行政院國家科學委員會專題研究計畫 成果報告

對上司之信任與目標困難度在預算控制系統情境下之角色

計畫類別: 個別型計畫 計畫編號: NSC94-2416-H-110-030- 執行期間: 94 年 08 月 01 日至 95 年 07 月 31 日 執行單位: 國立中山大學企業管理學系(所) 計畫主持人: 倪豐裕 計畫參與人員: 蘇錦俊、鍾紹熙、鄭國枝 報告類型: 精簡報告 處理方式: 本計畫可公開查詢中 華 民 國 95 年 9 月 30 日

行政院國家科學委員會補助專題研究計畫

■ 成 果 報 告

□期中進度報告

對上司之信任與目標困難度在預算控制系統情境下之角色

計畫類別:■ 個別型計畫 □ 整合型計畫

計畫編號:NSC

94-2416-H-110-030執行期間: 94 年 8 月 1 日至 95 年 7 月 31 日

計畫主持人:倪豐裕

共同主持人:

計畫參與人員:蘇錦俊、鍾紹熙、鄭國枝

成果報告類型(依經費核定清單規定繳交):■精簡報告 □完整報告

本成果報告包括以下應繳交之附件:

□赴國外出差或研習心得報告一份

□赴大陸地區出差或研習心得報告一份

□出席國際學術會議心得報告及發表之論文各一份

□國際合作研究計畫國外研究報告書一份

處理方式:除產學合作研究計畫、提升產業技術及人才培育研究計畫、

列管計畫及下列情形者外,得立即公開查詢

□涉及專利或其他智慧財產權,□一年□二年後可公開查詢

執行單位:

國立中山大學企業管理學系

中 華 民 國 95 年 9 月 30 日

對上司之信任與目標困難度在預算控制系統情境下之角色 摘要 本研究探討對上司之信任在預算參與對管理績效間之中介的角色,同時預算目 標困難度則扮演三者關係間的調節角色。本文自台灣證券交易所之上市製造業公 司經理人隨機抽樣,共取得 155 份有效問卷作為本研究之分析樣本。對於上司信 任的中介效果,本文採用路徑分析方式來驗證,而預算目標困難度的調節效果則 採用拆樣本的分群分析(Subgroup analysis)來檢驗。本研究結果印證該假設,認為 對上司之信任具有中介效果,同時預算目標困難度也有顯著的調節效果。另外, 本研究也對該研究及預算制度實務提出未來研究方向及具體建議。 關鍵詞:預算參與、對上司之信任、預算目標困難度、管理績效 Abstract

This study examined the relationship between budget participation and managerial performance as mediated by trust in supervisor and explored the moderating role of budget-goal difficulty on budget participation, trust in supervisor, and managerial performance. One-hundred-fifty-five useful responses were drawn at random from subordinate managers of manufacturing companies listed on the Taiwan Stock Exchange. The mediating effect of trust in supervisor is examined by path analysis. Subgroup analysis was used to examine the contingency effect of budget-goal difficulty on the mediating role of trust in supervisor between budget participation and performance. The findings support our hypotheses and demonstrate the mediating effect of trust in supervisor and the moderating effect of budget-goal difficulty.

Key Words: Budget Participation, Trust in Supervisor, Budget Goal Difficulty, Managerial Performance

1. Introduction

For decades, behavioral scientists have intensively discussed the importance of budget participation as a means of improving performance (Milani, 1975; Brownell, 1982, 1983; Chenhall and Brownell, 1988; Dunk, 1989; Kren, 1992; Nouri and Parker, 1998). Some studies indicate that the direct influence of budget participation on managerial attitudes and performance is inconsistent. Hence, factors that may influence the relationship between participation and performance need further investigation.

Numerous researchers from various disciplines agree that trust has important benefits for organizations and managers. Previous studies suggest that managers’ trust in their supervisors directly influences managerial performance (Earley, 1986; McAllister, 1995; Dirks & Ferrin, 2001; Atuahene-Gima & Li, 2002). Management accounting studies also regard trust as an important factor in budgeting systems (Otley, 1978; Ross, 1994), and trust is influenced by participation in a budgeting context (Magner, Welker, & Campbell, 1995). Therefore, this study first explored the relationships among budget participation, trust, and managerial performance.

Goal-setting theory indicates that goals with different levels of difficulty have different motivational effects (Hofstede, 1968; Locke, 1968). However, this study suggests that, at different goal difficulty levels, a participative budgeting system has different motivational effects on managers.This study views budget-goal difficulty as a contingency variable and classifies goal difficulty levels as high, medium, and low in order to examine the mediating role of trust in supervisor between budget participation and managerial performance.

The rest of this paper proceeds as follows. The next section contains a review of the related literature, the model used, and the hypotheses tested. The research method is then described, followed by the results. The final section presents a discussion of the major findings, the limitations, and the implications for future research and practice.

2. Literature Review and Hypotheses

2.1 Budget Participation and Managerial Performance

Previous empirical results indicate that the relationship between budget participation and performance is inconsistent. Whereas some findings report a significant positive relationship between budget participation and performance (Merchant, 1981; Brownell, 1982), others show insignificant positive (Milani, 1975; Brownell and Hirst, 1986; Dunk, 1989) or even negative associations (Stedry, 1960; Cherrington & Cherrington, 1973). Hence, to interpret this conflict, some researchers suggest a contingency view (Brownell, 1983, 1985; Mia, 1988, 1989), whereas others use intervening variables to reconcile inconsistencies (Chenhall & Brownell, 1988; Kren, 1992; Nouri & Parker, 1998; Shields, Deng & Kato, 2000). In this study, we employ an intervening approach to reconcile inconsistencies.

Previous studies of the budgeting process suggest that participation serves several functions. Kren (1992) suggests that managers’ possession of job-related information gained from participation in budgeting processes improve their performance. Chenhall and Brownell (1988) argue that participation decreases managers’ role ambiguity and promotes performance. In addition, Nouri and Parker (1998) propose that budget participation enhances managers’ organizational commitment and then improves performance. In this study, we argue that budget participation provides communication opportunities to enhance subordinate managers’

positive attitudes, thus facilitating managerial performance. Hence, we propose that there is a positive relationship between budget participation and managerial performance:

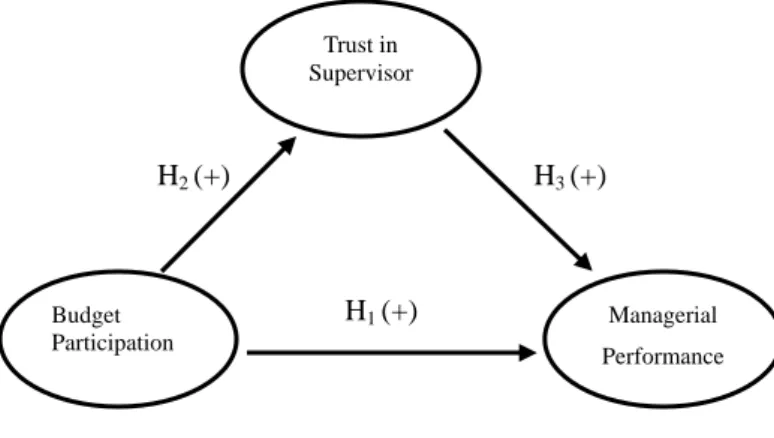

H1: Budget participation and managerial performance are positively correlated.

2.2 The Mediating Effect of Trust in Supervisor

2.2.1 Trust in Supervisor (Trust)

Trust is the belief that an individual can depend on another party, with positive, confident expectations (Das & Teng, 1998; Lewicki, McAllister, & Bies, 1998). Furthermore, McAllister (1995) indicates that affect-based trust, as developed by Lewis and Weigert (1985), is an individual’s belief that others care and are considerate. Such trust is considered to be significantly associated with an individual’s performance. Thus, this study specifies trust in supervisor as subordinates’ belief that their supervisor is caring and considerate, an affect-based trust.

2.2.2 Budget Participation (BP) vs. Trust in Supervisor

This study suggests that budget participation will positively influence trust in supervisor. Because budget participation provides opportunities for subordinates to express their opinions and views (Chenhall and Brownell 1988; Magner et al., 1995), a manager’s voice in a participative budget context promotes subordinates’ perceptions that a procedure is fair (Magner et al., 1995). Subordinates’ perception of procedural fairness will enhance their trust in supervisors (Kim & Mauborgne, 1993; Konovsky & Pugh, 1994). Thus, budget participation will promote perceptions of fairness and enhance trust in supervisor. Accordingly, we propose the following hypothesis:

H2: Budget participation and trust in supervisor are positively correlated.

2.2.3 Trust in Supervisor vs. Managerial Performance (MP)

Higher levels of trust lead to higher performance (Earley, 1986; McAllister, 1995; Dirks & Ferrin, 2001; Atuahene-Gima & Li, 2002). Because managers who possess high levels of trust in supervisor believe that they will receive fair treatment and reasonable rewards for achieving required objectives, trust will improve managerial performance (Atuahene-Gima & Li, 2002). Consequently, managers who possess higher levels of trust in supervisors will make more efforts to facilitate performance. The following hypothesis is proposed:

H3: Trust in supervisor and managerial performance are positively correlated.

2.2.4 Trust in Supervisor as an Intervening Variable

As discussed above, budget participation, trust in supervisor, and managerial performance are undoubtedly related. First, budget participation improves managerial performance. In addition, subordinate managers’ participation in budgetary settings enhances trust in supervisors, and this trust facilitates managerial performance. Therefore, we infer that trust in supervisor plays a mediating role between budget participation and managerial performance. The hypothesis is proposed below (the full theoretical model is presented in Figure 1):

H4: Trust in supervisor has a mediating effect on the relationship between budget

H3 (+) H2 (+) H1 (+) Trust in Supervisor Budget Participation Managerial Performance

Figure 1: Theoretical Model

2.3 The Contingency Effect of Budget-Goal Difficulty

Budget-goal difficulty specifies how difficult it is for managers to attain their budget goals (Steer, 1976; Kenis, 1979). This study suggests that the theoretical model proposed in Figure 1 will be moderated by budget-goal difficulty. This theoretical model will be untenable at both low levels and high levels of budget-goal difficulty and will be enhanced only at medium levels of budget-goal difficulty.

Because low levels of goal difficulty show that a goal can be achieved easily with less challenge, managers do not allocate much effort, time, skills, or knowledge to achieving their goal. Because the goal may be attained effortlessly, positive participation effects will not exist, and the relationship by which budget participation improves performance through trust will be absent.

High levels of budget-goal difficulty occur when a goal is very difficult to attain even if managers expend time and effort (Dunbar, 1971; Kenis, 1979). High levels of budget-goal difficulty mean that managers will not willingly accept a goal but will reject it mentally. Because managers mentally reject unattainable goals, positive budget-participation effects will be absent, making trivial the association between budget participation and managerial performance through trust.

This study suggests that at medium levels of budget-goal difficulty, the positive association between budget participation and managerial performance through trust in supervisor is obvious. Medium levels of goal difficulty refer to goals that are difficult but attainable if managers allocate efforts and time. To achieve their goals at medium levels of goal difficulty, subordinate managers must express their opinions and views through budget participation. Such participation provides opportunities for managers to communicate with their supervisors. The communication process will improve managers’ perceptions of fairness, thereby enhancing trust in supervisors (Magner et al., 1995). When managers’ high levels of trust in their supervisors convinces them of fair treatment and rewards (Atuahene-Gima & Li, 2002), they will exert more effort and time to improve their performance. Thus, trust in supervisor will improve managerial performance. Additionally, at this level of goal difficulty, the communication effects of budget participation will also facilitate managerial performance. As discussed above, indirect effects of budget participation on managerial performance through trust in supervisor will be noticeable at medium levels of goal difficulty. Therefore, this study proposes the following hypotheses: H5: At medium levels of budget-goal difficulty, relationships among budget

either low levels or high levels of budget-goal difficulty.

H6: At medium levels of budget-goal difficulty, indirect effects of budget

participation on managerial performance through trust in supervisor will be stronger than at either low levels or high levels of budget-goal difficulty.

3. Method

3.1 Sample and Data Collection

This study employed a cross-sectional survey to collect empirical data from a sample of 300 randomly selected manufacturing companies listed on the Taiwan Stock Exchange. A mail questionnaire with a cover letter and a self-addressed, prepaid envelope was forwarded to a sample of 900 subordinate managers chosen from three different functional departments, including marketing, accounting, and production operations in each company. These subordinate managers had a role in the budgeting process and in accountability for budget results.

Questionnaires were returned by 177 respondents; 22 of the responses received were removed for incompleteness, yielding an effective response rate of 17.2%. Therefore, 155 responses were available for data analysis. The average age of the respondents was 41.35 years, and the average time spent in their present organization and current position were 12.57 years and 4.55 years, respectively. The main functional areas in which respondents were employed included accounting (39.35%), production (31.61%), and marketing (21.94%). The majority (76.40%) of the respondents were male.

3.2 Measures

Four variables were measured in the questionnaire (see Appendix), including trust in supervisor, budget participation, budget-goal difficulty, and managerial performance. Measurements for these variables were taken primarily from previous studies. However, validity and reliability for each variable in this study are discussed below.

3.2.1 Trust in Supervisor

McAllister’s (1995) affect-based trust was employed to measure subordinates’ emotional trust in their supervisors. The five-item instrument was a seven-point Likert-type scale ranging from one (strongly disagree) to seven (strongly agree). McAllister (1995) provided evidence for the convergent and discriminate validity of this measure. Cronbach’s (1951) alpha coefficient in this study was 0.919, which was judged acceptable using Nunnally’s (1978) criteria of a minimum value of 0.6.

3.2.2 Budget Participation

This study used Milani’s (1975) six-item scale, which had been employed in prior studies. The instrument assessed the respondent’s involvement in and influence on the budget process using a seven-point Likert-type scale ranging from one (very little) to seven (very much). Previous studies report satisfactory validity and reliability for this scale (Brownell, 1982; Mia, 1988; Dunk, 1989, 1993; Nouri & Parker, 1998). Cronbach’s alpha coefficient was 0.836 for this study.

3.2.3 Budget-Goal Difficulty

Budget-goal difficulty as modified by Kenis (1979) from Steers (1976) was adopted for this study, using a five-item, seven-point Likert-type scale ranging from one (too loose) to seven (too tight). This instrument assessed the degree of managers’ effort, skill, and know-how in attaining their budget goals. Cronbach’s alpha coefficient was 0.771 for this study.

Managerial performance, as measured by a modified nine-item scale from Mahoney, Jerdee, and Carroll (1963, 1965), is a manager’s self-rating instrument consisting of eight performance facets and one overall effectiveness facet. Subordinate managers were asked to evaluate their managerial performance using these items. According to Mahoney et al. (1965), this study regressed the overall effectiveness dimension on the eight performance dimensions, finding the eight dimension model to be significant and to explain 62% of the variance for the overall effectiveness dimension. In addition, the overall effectiveness dimension was used frequently in previous studies (Mia, 1988; Dunk, 1989, 1993; Nouri & Parker, 1998). Thus, as Mahoney et al. (1965) suggested, this study employed the overall effectiveness dimension as an indicator for managerial performance evaluation.

4. Results

Descriptive statistics and the correlation matrix for the variables examined in this study appear in Tables 1 and 2. Table 2 shows the positive relationship between budget participation and trust. In addition, it shows that both budget participation and trust are positively related to performance. These results correspond to the theoretical model in Figure 1 and support our hypotheses one, two, and three.

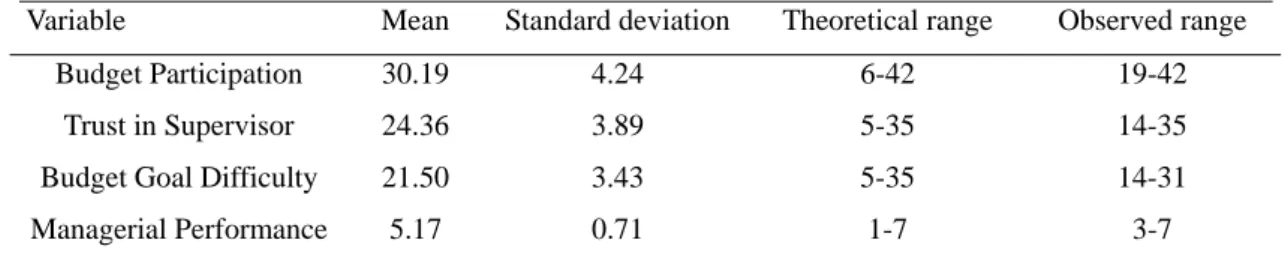

TABLE 1. Descriptive statistics

Variable Mean Standard deviation Theoretical range Observed range Budget Participation 30.19 4.24 6-42 19-42

Trust in Supervisor 24.36 3.89 5-35 14-35 Budget Goal Difficulty 21.50 3.43 5-35 14-31 Managerial Performance 5.17 0.71 1-7 3-7 n=155

TABLE 2. Matrix of inter-correlations

MP BP Trust

BP 0.248**

Trust 0.349** 0.223**

BGD - 0.025 0.029 0.224**

n=155; two tailed significance; **p < 0.01.

MP, Managerial Performance; BP, Budget Participation; Trust, Trust in Superviosr; BGD, Budget Goal difficulty.

4.1 The Mediating Effect of Trust in Supervisor

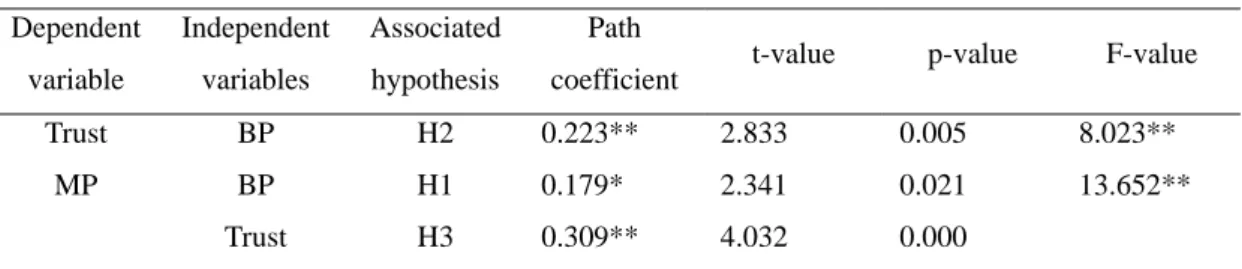

This study uses path analysis to evaluate the mediating effect of trust in supervisor. The path coefficients were estimated using regression and correlation analysis. Hypotheses one, two, and three and their corresponding path coefficients appear in Table 3. Hypotheses two and three have related path coefficients with P values less than .01. In addition, the path coefficient between BP and MP is significant (P = .021), showing that budget participation promotes managerial performance directly, whereas the relationship may also be mediated via trust.

TABLE 3. Path analysis results Dependent variable Independent variables Associated hypothesis Path

coefficient t-value p-value F-value Trust BP H2 0.223** 2.833 0.005 8.023** MP BP H1 0.179* 2.341 0.021 13.652**

Trust H3 0.309** 4.032 0.000 n=155; **p<0.01; *p<0.05

Decomposition of the observed correlation was employed, with results listed in Table 4. With regard to the total relationship between BP and MP, the zero order correlation is 0.248 (P < .01, Table 2). The results in Table 4 show that the correlation consists of a direct effect (0.179) and an indirect effect (0.069).

TABLE 4. Decomposition of observed correlations

Combination of variables Observed correlation = Direct effect + Indirect effect + Spurious effect

BP/Trust 0.223 0.223 - -

Trust/MP 0.349 0.309 - 0.040

BP/MP 0.248 0.179 0.069 -

According to Baron and Kenny (1986), this result suggests that trust functions as a mediator and that there exists a partial mediating effect between BP and MP. First, BP is significantly related to Trust (Table 2, P < .01). Second, Trust is significantly related to MP (Table 2, P < .01). Third, the relationship between BP and MP decreases after controlling for Trust but remains significant (Table 3, path coefficient = 0.179). Furthermore, as Baron and Kenny (1986) indicated, full mediation occurs when the relationship between an independent variable and a dependent variable is no longer significant after controlling for the mediator variable. Thus, we suggest that Trust has a partial mediation effect on the relationship between BP and MP, which supports hypothesis four.

4.2 The Moderating Effect of Budget-Goal Difficulty

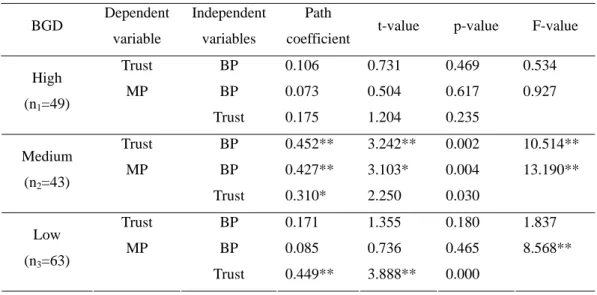

To test the moderating effect of BGD on the links among BP, Trust, and MP, we categorized the BGD variable into three subgroups. The responses were sorted in ascending order by BGD score. The bottom one-third of responses were classified as the “low level of BGD” group (mean of BGD = 3.625; range from 14 to 20), whereas the top one-third of responses were classified as the “high level of BGD” group (mean of BGD = 5.090; range from 24 to 31). The remainder of the responses was classified as the “medium level of BGD” group (mean of BGD = 4.390; range from 21 to 23). Because we hypothesized that all links among BP, Trust, and MP are stronger at medium BGD, the correlations and path coefficients under the three different levels of BGD were calculated and appear in Tables 5 and 6.

TABLE 5. Matrix of inter-correlations at different levels of budget goal difficulty

BGD High (n1=49) Medium (n2=43) Low (n3=63) z1 (High vs. Medium) z2 (Medium vs. Low) BP Trust BP Trust BP Trust BP Trust BP Trust Trust 0.106 0.452** 0.171 -1.761* 1.541

MP 0.092 0.183 0.567** 0.502** 0.162 0.464** -2.548** 1.697* 2.350** 0.243 Two-tailed significance of t: ** p<0.01; * p<0.05. Two-tailed significance of z: ** p<0.05 * p<0.1.

TABLE 6. Path analysis results at different level of budget goal difficulty BGD Dependent

variable

Independent variables

Path

coefficient t-value p-value F-value Trust BP 0.106 0.731 0.469 0.534 MP BP 0.073 0.504 0.617 0.927 High (n1=49) Trust 0.175 1.204 0.235 Trust BP 0.452** 3.242** 0.002 10.514** MP BP 0.427** 3.103* 0.004 13.190** Medium (n2=43) Trust 0.310* 2.250 0.030 Trust BP 0.171 1.355 0.180 1.837 MP BP 0.085 0.736 0.465 8.568** Low (n3=63) Trust 0.449** 3.888** 0.000 ** p< 0.01; * p<0.05

Hartmann and Moers (1999) suggested that subgroup analysis is appropriate for strength of moderation. They indicated that strength of moderation is supported when statistically significant differences exist in the value of correlation coefficients between variables across groups. Table 5 shows that all correlation coefficients among BP, Trust, and MP are statistically significant at medium BGD, whereas the correlations between PB and Trust and between PB and MP do not show statistically significant relationships under the other two levels of BGD. However, this study did not predict a significant relationship between Trust and MP, which might be an interesting topic for future research.

In addition, we demonstrated the significance of z-scores between correlation coefficients of the two subgroups in table 5(subgroup “high” vs. “medium”; subgroup “medium” vs. “low”). The z1 values, comparing the correlation coefficients of high

BGD with medium BGD, show that relationships among BP, Trust, and MP are stronger at medium levels than at high levels. However, the z2 values, comparing the

correlation coefficients of medium BGD with low BGD, show that relationships at medium BGD levels are not stronger than at low BGD levels, except for the relationship between BP and MP. Accordingly, the results partially support hypothesis five.

Through path analyses at different levels of BGD, we found that hypothesis six was supported (Table 6); these results were shown in Figure 2. The path coefficients between BP and Trust and between BP and MP are not statistically significant, other than at medium BGD. Again, we employ Baron and Kenny’s (1986) perspective. Indeed, only at medium BGD does the partial mediating effect of Trust exist. At this

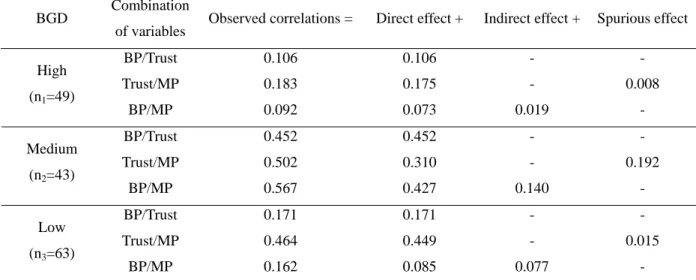

level, the relationship between BP and Trust is statistically significant (Table 5, P < 0.01). Additionally, Trust is significantly related to MP (Table 5, P < .01). Third, the relationship between BP and MP decreases after controlling for Trust but remains statistically significant (Table 6, path coefficient = 0.427). The decomposition of observed correlations at different levels of BGD appears in Table 7. Thus, the results show that the mediating effect of Trust does not exist except at medium BGD levels; these results support hypothesis six.

TABLE 7. Decomposition of observed correlations at different level of budget goal difficulty BGD Combination

of variables Observed correlations = Direct effect + Indirect effect + Spurious effect

BP/Trust 0.106 0.106 - - Trust/MP 0.183 0.175 - 0.008 High (n1=49) BP/MP 0.092 0.073 0.019 - BP/Trust 0.452 0.452 - - Trust/MP 0.502 0.310 - 0.192 Medium (n2=43) BP/MP 0.567 0.427 0.140 - BP/Trust 0.171 0.171 - - Trust/MP 0.464 0.449 - 0.015 Low (n3=63) BP/MP 0.162 0.085 0.077 - 0.449** (3.888) 0.171 (1.355) 0.310* (2.250) 0.452** (3.242) 0.175 (1.204) 0.106 (0.731) 0.179* (2.341) 0.309** (4.032) 0.223** (2.833) Trust BP MP All

High Medium Low

Trust BP MP Trust BP MP Trust BP MP

Figure 2. Path Analysis by subgroups of Budget Goal Difficulty **p< 0.01; *p< 0.05 (two-tailed tests); ( ) is t value.

0.073 (0.504) 0.427** (3.103) 0.085 (0.736) 5. Conclusion

The first purpose of this study was to examine the role of trust in supervisor in budget participation and managerial performance. Empirical results indicate a directly positive association between budget participation and performance and an indirect effect of trust in supervisor. Additionally, the relationships between budget

participation and trust and between trust and managerial performance are validated. The results suggest that participation could improve communication and interaction between subordinate managers and their supervisors to enhance their trust. Thus, we confirm the critical role of budget participation for enhancing subordinate managers’ trust in supervisors and for managerial performance. In addition, managers’ trust is important for improving performance.

Furthermore, we examined the moderating effect of budget-goal difficulty at different levels. Our study validated stronger relationships among budget participation, trust, and managerial performance at medium goal difficulty. These results support the hypothesis that medium goal difficulty is optimal (Kenis, 1979) and may imply a nonlinear relationship between goal difficulty and performance or attitude, as suggested by previous studies (Stedry & Kay, 1966; Hofstede, 1968; Erez & Ziden, 1984). Our results also suggest that a supervisor should set challenging and attainable goals, rather than goals that are too difficult, to generate the best participation effect on trust and performance.

For future research, we suggest that independent variables related to a budgeting system, such as budget emphasis, could play different roles in the model. Thus, we suggest the investigation of other potential models and other possible analytic methodologies to examine the role of trust in budget control systems.

However, our findings are subject to several limitations. Previous literature suggests other possible variables in trust-related studies, such as culture, which has been regarded as an important contextual variable (Atuahene-Gima & Li, 2002; Luo, 2002). Because our empirical data was drawn from Taiwan, our results might not be generalizable to other countries. In addition, the survey approach has limitations, such as self-rating measures of managerial performance. Despite these limitations, this study provides implications for budgeting system design and highlights the role of trust in supervisor in budgeting systems.

REFERENCE

Atuahene-Gima, K. & Li, H. (2002). When does trust Matter? Antecedents and contingent effects of supervisee trust on performance in selling new products in China and the United States. Journal of Marketing, 66, 61-81.

Baron, R. M. & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 1173-1182.

Brownell, P. (1982). The role of accounting data in performance evaluation, budget participation, and organizational effectiveness. Journal of Accounting Research, 20, 12-27.

Brownell, P. (1983). Leadership style, budgetary participation and managerial behavior. Accounting, Organizations and Society, 8, 307-322.

Brownell, P. (1985). Budgetary systems and the control of functionally differentiated organizational activities. Journal of Accounting Research, 23, 502-512.

Brownell, P. & Hirst M. (1986). Reliance on accounting information, budgetary participation and task uncertainty: Tests of a three-way interaction. Journal of

Accounting Research, 24:2, 241-249.

Cherrington, D. J. & Cherrington, J. O. (1973). Appropriate reinforcement contingencies in the budgeting process, Journal of Accounting Research, Supplement: 225-253.

Chenhall, R. H. & Brownell P. (1988). The effect of participative budgeting on job satisfaction and performance: Role ambiguity as an intervening variable.

Accounting, Organizations and Society, 13, 225-233.

Cronbach, L. T. (1951). Coefficient alpha and the internal structure of tests.

Psychometrika, 297-334.

Das, T. K. & Teng, B. S. (1998). Between trust and control: developing confidence in partner cooperation in alliances. Academy of Management Review, 23:3, 491-512.

Dirks, K. T. & Ferrin D. L. (2001). The role of trust in organizational settings.

Organization Science, 12:4 450-467.

Dunbar, R. L. M. (1971). Budgeting for control. Administrative Science Quarterly, 16:1, 88-96.

Dunk, A. (1989). Budget emphasis, budget participation and managerial performance: a note. Accounting, Organizations and Society, 14, 321-324.

Dunk, A. (1993). The effects of job-related tension on managerial performance.

Accounting, Organizations and Society, 18, 575-586.

Earley, P. C. (1986). Trust, perceived importance of praise and criticism, and work performance: An examination of feedback in the United States and England.

Journal of Management, 12, 457-473.

difficulty to performance. Journal of Applied Psychology, 69-78.

Hartmann, F. G. H. & Moers F. (1999). Testing contingency hypotheses in budgetary research:an evaluation of the use of moderated regression analysis. Accounting,

Organizations and Society, 24, 291-315.

Hirst, M. & Lowy, S. (1990). The linear additive and interactive effects of budgetary goal difficulty and feedback on performance. Accounting, Organizations and Society, 15, 425-436.

Hofstede, G. H. (1968). The Game of Budget Control. London: Tavistock.

Kenis, I. (1979). Effects of budgetary goal characteristics on managerial attitudes and performance. The Accounting Review, 54, 707-721.

Kim, W. C. & Mauborgne, R. A. (1993) Procedural justice, Attitude, and subsidiary top management compliance with multinationals’ corporate strategic decision.

Academy of Management Journal, 36, 502-526.

Konovsky, M. A. & Pugh, S. D. (1994). Citizenship behavior and social exchange.

Academy of Management Journal, 37:3, 656-669.

Kren, L. (1992). Budgetary participation and managerial performance: the impact of information and environmental volatility. The Accounting Review, 67, 511-526.

Latham, G. P. & Steele, T. P. (1983). The motivational effects of participation versus goal setting on performance. Academy of Management Journal, 26:3, 406-417.

Lewicki, R. J., McAllister, J. D. & Bies, R. J. (1998). Trust and distrust: new relationships and realities. Academy of Management Review, 23:3, 438-458.

Lewis, J. D. & Weigert, A. (1985). Trust as a social reality. Social Forces, 63, 967-985.

Libby, T. (1999). The influence of voice and explanation on performance in a participative budgeting setting. Accounting, Organization and Society, 24, 125-137.

Locke, E. A. (1968). Toward a theory of task motivation and incentives.

Organizational Behavioral and Human Performance, 159-189.

Luo, Y. (2002). Building trust in cross-cultural collaborations: toward a contingency perspective. Journal of Management, 28:5, 669-694.

Magner, N., Welker, R. & Campbell, T. (1995). The interactive effect of budgetary participation and budget favorability on attitudes toward budgetary decision makers: a research note. Accounting, Organization and Society, 20, 611-618.

Mahoney, T. A., Jerdee, T. H. & Carroll S. J. (1963). Development of Managerial performance: A research approach. Cincinnati, OH: South-western Publishing Company.

Mahoney, T. A., Jerdee, T. H. & Carroll S. J. (1965). The job of management.

Industrial Relationships, 97-110.

McAllister, D. J. (1995). Affect- and cognition-based trust foundations for interpersonal cooperation in organizations. Academy of Management Journal, 38:1,

24-39.

Merchant, K. A. (1981). The design of the corporate budgeting system: influences on managerial behavior and performance. The Accounting Review, 813-829.

Mia, L. (1988). Managerial attitude, motivation and the effectiveness of budget participation. Accounting, Organizations and Society, 13, 465-476.

Mia, L. (1989). The impact of participation in budgeting and job difficulty on managerial performance and work motivation: a research note. Accounting,

Organizations and Society, 19, 1-14.

Milani, K. (1975). Budget-setting, performance and attitudes. The Accounting Review, 5, 274-284.

Nouri, H. & Parker, R. (1998). The relationship between budget participation and job performance: the roles of budget adequacy and organizational commitment.

Accounting, Organizations and Society, 23, 467-483.

Nunnally, J. C. (1978). Psychometric Theory. New York: McGraw-Hill.

Otley, D. (1978). Budget use and managerial performance. Journal of Accounting

Research, 16, 122-149.

Ross, A. (1994). Trust as a moderator of the effect of performance evaluation style on job-related tension: a research note. Accounting, Organizations and Society, 19, 629-635.

Shield, M., Deng, F. J. & Kato, Y. (2000). The design and effects of control system: tests of direct- and indirect-effects models. Accounting, Organizations and Society, 25, 185-202.

Stedry, A. C. (1960). Budget control and cost behavior. Englewood Cliffs, NJ: Prentice-Hall.

Stedry, A. C. & Kay, E., (1966). The effects of goal difficulty on performance: A field experiment. Behavioral Science, 495-470.

Steer, R. M. (1976). Factors affecting job attitudes in a goal setting environment.

Academy of Management Journal, 19:1, 6-16.

Tiller, M. (1983). The dissonance model of participation budgeting: an empirical exploration. Journal of Accounting Research, 21, 581-595.

計畫成果自評 本研究結果與原計畫預期結果相符合,顯示本研究具有相當紮實的理論與實務 基礎,可做為未來學術理論研究及預算制度實務上有效的建議。在學術理論上, 本研究確認過去在管理會計領域,甚少提及的對上司信任之構念,做為預算參與 和管理績效間的中介角色,另外,預算困難度的調節角色也同樣獲得印證,確實 為預算制度的設計建構出新的理論基礎。在預算制度實務上,該理論同樣提供預 算制度設計一項新的思考方向與建議。本計畫認為本研究在預算制度設計上具有 相當大管理意涵及貢獻。