國

立

交

通

大

學

企業管理碩士學程

碩

士

論

文

南郵政通訊公司(VNPT)的新興移動商務生態系統--以DOCOMO I-MODE為標竿研究

EMERGING M-COMMERCE ECOSYSTEM OF VIETNAM POST AND

TELECOMMUNICATION COPORATION (VNPT) – USING DOCOMO I-MODE AS

THE BENCHMARK STUDY

指導教授:吳武明 教授

研 究 生:阮越雄

National Chiao Tung University

College of Management

Global Master of Business Administration Program

Thesis

南郵政通訊公司(VNPT)的新興移動商務生態系統--以 DoCoMo

i-Mode 為標竿研究

Emerging M-Commerce ecosystem of Vietnam Post and

Telecommunication Corporation (VNPT) – using DoCoMo i-Mode as

the Benchmark study

Advisor: Professor Francis Wu

Student: Nguyen Viet Hung

南郵政通訊公司(VNPT)的新興移動商務生態系統--以 DoCoMo 為

標竿研究

Emerging M-Commerce ecosystem of Vietnam Post and

Telecommunication Corporation (VNPT) – using DoCoMo as the

Benchmark study

指導教授: 吳武明 教授

Advisor: Francis Wu

研 究 生 :阮越雄

Student : Nguyen Viet Hung

國 立 交 通 大 學

管理學院

企業管理碩士學程

A Thesis

Submitted to Global Management Business Administration College of Management

National Chiao Tung University

in partial Fulfillment of the Requirements for the Degree of Master in

Global Management Business Administration June 2010

Hsinchu, Taiwan, Republic of China

摘要

移動電話的普及和移動通信的快速發展帶動移動電話的電子商務(E-Commerce)的進化. 現今,人們已不用一直坐在電腦前面,透過移動電話既能自由移動,亦可同時隨時隨地進 行多項交易.日本的 DoCoMo 公司就是一個大膽實行電子商務之成功案例,變成後來讓人 模仿的標竿範例. 越南是一個還在發展中的國家,其技術和市場趨勢還落伍他國.自 2010 年加入世貿後,而 且在此時其國內移動技術又升級到 3G.就在這樣的條件下給越南造就一個新的機會,不僅 加強接近其他國家在這方面的快速技術,而且更將其帶入到移動商務空間.利用新科技在 越南現今的移動環境建造一個可持續的市場對許多越南企業來說都是艱鉅的任務.作為第 一 個 在 越 南 市 場 發 展 3G 方 向 的 企 業 , 越 南 電 信 集 團 ( Vietnam Posts and Telecommunications Group, 以下簡稱 VNPT) 很快就意識到這些,其既是機遇又是障礙. 本研究探討理想情況下 DoCoMo 公司的 imode,以為 VNTP 建立一個類似的移動電子商務 生態系統舉出一些提示或建議.本研究將通過他們在不同時期、不同環境:越南—日本的 情況 下來作比較分析. 建議 VNTP 對商業價值的訂製.以 DoCoMo 的基準,針對一些服務內容提供過程與順序作 分析方向.建議 VNTP 將移動銀行、娛樂排列於數據庫、信息類之前,將其放於發展的第 一方位.指出以 VNTP 的資源如何建立一個類似的生態系統的結構與適當的地點.為建議今 後的研究劃出了定量方向,最後希望將來會有其他研究者對此議題進一步探討.ABSTRACT

The rapid development of mobile communications technology with the popularity of mobile phones has led an evolution of electronic commerce (E-Commerce) to the mobile commerce (M-Commerce). Nowadays, instead of being in front of PC, one can freely be mobile while able to make many kinds of transaction at anywhere by any time with a mobile phone. DoCoMo Japan is the first bold but successful volunteer company in M-Commerce trend. It has made DoCoMo the ideal case for the followers.

Vietnam is a developing country and sometime behind in technology and market trend. In 2010, upgrading to 3G mobile technology after being WTO member, Vietnam has an opportunity not only to be closer with other country in rapid technology pace but also to enter to the M-Commerce space. Utilizing new technology to make a sustainable market is a challenging task for any Vietnam Corporation in the current Vietnam moving environment. Viet Nam Posts and Telecommunications Group (VNPT), a state-owned group, soon realized both those opportunities and obstacle when being the first one participating in 3G direction.

This research examines the ideal case DoCoMo i-mode in order to draw some hints or suggestions for VNPT in building a similar M-commerce ecosystem. This is done by comparing two companies but analyzing them in different situation in Japan and Vietnam at different periods.

Suggestions of VNPT‘s centric role in commerce value chain have been drawn. After benchmarking DoCoMo, some elements of services offered and their process order are pinpointed. The suggestion for putting mobile banking, entertainment categories first then database, information classes later in action were also recommended for VNPT. Structure of resources for VNPT to setup a similar ecosystem was also pointed out and arranged in proper places. Recommendations for quantitative future researches were put in the end of this thesis with hope for other further study about these open topics.

ACKNOWLEDGEMENT

The fulfillment of the Master‘s degree is always a great personal achievement but it would not have been possible without the support of other people. From starting point to the end of writing process writing thesis always faced challenges and obstacles, therefore it needed countless guidance, ideas, and encouragement to be completed. I was lucky person to receive this kind of help from many sources.

First of all, I would like to express the deepest appreciation to my advisor, Prof. Francis Wu who taught me valuable courses like Global Technology Strategy and Information Management which gave me the motivation about technology topics for my thesis. He also a person, who was always willing to help correct my ideas bring me great guidance for completing this thesis.

I would like to thank the Prof. Tang and Prof. Han who help me to refine my thesis proposal and suggest me the direction for working on it.

In addition, a grateful thank to my classmates, I appreciate all input I received from you. I improved and enhanced myself a lot on help and support from everyone that I worked and study with during the GMBA program.

Furthermore, I would like to thank to my parents and my brothers who give me more strength and energy to continue whenever I felt stress along process.

Last but not least, I would like to give my thank to all other Professors who provided me and other GMBA students many interesting courses at National Chiao Tung University, which help prepare each student well for being potential manager in the future.

List of Table

Table 1 User‘s buying behavior on mobile internet vs. that on desktop ... 7

Table 2 Business model for mobile network commerce ... 15

Table 3 i-mode main characteristic ... 18

Table 4 i-Mode services... 20

Table 5 i-mode service fee ... 22

Table 6 Core concept of complex system ... 26

Table 7 i-mode content portfolio characteristic and requirement ... 26

Table 8 Vietnam mobile companies ... 34

Table 9 Mobile subscriptions of Vietnam mobile companies ... 35

Table 10 Statistics on Internet development up to 3/2010 ... 43

Table 11 Mobile money business model ... 45

Table 12 Comparison Vietnam and Japan in general ... 51

Table 13 Vinaphone‘s initial portal services ... 56

List of Figures

Figure 1 Global 3G subscribes ... 6

Figure 2 Mobile Internet vs. PC internet adaption rate ... 7

Figure 3 World mobile payment transaction value ... 8

Figure 4 Largest Asia Pacific mobile markets, Q1 2009 (millions) ... 10

Figure 5 Vinaphone - Road map for implementation 3G network ... 11

Figure 6 Vietnam software and digital content industry revenue ... 11

Figure 7 NTT Corporation Milestones ... 16

Figure 8 Details of NTT Group... 17

Figure 9 i-mode Timeline ... 18

Figure 10 i-mode network ... 19

Figure 11 DoCoMo‘s billing structure and revenue sharing machanism ... 21

Figure 12 Ohboshi‘ proposal S-Curves of mobile industry‘s growth ... 23

Figure 13 Value chain management ... 25

Figure 14 The i-mode content portfolio ... 27

Figure 15 Organization structure ... 27

Figure 16 Actions in building i-mode ... 28

Figure 17 VNPT landmark ... 30

Figure 18 VNPT Group structure... 31

Figure 19 Internet market share of VNPT ... 32

Figure 20 Two key VNPT‘s internet companies ... 33

Figure 21 Vietnam‘s mobile share market change over years ... 35

Figure 22 Mobile market share QI/2010 ... 37

Figure 23 Quality of Service index results for Vietnam mobile companies ... 39

Figure 24 GDP - composition by sectors -2009 ... 41

Figure 25 Vietnam age structure 2009 ... 41

Figure 26 Mobile phone subscribers per 100 inhabitants ... 42

Figure 27 Vietnam Internet Subscription ... 43

Figure 28 Internet Service Provider Market share 3/2010 ... 44

Figure 29 Number of POS and ATM ... 45

Figure 31 Mobile Network Operator (MNO) in m-commerce value chain ... 53

Figure 32 VNPT- M-commerce value chain ... 54

Figure 33 VNPT- ―I mode like‖ ecosystem structure ... 55

Table of Contents

摘要 ... I ABSTRACT ... II ACKNOWLEDGEMENT ...III LIST OF TABLE ... IV LIST OF FIGURES ... VI. BACKGROUND AND ISSUES ... 1

1.1 BACKGROUND ... 1

1.2 ISSUES, MOTIVATION AND RESEARCH METHODOLOGY ... 2

II. INDUSTRY OVERVIEW ... 6

2.1 THE 3G MOBILE TECHNOLOGY AND MOBILE COMMERCE TREND IN THE WORLD ... 6

2.2 VIETNAM MOBILE INDUSTRY OVERVIEW ... 9

2.2.1 Vietnam mobile network history ... 9

2.2.2 Vietnam participating the world trend ... 9

III. LITERATURE REVIEW ... 12

3.1 MOBILE COMMERCE ... 12

3.2 MOBILE COMMERCE VALUE CHAIN ... 13

3.3 M-COMMERCE ECOSYSTEM ... 13

3.4 BUSINESS MODELS FOR M-COMMERCE ... 14

IV. BENCHMARK ... 16

4.1 NTTDOCOMO WITH I-MODE ANALYSIS ... 16

4.1.1 NTT Coporation and NTT DoCoMo brief history ... 16

4.1.2 I-Mode Overview ... 17

4.1.2.1. What is I-Mode? ... 17

4.1.2.2. What are i-Mode services?... 19

4.1.2.3. What is I-Mode revenue model? ... 21

4.1.3 Why I-mode? ... 22

4.1.3.1 The saturation of voice service or second S-Curve of growing ... 23

4.1.3.2 Stand out of intensive competition by ecosystem ... 23

4.1.3.4 Content packet- New Services Emerge ... 24

4.1.4 How to build I-Mode? ... 24

4.1.4.1 Identify the roles ... 24

4.1.4.2 Identify the concepts... 25

4.1.4.1 Identify the organization’s structure ... 27

4.1.4.2 Identify the actions ... 28

4.1.5 Why I-Mode successful and lesson learnt? ... 28

4.2 WHY ―I-MODE‖VNPT ANALYSIS –INTERNAL FACTORS ... 29

4.2.1 VNPT brief history of development ... 29

4.2.2 VNPT –Vietnam internet market leader ... 32

4.2.3 VNPT – a big player in Vietnam mobile market ... 33

4.3 WHY ―I-MODE‖VIETNAM ANALYSIS –EXTERNAL FACTORS ... 41

4.3.1 Favor economic and social indicators of Vietnam ... 41

4.3.2 The saturation of voice service but non-data service ... 42

4.3.3 Low wired internet market penetration ... 42

4.3.4 Emerging mobile and banking bond-trend of mobile banking ... 44

4.3.5 Stand out of intensive competition by ecosystem ... 47

4.3.6 Emerging digital content industry ... 47

4.4 VIETNAM AND JAPAN GENERAL COMPARISON ... 48

4.5 VNPT―I-MODE‖ PROPOSAL ... 52

4.4.1 What is I-Mode revenue model ... 52

4.4.2 What are i-Mode services? ... 54

4.6 MANAGERIAL IMPLICATION FOR VNPT ECOSYSTEM ... 57

4.5.1 The role of VNPT in M-commerce value chain ... 57

4.5.2 Revenue model for VNPT ... 57

4.5.3 VNPT supportive model ... 58

V. CONCLUSION AND SUGGESTION ... 59

5.1. CONCLUSIONS ... 59

5.2. RECOMMENDATION FOR FURTHER RESEARCHES... 59

APPENDIX ... 61

AUTOBIOGRAPHY ... 68

1

I.

BACKGROUND AND ISSUES

1.1 Background

In the past, Vietnam's telecommunications market was closed, protected and regulated by Vietnam's government. As a result, Vietnam Post and Telecommunication Corporation (thereinafter called the VNPT) which is a state-owned corporation had controlled the whole market during 1990s. Taking advantage of monopoly position, VNPT as the only-one market player at that time has built a very good brand image. It also acquired a huge capital from profit and as well gained very strong resource capability. Since Vietnam issued market-opening policy in 2002, the telecommunications market in Vietnam has become more open and competitive.

In addition, Vietnam joined in World Trade Organization in the end of 2006. Under the WTO commitment, it has to fully open the Telecommunications market in 2012. Vietnam is obliged to enact a law on telecommunications that follow international practices and integration. It is considered as a step further with implementing the commitment. In this law, Vietnam will also allow foreign owned businesses to buy, transfer telecoms license and provide telecom services. In other words, this telecommunications law allows all businesses freely enter the telecoms market. So far has existed in the Vietnam telecom market many leading international telecoms companies, such as SK Telecom, Motorola, Ericsson, Nokia Siemens, Hutchison, Vimpelcom, AT&T and Cisco. The market is getting hot with the participation of big players in the world. The privatization of some state-owned company also offers a chance for foreign firms to create their early spot in this market.

Along with the movement of market, 3G infrastructure implementation was started in Vietnam at Q4 2009 by three network operators. Two of them are VNPT‘s key subsidiaries, which are Vinaphone and Mobifone. Vietnam Ministry of Information and Communications (thereinafter called the MIC) has strategically decided the technology 3G standard following European WCDMA standard. However, the cost of buying a license and investing infrastructure are about

2

carried out by network operators who won the 3G bidding competition. This huge cost of the license put a burden on network operators such as Vinaphone and Mobilefone.

Coming with new advanced network of 3G mobile, the mobile commerce becomes more visible. It opens both opportunity and challenges for these network operators who are volunteers in this market.

1.2 Issues, motivation and research methodology

When Vietnam fully opens its telecom market, progressive competition is inevitable. Such a situation presents several questions for VNPT to answer quickly and thoroughly since the market gradually opens up to foreign companies such as:

◦ How can VNPT still be a market player in a more intensively competitive mobile commerce market with emerging 3G technology?

◦ Can it follow any lesson from other companies in other countries as example of DoCoMo with i-Mode?

◦ What is the chance for VNPT to build platform or ecosystem for mobile

commerce around its key competence of network operator such as Vinaphone & Mobifone companies?

The purpose of this thesis is

◦ Firstly to study one successful i-mode case in Japan as benchmark for VNPT ◦ Secondly to address issues favoring and challenging to VNPT in Vietnam new

opening market

◦ Thirdly to evaluate the advantage and limitation of VNPT with such scenario ◦ Finally to break down each factor to build up the VNPT‘s ecosystem from its

3 Research methodology:

◦ Conduct investigation the most successful case for developing ecosystem model in Japan (DoCoMo with i-Mode)

◦ Study current situation of VNPT in Vietnam mobile market ◦ Then benchmark VNPT with that ideal case

◦ According to Harvard writing center[1], the thesis will do the benchmarking as a comparative analysis. The process is as followed

◦ Choose frame of reference - It will be: Service and Revenue model in which this research places two companies to compare and contract.

4

◦ Explain grounds for comparison – this thesis will show rationale behind the choice and make argument on difference or similarity between two companies

◦ Follow one organizational scheme: text-by-text, discuss all of DoCoMo with i-Mode, then all of VNPT.

◦ Link VNPT and DoCoMo to build a proposal for VNPT ecosystem like DoCoMo I-mode

Frame of Reference factors

◦ The research will go through all analysis part which was discussed in i-mode case, then places the two things DoCoMo with i-mode and VNPT with future ―i-mode like‖ with an intention to compare and contrast; it is the umbrella under which this research groups them. The frame of reference consists of a group of similar or different things from which investigation extracts for special attention: historical information, capability and technology are alike however economic, social condition in Vietnam and Japan are different. They will lead to two different models of service provided and revenue.

Grounds for Comparison

◦ The ground for comparison is that both VNPT and DoCoMo developed from a government-owned and existed long time in monopoly status. When facing more intensive competition from existing companies and new entrance they need to evolve to adapt with a new situation to stay at top. When comparing services using different technology, the research does not compare the separate technologies that are elements of each; it looks at the service as a final value bringing to users and evaluates. In other words, services will be analyzed in the specific conditions regarding to economic, social and future demand. Hence this research will show how to build them to put together in one proposal for VNPT.

◦ Each characteristic of DoCoMo with i-mode this research will compare and contract with that of VNPT. This research will organize them in ―text by text‖ scheme first discuss DoCoMo with i-mode above then VNPT to help realize the similarity and difference between them in order to construct an appropriate model for VNPT in terms of service

5

and revenue. Following this scheme will help a reader be able to see how logical and systematical in the research argument.

The expecting result of the thesis is to come up with

◦ Critical factors in setting up mobile commerce ecosystem in term of service and Revenue model

◦ Proposal of ecosystem for mobile commerce for VNPT in term of services and revenue model

6

II.

INDUSTRY OVERVIEW

2.1 The 3G mobile technology and mobile commerce trend in the world

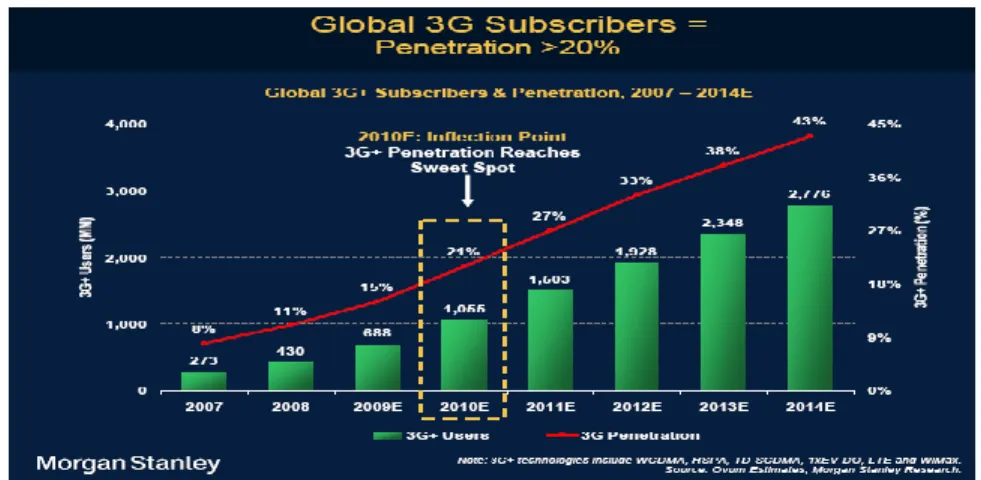

According to Morgan Standley, 3G technology is one of most important factors of infractures encouraging mobile commerce to develeop. In the Mobile Internet Report which Morgan Stanley released on December 15, 2009, the 3G mobile market over the world has recently been developed at a fast pace. This report showed a quick emerging and changing mobile Internet market. If there were only 273 million 3G mobile users three years ago with a growth rate of eight percent per year, last year this figure was 688 million subscriptions and developed with rate to fifteen percent per year. This year is considered the ―sweet spot‖ of the market when the 3G penetration rate reach to twenty one percent, and it is expected with over 1 billion 3G user milestone. In 2014 the world has 2.776 billion 3G users (see figure 1)

Figure 1 Global 3G subscribes

Source: Morgan Stanley Mobile Internet Report Dec, 2009

In this report, Morgan Stanley also drew a more detail the picture of development for several regions and areas. Japan now is the leading country in this technology trend with very high growth of penetration above ninety percent a year. Western Europe and USA are now also at steady growing with more than thirty percent of penetration each year meanwhile Asia and Pacific countries show themselves as the emerging market for thirteen to nineteen percent growth in the next two years.

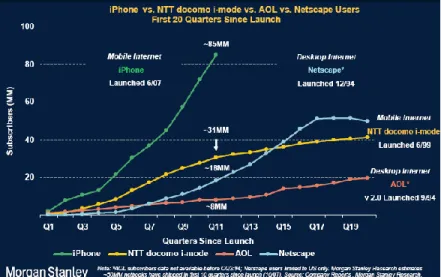

In addition, another recent report of Morgan Stanley reveals that impressive mobile devices equipped with high bandwidth (3G/4G) mobile technology have led much quicker adoption rate of mobile internet via phone(see figure 2) and caused an increased willingness to pay for content.

7

This happens due to it permit users to conveniently participate further in mobile commerce activities such as game, apps, movie, music, GPS, trading and so forth (table 1)

Figure 2 Mobile Internet vs. PC internet adaption rate Source: Morgan Stanley Mobile Internet Report Dec, 2009

Users Are Willing to Pay for Content On Mobile Internet

Users are LESS Willing to Pay for Content On Desktop Internet

Easy-to-Use / Secure Payment Systems – ‗Embedded‘ systems like carrier billing allows real-time payments;

Small Price Tags – Most content / subscriptions carry small price tags

Walled Gardens Reduce Piracy – Content exists in proprietary environments, difficult to get pirated content onto mobile devices

Established Store Fronts – Carrier decks / iTunes store allow easy discovery / purchase

Personalization – More important on mobiles than desktops

Difficult-to-Use / Fragmented Payment Mechanisms That Are More Susceptible to Security Issues – Too many payment options for vendors / consumers + widespread fraud

Often Expensive + Cumbersome to Purchase Legal Content – DRM protection limits usage

Open Internet + Piracy – Most content in digital formats is available for free (newspaper / pictures) or for illegal download (music / video / applications)

Lack of Centralized / Large-Scale Marketplace for Legal Content Discovery / Purchase – Few players beyond iTunes + Amazon.com

Table 1 User‘s buying behavior on mobile internet vs. that on desktop Source: Morgan Stanley Mobile Internet Report Dec, 2009

8

Sine new technologies offer more capabilities, users can utilize on mobile phone, the market for mobile commerce is expected to boom in next few years. According to ABI Research, mobile is going to get a lot bigger in the ecommerce market.

In 2009, ABI Research's report shows mobile commerce tripled in the United States, made up a US$1.2billions market from US$396 million in 2008. In Japan, which has one of the brightest mobile markets, mobile commerce surpassed $10 billion in last year.

Asian consumers are also increasingly using their mobiles for financial transactions, and users are expected to spend $1.6 billion via mobile commerce in 2010. This growth is primarily being driven by SMS, mobile Internet, and mobile application forms of payment. By 2013, more than $12 billion in revenue will be generated through mobile sources. The total value of mobile commerce in the world in 2009 accumulated over 14.4 billion. The research firm is projecting that $119 billion worth of goods and services will be purchased via a mobile phone in 2015.

Another research from Juniper also shows that robust growth of mobile payment transaction value is expected in the next few years. According to an even bolder prediction from Juniper Research, the global m-commerce market will reach an almost US$300 billion industry by 2013. Juniper also believes digital goods such as mobile entertainment – ringtones, games, wallpaper, gambling – will continue to be the largest application for trading via the mobile phone, but that ticket purchases will also emerge as a major application area by 2007, and make up over 44% of global m-commerce market next year.

Figure 3 World mobile payment transaction value Source: Juniper research 2009

9

2.2 Vietnam mobile industry overview

2.2.1 Vietnam mobile network historyVietnam mobile market was established in 1994 when Vietnam Post and Telecommunication Corporations (VNPT) unit- VMC signed one US$324 million business cooperation contract (BCC) with Sweden's telco Comvik International to form Mobilphone Company. BCC is a form of benefit-sharing concession that enables restricted market entry for a fixed period of time. The second VNPT‘s subsidiary – Vinaphone came into operation in 1999.

During 1995–2003, the mobile telecoms services sector had only one state-owned telecoms company firm—Vietnam Post and Telecommunications Corporation (VNPT). Vietnam signed a Bilateral Trade Agreement with the US in 2001 considered as major step for Vietnam joining to WTO five years later. This step also puts transition stage for private ownership of telecoms network and services. Foreign investment at transitional phase could change to joint venture form.

In 2003, another competitor (S-Phone) entered the market in the form of a BCC between Vietnamese companies Hanoi Telecom with a Korean partner(SK-Telecom). Local competition was more significant also in this year when two stated-owned companies directed by the electrical utility sector (EVN) and military (Viettel) received the licenses to compete with national monopoly VNPT.

Before Vietnam‗s WTO accession in late 2006, Foreign firms can only own up to 49% of the shares in Vietnamese telecoms firms and this limit will gradually rise to 51% by 2007 and up to 65% by 2010. Ministry of Information and Communications (MIC) reformed mobile market by setting up the pricing control regulations in 2002. In addition, Vietnam will pass The Telecom Law in July 1, 2010 to carry out its commitments to the WTO. Under this law foreign investor can run business with partner‘s license, buy, and sale shares in telecommunication firm or increase the share-owned percentage in local company.

2.2.2 Vietnam participating the world trend

On February 18, 2009, Vietnam Ministry of Information and Communication (MIC) received 3G applications from seven mobile telecom companies. After two months of reviewing all

10

application, MIC awarded four Vietnamese mobile firms for 3G licenses including: Vinaphone, Mobifone, Viettel and EVN Telecom.

Vinaphone, and MobiFone, both run by state-owned telecoms group VNPT, the military-owned Viettel, the joint venture EVN Telecom (state electricity owned) and Hanoi Telecom (Hutchison joint venture firm) have pledged to invest nearly US$2 billion within the next three years to develop 3G infrastructure. All are secured 15-year licenses

In November 2009, Vinaphone already run the 3G network while Mobifone and Vietel launched their network at the beginning of year 2010. The EVN Telecom and Hanoi Telecom expect to come out soon in mid 2010.

From statistic data of Information and Communications (MIC), Vietnam in Q1 2009 is one country whose penetration level is more than 80% with 72.3 million mobile users. This current figure will increase dramatically to total 120 million by 2014 in Pyramid Research Projection.

Figure 4 Largest Asia Pacific mobile markets, Q1 2009 (millions) Source: Ministry of Information and Communications (MIC)

Pyramid Research one company study about Vietnam mobile market forecast that there will be 43 million 3G subscribers by 2014, or 36% of total subscriptions at that time.

Vinaphone - Vietnam‘s second largest mobile operator came first as one telecoms firm launching the 3G network at the end of 2009. The upgrade phase, which took just two months, enabled Vinaphone to launch the country‘s first mobile broadband services.

11

In the end of year 2009, the 3G network first covers important spots in the country; such as big cities and commercial areas. The final phase will be finished in 2020 with 98% coverage of all country in 2020. First phase will be introduced with basic 3G services such as video call, music download then advances services will come later from the second phase such as mobile banking, mobile TV in this year.

Figure 5 Vinaphone - Road map for implementation 3G network Source: Ministry of Information and Communications (MIC)

Vinaphone expects that the development will differentiate its services in Vietnam‘s dynamic mobile market as demand for mobile data services grows fast.

Based on 3G infrastructure, according to KPMG Singapore, Vietnam is now showing strong adoption in a few areas such as top-up and gaming, but a slightly hesitated adoption in the more traditional areas of m-banking[2].

Along with this trend, there also exists a new fast growing digital content industry along with software industry in Vietnam in recent years

0% 20% 40% 60% 80% 100% 2005 2006 2007 2008 2009 198 283 498 680 880 110 180 440 700 R e ve nue ($U S m iil lion) Year Software Content

Figure 6 Vietnam software and digital content industry revenue Source: Ministry of Information and Communications (MIC)

12

III. LITERATURE REVIEW

3.1 Mobile Commerce

The early description of mobile commerce was first pointed out by Muller Veerse in 1999[3]. In his explanation, mobile commerce is a subset of electronic commerce, and any transaction made via mobile communication network or involved with monetary values is regard as mobile commerce. In later years, Tsalgatidou and Veijalainen[4], Clarke[5], and Barnes[6] approached with a perspective of transactions. They considered any kind and economic values transactions managed through at least one kind of mobile terminal equipments on the mobile network, as a part of mobile commerce. In 2001, Mackintosh[7] and Kannan et al[8] referred mobile commerce as an extension of electronic commerce on the Internet. Mylonopoulos and Doukidis had a systematic definition in 2003. It refers to an interactive ecology system of corporations and individuals, and this ecology system is built on the social economic background and various previous technologies [9].

The mobile market has seen significant growth in the past few years. Global m-commerce revenues expected to $88 billion by the end of 2009. It enables a new opportunity for the growth of m-commerce. M-commerce is attractive for research because of its relative rapid growth, and prospective applications [10]. According to Varshney and Vetter, M-commerce covers a broad applications[11]. There are twelve m-commerce applications identified and classified. Naming several important categories of m-commerce applications are mobile financial applications, mobile advertising, mobile inventory management, locating and shopping for products, proactive service management, wireless re-engineering, mobile auctions or reverse auctions, mobile entertainment services and games, mobile offices, mobile distance education, and wireless data centers. They then explained detail for each application and networking requirement. This gave systematic approach for those who want to develop mobile commerce application based on mobile network.

13

3.2 Mobile commerce value chain

In 1985, Michael Porter defined value chain as the linkage and integration of a series of activities in which enterprises deliver the created and valued products or services to customers[12]. He also indicated that the value chain of any company is included in a lager value hierarchy. This value system is created from the value chains between the many firms from its upstream to its downstream organizations. In this perspective, value chain concept both is analyzed in term of the enterprise‘s internal value activities, and the external entire industry to compare the cost with competitors. Mobile commerce comprises products and services. According to Barnes [6] in 2002, the practice of adding values to the ultimate users also relates many possible members, largely including bank, mobile network operator, customer, and other value providers [13]. This process of value creating activities both draws in more members such as content supplier and mobile service suppliers, enabling them an opportunity to join in the activities and also changes the value system of the traditional mobile communication [4]. When the new technologies came out such as 3G technology with new services offering, the number of providers is increasing. As Ying-Feng Kuo and Ching-Wen Yu classified in 2005[14] there are total of 11 identities involving mobile commerce value chain such as Technology platform vendors; Infrastructure and mobile equipment vendors; Infrastructure and mobile equipment vendors; Application developers; Content developers; Content aggregators; Mobile portal providers; 3G mobile network operators; Mobile service providers; Mobile equipment retailers; Customers. While each of them has own role, responsibility and value adding to the whole value chain they could merge with each other to be a bigger identity which has more capabilities. In the value chain, network operator has several advantages over the peer providers. They can act the any role in value chain so they also could fit in several types of business model.

3.3 M-Commerce ecosystem

In nature, an ecosystem consists of a world of plans and animal – herbivores, carnivores, insects and plants of all kind which are in balance. In 2003, Takeshi Natsuno defined ecosystem model includes mobile phone manufactures, content providers, carriers such as DoCoMo, server manufacturers, customers coexist, compete and prosper together[15]. M-commerce services require real-time delivery or service quality, security, location management, transactions support,

14

and wireless network reliability. Wireless LANs (WLANs), cellular networks, and satellite-based networks can support one or multi m-commerce services such as mobile auctions, interactive game, mobile finance service, mobile advertising, mobile entertainment services, proactive service management, and mobile inventory management[16]. Content of the service is made and integrated by one or many providers among Technology platform vendors; Infrastructure and mobile equipment vendors; Infrastructure and mobile equipment vendors; Application developers; Content developers; Content aggregators; Mobile portal providers; 3G mobile network operators; Mobile service providers; Mobile equipment retailers in the M-Mobile value chain. All coexist and cooperate base on mobile networks infrastructure creating M-commerce ecosystem.

3.4 Business models for M-Commerce

In the past few years, some interesting case of mobile commerce was conducted. Xianjun Geng and Andrew B. Whinston in 2001 pointed out that network operator could gain benefit from usage-based pricing or prepaid flat-rate plans[17]. In 2002 Mitsuru Kodama studied the market expansion and global strategy of DoCoMo [18]. He pointed out that one factor helped DoCoMo and i-Mode successful was building up ―portal community‖. It gives users ―one stop shop for all‖. DoCoMo took advantage as dominated player in supply chain creating and enforcing an exclusive group of service providers. With this power Japan‘ DoCoMo had built profound ecosystem for its 48 million customers around i-Mode. Users pay in usage-based. On the contrary, Vodafone[19] does not control third-party providers that its customers can access. News services and content are included in Vodafone‘s subscription charge for second-generation (2G) to 3G services. It offers flat rates for data services and event-based or per-minute charges for games, live TV and concerts. South Korea (SK) Telecom‘s created one business model to charge a fixed monthly subscription rate (around US$6) for voice, data, and SMS services. In 2008, still from control rights point of view, Upkar Varshney sum up two kind of business model for network operators [16]. They are centric business model and managed one. Their differentiation is the way network operation controlling network access and content like DoCoMo. In centric approach operators strictly take over both but in managed way they let user free to choose content

15

providers such as Vodafone. Decision upon each way also setup benefit sharing mechanism among partners. He finally came up with a hybrid model of these two.

Model Attributes Example

Centric Business Model

Network operators control both network access and content creating

and enforcing an exclusive set of service providers then redistributing benefit along partners

DoCoMo

Managed model Network operators control network access only let users free to access to third parties for content

Vodafone

Hybrid model The control right of network operators could vary depending on its capabilities and market power

Table 2 Business model for mobile network commerce

Source: U. Varshney, "Business Models for Mobile Commerce Services: Requirements, Design, and the Future," IT Professional, vol. Vol. 10, No. 6., pp. 48-55., 2008.

16

IV. BENCHMARK

4.1 NTT DoCoMo with I-mode analysis

4.1.1 NTT Coporation and NTT DoCoMo brief history

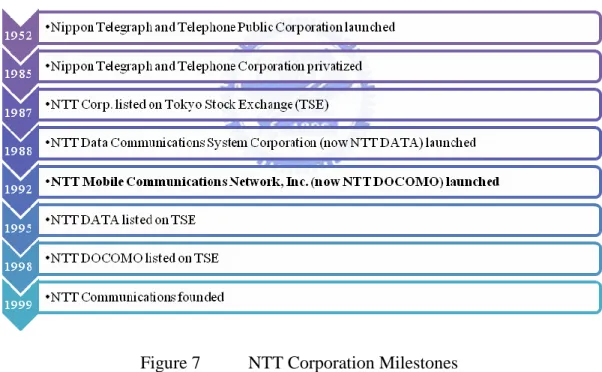

Nippon Telegraph & Telephone Corporation (NTT Corp) was originated in 1869 when the telegraph was first introduced in Japan. NTT used to be a monopoly government-owned. In 1985 TT was privatized. After that it have formed new subsidiaries, invested heavily and developed cutting-edge technologies. In 2009, NTT Corp. is a worldwide brand name ranked 44th in Fortune's Global 500. It has operating revenues of more than $103,684.4 million with 196,300 employees worldwide. Following are some millstones of NTT Corp

Figure 7 NTT Corporation Milestones Source: NTT website

The NTT Group led by NTT Corporation includes five major subgroups, (see figure 8) NTT Communications (Global data, IP, Voice and IT)

NTT East (local carrier) NTT West (local carrier)

NTT DOCOMO (mobile carrier) NTT Data (systems integration)

17

Figure 8 Details of NTT Group Source: NTT website

NTT DoCoMo (or DoCoMo hereinafter) is subsidiary of NTT Group. It was established in July 1992 when NTT Mobile Communications Network, Inc took over NTT Corp's mobile communications business. NTT DoCoMo focuses mainly mobile phone services. ,

4.1.2 I-Mode Overview

4.1.2.1. What is I-Mode?

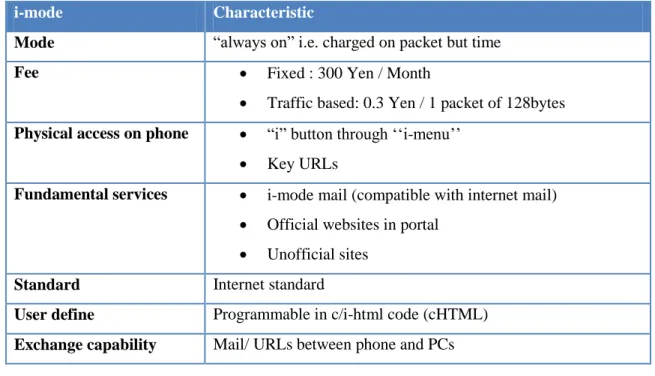

Back to January 1997, recognizing that future of wireless network lays on non-voice data, Koji Oboshi, president of DoCoMo charged Keiichi Enoki with setting up a new organization that would concentrate on non-voice communications for retail consumers. Named as Gateway Business, it was working on a new service, called i-mode. I-mode would offer a mobile Internet service to customers over their mobile phones. It was considered as an ecosystem for mobile Internet services including browsing, downloading, e-mail, and other applications. By the middle of 2001, i-mode had comprised around 20 million users approximately 20 per cent of the total Japanese population. In 2001, DOCOMO also introduced i-Mode on FOMA™, the world's first 3G commercial mobile service based on W-CDMA. It made the NTT DOCOMO more significant global brand. In 2001, DoCoMo also became the most widely used mobile Internet service in the world. Up to 2010 there are over 48 million subscribers using i-mode. It rapidly grew up and expanded into many services from the initial. The brief i-mode descriptions are listed in table 3 and milestones for i-mode history of development are followed, see figure 9.

18

i-mode Characteristic

Mode ―always on‖ i.e. charged on packet but time Fee Fixed : 300 Yen / Month

Traffic based: 0.3 Yen / 1 packet of 128bytes

Physical access on phone ―i‖ button through ‗‗i-menu‘‘

Key URLs

Fundamental services i-mode mail (compatible with internet mail)

Official websites in portal

Unofficial sites

Standard Internet standard

User define Programmable in c/i-html code (cHTML)

Exchange capability Mail/ URLs between phone and PCs

Table 3 i-mode main characteristic Source: T. Natsuno, "i-Mode Strategy," 2003

Figure 9 i-mode Timeline Source: NTT DoCoMo Website

19

The significance of i-mode is the way offering ―always-on‖ functionality. This allows users to keep their devices on but pay only for actual traffic because of the capacity of packet network[10]. Exchangeable data between phone and PCs also provides convenience for users. In one step DoCoMo at that time could make a mobile as pocket PC in narrow sense.

Customers use i-mode through the network carrier (DoCoMo) to access content provided by official or unofficial providers. Content providers provide content in form of data or application to users also via DoCoMo network. The process is depicted in Figure 11

Figure 10 i-mode network Source: T. Natsuno, "i-Mode Strategy," 2003

4.1.2.2. What are i-Mode services?

From i-menu of i-mode are provided numerous services to customer. Even though i-mode menu is in Japanese however users can also access content provided by content provider through English interface. Summary of i-mode service are listed in the table below

20

Service Launched Remark Description

i-mode 02/1999 mobile data

service

Mail and Information retrieve

i-appli 01/2000 i-mode with Java The software (programs) to automatically update weather forecast

displays, news and to play new games as well

i-area 07/ 2001 Location Based

Service

Application helps the user to check the traffic and store information, other convenient information and the weather forecast for local areas, as well as the map information to the user's current location

i-motion

10/ 2001 Dynamic Video

Content

This function related to video distribution programs for i-mode mobile phone terminals and the contents. The high-speed communication service of FOMA (3G) offers customers with the latest movie theater information and details of the sports highlights available in video

i-shot 06/ 2002 Digital Camera

Capability

A feature that provides transfer of still images captured with an i-mode compatible phone. The images could also be sent to phones of other carriers or PCs

i-motion mail 01/ 2003 Video captured

via email

This service transfers video captured with an i-motion compatible mobile phone via e-mail. It features a transmission speed of up to 15 frames/sec, thus permitting smooth motion video to be enjoyed with a mobile phone

"Osaifu-Keitai"

07/ 2004 wallet functions "Osaifu-Keitai" refers to mobile phones equipped with contactless IC

card, as well as its useful function/services enabled by the IC card. With this function, mobile phones can be utilized as electronic money, credit card, electronic ticket, membership card, airline ticket, and more

i-channel 09/ 2005 News and related This service distributes the latest news, weather forecasts and other

information to i-channel compatible i-mode phones. The information is displayed on a standby screen without any special operation and users can access to more detailed information with a press of a button

"ToruCa" 10/ 2005 info-capture

function

The ToruCa service enables users to capture information into their mobile phone with ease, using the mobile phones various interfaces (FeliCa, Mailer, and Infrared etc.). With the captured information you can perform an in-phone search, manage contents simply and easily with the sort function and exchange information hassle free with fellow ToruCa compatible mobile phones. Also, by pushing the "Details button", even more detailed information could be captured

Table 4 i-Mode services Source: NTT website

21

4.1.2.3. What is I-Mode revenue model?

Upkar Varshney classed the DoCoMo with i-Mode revenue model into the centric business model. The network operator (DoCoMo) controls both network access and content. It initiated and welcomed an exclusive set of service providers to join then redistributed benefit along partners [16]. In other words, the business model DoCoMo build on i-mode can be named as a supportive business model in which company shares high revenue with for official content providers [20]. The points of revenue model and benefit sharing mechanism

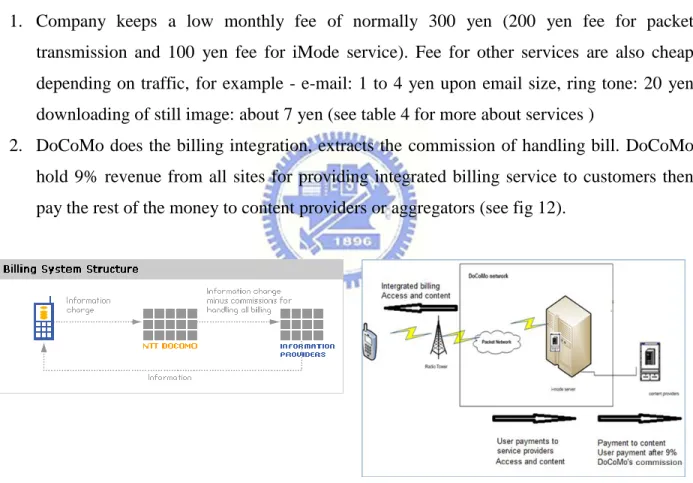

1. Company keeps a low monthly fee of normally 300 yen (200 yen fee for packet transmission and 100 yen fee for iMode service). Fee for other services are also cheap depending on traffic, for example - e-mail: 1 to 4 yen upon email size, ring tone: 20 yen downloading of still image: about 7 yen (see table 4 for more about services )

2. DoCoMo does the billing integration, extracts the commission of handling bill. DoCoMo hold 9% revenue from all sites for providing integrated billing service to customers then pay the rest of the money to content providers or aggregators (see fig 12).

Figure 11 DoCoMo‘s billing structure and revenue sharing machanism Source: NTT DoCoMo

22

Table 5 i-mode service fee Source: T. Natsuno, "i-Mode Strategy," 2003

4.1.3 Why I-mode?

I-mode came to reality because of combination of many factors but there were some strategic points they are combined and listed here:

23

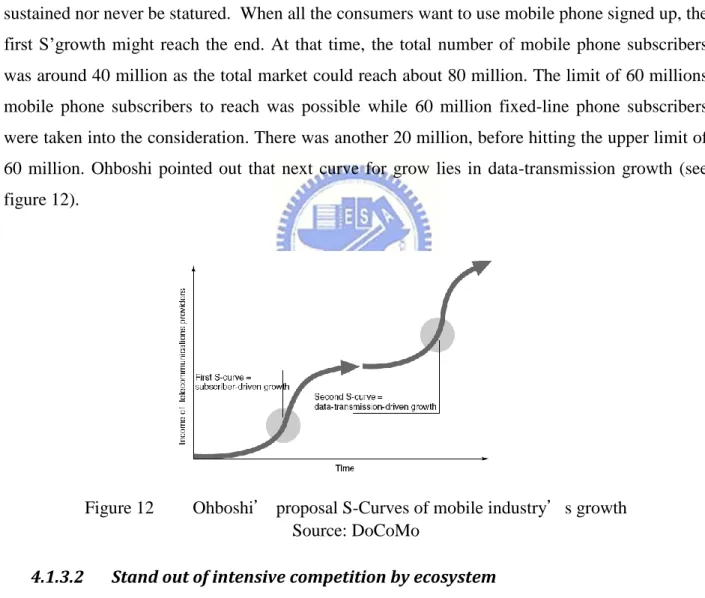

4.1.3.1 The saturation of voice service or second S-Curve of growing

When CEO of DoCoMo was initiating i-mode project, he had realized that DoCoMo‘s growth curve might be moving into ―a second S-curve‖ and proposed the a management policy forward to ‗Shifting from Volume to Value‘. At that time, Ohboshi already knew market well when he predicted the sign for first S-curve started when the number of subscribers began soaring. There was a first time in telecommunications industry history three years in row; mobile phone industry acquired 10 million new subscribers per year from 1996 to 1998. However it was not either sustained nor never be statured. When all the consumers want to use mobile phone signed up, the first S‘growth might reach the end. At that time, the total number of mobile phone subscribers was around 40 million as the total market could reach about 80 million. The limit of 60 millions mobile phone subscribers to reach was possible while 60 million fixed-line phone subscribers were taken into the consideration. There was another 20 million, before hitting the upper limit of 60 million. Ohboshi pointed out that next curve for grow lies in data-transmission growth (see figure 12).

Figure 12 Ohboshi’ proposal S-Curves of mobile industry’s growth Source: DoCoMo

4.1.3.2 Stand out of intensive competition by ecosystem

Before the existence of i-mode, there was a severe competition between big market players as KDDI, J-Phone and DoCoMo and a threat of big comer like Motorola. Even though DoCoMo dominated market and have great market power in whole supply chain it also saw the need of distinguished characteristic to stand out from crowd and remained at the peak. Using its power to

24

build i-Mode ecosystem was very smart strategic move of DoCoMo ahead its strong completion. Hence its market share bounded back in years after launched i-Mode, each month it hits around 80%

4.1.3.3 Text or e-mail culture emerges

In 1996, young Japanese people liked send text from mobile phone to pager. This is one way communication but not the way around. PHS (Personal Handyphone) came to exist in 1997 allowing people to send text between mobile phone but within same provider‘s system or PHS system, in other words it was still a closed system. Open system (i-mode) for sending email or message between mobile phones or between phone and PCs which was not limited in the same providers‘ network had chance for bringing into existence.

4.1.3.4 Content packet- New Services Emerge

Everyone likes the abundance or pool of information on internet but people confused about how good source of information is and which mean to access it. In Japan, PCs and Internet use are not yet as common but everyone has a mobile phone. That gave DoCoMo a considerably large base of users and an untapped market. In addition, the idea bring internet content such as email, website, finance, navigation to mobile phone was a new approach to bolster for i-mode idea. There was a need of one initiation step as i-mode ground, so then came to the mobile phone for many internet based contents.

4.1.4 How to build I-Mode?

4.1.4.1 Identify the roles

In order to build i-Mode and execute the centric business model as mentioned above some conditions DoCoMo must meet. The key steps and elements for building I-mode ecosystem would be also addressed as basis for the benchmark.

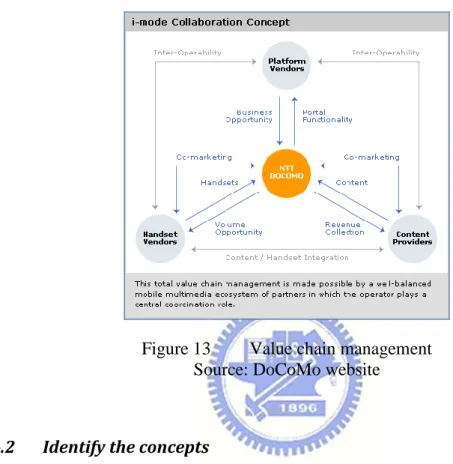

DoCoMo plays a central role in value chain. It cooperate closely with equipment manufacturers, content providers, and other platforms to guarantee that wireless technology, content quality, and

25

user experience evolve jointly. This synchronization ensures that customers, partners and shareholders share interests with end-user's, thus enabling all parties to maximize value and to continue to improve the quality of products and services connected with i-mode.

Figure 13 Value chain management Source: DoCoMo website

4.1.4.2 Identify the concepts

Becoming a coordinator for a system as a whole, DoCoMo try to fulfill four concepts to build one complex system as i-mode (see Table 6). DoCoMo had to carefully plan steps and chose right approach to take into action all concept and vision, which helped i-mode got off the ground and avoid the negative feedback loop. It designed the content portfolio and picked the stimulus to attract users to those. In the i-mode content portfolio, all content is divided into four categories (see summary in Table 6, 7 & figure 15)

26

Concept Definition

Positive feedback A virtual circle of subscribers, service providers and new development i.e. increase in subscribers leads more service

providers to take part in, which then appeals more subscribers and thus generates new positive development

Increasing returns Positive feedback will lead one side in a competitive relationship obtain an overwhelming victory

Emergence Emergence is evolution at the level of individual components which create new technologies and methodologies

Self-organization Evolution of the organization as a whole

Table 6 Core concept of complex system Source: ―i-Mode Strategy" book - 2003.

Category Characteristic Requirement

Information Time-sensitive information – news and weather Freshness

Depth

Continuity

Clear benefit Kee

p th e p o sitiv e fee d b ac k g o in g

e-commerce Banking, securities transactions, and ticket reservations

Databases Restaurant guides, dictionaries and other information, available in database form

Entertainment Fun

Table 7 i-mode content portfolio characteristic and requirement Source: T. Natsuno, "i-Mode Strategy," 2003

27

Figure 14 The i-mode content portfolio Source: T. Natsuno, "i-Mode Strategy," 2003

4.1.4.1 Identify the organization’s structure

In detail, to execute and follow the strategic concept of value chain as above , Gateway division in DoCoMo organized the structure to execute and follow the strategic concept of value chain (see figure 15).

‘ Figure 15 Organization structure

Source: DoCoMo website

Int er na l a nd ext er na l W in -W in re lat io n sh ip

28

4.1.4.2 Identify the actions

From viewpoint of roles and relationship between DoCoMo and other identities in Value chain management DoCoMo had done some courses of action (see figure 16)

Figure 16 Actions in building i-mode

First, it selected right technologies or De Facto Standard such as cHTML(compact HTML) which is a subset of HTML, a common language on internet as the language for i-mode sites. Even it was considered less efficient for wireless than WAP(Europe) or WML(USA) but its commonness required minor effort from partners which welcomed more partners.

Second it build centric but supportive business model in which DoCoMO processes the billing system, handles the hard word of collecting money while letting partners focus on their job that encourages more outside associates. In other words, DoCoMo was in charge of tedious job but charge a small portion of money (9% for commission) that motivate partners come even from the scratch(see appendix 3)

Third, it marketed i-mode services as service bringing convenient for customer rather than technology which build on. It became more easily understood and engaged.

4.1.5 Why I-Mode successful and lesson learnt?

In this part this research will sum up key factors which contribute to the success of DoCoMo‘s ecosystem i-Mode which might focuses on service offered and business model point of view regarding to all research findings in the past. It will later lead to the framework to benchmark VNPT

29

Low fees of content and data [20],[21],[22], [23], [24]

Services offered not only for business customer but for the wide-ranging population, in particular youth and women (e.g., entertainment) [21], [25], [24].

Content provided by companies rather than the operator, welcome for unofficial sites[20, 21, 23],[24], [25], DoCoMo did not compete with content provider but motivated

competition between content providers [26]

Harmony of the whole value chain, with ease of use, and appropriate handsets [21] [25]. Appropriate and supportive business model, i.e. with high revenue shares for official

content providers [16],[20].

Service not marketed as ―internet‖ [20], [24], [27]

Domination of operator over equipment manufacturers[20], [24], [26],[28]

The next part, the research will follow the same pattern of DoCoMo with i-mode analysis:

Firstly, take a glance at VNPT development with emphasis on area of its growth favoring to build an i-mode like ecosystem. It includes all VNPT‘s internal factors toward M-Commerce.

Secondly, explore the Vietnam mobile market to see whether the current status of VNPT especially its two subsidiaries in that market favor for building M-Commerce or not. It comprises VNPT‘s external factors toward M-Commerce in term of market position. Lastly, examine other external favor factors for setting up M-Commerce system such as

Vietnam technology trend, social economic to have a complete look the chances of VNPT‘s internal factors toward M-Commerce

4.2 Why “I-mode” VNPT analysis – Internal factors

4.2.1 VNPT brief history of developmentVietnam Post and Telecommunications Corp (VNPT) – is the state-owned cooperation. It comprise of many sub companies and resources. According to General Statistics Office of

30

Vietnam, VNPT contributed $USD 1.53 billion accounting for 75% of National telecoms revenue contribute to GDP during the first 6 months of 2009.

Establish and restructured from Vietnam Posts and Telecommunications Corporation on January 9, 2006 - VNPT Group has a vision in diversified of posts, IT and telecommunications market. Acquiring great capital and resource when being only monopoly-dominated, state-owned corporation in the past, VNPT now have to gather together all economic sectors to joint its process of development with a mixed ownership structure and flexible business model in order to achieve its vision. Here are some milestones of VNPT development.

Figure 17 VNPT landmark

Source: VNPT website

VNPT's organizational structure includes (see figure 18) 4 units of management and corporate executive 39 subsidiary units

31 Associated companies

The VNPT group combines systematically supportive companies ranging from service, manufacture, banking, finance units to invest, strategic ones. This corporation owns company running national and international business level such as Vietnam Telecom National (VTN) and Vietnam Telecom International (VTI). It has almost components in hand to build ecosystem for mobile commerce

Internet infrastructure provider such as Vietnam Data communications Company (VDC) Media & software Development (VASC), Optical companies

Mobile network providers such as Mobifone and Vinaphone Hospital, education Institute

Consulting, finance companies

Telecommunications equipments, contractions companies and other joint venture companies etc

(Full key subsidiaries and their characteristic see appendix 2 for more detail)

Figure 18 VNPT Group structure Source VNPT website

32

With its state-owned monopoly position VNPT has involved and grown its power in many Information & Communications Technology (ICT) sectors in Vietnam. Following part will examined its evolvements

4.2.2 VNPT –Vietnam internet market leader

From 1997 when internet came to exist in Vietnam, Vietnam had only four Internet service provider VNPT, FPT, SPT and Netnam. Up to now Vietnam has 16 ISP, however taking lead in developing internet in Vietnam, VNPT is always the leader of internet infrastructure and internet service provider. It booted the number of internet user from 300 people in 1997 to 21.430.463 in QI 2010. VNPT has increased market share and hold three quarter of Vietnam internet market after 13 year development from 1997.

Figure 19 Internet market share of VNPT Source: Ministry of Information and Communications (MIC)

VNPT has connected the biggest regional and international optical fiber cable links, joining Vietnam to 240 countries worldwide. Via the T-V-H, CSC, SEA-ME-WE3 and satellite links connected directly to 37 countries with over 5,000 communications circuits, the outgoing international traffic capacity has exceeded 800 Mbps.

33

In order to be the dominator in Internet domain, VNPT have an advantage when running two VNPT‘s key sub companies are

- Vietnam Data communications Company (VDC) - Media & software Development (VASC)

VDC VASC

Functions ISP/IAP Software, Internet

Solutions

Mobile Telecommunications Software/Solution

Service/Product - MegaVNN (ADSL)

- VNN / Internet Leased Line - VNN/VPN-MPLS - Frame Relay - iFone-VNN -Telehosting (Dedicated, Colocation, VPS) - Webhosting - Mail SMD - Mail Offline

- Sofware solutions for enterprises

- Online services

- Solution Consulting….

- Services on mobile networks - Internet Services - TV on mobile - Software solutions - Media Services - License business - VOIP Services - Other Services

Market share 75% market share of ISP 60% market of value added services on telecommunication network

Figure 20 Two key VNPT’s internet companies

Source: Ministry of Information and Communications (MIC) & VNPT

4.2.3 VNPT – a big player in Vietnam mobile market

In this part, this research creates a glance at Vietnam mobile market, and then thoroughly analyzes the current competition in that market in order to pinpoint advantage as well as

34

disadvantage of VNPT. A brief of related Vietnam’s conditions will be covered such as the technology, social economic situations in Vietnam. All factors are used as the ground for the proposal of services and revenue model for VNPT

In the end of 2009, Vietnam mobile market has total seven mobile telecom service providers. Among them there are five 3G service providers with four 3G licenses granted as shown in the table 8. The significantly high mobile penetration rate in Vietnam has built up the subscriber growth over recent years. At the middle of 2008, with a penetration level of around 76% of the population there were about 66.3 million mobile subscribers in Vietnam. However the number of mobile subscriptions in the country has been surpassed the Vietnam population of 86 million at the end of 2009 by reaching 94 million. According to Vietnam Ministry of Information and Communications (MIC) the real number of people using mobile phone is around 70 to 76 millions. In other words, the number of users needs to serve left around 10 to 16 millions in 2010 Announcing plan of acquiring new mobile subscriptions for three big players- Viettel, Mobifone, Vinaphone this year will archive more 18 million users. It means that in 2010 Vietam mobile market will go to the saturated status.

Company name (Commercial brand) Characteristic Owned Network Viettel Military-based 2G/3G Mobifone VNPT‘s subsidiary 2G/3G Vinaphone 2G/3G

EVN Telecom (E-mobile) State-owned utility Electricity of Vietnam 3G Hanoi Telecom(Vietmobile) Associated with Hong Kong's Hutchison

STelecom(Sphone) joint venture between SPT with Korean SK Telecom 2G/2.5G Gtel Mobile (Beeline) Russia's VimpelCom owned 2G

Table 8 Vietnam mobile companies

Source: Ministry of Information and Communications (MIC)

High growth rate of mobile using from beginning up to now is mainly encouraged by three first comers such as Viettel Vinaphone and Mobilfone (see table 9).

35 Network(Company) 2006 2007 2008 2009 QI 2010 Mobifone (VNPT) 6,272,303 14,951,304 21,712,970 12,320,000 29,186,824 Vinaphone (VNPT) 7,500,315 13,104,908 21,188,864 32,148,000 27,784,841 Viettel Telecom 4,307,485 12,159,193 26,130,436 37,299,200 39,188,264 S-Fone (S-Telecom) 812,377 3,782,860 4,866,700 4,705,000 10,150,433 Vietnamobile (Hutchison) 225,170 598,978 940,000 3,336,272 E-Mobile (EVNTelecom) 810,613 973,340 1,052,800 1,389,880 Beeline (GTEL-Mobile) 5,640,201 1,244,383 Total mobile subscriptions 18,892,480 45,034,048 74,872,310 94,105,201 112,280,897

Table 9 Mobile subscriptions of Vietnam mobile companies Source: Ministry of Information and Communications (MIC)

Even though there are new entrants in recent years, Viettel (military-owned) and 2 VNPT’s subsidiaries Vinaphone and Mobifone still control around 90% market share. VNPT always dominate and control over 50% of this market.

Figure 21 Vietnam‘s mobile share market change over years Source: MIC, VNGOS

36

To have insight of current situation of Vietnam mobile market this part of research will analyze mobile competition and mobile competitors in Vietnam. The analysis of ongoing competition will lie in seven domains which try to follow the frame work of ―Seven Rs Rule‖ in supply chain strategies: having the Right product, in the Right quantity, in the Right condition, at the Right place, at the Right time, for the Right customer, at the Right cost[29]. Some of them could overlap when examined but they can be accordingly arranged as below

Seven Rs Rule Analysis domain

Right product Competition in Brand

Right quantity Competition in Customer Care

Competition in Quality of Service (QoS) Right condition

Right place Competition in Distribution Right time Competition in Time

Right customer Competition in Customer Attraction Right cost Competition in Price

The Vietnam mobile market has its own characteristic due to low household income, slow fixed phone penetrate and pre-WTO closed and monopoly market therefore to draw out the complete picture of competition some elements will be combine to analyze together to see the connection and linkage in the next part.

The recent distinguished 5th Vietnam Mobile Award sponsored by the Ministry of Information and Communications in 2009 announced results for network operators as below.

The operator with the most popular brand recognition system: Viettel The operator with the most attractive service package: Beeline The most favorite mobile network: MobiFone

The operator with the best customer care service: MobiFone The operator with the most potential 3G services: Vinaphone

It will be addressed as a starting point to discuss further the current situation in Vietnam mobile market

37

In Vietnam mobile market: Right product to Right customer at Right cost or Completion in Brand to Attract Customer at Appropriate Price – Big gain for Viettel as well the later comers but great consequences

When the third network operators Viettel have not existed in market before 2003, the whole market was served by two subsidiaries of VNPT. Mobilfone and Vinaphone. The high demand was a simple voice service with no competitors which let Mobifone and Vinaphone enjoy the monopoly status. They so charged high price for whole market and focus only considerablely benefit customers. Viettel saw market potential then came to exist in 2003. Being a new entrance, it targeted to low income user such as student, farmer and countryside resident while Mobifone focused on high income one and Vinaphone aimed middle and urban habitants. As a result after three year, Viettel was quickly noticed and surpassed both VNPT‘s subsidiaries in term of mobile subscriptions in 2006. It gradually acquired more market share as shown in figure 19 above. Viettel are so successful in identifying potential demand for mobile services of very large customer segments from low-income level which account for the majority of Vietnam population. Knowing exact needs of the market is the source for success in the development of Viettel. It can establish the number one position on the market today and its subscriber number grew quickly.

Figure 22 Mobile market share QI/2010