1

Pre and Post-Convergence with IFRS and Value Relevance of

Financial Statements: Evidence from Two Decades’ Accounting

Standard Setting in Taiwan

TsingZai C. Wu

* National Cheng Kung UniversityWan-Ting Hsieh

†National KaoHsiung University of Applied Sciences

Chun-Chan Yu

††National Cheng Kung University

Hsin-Ti Chu

††Southern Taiwan University

Department of Accountancy National Cheng Kung University

1 University Road, Tainan City, Taiwan, Republic of China Tel: +886-6-275-7575 x 53426

Fax: +886-6-274-4104 Email:[email protected]

November 2013 __________________________

* Corresponding author, professor Accountancy and a member of Taiwan Financial Accounting Standards Committee (1996-2013). † Associate Professor, †† Ph. D. candidates.

We are grateful to comments from participants of Annual meetings of Taiwan Accounting

Association and Japan Accounting Association. Financial support was from the National Science Committee, Taiwan, Republic of China. (Research grant No. NSC 9424-16- H006- 031).

2

ABSTRACT: Although many countries around the world have adopted IFRS, convergence is

still an option for some countries (e.g., the U.S., Japan, and India). We examine whether the

value relevance of financial statements, especially before and after the convergence with IFRS

(“country-specific version of IFRS”) over the past two decades, have improved in Taiwanese

firms. Two differential methods are used to strength our results: Traditional adjusted R2

comparison and abnormal pricing errors. In summary, although we find a replacement effect

between earnings and book value of equity, convergence with IFRS does not lead to a further

increase in the joint value relevance of financial statements. Considering U.S. GAAP has

constituted the infrastructure of twGAAP, our findings are consistent with the notion that

financial reporting system is a function not only of accounting standards, but also of other

institutional factors. The empirical evidence from Taiwan may provide implications to

international standard setters and regulators, especially for countries which have not decided to

adopt or converge with IFRS.

3

I. INTRODUCTION

The purpose of this paper is to examine whether the value relevance of financial statements,

especially before and after the convergence with IFRS1, has improved over the past two decades

in Taiwan. Taiwan’s accounting standard setting body, the Taiwan Financial Accounting

Standards Committee (TFASC) of the independent Accounting Research and Development

Foundation (ADRF), was set up and started to issue financial accounting standards for firms in

Taiwan since 19842. The mission of ADRF is to enhance the quality of accounting and auditing

practices for public firms in Taiwan. Up to 2013, TFASChas issued 41 statements of financial

accounting standards (twSFAS) and more than 800 interpretations to the standards. From 1984 to

1999, Taiwan’s generally accepted accounting principles (twGAAP) basically follows U.S.

GAAP to ensure that twGAAP could be compatible with accounting standards with good

reputations. Realizing the importance of having globally acceptable standards for public firms in

Taiwan, TFASC initiated a project to review and modify all announced twSFAS in accordance

with the principles of IFRS (then IAS) in 1999. From then on, twGAAP began to converge3 with

IFRS until 2012. Although most of countries around the world have mandated or permitted the

1 Throughout this study, the term “IFRS” refers not only the narrowly defined International Financial Reporting

Standards issued by the International Accounting Standards Board (IASB), but also International Accounting Standards (IAS) issued by the IASB’s predecessor body, the International Accounting Standards Committee, some of which have been amended by the IASB.

2 Taiwan’s Securities and Futures Bureau (SFB) of the Financial Supervisory Commission (FSC) delegates

authority of setting up twGAAP to the ARDF.

3 In this study, we refer convergence to the definition of Ramanna and Sletten (2013) that “a country’s efforts to

4

adoption of IFRS (IASB 2012) now, some countries, such as the U.S., Japan, and India, are still in the stage of “limited convergence” with IFRS4. Given the complexity of cost-benefit analysis

based on individual country’s circumstances, the decision to adopt IFRS is difficult. Among

options, one strategy is to adopt a “country-specific version of IFRS”. Under this strategy,

although IFRS is the foundations of domestic GAAP, each jurisdiction still keeps the power to

issue accounting standards, interpretations, and related implementation guidance. In addition,

there can be supplemental disclosure requirements and standards that augment IFRS (Hail et al.

2010). Coincidentally, this is what TFASC adopted in its “IFRS-Convergence Period” during

2000–2012. Taiwan’s unique standard setting environment provides a feasible empirical testing

for the strategy suggested by Hail et al. (2010).

To focus on the long-term relations between stock price and financial statements, we

employ the Ohlson model (Feltham and Ohlson 1995) to investigate the value relevance of

accounting numbers. Two measures are used to examine the trends in value relevance of earnings

and book value of equity in the price model during 1990–20115. First, we use traditional adjusted

R2 comparison of cross-sectional regressions along years to test the joint and incremental value

Convergence projects often result in adopting IFRS with modifications and exceptions” (p.1).

4 We use the term “limited convergence” because compared with convergence strategy used by TFASC and

suggested by Hail et al. (2010), the differences with IFRS in accounting standards per se are relatively high in the present U.S, Japan, and India.

5 In this study, we refer “Developing Period” to year 1984–1999 and “IFRS Convergence Period” to year

5

relevance of earnings and book value of equity (Collins et al. 1997; Francis and Schipper 1999;

Ely and Waymire 1999). Second, we use abnormal pricing errors suggested by Gu (2007) to

eliminate the across-sample incomparability problem of adjusted 2

R and the scale effect

problem caused by direct usage of residuals. Considering there are still other factors affecting

value relevance, we also provide two alternative empirical results to control the stability of

economy and the incidence of negative earnings in our main analysis in addition to full sample

results.

The results indicate that, although a statistically increasing trend of joint value relevance is

found in the whole period (1990–2011), this trend is primarily driven by increase of value

relevance in the Developing Period (1984–1999). Since U.S. GAAP has constituted the

infrastructure of twGAAP in this Developing Period, the stated results are consistent with the

notion that financial reporting system is a function not only of accounting standards, but also of

interpretations, auditing, incentives, and the law environments (Ball et al. 2000; Ball et al. 2003;

Leuz et al. 2003; Lang et al. 2006; Bradshaw and Miller 2008). Hence, the marginal benefits of

convergence with IFRS in joint value relevance are limited. In terms of incremental value

relevance, the incremental relevance of earnings exhibits a significant downward trend during

the IFRS-Convergence Period (2000–2012), yet the incremental relevance of book value of

6

relevance of earnings is slowly being replaced by that of book value of equity, which is

consistent with what IFRS focuses on (i.e., asset/liability view rather than revenue/expense view).

To sum up, although convergence with IFRS does not lead to a further significant increase in the

joint value relevance of financial statements, the replacement effect in the IFRS-Convergence

Period show that at least the efforts of TFASC to stress the relevance of balance sheet have been

paid off. We also conduct three robustness tests: First, we use return model to explore short-term

relations between changes of stock price and accounting numbers. Second, we examine the

effects of nonrecurring earnings on value relevance in price model. Finally, to ensure accounting

information is available to the public, we use the stock price on the final regulatory

announcement dates of annual financial reports as the dependent variable in the price model. In

sum, the long-term relations between stock price and financial statements are robust, although

we do not find consistent results in the return model. This may be due to the different relations

between accounting numbers in explaining stock price in the short term, or the increase in

volatility of stock returns suggested by Francis and Schipper (1999).

Our study contributes the accounting literature in two aspects. First, we provide empirical

evidence for the “country-specific version of IFRS” (convergence) strategy proposed by Hail et

al. (2010). Specifically, in the context that a country had already followed a set of high quality

7

relevance of financial statements for investors. Although convergence with IFRS may bring other

benefits in qualitative characteristics (e.g., increases in comparability of financial statements

between domestic and foreign companies), countries with larger economic size continuously

using their domestic standards still can attract international investment (Ramanna and Sletten

2013). Thus, comparability of financial statements may be not a decisive concern in determining

convergence with or adoption of IFRS. The empirical evidence from Taiwan in the

IFRS-Convergence Period may provide implications to international standards setters and

regulators (especially for countries which have not decided to adopt or converge with IFRS).

Second, given the potentially mixed results caused by the use of different methods to measure

value relevance, the consistent results between adjusted R2 and abnormal pricing errors measures

in our study strengthen our inferences.

The rest of the paper is organized as follows. In Section Ⅱ, we describe the development of

accounting standards in Taiwan and review literature on the convergence with and adoption of

IFRS. The research design is described in Section Ⅲ. Section Ⅳ illustrates our sample data

and shows the empirical results. Section Ⅴ presents the results of robustness tests. Section Ⅵ

8

II. BACKGROUND AND RELATED LITERATURE

Financial Accounting Standard Setting History in TaiwanBased on changes in accounting standard setters, the development of twGAAP can be

divided into three periods: (1) the AIC period (1969–1980), (2) the FAB period (1981–1983),

and (3) the TFASC period (1984–2012)6.

The AIC (or Initial) Period, 1969–1980

In 1969, Taiwan government invited E. Waldo Mayritz, the U.S. finance and economics

expert, to visit Taiwan for providing suggestions and assistance to the accounting profession in

Taiwan. Urged by Mayritz, the CPA Association of Taiwan Province and the CPA Association of

Taipei City7 jointly organized the Accounting Issues Committee (AIC) on September 9, 1969. The AIC’s missions were to issue twGAAP, twGAAS (Taiwan’s Generally Accepted Auditing Standards), codify professional conducts, and conduct research on special accounting issues. In

November 1970, the first (and the only) twSFAS, The Preparation of Financial Reports, was

issued by the AIC. This statement was a general guideline on accounting treatments.

The TFAB (or Transition) Period, 1981–1983

6 In response to the adoption of IFRS in 2013 for listed companies and financial institutions (except for credit

cooperatives, credit card companies and insurance intermediaries) supervised by the Taiwan FSC, a new committee called “T-IFRS Committee” was organized by ADRF to substitute TFASC in 2012. However, the main function of T-IFRS Committee is to translate English IFRS into traditional Chinese version. Therefore, we do not regard it as an accounting standard setter.

7 There are four accounting profession organizations in Taiwan based on practice territories: the CPA Association of

9

In 1980, John C. Burton, Dean of the Business School of the Columbia University in the U.S.,

was invited to Taiwan. After observing Taiwan’s securities market and visiting the accounting

profession, he suggested that Taiwan should establish a permanent organization to promulgate

twGAAP. This organization should consist of CPAs, university professors, and representatives of

financial institutions, government institutions, and industrial and commercial communities.

Following his suggestions, in 1981, a new standard setter called Taiwan Financial Accounting

Board (TFAB) was organized to be responsible for issuing and revising twSFAS. During its

short-lived tenure (two years), the FAB issued four standards and two interpretations.

The TFASC Period, 1984–2012

During early 1980s, some financial scandals occurred in Taiwan8 shook the credibility and

reputations of public audit industry in Taiwan. The ARDF was set up in 1984 to restore the

public trust and enhance the setting of accounting standards. The ARDF had two subordinate

committees: TFASC and TASC (Taiwan Auditing Standards Committee). The TFASC, which

took over the function of FAB, was responsible for promulgating twSFAS. The TFASC

Federation of CPA Association, Republic of China (Taiwan).

8 For example, in early 1981, Taiwan branches of the Chase Manhattan Bank and several other foreign banks

incurred severe bad debts from loans based upon unqualified opinion of audit reports issued by Taiwan’s CPAs. The audit quality of practicing CPAs in Taiwan was highly questioned. The minister of Taiwan’s Ministry of Finance, Mr. Li-De Siu, interviewed with chairmen of CPA Associations in Taiwan and determined to form a four-member task force to study the issue of accounting quality. After visiting the U.S. Securities and Exchanges Commission, major exchanges, big CPA firms and Financial Accounting Foundation, this task force suggested to establish an independent accounting institution to issue accounting and auditing standards and to train the accountants in Taiwan for the improvement of professional services.

10

consisted of 13 committee members and 13 advisors selected from academia, CPA firms,

industry, and government agencies. Up to 2012, the TFASC has issued 41 twSFAS and more

than 800 interpretations9. Under the efforts of its constituents, the TFASC has established its

professional reputation and public trust in Taiwan. Most importantly, it obtained the legal

endorsement from the Taiwan’s Securities Exchange Law and authorization from Taiwan’s SFB

of the FSC to establish twGAAP. From the perspective of accounting standards development in

Taiwan, the TFASC period can be divided into two sub-periods:

Developing Period (1984–1999): During this period, twSFAS was basically in conformity

with U.S. GAAP, except for some carve-outs due to law requirements or special business

practices in Taiwan. This strategy ensured twGAAP to align a set of accounting standards with

good reputations and minimized the costs of trial and error. Important examples included

TFASC’s SFAS No. 18: Accounting for Pensions and SFAS No.22: Accounting for Income Taxes,

which were based on U.S. FASB’s SFAS No.87 and SFAS No.109 respectively.

IFRS-Convergence Period (2000–2012): In response to globalization and increasing

demand of comparability of financial information between domestic and foreign companies, the

TFASC initiated a project in 1999 to review and compare the differences between international

and Taiwan accounting standards, and then decided to revise twSFAS based on IFRS principles

11

(i.e., converge with IFRS) instead of conformity with U.S. GAAP. From then on, all old twSFAS

issued before 1999 were revised gradually per IFRS according to urgency, materiality, and

generality to transactions; new accounting standards converged with contemporaneous IFRS

(with some degree of carve-outs) since 2000. A milestone of convergence was the issuance of

twSFAS No.34: Accounting for Financial Instruments (2003), which was based on IAS No. 39:

Financial Instruments: Recognition and Measurement. New founding concepts such as fair value

for derivatives are introduced. By and large, there were three intended changes in the

fundamentals of twGAAP. First, twGAAP switched from the income statement approach

(revenue/expense view) to the balance sheet approach (asset/liability view) in measuring

accounting elements. Second, twGAAP switched from historical cost basis to fair value basis.

Finally, twGAAP switched from rule-based standards to principle-based standards. As we know,

the IASB (previous IASC) approach relies more on principles, whereas the FASB’s approach

relies more on rules (Barth et al. 2012).

IFRS: Convergence or Adoption?

In response to the trend of globalization, many countries around the world strive for

achieving a single set of high quality accounting standards in past decades. Since 2001, almost

120 countries have required or permitted the use of IFRS (IASB 2012). However, there are some

12

countries, such as the U.S., Japan, and India10, still in the stage of “limited convergence” with

IFRS. According to extant literature, positive effects from the adoption of IFRS can be attributed

to the benefits of increasing in comparability (e.g., Yip and Young 2012; Barth et al. 2012) and

accounting quality, such as less earnings management, timely loss recognition, and higher value

relevance (e.g., Barth et al. 2008; Chen et al. 2010)11. Concrete benefits brought by adoption of

IFRS include capital market benefits, for example, higher market liquidity, improvements in

equity valuation, lower cost of capital, more efficient capital markets, positive stock market

reaction, greater analyst coverage (e.g., Daske et al. 2008; Drake et al. 2010; Li 2010; Armstrong

et al. 2010; Kim and Shih 2012; Joos and Leung 201312; Daske et al. 2013); other benefits

include more favorable private debt contracting terms (Kim et al. 2011), decreases in information

processing costs (Chi 2009), and perceived lower transaction costs (Ramanna and Sletten 201313).

Ramanna and Sletten (2013) also find that the perceived network benefits due to the adoption of

IFRS are more relevant to small-size than large countries.Their findings may in part explain why

10 In the U.S., according to a staff report issued by the Office of the Chief Accountant of the U.S. SEC on July 13,

2012, the SEC postponed the decision of whether to adopt IFRS (SEC 2012). All the major convergence projects will be completed by the middle of 2013. In Japan, the Accounting Standards Board of Japan (ASBJ) and the IASB announced their achievements under “The Tokyo Agreement” which targeted June 2011 to reduce differences in specific items between Japan GAAP and IFRS. The ASBJ will issue new Japan GAAP in line with the new IFRS are issued in the future. In India, the Ministry of Corporate Affairs (MCA), a part of the Government of India had announced in January 2010 a multi-phase plan for transition beginning April 1, 2011 to the new Converged Indian Accounting Standards (India’s attempt to converge to IFRS, which has carve-outs that distinguish it from IFRS, and is now known as “Ind AS”). For the details, see PWC (2012).

11 However, comparability and accounting quality may not be independent events. Increases in accounting quality

may be the potential sources of increases in comparability. For empirical evidence, see Barth et al. (2012).

12 Joos and Leung (2013) is one of few studies which use data of U.S. firms. Although they find a positive market

reaction to the events that increase the likelihood of adoption, however, they also note that it cannot whereby infer that actual adoption can bring real benefits.

13

large countries such as the U.S., Japan, and India still do not adopt IFRS until now.

However, we have to realize factors that determine the extent of benefits mentioned above

and the incremental costs along with the adoption of IFRS. Financial reporting system is a

function not only of accounting standards, but also of interpretation, auditing, incentives, and the

law environment (e.g., Ball et al. 2000; Ball et al. 2003; Leuz et al. 2003; Lang et al. 2006;

Bradshaw and Miller 2008; Daske et al. 2008). In a recent study, Barth et al. (2012) find that

IFRS-based accounting amounts generally are comparable to U.S. GAAP-based accounting

amounts based on accounting quality for firms located in common law and high enforcement

countries. In terms of incremental costs, Kim et al. (2012) and De George et al. (2013) uses data

of EU countries and Australian companies respectively and find that IFRS triggers a significant

increase in audit fees at the time of adoption. Their findings may resort to increased audit efforts,

increased investment in audit resources, and an increased audit risk premium (De George et al.

2013).

Compared with direct adoption, converging with IFRS may be less costly because of

gradual, rather than overall and immediate, impact on financial reporting system. Moreover,

since the national standard setters and regulators still keep the authorities to promulgate

accounting standards, flexibility and exceptions for local circumstances could be allowed. For

14

example, no matter in the Developing Period or in the IFRS-Convergence Period, the TFASC

keeps the power to issue twGAAP, interpretations, and related implementation guidance. Finally,

although convergence cannot achieve the full comparability of accounting standards per se, it

still could improve comparability of accounting amounts to some degree. For example, Barth et

al. (2012) find that in contrast to earlier data (2005–2006), the comparability of accounting

amounts between U.S. firms and their matched counterparts that adopt IFRS has a further

increase in more recent years (2007–2009). Barth et al. (2012) argue that their findings are

consistent with efforts to converge accounting standards.

To summarize, it can be seen at least for the countries that do not adopt IFRS yet, cost

benefit analysis is still a complicated and difficult work. The stance of SEC confirmed this view:

…the Staff will gather information using a variety of methods, including, but not limited to, performing its own research; seeking comment from, holding discussions with, and analyzing information from constituents, including investors, issuers, auditors, attorneys, other regulators, standard setters, and academics; considering academic research; and researching the experiences of other jurisdictions that have incorporated or have committed to

incorporate IFRS into their financial reporting systems and foreign private issuers who currently report under

IFRS…

(SEC 2010, Appendix p.2)

After considering the political and economic environment of the U.S., Hail et al. (2010)

develop several scenarios (or strategies) for the evolution of accounting standards in the U.S.

15

replaced by IFRS as the foundations for U.S. accounting standards, but the authority to issue

accounting standards, interpretations, and implementation guidance is still complemented by a

SEC/FASB overlay. Hail et al. (2010) argue that “U.S.-specific version of IFRS” is likely to

result in a better fit with the U.S. institutional environment. Even in countries with complete

and/or well-recognized accounting standards, this strategy still requires a deeper and more

comprehensive convergence with IFRS. However, to our knowledge, there is no available

empirical evidence of the consequences of convergence strategy. As mentioned earlier, before

2000, twGAAP was based on U.S. GAAP; and in the next thirteen years (2000–2012), twGAAP

converged comprehensively with IFRS. This unique setting provides an environment to test the

strategy suggested by Hail et al. (2010). The empirical evidence of value relevance from Taiwan

may provide implications to countries which have not decided to adopt or converge with IFRS

yet.

III. Research Design

Valuation Model

Value relevance is frequently used as a summary measure of how well accounting amounts

reflect the underlying economics of a firm (Barth et al. 2008; Ewert and Wagenhofer 2009).

16

whether these accounting information reflect stock prices in this study.

We employ the Ohlson model (Feltham and Ohlson 1995). As suggested by Collins et al.

(1997) and Ely and Waymire (1999), stock price is the dependent variable, and earning per share

and value of equity per share are independent variables in the cross-sectional regression (1a) ,

referred as the price model. We use this model to focus on the long-term relations between stock

price and financial statements14.

it it it it EPS BVPS P

0

1

2

(1a) where:

Pit = the price of a share of firm i at the end of year t.

EPSit = the earnings per share of firm i during the year t.

BVPSit = the book value of equity per share of firm i at the end of year t.

Measuring Trend in Value Relevance along Years

Since accounting standard setting is a continuous process, time itself becomes an

appropriate proxy for investigating the achievement of accounting standards. In order to test

whether the quality of financial statements is improved after the setup of TFASC in Taiwan from

1990 to 2011, we use two measures to examine the trend in value relevance of accounting

17

information over the past two decades. The first method examines adjusted R2 of annual

cross-sectional regression to study the comparative explanatory powers of accounting

information over years; the second method examines the abnormal pricing errors proposed by Gu

(2007).

Comparing Adjusted R2 of Cross-sectional Regressions

We use adjusted R2 of (1a) to measure the degree of value relevance over years. In addition,

we decompose adjusted R2 to investigate whether the incremental explanatory powers of

earnings and book value of equity would change over time. This decomposition is derived

theoretically by Theil (1971) and used in Easton (1985) and Collins et al. (1997) as follows:

it it it

EPS

P

0

1

(1b) it it itBVPS

P

0

1

(1c)The adjusted R2 from (1a), (1b), and (1c) are denoted as Joint_R2, EPS_R2, and BVPS_R2respectively. Then, BVPS_ IncrR2(=Joint_R2– EPS_R2) represents the incremental explanatory power provided by book value of equity, and EPS_IncrR2 (=Joint_R2– BVPS_R2) represents the incremental power provided by earnings. We regress these adjusted R2 on the trend variable (Yeart) to examine the significance of time trend in equation (2a):

t t

t a b Year c

18 where: 2 t R = Joint_ 2 R , EPS_IncrR2, or BVPS_ IncrR2

Yeart = trend variable equal to one for 1990, two for 1991, etc.

For the interest of this study, we further separate the sub-period 2000–2011 (belongs to the

IFRS-Convergence Period) to check whether there is a structural change in equation (2b).

R

t2

a

b

1(

Y e a r

t)

b

2S

2

b

3S

2

Y e a r

t

c

t (2b) where:S2 = dummy variable representing the IFRS-Convergence Period (if the sample period is during

2000–2011, S2=1, and 0 otherwise)

The definitions of other variables are the same with equation (2a).

Examining Abnormal Pricing Errors

The across-sample adjusted R2 comparisons are commonly used in accounting research15.

However, econometricians have long argued that regression R2 is incomparable across different

samples. It is mainly because R2 gives “a measure of the explanatory power of an economic

15 Other studies examining R2 comparison include Basu (1997), Collins et al. (1997), Brown et al. (1999), Francis

and Schipper (1999), Ely and Waymire (1999), Lev and Zarowin (1999), Ali and Hwang (2000), Ball et al. (2000), Core et al. (2003), Ball et al. (2003), and Barth et al. (2012).

19

model only specific to a sample and the underlying population. For two separate samples that are

typically drawn from two different populations, a difference in the R2 could mechanically arise

even if the economic relations underlying the two samples are identical” (Gu 2007, 1074).

Therefore, it is difficult for us to attribute different adjusted R2 to a change in the value relevance

or to mere sampling differences16. Econometricians suggest that, rather than subjecting the

residual variances to the sample variance of the dependent variable to obtain the R2 metrics, it is

better to use directly the variance of residuals itself as the indicator for explanatory power

comparisons among different samples (Goldberger 1991). Chang (1999) also uses residual

variance as his value relevance measure and adopts the loglinear valuation model. In value

relevance studies, variance or magnitude of residuals are referred as the pricing errors that are

components in prices (or returns) not explained by independent variables. The larger the pricing

error is, the lower the value relevance of that year’s accounting information would be (Gu 2007).

However, residuals itself can be affected by scale effect too. High price (return) usually

produces high pricing errors. If stock price (return) levels change significantly over time, the

scale effects must be controlled properly. Recognizing this problem, Chang (1999) assumes that

normal pricing errors are proportional to the magnitude of price levels. Under this assumption,

16 Brown et al. (1999) argue that empirical test of Collins et al. (1997) ignored the scale effect and that the larger

(smaller) the scale effect is, the higher (lower) the expectable R2 will be. In addition, sample heterogeneity can also

20

pricing errors can be standardized to obtain comparable value-relevance measures.

However, the proportionality assumption may not be valid. Results of our study show that

pricing errors are not proportional to stock price (see Table 3). Since the available sample of

firms in our study does not have linear change in scales, using either the raw pricing errors or

standardized pricing errors is likely to yield misleading results. To account for the nonlinear scale

effect, we use abnormal pricing errors proposed by Gu (2007) as the measure of value relevance.

Abnormal pricing errors measure is similar to the size-adjusted abnormal return used in finance

research. First, normal or benchmark pricing errors are obtained from pooled observations based

on deciles of absolute fitted values of prices17. Second, the abnormal pricing error of an

individual observation is measured as the absolute value of difference between the actual pricing

error and the benchmark with a comparable scale (See the Appendix for detailed information

about the calculation of abnormal pricing errors). Finally, the OLS regression of (3a) reveals

trend in abnormal pricing errors during the whole period:

t t t

a

b

Year

c

AbPerr

(

)

(3a) where tAbPerr = abnormal pricing errors of year t.

Yeart = trend variable equal to one for 1990, two for 1991, etc.

17 Here, we use the absolute fitted value rather than the actual values of stock prices as the scale. Gu (2007) argues

21

Again, we further separate the sub-period 2000–2011 (IFRS-Convergence Period) to check

whether there is a structural change in equation (3a). The only difference between this equation and (2b) is that the dependent variable in (2b) is replaced byAbPerrt.

Other Factors Affecting Value Relevance

In addition to the across sample incomparability of R2 and scale effect problems existing in

abnormal pricing error method, there are some factors that are believed to have influences on

value relevance beyond accounting standards per se. For example, changes in industry

composition (Francis and Schipper 199918), the incidence of negative earnings (Collins et al.

1997), the frequency and magnitude of nonrecurring items (Collins et al. 1997), stability of

economics, and competing sources of financial information (Francis et al. 2002). Therefore, in

addition to the full sample (hereafter, scenario 1), we also provide two alternative empirical

results to control stability of economics and the incidence of negative earnings in our main

analysis. First, we delete observations of negative EPS (hereafter, scenario 2). Second, we

further delete results of year 2007 and 2008 to avoid the effects of global financial crisis

(hereafter, scenario 3). We deal with the problem of nonrecurring items in section Ⅴ.

18 Francis and Schipper (1999) partition their sample firms into high-technology industries and low- technology

industries. The underlying reason is that many potential assets (such as R&D expenditure) are not allowed to be recognized in financial statement under current GAAP. Therefore, financial statements for high-technology companies might be more value irrelevant. However, results for these two subsamples are similar to the findings for the full sample.

22

IV. Empirical Results

Sample and Descriptive Statistics

Data used in this study are retrieved from Taiwan Economic Journal (TEJ) databanks. We

take firms listed in the Taiwan Stock Exchange Corporation as our sample because these

companies have longer financial data streams than those listed in the GreTai Securities Market

(OTC). We delete firms in the utilities and financial service industries due to their special

accounting practices. The sample period covers 1990–2011. We take 1990 as the starting year for

two reasons. First, it is the first year that sample size is more than 100 complete financial data for

all of our models. Second, although a total of 12 SFAS had been released by 1989, most of them

are related to specific accounting issues, such as construction contracts and troubled debt

restructuring, rather than general applicable standards for financial reporting. We take year 2011

rather than 2012 as the last year of our study to avoid confounding effect, since 2012 is a

transition year to adopt IFRS in Taiwan19. We winsorize all variables at the 1% and 99% levels to

mitigate the effects of outliers on our inferences. The sample selection process yields 10,037

firm-year observations for the scenario 1 (full sample). In scenario 2 (eliminating firms with

negative EPS) and scenario 3 (eliminating firms with negative EPS and in years 2007 and 2008),

19 According to IFRS No.1, “First-time Adoption of International Financial Reporting Standards” and regulatory

requirements in Taiwan, firms adopt IFRS in 2013 will prepare two sets of financial statements per twGAAP and IFRS in 2012.

23

the sample sizes are reduced to 8,211 and 7,108 respectively.

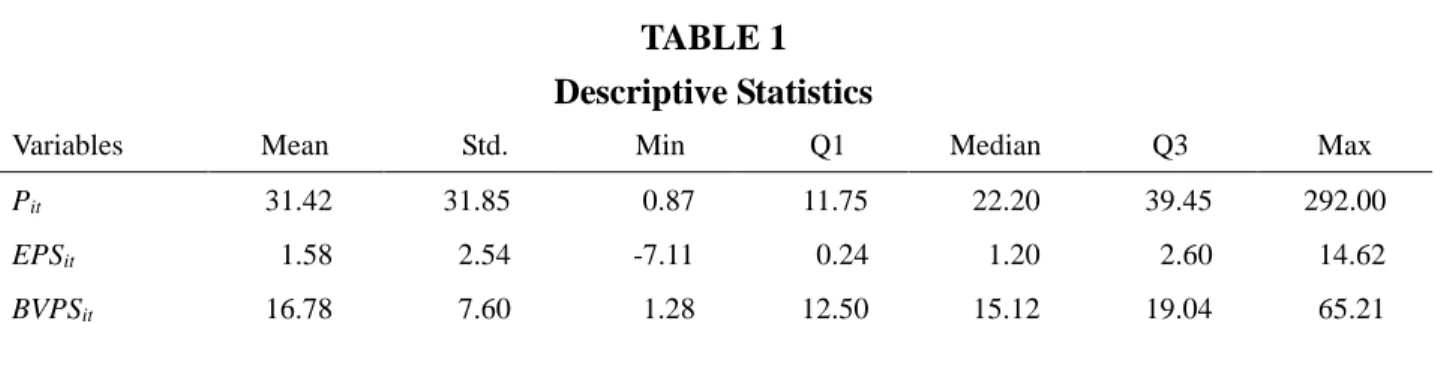

Table 1 presents descriptive statistics for variables used in the price model (1a) of scenario

120. The distributions of stock price, earnings per share and book value of equity per share are

typically skewed to right-hand tails, similar to prior literature such as Collins et al. (1997) and

Brown et al. (1999).

【Insert Table 1】

Tests on the Value Relevance of Earnings and Book Value of Equity: Adjusted R2 of

Cross-sectional Regressions

Figure 1 shows the trend in joint (PANEL A) and incremental (PANELB) explanatory

power of earnings and book values of equity across time for scenario 1. In Panel A of Figure 1,

the joint value relevance of financial statements generally shows an upward trend in the

Developing Period, especially during 1990–1996, but this increasing trend seems to cease in the

IFRS-Convergence Period. Two sudden decreases (1998–1999 and 2008–2009) coincide with the

East Asian and global financial crisis respectively. However, percentage of such a decline is

small, and joint adjusted R2 is still over 50%. In Panel B of Figure 1, the incremental relevance

of earnings per share (EPS) during 1990–1997 exhibited a steady upward trend, whereas the

24

incremental relevance of book value of equity per share (BVPS) did not show such trend.

However, the incremental relevance of EPS started to go down gradually from 2000 on, whereas

that of BVPS showed a slight growth. Combined with the results of the IFRS-Convergence

Period in Panel A of Figure 1, although the incremental value relevance of BVPS is not as high

as that of EPS, it shows the trend that information on income statements is being replaced by that

on the balance sheets. The effect of changing focus in accounting principles evidently reflects in

the financial reports.

【Insert Figure 1】

Panel A of Table 2 shows the estimated coefficients and joint, separate, and incremental

adjusted R2 of the price model for Scenario 1 (full sample). Regression coefficients are all

positive and significant except the book value of equity of equation (1a) in 2000. This indicates

that financial statements are value relevant generally and investors use such information.

In order to investigate whether separate value relevance of earnings and book value of

equity increase over the past two decades, we calculate the incremental relevance of earnings and

book value of equity as demonstrated in section Ⅲ. Panel B of Table 2 lists the results of

regressing adjusted R2 on time variables (equation 2a) for the years included in Scenarios 1, 2,

25

and 3. For joint adjusted R2 (Joint_R2), the coefficients of Year are positive and statistically

significant at the 0.01 level in all scenarios. This indicates an increasing trend of value relevance

in earnings and book value of equity in our sample period. The incremental adjusted R2

(EPS_IncrR2 and BVPS_ IncrR2), however, do not show any significant trend for the time

periods included in Scenario1, 2, and 3 respectively.

In Panel C of Table 2, we further divide sample period into two sub-periods, 1990–1999

(belongs to the Developing Period) and 2000–2011 (belongs to the IFRS-Convergence Period).

For Joint_R2, the significantly increasing trend in the Developing period does not change.

However, we do not find any trend in the IFRS-Convergence Period. For incremental adjusted R2,

EPS_IncrR2 exhibits a significantly upward trend in the Developing Period, but switch to a

significantly downward trend in the IFRS-Convergence Period in all scenarios; in contrast,

BVPS_ IncrR2 reported a statistically insignificant downward trend during the Developing

Period, but started its significantly increasing trend in the IFRS-Convergence Period in all

scenarios.

Overall, there are two main findings from the results above. First, the increasing trends of

Joint_R2 in Panel B of table 2 are primarily driven by increases of value relevance in the

Developing period, this results are consistent with prior literature that financial reporting system

26

and the law environments (Ball et al. 2000, 2003; Leuz et al. 2003; Lang et al. 2006; Bradshaw

and Miller 2008). Compared with the vacuity before 1990, U.S. GAAP has constituted the

infrastructure of twGAAP in the Developing Period. Key accounting standards, such as

long-term investment in equity securities, pensions, startup period, disclosure on segment

information, income taxes, interim financial reports, earning per share, and business

combinations, had been promulgated or revised during this period. The marginal benefits of

convergence with IFRS are limited. Second, the opposite movements between EPS_IncrR2 and

BVPS_Incr R2 in the IFRS-Convergence Period demonstrate the replacement effect of

accounting principles switching focus from income statement to balance sheet, consistent with

the preference of TFASC of switching from the revenue/expense view to the asset/liability view. 【Insert Table 2】

Tests on the Value Relevance of Earnings and Book Value of Equity: Abnormal Pricing

Errors

Considering problems that may occur while comparing adjusted R2 over different samples

(in section Ⅲ), we further employ the abnormal pricing errors suggested by Gu (2007) to

analyze the value relevance of financial statements for the last two decades in Taiwan’s history of

27

We first examine whether the linear proportionality assumption between pricing errors and

prices is valid or not. We pool all observations across years and divided them into ten classes

based on the absolute fitted value of stock prices. For each class, we calculate the normal pricing

error (the benchmark) which is the mean of the absolute value of the residuals in that class. The results are summarized in Table 3. We notice that (1) a positive association between mean Pˆ

and normal pricing errors is observed (except class 2), showing that the scale effect of pricing

errors does exist in the price model; (2) the increase in the pricing errors is not proportional to

stock price. For example, the scale measures of deciles 10 and 1 are approximately 19:1; yet the

pricing errors are only slightly more than 3.6:1 (Table 3). This indicates that the assumption that

pricing errors are linearly proportional to the stock prices is not valid. In other words, using

standardized pricing errors to interpret value relevance may lead to biased conclusions. 【Insert Table 3】

Figure 2 depicts the temporal changes of the abnormal pricing errors in years 1990–2011 for

the price model (1a). Notice that the abnormal pricing errors exhibit a downtrend from 1990 to

1996, and a sudden up and a down happen in 1999 and 2008 respectively (notice that the lower

the abnormal pricing errors was, the higher the value relevance would be). This result is

28

and accounting numbers may be affected by unusual economic conditions. 【Insert Figure 2】

Panel A of Table 4 shows the regression results of abnormal pricing errors in three scenarios

under the price model. All slope coefficients are negative and statistically significant. These

results are generally consistent with the method using adjusted R2 comparison of cross-sectional

regression. Panel B of Table 4 further divides the sample period into two sub-periods to test the

trend of abnormal pricing errors in each sub-period. The slope coefficients (b1) in the Developing

Period are all negative and statistically significant in two of the three scenarios. In the

IFRS-Convergence Period, however, the slopes (b1+b3) turn to be positive but are not significant

in all scenarios.

Overall, using abnormal pricing errors suggested by Gu (2007), we find evidence that the

strategy selected by TFASC increase only the value relevance of financial statements in the

Developing Period. The consistent results between adjusted R2 and abnormal pricing error

measures strengthen our inferences.

29

V. Robustness Tests

In this section, we conduct three additional robustness tests. First, we use return model to

check whether the short-term relations between stock returns and financial statement numbers

are similar to long-term relations of the price model. Second, we investigate the effects of

nonrecurring items on value relevance of the price model. Finally, instead of using balance sheet

date as the event date, we use the stock price on the regulatory final announcement dates of

annual financial reports (four months after the balance sheet date) as dependent variable in the

price model.

Short-term Relations between Stock Price and Financial Statements- the Return Model

We use the following model suggested by Barth et al. (2001) and employed in Gu (2007)21:

t i t i t i t i t i t i t i P EPS P BVPS P P, / , 1

0

1 , / , 1

2 , / , 1

, (4a)Equation (4a) is referred as the return model.

Similar to the price model, we decompose adjusted R2 in equations (4b) and (4c) to

investigate whether the incremental explanatory powers of changes in earnings and book value

of equity would respectively change over time22.

21 Mathematically, (4a) is just the first-differenced equation of (1a), and then be deflated by 1 ,t i

P .

22 In the return model, we do not use abnormal pricing errors to compare value relevance over years. Take Scenario

1 for example, except measures in decile 10 ( P /ˆ P =1.278, normal pricing errors=0.717), we do not find a positive association between normal pricing errors and corresponding mean P /ˆ P , this result suggests that methods that control for scale effect in return model is not applicable to our sample.

30 t i t i t i t i t i P EPS P P, / , 10 1 , / , 1 , (4b) t i t i t i t i t i P BVPS P P, / , 10 1 , / , 1, (4c) where

ΔPi,t = the price of a share of firm i at the end of year t minus the price of

a share of firm i at the end of year t-1.

ΔEPSit = the earnings per share of firm i during the year t minus the

earnings per share of firm i during the year t-1.

ΔBVPSit = the book value of equity per share of firm i at the end of year t

minus the book value of equity per share of firm i at the end of

year t-1.

Pi,t-1 = the price of a share of firm i at the end of year t-1.

Untabulated results indicate that, for joint adjusted R2 (Joint_ 2

R ), there are no significant

trends in the whole or sub-periods for three scenarios. Although we find consistent increasing

trends for BVPS_ Incr 2

R in the IFRS-Convergence Period, they are not statistically significant

in all scenarios. Most importantly, the replacement effects between BVPS_ Incr 2

R and

EPS_Incr 2

R do not exist in the IFRS-Convergence Period. Overall, we do not find consistent

31

relations between accounting numbers in explaining return (short term) and stock price (long

term), or increasing volatility of stock returns compared to stock price as suggested by Francis

and Schipper (1999).

The Cross-sectional Effects of Nonrecurring Items

Collins et al. (1997)document that the value relevance of earnings is lower when the

incidence of nonrecurring items is higher. The impact of nonrecurring items on our result will

depend on the magnitude of these items and their directional impact on earnings. Items which are

larger in absolute terms will have a greater dampening effect on the adjusted R2 from the

cross-sectional valuation model. Nonrecurring items which reduce earnings should dampen the

strength of association between earnings and stock prices further since they increase the

possibility of losses. However, this problem does not result in significant influence on our

original study. For example, among the 10,037 firm-year observations under the price model in

Scenario 1 (full sample), absolute value of total nonrecurring items only account for 0.14%

percent of total after-tax earnings. The impacts of nonrecurring items on the value relevance of

earnings may be ignored. Therefore, the possibility that the replacement effect of incremental

value relevance between earnings (decreasing) and book value of equity (increasing) during the

IFRS-Convergence Period is due to more frequent occurrence of nonrecurring items could be

32

Using Stock Prices on the Final Announcement Dates of Annual Financial Reports

In previous models, we conduct our tests by using the stock prices at the yearend. However,

the deadline of submitting annual financial reports to Taiwan’s SFB for listed companies is April

30. To ensure accounting information is in the public domain, we reconduct our tests by using

the stock prices in the end of the fourth month after fiscal yearend. The regression results are

shown in Table 5 and 6. The sample sizes for Scenarios 1, 2, and 3 are 10,285, 8,455, and 7,334

respectively. Except two insignificant but identical sign coefficients (BVPS_ IncrR2 in Scenario

3, Panel B of Table 5 and Joint_AbPerr in Scenario 1, Panel A of Table 6), the results are

basically consistent with those using stock prices at the yearend. Overall, our findings that the

increasing trends in value relevance of the price model and the replacement effect between

BVPS_ IncrR2 and EPS_IncrR2 are robust when using stock prices on the final announcement

dates of annual financial reports in Taiwan.

【Insert Table 5 and 6】

VI. Conclusion and Discussion

In this study, we investigate the trend of accounting quality for firms listed in the Taiwan

Stock Exchange Corporation during 1990–2011. As mentioned above, before 2000, twGAAP

33

with IFRS. This strategic swift is no doubt seminal. By focusing on the important dimension of

accounting quality, value relevance of financial statements, this study try to verify if TFASC has

succeeded in improving accounting quality of public firms in Taiwan.

We use two measures to examine the changes in joint value relevance of earnings and book

value of equity in the price model during 1990–2011: adjusted R2 comparison of cross-sectional

regression and abnormal pricing errors proposed by Gu (2007). We also decompose adjusted R2

to investigate whether the incremental explanatory powers of earnings and book value of equity

would respectively change over time. In terms of joint value relevance, the empirical findings

show that, although there is a statistically increasing trend during the whole period, it is primarily

driven by increases of value relevance in the Developing period. Due to U.S. GAAP has been the

infrastructure of twGAAP in the Developing Period, the results are consistent with prior

literature showing that financial reporting system is a function not only of accounting standards,

hence the marginal benefits of convergence with IFRS are limited. In terms of incremental value

relevance, the incremental relevance of earnings exhibits a significant downward trend during

the IFRS-Convergence Period, yet the incremental relevance of book value of equity reports a

significant upward trend in the meantime. This indicates that the incremental relevance of

earnings is slowly being replaced by that of book value of equity. However, consistent evidence

34

accounting numbers in explaining stock price in the short term, or increasing volatility of stock

returns suggested by Francis and Schipper (1999). Overall, empirical results in this study

indicate that, although convergence with IFRS does not lead to a further increase in the joint

value relevance of financial statements, the replacement effect in the IFRS-Convergence Period

show that at least the efforts of TFASC to stress the relevance of balance sheet have been paid

off.

There are some countries still in the stage of limited convergence with IFRS (e.g., the U.S.,

Japan, and India), and one of the possible alternatives is to adopt a “country-specific version of IFRS” (Hail et al. 2010). Taiwan’s unique standard setting history provides an environment to test the strategy. Specifically, in the context that a country had already followed a set of high

quality accounting standards, convergence with IFRS cannot significantly improve the joint

value relevance of financial statements for investors. Although convergence with IFRS may

bring other qualitative characteristic benefits (for example, increases in comparability between

domestic and foreign companies’ financial statements), however, countries with larger economic

size continuously using domestic standards still have the ability to attract international

investment and trade (Ramanna and Sletten 2013). Thus, comparability of financial statements

may be not a decisive concern in determining convergence with or adoption of IFRS. The

35

regulators.

There are some caveats to note here. First, to what extent our conclusions from Taiwan can

generalize to firms in other countries is not clear. Every country has its own unique institutional

features as well as economic development stage. Findings in emerging markets like Taiwan may

not be necessarily applicable to developed markets like the U.S. Second, as prior literature (e.g.,

Collins et al. 1997; Francis and Schipper 1999; Francis et al. 2002) has suggested, there may be

many factors influencing the magnitude of value relevance. Although we try to consider some of

them in this study (incidence of negative earnings, stability of economics, and nonrecurring

items), some omitted variables may still exist. Therefore, the findings of this study should be

interpreted with caution. Finally, we provide evidence with only one dimension of accounting

quality (i.e., value relevance), and it cannot substitute for a comprehensive quality analysis.

Naturally, this study cannot prove which one is better between convergence with and adoption of

36

APPENDIX

We use the abnormal pricing errors suggested by Gu (2007) to examine the value relevance

of earnings and book value of equity. The abnormal pricing errors are estimated as follows:

Step 1: Run the price model (1a) each year and find the residuals for each firm.

Step 2: Classify all absolute fitted values of stock prices/returns ( Pˆ ) across years into 10 classes

according to the size.

Step 3: For each class, normal pricing errors (benchmarks) are mean value in that class, calculated as

ii /n, where n is the number of observations of the class.Step 4: Each individual observation’s abnormal pricing error is calculate as the absolute value of difference between i and normal (benchmarks) pricing error.

Step 5: Then, we average the individual abnormal pricing errors of year t to generate the abnormal pricing errorAbPerrt.

37

REFERENCES

Ali, A., and L. Hwang. 2000. Country-specific factors related to financial reporting and the value relevance of accounting data. Journal of Accounting Research 38 (1): 1–21.

Armstrong, C. S., M. E. Barth, A. D. Jagolinzer, and E. J. Riedl. 2010. Market reaction to the adoption of IFRS in Europe. The Accounting Review 85 (1): 31–61.

Ball, R., S. P. Kothari, and A. Robin. 2000. The effect of international institutional factors on properties of accounting earnings. Journal of Accounting and Economics 29 (1): 1–51.

Ball, R., A. Robin, and J. S. Wu. 2003. Incentives versus standards: Properties of accounting income in four East Asian countries. Journal of Accounting and Economics 36 (1-3): 235–270.

Barth, M. E., W. H. Beaver, and W. R. Landsman. 2001. The relevance of the value-relevance literature for financial accounting standard setting: Another view. Journal of Accounting and Economics 31 (1–3): 77–104.

Barth, M. E., W. R. Landsman, and M. H. Lang. 2008. International accounting standards and accounting quality. Journal of Accounting Research 46 (3): 467–498.

Barth, M. E., W. R. Landsman, M. H. Lang, and C. Williams. 2012. Are IFRS-based and US GAAP-based accounting amounts comparable? Journal of Accounting and Economics 54 (1): 68–93.

Basu, S. 1997. The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics 24 (1): 3–37.

Bradshaw, M.T., and G. S. Miller. 2008. Will harmonizing accounting standards really harmonize accounting? Evidence from non-US firms adopting US GAAP. Journal of Accounting, Auditing and Finance 23 (2): 233–263.

Brown, S., K. Lo, and T. Lys. 1999. Use of 2

R in accounting research: Measuring changes in value relevance over the last four decades. Journal of Accounting and Economics 28 (2): 83–115.

Chang, J. 1999. The Decline in Value Relevance of Earnings and Book Value. Working paper, University of Pennsylvania.

Chen H., Q. Ting, Y. Jiang, and Z. Lin. 2010. The role of International Financial Reporting Standards in accounting quality: Evidence from the European Union. Journal of International Financial Management and Accounting 21 (3): 220–278.

Chi, S. 2009. Simultaneous presence of different domestic GAAPs and investors’ limited attention bias in U.S. equity Markets: Implications for convergence. Working paper, 2010 AAA Financial Accounting and Reporting Section.

Collins, D. W., E. L. Maydew, and I. S. Weiss. 1997. Changes in the value-relevance of earnings and book values over the past forty years. Journal of Accounting and Economics 24 (1): 39–67.

Core, J.E., W.R. Guay and A.V. Buskirk. 2003. Market valuation in the new economy: An investigation of what has changed. Journal of Accounting and Economics 34 (1–3): 43–67.

38

Daske, H., L. Hail, C. Leuz, and R. Verdi. 2008. Mandatory IFRS reporting around the world: Early evidence on the economic consequences. Journal of Accounting Research 46 (5): 1085–1142. Daske, H., L. Hail, C. Leuz, and R. Verdi. 2013. Adopting a label: heterogeneity in the economic

consequences around IAS/IFRS adoptions. Journal of Accounting Research 51 (3): 495–547. De George, E. T., C. B. Ferguson, and N. A. Spear. 2013. How much does IFRS cost? IFRS adoption and

audit fees. The Accounting Review 88 (2): 429–462.

Drake, M. S., L. A. Myers, and L. Yao. 2010. Are Liquidity Improvements Around the Mandatory Adoption of IFRS Attributable to Comparability Effects or to Quality Effects? Working paper, 2010 AAA Financial Accounting and Reporting Section.

Easton, P. 1985. Accounting earnings and security valuation: Empirical evidence of the fundamental links. Journal of Accounting Research 23 (Supplement): 54–77.

Ely, K., and G. Waymire. 1999. Accounting standard setting organizations and earnings relevance: longitudinal evidence from NYSE common stock, 1927-93. Journal of Accounting Research 37 (2): 293–317.

Ewert, R., and A. Wagenhofer. 2009. Earnings quality metrics and what they measure. Working paper, University of Graz.

Feltham, G. A., and J. A. Ohlson, 1995. Valuation and clean surplus accounting for operating and financial activities. Contemporary Accounting Research 11 (2): 689–731.

Francis, J., and K. Schipper. 1999. Have financial statements lost their relevance? Journal of Accounting Research 37 (2): 319–352.

Francis, J., K. Schipper, and L. Vincent. 2002. Earnings announcements and competing information. Journal of Accounting and Economics 33 (3): 313–342.

Goldberger, A. 1991. A Course in Econometrics. Boston: Harvard University Press.

Gu, Z. 2007. Across-sample incomparability of R2 and additional evidence on value relevance changes over time. Journal of Business Finance and Accounting 34 (7&8): 1073-1098.

Hail, L., C. Leuz, and P. Wysocki. 2010. Global accounting convergence and the potential adoption of IFRS by the U.S. (Part II): Political factors and future scenarios for U.S. accounting standards. Accounting Horizons 24 (4): 567–588.

International Accounting Standards Board (IASB). 2012. Who We Are and What We Do. Available at:

http://www.ifrs.org/The-organisation/Documents/WhoWeAre2012MarchEnglish.pdf

Joos, P. P. M., and E. Leung. 2013. Investor perceptions of potential IFRS adoption in the United States. The Accounting Review 88 (2): 577-609.

Kim, J-B., J. Tsui, and C. H. Yi. 2011. The voluntary adoption of International Financial Reporting Standards and loan contracting around the world. Review of Accounting Studies 16 (4): 779–811. Kim J-B., X. Liu, and L. Zheng. 2012. The impact of mandatory IFRS adoption on audit fees: Theory and

39

Kim, J-B., and H. Shi. 2012. Voluntary IFRS adoption, analyst coverage, and information quality: International evidence. Journal of International Accounting Research 11 (1): 45–76.

Lang, M. H., J. S. Raedy, and W. Wilson. 2006. Earnings management and cross listing: Are reconciled earnings comparable to US earnings? Journal of Accounting and Economics 42 (1–2): 255–283. Leuz, C., D. Nanda, and P. Wysocki 2003. Earnings management and investor protection: An

international comparison. Journal of Financial Economics 69 (3): 505–527.

Lev, B., and P. Zarowin. 1999. The boundaries of financial reporting and how to extend them. Journal of Accounting Research 37 (2): 353–385.

Li, S. 2010. Does mandatory adoption of International Financial Reporting Standards in the European Union reduce the cost of equity capital? The Accounting Review 85 (2): 607–636.

PricewaterhouseCoopers LLP (PwC). 2012. IFRS Adoption by Country. Available at:

http://www.pwc.com/en_US/us/issues/ifrs-reporting/publications/assets/pwc-ifrs-by-country-apr-2 012.pdf

Ramanna, K., and E. Sletten. 2013. Network Effects in Countries’ Adoption of IFRS. Working paper, Harvard Business School.

Securities and Exchange Commission (SEC). 2010. Commission Statement in Support of Convergence and Global Accounting Standards. Release No. 33-9109. Washington, DC: SEC.

Securities and Exchange Commission (SEC). 2012. Work Plan for the Consideration of Incorporating International Financial Reporting Standards into the Financial Reporting System for U.S. Issuers: Final Staff Report. Washington, DC: Government Printing Office.

Theil, H. 1971. Principles of Econometrics. New York: John Wiley.

Yip, R. W. Y., and D. Young. 2012. Does mandatory IFRS adoption improve information comparability? The Accounting Review 87(5): 1767-1789.

40 TABLE 1 Descriptive Statistics

Variables Mean Std. Min Q1 Median Q3 Max

Pit 31.42 31.85 0.87 11.75 22.20 39.45 292.00

EPSit 1.58 2.54 -7.11 0.24 1.20 2.60 14.62

BVPSit 16.78 7.60 1.28 12.50 15.12 19.04 65.21

This table presents descriptive statistics for variables used for the following cross-sectional price model of scenario 1 (full sample, N=10,037):

(1a) Sample period: 1990–2011.

Variable Definitions:

Pit = the price of a share of firm i at the end of year t;

EPSit = earnings per share of firm i for year t;

BVPSit = the book value of equity per share of firm i at the end of year t; it

it it

it EPS BVPS