行政院國家科學委員會專題研究計畫 成果報告

型一誤差重要還是檢定力重要?條件動差檢定中的非單調

檢定力問題

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 99-2410-H-004-057- 執 行 期 間 : 99 年 08 月 01 日至 100 年 07 月 31 日 執 行 單 位 : 國立政治大學經濟學系 計 畫 主 持 人 : 林馨怡 計畫參與人員: 博士班研究生-兼任助理人員:劉冬威 博士班研究生-兼任助理人員:胡玫英 處 理 方 式 : 本計畫涉及專利或其他智慧財產權,2 年後可公開查詢中 華 民 國 100 年 10 月 29 日

1

Introduction

Many applied researchers use statistical inference for different models in practice. An important issue in inferential methods for econometrics models is that some tests can exhibit nonmonotonic power (see, e.g., Nelson and Savin (1990), Vogelsang (1999), and Deng and Perron (2008)). That is, as the distance that alternative hypothesis deviates from the null grows, the power of the test actually decreases. The problem of nonmonotonic power is noted in a variety of tests such as tests in linear/nonlinear regression models of Hauck and Donner (1977), Bates and Watts (1988), and Nelson and Savin (1990), in the generalized method of moments (GMM) of Hall (2000) and Hall, Iuoue and Peixe (2003), and models with structural breaks in the mean of Andrews and Monahan (1992), Deng and Perron (2008), and Vogelsang (1999).

Applied researchers use consistent estimators for the variance covariance matrix when testing parameter restrictions on linear regressions such as the heteroskedas-ticity consistent covariance matrix estimators (HCCME) of White (1980) and the heteroskedasticity and autocorrelation consistent estimators (HACE) of Newey and West (1987). In the GMM literatures, Hall (2000) shows that the non-centered HACE in GMM method is not consistent when model is misspecified. Therefore, the overidentifying restriction test of GMM method base on the non-centered HACE may not be consistent under the alternative and exhibits nonmonotonic power in large sample. Hall (2000) considers a centered HACE and shows that the resulting overidentifying restriction test is consistent under both null and alternative; see also Hall and Inoue (2003), Chang (2005, 2007). However, Hall, Iuoue and Peixe (2003) shows that when the presence of neglected structural instability under the alterna-tive, even the HACE is based on non-centered or centered autocovariances, the rate of increase of the overidentifying restrictions test is depending on the form of the instability.

Most Monte Carlo studies indicate that the main reason for nonmonotonic power is that in finite samples some nuisance parameters such as the variance estimator are poorly estimated under the (global) alternative; see Hall (2000), Crainiceanu and Vogelsang (2007), Juhl and Xiao (2009). Allen (2007) compares the powers of the overidentifying restriction tests using the centered and non-centered HACEs, but his Monte Carlo simulation shows that very little power is gain. MacKinnon and White (1985), Flachaire (2005), Godfrey (2006) and Godfrey and Orme (2004)

propose several different forms of a variance-covariance matrix to control the finite sample significance levels. They find that hypothesis testings using the wild or jackknife bootstrap perform better in small samples. Goncalves and White (2005) show that tests based on the moving blocks bootstrap estimators have better finite samples performances. Recently, several authors impose a boundary condition for the HACE to restore the monotone power of tests; see Sul et al. (2005). Juhl and Xiao (2009) propose a modified variance estimator based on the nonparametrically demeaned data and show that the modified estimator diverges at a slower rate than the unmodified version; thus, tests based on the modified estimator retain their consistency under various diverging alternative hypotheses.

In many econometric and statistical applications, there often exist conditional moment (CM) restrictions that characterize the behavior of models of interest. For example, specifications for regression models and specifications for conditional prob-ability models can be represented as CM restrictions. Once a model is specified, it is important to have specification tests on its validity. A CM test based on CM restrictions is a general framework that includes most model specification tests. For example, Newey (1985), Tauchen (1985), Wooldridge (1990), Bierens (1982, 1990), Bierens and Ploberger (1997), Bierens and Ginther (2001), Zheng (1998) to mention only a few. Although the nonmonotonic power problem have been studied in many testing literature, this problem is not discussed in the framework of CM tests. As Nelson and Savin (1990) pointed, “While the existence of nonmonotonic power is not new, the surprising results are that this phenomenon occurs ... and it can be quite severe”. In this paper, the nonmonotonic power problem in the CM tests is investi-gated in finite samples by using Monte Carlo simulation. We show that the standard variance estimator used in the CM tests is consistent only under the null. Under the alternative, nonmonotonic power could arise from using an inconsistent estimate; CM tests can not retain their consistency under global alternatives. Therefore, the variance estimator is the main source of the nonmonotonic power problem in CM tests. Since the source of nonmonotonic power problem in CM test is the variance estimator, we suggest using the centered variance estimator in test with the aim of gaining power under global alternative. We examine the small sample performances of tests by Monte Carlo simulations. It is seen that the power functions of the tests are very sensitive to the behavior of the variance estimates.

2

Non-Centered Variance Estimators

Let yt be a finite-dimensional vector of dependent variable(s) with index t, and

Xt be the information set available in explaining yt. Suppose that it is interested

in estimating and testing a CM model of yt|Xt with a r × 1 vector of generalized

residuals mt := mt(yt, xt; θ) for some finite r ≥ dim(yt), in which xt denotes a

vector of Xt-measurable explanatory variables and θ ∈ Θ ⊂ Rp stands for a p × 1

parameter vector. This CM model is defined to be correctly specified, if and only if, the martingale difference condition:

H0 : IE[mot|Xt] = 0, mot := mt|θ=θ0,

is satisfied for some unique θo ∈ Θ. Let zt be a q × r matrix of Xt-measurable

mis-specification indicators, the q × 1 testing function: ztmtmust satisfy the

martingale-difference condition:

IE[ztmot|Xt] = ztIE[mot|Xt] = 0,

which further implies the unconditional moment restriction: IE[ztmot] = 0. The CM

test checks this restriction by examining whether the estimated moment: T−1PT

t=1ztmˆt

is significantly different from zero, in which ˆmt := mt|θ=ˆθT with ˆθT representing

es-timator of θo.

Let ut be the error term of the specified regression model. Suppose that the CM

test is based on an estimator of θo which is solved from the estimating equation:

T−1PT

t=1xtuˆt = 0, from some p × 1 estimating function that does not contain the

same components of the testing function ztmˆt, x0t = −∇θutis X -measurable function

and ˆut:= ut|θ=ˆθT. The estimator ˆθT has the following representation:

√ T (ˆθT − θo) = − " 1 T T X t=1 xt∇θut #−1 1 √ T T X t=1 xtut+ op(1) = IE(xtx0t) −1√1 T T X t=1 xtut+ op(1)

If mt= ut, then ∇θmt= ∇θut= −x0t. 1 √ T T X t=1 ztmˆt= 1 √ T T X t=1 ztmt+ 1 T T X t=1 zt∇θmt ! √ T (ˆθT − θo) + op(1) = √1 T T X t=1 ztmt− IE(ztx0t)IE(xtx0t) −1√1 T T X t=1 xtut+ op(1) = √1 T T X t=1 [zt− IE(ztx0t)IE(xtx0t) −1 xt]ut+ op(1).

Let zt∗ := zt− IE(ztx0t)IE(xtx0t)−1xt, we can rewrite the above equation as follows:

1 √ T T X t=1 ztuˆt = 1 √ T T X t=1 z∗tut+ op(1).

When model is correctly specified or say under the null hypothesis, one has IE(ut|Xt) = 0, and the test statistic converges to a normal distribution by central

limit theorem under suitable regularity conditions:

1 √ T T X t=1 ztuˆt d → N (0, V ),

where the asymptotic variance V := IE[zt∗utu0tz ∗ t 0

] is a q × q variance covariance matrix. Follow Hall’s (2000) suggestion, the non-centered and centered variance estimators are considered. The non-centered variance estimator is specified as:

ˆ ΣuT := 1 T T X t=1 (zt∗uˆt)(zt∗uˆt)0,

and a centered variance estimator of the variance

ˆ ΣcT := 1 T T X t=1 zt∗uˆt− 1 T T X t=1 zt∗uˆt ! z∗tuˆt− 1 T T X t=1 zt∗uˆt !0 .

Considering two test statistics for testing CM restrictions, I first define the statis-tic with normalizing centered variance estimator as

MTu := " 1 √ T T X t=1 ztuˆt #0 ( ˆΣuT)−1 " 1 √ T T X t=1 ztuˆt # ,

and define the statistic with non-centered variance estimator as MTc := " 1 √ T T X t=1 ztuˆt #0 ( ˆΣcT)−1 " 1 √ T T X t=1 ztuˆt # .

Under H0, both variance estimators converge to the asymptotic variance V , and it is

derived that Mu T d → χ2(q) and Mc T d

→ χ2(q), where χ2(q) the chi-square distribution

with q degrees of freedom. This result demonstrates that “centering” in construct-ing normalizconstruct-ing matrices leads to correct size and does not affect the asymptotic behavior when model is correctly specified.

If the model is incorrectly specified, the limiting distribution of the statistic is different from that under correctly specified model. In the following, I consider two types of alternatives; one is a global alternative and the other is the local alternative. Consider a general alternative hypothesis:

H1 : IE[ut|Xt] = wt0δ.

This test is expected to be powerful against H1 because the conditional expectation

of ztutbecomes IE[ztut|Xt] = ztwt0δ under H1, which implies that IE[ztut] = IE[ztw0t]δ

is a q × 1 nonzero vector provided that IE[ztwt0] is positive definite. The asymptotic

behavior of Mc

T or MTu depends on two terms: one is the asymptotic behavior of

T−1/2PT

t=1ztuˆt and the other is the asymptotic behavior of ˆΣuT and ˆΣcT. Because

1 √ T T X t=1 ztuˆt = 1 √ T T X t=1 z∗t(ut− wt0δ) + 1 √ T T X t=1 z∗twt0δ + op(1),

under H1 the first term on the right-hand-side of the above equation converges to

dis-tribution N (0, IE[zt∗utu0tz ∗ t 0

]) which is Op(1), and the asymptotics of T−1/2

PT

t=1ztuˆt

depends on the second term T−1/2PT

t=1z ∗ tw

0

tδ. In addition, under H1, the centered

variance estimator ˆΣc T

p

→ V and the non-centered variance estimator ˆ

ΣuT → V + IE(zp tw0t)δδ 0

IE(wtzt0),

which follows from

1 T T X t=1 ztuˆt = IE(ztw0t)δ + op(1).

The limits of ˆΣcT and ˆΣuT differ by an extra term: IE(ztwt0)δδ0IE(wtzt0). When T → ∞,

The power of the test based on MTc approaches 1 but the power of MTu is unknown depending on the functional form of the alternative hypothesis and the additional term IE(ztw0t)δδ0IE(wtz0t). This is the first finding of this paper that the CM test

based on uncentered variance may constitute nonmonotonic power.

Consider one special case that IE(ztwt0)δ = O(1) such as a constant function,

then MTu diverges and the power of MTu approaches 1. The other special case is the local alternatives:

H1A: IE[ut|Xt] = γ/

√ T .

This local alternative is approaching to the null when T goes to infinity. Under H1A, both ˆΣcT → V and ˆp ΣuT → V . Therefore, under Hp A

1 , when T → ∞, both statistics

MTc and MTu diverge and the power of the tests approach 1. Note that in these cases, although the asymptotic power of MTu and MTc approach 1 and both CM test are consistent, it is found that when T is small, the finite sample power of MTu and MTc are different. It is argued that the divergence rate of MTu is slower than that of MTc. Therefore, in practice, when the sample size is not large, the finite sample power of MTu is smaller than that of MTc. This is the motivation of this paper which focuses on the finite sample comparison of two CM tests.

3

Monte Carlo Simulation

In this section, three Monte Carlo experiments to examine the effectiveness of the proposed tests are conducted. In particular, we compare the powers of Mu

T and MTc

in sample mean and conditional mean examples. All examples consider sample sizes of T = 10, 20, 50, the nominal size is 5%, and the number of replication is 2000.

3.1

Sample Mean Example

For the following two hypotheses,

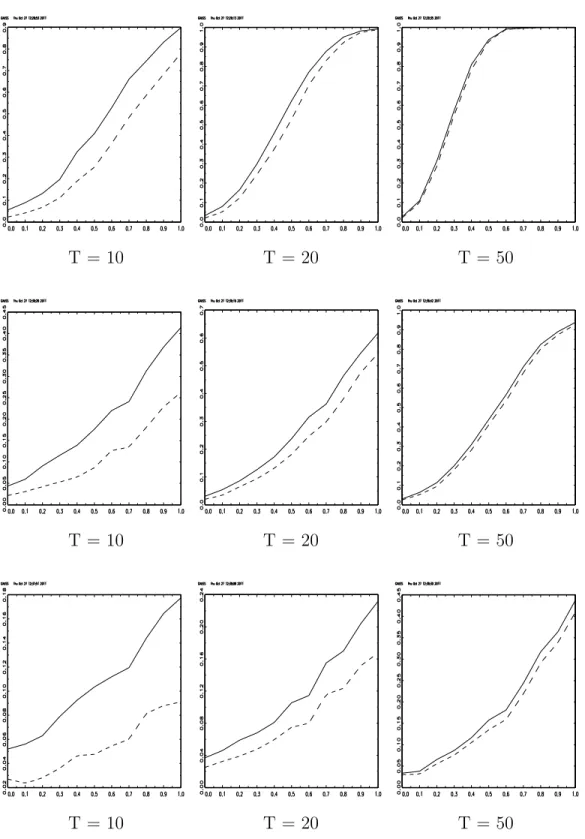

H0 : xt∼ N (0, σ20), H1 : xt∼ N (µ, σ02), (1) then ztuˆt= xt, ˆΣuT := (ˆσuT)2 = T−1 PT t=1x 2 t, ˆΣcT := (ˆσTc)2 = T−1 PT t=1(xt− ¯x)2, with ¯ x = PT

t=1xt/T . In the sample mean example, we consider cases with σ02 = 1, 2, 4.

the horizontal axis is µ which represents the deviation from the null, the vertical axis is the rejection rate of tests, the dashed line represents the rejection rate of MTu and the solid line shows those of MTc. From Figure 1, we can find that when the sample size is small, the finite sample power of MTc is higher than that of MTu; the difference between the powers becomes smaller as the sample size gets larger. In addition, for fixed sample size T , the difference between powers of MTc and MTu are smaller for σ02 = 1 and are larger when σ02 = 4.

3.2

Conditional Mean Example

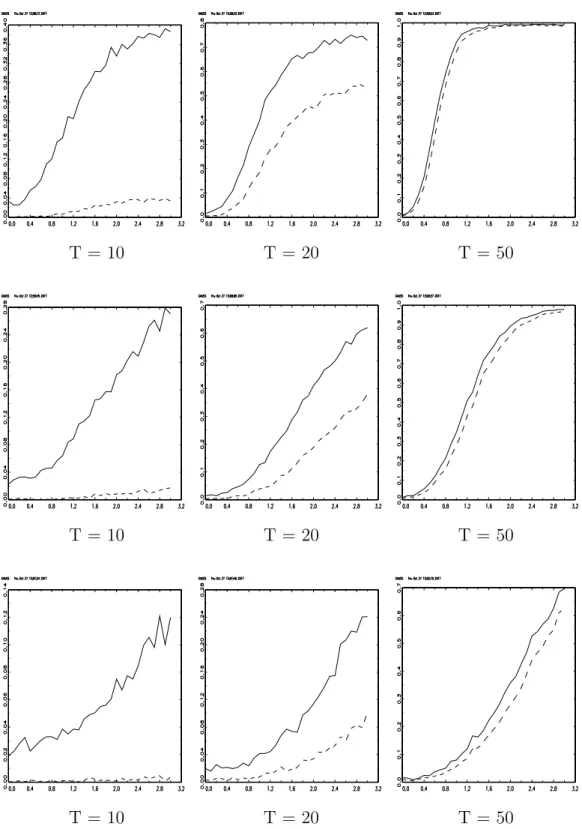

Ho : yt = x0tβ + ut, ut|Xt−1∼ N (0, σ21t);

H1 : yt = x0tβ + ut, ut|Xt−1 ∼ N (w0tδ, σ 2 2t),

(2)

with β a k × 1 vector of parameters. The CM restriction is IE(ut|Xt−1) = 0. Suppose

that xt is independent and identically distributed N (0, 1). The conditional mean

example is also considered with wt0δ = µ, σ21t = σ2t2 = 1, 2, 4. In this example, let ˆβ be the least square estimator, ˆut = yt− x0tβ, zˆ tuˆt = xtuˆt, ˆΣuT := T−1

PT t=1xtuˆ2tx0t, ˆ ΣcT := 1 T T X t=1 " xtuˆt− 1 T T X t=1 xtuˆt # " xtuˆt− 1 T T X t=1 xtuˆt #0 .

The rejection rates of conditional mean example is presented in Figure 2. In the figure, the horizontal axis is µ which represents the deviation from the null, the vertical axis is the rejection rate of tests, the dashed line represents the rejection rate of MTu and the solid line shows those of MTc. From Figure 2, we can find that when the sample size is small, the finite sample power of MTc is much higher than that of MTu; the difference between the powers becomes smaller as the sample size gets larger. In addition, for fixed sample size T , the difference between powers of MTc and MTu are smaller for σ02 = 1 and are larger when σ02 = 4.

4

Conclusions

In this paper, a modified CM test with centered variance estimator is proposed. The nonmonotonic power problem can be alleviated with considering the modified CM test. Our Monte Carlo simulation shows that the CM test based on centered variance has lower finite sample powers, while the CM test based non-centered variance has higher finite sample powers.

T = 10 T = 20 T = 50

T = 10 T = 20 T = 50

T = 10 T = 20 T = 50

Figure 1: Finite Sample Powers in Sample Mean Examples with σ20 = 1 for upper panel, σ02 = 2 for middle panel, σ20 = 4 for lower panel.

T = 10 T = 20 T = 50

T = 10 T = 20 T = 50

T = 10 T = 20 T = 50

Figure 2: Finite Sample Powers in Conditional Mean Examples with σ20 = 1 for upper panel, σ20 = 2 for middle panel, σ20 = 4 for lower panel.

References

Allen, J., (2007). Size matters: covariance matrix estimation under the alternative. Economic Journal, 10, 637-644.

Andrews, D.W.K., Monahan, J.C., (1992). An improved heteroskedasticity and autocorrelation consistent covariance matrix estimator. Econometrica, 60, 953-966.

Bates, D.M., Watts, D.G., (1988). Nonlinear Regression Analysis and Its Applica-tion. New York: Wiley.

Bierens, H. (1982). Consistent model specification tests. Journal of Econometrics, 20, 105-134.

Bierens, H. (1990). A consistent conditional moment test of functional form. Econo-metrica, 58, 1443-1458.

Bierens, H., Ploberger, W. (1997). Asymptotic Theory of Integrated Conditional Moment Tests. Econometrica, 65, 1129-1151.

Bierens, H., Ginther, D. (2001). Integrated conditional moment testing of quantile regression models. Empirical Economics, 26, 307-324.

Chang, S.K., (2007). The asymptotic global power comparisons of the GMM overi-dentifying restrictions tests. Working Paper, Wayne State University.

Chang, S.K., (2005). The approximate slopes and the power of the GMM overiden-tifying restrictions. Applied Economics Letters, 12, 845-848.

Crainiceanu, C., Vogelsang, T. (2007). Nonmonotonic power for tests of a mean shift in a time series. Journal of Statistical Computation and Simulation, 457-476.

Deng, A., Perron, P. (2008). A non-local perspective on the power properties of the CUSUM and CUSUM of squares tests for structural change. Journal of Econometrics, 142, 212-240.

Flachaire, E., (2005). More efficient tests robust to heteroskedasticity of unknown form. Econometrics Reviews, 24, 219-241.

Godfrey, L.G., Orme, C.D., (2004). Controlling the finite sample significance levels of heteroskedasticity-robust tests of several lineaar restrictions on regression

coefficients. Econometrics Letters, 82, 281-287.

Godfrey, L.G., (2006). Tests for regression models with heteroskedasticity of un-known form. Computation Statistics and Data Analysis, 50, 2715-2733.

Goncalves, S., White, H., (2005). Bootstrap standard error estimates for linear regression. Journal of the American Statistical Association, 100, 970-979.

Hall, A.R., (2000). Covariance matrix estimation and the power of the overidenti-fying restrictions test. Econometrica, 68, 1517-1527.

Hall, A.R., Inoue, A., (2003). The large sample behaviour of the generalized method of moments estimator in misspecified models. Journal of Econometics, 114, 361-394.

Hall, A.R., Inoue, A., Peixe, F.P.M., (2003). Covariance matrix estimation and the limiting behavior of the overidentifying restrictions test in the presence of neglected structural instability. Econometric Theory, 19, 962-983.

Hauck, W.m., Donner, A., (1977). Wald’s test as applied to hypotheses in logit analysis. Journal of American Statistical Association, 72, 851-853.

Juhl, T., Xiao, Z. (2009). Tests for changing mean with monotonic power. Journal of Econometrics, 148, 14-24.

MacKinnon, J.G., White, H., (1985). Some heteroskedasticity-consistent covariance matrix estimators with improved finite sample properties. Journal of Econo-metrics, 29, 305-325.

Nelson, F.D., Savin, N.E., (1990). The danger of extrapolating asymptotic local power. Econometrica, 58, 977-981.

Newey, W. (1985). Maximum likelihood specification testing and conditional mo-ment tests. Econometrica, 53, 1047-1070.

Newey, W., West K. (1987). A simple positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix, Econometrica, 55, 703-708.

Sul, D., Phillips, P.C.B., Choi, C.T., (2005). Prewhitening bias in HAC estimation. Oxford Bulletin of Economics and Statistics, 67, 517-546.

models. Journal of Econometrics, 30, 415-443.

Vogelsang, T. (1999). Sources of nonmonotonic power when testing for a shift in mean of a dynamic time series. Journal of Econometrics, 88, 283-299.

White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity, Econometrica, 48, 817-838.

Wooldridge, J. (1990). A unified approach to robust, regression-based specification. Econometric Theory, 6, 17-43.

Zheng, J. (1998). A consistent nonparametric test of parametric regression models under conditional quantile restrictions. Econometric Theory, 14, 123-138.

國科會補助計畫衍生研發成果推廣資料表

日期:2011/10/28國科會補助計畫

計畫名稱: 型一誤差重要還是檢定力重要?條件動差檢定中的非單調檢定力問題 計畫主持人: 林馨怡 計畫編號: 99-2410-H-004-057- 學門領域: 數理與數量方法無研發成果推廣資料

99 年度專題研究計畫研究成果彙整表

計畫主持人:林馨怡 計畫編號: 99-2410-H-004-057-計畫名稱:型一誤差重要還是檢定力重要?條件動差檢定中的非單調檢定力問題 量化 成果項目 實際已達成 數(被接受 或已發表) 預期總達成 數(含實際已 達成數) 本計畫實 際貢獻百 分比 單位 備 註 ( 質 化 說 明:如 數 個 計 畫 共 同 成 果、成 果 列 為 該 期 刊 之 封 面 故 事 ... 等) 期刊論文 0 0 100% 研究報告/技術報告 1 1 100% 研討會論文 0 0 100% 篇 論文著作 專書 0 0 100% 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 0 0 100% 博士生 0 2 100% 博士後研究員 0 0 100% 國內 參與計畫人力 (本國籍) 專任助理 0 0 100% 人次 期刊論文 0 1 100% 研究報告/技術報告 0 0 100% 研討會論文 0 0 100% 篇 論文著作 專書 0 0 100% 章/本 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 0 0 100% 博士生 0 0 100% 博士後研究員 0 0 100% 國外 參與計畫人力 (外國籍) 專任助理 0 0 100% 人次其他成果