalized management which also help to establish economic scale effects in integration of productions, marketing, supply chains, and develop co-brands with China IT companies to develop China market and then expand to the world-wide market. In this way, it can speed up the development of Taiwan IT industry in overall technology level, but also take care of China IT industry’s continuing growth which is a win-win solution to create advantages of both cross-strait IT industry in global network of work division.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 33. i Un. v.

(43) Reference 1. 論世界 IT 產業國際分工與重組及中國的應對措, 杨娜 潘鑫, http://www.hi138.com/jingjixue/hangyejingji/200806/45306.asp 2. 台灣電子資訊產業發展史 (年表), http://ccckmit.wikidot.com/in:taiwanelectronicstimeline 3. 參考陳信宏、史惠慈和高長(2002),<台商在中國大陸從事研發趨勢對台科技創新之 影響及政府因應策略之研究>,經濟部技術處委託研究計畫,中華經濟研究院,台北。 4. 華民,「”入世”後後國如何參與國際分工世界經濟與政治」,世界經濟與政治,2002 年第 4 期。 5. 華民,「新經濟的周期變動與 IT 產業國際分工的重組」,國際經濟評論,2002.3-4 6. <IT IS 產業評析(2002)>,台北:資策會 MIC,2002 年、World Trade Altas。 7. 陳杰,「從資源基礎理論探討台灣半導體產業企業經營策略之研究」,政治大學行 政管理碩士學程論文,2008。 8. 許璋慶,「MSCI 成份股調整對股票報酬之影響」,政治大學商學院經營管理碩士學 程. 財管組碩士論文,2010 年。 9. 高長,科技產業全球分工與 IT 產業兩岸分工策略,遠景季刊 ; 3 卷 2 期 (2002 / 04 / 01) , P225 – 256 10. 徐作聖(1999a),<科技政策與國家創新系統>,華泰。. 立. 政 治 大. ‧. ‧ 國. 學. sit. y. Nat. n. al. er. io. 11. 王鳳生、鄭育仁合著,2002,從高科技產業動態發展模式解析兩岸產業競合策略, 2002 中華民國科技管理研討會論文集 12. 夏逸葦, 台商投資與兩岸資訊科技產業之互動, 政治大學,中山人文社會科學研究所 碩士論文,2002 年。 13. 謝中興、江永裕,「勞動能力分配、生產可分割性與國際分工」,《經濟論文叢刊》, 33(3),257-285,2005 年。 14. 李志強,「大陸房市泡沫化問題簡析」,《大陸及兩岸情勢簡報》,頁 5-8,2012 年3月 15. 司徒達賢,「兩岸電子業分工體系之研究」,跨越大陸投資障礙研討會,行政院大 陸委員會,1993 年。. Ch. engchi. i Un. v. 16. 高希均、林祖嘉,「台商大陸投資對國內產業升級與兩岸垂直分工影響之研究」, 經濟部工業局委託研究報告,1993 年。 17. 徐作聖、賴賢哲,「兩岸高科技產業競合策略」,科技發展政策報導,2002。 18. 劉仁傑,《重建台灣產業競爭力》,台北:遠流出版社,1997 年。 19. 中國大陸投資環境簡介,經濟部投資業務處,http://www.dois.moea.gov.tw/main.asp。 20. 兩岸經濟交流,行政院大陸委員會, 34.

(44) http://www.mac.gov.tw/np.asp?ctNode=5597&mp=1。 21. 統計數據,大陸商務部,http://www.mofcom.gov.cn/tongjiziliao/tongjiziliao.html。 22. 進出口貿易統計,財政部,http://www.mof.gov.tw/ct.asp?xItem=12759&CtNode=130。 23. Gartner 市場研究公司,http://www.gartner.com 24. IC Insights,http://www.icinsights.com/ 25. 工研院產業情報網 IEK,http://ieknet.itri.org.tw/ 26. 半導體產業推動辦公室,http://www.sipo.org.tw 27. 台積電公司,http://www.tsmc.com/chinese/default.htm 28. 台灣半導體協會,http://www.tsia.org.tw/ 29. 經濟部工業局,http://www.moeaidb.gov.tw 30. MBA lib 智庫‧百科,. 政 治 大. http://wiki.mbalib.com/zh-tw/%E8%A6%81%E7%B4%A0%E7%A6%80%E8%B5%8B. 立. ‧. ‧ 國. 學. %E8%AE%BA 31. Roberts, E. B. & Berry, C. A. (1985) Entering new business: selecting strategies for success, Sloan Management Review 32. Boretsky, M. (1982), The threat to US High Technology Industries: Economic and National Security Implications Draft, International Administration, US Department of Commerce. 33. Kelly, R.K.(1977), The Impact of Technological Innovation on International Trade. sit. y. Nat. n. al. er. io. Patterns, Office of International Economic Research, U.S. Department of Commerce. 34. Kumar, N. (2001), Determinants of Overseas R&D Activity of Multinational Enterprise: The Case of US and Japanese Corporations, Research Policy, 30. 35. Pyke, D., Robb, D., and Farley, J. (2000), Manufacturing and supply Chain Management in China: a Survey of State-, Collective-, and Private-owned Enterprises, European Management Journal.. Ch. engchi. 35. i Un. v.

(45)

數據

+7

相關文件

Now, nearly all of the current flows through wire S since it has a much lower resistance than the light bulb. The light bulb does not glow because the current flowing through it

11/03/2019, 24/05/2019 EI0020180468 IT in Education Subject-related Series: Using IT Tools to Enhance Learning and Teaching Effectiveness in General Studies Lessons in

It is intended in this project to integrate the similar curricula in the Architecture and Construction Engineering departments to better yet simpler ones and to create also a new

Then, it is easy to see that there are 9 problems for which the iterative numbers of the algorithm using ψ α,θ,p in the case of θ = 1 and p = 3 are less than the one of the

double-slit experiment is a phenomenon which is impossible, absolutely impossible to explain in any classical way, and.. which has in it the heart of quantum mechanics -

Provide all public sector schools with Wi-Fi coverage to enhance learning through the use of mobile computing devices, in preparation for the launch of the fourth IT in

OpenGL 4.2 Reference card: Blue means!. deprecated

Therefore, the focus of this research is to study the market structure of the tire companies in Taiwan rubber industry, discuss the issues of manufacturing, marketing and