國際金融理論的發展

23

0

0

全文

(2) 經濟與管理論叢(Journal of Economics and Management). 2. 1. Introduction. The famous “purchasing power parity puzzle”, which refers to the issue of reconciling the high short-term volatility of real exchange rates with their high persistence, has attracted considerable research interest. The speeds at which the parity reversion reported in existing empirical studies takes place are too slow. Rogoff (1996) proposed that the substantial convergence to PPP should take one to two years. Recently, several relevant studies have tried to resolve the puzzle. Some research based on linear models of real exchange rates has applied the impulse response function to estimate the half life (Cheung and Lai, 2000; Murray and Papell, 2002). Other studies have used nonlinear models to study the purchasing power parity puzzle. According to the findings of previous studies, the speed of adjustment to a real exchange rate shock occurring in nonlinear models is faster than that in linear models (Taylor et al., 2001; Sarno et al., 2004). The above studies have all dealt with the purchasing power parity issues of developed countries. Recent studies have begun to analyze the adjustments in the real exchange rates of developing and emerging countries. Baharumshah et al. (2008) studied the real exchange rates of six Asian emerging countries. They found that the average half life for these Asian countries is 40 months. Mollick (2009) investigated the real exchange rates of seven Asian countries and five Latin American countries. He found the average half life for seven Asian countries to be 30 months and the average half life for five Latin American countries to be 24 months. Arize et al. (2010) discussed the real exchange rates of African countries. They found the average half life for African countries to be 24 months. More evidence has shown that real exchange rates may reveal nonlinearity. Thus, if the true models of real exchange rates are indeed nonlinear, then using linear ADF regression to test the unit root hypothesis of the real exchange rates will heavily lack testing power. Evidently, we have to test the unit root hypothesis based on nonlinear models of real exchange rates. Hence the application of linear models cannot completely and precisely account for the adjustment mechanism of real exchange rates. Furthermore, market frictions which exist in the international.

(3) Half Life of the Real Exchange Rate. 3. business environment cause a lack of perfect international arbitrage. However, market frictions should be interpreted as resulting not only from transportation costs and trade barriers, but also from the sunk costs of international arbitrage and the resulting tendency of traders to respond only to sufficiently large arbitrage opportunities. The absence of perfect international arbitrage in the presence of market frictions can result in the nonlinear adjustment of the real exchange rates. Hence we can use nonlinear models to characterize such market frictions. Emerging countries have more serious market frictions than developed countries. Therefore, we can use nonlinear models to more appropriately characterize the behavior of real exchange rates in emerging countries. The threshold autoregressive (TAR) model representing time series can suddenly and abruptly switch between different regimes (Tong, 1978; Tong and Lim, 1980; Tong, 1990). For many economic phenomena, the discrete adjustment may often prevail. When serious market frictions exist, economic agents do not adjust continuously. This also means that this kind of time series has heavier nonlinear phenomena. We can use the TAR models as heavier nonlinear models to characterize serious market frictions. However, many emerging countries often suffer from heavier market frictions than developed countries. While many emerging countries engage in international business, such countries evidently have the problems associated with heavier market frictions. Recent investment theory suggests that if international arbitrage involves such a degree of market frictions, then unhedgeable uncertainty can be levered up into a relatively large and sharp adjustment of real exchange rates. Thus, we can appropriately use the TAR model to characterize a more serious degree of market frictions occurring in emerging economies. For instance, in financial markets, the presence of market frictions may create bands in which asset prices can be free to fluctuate (i.e., arbitrage possibilities). If the deviation from the equilibrium exceeds the bands, agents will act to move the economy back towards the equilibrium. Hence we can apply the band threshold autoregressive model (band TAR model) to implement our study of emerging countries. Bec et al. (2004) developed a unit root test based on the band threshold autoregressive model. They assumed that the true model of time series is a band threshold autoregressive model. They applied sup likelihood ratio test statistics to.

(4) 經濟與管理論叢(Journal of Economics and Management). 4. test whether a time series had a unit root. After demonstrating the existence of stationarity, they also used sup LR test statistics to substantiate whether a time series was nonlinear. In the present study, we follow Bec et al. (2004) to apply the band TAR model to fit the real exchange rates of major emerging countries. We focus on the real exchange rates of the U.S. dollar vs. the currencies of six major emerging market countries. The empirical results of major emerging countries show that the real exchange rates of the U.S. dollar-Chinese yuan, U.S. dollar-Brazilian real, U.S. dollar-South African rand, U.S. dollar-Malaysian ringgit, U.S. dollar-Argentine peso and U.S. dollar-Thai baht are all stationary and can all be fitted by the band TAR model. Due to the nonlinearity, the traditional impulse response function analysis cannot be applied appropriately. Then, for the sake of quantifying the speed of parity reversion, we perform generalized impulse response function analysis, which was developed by Koop et al. (1996). The half-life estimate for the real exchange rate can be computed through the application of generalized impulse response analysis to the estimated band TAR model. The empirical results show that when the shock is 100%, the half lives of the dollar-Brazilian real, U.S. dollar-South African rand, U.S. dollar-Malaysian ringgit, U.S. dollar-Argentine peso and U.S. dollar-Thai baht are all below 2 years and the half lives for the real exchange rates of the U.S. dollar-Chinese yuan are just slightly larger than 2 years. This interesting finding indicates that by means of internationalization major emerging countries have done well in keeping the fluctuations in real exchange rates coherent with purchasing power parity. The remainder of this paper is organized as follows. Section 2 outlines the band TAR model and hypothesis testing for the unit root test and the threshold type nonlinearity test. We also discuss how to apply generalized impulse response function analysis to a nonlinear model to compute half-life estimates. Section 3 reports on and analyzes our empirical results. We present our conclusions in Section 4. Appendix A and Appendix B provide the precise procedures of the major methods applied to conduct the empirical study..

(5) Half Life of the Real Exchange Rate. 2. 5. The Econometric Model. We apply the band TAR model which has been discussed by Balke and Fomby (1997), Sarno et al. (2002) and Bec et al. (2004), to characterize the behavior of real exchange rates. The band-TAR model which is a specific type of three regime TAR model has an important advantage in analyzing the dynamic of the real exchange rate. While we evaluate whether any common time series have TAR-type nonlinearity, we can use the more general TAR model which includes a general two regime TAR, general three regime TAR, and other general multiple regime TAR to study the movements of such time series. In these circumstances, we can apply the model selection procedures suggested by Hansen (1997) to choose the most appropriate number of regimes and apply estimation procedures to estimate the general form of such a TAR model. Several previous studies (Wong and Li, 2001; Tsay, 2005; Medeiros and Veiga, 2009; Chen et al., 2010) have provided many arguments and examples to guarantee that even when some regime of the TAR model is nonstationary, the whole TAR model still has the possibility of being stationary. So if through model selection procedures we choose the most appropriate number of regimes for some time series to be two, we can then use the two-regime TAR process to properly model such a time series. However, when we study the behavior of the real exchange rate time series, the framework mentioned above is clearly not a proper methodology for analyzing the real exchange rate time series. When we study the impacts of market friction or a transaction cost on the fluctuations in the real exchange rate, the two-regime TAR scheme, which may be formally determined from model selection procedures, is not a good candidate to deal with this issue. Many previous studies provided the three-regime TAR scheme to analyze the effects of a transaction cost on the movements in real exchange rates. Due to the existence of a transaction cost, in the middle regime of the three-regime TAR model, the exchange rate only slightly deviates from PPP. The profit from international arbitrage is insufficient to compensate for the transaction cost. International arbitrage will not occur in the middle regime. Therefore, the behavior of the real exchange rate in the middle regime which is not interrupted by arbitrage.

(6) 經濟與管理論叢(Journal of Economics and Management). 6. follows a random walk. However, while the real exchange rate moves to the upper regime or the lower regime, international arbitrage will reverse the real exchange rate so that it comes back toward the middle regime. We can model the real exchange rate using the following general three-regime TAR model: p. μ1 + ρ1 qt −1 + ∑ α 1i Δqt −i + ε 1t , if qt −d ≤ λ1 , i =1. p. Δqt = μ 2 + ρ 2 qt −1 + ∑ α 2 i Δqt −i + ε 2 t , if λ1 < qt −d ≤ λ2 , i =1. (1). p. μ3 + ρ 3 qt −1 + ∑ α 3i Δqt −i + ε 3t , if qt −d > λ2 , i =1. where qt is the real exchange rate, which is measured by the deviation from its mean. d is the lag number of the threshold variable. λ1 and λ2 are the threshold values, i.e., the band of the regime. λ1 is the upper band, and λ2 is the lower band. The ε jt ( j = 1, 2, 3 ) are assumed to be an i.i.d. white noise sequence, i.e., ε jt ~ N (0, σ 2j ) . σ 2j is the variance of the jth regime. Brooks and Garrett (2002) applied such a general form of the three-regime TAR model to analyze the relationship between stocks and stock index futures. However, when we apply model (1) to study the impacts of transaction costs on the behavior of the real exchange rate, some restrictions must be imposed. Bec et al. (2004) used a specific form of model (1), i.e., the so-called band TAR model, to develop the unit root test for the TAR model. They assume a symmetric threshold value, i.e., λ1 = − λ , λ2 = λ , and also assume the lag order of the threshold variable to be one, i.e., d = 1 . Under these restrictions, they use classical statistical analysis to derive the asymptotic distribution of the test statistics for the unit root test. We can respectively base our analysis on classical statistical theory or Bayesian statistical theory to conduct estimations, make statistical inferences and perform tests using the TAR model. However, for the sake of proper testing and statistical inference, in classical statistical theory we must derive an asymptotic distribution of the test statistics, and in Bayesian statistical theory we must also derive a closed-form solution of the posterior distribution of the test statistics. Therefore, while we wish to apply model (1) to examine the PPP issue, we should use the.

(7) Half Life of the Real Exchange Rate. 7. specific model of Bec et al. (2004), the band TAR model, to fit the real exchange rate. Based on the more restricted model of Bec et al. (2004), we have an appropriate asymptotic distribution for the test statistics of the unit root test. Therefore, we can apply such a test to check whether the TAR model is stationary. From the economic aspect, if PPP holds, the real exchange rate must be zero based on the definition of the real exchange rate referred to later. So the symmetric threshold values λ and −λ guarantee that the center of the middle regime will coincide with PPP. As in many previous studies which apply the TAR model to study real exchange rates (Obstfeld and Taylor, 1997; O’Connell, 1998; Pippenger and Goering, 1998; Taylor, 2001; Lo and Zivot, 2001; Parsley and Wei, 2007), we also find the lag order of the threshold variable to appear to be one. In fact, the central bank often follows a foreign exchange market intervention rule based on the magnitude of the previous real exchange rate. The time series of the present real exchange rate will switch between different regimes when intervention occurs. So we can appropriately set the lag order of the threshold variable to one, i.e., d = 1 . Gourieroux and Robert (2006) proposed using a switching regime process which corresponds to the band TAR model to analyze PPP issues. In such a switching regime process, the random walk regime that is the middle regime of the band TAR model has its probability of occurrence, and the stationary regimes that are the outer regimes of the band TAR model also have their probability of occurrence. They studied the stationarity of such a switching regime process, and found that if the probability of occurrence of the random walk regime is less than one, then the time spent in the random walk regime is finite. Under this circumstance, the switching regime process is stationary. Kapetanios and Shin (2006) proposed the Wald test to directly test the linear unit root null versus the stationary three-regime self-exciting TAR model alternative, which also assumes the lag order of the threshold variable to be one. They used a Monte Carlo simulation to show that the Wald test proposed by them has more power than the traditional Dickey-Fuller test when the true time series model exhibits nonlinear stationarity. They also applied their Wald test to examine the stationarity of the real exchange rates of G7 countries. Their empirical evidence indicates that when the Dickey-Fuller test was used to perform the test, no real exchange rates could reject the null hypothesis of a linear unit root. However, when the Wald test was used to perform the test, three of.

(8) 8. 經濟與管理論叢(Journal of Economics and Management). the five real exchange rates could successfully reject the null hypothesis to favor the stationary three regime self-exciting TAR model. We can state the band TAR model of Bec et al. (2004) as follows: p. μ1 + ρ1 qt −1 + ∑ α 1i Δqt −i + ε 1t , if qt −1 ≤ −λ , i =1. p. Δqt = μ 2 + ρ 2 qt −1 + ∑ α 2 i Δqt −i + ε 2 t , if −λ < qt −1 ≤ λ , i =1. (2). p. μ3 + ρ 3 qt −1 + ∑ α 3i Δqt −i + ε 3t , if qt −1 > λ , i =1. To minimize the sum of the squared errors of the whole model (2), we can , , p ), ( j = 1, 2, 3 ). If we obtain the parameter estimates μˆ , ρˆ , αˆ , λˆ ( i = 1K J. J. JI. substitute these parameter estimates into model (2) and use actual real exchange rate observations, we can then obtain the residuals of each regime e j ( j = 1, 2, 3 ). We can use the residuals obtained above to calculate the sum of squared errors of each regime as: sse j = e′j e j ( j = 1, 2, 3 ). Then we can compute the estimated variance of each regime as: σˆ 2j = ( sse j n j − k ) ( j = 1, 2, 3 ). Here, the n j ( j = 1, 2, 3 ) are respectively the numbers of sample observations in each regime. k is the number of explanatory variables. We can deflate the nominal exchange rate by the ratio of the domestic price level to the foreign price level to define the real exchange rate. As a logarithm, the above definition can be represented as: qt = st + pt* − pt = ln( S t Pt * Pt ) . q t is the real exchange rate, and st is the nominal exchange rate, i.e., the amount of domestic currency that can be exchanged with foreign currency. q t and pt* are the domestic price level and foreign price level, respectively. We also follow Bec et al. (2004) and adopt two-step testing procedures. We firstly investigate whether or not the real exchange rates are stationary. Therefore, if the genuine model of real exchange rates can be described as model (2), we can use the following hypothesis to test the stationarity of the real exchange rates: H 01 : ρ1 = ρ 2 = ρ 3 = 0 .. (3). We apply the sup-likelihood ratio statistics to test the above hypothesis test of stationarity. When the null hypothesis of the unit root test for band TAR models is rejected, it means that the real exchange rates fitted by the band TAR models are.

(9) Half Life of the Real Exchange Rate. 9. stationary. If we substantiate this by assuming that the real exchange rates are stationary, we can then investigate whether the real exchange rates have the band threshold type of nonlinearity. That is to say, we can test whether the real exchange rates can be fitted by model (2). We can state the hypothesis of the nonlinear test as follows: H 02 : μ1 = μ 2 = μ 3 , ρ1 = ρ 2 = ρ 3 , α 1i = α 2 i = α 3i ∀i .. (4). We also apply the sup-likelihood ratio statistics to test the above hypothesis of nonlinearity. We choose the optimal threshold values λ to achieve the supreme likelihood ratio statistics LR . Hence the sup LR statistics are as follows: sup LR = sup LRT (λ ) , λ∈[ λL , λU ]. (5). where LR (λ ) = T ln(σ 2 σˆ 2 ) , σ~ 2 and σˆ 2 are the restricted and unrestricted sum of squared errors of the whole model (2), respectively, and T is the size of the sample. Chan (1991) has previously tabulated the asymptotic null distribution of the likelihood ratio test for the TAR model. Hansen (1996, 1997) and Hansen and Seo (2002) have developed the sup LM. test and supWald test to examine the. TAR-type nonlinearity. Bec et al. (2004) developed the sup LR test to investigate the stationarity of the TAR model. Although Bec et al. derived the asymptotic distribution of the sup LR test statistics to test the stationarity of the TAR model, in a finite sample the empirical distribution which is bootstrapped from actual data is still better than the asymptotic distribution. Moreover in the hypothesis testing for the linear null versus the band TAR alternative, the sup LR test statistics under the null hypothesis still have a nuisance parameter, i.e., the threshold values λ . Thus, we must apply the bootstrap method to derive the empirical distribution of the. sup LR statistics for the testing of nonlinearity. Hence we apply the bootstrap method to compute the empirical distribution of the sup LR statistics for the testing of both stationarity and nonlinearity. The Monte Carlo experiment applied by Hansen (1996) indicates that the testing procedures stated above have enough power to test. Hansen (2000) developed the distribution theory for the estimation of the TAR.

(10) 經濟與管理論叢(Journal of Economics and Management). 10. model. The distribution for the threshold value estimate is nonstandard and is composed of complex Brownian motions, but the distribution of the parameter estimates in each regime is normal. In order to measure the half life, we perform impulse response function analysis to calculate the half life of the real exchange rate. The half life is defined as the expected number of months for a PPP deviation to decay by an amount of 50%. If the model is linear, the traditional impulse response can be implemented to compute the half life. For a nonlinear model, the traditional impulse response function depends on initial conditions (history dependence) and the size and sign of the innovation (shock dependence). These are not good properties for impulse response analysis. Thus, we cannot use a traditional impulse response function to compute the half life estimates of nonlinear models. Hence Koop et al. (1996) developed a generalized impulse response function to solve how to perform impulse response analysis for nonlinear models. The generalized impulse response functions treat histories and shocks as random variables. Thus, histories and shocks, upon which the computation of the generalized impulse response function is based, are drawn from distributions. That is to say, the generalized impulse response function does not depend on particular histories and shocks. Hence, we have a well-constructed dynamic structure for a nonlinear model. The generalized impulse response functions are simulated realizations obtained by iterating the time series model, randomly drawing from the Gaussian distribution, and then averaging over the number of random draws. The generalized impulse response function can be expressed as the difference between two conditional expectations: GI q ( h, Vt , Ω t −1 ) = E[ qt + h Vt , Ω t −1 ] − E[ qt + h Ω t −1 ] ,. (6). where GI q is the generalized impulse response function of the real exchange rate qt , h is the forecasting horizon and Vt is the vector of i.i.d. random disturbances. vt is the shock that occurs in period t . vt is randomly drawn from Vt . Ω t −1 is. the information set which is used to forecast qt at time t − 1 . ωt −1 is the conditional information set at time t − 1 (reflecting the history or initial conditions of the real exchange rates) and ωt −1 is also randomly drawn from Ω t −1 . E[⋅] is the expectation operator. The above expression provides a way of measuring the.

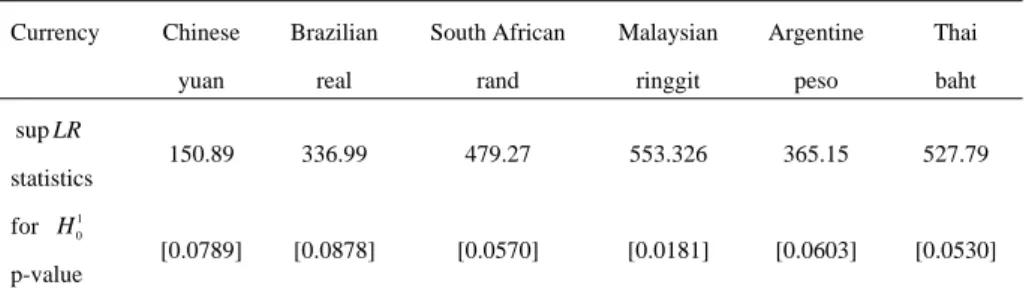

(11) Half Life of the Real Exchange Rate. 11. effect of the shock on the difference between the two conditional means of the real exchange rates.. 3 3.1. Empirical Results Data. We extract monthly data for the U.S.A., China, Brazil, South Africa, Malaysia, Argentina and Thailand from the International Monetary Fund’s International Financial Statistics database and the International Macroeconomic statistical database. The data include the consumer price indices for the U.S.A., Brazil, South Africa, Malaysia, Argentina and Thailand, the China corporate good price index (original wholesale price index) and the U.S. dollar-Chinese yuan, U.S. dollar-Brazilian real, U.S. dollar-South Africa rand, U.S. dollar-Malaysian ringgit, U.S. dollar-Argentine peso and U.S. dollar-Thai baht nominal exchange rates. Except for the corporate good price index data for China, all data cover the sample period from January 1973 through August 2010. The corporate good price index data for China cover the sample period from January 1990 to October 2009. The real exchange rates of China, Brazil, South Africa, Malaysia, Argentina and Thailand vis-à-vis the United States are applied to conduct our empirical study. All the series of real exchange rates are expressed in logarithmic form.. 3.2. Testing for the Stationarity of the Real Exchange Rates. We implement hypothesis testing, which can be represented as the unit root null versus no unit root alternative to test whether the real exchange rates are stationary. We apply the unit root test of the band TAR model developed by Bec et al. (2004) to investigate whether the real exchange rates have unit roots. Table 1 reports actual. sup LR test statistics and the bootstrap p-values of the sup LR statistics for the unit root test. We use the bootstrap method to replicate the sampling distribution of the sup LR test statistics. Then we can make appropriate statistical inferences about the stationarity of the real exchange rates based on the bootstrap distribution. The empirical results indicate that the real exchange rates of the U.S..

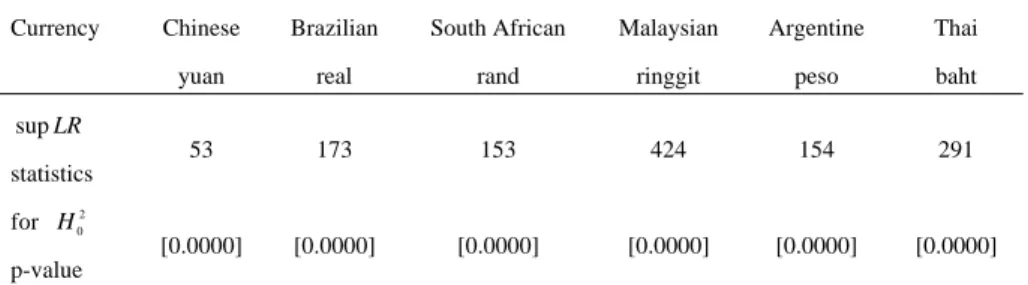

(12) 經濟與管理論叢(Journal of Economics and Management). 12. dollar-Chinese yuan, U.S. dollar-Brazilian real, U.S. dollar-South African rand, U.S. dollar-Malaysian ringgit, U.S. dollar-Argentine peso and U.S. dollar-Thai baht all reject the unit root null hypothesis at the 10% significance level. This means that all six real exchange rates are stationary when following band TAR processes. Holmes (2006) used the real exchange rates of 9 Asia-Pacific countries to test their stationarity. He found that none of the real exchange rates of the 9 Asia-Pacific countries reject the unit root null hypothesis. Divino et al. (2009) applied panel data for the real exchange rates of Latin America to study their stationarity. They found that for panel data the real exchange rates of Latin America can reject the unit root null hypothesis. However, through unit root tests for band TAR models, we demonstrate that under the specification of the band TAR model, the real exchange rates of the Chinese yuan, Brazilian real, South African rand, Malaysian ringgit, Argentine peso and Thai baht are all stationary. Table 1: Unit-root test for band TAR model Currency. Chinese. Brazilian. South African. Malaysian. Argentine. Thai. yuan. real. rand. ringgit. peso. baht. 150.89. 336.99. 479.27. 553.326. 365.15. 527.79. [0.0789]. [0.0878]. [0.0570]. [0.0181]. [0.0603]. [0.0530]. sup LR statistics for H 01 p-value The numbers in brackets are p-values of the sup LR statistics.. 3.3 Estimation and Testing for Band Threshold Autoregressive Model We apply the modified Schwarz information criterion to select the optimal lag in each regime of the band TAR model. The empirical results indicate that a lag order of 1 can minimize the modified Schwarz information criterion for all six real exchange rates. Thus, we choose the lag order p = 1 in model (2). Table 2 lists reports of actual sup LR test statistics and the bootstrap p-values of sup LR statistics for the nonlinear test. The empirical results show that all six real exchange rates strongly reject the linear null hypothesis at the 1% significance level. These.

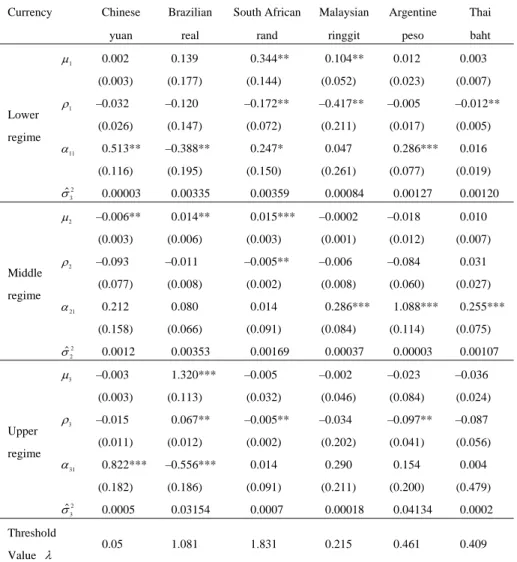

(13) Half Life of the Real Exchange Rate. 13. evident results mean that China, Brazil, South Africa, Malaysia, Argentina and Thailand have heavy market frictions in their international business. Hence all six real exchange rates exhibit strong nonlinear phenomena. Table 3 reports the estimates and their associated standard deviation of the parameters in each regime and also reports the estimates of the threshold value. Based on Hansen (1997), the asymptotic distributions of parameters in each regime are normal. Hence, we can apply t statistics to conduct hypothesis testing for the parameters in each regime. The lower regime, which corresponds to the first regime in model (2), means that the threshold variable qt −1 is smaller than −λ or equal to. −λ , where λ is a positive estimate of the symmetric threshold value. The middle regime, which corresponds to the second regime in model (2), means that the threshold variable qt −1 is larger than −λ and the threshold variable qt −1 is smaller than λ or equal to λ . The upper regime, which corresponds to the third regime in model (2), means that the threshold variable qt −1 is larger than λ . Table 2: Nonlinear test for band TAR model Currency. Chinese. Brazilian. South African. Malaysian. Argentine. Thai. yuan. real. rand. ringgit. peso. baht. 53. 173. 153. 424. 154. 291. [0.0000]. [0.0000]. [0.0000]. [0.0000]. [0.0000]. [0.0000]. sup LR statistics for H 02 p-value The numbers in brackets are p-values of the sup LR statistics.. The estimation results of the band TAR model for all six major emerging economies are shown in Table 3. The estimates include parameters for each regime and threshold value. From the empirical results, we can find that with the exceptions of the upper regimes of the Malaysian ringgit and Thai baht band TAR models, there are always significant coefficients in each regime of the six major emerging countries. This means that the band TAR modeling of the real exchange rates of the six major emerging countries is rather appropriate. The empirical results indicate that the estimates of the coefficient ρ 1 are significantly different from zero at the 5% significance level at the lower regime of the South African rand, Malaysian ringgit and Thai baht band TAR models..

(14) 經濟與管理論叢(Journal of Economics and Management). 14. Furthermore, from the empirical results, we can also find that the estimates of the coefficient ρ 3 are significantly different from zero at the 5% significance level for the upper regime of the Brazilian real, South African rand and Argentine peso band TAR models. This evidence indicates that when real exchange rates deviate from PPP sufficiently (beyond the bands), then the market forces will move the real exchange rates back to PPP. Table 3: Estimation of band TAR model Currency. Lower regime. Chinese. Brazilian. South African. Malaysian. Argentine. Thai. yuan. real. rand. ringgit. peso. baht. 0.344**. 0.104**. μ1. 0.002 (0.003). (0.177). (0.144). (0.052). (0.023). (0.007). ρ1. –0.032. –0.120. –0.172**. –0.417**. –0.005. –0.012**. (0.026). (0.147). (0.072). (0.211). (0.017). (0.005). –0.388**. 0.247*. 0.047. (0.195). (0.150). (0.261). α 11. 0.513** (0.116). Middle regime. σˆ 32. 0.00003. 0.00335. 0.00359. μ2. –0.006**. 0.014**. 0.015***. ρ2 α 21 σˆ 22 . μ3 ρ3 α 31. (0.077) 0.00127. 0.016 (0.019) 0.00120. –0.0002. –0.018. 0.010 (0.007). (0.003). (0.001). (0.012). –0.093. –0.011. –0.005**. –0.006. –0.084. 0.031. (0.077). (0.008). (0.002). (0.008). (0.060). (0.027). 0.212. 0.080. 0.014. (0.158). (0.066). (0.091). 0.0012 –0.003. –0.015. 0.822*** (0.182). σˆ 32. 0.286***. 0.003. (0.006). (0.011) regime. 0.00084. 0.012. (0.003). (0.003) Upper. 0.139. 0.00353 1.320*** (0.113) 0.067** (0.012) –0.556*** (0.186). 0.00169. 0.286*** (0.084) 0.00037. 1.088*** (0.114) 0.00003. 0.255*** (0.075) 0.00107. –0.005. –0.002. –0.023. –0.036. (0.032). (0.046). (0.084). (0.024). –0.005**. –0.034. –0.097**. –0.087. (0.002). (0.202). (0.041). (0.056). 0.014. 0.290. 0.154. 0.004. (0.091). (0.211). (0.200). (0.479). 0.0005. 0.03154. 0.0007. 0.00018. 0.04134. 0.0002. 0.05. 1.081. 1.831. 0.215. 0.461. 0.409. Threshold Value λ. The numbers in parentheses are the standard errors of the corresponding model coefficient estimates. Statistical significance is denoted by a single asterisk * for the 10% level, a double asterisk ** for the 5% level and a triple asterisk *** for the 1% level..

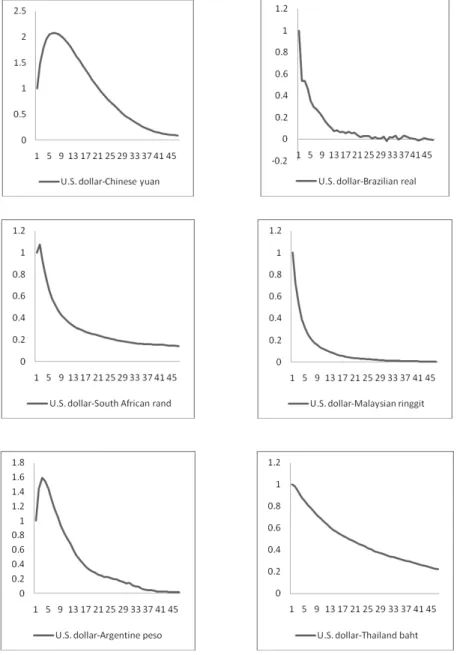

(15) Half Life of the Real Exchange Rate. 15. The empirical results also strongly indicate that with the exception of the South African rand, the estimates of coefficient ρ 2 are not significantly different from zero at the 10% significance level for the middle regime of the other five major emerging countries. This means that the majority of major emerging economies exhibit strong market frictions. Thus, when the real exchange rates deviate from PPP slightly, heavy market frictions will move the real exchange rates far away from PPP. We use σˆ 12 , σˆ 22 and σˆ 32 to represent the estimated variances of the first regime (lower regime), the second regime (middle regime), and the third regime (upper regime), respectively. For the real exchange rate of the U.S. dollar-Chinese yuan,. σˆ 12 = 0.00003 , σˆ 22 = 0.0012 and σˆ 32 = 0.0005 . For the real exchange rate of the U.S. dollar-Brazilian real, σˆ 12 = 0.00335 , σˆ 22 = 0.00353 and σˆ 32 = 0.03154 . For the real exchange rate of the U.S. dollar-South African rand, σˆ 12 = 0.00359 ,. σˆ 22 = 0.00169 and σˆ 32 = 0.00070 . For the real exchange rate of the U.S. dollar-Malaysian ringgit, σˆ 12 = 0.00084 , σˆ 22 = 0.00037 and σˆ 32 = 0.00018 . For the real exchange rate of the U.S. dollar-Argentine peso, σˆ 12 = 0.00127 ,. σˆ 22 = 0.00003 and σˆ 32 = 0.04134 , and for the real exchange rate of the U.S. dollar-Thai baht, σˆ 12 = 0.00120 , σˆ 22 = 0.00107 and σˆ 32 = 0.00020 .. 3.4 Generalized Impulse Response Analysis and Half Life Estimates The estimated models presented in Table 3 provide a basis for the estimation of the real exchange rate half lives. The way to obtain the speed of parity reversion of the estimated nonlinear models is through the impulse response function. The traditional impulse response function of linear models is not affected by the change in the history and in the sign and size of the shock. However, the traditional impulse response function of nonlinear models cannot hold these properties. Koop et al. (1996) developed a generalized impulse response function analysis of nonlinear models which is invariant with respect to the history and to the sign and size of the shock. In the following charts, we figure out the generalized impulse response function for the real exchange rates of six major emerging economies. We analyze the half lives of six different major emerging countries when the sizes of the shocks are.

(16) 16. 經濟與管理論叢(Journal of Economics and Management). 100%. The graphs of the 48-month generalized impulse response functions for 100% shocks are displayed in Figure 1.. Figure 1: The generalized impulse response function for the real exchange rates of six major emerging economies (the time horizons are measured by months).

(17) Half Life of the Real Exchange Rate. 17. Through the application of the generalized impulse response function to the estimated band TAR model, we can compute the speed of the PPP reversion of the real exchange rate when the real exchange rate suffers a shock. The half life is defined as the number of months it takes for a shock of a certain size to decay by 50%. However, shorter half-life estimates mean that the speed of convergence of the real exchange rate to PPP will be higher. Longer half-life estimates mean that the speed of convergence of the real exchange rate to PPP will be slower. From the generalized impulse response function analysis, we can find that the speed of the mean reversion of the real exchange rate in each major emerging country is rather fast. This indicates that although major emerging countries are characterized by heavier market friction in international business, through globalization the real exchange rates of major emerging countries deviate only slightly from PPP. Thus, the real exchange rates of major emerging countries can convert back to PPP very quickly. The half-life estimates for the shocks with sizes of 100% are given in Table 4. When the shock is 100%, the half-life estimate of the U.S. dollar-Chinese yuan real exchange rate is 28 months, the half-life estimate of the U.S. dollar-Brazilian peso real exchange rate is 4 months, the half-life estimate of the U.S. dollar-South African rand real exchange rate is 7 months, the half-life estimate of the U.S. dollar-Malaysian ringgit is 4 months, the half-life estimate of the U.S. dollar-Argentine peso real exchange rate is 14 months and the half-life estimate of the U.S. dollar-Thai baht real exchange rate is 18 months. Moreover, we can compare the half-life estimates obtained in the present study with those from previous research. The half-life estimates of the real exchange rates of the Brazilian real, South African rand and Malaysian ringgit are all below 1 year. The half-life estimates for the Argentine peso and Thai baht are below 2 years. The half-life estimate for the Chinese yuan is longer, but it is only 2.3 years. Table 4: Half-life estimates under a 100% shock Chinese. Brazilian. South African. Malaysian. Argentine. Thai. yuan. real. rand. ringgit. peso. baht. 28. 4. 7. 4. 14. 18. Currency. The estimates of the half life are measured in months..

(18) 18. 經濟與管理論叢(Journal of Economics and Management). Among several previous studies on developed countries, Abuaf and Jorion (1990) reported an average half life of 3.3 years for eight series of real exchange rates. Lothian and Taylor (1996) estimated the half life of dollar-pound rates to be 4.7 years. In examining pooled data on the real exchange rates of a group of currencies, Frankel and Rose (1996) found the half life to be roughly 2.5 years, whereas Wei and Parsley (1995) obtained half life estimates of around 4.5 years. Recently, Cheung and Lai (2000) fit the real exchange rate as the ARMA model and used an impulse response function to compute the half-life estimates. They reported the average of all half-life estimates to be approximately 3.3 years. Moreover, several previous studies have analyzed the half-life estimates of emerging countries. Our half-life estimates for Asian emerging countries are obviously shorter than those of Baharumshah et al. (2008) and Mollick (2009). The half-life estimates for Latin American emerging countries in our study also cover shorter periods than those reported by Mollick (2009). The half-life estimate in our study for an African emerging country still covers a shorter period than that in Arize et al. (2010). The half-life estimates of six major emerging economies are coherent with the criterion for the speed of PPP reversion proposed by Rogoff (1996). Such evidence indicates that many developing countries keep the movements of their exchange rates in accordance with PPP. This phenomenon reflects the progress of globalization among major emerging countries.. 4. Conclusion. Our empirical results indicate that the real exchange rates of six major emerging economies are all stationary. The real exchange rates of six major emerging economies all exhibit nonlinearity. These real exchange rates can be well fitted by the band TAR model. We also calculate the generalized impulse response functions from our estimated band TAR real exchange rate models. The adjustment dynamics of real exchange rates under shocks can be characterized by generalized impulse response analysis. The half-life estimates of the band TAR model for six major emerging economies are rather short in comparison with the findings of previous studies on developed and developing countries. The empirical results for the real exchange rates of the U.S. dollar-Chinese.

(19) Half Life of the Real Exchange Rate. yuan,. U.S.. dollar-Brazilian. real,. U.S.. dollar-South. 19. African. rand,. U.S.. dollar-Malaysian ringgit, U.S. dollar-Argentine peso and U.S. dollar-Thai baht presented here provide us with a meaningful understanding of the purchasing power parity issues of major emerging countries. Rogoff (1996) has indicated that appropriate half-life estimates should be approximately one or two years. Our empirical evidence confirms that major emerging economies indeed have heavier market frictions. However, through the progress of internationalization, the real exchange rates of major emerging economies adjust back to PPP rather quickly.. Appendix A: Bootstrap Method for SupLR Test Statistics The program codes used in this paper are written in the GAUSS language. The following procedures provide a precise interpretation regarding how to obtain the p-value of the sup LR test statistics for testing the null hypothesis of the unit root H 01 : ρ1 = ρ 2 = ρ 3 = 0 and the null hypothesis of threshold type nonlinearity H 02 : μ1 = μ 2 = μ 3 ,. ρ1 = ρ 2 = ρ 3 , α 1i = α 2 i = α 3 i. ∀i . The bootstrap method. proposed by Hansen (1996) is stated as follows: (1) Estimate model (2) under the null hypothesis H 01 and the null hypothesis H 02 , respectively. Then we can obtain the estimated parameters and residuals. (2) Generate the random sample ε t* , t = 1, K , T , by sampling with replacements from the residuals obtained from the previous procedure. Next, for each random sample, we generate a corresponding sample qt* with the estimated parameters of the model under the null hypothesis H 01 and under the null hypothesis H 02 , respectively. The initial conditions are given by the historic data. (3) For each possible threshold value (where we take data for qt* generated from the above procedure (2) as the candidates), we can calculate the corresponding sum of squared errors by estimating the restricted model (2). (4) For each possible threshold value (where we take data for qt* generated from the above procedure (2) as the candidates), we can calculate the corresponding sum of squared errors by estimating the unrestricted model (2). (5) From procedure (3) and procedure (4), for each possible threshold value, we can calculate the corresponding LR statistics. Then we can choose the maximum LR.

(20) 經濟與管理論叢(Journal of Economics and Management). 20. statistics from the set of these corresponding LR statistics. This is one sup LR statistic. (6) Repeat procedures (2) to (5) one thousand times and generate the empirical distribution of the sup LR statistics. The p-value is the percentage of simulated. sup LR statistics which exceed the actual sup LR statistics.. Appendix B: Monte Carlo Integration for Computation of Generalized Impulse Response Function The half lives are measured by how long the real exchange rates take for the generalized impulse response function to dissipate by a half amplitude from the occurrence of the shock. We state the procedures which Koop et al. (1996) adopt to compute the generalized impulse response function by means of Monte Carlo integration as follows: (1) Pick qt −1 , L , qt −n from the observations as the given history ωt −1 . (2) If the size of the shock occurring in period t is δ , i.e., vt = δ , we can then randomly draw vt +1 , vt + 2 , K , vt + n from the standard normal distribution. (3) Use the n random shocks obtained from the previous procedure to compute the realizations of qt1+1 (ωt −1 ) , i = 1, K, n , by iterating on the band TAR model given the initial ωt −1 . (4) Use the first n random shocks plus the additional shock from the exogenous shock ( δ = 100% here) to compute the realizations of qt1+i (vt = δ , ωt −1 ) ,. i = 0, 1, K, n by also iterating on the band TAR model given the initial vt = δ , ω t −1 .. (5) Repeat procedures (2), (3) and (4) R times, so that we can respectively. q R , t +i (vt = δ , ωt −1 ) = (1 R)∑ j=1 qtj+i (vt = δ , ωt −1 ) , R i = 1, K, n and q R , t +i (ωt −1 ) = (1 R)∑ j=1 qtj+i (ωt −1 ) , i = 1, K, n . If R is large. compute the sample mean. R. enough, by the Law of Large Numbers, the above Monte Carlo replications will respectively converge to the conditional expectation E [ qt + n vt = δ , ω t −1 ] and E[ q t + n ω t −1 ] .. (6) Take the difference between q R , t +i (vt = δ , ωt −1 ) and q R , t +i (ω t −1 ) , so that we can then obtain the generalized impulse response function..

(21) Half Life of the Real Exchange Rate. 21. References Abuaf, N. and P. Jorion, (1990), “Purchasing Power Parity in the Long Run,” Journal of Finance, 45, 157-174. Arize, A. C., J. Malindretos, and K. Nam, (2010), “Cointegration, Dynamic Structure, and the Validity of Purchasing Power Parity in African Countries,” International Review of Economics and Finance, 19, 755-768. Baharumshah, A. Z., C. T. Haw, and S. Fountas, (2008), “Re-Examining Purchasing Power Parity for East-Asian Currencies: 1976-2002,” Applied Financial Economics, 18, 75-85. Balke, N. S. and T. B. Fomby, (1997), “Threshold Cointegration,” International Economic Review, 38, 627-645. Bec, F., M. B. Salem, and M. Carrasco, (2004), “Test for Unit-Root versus Threshold Specification with an Application to the Purchasing Power Parity Relationship,” Journal of Business and Economic Statistics, 22, 382-395. Brooks, C. and I. Garrett, (2002), “Can We Explain the Dynamics of the UK FTSE 100 Stock and Stock Index Futures Markets?” Applied Financial Economics, 12, 25-31. Chan, K. S., (1991), “Percentage Points of Likelihood Ratio Tests for Threshold Autoregression,” Journal of the Royal Statistical Society, Series B, 53, 691-696. Chen, C. W. S., R. Gerlach, and A. M. H. Lin, (2010), “Falling and Explosive, Dormant, and Rising Markets via Multiple-Regime Financial Time Series Models,” Applied Stochastic Models in Business and Industry, 26, 28-49. Cheung, Y. W. and K. S. Lai, (2000), “On the Purchasing Power Parity Puzzle,” Journal of International Economics, 52, 321-330. Divino, J. A., V. K. Teles, and J. P. De Andrade, (2009), “On the Purchasing Power Parity for Latin-American Countries,” Journal of Applied Economics, 12, 33-54. Frankel, J. A. and A. K. Rose, (1996), “A Panel Project on Purchasing Power Parity: Mean Reversion Within and Between Countries,” Journal of International Economics, 40, 209-224..

(22) 經濟與管理論叢(Journal of Economics and Management). 22. Gourieroux, C. and C. Y. Robert, (2006), “Stochastic Unit Root Models,” Econometric Theory, 22, 1052-1090. Hansen, E. B., (1996), “Inference When a Nuisance Parameter Is Not Identified under the Null Hypothesis,” Econometrica, 64, 413-430. Hansen, B., (1997), “Inference in TAR Models,” Studies in Nonlinear Dynamics and Econometrics, 2, 1-14. Hansen, B., (2000), “Sample Splitting and Threshold Estimation,” Econometrica, 68, 575-603. Hansen, B. and B. Seo, (2002), “Testing for Two-Regime Threshold Cointegration in Vector Error-Correction Models,” Journal of Econometrics, 110, 293-318. Holmes, M. J., (2006), “Asia-Pacific Real Exchange Rates, Purchasing Power Parity and Regime Switching,” Department of Economics, Waikato University, New Zealand. Kapetanios, G. and Y. Shin, (2006), “Unit Root Tests in Three-Regime SETAR Models,” The Econometrics Journal, 9, 252-278. Koop, G., M. H. Pesaran, and S. M. Potter, (1996), “Impulse Response Analysis in Nonlinear Multivariate Models,” Journal of Econometrics, 74, 119-147. Lo, M. C. and E. Zivot, (2001), “Threshold Cointegration and Nonlinear Adjustment to the Law of One Price,” Macroeconomic Dynamics, 5, 533-576. Lothian, J. R. and M. P. Taylor, (1996), “Real Exchange Rate Behavior: The Recent Float from the Perspective of the Past Two Centuries,” Journal of Political Economy, 104, 488-509. Medeiros, M. C. and A. Veiga, (2009), “Modeling Multiple Regimes in Financial Volatility with a Flexible Coefficient GARCH(1,1) Model,” Econometric Theory, 25, 117-161. Mollick, A. V., (2009), “Crisis and Volatility in Asian versus Latin American Real Exchange Rates,” Economie Internationale, 117, 5-29. Murray, C. J. and D. H. Papell, (2002), “The Purchasing Power Parity Persistence Paradigm,” Journal of International Economics, 56, 1-19. Obstfeld, M. and A. M. Taylor, (1997), “Nonlinear Aspects of Goods-Market Arbitrage and Adjustment: Heckscher’s Commodity Points Revisited,” Journal of the Japanese and International Economies, 11, 441-479. O’Connell, P. G. J., (1998), “Market Frictions and Real Exchange Rates,” Journal of.

(23) Half Life of the Real Exchange Rate. 23. International Money and Finance, 17, 71-95. Parsley, D. C. and S. J. Wei, (2007), “A Prism into the PPP Puzzles: The Micro-Foundations of Big Mac Real Exchange Rates,” The Economic Journal, 117, 1336-1356. Pippenger, M. K. and G. E. Goering, (1998), “Exchange Rate Forecasting: Results from a Threshold Autoregressive Model,” Open Economies Review, 9, 157-170. Rogoff, K., (1996), “The Purchasing Power Parity Puzzle,” Journal of Economic Literature, 34, 647-668. Sarno, L., M. P. Taylor, and I. Chowdhury, (2004), “Nonlinear Dynamics in Deviations from the Law of One Price: A Broad-Based Empirical Study,” Journal of International Money and Finance, 23, 1-25. Taylor, A. M., (2001), “Potential Pitfalls for the Purchasing Power Parity Puzzle? Sampling and Specification Biases in Mean Reversion Tests of the Law of One Price,” Econometrica, 69, 473-498. Taylor, M. P., D. A. Peel, and L. Sarno, (2001), “Nonlinear Mean-Reversion in Real Exchange Rates: Toward a Solution to the Purchasing Power Parity Puzzles,” International Economic Review, 42, 1015-1042. Tong, H., (1978), “On a Threshold Model,” Pattern Recognition and Signal Processing, Amsterdam: Sijhoff and Noordoff. Tong, H. and K. S. Lim, (1980), “Threshold Autoregression, Limit Cycles and Cyclical Data,” Journal of the Royal Statistical Society, Series B, 42, 245-292. Tong, H., (1990), Non-Linear Time Series: A Dynamical System Approach, Oxford: Oxford University Press. Tsay, R. S., (2005), Analysis of Financial Time Series, 2nd edition, New York: Wiley. Wei, S. J. and D. C. Parsley, (1995), “Purchasing Power Disparity during the Floating Rate Period: Exchange Rate Volatility, Trade Barriers and Other Culprits,” NBER Working Paper, No. 5032. Wong, C. S. and W. K. Li, (2001), “On a Mixture Autoregressive Conditional Heteroscedastic Model,” Journal of the American Statistical Association, 96, 982-995..

(24)

數據

+2

相關文件

本學系宗旨培育學生成為「具財金專業之金融實 務人才」 ,除基礎財務理論外,發展方向為「銀 行」 、 「證券」 、 「保險」

To this end, we introduce a new discrepancy measure for assessing the dimensionality assumptions applicable to multidimensional (as well as unidimensional) models in the context of

For a polytomous item measuring the first-order latent trait, the item response function can be the generalized partial credit model (Muraki, 1992), the partial credit model

Jiunnren LAI, Chih-Peng YU, and Chia-Chi CHENG (2007) “ASSESSMENT OF LOCAL STIFFNESS FOR SLENDER CONCRETE MEMBERS USING IMPULSE RESPONSE TEST”, the Proceedings of 2nd

Wallace (1989), "National price levels, purchasing power parity, and cointegration: a test of four high inflation economics," Journal of International Money and Finance,

The evidence presented so far suggests that it is a mistake to believe that middle- aged workers are disadvantaged in the labor market: they have a lower than average unemployment

Finally, we use the jump parameters calibrated to the iTraxx market quotes on April 2, 2008 to compare the results of model spreads generated by the analytical method with

Keywords: pattern classification, FRBCS, fuzzy GBML, fuzzy model, genetic algorithm... 第一章