行政院國家科學委員會補助專題研究計畫成果報告

期末報告

審計失敗對簽證合夥會計師聲譽的影響

計 畫 類 別 : 個別型計畫 計 畫 編 號 : NSC 101-2410-H-004-073- 執 行 期 間 : 101 年 08 月 01 日至 102 年 10 月 31 日 執 行 單 位 : 國立政治大學會計學系 計 畫 主 持 人 : 戚務君 計畫參與人員: 碩士班研究生-兼任助理人員:陳韋伶 碩士班研究生-兼任助理人員:彭珮欣 碩士班研究生-兼任助理人員:林姿均 碩士班研究生-兼任助理人員:黃敏雄 博士班研究生-兼任助理人員:謝昇樺 博士班研究生-兼任助理人員:陳漢鐘 報 告 附 件 : 出席國際會議研究心得報告及發表論文 處 理 方 式 : 1.公開資訊:本計畫涉及專利或其他智慧財產權,1 年後可公開查詢 2.「本研究」是否已有嚴重損及公共利益之發現:否 3.「本報告」是否建議提供政府單位施政參考:否中 華 民 國 103 年 02 月 21 日

中 文 摘 要 : 以受查客戶的財務報表發生重編做為審計品質不佳的代理變 數,本文檢視若簽字會計師於某特定客戶的審計品質不佳, 是否會全面性影響該會計師未來其他客戶的盈餘品質。這個 計畫的研究動機係源於美國 Public Companies Accounting Oversight Board(PACOB)於 2011 年 10 月關於要求應於審計 報告揭露提供審計服務之合夥會計師姓名。PCAOB 相信這個 規定若能實施,基於以下二項理由;將提高財務報告的透明 度與審計品質。首先,對於提供審計服務的會計師而言,藉 由被財務報表使用者究責(accountability)的程度提高,會 使得該會計師更認真提高其審計服務的投入與品質。第二, 對於投資者而言,提供一個研讀財務報表是被誰簽證的有用 資訊,將會影響企業慎選簽字會計師的正面誘因。利用我國 簽證會計師之資訊係公開取得的特性,本研究擬利用財務報 表重編事件,去分析當某位合夥會計師的客戶發生「過去報 表係淨利高估的重編」,是否提高該簽證會計師未來其他客 戶的財務報表被重編的機率。除此之外,本計畫也預期股票 市場對被該會計師簽證之「其他」公司的股價,於發生該財 務報表重編時,會有負面的影響。期望藉由本計畫的完成可 以提供 PCAOB 關於財務報告是否應提供合夥會計師姓名的參 考。 中文關鍵詞: 審計失敗、會計師聲譽、合夥會計師、財務報表重編

英 文 摘 要 : Using data from Taiwan where audit partner names are disclosed, we examine whether an audit partner's reputation, as measured by prior misstatements of clients' annual financial statements, is informative about actual and perceived audit quality. With

respect to actual audit quality, we find that misstatements predict misstatements at the audit partner level in that the likelihood of an audit client misstating its financial statements in the current (or subsequent) year is significantly higher when at least one of its audit partner's clients misstated its annual financial statements in the prior year. This effect is mitigated, however, for partners with more overall audit experience and with more industry-specific experience. In addition, the likelihood of an audit client misstating its

financial statements in a three year window is significantly higher when at least one of its audit partner's clients restated its annual financial

statements in the prior three years, suggesting that investors, audit committees, and regulators can use restatements as a signal of future audit quality at the audit partner level. With respect to perceived audit quality, we find that an audit partner's reputation for past client misstatements (revealed through financial statement restatements) is

associated with a larger decline in the audit partner's market share. Collectively, our results suggest that audit partner reputation is informative about actual and perceived audit quality, supporting the Public Company Accounting Oversight Board's proposal to disclose the names of audit partners in the United States. In addition, our results suggest that audit experience and industry-specific

experience are important determinants of audit quality at the audit partner level, and that these factors can mitigate of the relation between

partners' past misstatement histories and their future audit quality outcomes.

英文關鍵詞: audit failure, misstatements, restatements, audit partner reputation, audit quality

The Persistence of Audit Quality at the Partner Level and the Informativeness

of Audit Partner Reputation

Wuchun Chi

National Chengchi University [email protected]

Ling Lei Lisic George Mason University

[email protected] Linda A. Myers University of Arkansas [email protected] Mikhail Pevzner University of Baltimore [email protected] ____________________________________

We thank Dick Larsen, Matt Medlin, and participants at the AAA 2013 Auditing Section Midyear Meeting and at workshops at George Mason University and at National University of Singapore for their helpful insights. We thank Samwa Hsieh for excellent research assistance. Wuchun Chi gratefully acknowledges the financial support from National Science Council (101-2410-H-004-073), Linda Myers gratefully acknowledges financial support from the Garrison/Wilson Chair at the University of Arkansas, and Mikhail Pevzner gratefully acknowledges support from the EY Chair in Accounting at the University of Baltimore.

The Persistence of Audit Quality at the Partner Level and the Informativeness of Audit Partner Reputation

Abstract: Using data from Taiwan where audit partner names are disclosed, we examine whether an audit partner’s reputation, as measured by prior misstatements of clients’ annual financial statements, is informative about actual and perceived audit quality. With respect to actual audit quality, we find that misstatements predict misstatements at the audit partner level in that the likelihood of an audit client misstating its financial statements in the current (or subsequent) year is significantly higher when at least one of its audit partner’s clients misstated its annual financial statements in the prior year. This effect is mitigated, however, for partners with more overall audit experience and with more industry-specific experience. In addition, the likelihood of an audit client misstating its financial statements in a three year window is significantly higher when at least one of its audit partner’s clients restated its annual financial statements in the prior three years, suggesting that investors, audit committees, and regulators can use restatements as a signal of future audit quality at the audit partner level. With respect to perceived audit quality, we find that an audit partner’s reputation for past client misstatements (revealed through

financial statement restatements) is associated with a larger decline in the audit partner’s market share. Collectively, our results suggest that audit partner reputation is informative about actual and perceived audit quality, supporting the Public Company Accounting Oversight Board’s proposal to disclose the names of audit partners in the United States. In addition, our results suggest that audit experience and industry-specific experience are important determinants of audit quality at the audit partner level, and that these factors can mitigate of the relation between partners’ past misstatement histories and their future audit quality outcomes.

1

1. Introduction

In October 2011, the Public Company Accounting Oversight Board (PCAOB) proposed that U.S. companies disclose their engagement partners’ names on audit reports,1 arguing that

[a] requirement for the engagement partner to sign the audit report could improve audit quality in two ways. First, it might increase the engagement partner’s sense of accountability to financial statement users, which could lead him or her to exercise greater care in performing the audit. Second, it would increase transparency about who is responsible for performing the audit, which could provide useful information to investors and, in turn, provide an additional incentive to firms to improve the quality of all of their engagement partners.

The PCAOB’s position seems to imply that audit partner reputation is informative about audit quality. In addition, audit partner name disclosure is meant to increase the audit partner’s sense of accountability (King et al. 2012), suggesting that name disclosure could affect audit quality.

This proposal has received strong opposition from some audit practitioners. For example, a comment letter on the proposal written by Texas Society of Certified Public Accountants (TSCPA) states,2

the exposure draft, which poses numerous questions for review, is flawed, misguided, and is being proposed to correct inadequacies of those responsible for audit engagements by identifying them and publicizing a perceived perception of inappropriate or inadequate performance. In addition, … the proposed amendments would lead the public to think that a majority of audit partners in charge of audit engagements are inept or unconcerned with their professional responsibilities.

Interestingly, the TSCPA’s comment letter claims that the PCAOB’s exposure draft is based on “inconclusive research provided by the academic community” (TSCPA 2011, pg. 1). The sentiments in this comment letter are echoed by PCAOB board member Jeannette Franzel who, when the PCAOB re-proposed this standard in late 2013, stated,3

1 See http://pcaobus.org/Rules/Rulemaking/Docket029/2009-07-28_Release_No_2009-005.pdf.

2See “RE: Improving the Transparency of Audits: Proposed Amendments to PCAOB Auditing Standards and Form

2.” Available at: http://www.accountingtoday.com/news/TSCPAletterPCAOBImprovingTransparencyinAudits.php.

2

I'm starting to think that naming the audit engagement partner in the auditor's report is a solution in search of a problem. First, as I said, the objectives of this project are difficult to follow over its various iterations. Second, the current release does not articulate how the proposed solution addresses any particular problem; nor does it present an analysis of benefits that is supported by data. Finally, many questions remain unanswered about the potential costs and exposure of auditors to additional liability.

In addition, PCAOB board member, Jay Hanson expressed concerns disclosing the audit

partner’s name in the actual audit report, as opposed to in the PCAOB Annual Filing (Form 2) or in some other filing (e.g., the proxy statement) has not been proven beneficial and is potentially risky.4 Thus, it seems that some opponents are concerned about the potential for increased liability of audit partners especially given that substantial benefits from these disclosures are undocumented. However, according to PCAOB board member Lewis Ferguson, these benefits will come, at least in part, from a greater ability to collect information about audit partners’ past reputations for malfeasance. In particular, in his public remarks on the standard’s re-proposal, Mr. Ferguson stated,5

I do think over time, however, that information will be gathered about these auditor partners, probably by third-party information providers, including things like the industry experience of that auditor, the public companies with which the auditor has been associated, whether the auditor has been involved in … publicly-disclosed financial restatements, as well as information about the professional activities of the auditor. I believe that this would be useful information to investors. We certainly know that an increasing amount of information is available about other professionals such as doctors and lawyers…

Because prior research on the reputational effects of audit partner name disclosure is just beginning to emerge and therefore the evidence on the purported benefits of partner name

disclosure is scant,6 one of our goals is to provide additional evidence on whether such disclosure is informative. We posit that, as is the case with any professional service provider, an audit

4 See http://pcaobus.org/News/Speech/Pages/12042013_Hanson_Transparency.aspx. 5 See http://pcaobus.org/News/Speech/Pages/12042013_Ferguson_oral.aspx. 6 See, for example, the discussion of Knechel et al. (2013a) in Section 2.

3

partner’s reputation for the quality of his prior work matters. Specifically, we suggest that current and prospective audit clients care about the audit partner’s history of audit failures. Our second goal is to examine whether other mechanisms (i.e., an audit partner’s overall experience, industry-specific experience, or tenure with the client) can mitigate any reputational effects related to an audit partner’s past audit quality.

Using data from Taiwan, where audit partner names are disclosed, we examine whether audit partner reputation is informative about actual and perceived audit quality. We proxy for audit partner reputation using annual financial statement misstatements disclosed by clients for whom the audit partner was the partner in charge.7 First, we examine whether companies with an audit partner whose other clients misstated their annual financial statements in the past year are more likely to misstate their annual financial statements in the current year.8 We also examine whether an audit partner is more likely to lose market share when at least one of his clients restates in the current year. Additionally, we test whether a reputation for past restatements increases the likelihood of an audit partner misstating in the future. Finally, we examine whether these relations (if any) are affected by an audit partner’s overall experience, industry-specific experience, and tenure with the audit client.

Francis and Michas (2013) find that audit failures tend to cluster in audit offices. We suggest that this effect could occur because audit partners in those offices bring their unique human capital to the firm. If ability varies across audit partners or if audit partner compensation structures induce some audit partners to compromise audit quality, then audit failures should be

7 Note that we distinguish between misstatements (which are errors in financial reports) and restatements (which are

revealed misstatements) in our discussions and in our tests.

8 We examine this likelihood relative to companies with an audit partner whose other clients did not misstate their

4

concentrated at the audit partner level, but because partner-level data are not available in the U.S., Francis and Michas (2013) do not explore whether audit failures cluster by audit partner.

Prior research implies that individual management characteristics matter for financial reporting quality. For example, management’s propensity to commit fraud is linked to religious background (Dyreng et al. 2010), educational background, age, prior military service (Schrand and Zechman 2011), as well as equity incentives and power of the executives (Feng et al. 2011). Ge et al. (2011) also find that management “styles” affect company financial reporting policies. Taken together, these results suggest that management characteristics affect financial reporting quality. Similarly, we posit that audit partner characteristics should affect audit quality because these characteristics affect audit partners’ ability to detect their clients’ aggressive accounting choices as well as their willingness to allow clients to make these choices.

We argue that individual audit partners build reputations for audit quality. Consistent with this, Koch (2011) finds that sources of audit partner reputation (e.g., education and client or industry experience) affect audit pricing in Germany. In addition, research using data from Taiwan and Australia suggests that individual audit partner tenure and experience are associated with proxies for audit quality (Carey and Simnett 2006, Chen et al. 2008, Chin and Chi 2009).9 Similar results are found in the non-profit audit market (Feng et al. 2013).

We thus examine whether an audit partner’s reputation for past audit failures is reflected in actual and perceived audit quality. We find that the likelihood of a client misstating its financial statements in the current year is significantly higher if at least one of its audit partner’s other clients misstated their annual financial statements in the prior year. We also find that an

9 For example, Carey and Simnett (2006) find that in Australia, longer audit partner tenure is associated with greater

earnings management (e.g., higher levels of discretionary accruals and a higher propensity to meet or just beat earnings expectations) as well as a lower likelihood of issuing going concern opinions. Alternatively, Chen et al. (2008) find evidence consistent with audit partner tenure reducing earnings management in Taiwan.

5

audit partner with at least one client restatement in the current year is more likely to lose market share. Finally, we find that an audit partner’s misstatement history over the prior three years predicts future misstatements of her other clients over the subsequent three years, suggesting that investors, audit committees, and regulators can use revealed misstatements as a signal of future audit quality at the audit partner level. Overall, our study provides evidence that the disclosure of individual audit partner names is informative about future audit quality, providing indirect support for the PCAOB’s proposal to disclose audit partner names.

Our paper proceeds as follows. Section 2 reviews the literature and develops our

hypotheses. Section 3 describes our research design. Section 4 describes the sample selection and empirical results. Section 5 concludes.

2. Literature Review and Development of Hypotheses

Until recently, researchers have focused on audit firm-level auditor characteristics as determinants of financial reporting quality. The literature on audit quality concludes that financial reporting quality is higher when the auditor firm is large (i.e., one of the Big N audit firms), has industry expertise, and has longer tenure with the client.10 However, Francis (2011) suggests supplementing findings at the audit firm-level research on the impact of individual auditors.11

We answer the call for research in Francis (2011) and argue that characteristics of the individual auditors conducting the audit matter for audit quality. One of the most important audit partner characteristics is her ability to exercise professional skepticism and withstand client pressures, especially when the client is important to the audit firm or to the partner’s client portfolio. Experimental evidence suggests that inherent traits related to professional skepticism

10 See Francis (2011) and Knechel et al. (2013a) for reviews of this prior literature.

11 Specifically, Francis (2011, p. 134) states, “archival studies of partner characteristics illustrate the importance of

6

affect how auditors react to audit evidence (Hurtt et al. 2008). Moreover, audit partners lead other members of the audit team and tend to steer audit team judgments towards their own (Peytcheva and Gillett 2011). For instance, when audit managers perceive stronger partner pressure to increase client billings, they are more likely to acquiesce to the client’s aggressive accounting choices (Cohen and Trompeter 1998). Similarly, an audit partner’s focus on audit efficiency can lead audit managers to place inappropriate reliance on the work of internal auditors and to exercise lower levels of professional skepticism (Brown et al. 1999, Gramling 1999, Knechel et al. 2013a). Exacerbating this problem, Messier et al. (2008) find that audit partners tend to be overconfident about their subordinates’ abilities to detect accounting malfeasance.12

Because individual audit partners play a crucial role in determining the level of audit quality, an audit partner’s reputation for conducting good or, more importantly, bad audits should be important to financial statement users. This is one of the basic arguments in the PCAOB’s proposal to require companies to disclose engagement partner names. As indicated in Mr.

Ferguson’s remarks above, at least some regulators believe that knowledge of a partner’s identity could allow financial statement users to access information that would serve as a signal about the audit partner’s future performance.

Consistent with the notion that the disclosure of audit partner names may be useful, some prior research suggests that individual audit partner characteristics affect audit quality. For example, using data from Sweden, Knechel et al. (2013c) show that individual audit partners have persistent reporting styles. More specifically, they find that both aggressive and

conservative auditor reporting, measured by the frequency of historical Type 2 and Type 1 going concern error rates, persist over time and extend across clients of an audit partner. Their

12 Note, however, that concurring partner reviews can reduce biases in financial reporting (Woods 2011, Knechel et

7

supplementary analyses of earnings informativeness and abnormal accruals corroborate their findings and also suggest that degree of audit partner aggressiveness (versus conservativeness) is a systematic audit partner attribute. In prior work, Chin and Chi (2009) find that audit partner experience is associated with a lower likelihood of future restatements, and Chi et al. (2013) find that greater client-specific audit partner experience and greater general “pre-client” audit partner experience are associated with higher accounting quality (as measured through discretionary accruals). Other research suggests that individual auditor characteristics are valued by the market. For example, Zerni (2012) finds that audit partners with more industry and public firm

experience are able to charge their clients higher audit fees and Chi et al. (2013) find that credit markets reward clients audited by more experienced partners with a lower cost of debt capital.13

In addition to experience, audit partner compensation systems can also affect audit quality. Francis (2011, pg. 138) argues that “partners will face more threats to their objectivity and independence if their compensation is locally tied to their personal portfolios or to office- level clienteles.” Consistent with this reasoning, experimental evidence suggests that when audit partner compensation is tied to client retention, downward audit adjustments are less likely (Trompeter 1994). In addition, Knechel et al. (2013b) find that audit partner compensation is negatively associated with Type 1 and Type 2 errors in issuing prior year going concern opinions.14 Thus, poorly structured audit partner compensation arrangements could lead to an

13 Recent work by Carcello and Li (2013) also studies the effect of requiring audit partners to sign their audit reports

in the U.K., and suggests that when partners are required to sign their audit reports, they exercise greater care. Our study differs from theirs in that we study the effect of partner identification rather that partner signatures (which can involve both the effect of identification and a psychological effect related to the act of signing itself). However, as Carcello and Li (2013, p. 1512) state, “[a]lthough identifying the engagement partner by name is not identical to requiring the partner to sign the report, such public identification may serve to increase partner accountability and transparency”.

14 Type 1 errors result when going concern opinions are issued to non-failing clients and Type 2 errors result when

failing clients do not receive going concern opinions. The observed frequency of Type 1 and Type 2 errors are indirect measures of audit quality because what causes auditors to issue or not issue going concern opinions in

8

increase in the likelihood of client misstatements but these compensation arrangements are unobservable.

Emerging evidence on the roles of individual preferences and individual risk-aversion in determining firms’ financial and accounting policies also suggests that individual partner

characteristics should matter for audit quality. The traditional view in financial economics – that individual managerial traits are irrelevant for financial and accounting policies – is challenged by Bertand and Schoar (2003) who show that managerial styles affect investment and financial policies (e.g., the investment sensitivity to cash flows, the propensity to make acquisitions, and levels of firm debt and cash holdings).15 Recent papers in accounting also suggest that

managerial styles affect accounting and disclosure quality (Bamber et al. 2010, Ge et al. 2011, McGuire et al. 2012). Furthermore, recent studies demonstrate that because religious beliefs affect risk-aversion, religion affects both financial policies and accounting quality (Hilary and Hui 2009, Dyreng et al. 2010). Finally, religion also affects how trusting people are (Guiso et al. 2009, Pevzner et al. 2012), and thus, partner religion might affect professional skepticism and, in turn, the observed restatement rate. In addition, more risk-tolerant partners may be more likely to accept aggressive financial reporting by clients. Moreover, an individual audit partner’s level of risk aversion could affect her general attitude towards audit quality.

Because individual audit partner-level data are not available in the U.S., direct support for the notion that the likelihood of audit failures varies across individual partners cannot be found in the U.S. audit market. U.S.-based audit research therefore tends to focus on audit firm characteristics (e.g., firm-wide audit specialization, firm-level auditor tenure, and firm-level auditor size) as determinants of financial reporting quality (Francis 2011, Knechel et al. 2013a). different situations it is not entirely clear (Knechel et al. 2013a). Knechel et al. (2013c) pool Type 1 and Type 2 errors in their analyses of the relation between going concern errors and partner compensation.

9

More recently, however, archival auditing research has begun to investigate office-level audit characteristics. The logic behind these studies is that individual offices are autonomous, have different human capital profiles and different client profiles, and generally represent client portfolios with undiversified audit risk. Hence, audit quality levels are likely to vary by office. Consistent with this reasoning, Francis and Yu (2009) find that audit office size (measured using total audit fees charged) is positively associated with discretionary accruals. In addition, Francis and Michas (2013) find that the presence of accounting restatements in a particular office is associated with lower discretionary accruals among non-restating clients in that office.

We suggest that these office-level results may be an artifact, at least in part, of the individual partners in these offices. Audit partners tend to specialize in particular industries and vary in terms of power and level of expertise within an office or firm. Thus, the effect of individual audit partners on audit quality can be measured separately from overall firm- or office-level effects. Alternatively, individual audit partners could have little effect on audit quality because audit quality is driven by the audit firm as a whole. Consistent with this belief, the TSCPA’s comment letter argues that audit firms’ quality control policies, professional ethics, rules, and peer review programs should prevent systematic malfeasance by certain audit

partners.16, 17 Moreover, Hilary and Lenox (2005) suggest that audit firms’ peer review programs are potentially effective in improving audit quality because negative peer review opinions result in client losses. Hence, at least some negative individual audit partner effects on audit quality could be mitigated by firm- and profession-level institutional safeguards, such as quality control

16 See “RE: Improving the Transparency of Audits: Proposed Amendments to PCAOB Auditing Standards and Form

2,” available at: http://www.accountingtoday.com/news/TSCPAletterPCAOBImprovingTransparencyinAudits.php.

17 Note, however, that academic research finds that quality control policies within firms, while generally beneficial,

are not always effective (Knechel et al. 2013a). Some factors identified in prior literature as negatively affecting quality control reviews are known reviewer preferences, partner over-confidence, assumed preparer reputation, and congruency of the opinions of reviewers and preparers. These negative factors can be mitigated, however, when the level of review is higher (Knechel et al. 2013a).

10

procedures, concurrent partner reviews, and peer reviews (although recent PCAOB sanctions against Big 4 audit firms may be interpreted as suggesting otherwise). Thus, it is an empirical question whether an individual partner’s reputation for audit quality is associated with the audit quality of her other clients. Our first alternative hypothesis is as follows:

H1: Client audit quality will be lower when at least one of the audit partner’s other clients misstated its annual financial statements in the prior year.

A factor that could mitigate the persistence of misstatements is audit partner experience (with a particular client, in the industry, or overall). For example, prior research demonstrates that longer audit partner tenure is associated with higher accounting quality (Myers et al. 2003, Manry et al. 2008) and the length of an audit partner’s general (i.e., non-client specific)

experience and industry experience are positively associated with accounting quality (Chen et al. 2008). In addition, prior research also shows that more experienced auditors are better at

detecting financial statement errors, have more accurate knowledge of error occurrence rates, and are better able to categorize errors (Libby and Frederick 1990). Thus, misstatements of more experienced auditors, of auditors with more industry-specific experience, and/or of auditors with longer client-specific tenure may be more transitory in nature.18 We investigate this possibility in our empirical tests.

Because restatements are costly, both in terms of audit fees and in terms of market perceptions,19 prospective audit clients should want to avoid audit partners who are more likely to produce audits requiring restatements. If certain partners are known to be associated with audit failures, we expect their personal reputations to suffer, reducing their ability to attract new

18 For example, conditional on failing to detect a past financial statement error, a partner with more experience could

be more likely to recognize risk factors associated with future financial statement errors.

19 For example, Feldmann et al. (2009) document an average in audit fees of 17 percent following a restatement and

Palmrose et al. (2004) document an average stock price reaction of -9 percent to restatements announced in the U.S. during the pre-Sarbanes Oxley period.

11

business and to retain their current clients. In other words, restatements cause partners to suffer reputational losses. For example, Firth (1990) finds that when U.K. auditors were criticized by the U.K. Department of Trade, these auditors lost client market share and suffered declines in audit fees. As a result, announced audit failures (in the form of restatements), should be

associated with future client losses. Consistent with this argument, Hennes et al. (2012) find that non-Big 4 clients are more likely to dismiss their audit firm following the announcement of accounting irregularities, and that their stock prices react positively to such dismissals. In

addition, Hillary and Lennox (2005) find that audit firms lose clients following unfavorable peer review reports, and Daugherty et al. (2011) and Abbott et al. (2013) find that negative PCAOB inspection findings are associated with a higher likelihood of auditor dismissal. Finally, large and well-publicized audit failures result in a substantial loss of market share for audit firms (Blouin et al. 2007, Weber et al. 2008, Skinner and Srinivasan 2012).20 All of these studies suggest that partner-associated audit failures, if known to outsiders, will lead to a future reduction in that individual audit partner’s market share. Our second alternative hypothesis is as follows:

H2: Restatements are associated with an audit partner’s loss of market share. 3. Sample selection and research design

We use data from Taiwan to test our hypotheses because in Taiwan, audit reports include the names of the two audit partners along with the name of the audit firm. Following Chin and Chi (2009), we treat the first signing partner as the audit partner in all of our analyses. However, our results are robust to treating the partner with the longer tenure as the audit partner (as in Chen et al. 2008). Another unique feature of the Taiwanese audit market is that data are available

20 This is also consistent with results in Lambert et al. (2012), who show in an experimental setting that prospective

12

for both publicly owned and privately owned companies.21 We use the database provided by the Taiwan Economic Journal (TEJ) to collect data about all publicly disclosed financial statements. Thus, we can include both the publicly listed and unlisted clients of each audit partner in our analyses.

H1 predicts that a client is more likely to misstate if its engagement partner was

associated with at least one misstatement made by other clients in the prior year. To test H1, we follow prior research (Hribar and Jenkins 2004, Palmrose et al. 2004, Desai et al. 2006, Cao et al. 2012) and use the likelihood of misstatements to proxy for earnings quality. To test H1, we estimate the following logitisic regression, including untabulated year fixed effects:

Misstatet = a0 + a1Reputation_Partnert-1 + a2Reputation_Firmt-1

+ a3PARTNER EXPERTt + a4LASSETt + a5∆ASSETt + a6AR_INt-1

+ a7FOREIGNt-1 + a8FINANCINGt-1 + a9LISTEDt + a10OWNERSHIPt-1

+ a11 LEVt-1 + a12PARTNER_INDEXPt + a13PARTNER EXPt

+ a14 PARTNER_TENUREt + a15ROAt-1 + a16FIRM_TENUREt

+ a17LBOARD_SIZEt-1 + a18LOSSt-1 + a19STD_CFOt + a20HERFt-1 + e (1A) where Misstatet is an indicator variable set to one if the current year’s annual financial statements are misstated, and zero otherwise. Reputation_Partnert-1 is an indicator variable set to one if the client’s audit partner was associated with at least one misstatement (made by another client) in the past year, and zero otherwise. To control for audit firm-level reputation

(Reputation_Firmt-1), we include an indicator variable set to one if the audit firm was associated with at least one misstatement (made by another client) in the past year, and zero otherwise. We follow Cao et al. (2012) to the extent possible when selecting control variables that affect

21 The Taiwan Securities and Exchange Act mandates that all companies issuing securities, including those listed on

the Taiwan Stock Exchange Corporation (TWSE) and GreTai Securities Market (GTSM) as well as unlisted companies, publicly disclose audited financial statements. Before 2001, the mandatory reporting requirement applied to both publicly listed firms and privately held firms with contributed capital exceeding a certain threshold, which was Taiwan dollars (TWD) 200 million after 1981 and TWD 500 million after 2000. The reporting

requirement for privately held firms was rescinded in 2001 so public disclosure of audited financial statements was at management’s discretion, but publicly listed firms continued to report. Thus, not all unlisted companies are included in the TSE database.

13

misstatements.22 These variables are defined in detail in the Appendix. To mitigate the influence of potential outliers, here an in all regression analyses, we winsorize all continuous variables at their 1st and 99th percentiles, respectively and we follow Gow et al. (2010) and report all test statistics using two-way cluster-robust standard errors (clustered by client and by year), which adjust for both cross-sectional and time-series dependence in panel data.

H1 predicts a positive coefficient on Reputation_Partnert-1. That is, we expect that a client to be more likely to misstate its annual financial statements if at least one of its audit partner’s other clients misstated their annual financial statements in the prior year. In addition, if the reputation effect occurs at the audit-firm level, we would expect a positive coefficient on

Reputation_Firmt-1.

In addition to testing whether misstatements are preceded by misstatements (made by other clients of the audit partner) in the prior year using company-level data, we also investigate whether misstatements precede misstatements when we consider that data at the audit partner’s portfolio level. Specifically, we estimate the following logitistic regression to test whether the probability of that at least one of an audit partner’s clients misstate in a two or three year period is greater when at least one of his clients has misstated in the preceding two or three years:

Fut2(3)_Misstatet = a0 + a1Reputation_Partner2(3)t-1 + a2Reputation_Firm2(3)t-1

+ a3PARTNER EXPERTt + a4LASSETt + a5∆ASSETt + a6AR_INt-1

+ a7FOREIGNt-1 + a8FINANCINGt-1 + a9LISTEDt + a10OWNERSHIPt-1

+ a11 LEVt-1 + a12PARTNER_INDEXPt + a13PARTNER EXPt

+ a14 PARTNER_TENUREt + a15ROAt-1 + a16FIRM_TENUREt

+ a17LBOARD_SIZEt-1 + a18LOSSt-1 + a19STD_CFOt + a20HERFt-1 + e (1B)

22 We do not include company reputation, mergers and acquisitions, and segments data because this information is

not available in Taiwan. In addition, audit fees and nonaudit fees are required disclosures only when the ratio of non-audit to audit fees at least 0.25 or the amount of non-audit fees is at least 500,000 TWD, the client switches audit firms and the subsequent audit firm fees are less than the previous fees, or when audit fees are at least 15 percent lower than in the prior year. We do not include market-to-book ratio and return volatility because our sample includes non-listed companies. We do not include board independence because it is not machine-readable for our sample. Finally, we consider financing activity but use a different measure since the measure in Cao et al. (2012) requires data about mergers and acquisitions (which is unavailable).

14

where Fut2(3)_Misstatet is an indicator variable set to one if at least one of the audit partner’s clients’ annual financial statements are misstated in the following two (or three) years, and zero otherwise. Reputation_Partner2(3)t-1 is an indicator variable set to one if the audit partner is associated with at least one misstatement in the two (or three) year period, and zero otherwise. Similarly, Reputation_Firm 2(3)t-1 is an indicator variable set to one if the audit firm is

associated with at least one misstatement in the two (or three) year period, and zero otherwise. If audit quality is persistent at the audit partner level, the coefficient on Reputation_Partner2(3)t-1 will be positive.

We supplement the above analyses by investigating whether restatements (i.e., disclosures of prior period misstatements at the audit partner level) are associated with future misstatements. We estimate the following logitistic regression:

Misstatet = a0 + a1Reputation_Partner_RESTt-1 + a2Reputation_Firm_RESTt-1

+ a3PARTNER EXPERTt + a4LASSETt + a5∆ASSETt + a6AR_INt-1

+ a7FOREIGNt-1 + a8FINANCINGt-1 + a9LISTEDt + a10OWNERSHIPt-1

+ a11 LEVt-1 + a12PARTNER_INDEXPt + a13PARTNER EXPt

+ a14 PARTNER_TENUREt + a15ROAt-1 + a16FIRM_TENUREt

+ a17LBOARD_SIZEt-1 + a18LOSSt-1 + a19STD_CFOt + a20HERFt-1 + e (1C) where Reputation_Partner_RESTt-1 is an indicator variable set to one if the client’s audit partner was associated with at least one restatement announcement (made by another client) in the past year, and zero otherwise. Similarly, Reputation_Firm_RESTt-1 is an indicator variable set to one if the audit firm was associated with at least one restatement announcement (made by another client) in the past year, and zero otherwise. If restatements predict future misstatements at the audit partner level, the coefficient on Reputation_Partner_RESTt-1 will be positive.

We further examine whether the ability of prior misstatements to predict future misstatements varies with audit partners’ overall audit experience, industry-specific audit experience, or client-specific experience (i.e., tenure) by estimating the following regression

15 models:

Misstatet-= a0 + a1Reputation_Partnert-1 + a2LONG EXPt

+ a3Reputation_Partnert-1*LONG EXPt + a4Reputation_Firmt-1

+ a5PARTNER EXPERTt + a6LASSETt + a7∆ASSETt + a8AR_INt-1 + a9FOREIGNt-1

+ a10FINANCINGt-1 + a11LISTEDt + a12OWNERSHIPt-1 + a13LEVt-1

+ a14PARTNER_INDEXPt + a15PARTNER EXPt + a16PARTNER_TENUREt + a17ROAt-1

+ a18FIRM_TENUREt-1 + a19LBOARD_SIZEt-1 + a20LOSSt-1 + a21STD_CFOt

+ a22HERFt-1 + e (1D)

Misstatet= a0 + a1Reputation_Partnert-1 + a2LONG IND EXPt

+ a3Reputation_Partnert-1*LONG IND EXPt + a4Reputation_Firmt-1

+ a5PARTNER EXPERTt + a6LASSETt + a7∆ASSETt + a8AR_INt-1 + a9FOREIGNt-1

+ a10FINANCINGt-1 + a11LISTEDt + a12OWNERSHIPt-1 + a13 LEVt-1

+ a14PARTNER_INDEXPt + a15PARTNER EXPt + a16PARTNER_TENUREt + a17ROAt-1

+ a18FIRM_TENUREt + a19LBOARD_SIZEt-1 + a20LOSSt-1 + a21STD_CFOt

+ a22HERFt-1 + e (1E)

Misstatet = a0 + a1Reputation_Partnert-1 + a2LONG PARTNER TENUREt

+ a3Reputation_Partnert-1*LONG PARTNER TENUREt + a4Reputation_Firmt-1

+ a5PARTNER EXPERTt + a6LASSETt + a7∆ASSETt + a8AR_INt-1 + a9FOREIGNt-1

+ a10FINANCINGt-1 + a11LISTEDt + a12OWNERSHIPt-1 + a13LEVt-1

+ a14PARTNER_INDEXPt + a15PARTNER EXPt + a16PARTNER_TENUREt + a17ROAt-1

+ a18FIRM_TENUREt + a19LBOARD_SIZEt-1 + a20LOSSt-1 + a21STD_CFOt

+ a22HERFt-1 + e (1F)

where LONG EXPt is an indicator variable set to one if the partner’s total auditing experience (i.e., the number of years as an audit partner for any client) exceeds the sample median, and zero otherwise, LONG IND EXPt is an indicator variable set to one if the partner’s total industry experience (i.e., the number of years auditing clients in the current client’s industry) exceeds the sample median, and zero otherwise, and LONG TENUREt is an indicator variable set to one if the partner’s tenure with the current client since 1983 exceeds the sample median, and zero

otherwise.23 These three variables capture the audit partner’s general, industry-specific, and client-specific audit experience, respectively. If audit partner experience mitigates the persistence of poor audit quality, then the coefficients on Reputation_Partnert-1*LONG EXPt,

23 Because corporate governance control variables are not available before 1995, our sample period starts in that year.

However, our measures of audit partner experience and tenure are calculated from 1983 onward because this is the first year that audit reports in Taiwan were required to be signed by two audit partners.

16

Reputation_Partnert-1*LONG IND EXPt, and Reputation_Partnert-1*LONG PARTNER TENUREt

will be negative. We also estimate the effects of partner overall experience, industry-specific experience, and audit tenure in a single combined model to examine whether one effect dominates the others. The model is as follows:

Misstatet = a0 + a1Reputation_Partnert-1 + a2LONG EXPt

+ a3Reputation_Partnert-1*LONG EXPt + a4LONG INDEXPt-1

+ a5Reputation_Partnert-1*LONG INDEXPt+ a6*LONG PARTNER TENUREt

+ a7Reputation_Partnert-1*LONG PARTNER TENUREt +a8Reputation_Firmt-1

+ a9PARTNER EXPERTt + a10LASSETt + a11∆ASSETt + a12AR_INt-1 + a13FOREIGNt-1

+ a14FINANCINGt-1 + a15LISTEDt + a16OWNERSHIPt-1 + a17LEVt-1

+ a18PARTNER_INDEXPt + a19PARTNER EXPt + a20PARTNER_TENUREt + a21ROAt-1

+ a22FIRM_TENUREt + a23LBOARD_SIZEt-1 + a24LOSSt-1 + a25STD_CFOt

+ a26HERFt-1 + e (1G)

To examine the prediction in H2 – that audit partners’ market shares decrease if they are associated with a prior client restatement – we estimate the following regression model at the audit partner level (including year fixed effects):

Ch_MKS_Partnert = d0 + d1Ch_MKS_Firmt + d2RESTATEt + d3PARTNER INDEXPt

+ d4PARTNER EXPt + d5PARTNER EXPERTt + d6FIRM EXPERTt +e (2)

where, similar to DeFond et al. , Ch_MKS_Partnert is either Ch_MKS_SALEt which denotes the change in a partner’s market share based on client sales audited during year t as compared to year t-1 or CH_MKS_ASSETt which denotes the change in a partner’s market share based on

client assets audited during year t as compared to year t-1 RESTATEt-1 is an indicator variable equal to one if least one of the audit partner’s clients discloses a restatement (i.e., reveals a prior misstatement) in the prior year, and zero otherwise, and all other variables are as previously defined. If partners whose clients restate earnings are more likely to lose market share, then the coefficient on RESTATEt will be negative.

We further examine whether the loss of market share related to restatements varies with the partner’s overall audit experience, industry-specific audit experience, or client-specific

17

experience by estimating the following regression models:

Ch_MKS_Partnert = d0 + d1RESTATEt + d2LONG EXPt-+ d3RESTATE t*LONG EXPt

+ d4Ch_MKS_Firmt + d5PARTNER INDEXPt + d6PARTNER EXPt

+ d7PARTNER EXPERTt + d8FIRM EXPERTt +e (2A)

Ch_MKS_Partnert = d0 + d1RESTATEt + d2LONG IND EXPt

+ d3RESTATE t*LONG IND EXPt + d4Ch_MKS_Firmt + d5PARTNER INDEXPt

+ d6PARTNER EXPt +d7PARTNER EXPERTt + d8FIRM EXPERTt +e (2B)

Ch_MKS_Partnert = d0 + d1RESTATEt-1 + d2LONG PARTNER TENUREt-1

+ d3RESTATEt-1*LONG PARTNER TENUREt-1 + d4Ch_MKS_Firmt

+ d5PARTNER INDEXPt + d6PARTNER EXPt + d7PARTNER EXPERTt

+ d8FIRM EXPERTt +e (2B)

To assess relative contribution of each factor (total experience, industry-specific experience, and tenure) on the impact of restatements of market share, we also estimate a model which includes all of the interaction terms (similar to equation 1G). If audit partners with more experience suffer a greater loss of reputation when their clients restate, then we expect the coefficients on

RESTATEt-1*LONG EXPt and RESTATEt-1*LONG IND EXPt to be negative.

4. Empirical Results and Additional Analyses

We obtain all non-financial observations from the TEJ database for the years 1995 through 2010 and require that data be available to construct the variables in all six models ((1A) through (2B)). Our sample period starts in 1995 because the TEJ database provides stable

coverage starting in that year and some control variables used in our study are not available prior to 1995. For tests of H1, we restrict our sample to companies whose audit partners audit at least three clients in year t. This results in a sample comprised of 13,505 company-year observations for tests of H1 and of 3,539 partner-year observations for tests of H2.

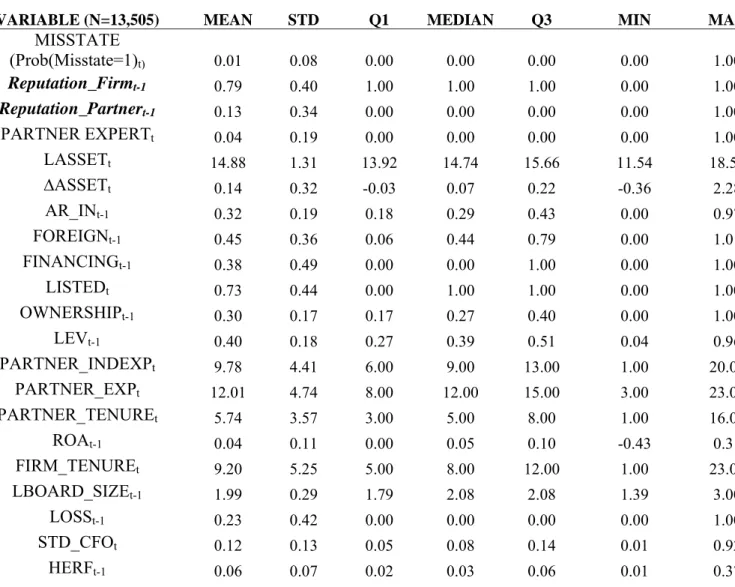

Table 1 presents descriptive statistics. On average, one percent of companies in Taiwan report misstatements of their financial statements in a given year. Seventy nine (79) percent of audit firms had at least one client restate in the prior year and 13 percent of audit partners have at

18

least one client restate in the prior year. On average, the audit partner’s tenure is 5.74 years, and 34 percent of audit partners are industry experts (in that they audit the largest market share, based on assets, in their client’s industry). Finally, seventy three (73) percent of sample companies are listed companies.

Table 2 presents correlations. Reputation_Partner is positively correlated with Misstate, suggesting that when a partner’s other clients have misstated in the past year, there is a higher likelihood that her current clients will misstate. However, we do not find a significant correlation between past misstatements and current misstatements at the audit firm level.

To determine whether the impairment of audit partner reputation from past client

misstatements is associated with current client misstatements, we present our logisitic regression results in Table 3. Panel A present the results from estimating Equation (1A). We find a positive coefficient on Reputation_Partner (p-value = 0.03). This result, which is consistent with the univariate result in Table 2, suggests that when at least one of the audit partner’s clients

misstated in the prior year, the likelihood that a current client misstates is higher. The coefficient on Reputation_Firm is insignificant (p-value = 0.83), suggesting that misstatements are not persistent at the audit-firm level.

When we consider the rolling period of two (or three) years for presence of misstatements and the predictive power of those misstatements for the next two (or three) years in Panel B1 (B2), we find similar results. In Panel B1, when Fut2_Misstate is used as the dependent variable, the coefficient on Reputation_Partner2 is significantly positive (p-value = 0.08) but the

coefficient on Reputation_Firm2 is insignificant (p-value = 0.23). In Panel B2, we expand our prediction window to three years and find that the coefficient on Reputation_Partner3 is significantly positive (p-value = 0.05). In addition, we find in Panel C that a partner’s past

19

restatements (i.e., revealed misstatements) are also associated with a higher likelihood of future misstatements; the coefficient on Reputation_Parnter_REST is significantly positive (p-value = 0.02). Taken together, these findings suggest that an audit partner’s reputation for past audit quality problems predicts future audit quality problems.

We next examine whether the association between an audit partner’s past client

misstatements and current client misstatements varies with audit partner experience. In Panel A of Table 4, Panel D, we find a negative and significant coefficient on

Reputation_Partner*LONG EXP (p-value = 0.00), suggesting that when audit partners are more

experienced, the persistence of client misstatements is significantly lower. Similarly, in Column 2, we find a negative coefficient on Reputation_Partner*LONG IND EXP (p-value = 0.00), suggesting that, when audit partners have experience in the industry, the persistence of client misstatements is also significantly lower. Finally, we do not find evidence that audit partner tenure has an impact on the relation between the past misstatements and current misstatements because the coefficient on Reputation_Partner*LONG PARTNER TENURE is insignificant

(p-value = 0.82). However, when we estimate the full model (Equation 1G), only the

Reputation_Partner*LONG EXP interaction remains significant and negative, suggesting that

overall audit experience is the most important factor in determining the persistence of misstatements.

Finally, we examine whether the tarnished reputation that an audit partner suffers from client restatements is associated with the loss of audit partner market share in the subsequent year. Using the audit partner’s total client sales audited (CH_MKS_ASSETt) to proxy for partner market share in Panel A of Table 4, we find a negative coefficient on RESTATEt- (p-value = 0.00). This suggests that tarnished audit partner reputation from prior restatements is associated

20

with a loss of audit partner market share. When we measure market share based on total client assets audited (CH_MKS_ASSETt), the results are similar in that the coefficient on RESTATEt is also negative (p-value = 0.00). These results support H2. In untabulated analyses, we use client count to measure market share and find that a partner’s client count decreases in the year a restatement is announced. Thus, our results are consistent with the notion that partners suffer reputational losses as a result of announced restatements.

We next examine whether this relation varies with audit partner experience. In Panel B of Table 4, we find a negative and significant coefficient on RESTATE*LONG EXP (p-value ≤ 0.10 when market share is measured using client assets or sales audited). This suggests that when audit partners are more experienced, the consequences of a loss of reputation are stronger (i.e., clients are more likely to engage other audit partners when more experienced auditors are associated with misstatements). Similarly, in Panel C, we find a negative coefficient on

RESTATE*LONG IND EXP (p-value ≤ 0.01 when market share is measured using client assets

or sales audited). This suggests that when audit partners have more industry experience, the consequences of restatements are stronger. These results, coupled with earlier results reported in Panel D of Table 3, suggest that more experienced partners suffer greater reputational loss when clients restate, which may explain why audit partners with greater experience are less likely to be associated with persistent misstatements. In Panel D, we do not find that audit partner tenure affects partner market share losses following restatement announcements. When we combine all measures of partner experience (total experience, industry-specific experience, and partner tenure) in a single model in Panel E, we find that only industry experience effects market share losses when market share is calculated using sales.

21

In this study, we examine the association between an audit partner’s reputation for past audit failures and actual and perceived audit quality. More specifically, we find when at least one of an audit partner’s clients misstates its financial statements in the prior year, the likelihood of the audit partner’s current clients misstating increases. Moreover, we find that audit partners are more likely to lose market share following client restatements.

Our study contributes to the ongoing debate about whether disclosure of engagement partner names is useful for investors. Our results give additional credence to the notion that investors benefit from knowing audit partner names and thus may inform debates related to the recent PCAOB proposal suggesting such disclosure. We acknowledge, however, that because our data are drawn from the Taiwan audit market, our conclusions may not be generalizable to the U.S. audit market.

22

References:

Abbott, L., K. Gunny, and T. Zhang. (2013). When the PCAOB Talks, Who Listens? Evidence from Stakeholder Reaction to GAAP-Deficient PCAOB Inspection Reports of Small Auditors. Auditing: Journal of Practice and Theory 32(1), 1-31.

Amihud, Y. (2002). Illiquidity and Stock Returns: Cross-section and Time-series Effects.

Journal of Financial Markets 5(1), 31-56.

Bamber, L., J. Jiang, and I.Wang. (2010). What’s My Style? The Influence of Top

Managers on Voluntary Corporate Financial Disclosure. The Accounting Review (85): 1131-1162.

Bardos, K. (2011). Quality of Financial Information and Liquidity. Review of Financial

Economics 20(2), 49-62.

Bertrand, M. and A. Schoar (2003). Managing With Style: The Effects of Managers on Firm Policies. Quarterly Journal of Economics 118(4), 1169-1208

Blouin, J., B. Grey, and B. Rountree. (2007). An Analysis of Forced Auditor Change: The Case of Former Arthur Andersen Clients. The Accounting Review 82(3), 621-650.

Brown, C. E., M. E. Peecher, and I. Solomon. (1999). Auditors’ Hypothesis Testing in Diagnostic Inference Tasks. Journal of Accounting Research 37 (1), 1-26.

Burghstahler, D. and I. Dichev. (1997). Earnings Management to Avoid Earnings Decreases and Losses. Journal of Accounting and Economics 24(1), 99-126.

Barton, J. (2005). Who Cares about Auditor Reputation? Contemporary Accounting Research 22(3), 549-586.

Cao, Y., L. A. Myers, and T. C. Omer. (2012). Does Company Reputation Matter for Financial Reporting Quality? Evidence from Restatements. Contemporary Accounting Research 29(3), 956-990.

Carcello, J. and C. Li. (2013). Costs and Benefits of Requiring an Engagement Partner Signature: Recent Experience in the United Kingdom. The Accounting Review 88(5), 1511-1546. Carey, P. and R. Simnett. (2006). Audit Partner Tenure and Audit Quality. The Accounting

Review 81 (3), 653-676.

Chaney, P. and K. Philipich. (2002). Shredded Reputation: The Cost of Audit Failure. Journal of

23

Chen, C. Y., C. J. Lin, and Y. C. Lin. (2008). Audit Partner Tenure, Audit Firm Tenure, and Discretionary Accruals: Does Long Auditor Tenure Impair Earnings Quality?

Contemporary Accounting Research 25(2), 415-445.

Chi, W., L. A. Myers, T. C. Omer, and H. Xie. (2013). The Effects of Audit Partner Pre-Client and Client-Specific Experience on Earnings Quality and on Perceptions of Audit Quality. Working paper, National Chengchi University, University of Arkansas, Texas A&M University, and University of Kentucky.

Chin, C. and H. Chi. (2009). Reducing Restatements with Increased Industry Experience.

Contemporary Accounting Research 26(3), 729-765.

Cohen, J. and G. Trompeter. (1998). An Examination of Factors Affecting Audit Practice Development. Contemporary Accounting Research (Winter): 481-476.

Daugherty, B., D. Dickins, and W. Tervo. (2011). Negative PCAOB Inspections of Triennially Inspected Auditors and Involuntary and Voluntary Client Losses. International Journal

of Auditing 15(3), 231-246.

Dee, C., A. Lulseged, and T. Zhang. (2011). Client Stock Market Reaction to PCAOB Sanctions Against a Big 4 Auditor. Contemporary Accounting Research 28(1), 263-291.

DeFond, M., T. Wong, and S. Li. (2000). The Impact of Improved Auditor Independence on Audit Market Concentration in China. Journal of Accounting and Economics 28, 269-305. Desai, H., S. Krishnamurthy, and K. Venkataraman. (2006). Do Short Sellers Target Firms with

Poor Earnings Quality? Evidence from Restatements. Review of Accounting Studies 11(1), 71-90.

Dyreng, S., W. Mayew, and C. Williams. (2010). Religious Social Norms and Corporate Financial Reporting. Working paper, Duke University and University of Michigan. Feldmann, D., W. Read, and M. Abdolmohammadi (2009). Financial Restatements, Audit Fees,

and the Moderating Effect of CFO Turnover. Auditing: Journal of Practice and Theory 28(1), 205-233.

Feng, M., W. Ge, S. Luo, and T. Shevlin. (2011). Why Do CFOs Become Involved in Material Accounting Manipulations? Journal of Accounting and Economics 51(1-2), 21-36.

Feng, N., K. Kitching, and L. A. Myers. (2013). Do Auditor-in-Charge Characteristics Matter for Audit Quality? Evidence from Nonprofits in the U.S. Working paper, Suffolk University, George Mason University, and University of Arkansas.

Ferguson, L. (2011). Statement on Proposed Amendments to Improve Transparency Through Disclosure of Engagement Partner and Certain Other Participants in Audits. Public

24

Firth, M. (1990). Auditor Reputation: The impact of Critical Reports Issued by Government Inspectors. Rand Journal of Economics 21(3), 374-389.

Francis, J. R. (2011). A Framework for Understanding and Researching Audit Quality. Auditing:

Journal of Practice and Theory 30(2), 125-152.

Francis, J. R., and P. Michas. (2013). The Contagion Effect of Low-Quality Audits. The

Accounting Review 88(2), 521-553.

Francis, J. R., and M. Yu. (2009). The Effect of Big Four Office Size on Audit Quality. The

Accounting Review 84(5), 71-97.

Ge, W., D. Matsumoto, and J. Zhang. (2011). Do CFOs Have Styles of Their Own? An Empirical Investigation of the Effect of Individual CFOs on Accounting Practices.

Contemporary Accounting Research 28 (4): 1141-1179

Gleason, C., N. Jenkins, and B. Johnson. (2008). The Contagion Effects of Accounting Restatements. The Accounting Review 83(1), 83-110.

Gow, I., G. Ormazabal, and D. Taylor. (2010). Correcting for Cross‐Sectional and Time‐Series Dependence in Accounting Research. The Accounting Review 85 (2), 483-512.

Gramling, A. A. 1999. External Auditors’ Reliance on Work Performed by Internal Auditors: The Influence of Fee Pressure on this Reliance Decision. Auditing: A Journal of Practice

& Theory 18 (Supplement), 117-135.

Guiso, L., P. Sapienza, and L. Zingales. (2009). Cultural Biases in Economic Exchange.

Quarterly Journal of Economics 124 (3), 1095-1131.

Hennes, K. M., A. J. Leone, and B. P. Miller. (2012). Auditor Dismissals After Accounting Restatements. Working paper, University of Oklahoma, University of Miami and Indiana University.

Hilary, G. and K. Hui. (2009). Does Religion Matter in Corporate Decision Making in America?

Journal of Accounting and Economics 93(3), 455-473.

Hilary, G. and C. Lennox. (2005). The Credibility of Self-Regulation: Evidence from the

Accounting Profession’s Peer Review Program. Journal of Accounting and Economics 40, 211-229.

Hribar, P. and N. Jenkins. (2004). The Effect of Accounting Restatements on Earnings Revisions and the Estimated Cost of Capital. Review of Accounting Studies 9, 337-356.

Hurtt, K., M. M. Eining, and D. Plumlee. (2008). An Experimental Examination of Professional Skepticism. Working paper, Baylor University and University of Utah.

25

Kim, Y., M. Lacina, and M. Park. (2008). Positive and Negative Information Transfers from Management Forecasts. Journal of Accounting Research 46(4), 885-908.

King, R., S. Davis, and N. Mintchik. (2012). Mandatory Disclosure of Audit Partner Identity: Potential Benefits and Unintended Consequences. Accounting Horizons 26(3), 533-561. Knechel, W. R., G. Krishnan, M. Pevzner, L. Shefchik, and U. Velury. (2013a). Audit

Quality Indicators: Insights from Academic Literature. Auditing: Journal of Practice and

Theory 32(Supplement 1), 385-421.

Knechel, W. R., L. Nielmi, and M. Zerni. (2013b). Empirical Evidence on the Implicit

Determinants of Compensation in Big 4 Accounting Partnerships. Forthcoming, Journal

of Accounting Research.

Knechel, W. R., L. Nielmi, and M. Zerni. (2013c). Does the Identity of Engagement Partners Matter? An Analysis of Audit Partner Reporting Decisions. Working paper, University of Florida.

Koch, C. (2011). The Pricing of Engagement Partner Expertise. Working paper, University of Mannheim.

Kravet, T. and T. Shevlin. (2010). Accounting Restatements and Information Risk. Review of

Accounting Studies 15(2), 264-294.

Krishnamoorthy, S., J. Zhou, and N. Zhou. (2006). Auditor Reputation, Auditor Independence, and the Stock-Market Impact of Andersen’s Indictment on Its Client Firms.

Contemporary Accounting Research 23(2), 465-490.

Lambert, T., B. Luippold, and C. Stefaniak. (2012). Audit Partner Disclosure: An Examination of Investor Reaction to Negative Information and Potential Implications for Auditor Independence. Working paper, University of Massachusetts at Amherst, Georgia State University, and Oklahoma State University.

Lee, E., C. Hadlock and J. Pierce. (2013). Managers With and Without Style: Evidence Using Exogenous Variation. Review of Financial Studies 26(3), 571-601.

McGuire, S. T., T. C. Omer, and N. Y. Sharp. (2012). The Impact of Religion on Financial Reporting Irregularities. The Accounting Review 87(2), 645-673.

Messier, W., V. Owhoso, and C. Rakowski. (2008). Can Partners Predict Subordinates’ Abilities to Predict Errors. Journal of Accounting Research 46(5), 1241-1264.

Palmrose, Z., V. Richardson, and S. Scholz. (2004). Determinants of Market Reactions to Restatement Announcements. Journal of Accounting and Economics 37(1), 59-89.

26

Pandit, S., C. Wasley, and T. Zach. (2011). Information Externalities Along the Supply Chain: The Economic Determinants of Suppliers Stock Price Reaction to Their Customers’ Earnings Announcements. Contemporary Accounting Research 28(4), 1304-1343. Pevzner, M., F. Xie, and X. Xin. (2012). When Firms Talk, Do Investors Listen? The Role of

Trust in Stock Market Reactions to Corporate Earnings Announcements. Working paper, George Mason University, Clemson University, and Chinese University of Hong Kong. Peytcheva, M. and P. Gillett. (2011). How Partner’s Views Influence Auditor Judgments.

Auditing: Journal of Practice and Theory 30(4), 285-301.

Reynolds, K. and J. R. Francis. (2000). Does Size Matter? The Influence of Large Clients on Office-Level Auditor Reporting Decisions. Journal of Accounting and Economics 30(3), 375-400.

Schrand, C. and S. Zechman. (2011). Executive Overconfidence and the Slippery Slope to Financial Misreporting. Journal of Accounting and Economics 53(1-2), 311-329 Skinner, D. and S. Srinivasan. (2012). Audit Quality and Auditor Reputation: Evidence

from Japan. The Accounting Review 87(5), 1737-1766.

Texas CPA Society (TSCPA). (2011). RE: Improving the Transparency of Audits: Proposed Amendments to PCAOB Auditing Standards and Form 2. Available at:

http://www.accountingtoday.com/news/TSCPAletterPCAOBImprovingTransparencyinA udits.php.

Trompeter, G. (1994). The Effect of Partner Compensation Schemes and Generally Accepted Accounting Principles on Audit Partner Judgment. Auditing: Journal of Practice and

Theory 13(2), 56-68.

Weber, J., M. Willenborg, and J. Zhang. (2008). Does Auditor Reputation Matter? The Case of KPMG Germany and ComROAD AG. Journal of Accounting Research 46(4), 941-972. Woods, A. (2011). Monitoring the Monitor: When do Higher-Level Reviewers Adjust

Supervisors’ Subjective Performance Evaluations of Internal Audit Employees? Working paper, College of William and Mary.

Zerni, M. (2012). Audit Partner Specialization and Audit Fees: Some Evidence from Sweden. Contemporary Accounting Research 29(1), 312-340.

27

Appendix Variable Definitions Variable Definition

Misstate An indicator variable equal 1 if the firm reported an accounting misstatement in year t, 0 otherwise Fut3_MISSTATE An indicator variable equal 1 if the firm reported an

accounting misstatement in years t, t+1, t+2 Reputation_Partner

An indicator variable equal 1 if a partner is associated with at least one misstatement in other clients in the past year (t-1)

Reputation_Firm

An indicator variable equal 1 if an audit firm is associated with at least one misstatement in other clients in the past year (t-1)

Reputation_Partner3

An indicator variable equal 1 if a partner is associated with at least one misstatement in other clients in the past three years (t-4 through t-1)

Reputation_Firm3

An indicator variable equal 1 if an audit firm is associated with at least one misstatement in other clients in the past three years (t-4 through t-1)

Reputation_Partner_REST

An indicator variable equal 1 if a partner is associated with at least one restatement announcement in other clients in the past year (t-1)

Reputation_Firm_REST

An indicator variable equal 1 if an audit firm is associated with at least one restatement announcement in other clients in the past year (t-1)

PARTNER EXPERT

Indicator variable equal 1 if a partner is an industry expert in her industry

LASSET Natural log of total assets

∆ASSET Percentage change in firm’s assets AR_IN

Sum of accounts receivable and inventory deflated by total assets

FOREIGN

A measure of complexity based on the proportion of company sales generated in foreign countries

FINANCING

Indicator variable equal 1 if a firm issues financing during the period

LISTED Indicator variable equal 1 if a firm is listed on an exchange OWNERSHIP

the percentage of stock owned by insiders (i.e., the company’s top managers and directors);

LEV Firm leverage

PARTNER_INDEXP Partner industry experience PARTNER_EXP Partner total experience

PARTNER_TENURE Partner tenure with the client

ROA Firm’s ROA

FIRM_TENURE Audit firm tenure with the client LBOARD_SIZE Natural log of board size

28 income

STD_CFO Standard deviation of operating cash flows. HERF Herfendahl index for a particular industry PARTNER EXP Partner’s total industry experience

PARTNER INDEXP Partner’s total industry experience PARTNER TENURE Partner’s tenure with the client

LONG EXP An indicator variable equal 1 if partner’s total experience exceeds sample median (12 years in our sample)

LONG INDEXP An indicator variable equal 1 if a partner’s industry

experience exceeds sample median (9 years in our sample) LONG TENURE An indicator variable equal 1 if a partner’s tenure with the

client exceeds sample median (6 years in our sample) CH_MKS_SALE The change in an audit partner’s market share basedon total

sales of all clients audited (from year t-1 to year t)

CH_MKS_ASSET The change in an audit partner’s market share basedon total assets of all clients audited (from year t-1 to year t)

CH_MKS_FIRM The change in the auditing firm’s market share based on total sales or assets of all clients audited (from year t-1 to year t)

29

Table 1 Descriptive Statistics

VARIABLE (N=13,505) MEAN STD Q1 MEDIAN Q3 MIN MAX

MISSTATE (Prob(Misstate=1)t) 0.01 0.08 0.00 0.00 0.00 0.00 1.00 Reputation_Firmt-1 0.79 0.40 1.00 1.00 1.00 0.00 1.00 Reputation_Partnert-1 0.13 0.34 0.00 0.00 0.00 0.00 1.00 PARTNER EXPERTt 0.04 0.19 0.00 0.00 0.00 0.00 1.00 LASSETt 14.88 1.31 13.92 14.74 15.66 11.54 18.50 ∆ASSETt 0.14 0.32 -0.03 0.07 0.22 -0.36 2.28 AR_INt-1 0.32 0.19 0.18 0.29 0.43 0.00 0.97 FOREIGNt-1 0.45 0.36 0.06 0.44 0.79 0.00 1.01 FINANCINGt-1 0.38 0.49 0.00 0.00 1.00 0.00 1.00 LISTEDt 0.73 0.44 0.00 1.00 1.00 0.00 1.00 OWNERSHIPt-1 0.30 0.17 0.17 0.27 0.40 0.00 1.00 LEVt-1 0.40 0.18 0.27 0.39 0.51 0.04 0.96 PARTNER_INDEXPt 9.78 4.41 6.00 9.00 13.00 1.00 20.00 PARTNER_EXPt 12.01 4.74 8.00 12.00 15.00 3.00 23.00 PARTNER_TENUREt 5.74 3.57 3.00 5.00 8.00 1.00 16.00 ROAt-1 0.04 0.11 0.00 0.05 0.10 -0.43 0.31 FIRM_TENUREt 9.20 5.25 5.00 8.00 12.00 1.00 23.00 LBOARD_SIZEt-1 1.99 0.29 1.79 2.08 2.08 1.39 3.00 LOSSt-1 0.23 0.42 0.00 0.00 0.00 0.00 1.00 STD_CFOt 0.12 0.13 0.05 0.08 0.14 0.01 0.92 HERFt-1 0.06 0.07 0.02 0.03 0.06 0.01 0.37