行政院國家科學委員會專題研究計畫 成果報告

體制差異與體制移轉對公司治理與公司表現的影響

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 99-2410-H-009-024- 執 行 期 間 : 99 年 08 月 01 日至 100 年 07 月 31 日 執 行 單 位 : 國立交通大學財務金融研究所 計 畫 主 持 人 : 潘李賢 計畫參與人員: 碩士班研究生-兼任助理人員:楊珮琪 碩士班研究生-兼任助理人員:陳怡妡 碩士班研究生-兼任助理人員:洪于婷 報 告 附 件 : 國外研究心得報告 出席國際會議研究心得報告及發表論文 處 理 方 式 : 本計畫可公開查詢中 華 民 國 100 年 10 月 30 日

ADR Characteristics and Corporate Governance from the Greater China

Region

Abstract

We examine the relationship between firm valuation and governance mechanisms, firm

characteristics, and institutional factors of American Depository Receipts (ADRs) in the

greater China region listed on the NYSE, AMEX and NASDAQ. We find that Chinese

firms cross-list in the US have the highest market-to-book value followed by Hong Kong

and Taiwan firms. It appears that Chinese firms with the poorest external governance

environment stand to benefit the most by successfully listed under the ADR programs.

Listing in the US that requires more stringent regulations and disclosure rules may

strengthen the firms’ governance practices and thereby enhance their firm value. Among the

internal governance mechanisms, institutional ownership and insider ownership are

important for firm value.

Keywords: External governance environments; Internal governance mechanisms; ADRs;

1. Introduction

Good corporate governance mechanisms are value enhancing. Its importance on firm

value has long been established since the pioneering work of Jensen and Meckling (1976)

in a nexus of contracts among various stakeholders. Under the rubrics of principal-agent

conflicts, Shleifer and Vishny (1997) emphasize that investor protection is crucial. La Porta

et al. (1998, 2000, and 2002) who examine the importance of external governance around

the world show that countries with common laws provide better shareholder protection than

those with civil laws. They document that the difference in the legal regimes and law

enforcement has led to higher valuation of corporate assets in common law regimes.

Recent research has focused on the combined determinants of corporate governance

on firm performance. In particular, board structure (Yermack (1996), Boone, Field, Karpoff,

and Raheja (2007), and Linck, Netter, and Yang (2008)), CEO characteristics (Hermalin

and Weisbach (1998), Basu, Hwang, Mitsudome, and Weintrop (2007), and Brookman and

Thistle (2009)) and ownership structure (Lemmons and Lins (2003), and Ali, Chen and

Radhakrishnan (2007)) have been identified as key determinants of a firm’s governance

practices. Firms with more independent directors and higher managerial ownership are

findings, Gillan’s (2006) provide a comprehensive review of internal and external

governance systems, and their interactions,

In this study, we contribute to the literature as we examine firm performance across

different external governance regimes under the American Depository Receipts (ADRs)

programs. In particular, we examine firm performance from the greater China region,

namely China, Hong Kong, and Taiwan, that cross-list in the US with stronger law

enforcement and investor protection (see La Porta et al. (1998)). This is especially the case

for ADRs under type II and III listings that are required to follow the same stringent

requirements on governance, disclosure requirements, and accounting standards as those of

the U.S. firms especially after the Sarbane-Oxley Act in 2002 (see Durnev and Kim (2005)

and Doidge, Karolyi, and Stulz (2003)).1 It could be argued that ADRs from the greater

China region should benefit from higher market valuation.

Part of our interest in examining the impact of ADRs from the greater China region in

relation to corporate governance on firm value is motivated by the contrasting external

legal environment and the internal governance mechanisms (or the lack of it) among these

markets. Although China’s regulatory framework is evolving rapidly, its external and

internal governance remain the weakest in comparison to Hong Kong and Taiwan (see e.g.

Sun and Tong (2003), Wei (2007), and Tian and Estrin (2008)).2 According to La Porta et

al. (1998), Taiwan which follows civil law regime and with weaker investor protection is

related to poorer governance environment. Hong Kong with its historical ties to common

law regime tends to enjoy stronger legal enforcement.

It follows that while firms within greater China region enjoy close business ties and

trades, their difference in the governance environments should provide a fertile ground to

examine the differential impact of ADR listings on firm value. One would therefore

hypothesize that Chinese ADRs with the weakest governance mechanism may on average

benefit the most in the form of higher firm valuation followed by those from Taiwan and

Hong Kong.

Our results confirm that Chinese ADRs enjoy on average the highest market-to-book

value after controlling for governance measures and firm characteristics. It suggests that

Chinese firms, moving from the poorest external governance regime to the US, tend to

benefit the most via the ADRs experience.

However, Hong Kong ADRs, which enjoy stronger governance at home, has the next

highest market-to-book equity after listing in the US. Taiwan ADRs which come from a

weaker governance regime, on the other hand, appear to gain the least from the region in

terms of market valuation. In our view, these results may be driven by firm effects that exist

between the markets. More specifically, Hong Kong ADRs include both Hong Kong based

firms in private sector and China’s state owned enterprises listed in Hong Kong while all

Taiwan ADRs consist of firms in high-tech industries. This contrast in firm type implies

that Taiwan ADRs are likely to be in more competitive industries compared to Hong Kong

ADRs. As Giroud and Mueller (2011) argue that product market competition is a good

substitute of governance, Taiwan ADRs should therefore experience stronger governance. It

follows that Hong Kong ADRs which tend to be in less competitive industries and weaker

governance should benefit more than Taiwan ADRs from the ADR listings.

Among the governance measures, institutional investor ownership and insider

ownership are important for firm value. The results are consistent with prior studies (e.g.

McConnell and Servaes (1990), Hartzell and Starks (2003), and Cornett et al. (2007)), that

higher insider ownership reduces potential agency conflicts between insiders and minority

shareholders, and institutional ownership seems to play an effective monitoring role for

privatization in China is positively related to firm performance but state ownership is

negatively related to firm performance.

The remainder of the paper is organized as follows. Section 2 provides an overview of

the corporate governance environment in the greater China region. Section 3 and 4

discusses the sample and methodology respectively. Empirical results are reported in

Section 5 and Section 6 concludes the paper.

2. Corporate Governance in the Greater China Region

2.1 China

China’s legal regime can inherently be traced to German’s civil-law which is on

average weaker than English’s common-law in terms of investor protection (La Porta et al.

(1998)). Coupled with high proportion of state ownership and control for publicly listed

firms, corporate governance environment in China is arguably the weakest of the three

markets in the region (see Sun and Tong (2003), Wei (2007), and Tian and Estrin (2008)).3

Since 1990s, China adopts a two-tier board structure that comprises the board of

directors and the supervisory board to improve governance. The aim is to impose a

two-layer oversight on the duty and performance of senior management. That is, the

supervisory board monitors and evaluates the performance of senior managers and the

board of directors who in turn monitor senior managers. The governance of board structure

has further been strengthened after the Code of Corporate Governance for Listed

Companies in China was in introduced in 2002 that requires some independence of

directors on the board, and qualifications and knowledge of members of supervisory

boards.

However, Wei (2007) contends that although these governance measures are put in

place, the board is still characterized by insider control and weak independence. Tam

(2002), Lin (2004), and Wang (2007) also find that supervisory boards are ineffective in

playing their roles of overseeing the performance of directors and managers.

The lack of independence of directors and supervisory members is perhaps not

surprising as the predecessors of Chinese listed firms are mostly state-owned enterprises

(SOEs). Managers of these former SOEs are likely to be appointed as directors. It follows

that directors are rarely independent and managers tend to dominate the governance of the

board. Similarly, most supervisory members are considered insiders because they tend to

Dahya et al. (2003)). Furthermore, the supervisory board has limited access to firm

information and has no power in removing directors and managers (see Lin (2004) and

Wang (2007)).

Despite the partial privatization of SOEs, much of the ownership structure of Chinese

firms remains in the hands of the state, with the majority of shares outstanding held by the

state as non-tradable shares. Institutional ownership may therefore play a relatively more

important role on firm performance especially in China. Consistent with this argument,

Chen et al. (2006) examine the effect of outside directors on corporate fraud and document

that Chinese firms with a higher percentage of outside directors such as those by

institutional investors tend to reduce corporate fraud. Zhang et al. (2001) and Xu et al.

(2005) also show that foreign ownership is positively related to the efficiency of Chinese

industrial firms.

2.2 Hong Kong

Unlike China, Hong Kong follows the common-law regime, or the Anglo-Saxon legal

and governance system. La Porta et al. (1998) show that common-law countries provide

other types of legal regimes. Within the common-law countries, Hong Kong scores well

above the average in efficiency of judicial system, rule of law, and the level of corruption.

Cheung et al. (2007) suggest that stock market in Hong Kong shares similar characteristics

and practices observed in developed economies. International rating agencies rank Hong

Kong as one of the more advanced markets in the Asia-Pacific region.

However, firms in Hong Kong are characterized by less diffused ownership structure

than firms in developed markets. They tend to be family owned and managed by family

members as commonly found in the region. It is common that the chairman of the board is

also the chief executive officer of the firm. Agency conflicts may therefore arise from this

particular type of ownership structure between controlling families and minority

shareholders.

Since 2005, each publicly listed firm in Hong Kong is required to have a minimum of

three independent non-executive directors on its board. Such requirement may reduce

agency costs of the firm as outsiders tend to play a more effective role in monitoring

managers. In sum, corporate governance external environment and governance practices in

2.3 Taiwan

Similar to China, Taiwan’s legal origin comes from German civil law. La Porta et al.

(1998) report that Taiwan’s efficiency of judicial system and corruption are poorly ranked

compared to those of other countries in German legal origin and weaker legal families. The

overall poor investor protection in Taiwan due to poor investor protection suggests that

internal governance may play a more critical role.

Following the German corporate governance structure, board members in a Taiwanese

firm consist of both directors and supervisors. The role of supervisors is to monitor

directors on their corporate decisions and to review and audit reports prepared for the

shareholders. However, the supervisory board is not as independent as in the German’s

two-tier system. Its members can be elected from family members of current employees

and directors.

Lee and Yeh (2004) emphasize that controlling families in Taiwan may also set up

nominal investment firms to increase their controls by sending family members or their

designated persons to the board after the investment firms are elected for the positions of

directors and/or supervisors. With these governance practices by controlling families,

ownership and family control. They find that 64% of firms in Taiwan do not appoint an

independent director and another 21% of firms hire only one independent director despite

the mandatory requirement of two independent directors for IPO firms in 2002.

Given the considerations of legal regimes and internal governance that vary across the

Greater China Region, it could be argued that firms in Hong Kong on average tend to

associate with the strongest governance mechanisms while those in China tend to exhibit

the weakest governance practices.

3. Data and Variable Definitions

3.1 Sample

Sample ADRs from China, Hong Kong, and Taiwan listed on NYSE, AMEX, and

NASDAQ and their financial data are obtained from Factset database. Our sample period

begins from 2005 after these markets adopt governance measures similar to those in

Sarbanes Oxley Act, and ends in 2010. After removing ADRs that contain missing financial

and governance information and therefore do not meet our data requirement, we collect 48

Chinese ADRs, 18 Hong Kong ADRs, and 8 Taiwan ADRs for a total of 74 ADRs and 444

both Hong Kong and Taiwan. All of the ADRs in the sample belong to either type II or III

listing which is required to adopt the US disclosure and governance rules.

A closer look at the sample reveals that the firm type of ADRs varies across these three

markets. For example, Chinese ADRs are predominately related to state owned enterprises

over a range of diverse industries. Hong Kong ADRs, on the other hand, consists of both

firms in the private sector and China’s state owned enterprises initially listed in Hong Kong

across different industries. In contrast, all Taiwan ADRs come from high-tech sector. As a

result, their listings are either on NYSE and NASDAQ rather than across all three

exchanges.

3.2 Market-to-Book Ratio

Following Chen et al. (2006), Harford et al. (2008), Cheung et al. (2008), and Linck et

al. (2008), we use market-to-book value ratio (M/B) for measuring firm performance.

Demsetz and Villalonga (2001) suggest that market-based measures such as M/B are more

preferable than accounting-based profit ratios (i.e. ROA and ROE) because the former are

forward looking measures of corporate performance whereas the latter are backward

may apply differently to valuing tangible and intangible capitals and taxation systems may

vary with firms of different ownership structure. In contrast, M/B should fairly reflect

future profitability of a firm by markets without the accounting constraints. Furthermore,

M/B tends to capture markets’ views on governance mechanisms as a means to reduce

agency costs and enhance corporate performance.

For explanatory variables of M/B, we follow extant literature and categorize measures

of governance mechanisms, firm characteristics, and institutional factors into 6 groups as

follows: board structure, CEO characteristics, ownership structure, firm characteristics,

country dummies, and stock exchange dummies. These measures are defined in Appendix I.

3.3 Board Structure

We include percentage of independent directors, CEO duality, and non-executive

chairman when the chairman is not an executive member of the company for measures

under board structure. Independent directors are non-executive or non-employee directors

who may play a more effective role in monitoring management to meet shareholders’

expectations. Borokhovich et al. (1996), Krivogorsky (2006), and Adams and Ferreira

performance.

When the CEO is also the chairman of the board, Fama and Jensen (1983) contend that

it may impede the effectiveness of board monitoring as the decision making and control is

endowed within one individual. Rechner and Dalton (1991), and Bhagat and Bolton (2008)

show that non-duality firms outperformed duality firms. Bai, Liu, Lu, Song, and Zhang

(2004) also report a negative relationship between CEO duality and market value for

Chinese firms.

3.4 CEO characteristics

CEO characteristics refer to the number of years that a CEO has held the position.

Hermalin and Weisbach (1991) suggest that CEO tenure does not seem to affect firm

profitability for shorter CEO tenures but firm profitability declines when CEO tenure is

more than 15 years. In a follow-up study, Hermalin and Weisbach (1998) conclude that

board independence will generally decline with CEO tenure. When a CEO has worked for

the company for a longer period of time, they tend to have more influence on the directors

of the board, which is detrimental to board independence and the effectiveness of

On the other hand, CEO tenure may proxy for board leadership and measures the

extent of CEO experience that may help companies to tackle difficulties and increase

profits. This argument is supported by Linck et al. (2008) and Brookman and Thistle (2009)

who show that CEO tenure has a positive effect on firm performance.

3.5 Ownership Structure

Insiders include employees, directors, and managers who enjoy information advantage

about the firm over the market. McConnell and Servaes (1990) suggest that insider

ownership may also perform a monitoring role for the firm. Therefore, as the share

ownership of insider ownership increases and that their interests are more aligned with

those of shareholders, the cost of monitoring tends to be lowered.

Conversely, firms whose managers have high levels of control rights (relative to cash

flow rights) experience lower stock returns. Lemmon and Lins (2003) show that ownership

structure of firms in eight East Asian countries plays an influential role in wealth

expropriation of insiders from minority shareholders. In examining the relation between

ownership and market value among Chinese firms, Bai et al. (2004) report that high

Based on the findings, we include percentage of institutional ownership and insider

ownership as proxies for ownership structure. However, McConnell and Servaes (1990)

suggest that when the percentage of insider ownership reaches a threshold, an increase in

insider ownership may decrease firm value. Hence, we also include a squared term of

insider ownership as a measurement of the potential non-linear relationship between

percentage of insider ownership percentage and firm profitability.

3.6 Firm Characteristics and Institutional Factors

We further include firm-specific and institutional control variables to isolate the effect

of governance measures on firm performance. They include debt-to-equity ratio, trading

volume, company age, and firm size (natural log). Country dummies (CHINA,

HONGKONG, and TAIWAN) as discussed in Section 2, and stock exchanges dummies

(NYSE, AMEX, and NASDAQ) are used to control for the fixed effects of the countries

and stock exchanges.

4. Empirical Results

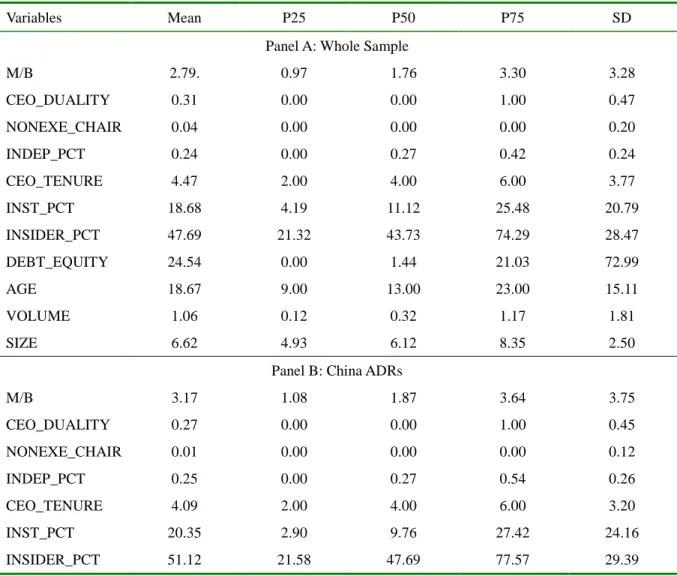

We first present the summary statistics of the sample ADRs in Table 1. Panel A reports

the aggregate statistics for the whole sample, and Panel B, C, and D report for individual

market of China, Hong Kong, and Taiwan respectively.

We find that the average market-to-book value (M/B) ratio is 2.79 for the whole sample,

a high market valuation relative to book value. It implies that the sample ADRs with high

market valuation are perhaps seeking external funding and/or increasing investor base

beyond their local markets by listing in the U.S. stock exchanges. Among them, those from

China enjoy the highest market-to-book ratio of 3.17, followed by those from Taiwan of

1.99 and Hong Kong of 1.96. Firms from the weakest external governance regime (i.e.

China) appear to enjoy the highest market valuation relative to those from stronger

governance regime.

Consistent with the literature that CEO duality is more common in the region than in

the US or UK, thirty-one percent of the sample ADRs appoint their CEOs as the chairman

of the board (CEO_DUALITY) and only four percent with non-executive chairman

(NONEXE_CHAIR). As discussed in Section 2, firms in Hong Kong and Taiwan are more

likely to be family-controlled such that CEOs who tend to be a family member also serve as

those in Hong Kong and Taiwan, it remains high by western standards.

The average age of sample ADRs is more than 18 years across which Hong Kong

ADRs are on average more mature (20.77 years) than their counterparts (18.05 and 17.75

years for China and Taiwan respectively). Compared to the average ADR age, the average

CEO tenure is only 4.47 years that range from 4.09 years of Chinese ADRs to 6.17 years of

Taiwan ADRs, implying frequent CEO turnovers.

Since regulations in all three markets require mandatory independent directors, the

average percentage of independent directors is relatively high at 24 percent. However, the

variability across these three markets appears to be small, with the highest percentage of

independent directors of 26 percent found among Taiwan ADRs.

Insider ownership on average nears 50 percent, driven largely by high insider

ownership of China and Hong Kong ADRs that are above 50 percent. In contrast, Taiwan

ADRs are skewed towards computer-related firms characterized by more diffused

ownership. Its average insider ownership is a relatively low of 20 percent.

Finally, institutional investors seem to actively invest in ADRs. They hold an average

of 18.68 percent of total shares outstanding. Most noticeably, China and Taiwan ADRs

Kong ADRs. It appears that institutional investors in recent years have shown more interest

in Chinese firms. Taiwan ADRs which tend to be computer-related firms also appear to

draw a similar level of interest.

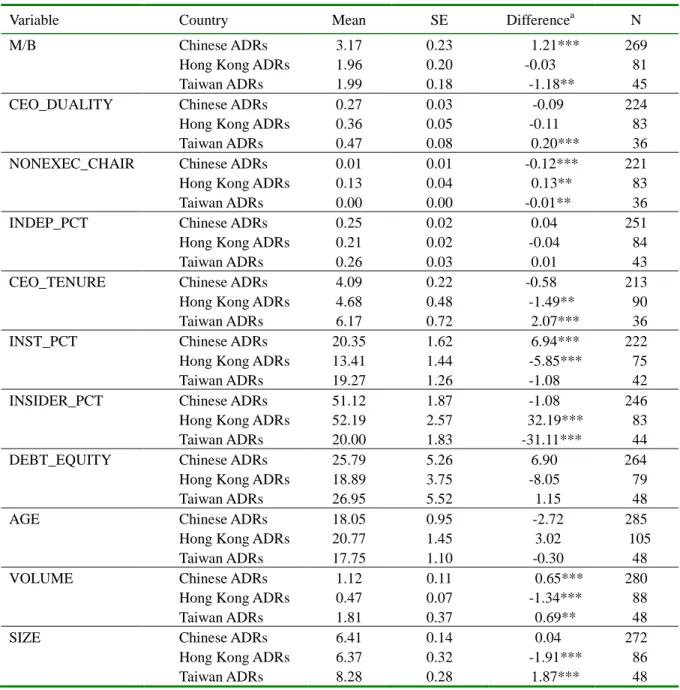

4.2 Univariate Results

Table 2 reports the results of differences in means of M/B, governance measures, and

firm characteristics among Chinese, Hong Kong, and Taiwan ADRs reported in Table 1.

The first row for each variable shows the statistical difference, if any, between Chinese and

Hong Kong ADRs. The second row reports the difference between Hong Kong and Taiwan

ADRs while the third row reports the difference between Taiwan and Chinese ADRs.

Among the ADRs from the three markets, Chinese ADRs exhibit higher market

valuations than Hong Kong and Taiwan ADRs. There appears however little difference in

M/B between Hong Kong and Taiwan ADRs. We find that very few firm characteristics or

internal governance measures shown in Table 2 are consistent with the differences in M/B.

The country of domicile where external governance environment differs significantly

between China and the other two markets remains the primary candidate to explain the

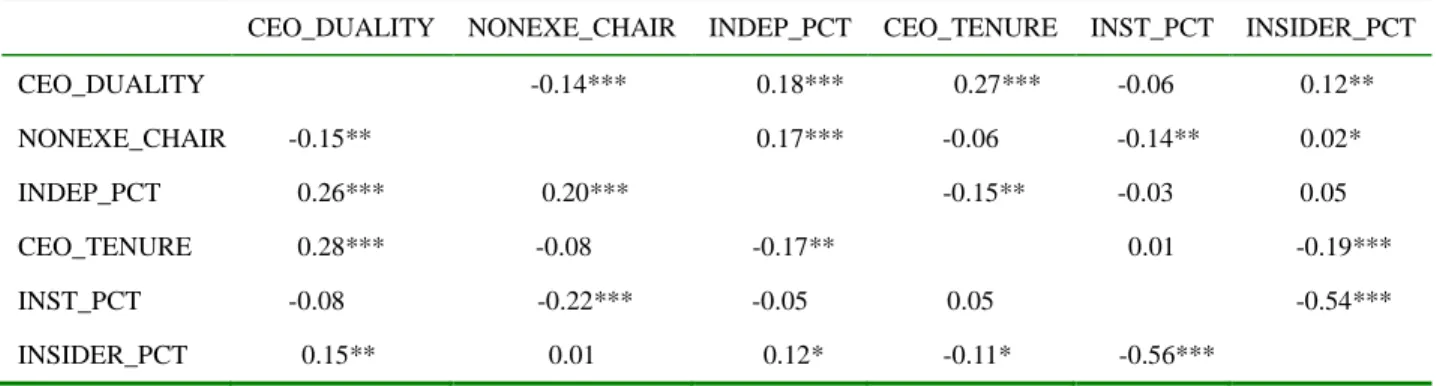

Before we estimate multivariate regression analysis on the effect of governance

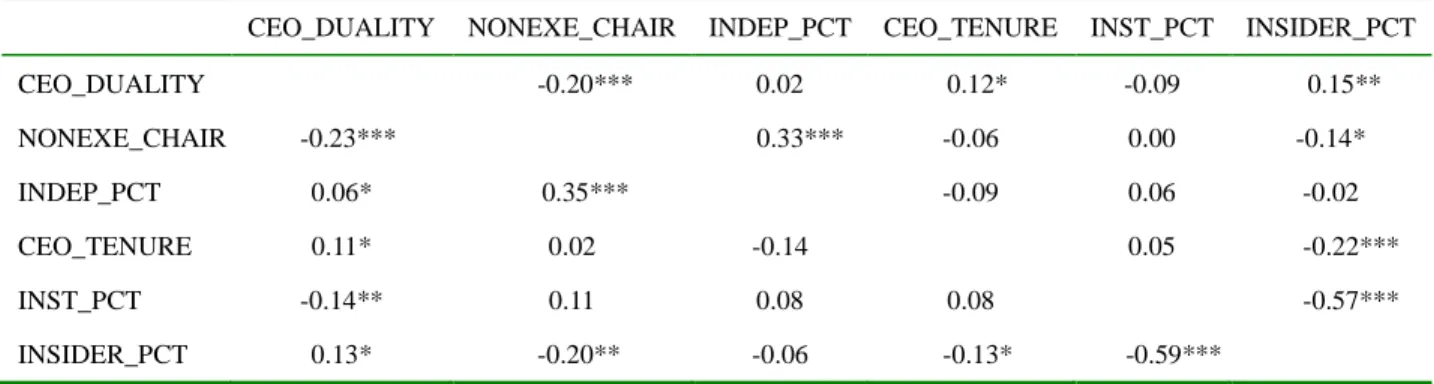

measures on firm performance, we calculate the correlations between governance measures

to examine potential multicollinearity problems. Table 3 presents the correlations using

both Pearson (in upper diagonal) and Spearman rank (in lower diagonal) estimates.

The cross correlations between the six governance variables are generally low with the

exception between institutional and insider ownership (0.54 or 0.56). These two measures

are however expected to contrast each other because a higher proportional of insider

ownership implies a lower institutional ownership. Institutional investors also become less

important in monitoring managers as agency costs tend to be lower when insiders hold a

higher proportion of share ownership. To ensure regression results are robust to the

potential multicollinearity problem, we run several regression estimates with various

combinations of controlled variables.

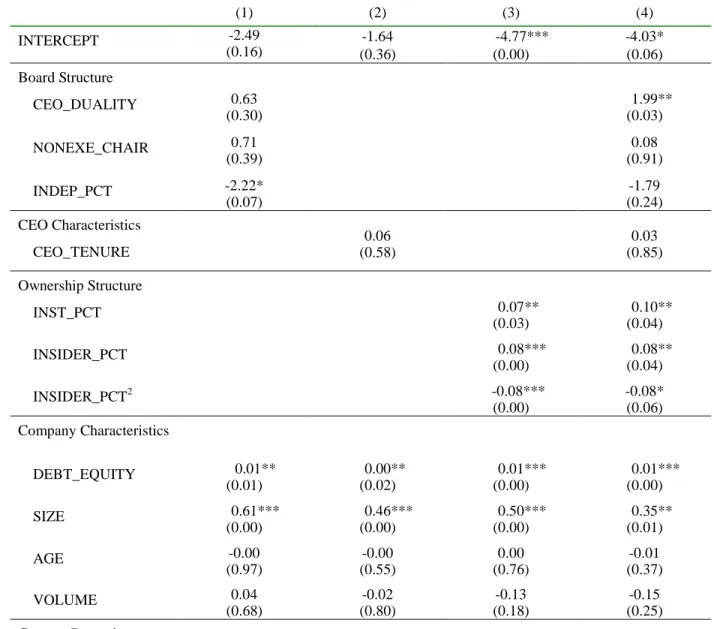

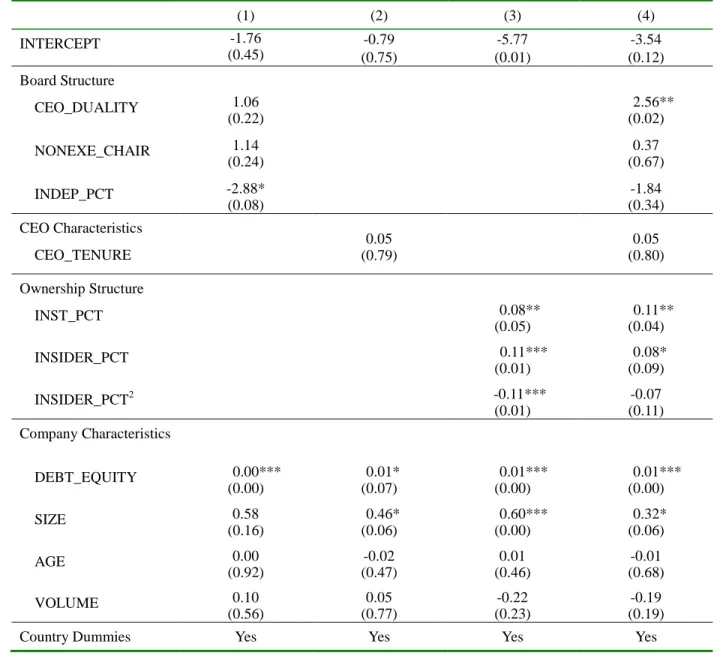

4.3 Regression Results

Sequel to the preliminary results, we estimate the following regressions to examine the

i

i BS CEO OS CC CD SD

B

M/ =α +β1 +β2 +β3 +β4 +β5 +β6 +ε (1)

where M /Biis market-to-book value ratio for firm i ; BS , CEO, OS, and CCare

vectors of board structure variables, CEO characteristics, ownership structure, and

company characteristics respectively; CDand SDare dummy variables for countries and

stock exchanges respectively; εi is the error term.

One common problem in examining the relationship between corporate governance and

firm performance is the potential endogeneity effect of governance measures documented

in Himmelberg et al. (1999), Cho (1998), and Bhagat and Bolton (2008). An increase in

firm value may lead to better governance practices rather than what is being investigated

here. To address such effect, we use firm size, debt-to-equity ratios, and return on equity as

instrument variables for institutional ownership. We then use the predicted institutional

ownership in the regression analysis. Furthermore, we consider lagged market-to-book ratio,

lagged leverage, and lagged board structure. Results using these instruments are robust to

those reported in this section. We also follow Black, et al. (2006) and Petersen (2008) by

applying adjusted standard errors due to the correlations between the same companies in

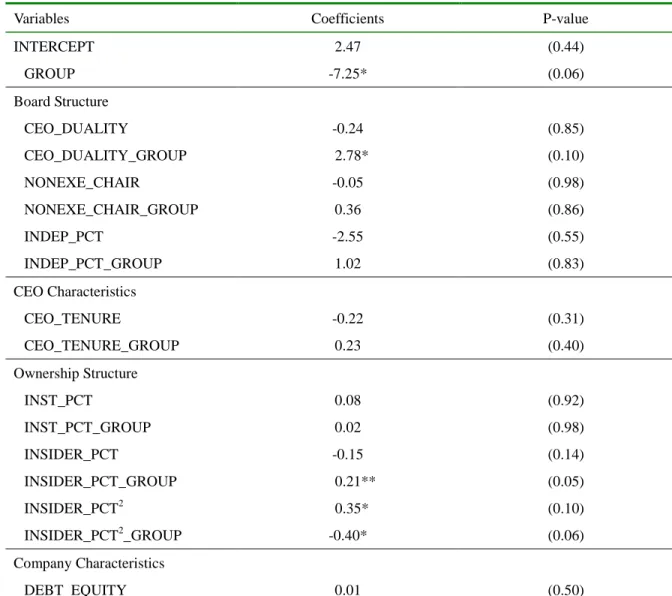

Table 4 reports the regression results based on Eq. (1). Column 1 first shows the effect

of board structure along with firm characteristics, country dummies, and exchange

dummies on market-to-book value ratio (M/B). Among the measures for board structure,

only percentage of independent directors (INDEP-PCT) is marginally but negatively

significant at the 10 percent level. The negative relation therefore contradicts the standard

agency theory which posits that an increase in the proportion of independent directors

reduces principal-agent conflicts. Including other governance measures however shows that

it is not an important consideration for market valuation (see column 4 in Table 4).

Similar to board structure measures, the duration of CEO tenure as shown in columns 2

and 4 carries little consequence on ADR performance. Given that the average time period is

4.47 years (see Table 1), the short CEO tenure and its lack of variability across ADRs may

explain why it fails to account for firm performance.

For the effect of ownership structure, we include the percentage of institutional and

insider ownership. Since the effect of insider ownership may potentially be curvilinear, we

also include a square term. Columns 3 and 4 of Table 4 show that these two governance

mechanisms are positively related to M/B ratio. While these results are consistent with the

conflict between management and minority shareholders, their relationships do not appear

to be economically significant. An increase of one standard deviation in insider ownership

and institutional ownership corresponds with 2.1 percent and 2 percent in M/B respectively.

It suggests that their impacts on market valuation are limited.

In contrast to the limited effects of governance measures and firm characteristics, we

find that country of domicile explains greater variations in the M/B ratio. Reported in Table

4, Chinese ADRs experience significantly higher M/B than both Hong Kong and Taiwan

ADRs. In fact, switching from Chinese ADRs to either Hong Kong or Taiwan ADRs on

average lowers market equity relative to book equity by more than a factor of 1. As China

has the weakest governance environment in the greater China region, Chinese firms under

the ADR programs have the most to benefit from listing in the US.

However, Hong Kong ADRs enjoy higher market valuation than Taiwan ADRs after

listing in the US. This result appears to contradict the hypothesis that ADRs from a weaker

governance regime should benefit more from the ADR programs. However, when we

investigate firm types between Hong Kong and Taiwan ADRs, we find that Hong Kong

ADRs are made up of both Hong Kong based firms in the private sector and China’s state

firms in high-tech industries. The apparent firm effects suggest that Taiwan ADRs are likely

to be in more competitive industries compared to Hong Kong ADRs. As Giroud and

Mueller (2011) argue that product market competition is a good substitute of governance,

Taiwan ADRs should on average experience stronger governance. Consequently, Hong

Kong ADRs with weaker governance on average tend to gain more from ADR listings.

5. Conclusion

In their seminal papers on corporate governance, La Porta et al. (1998, 2000, and 2002)

show that external governance regime is an important determinant for firm performance.

Stronger governance that provides better investor protection leads to higher firm value. We

extend their studies by comparing the performance of firms from the greater China region

that cross-list in the US under the ADR programs. In particular, we compare firm valuation

between ADRs from China, Hong Kong , and Taiwan, which although share close business

and trade ties differ significantly in their external governance backgrounds.

Consistent with the extant literature, we find that Chinese firms with the weakest

governance environment tend to gain the most under the ADR programs after subject to the

and Taiwan experience relatively lower market valuation due to their stronger external

governance environments at home.

Despite the importance of some firm characteristics and internal governance

mechanisms on firm value, our results suggest that the impact of external governance

backgrounds far outweighs those within the firms. They imply that policy efforts should be

directed more at the macro level than at the firm level as the former appears to be more

References

Adams, R., and D. Ferreira, 2007, “A theory of friendly boards,” Journal of Finance, Vol.

62, pp. 217–250.

Ali, A., T.Y. Chen, and S. Radhakrishnan, 2007, “Corporate disclosures by family firms,”

Journal of Accounting and Economics, Vol. 44, pp. 238-286.

Bai, C.E., Q. Liu, J. Lu, F. M. Song, and J. Zhang, 2004, “Corporate governance and

market valuation in China,” Journal of Comparative Economics, Vol. 32, pp. 599-616.

Basu, S., L.S. Hwang, T. Mitsudome, and J. Weintrop, 2007, “Corporate governance, top

executive compensation and firm performance in Japan,” Pacific-Basin Finance Journal,

Vol. 15, pp. 56-79.

Bhagat, S., and B. Bolton, 2008, “Corporate governance and firm performance,” Journal of

Corporate Finance, Vol. 14, pp. 257-273.

Black, B. S., I. Love, and A. Rachinsky, 2006, “Corporate governance indices and firms’

market values: Time series evidence from Russia,” Emerging Markets Review, Vol. 7, pp.

361-379.

Boone, A. L., L.C. Field, J. M. Karpoff, and Charu G. Raheja, 2007, “The determinants of

Studies, Vol. 85, pp. 66-101.

Borokhovich, K.A., R. Parrino, and T. Trapani, 1996, “Outside directors and CEO

selection,” Journal of Financial and Quantitative Analysis, Vol. 31, pp. 337–355.

Brookman, J. and P. D. Thistle, 2009, “CEO tenure, the risk of termination and firm value,”

Journal of Corporate Finance, Vol. 15, pp. 331-344.

Chen, G., M. Firth, D. N. Gao, and O. M. Rui, 2006, “Ownership structure, corporate

governance, and fraud: Evidence from China,” Journal of Corporate Finance, Vol. 12,

pp. 424-448.

Cheung, Y.L., J.T. Connelly, P. Limpaphayom, and L. Zhou, 2007, “Do investors really value

corporate governance? Evidence From the Hong Kong market,” Journal of International

Financial Management and Accounting 18, 86-122.

Cheung, Y.L., P. Jiang, P. Limpaphayom, and T. Lu, 2008, “Does corporate governance

matter in China?” China Economic Review, Vol, 19, pp. 460-479.

Cho, M.H., 1998, “Ownership structure, investment, and the corporate value: An empirical

analysis,” Journal of Financial Economics, Vol. 47, pp. 103-121.

Cornett, M. M., Marcus, A. J., Saunders, A., & Tehranian, H. (2007). “The impact of

Finance, 31, 1771-1794.

Dahya, J., Y. Karbhari, J. Z. Xiao, and M. Yang, 2003, “The usefulness of the supervisory

board report in China,” Corporate governance: an international review, Vol.11, pp.

308-321.

Demsetz, H. and B. Villalonga, 2001, “Ownership structure and corporate performance,”

Journal of Corporate Finance, Vol. 7, pp. 209-233.

Doidge, C. A., G. A. Karolyi, and R. M. Stulz, 2003, “Why are foreign firms listed in the

U.S. worth more?” Journal of Financial Economics, Vol. 71, pp. 205-238.

Durnev, Art, and E. Han Kim, 2005, “To steal or not to steal: firm attributes, legal

environment, and valuation,” Journal of Finance, Vol. 60, pp. 1461-1493.

Fama, E. F., and M. C. Jensen, 1983, “Separation of ownership and control,” Journal of

Law and Economics, Vol. 26, pp. 301-325.

Gillan, S. L., 2006, “Recent developments in corporate governance: an overview,” Journal

of Corporate Finance, Vol. 12, pp. 381-402.

Giroud, X. and H. Mueller, 2011, “Corporate governance, product market competition, and

equity price,” Journal of Finance, 66, 563-600.

holdings in the U.S.,” Journal of Financial Economics, Vol. 87, pp. 535-555.

Hartzell, Jay C., and Laura T. Starks, 2003, “Institutional investors and executive

compensation,” Journal of Finance, Vol. 58, pp. 2351-2374.

Hermalin, B. E., and M. S. Weisbach, 1991, “The effects of board composition and direct

incentives on firm performance,” Financial Management, Vol. 20, pp. 101-112.

Hermalin, B.E., and M. S. Weisbach, 1998, “Endogenously chosen boards of directors and

their monitoring of the CEO,” American Economic Review, Vol. 88, pp. 96-118.

Himmelberg, C. P., R. G. Hubbard, and D. Palia, 1999, “Understanding the determinants of

managerial ownership and the link between ownership and performance,” Journal of

Financial Economics, Vol. 53, pp. 353-384.

Jensen, M. C. and W.H. Meckling, 1976, “Theory of the firm: Managerial behavior, agency

costs and ownership structure,” Journal of Financial Economics, Vol. 3, pp. 305-360.

Krivogorsky, V., 2006, “Ownership, board structure, and performance in continental

Europe,” The International Journal of Accounting, Vol. 41, pp. 176-197.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R.W. Vishny, 2002, “Investor protection

and corporate valuation,” Journal of Finance,Vol. 57, pp. 1147-1170.

and corporate governance,” Journal of Financial Economics, Vol. 58, Issue 1, pp. 3-27.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. W. Vishny, 1998, “Law and finance,”

Journal of Political Economy, Vol. 106, Issue 6, pp. 1113-1155.

Lee, Tsun-Siou and Yin-Hua Yeh, 2004, “Corporate governance and financial distress:

evidence from Taiwan,” Corporate Governance: An International Review, Vol. 12, Issue

3, pp. 378-388.

Lemmon, M. and K. Lins, 2003, “Ownership structure, corporate governance, and firm

value: Evidence from the East Asian financial crisis,” Journal of Finance, Vol. 58, Issue

4, pp. 1445-1468.

Lin, T.W., 2004, “Corporate governance in China: recent developments, key problems, and

solutions,” Journal of Accounting and Corporate Governance, Vol. 1, pp. 1-23.

Linck, J. S., J. M. Netter, and T. Yang, 2008, “The determinants of board structure,”

Journal of Financial Economics, Vol. 87, pp. 308-328.

McConnell, J. J., and H. Servaes, 1990. “Additional evidence on equity ownership and

corporate value,” Journal of Financial Economics, Volume 27, pp. 595-612.

Petersen, M. A., 2008, “Estimating standard errors in finance panel data sets: comparing

Rechner, P.L., and D.R. Dalton, 1991, “Research notes and communications CEO duality

and organizational performance: A longitudinal analysis,” Strategic Management

Journal, Vol. 12, pp. 155-160.

Sun, Q. and W.H.S. Tong, 2003, “China share issue privatization: the extent of its success,”

Journal of Financial Economics, Vol. 70, pp. 183-222.

Shleifer, A., and R. W. Vishny, 1997, “A survey of corporate governance,” Journal of

Finance, Vol. 52, pp. 737-783.

Tam, O.K., 2002, “Ethical issues in the evolution of corporate governance in China,”

Journal of Business Ethics, Vol. 37, pp. 303-320.

Tian, L. and S. Estrin, 2008, “Retained state shareholding in Chinese PLCs: does

government ownership always reduce corporate value?” Journal of Comparative

Economics, Vol. 36, pp. 74-89.

Wang, J., 2007, “The strange role of independent directors in a two-tier board structure of

China‘s listed companies,” Compliance and regulatory journal, Vol. 3, pp. 47-55.

Wei, G., 2007, “Ownership structure, corporate governance and company performance in

China,” Asia Pacific Business Review, Vol. 13, pp.519-545.

reform: evidence from China,” Economics of transition, Vol. 13, 1-24.

Yermack, D., 1996, “Higher market valuation of companies with a small board of

directors,” Journal of Financial Economics, Vol. 40, pp. 185-211.

Young, C. S., L. C. Tsai, and P. G. Hsieh, 2008, “Voluntary Appointment of Independent

Directors in Taiwan: Motives and Consequences,” Journal of Business Finance and

Accounting, Vol. 35, Issue 9-10, pp. 1103-1137.

Zhang, A., Y. Zhang, and R. Zhao, 2001, “Impact of ownership and competition on the

productivity of Chinese enterprises,” Journal of Comparative Economics, Vol. 29,

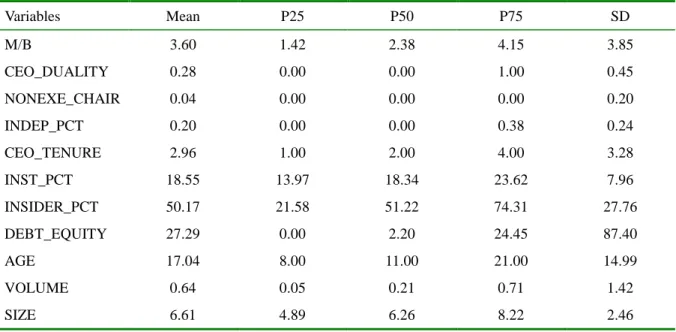

Table 1. Summary Statistics of the Sample Firms

This table presents the summary statistics of ADRs in the greater China region during 2005-2010. M/B is the stock price per share divided by book value per share. CEO_DUALITY is a dummy variable that equals one when the CEO is also the chairman of the board, and zero otherwise. NONEXE_CHAIR is a dummy variable that equals one when the chairman of the board is not an executive member, and zero otherwise. INDEP_PCT is the percentage of independent directors on the board. CEO_TENURE is the number of years the CEO has held his/her title. INST_PCT is the number of shares held by institutional investors as a percentage of the current total shares outstanding. INSIDER_PCT is the number of shares held by insiders as a percentage of the current total shares outstanding. DEBT_EQUITY is the long-term debt-to-equity ratio; SIZE is the natural log of market capitalization, where the firm's market value is measured in millions of dollars. AGE is the number of years since the company starts (up to 2010). VOLUME is the 52-week average of the volume of shares traded.

Variables Mean P25 P50 P75 SD

Panel A: Whole Sample

M/B 2.79. 0.97 1.76 3.30 3.28 CEO_DUALITY 0.31 0.00 0.00 1.00 0.47 NONEXE_CHAIR 0.04 0.00 0.00 0.00 0.20 INDEP_PCT 0.24 0.00 0.27 0.42 0.24 CEO_TENURE 4.47 2.00 4.00 6.00 3.77 INST_PCT 18.68 4.19 11.12 25.48 20.79 INSIDER_PCT 47.69 21.32 43.73 74.29 28.47 DEBT_EQUITY 24.54 0.00 1.44 21.03 72.99 AGE 18.67 9.00 13.00 23.00 15.11 VOLUME 1.06 0.12 0.32 1.17 1.81 SIZE 6.62 4.93 6.12 8.35 2.50

Panel B: China ADRs

M/B 3.17 1.08 1.87 3.64 3.75 CEO_DUALITY 0.27 0.00 0.00 1.00 0.45 NONEXE_CHAIR 0.01 0.00 0.00 0.00 0.12 INDEP_PCT 0.25 0.00 0.27 0.54 0.26 CEO_TENURE 4.09 2.00 4.00 6.00 3.20 INST_PCT 20.35 2.90 9.76 27.42 24.16 INSIDER_PCT 51.12 21.58 47.69 77.57 29.39

DEBT_EQUITY 25.79 0.00 0.50 18.42 85.43

AGE 18.05 9.00 12.00 20.00 16.09

VOLUME 1.12 0.10 0.31 1.27 1.84

SIZE 6.41 4.95 5.91 7.82 2.30

Panel C: Hong Kong ADRs

M/B 1.96 0.61 1.46 2.61 1.83 CEO_DUALITY 0.36 0.00 0.00 1.00 0.48 NONEXE_CHAIR 0.13 0.00 0.00 0.00 0.34 INDEP_PCT 0.21 0.00 0.21 0.40 0.20 CEO_TENURE 4.68 2.00 4.00 6.00 4.55 INST_PCT 13.41 3.03 8.98 22.26 12.51 INSIDER_PCT 52.19 27.03 64.41 70.19 23.48 DEBT_EQUITY 18.89 0.00 4.53 22.49 33.30 AGE 20.77 10.00 15.00 31.00 14.84 VOLUME 0.47 0.05 0.19 0.51 0.70 SIZE 6.37 4.18 5.64 8.90 2.99

Panel D: Taiwan ADRs

M/B 1.99 1.29 1.88 2.62 1.18 CEO_DUALITY 0.47 0.00 0.00 1.00 0.51 NONEXE_CHAIR 0.00 0.00 0.00 0.00 0.00 INDEP_PCT 0.26 0.00 0.33 0.38 0.20 CEO_TENURE 6.17 3.00 5.00 7.50 4.32 INST_PCT 19.26 12.49 18.32 25.48 8.17 INSIDER_PCT 20.00 7.72 18.94 36.28 12.17 DEBT_EQUITY 26.95 0.08 4.38 49.84 38.23 AGE 17.75 11.00 17.00 24.50 7.60 VOLUME 1.81 0.54 0.95 1.89 2.58 SIZE 8.28 7.06 8.81 9.56 1.97

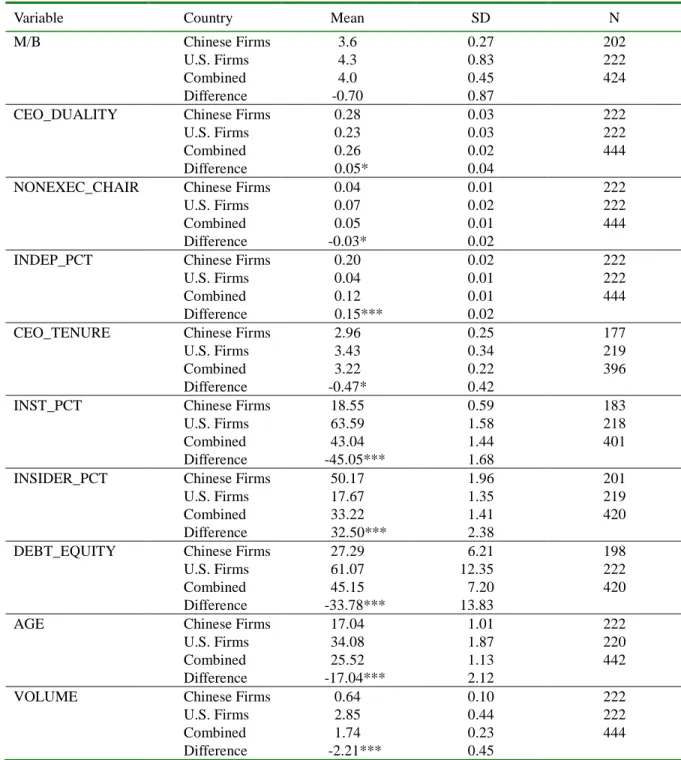

Table 2. Sample Comparison among Chinese, Hong Kong, and Taiwan ADRs

This table provides sample mean comparisons and t-test values for Chinese, Hong Kong and Taiwan ADRs listed during 2005-2010. *** and ** denote significance levels of 1% and 5% respectively. a reports difference in means in the following order: between Chinese ADRs and Hong Kong ADRs, between Hong Kong ADRs and Taiwan ADRs, and between Chinese ADRs and Taiwan ADRs.

Variable Country Mean SE Differencea N

M/B Chinese ADRs 3.17 0.23 1.21*** 269

Hong Kong ADRs 1.96 0.20 -0.03 81 Taiwan ADRs 1.99 0.18 -1.18** 45

CEO_DUALITY Chinese ADRs 0.27 0.03 -0.09 224

Hong Kong ADRs 0.36 0.05 -0.11 83 Taiwan ADRs 0.47 0.08 0.20*** 36 NONEXEC_CHAIR Chinese ADRs 0.01 0.01 -0.12*** 221 Hong Kong ADRs 0.13 0.04 0.13** 83 Taiwan ADRs 0.00 0.00 -0.01** 36

INDEP_PCT Chinese ADRs 0.25 0.02 0.04 251

Hong Kong ADRs 0.21 0.02 -0.04 84

Taiwan ADRs 0.26 0.03 0.01 43

CEO_TENURE Chinese ADRs 4.09 0.22 -0.58 213

Hong Kong ADRs 4.68 0.48 -1.49** 90 Taiwan ADRs 6.17 0.72 2.07*** 36 INST_PCT Chinese ADRs 20.35 1.62 6.94*** 222 Hong Kong ADRs 13.41 1.44 -5.85*** 75 Taiwan ADRs 19.27 1.26 -1.08 42 INSIDER_PCT Chinese ADRs 51.12 1.87 -1.08 246 Hong Kong ADRs 52.19 2.57 32.19*** 83 Taiwan ADRs 20.00 1.83 -31.11*** 44

DEBT_EQUITY Chinese ADRs 25.79 5.26 6.90 264

Hong Kong ADRs 18.89 3.75 -8.05 79 Taiwan ADRs 26.95 5.52 1.15 48

AGE Chinese ADRs 18.05 0.95 -2.72 285

Hong Kong ADRs 20.77 1.45 3.02 105 Taiwan ADRs 17.75 1.10 -0.30 48

VOLUME Chinese ADRs 1.12 0.11 0.65*** 280

Hong Kong ADRs 0.47 0.07 -1.34*** 88 Taiwan ADRs 1.81 0.37 0.69** 48

SIZE Chinese ADRs 6.41 0.14 0.04 272

Hong Kong ADRs 6.37 0.32 -1.91*** 86 Taiwan ADRs 8.28 0.28 1.87*** 48

Table 3. Cross Correlations of Governance Measures

This table presents the correlation coefficients between the governance measures. The Pearson correlation coefficients are above the diagonal and the Spearman rank correlation coefficients are below the diagonal. ***, **, *, denote significance levels of 1%, 5%, and 10%, respectively.

CEO_DUALITY NONEXE_CHAIR INDEP_PCT CEO_TENURE INST_PCT INSIDER_PCT CEO_DUALITY -0.14*** 0.18*** 0.27*** -0.06 0.12** NONEXE_CHAIR -0.15** 0.17*** -0.06 -0.14** 0.02* INDEP_PCT 0.26*** 0.20*** -0.15** -0.03 0.05 CEO_TENURE 0.28*** -0.08 -0.17** 0.01 -0.19*** INST_PCT -0.08 -0.22*** -0.05 0.05 -0.54*** INSIDER_PCT 0.15** 0.01 0.12* -0.11* -0.56***

Table 4. Regressions of Firm Performance on Governance Measures

This Table presents the regressions results of firm performance as proxy by Market-to-Book ratio on governance measures. CEO_DUALITY is a dummy variable that equals one when the CEO is also the chairman of the board, and zero otherwise. NONEXE_CHAIR is a dummy variable that equals one when the chairman of the board is not an executive member, and zero otherwise. INDEP_PCT is the percentage of independent directors on the board; CEO_TENURE is the number of years the CEO has held his/her title. INST_PCT is the number of shares held by institutional investors as a percentage of the current total shares outstanding. INSIDER_PCT is the number of shares held by insiders as a percentage of the current total shares outstanding. INSIDER_PCT2 is the square of the insider ownership percentage. DEBT_EQUITY is the long-term debt-to-equity ratio; SIZE is the natural log of market capitalization in millions of dollars. AGE is the number of years the company has been in existence (up to 2010); VOLUME is the 52-week average of the volume of shares traded; Country dummies are dummy variables to indicate the country of domicile for the firm. Exchange dummies are stock exchange dummy variables where the stock is traded. ***, **, *, denote significance levels of 1%, 5%, and 10%, respectively. P-values are presented in the parentheses.

(1) (2) (3) (4) INTERCEPT -2.49 (0.16) -1.64 (0.36) -4.77*** (0.00) -4.03* (0.06) Board Structure CEO_DUALITY 0.63 (0.30) 1.99** (0.03) NONEXE_CHAIR 0.71 (0.39) 0.08 (0.91) INDEP_PCT -2.22* (0.07) -1.79 (0.24) CEO Characteristics CEO_TENURE 0.06 (0.58) 0.03 (0.85) Ownership Structure INST_PCT 0.07** (0.03) 0.10** (0.04) INSIDER_PCT 0.08*** (0.00) 0.08** (0.04) INSIDER_PCT2 -0.08*** (0.00) -0.08* (0.06) Company Characteristics DEBT_EQUITY 0.01** (0.01) 0.00** (0.02) 0.01*** (0.00) 0.01*** (0.00) SIZE 0.61*** (0.00) 0.46*** (0.00) 0.50*** (0.00) 0.35** (0.01) AGE -0.00 (0.97) -0.00 (0.55) 0.00 (0.76) -0.01 (0.37) VOLUME 0.04 (0.68) -0.02 (0.80) -0.13 (0.18) -0.15 (0.25)

Hong Kong -1.10** (0.03) -1.17* (0.05) -0.67 (0.21) -1.13* (0.09) Taiwan -1.53** (0.01) -1.27* (0.06) -1.53** (0.01) -2.15* (0.05) Exchange Dummies NASDAQ 3.31*** (0.00) 3.00*** (0.00) 2.92*** (0.00) 2.82*** (0.00) AMEX 2.38** (0.04) 1.66* (0.09) 1.96*** (0.00) 1.64 (0.12)

Year Dummies Yes Yes Yes Yes

N 296 293 286 184

Appendix 1

Variables are classified into seven categories: performance measures, board structure, CEO characteristics, ownership structure, company characteristics, country dummies, and stock exchange dummies.

Variable Definition

Performance Measure

M/B Price per share of common stock divided by book value per share of common stock, measured in percentage

Board Structure

CEO_DUALITY Dummy variable equals one when the CEO is also the chairman of the board, and zero otherwise

NONEXE_CHAIR Dummy variable equals one when the chairman of the board is not an executive member, and zero otherwise

INDEP_PCT The percentage of independent directors in the board CEO Characteristics

CEO_TENURE The number of years the CEO has held his/her title Ownership Structure

INST_PCT The number of shares held by institutional investors as a percentage of the current total shares outstanding

INSIDER_PCT The number of shares held by insiders as a percentage of the current total shares outstanding

Company Characteristics

DEBT_EQUITY Debt to equity ratios, which is long term debt divided by total equity measured in percentage

SIZE The natural log of market cap, where the market cap is measured in millions of U.S. dollars

AGE The number of years the company has been in existence (up to 2010)

VOLUME The 52-week average of the volume of shares traded, which is measured in millions of shares

Country Dummies

CHINA Dummy variable to indicate which country a firm is from, one is China and zero otherwise

HONGKONG Dummy variable to indicate which country a firm is from, one is Hong Kong and zero otherwise

TAIWAN Dummy variable to indicate which country a firm is from, one is Taiwan and zero otherwise

Stock Exchange Dummies

NYSE Dummy variable which equals one if a firm's stock is listed on NYSE, and zero otherwise

AMEX Dummy variable which equals one if a firm's stock is listed on AMEX, and zero otherwise

NASDAQ Dummy variable which equals one if a firm's stock is listed on NASDAQ, and zero otherwise

Nanyang Technological University

Singapore July 17-20, 2011

Travel Report

Nangyang Technological University is one of the top 10 technological universities in the Asia Pacific region and one of the top schools throughout the world. Prof. Qu invited me to visit the department of economics at Nangyang Technological University for scholarly exchange. I visited the campus and found that Nangyang Technological University has not only the modern buildings and facilities but also the efficient management and leadership. What impressed me is that scholars from all over the world are frequently invited not only to present papers but also to work on research projects with colleagues at Nangyang Technological University.

The department provided me with a research office during my visit. During my stay, I exchanged research ideas, searched database, and explored possible research topics with professors Qu and Hu. We discuss how to efficiently use the modules of WRDS, one of the major databases used in business areas on the research projects. In addition to research, we share experience in teaching and supervising students.

I would like to take this chance to thank NSC for providing me with this grant. Through scholarly exchange, the scope of my research, teaching, and helping students is broadened. I benefited a lot from this experience.

Global Finance Conference

Bangkok, Thailand April 3-5, 2011

Travel Report

Global Finance Conference is sponsored annual by the Global Finance Association (GFA), a non-profit organization providing a platform for finance and accounting professionals to debate, learn and exchange ideas for academic and practical application. The conference has held 18th

annual meeting throughout the world. During the conference, I attended several sessions, met some reputable editors, and exchanged ideas with many professional researchers. When I presented the paper, I received lots of good comments, which helped me sharpen my ideas and refine the article substantially. I would like to take this chance to thank NSC for giving me the grant support to attend this conference.

Each year, the best papers presented at the conference are “conditionally” accepted for publication in Global Finance Journal. I was fortunate to receive the “Best Paper Award” from the Global Finance Conference dated April 3-5, 2011 at Bangkok Thailand. Below are the letter of evidence and certificate of best paper award from the founder, editor, and executive director of Global Finance Journal. The paper that was conditionally accepted is attached as well.

<Evidence 1>

論文已正式被 Global Finance Journal(國科會 B+等級期刊論文)條件式接受之證明 --- 原文 --- 主旨: Re: Submission to GFJ

寄件者: "Manuchehr Shahrokhi" <[email protected]> 日期: Sat, 四月 16, 2011 4:40 am

收件者: [email protected] 副本: [email protected]

"Hooman Shahrokhi" <[email protected]>

--- Dear Lee-Hsien

Congratulations. We are also pleased to have scholars like you attend the GF Conference in Bangkok. As you know the top papers presented at the Conference are "conditionally" accepted for publication of a special issue of the GFJ. Dr. KC Chen, a dear friend and colleague, serves on the editorial board of the GFJ. He is also editor of the International Journal of Finance.

For payment of your submission fees via our website, I will have my staff check our website to see why you can not make submission fee online via our website.

In the meantime, please go ahead and submit your paper via our website and for submission fee you can send us a check for US$150.00 to my address below:

Professor M. Shahrokhi

Editor, Global Finance Journal Craig School of Business

California State University Fresno, CA 93740-0008

---

Manuchehr Shahrokhi, Ph.D. Professor of Finance

Editor, *Global Finance Journal <http://www.glofin.org/Journal/>* Executive Director, Global Finance

Association-Conference<http://www.glofin.org/> California State University, Fresno, CA 93740 1-559-278-4058; Fax: 1-559-278-4911

<Evidence 2>

論文獲得 Global Finance Conference 最佳論文獎(Best Paper Award)之證 明

Corporate Governance and Firm Performance: A Comparative Analysis

of Chinese ADRs and US Firms

Abstract

We examine the relationship between firm performance and board structure, CEO

characteristics, and ownership structure of Chinese ADRs in the greater China region listed

on the NYSE, AMEX and NASDAQ. Among the governance mechanisms, CEO duality,

institutional ownership, and insider ownership are positively related to firm performance.

While we find that the extent to which governance mechanisms affect firm performance

between Chinese ADRs and U.S. matched firms are mostly similar, the positive impact of

insider ownership appears to be stronger for Chinese ADRs. Overall, cross-listings in the

U.S. stock markets appear to be beneficial for Chinese firms in improving their governance

mechanisms.

Keywords: Corporate governance; Chinese ADRs; CEO duality; Institutional ownership;

1. Introduction

The importance of corporate governance on firm value has long been recognized

since the pioneering work of Jensen and Meckling (1976) in a nexus of contracts among

various stakeholders. Under the rubrics of principal-agent conflicts, Shleifer and Vishny

(1997) emphasize that investor protection is crucial. La Porta et al. (1998, 2000, and 2002)

who examine the importance of external governance around the world show that countries

with common laws provide better shareholder protection than those with civil laws. They

document that the difference in the legal regimes and law enforcement has led to higher

valuation of corporate assets in common law regimes. In a more recent work, Gillan (2006)

provides a comprehensive review on different aspects of internal and external governance

systems. He suggests that the next wave of governance research will broaden the scope of

what constitutes corporate governance, and address multiple governance mechanisms and

their interactions.

In line with Gillan’s (2006) prediction, recent research has focused on the

determinants of corporate governance on firm performance. In particular, board structure

(Yermack (1996), Boone, Field, Karpoff, and Raheja (2007), and Linck, Netter, and Yang

and Weintrop (2007), and Brookman and Thistle (2009)) and ownership structure

(Lemmons and Lins (2003), and Ali, Chen and Radhakrishnan (2007)) have been identified

as key components for a firm’s governance practices. Firms with more independent

directors, less executive compensation, and higher managerial ownership are linked to

stronger governance and better firm performance.

In this study, we contribute to the literature as we examine the effect of the governance

practices on cross-listing firms in greater China Region (i.e. China, Hong Kong, and

Taiwan) under the American Depository Receipts (ADRs) programs. A firm that cross-lists

via an ADR is subject to more stringent governance and disclosure requirements (see

Durnev and Kim (2005) and Doidge, Karolyi, and Stulz (2003)) especially after the

Sarbane-Oxley Act in 2002. Coupled with the common law regime and stronger law

enforcement in the U.S. (see La Porta et al. (1998)), Chinese firms under the ADR

programs should arguably improve a range of governance measures as a result of the

cross-listings.

Part of our interest in examining Chinese ADRs in relation to their governance is

China despite its rapidly evolving regulatory framework.1 Evidence suggests that Chinese

firms tend to be characterized by ineffective supervisory boards and weak independence of

board directors (Tam (2002), Dahya, Karbhari, Xiao and Yang (2003), Lin (2004), and

Wang (2007)), high proportion of state share ownership (Sun and Tong (2003), Wei, Xie,

and Zhang (2005), Wei (2007), and Tian and Estrin (2008)), and common CEO duality

roles (Zhong (2002)).

As Chinese ADRs cross-list in the U.S., they face similar governance environment -

both internal and external as their U.S counterparts. As a result, the same governance

mechanisms may presumably have similar impact on firm performance. Alternatively, firm

characteristics related to the country of domicile may continue to play an important role in

the effectiveness of a firm’s governance practices. Comparing the extent to which

governance affects firm performance between Chinese ADRs and U.S. matched firms may

shed light on the differential importance of governance determinants.

Examining the impact of cross-listings of Chinese ADRs is also important because the

sustaining growth in China may require Chinese firms to raise external capitals in

international markets such as those in the U.S. Foreign direct investment (FDI) and

cross-border mergers and acquisitions continue to accelerate especially in commodity and

resource sectors as the need for energy keeps growing.2 In 2010, China has replaced Japan

as the second largest economy in the world. Therefore, understanding the effects of

corporate governance on Chinese ADRs performance should be of particular interest to

markets and investors.

Our analysis yields several interesting findings on the impact of board structure, CEO

characteristics, and ownership composition on the firm performance of Chinese ADRs.

First, CEO duality has a positive effect on firms’ market-to-book ratio. It suggests that

CEOs of Chinese ADRs are perhaps more motivated and have superior ability to lead the

company albeit reducing the monitoring role of the boards. It may also reflect why these

Chinese firms are successfully listed on the U.S. stock exchanges. Comparing the effect of

CEO duality between Chinese ADRs and their matched U.S. firms also reveals that the

duality factor is marginally more important for the former. The behaviors of Chinese ADRs

may therefore not apply to Rechner and Dalton (1991), and Bhagat and Bolton (2008) who

generally find that non-duality firms outperform duality firms.

Second, there appears to be little relation between CEO tenure and firm performance.

This result is perhaps not surprising since the average CEO tenure is only three years and

the top quartile group is four years. Given that firm performance may take a longer time to

improve than during the short CEO tenure years, it is a lesser important governance

measure than others for Chinese ADRs.

Third, insider and institutional ownership are positively related to firm performance.

Consistent with prior studies (e.g. McConnell and Servaes (1990), Hartzell and Starks

(2003), and Cornett, Marcus, Saunders, and Tehranian, (2007)), higher insider and

institutional ownership improves firm performance. It suggests that an increase in insider

ownership helps to lower potential conflicts of interest between managers and shareholders

and thereby increases firm value. Similarly, institutional ownership seems to play an

effective monitoring role for Chinese firms. Our results complement Sun and Tong (2003)

who document that share issue privatization in China is positively related while state

ownership is negatively related to firm performance.

Fourth, when we compare the governance effects between Chinese ADRs and U.S.

matched firms, there is little difference between them except for insider ownership where

the effect is relatively more pronounced on Chinese ADRs. It appears that while firm

measures as those of the U.S. firms, a few local institutional factors such as insider

ownership (versus state ownership) remain just as influential.

The remainder of the paper is organized as follows. Section 2 provides an overview of

the effect of corporate governance on firm performance and develops testable hypotheses.

Section 3 and 4 discusses the sample and methodology respectively. Empirical results are

reported in Section 5 and Section 6 concludes the paper.

2. Literature Review and Hypotheses Development

2.1 The Trends in Corporate Governance Framework

Due to globalization and increasing competition among firms, there has been an

ongoing argument on the convergence of corporate governance across countries. For

example, Hermalin (2005) show in his model that greater board diligence, more external

candidates of CEOs, shorter tenures for CEOs, less perquisite consumption by CEOs, and

more compensation for CEOs are the trends in a firm’s governance mechanisms. Similarly,

Khanna, Kogan, and Palepu (2006) report in a cross-country analysis that economically

interdependent countries have similar corporate governance rules as a result of

governance framework that explicitly incorporates internal governance such as the board of

directors and management, and external governance such as laws and capital markets. He

contends that the focus on the broader perspective of corporate governance is likely to be

the future trend.

However, other studies espouse that while some agreements on the best corporate

governance system may be reached, there remains a divergence on corporate governance as

firms in different countries/economies would choose what constitutes the best corporate

governance for themselves (see Aoki, 1994; Bebchuk and Roe, 1999; Hansmann and

Kraakman, 2001; and Gillan and Starks, 2003).

In the follow sub-sections, we discuss the well accepted corporate governance

determinants in the literature that may affect firm behavior and performance. They can be

classified into board structure, CEO characteristics, and ownership structure.

2.2 Board Structure

The impact of board structure on firm performance can be subdivided into board size,

board independence, board composition and board activities. In earlier studies, Yermack

and firm performance and show that smaller boards are generally more effective in

monitoring and advising top management. Vafeas (1999) complement these findings as he

documents that board meeting frequency is negatively related to firm value.

Recent findings however indicate that board size may not be strictly and negatively

related to firm performance. Linck et al. (2008) question whether smaller boards are

necessarily better than bigger boards. They find that the board size of large firms fell in the

1990s, but the board size of small firms remained relatively flat. Raheja (2005) suggests

that optimal board size is a function of the firm’s characteristics and its directors. In line

with this argument, Boone et al. (2007) report that board size and independence increase

when companies grow and mature over time. Coles, Daniel, and Naveen (2008) find that

the relation is perhaps U-shape in which Tobin’s Q increases in board size for complex

firms but decreases for simple firms. What is more important they suggest is the number of

inside vs. outside directors. Complex firms which have higher proportion of inside directors

are related to higher Tobin’s Q because insiders possess firm-specific knowledge that is

particularly important to these firms.

Independent directors are non-executive or non-employee directors, who may arguably

Consistent with the standard theory, Brickley, Coles, and Terry (1994), Borokhovich,

Parrino and Trapani (1996), Krivogorsky (2006), and Adams and Ferreira (2007) provide

some evidence that independent directors improve monitoring or lower its cost that in turn

enhance firm performance.

However, Wei (2007) argues that boards of directors in Chinese firms suffer from weak

independence, insider control, and CEO duality. In response to dubious party-related

transactions between directors and their firms, China imposes a two-tier board system to

promote better governance. A supervisory board of each firm is charged with the

responsibility and the oversight of the performance of directors and top management.

However, Schipani and Liu (2001), Tam (2002), and Wang (2007) report that supervisory

boards in Chinese firms are also ineffective in their governance roles undermined by their

weak composition and by a poorly defined monitoring role. In essence, creating a two-tier

board system has not removed the weak independence of directors and insider controls

within the boards. This leads to our first hypothesis as to whether independent directors in

Chinese ADRs play a more effective role under the U.S. regulatory environment.

Chinese ADRs.

When the CEO is also the chairman of the board, Fama and Jensen (1983) contend that

it may impede the effectiveness of board monitoring as the decision making and control is

endowed within one individual. Rechner and Dalton (1991), and Bhagat and Bolton (2008)

show that non-duality firms outperformed duality firms. Bai, Liu, Lu, Song, and Zhang

(2004) also report a negative relationship between CEO duality and market value for

Chinese firms. This leads to the second hypothesis:

H2: CEO duality is negatively related to performance of Chinese ADRs.

2.3 CEO Tenure

CEO tenure and its impact on firm profitability have often been discussed in the

governance literature. Hermalin and Weisbach (1991) suggest that CEO tenure does not

seem to affect firm profitability for shorter CEO tenures but firm profitability declines

when CEO tenure is more than 15 years. In a follow-up study, Hermalin and Weisbach