行政院國家科學委員會專題研究計畫 成果報告

強制性合夥人輪調制度對盈餘品質影響的實證研究

計畫類別: 個別型計畫 計畫編號: NSC93-2416-H-004-036- 執行期間: 93 年 08 月 01 日至 94 年 07 月 31 日 執行單位: 國立政治大學會計學系 計畫主持人: 戚務君 報告類型: 精簡報告 報告附件: 出席國際會議研究心得報告及發表論文 處理方式: 本計畫可公開查詢中 華 民 國 94 年 10 月 4 日

Mandatory Audit-Partner Rotation, Audit Quality and Market Perception: Evidence from Taiwan

Wuchun Chi Department of Accounting National Chengchi University

Taipei, Taiwan Huichi Huang Department of Accounting National Taiwan University

Taipei, Taiwan Yichun Liao Department of Accounting National Taiwan University

Taipei, Taiwan Hong Xie*

Department of Accountancy University of Illinois at Urbana-Champaign

Champaign, IL 61820

September 2005

*Corresponding author. Department of Accountancy, University of Illinois at Urbana-Champaign, 1206 South Sixth Street, Champaign, IL, USA. Email: [email protected]. Phone: (217) 244-4608. Fax: (217) 244-0902. We thank Chan-Jane Lin, James Myers, Ira Solomon, Theodore Sougiannis and workshop participants at National Chengchi University and National Taipei University for help, comments and suggestions. Professor Chi gratefully acknowledges the financial support from National Science Council (Project No. NSC 93-2416-H-004-036).

Mandatory Audit-Partner Rotation, Audit Quality and Market Perception: Evidence from Taiwan

Abstract:

We examine the effectiveness of mandatory audit-partner rotation in promoting audit quality using audit data in Taiwan where a five-year audit-partner rotation became de facto mandatory in 2004. Using both absolute and signed performance-matched abnormal accruals and other accrual-based measures as proxies for audit quality, we find that audit quality of companies subject to mandatory audit-partner rotation in 2004 is largely indistinguishable from audit quality of companies not subject to mandatory rotation in 2004 and companies whose audit partners were voluntarily rotated before 2003. Moreover, audit quality of companies subject to mandatory rotation in 2004 under new audit partners is lower than audit quality of these same companies in 2003 under old audit partners. Our early evidence, therefore, is inconsistent with the notion that

mandatory audit-partner rotation enhances audit quality, as measured by auditors’ constraining management’s extreme income-increasing or extreme income-decreasing accruals. In contrast, using the earnings response coefficient as a proxy for investor perceptions of audit quality, we consistently find that investors perceive mandatory audit-partner rotation as enhancing audit quality, suggesting that mandatory audit-audit-partner rotation enhances auditor independence in appearance.

Keywords Mandatory audit-partner rotation; Auditor tenure; Audit quality; Perceptions

Mandatory Audit-Partner Rotation, Audit Quality and Market Perception: Evidence from Taiwan

1. Introduction

Recent high profile failures in corporate financial reporting, such as the collapses of Enron and WorldCom, have eroded the public’s confidence in audited financial statements and rekindled a national debate on auditor independence and audit quality. During the debate, mandatory audit-firm rotation and mandatory audit-partner rotation, which set a limit on the period of years an audit firm and audit partner, respectively, may audit a particular company’s financial statements, are often proposed as a means to enhance auditor independence and audit quality. These proposals are based on an implicit assumption that extended audit-firm or audit-partner tenure can impair auditor

independence and thus setting a limit on audit-firm or audit-partner tenure would improve audit quality. Reflecting such an assumption, the Sarbanes-Oxley Act of 2002 (hereafter, the SOX Act) mandates a five-year rotation for the lead and concurring audit partners.1

Mandatory audit-partner rotation has existed in the U.S. for some time. American Institute of Certified Public Accountants (AICPA) has long required that audit partners in charge of SEC audit engagements be rotated at least once every seven years. The SOX Act further strengthens this requirement by reducing the rotation period from seven to five years with the intent to enhance auditor independence and audit quality. Despite the practice of mandatory partner rotation in the U.S., the efficacy of mandatory

1 Mandatory audit-firm rotation was also considered during the congressional hearings before the SOX Act,

but was not included in the act. Congress decided that mandatory audit-firm rotation needed further study and required the GAO to study the potential effects of mandatory audit-firm rotation within one year of the passage of the SOX Act. The ensuing GAO (2003) report concludes that “the potential benefits of

mandatory audit firm rotation are harder to predict and quantify, though we are fairly certain that there will be additional costs” (p. 8) and that “the most prudent course at this time is for the SEC and the PCAOB to monitor and evaluate the effectiveness of the act’s requirements to determine whether further revisions,

partner rotation in promoting audit quality has not been systematically investigated. One roadblock has been that U.S. audit reports contain the names of audit firms, but not audit partners, i.e., information about audit-partner tenure and audit-partner rotation is not publicly available in the U.S. Consequently, researchers using U.S. audit data are unable to directly examine the effect of mandatory audit-partner rotation on audit quality.

Unlike the U.S., audit reports in Taiwan contain both firm names and audit-partner names. Exploiting this institutional feature in Taiwan, Chen, Lin and Lin (2005) examine the relation between audit-partner tenure and earnings quality. They find a negative relation between absolute abnormal accruals and audit-partner tenure, consistent with findings in the U.S. based on audit-firm tenure. However, their sample period is between 1990 and 2001 when audit-partner rotation in Taiwan was voluntary. Since the incentives and behavior of audit partners may change significantly under a mandatory rotation regime, whether their findings under the voluntary audit-partner rotation regime can be generalized to the current mandatory rotation regime is an empirical question. In short, the extant literature has not investigated the effect of mandatory audit-partner rotation on audit quality and has not tested the validity of an implicit assumption in the SOX Act that mandatory audit-partner rotation enhances audit quality.

In this paper, we investigate the effectiveness of mandatory audit-partner rotation in promoting audit quality using Taiwanese data. Inspired by the SOX Act in the U.S., two main stock exchanges in Taiwan, Taiwan Stock Exchange Corporation (TSEC) and Gretai Securities Market (GTSM), adopted a set of rules in April 2003 that, in effect, require a five-year mandatory audit-partner rotation for all listed companies in Taiwan.2 These rules became fully effective in 2004 for both semi-annual and annual reports with

2003 as a transition period (more details below). We use the 2004 semi-annual reports of listed Taiwanese companies in the Taiwan Economic Journal (TEJ) database for this study. Semi-annual reports in Taiwan are audited just like annual reports and the 2004 semi-annual reports are the first set of data that reflect the full force of the mandatory audit-partner rotation requirement in Taiwan as of the time of this study.

Following prior studies (e.g., Myers, Myers Omer 2003), we use both absolute and signed performance-matched abnormal accruals (Kothari, Leone and Wasley 2005) as proxies for audit quality and examine the effect of mandatory audit-partner rotation on audit quality. We identify a sample of companies whose audit-partners were rotated in 2004 within the same audit firm due to the mandatory audit-partner rotation requirement (the mandatory rotation sample). We compare our mandatory rotation sample with three benchmark samples to examine the effect of mandatory audit-partner rotation on audit quality. First, we compare the mandatory rotation sample with companies in 2004 whose audit-partners were not required to rotate (the non-rotation sample). We find that audit quality of the mandatory rotation sample is indistinguishable from that of the non-rotation sample after controlling for company age, size, industry growth, cash flows, auditor type (Big 4 versus non-Big 4) and audit-firm tenure. Second, we compare the mandatory rotation sample with itself one year ago in 2003 (the mandatory rotation sample in prior year). We find that audit quality of companies in the mandatory rotation sample under new audit partners is lower than audit quality of these same companies one year ago under old audit partners. Third, we compare our mandatory rotation sample with companies in years before 2003 whose audit-partners were voluntarily rotated within the same audit firm (the voluntary rotation sample). We again find that audit quality of the

mandatory rotation sample is indistinguishable from audit quality of the voluntary rotation sample.Our findings are robust to various sensitivity checks.

In addition, we use the earnings response coefficient (ERC), a market-based proxy for investor perceptions of audit quality (e.g., Ghosh and Moon 2005), to examine the effect of mandatory audit-partner rotation on investor perceptions of audit quality. After controlling for company age, auditor type, growth, earnings persistence, earnings volatility, systematic risk, size, financial leverage and audit-firm tenure, we find that ERC is larger for the mandatory rotation sample relative to each of our three benchmark samples: (1) the non-rotation sample, (2) the mandatory rotation sample in prior year, and (3) the voluntary rotation sample. Thus, we obtain consistent evidence suggesting that investors perceive mandatory audit-partner rotation as enhancing audit quality.

Accrual-based and market-based proxies for audit quality capture different aspects of audit quality. As explained in more details below, accrual-based proxies (e.g., abnormal accruals) gauge the extent to which auditors constrain management’s extreme income-increasing or extreme income-decreasing accruals and thus capture audit quality stemming from auditor competence and/or auditor dependence in fact.3 On the other hand, market-based proxies (e.g., ERC) reflect investor perceptions of audit quality and as such capture audit quality stemming from auditor independence in appearance (e.g., Ghosh, Kallapur and Moon 2005).

This paper contributes to the literature on auditor tenure and audit quality in two ways. First, to our knowledge, our paper is the first to directly examine the effectiveness of mandatory audit-partner rotation on audit quality. Prior studies find that audit quality is

3 DeAngelo (1981) defines audit quality as the joint probability that an auditor will both (a) discover a

breach (i.e., auditor competence) and (b) report the breach (i.e., auditor independence). Auditor independence can be further decomposed into auditor independence in fact and in appearance.

positively associated with audit-firm tenure or audit-partner tenure under the voluntary audit-firm or audit-partner rotation regime, but these findings do not speak directly to the effectiveness of mandatory audit-partner rotation in promoting audit quality.

Second, we shed light on the cost and benefit of mandatory audit-partner rotation. The fact that audit quality of our mandatory rotation sample (with short audit-partner tenure) is not lower than audit quality of the non-rotation sample (with medium audit-partner tenure) suggests that there is some benefit from a “fresh look” from new audit partners under the mandatory audit-partner rotation regime because Chen et al. (2005) would have predicted lower audit quality under the voluntary rotation regime for our mandatory rotation sample due to its shorter audit-partner tenure. We conjecture that this benefit comes from enhanced auditor independence in fact. This benefit, however, is offset by new audit partners’ relative lack of client-specific knowledge and experience (i.e., reduced auditor competence) due to their relatively shorter audit-partner tenure compared to audit partners in the non-rotation sample. Moreover, our analyses based on ERC suggest that mandatory audit-partner rotation also enhances investor perceptions of audit quality, i.e., auditor independence in appearance.

On the other hand, we find that audit quality of companies in the mandatory rotation sample under new audit partners (with short audit-partner tenure) is lower than audit quality of these same companies one year ago under old audit partners (with long audit-partner tenure). This suggests that the enhanced auditor independence in fact from mandatory rotation is not enough to compensate for new audit partners’ extreme lack of client-specific knowledge and experience compared to old audit partners (much reduced auditor competence).

To summarize, our findings suggest that the benefit of mandatory audit-partner rotation is enhanced auditor independence both in fact and in appearance but the cost is reduced auditor competence due to new audit partners’ lack of client-specific knowledge and experience, which can offset or even overweigh the benefit of enhanced auditor independence in fact.

Our findings based on Taiwanese data have implications for the U.S. audit market. Specifically, our paper seems to imply that the effectiveness of the mandatory audit-partner rotation clause in the SOX Act in promoting audit quality, as measured by auditors’ constraining management’s extreme increasing or extreme income-decreasing accruals, may be limited due to reduced auditor competence offsetting

enhanced auditor independence in fact. This echoes the concern in Francis (2004, p. 359) that the SOX Act was hastily passed without serious academic inputs. On the other hand, our findings also suggest that mandatory audit-partner rotation enhances investor

perceptions of audit quality, i.e., auditor independence in appearance. Since perceptions are very important for audit services due to difficulty in directly observing audit quality, our paper seems to imply that the mandatory audit-partner rotation clause in the SOX Act is of value in restoring investors’ confidence by enhancing auditor independence in appearance.

Our findings, however, must be interpreted with caution because they are based on the first set of semi-annual reports after the mandatory rotation rule in Taiwan. The effect of mandatory audit-partner rotation on audit quality may take some time to realize. In addition, our findings only have implications for but may not be generalizable to the

U.S. audit market due to institutional differences between Taiwan and the U.S. We discuss strengths and limitations of our study in the conclusion section.

The remainder of the paper is organized as follows. Section 2 describes Taiwanese regulation of mandatory audit-partner rotation and develops hypotheses. Section 3 describes data and sample selection. We present our empirical models and findings in Section 4 and conclude in Section 5.

2. Taiwanese Regulation and Hypothesis Development 2.1. Mandatory Audit-Partner Rotation in Taiwan

Unlike the U.S. where audit reports of public companies only show audit-firm names, audit reports in Taiwan show both audit-firm names and names of two signing audit partners.4 Again unlike the U.S. where audit-partner rotation every seven years has been required by AICPA for some time and audit-partner rotation every five years is mandated in the SOX Act, audit-partner rotation in Taiwan has been entirely voluntary until 2003.

In April 2003, after the passage of the SOX Act in the U.S., Taiwan Stock Exchange Corporation (TSEC) and Gretai Securities Market (GTSM), two main stock exchanges in Taiwan, promulgated two rules that, in effect, require a five-year mandatory audit-partner rotation. First, both stock exchanges amended their procedures for auditing the financial statements of listed companies and added a clause stating that if the lead or

4 Annual and semi-annual financial statements of listed companies in Taiwan must be audited. Before 1983,

annual financial statements must be certified by one audit partner with the audit report showing the name of that audit partner and the name of the audit firm. Beginning in 1983, annual reports in Taiwan must be certified by two audit partners with the audit report showing the names of two audit partners and the name of the audit firm. Starting 1988, the Securities and Exchange Act (Amended) requires that semi-annual

concurring audit partner has performed audit services for a listed company in the recent five years then that company’s financial statements are subject to the stock exchange’s “substantive review” procedure.5 Substantive review is a procedure instituted by both exchanges to protect investors’ interests. Specifically, the stock exchange would routinely review financial statements of listed companies and conduct checks on their business and stock transactions. If the stock exchange finds significant irregularities, it will take appropriate actions (see below). Second, the original texts of the new clause stipulate that the five-year rule for both lead and concurring audit partners becomes effective

immediately after the promulgation. However, there was a large percentage of audit firms with two audit partners auditing the same client in the previous four or more years in Taiwan as of 2003. Taiwan Accountants Union argued that it would be difficult for audit firms, especially small audit firms, to rotate two audit partners in the same year. In response to this and other concerns, both stock exchanges changed the effective time for full implementation of the five-year rotation rule for both audit partners to 2004 with 2003 as a transition period when audit firms are allowed to have one audit partner, but not both, auditing the same client for five or more years up to the end of 2003.

After a stock exchange determines that a company’s financial statements are subject to substantive review, it will request and review audit working papers from the audit partners. If the exchange finds any violations of auditing standards or accounting standards, it will refer the case to relevant government agencies for administrative or

5 Note that the five-year rule in Taiwan disallows both audit partners to audit a client’s financial statements

for a consecutive five years including the current year, which differs from the five-year rule in the U.S. that allows an audit partner to audit a client’s financial statements for a consecutive five years including the current year. See Section 4-2-2-4 of Taiwan Stock Exchange Corporation Procedures for Auditing the Financial Report of Listed Companies and Section 4-2-2-5 of Gretai Securities Market Procedures for Auditing the Financial Report of Listed Companies.

punitive actions according to Certified Accountant Law, Securities and Exchanges Law and related regulations. According to these relevant laws and regulations in Taiwan, appropriate punishments range from reprimand to suspension of license or even criminal charges. Since the potential punishments are severe, these two stock exchanges’ recent rules to subject a company’s financial statements to substantive review when audited by the same lead or concurring audit partner in the recent five years, in effect, mandate a five-year audit-partner rotation for both lead and concurring audit partners.

2.2. Literature Review and Hypothesis Development

The separation of ownership and control in public companies creates conflict of interests between management and outside stakeholders. Given the conflict of interests and asymmetric information, financial statements prepared by management are audited by a third party (an auditor) to mitigate agency costs between management and

stakeholders (Dopuch and Simunic 1982; Watts and Zimmerman 1986). The value of an audit, however, depends on audit quality, which, in turn, depends on auditor competence and independence (DeAngelo 1981). Auditor competence and auditor independence, both in fact and in appearance, therefore, are critically important for the value or perceived value of audit services.

Recent high profile failures in corporate financial reporting has brought to the fore the issue of auditor independence and audit quality. A recurring debate is whether

extended firm tenure impairs auditor independence and whether mandatory audit-firm rotation enhances audit quality. The arguments for and against mandatory audit-audit-firm rotation center on the costs and benefits associated with mandatory rotation. The costs of mandatory audit-firm rotation include (1) direct increases in costs incurred by both audit

firms and auditee companies and (2) increased likelihood of audit failures due to new auditors’ lack of client-specific knowledge of risk, operations and financial reporting practices in initial years. The benefits of mandatory audit-firm rotation include (1) a “fresh look” by the new audit firm and (2) increased auditor independence in fact and/or in appearance. Proponents of mandatory audit-firm rotation argue that the benefits overweigh the costs while opponents contend otherwise.

Prior studies typically use absolute and signed abnormal accruals estimated using the Jones (1991) model as proxies for audit quality. A main justification for using

accrual-based measures as proxies for audit quality is that abnormal accruals have become an accepted proxy for earnings management and earnings quality in the accounting literature (e.g., Jones 1991; Healy and Wahlen 1999; Dechow and Dichev 2002) and that audited financial statements should be viewed as a joint outcome from the audit firm and company management (Antle and Nalebuff 1991). Since abnormal

accruals measure earnings management and thus gauge the extent to which auditors constrain management’s extreme income-increasing or extreme income-decreasing accruals, they capture auditor competence and/or auditor independence in fact. Using accrual-based proxies for audit quality, recent studies have examined the relation between audit-firm tenure and audit quality. For example, Johnson et al. (2002) document that short audit-firm tenure of two to three years are associated with lower-quality financial reporting, as measured by absolute abnormal accruals and accrual persistence, relative to medium (four to eight years) or long (nine or more years) audit-firm tenure. Similarly, Myers et al. (2003) find a positive relation between audit quality and audit-firm tenure. These findings are inconsistent with the claim that audit quality deteriorates with

prolonged audit-firm tenure under the current voluntary audit-firm rotation regime in the U.S.

Recent studies also use market-based measures, such as the cost of debt and ERC, as proxies for investor perceptions of audit quality. For example, Mansi, Maxwell and Miller (2004) find a significantly negative relation between the cost of debt and audit-firm tenure, suggesting that audit-audit-firm tenure enhances, rather than impairs, audit quality. On the other hand, Ghosh and Moon (2005) use ERC estimated from concurrent returns-earnings regressions as a proxy for investor perceptions of audit quality, i.e., auditor independence in appearance (see also Ghosh et al. 2005), and document a positive association between investor perceptions of audit quality and audit-firm tenure. Findings using market-based proxies for perceived audit quality, therefore, are consistent with findings using accounting-based proxies for audit quality.

To summarize, recent calls for mandatory audit-firm rotation have stimulated a national debate on pros and cons of mandating audit-firm rotation and spawned an emerging literature on auditor tenure and audit quality. Overall, evidence from academic research does not support the claim that extended audit-firm tenure impairs audit quality or perceptions of audit quality under the current voluntary audit-firm rotation regime in the U.S.

In sharp contrast to the debate on mandatory firm rotation, mandatory audit-partner rotation has already existed in the U.S. for some time although the pros and cons of mandatory audit-firm rotation are applicable to mandatory audit-partner rotation to a large extent. AICPA requires audit-partner rotation every seven years. The IFAC Report (2003, p. 33) recommends that the lead and reviewing audit partners be compulsorily

rotated after a period not exceeding seven years. Most significantly, Section 203 of the SOX Act mandates a five-year rotation for the lead as well as reviewing audit partners. Implicitly in the AICPA professional requirement, the IFAC recommendation and the SOX Act is an assumption that mandatory audit-partner rotation enhances audit quality. However, the validity of such an assumption is not tested in the accounting literature due to the lack of audit-partner information in U.S. public databases.

The purpose of this study is to investigate the effect of mandatory audit-partner rotation on audit quality and investor perceptions of audit quality using audit data in Taiwan where a five-year rotation became de facto mandatory in 2004. Following prior studies, we use absolute and signed accrual measures as a proxy for audit quality (Johnson et al. 2002; Myers et al. 2003) and ERC as a proxy for investor perceptions of audit quality (Teoh and Wong 1993; Ghosh and Moon 2005). We formulate the following two hypotheses (stated in alternative form) based on the implicit assumption in the SOX Act:

HYPOTHESIS 1. Audit quality of companies whose audit-partners are mandatorily

rotated is higher than audit quality of companies whose audit-partners are not required to rotate.

HYPOTHESIS 2. Investor perceptions of audit quality of companies whose

audit-partners are mandatorily rotated are higher than investor perceptions of audit quality of companies whose audit-partners are not required to rotate.

Data for this study are collected from the 2004 semi-annual TEJ database for companies listed on TSEC or GTSM. We identify a sample of companies whose audit-partners (at least one of them) were required to rotate within the same audit firm in 2004 (MROTA sample) and another sample of companies whose audit-partners (both of them) were not required to rotate in 2004 (NROTA sample) using the following procedure. First, we identify 1,022 companies in 2002 from the TEJ database after excluding all Taiwan Depository Receipts (TDR) because semi-annual financial statements of TDRs are only reviewed rather than audited. We delete 21 companies with missing audit-partner information and 3 companies with a non-calendar fiscal year end. We thus obtain a preliminary sample of 998 companies in 2002. Second, we trace audit partners of these 998 companies in past years up to 2002, and find 832 companies with at least one audit partner who had performed audit services for the same client for at least four consecutive years as of 2002 and 166 companies with both audit partners who had performed audit services for the same client for less than four consecutive years as of 2002. We classify the 832 companies identified above into our mandatory rotation sample (MROTA) since at least one of their audit partners needs to be rotated for the 2004 semi-annual audits and the 166 companies into non-mandatory rotation sample (NROTA) since none of their audit partners has to be rotated for the 2004 semi-annual audits.

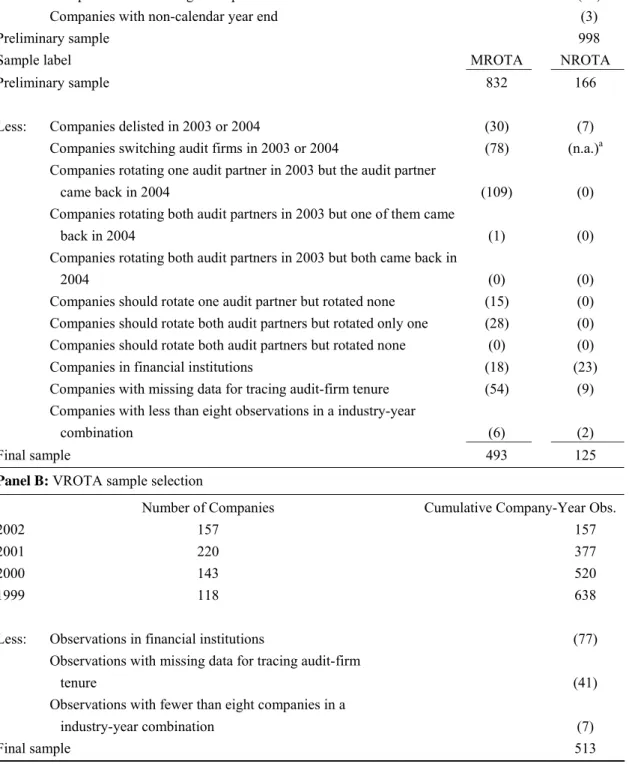

Third, we trace audit partners of companies in our MROTA sample and NROTA sample to years 2003-2004 to determine whether audit partners are rotated in 2004. We lose additional companies for the following reasons in MROTA sample (NROTA sample): (i) 30 (7) companies due to delisting; (ii) 78 (n.a.) companies due to their

changing audit firms during 2003-2004;6 (iii) 109 (0) companies because one of their audit partners was rotated off in 2003 but came back in 2004; (iv) 1 (0) company because both audit partners were rotated off in 2003 but at least one came back in 2004;7 (v) 15 (0) companies for which one audit partner should be rotated in 2004 but was not rotated; (vi) 28 (0) companies for which both audit partners should be rotated in 2004 but only one audit partner was rotated; (vii) 18 (23) companies in financial industries whose accruals are difficult to interpret; (viii) 54 (9) companies with missing data for tracing audit-firm tenure; and (ix) 6 (2) companies for which there are less than eight observations in the same industry classification in a year since we require at least eight observations to estimate abnormal accruals for each industry-year combination using the modified Jones (1991) model. The above process generates 493 (125) companies in our MROTA sample and NROTA sample, respectively. Table 1, panel A, summarizes the sample selection process.

[Insert Table 1 here]

In testing our hypotheses, we compare our mandatory rotation sample (MROTA) with three benchmark samples. The first benchmark is the non-rotation sample (NROTA) described above. Our purpose is to examine whether audit quality of the mandatory rotation sample is higher than audit quality of the non-rotation sample. The second benchmark is the mandatory rotation sample itself in prior year (MBEFR sample). Our

6 When companies switch audit firms, their audit partners are automatically changed. These audit-partner

changes are excluded from MROTA sample but are not excluded from NROTA sample because they are not due to the mandatory rotation rule.

7 The rotation requirement in Taiwan only forbids audit partners from providing audit services for the client

for five consecutive years with no other clear guidance such as the cooling off period. This ambiguity provides some companies with an opportunity to circumvent the requirement by rotating audit partners with at least four consecutive years of audit services as of 2002 off in 2003 and then rotate them back in 2004. We exclude these companies in our mandatory rotation sample because audit partners who came back in 2004 cannot be considered as new audit partners for their clients as they were rotated off only for one year in 2003.

purpose is to examine whether audit quality of companies in the mandatory rotation sample under new audit partners is higher than audit quality of these same companies one year ago under old audit partners. The third benchmark consists of companies in years before 2003 whose audit-partners (at least one of them) were voluntarily rotated within the same audit firm (VROTA sample). Our purpose is to examine whether audit quality of the mandatory rotation sample is higher than audit quality of the voluntary rotation sample.

The sample selection process for our VROTA sample is summarized in panel B, Table 1. Specifically, we identify companies in 2002 and earlier years for which at least one of audit partners was voluntarily rotated. We do not include audit partner rotation in 2003 because it is not clear whether the rotation was entirely voluntary given that 2003 is the transition year for mandatory audit-partner rotation. We only need to go back to 1999 because we already identify a total of 638 company-year observations, larger than 493 companies in our MROTA sample, during 1999-2002 who voluntarily rotated at least one of their audit partners. We delete 77 observations in financial institutions, 41 observations due to missing data for tracing audit-firm tenure, and seven observations due to less than eight companies in their industry classifications in a year. The final VROTA sample consists of 513 company-year observations, which is comparable in size to MROTA sample.

In sum, our mandatory audit-partner rotation sample consists of 493 companies in 2004 whose audit partners (at least one of them) were mandatorily rotated (MROTA). We construct three benchmark samples to compare with the mandatory rotation sample: (1) companies in 2004 whose audit partners (both of them) were not required to rotate

(NROTA); (2) the same companies in MROTA sample in 2003 under old audit partners (MBEFR); and (3) companies whose audit partners (at least one of them) were

voluntarily rotated during 1999-2002 (VROTA).

4. Empirical Models and Findings

In this section, we examine the effect of mandatory audit-partner rotation on audit quality and investor perceptions of audit quality. We first present the empirical model and findings using accrual-based proxies for audit quality. We then present the empirical model and findings using the market-based proxy for investor perceptions of audit quality. 4.1. Accrual-Based Proxies for Audit Quality

4.1.1. Variable Measurement and Empirical Model

Johnson et al. (2002) and Myers et al. (2003) use the Jones (1991) model-estimated abnormal accruals as proxies for financial reporting quality and audit quality. However, the Jones model and modified Jones model are mis-specified for firms with extreme financial performance (Dechow, Sloan and Sweeney 1995). Kothari et al. (2005) demonstrate that performance-matched abnormal accruals capture earnings management better than do traditional Jones model-estimated abnormal accruals. We, therefore, use performance-matched abnormal accruals (PMABNACt) as our primary measure of audit quality. We also use several other accrual-based measures of audit quality in sensitivity tests.

Following Kothari et al. (2005), we calculate performance-matched abnormal accruals in a two-stage process. In the first stage, we estimate raw abnormal accruals

(ABNACt) as the residuals from the cross-sectional modified Jones (1991) model below (company subscript is omitted for ease of exposition):

t t t t t t t t t t t t ε TA PPE γ TA AR SALES β TA α TA TAC + + Δ − + = − − − −1 1 1 1 Δ 1 (1) where:

TACt = total accruals in the first half of year t, calculated using the statement of cash flow approach recommended by Hribar and Collins (2002), = income before discontinued operations and extraordinary items – (cash from operations – discontinued operations and extraordinary items from the statement of cash flows);

ΔSALESt = change in sales revenue between the first half of year t and the first half of year t-1;

ΔARt = change in accounts receivable between the first half of year t and the first half of year t-1;

PPEt = gross amount of property, plant and equipment at the end of the first half of year t; and

TAt-1 = total assets at the end of year t-1 (i.e., total assets at the beginning of the first half of year t).

We estimate equation (1) in the cross section in each year (from 1999 to 2004) for each industry classification with at least eight observations using all companies with required data in the TEJ database.8 The residuals from equation (1) are our measures of raw abnormal accruals (ABNACt).

In the second stage, we do performance matching based on current period return on assets (ROAt). Specifically, for each company i (i = 1, 2, ..., N and N >= 8) in an industry-year combination in year t, we find another company j, where j ≠ i, among the remaining companies (N – 1) in the same industry-year combination whose return on assets in year t (ROAjt) is closest to return on assets of company i (ROAit). Our performance-matched abnormal accruals (PMABNACt) for firm i in year t are the

differences in raw abnormal accruals between firm i and firm j, i.e., PMABNACt = ABNACit – ABNACjt.

After obtaining performance-matched abnormal accruals through the above two-stage procedure for all companies with required data in TEJ database during 1999-2004, we keep only company-year observations in our mandatory rotation sample (MTOTA) and three benchmark samples (NROTA, MBEFR and VROTA).

We examine the effectiveness of mandatory audit-partner rotation in promoting audit quality using the regression model below following Myers et al. (2003):

+ + + + + +

=α βBMK Age β Size β IndGrw CFO

Acc 1

β

2 3 4β

5ε β

β6Big4+ Tenure7 + (2)

where:

Acc = performance-matched abnormal accruals (PMABNACt), measured in absolute, positive and negative values;

BMK = a dummy variable equal to 1 if observations are from one of the three benchmark samples: NROTA, MBEFR or VROTA, and equal to 0 otherwise;

Age = number of years since the company was listed;

Size = natural logarithm of total assets at the end of the first half of year t; IndGrw = industry growth =

∑

∑

= − = N i t i N i t i SALES SALES 1 1 , 1

, / by the TEJ industry

classification, and t and t-1 refer to the first half of years t and t-1, respectively;

CFO = cash from operations from the statement of cash flows for the first half of year t, scaled by total assets at the end of the first half of year t-1;

Big4 = a dummy variable equal to 1 if the auditor is from a Big 4 or Big 5 audit firm, and equal to 0 otherwise;9

Tenure = Audit-firm tenure traced back to 1988 when semi-annual financial statements are required to be certified by two audit partners.

We estimate equation (2) in each of the three comparison samples: MROTA vs. NROTA, MROTA vs. MBEFR and MROTA vs. VROTA. Following Myers et al. (2003), we first estimate equation (2) over the entire comparison sample using the ordinary least

9 The earliest year in our samples is 1999 (VROTA). There were still five big audit firms before 2003. We

squares (OLS) method when the absolute value of accruals (|PMABNAC|) is the dependent variable. We then estimate equation (2) over truncated sub-samples, PMABNAC >= 0 and PMABNAC < 0, respectively, using the maximum likelihood method when truncated signed value of accruals is the dependent variable.10

Our variable of primary interest is BMK. Our Hypothesis 1 predicts a positive coefficient on BMK when using |PMABNAC| as the dependent variable and a positive (negative) coefficient on BMK for the positive (negative) PMABNAC sub-sample in a truncated regression. In other words, our first hypothesis predicts that accruals are more extreme (i.e., absolute values are larger or signed values are more extremely positive for the positive sub-sample and more extremely negative for the negative sub-sample) for the benchmark sample (i.e., BMK = 1) relative to the mandatory rotation sample (i.e., BMK = 0), which is equivalent to say that accruals are less extreme (and thus audit quality is higher) for the mandatory rotation sample as compared to the benchmark sample.

We include several control variables for other known determinants of accruals in equation (2) based on Myers et al. (2003) and other prior studies. First, we include Age to control for changes in accruals over a company’s life cycle (Anthony and Ramesh 1992; Dechow et al. 2001). Based on Myers et al., we expect that accruals become less extreme as a company’s age increases. Second, since large companies face higher political cost (Watts and Zimmerman 1986; 1990) and higher litigation risk (Land and Lundholm 1993), they are likely to be less engaged in earnings management. In addition, Dechow and Dichev (2002) suggest that large companies tend to report larger and more stable accruals. Based on these studies, we include Size to control for the size effect and expect

that accruals for larger companies are less extreme. Third, we include IndGrw to control for a potentially positive effect of industry growth on a company’s accruals. However, Myers et al. show a mixed relation between accruals and IndGrw. We, therefore, do not predict the sign for IndGrw. Fourth, we include CFO to control for a negative relation between accruals and cash from operations (Dechow 1994; Sloan 1996). Based on findings in Myers et al., we expect a negative coefficient on CFO. Fifth, we include Big4 to control for prior findings that Big 4 or Big 5 audit firms tend to be more conservative and tend to limit their clients’ extreme accruals. However, Myers et al. find mixed results for Big4 and we thus do not predict the sign for Big4. Finally, we include Tenure to control for the effect of audit-firm tenure on accruals and expect a negative coefficient on Tenure based on Johnson et al. (2002) and Myers et al. (2003).

4.1.2. Empirical Findings Based on Performance-Matched Abnormal Accruals To mitigate potential undue influences of extreme values, we winsorize PMABNAC, Age, Size, IngGrw, and CFO at the top and bottom 1% of their respective distributions.11 We report descriptive statistics for variables in equation (2) in panel A, Table 2. First, we compare the mandatory rotation sample with the non-rotation sample. The mean |PMABNAC| for MROTA sample is 0.063 whereas that for NROTA sample is 0.068. A two-tailed t-test suggests that the difference of -0.005 is insignificantly different from zero. In addition, a two-tailed non-parametric Wilcoxon z-test suggests that the median |PMABNAC| for MROTA sample is insignificantly different from that for NROTA sample. Thus, univariate comparisons of the mean and median |PMABNAC| suggest that audit quality of the mandatory rotation sample is indifferent from audit

11 Deleting, instead of winsorizing, these variables at the top and bottom 1% produces qualitatively

quality of the non-rotation sample, failing to support our Hypothesis 1. Turning to other variables, the differences in means and medians between MROTA sample and NROTA sample are all insignificant except for Big4 and Tenure. The mean Big4 for MROTA sample is 0.826 whereas that for NROTA sample is 0.744. A two-tailed t statistic suggests that the difference of 0.082 is significant at the 0.1 level. We indicate this significance by placing a # sign on the mean Big4 for NROTA sample without reporting the specific t-statistic.12 As for Tenure, the mean and median Tenure for MROTA sample are both significantly smaller than their respective counterpart for NROTA, which is only expected given the construction of MROTA and NROTA samples.

[Insert Table 2 here]

Second, we compare MROTA sample with itself one year ago (MBEFR sample). We find that the mean, but not the median, |PMABNAC| for MROTA sample is

significantly larger (i.e., audit quality lower) than that for MBEFR sample, inconsistent with our Hypothesis 1.13 Third, we find no significant differences in the mean and median |PMABNAC| between MROTA sample and VROTA sample, again inconsistent with our Hypothesis 1.

Next, we examine the effect of mandatory audit-partner rotation on audit quality in a multivariate setting using equation (2). Panel B, Table 2, reports our findings using absolute abnormal accruals (|PMABNAC|) as the dependent variable. First, we find that the coefficient on BMK is positive but not significant (0.001, t = 0.166) in the “MROTA vs. NROTA” column. This suggests that absolute performance-matched abnormal

12 In other words, when a mean or median value in the NROTA column (or other columns) in panel A of

Table 2 bears a # sign, that means the said mean or median value is significantly different from its corresponding mean or median value for MROTA sample.

accruals for our mandatory rotation sample are not significantly smaller (i.e., audit quality higher) than those for the non-rotation sample after control variables are included in equation (2). Second, the coefficient on BMK is significantly negative (0.010, t = -2.750) in the “MROTA vs. MBEFR” column. This suggests that audit quality of

companies subject to mandatory audit-partner rotation in 2004 is lower than audit quality of these same companies one year ago under old audit partners, inconsistent with our Hypothsis 1. Third, the coefficient on BMK is insignificant in the “MROTA vs. VROTA” column (-0.002, t = -0.521), suggesting that audit quality of the mandatory rotation sample is indistinguishable from audit quality of companies whose audit partners were voluntarily rotated in years before 2003.

Following Myers et al. (2003), we also estimate equation (2) for positive and negative abnormal accruals separately.14 We report our findings from the truncated regressions in panels C and D, Table 2. First, for income-increasing accruals (see panel C), the coefficient on BMK is significantly negative (-0.022, t = -1.756) for the “MROTA vs. MBEFR” column, suggesting that new audit partners in the mandatory rotation sample constrain extremely positive accruals to a less extant relative to old audit partners in the MBEFR sample. Second, for income-decreasing accruals (see panel D), the

coefficient on BMK is significantly positive (0.066, t = 1.998) for the “MROTA vs. MBEFR” column, again suggesting that new audit partners in the mandatory rotation sample constrain extremely negative accruals to a less extent than do old audit partners in the MBEFR sample. Both findings suggest that audit quality of companies subject to

14 Myers et al. (2003, p. 790) argue that regulators are not only concerned about the dispersion in accruals

(i.e., absolute accruals) but also about extreme income-increasing and/or income-decreasing accruals. Income-increasing accruals can be used to inflate current earnings whereas income-decreasing accruals can be used to create “cookie jar reserves,” which can be used to increase future earnings.

mandatory rotation under new audit partners is lower than audit quality of these same companies one year ago under old audit partners. Third, audit quality of the mandatory rotation sample is indistinguishable from audit quality of the non-rotation sample (the “MROTA vs. NROTA” column) and from the voluntary rotation sample (the “MROTA vs. VROTA” column) as indicated by an insignificant coefficient on BKM for both positive and negative accruals sub-samples (see panels C and D).

In sum, our findings from multivariate regressions in panels B, C and D in Table 2 are consistent with findings from univarite analyses in panel A. Specifically, we have two major findings in Table 2. First, audit quality of the mandatory rotation sample is indistinguishable from audit quality of the non-rotation sample and the voluntary rotation sample when audit quality is measured by auditors’ constraining management’s extreme income-increasing or income-decreasing accruals. Second, audit quality of companies in the mandatory rotation sample under new audit partners is lower than audit quality of these same companies one year ago under old audit partners.

Chen et al. (2005) document that audit quality is positively related to audit-partner tenure under the voluntary audit-partner rotation regime in Taiwan before year 2002. The essence of Chen et al. (2005), Johnson et al. (2002) and Myers et al. (2003) is that client-specific knowledge and experience that can only be accumulated over time are vitally important for auditors to provide a high quality audit. Since audit-partner tenure for MROTA sample (average 1.506 years), by construction, is shorter than audit-partner tenure for NROTA sample (average 2.332 years), Chen et al. (2005) would have predicted lower audit quality under the voluntary rotation regime for MROTA sample. The fact that audit quality of our MROTA sample is not lower than that of NROTA

sample suggests that there is some benefit from a “fresh look” from new audit partners under the mandatory rotation regime. We conjecture that this benefit is enhanced auditor independence in fact.15 The benefit of enhanced auditor independence in fact from new audit partners, however, is offset by their relative lack of client-specific knowledge and experience (reduced auditor competence) compared to audit partners in NROTA sample (on average, audit-partner tenure in MROTA sample is 0.826 year shorter than that in NROTA sample).

When we compare MROTA sample (average 1.506 years) with MBEFR sample (average 4.825 years), new audit partners’ lack of client-specific knowledge and

experience is extreme (on average, audit-partner tenure in MROTA sample is 3.319 years shorter than that in MBEFR sample). The benefit of enhanced auditor independence in fact from new audit partners is not enough to compensate their extreme lack of client-specific knowledge and experience compared to older audit partners in MBEFR. To summarize, our analyses using performance-matched abnormal accruals seem to suggest that the benefit of mandatory audit-partner rotation is enhanced auditor independence in fact but the cost is reduced auditor competence due to new audit partners’ lack of client-specific knowledge and experience.

We now turn to discussion of control variables in Table 2. Results on Age are generally consistent with our prediction. Specifically, absolute performance-matched abnormal accruals are negatively related to Age in all three comparisons (panel B) and so are positive accruals (panel C). However, negative performance-matched abnormal accruals are not significantly related to Age (panel D). Our findings on Size are mostly

15 Recall, accrual-based measures of audit quality capture auditor competence and/or auditor independence

opposite to our prediction based on prior studies. We did not make prediction for IndGrw and Big4 because findings on these two variables in Myers et al. (2003) are mixed. We consistently find that CFO is negatively related to absolute abnormal accruals, positive abnormal accruals and negative accruals, consistent with our prediction and Myers et al. (2003) and Chen et al. (2005). Finally, we find that the absolute value of performance-matched abnormal accruals is significantly negatively related to audit-firm tenure (Tenure) in the “MROTA vs. MBEFR” and “MROTA vs. VROTA” columns (panel B), consistent with Johnson et al. (2002) and Myers et al. (2003).

4.1.3. Sensitivity Tests Based on Alternative Measures of Accruals

We conduct several additional analyses to test the robustness of our findings based on performance-matched abnormal accruals (estimated using the modified Jones model). Specifically, we calculate abnormal accruals using three alternative approaches: (1) performance-matched abnormal accruals estimated using the Jones (1991) model, which is similar to equation (1) except that the change in accounts receivable (ΔARt) is not subtracted from the change in sales revenue (ΔSALESt); (2) raw abnormal accruals estimated using the modified Jones model without performance matching; and (3) raw abnormal accruals estimated using the Jones model without performance matching.

With abnormal accruals estimated using the above three alternative approaches, we re-estimate equation (2). To save space, we only report the coefficient on BMK in Table 3.16 To facilitate comparison, we repeat our main findings in Table 2 at the top of each panel in Table 3. Overall, results based on these three alternative models are qualitatively similar to our main results with the following key exceptions. First, the

coefficient on BMK in the “MROTA vs. NROTA” column in panel B is significantly negative for the modified Jones model-estimated accruals (-0.029, t = -1.871), suggesting that audit quality of the mandatory rotation sample is lower than audit quality of the non-rotation sample. Second, the coefficient on BMK in the “MROTA vs. NROTA” column in panel C is significantly negative for the modified Jones model-estimated accruals (-0.060, t = -2.703) and for the Jones model-estimated accruals (-0.079, t = -2.630),

suggesting that audit quality of the mandatory rotation sample is higher than audit quality of the non-rotation sample. Since these two results are contradictory, we conclude that there is no consistent evidence regarding whether audit quality of the mandatory rotation sample is higher or lower than audit quality of the non-rotation sample. We thus maintain our previous conclusion that audit quality of the mandatory rotation sample is not

significantly different from that of the non-rotation sample. [Insert Table 3 here]

Prior studies (e.g., DeFond and Park 2001) suggest that current accruals are more susceptible to earnings management than total accruals. Consequently, measures of current accruals or working capital accruals might capture earnings management or audit quality better than measures based on total accruals. Following Myers et al. (2003) and DeFond and Park (2001), we use current accruals (CACt) and abnormal working capital accruals (AWCAt) as two additional measures of audit quality. These two measures are calculated below: 1 ) ( ) ( − Δ − Δ − Δ − Δ = t t t t t t TA STD CL Cash CA CAC (3) where:

of year t-1;17

ΔCasht = change in cash and cash equivalent between the first half of year t and the second half of year t-1;

ΔCLt = change in current liabilities between the first half of year t and the second half of year t-1;

ΔSTDt = change in short-term debt between the first half of year t and the second half of year t-1;

TAt-1 = total assets at the end of year t-1.

1 1 1/ ) ( − − − × − = t t t t t t TA SALES SALES WC WC AWCA (4) where:

WCt = noncash working capital in the first half of year t = (current assets – cash and short-term investments) – (current liabilities – short-term debt); SALESt = sales revenue in the first half of year t;

TAt-1 = total assets at the end of year t-1.

We re-estimate equation (2) using these two alternative measures of audit quality and report the coefficients on BMK in Table 3. Again, the tenor of our main findings in Table 2 is unchanged. The only key exception is a significantly negative coefficient on BMK in panel C for abnormal working capital accruals in the “MROTA vs. NTOTA” comparison sample (-0.541, t = -1.676), which provides some weak evidence that audit partners in the mandatory rotation sample constrains extreme income-decreasing working capital accruals to a greater extent than do audit partners in the non-rotation sample.

To summarize, our main findings using performance-matched modified Jones model abnormal accruals in Table 2 are robust to five alternative accrual-based measures of audit quality. Taken together (Tables 2 and 3), we find that (1) audit quality of the mandatory rotation sample is largely indistinguishable from audit quality of the non-rotation sample and the voluntary non-rotation sample and (2) audit quality of companies in

the mandatory rotation sample under new audit partners is lower than audit quality of these same companies one year ago under old audit partners. We, therefore, do not find support for our Hypothesis 1 that mandatory audit-partner rotation enhance audit quality, as measured by auditors’ constraining management’s extreme income-increasing or income-decreasing accruals.

4.2. Market-Based Proxy for Investor Perceptions of Audit Quality

In this section, we use the earnings response coefficient (ERC) estimated in concurrent returns-earnings regressions as a market-based proxy for investor perceptions of audit quality following Toeh and Wong (1993) and Ghosh and Moon (2005). We first present the empirical model and then report our findings.

4.2.1. Empirical Model and Variable Measurement

Following Ghosh and Moon (2005), we use the following model to examine whether investors perceive mandatory audit-partner rotation as enhancing audit quality:

+ + Δ + + + Δ + +

=α E E β BMK β EBMK EBMK Loss

CAR β1 β2 3 4 β5 β6 ε β β β β + + + Δ +

∑

+ = 18 11 10 9 8 7 j j jCV ETenure β ETenure Tenure ELoss (5) where:CAR = cumulative value-weighted market-adjusted abnormal returns over eight months during January-August;18

E = income from continuing operations for the first half of year t, scaled by the market value of equity at the beginning of January of year t;

ΔE = change in income from continuing operations between the first half of year t and the first half of year t-1, scaled by the market value of equity at the beginning of January of year t;

BMK = a dummy variable equal to 1 if observations are from one of the three benchmark samples: NROTA, MBEFR or VROTA, and equal to 0 otherwise;

18 Companies in our samples are all calendar year-end companies with semi-annual accounting periods

ending at the end of June. Since Taiwanese regulations require public companies to release semi-annual reports within two months after the end of the semi-annual period, our return accumulation periods end in August to ensure that semi-annual reports is released to the market and reflected in returns.

EBMK = E×BMK, the interaction between E and BMK; ΔEBMK = ΔE×BMK, the interaction between ΔE and BMK;

Loss = A dummy variable equal to 1 if E <= 0, and equal to 0 otherwise; ELoss = E×Loss, the interaction between E and Loss;

Tenure = Audit-firm tenure traced back to 1988;

ETenure = E×Tenure, the interaction between E and Tenure; ΔETenure = ΔE×Tenure, the interaction between ΔE and Tenure;

CVj = one of the eight additional control variables discussed below.

We measure cumulative abnormal returns (CAR) over an eight-month period (January-August) ending two months after the end of the semi-annual period. The reason we measure an eight-mouth CAR, instead of a six-mouth contemporaneous CAR (March-August), is that Ghosh and Moon (2005) argue that ERC estimated from equation (5) using a six-month contemporaneous CAR might be biased downwards due to prices leading earnings (see also, Kothari 1992; Kothari and Sloan 1992). Ghosh and Moon (2005) recommend the use of a longer period CAR to mitigate the potential bias in estimated ERC from using contemporaneous CAR (see also, Collins and Kothari 1989).

As in Ghosh and Moon (2005), we include both earnings levels and earnings changes in equation (5) because prior studies show that both of them explain concurrent returns (e.g., Easton and Harris 1991; Ali and Zarowin 1992). Unlike Ghosh and Moon (2005), we also include a loss dummy and its interaction with earnings levels in the model to allow ERC for profit firms (E > 0) and loss firms (E <= 0) to differ. Prior studies (e.g., Hayn 1995; Collins, Pincus and Xie 1999) find that losses are not

informative about future expected earnings and thus ERC for loss firms is much smaller than that for profit firms. We therefore focus on ERC for profit firms and use it to make inferences about investor perceptions of audit quality.

compare ERC for profit firms in the mandatory rotation sample (BMK = 0) with ERC for profit firms in a benchmark sample (BMK = 1). The full ERC for profit firms in the mandatory rotation sample is the sum of the coefficients on earnings levels and earnings changes (β1 + β2). The sum of the coefficients on EBMK and ΔEBMK (β4 + β5) is the incremental ERC for a benchmark sample. If investors perceive mandatory audit-partner rotation as enhancing audit quality, then ERC for profit firms in the mandatory rotation sample will be larger than ERC for profit firms in the benchmark sample. Our Hypothesis 2, thus, predicts a negative incremental ERC for the benchmark sample, i.e., β4 + β5 < 0. Finally, the full ERC for profit firms in a benchmark sample is the sum of ERC for profit firms in the mandatory rotation sample and the incremental ERC for the benchmark sample (β1 + β2 + β4 + β5).

We include several control variables in equation (5). The first control variables are audit-firm tenure (Tenure) and its interactions with earnings levels (ETenure) and with earnings changes (ΔETenure). Ghosh and Moon (2005) document that ERC

increases in audit-firm tenure, i.e., the sum of the coefficients on ETenure and ΔETenure is significantly positive. Moreover, we include eight additional control variables in Ghosh and Moon (2005) but without including their interactions with earnings levels and

earnings changes.19 They are: (1) company age, Age, defined before; (2) auditor type, Big4, defined before; (3) Growth potential, Growth, calculated as the sum of market value of equity and book value of total debt divided by book value of total assets, all

19 We do not include the interactions of these eight control variables with earnings levels and earnings

changes for two primary reasons. First, unlike Tenure where we want to examine whether ERC increases in

tenure, we are not interested in examining whether ERC varies with each of these eight control variables. Second, our samples are much smaller compared to those in Ghosh and Moon (2005). Adding more explanatory variables reduces the degree of freedom and potentially reduces the power of tests for our small samples.

measured at the end of the first half of year t; (4) earnings persistence, Persist, calculated as the first-order autocorrelation of income from continuing operations for the past 16 quarters; (5) earnings volatility, Volaty, calculated as the standard deviation of income from continuing operations for the past 16 quarters; (6) systematic risk, Beta, calculated using the past 60 monthly returns; (7) size, MVE, measured as the natural logarithm of market value of equity at the end of the first half of year t; and (8) financial leverage, LEV, measured as the ratio between total debt and total assets at the end of the first half of year t.

4.2.2. Empirical Findings Based on Earnings Response Coefficients

Due to the need for additional variables, our three comparison samples, MROTA vs. NROTA, MROTA vs. MBEFR and MROTA vs. VROTA, are all reduced in size. We lose some observations due to missing cumulative abnormal returns (CAR). The biggest source for data loss is by far the need of 60 past monthly returns to calculate Beta. Panel A, Table 4, summarizes the derivation process for our three comparison samples used in this part of the study.

[Insert Table 4 here]

To mitigate potential undue influence of extreme values, we winsorize CAR, E, ∆E, Age, Growth, Persist, Volaty, Beta, MVE, and LEV at the top and bottom 1% of their distributions. Panel B, Table 4, presents descriptive statistics for our three comparison samples. The mean CAR is positive (0.003) whereas the median is negative (-0.014) for the “MROTA vs. NROTA” comparison sample. The mean and median CAR are both negative (-0.046 and -0.072) for the “MROTA vs. MBEFR” comparison sample, and both negative (-0.018 and -0.062) for the “MROTA vs. VROTA” comparison sample.

The mean CAR is larger than median CAR for all three samples, suggesting that returns are right skewed. The mean E is smaller than median E for all three samples, similar to the patterns in the U.S. (see for example, Ghosh and Moon 2005). The mean and median ΔE are both positive, also similar to the U.S. data reported in Ghosh and Moon (2005). The means of BMK for three comparison samples are 0.190, 0.459 and 0.410,

respectively, suggesting that 19.0%, 45.9% and 41.0% of these comparison samples are companies not subject to mandatory audit-partner rotation (i.e., benchmark). The percentage of companies reporting losses in the “MROTA vs. MEFR” comparison sample and in the “MROTA vs. VROTA” comparison sample is slightly higher than that in the “MROTA vs. NROTA” comparison sample. The means and medians of remaining variables, Age, Big4, Growth, Persist, Volaty, Beta, MVE, LEV and Tenure, appear similar across three comparison samples.

Our findings from estimating equation (5) are reported in Table 5. The

coefficients on earnings levels, β1, are significantly positive for all three regressions. The coefficients on earnings changes, β2, are also significantly positive for all three

regressions. The full ERC for profit firms in the mandatory rotation sample (MROTA) is equal to β1 + β2. F-test results (testing β1 + β2 = 0) suggest that the full ERC for profit firms in the mandatory rotation sample is highly significantly positive in each of three regressions (ERC ranging from 2.713 to 2.869; F-statistic ranging from 15.552 to 24.527). Our findings, thus, confirm prior studies that both earnings levels and earnings changes explain concurrent returns.

Our primary interest is the incremental ERC (β4 + β5) for the benchmark sample. In all three regressions, the incremental ERCs are significantly negative (ERC ranging from -0.785 to -1.170; F-statistic ranging from 3.732 to 8.180). That is, the full ERC for each benchmark sample, NROTA, MBEFR or VROTA, is smaller than the full ERC for the mandatory rotation sample (MROTA) in each of the three comparison samples. This suggests that investors perceive mandatory audit-partner rotation as enhancing audit quality, consistent with our Hypothesis 2. Lastly, the full ERC for profit firms in each benchmark sample (β1 + β2 + β4 + β5) is significantly positive (ERC ranging from 1.699 to 1.928; F-statistic ranging from 5.432 to 16.039).20

We now turn to the discussion of control variables in Table 5. First, the

coefficient on Tenure is positive but not significant in all three regressions. Moreover, the sum of the coefficients on ETenure and ΔETenure (β9 + β10) is insignificantly different from zero in each of the three regressions. We thus are unable to document a positive relation between ERC and audit-firm tenure using Taiwanese data. Second, the

coefficients on Age and Big4 are insignificant for all three regressions but they are both significantly positive in Ghosh and Moon (2005). Third, we find that investors positively price growth potential as the coefficients on Growth are significantly positive in two out of three regressions, consistent with Ghosh and Moon and prior studies. The coefficient on Persist is significantly positive only in one regression. Fourth, our coefficient on Volaty (Beta) is insignificant (significantly negative) whereas the coefficient on Volaty

20 Recall that we use an eight-month CAR in estimating ERC in equation (5). To test the robustness of our

findings, we re-estimate equation (5) using a six-month (March-August) CAR (Note, the deflator for E and ΔE is the market value of equity at the beginning of March for this test). In untabulated results, we find that

(1) the full ERC for profit firms in the mandatory rotation sample (β1 + β2) is highly significantly positive

in each of the three comparison samples and (2) the incremental ERC for the benchmark sample (β4 + β5) is

(Beta) in Ghosh and Moon is significantly negative (insignificant). Finally, our

coefficients on MVE and LEV are insignificant in two out of three regressions and these two coefficients are also insignificant in Ghosh and Moon.

To summarize, our analyses using ERC suggest that investors perceive mandatory audit-partner rotation as enhancing audit quality, i.e., auditor independence in

appearance (e.g., Ghosh et al. 2005). Combining with our analyses using accrual-based proxies for audit quality, our findings suggest that the benefit of mandatory audit-partner rotation is enhanced auditor independence in fact and in appearance but the cost is reduced auditor competence due to new audit partners’ lack of client-specific knowledge and experience.

5. Conclusion

Audit-partner rotation has existed in the U.S. for some time and is recently strengthened in the SOX Act. An implicit assumption in the SOX Act is that mandatory audit-partner rotation enhances auditor independence and audit quality. However, this assumption is not systematically tested in the literature due to the lack of audit-partner information in the U.S. audit reports. We examine the effectiveness of mandatory audit-partner rotation in promoting audit quality using Taiwanese data. Audit-audit-partner rotation has been entirely voluntary in Taiwan until 2003 when two main Taiwanese stock exchanges introduced regulations that, in effect, require a five-year mandatory audit-partner rotation, fully effective in 2004. In addition, Taiwanese audit reports contain both audit-firm names and two signing audit-partner names, allowing researchers to identify years in which audit partners are rotated either voluntarily or mandatorily. These

important features of Taiwanese data provide a unique opportunity for us to examine the effectiveness of mandatory audit-partner rotation in promoting audit quality.

Following Myers et al. (2003) and Johnson et al. (2002), we use accrual-based proxies for audit quality, such as performance-matched abnormal accruals and abnormal working capital accruals, to examine the effect of mandatory audit-partner rotation on audit quality. We have two main findings. First, audit quality of companies subject to mandatory audit-partner rotation in 2004 is largely indistinguishable from audit quality of companies not subject to mandatory rotation in 2004 and companies whose audit partners were voluntarily rotated before 2003. Second, audit quality of companies subject to mandatory audit-partner rotation in 2004 under new audit partners is lower than audit quality of these same companies one year ago under old audit partners. We, therefore, do not find support for our Hypothesis 1 that mandatory audit-partner rotation enhances audit quality.

Following Ghosh and Moon (2005), we also examine the effect of mandatory audit-partner rotation on investor perceptions of audit quality, as measured by the earnings response coefficient. We find that ERC for our mandatory rotation sample is significantly larger than that for each of our three benchmark samples. We, thus, find that mandatory audit-partner rotation enhances investor perceptions of audit quality, i.e., auditor independence in appearance (e.g., Ghosh et al. 2005), consistent with our Hypothesis 2.

Taken together, our findings suggest that the benefit of mandatory audit-partner rotation is enhanced auditor independence in fact as well as in appearance but the cost is reduced auditor competence due to new audit partners’ lack of client-specific knowledge