行政院國家科學委員會專題研究計畫 成果報告

綠色供應鏈中逆物流系統之建置 – 以華碩電腦為例

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 99-2410-H-004-134- 執 行 期 間 : 99 年 08 月 01 日至 100 年 11 月 30 日 執 行 單 位 : 國立政治大學企業管理學系 計 畫 主 持 人 : 羅明琇 計畫參與人員: 碩士班研究生-兼任助理人員:林筱雯 博士班研究生-兼任助理人員:劉晏孜 報 告 附 件 : 出席國際會議研究心得報告及發表論文 公 開 資 訊 : 本計畫涉及專利或其他智慧財產權,2 年後可公開查詢中 華 民 國 101 年 02 月 23 日

中 文 摘 要 : 綠色供應鏈管理在近年來的相關文獻中多所討論。然而,企 業在供應鏈中所處的位置如何對其進行綠化的動機及實行的 策略造成影響,其探討仍舊十分有限。 本研究透過個案研究方式,針對台灣地區高科技產業的十二 家公司進行探討,透過深度訪談及相關資料收集,瞭解各公 司在供應鏈中所處的位置,是否直接影響到其在進行綠化活 動時所面對的不確定性,而這些不確定性是否也導致公司受 到不同的驅動因子,進而提出其適當的綠色相關活動方案。 本研究結果顯示,企業在供應鏈中所處的位置對企業所面臨 的不確定性造成了影響。位於供應鏈上游,中游,及下游的 企業,其所面臨的不確定性主要來自於競爭環境,供應端, 以及需求端。面對的競爭環境不確定性越高,企業在進行綠 化活動時所受的外部驅動因子也越強烈,而內部因子則越不 強烈;面對的供應端不確定性越高,企業在進行綠化活動時 所受的外部驅動因子也越強烈,而內部因子則越不強烈;面 對的需求端不確定性越高,企業在進行綠化活動時所受的內 部驅動因子也越強烈,而外部因子則越不強烈。 中文關鍵詞: 綠色供應鏈管理,供應鏈不確定性,供應鏈位置 英 文 摘 要 :

英文關鍵詞: Green supply chain management (Green SCM), supply chain position, case study

The Effect of Supply Chain Position on the Motivation and Practices of Firms for Going Green

1. Introductions

In the global trend of pursuing a balance between sustainable economic and environmental development, the effective use of energy and the reuse of resources are among the principal global concerns. Numerous scholars have conducted studies related to green supply chains (Srivastava, 2007; Tibben-Lembke, 2002; Wu & Dunn, 1995); some scholars have investigated recycling network design (Guide Jr., 2000; Krikke, van Harten, & Schuur, 1999a, 1999b); others have discussed methods for prolonging product lifecycles from the perspective of manufacturing and remanufacturing (Amini, Retszaff-Roberts, & Bienstock, 2005; Fleischmann, Krikke, Dekker, & Flapper, 2000; van der Valk & Rozemeijer, 2009); and still other scholars explore the motivations of firms for going green (Carter & Ellram, 1998; Hu & Hsu, 2010; Zhu & Sarkis, 2006). These scholars believe that attaining an understanding of their motivations would allow the firms to gain confidence in going green.

Environmental uncertainties are a decisive factor for firms in making decisions related to supply chains (Fisher, 1997; H. L. Lee, 2002; Lo & Power, 2010), and the position of a firm in a supply chain frequently causes the firm to confront various environmental uncertainties. However, the literature on green supply chains is limited in its discussion on the effect that these uncertainties may have on the motivation of a firm to go green, and whether the green practices that a firm adopts vary with the position of the firm in the supply chain.

The aim of this study is to understand the effect of a firm’s position in a supply chain on the firm’s attitude toward green strategies, through empirical data analysis. Specifically, the research questions of this study are:

‐ Do the environmental uncertainties that a firm faces differ with the firm’s position in the supply chain when going green?

‐ Would the driving force of a firm for going green vary with the uncertainties it faces in the supply chain?

‐ Would the green-related practices a firm accept or execute vary with the firm’s position in the supply chain?

This article is divided into six major sections. The next section reviews the literature concerning green supply chain and the impact of firms’ positions on strategy. Additionally, because the primary targets of this study are high-tech industry in Taiwan, an introduction of the industry is included in the next section. The third section introduces the qualitative analytical steps of this study. The findings obtained through case study are analyzed and discussed in Section 4. The fifth section

describes the proposed hypotheses based on the results of data analysis. Finally, Section 6 details the conclusions and suggestions for future studies.

2. Literature Review

2.1 Green Supply Chain Management

Discussion of scholars on green supply chain is variable, as the industries and research topics differ. To most scholars (e.g., Green, Morton, & New, 1996; Ho, Shalishali, Tseng, & Ang, 2009; Rao, 2002; Srivastava, 2007; Wu & Dunn, 1995; Zhu, Sarkis, & Lai, 2008), the “green supply chain” contains two basic but crucial factors: environmental impact and supply chain management. In other words, scholars typically expect that green supply chain management involves the discovery of the environmental impact of firm practices from the traditional supply chain management viewpoint. In this study, we use the definition provided by Zsidisin and Seferd (2001), which considers green supply chain management to include all environment-relevant practices, the relationships among chain partners, and the minimization of the impact of firm practices on the natural environment through the use of recycled and reused products/services (Zsidisin & Siferd, 2001).

Previous literature has discussed various topics on green supply chain management. A number of scholars explore the driving forces and obstacles to firms in implementing green-related practices. These scholars believe that at the start of green supply chain implementation, firms are driven by multiple factors, such as legislation, customers, suppliers, and corporate awareness (Carter & Ellram, 1998; Forman & Jorgensen, 2004; Hsu & Hu, 2008; Zhu, Dou, & Sarkis, 2010). Another group of scholars led by Zhu and Sarkis explore what green supply chain practices firms might take, and how these practices affect their performance (Zhu et al., 2010; Zhu & Sarkis, 2004, 2006; Zhu, Sarkis, & Geng, 2005; Zhu, Sarkis, & Lai, 2007). According to these scholars, green-related practices could be grouped into five major categories: internal environmental management (e.g. green committee), green purchasing, cooperation with customers including environmental requirements, investment recovery, and eco-design; and these practices result in different performances in terms of environment, operations, and economics.

Firm attitude toward green is another theme of interests in the knowledge body of green supply chain management. For example, Walton et al. (1998) extend an earlier work (Kopicki, Berg, & Legg, 1993) and propose six strategies that firms might take when going green. From the reluctant to aggressive side, these strategies include: resistant adaptation, embracing without innovating, reactive, receptive, constructive, and proactive (Walton, Handfield, & Melnyk, 1998). van Hoek (1999)

grouped these attitudes to two major categories: reactive and proactive. For firms possessing a reactive attitude, green practices are considered to be a burden to the firm. These firms respond to these practices only when necessary, and in the most basic manner necessary to comply with legislation. In contrast, firms with a proactive attitude regard “going green” as a practice that adds value to the firm. Therefore, these firms go a step beyond legislation, and treat all business associates as partners with which they can work to create an environment advantageous to the supply chain.

Though scholars have investigated the driving forces and obstacles confronted by firms in implementing green-related practices, the amount of discussion in the literature regarding dissimilar attitudes among firms is limited. One of the few available discussions is a study which investigated the motivations of three major industries in China (Zhu & Sarkis, 2006). This study found that different industries have different characteristics and these characteristics in turn result in different impacts on firms’ green approaches.

2.2 Supply Chain Position

A firm’s position in a supply chain is a crucial component to review when its supply chain structure is analyzed (Choi & Hong, 2002; Lambert & Cooper, 2000). The supply chain position does not only affect firms’ ability of grasping information at the supplier and consumer ends, but also has a profound impact on relevant supply chain strategies (Lo & Power, 2010). Therefore, investigating how firms should establish their strategy in reflection of their chain position has always been one issue of interests among scholars.

The bullwhip effect is the most well-known theory among previous literature concerning supply chain positions (H. L. Lee, Padmanabhan, & Whang, 1997a, 1997b). Lee et al. considered that because of the delayed transmission of information, firms further away from end consumers in a supply chain face greater demand uncertainties, and thus bear greater risk in the form of fluctuations in order quantities. These effects consequently are reflected on the inventory and product decisions. Continuing with the discussion of the bullwhip effect, scholars further validated that different positions of firms in a supply chain have effects on their supply chain decisions (Adebanjo, 2009; Chow et al., 2008; Lo & Power, 2010; Mckone-Sweet & Lee, 2009). However, these discussions are based on general supply chain management, and have not focused on the implementation of green-related practices.

van Hoek (1999) discussed the effect of firm position in a supply chain when implementing green-related practices. From a theoretical perspective, van Hoek (1999) divided supply chains into three main segments (upstream, midstream, and downstream), and considered that firms of each stream have different emphases on

green practices. For example, raw material suppliers located upstream of the chain may emphasize material selection and the reuse of materials, whereas distributors and retailers downstream of the chain may devote their efforts to green practices such as packaging and return shipments. These discussions have not been validated in practice.

2.3 The High-tech Industry in Taiwan

East Asian countries, such as Taiwan and China, play a crucial role in the global electronics industry supply chain. Taiwan is the world’s largest manufacturer of computer-related products, such as notebook computers, motherboards, and modems (Chow et al., 2008). Taiwan’s integrated circuits (IC) output value accounts for nearly a quarter of global output, and Taiwan produces approximately 26% of the global supply of desktop computers, over 60% of the world’s notebooks, and more than 90% of the global supply of motherboards (Koh, Gunasekaran, & Tseng, 2011). These figures demonstrate the importance of the high-tech industry in Taiwan to global technology development.

Figure 1 is a schematic diagram showing the supply chain of high-tech industry in Taiwan. In this supply chain, Taiwan’s high-tech manufacturers exist in the upstream, midstream, and downstream as raw material suppliers, original design manufacturers/original equipment manufacturers (ODM/OEMs), and brand companies, respectively. Raw material suppliers provide raw materials; ODM/OEMs manufacture products according to the product specifications given by brand companies; finally, the products are sold by brand companies to end consumers. To make products that fulfill legislation for environmental protection in various export regions (for example, European Union legislation such as WEEE, RoHS, and EuP), all brand companies, ODM/OEMs, and raw material suppliers are committed to developing and providing parts that conform with these regulations. With this regard, there is little doubt that the high-tech manufacturers of Taiwan cannot escape from green supply chains under rising global environmental awareness.

Figure 1 A simplified supply chain of high-tech IT industry in Taiwan

3. Research Methodology

As this study is of an exploratory nature, we took a case study approach to collect qualitative data. Though this method has innate defects that cannot be overcome (for example, the limitation of the sample size and the subjective

interpretations of the researchers (Yi, Ngai, & Moon, 2011)), the case study method is widely used in supply chain management (e.g., Choi & Hong, 2002; Pagell, 2004; Zhu et al., 2007), and is regarded as an appropriate approach for exploring and understanding specific topics (Yin, 2003).

In case study research, scholars have suggested the use of at least two to four, but no more than ten to fifteen cases (Perry, 1998). The main objects of this study are firms in the high-tech industry of Taiwan, and twelve firms were selected for in-depth investigation. The purpose of data collection from multiple firms of the same industry is to establish a general principle that conforms to the industry through single-case and cross-case analysis. Too few cases could result in overly subjective results, and too many cases might produce results that are excessively dispersed. To avoid these issues, twelve cases were selected in this study.

The unit of analysis in this study is a firm. We conducted face-to-face in-depth interviews with each of the twelve cases based on a pre-planned interview protocol (see Appendix), and the respondents were invited to answer open-ended questions during the semi-structured interviews. Yin (2003) believes that a good interview protocol would reduce biases caused by different interviewers and respondents, and would assist respondents in rationally developing suitable procedures for answering question.

The research team conducted interviews of 90 to 105 min with each case. The respondents interviewed were middle to high level managers, such as directors of supply chain management, quality managers, R&D managers, and procurement managers, who were involved in and understood the green practices of the firm. With the respondents’ consent, each interview was recorded and later transcribed by members of the research team. The transcripts were organized and sent back to the respondents to validate the contents. If answers to a question were found to be unclear or inappropriate during transcription, the researchers would follow-up by telephone or email. Additionally, second-hand information was acquired regarding each case through channels such as firm websites, related documents (such as a corporate social responsibility report), and media reports. The second-hand information was matched to the information collected from the interviews to more comprehensively understand the performance of the firm in the related research topics (Yin, 2003).

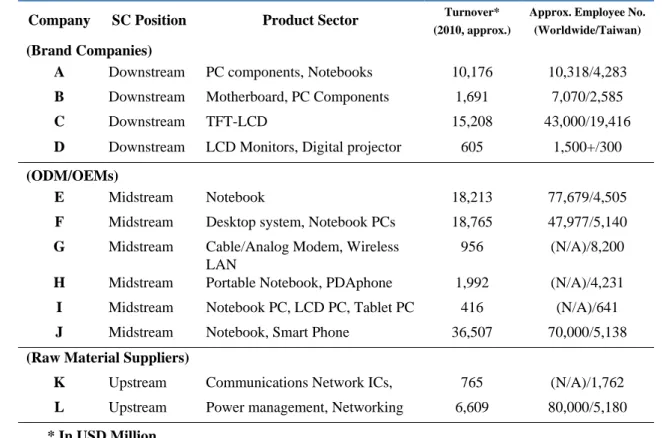

One of the major dimensions of this study was the position of a firm in its corresponding supply chain. Based on the review of literature (van Hoek, 1999), we divided Taiwan’s high-tech industry into upstream, midstream, and downstream firms, and used brand companies, ODM/OEMs, and raw material suppliers as representatives for each category. In this study, information on four brand companies, six ODM/OEMs, and two material suppliers were collected. The basic information of

the twelve cases is shown in the table below.

Table 1 Background information of the case companies

Company SC Position Product Sector Turnover*

(2010, approx.)

Approx. Employee No. (Worldwide/Taiwan)

(Brand Companies)

A Downstream PC components, Notebooks 10,176 10,318/4,283 B Downstream Motherboard, PC Components 1,691 7,070/2,585 C Downstream TFT-LCD 15,208 43,000/19,416 D Downstream LCD Monitors, Digital projector 605 1,500+/300 (ODM/OEMs)

E Midstream Notebook 18,213 77,679/4,505 F Midstream Desktop system, Notebook PCs 18,765 47,977/5,140 G Midstream Cable/Analog Modem, Wireless

LAN

956 (N/A)/8,200 H Midstream Portable Notebook, PDAphone 1,992 (N/A)/4,231 I Midstream Notebook PC, LCD PC, Tablet PC 416 (N/A)/641 J Midstream Notebook, Smart Phone 36,507 70,000/5,138 (Raw Material Suppliers)

K Upstream Communications Network ICs, 765 (N/A)/1,762 L Upstream Power management, Networking 6,609 80,000/5,180 * In USD Million

After the validation of each firm’s interview manuscript and the collection of relevant data, members of the research team further inspected all data. The data of each firm that related to the research topics were defined by the research team members following discussion. Through integrating data among each firm, we tried to identify the correlation among these firms. After the conclusions of these systematic discussions were transcribed, their reasonableness was examined by a single researcher. According to Yin (2003), the accuracy of data can be further validated and a research topic can be explored by establishing a complete database. The findings and discussions in this aspect are described in a later chapter (Section 4).

4. Results, Analysis, and Discussion

This section describes the results of analysis and a discussion of the data collected on each firm, including the uncertainty confronted by each firm (Section 4.1), the motivation of each firm for going green (Section 4.2), and the practices implemented by each firm (Section 4.3).

4.1 Supply Chain Uncertainty

its decision-making on related issues (Kocabasoglu, Prahinski, & Klassen, 2007; Mckone-Sweet & Lee, 2009; Yi et al., 2011). However, studies regarding the impact of uncertainty on green-related decision-making are limited. Numerous firms did mention that they faced particular uncertainties in their industry. These factors have further become a concern when creating strategies for going green.

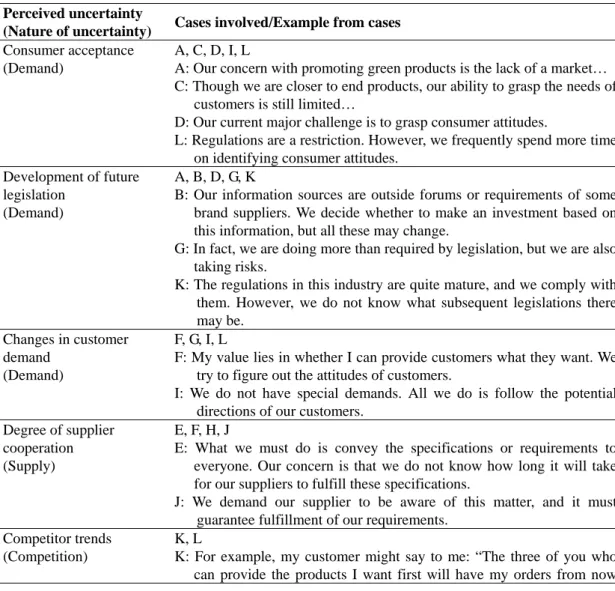

A study by Yi et al. (2011) indicated that the uncertainties faced by firms can be divided into three categories: demand, supply, and competition. In this study, the uncertainty factors mentioned by the case companies include consumer acceptance, the development of future legislation, changes in customer demand, the degree of supplier cooperation, and the competitor trends. By integrating the description of the uncertainty of each case firm, this study categorized customer acceptance, the development of future legislation, and changes in customer demand as demand uncertainty; the degree of supplier cooperation as supply uncertainty; and competitor trends as competition uncertainty. Each uncertainty and its correlation with the companies examined were organized and displayed in Table 2.

Table 2 Summary of case study results on perceived supply chain uncertainty

Perceived uncertainty

(Nature of uncertainty) Cases involved/Example from cases Consumer acceptance

(Demand)

A, C, D, I, L

A: Our concern with promoting green products is the lack of a market… C: Though we are closer to end products, our ability to grasp the needs of

customers is still limited…

D: Our current major challenge is to grasp consumer attitudes.

L: Regulations are a restriction. However, we frequently spend more time on identifying consumer attitudes.

Development of future legislation

(Demand)

A, B, D, G, K

B: Our information sources are outside forums or requirements of some brand suppliers. We decide whether to make an investment based on this information, but all these may change.

G: In fact, we are doing more than required by legislation, but we are also taking risks.

K: The regulations in this industry are quite mature, and we comply with them. However, we do not know what subsequent legislations there may be.

Changes in customer demand

(Demand)

F, G, I, L

F: My value lies in whether I can provide customers what they want. We try to figure out the attitudes of customers.

I: We do not have special demands. All we do is follow the potential directions of our customers.

Degree of supplier cooperation (Supply)

E, F, H, J

E: What we must do is convey the specifications or requirements to everyone. Our concern is that we do not know how long it will take for our suppliers to fulfill these specifications.

J: We demand our supplier to be aware of this matter, and it must guarantee fulfillment of our requirements.

Competitor trends (Competition)

K, L

K: For example, my customer might say to me: “The three of you who can provide the products I want first will have my orders from now

on.” Therefore, we also guess what our competitors may do.

L: In addition to customer demands, we often have to keep up with the subsequent development of our competitors.

The case study result firstly indicates that the uncertainties encountered by most of the brand companies positioned in the downstream of the supply chain are concentrated on consumer acceptance (Companies A, C, and D) and the development of future legislation (Companies A, B, and D). In general, these brand companies think that they can offer green product designs, but their major concern regarding their investments is whether consumers are willing to purchase products at a higher price, and whether future legislation will correspond with their investments. After all, “greening itself is costly” (Company C). Therefore, green investment presents a risk to these companies. Although these demand-related uncertainties are also mentioned by some of the ODM/OEMs and raw material suppliers, the result indicates that these uncertainties appear not to be the major concern to them.

Interestingly, none of the brand companies was worried about the capability of their suppliers. Some of these brand companies even mentioned that their suppliers’ cooperative attitudes gave them more confidence to implement new design ideas. For example, Company A said: “We have a long cooperative relationship with our suppliers. Our technical capacity is comparable to theirs. Therefore, we believe that they are capable of manufacturing the products we design. They (the suppliers) know it, too.” Company D also stated: “We are a brand company, a large firm. We can strongly demand our suppliers to act in concert. They would not give up a major client like us.” This finding echoes the previous research (Hall, 2000) that the existing of a channel leader with sufficient channel power would effectively emerge the dynamics in a supply chain.

In contrast to the brand companies, four of the six ODM/OEMs (Companies E, F, H, and J) stated concerns with their suppliers’ technical capacity to fulfill their requirements or their ability to cooperate. In addition to the ability of upstream suppliers to cooperate, these ODM/OEMs also worry about changing requirements from downstream customers. These ODM/OEMs often have to anticipate the next developmental direction of their customers, and ask their suppliers to make early preparations accordingly.

The main source of uncertainty for raw material suppliers (Companies K and L) comes from the pace of their competitors. These companies expressed their concerns that because they are at the upstream of the supply chain, they have enough time to respond to legislation or customer demands. However, for new demand, these manufacturers worry about whether they are able to provide products that their competitors can offer. If they are unable to provide the same products as their

competitors, they will have to give up the orders.

4.2 Drivers

Zhu and Sarkis (2006) tried to analyze the major drivers for firms of different industries in implementing green practices. They found that because the properties and competitive environments are different, the driving forces vary accordingly. For example, the driving force of marketing has a greater impact on the automotive industry than on power companies. In a later research (S. Y. Lee, 2008), the initiatives for small- and medium-enterprises in participating green practices were examined. It is found that the environmental requirements and support of buyers positively link to suppliers’ willingness. Hu and Hsu (2010) took the high-tech industry in Taiwan as their study object and explored the key factors of firms for successfully implementing green practices. In their study, the dimensions of factors possibly affecting firms going green include supplier management, product recycling, organization involvement, and life cycle management.

Carter and Ellram’s research (1998), which explores the motivations of going green from the external and internal perspectives, is one of the frameworks widely accepted (e.g., de Brito & Dekker, 2004; Srivastava, 2007; Vachon & Klassen, 2008). With regards to this framework, the case study results in terms of the drivers of firms going green are divided. The external factors include legislation, customers, and competitors; whereas the internal driving factors include reputation, cost, and support from top management. The relevant interview contents are organized and shown in Table 3.

Table 3 Summary of case study results on perceived drivers of GSCM

Perceived driver Cases involved/Example from cases Legislation A, B, C, D, E, F, G, H, I, J, K, L

B: We (Taiwan) may be considered an IT country. Legislation is a major concern for implementing green practices.

G: … (compliance with legislation) is one of our approaches for survival. I: Fundamentally, we follow the legislation.

Customers B, E, F, G, H, I, J, K

E: We act in line with our customers. In fact, they have progressively demanded this (green practices). We do whatever our customers ask us to do.

G: We change with the environment, because you have to change to survive. If you wish to grasp the opportunities you must follow the trends and go along with the activities.

H: It seems like all actions of each part of the supply chain are driven by customers.

J: The main cause is pressure from customers. Competitors E, F, H, J, K, L

J: If your competitors can achieve a certain goal but you cannot, you will try everything you can to achieve that goal.

K: We have competitors. If our competitors possess new products or technologies, we have to follow suit or we will lose the market.

Reputation A, B, C, D, E, F, G, H

A: It (going green) is a display of technology, a promotion of the brand image. C: Because current market conditions are unclear, the earlier you enter the

market, the greater the chance of establishing a foothold. We are currently trying to take initiative in the hope of establishing a green image.

H: If you wish to be a leader in green practices, you must be the first and the best in green products for people to remember you. People will not remember the followers.

Cost A, B, C, F, G, I, J, K

B: These things reduce cost, just like going green does. Manufacturing and assembly values are the lowest, and all is centered on generating profit. G:…to be honest, it (going green) also saves the company some energy, and

indirectly reduces costs. Going green also means saving for us. Support from top

management

A, B, C, D, F, H

D: Our chairman has a long-term vision. He is the promoter of many practices. F: We are unable to predict what our customers want, but we know what our

manager hopes to accomplish. Our manager is a great force in sustaining our continuous promotion of going green.

All twelve firms interviewed mentioned the importance of legislation in their implementation of green practices. Because Europe is a crucial export region of industrial output, the high-tech industry in Taiwan have been actively fulfilling the legislations of the European Union over the past few years to survive. Brand companies must act in accordance with legislations for their products to enter these markets, and ODM/OEMs must understand legislations to fulfill the demands of their customers (brand companies). As a result of this is that raw material suppliers must develop materials that fulfill the legislations. As Company K indicated, because legislations in the industry are quite mature, manufacturing processes that comply with green conditions are prerequisite to the survival of firms in this industry.

The impact of the other two external driving factors, customers and competitors, are significantly greater on firms positioned in the midstream and upstream of the supply chain. All ODM/OEMs express that customers are a stronger driving force than competitors. These manufacturers believe that their customers (brand companies) will eventually ask them to comply with relevant green practices in the future. Therefore, these ODM/OEMs endeavor to fulfill the requirements of their customers to the extent of their capabilities. However, brand companies have not yet sensed the demands for green products from end consumers. Thus, only one firm (Company B) considered customers as one of the crucial driving forces. As for the “competitor” factor, Company J, which is positioned in the midstream of the supply chain, indicated that they must keep pace with their competitors or they will be eliminated from the market.

A relatively larger number of companies positioned in the midstream and downstream of the supply chain mentioned the importance of internal driving factors to their promotion of green practices. For example, all brand companies and four of

the six ODM/OEMs mentioned the importance of reputation. This discovery is not surprising to brand companies (Companies A, B, C, and D). As stated by many firms, corporate image affects the consumers’ impression of the brand, thereby affecting their desire to purchase their products. From the perspective of ODM/OEMs, because many brand companies are inclined to select highly recognizable green manufacturers to indirectly increase the warranty for green, numerous ODM/OEMs (Companies E, F, G, and H) also desire to improve their green reputation to attract more orders from brand companies.

From the perspective of cost, lean and green are not necessarily mutually exclusive, as stated (Mollenkopf, Stolze, Tate , & Ueltschy, 2010). In the long term, green practices can reduce firm operating costs. Therefore, cost is mentioned as a driving factor for going green to most manufacturers positioned in the midstream and downstream of the supply chain (seven out of ten). Additionally, all brand companies (Companies A, B, C, and D) and two ODM/OEMs (Companies F, and H) stated that because they do not know the future direction of the market, internal persistence appears to be more important. As a consequence the support of high-level management has become significantly more important.

4.3 Practices

Because uncertainty in the supply chain and the driving forces for going green confronted by each firm are different, the corresponding measures taken by each firm differ. The SCOR model (The Supply Chain Council, 2011) provides an integrated process architecture for analyzing supply chain operations and is widely accepted by scholars (Kaplan & Norton, 2005; Lages, Lages, & Lages, 2005; Lo & Power, 2010; Wang, Huang, & Dismukes, 2004). Therefore, the relevant green supply chain practices mentioned by each case were divided into green design, green purchase, green manufacturing, and green logistics (including reverse logistics) as corresponds to the plan, source, make, and deliver/return processes of the SCOR model. Additionally, some cases mentioned that they have modified their organizational structure to accommodate green practices. Thus we also made observations from the organizational perspective to determine whether the firms have established dedicated units (internal environmental management) for planning and executing green practices.

The green practices promoted by each interviewed case were extracted and are as shown in Table 4.

Table 4 Summary of cases on perceived GSC practices

Perceived practice Cases involved/Example from cases Green design A, C, D, F, G, K

A: Because consumers value environmental design, our products must pay particular attention to this.

C: Designs based on environmental protection as the starting point have always been the direction of our effort.

K: We are raw material (suppliers); thus, for end products, we wish to make a contribution to energy conservation from the angle of raw materials. Green purchase A, B, C, D

B: We cooperate with certain suppliers, and the degree of greening of these suppliers is within our scope of consideration. This most directly influences our purchasing decisions.

D: When looking for suppliers, we consider aspects such as their toxic substance reports, recycling procedures, and green marks. That is green purchases.

Green manufacturing A, E, F, G, H, J

E: We have considered using materials free of lead and halogen and low in carbon in our manufacturing processes.

G: Though it is not an easy matter, we try to make carbon footprint calculations.

J: Carbon reduction, lead-free manufacturing processes…we are already doing so in our manufacturing processes.

Green logistics A, E, F, G, H, I

A: Consumer disposal of computers was not our concern in the past. But currently we provide a recycling venue that repairs computers for further use.

F: We care more about reducing the volume of packaging material and using and recycling these materials when delivering products to the customers. G: We implement voluntary packaging reduction, which includes reducing

transportation volume, reducing the use of paper boxes, and lowering the rate of ink coverage on paper boxes.

Internal environmental management

A, B, C, D, H, J

A: We have a legislation monitoring group that monitors green logistics, green supply chains, and carbon disclosures. We only perform it ourselves, but also hope that we can drive the whole supply chain to get involved. B: Internally, we have a laboratory and equipment required for making sample

testing. This reflects the importance we attach to going green.

H: We have a committee which is a cross-organizational unit. This committee was founded specifically for the execution of green-related practices.

First, in this study, most brand companies were found to have promoted relevant practices for green design and green purchase. Companies A and B indicated that because they make direct contact with consumers, products with energy-saving and carbon-reducing functionalities might be a major consideration for consumers when purchasing products. Therefore these companies are committed to designing green products to improve their brand image and customer satisfaction. This concept is also reflected in green purchase. The degree of greening has become a selection criterion for brand companies when selecting suppliers, because suppliers with the same ideas can promote the green image of brand company products.

From the perspective of green manufacturing and logistics, only one (Company A) of the four brand companies interviewed had implemented related practices, but five of the six ODM/OEMs were involved in each. For green manufacturing, in addition to avoiding the use of materials prohibited by legislation, these companies

have also considered using halogen-free and low carbon conditions in their manufacturing processes. As for green logistics, these firms stated the importance of green packaging and product recycling. In addition to remanufacturing and reconditioning the recycled products, reducing the volume of product packaging materials to save on transportation costs is an important issue for the firms regarding green logistics.

Finally, all four brand companies and two other manufactures (Companies H and J) have devoted efforts to internal environmental management. These companies have established specialized units for monitoring the development of legislation, understanding the anticipation of consumers for green products, and integrating related internal resources. Some of these manufacturers even have invested in a dedicated laboratory to perform sample inspections of materials delivered from suppliers to ensure product quality. Through these inter-departmental teams, these companies are able to attain more systematic plans when implementing green practices.

5. Development of Research Hypotheses

The aims of this study are to establish the relationship between the position of a firm in the supply chain and (1) the uncertainties it faces in promoting green practices, (2) its driving forces, and (3) its focus on green practices. Through case studies, we propose the following hypotheses.

Figure 2 Research hypotheses

First, we divided the role of firms in the supply chain into three types to discuss the uncertainties that the firms encounter during the implementation of green practices. The three types of roles are the brand companies in the downstream, the ODM/OEMs in the midstream, and the raw material suppliers in the upstream. According to the

analytical results of the interviews, we reason that because of the relatively shorter life cycle of high-tech products, consumer requirements are more difficult to predict. A crucial factor for brand companies in deciding whether to participate in green practices therefore is consumer acceptance of the products. However, consumer acceptance is not the chief concern for ODM/OEMs and raw material suppliers that already have a fixed collaborative model. In contrast, ODM/OEMs are frequently more concerned with whether the upstream suppliers can provide qualified raw materials to manufacture products that fulfill the requirements of customers; whereas the concerns of raw material suppliers are often whether the competitors’ next strategy will affect their market share, which in turn will affect the desire of these suppliers to invest.

Briefly, the first hypothesis was formulated as follows:

H1: The uncertainties a firm encounters when implementing green practices are related to its position in the supply chain.

H1.1: The closer a firm is to the upstream of the supply chain, the higher the competitive uncertainty.

H1.2: The closer a firm is to the midstream of the supply chain, the higher the supply uncertainty.

H1.3: The closer a firm is to the downstream of the supply chain, the higher the demand uncertainty.

In this study, we have also revealed that because of the different uncertainty each firm encounters, the reasons for each firm to participate in greening vary. Because the principal uncertainties they face are consumer preferences, brand companies are inclined to take an active role and hope to attract consumers with their green image. In other words, their major driving force is internal self-expectations, such as reputation, cost, and support from top management. In contrast, the uncertainties of raw material suppliers come from competition; thus, their major driving force is external, and includes customers and competitors. Moreover, outshining competitors and fulfilling customer requirements are crucial to the survival of ODM/OEMs. With this respect external driving factors are more important than internal ones to ODM/OEMs. A second hypothesis was thus formulated as follows:

H2: The internal and external driving forces of firms in promoting green practices are related to the types of uncertainties the firms encounter in the supply chain.

H2.1: The higher the competition uncertainty a firm faces, the smaller the internal driving force.

H2.2: The higher the competition uncertainty a firm faces, the greater the external driving force.

H2.3: The higher the supply uncertainty a firm faces, the smaller the internal driving force.

H2.4: The higher the supply uncertainty a firm faces, the greater the external driving force.

H2.5: The higher the demand uncertainty a firm faces, the greater the internal driving force.

H2.6: The higher the demand uncertainty a firm faces, the smaller the external driving force.

Though Zhu and Sarkis (2006) suggested that a particular relationship exists between drivers and practices in the implementation of green practices, the results of this study suggest that the drivers for a firm to implement green practices often originate from the uncertainty it encounters, which in turn is related to the position of the firm in the supply chain. We therefore believe that a firm’s position in the supply chain is a more appropriate entry point for discussing the suitable green practices for a firm to adopt to improve its performance.

In this study, green practices were divided into green design (plan), green purchase (source), green manufacturing (make), and green logistics (deliver/return) based on the SCOR model (The Supply Chain Council, 2011). Additionally, because several interviewed cases mentioned the adjustment of internal organization structure in response to the implementation of green practices, this study has included internal environmental management in the discussion.

Two trends were observed from the interviews: the green practices implemented by brand companies positioned in the downstream of the supply chain focused on green design, green purchase, and internal environmental management; whereas most ODM/OEMs positioned in the midstream of the supply chain implemented green manufacturing and logistics. Therefore, the following hypothesis was formulated in this study:

H3: To achieve better performance, firm willingness to promote green practices differs with firm position in the supply chain.

H3.1: The closer a firm is to the downstream of the supply chain, the stronger its willingness to promote green design.

its willingness to promote green purchase.

H3.3: The closer a firm is to the midstream of the supply chain, the stronger its willingness to promote green manufacturing.

H3.4: The closer a firm is to the midstream of the supply chain, the stronger its willingness to promote green logistics.

H3.5: The closer a firm is to the downstream of the supply chain, the stronger its willingness to promote internal environmental management.

6. Conclusions and Implications

With continuously increasing international awareness for environmental protection, firms have focused on the environmental performance when implementing related operating practices through methods such as corporate social responsibility (CSR). The high-tech industry of Taiwan is not an exception. The output value of Taiwanese high-tech products is the third largest globally (Government Information Office, 2012), and the primary export targets are the U.S. and European markets. Therefore, leading Taiwanese firms toward green products through the relevant driving forces and practices is crucial to Taiwan’s high-tech industry.

Firms of different natures have significantly different attitudes toward going green. Because brand companies directly deal with consumers, they have to fulfill the expectations of the firms themselves, the environment, and society, from the perspective of social responsibility. Therefore, brand companies tend to hold a proactive attitude toward going green. In addition to fulfilling the basic legislative requirements, brand companies actively provide energy-saving and carbon-reducing green products for their consumers. They also provide relevant information, such as a product’s carbon footprint, to allow the consumers to better understand the impact of a product on the environment. Large international companies (such as Sony) have a proactive attitude toward going green. They are even willing to invest to establish common standards for the industry. These large companies use their influence to promote the progress of the entire industry and to reduce the damage of the industry to the environment.

In contrast, the attitude of unbranded ODM/OEMs and raw material suppliers toward green practices is apparently much more reactive and conservative. The major concern of ODM/OEMs and raw material suppliers is fulfilling basic legislative requirements (Karakayali, Emir-Farinas, & Akcali, 2007). They only take further action when their customers ask them to. This is not surprising, because green practices are currently highly costly to firms, and the time required to recover these costs is still unknown. Additionally, ODM/OEMs are at a relatively low profit point in the smile curve. Therefore, “the desire of profit-oriented firms to get involved in green

practices is limited” (Company F).

The results of this study also indicate that though the cases interviewed generally believe that becoming involved in green practices is an inevitable trend, this type of investment can hardly become one of the core competencies of the company. The underlying reason for this is that consumer recognition and acceptance of green products has yet to be enhanced. In other words, though consumers understand the benefits that green products have on the environment, they may not be able or willing to accept green products if these products are more costly. Consumer recognition has become one of the concerns for firms in deciding whether to continue their investment on going green.

6.1 Implications

From an academic aspect, this study has expanded the discussion of green supply chain management. This study begins from the position of firms in the supply chain to discuss the uncertainties these firms must face, and subsequently establishes the relationship between these uncertainties and the major driving forces of firms for implementing green practices. This approach is rare in previous literature. Furthermore, past literature has suggested that a specific relationship exists between driving factors and firm practices. We believe that such a relationship must be based on the position of firms in the supply chain. Thus, we have identified the relationship between supply chain position and green practices.

This study has also made a contribution to managers in practice. Using the SCOR model as the framework to facilitate organizational adjustment, this study proposes five major dimensions of green practices. These dimensions can assist practitioners to better understand the complete picture of relevant green practices. This study also assists practitioners in understanding the potential type of uncertainty a firm may face resulted from its position in the supply chain. This information allows firms to educate their staff and their supply chain partners to jointly achieve the goal of green supply chain through internal or external driving forces, based on the type of uncertainty. Finally, the analysis allows companies to focus on the green practices most appropriate to them, and to make proper investments to attain benefits for the environment, the company, and society.

6.2 Limitations

Though we seek perfection in this study, some limitations cannot be overcome. First, the data for this study were collected from the high-tech industry in Taiwan, thus our ability for generalization of the data is limited. Second, the data collected were analyzed by the research team, which may involve some subjective factors.

6.3 Further Research

Scholars may expand upon the incomplete areas of this study in the future. Relevant studies may be conducted on different industries and in different areas to further generalize the results of this study. To solve for potential subjective factors of qualitative data analysis, we suggest that quantitative data be collected for discussions. Once the relationships of research constructs have been established, scholars may further discuss the relationship between green practices and performance to verify whether coordination between supply chain position and green practices can improve firm performance.

References

Adebanjo, D. (2009). Understanding demand management challenges in intermediary food trading: A case study. Supply Chain Management: An International

Journal, 14(3), 224-233.

Amini, M. M., Retszaff-Roberts, D., & Bienstock, C. C. (2005). Designing a reverse logistics operation for short cycle time repair service. International Journal of

Production Economics, 96(3), 369-380.

Carter, C. R., & Ellram, L. M. (1998). Reverse logistics: A review of the literature and framework for future investigation. Journal of Business Logistics, 19(1), 85-102.

Choi, T. Y., & Hong, Y. (2002). Unveiling the structure of supply networks: Case studies in Honda, Acura, and DaimlerChrysler. Journal of Operations

Management, 20(5), 469-493.

Chow, W. S., Madu, C. N., Kuei, C.-H., Lu, M. H., Lin, C., & Tseng, H. (2008). Supply chain management in the US and Taiwan: An empirical study. Omega,

36(5), 665-679.

de Brito, M., & Dekker, R. (2004). A framework for reverse logistics. In R. Dekker, M. Fleischmann, K. Inderfurth & L. V. Van Wassenhove (Eds.), Reverse logistics:

Quantitative models for closed-loop supply chains (pp. 3-27): Springer-Verlag,

Germany.

Fisher, M. L. (1997). What is the right supply chain for your product? Harvard

Business Review, 75(2), 105-116.

Fleischmann, M., Krikke, H. R., Dekker, R., & Flapper, S. D. P. (2000). A characterisation of logistics networks for product recovery. Omega, 28(6), 653-666.

Forman, M., & Jorgensen, M. S. (2004). Organising environmental supply chain management: Experience from a sector with frequent product shifts and complex product chains: The case of the Danish textile sector. Greener

Management International, 45(Spring), 43-62.

Government Information Office. (2012). Taiwan yearbook 2011: Economy.

Green, K., Morton, B., & New, S. (1996). Purchasing and environmental management: Interaction, policies and opportunities. Business Strategy and the Environment,

5, 188-197.

Guide Jr., V. D. R. (2000). Production planning and control for remanufacturing: Industry practice and research needs. Journal of Operations Management,

18(4), 467-483.

Hall, J. (2000). Environmental supply chain dynamics. Journal of Cleaner Production,

8(6), 455-471.

Ho, J. C., Shalishali, M. K., Tseng, T.-L. B., & Ang, D. S. (2009). Opportunities in green supply chain management. The Coastal Business Journal, 8(1), 18-31. Hsu, C.-W., & Hu, A. H. (2008). Green supply chain management in the electronic

industry. International Journal of Environmental Science and Technology, 5(2), 205-216.

Hu, A. H., & Hsu, C.-W. (2010). Critical factors for implementing green supply chain management practice -- An empirical study of electrical and electronics industries in Taiwan. Management Research Review, 33(6), 586-608.

Kaplan, R. S., & Norton, D. P. (2005). The balanced scorecard: Measures that drive performance. Harvard Business Review, 83(7), 172-180.

Karakayali, I., Emir-Farinas, H., & Akcali, E. (2007). An analysis of decentralized collection and processing of end-of-life products. Journal of Operations

Management, 25(6), 1161-1183.

Kocabasoglu, C., Prahinski, C., & Klassen, R. D. (2007). Linking forward and reverse supply chain investments: The role of business uncertainty. Journal of

Operations Management, 25(6), 1141-1160.

Koh, S. C. L., Gunasekaran, A., & Tseng, C. S. (2011). Cross-tier ripple and indirect effects of directives WEEE and RoHS on greening a supply chain.

International Journal of Production Economics, In Press.

Kopicki, R., Berg, M. J., & Legg, L. (1993). Reuse and recycling -- Reverse logistics

opportunities. Oak Brook, IL: Council of Logistics Management.

Krikke, H. R., van Harten, A., & Schuur, P. C. (1999a). Business case Oce: Reverse logistic network re-design for copiers. OR Spektrum, 21(3), 381-409.

Krikke, H. R., van Harten, A., & Schuur, P. C. (1999b). Business case Roteb: Recovery strategies for monitors. Computers & Industrial Engineering, 36(4),

739-757.

Lages, L. F., Lages, C., & Lages, C. R. (2005). Bringing export performance metrics into annual reports: The APEV scale and the PERFEX scorecard. [Article].

Journal of International Marketing, 13(3), 79-104.

Lambert, D. M., & Cooper, M. C. (2000). Issues in supply chain management.

Industrial Marketing Management, 29(1), 65-83.

Lee, H. L. (2002). Aligning supply chain strategies with product uncertainties.

California Management Review, 44(3), 105-119.

Lee, H. L., Padmanabhan, V., & Whang, S. (1997a). The bullwhip effect in supply chains. Sloan Management Review, 38(3), 93-102.

Lee, H. L., Padmanabhan, V., & Whang, S. (1997b). Information distortion in a supply chain: The bullwhip effect. Management Science, 43(4), 546-558. Lee, S. Y. (2008). Drivers for the participantion of small and medium-sized suppliers

in green supply chain initiatives. Supply Chain Management: An International

Journal, 13(3), 185-198.

Lo, S. M., & Power, D. J. (2010). An empirical investigation of the relationship between product nature and supply chain strategy. Supply Chain Management:

An International Journal, 15(2), 139-153.

Mckone-Sweet, K., & Lee, Y.-T. (2009). Development and analysis of a supply chain strategy taxonomy. Journal of Supply Chain Management, 45(3), 3-24.

Mollenkopf, D., Stolze, H., Tate , W. L., & Ueltschy, M. (2010). Green, lean, and global supply chains. International Journal of Physical Distribution &

Logistics Management, 40(1/2), 14-41.

Pagell, M. (2004). Understanding the factors that enable and inhibit the integration of operations, purchasing and logistics. Journal of Operations Management,

22(5), 459-487.

Perry, C. (1998). Processes of a case study methodology for postgraduate research in marketing. European Journal of Marketing, 32(9/10), 785-802.

Rao, P. (2002). Greening the supply chain: A new initiative in South East Asia.

International Journal of Operations & Production Management, 22(6),

632-655.

Srivastava, S. K. (2007). Green supply-chain management: A state-of-the-art literature review. International Journal of Management Reviews, 9(1), 53-80.

The Supply Chain Council. (2011). SCOR Model Version 10.0 (http://www.supply-chain.org/) Retrieved 12, 2011, from http://www.supply-chain.org/

Tibben-Lembke, R. S. (2002). Life after death: Reverse logistics and the product life cycle. International Journal of Physical Distribution & Logistics Management,

32(3), 223-244.

Vachon, S., & Klassen, R. D. (2008). Environmental management and manufacturing performance: The role of collaboration in the supply chain. International

Journal of Production Economics, 111(2), 299-315.

van der Valk, W., & Rozemeijer, F. (2009). Buying business services: Towards a structured service purchasing process. Journal of Services Marketing, 23(1), 3-10.

van Hoek, R. I. (1999). From reversed logistics to green supply chains. Supply Chain

Management: An International Journal, 4(3), 129-135.

Walton, S. V., Handfield, R. B., & Melnyk, S. A. (1998). The green supply chain: Integrating suppliers into environmental management processes. International

Journal of Purchasing & Materials Management, 34(2), 2-11.

Wang, G., Huang, S. H., & Dismukes, J. P. (2004). Product-driven supply chain selection using integrated multi-criteria decision-making methodology.

International Journal of Production Economics, 91(1), 1-15.

Wu, H.-J., & Dunn, S. C. (1995). Environmentally responsible logistics systems.

International Journal of Physical Distribution & Logistics Management, 25(2),

20-38.

Yi, C. Y., Ngai, E. W. T., & Moon, K.-L. (2011). Supply chain flexibility in an uncertain environment: Exploratory findings from five case studies. Supply

Chain Management: An International Journal, 16(4), 271-283.

Yin, R. K. (2003). Case study research: Design and methods. Thousand Oaks, Calif.: Sage Publications.

Zhu, Q., Dou, Y., & Sarkis, J. (2010). A portfolio-based analysis for green supplier management using the analytical network process. Supply Chain Management:

An International Journal, 15(4), 306-319.

Zhu, Q., & Sarkis, J. (2004). Relationships between operational practices and performance among early adopters of green supply chain management pracices in Chinese manufacturing enterprises. Journal of Operations

Management, 22(3), 265-289.

Zhu, Q., & Sarkis, J. (2006). An inter-sectoral comparison of green supply chain management in China: Drivers and practices. Journal of Cleaner Production,

14(5), 472-486.

Zhu, Q., Sarkis, J., & Geng, Y. (2005). Green supply chain management in China: Pressures, practices and performance. International Journal of Operations &

Production Management, 25(5), 449-468.

Zhu, Q., Sarkis, J., & Lai, K.-H. (2007). Green supply chain management: Pressures, practices and performance within the Chinese automobile industry. Journal of

Cleaner Production, 15(11-12), 1041-1052.

Zhu, Q., Sarkis, J., & Lai, K.-H. (2008). Green supply chain management implications for "closing the loop". Transportation Research. E, Logistics and

Transportation Review, 44, 1-18.

Zsidisin, G. A., & Siferd, S. P. (2001). Environmental purchasing: A framework for theory development. European Journal of Purchasing & Supply Management,

7(1), 61-73.

Appendix Interview Protocol

Before the interview, the researcher explained the research objective, the information intended to be collected, and the explanation of the research concepts to each informant.

The questions are structured as below:

Please describe your industry section and your business nature. Please describe your relationships with your suppliers and customers. Please describe your process of being “green”.

‐ Please indicate the uncertainties you face when being “green”. Which ones concern you most?

‐ Please indicate the forces drive you to be “green”.

‐ Please describe what practices you have done to be “green”.

According to your experience and observation, how do you perceive the associations a.) between your supply chain position and the uncertainties you face, b.) the uncertainties you face and the forces driving you to be “green”, and c.) your supply chain position and the practices you take to be “green”?

Is there anything that I have not asked that you think might be relevant to this research?

行政院國家科學委員會補助國內專家學者出席國際學術會議報告

2011 年 11 月 4 日 報告人姓名 羅明琇 服務機構 及職稱 國立政治大學企業管理學系 助理教授 時間 會議 地點 2011 年 10 月 19 日至 22 日 Elounda, Crete, Greece本會核定 補助文號

99-2410-H-004-134

會議

名稱 The 4th EuroMed Conference of the EuroMed Academy of Business 發表

論文 題目

1) How do Reverse Logistics React to Green Supply Chains? A Case Study 2) Transforming After-Sales Service to Customer Support System (CSS): A

Case Study

一、 參加會議經過

本屆 The 4th EuroMed Conference of the EuroMed Academy of Business 於 2011 年 10 月 19 日至 22 日於希臘 Crete 上的 Elounda 小鎮,假度假飯店 Porto Elounda De Luxe Resort, Agios Nilolaos 舉行。本次研討會由 Technological Educational Institute of Crete, Greece 主辦,主題為:“Business Research Challenges in a Turbulent Era”。參加對象包括來自世界各大 學學者,各研究單位研究人員,以及相關產業界人士共計二百餘人。 本次研討會的舉辦經歷了許多波折,最大的原因在於希臘近期的經濟動盪,使得當地的 交通及其他行業都存在著許多不可預期的變動因素。例如研討會預計舉行的 20 及 21 日, 希臘所有國際及國內的機場控管人員便舉行罷工,所有的公車及計程車司機也在公會的支持 下採取相同的動作,以表達對政府政策的不滿意見。這兩日,不但是希臘有史以來最大的罷 工事件,在市區多處也發生大小不斷地流血衝突。這些不穩定的社會因素,都對參加研討會 的人員造成了許多的不確定性。 研討會的行程共計四天。第一天 (10.19) 為報到及簡便的歡迎酒會,第二天及第三天 (10.20 及 21) 為與會者交換研究心得及簡報的時間,第四天 (10.22) 則是讓與會者在輕鬆的 環境中做非正式的交流。然而,由於罷工的原因,許多與會者無法在第二天開始前抵達會場, 因此議程不斷地變動,最後有部分報告議程挪至第四天舉行。 此研討會總計收錄作業管理領域相關研討會文章一百餘篇,每篇皆以口頭報告 (Oral Presentation) 的方式呈現。這些文章總共在八間不同的會議室中同時進行,每篇文章約有三 十分鐘的報告及討論時間。研討會文章包含廣泛的作業管理領域相關主題,例如:供應鏈管 理,行銷與作業,策略管理等等,此外,也有針對特定產業所進行的討論,如:製酒產業, 旅遊及餐飲管理等等。

本人此次共計有兩篇文章被大會所接受,分別是:1) How do Reverse Logistics React to

附

件

Green Supply Chains? A Case Study 以及 2) Transforming After-Sales Service to Customer Support System (CSS): A Case Study。兩篇文章都被安排在 “策略管理” 的主題下發表。然而, 受到許多與會者的抵達時間變動的影響,大會建議本人擇一發表,以讓整個大會的流程可進 行地更順利。本人因此同意僅對第二篇文章進行口頭分享。(因此第一篇僅收錄於 proceedings 中,未在會場上進行口頭報告。) 在第二篇文章的發表過程中,本人與相關領域的其他學者針對相關主題有了許多的互 動,在討論的過程中學者給予本人研究方法以及資料收集上的具體建議,也針對目前學術界 相關主題的發展有了進一步地交流。最後本人也與其中數位對本人的研究主題表露出濃厚興 趣的學者交換聯絡方式,希望能夠在日後能有更多的意見分享與合作。 二、 與會心得 在 這 一 次 的 議 程 中 , 除 了 學 者 們 的 研 究 交 流 , 主 辦 單 位 也 舉 辦 了 多 場 的 工 作 坊 (Workshop),以協助同樣在研究領域的與會人員能夠在相關的職涯生活中有更多的認識,例 如:在 “Meet the Editors” 的時段中,大會邀請了多位在管理領域相關期刊中擔任總編輯、編 輯,以及客座編輯的資深學者,與年輕學者們進行經驗分享。在分享的過程中,這些資深學 者提醒了我們:在撰寫研究論文時,該如何開門見山地讓總編輯能夠在第一時間知道要表達 的重點,如何清楚地描述研究邏輯的發展過程以及資料收集的合理性,資料分析的架構,以 及對學術及產業界的貢獻等等。這些學者們也很清楚地說明了研究倫理 (Research Ethics) 對 我們人文社會科學領域的重要性,也提醒我們在研究進行的過程中,如何避開可能會引起爭 議的部分,但又同時收集到符合研究目的的資料。這些分享對本人來說都是很大的收穫。

此外,在 “Research Proposals: Funding Opportunities, Submission and Implementation Challenges” 的時段中,多位資深學者也非常熱心地提供許多可能的研究經費來源及管道給在 場的年輕學者。在這樣分享的過程中,本人看到了這些學者無私的付出,只希望能夠集結自 己小小的力量,讓整個研究團隊/領域可以發展地更完善,進而對相關的產業或是國家經濟有 所貢獻。這樣的精神是本人認為值得學習的。 透過這一次的會議,本人很開心結識了多位來自中歐地區進行相關研究的學者。在本人 過去的經歷及所學中,較少機會針對中歐地區的作業管理相關發展進行深入瞭解,但是這一 次,透過與來自該地學者的對談 (如:Cyprus, Croatia, Israel 等國家),本人瞭解到,雖然我 們每一個人所處的地域性並不同,但是隨著網路科技的進步,以及交通的易趨便利,區域與 區域之間的隔閡已不再是經濟活動發展時的限制,也因此,對於同樣以商業交易行為下所衍 生出來的企業活動為主要研究的我們來說,地域性的隔閡不該是研究上的盲點。甚至,透過 彼此之間共有的主要市場 (如:歐、美),連結起過去看似陌生的兩個研究體,這是本人在未 來有機會與這些學者朋友進行努力的方向。 三、 建議 本人多次參加在歐洲地區舉辦的國際學術研討會,在每一次參加的過程中,都深刻感受 到亞洲研究人員參與的情形並不算踴躍。這次也不例外。在這一次的會議中,全場約兩百餘 人,僅有本人及本校另一位老師來自亞洲。本人推測可能的原因,是因為歐洲的學術研討會

在台灣一直都是未被廣為宣傳,即使會議中有知名學者來進行交流分享,也常常不經意地被 忽略。這一點甚為可惜。因此本人認為,對台灣的研究團體而言,若有機會,應可多邀請歐 洲地區的學者來台灣進行交流分享,這樣不但可擴展台灣研究人員對相關領域的視野,也可 讓更多國外的研究團體瞭解台灣研究人才的優異。 此外,由於這一次會議行程的安排受到了希臘國家罷工因素的影響,讓整趟行程充滿了 許多變數。在行程不斷更動地情形下,也著實提高了這一趟旅程的成本。因此,本人建議貴 單位,未來若有類似的情形,或可適度地調整參與人員相關經費應用的規定,以讓與會人員 在安全的前提下能夠對行程做更適切的安排。 四、 攜回資料名稱及內容

研討會論文集光碟 (The 4th EuroMed Conference of the EuroMed Academy of Business: Business Research Challenges in a Turbulent Era (Electronic ISBN 978-9963-711-01-7))

1

How Do Reverse Logistics React to A Green Supply Chain?

A Case Study

Abstract Purpose

Following changes brought on by globalization, the establishment of regulatory bodies (such as WEEE, RoHS) in the EU economic market has had a dramatic influence on the supply chain of entire information technology industry. This has driven the development of Green Supply Chain. From the perspective of green operations, Srivastava (2007) believes that a product can generate significant added value, or be used again for other useful purposes, after it is recovered at the end of its life cycle, and taken through re-manufacturing, updating, re-use, or other processes. Carter and Ellram (1998) believe that green supply chains go through this reverse logistics process to reach their final objective of reducing their use of resources. In view of the important role reverse logistics system plays in the management of green supply chains, this study has chosen reverse logistics as its main focus of research.

This study aims to learn how reverse logistics systems can extend product life cycle and how increased added value can be generated, through the process of reconditioning. The research problem is stated as: “What factors drive the construction of reverse logistics system under the wave of Green Supply Chain? How does the system react to these factors in terms of its players and activities?”

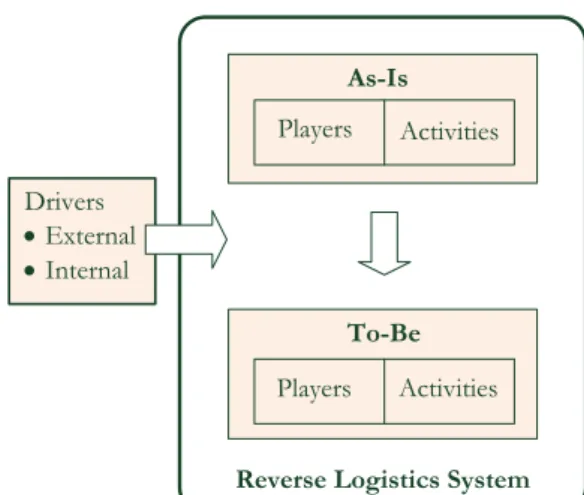

In order to answer this question, a well-known computer manufacturing company in Taiwan is used as the subject for research into reverse logistics systems, as an extension of the back-end operation of that company. We firstly examine the potential drivers from both internal and external as suggested by Carter and Ellram (1998). The resource dependency theory (RDT) is then adopted as a starting point for an investigation into the impact of how these motivational factors have had on the system. The “As-Is” and “To-Be” models of the system are observed, focusing particularly on the "players" of and their "activities" in the system. The overall concept of this study is depicted as below.

Players Activities As-Is To-Be Players Activities Drivers • External • Internal

Reverse Logistics System

Figure 1. Overall concept for the study

Design/methodology/approach

This study uses a case study method to approach the collection and validation of qualitative data. Focusing on the selected case company, we adopted the multiple data collection method as the way to collect our data. These methods include in-depth interviews, plant tours, documentation, and archival records.

Findings

Regarding the forces that compel businesses to transform their original reverse logistics systems into one based on green supply chain management, we found that external pressure was due mainly to outside regulations and pressure from competition, as a tactical shift in their strategic dimension. Internally, the main driving force came from support and policy implementation of top management, forcing the business, (within the scope of its operational dimension), to establish communication and procedures internally from the top down.

Product recovery supply chains include four major players: consumers, distributors, manufacturers, and suppliers. The roles of these players are repositioned or renewed following the transformation. Manufacturers move from the original system of disposing recycled products as scrap to extract precious metal from the recycled products that can no longer be repaired. By increasing the exchange of information, manufacturers can gain valuable information regarding the amount of precious metal available for extraction from recycled products or the proportion of original raw materials that could be recovered. This information can then be fed back to the front-end of the product design stage. Where once