國立臺灣大學管理學院資訊管理研究所 碩士論文

Department of Information Management College of Management

National Taiwan University Master Thesis

不完整資訊下動態頻寬交易之最佳定價方法 Optimal Pricing for Dynamic Bandwidth Trading with

Incomplete Information

呂明龍 Ming-Lung Lu

指導教授﹕孫雅麗 博士 Advisor: Yeali S. Sun, Ph.D

中華民國 一百 年 八 月

August, 2011

不完整資訊下動態頻寬交易之最佳定價方法 Optimal Pricing for Dynamic Bandwidth Trading with

Incomplete Information

本 論 文 係 提 交 國 立 台 灣 大 學 資 訊 管 理 學 研 究 所 作 為 完 成 碩 士

學 位 所 需 條 件 之 一 部 份

研 究 生 : 呂 明 龍 撰 中 華 民 國 一 百 年 八 月

國立臺灣大學碩士學位論文

I

謝 詞

本 論 文 得 以 順 利 完 成 , 首 先 要 感 謝 恩 師 孫 雅 麗 教 授 。 在 論 文 的 撰 寫 中 , 老 師 不 斷 的 強 調 要 寫 出 讓 讀 者 都 能 看 得 懂 的 論 文 , 訓 練 我 將 腦 袋 中 想 法 轉 化 為 文 字 的 能 力 , 在 這 學 習 過 程 中 , 我 學 到 了 該 如 何 以 讀 者 的 角 度 來 看 待 論 文 的 不 足 之 處 , 這 讓 我 的 論 文 更 加 具 有 可 讀 性 。 同 時 老 師 在 其 他 領 域 的 淵 博 知 識 , 更 指 出 了 在 宏 觀 上 一 個 學 術 研 究 者 所 應 具 備 的 眼 光 , 令 我 受 益 良 多 。 也 要 感 謝 陳 孟 彰 老 師 的 指 點 , 讓 我 在 研 究 的 過 程 中 , 學 到 如 何 先 專 注 在 問 題 本 身 , 然 後 才 專 注 在 要 用 哪 種 方 式 去 解 決 , 這 清 晰 的 架 構 簡 化 了 如 何 表 達 清 楚 自 己 意 見 的 難 度 。 此 外 , 特 別 感 謝 蔡 志 宏 教 授 , 林 宗 男 教 授 以 及 潘 育 群 學 長 在 口 試 時 給 予 的 寶 貴 意 見 , 讓 本 論 文 更 加 完 備 , 在 此 謹 致 最 誠 摯 的 謝 意 。

另 外 要 感 謝 的 是 A N T S L a b 的 學 長 姐 、 同 學 、 學 弟 妹 們 , 感 謝 優 秀 的 學 長 姐 在 我 陷 入 瓶 頸 時 給 予 指 點 , 感 謝 一 起 奮 鬥 的 同 學 們 平 時 討 論 時 給 予 的 珍 貴 想 法 , 感 謝 可 靠 的 學 弟 妹 在 許 多 地 方 給 予 的 協 助 , 支 持 我 完 成 本 論 文 , 讓 我 這 兩 年 是 過 得 十 分 充 實 。 最 後 要 感 謝 我 的 家 人 們 , 父 母 給 予 的 學 習 經 驗 , 如 何 處 理 生 活 、 學 業 上 的 眾 多 瑣 事 , 兄 弟 姊 妹 時 不 時 與 我 聊 天 , 放 鬆 我 的 心 情 , 我 能 夠 安 心 寫 作 本 論 文 都 多 虧 了 家 人 們 的 關 懷 , 失 去 了 您 們 的 關 懷 , 我 想 必 沒 辦 法 專 心 在 學 業 上 , 謝 謝 您 們 !

呂 明 龍 謹 識 于 台 大 資 訊 管 理 學 研 究 所 中 華 民 國 一 百 年 八 月

II

論 文 摘 要

論 文 題 目 : 不 完 整 資 訊 下 動 態 頻 寬 交 易 之 最 佳 定 價 方 法

作 者 : 呂 明 龍 一 百 年 八 月

指 導 教 授 : 孫 雅 麗 博 士

頻 寬 是 很 稀 少 且 珍 貴 的 資 源 。 為 了 增 進 頻 寬 使 用 效 率 , 解 決 原 先 使 用 方 法 的 低 效 率 , 感 知 無 線 電 ( cognitive radio) 以 及 動 態 頻 譜 分 配 ( d y n a m i c s p e c t r u m a l l o c a t i o n ) 的 概 念 被 提 了 出 來 。 在 此 篇 論 文 , 我 們 考 慮 一 個 由 單一 mobile network operator (MNO) 以及眾多有著不同類 別(type)的 mobile virtual network operators (MVNOs) 組成的無線網路。我們以下提供 一 個 由 兩 個 階 段 組 成 的 開 放 式 動 態 頻 寬 交 易 模 型 來 讓 MNO 將 頻 寬 販 賣 給 MVNOs。

這個開放式動態頻寬交易模型的第一個階段的目的是在一連串MNO與MVNOs的 互動中,去找到參與的MVNOs的購買意願或者他們的類別,並且計算出要被販賣的頻 寬的最佳價目表。計算最佳價目表的同時也會考慮到MVNOs的需求價格函數以及效用 函數。最重要的是,最佳價目表必須滿足誘因相符性(incentive compatible, IC) 以及個 體理性(individually rational, IR)的限制。前者確保了為某個類別的MVNO設計的數量- 價格組能給該MVNO帶來最大的效用;後者確保了為其設計的數量-價格組可以給其非 零的效用。我們同時也提供了一個將連續的最佳價目表轉成離散形式,以提供一個比 較容易閱讀的格式;此時每個MVNO都會去選擇最靠近其在連續最佳價目表中類別的 數量-價格組。在反覆進行的互動收斂且停止之後,如果全部的需求超出了可以提供的 頻寬,那麼此模型就會使用背包問題的解法來將頻寬分配給一部分的MVNOs,已使得 分配出去的頻寬不會超出可提通頻寬的限制。最後,我們用一個例子來說明這個開放 式動態頻寬交易模型是如何運作的。

III

關 鍵 詞 : 動 態 頻 譜 分 配 、 誘 因 相 符 性 、 頻 寬 交 易 、 最 佳 價 目 、 定 價 方 法 、 有 限 頻 寬 分 配

IV

THESIS ABSTRACT

Optimal Pricing for Dynamic Bandwidth Trading with Incomplete Information

By Ming-Lung Lu

DEPARTMENT OF IMFORMATION MANAGEMENT NATIONAL TAIWAN UNIVERSITY

AUGUST 2011

ADVISOR : Yeali S. Sun, Ph.D

The wireless spectrum is a limited resource. The concepts of cognitive radio and dynamic spectrum allocation (DSA) have been considered as a possible mechanism to improve the efficiency of bandwidth usage and solve the bandwidth deficiency problem. In this work, we consider a wireless network access environment comprised of a mobile network operator (MNO) and a distribution of different types of mobile virtual network operators (MVNOs).

We propose an open dynamic bandwidth trading model that comprises of two phases. The goal of the phase one is to find out the distribution of the buying preferences or types of the participating MVNOs through a sequence of interactive rounds and compute the optimal price schedule for the unused bandwidth for sale. The derivation of the optimal price schedule also considers the demand and utility functions of the MVNOs. Most importantly, the optimal price schedule satisfies the incentive compatible (IC) and the individually rational (IR) constraints. The former ensures that the quantity-price pair designed for MVNO of a specific type will choose the pair that maximizes its utility; while the latter assures that the pairs cause non-negative utility. We also give an algorithm to convert the

V

continuous optimal price schedule to a discrete one so as to provide a simple easy-to-read format for MVNOs’ selection while ensuring that individual type of MVNOs will choose the pair whose corresponding utility value is closest to the value in the original function.

After the iterative process converges and terminates, if the total number of bandwidth requests exceeds the total capacity constraint, the process proceeds to address the finite capacity constraint by solving a bounded knapsack problem for final bandwidth allocation.

Lastly, an example is provided to explain how the proposed open dynamic bandwidth trading process with optimal incentive-compatible price schedule is derived.

keywords: dynamic spectrum sharing; incentive-compatible pricing; bandwidth trading;

optimal price schedule; finite bandwidth sharing

VI

Table of Contents

謝 詞 ... I 論 文 摘 要 ... II THESIS ABSTRACT ... IV Table of Contents ... VI List of Figures ... VII List of Tables ... VIII

Chapter 1 Introduction ... 1

Chapter 2 Related Work ... 4

Chapter 3 System Model ... 7

3.1 MVNO: the Buyer ... 7

3.2 MNO: the Seller ... 8

Chapter 4 Optimal Price Schedule ... 11

4.1 Optimal Bandwidth Quantity ... 14

4.2 Optimal Price ... 15

4.3 Discrete Price Schedule ... 15

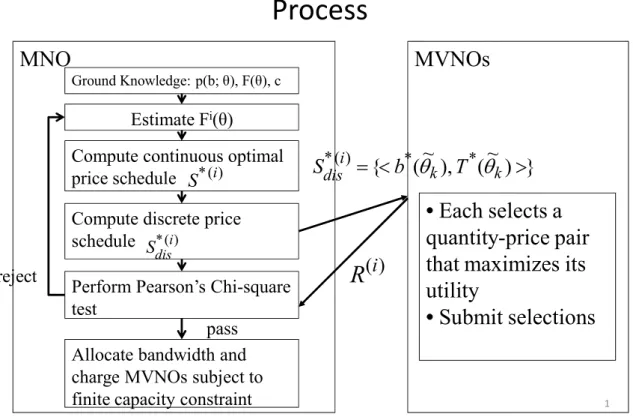

Chapter 5 Open Dynamic Bandwidth Trading Model ... 20

5.1 Re-estimation of MVNO Type Distribution ... 21

5.2 Estimation of F(i)(θ) from R(i) ... 22

5.3 Capacity Constraint ... 23

5.4 Example ... 25

A. Optimal Price Schedule ... 26

B. Discrete Price Schedule ... 27

C. Quantity-Price Selection ... 28

D. Hypothesis Testing... 28

E. Estimation of MVNO Type Distribution ... 29

F. Bandwidth Allocation ... 32

Chapter 6 Conclusion ... 33

Reference ... 35

VII

List of Figures

Figure 1 The K subintervals in the determination of the discrete price schedule and the illustration of the utility values in price pair selection. ... 19 Figure 2. Flowchart of the open dynamic bandwidth trading process ... 23 Figure 3. Distribution of the ten MVNOs that join the open dynamic bandwidth

trading process initially ... 27

VIII

List of Tables

TABLE I. THE DISCRETE PRICE SCHEDULE AND THE TYPE SUBINTERVALS IN THE

FIRST ROUND ... 28 TABLE II. The FREQUNCY TABLE AFTER THE FIRST ROUND ... 29 TABLE III. THE DISCRETE PRICE SCHEDULE AND THE TYPE SUBINTERVALS IN THE

SECOND ROUND ... 30 TABLE IV. FREQUENCY TABLE AFTER THE SECOND ROUND ... 31

1

Chapter 1 Introduction

Since spectrum is a limited and therefore precious resource, how to achieve efficient

and fair spectrum sharing and allocation among different demand groups is an important

issue. Traditional spectrum allocation schemes adopt the long-term lease business model,

which assigns different wireless technologies with a static amount of bandwidth to different

frequency band in order to prevent interference between them. A study sponsored by the US

Federal Communications Commission observed that the traditional fixed spectrum

assignment model, which results in over-allocation of spectrum to some operators and

applications as well as inefficient bandwidth usage, is unable to meet the growth in demand

arising from today’s wireless technologies [1].

One possible way to overcome the above limitations is to allow periodic trading of

dynamic unused bandwidth by licensed spectrum owners, who sublet their surplus resources

to service providers that need bandwidth for a short period. In this work, we consider a

wireless network access environment comprised of a mobile network operator (MNO) and

various mobile virtual network operators (MVNOs) of different buying preferences or types.

It is assumed that an MNO is a telecommunications company that owns a frequency license

and mobile infrastructure, and also provides services for mobile phone subscribers. An

MVNO is a company that provides mobile phone/network services, but it does not have a

frequency license or a mobile infrastructure. However, it does have access to a niche market,

which an MNO finds hard to enter. The spectrum owner (MNO) periodically offers its

2

unused bandwidth on the open market for short-term lease to MVNOs that need extra

bandwidth to meet their service needs and business goals.

In dynamic bandwidth trading, how to allocate and price bandwidth among different

demand groups of potential buyers are two fundamental issues. To address the issues, we

propose an open dynamic bandwidth trading model that comprises of two phases. The goal

of the phase one is to find out the type distribution of the participating MVNOs through a

sequence of interactive rounds between an MNO and MVNOs. In each round, the MNO

first revises its estimate of the distribution of the types of the participating MVNOs based

on their selections submitted in the previous round. It then re-computes the optimal price

schedule and announces it to the MVNOs for a new round of selection. The derivation of

the optimal price schedule considers the distribution of the types of MVNOs as well as their

demand and utility functions. The optimal price schedule comprises a number of pairs, each

representing the optimal bandwidth quantity and the associated price designed especially for

a type θ MVNO. Since the schedule is computed based on the assumption that all MVNOs

are rational, each MVNO will select the quantity-price pair designed for its type in order to

maximize its utility function, and the profit of the resource owner (MNO).

Through each round of interaction, the MNO learns more about the MVNOs that are

interested in purchasing extra bandwidth. As a result, the MNO revises its estimate of the

cumulative distribution function of the types of MVNOs to derive the optimal price schedule

for the sale of the unused bandwidth. We also present an algorithm to convert the continuous

3

optimal price schedule to a discrete form so as to provide a simple easy-to-read format for

MVNOs’ selection. In the second phase, we consider the finite capacity constraint in

bandwidth trading. After the process converges and terminates, if the total demand for

bandwidth exceeds the total capacity, we resolve the bandwidth contention problem by

mapping it to a bounded knapsack problem.

The proposed open dynamic bandwidth trading model creates a win-win situation for

the profit-maximizing MNO and individual MVNOs that need extra bandwidth. We believe

the model achieves better spectrum utilization and meets the business goals of MNOs and

MVNOs.

The remainder of the paper is organized as follows. Chapter 2 contains a review of

related works. In Chapter 3, the system model of the buyers (MVNOs) and the seller (MNO)

engaged in open dynamic bandwidth trading is given. In Chapter 4, we present the

derivation of the continuous optimal price schedule, and the algorithm to convert the

continuous optimal schedule to a discrete form to provide a simple easy-to-read format for

MVNOs’ selection. In Chapter 5, the proposed open dynamic interactive bandwidth trading

process of the MNO and MVNOs is described in detail. We also provide an example to

illustrate the key designs of the proposed open dynamic bandwidth trading process. Chapter

6 contains some concluding remarks.

4

Chapter 2 Related Work

A number of system models have been proposed for bandwidth allocation and pricing

in wireless environments. They address the problem by considering different combinations

of service providers, customers, and government regulations. Moreover, they use various

concepts, such as auction [2][3][4], game theory [5][6][7][8], or economic analysis [9][10],

to tackle the problem. In these works, spectrum/bandwidth buyers are typically modeled by

using some simple parameters, e.g., the maximum budget or the maximum amount of

money that buyers are willing to pay for a certain amount of bandwidth. In this work, we

model the behavior of an MVNO by its type, demand curve and utility function to capture

the essential characteristics of a potential bandwidth buyer.

Among all the methods used for spectrum management, auction is the most popular

approach. For example, under the method proposed in [2], a spectrum manager periodically

auctions short-term spectrum licenses to multiple CDMA network operators with the goal of

maximizing revenue. Each operator determines its own price based on the amount that users

are willing to bid. In [3], two auction mechanisms are proposed for spectrum sharing by a

number of users based on the signal to interference-plus-noise ratio (SINR) and received

power. The authors of [4] introduce a spectrum auction framework that formulates

conflict-free spectrum allocation between users as an optimization problem. They also

discuss the tradeoffs between the auctioneer’s revenue and fairness to buyers under different

pricing strategies. The main drawback of the auction approach is that it is time-consuming

5

and it may incur high operating costs. It is also known for its unfavorable spectrum

utilization [5].

Another popular approach uses game theory to solve the spectrum allocation and

pricing problem. In [5], the authors consider the problem of spectrum sharing between a

primary user who is eligible to access a licensed radio spectrum and a number of secondary

users who have no access rights to the licensed spectrum. The problem is formulated as a

Cournot game in which a pricing function is used to constrain secondary users from

requesting excess spectrum. It is assumed that the total spare spectrum available for

allocation is not finite, which is rather unrealistic. In [6], the authors consider the same

problem with multiple primary and secondary users. Two different games are used to model

the behavior of each type of users. The interaction between the games is that the spectrum

and price offered by the primary users will affect the equilibrium of the secondary users’

game. It continues until both of them reach equilibrium. In [7], a framework is developed to

model the competition between multiple network operators for customers and the available

spectrum as a non-cooperative game under the regulation of a spectrum policy server. The

main disadvantage of this approach is that there is no real mediator in practice, so the

players need to propose individual strategies iteratively to reach equilibrium; hence, the

convergence period is often long.

There are also approaches that consider the price when allocating spectrum to users

with different demands. In [9], the authors consider how a service provider sets the

6

spectrum price to maximize profits and how users decide the amount of spectrum to

purchase. They apply economic analysis techniques in a monopoly market to determine the

optimum price for the service provider. The approach in [10] uses game theory to study

demand-responsive pricing for radio resource management where multiple access points

compete for users.

It is widely recognized that user satisfaction is an important factor that must be

considered in the provision of services. Indeed, some works regard user satisfaction as the

primary consideration rather than revenue-maximization. In [11], the authors propose a

model of user satisfaction in which the requested QoS and the price paid are considered in

radio resource management. Based on their model, the authors of [7] study how customers

choose a network operator for service when multiple operators compete with each other. In

contrast to the above works, we use a non-linear optimal price schedule to discriminate

between different types of MVNOs. We propose an open dynamic trading model in which,

through each round of interaction, the MNO learns more about the distribution of the types

of the potential buyer MVNOs so to derive the optimal price schedule that will maximize its

expected return.

7

Chapter 3 System Model

There are two kinds of players in the proposed dynamic bandwidth trading model:

buyers (multiple MVNOs) and the seller (the MNO). The MNO only owns one product, i.e.,

surplus bandwidth, with a constant marginal cost c. Based on that cost, c, and its knowledge

of the distribution of the types of buyer MVNOs, the MNO will publish an optimal price

schedule for the MVNOs’ selection which is specially designed so that an MVNO based on

its type will choose the quantity-price pair that maximizes its utility.

3.1 MVNO: the Buyer

We assume there are different buying preferences or types of MVNOs and use the

parameter θ, which is bounded by [θL, θU], to describe them. A type θ MVNO’s preference is

represented by the utility function, which follows the standard consumer surplus approach:

T dx x p T

b

U( , ;)

0b ( ;) , (1) where b is the amount of bandwidth purchased, T is the total price paid, and p(x; θ) is thedemand price function of a type θ MVNO. The integration of the demand price function

gives the total price the buyer is willing to pay for the total number of units of bandwidth b.

We also assume that there exists an efficient consumption level for which the demand price

exceeds the marginal cost for type θ MVNOs, denoted by be(θ). We make two other

assumptions:

8

Assumption 1. For all feasible θ, (1) the demand price function p(b; θ) is non-increasing in

b and non-negative1; (2) be(θ) ≥ 0 and p(b; θ) is decreasing in b for b ≤ be(θ), and p(b; θ)

≥ c if and only if b ≤ be(θ); and (3) p(b; θ) is twice continuously differentiable.

Assumption 2. Higher levels of θ are associated with higher demand. That is, p(b; θ) is

strictly increasing in θ whenever p(b; θ) is positive.

It is assumed that MVNOs use the utility functions to measure and evaluate the price

schedule announced by the MNO, and that each MVNO will choose the quantity-price pair

that maximizes its utility. If more than one pair yields the same maximal utility, we assume

that the MVNO will choose the one with the largest amount of bandwidth.

Let the types of MVNOs follow a continuous distribution represented by the cumulative

distribution function (CDF) F(θ). It is assumed that the population of MVNOs are drawn

independently according to F(θ). We also make the following assumption:

Assumption 3. The cumulative distribution function for θ, F(θ), is a strictly increasing,

continuously differentiable function on the interval [θL, θU] with F(θL) = 1 – F(θU) = 0.

3.2 MNO: the Seller

We assume that the demand price functions, p(b; θ), and the utility functions, U(b, T;

θ), for all θ are known to the MNO because they can be obtained by analyzing historical

information. However, the MNO does not know the exact types of the MVNOs participating

in the trading.

1 The non-increasing property might not be suitable for scarce resources. Although the spectrum is scarce, we still consider this property in our work.

9

The MNO’s objective is to construct and publish a price schedule (S) of pairs <bs, Ts>

that maximizes its profit. If an MVNO chooses a pair s of S, it will receive bs and pay for a

total of Ts. In the next section, we explain how to derive the optimal price schedule such that

each type of MVNO will choose the pair designed for it, and that pair will give the MVNO

the maximal utility. First, we define the MNO’s profit or "return" as follows:

b c T

Rˆ ˆ ˆ. (2)

Let N(b; θ) denote the social surplus generated by the sale of a type θ MVNO, i.e.,

bpb dx cb b

N( ;) 0 ( ;) . (3)

The utility of a type θ MVNO that chooses pair <b, T> is defined as the social surplus N(b;

θ) less the MNO’s profit R, i.e.,

bp x dx cb R N b R

R b

U( , ;) 0 ( ;) ( ;) . (4)

Two properties are important to the MNO in the construction of the optimal price

schedule. First, the MNO must ensure that the schedule contains a specific quantity-price

pair for each type of MVNO. Second, the MVNOs are rational, meaning every type θ

MVNO will only choose the pair <b(θ), T(θ)> designed for it, and that pair will give the

MVNO the maximal utility. That is, the price schedule will satisfy the following two

constraints [12].

C1: [Incentive Compatibility (IC)]: for each θ,

L U

v v

T v b U T

b

U( (), ();) ( ( ), ( );), , . (5)

C2: [Individually Rational (IR)]: for each θ,

10 0 ) );

( ), (

(b T

U . (6)

The IC constraint ensures that the pair <b(θ), T(θ)> designed for the type θ MVNO is the

pair that would maximize its utility; while the IR constraint ensures that the pair <b(θ),

T(θ)> causes non-negative utility. Given a price schedule S that satisfies the two constraints,

every type θ MVNO will choose the pair <b(θ), T(θ)>. Such a quantity-based price schedule

is described as incentive compatible. An incentive-compatible quantity-based price schedule

is said to be optimal for a subinterval [θL, θU] if it yields profits for the MNO that are at

least as high as any other incentive-compatible quantity-based price schedule designed

exclusively for customers in the range [θL, θU][12].

11

Chapter 4 Optimal Price Schedule

In this section, we explain how to construct the optimal price schedule, S*, of pairs

<(bs*, Ts*)> that will maximize the MNO’s profit and satisfy the IC and IR constraints. We

adopt the method in [13], which satisfies the self-selection constraints. Both the

self-selection and the IC constraints require that each type of MVNO will be more satisfied

with the quantity-price pair designed for it than with a pair designed for any other type of

MVNOs. For example, consider n different types of MVNO, θ1 < θ2 < ... < θn. The optimal

price schedule {<b(θ), T(θ)>} that satisfies the self-selection constraints has two necessary

properties. The first property is that b(θ) is a non-decreasing function. Let us consider any

two neighboring types of MVNOs, θi and θi+1, and assume that the pair <b(θi), T(θi)>

designed for θi is known. Then, the pair <b(θi+1), T(θi+1)> designed for θi+1 should be the

same as the pair <b(θi), T(θi)>; otherwise, it should be located on or below the indifference

curve of type θi+1 through <b(θi), T(θi)> to prevent the higher type θi+1 from switching to

the pair designed for the lower type θi. Moreover, the pair <b(θi+1), T(θi+1)> should be

located on or above the indifference curve of the type θi through <b(θi), T(θi)> to prevent

the lower type θi from switching to the pair designed for the higher type θi+1. Hence, we

have b(θi+1) ≥ b(θi) for any two neighboring types, so b(θ) is a non-decreasing function.

The second property is called the "local downward" constraint:

n i

T b U T

b

U( (i), (i);i) ( (i1), (i1);i), 2,, , (7)

which implies that the lowest type would yield zero utility, i.e.,

12

0 )

; 0 , 0 ( ) );

( ), (

(b1 T 1 1 U 1

U . (8)

The local downward constraint is the only self-selection constraint that is binding.

The two properties are sufficient to ensure that all self-selection constraints will be

satisfied. That is, if the price schedule satisfies the two properties, then it will also satisfy

the self-selection constraints. Consider two neighboring types of MVNOs, θi and θi+1 with

the known pair <b(θi), T(θi)> designed for θi. The local downward constraint makes the pair

<b(θi+1), T(θi+1)> locate on the indifference curve of θi+1 through <b(θi), T(θi)>. Since the

indifference curve of θi+1 is steeper than that of θi and the non-decreasing property implies

that b(θi+1) should be equal to or greater than b(θi), the pair <b(θi+1), T(θi+1)> is above the

indifference curve of θi and U(b(θi+1), T(θi+1); θi) < U(b(θi), T(θi); θi). Therefore, the lower

type θi would not switch to the pair designed for the higher type θi+1.

With <b(θ), p(θ)> optimal for each type θ MVNO, we can write the maximized utility

as

) ( ) );

( ( )

*( N b R

U . (9)

According to Assumptions 1 and 2 and the "local downward" constraint, a type θ MVNO

would derive no extra advantage by choosing the offers for the MVNOs with lower types

than θ. Thus, we have

L

dx x x N b b

N

R( ) ( ( ); ) ( ( ); ) . (10)

Therefore, the expectation of R(θ) is calculated as follows:

13

U

L L

dF dx x x N b b

N R

E

); ) ( ( ); ) ( )

( ( ]

[ . (11)

After integration by parts, we have [13]:

U

L

F dF b F

b N N R

E

( )

) ( '

) ( )1 );

( ( ) );

( ( ]

[ . (12)

Let I(b(θ); θ) denote the terms in the brackets. Then, we can rewrite (12) as follows:

U

L

dF b

I R

E

( ();) () ]

[ . (13)

The goal of the MNO is to find the optimal price schedule that maximizes its expected

return. The derivation of the optimal price schedule involves two steps. First is to find the

optimal bandwidth {b*(θ)} that would maximize the expected return. Note that the optimal

price schedule must satisfy the self-selection constraints. It has been proved that, for any

non-decreasing function b(θ) on [θL, θU], there exists a unique return function, R(θ), as

given in (10) such that <b(θ), R(θ)> satisfies all the self-selection constraints and U*(θL) = 0,

which is the maximal utility designed for the lowest potential buyer θL[13]. The following

two assumptions are made to ensure that the non-decreasing price elasticity property of b(θ)

does not offer random pairs of a schedule, and for convenience in the choice of

parameterization of θ.

Assumption 4. Demand elasticity is non-decreasing in the demand price, i.e.,

0

b p p

b

. (14) Assumption 5. The second-derivative of the demand price function with respect to θ is

non-positive,

14 0 )

;

2 (

2

pb . (15) After obtaining b*(θ), in the second step we substitute b*(θ) for b(θ) in (10) to obtain R*(θ).

We also obtain the optimal price T*(θ) as follows:

) ( ) ( )

( * *

* R cb

T . (16)

In the following, we explain how to derive the optimal price schedule in details.

4.1 Optimal Bandwidth Quantity

Finding the maximum expected return in (13) involves maximizing I(b(θ); θ) for all

feasible θ. That is, if b*(θ) maximizes I(b(θ); θ) for all feasible θ, b*(θ) would also

maximize the expected return. We prove the above statement by contradiction. Suppose that

b*(θ) maximizes I(b(θ); θ) and there exists a b**(θ) such that b**(θ) yields a higher expected

return than b*(θ). Since b**(θ) will yield a higher expected return and the expected return is

the integration of I(b**(θ); θ), then I(b**(θ); θ) should be greater than I(b*(θ); θ) at some

point. This means that there would exist at least one point, say θa, such that I(b**(θa); θa) >

I(b*(θa); θa). We can prove this easily because if I(b**(θ); θ) ≤ I(b*(θ); θ) for all feasible θ,

the integration of I(b**(θ); θ) would be smaller than that of I(b*(θ); θ). As we have I(b**(θa);

θa) ≤ I(b*(θa); θa) for all feasible θ, it would not be possible for the expected return from

b**(θ) to be greater than that from b*(θ). Therefore, b**(θa) cannot exist.

Given Assumptions 1, 2, 3, 4, and 5, we know the b*(θ) that solves maxI(b;)

b must be

non-decreasing. Suppose b*(θ) maximizes I(b; θ) for all feasible θ. Then, b*(θ) should

satisfy the following equation:

15

L U

b b

I ( *();)0, ,

. (17)

Note that we assume the b(θ)s in the published price schedule are non-negative. To convert

b*(θ) to a non-negative function, let b0(θ) be the optimal bandwidth function for all feasible θ. We eliminate the negative part of b0(θ) to obtain the optimal bandwidth quantity function

b*(θ). Specifically, b0(θ) is computed by the following equation:

L U

b b

I ( 0();)0, ,

. (18)

We also have

L U

b

b*()max{0, 0()}, , . (19)

4.2 Optimal Price

The optimal price function is computed by substituting b*(θ) for b(θ) in (10), i.e.,

L U

L

dx x x N b b

N

R

( ( ); ) , ,

) );

( ( )

( * *

*

. (20)The function gives the optimal return (profit) R*(θ) derived by selling b*(θ) units of

bandwidth to a type θ MVNO. We also have the following optimal price function T*(θ):

L U

cb R

T*() *() *(), , . (21)

Finally, we have the optimal price schedule S*, which comprises a number of pairs {<b*(θ),

T*(θ)>}, each representing the optimal bandwidth quantity and the associated price designed

especially for a type θ MVNO.

4.3 Discrete Price Schedule

Thus far, we have assumed that the demand price functions and the type distribution

functions of MVNOs are all continuous, and the resulting optimal price schedule is a pair of

16

continuous functions of the MVNO type. Although the continuous forms are convenient for

deriving the model and the optimal price schedule, in practice, the units of bandwidth are

usually sold in a discrete format. Here, we will convert the continuous optimal price

schedule to a discrete form. Assume K different quantity-price pairs are selected from the

continuous optimal price schedule such that the resulting expected return is as high as

possible. K is assumed to be defined by the MNO's policy. Let the resulting discrete price

schedule be denoted by Sdis* = { ~) (

~),

( *

* k T k

b , k = 1 ~ K}. Given Sdis* , it is obvious that

a type ~k MVNO will choose the pair ~) (

~),

( *

* k T k

b . Next, we examine the types

within the range of ~k and ~k1. Consider a θ in ~ )

~,

(k k1 . Let us compute the difference

in the utility of choosing either pair, i.e.,

)

~ );

(

~ ), ( ( )

~);

(

~), (

(b* k T*k U b*k1 T*k1

U . (22)

Differentiating (22) with respect to θ, we have

(~ )

~) (

* 1

* k ( ; )

k

b

b p x dx

. (23) Since p(b; θ) is increasing in θ and b*(θ) is non-decreasing, the derivative of the utility

difference in (22) is negative, and the utility difference is decreasing in θ. That is, when θ

moves outside the range of ~k and ~k1, the utility obtained by choosing ~) (

~),

( *

* k T k

b

would be higher until at type kb or type (k1)a the utility derived by choosing either

~)

(

~),

( *

* k T k

b or ~)

(

~ ),

( 1 * 1

* k T k

b would become the same. Thereafter, the types

between ~ ]

,

[(k1)a k1 will choose the pair kb that yields a higher utility than selecting

~)

(

~),

( *

* k T k

b . Here, we assume that if two possible price pairs render the same utility, an

17

MVNO would choose the one with greater amount of bandwidth. Hence, type kb will

choose ~ ) (

~ ),

( 1 * 1

* k T k

b instead of ~)

(

~),

( *

* k T k

b . For the types in the subintervals

~) ,

[L 1 and (~K,K], the pairs ~) (

~),

( 1 * 1

* T

b and ~ )

(

~ ),

( *

* K T K

b will be chosen,

respectively. In summary, we assume that the discrete price schedule contains K pairs of

bandwidth quantity and the associated price, and we want to determine which K pairs in the

continuous optimal price schedule will maximize the expected return. The K pairs

correspond to the K types (points) of MVNOs, which in turn divide the type distribution

range [θL, θU] into K mutually exclusive subintervals, denoted by [ 1 , 1 )

b a

, [ 2 , 2 )

b a

, ...,

) ,

[ 1 1

b

a K

K

, [ , ]

b

a K

K

, 1a Land Kb U. The selection of the set {~k, k1,..,K} has

the property ~ ); )

(

~), (

( * *

kb

k

k T

b

U = ~ ); )

(

~ ), (

( * 1 * 1 ( 1)

k a

k

k T

b

U , k = 1 ~ K–1. Thus, the

problem can be formulated by solving the following non-linear optimization problem.

K

k

k k

k

k cb F b F a

T

1

*

*(~ ) (~) ( ) ( )

max (24)

s.t.

a L

1 (25)

U Kb

(26)

1 ,..., 1

1 ,

k K

b

a k

k

(27)

1 ..., , 1 ),

~ );

(

~ ), ( ( )

~);

(

~), (

(b* T* Ub* 1 T* 1 (1) k K

U k k kb k k k a (28)

1

~ 1

~ ,

~

1

k k K

k

(29)

K

b k

a k k

k ~ , 1~

(30)

} 0 ) (

|

~ min{ *

1

b (31)

18

K k b ~k) , 1~

*( (32)

In the formulation, we know that when the ~k’s are determined, the ranges of the

K intervals are also determined, i.e., {[ , ),k 1,...,K}

b

a k

k

based on the constraint

)

~ );

(

~), (

(b* k T* k kb

U = ~ ); )

(

~ ), (

(b* k 1 T* k 1 (k 1)a

U . Here, the boundaries are presented as

implicit functions that are parts of the constraints.

Moreover, we would like the ~)

*(

b k s to be integral values. Note that, in non-linear (mixed) integer programming problems, the integer property should only be applied to

decision variables. However, in the formulation proposed above, the integer property is

applied to ~)

*(

b k , not ~k. We therefore make a conversion as follows. We convert the price function T*(θ) to T*(b) by T*(b) = T*(b*-1(b)) where b*-1(b) is the inverse function of b*(θ).

The problem then becomes the problem of selecting K different quantities, b~k

, k = 1 ~ K,

from a finite set {b|0b

b*(U)

&bΝ} such that the expected return

K

k

k k

k

k cb F b F a

b T

1

* ~ ( ) ( )

~)

( is maximized. We thus formulate the problem as a non-linear

mixed integer problem. Since the problem is a combinatorial optimization problem, once

b~k

s have been decided, the expected return can be obtained in constant time. In addition, the

problem can be solved in polynomial time O(

b*(U)K

) by examining all possible combinations,

*( )

1!(

*( )

)( *( )

1)...(

*( )

1)

b b b K

K K b

U U

U U

given a constant K.

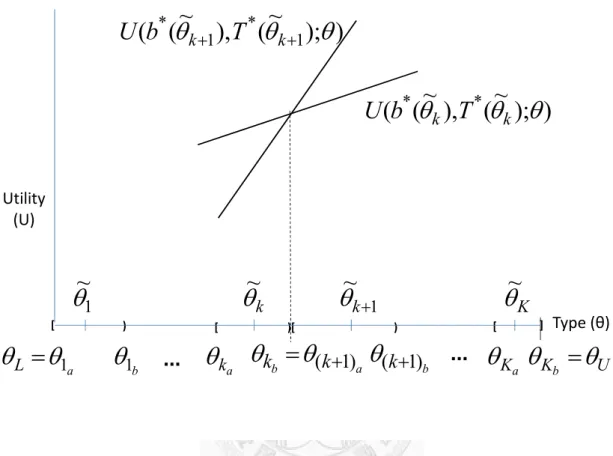

Fig. 1 shows the K subintervals of the type distribution range. An example of utility

values is also depicted to show that for the MVNOs of the types in the range of