行政院國家科學委員會專題研究計畫 成果報告

股票獎酬制度與代理問題之研究(第 2 年)

研究成果報告(完整版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 95-2416-H-004-047-MY2 執 行 期 間 : 96 年 08 月 01 日至 98 年 04 月 30 日 執 行 單 位 : 國立政治大學會計學系 計 畫 主 持 人 : 梁嘉紋 共 同 主 持 人 : 金成隆 計畫參與人員: 碩士班研究生-兼任助理人員:黃于庭 碩士班研究生-兼任助理人員:鄭卉霞 碩士班研究生-兼任助理人員:李智蕙 報 告 附 件 : 出席國際會議研究心得報告及發表論文 處 理 方 式 : 本計畫涉及專利或其他智慧財產權,2 年後可公開查詢中 華 民 國 98 年 07 月 30 日

Stock-based Compensation in a Concentrated Ownership Setting: An Empirical Investigation

Abstract:

This study examines the determinants and the performance consequences of stock-based compensation in a context of concentrated ownership structure. Stock-based compensation has been viewed to be a mechanism of alleviating the agency problem between the shareholders and the managers. This view stems from a diffused ownership structure and managers owning very little of the firms they manage. However, in the situation where concentrated ownership results in agency conflict between controlling owners and the minority shareholders, the use of

stock-based compensation becomes a potential self-dealing tool for rent extraction by the controlling owners in depriving minority shareholders. Based on a sample of Taiwanese firms, we find that the use of stock-based compensation is consistent with incentive alignment perspective when control concentration is low, but becomes a self-dealing tool for large shareholders when control is more concentrated. Key words: Stock-based compensation, corporate governance, agency problem, concentrated ownership, cash flow right and voting right

Stock-based Compensation in a Concentrated Ownership Setting: An Empirical Investigation

1. Introduction

The objective of this study is to examine the determinants and the performance consequences of stock-based compensation in a context of concentrated ownership structure. Stock-based compensation has been viewed to be an important

mechanism of tying managers’ wealth to firm performance and thus alleviating the agency problem between the shareholders and the managers (Jensen and Meckling 1976). Many existing studies have predicted their analyses based on this incentive alignment framework as a solution for the moral hazard problem (e.g. Himmelberg et al., 1999; Core and Guay, 1999; Rajgopal and Shevlin, 2002). This perspective stems from managers owning very little of the firms they manage and most empirical studies from this perspective examine the executive compensation contracts of large U.S. firms that are widely-held. However, in emerging markets, such as Hong Kong, Taiwan, India, and Singapore, high ownership concentration results in agency conflict between controlling owners and the minority shareholders (La Porta et al. 1999; Claessens et al 2002; Fan and Wong, 2004) and makes this agency solution questionable.

Despite its potential benefit of incentive alignment between managers and shareholders, the use of stock-based compensation has long been criticized for its transfer of claims on equity from existing shareholders to employees and diluting existing shareholders’ interest. Researchers have also shown that managers use stock compensation for their own benefit (e.g., Yermack, 1997; Aboody and Kasznik, 2000). This problem could be even more severe under a concentrated ownership structure because the management group (and its family members) is usually the largest

block-holders of a firm at the top of the pyramid and has control over the pay-setting process. When the management block-holder possess control rights that exceed their cash flow rights in the firm, stock-based compensation becomes a potential

self-dealing tool for rent extraction by the controlling owners in depriving minority shareholders (rent extraction perspective). However, this entrenchment problem can come at a price to the controlling owners and the firms, i.e. outside investors

anticipate the problem and thus discount the share prices (Classens et al. 2002; Fan and Wong, 2005) and raise the cost of issuing equities in the future.

Hanlon, Rajgopal, and Shevlin (2003) examine the association between

executive stock options (ESOs) and future earnings and find that the payoffs to ESOs appear to be driven predominantly by economic determinants of option grants and not poor governance quality. Their results are based on a sample of US large firms with diffuse ownership and may not be generalized to firms with concentrated ownership. The objective of this study is to examine the determinants and the performance consequences of stock-based compensation in the emerging market typified with a concentrated ownership structure. Specifically, we investigate whether the use of stock-based compensation in a concentrated ownership setting is consistent with the economic motivation of incentive alignment between managers and shareholders or is a result of rent extraction stemming from the agency conflict between controlling owners and minority shareholders.

We use a sample of Taiwanese firms to examine the predictions from the incentive alignment perspective and the rent extraction perspective in a concentrated ownership structure. In Taiwan, a large percentage of publicly-traded companies has high concentration of ownership. On average, various family groups control 78% of listed companies on the Taiwan Stock Exchange. In 57.6% of family-controlled

companies, the largest family holds more than half of the board seats (Ko, Ding, Liu and Yeh, 1999). In addition, the use of stock-based compensation in Taiwan has been of interest to the local capital market and foreign institutional investors.1 For example, on July 18, 2002, the headline of the Asian Wall Street Journal points out that the stock bonuses practice in Taiwan triggers foreign investors’ concerns in share dilution and transparency to outside shareholders. Taiwan Company Law requires firms to distribute some percentage of their net income each year as employees’ bonus. The total bonus is distributed to employees based on their ranks, thus higher-level employees get more from the bonus pool. It is common that controlling owner actively participates in the operation of the company and serves on the board and as executive officers of the company as well. Thus, through their power on the board, controlling owner, who is also the manager, is able to influence the decision on the percentage of earnings distributed to the employees, if the bonus rate is not specified as a fixed rate in the firm’s articles of incorporation, and the subsequent bonus allocation among employees. Despite that corporate management in Taiwan often claims that employee stock bonuses is an important mechanism in aligning employees’ incentives, the concentrated ownership structure essentially shift the agency problem away from manager-shareholder conflicts to the conflicts between the management block-holder and minority shareholders. Thus, it is not clear whether firms use employee stock bonuses effectively.

To capture the agency conflict typified in the East-Asia emerging markets, we use the level of the largest shareholders’ cash flow right (ownership) to proxy for the incentive alignment effect and the level of the largest shareholders’ voting right

1

Stock-based compensation in Taiwan includes employee stock bonuses and employee stock option plans. Employee stock bonus has been widely used since the 1990s, especially in the high-hech industries. Stock option plans were not permitted under Taiwanese regulation until 2001 and relatively few firms adopt stock option plans to date. For this proposal, we focus on employee stock bonus and

(control) to proxy for the degree of rent extraction. When the largest shareholders’ wealth is more tied to the company (i.e. as cash flow right increases), his/her interest is more aligned with minority shareholders. On the other hand, the largest

shareholder has greater ability to deprive minority shareholders when his control (voting right) over the company increases. The agency conflict between controlling owners and the minority shareholders is thus more severe when the level of the largest shareholder’s voting right is deviated from the level of his/her cash flow right. In addition to these two variables, we also include other economic factors related to the incentive alignment perspective, corporate governance factors related to the rent extraction perspective, and other control variables.

Our analysis contains two sets of tests. The first examines the determinants of stock-based compensation in Taiwan. This test is aimed to investigate whether stock-based compensation in a concentrated ownership setting, on average, is used as a solution for the agency problem or is a reflection of the agency conflict between controlling owners and minority shareholders. The second set of tests then examines whether stock-based compensation is associated with firms’ future performances. We expect that if the stock-based compensation is used as a solution to the agency problem, then stock-based compensation should be positively associated with firms’ future performances. On the other hand, if stock-based compensation is used as a self-dealing tool by the controlling owner, we expect stock-based compensation to be negatively associated with firms’ future performances.

Controlling for other economic factors related to stock-based compensation, our evidence shows that when voting rights are more concentrated (voting rights ≧ 30%), stock-based compensation is positively associated with the divergence between voting rights and cash flow rights, suggesting that large shareholder entrenchment is

more prevalent. By contrast, the association is not significant in the low-control subsample (voting rights < 30%). We also find that only the subsample with voting rights less than 30% (low-control-concentration group) exhibits a positive association between stock-based compensation and future performance. For the subsample with voting rights greater than 30%, we do not find stock-based compensation to be positively associated with future performance. Taken together, these results suggest that the use of stock-based compensation is consistent with incentive alignment perspective when control concentration is low, but becomes a self-dealing tool for large shareholders when voting rights are more concentrated.

The contribution of this study is two-fold. First, we shed light on the use of stock-based compensation in the context of concentrated ownership structure. Prior theory and empirical evidence on stock-based compensation mostly focus on western firms that are widely-held. However, to our best knowledge, no study to date examines the use of stock-based compensation in the presence of concentrated ownership. This study contributes to the corporate governance literature by linking stock-based compensation to the agency problem embedded in the concentrated ownership structure. Second, firms intensively using stock-based compensation usually claim that stock-based compensation helps to alleviate the agency problems between employees and shareholders. Our study provides evidence and policy implication that instead of being an agency solution between employee and

shareholder, stock-based compensation could also be a self-dealing tool resulted from the agency problem between large shareholder and minority shareholders.

In section 2, we review the literature related to incentive alignment and rent extraction aspects of stock-based compensation, discuss the agency problem in the emerging markets, and develop our hypotheses. Section 3 describes the sample and

empirical models. Section 4 summarizes the results, followed by a conclusion.

2. Background and hypothesis development

In this section, we discuss the literature related to stock-based compensation and the agency problem specific to the emerging markets, develop our hypotheses, and describe variables used to test each hypothesis.

2.1 Stock-based compensation

Jensen and Meckling (1976) illustrate that equity-based compensation can induce managers to behave as if he/she were maximizing the shareholder’s welfare and thus shareholders are expected to tie managers’ wealth to firm performance for inducing managers to take actions that increase firm value. A number of researchers have largely worked within this incentive alignment framework to explain various features observed in compensation contracts and variation in compensation contracts across firms. For example, Core and Guay (1999) show that firms grant options and shares to CEOs in a manner that is consistent with the optimal level of equity incentives and firm value maximization. Himmelberg, Hubbart, and Palia (1999) argue that the cross-sectional variation in managerial ownership is explained by firm heterogeneity, such as stock price variability, firm size, capital intensity, R&D intensity, etc and is consistent with the predictions of principal-agent models. This line of research has predicted their analyses on the premise of dispersed ownership and argued that equity compensation is consistent with firm value maximization.

However, the existing evidence on the link between equity ownership and future performance is mixed. Morck, Shleifer, and Vishny (1988) and Hanlon, Rajgopal, and Shevlin (2003) show that equity ownership and employee stock option (ESO)

grants are associated with improved future performance. Yet, Himmelberg, Hubbart, Palia (1999) and Loderer and Martin (1997) fail to find evidence that changes in managerial ownership affect firm performance. Possible reasons for the mixed evidence include that managers may control the pay-setting process and compensate themselves beyond the level optimal for shareholders (Hanlon, Rajgopal, and Shelvin 2003; Shivdasani and Yermack 1999) and that options/shares are an inefficient way to compensate managers (e.g. Hall and Murphy 2002, Lambert and Larcker 2002). Another possible reason that has been relatively less studied in the literature is that even in the United States, ownership is not completely dispersed and concentrated holdings by families and wealthy investors are more common than is often believed (Shleifer and Vishny 1997; Lins 2003; Klasa 2005). This contradicts the premise of diffuse ownership and thus the empirical finding may be inconsistent with the

predictions derived from the traditional principal-agent framework.

2.2 Agency problem with concentrated ownership

Concentrated ownership are not domiciled in the U.S. or a few other developed countries (Shleifer and Vishny 1997 La Porta, Lopez-de-Silanes, and Shleifer 1999; Claessens, Djankov, and Lang 2000). Research on corporate governance issues in emerging market has also frequently emphasized on the feature of high concentrated ownership in these markets (e.g. Lins 2003 and Fan and Wong 2005). Concentrated ownership coincides with a lack of investor protection (i.e. weak property right) to solve the managerial agency problem and thus shareholders seek to discipline management and protect themselves by becoming controlling owners (La Porta, Lopez-de-Silanes, and Shleifer 1999). Controlling owners obtain the power through high voting right and the incentives through high cash flow rights to negotiate and

enforce corporate contracts with various stakeholders, including minority shareholders, managers, laborers, suppliers, customers, and governments.2

Through pyramid structures, controlling owner may possess control (control right) in excess of the proportional ownership (cash flow right) and this creates another agency problem that the interests of controlling and minority shareholders are not perfectly aligned (Claessens, Djankov, Fan, and Lang 2002). Specifically, when ownership is sufficiently concentrated and an owner obtains dominant control of a firm, the controlling owner is able to determine the profit distribution and may engage in entrenchment behaviors to deprive minority shareholders’ interests, especially when the controlling owner possesses high levels of control, with low equity ownership level.

When the controlling owner is intensively involved in the operation of the firm, he/she and his/her family members usually become the managers of the firm and the managers of each firm down the line in the pyramid. Through granting employee stock bonuses, the controlling owner then is able to deprive existing minority shareholders’ interest and to distribute more earnings to himself/herself.3 The Taiwanese law requires firms to distribution a certain percentage of earnings to employees as employees’ bonuses in a form of either stock (calculated based on the face value of NT$10) or cash. The form of employee bonuses distributed and the distribution of employee bonuses among employees are subject to the

management/controlling owners’ discretion.4 If the management group is granted with employee bonuses in the share form, its actual payoff at fair value is greater than

2

For detained discussion, see Fan and Wong (2002)

3

According to Taiwanese law, employee stock bonus is considered as a mechanism of earnings distribution.

4

Firms’ articles of incorporation usually state that the total bonus is distributed to employees based on their ranks. Thus, it is reasonable to assume that the management group receives more employee bonuses from the bonus pool than lower level employees do.

the face value of the shares when the shares are traded at a price greater than the par value. Although the employee bonus shares granted dilutes existing shareholder’s interest, the cost of dilution to the controlling owners is less than the benefits he receives from the outright employee bonus shares, which can be traded right after receiving the shares. Thus, the agency conflict between controlling owner and minority shareholder makes stock-based compensation a potential entrenchment tool for the controlling owners in depriving minority shareholders.

2.3 Determinants of stock based compensation

In this subsection, we discuss the determinants of stock based compensation drawn from prior literature and factors specific to the regulation/business environment in Taiwan.

Cash flow right

If the management, who is also the controlling owner, already holds a substantial amount of shares, then the marginal benefit of granting additional shares to the

manager for incentive alignment is decreasing in controlling owner’s ownership (cash flow right). Under the incentive alignment framework, Core and Guay (1999) report that current year stock grant adjust deviation of the incentive effects of the

management’s existing portfolio from target level of incentives. This suggests a negative association between employee stock bonus grants and controlling owner’s cash flow right.

However, Fan and Wong (2002) suggest that one way to mitigate the problem of controlling owner entrenchment is to increase further the controlling owner’s

increases in his/her cash flow rights in the firm mean that it will be more costly for the controlling owner to divert the firm’s cash flows for private gain. Specifically, if the controlling owner extract excessive private benefits when he/she still holds a

substantial amount of share, their share value will be reduced because minority shareholders discount the stock price accordingly. Thus, we expect that the association between employee stock bonuses and cash flow right is decreasing in a decreasing rate (a convex function).

Divergence between control right and cash flow right

The cross-holding structure in Taiwan, as well as other East Asia Emerging markets, allows controlling owners to commit low equity investment while maintaining effective control of the firm, creating a separation in control (voting rights) and ownership (cash flow rights) (Fan and Wong 2002). This divergence between voting and cash flow rights results in low degree of alignment between the controlling owner and minority shareholders. A controlling owner, who is also the manager, could extract wealth from minority owners by compensating himself with excessive stock compensation, while only bears a fraction of the dilution costs. Thus, we expect a positive association between stock bonus grants and the divergence

between control right and cash flow right.

Following Fan and Wong (2002), we use a ratio of voting rights over cash flow right (VC ratio) to measure the degree of divergence between voting right and ash flow right. The larger of the ratio indicates a larger divergence between control right and cash flow right.

Taiwan accounting rules allows company to record employee bonuses as

earnings distribution without any charge against earnings. Besides, employee stock bonuses are recorded at par value (NT$10), regardless of the share prices. This financial reporting treatment for employee stock bonuses provides a means of

boosting reported income. Specifically, if a firm expects reported income to be low, it could reduce reported compensation expense by substituting bonus shares for other forms of compensation. In other words, if a firm receives a benefit from reporting higher levels of income, the effective cost of granting employee stock bonuses is reduced. Thus, firms facing large financial reporting costs might use employee stock bonuses as an instrument of earnings management. To proxy for financial reporting costs, we use the following measures

1) Interest coverage: Matsunaga, Shevlin, and Shore (1992) and Yermack (1995) suggest that firms with low interest coverage may have low profitability and high risks of violating debt covenants and thus interest coverage is a common proxy for financial reporting costs. Interest coverage is measured as operating income divided by interest expense. 2) ADR: firms issue American Depositary Receipts (ADRs) are required

to recognize the share bonuses as an expense on their filings to comply with US accounting procedures. This requirement often creates large discrepancies between reported income figures under Taiwanese GAAP and US GAAP and draws attention from investors and business press. This variable is a dummy variable with value equal to 1 if the firm issues ADR and 0 otherwise.

3) Stock price: as employee stock bonuses are recorded at par value (NT$10), regardless of the share prices, we expect that the benefit from

reducing financial reporting costs increases with the share price on the market when firms’ stock price is greater than NT $10.

Investment opportunity:

Smith and Watts (1992) and Gaver and Gaver (1993) show that firms with greater investment opportunities are likely to use more stock-based compensation. Information asymmetry emerges when managers have more private information about the value of investment opportunities than the shareholders. Therefore, companies with large investment opportunities should use more stock-based compensation to tie managers’ wealth to shareholders’ interests (e.g. Bizjak, Brickley, and Coles 1993). Based on a sample of Taiwanese firms, Chen (2003) also shows that firm equity value is positively related to the amount of earnings distributed as stock bonus and the positive relation is stronger when the firm has greater future investment opportunities.

Prior studies use various measures to capture firms’ investment opportunities. For example, Smith and Watts (1992) use book to market value of total assets, while Core et al. (1999) use market to book value of equity to proxy for future investment opportunities. Yermack (1995) defines a variable approximately equal to Tobin’s Q by adding together the book value of assets and the difference between the market and book values of common stock, and dividing the total by the book value of assets. Matsunaga (1995) use the market to book ratio and the level of R&D expenditure (deflated by total assets) to measure the firm’s growth opportunity. Hanlon,

Rajgopal, and Shelvin (2003) use R&D/sales and book to market value of total assets to measure investment opportunities. Gaver and Gaver (1993) and Chen (2003) use a group of measures to construct an index that captures the investment opportunity concept. They include past investment intensity, geometric mean annual growth rate

of market value of assets, market to book value of equity/assets, R&D expenditure to book value of total assets, R&D expenditure to total revenues, earnings-to-price ratio, etc. In this study, we use market to book ratio to proxy for investment and growth opportunities.

Tax consideration:

Employee stock bonus in Taiwan provides no tax deduction for firms and thus firms with tax loss carry-forward have lower marginal tax rates and should provide a less fraction of employee compensation in the form of stock-based compensation. We expect that firms with a tax loss carry-forward would be less likely to use employee stock bonuses

Liquidity:

Compensating employees through share bonuses allows firms to conserve cash, while being competitive in attracting/retaining high quality employees. Following Matsunaga, we measure a firm’s liquidity as beginning working capital deflated by beginning total assets.

Dividend payout policy:

Dividend payout policy may influence the use of stock-based compensation in Taiwan in two ways. First, similar to the argument in prior studies, such as Yermack (1995), Dechow et al (1996), Hanlon et al (2004), firms with more dividend

constraints (or liquidity constraints) are expected to employ stock options as a substitute to cash compensation. However, in Taiwan, employees receiving bonus shares are entitled to receive dividends when firms pay dividends. Thus, controlling

owners may be able to extract more rent from minority shareholders if the firm pays dividends.

To differentiate the prediction from the incentive alignment perspective and the rent extraction perspective, we use different measures of dividend payout variables. Following Hanlon et al. (2003), we use a dividend constraint dummy with value equal to one if retained earnings at the end of year t-1 divided by year t-1’s dividends is less than two in any of the previous three years, otherwise the dummy is set equal to zero. This measure captures firms’ dividend constraint or liquidity constraint.

To test the prediction from rent extraction perspective, we use a dividend payout dummy with value equal to 1 if the firm pays dividend to its common stockholders following the issuance of employee bonus shares. This measure captures the controlling owner’s ability to extract more rent from minority shareholders.

Equity Offering

Although stock-based compensation can be used as a self-dealing tool by controlling owners in depriving the minority shareholders, this rent extraction behavior comes at a cost of raising the difficulty of issuing equity in the future. Specifically, potential investors may anticipate the problem and discount the share prices. Thus, we expect that the cost of stock-based compensation is greater for firms engaging in more frequent equity offerings.

Leverage:

Prior studies suggest that leverage could serve as proxies for many different effects, such as the variance of cash flows, financing policies, ownership

3 Empirical Design

3.1 Data

Our sample includes Taiwanese publicly-listed non-financial companies. The corporate ownership structure data, including control rights, cash rights, and stock pyramids, cross-shareholdings etc., are collected from the Taiwan Economics Journal (TEJ) databases. We require the sample firm-years to have sufficient financial data and corporate ownership structure data, including control rights, cash rights, and stock pyramids, cross-shareholdings etc., available in the TEJ databases. Firms in regulated

industries, such as finance, banking, and utilities industries, are excluded from the sample. Our sample consists of 5,090 firm-year observations during 1996-2004.

Table 1 shows the descriptive statistics of our sample firms.

3.2 Empirical Models

Our analysis contains two sets of tests. The first set of the tests examines the determinants of stock-based compensation in Taiwan. The second set of tests then examines whether stock-based compensation is associated with firms’ future

performances.

3.2.1 Regression Analysis on the determinants of stock bonuses

Based on the discussion in Section 2, we first estimate the following models to examine the determinants of stock bonuses grants:

1 5 4 1 3 1 2 1 1 0 it it it i it

it CF VC INTCOV ADR MtoB

SBratio it it it it i it it it it it Shareprice RE LEV ring EquityOffe DivPayout DivConstra WKCP TAX D R 1 14 1 13 1 12 11 1 10 1 9 1 8 1 7 1 6 & int

where:

SBratio = fair value of stock bonuses granted by the firm in a given year divided by the sum of cash bonus and stock bonus.

CF = the ultimate controlling owner’s cash flow right

VC = CV ratio, the ratio of ultimate controlling owner’s voting right over cash flow right.

INTCOV = interest coverage, measured as operating income / interest expense ADR = dummy variable with value equal to one if the firm issues American

Depositary Receipts (ADRs) and zero otherwise

MtoB = Market to book ratio, measured as (Market value of equity + Book value of debt + Book value of preferred stock) / Beginning total assets

R&D = R&D expense / Beginning Total assets

Tax = dummy variable with value equal to one if the firm has a tax loss Carry-forward for the given year and zero otherwise

WKCP = working capital, measured as (Beginning Current Assets – Current Liabilities) / Beginning Total Assets

DivConstraint = dummy variable with value equal to one if retained earnings at the end of year t-1 divided by year t-1’s dividends is less than two in any of the previous three years and zero otherwise.

DivPayout = dummy variable with value equal to 1 if the firm pays dividend to its common stockholders following the issuance of employee bonus shares and zero otherwise.

EquityOffering= number of years in which the firm made equity offerings / number of

available annual observations for the firm

Leverage = Beginning Book Value of Debt / Beginning Total assets SharePrice= Share price

= an error term at year t.

Because the dependent variable cannot be negative and we expect a significant number of observations with the dependent variable equal to zero, the above

regression is estimated using Tobit. Following Matsunaga (1995), we assume a two-stage decision process. A firm first decides whether to grant employee stock bonuses and if they decide to grant stock bonuses, the firm determines the fraction of bonuses being granted in stock form (i.e. stock bonuses). Probit is used to estimate the first stage (the dependent variable is equal to 1 if the firm grants stock bonuses and 0 otherwise) and OLS is used to estimate the second stage (the value of options granted given that the firm grant employee bonuses, i.e. observation with dependent variable equal to 0 are excluded).

The dependent variable, SBratio, is measured as all stock bonus granted by the firm in a given year divided by the sum of cash bonus and stock bonus. The value of stock bonus is calculated by multiplying the number of shares granted by the share price at the year end.

3.2.2 The link between stock-based compensation and firm performance

To examine whether stock based compensation in Taiwan, on average, is used as a tool for incentive alignment or as an entrenchment tool, we estimate the association between stock-based compensation and firm performance. If stock-based

stock-based compensation is positively associated with future firm performance; on the other hand, if it is used as an entrenchment tool in diluting minority shareholders’ interest and thus not consistent with firm value maximization, then we expect a negative/weaker association between stock-based compensation and future firm performance. In this study, we adapt the model that Hanlon, Rajgopal, and Shelvin (2003) use to estimate the association between executive stock options and future earnings and estimate the following model:

1 3 1 2 1 1 0 ( / ) ( / ) ( & / ) ) / (OI S it TA S t STOCKBONUS S t R D S t (FixedEffects)it (2) where:

OI = annual operating income, before R&D expenses S = the annual sales

TA = balance sheet value of total assets

STOCKBONUS = the year-end fair value of employee stock bonus granted R&D = research and development expense

Fixed effects are the industry dummies and the year dummies.

4. Results

In table 2, we report a correlation matrix, which contains Pearson product moment correlation between the regression variables. As expected, the use of stock bonus is positively associated with growth opportunity, cash constraint, and leverage. We also find the use of stock bonus to be negatively correlated with controlling owner’s cash flow right at a p< 0.01 significance level, but not with the controlling owner’s voting right.

We perform Tobit regression to examine the determinants of stock bonus. Table 3 presents Tobit estimates for the model of the ratio of stock bonus over the total bonus pay (i.e. the sum of cash bonus and stock bonus). Based on the full sample, we find that the use of employee stock bonuses is negatively associated with ultimate controlling owners’ cash flow rights, significant at the 1% level. This suggest that when large shareholder’s wealth is more tied to the company, firms shift the mix of bonus pay away from stock bonus to avoid diluting large shareholder’s interest in the firm. The coefficient on the divergence between voting rights and cash flow rights is insignificant. The signs of the estimated coefficients on control variables are generally consisted with our prediction. We find that the use of stock bonus is positively associated with financial reporting costs, cast constraint, growth opportunity, and leverage.

Table 3 also reports the results of two subsamples decomposed by the control concentration: voting rights <30% and voting rights >= 30%. We find that when voting rights are more concentrated (voting rights >= 30%), the coefficient on cash flow rights remain significantly negative and, contrary to the full sample results, the coefficient on the divergence between voting rights and cash flow rights turns significantly positive at the 1% level, suggesting that large shareholder entrenchment is more prevalent. On the other hand, when the voting rights are less than 30%, we do not find the coefficients on cash flow rights or on the divergence measure to be significant.

Over all, the results from Tobit regressions suggest that when control is less concentrated, ownership structure has little impact on the use of stock bonus and the mix of bonus pay tend to be determined by other economic factors, such growth opportunity, tax considerations, cash constraint, and leverage, etc. However, when

control is more concentrated, the mix of compensation is shifted toward cash bonus as controlling owner’s cash flow right increases. Besides, controlling for large shareholder’s cash flow right, firms are more likely to shift the bonus mix toward stock bonus when the agency conflict, captured by the divergence of voting right from cash flow right, is more severe This is consistent with our hypothesis that when control is concentrated, stock bonus becomes a self-dealing tool by the controlling owners in depriving minority shareholders.

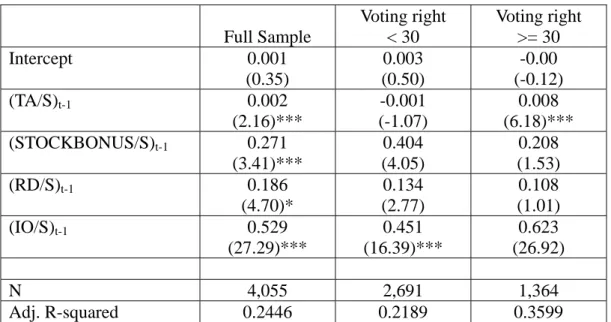

Table 4 reports the results from OLS regressions on the relation between employee stock bonus and future performance. Based on the full sample, we find that the estimated coefficient on stock bonus granted in prior year is significantly positive. This suggests that on average, the use of employee stock bonuses is positively associated with future performance. However, when splitting the sample based on control concentration, we find that only the subsample with voting rights less than 30% exhibits such positive association. For the subsample with voting rights greater than 30%, we do not find employee stock bonuses to be positively associated with future performance.

In sum, the results indicate that the use of stock bonus is more effectively, in terms of maximizing firm value, when control concentration is low, and it becomes a self-dealing tool for large shareholders when control is more concentrated.

5. Additional test on employee stock options

Starting 2001, firms in Taiwan are permitted to grant employee stock options.

Thus, we also attempt to look at employee stock options, in addition to employee

stock bonuses. However, the results on employee stock options are weak. There

stock options is low and thus may reduce the power of our tests. Second, Taiwanese

companies used to grate employee stock bonuses and thus are in the early stage of

granting stock options to employees, so the extent of ESO grants may be influenced

by other factors not included in our model. Third, firms in Taiwan may treat employee

stock option grants as a substitute for employee stock bonuses and the costs of

switching to new systems may outweigh the potential benefits. Overall, future work

for the grants of employee stock options with more years of data may lead to different

empirical results.

6. Conclusion

This study examines the determinants and the performance consequences of

employee stock bonus granted by publicly listed firms in Taiwan, with a feature of

high ownership concentration. Firms intensively using stock-based compensation

often claim that the equity compensation helps to align employees’ and shareholders’

interests and thus is consistent with firm value maximization. The results in this

study suggest that the use of stock-based compensation is consistent with incentive

alignment perspective only when control concentration is low and becomes a

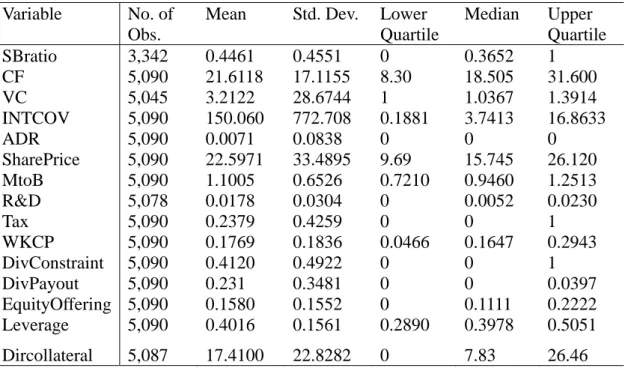

Table 1 Descriptive Statistics and Variable Definitions (N=5,090, 1996-2004)

Variable No. of

Obs.

Mean Std. Dev. Lower

Quartile Median Upper Quartile SBratio 3,342 0.4461 0.4551 0 0.3652 1 CF 5,090 21.6118 17.1155 8.30 18.505 31.600 VC 5,045 3.2122 28.6744 1 1.0367 1.3914 INTCOV 5,090 150.060 772.708 0.1881 3.7413 16.8633 ADR 5,090 0.0071 0.0838 0 0 0 SharePrice 5,090 22.5971 33.4895 9.69 15.745 26.120 MtoB 5,090 1.1005 0.6526 0.7210 0.9460 1.2513 R&D 5,078 0.0178 0.0304 0 0.0052 0.0230 Tax 5,090 0.2379 0.4259 0 0 1 WKCP 5,090 0.1769 0.1836 0.0466 0.1647 0.2943 DivConstraint 5,090 0.4120 0.4922 0 0 1 DivPayout 5,090 0.231 0.3481 0 0 0.0397 EquityOffering 5,090 0.1580 0.1552 0 0.1111 0.2222 Leverage 5,090 0.4016 0.1561 0.2890 0.3978 0.5051 Dircollateral 5,087 17.4100 22.8282 0 7.83 26.46 Variable definitions:

SBratio = fair value of stock bonuses granted by the firm in a given year divided by the sum of cash bonus and stock bonus.

CF = the ultimate controlling owner’s cash flow right

VC = CV ratio, the ratio of ultimate controlling owner’s voting right over cash flow right.

INTCOV = interest coverage, measured as operating income / interest expense ADR = dummy variable with value equal to one if the firm issues American

Depositary Receipts (ADRs) and zero otherwise Shareprice = Share price

MtoB = Market to book ratio, measured as (Market value of equity + Book value of debt + Book value of preferred stock) / Beginning total assets R&D = R&D expense / Beginning Total assets

Tax = dummy variable with value equal to one if the firm has a tax loss Carry-forward for the given year and zero otherwise

WKCP = working capital, measured as (Beginning Current Assets – Current Liabilities) / Beginning Total Assets

DivConstraint = dummy variable with value equal to one if retained earnings at the end of year t-1 divided by year t-1’s dividends is less than two in any of the previous three years and zero otherwise.

DivPayout = dummy variable with value equal to 1 if the firm pays dividend to its common stockholders following the issuance of employee bonus

shares and zero otherwise.

EquityOffering= number of years in which the firm made equity offerings / number of available annual observations for the firm

Leverage = Beginning Book Value of Debt / Beginning Total assets Dircollateral = Director collateral.

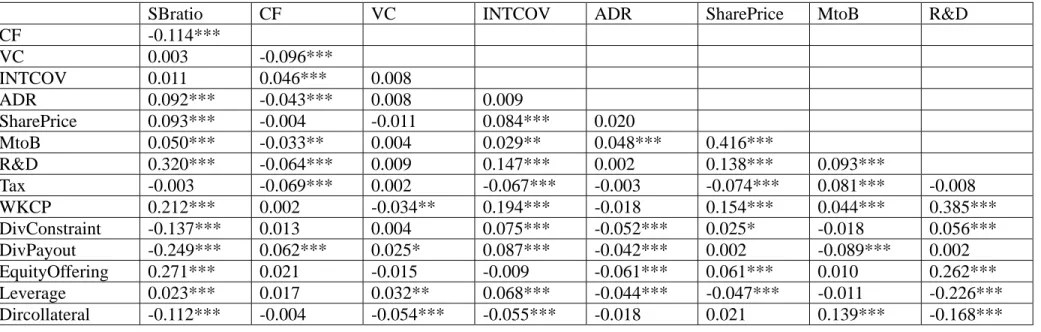

Table 2 Pearson Correlations Matrix (N=5,090, 1996-2004)

SBratio CF VC INTCOV ADR SharePrice MtoB R&D

CF -0.114*** VC 0.003 -0.096*** INTCOV 0.011 0.046*** 0.008 ADR 0.092*** -0.043*** 0.008 0.009 SharePrice 0.093*** -0.004 -0.011 0.084*** 0.020 MtoB 0.050*** -0.033** 0.004 0.029** 0.048*** 0.416*** R&D 0.320*** -0.064*** 0.009 0.147*** 0.002 0.138*** 0.093*** Tax -0.003 -0.069*** 0.002 -0.067*** -0.003 -0.074*** 0.081*** -0.008 WKCP 0.212*** 0.002 -0.034** 0.194*** -0.018 0.154*** 0.044*** 0.385*** DivConstraint -0.137*** 0.013 0.004 0.075*** -0.052*** 0.025* -0.018 0.056*** DivPayout -0.249*** 0.062*** 0.025* 0.087*** -0.042*** 0.002 -0.089*** 0.002 EquityOffering 0.271*** 0.021 -0.015 -0.009 -0.061*** 0.061*** 0.010 0.262*** Leverage 0.023*** 0.017 0.032** 0.068*** -0.044*** -0.047*** -0.011 -0.226*** Dircollateral -0.112*** -0.004 -0.054*** -0.055*** -0.018 0.021 0.139*** -0.168***

Table 2 Pearson Correlations Matrix (continued)

TAX WKCP DivConstraint DivPayout EquityOffering Leverage

WKCP -0.192*** DivConstraint -0.184*** 0.190*** DivPayout -0.211*** 0.177*** 0.404*** EquityOffering 0.011 0.188*** 0.028** -0.047*** Leverage 0.153*** -0.460*** -0.167*** -0.131*** 0.068*** Dircollateral 0.079*** -0.209*** -0.126*** -0.116*** -0.157*** 0.161*** Variable definitions:

SBratio = fair value of stock bonuses granted by the firm in a given year divided by the sum of cash bonus and stock bonus.

CF = the ultimate controlling owner’s cash flow right

VC = CV ratio, the ratio of ultimate controlling owner’s voting right over cash flow right. INTCOV = interest coverage, measured as operating income / interest expense

ADR = dummy variable with value equal to one if the firm issues American Depositary Receipts (ADRs) and zero otherwise

Shareprice = Share price

MtoB = Market to book ratio, measured as (Market value of equity + Book value of debt + Book value of preferred stock) / Beginning

total assets

R&D = R&D expense / Beginning Total assets

Tax = dummy variable with value equal to one if the firm has a tax loss carry-forward for the given year and zero otherwise WKCP = working capital, measured as (Beginning Current Assets – Current Liabilities) / Beginning Total Assets

DivConstraint = dummy variable with value equal to one if retained earnings at the end of year t-1 divided by year t-1’s dividends is less than two in any of the previous three years and zero otherwise.

DivPayout = dummy variable with value equal to 1 if the firm pays dividend to its common stockholders following the issuance of employee bonus shares and zero otherwise.

EquityOffering= number of years in which the firm made equity offerings / number of available annual observations for the firm Leverage = Beginning Book Value of Debt / Beginning Total assets

Table 3 Tobit Regression on the Determinants of Employee Stock Bonus

Dependent variable: SBratio

Full Sample Voting right < 30 Voting right >= 30 Intercept -0.137 (-2.18)*** -0.146 (-2.00)*** -0.194 (-1.53) CF -0.005 (-6.85)*** -0.002 (-1.56) -0.007 (-4.16)*** VC 0.000 (0.12) -0.001 (-1.42) 0.003 (3.08)*** INTCOV -0.000 (-1.06) -0.000 (-0.20) -0.000 (-1.25) ADR 0.613 (4.96)*** 0.588 (4.80)*** 0.838 (1.64) SharePrice 0.001 (1.42) 0.000 (0.86) 0.000 (1.31) MtoB 0.038 (1.55) 0.045 (1.57) 0.044 (0.96) R&D 4.72 (11.32)*** 4.999 (10.16)*** 3.953 (5.10)*** Tax -0.089 (-2.20)*** -0.098 (-2.07)*** -0.033 (-0.44) WKCP 0.802 (8.76)*** 0.638 (5.95)*** 1.052 (6.06)*** DivConstraint -0.084 (-2.95)*** -0.021 (-0.63) -0.190 (-3.52)*** DivPayout -5.036 (-11.47)*** -5.447 (-10.21)*** -3.953 (-5.20)*** EquityOffering 0.980 (11.22)*** 0.714 (7.04)*** 1.456 (8.44)*** Leverage 0.581 (5.63)*** 0.641 (5.20)*** 0.386 (2.05)*** Dircollateral -0.003 (-3.84)*** -0.002 (-1.95)*** -0.006 (-3.96)*** N 3,305 2,100 1,205 Pseudo R-squared 0.1426 0.1274 0.1728

***, ** Indicate significance at 1 percent and 5 percent levels in a two-tailed test respectively.

Table 4 OLS Regression on the Association between Stock Bonus and Firm Performance

Dependent Variable: (OI/S)t

Full Sample Voting right < 30 Voting right >= 30 Intercept 0.001 (0.35) 0.003 (0.50) -0.00 (-0.12) (TA/S)t-1 0.002 (2.16)*** -0.001 (-1.07) 0.008 (6.18)*** (STOCKBONUS/S)t-1 0.271 (3.41)*** 0.404 (4.05) 0.208 (1.53) (RD/S)t-1 0.186 (4.70)* 0.134 (2.77) 0.108 (1.01) (IO/S)t-1 0.529 (27.29)*** 0.451 (16.39)*** 0.623 (26.92) N 4,055 2,691 1,364 Adj. R-squared 0.2446 0.2189 0.3599

***, ** Indicate significance at 1 percent and 5 percent levels in a two-tailed test respectively.

Variable definitions:

OI = annual operating income, before R&D expenses S = the annual sales

TA = balance sheet value of total assets

STOCKBONUS = the year-end fair value of employee stock bonus granted R&D = research and development expense

References

Aboody, D., Kasznik, R. 2000. CEO stock option awards and the timing of corporate voluntary disclosures. Journal of Accounting and Economics 29.: 73-100.

Bizjak, J., Brickley, J., Coles, J.1993. Stock-based incentive compensation and investment behavior. Journal of Accounting and Economics 16: 349-372.

Chen, C.Y., 2003. Investment Opportunities and the Relation Between Equity Value and Employees’ Bonus. Journal of Business, Finance, and Accounting 30: 941-973. Claessens, S., S. Djankov, J. P. H. Fan, and L. H. P. Lang. 2002. Disentangling the incentive and entrenchment effects of large shareholdings. Journal of Finance 57: 2741–71.

, and L. H. P. Lang. 2000. The Separation of Ownership and Control in East Asian Corporations. Journal of Financial Economics 58: 81–112. Core, J., Guay, W., 1999. The use of equity grants to manage optimal equity incentive levels. Journal of Accounting and Economics 28: 151-184.

, J., Holthausen, R., Larcker, D., 1999. Corporate governance, chief executive officer compensation, and firm performance. Journal of Financial Economics 51: 371-406.

Dechow, P., Hutton, A., Sloan, R., 1996. Executive incentives and the horizon problem: an empirical investigation. Journal of Accounting and Economics 14: 51-89. Fan, J. P. H., and T. J. Wong. 2005. Do external auditors perform a corporate governance role in emerging markets? Evidence from East Asia. Journal of

Accounting Research. 43: 35-72.

. 2002. Corporate ownership structure and the informativeness of accounting earnings in East Asia. Journal of Accounting and

Economics 33: 401–26.

Gaver, J., Gaver, K., 1993. Additional evidence on the association between the investment opportunity set and corporate financing, dividend, and compensation policies. Journal of Accounting and Economics16: 125-160.

Hall, B.J., Murphy, K., 2002. Stock options for undiversified executives. Journal of

Accounting andEconomics 1: 3-42.

Hanlon, M., Rajgopal, S., and Shelvin, T., 2003. Are executive stock options associated with future earnings? Journal of Accounting and Economics 36: 3-43. Himmelberg, C., Hubbard, G., Palia, D., 1999. Understanding the determinants of managerial ownership and the link between ownership and performance. Journal of

Financial Economics 53: 353-384.

costs and ownership structure. Journal of Financial Economics 3 : 305–60.

Klasa, S. 2005. Why do controlling families of public firms sell their remaining ownership stake? Journal of Financial and Quantitative Analysis, forthcoming.

Ko, C., K. Ding, C. Liu, and Y. Yeh. 1999. Corporate governance in Chinese Taipei,

Proceeding paper I the conference on “Corporate Governance in Asia: A Comparative Perspective, held .in Seoul, South Korea.

Lambert, R., Larcker, D., 2002. Stock options, restricted stock and incentives. Working Paper, The Wharton School, University of Pennsylvania.

La Porta, R.; F. Lopez-de-Silanes; and A. Shleifer. 1999. Corporate ownership around theworld. Journal of Finance 54: 471–518.

Lins, K. V. 2003. Equity ownership and firm value in emerging markets. Journal of

Financial and Quantitative Analysis. 38: 159-184.

Loderer, C., Martin, K., 1997. Executive stock ownership and performance: tracking faint traces. Journal of Financial Economics 45: 223-255.

Matsunaga, S., 1995. The effects of financial reporting costs on the use of employee stock options. The Accounting Review 70: 1-26.

, T. Shevlin, and D. Shores. 1992. Disqualifying dispositions of incentive stock options: Tax benefits versus financial reporting costs. Journal of

Accounting Research 30: 37-68.

Morck, R., A. Shleifer R., and R. Vishny. 1988. Management ownership and market valuation: an empirical analysis. Journal of Financial Economics 20: 293–315.

Rajgopal, S., Shevlin, T., 2002. Empirical evidence on the relation between stock option compensation and risk taking. Journal of Accounting and Economics 2 : 145-171.

Shivdasani, A., Yermack, D., 1999. CEO involvement in the selection of new board members: an empirical analysis. Journal of Finance 54: 1829-1853.

Shleifer, A., and R. Vishny. 1997. A survey of corporate governance. Journal of

Finance 52: 737–83.

Smith, C., Watts, R., 1992. The investment opportunity set and corporate financing, dividend, and compensation policies. Journal of Financial Economics 7: 117-161. Yeh, Y. H., T. S. Lee, and T. Woidtke. 2001. Family control and corporate governance: Evidence form Taiwan. International Review of Finance 2: 21-48.

Yermack, D., 1997. Good timing: CEO stock option awards and company news announcements. Journal of Finance 52: 449-477.

Yermack, D., 1995. Do corporations award CEO stock options effectively? Journal of

行政院國家科學委員會補助國內專家學者出席國際學術會議報告 97 年 8 月 31 日 報告人姓名 梁嘉紋 服務機構 及職稱 國立政治大學助理教授 會議時間 8/3-8/6, 2008

會議地點 Anaheim, CA, USA

會議名稱 (中文)美國會計學會 2008 年年會

(英文)American Accounting Association 2008 Annual Meeting 發表論文標

題

(中文) 研發與高階主管獎酬

(英文) R&D Activities and CEO Compensation 報告內容含下列各項:

一、參加會議經過 8/3 Registration

Early Bird Reception

8/4 8:30-9:45 AM Opening Plenary Session 10:15-11:45 AM Concurrent Sessions 12:00-1:45 PM Section Luncheons 2:00-3:30 PM Concurrent Sessions 4:00-5:30 PM Concurrent Sessions 6:30-8:30 PM Welcome Reception 8/5 8:30-9:45 AM Plenary Session 10:15-11:45 AM Concurrent Sessions 12:00-1:45 PM Luncheon

2:00-3:30 PM Concurrent Sessions (presenting paper) 4:00-5:30 PM Concurrent Sessions 6:30-8:30 PM Reception 8/6 8:30-9:45 AM Plenary Session 10:15-11:45 AM Concurrent Sessions 12:00-1:45 PM Luncheons 2:00-3:30 PM Concurrent Sessions 4:00-5:30 PM Concurrent Sessions 6:30-8:30 PM Reception 二、與會心得 此次在美國會計學會 2008 年年會中發表論文,獲得 Discussant 及其

他學者許多具建設性的專業建議。 Discussant 為 University of California at Irvine 的教授 Cristo Karuna。 Professor Karuna 對發表之論文提出之評 論及建議彙整如下:

‧ Improve motivation; add more tests and provide more results to increase incremental contribution

‧ Develop multidimensional nature of R&D reasoning

‧ Can you show that stock price undervalues R&D capital? Discuss link between valuation and stewardship roles of performance measures

‧ Include main effect for RDC, LONG, and SHORT in regression equations

‧ Include important control variables in regressions ‧ Use change in ROA as accounting return variable

‧ Combine equations 2 and 3 – have one indicator variable for R&D payoff; assign values based on years, not industries

‧ Elaborate on “additional tests” to rule out “Horizon problem” – isn’t your reasoning based on R&D horizon?

Professor Karuna 對研究方法及論文寫作的建議將有助於提高本文的品 質,獲益良多。 除了論文的發表之外,在參與其他的 concurrent sessions 中也獲得很 多寶貴的資訊,藉由其他學者的論文發表可知道目前的研究趨勢及研究者 所關心的研究議題,有助於未來的研究工作。 在會議之外,也有機會與國際學者的互動交流,對後續的研究極有幫 助。 三、考察參觀活動(無是項活動者省略) 無。 四、建議 希望可以多提供國內學者參與類似國際學術會議的機會,以幫助國內的研 究者獲得最新的研究資訊並增加與國外的學者互相交流的機會。 五、攜回資料名稱及內容 1. 大會議程

六、其他 無。