行政院國家科學委員會專題研究計畫 成果報告

住宅抵押貸款提前清償風險與違約風險之分析與評價:理

論與實證(第 2 年)

研究成果報告(完整版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 95-2416-H-004-035-MY2 執 行 期 間 : 96 年 08 月 01 日至 97 年 07 月 31 日 執 行 單 位 : 國立政治大學金融系 計 畫 主 持 人 : 廖四郎 計畫參與人員: 碩士班研究生-兼任助理人員:曾彥勝 博士班研究生-兼任助理人員:陳鴻隆 博士班研究生-兼任助理人員:張瑞珍 處 理 方 式 : 本計畫涉及專利或其他智慧財產權,2 年後可公開查詢中 華 民 國 97 年 10 月 29 日

行政院國家科學委員會補助專題研究計畫

■ 成 果 報 告

□期中進度報告

Pricing Mortgage Value and Analysis of Prepayment and Default Risks: Theory

and Empirical Evidence

住宅抵押貸款提前清償風險與違約風險之分析與評價:理論與實證

計畫類別:█ 個別型計畫 □ 整合型計畫

計畫編號:NSC 95-2416-H-004-035-MY2

執行期間: 96 年 8 月 1 日至 97 年 7 月 31 日

計畫主持人:

廖四郎

計畫參與人員: 張瑞珍、陳鴻隆、曾彥勝

成果報告類型(依經費核定清單規定繳交):█精簡報告 □完整報告

本成果報告包括以下應繳交之附件:

□赴國外出差或研習心得報告一份

□赴大陸地區出差或研習心得報告一份

□出席國際學術會議心得報告及發表之論文各一份

□國際合作研究計畫國外研究報告書一份

處理方式:除產學合作研究計畫、提升產業技術及人才培育研究計畫、列管計畫

及下列情形者外,得立即公開查詢

□涉及專利或其他智慧財產權,□一年□二年後可公開查詢

執行單位:國立政治大學金融系

中 華 民 國 97 年 10 月 29 日

行政院國家科學委員會專題研究計畫成果報告

Pricing Mortgage Value and Analysis of Prepayment and Default Risks: Theory

and Empirical Evidence

住宅抵押貸款提前清償風險與違約風險之分析與評價:理論與實證

計畫編號:

NSC 95-2416-H-004-035-MY2

執行期限:

96年8月1日至97年7月31日

主持人:廖四郎 國立政治大學金融學系

(第二年計畫)

I. Abstract

The possibility of early termination complicates the pricing procedure of a mortgage and hedging efficiency. Thus, most mortgage market practitioners and academic researchers are concerned with the investigation on prepayment and default risks by theoretical models and empirical analyses. Since different borrowers’ characteristics will determine their termination decisions at different circumstances, the suboptimal exercise of the termination option in a mortgage is a common phenomenon. This study intends to use the mortgage data to analyze the prepayment and default risks by the threshold model. Through the threshold estimates of different variables, we can analyze the changes in the effects of the important variables on the intensities of prepayment and default at below and above the threshold values. We further embed the concept of the threshold into our theoretical pricing model. Using this model we can appraise mortgage more accurately. Furthermore, we also perform our model by using the mortgage historical data and analyze the changes inn the mortgage value based on OLS model and threshold model with different threshold variables.

中文摘要

由於住宅抵押貸款人的提前清償及違約風險所造成貸款契約終止不確定性,使之加深評價過程之 複雜性。因此,許多貸款市場參與者與學者經由理論模型與實證分析的方法進行關於提前清償及違約 風險的研究。再者,因不同貸款人的一些特質會影響其做終止貸款契約之決策,使得提前清償及違約 選擇權常常是在次佳情況被履行成為一種常見之現象。本計畫即利用門檻模型進行提前清償及違約風 險之研究。透過模型估計之各個不同變數之門檻值及其參數值,可分析在門檻變數的何種水準下借款 人行為會產生明顯的轉變,以及在門檻值前後重要變數對提前清償與違約強度之影響。本研究進一步 的將此概念加入評價模型中,並且透過住宅抵押貸款的實際資料進行模型之實証估計。透過此方法可 更準確的評價住宅抵押貸款的價值。此外,本研究亦將透過數值分析方式進行不同模型與不同門檻變 數下,對住宅抵押貸款價值之影響分析。 關鍵字:提前清償,違約,門檻模型,縮減式模型Ⅱ. Introduction

Most mortgage market practitioners and academic researchers are concerned with how to measure the value of a mortgage with prepayment and default risks, since the mortgage market is increasing in importance in the domestic and overseas financial markets. The possibility of early termination complicates the pricing procedure of a mortgage. Thus, the lenders and the risk manager for their holdings have a demand to evaluate the complicated mortgage securities and estimate the probabilities of prepayment and default by appropriate analytical techniques. This study intends to use the threshold model to investigate the prepayment and default risks, and then extend the model that will be derived in the first year of this project by embedding the concept of threshold. Moreover, we will also implement the valuation model through market data and investigate the influences of various variables on the mortgage value by numerical analyses.

There are many factors affecting the borrower’s prepayment or default behavior provided by some previous researches. For instance, higher house prices will increase the likelihood of prepayment and decrease the probability of default, as a borrower will make the decision that offers the greatest benefit. Recently, some studies use a backward finite technique to determine the prepayment and default hurdle rates of the different relevant variables, and then adopts them to estimate the probabilities of prepayment and default and appraise the mortgage or specify the critical termination boundary through contingent-claims model (see, Yang, Buist

and Megbolugbe (1998), Buist and Yang (1998), Deng, Quigley and Van Order (2000)). The borrowers have incentives not to ruthlessly choose to prepay or default for avoiding a bad credit rating and prepayment penalty. They decide to prepay or default only at the low or high enough level of relevant variables (such as, interest rate, house price and income).

Furthermore, most literature investigates how the phenomenon of “burnout” affects the prepayment model estimation (see, for example,Archer and Ling (1993), Hall (2000), Charlier and Van Bussel (2003)). Those more likely to prepay tend to leave earlier, leading the mortgage pool to be increasingly concentrated in borrowers who are unlikely to prepay and therefore to have a lower prepayment rate. This phenomenon results from the heterogeneity of borrowers since the different borrower’s characteristics (such as, temperament, knowledge, or risk preference) lead to their prepayment decisions at different level of interest rate. Similarly, the influences of the heterogeneity of borrowers not only on prepayment risk but also on default risk are significant. Many researchers have proposed the important relevant variables as sources of unobserved heterogeneity in prepayment and default behaviors (see, for example, Schwartz and Torous (1989, 1993), Ciochetti et al. (2003), and Ambrose and Sanders (2003)). Therefore, there are the changes in the effects of the important variables on the intensities of prepayment and default at below and above the critical values of threshold variables. For this reason and to fit the market data well, we will attempt to investigate the most significant factors that influence the probabilities of default and prepayment and calculate the mortgage value using threshold model.

Ⅲ. Model

Description

1. The Model for Analyzing Prepayment and Default Risks 1.1 Threshold model

In this research, we focus the investigation on a fixed-rate mortgage (FRM), which is the basic building block of the mortgage market, time to maturity of T years. Chan (1993) showed that the least squares estimator of the threshold is super-consistent and derived its asymptotic distribution. To investigate the prepayment and default risks, we use least squares estimation to estimate the threshold model, and adopt the bootstrap procedure by Hansen (1996) obtain the desired critical value that can be used to test whether there is threshold effect. Hence, the hazard rates of default and prepayment are assumed to be linear functions of the various relevant variables, such as interest rate, house price, income, and so on.

1.2 Estimation and Testing Threshold

For estimating the parameters, we can adopt ordinary least squares (see, Chan(1993)). Then, the estimates of the thresholds of prepayment and default can be calculated by minimizing the concentrated sum of squared errors.

Using the threshold model to investigate the prepayment and default risks, the most important thing is to test whether the threshold effect is statistically significant. The hypothesis of no threshold effect in Equations (1) and (2) can be presented by the linear constraints:

2 1 0 :λ =λ p H , 2 1 0 :k k Hd = .

Consequently, Hansen (1996) suggested a bootstrap procedure to simulate the asymptotic distribution of the likelihood ratio test. As we know, under the null hypothesis of no threshold. The likelihood ratio tests of H0p

and H0d are based on

p p p p p S S F σ ψ ˆ ) ˆ ( 1 0 1 − = , (1) d d d d d S S F σ ψ ˆ ) ˆ ( 1 0 1 − = . (2)

We then use a bootstrap procedure to obtain the asymptotic distributions of F1p and F1d. The critical values constructed from the bootstrap are asymptotically valid under p

H0 and

d

H0 . The null of no threshold

effect is rejected if the p-value is smaller than the desired critical value.

We will use the mortgage market data of FRM to analyze the prepayment and default risks through this model. From the empirical study of whether the influence of the relevant variables on intensities of prepayment and default are statistically significant, we can determine the key factors that affect the termination mortgage. Furthermore, one can investigate under what circumstances that the borrower’s choice to prepayment or default will depend on the threshold value of various variables.

2. The Valuation Model

In this part, we will extend the theoretical model that is derived in the first year of this project and use the market data to perform this model. This model focuses the investigation on a fixed-rate mortgage (FRM),

which is a fully amortized mortgage, having an initial mortgage principal M0, with a fixed coupon rate c

and time to maturity of T years. This study employs the intensity-form approach to evaluate the termination risk since the intensity-form approach captures the probabilities of prepayment and default accurately through market data. If the testing results indicate that there are threshold effects, the intensity of prepayment θt and intensity of default πt are set as

p nt n t t r t λ λ r λ e λ e t ς θ = 10 + 1 1 + 11 11 +"+ 1 1 , ≤ , (3) ) ) 1 ( ( ) ) 1 ( ( 1 2 21 11 1 21 1 2 20 r rt Ir rtIr e t I e tI t =λ +λ − + +λ − + θ p n nt n nt n e I e I t ς λ − + > + +" 2 ( 1 (1 ) 2 ), , (4) and d nt n t t r t k k r k e k e t ς π = 10+ 1 1 + 11 11 +"+ 1 1 , ≤ , (5) ) ) 1 ( ( ) ) 1 ( ( 1 2 21 11 1 21 1 2 20 k r I r I k e I e I k r t r t r t t t = + − + + − + π p n nt n nt n e I e I t k − + >ς + +" 2 ( 1 (1 ) 2 ), , (6) where λ10,λ20,λ1r,λ2r,",λ2n,k10,k20,k1r,k1r,"k2nare constants. The first numeral of the parameter’s index

“ 1” and “2” represent before and after the time ςp and ςd.Ir,I1,",In are indicator variables. That is, if the variable is the threshold variable in the threshold model, its value is one; otherwise, its value is zero. Given these expressions, the value of the mortgage can be rewritten as

ds

e

E

Y

V

T Q A u du A u du A u du s T∫

⎥

⎥

⎦

⎤

⎢

⎢

⎣

⎡ ∫

∫

∫

=

∧ ∨ ∧ + ∨ + − 0 ) ) ( ) ( ) ( ( 0 0 d p 0 d p d p 2 p d 3 1 ς ς ς ς ς ς ς ς , ⎥ ⎥ ⎦ ⎤ ⎢ ⎢ ⎣ ⎡ ∫ ∫ ∫ +∫

∫

∧ ∨ ∧ + ∨ + − T t du u A du u A du u A s Q t T t MsE he ds s T ) ) ( ) ( ) ( ( d p 0 d p d p 2 p d 3 1 ς ς ς ς ς ς ς ς ⎥ ⎥ ⎦ ⎤ ⎢ ⎢ ⎣ ⎡ ∫ ∫ ∫ − +∫

∫

∧ ∨ ∧ + ∨ + − T t du u A du u A du u A s Q t T t Ms l E e ds s T ) ) ( ) ( ) ( ( d p 0 d p d p 2 p d 3 1 ) 1 ( ς ς ς ς ς ς ς ςπ

, (7) where A1(u)=g10 +g1rr11u +g11e11u+"+g1ne1nu ) ) 1 ( ( ) ) 1 ( ( ) ) 1 ( ( ) ( 2 1 22 1 21 2 22 2 12 221 11 211 1 21 1 11 22 11 21 20 2 n nu n nu n nu n u u u u u r u r I r I r g e g I r I r g e g I r I r g r g g u A + − + + + − + + + − + + = " nu n u u rr g e g e g g u A3( )= 30 + 3 2 + 31 21 +"+ 3 2 Moreover, we denote g10 =λ10+k10, g1r =1+λ1r +k1r, g11 =λ11+k11, " , g1n =λ1n +k1n. If ςp >ςd ,then g20 =λ20+k10, g21r =λ2r, g22r =1+k1r, g211=λ21 g221=k11, ",g22n =k1n . Alternatively, if d p ς ς > ,theng20 =λ10 +k20 , g21r = k2r, g22r =1+λ1r, g211 =k21, g221 =λ11,", n n g22 =λ1 ,g30 =λ20 +k20 ,g3r = 1+λ2r +k2r, g31 =λ21 +k21, ", g3n =λ2n +k2n.

In the following section, we will implement the threshold model and valuation model to analyze the impact of various parameters on the risks of prepayment and default, and the value of the mortgage through empirical analysis.

Ⅳ

. Empirical AnalysisIn this study, we adopt the mortgage market data provided by Freddie Mac and the other macroeconomic data adopted by DataStream to investigate the termination risk. From the statistical results, one can analyze how the relevant variables influence the intensities of prepayment and default, and obtain the important factors that affect the termination risk. We further employ the best performance model to estimate the risks of prepayment and default by comparing the MESs of the model with thresholds of different variables. Moreover, one can investigate the critical values of the borrower’s decision to prepayment or default through the thresholds of various variables. We incorporate the threshold effect into our pricing framework, and then the fair value of mortgage can be obtained using our model. In this study, another important task is to present and discuss how the changes of the parameters in the processes of relevant variables and to make a contrast with the results of the model with threshold and the model without threshold.

The latest studies on mortgages focus on how to appropriately estimate the parameters for the probabilities of prepayment and default using Cox’s proportional hazard model, or Poisson regression. They investigate the most significant factors that influence the probabilities of default and prepayment, such as interest rates, loan-to-value ratio, house price, debt service coverage ratio, salary (see, for example, Schwartz and Torous (1989, 1993), Quigley and Van Order (1990, 1995), Lambrecht, Perraudin and Satchell (2003)). Thus, according to these empirical results, there are ten variables denoted as explanatory variables including in our prepayment and default hazard regressions. They are shown in Table 1.

Table 1 The Parameters Illustration

Short name Description

t

TR 10-year Treasury rate (%)

t

SP Yield spread between Aaa and Baa rated coporate bonds (%)

t

LTV Loan-to-price ratio

t

HPI House prices index

t

MO Mortgage debt outstanding ($ thousands)

t

DSR Household debt service ratio

t

GDP Gross domestic product ($ 100 billions)

t

PI Personal Income ($ 100 billions)

t

CPI Consumer price index

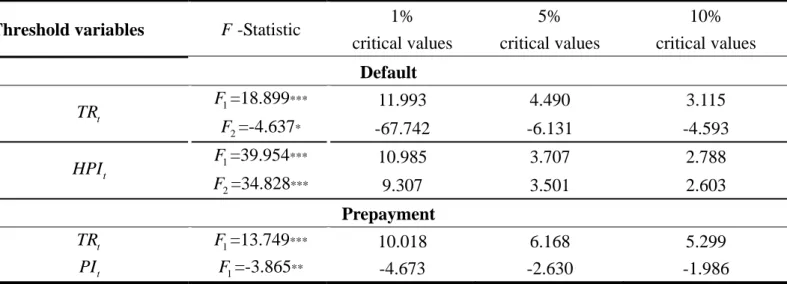

In order to determine the number of thresholds, Equations (3), (4), (5) and (6) are estimated by ordinary least squares, allowing for (sequentially) zero, one, and two thresholds. The test statistics F1 and F2 along with their bootstrap 1%, 5% and 10% critical values are shown in table 2. We choose TRt and HPIt as the threshold variables in default hazard regression, and TRt and PIt as the threshold variables in prepayment hazard regression. The results show that the test for a single threshold F1 is strongly significant for two hazard functions. The test for a double threshold F2 is significant for default hazard regression. We conclude that there is strong evidence that there are thresholds in the two hazard functions.

Table 2 Tests for Threshold Effects

Threshold variables F -Statistic 1% critical values 5% critical values 10% critical values Default 1 F =18.899*** 11.993 4.490 3.115 t TR 2 F =-4.637* -67.742 -6.131 -4.593 1 F =39.954*** 10.985 3.707 2.788 t HPI 2 F =34.828*** 9.307 3.501 2.603 Prepayment t TR F1=13.749*** 10.018 6.168 5.299 t PI F1=-3.865** -4.673 -2.630 -1.986

Notes: ***, ** and * denote significance at 1%, 5% and 10% levels respectively.

According to the test for threshold effects, the threshold variable values for TRt, HPIt, TRt and PIt

can be found. The estimated values of the model with thresholds are presented in Table 3. The most important feature is clearly the difference in the behavior of the series in each regime. The results show that the influences of threshold variables on the prepayment and default hazard rates are greater in the first regime than that in other regimes. The influences of threshold variables on the default hazard rate are second significant in the third regime. We can infer that the threshold variables have different influences for the

prepayment and default hazard rates in the different regimes.

Table 3 Estimated coefficients of the prepayment and default regressions by the OLS model and the OLS model with thresholds

OLS model Threshold model

Default Prepayment Default Prepayment

Threshold variables Threshold variables Variables TRt HPIt TRt PIt 1 I =4.65 2 I =6.48 1 I =121.38 2t I =186.12 1 I =3.87 I1t=88.14 1t th (wt ≤ ) I1 0.470*** 0.595*** 0.252* -0.174** (1101.765) (848.066) (2.956) (-10.818) 2t th (I1<wt ≤I2 or I1< ) wt 0.035** 0.015 0.139 -0.156*** (11.925) (3.730) (1.637) (-10.352) 3t th ( I2 < ) wt -0.096*** 0.188*** (-1578.342) (47.656) c 0.050*** 5.845 0.064** 0.028 0.635 0.244*** (3.157) (1.828) (10.452) (4.555) (5.229) (6.709) t TR 0.456*** 0.415*** 0.009 -0.852*** (5.215) (4.004) (2.592) (-11.739) t HPI 0.026*** -0.348*** -0.075** 0.094 -0.013 (3.203) (-8.451) (-16.867) (1.943) (-3.339) t SP -0.016*** 0.681*** -0.003 0.026** 0.941*** -0.044 (-3.395) (9.528) (-2.150) (9.025) (16.341) (-3.861) t LTV -0.166*** -0.349*** -0.193*** -0.066** 0.133** 0.137*** (-4.333) (-3.138) (-43.098) (-17.167) (8.477) (6.023) t MO -0.022*** 0.009 -0.009* -0.029*** -0.087*** -0.085 (-2.750) (0.323) (-3.633) (-5.336) (-4.413) (-2.332) t DSR 0.023 -0.103** 0.011** 0.039*** 0.302** -0.034 (1.466) (-2.238) (2.893) (4.135) (2.977) (-2.981) *** t GDP -0.011 0.061 -0.028** 0.011* 0.382*** 0.046 (-1.158) (0.449) (-7.325) (2.774) (11.133) (1.554) t PI 0.421 -0.206*** 0.074*** 0.110*** -0.215*** (1.417) (-8.195) (129.154) (156.584) (-6.459) t CPI 0.579** 0.023 0.229*** 0.890*** 0.698 0.953*** (2.254) (0.529) (535.901) (7748.467) (3.279) (5.632) Notes: ***, ** and * denote significance at 1%, 5% and 10% levels respectively. The values inbrackets are t-ratios. wt represents

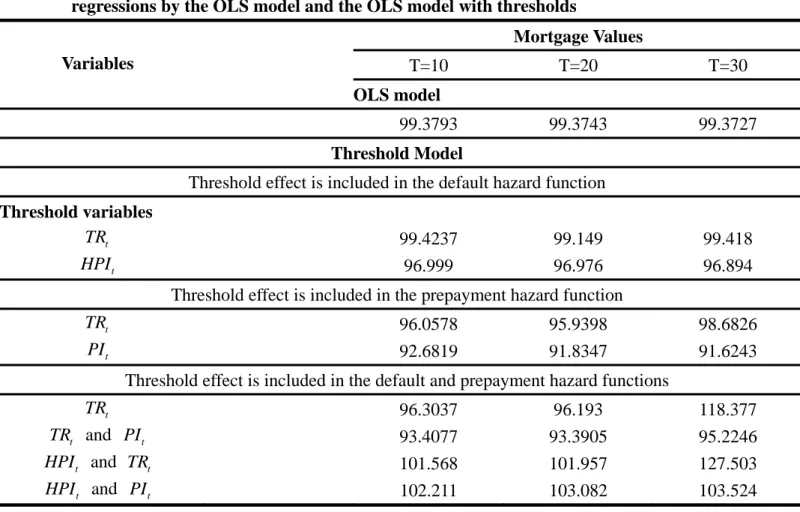

Table 4 Calculated mortgage values based on estimated the coefficients of the prepayment and default regressions by the OLS model and the OLS model with thresholds

Mortgage Values

Variables T=10 T=20 T=30

OLS model

99.3793 99.3743 99.3727 Threshold Model

Threshold effect is included in the default hazard function Threshold variables

t

TR 99.4237 99.149 99.418

t

HPI 96.999 96.976 96.894

Threshold effect is included in the prepayment hazard function

t

TR 96.0578 95.9398 98.6826

t

PI 92.6819 91.8347 91.6243 Threshold effect is included in the default and prepayment hazard functions

t TR 96.3037 96.193 118.377 t TR and PIt 93.4077 93.3905 95.2246 t HPI and TRt 101.568 101.957 127.503 t HPI and PIt 102.211 103.082 103.524 We put the estimated parameter values into the mortgage valuation model (i.e. Equation (7)) to discuss the mortgage values under different situations. According to table 4, the mortgage values estimated by the threshold model including the prepayment hazard function with threshold effect are lower than these values estimated by the OLS model and the threshold model including the default hazard function with threshold effect. Thus, we can infer that the threshold effect embedded into the hazard functions, the influence of the threshold effect embedded into the prepayment hazard function on the mortgage values is greater than the influence of the threshold effect included into the default hazard function on the mortgage values.

When threshold effects are simultaneously included in the default and prepayment hazard functions, the estimated mortgage values calculated by threshold model including the threshold variables HPIt and TRt,

and HPIt and PIt are larger than that estimated by OLS model. Alternatively, the estimated mortgage values calculated by threshold model including the threshold variables TRt, and TRt and PIt are lower

than that estimated by OLS model. The estimated mortgage values are significant difference between the OLS model and the threshold models expect for the threshold models including the TRt threshold variable. We

V. Conclusion

Most mortgage market practitioners and academic researchers are concerned with how to accurately measure the mortgage value by reasonably model prepayment and default risks. There are many factors affecting the borrower’s prepayment or default behavior provided by some previous researches. Thus, this study intends to be able to appropriately price the mortgage by embedding the concept of the threshold into our pricing framework. This modeling framework provides a more appropriate approach to estimate the termination probability and price the mortgage value. Also, this approach values the complicated mortgage more accurately and efficiently. Furthermore, the estimated mortgage values are significant difference between the OLS model and the threshold models expect for the threshold models including the TRt threshold variable. Therefore, we can conclude that the threshold effect needs to be considered when one prices the mortgage value. This valuation method also provides a useful tool for the investors and mortgage portfolio management to undertake the hedging analysis and determine their investing strategies.

Ⅵ. Evaluation of the Study

Many researchers have proposed the important relevant variables as sources of unobserved heterogeneity in prepayment and default behaviors. Therefore, there are the changes in the effects of the important variables on the intensities of prepayment and default at below and above the critical values of threshold variables. In order to appropriately price the mortgage based on the reasonable prepayment and default hazard functions, we attempt to investigate the most significant factors that influence the probabilities of default and prepayment, and then calculate the mortgage value according to the estimated parameter values by the threshold model. From our calculated results, we find that the threshold effect indeed influences the estimated mortgage values. Thus, the threshold effect needs to be considered into the model when one prices the mortgage value. The main contribution of this study is to provide a more appropriate approach to estimate the termination probability and more accurately and efficiently price the mortgage value. Our results also provide further information about the borrower’s behavior of prepayment and default, and the termination risk of a mortgage.

References

Ambrose, B.W. and C. A. Capone. 2000. The Hazard Rates of First and Second Defaults. Journal of Real Estate Finance and Economics 20(3): 275-293.

Ambrose, B.W. and R.J. Buttimer, JR.. 2000. Embedded Options in the Mortgage Contract. Journal of Real Estate Finance and Economics 21(2): 95-111.

Ambrose, B.W. and A.B. Sanders. 2003. Commercial Mortgage-Backed Securities: Prepayment and Default. Journal of Real Estate Finance and Economics 26(2/3): 179-196.

Archer, W .R. and D. C. Ling. 1993. Pricing Mortgage-Backed Securities - Integrating Optimal Call and Empirical-Models of Prepayment. AREUEA Journal 21 (4): 373-404.

Archer, W .R., D. C. Ling and G. A. McGill. 1997. Demographic versus Option-Driven Mortgage Terminations. Journal of Housing Economics 6: 137-163.

Archer, W .R., D. C. Ling and G. A. McGill. 2003. Housing Income, Termination Risk and Mortgage Pricing. Journal of Real Estate Finance and Economics 27(1): 111-138.

Azevedo-Pereira, J.A., D.P. Newton and D.A. Paxson. 2003. Fixed-Rate Endowment Mortgage and Mortgage Indemnity Valuation. Journal of Real Estate Finance and Economics 26(2/3): 197-221.

Buist, H. and T. T. Yang. 1998. Pricing the Competing Risks of Mortgage Default and Prepayment in Stochastic Metropolitan Economies. Managerial Finance 24 (9/10): 110-128.

Capozza, D.R., D. Kazarian and T.A. Thomson. 1998. The Conditional Probability of Mortgage Default. Real Estate Economics 26(3): 359-389.

Chan, K. S.. 1993. Consistency and Limiting Distribution of the Least Squares Estimator of a Threshold Autoregressive Model. The Annals of Statistics 21: 520-533.

Charlier, E. and A. Van Bussel. 2003. Prepayment Behavior of Dutch Mortgagors: An Empirical Analysis. Real Estate Economics 31 (2): 165-204.

Ciochetti, B.A., Y. Deng, G. Lee, J.D. Shilling, R. Yao. 2003. A Proportional Hazards Model of Commercial Mortgage Default with Originator Bias. Journal of Real Estate Finance and Economics 27(1): 5-23.

Clapp, J.M., G..M. Goldberg, J.P. Harding and M. LaCour-Little. 2001. Movers and Shuckers: Interdependent Prepayment Decisions. Real Estate Economics 29(3): 411-450.

Cox, D.R. and D. Oakes. 1984. Analysis of Survival Data . London: Chapman and Hall.

Collin-Dufresne, P. and J.P. Harding. 1999. A Closed Form Formula for Valuing Mortgages. Journal of Real Estate Finance and Economics 19(2): 133-146.

Deng, Y., J.M. Quigley and R. Van Order. 1996. Mortgage Default and Low Downpayment Loans: The Costs of Public Subsidy. Regional Science and Urban Economics 26: 263-285.

Duffie, D. and K.J. Singleton. 1999. Modeling Term Structures of Defaultable Bonds. The Reviews of Financial Studies 12(4): 687-720.

Hall, A. 2000. Controlling for Burnout in Estimating Mortgage Prepayment Models. Journal of Housing Economics 9 (4): 215-232.

Hansen, B. E.. 1996. Inference When a Nuisance Parameter is not Identified under the Null Hypothesis. Econometrica 64: 413-430.

Heath, D., R. Jarrow and A. Merton. 1992. Bond Pricing and the Term Structure of Interest Rates: A New Methodology for Contingent Claims Valuation. Econometrica 60: 77-106.

Hilliard, J.E., J.B. Kau and V.C. Slawson, Jr.. 1998. Valuing Prepayment and Default in a Fixed-Rate Mortgage: A Bivariate Binomial Options Pricing Technique. Real Estate Economics 26(3): 431-468. Jarrow, R. and S. Turnbull. 1995. Pricing Options on Financial Securities Subject to Default Risk. Journal of

Finance 50: 481-523.

Jarrow, R. 2001. Default Parameter Estimation Using Market Prices. Financial Analysis Journal 5: 74-92. Kau, J.B., D.C. Keenan, W.J. Muller,Ⅲ and J.F. Epperson. 1990. Pricing Commercial Mortgages and Their

Mortgage-Backed Securities. Journal of Real Estate Finance and Economics 3(4): 333-356.

Kau, J.B., D.C. Keenan, W.J. Muller,Ⅲ and J.F. Epperson. 1992. A Generalized Valuation Model for Fixed-Rate Residential Mortgages. Journal of Money, Credit and Banking 24(3): 279-299.

Kau, J.B., D.C. Keenan, W.J. Muller,Ⅲ and J.F. Epperson. 1993. Option Theory and Floating-Rate Securities with a Comparison of Adjustable- and Fixed-Rate Mortgages. Journal of Business 66: 595-618.

LaCour-Little, M. and S. Malpezzi. 2003. Appraisal Quality and Residential Mortgage Default: Evidence from Alska. Journal of Real Estate Finance and Economics 27(2): 211-233.

Lambrecht, B.M., W.R.M. Perraudin and S. Satchell. 2003. Mortgage Default and Possession Under Recourse: A Competing Hazards Approach. Journal of Money, Credit and Banking 35(3): 425-442.

Lancaster, Tony. 1992. The Econometric Analysis of Transition Data. Cambridge pressed.

Quigley, J. and R. Van Order. 1990. Efficiency in the Mortgage Market: The Borrower’s Perspective. AREUEA Journal 18(3): 237-252.

Quigley, J. and R. Van Order. 1995. Explicit Tests of Contingent Models of Mortgage Default. Journal of Real Estate Finance and Economics 11(2): 99-117.

Schwartz, E.S. and W.N. Torous. 1989. Prepayment and the Valuation of Mortgage-Backed Securities. Journal of Finance 44: 375-392.

Schwartz, E.S. and W.N. Torous. 1993. Mortgage Prepayment and Default Decisions: A Poisson Regression Approach. AREUEA Journal 21(4): 431-449.

177-188.

Yang, T.T., H. Buist and I.F. Megbolugbe. 1998. An Analysis of the Ex Ante Probabilities of Mortgage Prepayment and Default. Real Estate Economics 26(4): 651-676.