策略型態對廣範圍管會系統、工作資

訊認知與管理績效之關聯性的影響

The Impact of Strategy Type on the Relationships among

Broad Scope Management Accounting System, Job

Information Perceptions, and Managerial Performance

鍾紹熙1 Shao-Hsi Chung

美和技術學院 企業管理學系

Department of Business Administration, Mei-Ho Institute of Technology

倪豐裕 Feng-Yu Ni

國立中山大學 企業管理學系

Department of Business Administration, National Sun Yat-Sen University

蘇英芳 Ying-Fang Su

國立中山大學 企業管理學系

PhD. of Business Administration, National Sun Yat-Sen University

邱炳乾 Bing-Chyan Chiou

國立屏東商業技術學院 財務金融系

Department of Finance, National Pingtung Institute of Commerce

蘇錦俊 Chin-Chun Su

高苑科技大學 國際商務系

Department of International Business, Kao-Yuan University

摘要:本研究主要目的,在探討廣範圍管理會計系統與管理績效之關係,是 否受到工作攸關資訊認知的中介影響,以及廣範圍管理會計系統的使用程 度、廣範圍管理會計系統和工作攸關資訊認知以及工作攸關資訊認知和管理

1 Corresponding author: Department of Business Administration, Mei-Ho Institute of

Technology, Pingtung, City, Taiwan. E-mai: [email protected] The authors thank two anonymous reviewers for their treasured opinions.

績效的聯結關係,是否受到不同策略型態的影響。為驗證這些關係,本研究 使用路徑分析法,並採問卷調查法進行研究,研究對象係台灣地區電子產業 上市 (櫃) 公司的廠長及其下屬員工。研究結果發現,廣範圍管理會計系統 對於管理績效之影響,並非直接而係完全經由工作攸關資訊認知的中介效 果,尤其在企業傾向差異化策略時,此完全中介效果會更為明顯。 關鍵詞:廣範圍管理會計系統;工作攸關資訊認知;管理績效;策略型態

Abstract:The main purpose of this study is to examine the effect of perception of

job- relevant information (PJRI) as an intervening variable between broad scope management accounting system (broad scope MAS) and managerial performance. Further, this study also examines the impact of strategy type on the level of using broad scope MAS and the relationships between broad scope MAS and PJRI, and between PJRI and managerial performance. The results, based on path analysis and a questionnaire survey of plant managers and their subordinate in Taiwan’s public electronic firms, demonstrate that broad scope MAS affects managerial performance, not directly, but completely through PJRI. In particular, the full mediating effect of PJRI is more pronounced when firms tend to adopt a differentiation strategy. However, when they tend to adopt the low-cost strategy, the relationship between broad scope MAS and PJRI disappears.

Keywords: Broad Scope Management Accounting System; Perception of

Job-Relevant Information; Managerial Performance; Strategy Type

1. Introduction

In face of technological advancement and global competitions, corporate managers are working in an increasingly complicated environment. To cope with this highly competitive environment, they should be given adequate information (Galbraith, 1973). Management accounting system (MAS) is intended to help managers access and use management accounting information necessary for accomplishing goals of their work, so it can effectively enhance their managerial performance (Baines & Langfield-Smith, 2003; Chong & Chong, 1997). However,

the simple and direct relationship between MAS and managerial performance has been questioned by many previous researchers (Chenhall & Brownell, 1988; Gul, 1991; Mia & Chenhall, 1994). They have provided two different perspectives. In one perspective, the relationship between the two is considered as moderated by certain contextual factors, such as environmental uncertainty, task uncertainty, organizational structure, and job properties (Chia, 1995; Chong, 1996; Gul & Chia, 1994; Mia & Chenhall, 1994). In the other, it is influenced by certain intervening factors, such as perception of role clarity, perception of job-relevant information, and perception of job stress (Hall, 2008; Kren, 1992; Shields, Deng & Kato, 2000).

An MAS provides information necessary to decision making, including cost accounting information, product price, and profit information (Tiessen & Waterhouse, 1983). The information it provides can be classified into broad scope information and narrow scope information. The broad scope MAS information includes external (e.g. customer preference, competitor activity, and technology development), non-financial (e.g. yield, defect rate, and machine operating efficiency), and future-oriented information (e.g. probability that a new law is legislated), while the narrow scope MAS information includes internal, financial, and historical information (Chenhall & Morris, 1986). This study focuses on the broad scope MAS information and uses perception of job-relevant information (PJRI) as a mediator variable to explore the relationship between broad scope MAS and managerial performance. Besides, the moderating effect of strategy type (differentiation and low-cost) on the relationship between broad scope MAS and managerial performance is also examined. Thus, the motivation behind this study is to investigate the practical correlation between broad scope MAS and managerial performance using a mediator variable (PJRI) and a moderator variable (strategy type). The objectives of this study are as follows: Theoretically, we aim to construct a relationship model of broad scope MAS and managerial performance with consideration of a mediator variable and a moderator variable. Practically, we expect to provide enterprises with some suggestions on how to make use of broad scope MAS to improve managerial performance.

hypotheses are presented in Section 2. Research methods are explained in Section 3. Empirical results and analysis are detailed in Section 4. Finally, conclusions and research limitations are proposed in Section 5.

2. Literature Review and Hypotheses

2.1 The Relationship Between Broad Scope MAS and

Managerial Performance

To find out whether broad scope MAS can effectively enhance managerial performance, previous researchers usually adopted the contingency theory to test the effectiveness of broad scope MAS, with no consideration of the effect of any mediator. For instance, Mia and Chenhall (1994) examined the managerial performance of different functional departments of an enterprise using broad scope MAS. They argued that broad scope MAS is more effective for the marketing department than for the production department. Their argument was empirically supported. Gul and Chia (1994) explored the effect of perceived environmental uncertainty, decentralization, and broad scope MAS on managerial performance. Results of their study indicated that only when the perceived environmental uncertainty is high, use of decentralization and broad scope MAS has a positive effect on managerial performance. Chong (1996) investigated the effect of broad scope MAS on managerial performance at different levels of task uncertainty. Results revealed that under high task uncertainty situations, high extent of use of broad scope MAS could lead to improved managerial performance; under low task uncertainty situations, high extent of use of broad scope MAS would cause information overload and reduction of managerial performance. Ni, Chuang and Chiou (2006) studied the effect of broad scope MAS on managerial performance with consideration of organizational commitment and task uncertainty. They found that heavy use of broad scope MAS could enhance managerial performance only when organizational commitment and task uncertainty are high.

2.2 The Mediation of PJRI

Many researchers of management accounting have pointed out that the effects of many MAS-related antecedent variables (e.g. performance measurement system, budgetary participation) on managerial performance require mediation of psychological perceptions (e.g. budgetary goal acceptance, perception of role clarity, perception of job-relevant information, and perception of job stress) (Hall, 2008; Kren, 1992; Shields, Deng & Kato, 2000; Zhu, Lin & Ni, 2003). For instance, Hall (2008) confirmed that the relationship between performance measurement systems and managerial performance is mediated by perception of role clarity. Kren (1992) argued that budgetary participation influences managerial performance through PJRI and also empirically validated this argument. However, so far, broad scope MAS has never been used as an antecedent to discuss how its relationship with managerial performance is affected by mediator variables. Managers usually apply broad scope MAS information to task planning and decision making (Chenhall, 2003). In this study, we define information provided by broad scope MAS as job-relevant information2 to examine the relationship between broad scope MAS and managerial performance. Besides, as suggested by Kren (1992), PJRI is a key factor affecting a manager’s use of MAS to enhance his/her performance. Hence, we set PJRI as a mediator variable to examine its relationships with the antecedent variable (broad scope MAS) and the outcome variable (managerial performance).

PJRI refers to managers’ perception of the degree to which they can receive task-relevant information (Kren, 1992), such as whether they understand how to accomplish a certain task, whether they have sufficient information to make an optimal decision, and whether they can obtain important information to assist their decision of an important solution. Therefore, PJRI is a belief of managers

2 In previous studies of management accounting, organizational information was considered as

inclusive of decision-facilitating information and decision-influencing information. Decision-facilitating information is the information collected prior to making a decision. Decision-influencing information is related to managerial behavior. It is mainly used to evaluate a manager’s behavioral performance (Baiman, 1982; Tiessen & Waterhouse, 1983). Kren (1992) defined decision-facilitating information as job-relevant information. Williams and Seaman (2002) generalized the two kinds of information as managerial relevant information.

about whether they can obtain information necessary for evaluating, planning, and executing task decisions to accomplish the goal of their jobs.

From a broad scope MAS, managers can retrieve broad scope information, including future events (e.g. new legislations), external situations (e.g. threat from competitors, economic conditions), and non-financial information (e.g. market share and yield). Such information can make them believe that they have obtained sufficient information for planning and executing task decisions (Chong, 1996). In other words, broad scope MAS information elevates the degree to which managers can obtain job-relevant information according to their perceptions. Therefore, we argue that there is a positive relationship between broad scope MAS and PJRI.

Provided with sufficient information related to the environment and job, managers can reduce the interference of information gap and role ambiguity to enhance their job performance (Chenhall & Brownell, 1988; Galbraith, 1977). PJRI and role ambiguity are based on a similar concept (Kren, 1992). It can be inferred that PJRI also has positive and substantial influence on managerial performance. Thus, we propose that there is a positive relationship between PJRI and managerial performance. In sum, there is no direct relationship between broad scope MAS and managerial performance, and PJRI plays the important role as a mediator in this relationship. It is a key factor that determines whether use of broad scope MAS can enhance managerial performance. As illustrated in Figure 1, the following hypotheses are proposed.

H1: The relationship between broad scope MAS and managerial performance is

mediated by PJRI.

H1a: There is a positive relationship between broad scope MAS and PJRI.

H1b: There is a positive relationship between PJRI and managerial performance (when both broad scope MAS and PJRI are independent variables of managerial performance).

H1c: There is no direct relationship between broad scope MAS and managerial performance (when both broad scope MAS and PJRI are independent variables of managerial performance).

2.3 The Influence of Strategy Type on Relationships among Focus

Variables

Strategy refers to the courses of action and the allocation of resources necessary for carrying out the long-term goals of an enterprise (Chandler, 1962). Previous researchers have proposed varying typologies of business strategies. For instance, Miles and Snow (1978) classified strategies into prospector strategy, defender strategy, and analyzer strategy, according to market characteristics. Porter (1980) proposed three competitive strategies, namely differentiation, overall cost leadership, and focus. According to Govindarajan and Gupta (1985), corporate strategies should be positioned on a continuum between build and harvest. In academic research and corporate practices, Porter’s typology (1980) is most commonly adopted. For example, Govindarajan and Fisher (1990) applied differentiation and lost-cost strategies to explore the effects of strategy, control systems, and resource sharing on business unit performance. Van der Stede (2000) also used the same strategies to examine the effects of strategy type and past performance on budgetary control, budgetary slack, and managerial short-term orientation. Accordingly, we also classify corporate strategies into differentiation strategy and low-cost strategy in this study. Due to the fact that management accounting information is helpful for selection and execution of strategies, there is a close relationship between use of MAS and strategy type (Chenhall, 2003). To understand the effect of strategy type on the level of using broad scope MAS and relationships between broad scope MAS and PJRI, and between PJRI and managerial performance, we will use these two strategies to

Figure 1

The Relationships among Broad Scope MAS, PJRI, and Managerial Performance

Managerial Performance

H1c

H1b PJRI

examine the effect of strategy type on the above-mentioned relationships.

In an environment of high uncertainty, enterprises tend to adopt a differentiation strategy in its production (Miller, 1988; Porter, 1985). With an aim to produce unique products, managers need to understand customer preference, threat from competitors, technology development, and other external, non-financial, future-oriented information. For them, broad scope management accounting information is urgently needed (Baines & Langfield-Smith, 2003). In the study of the effect of environmental uncertainty on budgetary participation and the effect of budgetary participation on managerial performance, Kren (1992) discovered that under environmental uncertainty, managers’ high degree of budgetary participation can increase PJRI, which further enhances managerial performance. Besides, Williams and Seaman (2002) probed into the effects of management accounting and control system changes on departmental performance. They validated the full mediating effect of perception of managerial relevant information and found that it becomes more pronounced when job uncertainty is high. Therefore, we argue that when enterprises tend to adopt a differentiation strategy, their managers will have a high level of use of broad scope MAS. Besides, despite the adoption of the differentiation strategy, there is no direct relationship between broad scope MAS and managerial performance.

When a differentiation strategy is employed, managers’ heavy use of broad scope MAS can help them acquire necessary broad scope management accounting information (Bouwens & Abernethy, 2000). With sufficient broad scope information, such as those involved in budgetary participation, managers will have a higher degree of PJRI and thus exhibit higher managerial performance (Kren, 1992). It can be inferred that when an enterprise tend to employ a differentiation strategy, broad scope MAS is positively correlated with PJRI, and PJRI is also positively correlated with managerial performance.

In a relatively more stable environment, enterprises may tend to adopt the low-cost strategy (Miller, 1988; Porter, 1985). In this stable environment, production processes are highly standardized and specified, and managers have clear understanding of the properties of their jobs. Therefore, they do not need to highly rely on broad scope MAS (Chong & Chong, 1997) to acquire more

job-relevant information to enhance managerial performance (Chong, 1996). Meanwhile, high level of use of broad scope MAS would rather cause information overload, resulting in the loss of focus and increase of load on managers. PJRI and managerial performance will not be positively influenced. Because most of the processes have been standardized and specified, tasks can be operated like routines. Managers can only follow existing rules and processes to effectively accomplish goals of their jobs. Hence, a high degree PJRI has limited effect on improvement of managerial performance (Leblebici & Salancik, 1981). It can be inferred that when an enterprise tends to employ a low-cost strategy, the level of using broad scope MAS will not be high. Broad scope MAS has no effect on managerial performance or PJRI, and PJRI and managerial performance are also not positively correlated to a high extent.

In sum, we argue that high level of using broad scope MAS, and the relationship between broad scope MAS and managerial performance with consideration of PJRI as a mediator is more applicable to enterprises inclined to employ the differentiation strategy. In other words, the level of using broad scope MAS, the correlation between broad scope MAS and PJRI, and the correlation between PJRI and managerial performance are lower when the low-cost strategy is employed. As illustrated in Figure 2, the following hypotheses are established:

Figure 2

The Effect of Strategy Type on Broad Scope MAS and Relationships among Broad Scope MAS, PJRI, and Managerial Performance

H2: Compared with the low-cost strategy, when enterprises tend to employ the

differentiation strategy:

H2a: the level of using broad scope MAS is higher; H2a H2c H2b Strategy Type (Differentiation/Low-cost) Broad Scope MAS PJRI Managerial Performance

H2b: the positive relationship between broad scope MAS and PJRI is higher;

H2c: the positive relationship between PJRI and managerial performance is higher.

3. Research Methods

3.1 Sample Source and Data Collection

The research sample comprised of publicly listed electronic firms in Taiwan. By consulting the prospectus of the selected electronic firms, we obtained the plant address of each firm. Two questionnaires were mailed to only one plant of each firm. Before mailing the questionnaire, the researchers telephoned the personnel department of each firm to acquire consent and names of the plant manager3 and one selected subordinate of the manager. One questionnaire was mailed to the plant manager. This questionnaire was designed on the basis of three variables, including broad scope MAS, PJRI, and strategy type. The other questionnaire was mailed to the subordinate, who was required to evaluate the plant manager’s managerial performance4 using perception measurement5. The questionnaires were responded on anonymity and directly mailed to the researcher. A total of 680 firms were selected at random. Of the questionnaires returned, 124 were collected from plant managers, and 153 from subordinates. However, only 107 effective pairs of questionnaires were obtained, making the valid response rate 16%. The age, seniority, and education background of the respondents are

3 In this paper, plant manager was selected as a representative of managers of an enterprise. 4 Among the studies using perceived performance as the basis of managerial performance,

Brownell and McInnes (1986) suggested that self-evaluation should be avoided. Besides, Kim and Yukl (1995) mentioned that when evaluating the managerial performance of the superior through perception measurement, evaluation by subordinates would be better than self-evaluation of the superior. Although letting a plant manager’s performance evaluated by his/her superior is also a reasonable and effective approach in perception measurement, the superior of the plant manager (i.e. general manager) may be too busy to answer our questionnaire. Therefore, considering time and efficiency, we let the plant manager’s managerial performance evaluated by only their subordinates.

5 Perception measurement is a way to evaluate the weight of a question according to personal

provided in Appendix 1.

3.2 Measures

All the measures used in this study were extracted from questionnaires developed by previous researchers (see Appendix 2), so the content validity of these measures could be ensured. Besides, reliability of broad scope MAS and PJRI was tested using Cronbach α (1951), and the convergent validity and uni-dimensionality of these variables were evaluated using confirmatory factory analysis. All these variables (excluding strategy type) were designed to be evaluated on seven-point Likert scale. These measures are respectively explained as follows:

3.2.1 Broad Scope MAS

To measure the extent to which each plant manager uses the broad scope MAS, the scale comprising six items developed by Chenhall and Morris (1986) was adopted (Item 1 and 2 were focused on future-oriented information, Item 3 and 4 on external information, and Item 5 and 6 on non-financial information). Chenhall and Morris (1986) have verified the reliability and validity of the scale. Most of the foreign researchers on broad scope MAS also adopted this scale (Bouwens & Abernethy, 2000; Chia, 1995; Chong, 1998; Chong & Chong, 1997; Fisher, 1996; Gul, 1991; Gul & Chia, 1994; Mia & Chenhall, 1994). Besides, the majority of domestic researchers on this subject also adopted this scale (Chang & Chang, 2001; Chang, Chang & Ni 2000; Ni, Chuang & Chiou, 2006; Ni & Su, 2001). In this study, the Cronbach α of this variable was 0.77. In Chenhall and Morris (1986), it was 0.76.

3.2.2 Perception of Job-Relevant Information (PJRI)

In this study, PJRI was measured using the scale developed by Kren (1992) on the basis of information overload index introduced by O’Reilly (1980). This scale consisted of three items which can be used to evaluate whether the plant manager clearly understands how to accomplish the tasks, whether he has

sufficient information to make optimal decisions to achieve the performance goal, and whether he can obtain important information for decision making. In this

study, the Cronbach α of this variable was 0.83. In Kren (1992), it was 0.72.

3.2.3 Managerial Performance

Managerial performance was measured using the scale developed by Mahoney, Jerdee & Carroll (1965), and the result of the subordinate’s perception measurement was used as a measure of this variable (Abernethy & Brownell, 1997; Chalos & Poon, 2000; Mia & Chenhall, 1994). This scale consisted of eight sub-dimensions, including planning, investigating, coordinating, evaluating, supervising, staffing, negotiating and representing as well as one dimension of overall performance rating. Mahoney et al. (1965) pointed out that the eight sub-dimensions should be independent and account for at least 55% variance of the overall performance rating, with the remaining 45% being explained by specific job factors of managers. To verify the independency of these sub-dimensions, we used the experiential approach suggested by Pindyck and Rubinfeld (1976) to test the multicollinearity of the independent variables (i.e. eight sub-dimensions). This approach defines that multicollinearity occurs if the correlation coefficient between two independent variables is greater than the coefficient between the two variables and the dependent variable (i.e. overall performance rating). In this study, among the 28 pairs, only 4 satisfied this criterion. Brownell and McInnes (1986) and Kren (1992) obtained 3 and 4 pairs respectively, using the same approach. Hence, the eight sub-dimensions featured a certain level of independence.

We later conducted multiple regression analysis of the eight sub-dimensions to test their explanatory power for the overall performance rating. Result showed R2 = 63%, which exceeded the 55% standard6. R2 was 78% in Brownell and McInnes (1986), 68% in Chia (1996), 60% in Chong (1995), and 57% in Chong (1998). R2 = 63% indicated that the eight sub-dimensions accounted for 63% variance of overall performance rating, and the remaining 37%, as suggested by Mahoney et al. (1965), could be explained by specific job-relevant factors of managers. The dimension of overall performance rating

6 According to Brownell and McInnes (1986), the main purpose of this test is to enhance the

consisted of 63% explained by the eight sub-dimensions and 37% explained by specific job-relevant factors. This indicated that the eight sub-dimensions could be covered if only the overall performance rating was measured. Among the studies focused on the effects of MAS on managerial performance, most of those using the approach proposed by Mahoney et al. (1965) employed only one item (i.e. the overall performance rating) to measure managerial performance (Abernethy & Brownell, 1997; Brownell & McInnes, 1986; Chong, 1996; Chong & Edmund, 2002; Gul & Chia, 1994; Zhu, Lin & Ni, 2003). Therefore, in this study, we also measured managerial performance only using overall performance rating.

3.2.4 Strategy Type

To measure the strategy type that enterprises tend to employ, we adopted the one item approach developed by Govindarajan and Fisher (1990). Every plant manager would measure the percentage of total turnover (in 100%) gained from differentiation strategy and the percentage from low-cost strategy. We multiplied the percentage from differentiation strategy by 1 and the percentage from low-cost strategy by -1. The sum of the two values was then used to denote strategy type. This value should range between -1 and 1. The closer it was to 1, the more that the enterprise tended to employ the differentiation strategy; the closer it was to -1, the more that it tended to employ the low-cost strategy. We used the median (= 0) to classify the samples by strategy type. The numbers of the firms classified into the differentiation and low-cost strategy groups were 54 and 53. The difference between the two groups was further tested using independent sample t-test. A significant difference was detected (t = -11.471, p < 0.000).

3.2.5 Evaluation of Uni-Dimensionality

To ensure the uni-dimensionality of broad scope MAS and PJRI, we conducted confirmatory factor analysis of the two variables. A measurement model was constructed and LISREL was used as analytical tool. Results showed that the overall model fit was good (χ2 = 43.85, d.f. = 24, p = 0.008, χ2/ d.f. = 1.83, GFI = 0.92, CFI = 0.94, NNFI= 0.91, RMSEA= 0.088). As shown in Table 1, all the standardized factor loadings of the construct variables on items reached the

level of significance in the t-test (p < 0.01), so the scales of the variables had convergent validity (Anderson & Gerbing, 1988). Besides, all the composite reliability values and Cronbach α of the two variables also exceeded the 0.7 criterion, indicating the two variables had an acceptable level of internal consistency. Through the above analyses, we verified the uni-dimensionality of broad scope MAS and PJRI.

Table 1

Evaluation of Uni-Mimensionality

Standardized parameters

Variable Factor loading (t-value) Measurement error Composite reliability Cronbach α

Broad scope MAS 0.74 0.77

BSMAS 1 0.46 (—a) 0.79 BSMAS 2 0.62 (5.08**) 0.62 BSMAS 3 0.61 (3.43**) 0.62 BSMAS 4 0.51 (3.11**) 0.74 BSMAS 5 0.56 (3.34**) 0.68 BSMAS 6 0.61 (3.44**) 0.63 PJRI 0.85 0.83 PJRI 1 0.53 (—a) 0.72 PJRI 2 0.96 (5.82**) 0.07 PJRI 3 0.90 (5.96**) 0.19

Note: a fixed parameter. **p < 0.01.

3.3 Analysis Method

Path analysis was conducted to explore the causal relationships among broad scope MAS, PJRI, and managerial performance (as shown in Figure 1). If the causal relationship between research variables is theoretically supported, verification of the relationship through path analysis is considered as appropriate.

The purpose of path analysis is to verify whether the causal model proposed by the researcher fits practical data (Banker, Bardhan & Chen, 2008; DeGroot & Brownlee, 2006). Before estimating path coefficients, data should be standardized. The values are later computed through regression analysis (Asher, 1983). Through path analysis, correlation coefficient between two variables (total effect) can be decomposed into direct effect and indirect effect or spurious effect to judge if there is any mediator variable between the two variables.

4. Empirical Results and Analysis

Table 2 and Table 3 respectively show the descriptive statistics and the correlation matrix of the variables. As shown in Table 3, there are positive and significant relationships between broad scope MAS and PJRI, and between broad scope MAS and managerial performance. Also, there is a positive and significant relationship between PJRI and managerial performance. These findings are consistent with conclusions in several previous studies (Baines & Langfield-Smith, 2003; Chong & Chong, 1997; Kren, 1992; Williams & Seaman, 2002).

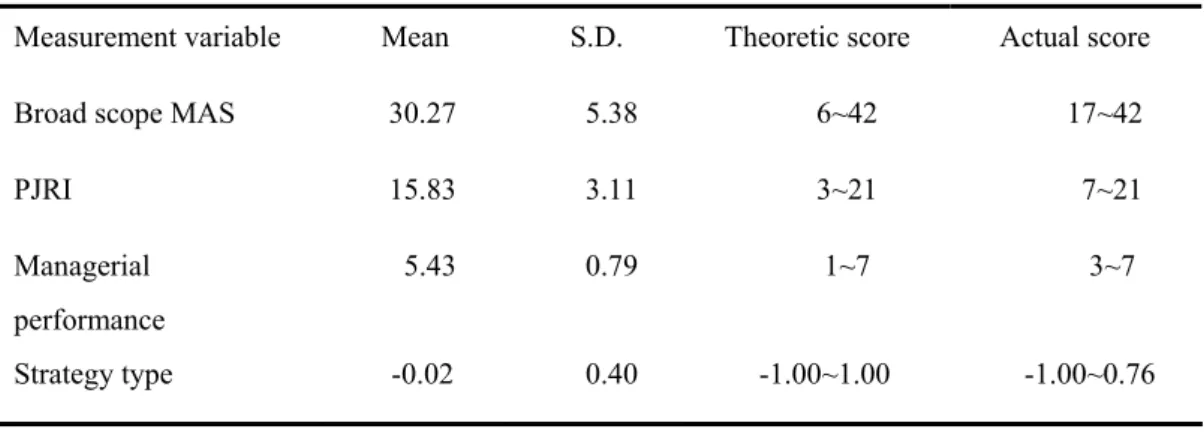

Table 2

Descriptive Statistics (n = 107)

Measurement variable Mean S.D. Theoretic score Actual score

Broad scope MAS 30.27 5.38 6~42 17~42

PJRI 15.83 3.11 3~21 7~21

Managerial performance

5.43 0.79 1~7 3~7

Table 3

Correlation Matrix (n = 107)b

Measurement variablea Broad scope MAS PJRI Managerial performance

PJRI 0.310**

Managerial performance 0.241* 0.475**

Strategy type 0.068 0.188 0.132

Note: a all variables have been standardized. btwo-tailed test was adopted.

**p < 0.01. * p < 0.05.

4.1 The Meditating Effect of PJRI

We applied path analysis to verify the effect of broad scope MAS on managerial performance through PJRI. In Figure 3, Z1 denotes broad scope MAS, Z2 denotes PJRI, and Z3 managerial performance. All these variables have been standardized. Path coefficients are denoted by pij (i.e. p21, p31, and p32). Ru and Rv represent the unexplained parts in PJRI and managerial performance, respectively. The structural equations are shown in Equation (1) and Equation (2):

Z2 =p21 Z1 + Ru (1) Z3 =p31 Z1 + p32 Z2 + Rv (2)

The solution of the path coefficients pij is derived from regression analysis and estimated using the ordinary least squares method. In fact, p21 is the standardized regression coefficient, while p31 and p32 are partial regression coefficients. Each pij denotes the influence of variable j on the variance of variable i. The variance is expressed by standard deviation as the unit. When variable j varies by one unit of standard deviation, variable i will vary by p unit of standard deviation. Besides, the residual terms Ru and Rv in the equations are hypothesized as non-correlated with the explanatory variables.

The results of Equation (1) and Equation (2) with all samples after regression analysis are presented in the third and fourth columns of Table 4, and

shown in Figure 3. The results indicate that Equation (1) and Equation (2) with all samples have reached the significant level. F-values are respectively 11.129 (p < 0.01) and 16.033 (p < 0.01). Besides, the path coefficient between broad scope MAS and PJRI (p21), and the path coefficient between PJRI and managerial performance (p32) are significant. However, the direct path between broad scope MAS and managerial performance (p31) is insignificant. Therefore, H1a, H1b, and H1c are supported. This manifests that PJRI plays the role of a mediator in the relationship between broad scope MAS and managerial performance.

Table 4

Path Analysis Result

All samples

(n = 107) strategy (n = 54)Differentiation Low-cost strategy (n = 53) Links Path

coefficient

estimate t-value estimate t-value estimate t-value Equation (1) PJRI/BSMAS p21 0.310 3.336** 0.474 3.877** 0.184 1.339 Equation (2) Managerial performance/PJR I p32 0.443 4.918** 0.477 3.580** 0.415 3.191* * Managerial performance/BS MAS p31 0.103 1.146 0.124 0.930 0.056 0.429

Equation (1) All samples, R2 = 0.096, F = 11.129**.

Differentiation strategy, R2 = 0.224, F = 15.031**.

Low-cost strategy, R2 = 0.034,F = 1.792.

Equation (2) All samples, R2 = 0.236, F = 16.033**.

Differentiation strategy, R2 = 0.298, F = 10.850**.

Low-cost strategy, R2 = 0.184,F = 5.625**.

Note: BSMAS = broad scope MAS. PJRI = perception of job-relevant information. **p < 0.01.

Later, we decomposed the correlation coefficient rij using the following equations into direct effect, indirect effect or spurious effect.

r12 = p21 (3) r13 = p31 + p32 r12 (4) r23 = p32 + p31 r12 (5)

In the above Equation (3), the value of p21 is equal to the correlation coefficient r12. This means if one variable has only one antecedent variable, the path coefficient between the two variables is the correlation coefficient between the two variables. In Equation (4) and Equation (5), the first term on the right side of the equations, pij, is the direct effect, while the second term pijrij denotes the indirect effect or spurious effect. Equation (4) decomposes the correlation coefficient between broad scope MAS and managerial performance r13 into direct effect p31 and the indirect effect p32r12. Equation (5) decomposes the correlation coefficient between PJRI and managerial performance r23 into direct effect p32 and spurious effect p31r12. This spurious effect is induced by the common antecedent

Ru Rv p31 = 0.103 PJRI (Z2) Broad Scope MAS (Z1) Managerial Performance (Z3)

Figure 3

Path Diagram for All Samples

p21 =0.310**

p32 =

0.443**

variable of PJRI and managerial performance—broad scope MAS.

The decomposition results of Equation (3), (4), and (5) with all samples are presented in the second ~ fourth columns of Table 5. The results of Equation (4) reveal that the total effect of broad scope MAS on managerial performance (0.241) can be decomposed into direct effect (0.103) and indirect effect of PJRI (0.138). The indirect effect is greater than the direct effect. According to Baron and Kenny (1986), for a mediator variable between an independent variable and a dependent variable to be supported, three conditions must be satisfied: (1) the independent variable has a significant effect on the mediator variable; (2) the independent variable has a significant effect on the dependent variable; and (3) after the dependent variable is regressed on both the independent and mediator variables, the mediator variable has a significant effect on the dependent variable, and the regression coefficient of the independent variable over dependent variable is lower than the regression coefficient under Condition (2). Moreover, in condition (3), if the regression coefficient of the independent variable over the dependent variable is also significant, the mediator has only partial mediating effect; if not, the mediator has full mediating effect.

It can be inferred from Equation (3) that when a variable has only one antecedent variable, the correlation coefficient of the two variables is the regression coefficient of the two variables. As shown in Table 3, the relationship between broad scope MAS (independent variable) and PJRI (mediator variable) is significant, and that between broad scope MAS (independent variable) and managerial performance (dependent variable) is also significant. Condition (1) and Condition (2) of mediation proposed by Baron and Kenny (1986) are satisfied. Through regression analysis of Equation (2) and the results shown in Table 4, we find that when managerial performance is regressed on both broad scope MAS and PJRI, the relationship between PJRI and managerial performance is significant (p32 = 0.443, p < 0.01), and the regression coefficient of broad scope MAS over managerial performance (p31 = 0.103, p > 0.1) is smaller than the regression coefficient (0.241) derived in Condition (2). Thus, Condition (3) is also satisfied. Besides, under Condition (3), the regression coefficient of broad scope MAS over managerial performance is not significant. This reveals that mediation

of PJRI in the relationship between broad scope MAS and managerial performance is supported, and PJRI has full mediation effect. Thus, H1 is supported. This finding is consistent with the conclusions of Kren (1992) and William and Seaman (2002) that the relationship between management accounting systems and performance is mediated by perceptions of job-relevant or managerial relevant information.

Table 5

Decomposition of the Path Analysis Model

Links All samples

(n = 107) Differentiation strategy (n = 54) Low-cost strategy (n = 53) Total effect Direct effect Indirect or Spurious effect Total effect Direct effect Indirect or Spurious effect Total effect Direct effect Indirect or Spurious effect Equation (3) PJRI/BSMA S 0.310* * 0.310** --- 0.474** 0.474** --- 0.184 0.184 --- Equation (4) Managerial performance/ BSMAS 0.241* 0.103 0.138a 0.350** 0.124 0.226a 0.132 0.056 0.076a Equation (5) Managerial performance/ PJRI 0.475* * 0.443** 0.032b 0.535** 0.477** 0.058b 0.425** 0.415** 0.010b

Note: a indirect effect. b spurious effect. BSMAS = broad scope MAS. PJRI = perception of job-relevant

information. **p < 0.01. *p < 0.05.

4.2 The Influence of Strategy Type on Relationships among Focus Variables

As shown in Table 3, strategy type is positively correlated with broad scope MAS but not to a significant extent (r = 0.068, p > 0.1). This manifests that strategy type does not influence the level to which managers use broad scope MAS. Thus, H2a is not supported. This finding is consistent with the conclusion of Baines and Langfield-Smith (2003). Baines and Langfield-Smith (2003) maintained that

when enterprises tend to employ the differentiation strategy, they will rely more on non-financial management accounting information. However, such hypothesis was not empirically supported.

Table 6

Correlation Matrix (Differentiation Strategy, n = 54)

Measurement Variable Broad Scope MAS PJRI Managerial Performance PJRI 0.474** Managerial Performance 0.350** 0.535** Strategy Type -0.068 0.106 -0.079 Note:**p < 0.01. Table 7

Correlation Matrix (Low-Cost Strategy, n = 53)

Measurement Variable Broad Scope MAS PJRI Managerial Performance

PJRI 0.184

Managerial Performance 0.132 0.425**

Strategy Type 0.216 0.284* 0.057

Note:** p < 0.01. *p < 0.05.

To test the effect of strategy type on the relationship between broad scope MAS and PJRI, and the relationship between PJRI and managerial performance, we divided the samples by median into two groups: differentiation strategy (n = 54) and low-cost strategy (n = 53). The correlation matrices of the two groups are presented in Table 6 and Table 7. We further conducted path analysis to estimate path coefficients pij. The results are shown in the fifth and sixth columns (differentiation strategy) and the seventh and eighth columns (low-cost strategy) of Table 4, and shown in Figure 4 and Figure 5.

Like for all samples, the direct link between broad scope MAS and managerial performance (p31) is insignificant for either group of different strategy. This indicates that there is no correlation between broad scope MAS and

managerial performance no matter which strategy type is employed. On the other hand, the path coefficient between broad scope MAS and PJRI (p21) becomes extremely significant (0.474, p < 0.01) when an enterprise tends to employ the differentiation strategy. This result indicates that broad scope MAS is positively correlated with PJRI. If the enterprise tends to employ the low-cost strategy, p21 becomes insignificant (0.184, p > 0.1), meaning that there is no correlation between broad scope MAS and PJRI. It can be inferred that when an enterprise tends to adopt the differentiation strategy, there will be a stronger relationship between broad scope MAS and PJRI. The result of the general linear test7 (Neter & Wasserman, 1974) shows a significant difference between path coefficients (p21) under the two strategy types (F*2,103 = 2.530 > F2,103,0.1 = 2.347). Therefore, H2b is supported. This finding is consistent with the argument of Williams and Seaman (2002) that when task difficulty is high, changes in management accounting and control system can induce a higher level of perception of managerial relevant information.

However, the analysis result does not support H2c. As shown in Table 4, the path coefficient between PJRI and managerial performance (p32) is greater under differentiation strategy (0.477, p < 0.01) than under low-cost strategy (0.415, p < 0.01). Under both strategies, PJRI is significantly correlated with managerial performance. Besides, the result of general linear test shows no significant difference between the two (F*3,101 = 0.593 < F3,101,0.1 = 2.130). This implies that the positive relationship between PJRI and managerial performance cannot be augmented through adoption of the differentiation strategy. As a result, H2c is not empirically supported. This finding is consistent with the conclusion of Kren (1992) that whether there will be a stronger relationship between PJRI and managerial performance under a high level of environmental uncertainty cannot

7 General linear test is usually applied to test the correlation between an independent variable and

a dependent variable is significant different in two groups of data, one high and one low. In the test of the difference between the regression models of the two groups, the estimate (F*) derived under the numerator’s degree of freedom K+1 and denominator’s degree of freedom n+M-2(K+1) is compared with the test value (F) (where K denotes the number of regression coefficients to be estimated; n and M are respectively the sample size of the two groups). If F* is greater than F, there is significant difference between the two regression models (Neter & Wasserman, 1974).

be verified. Besides, Williams and Seaman (2002) also mentioned that whether the relationship between perception of managerial relevant information and departmental performance can be stronger under high task uncertainty cannot be validated.

The decomposition results of Equation (3) ~ (5) are shown in the fifth ~ seventh columns (differentiation strategy) and eighth ~ tenth columns (low-cost strategy) of Table 5. As indicated by the results of Equation (4), for both groups of enterprises, broad scope MAS has a stronger indirect effect (through PJRI) than direct effect on managerial performance. Besides, the indirect effect under the differentiation strategy (0.226) is greater than the indirect effect under low-cost strategy (0.076). This is the expected result of this study: when an enterprise tends to employ the differentiation strategy, a higher degree of use of broad scope MAS can lead to a higher level of PJRI and hence improved managerial performance.

The correlation matrix in Table 6 shows that under differentiation strategy, broad scope MAS has a significant effect on PJRI and also managerial performance. Hence, Conditions (1) and (2) of mediation proposed by Baron and Kenny (1986) are met. Besides, as shown in the fifth and sixth columns of Table 4, after managerial performance is regressed on both broad scope MAS and PJRI, PJRI has a significant effect on managerial performance (p32 = 0.477, p < 0.01). The regression coefficient of broad scope MAS over managerial performance (p31 = 0.124, p > 0.1) is smaller than the regression coefficient in Condition (2) (0.350), and under the level of significant. According to Baron and Kenny (1986), PJRI has full mediating effect. Through a comparison between Figure 3 and Figure 4, we found that the path coefficient between broad scope MAS and PJRI (p21 = 0.474) and the path coefficient between PJRI and managerial performance (p32 = 0.477) obtained from enterprises using the differentiation strategy are greater than the path coefficients obtained from all samples (p21 = 0.310, p32 = 0.443). Therefore, when an enterprise tends to adopt the differentiation strategy, the full mediating effect of PJRI on the relationship between broad scope MSA and managerial performance will become more pronounced.

As shown in Table 7, under the low-cost strategy, the effect of broad scope MAS on either PJRI or managerial performance is not significant. The conditions of mediation proposed by Baron and Kenny (1986) cannot be satisfied, so mediation of PJRI is not supported. This also indicates that when an enterprise tends to employ the low-cost strategy, high level of use of broad scope MAS cannot enhance PJRI and managerial performance.

Ru Rv p31 = 0.124 PJRI (Z2) Broad Scope MAS (Z1) Managerial Performance (Z3)

Figure 4

Path Diagram for Samples of Differentiation Strategy

p21 = 0.474** p32 = 0.477** Note:**p<0.01. Ru Rv p31 = 0.056 PJRI (Z2) Broad Scope MAS (Z1) Managerial Performance (Z3)Figure 5

Path Diagram for Samples of Low-Cost Strategy

p21 =0.184

p32 =

0.415**

In sum, for all samples or those inclined to employ the differentiation strategy, the mediation of PJRI is supported. However, the effect of strategy type on the relationships among variables is only partially supported. That is to say, for enterprises inclined to adopt the differentiation strategy, there is a stronger correlation between broad scope MAS and PJRI, but the level of using of broad scope MAS is not necessarily higher, and the correlation between PJRI and managerial performance is not stronger either. The reason may be the fact that in face of uncertainty of the external environment, managers need broad scope MAS to provide external, non-financial, and future-oriented information, so the level of using broad scope MAS is not affected by the strategy type adopted by enterprises. However, when enterprises are inclined to take the differentiation strategy, they need broad scope management accounting information, including customer preference and technology development. Therefore, using broad scope MAS at a high level can lead to a high level of PJRI. In addition, the relationship between PJRI and managerial performance is extremely significant under either type of strategies, implying that managers consider job-relevant information as critical for accomplishing goals of their jobs. So, no matter which strategy is adopted, PJRI of managers has absolutely positive effect on their managerial performance.

5. Conclusions and Limitations

In this study, we probed into the relationship between broad scope MAS and managerial performance using PJRI as a mediator variable. Expected results were obtained. The relationship between broad scope MAS and managerial performance is indeed mediated by PJRI. That is to say the positive effect of broad scope MAS on managerial performance is attributed to an increased level of PJRI. Besides, PJRI has full mediating effect on this relationship, and this effect becomes more pronounced when enterprises are inclined to employ the differentiation strategy.

Theoretically, our inclusions of moderator and mediator variables in the discussion of the relationship between broad scope MAS and managerial performance better explained the relationship in a more complete model. In addition to the findings from the perspective of the contingency theory, there is full mediation of PJRI, which becomes stronger when the differentiation strategy is adopted. Practically, the following managerial implications were provided: The effect of broad scope MAS on managerial performance is supported only when managers’ PJRI can be induced. When enterprises are inclined to adopt the differentiation strategy, broad scope MAS should be adopted at the same time, so as to enhance managers’ PJRI and performance. If the low-cost strategy is adopted, managers are able to accomplish tasks without much additional information. In this case, it is not necessary to use broad scope MAS. Adoption of broad scope MAS may only cause information overload and waste of its cost. It has no positive effect on the managers’ PJRI and performance. In addition, the positive correlation between PJRI and managerial performance does not vary under different strategies. Whether the differentiation strategy or the low-cost strategy is adopted, efforts should be made to enhance managers’ PJRI to further improve their performance. All these findings can help enterprises make a better use of broad scope MAS.

Future researchers are suggested to explore whether the mediating effect of PJRI on the relationship between broad scope MAS and managerial performance would vary in different contexts (such as a decentralized organizational structure and different information processing abilities). In this study, the plant manager’s managerial performance was not evaluated by both the manager’s superior and subordinate. Possible inconsistency between the superior’s and the subordinate’s evaluations was not considered. Therefore, future researchers are advised to let a manager’s managerial performance evaluated by both the superior and subordinate when perception measurement is used.

Questionnaire survey method was adopted in this study, so there would be some general limitations of this method. Take the items designed to measure PJRI as an example. The variable’s composite reliability and Cronbach α exceeded the

0.7 standard, so the first item8 with a larger measurement error was not deleted. This was one of the limitations of this study. Besides, the subjects of this research were plant managers and their subordinates of electronic firms in Taiwan. Thus, the research results cannot be generalized and applied to different departments, industries or companies in other nations.

Appendix 1

Basic Data of The Respondents

Demographic Variable

Group Plant Manager Subordinate

23-29 Years Old 2 1.9% 29 27.1% 30-39 Years Old 18 16.8% 43 40.2% 40-49 Years Old 57 53.3% 22 20.6% 50-59 Years Old 25 23.4% 6 5.6% 60-69 Years Old 1 0.9% 4 3.7% N/A 4 3.7% 3 2.8% Age Total 107 100.0% 107 100.0% 0-5 Years 83 77.6% 80 74.8% 6-10 Years 17 15.9% 18 16.8% 11-15 Years 1 0.9% 6 5.6% N/A 6 5.6% 3 2.8% Seniority Total 107 100.0% 107 100.0% Graduate Institute 11 10.3% 12 11.2% College/University 81 75.7% 83 77.6% Senior High/Vocational School 10 9.3% 7 6.5%

Junior High School 0 0 2 1.9%

N/A 5 4.7% 3 2.8%

Education Background

Total 107 100.0% 107 100.0%

8 The measurement error in this item could be caused by respondents attributes their performance

Appendix 2 Questionnaire

Broad Scope MAS

Please evaluate the degree to which you use the following information in your work. Put in box to the box to indicate your answer.

Never Less

than Seldom

Seldom Sometimes More than

Sometimes Frequently Always

1.Information related to possible future events (e.g. new

legislation)……….… □ □ □ □ □ □ □

2.Quantification of the likelihood of future events occurring (e.g. probability estimates)……… … □ □ □ □ □ □ □ 3.Non-economic information (e.g. customer preferences, employee attitudes, labor relations, attitudes of government and consumer bodies, competitive threats, etc.)... □ □ □ □ □ □ □ 4. Information on broad factors external to your organization (e.g. economic conditions, population growth,

technological developments, etc.)……..

□ □ □ □ □ □ □

5. Non-financial

information that relates to production

information (e.g. output rates, scrap levels, machine efficiency, employee absenteeism,

etc.)……….... □ □ □ □ □ □ □

6. Non-financial

information that relates to market information (e.g. market size, growth share,

etc.)……….. …

Perception of Job Relevant Information (PJRI)

Strategy Type

Please evaluate the percentage of total turnover of your plant (in 100%) gained from the differentiation strategy and the percentage from the low-cost strategy? (Please note the explanation below)

Differentiation strategy: ( )﹪ Low-cost strategy: ( )﹪ 100﹪ Explanation:

Differentiation Strategy: The main goal of this strategy is to create certain product features. Strategies such as working out outstanding designs, providing good customer service, establishing brand awareness, and producing high-quality products can be classified as differentiation strategy.

Low-cost strategy: The main goal of this strategy is to reduce product cost to the level that competitors cannot reach.

Please evaluate the degree to which you agree each of the following questions? Put a check in the box to indicate your answer.

Strongly Disagree

Very

Disagree Disagree Neutral Agree

Very Agree

Strongly Agree 1. You are always clear about what is

necessary for you to perform well

on your job……… □ □ □ □ □ □ □

2. You have adequate information to make optimal decisions to accomplish your performance

objectives………..… □ □ □ □ □ □ □

3. You are able to obtain the strategic information necessary to evaluate

Managerial Performance

6. References

Abernethy, M. A. and Brownell, P. (1997), “Management Control Systems in Research and Development Organizations: The Role of Accounting, Behavior and Personnel Controls,” Accounting, Organizations and Society, 22(3/4), 233-248.

Please evaluate the performance of your plant manager in comparison with executives of other departments in the following aspects. Put a check in the box to indicate your answer.

Awful Very Poor

Poor Acceptable Good Very Good

Excellent

1. Goal and task scheduling………….… □ □ □ □ □ □ □ 2. Information processing and task

research … ……….…. □ □ □ □ □ □ □

3. Communication and coordination

with other departments…………..… □ □ □ □ □ □ □ 4. Appraisal of personnel and task

relevant items………..…. □ □ □ □ □ □ □

5. Supervision over personnel and task

relevant items……….… □ □ □ □ □ □ □

6. Employment of personnel……… □ □ □ □ □ □ □

7. Negotiation with external organizations (such as suppliers and

customers)……… □ □ □ □ □ □ □

8. Increase of the organizational

interest………... □ □ □ □ □ □ □

Anderson, J. C. and Gerbing, D. W. (1988), “Structural Equation Modeling in Practice: A Review and Recommended Two-Step Approach,” Psychological Bulletin, 103(3), 411-423.

Asher, R. (1983), Causal Modeling, London: Sage.

Baiman, S. (1982), “Agency Research in Managerial Accounting: A Survey,”

Journal of Accounting Literature, 1, 154-213.

Baines, A. and Langfield-Smith, K. (2003), “Antecedents to Management Accounting Change: A Structural Equation Approach,” Accounting,

Organizations and Society, 28(7/8), 675-698.

Banker, R. D. Bardhan, I. R. and Chen, T.Y. (2008), “The Role of Manufacturing Practices in Mediating the Impact of Activity-Based Costing on Plant Performance ,” Accounting, Organizations and Society, 33(1), 1-19.

Baron, R. M. and Kenny, D. A. (1986), “The Moderator-Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic and Statistical Considerations,” Journal of Personality and Social Psychology, 51(6), 1173-1182.

Bouwens, J. and Abernethy, M. A. (2000), “The Consequences of Customization on Management Accounting System Design,” Accounting, Organizations

and Society, 25(3), 221-241.

Brownell. P. and McInnes, M. (1986), “Budgetary Participation, Motivation, and Managerial Performance,” The Accounting Review, 61(4), 587-600.

Chalos, P. and Poon, M. C. C. (2000), “Participation and Performance in Capital Budgeting Teams,” Behavioral Research in Accounting, 12, 199-229. Chandler, A. D. Jr. (1962), Strategy and Structure, Cambridge, MA: MIT Press. Chang, R. D. and Chang, Y. W. (2001), “The Effects of Strategy, Organizational

Structure and Environment on the Characteristics and Performance of Management Accounting Information Systems,” Management Review, 20(4), 137-173.

Chang, R. D. Chang, Y. W. and Ni, F. Y. (2000), “The Effect of Task Attributes and AIS Characteristics on Users’ Satisfaction: An Empirical Test,”

Chenhall, R. H. (2003), “Management Control Systems Design Within Its Organizational Context: Findings from Contingency-Based Research and Directions for the Future,” Accounting, Organizations and Society, 28(2/3), 127-168.

Chenhall, R. H. and Brownell, P. (1988), “The Effects of Participative Budgeting on Job Satisfaction and Performance: Role Ambiguity as an Intervening Variable,” Accounting, Organizations and Society, 13(3), 225-233.

Chenhall, R. H. and Morris, D. (1986), “The Impact of Structure, Environment, and Interdependence on the Perceived Usefulness of Management Accounting Systems,” The Accounting Review, 61(1), 16-35.

Chia, Y. M. (1995), “Decentralization, Management Accounting Systems (MAS) Information Characteristics and Their Interaction Effects on Managerial Performance: A Singapore Study,” Journal of Business Finance

and Accounting, 22(6), 811-830.

Chong, M. L. and Edmund, W. L. (2002), “The Intervening Effects of Participation on the Relationship between Procedural Justice and Managerial Performance,” British Accounting Review, 34(1), 55-78.

Chong, V. K. (1996), “Management Accounting Systems, Task Uncertainty and Managerial Performance: A Research Note,” Accounting, Organizations

and Society, 21(5), 415-421.

Chong, V. K. (1998), “Testing the Contingency “fit” Between Management Accounting Systems and Managerial Performance: A Research Note on the Moderating Role of Tolerance for Ambiguity,” British Accounting Review, 30(4), 331-342.

Chong, V. K. and Chong, K. M. (1997), “Strategic Choices, Environmental Uncertainty and SBU Performance: A Note on the Intervening Role of Management Accounting Systems,” Accounting and Business Research, 27(4), 268-276.

Cronbach, L. J. (1951), “Coefficient Alpha and the Internal Structure of Tests,” Psychometrika, 16(3), 297-334.

DeGroot, T. and Brownlee, A. L. (2006), “Effect of Department Structure on the Organizational Citizenship Behavior–Department Effectiveness

Relationship,” Journal of Business Research, 59(10/11), 1116-1123.

Fisher, C. (1996), “The Impact of Perceived Environment Uncertainty and Individual Differences on Management Information Requirements: A Research Note,” Accounting, Organizations and Society, 21(4), 361-369. Galbraith, J. R. (1973), Designing Complex Organization, Boston, MA:

Addison-Wesley.

Galbraith, J. R. (1977), Organization Design, Boston, MA: Addison-Wesley. Govindarajan, V. and Fisher, J. (1990), “Strategy, Control Systems, and Resource

Sharing: Effects on Business-Unit Performance,” Academy of Management

Jourmal, 33(2), 259-285.

Govindarajan, V. and Gupta, A. K. (1985), “Linking Control Systems to Business Unit Strategy: Impact on Performance,” Accounting, Organizations and

Society, 10(1), 51-66.

Gul, F. A. (1991), “The Effects of Management Accounting Systems and Environmental Uncertainty on Small Business Managers’ Performance,”

Accounting and Business Research, 22(85), 57-61.

Gul, F. A. and Chia, Y. M. (1994), “The Effects of Management Accounting Systems, Perceived Environmental Uncertainty and Decentralization on Managerial Performance: A Test of Three-Way Interaction,” Accounting,

Organizations and Society, 19(4/5), 413-426.

Hall, M. (2008), “The Effect of Comprehensive Performance Measurement Systems on Role Clarity, Psychological Empowerment and Managerial Performance,” Accounting, Organizations and Society, 33(2-3), 141-163.

Kim, H. and Yukl, G. (1995), “Relationships of Managerial Effectiveness and Advancement to Self-Reported and Subordinate-Reported Leadership Behaviors from the Multiple-Linkage Model,” Leadership Quarterly, 6(3), 361-377.

Kren, L. (1992), “Budgetary Participation and Managerial Performance: The Impact of Information and Environmental Volatility,” The Accounting

Review, 67(3), 511-526.

on Information and Decision Processes in Banks,” Administrative Science

Quarterly, 26(December), 578-596.

Mahoney, T. A. Jerdee, T. H. and Carroll, S. J. (1965), “The Job(s) of Management,” Industrial Relations, 4(2), 97-110.

Mia, L. and Chenhall, R. H. (1994), “The Usefulness of Management Accounting Systems, Functional Differentiation and Managerial Effectiveness,”

Accounting, Organizations and Society, 19(1), 1-13.

Miles, R. H. and Snow, C. C. (1978), Organizational Strategy, Structure,

and Process, New York: McGraw-Hill.

Miller, D. (1988), “Relating Porter’s Business Strategies to Environment and Structure: Analysis and Performance Implications,” Academy of

Management Journal, 31(2), 280-308.

Neter, J. and Wasserman, W. (1974), Applied Linear Statistical Models, Homewood, IL: Richard D. Irwin, Inc.

Ni, F. Y. Chuang, Y. K. and Chiou, B. C. (2006), “Perceived Task Uncertainty, Organizational Commitment, Managerial Accounting Systems and Their Three-Way Interaction Effects on Managerial Performance,” Journal of

Management & Systems, 13(1), 1-14.

Ni, F. Y. and Su, J. T. (2001), “The Impact of Perceived Environmental Uncertainty, Task Uncertainty, Organizational Decentralization on the Perceived Usefulness of Management accounting Systems,” Journal of

Management & Systems, 8(2), 147-168.

O'Reilly, C. A. (1980), “Individuals and Information Overload in Organizations: Is more Necessarily Better?” Academy of Management Journal, 23(4), 684-696.

Pindyck, R. S. and Rubinfeld, D. L. (1976), Econometric Models and Economic

Forecasts, New York: McGraw-Hill.

Porter, M. E. (1980), Competitive Strategy, New York, NY: Free Press. Porter, M. E. (1985), Competitive Advantage, New York, NY: Free Press.

Shields, M. Deng, F. J. and Kato, Y. (2000), “The Design and Effects of Control Systems: Tests of Direct- and Indirect-Effects Models,” Accounting,

Tiessen, P. and Waterhouse, J. H. (1983), “Towards a Descriptive Theory of Management Accounting,” Accounting, Organizations and Society, 8(2/3), 251-267.

Van der Stede, W. A. (2000), “The Relationship between Two Consequences of Budgetary Controls: Budgetary Slack Creation and Managerial Short-Term Orientation,” Accounting, Organizations and Society, 25(6), 609-622. Williams, J. J. and Seaman, A. E. (2002), “Management Accounting Systems

Change and Departmental Performance: The Influence of Managerial Information and Task Uncertainty,” Management Accounting Research, 13(4), 419-445.

Zhu, D. S. Lin, S. M. and Ni, F. Y. (2003), “A Study of the Effect of Budgetary Goal Difficulty on the Relationships Among Budgetary Participation, Budgetary Goal Acceptance, and Managerial Performance: Manufacturing Industry in Taiwan as Example,” Journal of Management, 20(5), 1023-1043.