國

立 交 通 大 學

財 務 金 融 研 究 所

碩 士 論 文

新興市場內部公司治理機制之

替代效果與互補效果分析

An Analysis of the Substitution and Complement Effects of

Internal Corporate Governance Mechanisms:

Evidence from an Emerging Country

研 究 生: 郭愛琳

指導教授: 鍾惠民 博士

陳達新 博士

新興市場內部公司治理機制之

替代效果與互補效果分析

An Analysis of the Substitution and Complement Effects of

Internal Corporate Governance Mechanisms:

Evidence from an Emerging Country

研 究 生:郭愛琳 Student: Ai-Lin

Kuo

指導教授: 鍾惠民博士

Advisor: Dr.

Huimin

Chung

陳達新博士

Dr.

Dar-Hsin

Chen

國立交通大學

財務金融研究所

碩士論文

A Thesis Submitted to Graduate Institute of Finance

National Chiao Tung University

in partial Fulfillment of the Requirements

for the Degree of

Master of Science in

Finance

January 2008

Hsinchu, Taiwan, Republic of China

中華民國九十七年一月

新興市場內部公司治理機制之

替代效果與互補效果分析

學生:郭愛琳

指導教授: 鍾惠民 博士

陳達欣 博士

國立交通大學財務金融研究所

中華民國九十七年一月

中文摘要 自2002年以降,獨立董監制度已在台灣部分實施五年。自2007開始,獨立董 監制度將在台灣上市公司全面實施。年本論文從過去五年來獨立董監制度與其他 內部公司治理機制間之交互關係審視其效力及效率。研究結果有三:第一,董事 會獨立性、本國法人持股、與外資法人持股皆與公司之價值有正向關係。第二, 獨立董監與本國法人持股之監督效果為替代關係、而獨立董監與外資法人持股之 監督效果為互補關係,且雙重完善公司治理機制之價值效果大於單一完善公司治 理機制之價值效果。第三,公司治理機制間之交互關係與公司特性相關,其中互 補作用在規模較小之公司或舉債較少之公司較為顯著,而替代關係在規模較大之 公司或舉債較多之公司較為顯著。本論文之啟示為,多重公司治理未必對所有公 司皆為最適安排,對於公司治理機制之間替代作用較為顯著之公司而言,可能適 合集中資源強化單一公司治理機制,避免造成多項公司治理機制之效力重複而成 本浪費;而對於公司治理機制之間互補作用較為顯著之公司而言,可能適合分散 資源於多重公司治理使其達到互補效果。 關鍵詞 公司治理、台灣、獨立董監、交互作用An Analysis of the Substitution and Complement Effects of

Internal Corporate Governance Mechanisms:

Evidence from an Emerging Country

Student:

Ai-Lin

Kuo

Advisor: Dr.

Huimin

Chung

Dr. Dar-Hsin Chen

Graduate Institute of Finance

National Chiao Tung University

January 2008

ABSTRACT

Independent director has been partially enforced in Taiwan for 5 years and is about to instituted thoroughly. This thesis examines the effectiveness and efficiency of independent director in Taiwanese corporate governance system by investigating how it interacts with other internal governance mechanisms, including domestic institutional investor and foreign institutional investor. The result acknowledges the positive valuation effect of independent director, as well as domestic institutional investor and foreign institutional investor, and finds that the governance effect of independent director substitutes the effect of domestic institutional investor and complements the effect of foreign institutional investor. Moreover, the interactions between internal governance mechanisms depend on firm characteristics. The substitution effect exists in large or high-leveraged firms while the complementary effect exists in small or low-leveraged firms. The implication of this research is that multiple governance mechanism is not necessarily optimal for every firm. For some firms it might be better to concentrate their resources in refining a single governance mechanism, while for others, it is more beneficial to diversify into many governance mechanisms with complementary effects.

KEYWORDS

誌 謝

本論文得以完成首先需感謝鍾惠民博士及陳達欣博士之悉心指導,亦得力於 口試委員謝文良博士及李漢星博士之不吝賜教,給予我許多寶貴的意見,此外財 金所諸多教授春風化雨之教導皆使我受益良多,使我在浩瀚之研究領域中得到啟 發,其言教身教亦是我終生之楷模。同時也要感謝陪我熬夜爆肝給予我許多論文 意見的 Yuposu、一起奮鬥論文一起流浪天涯的善體人意好夥伴哩哩、試鍊我使 我越挫越勇的艾力克斯魔、一路支持我陪我解悶的東引戰士凱秩、不厭其煩幫我 解惑的小翠、時常幫我打氣的倩如、帶給我許多歡笑的好咖王克鈞、以及諸多以 過來人經驗提供我許多小道消息讓我安心的交大財金所94級同學、在我宅在交 大時帶我出去吃頓好料的世顯、有求必應又好笑的學弟小田、一起奮鬥個案的瑪 莉及嵐鈞、一起奮鬥作業的小坦克、讓我半年可以安居樂業的婉茜、每晚一起熬 夜聊天的親愛室友們、一起宅在研究室的夥伴大熊、每週一起打羽毛球的好伙伴 阿 Sam、建佑、以文、文誠、俊儒等等、最了解我的蛞ㄩ、所有關懷我鼓勵我並 且寬容我疏於聯絡的好姐妹們。特別要感謝慷慨提供我資料來源的徐咪咪,如果 沒有妳的大力相助,我的論文就不會完成。最後要感謝我的父母和最親愛的妹 妹,因為你們的愛和支持,才有今天的我。 愛琳 二零零八年一月 謹誌於 新竹交大T

ABLE OFC

ONTENTS 中文摘要... I ABSTRACT ...II TABLE OF CONTENTS ... IV LIST OF TABLES ... V LIST OF FIGURES... VI 1. INTRODUCTION...1 2. THEORETICAL BACKGROUND...6 3. LITERATURE REVIEW...73.1. INDEPENDENT DIRECTOR AND FIRM PERFORMANCE...7

3.2. DOMESTIC BLOCKHOLDER AND FIRM PERFORMANCE...8

3.3. FOREIGN BLOCKHOLDER AND FIRM PERFORMANCE...9

3.4. SHAREHOLDING LEVERAGE AND FIRM PERFORMANCE...9

3.5. BLOCKHOLDER AND INTERACTION... 11

3.6. ABNORMAL RETURN,VALUATION AND CORPORATE GOVERNANCE... 11

4. DATA AND DESCRIPTIVE STATISTICS...13

4.1. OVERVIEW...13

4.2. GOVERNANCE-RELATED VARIABLES...13

4.3. FIRM-RELATED VARIABLES...15

4.4. DEPENDENT VARIABLE-TOBIN’S Q ...16

4.5. DESCRIPTIVE STATISTICS...16

5. METHODOLOGY AND RESEARCH RESULTS ...19

5.1. PRELIMINARY REGRESSION...19

5.2. GRAPHIC ANALYSIS OF GOVERNANCE MECHANISM VALUATION EFFECT...20

5.2.1VALUATION EFFECT OF SINGLE GOVERNANCE MECHANISM...20

5.2.2VALUATION EFFECT OF MULTIPLE GOVERNANCE MECHANISMS...22

5.3. GOVERNANCE MECHANISM INTERACTION TEST...24

5.4. FIRM SPECIFIC CHARACTERISTIC DEPENDENT TEST...26

5.5. ROBUST TEST...28

6. INTERPRETATION AND IMPLICATION...29

7. CONCLUSION ...33

TABLES AND FIGURES ...35

L

IST OFT

ABLESTable 1 definition of variables... 35

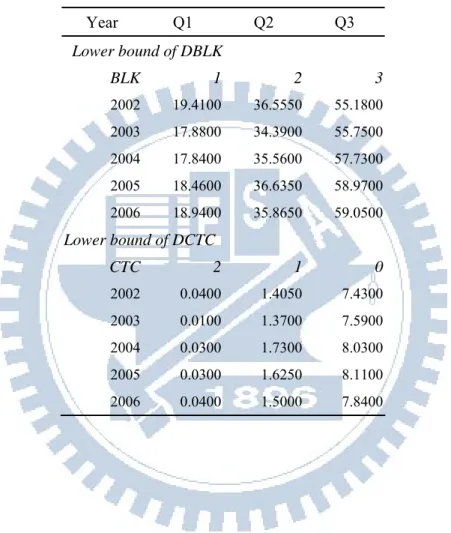

Table 2 lower bound of DBLK and DCTC each year (%) ... 37

Table 3 descriptive statistics... 38

Table 4 governance mechanisms condition each year... 39

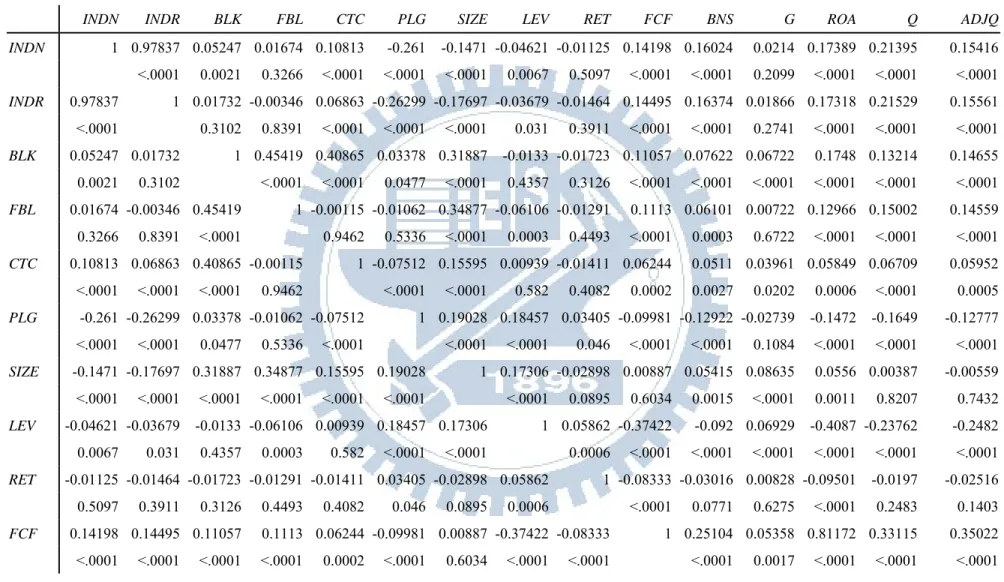

Table 5 Pearson correlation coefficient of variables... 41

Table 6 preliminary regression analysis results... 43

Table 7 regression analysis of governance mechanism interaction test and firm characteristic dependence test... 44

Table 8 robust Test... 45

L

IST OFF

IGURESFigure 1 valuation effect of independent director ... 46

Figure 2 valuation effect of blockholder ... 46

Figure 3 valuation effect of foreign blockholder... 47

Figure 4 conditional valuation effect of independent director and blockholder... 48

1. INTRODUCTION

Corporate governance are defined as a set of mechanisms–both internal and external-that induces the self-interested controllers of a company to make decisions that maximize the value of the company to its owners (Denis and McConnell 2003). The internal governance mechanisms of primary interest are the board of directors and the equity ownership structure of the firm (Denis and McConnell 2003). Among the board, independent directors are in a better position to monitor managerial behavior as they would not scruple to contradict the management (Choi et al. 2007). Regarding the equity ownership, large shareholders have the incentive to monitor management to make decisions that maximize the welfare of all shareholders (Shleifer and Vishny 1986 cited in Cremers and Nair 2005). As such, an appropriate corporate governance mechanism design is suppose to enhance firm valuation. However, each governance mechanism may not work independently to affect firm valuation (Danielson and Karpoff 1998). The aim of this thesis is trying to provide a better understanding of how these internal governance mechanisms interact. The thesis proceeds via four questions: Which governance mechanisms are value-enhancing? How do independent director and blockholder interact to affect firm valuation? How does this interaction depend on firm characteristics? And what implementation does it have for the corporate governance mechanism design?

Theoretical viewpoints regarding how governance mechanisms interact with each other are dichotomized. On the one hand, Shleifer and Vishny (1986 cited in Cremers and Nair 2005) suggest that different mechanisms might be complements and substantially facilitate each other. On the other hand, Pound (1992 cited in Cremers and Nair 2005) proposes that different mechanisms can be viewed as substitutes if their effects overlap each other. Accordingly, firms with both

mechanisms obtain similar governance outcome to those with only one mechanism. Independent director and blockholder both have some trait that the other party is short of and thus may function as complements. On the one hand, the more abundant wealth incentive of blockholder complements the shortcoming of independent director for mitigating shareholders’ collective action problem (Becht et al. 2003 p.18); on the other hand, the neutrality of independent director complements the tendency of blockholder to collude with management when the entrenchment effect exceeds the alignment effect (Morck et al. 1988 and McConnell and Servaes 1990 cited in Denis and McConnell 2003 p.10). However, independent director and blockholder also have some similar trait that may function as substitutes. Fama and Jensen (1983) points out that independent director is induced by the “reputation incentive” to monitor the management in order to develop the expert prestige. Yermack (2004) corroborates this argument by an empirical research, finding that independent director receives positive performance incentives of compensation, turnover, and opportunities to obtain new board seats. The reputation incentive of independent director might play a substitute role for the wealth incentive of blockholder in the governance outcome.

This thesis tries to clarify whether the substitution effect or the complementary effect outweighs the other between independent director and blockholder. Independent director has been obligate to newly-public firms in Taiwan since 2002. Other public-listed firms can choose to set it or not during the buffer period. Starting from 2007, independent director is instituted thoroughly; all public listed firms that exceed a certain capital amount have to set at least two seats of independent director and at least 20 percent of the board comprising of independent directors (United Group Daily News 2005). Since during the past 5 year, independent director was optional for firms, this thesis conducts a retrospective research, investigating whether this

legitimated standard of board independence had a positive valuation effect on firms adopt it.

The importance of the interaction between governance mechanisms lies in the construction of a cost-efficient governance mechanism design. Each corporate governance mechanism that initiated to monitor management discretion and mitigate agency costs actually has its opportunity cost1. To avoid either paying multiple costs yet receiving overlapping effects, or receiving inefficient effect due to lack of complementary mechanisms, it is crucial to understand how governance mechanisms interact with each other, so that it is feasible to construct a cost-efficient governance mechanism design.

Recently the research is increasingly interested in the effect of multiple governance mechanisms (Gillan 2005). Some analyses have attempted to study this issue by principle analysis yet find it difficult to interpret. Other researches alternatively choose to study this issue means of the substitution or complementary effect analysis. Shleifer and Vishny (1986 cited in Cremers and Nair 2005) take blockholder and anti-takeover provision as example, arguing that the latter in some cases can not perform successfully without the existence of the former. Following Shleifer and Vishny (1986), Cremers and Nair (2005) further prove that not only anti-takeover provisions but also blockholder can not function efficiently alone. So far

1 For instance, firstly, independent directors are paid good salaries. Basing on Taiwan Economic

Journal Great China Database (TEJ), on average each firm paid 1.8 percent of its pre-tax income to directors in 2006, and the average salary of each director is 2.33 million. Secondly, blockholder, via its tremendous influence, intervenes in management decision and sacrifices firm autonomy (Aghion and Tirole 1997, Burtkart et al. 1997 and Paganoand and Roell 1998 cited in Becht et al. 2003 p.26). Thirdly, diminishing the anti-takeover provisions exposes the company to the highly disruptive and costly takeover market, and induces management to seek after short-term profit (Gompers et al. 2003 and Becht et al. 2003 p.19). Fourthly, minimizing the control rights in excess of cash flow rights, a mechanism more prevailing in non-US market (Denis and McConnell 2003 p.19), forces insiders to plunge more money into shareholding and thus subjects insiders to high level of idiosyncratic risk,

western literatures mostly deal with the interaction of anti-takeover provisions and other governance mechanisms (for example, Shleifer and Vishny 1986 and Cremers and Nair 2005 compare it with blockholder, while Danielson and Karpoff 1998 compare it with independent director). To the best of my knowledge, there has not been any paper discussing the interaction of governance mechanisms in the emerging market such as Taiwan. As takeover activities are only active in US and UK markets and very rare in most of emerging markets (Becht et al. 2003), this thesis examines the substitution and complementary effects of the internal corporate governance mechanism in association with firm valuation in Taiwan following Cremers and Nair’s (2005) methodology.

In order to make up for the shortage of not discussing the takeover mechanism, this thesis discusses an alternative equity ownership structure issue that is especially prominent in emerging markets: the shareholding leverage. Deviation of control rights away from cash flow rights is one form of the “shareholding leverage” concept and is especially prevailing in emerging countries (Denis and McConnell 2003 p.19). A similar and more specific form of shareholding leverage in Taiwan is the pledge ratio, defined as the percentage of the shareholding of controlling shareholder pledged for bank loans (Lee and Yeh 2004). Both forms of shareholding leverage enable the incumbents to leverage small amount of own capital to hold large stake of firm control, which offers them the ability and incentive to gain private benefits and expropriate from minority shareholders (Claessens et al. 2000). This thesis also examines the valuation effect of these negative governance mechanisms.

The findings of this thesis are easily summarized as follows. Independent director, as well as domestic blockholder and foreign blockholder have significant positive valuation effects, while both forms of shareholding leverage show

insignificant effects. Moreover, independent director show substitution effect to domestic blockholder and complementary effect to foreign blockholder. These interactions depend on firm characteristics. Substitution effect exists in large or high-leveraged firms and complementary effect exists in small or low-leveraged firms.

The remainder of this thesis is presented in the following sequence. Section 2 illustrates the theoretical background. Section 3 reviews the literatures. Section 4 introduces the data. Section 5 elaborates the methodology. Section 6 interprets the results, and section 7 draws the conclusions.

2. THEORETICAL BACKGROUND

The main objective of this paper is to distinguish whether different governance mechanisms are substitute goods or complementary goods. This section applies the economic theory of substitute and complement to illustrate how firm valuation reflects governance mechanism interaction. Comparing the capital market to a commodity market, different governance mechanisms can be viewed as related goods and equity can be viewed as a bundle package containing different governance mechanisms. In this market, shareholders are the demand side and the managers are the supply side. If shareholders perceive better protection under a certain bundle of corporate governance mechanisms, they are willing to give premium value to that bundle.

Analogically, if a firm consists of two governance mechanisms which substitute each other, for a rational consumer, buying these two mechanisms with overlapping functions will not bring higher utilities than buying only either of them, so she is unwilling to pay extra money for this firm comparing with a firm comprising of either one mechanism alone. For a supplier, as this bundle costs higher but can not be valued higher in response, the extra costs spent are wasted. On the contrary, if a firm consists of two governance mechanisms which complement each other, consumers are more willing to pay higher price for this one-stop shopping bundle than paying double searching efforts to buy them in different places. A firm with single governance mechanism is likely to be valued in a discount than the firm with dual mechanisms in the capital market. In conclusion, firms with substitute governance mechanisms show discount valuation while firms with complementary governance mechanisms show premium valuation.

3. LITERATURE REVIEW

3.1. INDEPENDENT DIRECTOR AND FIRM PERFORMANCE

Until recently, most research on the impact of independent director is empirical, and the results are mixed (Becht et al. 2003 p.31). While some research in US find that companies with higher percentage of independent director are more likely to dismiss the poorly performed CEO (Weisbach 1988 cited in Becht et al. 2003 p.31-32), and have higher appointment announcement date equity abnormal returns (Rosenstein and Wyatt 1990 cited in Becht et al. 2003 p.32), other research find that board compositions are unrelated to firm performance (Hermalin and Weisbach 2003).

Regarding international corporate governance literatures, early Japanese evidence shows that appointment of independent director from bank to non-financial companies stabilize and modestly improve firm performances, measured by stock returns, operating performance and sales growth (Kaplan and Minton 1994). In European countries, the role of the board of director is usually not prescribed in law, as Europeans do not consider shareholder wealth maximization as the paramount goal of a corporation (Wymeersch 1998 cited in Denis and McConnell 2003 p.6). Nevertheless, starting from the Code of Best Practice in UK in year 1992, European countries have begun to embrace the idea of board composition appropriateness (Denis and McConnell 2003 p.7). The evidences in UK are mixed as well. While the result of Dahya et al. (2002 cited in Denis and McConnell 2003 p.7) shows that the independent director is associated with higher management turnover following poor performance, Frank et al. (2001 cited in Denis and McConnell 2003 p.7) find that in poor performing firms, independent director impedes discipline of poorly-performing managers.

In terms of emerging market, Korea instituted outside director after Asian financial crisis under the command of International Monetary Fund (IMF), requiring all the public-listed firm to have at least 25 percent of the board comprising of outside directors, and the empirical result shows that the valuation effect of outside director is strongly positive (Choi et al. 2007). China instituted outside director in 2001 after several corporate governance scandals, yet the empirical result shows that outside directors only have positive impact on sales growth but little impact on financial performance measured by return on equity (Peng 2004 and Clarke 2006).

3.2. DOMESTIC BLOCKHOLDER AND FIRM PERFORMANCE

Blockholder utilizes its influence on management to make decisions that increase overall shareholders’ welfare and is a candidate solution to mitigate the agency problem (Denis and McConnell 2003). Among them, institutional investor is becoming increasingly prominent for its sophisticated and active investing style (Gillan and Starks 2000). Literatures of institutional investor are inconclusive. Although Hartzell and Starks (2003 cited in Gillan 2006) approve the impact of concentrated institutional ownership in moderating executive compensation, others argue that interest conflictions (Woidtke 2002 cited in Gillan 2006) and business ties (Davis and Kim in press cited in Gillan 2006) compromise the monitoring role of institutional investors. In Asia, Mitton (2002) acknowledges the positive effect of outside blockholder on firm’s performance immunity against financial distress. Korean evidence are inconclusive, while Chang and Hong (2000) find that group-affiliated firms are benefit from group member through resources sharing, Choi et al. (2007) find that domestic institutional investors such as Chaebol or family control are negative or insignificant associated with firm performance. In Taiwan, Filatotchev et al. (2005) find that institutional investors have positive impact on firm

performance.

3.3. FOREIGN BLOCKHOLDER AND FIRM PERFORMANCE

Starting from the end of year 2003, the regulation of Qualified Foreign Institutional Investor (QFII) and investment amount ceiling for foreign institutions are abolished (United Group Daily News 2003). As the equity markets are increasingly globalizing and integrating, foreign institutions start to play an important role in the Taiwanese equity market, and empirical studies start to pay attention to their differently investment objectives and decision-making horizons (Filatotchev et al. 2005). Most research acknowledge their contributions to firm performance, with their more experienced monitoring ability (Thomsen and Pedersen 2000), more abundant international financial resources (Taylor 1990), and more professional strategic expertise (Tihanyi et al. 2003). Evidence in Korea shows that foreign investor has significant positive valuation effect (Choi et al. 2007). Evidence in Taiwan also confirms that foreign bank investment is significant positive associated with firm performance measured by return on capital and market to book ratios (Filatotchev et al. 2005).

3.4. SHAREHOLDING LEVERAGE AND FIRM PERFORMANCE

Shareholding leverage is embodied in two forms: one is the deviation of control rights away from cash flow rights, and the other is the pledge ratio. La Porta et al. (cited in Claessens et al. 2000) initiate the discussion of ultimate control, and find that ownership and controlling rights can be separated to the benefit of incumbents. When control rights bring about private benefits that have value beyond the cash flow rights, incumbents have incentives to hold excess control rights than cash flow rights, by cross holdings, design of superior-voting shares, and pyramid structure (Denis and

McConnell 2003 p.16). Bebchuk e al. (2000) argue that deviation of control rights away from cash flow rights creates large agency cost. Therefore, investor protection appears to improve with the concentration of cash flow rights, but decreases as the controlling shareholders acquire more control rights in excess of their cash flow rights (Durnev and Kim 2005). An empirically research across 18 emerging countries has demonstrated this viewpoint, discovering that accumulation of control rights in excess of cash flow rights is generally value-reducing for a company (Lins 2003 cited in Denis and McConnell p.18). In East Asia, Classens et al. (2000) find that the deviation of control rights and cash flow rights is especially pronounced in family-controlled firms in Korea, Singapore and Taiwan, while less common in Japan. In Western Europe, Faccio and Lang (2002) only find significant discrepancy of control rights and cash flow rights in Switzerland, Norway, and Italy.

In terms of pledge ratio, pledging for loans effectively reduces the funds required for shareholding, resulting in personal credit expansion and over-investment (Lee and Yeh 2004). In Korea, Joh (2003) finds that before the financial crisis, firms with higher disparity of control rights and cash flow rights are associated with lower profitability, especially in public-listed firms. Evidence in Taiwan shows that pledge ratio has better explanatory ability than discrepancy of control rights and cash flow rights when it comes to abnormal equity returns (Chen 2003). Yeh et al. (2003) suggest that Classens et al. (2000) underestimate the control right of the controlling shareholder in Taiwan due to the insufficient disclosure of ultimate control. Yeh et al. (2003) recalculate the discrepancy of control rights and pledge ratio during 1997-1998 in Taiwan, and find that these two measurements are negatively associated with firm value. Further, Lee and Yeh (2004) find that these two measurements are associated with higher possibilities of financial distress.

3.5. BLOCKHOLDER AND INTERACTION

Some previous studies investigate how blockholder interacts with other conditions. Regarding the interaction between takeover mechanism, Grossmand and Hart (1980 cited in Becht et al. 2003 p.24) find that blockholder facilitates the implement of takeover activities; and Cremers and Nair (2005) prove that the other way around relationship is true. In terms of the interaction between market liquidity, Hirschman (1970 cited in Becht et al. 2003 p.25) suggests that blockholder can not be relied upon once the market has abundant liquidity and the blockholder has the option to sell the stake rather than to intervene. This explains the reason why in US market blockholder has less incentive to monitor management than many other emerging countries (Mayer 1988, Black 1990, Coffee 1991, Roe 1994 and Bhide 1993 cited in Becht et al. 2003 p.25). To summarize, blockholder mechanism is complementary to anti-takeover mechanism and relies on the incentive rooted in the illiquid secondary market to function well.

3.6. ABNORMAL RETURN,VALUATION AND CORPORATE GOVERNANCE

remers and Nair (2005), whose methodology is adopted in this thesis, examine how governance mechanisms interact in being associated with equity abnormal returns, yet this these investigates how governance mechanisms interact in being associated with firm valuation. Regarding abnormal return, Gompers et al. (2003) find intriguing evidence and conjecture that investors are surprised by the higher-than-expected agency costs resulted from weaker corporate governance, and hence firm with weak governance has significantly negative equity abnormal returns and vice versa. However, Core et al. (2006) detect analysts forecasting errors and earning announcement date abnormal returns as measurements of the accuracy of investor

resulted from different corporate governance practices between companies beforehand. Furthermore, after either extending the sample period to year 2000-2003 or excluding the technology firms from the original sample period, the significant relationship between equity abnormal returns and corporate governance found by Gompers et al. (2003) fades out. Consequently, Core et al. (2006) conclude that rather than the expectation effect, the abnormal returns to shareholder rights are caused by the larger “new economy pricing puzzle” of the late 1990s.

In terms of valuation and corporate governance, LaPorta et al. (1998) argue that greater investor protection increases investors’ willingness to provide financing and lead to a lower cost of capital and a higher firm valuation. An empirical study cross 14 emerging market also finds that better corporate governance is significantly correlated with better firm performance and valuation (Klapper and Love 2004). In single country empirical studies, the positive valuation effect of corporate governance, including outside blockholder, foreign institution, and outside director, is also found in China (Bai et al. 2004) and Korea (Black et al. 2006).

4. DATA AND DESCRIPTIVE STATISTICS

4.1. OVERVIEW

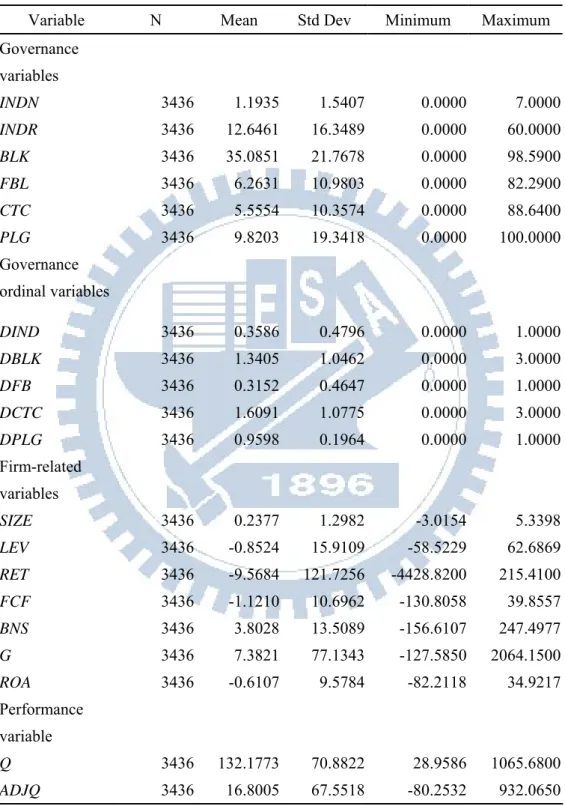

The data of this paper can be classified into three categories: governance-related variables, firm-related variables, and the dependent variable. Table 1 presents the definition of all variables. All of them are extracted from Taiwan Economic Journal Great China Database (TEJ). TEJ is a database specializing in capital market data in Taiwan and China and is the data provider of many professional data providing institutions such as DataStream, and Reuters (TEJ n. d.) The sample contains all the public listed firms in Taiwan Stock Exchange excluding financial institutions from year 2002 to 2006 as 2002 is the first year in which the independent director regulation is partial enforced on newly-public firms. Besides, corporate governance data from year 1996 to 2001 is also supplemented to observe the evolution of corporate governance in Taiwan. In order to avoid endogeneity, all the governance-related variables and firm-related variables are observed one year lagged comparing with their dependent variable counterpart. After dropping those with missing values, there are totally 3436 firm-year in the sample.

4.2. GOVERNANCE-RELATED VARIABLES

In this section, six governance variables, INDN, INDR, BLK, FBL, CTC, PLG, and their relevant ordinal or dummy variables, DIND, DBLK, DFB, DCTC, DPLG, are elaborated. This paper discusses three primary governance mechanisms in Taiwan: independent director, blockholder, and shareholding leverage. Among them, blockholder refers to institutional investors, comprising of domestic institutional investors and foreign institutional investors, both of which are usually deemed to be a positive impact on corporate governance. Shareholding leverage is embodied in two

forms: deviation of control rights away from cash flow rights, and the pledge ratio. Both of them are negative governance measurement. The higher the pledge ratio or the more the control rights deviated from cash flow rights, the worse the corporate governance is.

In terms of board independence, two variables INDN and INDR represent the number of independent director and the percentage of independent director among the board, respectively. A dummy variable DIND in relate to independent director is created according to the new regulation, taking both absolute number and relative percentage into consideration. The variable DIND is coded “1” if the firm has at least two seats of independent director and 20 percent of independent director among the board; otherwise DIND is coded “0”.

Regarding blockholder, the variable BLK is defined as the percentage shareholding of domestic institutions; the variable FBL is defined as the percentage shareholding of foreign institutions, calculated as percentage shareholding of foreign financial institutions plus percentage shareholding of other foreign institutions. Meanwhile, an ordinal variable DBLK in relate to blockholder and a dummy variable DFB in relate to foreign blockholder are created. For DBLK, the percentage shareholding of blockholder, BLK, of each firm is ranked in a yearly base, and they are equally classified into 4 categories by the quartiles. The ordinal variable DBLK is coded “3” if the firm is ranked in the highest quarter; “2” if the firm is ranked in the sub-highest quarter; “1” if the firm is ranked in the sub-lowest quarter; and “0” if the firm is ranked in the lowest quarter. The quarters of the blockholder shareholding percentage each year are listed in Table 2. The dummy variable DFB in related to foreign blockholder shareholding percentage is coded “1” if the foreign blockholder shareholding percentage, FBL, of the firm exceeds 5 percent and “0” otherwise.

In terms of shareholding leverage, the variable CTC is defined as the percentage control rights of the controlling shareholder minus the percentage cash flow rights of the controlling shareholder. This variable is directly extracted from the calculation results in the TEJ database. An ordinal variable DCTC in relate to CTC is created in the same way as the blockholder variable. Firstly, CTC of each firm in the same year is ranked and classified into 4 categories by the quarters listed in Table 2. Secondly, the ordinal variable DCTC is coded “0” if the firm is ranked in the highest quarter; “1” if the firm is ranked in the sub-highest quarter; “2” if the firm is ranked in the sub-lowest quarter; and “3” if the firm is ranked in the lowest quarter. The reason why the coding logic is contrary to that of blockholder-related ordinal variables is that CTC is a negative governance measurement. Higher deviation of control rights away from cash flow rights implies higher agency problem. Therefore, “3” refers the level of worst corporate governance, while “0” refers the level of best corporate governance.

Regarding the second proxy of shareholding leverage, the pledge ratio, the variable PLG is defined as the percentage of the shareholding of controlling shareholding pledged for bank loans (Lee and Yeh 2004). This variable is also directly extracted from the TEJ database. A related dummy variable DPLG is defined basing on the standard of a recently proposing regulation, which submits that the controlling shareholders of public-listed firms can no longer borrow from the bank whenever the pledge ratio exceeds 60 percent (United Group Daily News 2007). Accordingly, the dummy variable DPLG is coded “0” if the pledge ratio exceeds 60 percent and “1” otherwise.

and ROA. In order to observe the valuation effect of corporate governance, the impacts of firm specific characteristics should to be controlled. SIZE is defined as the natural log of total assets. LEV is defined as the percentage of total debt to total assets and measures thes credit risk of the firm. RET is defined as one minus the dividend ratio and implies the growth prospect ex ante. FCF is defined as earnings before depreciation, interests and tax (EBDIT) minus interests, tax, and investment expenditure, scaled by total assets. It is a measurement of liquidity and the managerial competence. BNS is defined as the market value of stock bonus scaled by net income, and measures the level of employee alignment effect. G is defined as the growth rate of sales and describes the growth prospect ex post. ROA is defined as the net income scaled by the total assets and is a measurement of operating performance. Each of these variables is industry-adjusted by subtracting the industrial yearly medium of this measure following Gompers et al. (2003). The industry identification is based on the Taiwan Stock Exchange industry category.

4.4. DEPENDENT VARIABLE-TOBIN’S Q

The dependent variable in this paper is firm valuation measured by Tobin’s Q. Tobin’s Q is calculated as the market value of total assets divided by the book value of total assets, where the market value of total assets is computed as book value of total assets plus the market value of common stock less the book value of common stock following Gompers et al. (2003). The variable ADJQ is industry-adjusted by subtracting the industrial-yearly medium in order to eliminate the industry impact. 4.5. DESCRIPTIVE STATISTICS

The descriptive statistics of the variables are listed in Table 3. From 2002 to 2006, there are, in total, 3,436 firm-year samples. On average domestic institutional

investors hold 35 percent of the share while foreign institutional investors hold 6 percent. The domestic institutional shareholding outweighs the foreign institutional shareholding. Both domestic and foreign institutional shareholding percentage deviate largely, from 0 percent to 98.59 percent for domestic institutions and to 82.29 percent for foreign institutions, implying that institutional investors, especially foreign institutional investors, focus on some specific stocks.

The deviation of control rights away from cash flow rights is 5.56 percent on average. In other words, in Taiwan, the controlling shareholders hold 5.56 percent more control rights than cash flow rights on average. However, the inter-firm difference is tremendous, from the lowest 0 percent to the highest 88.64 percent, revealing that the corporate governance qualities in Taiwan deviate enormously. The average pledge ratio is 9.82 percent, implying that 9.82 percent of the shareholding of the controlling shareholder is financed by the bank pledge loan on average. Again there are vast differences between firms, ranging from 0 percent to 100 percent. In order to compare these different governance mechanisms, they are transformed into ordinal or dummy variables.

The Tobin’s Q on average is 132%, implying that on average Taiwanese firms have assts market values of 1.32 times their book value. The rest of the variables are the industrial-adjusted firm specific characteristics.

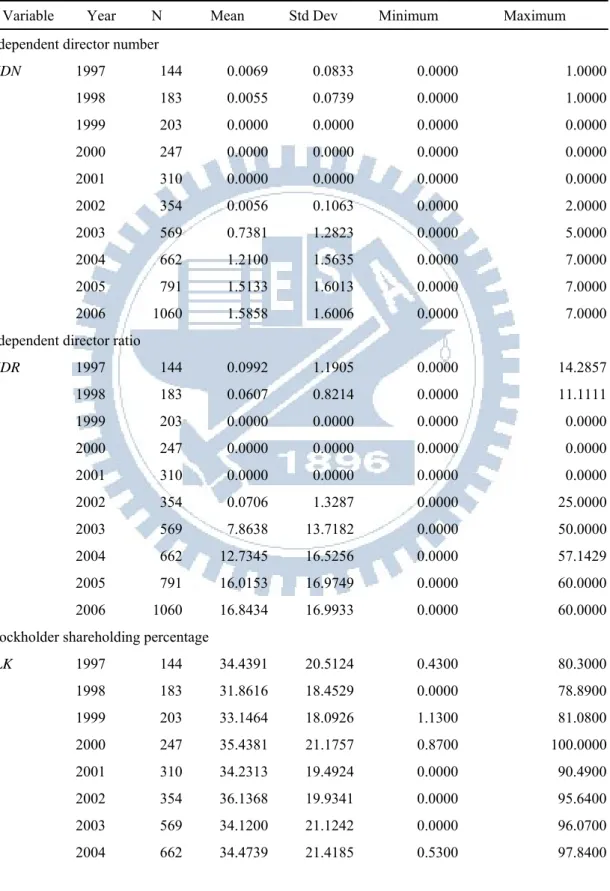

Table 4 presents the evolution of corporate governance from year 1997 to 2006. Before the regulation partially enforce in 2002, although there are some firms set independent director, the maximum number of independent director does not exceed 2 and the maximum ratio of independent director does not exceed 20 percent. After year 2002, the maximum number of independent director exceeds 2 and the maximum

Regarding blockholder, the annual average of domestic blockholder percentage shareholding is quite stable. In terms of foreign blockholder, although the regulation on qualified foreign institution investor (QFII) and the investment limit of $3 billion are released starting from year 2004, the change of foreign institutional shareholding percentage is not very clear. The average foreign institutional shareholding percentage changes from 5.06 percent in 2003 to 5.43 percent in 2004, and the maximum foreign institutional shareholding percentage changes from 71.8 percent in 2003 to 82.9 percent in 2004. The possible reason is that the signal effect of the abolishment of QFII regulation is more substantial than the actual effect since in 2003 none of the foreign institution reaches 83 percent of the investment quota, and it is very unlikely for a foreign institution to invest more than $3 billion, equivalent to NT$ 100 billion, in Taiwan all at once (United Group Daily News 2003).

In regard to shareholding leverage, the discrepancy of control rights and cash flow rights is quite stable, maintaining at about 5 percent on average over the ten years. However the maximum of discrepancy of control rights rises from 44.92 percent in 1997 to 74.16 percent in 2006, implying that the inter-firm differences might increase and shareholding leverage tactic has been utilized by certain firms more extremely over the ten years. The pledge ratio improves over the ten years, from 14.09 percent in 1997 to 8.32 percent in 2006, reflecting the fact that people paying more and more attention to the pledge problem of controlling shareholders.

5. METHODOLOGY AND RESEARCH RESULTS

5.1. PRELIMINARY REGRESSION

The first stage of this research is to clarify which governance mechanisms show significant valuation effect after controlling for other firm specific characteristics by regression analysis. Preliminary regression equations are estimated as the following equation (1) and (2): 2 3 4 5 6 7 8 1 2 3 4 5 6 7 8 where , , , . (1) A i i i i

ADJQ GM SIZE LEV RET FCF BNS G ROA

GM DBLK DFB DCTC or DPLG DJQ DIND DBLK DFB DCTC DPLG SIZE LEV RE α β β β β β β β β ε α β β β β β β β β = + + + + + + + + + = = + + + + + + + + T+β9FCF+β10BNS+β11G+β12ROA+εi (2) The first equation tests the governance mechanism valuation impact in isolation and the second equation tests the joint valuation impact of all governance mechanisms. In order to avoid endogeneity, all the governance-related variables and firm-related variables are observed one year lagged comparing with their dependent variable counterpart. The null hypothesis isβi =0,i=1...4. If any of the parameters of governance-related variables is statistically significant, it indicates that the governance mechanism has significant valuation effect. The estimated parameters of equation (1) are presented in the first five column of Table 6 and the estimated parameters of equation (2) are presented the last column of Table 6.

As shows in the first five column of Table 6, DIND DBLK, and DFB all have significant positive parameters under α=0.01 significance level yet DCTC and DPLG do not have, indicating that the mechanisms of independent director, domestic blockholder, and foreign blockholder all have significant valuation effects while discrepancy of control rights and pledge ratio do not.

The result of equation (2) shows in the last column of Table 6. The result shows that both DBLK and DFB have significantly positive valuation effects under α=0.01 significance level and DIND has significant positive valuation effects under α=0.05 significant level. DCTC and DPLG still do not show significance.

In terms of other firm specific variables, there are some other significant valuation factors revealed in Table 6. Firstly, leverage has a significantly negative impact on firm valuation which fit in with the expectation that leverage increases the credit risk and discount firm value. Secondly, both bonus and ROA show significant positive valuation effects. The former reveals the employee incentive effect and the latter shows the operating profitability is value increasing.

5.2. GRAPHIC ANALYSIS OF GOVERNANCE MECHANISM VALUATION EFFECT

5.2.1VALUATION EFFECT OF SINGLE GOVERNANCE MECHANISM

The second stage of this research follows Gompers et al. (2003), calculating and comparing firm valuation (which, in Gompers et al.’s (2003) case, is firm’s equity abnormal returns) under different levels of corporate governance, to distinguish whether the governance mechanism is associated with firm valuation. Here a graphical presentation is utilized together with the table to facilitate analyzing the structures and trends of governance mechanisms’ valuation effect under different levels. The following step executions are performed on each governance mechanism in turn in order to recognize the validity of each governance mechanism. First of all, a regression equation is estimated to derive a residual Tobin’s Q in which the effects of the other 3 governance mechanisms plus other firm factors are eliminated. To examine the valuation effect of independent director, the following regression equation is estimated:

1 2 3 4 5 6 7

8 9 10 11 (3)

excind

i

ADJQ DBLK DFB DPLG CTC SIZE LEV RET

FCF BNS G ROA

α β β β β β β β

β β β β ε

= + + + + + + +

+ + + + +

To examine the valuation effect of domestic institutional investor, the following regression equation is estimated:

1 2 3 4 5 6 7

8 9 10 11 (4)

excblk

i

ADJQ DIND DFB DPLG CTC SIZE LEV RET

FCF BNS G ROA

α β β β β β β β

β β β β ε

= + + + + + + +

+ + + + +

To examine the valuation effect of foreign institutional investor, the following regression equation is estimated:

1 2 3 4 5 6 7

8 9 10 11 (5)

excfbl

i

ADJQ DIND DBLK DPLG CTC SIZE LEV RET

FCF BNS G ROA

α β β β β β β β

β β β β ε

= + + + + + + +

+ + + + +

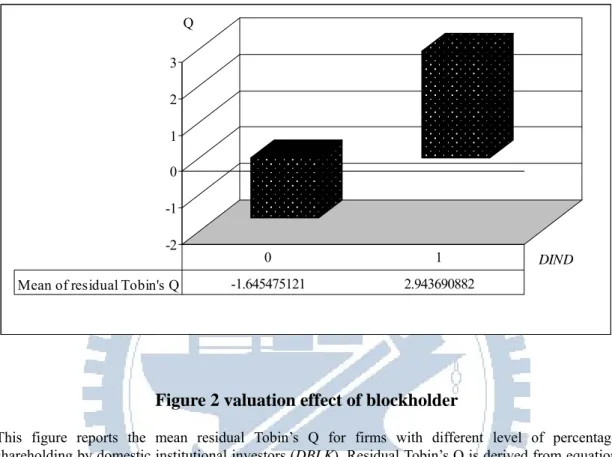

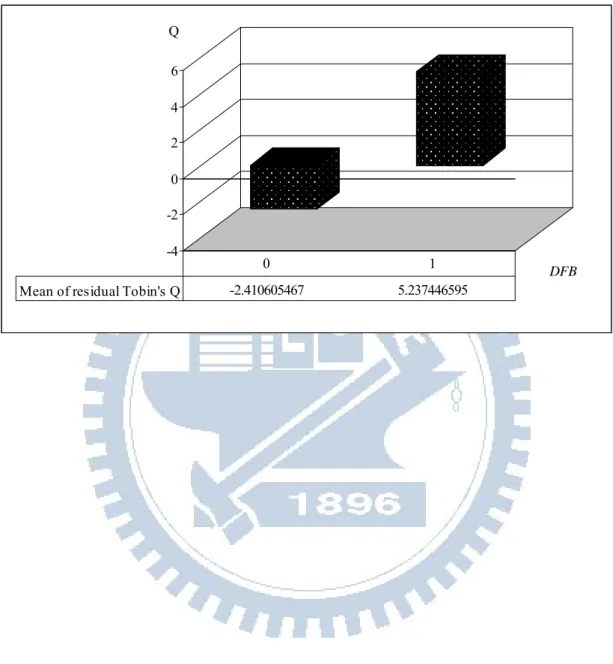

Second, samples are separated into different groups by the levels of governance mechanism. Third, the average residual Tobin’s Q of each group is calculated and a mean comparison graph is drawn accordingly. Figure 1 to Figure 3 present the average residual Tobin’s Q under different levels of independent director, domestic blockholder, and foreign blockholder respectively. If a clear incremental trend is shown in the graph, it indicates that higher level of the governance mechanism is associated with better firm valuation in the stock market. Figure 1 presents the mean residual Tobin’s Q for firms which have accommodated the new regulation of independent director (DIND=1) and firms have not accommodate (DIND=0). As shown in Figure 1, firms with sufficient board independence has 4.5 percent higher valuation than firms has not given other things being equal. Figure 2 presents the mean residual Tobin’s Q for firms with different level of percentage shareholding by domestic institutional investors. As a clear trend displayed in Figure 2, firms with more share percentage hold by domestic institutional investors are associated with higher market valuation. Firms with the highest percentage of domestic institutional

shareholding enjoy 6.82 percent premium market value. Figure 3 presents the mean residual Tobin’s Q for firms with lower or higher than 5 percent of shares hold by foreign institutional investors. Figure 3 shows that firm with higher foreign institutional shareholding percentage enjoy 7.6 percent higher valuation in the market. Overall, the residual valuation graphic analysis concludes that independent director, domestic blockholder, and foreign blockholder are associated with higher valuation premium.

5.2.2VALUATION EFFECT OF MULTIPLE GOVERNANCE MECHANISMS

The third stage of this research follows Cremers and Nair’s (2005) methodology, analyzing the valuation effect (which, in Cremers and Nair’s (2005) case, is firm’s equity abnormal returns) of one governance mechanism condition on the level of the other governance mechanism. The main objective of this step is to find the answer of the following question:

Are firms with two strong governance mechanisms valued higher than firms with only one of them?

A two-step execution is performed to each pair of governance mechanisms in turn to examine how governance mechanisms interact to affect firm valuation and distinguish the substitution effect or complementary effect. This research focuses on the interactions of two pairs of governance mechanisms: domestic blockholder vs. independent director, and foreign blockholder vs. independent director. Firstly, a regression is estimated to derive a residual Tobin’s Q in which the effects of the other governance mechanisms plus other firm factors have been eliminated. The following three regression equations are estimated to derive the residual Tobin’s Q for observing the interaction of DIND vs. DBLK, and DIND vs. DFB respectively.

1 2 3 4 5

6 7 8 9 10 (6)

excib

i

ADJQ DFB DCTC DPLG SIZE LEV

RET FCF BNS G ROA α β β β β β β β β β β ε = + + + + + + + + + + + 1 2 3 4 5 6 7 8 9 10 (7) excif i

ADJQ DBLK DCTC DPLG SIZE LEV

RET FCF BNS G ROA

α β β β β β

β β β β β ε

= + + + + +

+ + + + + +

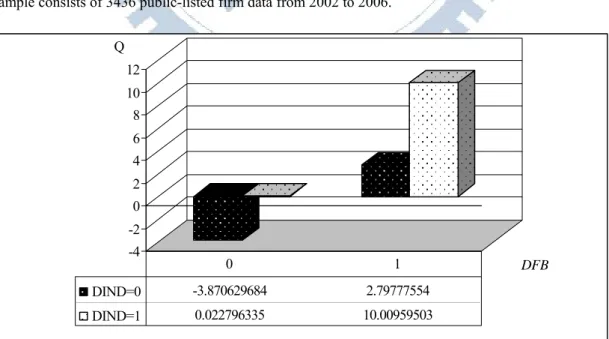

Secondly, samples are cross selected into N M× different groups, where N and M denote the levels of the two governance mechanisms. Specifically, the variable DIND has two levels and the variable DBLK has four levels. Thus the residual Tobin’s Q derived from equation (6) are separated into2 4 8× = groups. On the other hand, the variable DIND and DFB both have two levels. Thus the residual Tobin’s Q derived from equation (7) are separated into 2 2 4× = groups. Third, the average residual Tobin’s Q of each group is calculated and listed in the histogram. This figure indicates the joint residual valuation effect of different of corporate governance mechanisms packages. How much premium market value a set of governance mechanisms can earn implies the market viewpoint of how the two governance mechanisms interact. Figure 4 presents the conditional residual Tobin’s Q of independent director and domestic blockholder. Samples are separated into 2 4 8× = groups, comprising all the possible arrangement of these two governance mechanisms. For example, the left pillar in the histogram shows the mean residual Tobin’s Q of firms in which both governance mechanisms are weak; while the right pillar in the histogram shows the mean residual Tobin’s Q of firms in which both governance mechanisms are strong. As shown in Figure 4, on average, firms with unqualified board independence and the highest percentage institutional investor shareholding enjoy 5.75 percent premium market value and firms with qualified board independence and the highest percentage institutional investor shareholding enjoy 8.85 percent premium market value. Firms with multiple strong governance mechanisms enjoy a higher premium valuation than

Figure 5 presents the conditional residual Tobin’s Q of independent director and foreign blockholder. Samples are separated into2 2 4× = groups, comprising all the possible arrangement of these two governance mechanisms. For example, the left pillar in the histogram shows the mean residual Tobin’s Q of firms in which both governance mechanisms are weak; while the right pillar in the histogram shows the mean of residual Tobin’s Q of firms in which both governance mechanisms are strong. As shown in Figure 5, firms with qualified board independence and the highest percentage foreign institutional investor shareholding enjoy 10 percent premium market value while firms with unqualified board independence and the highest percentage foreign institutional investor shareholding only enjoy 2.8 percent premium market value. Firms with multiple strong governance mechanisms enjoy a higher premium valuation than firms with strong foreign blockholder in isolation.

5.3. GOVERNANCE MECHANISM INTERACTION TEST

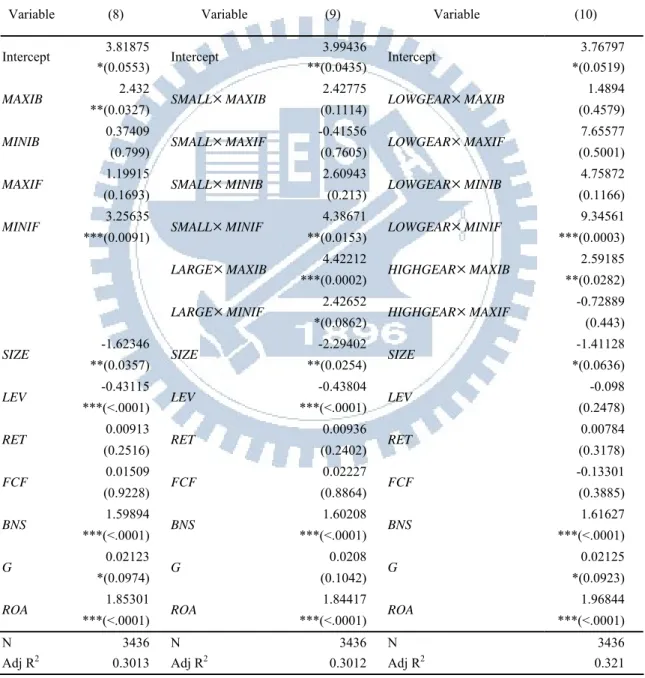

The forth step of this research follows Cremers and Nair (2005), utilizing the regression approach to distinguish the substitution effect and complementary effect between governance mechanisms. In the beginning, four variables capture the substitution effect and the complementary effects have to be defined. Given that governance mechanisms do associate higher valuation, if two governance mechanisms are substitutes, then it is the level of the more sophisticated one that matters to the firm valuation, because the effect of the more sophisticated governance mechanism outweighs and substitutes the effect of the less sophisticated mechanism. Accordingly, the following two variables capture the substitution effect between pairs of governance mechanisms. The variable MAXIB denotes the maximum level of DBLK and three times of DIND, the two variables representing domestic blockholder and independent director. The variable MAXIF denotes the maximum level of three times

of DIND and three times of DFB, the two dummy variables representing independent director and foreign blockholder. Contrarily, if two governance mechanisms are complements, then it is the level of the less sophisticated one that matters to the firm valuation, because it is the level two governance mechanisms both attain. Accordingly, the following two variables capture the complementary effect between pairs of governance mechanisms. The variable MINIB denotes the minimum level of three times of DIND and DBLK, the two variables representing independent director and domestic blockholder. The variable MINIF denotes the minimum level of three times of DIND and three times of DFB, the two dummy variables representing independent director and foreign blockholder. After defining the necessarily variables, the following regression equation is estimated to distinguish whether the substitution effect and complementary effect determine the firm valuation given other things being equal.

1 2 3 4

5 6 7 8 9 10 11 i (8)

ADJQ MAXIB MINIB MAXIF MINIF

SIZE LEV RET FCF BNS G ROA

α β β β β

β β β β β β β ε

= + + + +

+ + + + + + + +

The null hypothesis isβi =0,i=1...4. If the parameter of MAXIB or MAXIF is statistically significant, it indicates that the valuation effects of the corresponded two governance mechanisms substitute each other. On the contrarily, if the parameter of MINIB or MINIF is statistically significant, it indicates that the valuation effects of the corresponded two governance mechanisms complement each other. The results are shown in the first column of Table 7.

As presented in Table 7, the variables MAXIB are significantly associated with higher valuation under α=0.05 significance level, indicating that independent director and domestic blockholder can replace each other; the market views these two governance mechanisms as substitutes. On the other hand, MINIF shows significant

association with higher firm valuation under α =0.01 significance level, indicating that independent director and foreign blockholder can facilitate each other; the market views these two governance mechanisms as complements.

5.4. FIRM SPECIFIC CHARACTERISTIC DEPENDENT TEST

After distinguishing the interaction between governance mechanisms, the fifth step of this research follows Cremers and Nair (2005), considering the interaction between governance mechanisms in the presence of firm size and leverage. The main objective of this step is to examine how the governance mechanisms’ interaction depends on firm specific characteristics. In the beginning, two pairs of variable denote size and leverage are defined respectively. Firstly, regarding firm size, two dummy variables SMALL and LARGE take the value of 1 for firms with lower than medium and higher than medium industry-adjusted size respectively and 0 otherwise. Secondly, regarding leverage, two dummy variables LOWGEAR and HIGHGEAR take the value of 1 for firms with lower than first quartile and higher than first quartile industry adjusted leverage respectively and 0 otherwise. After defining the necessary variables, the following two regression equations are estimated in sequence to examine how governance mechanism interactions depend on firm size and leverage.

1 2 3

4 5 6

7 8 9 10 11 12 13

+

+ i (9)

ADJQ MAXIB SMALL MAXIF SMALL MINIB SMALL MINIF SMALL MAXIB LARGE MINIF LARGE

SIZE LEV RET FCF BNS G ROA

α β β β β β β β β β β β β β ε = + × + × + × × + × + × + + + + + + + 1 2 3 4 5 6 7 8 9 10 11 12 13 + i (10)

ADJQ MAXIB LOWGEAR MAXIF LOWGEAR MINIB LOWGEAR MINIF LOWGEAR MAXIB HIGHGEAR MAXIF HIGHGEAR

SIZE LEV RET FCF BNS G ROA

α β β β β β β β β β β β β β ε = + × + × + × + × + × + × + + + + + + +

To avoid perfect collinearity with the intercept, the interaction

either regression equations.

The second and third column of Table 7 presents the regression results of both regression equations. The null hypothesis isβi =0,i=1...6. The second column presents the result of governance mechanism interaction in the presence of firm size; the second column presents the result of governance mechanism interaction in the presence of firm leverage. As shown in the second column, the parameters of SMALL×MINIF and LARGE ×MAXIB are significant under α =0.01 significance level, implying that the complementary effect between independent director and foreign blockholder is more likely to appear in small firms and the substitution effect between independent director and domestic blockholder is more likely to appear in large firms. The result indicates that governance mechanisms’ substitution or complementary interactions depend on the firm characteristic. Specifically, in large firms, one point increase in the higher of the score of domestic blockholder shareholding and independent director leads to 4.42 percent incremental market valuation premium; one point increase in the lower of the score of foreign blockholder shareholding and independent director leads to 4.49 percent higher market valuation. The other parameters are insignificant.

The third column of Table 7 presents the estimates of equation (10). As it shows, the substitution effect between independent director and domestic blockholder appears in high-leveraged firms under α =0.05 significance level while the complementary effect between independent director and foreign blockholder appears in low-leveraged firms under α=0.01significance level, indicating that governance mechanisms’ substitution or complementary interactions depend on the firm characteristic, and the complementary effect are especially active in firms with low leverage while the substitution effect are especially active in firms with high leverage.

Specifically, in firms with low leverage, one point increase in the lower of the score of foreign blockholder shareholding and independent director leads to 9.35 percent higher market valuation; in firms with high leverage, one point increase in the higher of the score of domestic blockholder shareholding and independent director leads to 2.59 percent incremental market valuation premium.

5.5. ROBUST TEST

This section testify the robustness of the governance mechanism interaction test in equation (8) and firm characteristic dependence test in equation (9) and (10) by incrementally controlling for board size (BRD) with the results presented in Table 8. The results show that board size is insignificantly negative associated with firm value. This result corresponds to the argument of Jensen (1993), Yermack (1996), Eisenberg, Sundgren and Wells (1998) that there is a cost of slower decision-making and having a less candid culture with larger boards. Other results remain the same. The results of the governance mechanism interaction test in equation (8) and firm characteristic dependence test in equation (9) and (10) is robust to controlling for board size.

6. INTERPRETATION AND IMPLICATION

This thesis examines the necessity of multiple governance mechanism design. The research process can be separated into three parts: the first part confirms the effectiveness of each governance mechanism; the second part distinguishes whether incremental governance mechanism adds more value or not. The third part examines if the governance mechanism interaction depends on firm characteristics.

The first part clarifies which governance mechanism is effective in eliminating the agency problem and thus augmenting firm valuation. The preliminary regression shows that firms with higher percentage shareholding by institutional investors, either domestic or foreign, are associated with higher market valuation premium, implying that institutional investors, based on superior professional know-how and abundant incentive, play important roles in monitoring the incumbents and effectively increase firm value in Taiwan. Furthermore, the regression results also show that firm with qualified independent director arrangement are associated with higher market valuation premium, implying that independent director is also a vigorous governance mechanism in monitoring the incumbents and increasing firm value. Meanwhile, the valuation effect of discrepancy of control rights and pledge ratio are not significant in the regression results. The reason why the stock market do not giver premium value to firms for temperance in discrepancy of control rights and pledge ratio might results from the specific business background in Taiwan that cross-holding, pyramid shareholding structure and pledge ratio are commonly utilized even in many first-tier companies such as Foxconn, Formosa Plastic Group and China Trust (United Group Daily News 2006). In addition, both functions, i.e. less discrepancy of control rights or less pledge ratio, are merely passive governance mechanisms that reduce incumbents’ incentive to seek private benefits, instead of active monitoring

mechanism to prohibit them. Last but not least, the reason why the result contradicts to that of Yeh et al. (2003) might result from the different economic conditions in the two sample periods. As the discrepancy of control rights mostly appears in the best and the worst firms like a “M distribution”, the Asia financial crisis in the late 90’s has washed out most of the worst firms and thus the negative relationship between the discrepancy of control right and firm value is not so significant later on. In conclusion, in Taiwanese market, independent director and blockholder might be the definitive governance mechanisms in firm valuation. The results of graphic analysis also correspond to this result, showing that better board independence and higher percentage of blockholder shareholding, either domestic or foreign, contribute incremental premium on firm value given other things being equal. A clear trend of increasing value can be seen for firms with either better board independence or higher blockholder shareholding from the graphs.

The second part tries to find out whether two joint governance mechanisms performs better in eliminating agency problem than single governance mechanism. The results of graphic analysis show that the highest percentage of blockholder shareholding combining with qualified board independence are associated with higher market valuation than either highest percentage of blockholder shareholding or qualified board independence in isolation. It denotes that both blockholder and independent director are valued higher when coexisting with each other than functions alone. The results indicate that market may view multiple governance mechanisms as better shareholding protection mechanism and give it higher premium. The regression shows that when considering independent director and domestic blockholder, the substitution effect outweighs the complement effect in valuation; it is the more sophisticated governance mechanism that matters to the firm valuation. When

regarding independent director and foreign blockholder, the complementary effect outweighs the substitution effect in valuation; it is the more coexisting level that matters to the firm valuation. It indicates that the market views independent director and domestic blockholder as substitutes and only gives premium value to the highest level of either of them. On the other hand, market views independent director and foreign blockholder as complements and only give premium value to the extent in which both governance mechanisms coexist. The reason why the governance effect of independent director substitutes the effect of domestic blockholder while complements the effect of foreign blockholder might be rooted in the time horizon of the incentives. As foreign blockholder prefers short-term investment, it tends to monitor management by the short-term performance. In contrast, domestic blockholder prefers relatively long-term investment, so it tends to monitor management by the long-term performance. Independent directors are induced by the “reputation incentive.” As reputation can not be built in a short period of time, independent directors also tend to monitor management by the long-term performance so that they can gain and maintain long-term prestige. Therefore the monitoring effect of independent directors overlaps the effect of domestic blockholder while complements the effect of foreign blockholder.

The third part examines whether the interaction between governance mechanisms are specific in firms with certain characteristics. The results show that the substitution effect between independent director and domestic blockholder is especially significant in large or high-leveraged firms, and the complement effect between independent director and foreign blockholder is especially significant in small or low-leveraged firms. Regarding the size factor, it perhaps is due to the reason that large firms can attract more attention of institutional investors and can recruit more competent

independent director in an independent director market with excess demand, while small firms are inferior in attracting the attention of blockholder and find it more difficult to recruit prestigious independent director, thus the governance mechanism quality of large firms tend to be stronger and can function well independently and the governance mechanism quality of small firms tend to be weaker and can not function well without the facilitating of the other mechanism. In terms of the leverage factor, in high-leveraged firms the free cash flow is constrained which serves as a self-enforcing function to prevent management appropriation (Grossman and Hart 1982, Jensen, 1986, 1993 cited in Gillan 2005). Accordingly, the agency problem in firms with high leverage is less serious and hence independent dependent and domestic blockholder can substitute each other and function well in isolation. Contrarily, the agency problem in low-leveraged firms are severer and hence independent director and foreign blockholder can not function well along; instead, they need the complement of each other.

To conclude, while in large or high-leveraged firms the design of an optimal governance mechanism should avoid overlapping problem and should focus on refining single governance mechanism, in small or low-leveraged firms the design of an optimal governance mechanism should diversify to multiple governance mechanisms and hence enable them to facilitate each other.

7. CONCLUSION

This thesis, motivated by the newly-instituted regulation, discusses the appropriateness of multiple governance mechanism design in Taiwanese market. The research follows the issue and the methodology of Cremers and Nair (2005) about governance mechanism interaction, and adds elements in relate to other governance mechanisms, such as independent director, and elements specific in the emerging market, such as the discrepancy of control rights and the pledge ratio.

The following three conclusions are raised from the research results. Firstly of all, in Taiwanese market, independent director, as well as domestic institutional investor shareholding and foreign institutional investor shareholding all have incremental effects in eliminating agency problem and increasing firms’ market valuation premium. Contrarily, discrepancy of control rights and pledge ratio show insignificant valuation effects.

Second, firms with strong domestic or foreign blockholder and sufficient board independence enjoy higher valuation than firms with only strong domestic or foreign blockholder. Moreover, domestic blockholder plays a substitutive role to independent director while foreign blockholder plays a complementary role to independent director. In other words, in firms with sufficient domestic blockholder shareholding, independent director serve as a substitute and the incremental valuation effect is overlapping, while in firms with sufficient foreign blockholder shareholding, independent director serve as a complement and the effects facilitate each other. Thus a cost-efficient governance mechanism design of firms with sufficient domestic blockholder should be concentrating resources on strengthening single governance mechanism, while a cost-efficient governance mechanism design of firms with

director mechanism.

Third, the substitution effect between governance mechanisms is more significant in large or high-leveraged firms while the complementary effect between governance mechanisms is more significant in small or low-leveraged firms. Therefore firms with large size and high leverage should specifically take into consideration the governance mechanism overlapping problem while firms with small size and low leverage should specifically take into consideration the cooperation function of governance mechanisms.